Embed Size (px)

Citation preview

Returns in goods and services tax

A brief overview

byShri Sunil Lahane,

Dy Commissioner, Sales Tax

Outline

• What’s special about GST return?• Overview of Returns to be submitted by regular

tax payers• Process of filing of return and the rationale• Returns to be filed by some specific tax payers• ITC Matching and Reversal• Correction of Returns• Annual Return• First and final Return• How can we make it happen?

2

Why Returns

• Mode for transfer of information to tax administration

• To declare tax liability for a given period

• Furnish details about the taxes paid in accordance with that return

• Compliance verification program of tax administration

• Providing necessary inputs for taking policy decision

• Management of audit and anti-evasion programs of tax administration

3

Features of Tax Returns in GST

• Based on transactions – Invoice based

• Designed for system based matching of Input Tax Credit and other details (import, export etc.)

• Auto-population from details of outward supplies

• Auto-reversal of ITC in case of mismatch

• Concepts of ledgers – cash, ITC and liability

• No revised returns – changes through amendments to original details

4

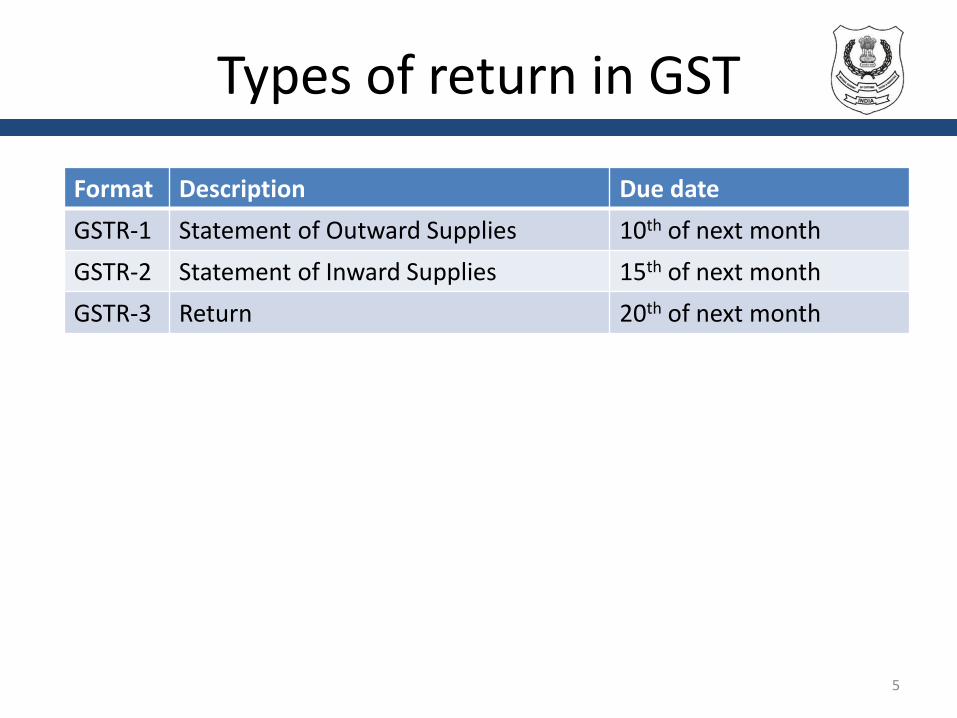

Types of return in GST

Format Description Due date

GSTR-1 Statement of Outward Supplies 10th of next month

GSTR-2 Statement of Inward Supplies 15th of next month

GSTR-3 Return 20th of next month

5

Statement of Outward Supplies

• Basic details – GSTIN, Name, period, Turnover in last financial year – mostly auto-populated

• Invoice level details

B2B supplies, interstate and intrastate, interstate B2C supplies more than Rs. 2.5 lakh– GSTIN of recipient

– Invoice details – Number, date, Value, HSN/SAC, Taxable value

– Tax – IGST, CGST, SGST – Rate and Tax amount

– Place of Supply (relevant for interstate supplies)

Section 37 of the CGST Bill6

Statement of Outward Supplies

• Details of supplies to customers– HSN/SAC

– Place of Supply

– Aggregate value

– Tax – IGST, CGST, SGST – Rate and tax amount

• Credit and Debit Notes – linkage to original invoice– Document number

– Original Invoice Number

– Deferential amount and deferential tax

Section 37of the CGST Bill7

Statement of Outward Supplies

• Reverse Charge

• Details of exports – with and without payment of tax– Invoice details, Shipping Bill/Bill of Export, tax details

