Embed Size (px)

Citation preview

1

Kenneth BanetRetired Senior Partner of Grant Thornton US

Consultant to Grant Thornton China

2

Improving Financial

Performance

3

Principal business purposes are to:◦Increase each others success

◦Maximize earnings

“One for all; all for one”

Partnership

4

Importance of managing financial performance

Counting cash at the end of the year is not management

Financial Management

5

Do you know what each engagement really costs your firm?

Do you know whether each engagement is profitable – or how profitable?

Do your partners know what financial performance objectives are expected of them?

Financial Management

6

Some basics are required

◦A budget from each partner◦A consolidated budget for each department/ office and the firm

◦Reporting of actual hours devoted to each client by all personnel

◦Rate per hour for all personnel

Financial Management

7

Financial Management requires basic information:

◦ An engagement revenue budget from each partner, listing Total revenues expected Collections of revenue by month

Financial Management

8

Financial Management requires basic information

◦ Number of hours required for each engagement By level of personnel By month To complete the engagement

Financial Management

9

Can you recognize where changes are necessary?◦Net revenues◦Salaries and number of personnel◦Operating expenses◦Number of charged hours to clients◦Average rate per hour to be charged to

clients◦Average realization rate of fees

The Budget – a “Plan” or a “Wish”

10

A TOOL◦to create a financial strategy◦to manage the financial strategy

◦to establish partner objectives◦to identify variances ◦to correct variances - timely

A Budget IS

11

Starts with the Partners’ Plans◦Expected revenues for each client◦Expected hours by staff level to complete engagement

◦Expected cost of engagement, including potential profit

The Firm Plan

12

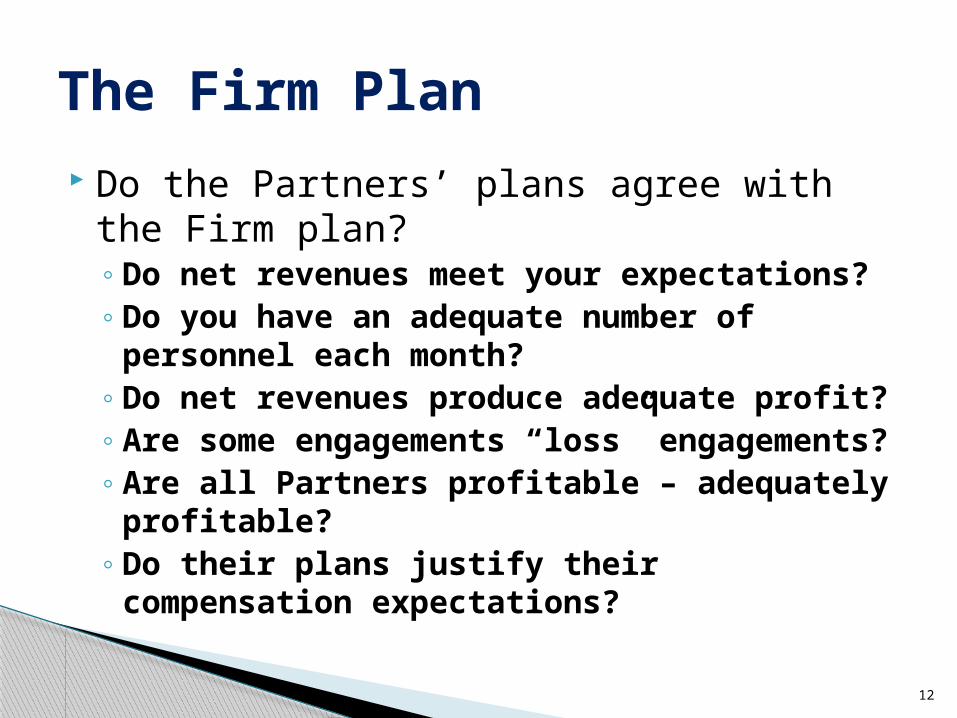

Do the Partners’ plans agree with the Firm plan?◦Do net revenues meet your expectations?◦Do you have an adequate number of

personnel each month?◦Do net revenues produce adequate profit?◦Are some engagements “loss”

engagements?◦Are all Partners profitable – adequately

profitable?◦Do their plans justify their compensation

expectations?

