Embed Size (px)

Citation preview

November 23rd, 2010

Presented by:

Dr. Christian Thun, Senior DirectorDr. Juan M. Licari, Senior DirectorDr. Mark Zandi, Chief Economist

Reverse Stress Testing: Challenges & Benefits

2

Reverse Stress Testing: Introduction & Agenda

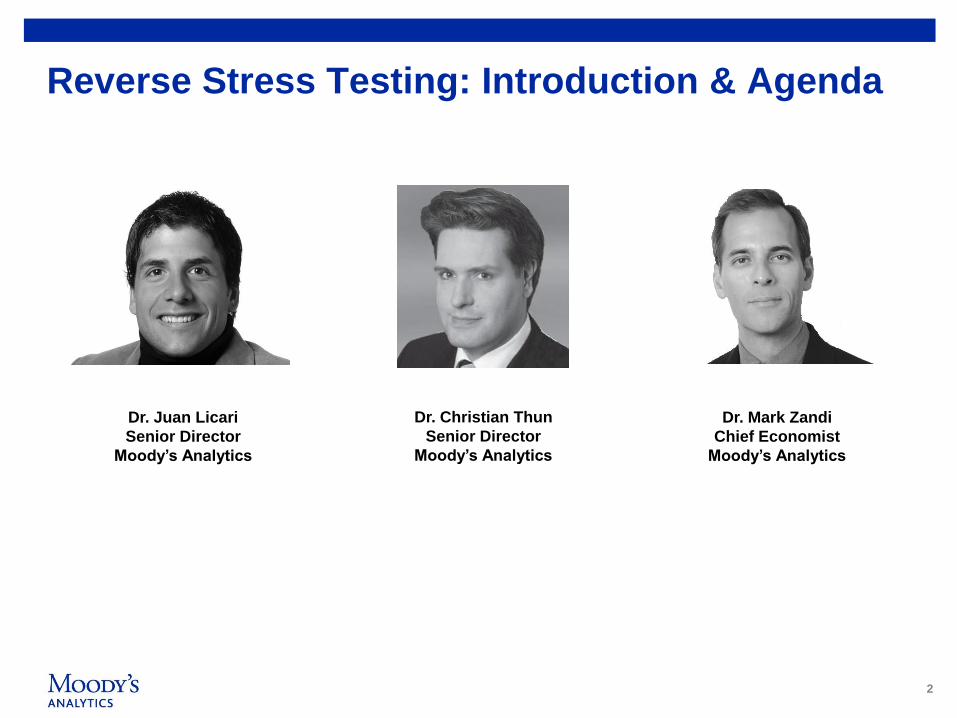

Dr. Mark Zandi

Chief Economist

Moody‟s Analytics

Dr. Christian Thun

Senior Director

Moody‟s Analytics

Dr. Juan Licari

Senior Director

Moody‟s Analytics

33

Today‟s Participants

» Reverse stress testing is a hot topic around the world

» 700+ registrations from Europe, North and Latin America,

the Middle East, Africa and Asia

4

4

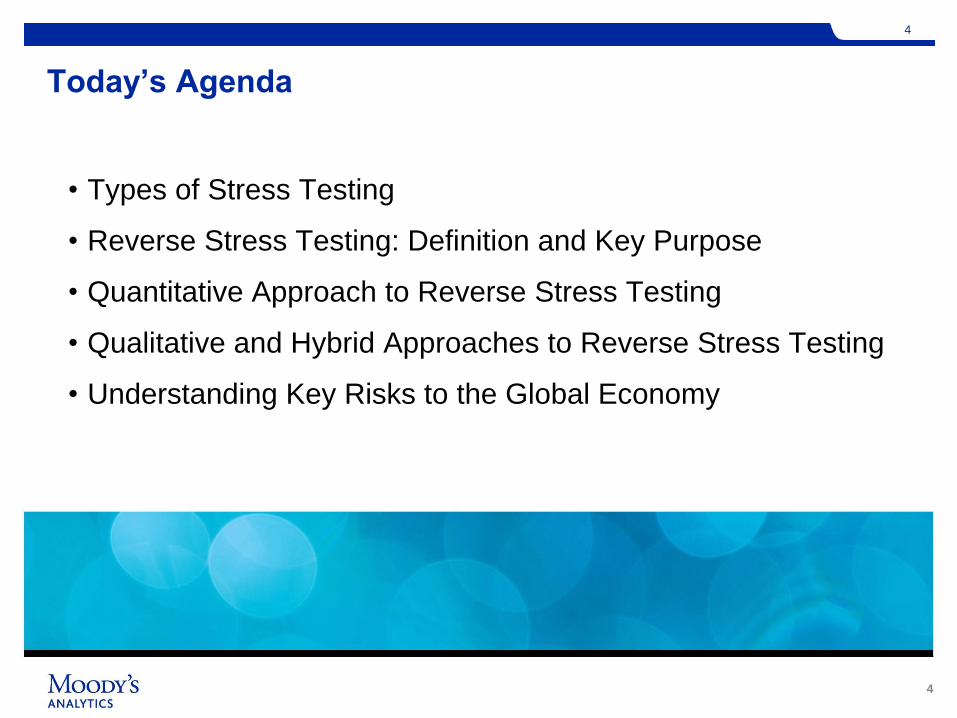

Today‟s Agenda

• Types of Stress Testing

• Reverse Stress Testing: Definition and Key Purpose

• Quantitative Approach to Reverse Stress Testing

• Qualitative and Hybrid Approaches to Reverse Stress Testing

• Understanding Key Risks to the Global Economy

5

5

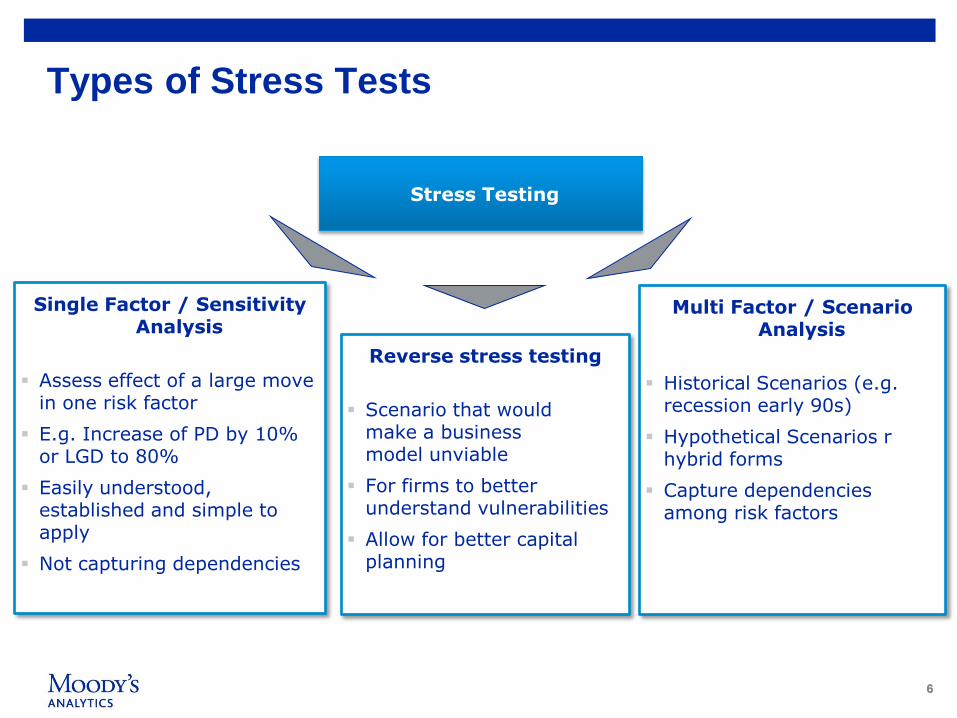

Stress Testing

66

Single Factor / Sensitivity Analysis

Assess effect of a large move in one risk factor

E.g. Increase of PD by 10% or LGD to 80%

Easily understood, established and simple to apply

Not capturing dependencies

Stress Testing

Multi Factor / Scenario Analysis

Historical Scenarios (e.g. recession early 90s)

Hypothetical Scenarios r hybrid forms

Capture dependencies among risk factors

Types of Stress Tests

Reverse stress testing

Scenario that would make a businessmodel unviable

For firms to betterunderstand vulnerabilities

Allow for better capital planning

77

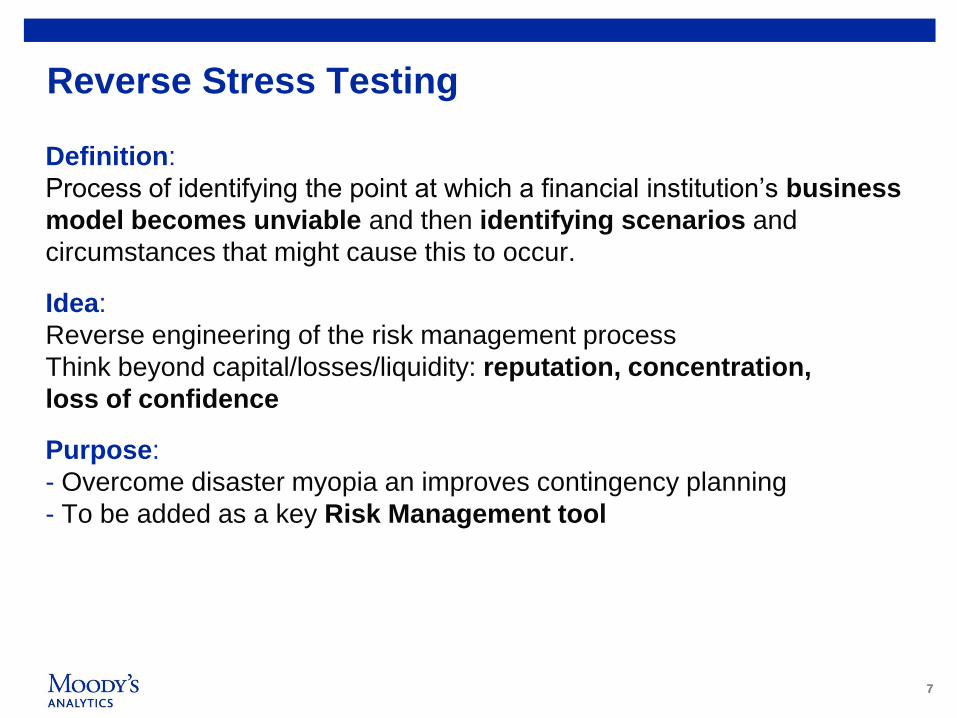

Reverse Stress Testing

Definition:

Process of identifying the point at which a financial institution‟s business

model becomes unviable and then identifying scenarios and

circumstances that might cause this to occur.

Idea:

Reverse engineering of the risk management process

Think beyond capital/losses/liquidity: reputation, concentration,

loss of confidence

Purpose:

- Overcome disaster myopia an improves contingency planning

- To be added as a key Risk Management tool

8

8

Quantitative Reverse Stress Testing

99