• Details of exempt, Nil rated and Non-GST supplies– Interstate and Intrastate B2B and B2C supplies

• Tax paid on advances and adjustment of advances

• Amendment of any of the above details filed in previous months

Section 37 of the CGST Bill8

Statement of Inward Supplies

• Basic Details• Statement of Inwards Supplies

– Auto-populated from Statements of outward supplies– Claimed – non auto-populated– Supplies attracting reverse charge

• Invoice level details– As in statement of outward supplies– Input Tax Credit available, eligibility and availed

• Import of Services– Invoice details, IGST rate and amount, ITC

Section 38 of the CGST Bill 9

Statement of Inward Supplies

• Details of credit and debit notes– Auto-populated from statement of outward

supplies

– Claimed – non auto-populated

• ISD Credit received

• TDS Credit received

• Other details of inward supplies– From exempt/composition suppliers

– Exempt, nil rated and non-GST supplies

Section 38 of the CGST Bill 10

Return

• Auto-populated based on GSTR-1 and GSTR-2• Outward Supplies

– B2B and B2C inter and intra state supplies– Exports– Revision of tax of previous periods

• Inward Supplies– Inter and intra state supplies received– Imports– Amendment to tax of previous periods– Credit to ITC Ledger

Section 39 of the CGST Bill11

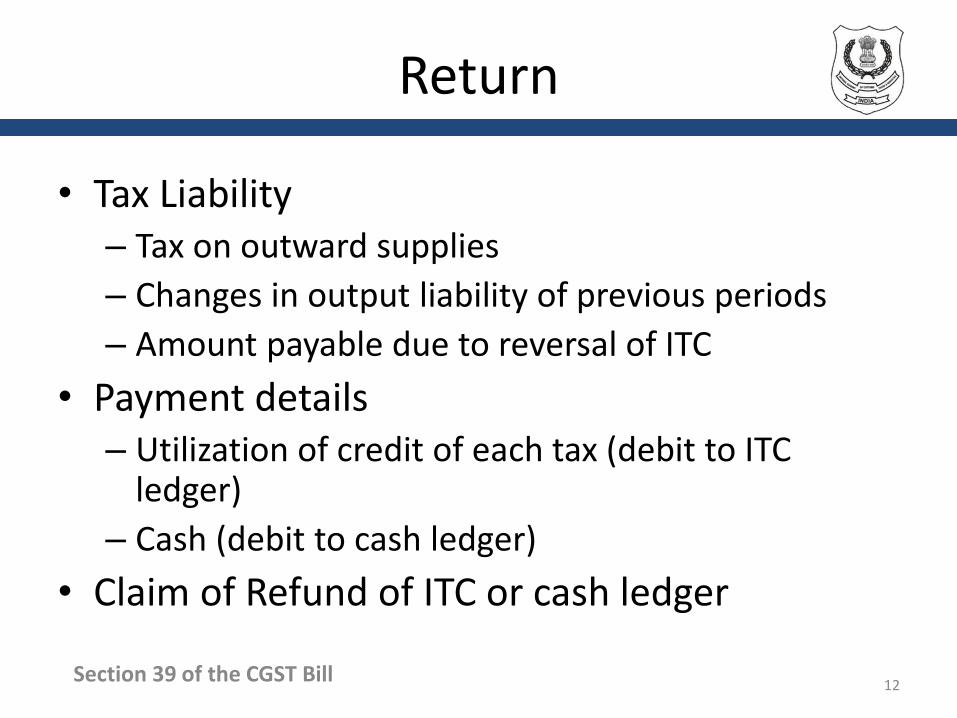

Return

• Tax Liability– Tax on outward supplies

– Changes in output liability of previous periods

– Amount payable due to reversal of ITC

• Payment details– Utilization of credit of each tax (debit to ITC

ledger)

– Cash (debit to cash ledger)

• Claim of Refund of ITC or cash ledger

Section 39 of the CGST Bill12

Salient features

• Mostly based on timely filing of GSTR-1• GSTR-2 shall be auto-populated based on GSTR-1• Some additional details to be entered in GSTR-2

– Claims of ITC not auto-populated– Details of import– Other inward supplies

• HSN Classification– 4 digit compulsory for turnover above Rs. 5 crore– 2 digit optional in first year and compulsory from

second year

13

How does Return get filed

• All registered persons to file GSTR-1by 10th

– Can be filed during the month as well

• GSTR-2 of all registered persons allowed to view their inward supplies uploaded by their suppliers

