Embed Size (px)

Citation preview

1 © Wärtsilä

Marine Money 28th Annual Marine Money Week The Pierre Hotel NY City, NY 18 June 2015

John Hatley PE

VP Ship Power Wartsila No. Am. [email protected]

Retrofitting Handy Bulkers – Business Case & Alternative Financing

Pace Ralli

Co-Founder Clean Marine Energy LLC [email protected]

Agenda

2 © Wärtsilä

What ?

History & Competitive Forces Shale Gas, Oil Resources

Oil Price Shock !

Business Case Stress Test

Appendix

Business Case Details

Business Case Handysize Bulker Returns

Financing Alternatives

Agenda

3 © Wärtsilä

What ?

History & Competitive Forces Shale Gas, Oil Resources

Oil Price Shock !

Business Case Stress Test

Appendix

Business Case Details

Business Case Handysize Bulker Returns

Financing Alternatives

A history moment…

4 © Wärtsilä

Source: http://www.google.com/imgres?imgurl=http://www.gstatic.com/tv/thumb/movieposters/742/p742_p_v7_aa.jpg&imgrefurl=http://google.com/search?tbm%3Disch%26q%3DHow%2Bthe%2BWest%2BWas%2BWon&h=720&w=480&tbnid=kcq_aqWoOuqw4M:&zoom=1&tbnh=160&tbnw=106&usg=__yuSwwygUDbOjmASN9n-Zr_b_Meo=&docid=c47h65w6_PrzpM&itg=1&hl=en

Early Westward Expansion

5 © Wärtsilä

Homestead land grab… first settler waves faced severe hardship from land; incumbent natives, many were friendly & some not.

Source: https://thislifeofwander.wordpress.com/2011/04/09/go-west-young-man/

Go West Young Man

Next Wave Westward Expansion

6 © Wärtsilä

1860’s Transcontinental Railroad

Waves of settlers rode the rail… many homesteaded the rich western lands, flourished, and prospered.

Source: http://www.pkwy.k12.mo.us/INTRA/PROFESSIONAL/STUDENT_WORK/west_web/scotts.htm

Moral of Story

7 © Wärtsilä

LNG Fuel for emissions sensitive coastal & port areas; rare win-win: OPEX savings + emissions reduction.

Source: http://bridgtonhistory.org/Portals/0/photos/narrowgauge/RR%2013%20-%20Full.jpg

Don’t miss the train !

US & Canada 18 LNG Fuel Contracted Vessels… + a number Gas Ready Vessels … exceeds $3.5 Billion CAPEX Commitments

Competition Model Forces

Government Legislation: Political power exercising market influence: Trade Behavior, Emissions

Porter’s 5 Forces + 1… Government Legislation exercises market influence… emissions

Global Non Conventional Shale Gas & Oil

22 June 2015

Source:http://www.eia.gov/analysis/studies/worldshalegas/

Recoverable Gas Resource: 7,796 tcf

Global Recoverable Shale Gas Resource

22 June 2015

Top 5 hold over half of world’s shale gas resource

tcf Source: http://www.eia.gov/conference/2013/pdf/presentations/kuuskraa.pdf

Global Gas Production

22 June 2015

Source: LNG for Marine Transportation USA, Houston TX, June 12, 2013; David Sweet President Natural Gas Roundtable http://lngmarineevent.com/presentations/2013/David-Sweet.pdf

BILLION M3

USA is world’s #1 gas producer… US Shale gas production, by itself, exceeds all nations except Russia

US #1 Shale Resources

12 © Wärtsilä

1,161 tcf gas & 120 billion barrels oil

Development rapid with technology advances in horizontal drilling, fracking, and computer seismic abilities.

In 5 years US became world’s largest producer of gas

Strong infrastructure & know how

Source:http://www.eia.gov/conference/2013/pdf/presentations/kuuskraa.pdf

China #2 Shale Gas Resource

22 June 2015

1,115 tcf gas & 32.8 billion barrels oil

Development slow despite vast shale gas potential

Geological challenges fundamentally different than US

Water scarcity & environmental concerns

Limited infrastructure & know how

Source:http://www.eia.gov/conference/2013/pdf/presentations/kuuskraa.pdf

Argentina #3 Shale Gas Resource

22 June 2015

802 tcf gas & 27.0 billion barrels oil

Shale Gas: possibly best shale basin outside N. America

Active with mostly vertical gas wells

Source:http://www.eia.gov/conference/2013/pdf/presentations/kuuskraa.pdf

Shale Gas

15 © Wärtsilä

Shale Oil

16 © Wärtsilä

2014 Oil Production

17 © Wärtsilä

US vaults to 3rd in world crude production in 2014

Source: http://en.wikipedia.org/wiki/List_of_countries_by_oil_production

Source: http://www.businessinsider.com/citi-saudi-arabia-wont-win-this-oil-standoff-2014-11 18 © Wärtsilä