What the Regulator says

“We are proposing to introduce a „reverse-stress test‟ requirement, which

would apply to banks, building societies, CRD investment firms and insurers,

and would require firms to consider the scenarios most likely to cause

their current business model to become unviable”

“A key objective of the reverse stress testing is to overcome disaster

myopia and the possibility that a false sense of security might arise from

regular stress testing in which institutions identify manageable impacts”

“Our aim is to ensure that firms more fully explore „Tail Risks‟ which, if they

were to crystallize, would cause counterparties and investors to lose

confidence in them, so that a firm is more aware of its business model

vulnerabilities when making strategic business decisions, when contingency

planning, and when considering its risk management arrangements”

Financial Service Authority CP 08/24, PS 09/20 and GL32

1010

Reverse Stress Testing – Identifying Unmanageable Impacts

What losses lead to dropping below a minimum capital ratio X and what

events and business lines could cause these losses?

When a financial institution should be recapitalized under a given (macro)

scenario?

What risk factors drive the losses and their connections with portfolio‟s

performance (e.g. insolvency, bankruptcy…etc.)?

What are the hidden vulnerabilities of my business model?

Is there any relationship between the Stress Testing and the Reverse

Stress Testing outcomes? Reconciliation?

Moody‟s Analytics can “reverse engineer” via the RiskFrontierTM Trial-by-

Trial capability which specific factors could cause the business model to

become unviable: hidden vulnerabilities and unmanageable impacts that

are not detected in the stress testing analysis

1111

The Portfolio Loss Distribution

Pro

bab

ilit

y o

f lo

ss

Loss

Aa

1 in 2000

A

1 in 1000

Aaa

1 in 5000

Extreme

tail

event

Expected loss

0

Unexpected loss

Economic Capital

Capital Zone: Capital required to cover and protect the

shareholder from potential economic losses

(unexpected negative changes in economic value)

within a given confidence level, over a given time

horizon.