• GSTR-2 of taxpayers to be auto-populated after 10th

• Recipients to prepare GSTR-2 based on auto-populated details

• Recipients to upload details not auto-populated• GSTR-2 to be filed by 15th

14

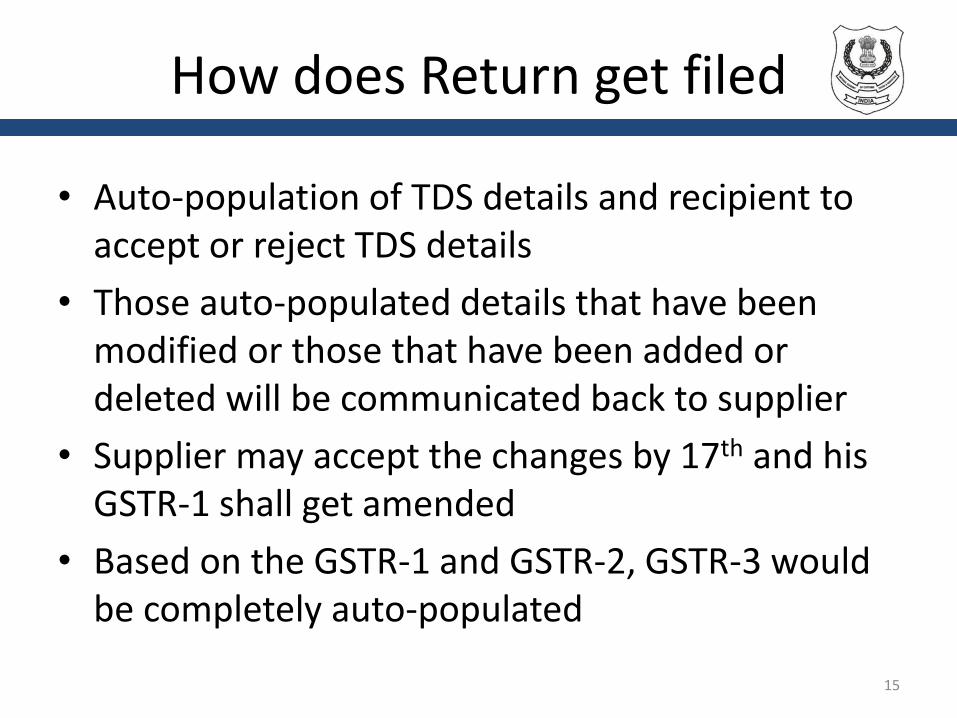

How does Return get filed

• Auto-population of TDS details and recipient to accept or reject TDS details

• Those auto-populated details that have been modified or those that have been added or deleted will be communicated back to supplier

• Supplier may accept the changes by 17th and his GSTR-1 shall get amended

• Based on the GSTR-1 and GSTR-2, GSTR-3 would be completely auto-populated

15

How does Return get filed

• Tax payers can avail ITC credit for payment of taxes and pay the rest by debiting their cash ledger

• Tax payer to credit the cash ledger by making payment by filling challan on GSTN

• Submit GSTR-3 and at the same time following actions happen simultaneously– ITC ledger gets credited by the ITC availed as per GSTR-2– ITC ledger gets debited by the ITC utilized for payment of

taxes– Cash ledger gets credited by the amount of TDS claimed– Cash ledger get debited by the amount utilized for

