Embed Size (px)

Citation preview

RETAIL SUPPLY CHAIN CONFERENCE 2015

RETAIL SUPPLY CHAINCONFERENCE 2015

Real People. Real Experiences. Real Education.

Title Sponsor

RETAIL SUPPLY CHAIN CONFERENCE 2015

RETAIL SUPPLY CHAINCONFERENCE 2015

BENCHMARKING EUROPE‘S SUPPLY CHAINS

RETAIL SUPPLY CHAIN CONFERENCE 2015

RETAIL SUPPLY CHAINCONFERENCE 2015

Marc LiebaugDirector Suppliers Contracts & Process Mgmt.METRO LOGISTICS Germany

Peter KlausProf. Business Logistics, Friedrich-Alexander-University, Nuernberg, Member Advisory Board NAGEL-GROUP, Versmold

RETAIL SUPPLY CHAIN CONFERENCE 2015

Agenda.

I. Where we are coming from

II. Benchmarking What? A Bird’s Eyes View on Today’s European Retail Supply Network

III. The Grassroots Level: Three Selected European Retail SC-Practices

1. SC Complexity Reduction: Metro’s unified Inbound Logistics Concept2. Retail Industry Collaboration taken one Step further:

The Metro-Markant Industry Initiative 3. Towards a “supra-adaptive” Supply Network configuration:

Leveraging the capabilities of a Pan-European temp-controlled LTL- net

IV. Benchmarking across the Atlantic? The opportunities !

RETAIL SUPPLY CHAIN CONFERENCE 2015

I-1. Where we are coming from: METRO GROUP

• One of the world’s leading retail and wholesale companies

• Successful stock-listed company

• Presence in more than 2,200 locations in 31 countries

• Around 249,000 employees from 170 nations

• All sales lines are closely linked to online shops

• METRO GROUP: Made for Success!

RETAIL SUPPLY CHAIN CONFERENCE 2015

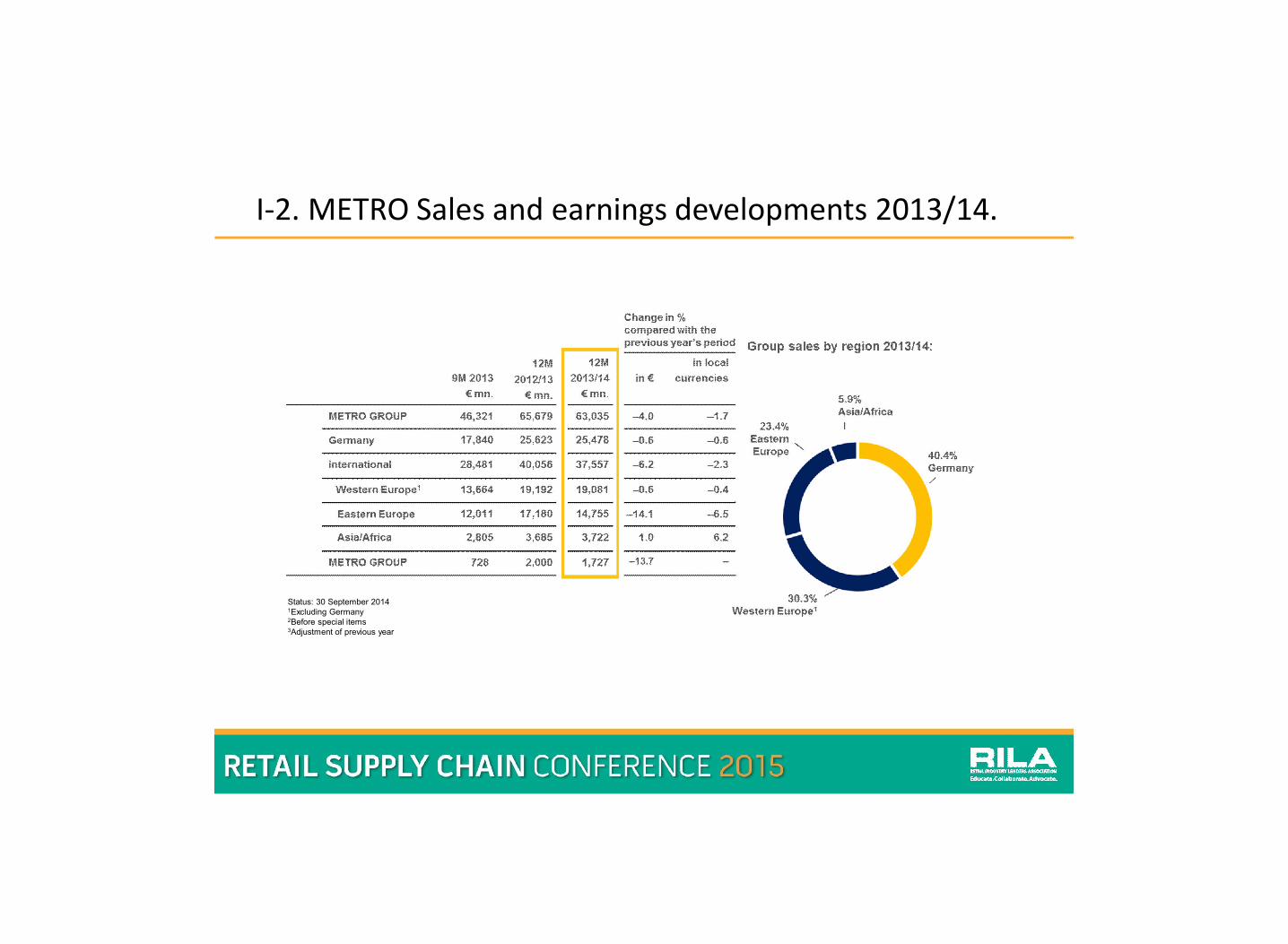

I-2. METRO Sales and earnings developments 2013/14.

Status: 30 September 20141Excluding Germany2Before special items 3Adjustment of previous year

RETAIL SUPPLY CHAIN CONFERENCE 2015

I-3. METRO Group structure – at a glance.

RETAIL SUPPLY CHAIN CONFERENCE 2015

I-4. METRO LOGISTICS (MLG): The Group’s own “4PL”

• Controlling the merchandise flows of all METRO GROUP sales lines METRO Cash & Carry, Real, Redcoon, Media Markt and Saturn as well as Galeria Kaufhof.

• Network of warehouses and platforms in the categories fresh, frozen and dry foods fruits and vegetables, fresh fish and non-food, own fleet

• Responsibilty for all warehousing and distribution activities in Germany, and handling for Austria, Switzerland and Benelux.