Very low probability of extreme loss

High probability of average loss

1212

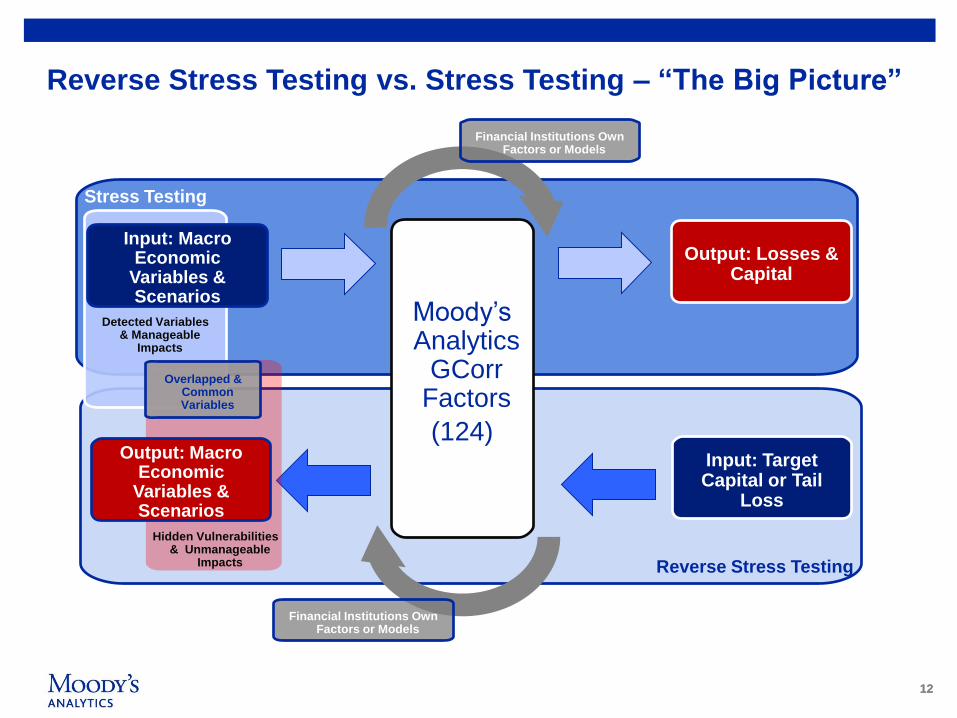

Reverse Stress Testing vs. Stress Testing – “The Big Picture”

Stress Testing

Output: Losses & Capital

Reverse Stress Testing

Moody‟s Analytics

GCorrFactors

(124)Input: Target Capital or Tail

Loss

Input: Macro Economic

Variables & Scenarios

Output: Macro Economic

Variables & Scenarios

Overlapped & Common Variables

Hidden Vulnerabilities & Unmanageable

Impacts

Detected Variables & Manageable

Impacts

Financial Institutions Own Factors or Models

Financial Institutions Own Factors or Models

1313

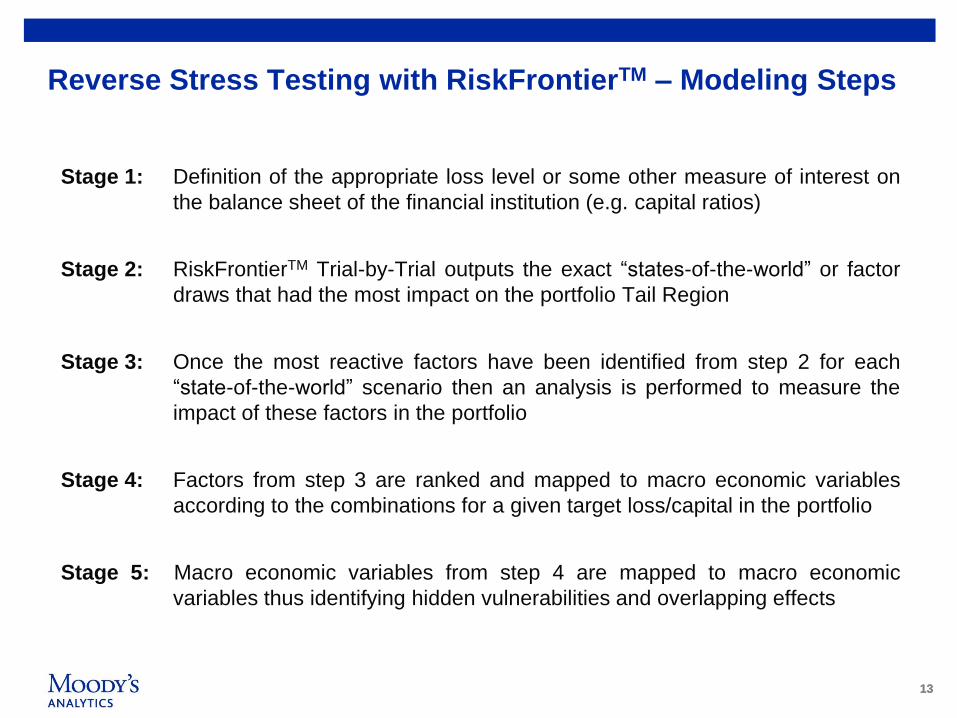

Reverse Stress Testing with RiskFrontierTM – Modeling Steps

Stage 1: Definition of the appropriate loss level or some other measure of interest on

the balance sheet of the financial institution (e.g. capital ratios)

Stage 2: RiskFrontierTM Trial-by-Trial outputs the exact “states-of-the-world” or factor

draws that had the most impact on the portfolio Tail Region

Stage 3: Once the most reactive factors have been identified from step 2 for each