Profits negative… Severe Pain

Profits squeezed… Manageable Pain

45 $/BBL

Key Oil Production Cost

60$/BBL

Total Liquids Production

Brent Breakeven Price

Government Breakeven Budgets

19 © Wärtsilä

Severe shortfalls @ prices under 100$/BBL, present oil glut & soft prices challenge sustainability beyond short run

Source: https://alfinnextlevel.files.wordpress.com/2014/04/oil_breakeven_deutsche_bank_oct_14.png

60 $/BBL

Agenda

20 © Wärtsilä

What ?

History & Competitive Forces Shale Gas, Oil Resources

Oil Price Shock !

Business Case Stress Test

Appendix

Business Case Details

Business Case Handysize Bulker Returns

Financing Alternatives

Handysize Route… Baton Rouge to Veracruz

21 © Wärtsilä

Mostly Emission Control Area route “ECA” Bound…

Foreign Flag Vessel & US Corporation

37,000 DWT Capacity

Speed 13 knots… single Screw … 2 Stroke Power 6,625 HP ( 4,940 kW )

Manning & SOLAS Compliant

Certified Major Class Society

Source: http://www.dnv.com.cn/Binaries/Green%20Dolphin%20-%20brochure_tcm142-518925.pdf

Then… 5 August 2014

22 Wärtsilä

Recent Prices: LS180 1% 636 $/mt… LSMGO 0.1% 971 $/mt

Source: http://www.bunkerworld.com/prices/port/us/hou/

Cargo Owner Transport safely at optimal cost reliably

23 © Wärtsilä

Shipper captures competitive advantage, compelling $1.4 Millions savings every 5 years per ship

Ship Owner A fair return capturing risks

24 © Wärtsilä

Investor Competitive Advantage… LNG returns highest & preserves cargo owner savings = capture market share

Vessel Stress Test

BASELINE LNG Revenue $8.8 M CAPEX $31 M Bank Interest 5.0 % LNG Price 431 $/mt Engine M&R $67K / yr

Sensitivity Rankings Revenue CAPEX LNG Price Bank Interest Rate

25 © Wärtsilä

Main investment attributes focus executive attention where it matters most.

Deviation

ROE

Banker Are risks understood & I’m repaid !

26 © Wärtsilä

Banker finds debt cover is weakest on MDO fuel, LNG is strongest.

27 © Wärtsilä

Years

EBIT

MDO Fuel

HFO + Scrubber

LNG Fuel

Banker Are risks understood & I’m repaid !

LNG has strongest EBIT… Depreciation 10 Year MACRS ½ Year Convention… Dry docking years 5,10,15,20

Agenda

28 © Wärtsilä

What ?

Competitive Forces Shale Gas Resources

Oil Price Shock !

Business Case Stress Test

Appendix

Business Case Details

Business Case Handysize Bulker Returns

Financing Alternatives

Brent Crude Oil Prices

29 © Wärtsilä

Source: http://www.nasdaq.com/markets/crude-oil-brent.aspx?timeframe=1y

THEN

Crude severe price drop past year as abundant supplies face weak demand

Nadir

Nadir… 26 January 2015

30 Wärtsilä

Prices : LS180 1% 430 $/mt… LSMGO 0.1% 613 $/mt

Source: http://www.bunkerworld.com/prices/port/us/hou/

Owner At fair return capturing risks of oil fall 26 Jan 2015

31 © Wärtsilä

LNG competitive advantage retains millions savings for shipper but returns narrow for investor amidst oil glut steep price dive.