RETAIL SUPPLY CHAIN CONFERENCE 2015

I-5. Where we are coming from: “PK” - one-half academic …

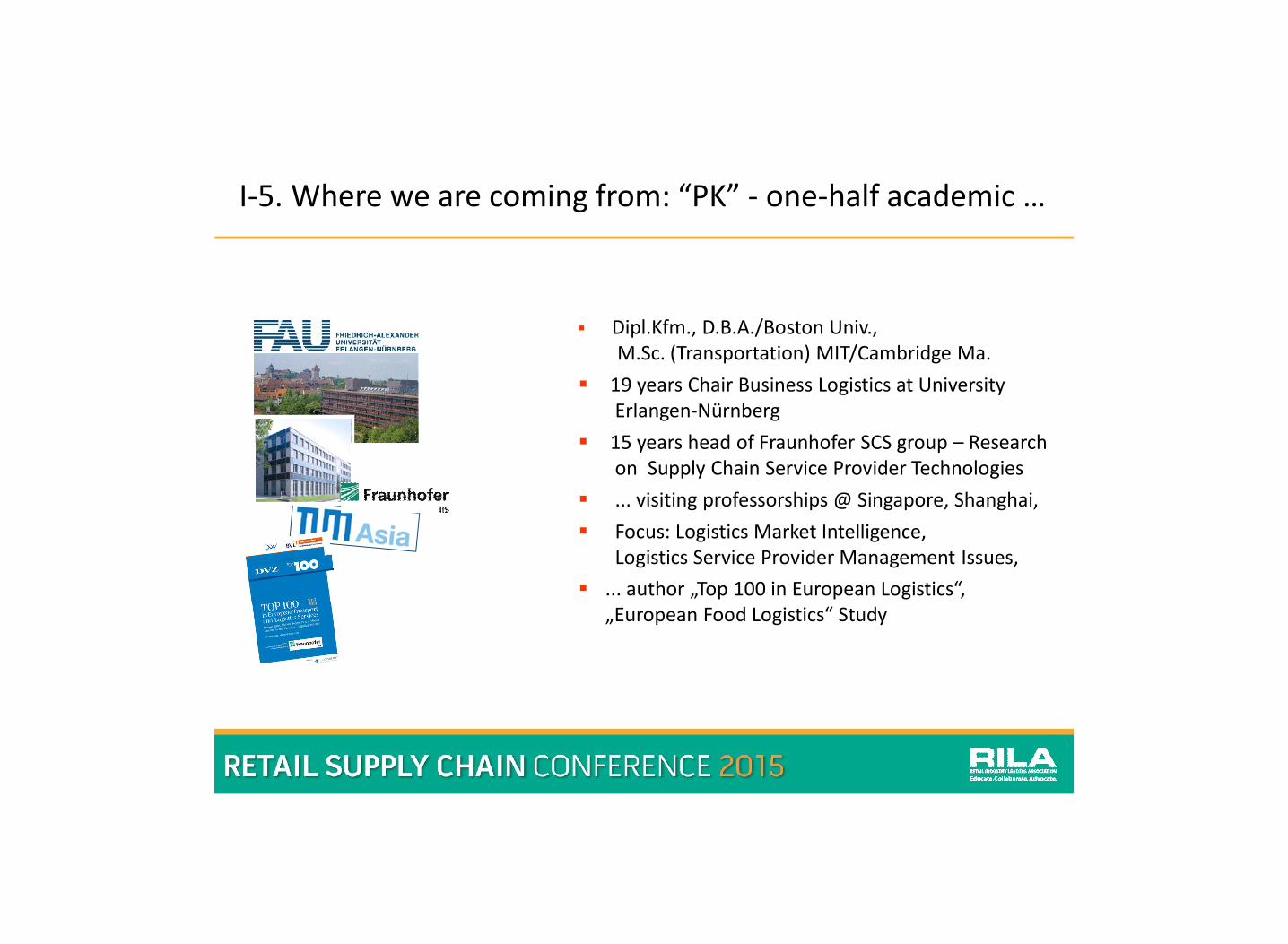

Dipl.Kfm., D.B.A./Boston Univ., M.Sc. (Transportation) MIT/Cambridge Ma.

19 years Chair Business Logistics at University Erlangen-Nürnberg

15 years head of Fraunhofer SCS group – Researchon Supply Chain Service Provider Technologies

... visiting professorships @ Singapore, Shanghai,

Focus: Logistics Market Intelligence, Logistics Service Provider Management Issues,

... author „Top 100 in European Logistics“,„European Food Logistics“ Study

RETAIL SUPPLY CHAIN CONFERENCE 2015

I-6. Where we are coming from - one-half “real world”

Specialized food logistics services

„from farm to fork“

LTL, FTL, Warehousing, VA-Serivces

overing 17 European countries - LTL, FTL,

11.000 associates

• Leading pan-European

food logistics service rovider

• € 2 bill. rev., 11.000 associates

• Supply Chain network services ...

RETAIL SUPPLY CHAIN CONFERENCE 2015

I-7. First comprehensive European Food-Logistics Study

„from Farm to Fork“

28 countries12 categories4 principal SC-stages4 main delivery channels

RETAIL SUPPLY CHAIN CONFERENCE 2015

Agenda.

I. Where we are coming from

II. Benchmarking What? A Bird’s Eyes View on Today’s European Retail Supply Network

III. The Grassroots Level: Three Selected European Retail SC-Practices

1. SC Complexity Reduction: Metro’s unified Inbound Logistics Concept2. Retail Industry Collaboration taken one Step further:

The Metro-Markant Industry Initiative 3. Towards a “supra-adaptive” Supply Network configuration:

Leveraging the capabilities of a Pan-European temp-controlled LTL- net

IV. Benchmarking across the Atlantic? The opportunities !

RETAIL SUPPLY CHAIN CONFERENCE 2015

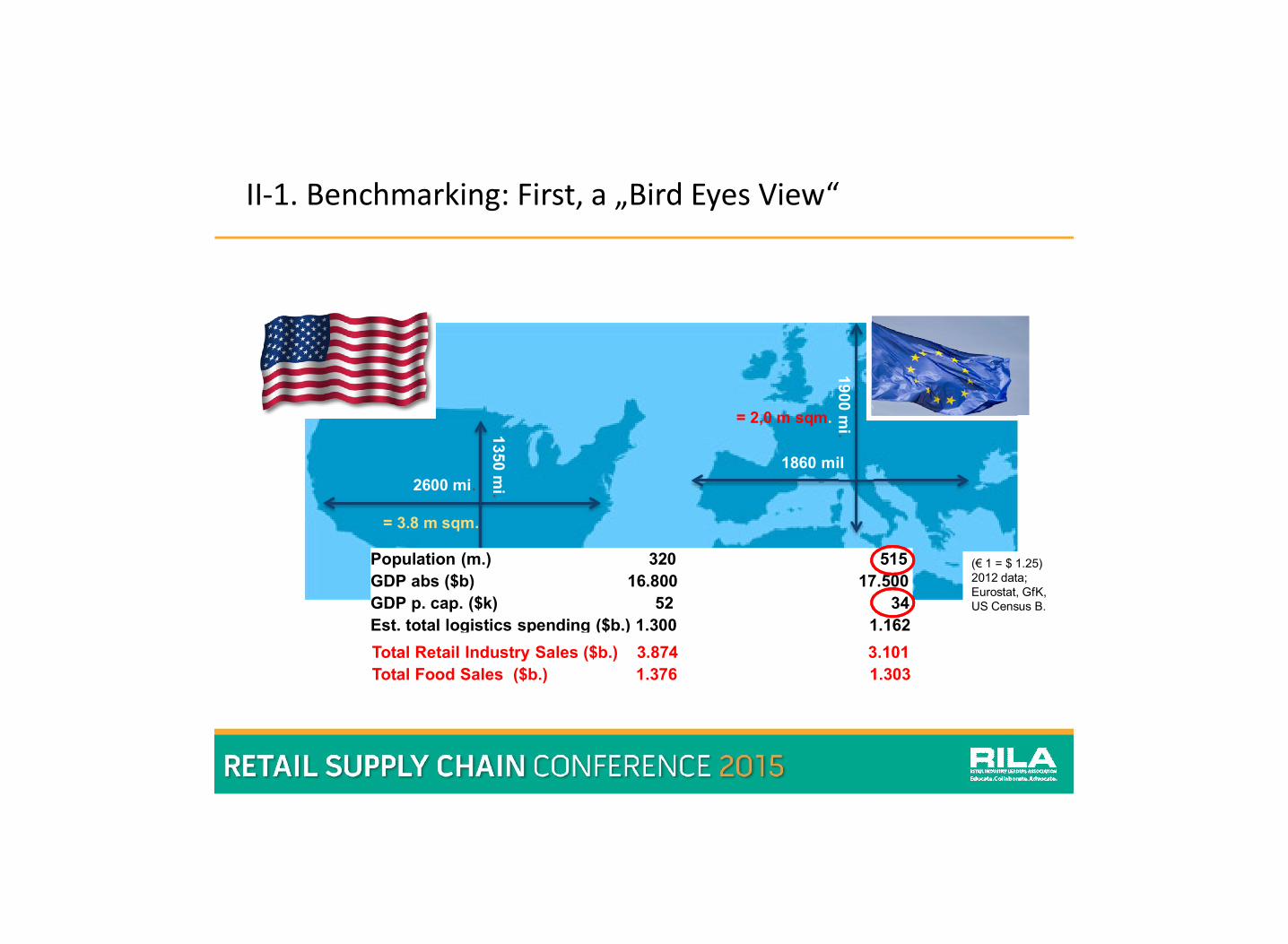

1860 mil 2600 mi.

1350 m

i.

1900 m

i.

= 3.8 m sqm.

= 2,0 m sqm.

II-1. Benchmarking: First, a „Bird Eyes View“

Population (m.) 320 515

GDP abs ($b) 16.800 17.500

GDP p. cap. ($k) 52 34

Est. total logistics spending ($b.) 1.300 1.162

(€ 1 = $ 1.25)2012 data;Eurostat, GfK,US Census B.