“state-of-the-world” scenario then an analysis is performed to measure the

impact of these factors in the portfolio

Stage 4: Factors from step 3 are ranked and mapped to macro economic variables

according to the combinations for a given target loss/capital in the portfolio

Stage 5: Macro economic variables from step 4 are mapped to macro economic

variables thus identifying hidden vulnerabilities and overlapping effects

1414

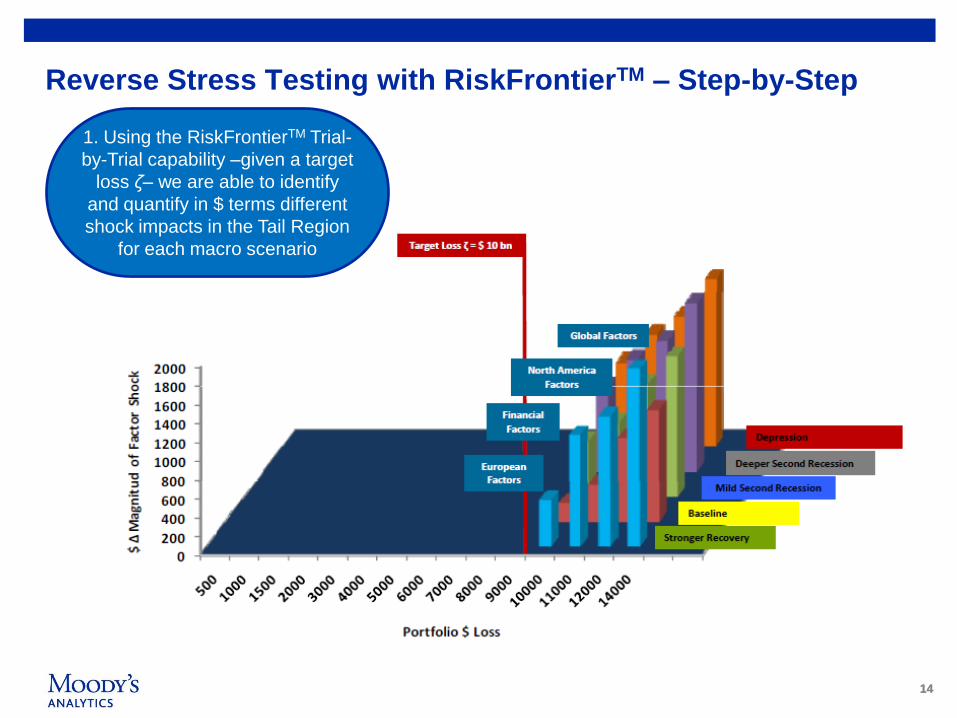

Reverse Stress Testing with RiskFrontierTM – Step-by-Step

1. Using the RiskFrontierTM Trial-

by-Trial capability –given a target

loss ζ– we are able to identify

and quantify in $ terms different

shock impacts in the Tail Region

for each macro scenario

1515

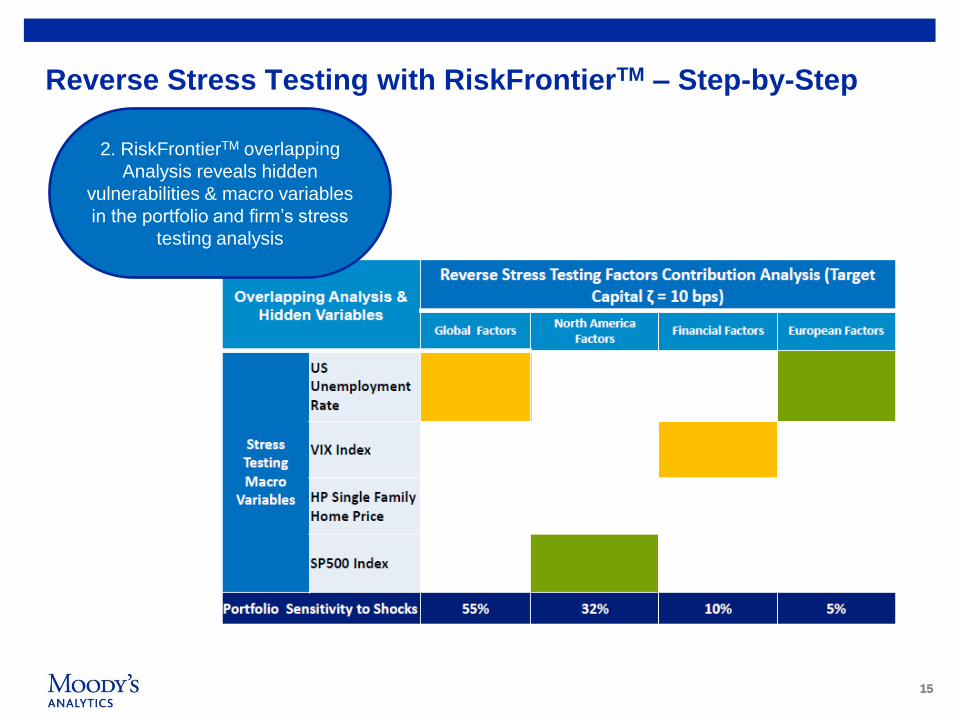

2. RiskFrontierTM overlapping

Analysis reveals hidden

vulnerabilities & macro variables

in the portfolio and firm‟s stress

testing analysis

Reverse Stress Testing with RiskFrontierTM – Step-by-Step

1616

Reverse Stress Testing with RiskFrontierTM – Step-by-Step

0

2000

4000

6000

0 500 1000 1500 2000

Cap

ital

Mil

lio

ns

Tail Exposure

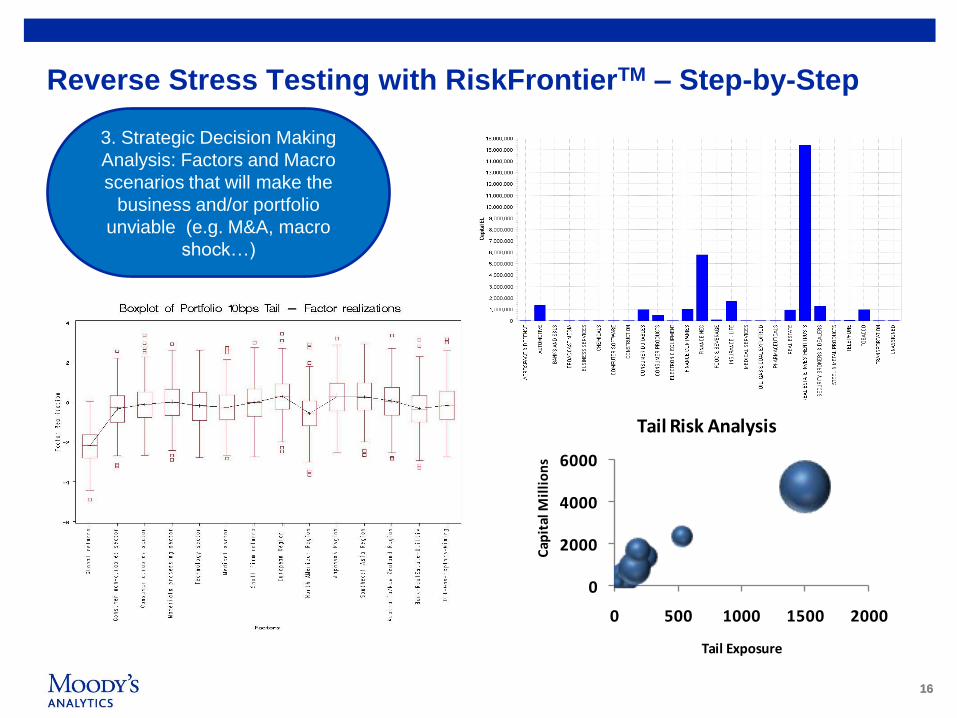

Tail Risk Analysis

3. Strategic Decision Making

Analysis: Factors and Macro

scenarios that will make the

business and/or portfolio

unviable (e.g. M&A, macro

shock…)