Recent Nadir 26 Jan 2015

Fuel Stress Test

THEN 5 August 2014

11.3% @ LNG 475 $/mt 7.3% @ MDO 971 $/mt 8.5% @ HFO 636 $/mt

32 © Wärtsilä

Deviation

ROCE

Nadir 26 January 2015

11.7% @ LNG 431 $/mt 12.4% @ MDO 613 $/mt 11.3% @ HFO 430 $/mt

LNG returns robust despite steep drop in MDO and HFO: oil irrational conditions not sustainable in long run! Greatest volatility MDO, least volatility LNG.

Agenda

33 © Wärtsilä

What ?

History & Competitive Forces Shale Gas, Oil Resources

Oil Price Shock !

Business Case Stress Test

Appendix

Business Case Details

Business Case Handysize Bulker Returns

Financing Alternatives

Widespread Shift to LNG

as Marine Fuel

Fuel Cost Spread Emissions Regulation

Short Window of Opportunity to Build the

LNG Infrastructure

LNG fueling driven by economic and regulatory forces

Commodity spread favors LNG, but remains uncertain

• One undeniable fact… Dual-fuel is better than single fuel • Optionality ensures the lowest future fuel costs

Technology Risk: mitigate risk that the LNG fueling technology will not work

Risks of Conversion

Risk of LNG Supply: mitigate risk that the LNG supply will not be available in time

Risk of LNG Bunkering: mitigate risk that the bunker infrastructure will not be ready

Commodity Risk: risk that the commodity spread could decrease

However, the upfront capital requirement remains a barrier, and switching to dual-fuel has payback risks

• These risks can be understood and effectively mitigated • Requires certainty of LNG supply and distribution

CME is a first-mover in LNG infrastructure for ship fuel

• CME has partnered with WesPac Midstream to build a vertically integrated platform, funded by Oaktree Capital

• Ability to tie together supply, distribution and conversion finance into a cost-effective fueling option for ship owners

Best-in-class platform partnership established in 2014

WesPac constructs, owns and operates LNG infrastructure projects in select locations to serve major high horsepower transportation hubs and high-traffic marine ports, guaranteeing LNG supply

CME is the marine arm of WesPac focusing on sourcing demand by converting ships to fuel with LNG, and developing the distribution infrastructure for LNG delivery by building small-scale LNG vessels

Oaktree is the majority owner of the WesPac / CME partnership and has allocated significant capital to the development of LNG infrastructure for marine and transportation purposes

• Founded in 1998 based in Irvine, CA and Houston, TX

• Geographic emphasis on North America, with 40+ employees

• Since 2011 WesPac has focused on LNG liquefaction facilities, storage and transportation

• Projects can be customized and located to meet specific customer requirements

• Capital investment and operational costs are paid through a mid- to long-term tolling arrangement

• Natural gas commodity and transportation costs are a direct pass through to customer

• Founded in 2012, based in South Norwalk, CT

• Affiliate of MidOcean Marine, a US Jones Act ship owning company, with 30 years experience in owning US-flagged vessels

• Leading construction of the first North American LNG bunker barge designed to begin service in 2016

• Offers a proprietary Emissions Compliance Service Agreement (ECSA) to solve ship owner's capital dilemma of funding an expensive LNG conversion

• Completed deal in August 2014 for partnership with WesPac/Oaktree

• $95 billion AUM private equity firm founded in 1995 based in Los Angeles, CA

• The largest single investor in shipping assets worldwide

• Believes in the short window of opportunity to effectively put ‘steel in the ground’ to serve the future of marine fueling and investing in the first phase of infrastructure projects

• Other well-known portfolio companies include Kinder Morgan, Ports America, and Southern Star

• Has committed $300 million to fund WesPac / CME project equity

Supply - developing a strong foothold in strategic ports

Distribution – investing in LNG bunkering vessels

Barge Description

Builder Conrad Orange Shipyard

Class XA1 Liquefied Gas Tank Barge, Vessel Type IIG, Oceans

Flag US Flag, unmanned barge

Cargo Tank Gaztransport & Technigaz SAS - Mark III Flex membrane tank

Cargo LNG to -163C temperature, maximum 0.5 specific gravity

Deadweight 1,112 LT

LOA 222’

Beam 49’

Draft 8’

Tank Volume Total net volume @ 100% - about 2,200 cubic meters Total net volume @ 98% filling height: about 2,156

FCSA STRUCTURE

0 1 2 3 4 5 6 7 8 9 10 Year

LSMGO

WesPac/CME offers a capital efficiency solution that leverages 3rd party capital to fund capex investments without adding to the ship’s cost-basis, transitioning capex to opex