Total Retail Industry Sales ($b.) 3.874 3.101

Total Food Sales ($b.) 1.376 1.303

RETAIL SUPPLY CHAIN CONFERENCE 2015

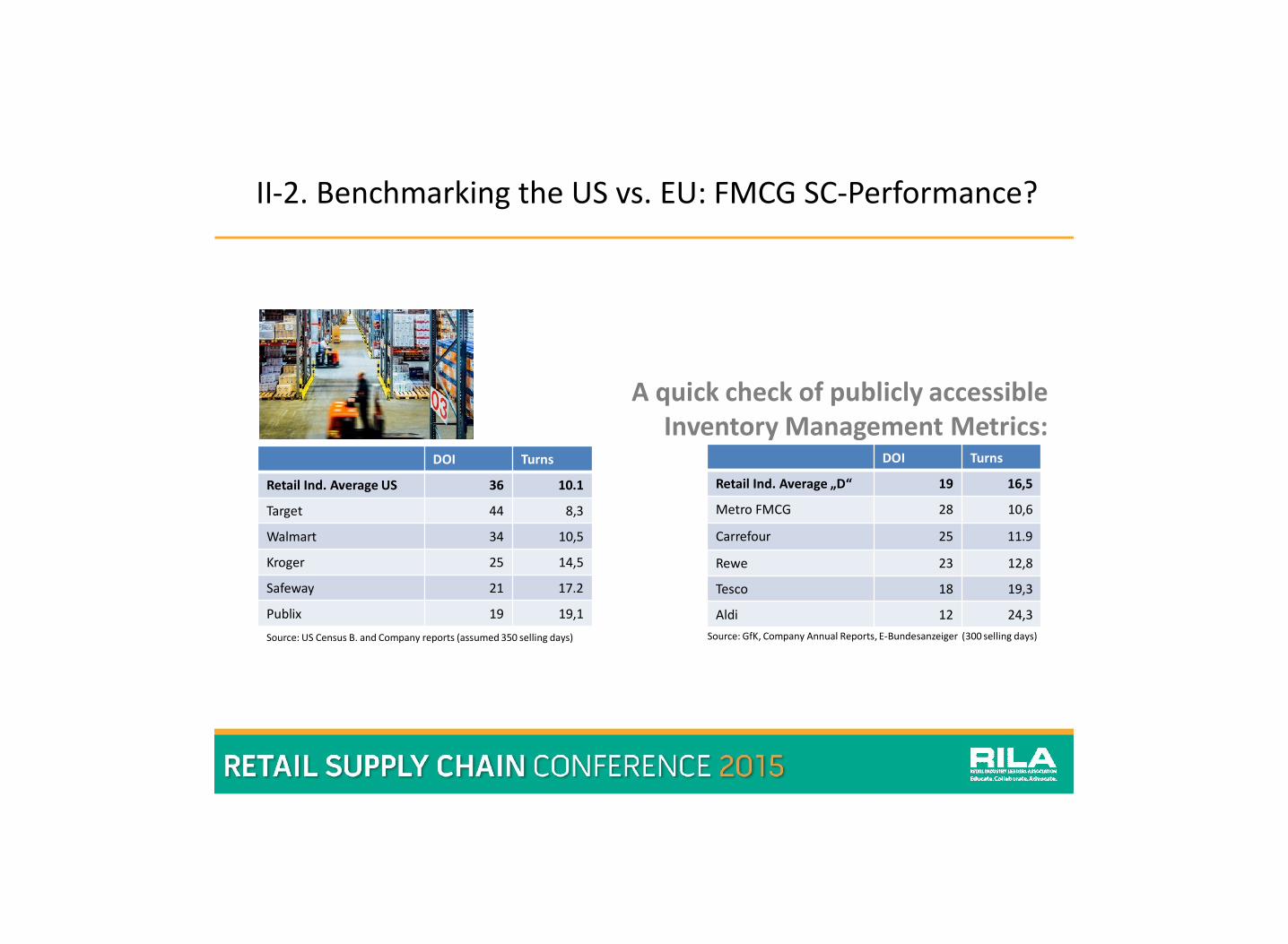

II-2. Benchmarking the US vs. EU: FMCG SC-Performance?

A quick check of publicly accessibleInventory Management Metrics:

DOI Turns

Retail Ind. Average US 36 10.1

Target 44 8,3

Walmart 34 10,5

Kroger 25 14,5

Safeway 21 17.2

Publix 19 19,1

DOI Turns

Retail Ind. Average „D“ 19 16,5

Metro FMCG 28 10,6

Carrefour 25 11.9

Rewe 23 12,8

Tesco 18 19,3

Aldi 12 24,3

Source: US Census B. and Company reports (assumed 350 selling days) Source: GfK, Company Annual Reports, E-Bundesanzeiger (300 selling days)

RETAIL SUPPLY CHAIN CONFERENCE 2015

II-3. A first observation: so far surprising similiarities ...

... and also: same challenges toSupply Chain Management:

• SKU-proliferation, E-Commerce, the „multi-channel“ revolution: exploding complexity

• The sustainability challenge: Forcing industry-and SC-wide initiatives & collaboration

• Meeting the „Age of Volatity“: Changingconsumer behaviors, new technologies: towards a „supra-adaptive“ retailing future?

++

=

RETAIL SUPPLY CHAIN CONFERENCE 2015

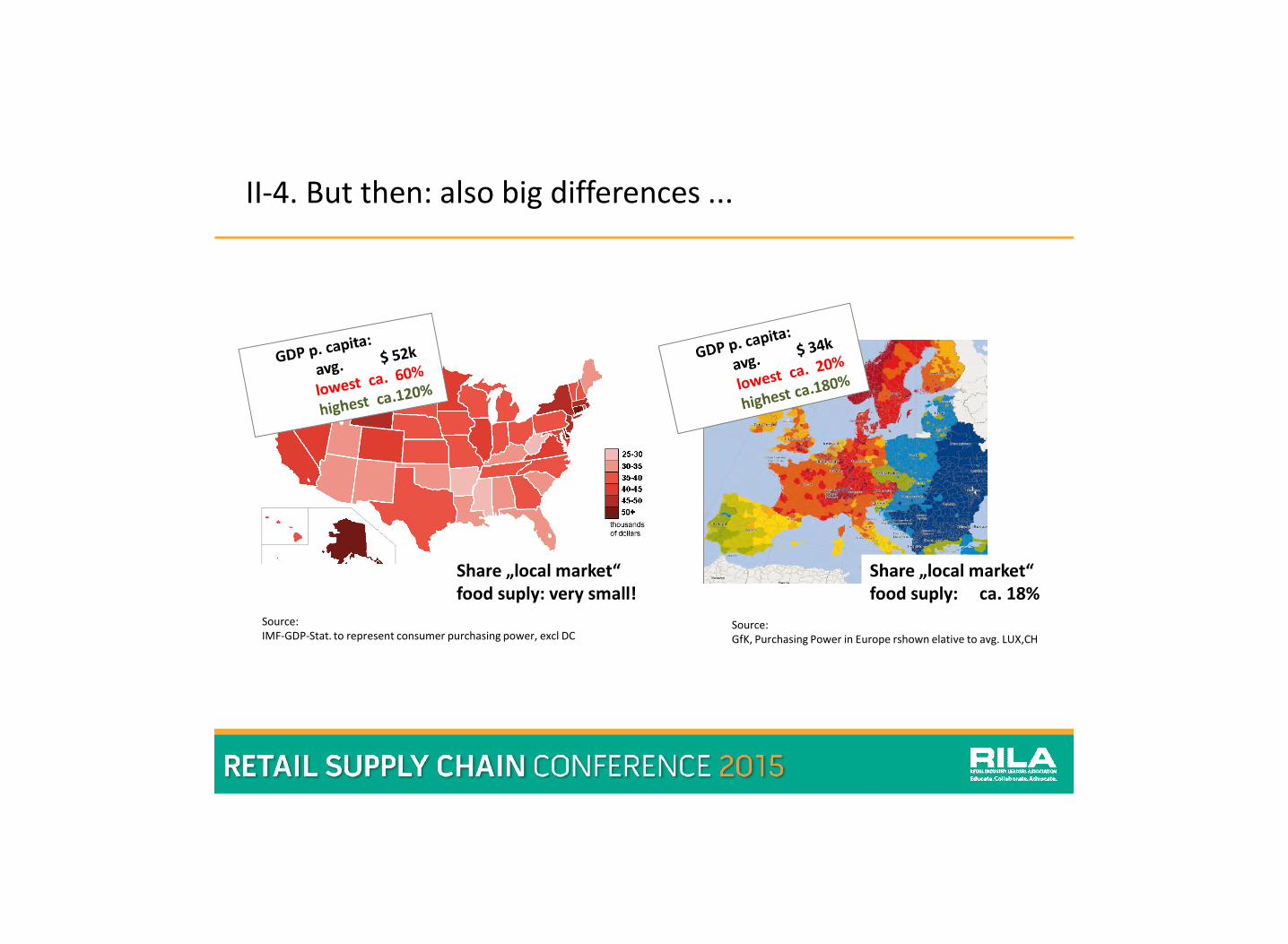

Source: IMF-GDP-Stat. to represent consumer purchasing power, excl DC

II-4. But then: also big differences ...

Source: GfK, Purchasing Power in Europe rshown elative to avg. LUX,CH

Share „local market“ food suply: ca. 18%

Share „local market“ food suply: very small!