1717

Reverse Stress Testing with RiskFrontierTM – Step-by-Step

4. Moody‟s Analytics Reverse

Stress Testing Reports help

senior management to put in

place capital contingency plans

and to develop the firm‟s risk

appetite, business strategy and

risk limits

1818

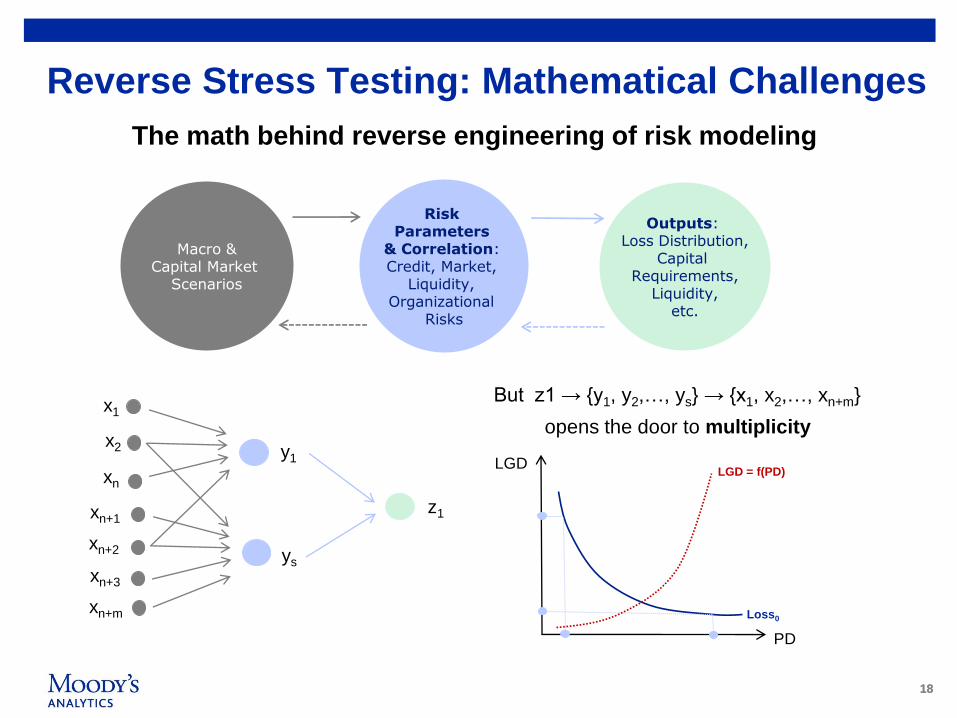

The math behind reverse engineering of risk modeling

Macro &Capital Market

Scenarios

Risk Parameters

& Correlation: Credit, Market,

Liquidity, Organizational

Risks

Outputs: Loss Distribution,

Capital Requirements,

Liquidity,etc.

x1

x2

xn

xn+1

xn+2

xn+3

xn+m

y1

ys

z1

But z1 → {y1, y2,…, ys} → {x1, x2,…, xn+m}

opens the door to multiplicity

PD

LGD

Loss0

LGD = f(PD)

Reverse Stress Testing: Mathematical Challenges

1919

The math behind reverse engineering of risk modeling

Macro &Capital Market

Scenarios

Risk Parameters

& Correlation: Credit, Market,

Liquidity, Organizational

Risks

Outputs: Loss

Distribution,Capital

Requirements,etc.

x1

x2

xn

xn+1

xn+2

xn+3

xn+m

y1

ys

z1

From PD, LGD, Correlation and other Risk

Parameters to Consistent Macro and Capital

Market Scenarios:

Multiplicity is still an issue!

Identification problems to be dealt with.

Reducing the dimension of the Macro Scenarios

(factor analysis) could match the two dimensions

Reverse Stress Testing: Mathematical Challenges

2020

Squeeze Box Approach to Stress Testing

Consider year-on-year log-returns of 4 major indices at monthly frequency:

DJEuroStoxx 50, FTSE 100, S&P 500, SPTSX60 (Jan 01 – Sep 10)

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

DJEUROSTOXX50 FTSE100 SP500 SPTSX60

2121

Squeeze Box Approach to Stress Testing

Return correlation is strong and growing…

DJEuro

Stoxx 50FTSE 100 S&P 500

SPTSX

60

DJEuro

Stoxx 501

FTSE 100 0.99 1

S&P 500 0.92 0.92 1

SPTSX 60 0.87 0.87 0.92 1

2001-2005

DJEuro

Stoxx 50FTSE 100 S&P 500

SPTSX

60

DJEuro

Stoxx 501

FTSE 100 0.98 1

S&P 500 0.96 0.97 1

SPTSX 60 0.94 0.94 0.95 1

2006-2010

DJEuro

Stoxx 50FTSE 100 S&P 500 SPTSX 60

DJEuro

Stoxx 501

FTSE 100 0.98 1

S&P 500 0.94 0.95 1

SPTSX 60 0.91 0.91 0.93 1

2001-2010

2222

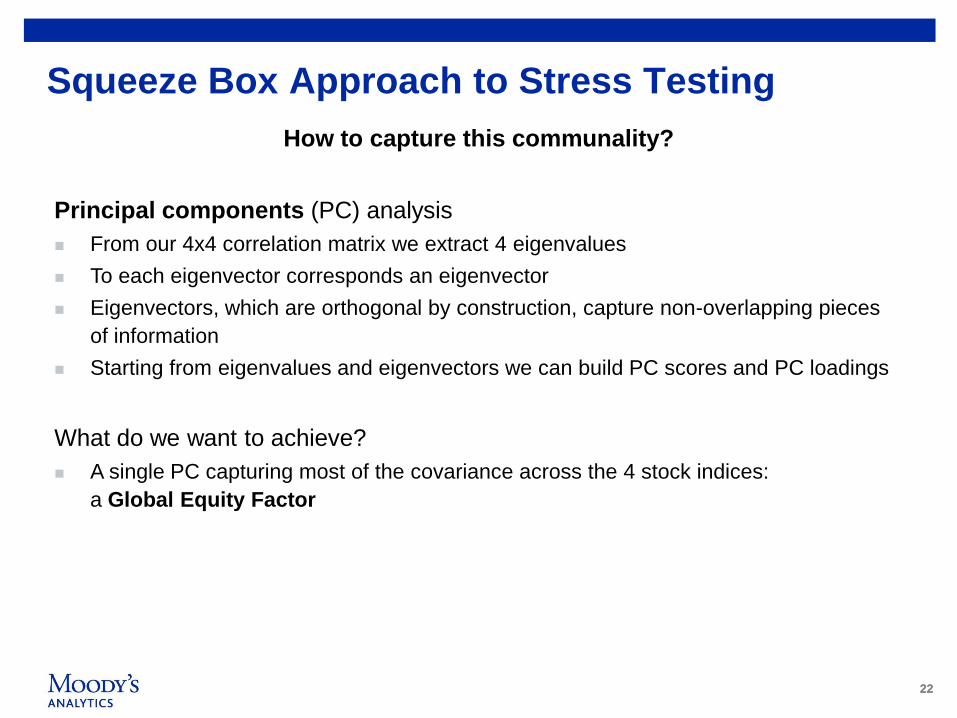

Squeeze Box Approach to Stress Testing

How to capture this communality?