The Firm Plan

13

Time is money

We sell time – ◦Service is a result of our time

Time Reporting

14

We always correctly estimate how many hours it will take to complete an engagement!

All client engagements proceed exactly as planned!

Client financial records are always orderly and complete!

We can always easily obtain the documentation requested!

Time Reporting Myths

15

Therefore, the need for everyone to keep track of the time devoted to each engagement

Daily or weekly time reporting requirement

“Time is money” - “Service is the result of our time”

Time Reporting

16

Converts time to money◦Charge rate per hour - composed of

1. Cost of average salaries by level, plus2. Cost of operating expenses, plus3. Potential profit percent

Often regarded as the “Rule of Thirds”◦But …

What is a Charge Rate?

17

Keeping financial performance “on track”◦Periodic financial statements◦Analysis of key data◦Comparison of data to the budget◦Determine reasons for variations◦Timely corrective actions

Analyzing Variances

18

Operating Metrics◦Financial statement performance

Performance Metrics◦Detail financial measurements

Measurements - Metrics

19

Operating metrics (similar to many companies you audit)

◦Gross Revenues◦Net Revenues◦Realization Rate◦Gross Margin◦Operating Profit

Measurements - Metrics

20

Performance Metrics◦Net rate per hour◦Number of charge hours◦Net revenues per partner◦Gross margin per professional◦Utilization rate◦Number of charge hours per professional

Measurements - Metrics

21

What they tell you◦Where are you compared to budget and

compared to last year?◦Where is corrective action necessary?◦Which engagements are profitable – more

profitable?◦Which partners are profitable – more

profitable?◦Do we have enough or too many staff?◦What goals do I need to set for my partners? And much, much more

Measurements - Metrics

22

Example Firm

For the period ending December 31, 2011

Operating Metrics 运营指标 Actual Budget Actual

2011 2011 2010

实际 2011 年 % 预算 2011 年 % 实际 2010 年 %

Gross revenues from client services 客户服务总收入 ¥ 452,000,000 100.0% ¥ 531,675,000 100.0% 452,600,000 100.0%

Adjustments to gross revenues 毛收入调整

Write-offs 核销 (136,000,000) 30.1% (128,100,000) 31.5% (143,900,000) 31.8%

Net client service revenues 新客户服务收入 316,000,000 69.9%/ 100% 365,261,000 68.7% / 100.0% 308,700,000 68.2% / 100.0%

Salaries and compensation 薪酬与福利

Employees 员工

Salaries of client facing personnel 业务人员薪酬 ¥ xxxxx ¥ xxxxx ¥ xxxxx

Salaries of administrative personnel 行政人员薪酬 ¥ xxxxx ¥ xxxxx ¥ xxxxx

Social taxes 社保 ¥ xxxxx ¥ xxxxx ¥ xxxxx

160,500,000 50.8% 187,014,000 51.2% 164,537,000 53.3%

Gross margin for services 毛利润 155,500,000 49.2% 178,247,000 48.8% 144,163,000 46.7%

Operating expenses 营业成本

Personnel 人员 ¥ yyyyy ¥ yyyyy ¥ yyyyy

Facilities 设施 ¥ yyyyy ¥ yyyyy ¥ yyyyy

Technology 技术 ¥ yyyyy ¥ yyyyy ¥ yyyyy

Marketing and sales 市场和销售 ¥ yyyyy ¥ yyyyy ¥ yyyyy

Travel and entertainment 差旅与业务招待费 ¥ yyyyy ¥ yyyyy ¥ yyyyy

Office supplies and services 办公费用 ¥ yyyyy ¥ yyyyy ¥ yyyyy

Outside services 外部服务 ¥ yyyyy ¥ yyyyy ¥ yyyyy

Risk management 风险管理 ¥ yyyyy ¥ yyyyy ¥ yyyyy

Other expense (income) 其他费用 (收入) ¥ yyyyy ¥ yyyyy ¥ yyyyy

44,633,000 14.1% 51,867,000 14.2% 44,453,000 14.4%

Operating income (loss) 营业收入 ( 亏损 ) ¥ 97,452,100 35.1% ¥ 126,380,000 34.6% 99,710,000 32.3%

23

Kenneth BanetRetired Senior Partner of Grant Thornton US

Consultant to Grant Thornton China

THANK YOU