RETAIL SUPPLY CHAIN CONFERENCE 2015

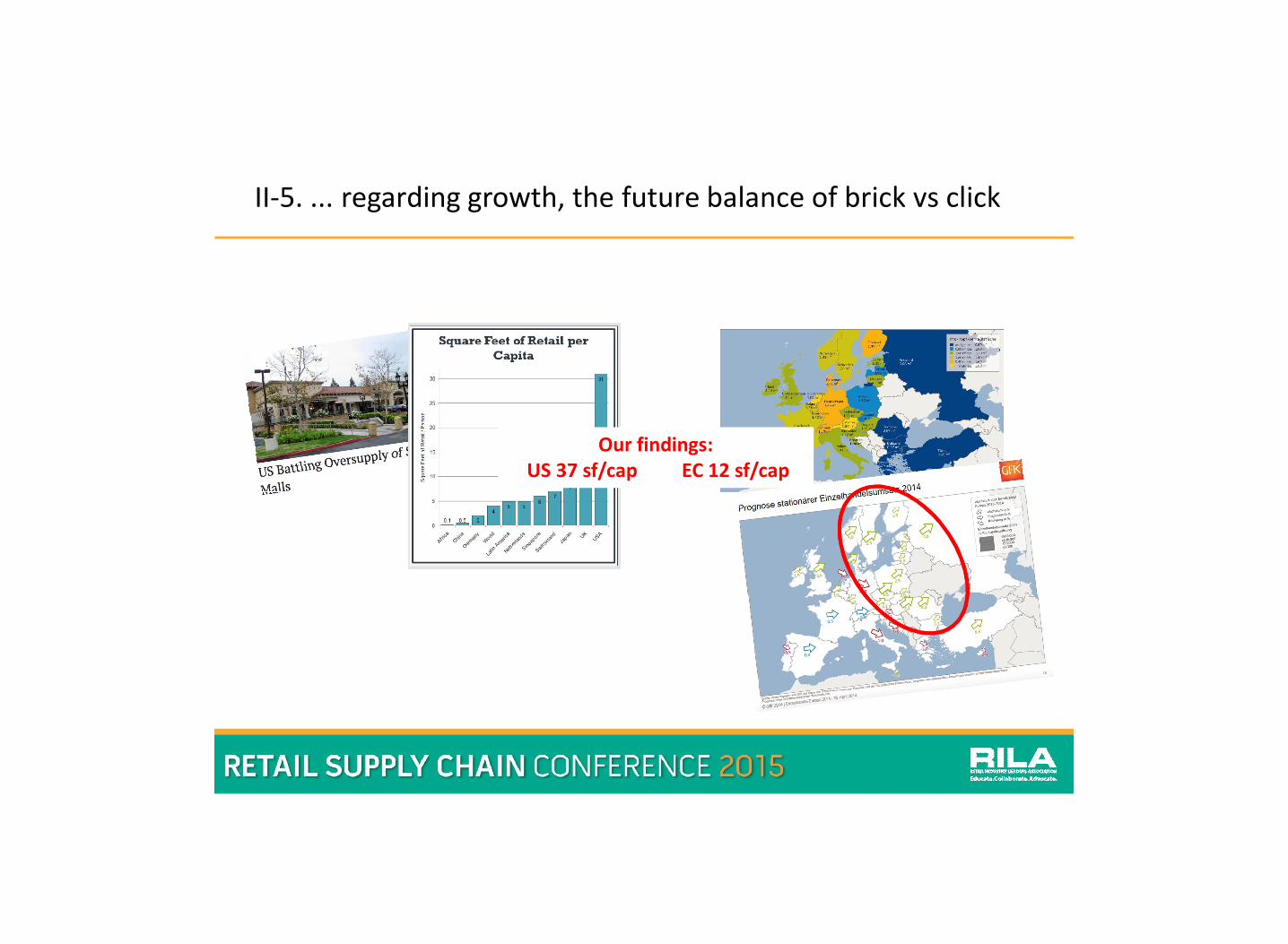

II-5. ... regarding growth, the future balance of brick vs click

Our findings:US 37 sf/cap EC 12 sf/cap

RETAIL SUPPLY CHAIN CONFERENCE 2015

II-6. Now, into some detail: Discussing „Best Practices“

RETAIL SUPPLY CHAIN CONFERENCE 2015

Agenda.

I. Where we are coming from

II. Benchmarking What? A Bird’s Eyes View on Today’s European Retail Supply Network

III. The Grassroots Level: Three Selected European Retail SC-Practices

1. SC Complexity Reduction: Metro’s unified Inbound Logistics Concept2. Retail Industry Collaboration taken one Step further:

The Metro-Markant Industry Initiative 3. Towards a “supra-adaptive” Supply Network configuration:

Leveraging the capabilities of a Pan-European temp-controlled LTL- net

IV. Benchmarking across the Atlantic? The opportunities !

RETAIL SUPPLY CHAIN CONFERENCE 2015

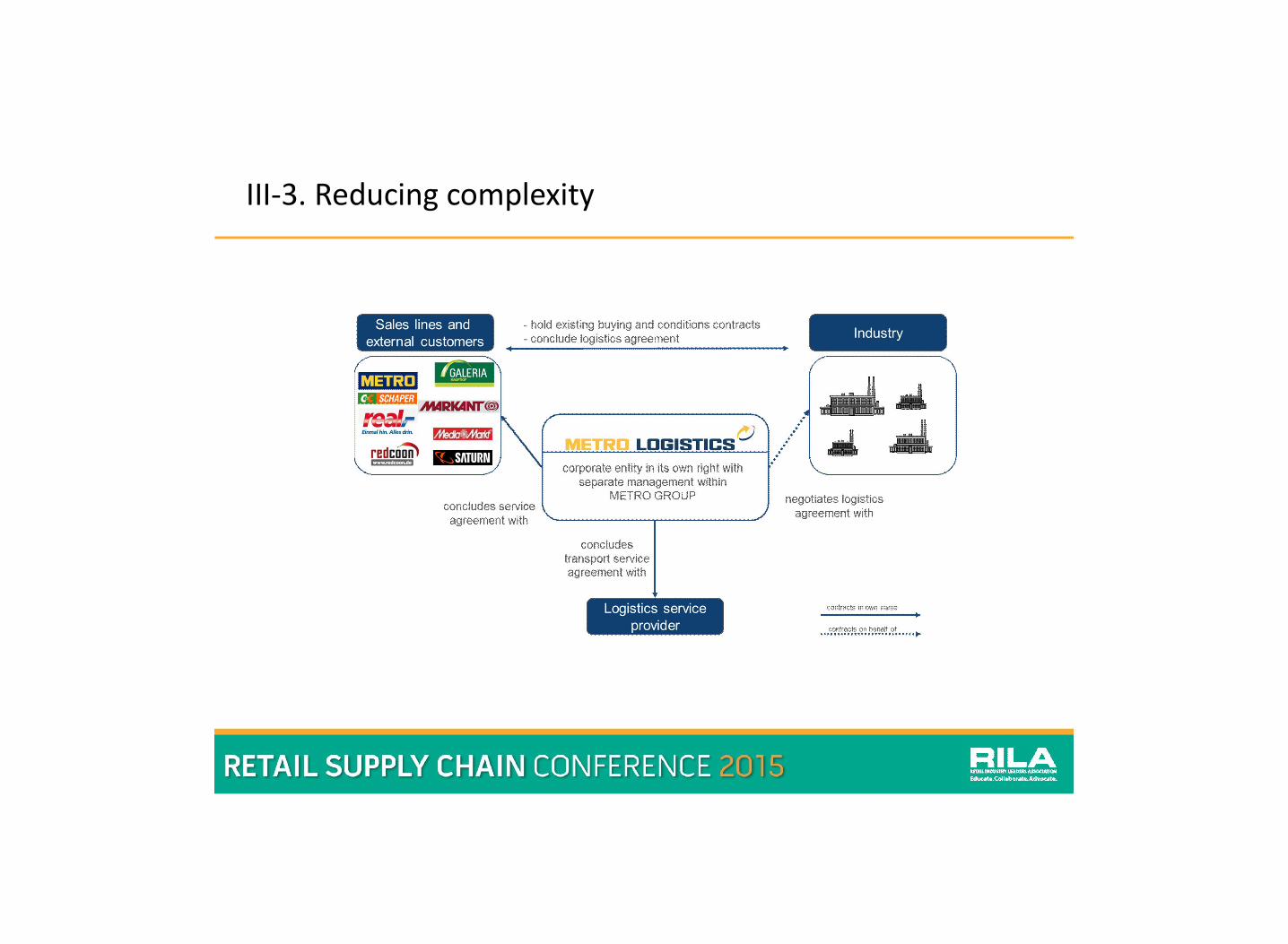

III-1. METRO LOGISTICS‘ unified Inbound Logistics

• Since 1995, the proprietary inbound logistics concept has been an important pillar for the success of the company.

• METRO LOGISTICS takes charge of picking up from approx. 4,100 suppliers the goods designated for METRO GROUP sales lines and bringing them directly to the respective stores.

• Delivery is usually made to the stores within 24 hours after pick-up, eliminating the need for interim storage. This strategy reduces the amount of stock that must be kept in the stores as well as the associated stock-keeping costs.

• Besides commercial success, METRO LOGISTIC's concept shows a positive ecologicalbalance.

RETAIL SUPPLY CHAIN CONFERENCE 2015

III-2. An optimized logistics structure, serving to ...

Traditional logistics concept. METRO LOGISTICS inbound logistics.