Principal components (PC) analysis

From our 4x4 correlation matrix we extract 4 eigenvalues

To each eigenvector corresponds an eigenvector

Eigenvectors, which are orthogonal by construction, capture non-overlapping pieces

of information

Starting from eigenvalues and eigenvectors we can build PC scores and PC loadings

What do we want to achieve?

A single PC capturing most of the covariance across the 4 stock indices:

a Global Equity Factor

2323

Squeeze Box Approach to Stress Testing

The PC 1, or GEF, captures most of the variance in equity returns

0

10

20

30

40

50

60

70

80

90

100

PC1 PC2 PC3 PC4

% of explained variance

-6

-5

-4

-3

-2

-1

0

1

2

3

4

01

02

03

04

05

06

07

08

09

10

2424

Squeeze Box Approach to Stress Testing

1- Model the GEF conditional on different macroeconomic scenarios

2- Link GEF with Risk Parameters: PD, LGD, Correlations, etc

3- Condition our original stock indices on the GEF forecasts

to get predictions across alternative scenarios.

DJ EuroStoxx 50 FTSE 100 S&P 500 SPTSX 60

GEF

Condition GEF on Alternative Macro Scenarios

Condition DJ EuroStoxx 50 FTSE 100 S&P 500 SPTSX 60 on GEF

Link to

Risk Parameters

2525

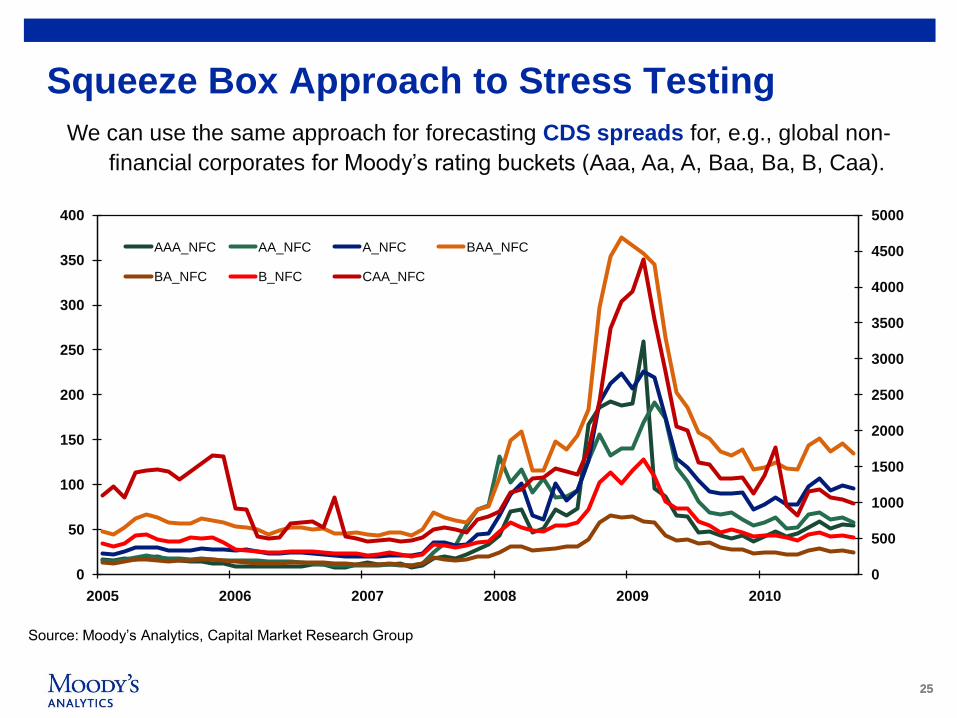

Squeeze Box Approach to Stress Testing

We can use the same approach for forecasting CDS spreads for, e.g., global non-

financial corporates for Moody‟s rating buckets (Aaa, Aa, A, Baa, Ba, B, Caa).