LNG Con

vers

ion

Finance Term • Ship owner pays no upfront capital for ECA compliance

• Fuel payer continues to pay what they would have paid anyway, with some immediate shared savings during term

• After the financing term, the ship benefits from 100% of the fuel cost savings for the remaining life of the asset

• Compliance becomes a NPV positive activity with no capital requirement… ship owner can use it’s capital for other more accretive investments

Ann

ual F

uel C

ost

Conversion – providing financing for ships to switch

Currently in Progress – Jacksonville, FL Project Highlights

Lot Size 36 acres

Capacity Up to 300k gallons per day

Expected Commissioning 2Q 2017

Anchor Client TOTE, Inc. - 2 Marlin Class, 3,100

TEU Container ships

Natural Gas Provider AGL Pivotal (NYSE: GAS)

Site Features Marine jetty Bunker barge Trucking manifold Expansion opportunities

Site Information Timing 2nd Quarter 2016

Gas Source

Fortis BC

Volume 250k gpd

Fueling Logistics

Bunker barge

Status In Construction

Currently in Progress – Tilbury, BC

Moral of Story

44 © Wärtsilä

LNG Fuel for emissions sensitive coastal & port areas; rare win-win: OPEX savings + emissions reduction.

Source: http://bridgtonhistory.org/Portals/0/photos/narrowgauge/RR%2013%20-%20Full.jpg

Don’t miss the train !

US & Canada 18 LNG Fuel Contracted Vessels… + a number Gas Ready Vessels … over $3.5 Billion CAPEX Commitments

APPENDIX Business Case Details

45 Wärtsilä

Financials

46 Wärtsilä

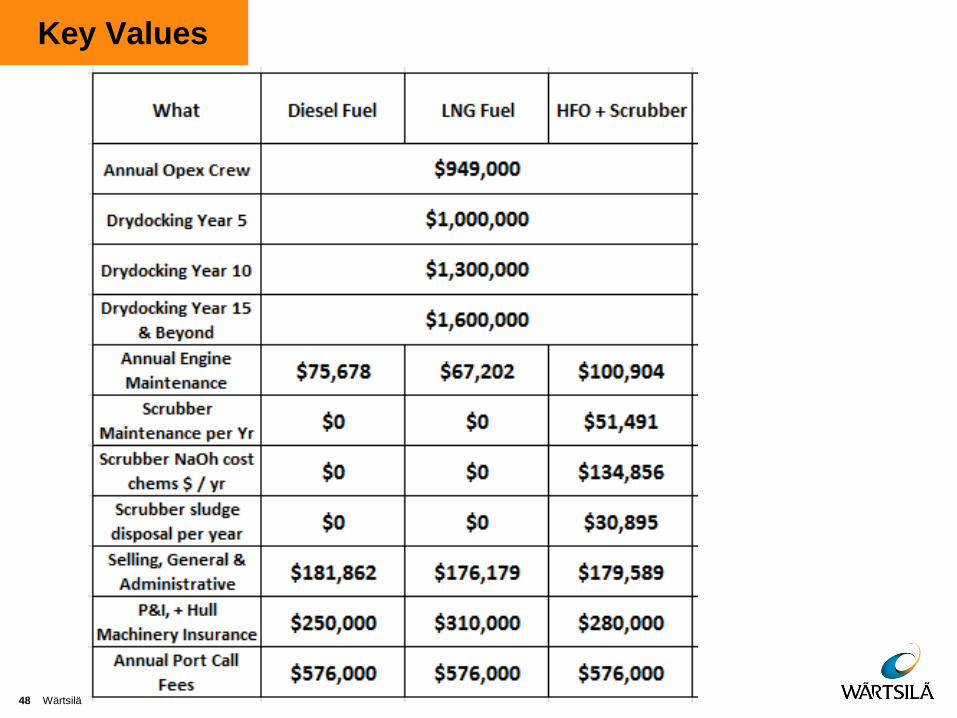

Key Values`

47 Wärtsilä

Key Values

48 Wärtsilä

Fuel Attributes

49 © Wärtsilä

Utilize fuels specific for regional case... As fuels widely vary, the historic dollars per ton or gallon is challenging to use as differing fuels host widely varying energy content, density, value... These values shown are generally representative.