METRO LOGISTICS driven logisticsStores

4 LSPs

Supplier driven logistics Supplier

RETAIL SUPPLY CHAIN CONFERENCE 2015

III-3. Reducing complexity

RETAIL SUPPLY CHAIN CONFERENCE 2015

III-4. Rationalizing Supplier negotiations/compensation

RETAIL SUPPLY CHAIN CONFERENCE 2015

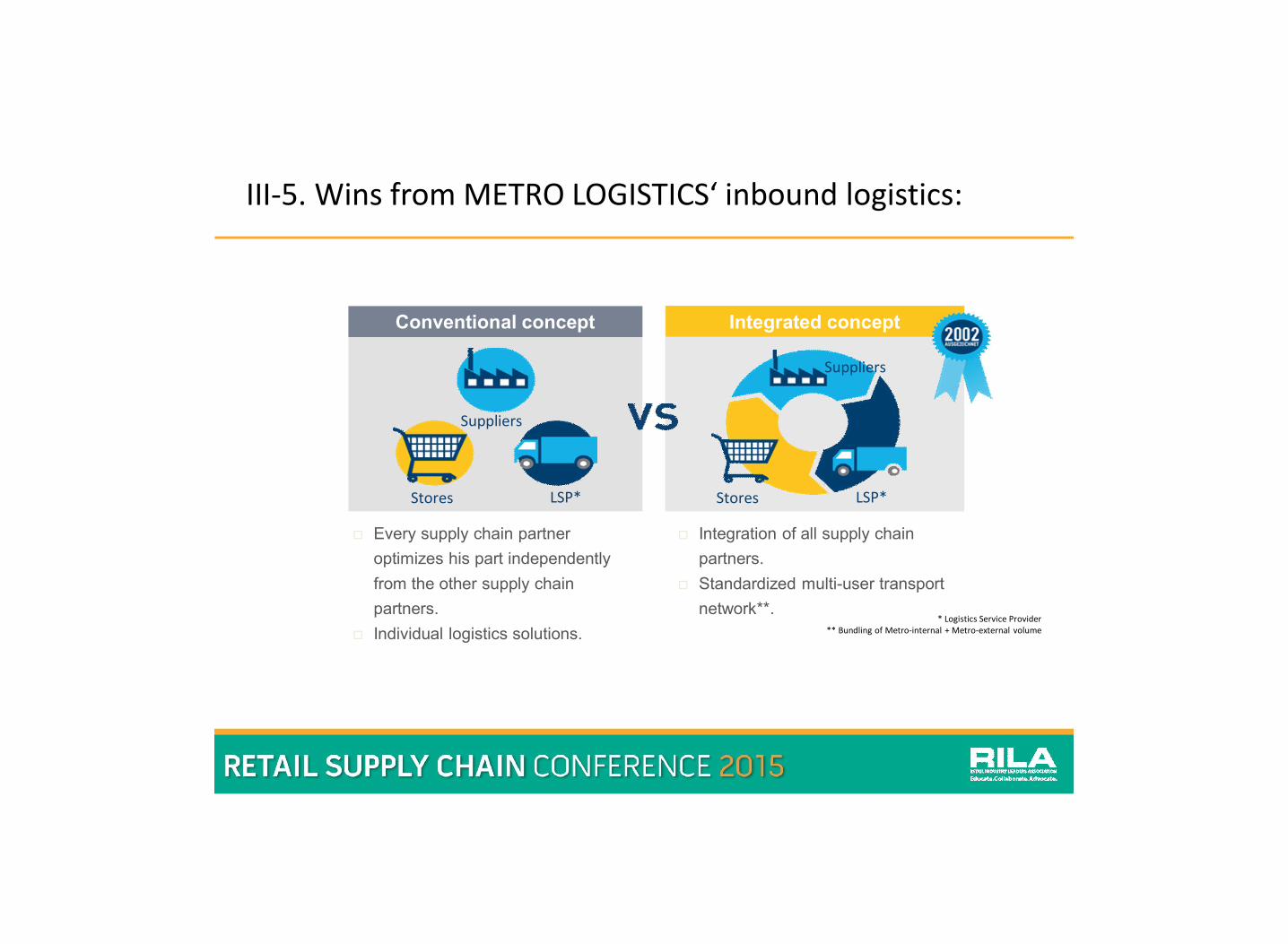

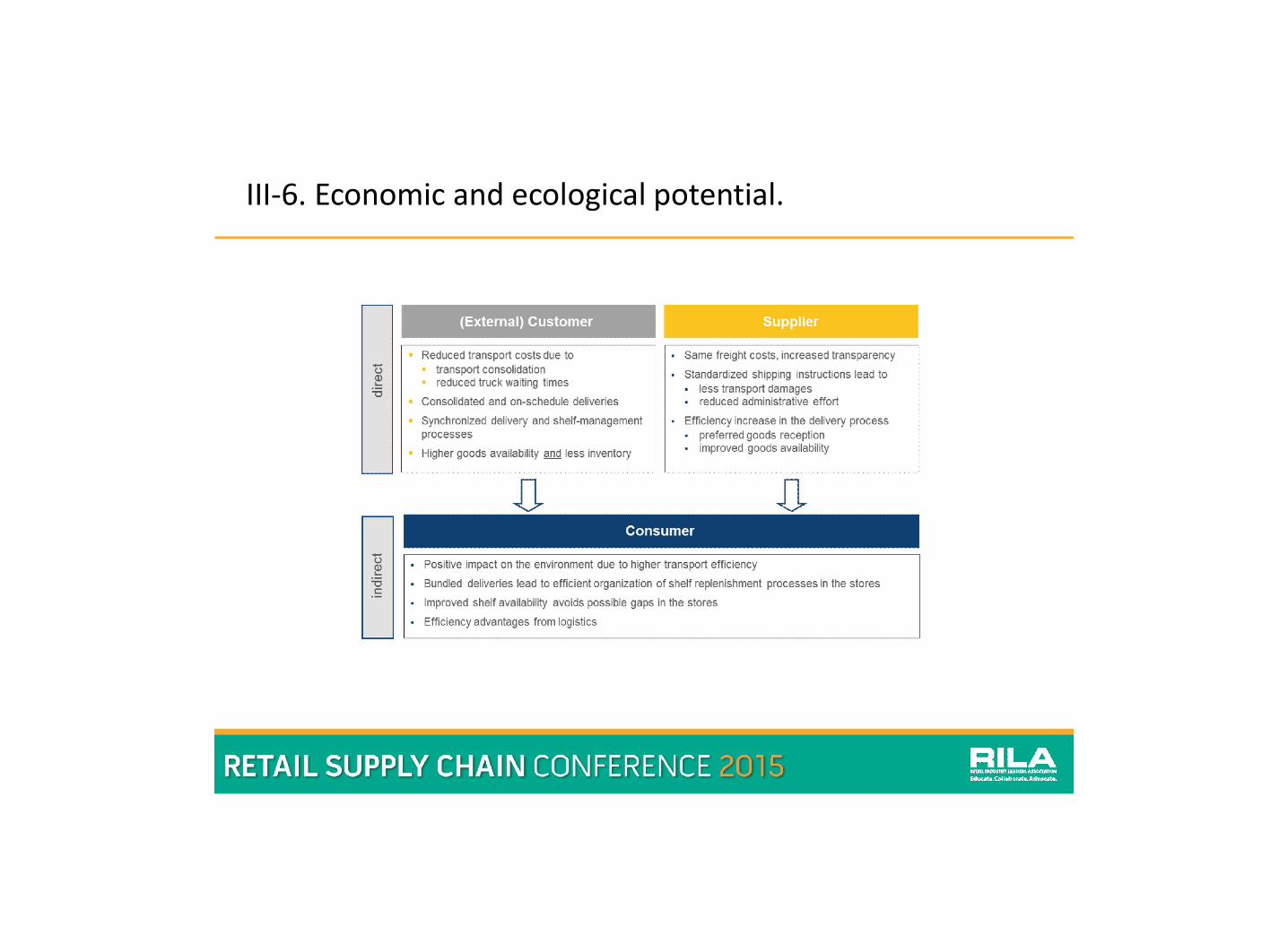

III-5. Wins from METRO LOGISTICS‘ inbound logistics:

vConventional concept Integrated concept

Suppliers

Stores LSP*

Suppliers

Stores LSP*

Every supply chain partner

optimizes his part independently

from the other supply chain

partners.

Individual logistics solutions.

Integration of all supply chain

partners.

Standardized multi-user transport

network**.* Logistics Service Provider

** Bundling of Metro-internal + Metro-external volume

RETAIL SUPPLY CHAIN CONFERENCE 2015

III-6. Economic and ecological potential.