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

0

50

100

150

200

250

300

350

400

2005 2006 2007 2008 2009 2010

AAA_NFC AA_NFC A_NFC BAA_NFC

BA_NFC B_NFC CAA_NFC

Source: Moody‟s Analytics, Capital Market Research Group

2626

Squeeze Box Approach to Stress Testing

-4

-2

0

2

4

6

8

05 06 07 08 09 10

0

10

20

30

40

50

60

70

80

90

100

PC1 PC2 PC3 PC4 PC5 PC6 PC7

% of explained variance

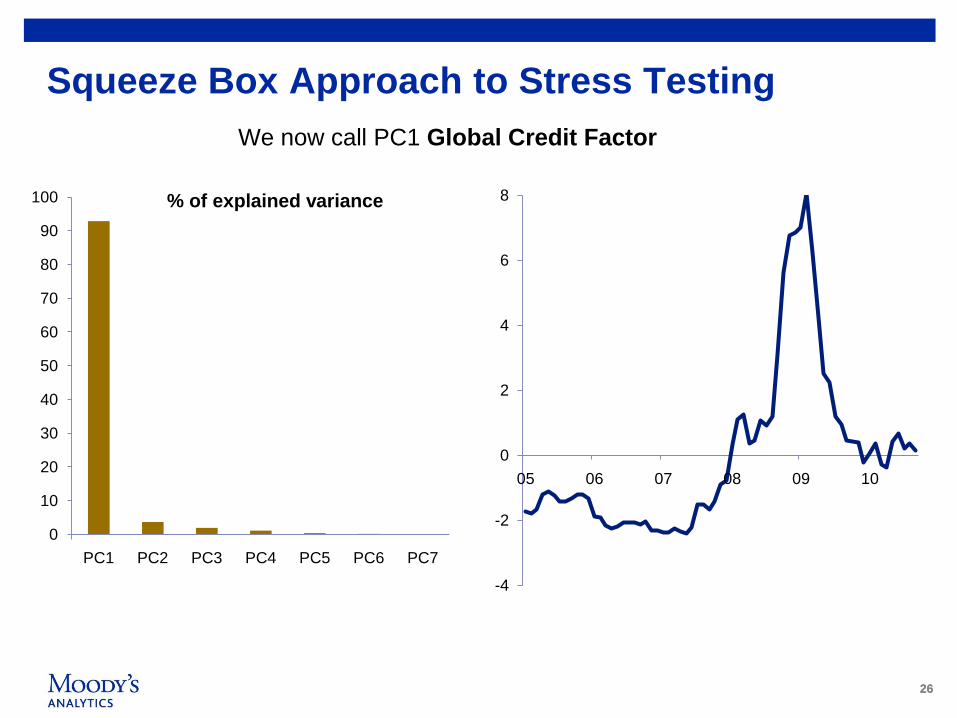

We now call PC1 Global Credit Factor

2727

Squeeze Box Approach to Stress Testing

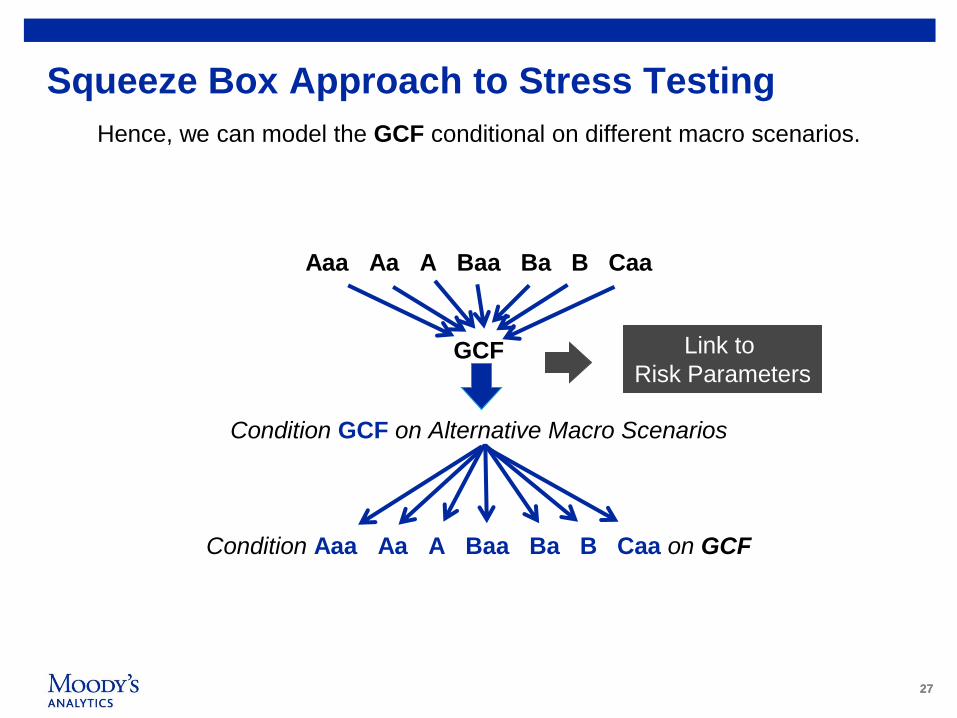

Hence, we can model the GCF conditional on different macro scenarios.

Aaa Aa A Baa Ba B Caa

GCF

Condition GCF on Alternative Macro Scenarios

Condition Aaa Aa A Baa Ba B Caa on GCF

Link to

Risk Parameters

2828

Squeeze Box Approach to Stress Testing

Challenge to model pure macroeconomic series:

REAL BUSINESS

CYCLE

Econ Activity

MONETARY

CYCLE

Inflation

CREDIT

CYCLE

Rates

0

5

10

15

20

25

30

35

PC1 PC2 PC3

% of explained variance

29

29

Qualitative and Hybrid Reverse Stress Testing

3030

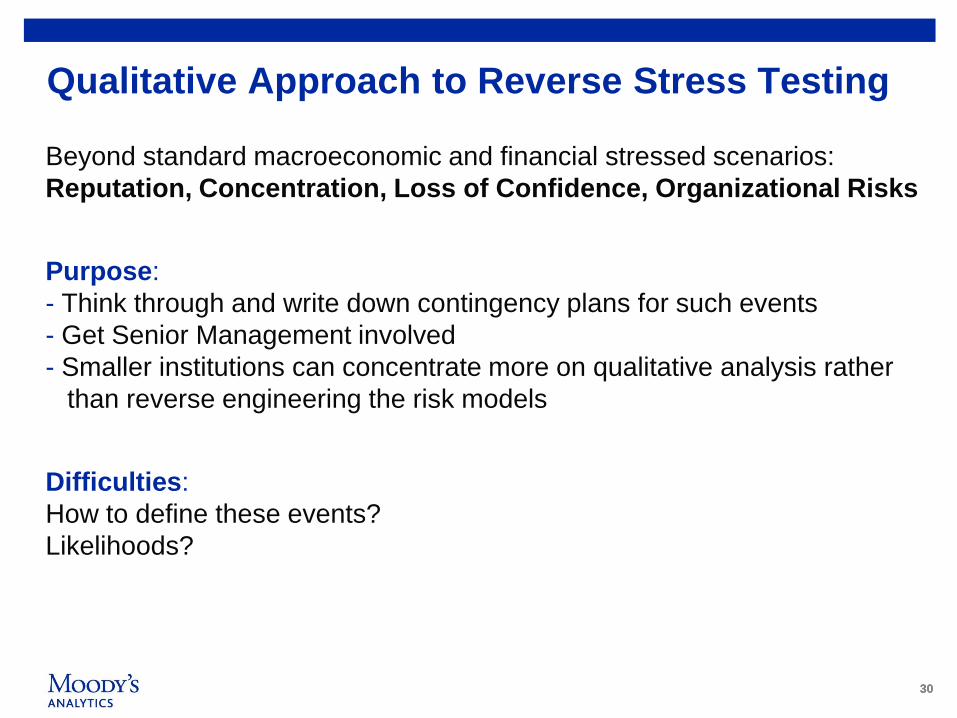

Qualitative Approach to Reverse Stress Testing

Beyond standard macroeconomic and financial stressed scenarios:

Reputation, Concentration, Loss of Confidence, Organizational Risks

Purpose:

- Think through and write down contingency plans for such events

- Get Senior Management involved

- Smaller institutions can concentrate more on qualitative analysis rather

than reverse engineering the risk models

Difficulties:

How to define these events?

Likelihoods?

3131

Hybrid Approach to Reverse Stress Testing

Stress on Business

Model

Qualitative Analysis: Key Risks

Potential Scenarios

Time Series of Macro &Financial

Series

Implement scenarios into Risk

Management Tools

Calculate Losses,

Capital and Liquidity

Qualita

tive R

evers

e

Stre

ss T

estin

g

Quantita

tive S

tandard

Stre

ss T

estin

g

32

32

Today‟s Key Risks to the Global Economy

33

» European Sovereign Debt and Banking Crisis

» Deflationary Trap in U.S.

» Global Protectionism and Currency Wars

» Chinese Hard Landing

» Crashing Commodity Price Bubble

» Runaway Global Inflation

» Terrorist Attack

» U.S. Fiscal Crisis and $ Crash

Top Global Economic Threats

Based on expected value of global economic loss

34

0

200

400

600

800

1,000

Jan-10 Mar-10 May-10 Jul-10 Sep-10 Nov-10

Greece

Ireland

Portugal

Spain

Italy

U.K.