payment of taxes

16

Types of return in GST

Format Description Due date

GSTR-1 Statement of Outward Supplies 10th of next month

GSTR-2 Statement of Inward Supplies 15th of next month

GSTR-3 Return 20th of next month

GSTR-4 Return for Compounding suppliers 18th of month in next quarter

GSTR-5 Return for Non-resident suppliers 20th of next month

GSTR-6 Return for ISD 13th of next month

GSTR-7 Return for TDS Deductors 10th of next month

17

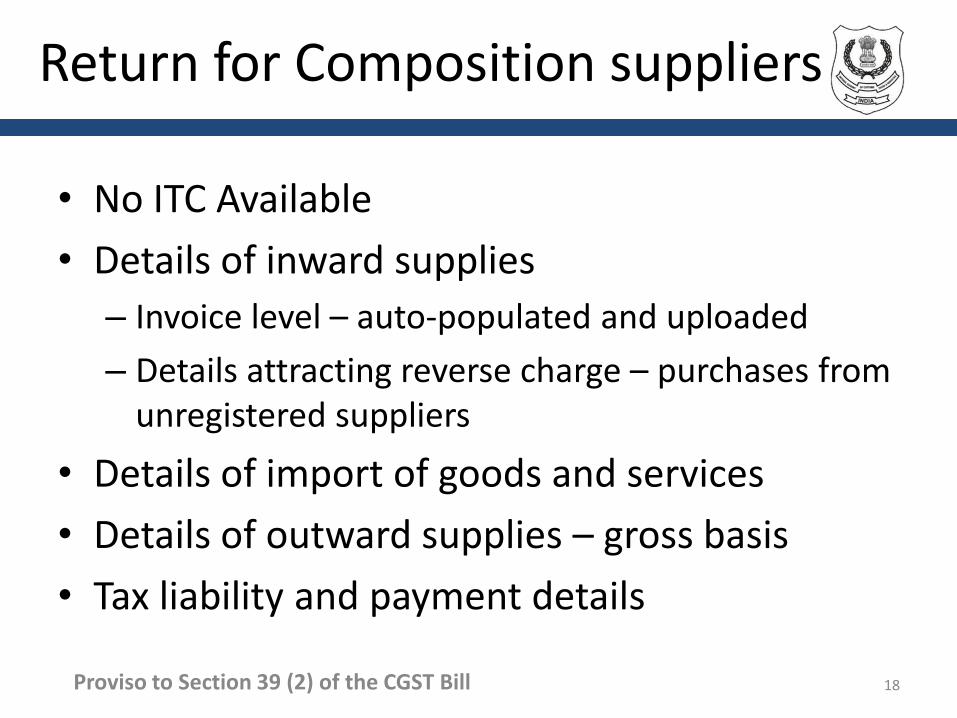

Return for Composition suppliers

• No ITC Available

• Details of inward supplies

– Invoice level – auto-populated and uploaded

– Details attracting reverse charge – purchases from unregistered suppliers

• Details of import of goods and services

• Details of outward supplies – gross basis

• Tax liability and payment details

Proviso to Section 39 (2) of the CGST Bill 18

Return for Non-resident tax payers

• Backed by advance tax

• They can take credit of IGST on import and pass on credit on all supplies

• Credit of tax paid on imports

• Details of outward supplies

– Similar to GSTR-1

• Details of tax paid – ITC ledger and cash ledger

• Closing stock of goods

19

Return for ISD

• Details of inward supplies– Similar to GSTR-2

• Details of credit distributed– GSTIN of recipient

– Invoice details

– Credit distributed – IGST, CGST, SGST

• ITC account– ITC received

– ITC distributed

Section 39 (4) of the CGST Bill20

Return for TDS Deductors

• Pertains to cash ledger and not credit ledger

• TDS details

– GSTIN of deductee

– Invoice details – number, date value

– TDS details – rate and amount – IGST, CGST, SGST

• Details of payment – only by cash ledger

• TDS amount cannot be paid by debiting ITC ledger

Section 39 (3) of the CGST Bill21

ITC Matching Reversal – Why at all?

• Seamless availability of credit in one State of tax paid in another State

• IGST Model– Credit of IGST paid in one State available for payment of local

tax in another State – Central Government to transfer funds to State

– Credit of local taxes paid in one State available for payment of IGST in another State – State Government to transfer funds to Centre

• No Government can transfer funds unless collection of tax is ensured

• But recipient have to be given an opportunity to claim ITC• ITC matching and auto-reversal is the workable solution

22

What gets matched

• Tax invoices [Section 31]– Issued for every supply by every taxpayer other

than composition

– Including supplementary and revised invoices

• Debit and credit notes [Section 34]– To be issued only against an invoice

– To be issued before end of September of next year

– Conditions and restrictions about discounts regulated by law

Sections 31 and 34 of the CGST Bill23

24

Typical Invoice Details

Buyer’s GSTIN /Departmental ID/ Address Invoice Number & DateHSN Code/Accounting Code for each line item of an invoice in case of multiple codes in an invoice