RETAIL SUPPLY CHAIN CONFERENCE 2015

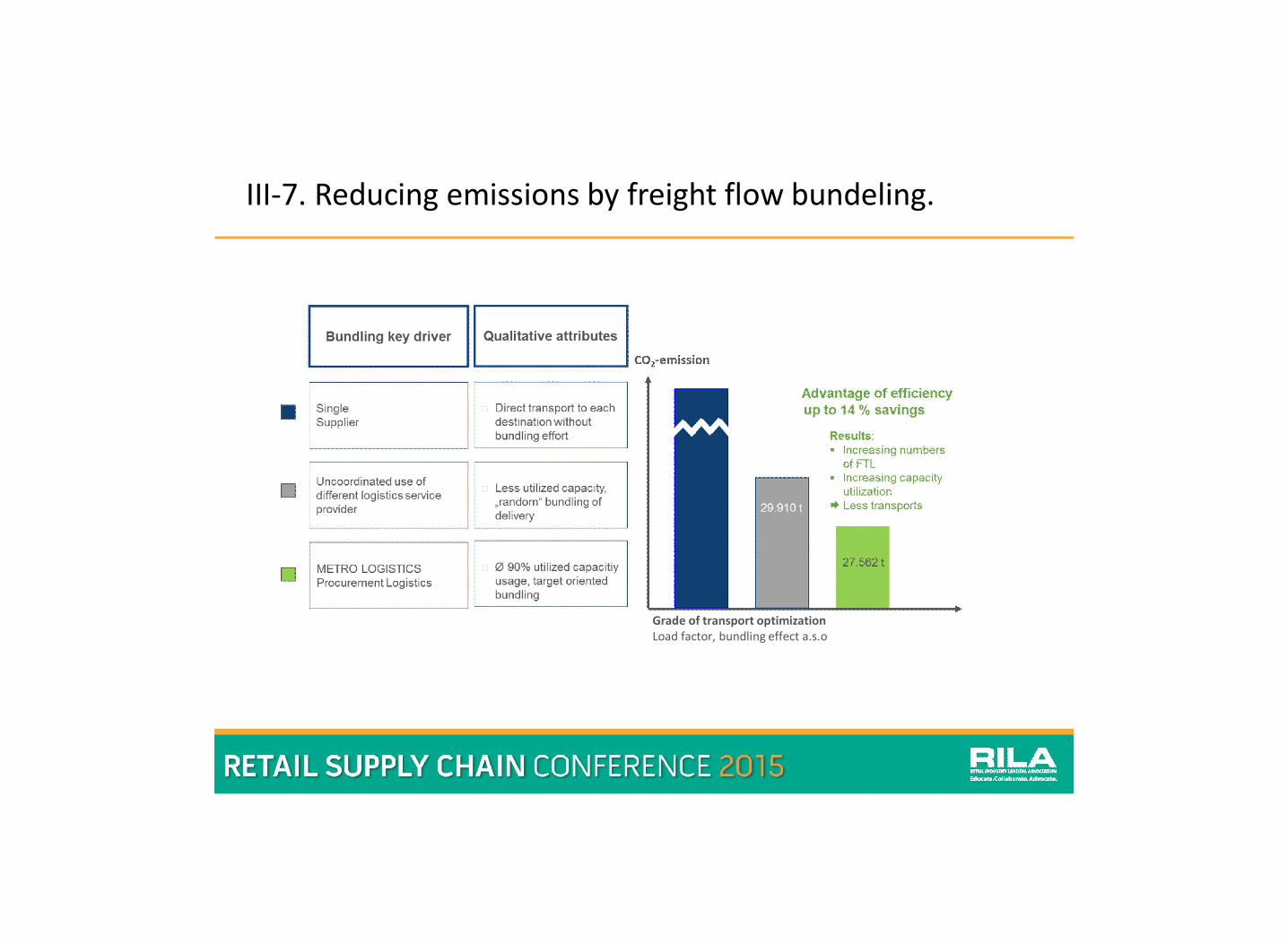

III-7. Reducing emissions by freight flow bundeling.

Grade of transport optimizationLoad factor, bundling effect a.s.o

RETAIL SUPPLY CHAIN CONFERENCE 2015

Agenda.

I. Where we are coming from

II. Benchmarking What? A Bird’s Eyes View on Today’s European Retail Supply Network

III. The Grassroots Level: Three Innovative European Retail SC-Practices

1. SC Complexity Reduction: Metro’s unified Inbound Logistics Concept2. Retail Industry Collaboration taken one Step further:

The Metro-Markant Industry Initiative 3. Towards a “supra-adaptive” Supply Network configuration:

Leveraging the capabilities of a Pan-European temp-controlled LTL- net

IV. Benchmarking across the Atlantic? The opportunities !

RETAIL SUPPLY CHAIN CONFERENCE 2015

III-8. Retail industry collaboration taken on step further:

1996 1998 2000 2002 2004 2006 2008 2010 2011

Start of MLG Procurement Logistics

Start of internationalization of MLG Procurement Logistics

Merger and integration of variouslogistics locations into MLG Warehousing

Outstanding logistics concept:MLG Procurement Logistics receives the German logistics award

Sustainable logistics: MLG is awarded with the Eco

Performance Award

Development ofan internationalconsulting team

Portfolio enlargement:buying, logistics and quality assurance of Fruits & Vegetables

Launch of an own logistics centre for wet fish

Extension of Import / Export execution

Start procurrement cooperation with ZHG / Markant

RETAIL SUPPLY CHAIN CONFERENCE 2015

III-9. Opening up MLG: The Markant connection

Cooperation members

Potential € 6,3 Mrd.

RETAIL SUPPLY CHAIN CONFERENCE 2015

III-10. Potential for adding external logistics partners1

Participation in an established system leads to a quick implementation with a minimzed risk szenario and a maximum of earnings.

RETAIL SUPPLY CHAIN CONFERENCE 2015

Agenda.

I. Where we are coming from

II. Benchmarking What? A Bird’s Eyes View on Today’s European Retail Supply Network

III. The Grassroots Level: Three Selected European Retail SC-Practices

1. SC Complexity Reduction: Metro’s unified Inbound Logistics Concept2. Retail Industry Collaboration taken one Step further:

The Metro-Markant Industry Initiative 3. Towards a “supra-adaptive” Supply Network configuration:

Leveraging the capabilities of a Pan-European temp-controlled LTL- net

IV. Benchmarking across the Atlantic? The opportunities !

RETAIL SUPPLY CHAIN CONFERENCE 2015

III-11. Welcome in „the Age of Volatily“ ?

• Reduce Inventories by true daily replenishment

• Avoid „brick-and-mortar“ warehouse investments

• Allow for short notice network structure changes

• Have flexibility in positioning multi-channeldistribution operations upstream/downstream, asrequired

A vision of „supra-adaptive“ food retail logistics

RETAIL SUPPLY CHAIN CONFERENCE 2015

III-12. leveraging capabilities of pan-continental 3PLs

Flexibility to choose from 70+ locations for ...

- temporary and permanent inventory loc options- ... SKU-mixing center and X-docking operations- fully temp-controlled, IT-integrated, one-stop

LTL shipment capability- A „supra-adaptive“ supply network!

RETAIL SUPPLY CHAIN CONFERENCE 2015

Agenda.

I. Where we are coming from

II. Benchmarking What? A Bird’s Eyes View on Today’s European Retail Supply Network

III. The Grassroots Level: Three Selected European Retail SC-Practices

1. SC Complexity Reduction: Metro’s unified Inbound Logistics Concept2. Retail Industry Collaboration taken one Step further:

The Metro-Markant Industry Initiative 3. Towards a “supra-adaptive” Supply Network configuration:

Leveraging the capabilities of a Pan-European temp-controlled LTL- net

IV. Benchmarking across the Atlantic? The opportunities !

RETAIL SUPPLY CHAIN CONFERENCE 2015

IV. A promise of trans-Atlantic Benchmarking

• Comparability of basic retail structures, volumes,and SCM challenges

• ... yet inspiring differences in growth perspectives,business practices, and experiences

• ... little overlap of competitive turf• availability of industry-level platforms allowing

„neutralized“ exchange of Benchmark data andBest Practices

• ... RILA/HDE, GS1, GTAI, and international LSPs

RETAIL SUPPLY CHAIN CONFERENCE 2015

Dankeschön!