Sources: Bloomberg, Moody‟s Analytics

Spread between 10-year sovereign and German bunds, bp

Europe‟s Sovereign Problems Boil Over

35

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10

Core CPI

Wage Growth

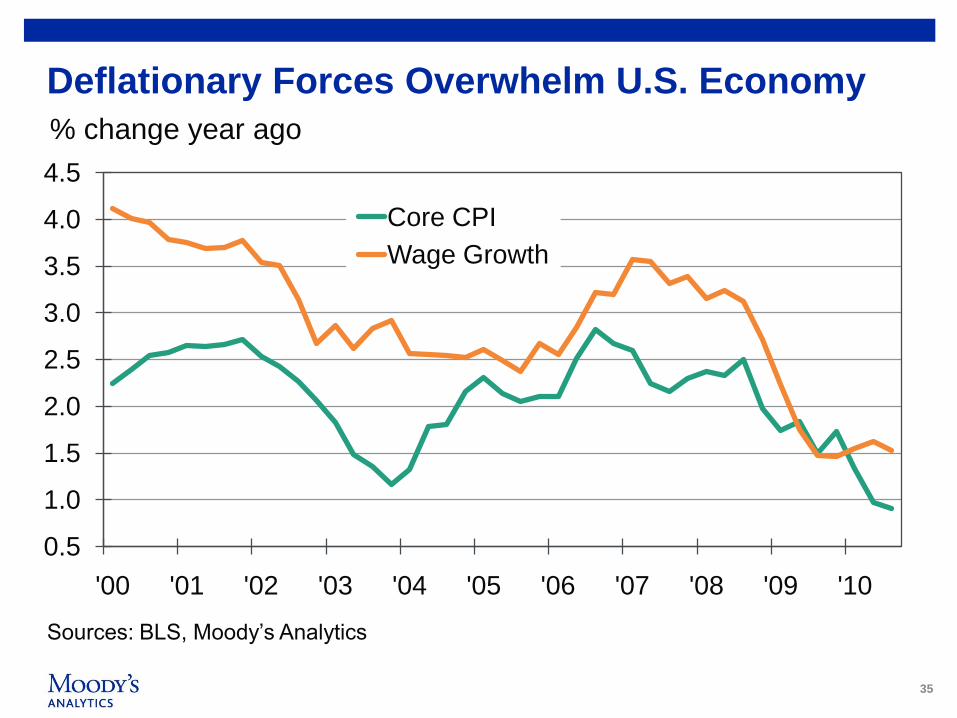

Deflationary Forces Overwhelm U.S. Economy

Sources: BLS, Moody‟s Analytics

% change year ago

36

-5

0

5

10

15

0 5 10 15 20

% C

hange in R

eal E

ffective

Exchange R

ate

Change in International Reserves as a % of GDP

Chile

India

Turkey

Brazil

Mexico

Korea

Poland

Indonesia

RussiaMalaysia

Philippines

China

Taiwan

ThailandSingapore

Hong Kong

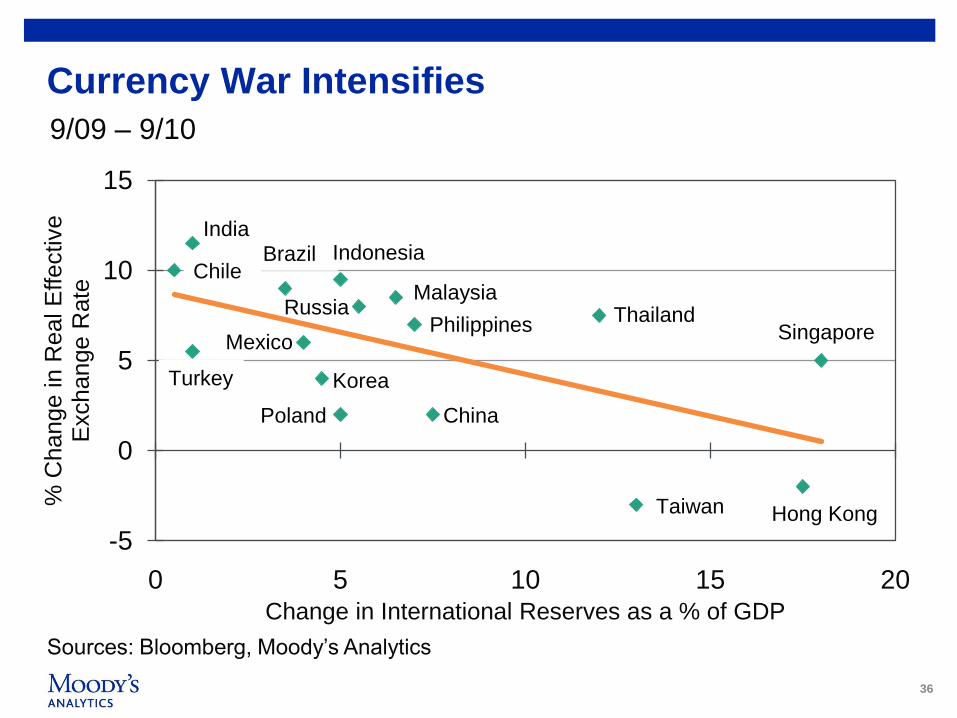

Currency War Intensifies

Sources: Bloomberg, Moody‟s Analytics

9/09 – 9/10

37

37

Concluding Remarks

• Reverse Stress Testing represents a challenge to risk management

traditional thinking.

• Pushes management to think about multiple business risks, beyond

capital, liquidity and losses.

• Its application and practical advantages yet to be tested.

Is it here to stay?

• Started in the UK and other European countries; if successful it could

expand to the global economy.

• Combination of quantitative and qualitative analysis to be expected

38

38

Q&A Session

39

39

Thank you!

www.moodys.com

Dr. Mark Zandi, Chief Economist

Moody‟s Analytics

Email: [email protected]

Dr. Christian Thun, Senior Director

Moody‟s Analytics

Email: [email protected]

Dr. Juan Licari, Senior Director

Moody‟s Analytics

Email: [email protected]

4141

© 2010 Moody‟s Analytics, Inc. and/or its licensors and affiliates (collectively, “MOODY‟S”). All rights reserved. ALL INFORMATION CONTAINED HEREIN IS

PROTECTED BY COPYRIGHT LAW AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER

TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN

WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY‟S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY‟S from sources believed by it to be accurate and reliable. Because of the possibility of human or

mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. Under no circumstances shall

MOODY‟S have any liability to any person or entity for (2) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or

otherwise) or other circumstance or contingency within or outside the control of MOODY‟S or any of its directors, officers, employees or agents in connection with

the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (1) any direct, indirect, special,

consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if MOODY‟S is advised in advance of the possibility

of such damages, resulting from the use of or inability to use, any such information. The ratings, financial reporting analysis, projections, and other observations, if

any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or

recommendations to purchase, sell or hold any securities. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS,

MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE

BY MOODY‟S IN ANY FORM OR MANNER WHATSOEVER. Each rating or other opinion must be weighed solely as one factor in any investment decision made

by or on behalf of any user of the information contained herein, and each such user must accordingly make its own study and evaluation of each security and of

each issuer and guarantor of, and each provider of credit support for, each security that it may consider purchasing, holding, or selling.