Taxable ValueInvoice Value Tax Rate

Tax Amount (CGST & SGST or IGST &/or cess) Place of Delivery/Place of Supply

only if different than the location of buyer

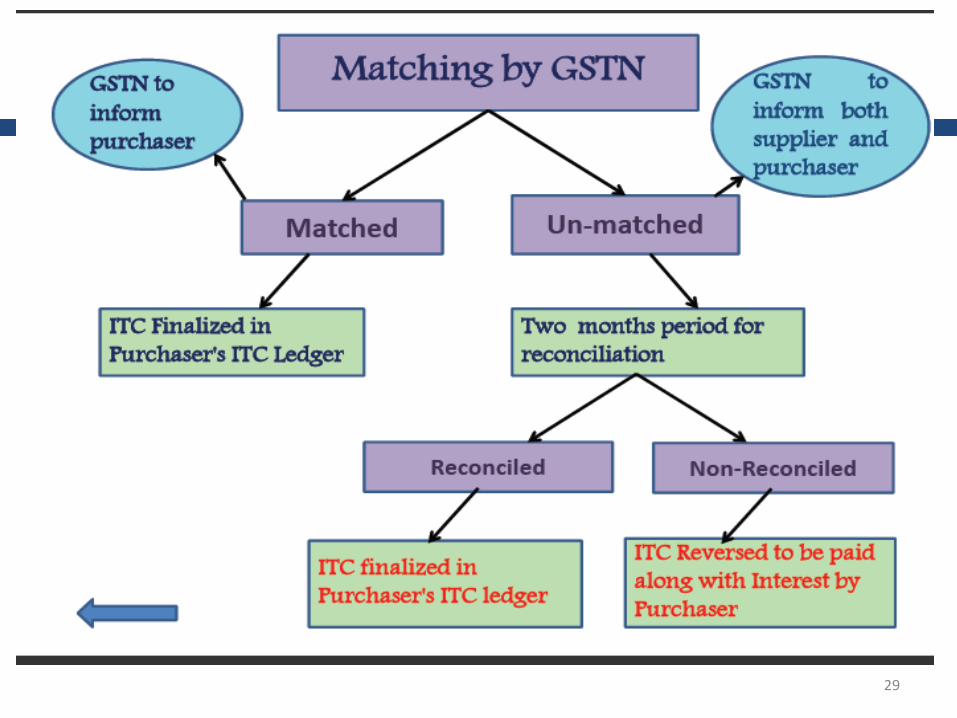

ITC Matching and Reversal

• All returns filed with payment of taxes are treated as valid return.

• Self assessment – ITC to be allowed on filing of return– Provisionally allowed for payment of taxes in that return as

per his claim [Section 41 of the CGST Bill]

• After filing of return– ITC claims checked for duplication

– ITC claims matched with tax paid in valid returns

– Claims that come as a result of auto-population taken as matched if tax paid by supplier

– Uploaded invoices matched with supply invoices

25

ITC Matching and Reversal

• Duplicate claims communicated to recipient and unmatched claims communicated to both

• ITC claimed on duplicate invoice added in next return

• Unmatched invoices– Either supplier owns up in next return and uploads it

as part of his next month’s GSTR-1 – match in that return cycle

– Otherwise, ITC claim remains unmatched in next month return and gets added in next return

Section 42 of the CGST Bill26

Reclaim of reversal

• Any invoice uploaded in a month that does not match with a supply invoice in a valid return gets reversed in two months

• Once reversed, recipient should not reclaim it again unless uploaded by supplier

• At any time it gets automatically reclaimed if supplier uploads the invoice

• Interest on reversal– Refund of interest on reclaim – supplier to pay interest

on delayed payment of tax

Section 42 of the CGST Bill27

Matching of Credit Notes

• Process in previous slides applicable to invoices and debit notes – both lead to payment of tax in the hands of supplier and ITC in hands of recipient

• Credit Note– Reduction of tax liability in hands of supplier

– Reduction of ITC in hands of recipient

• Same matching and auto-reversal process but different consequence– The reduction of output liability claimed gets added to his

liability if recipient does not own it and reduce his ITC clam

– Same two month cycle

28

29

30

Valid Return

• Unless tax is paid, the return does not go for matching – ITC for invoices that have been uploaded but tax not paid will get reversed

• ITC claimed in a return that is not valid available only for utilization for liability in that return

• No tax payer can file a monthly return unless he has filed a valid return for previous month’s return

• If a State has transferred funds to Centre and supplier fails to pay SGST, the recipient shall pay the SGST credit used but not paid

• If a State has transferred funds to Centre and supplier fails to pay IGST, the recipient shall pay the IGST credit used but not paid

31

Correction in returns

• No Revision of returns– As per the return taxes have already been paid and fund

transfers already settled

– No significance as the basis now is individual transaction

• All changes through amendments in subsequent returns

• If an invoice has been left out in GSTR-1 or GSTR-2 –can be uploaded in subsequent returns

• If and invoice has been wrongly entered but remains unmatched – can be amended in subsequent returns

32

Correction in returns

• Post transaction changes to be done through debit or credit notes

• Other details like B2C supplies can be amended in subsequent returns

• Delayed uploading coupled with payment of interest

• All changes, credit or debit notes to be carried out before September of the next financial year

– To enable any auto-reversal before Annual Return

33

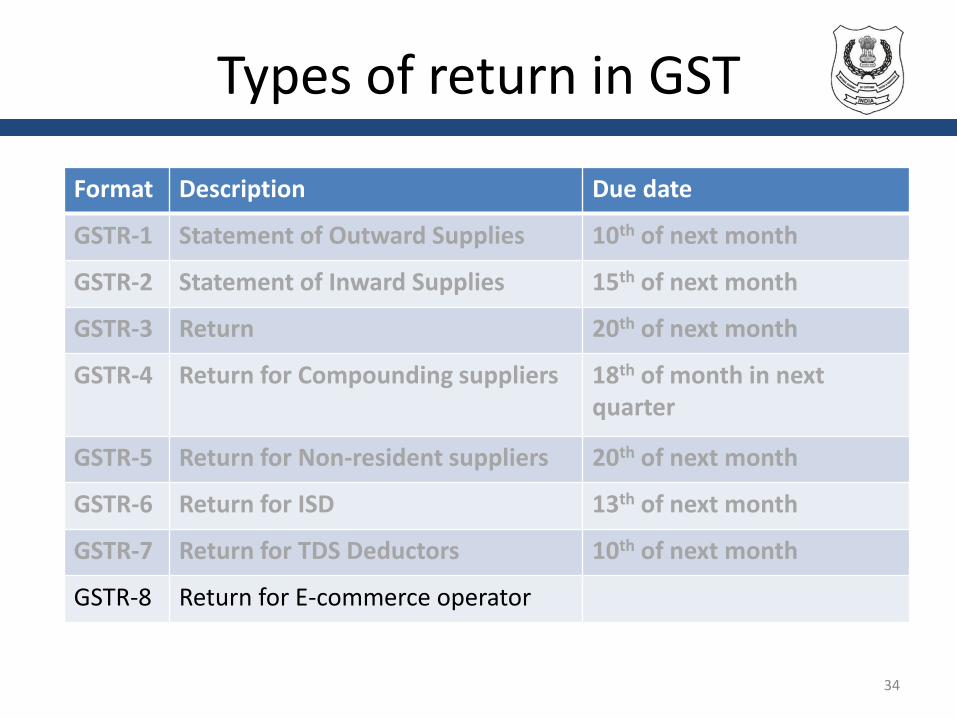

Types of return in GST

Format Description Due date

GSTR-1 Statement of Outward Supplies 10th of next month

GSTR-2 Statement of Inward Supplies 15th of next month

GSTR-3 Return 20th of next month

GSTR-4 Return for Compounding suppliers 18th of month in next quarter

GSTR-5 Return for Non-resident suppliers 20th of next month

GSTR-6 Return for ISD 13th of next month

GSTR-7 Return for TDS Deductors 10th of next month

GSTR-8 Return for E-commerce operator

34

Annual Return

• Annual summary of all transactions ( in GSTR-9)• Accounts to be certified by Chartered Accountant

etc. if turnover more than Rs. 2 Crore• Personal Details• Details of Expenditure

– Purchases – goods/services – intra/inter state– Imports

• Details of Income– Supplies – goods/services – intra/inter state – Exports

Section 44 of the CGST Bill35

Annual Return

• Account of taxes payable and paid

• Arrears of taxes

• Refunds

• Profit and Loss

• Reconciliation Statement

• Not to be filed by ISD, TDS Deductor, Casual Taxpayer, and Non resident taxpayer

Section 44 of the CGST Bill36

First and Final Returns

• First Return– Required when the liability to register and pay tax

arose before grant of registration.

– To pay tax where supplies were made before registration

– To take credit on receipts that happened before registration

• Final Return(GSTR-10)– On closure of business

– Reversal of credit on goods in stock

Sections 40 and 45 of CGST Bill37

Post Return Filing

• System based notice in case of failure to file return

• Late fee – Rs. 100 per day

• Non-filer assessment

• Analysis of Returns

• System based scrutiny

• Scrutiny Assessments

• Compliance verification

38

3939

THANK YOU39