Embed Size (px)

Citation preview

Retail in

ABSTRACT Many

Business Adjustment Rural Hierarchies

DAVID HENDERSON GEORGE WALLACE

rural hierarchies are becoming increasingly dominated by a few regional growth centers while the retail sector in adjacent smaller communities either stagnates or declines. This study tests the hypothesis that the rate of adjustment of the retail sector to changing consumer spending patterns is uniform across different ordered communities in a rural hierarchy. Neoclassi- cal investment theory is combined with central place theory to develop a conceptual model of the relationship between the retail sector and investment in a community. A three tiered 49 community hierarchy is constructed using data from the Minnesota Department of Revenue and the Report of Condition and Income of the Board of Governors of the Federal Reserve System. A cross- sectional time series ordinary least squares regression model is employed to estimate retail coefficients of adjustment for the hypothesis testing. Regional estimates indicate only partial adjustment in the retail sector across the whole hierarchy to shifts in consumer spending patterns. Community estimates, which decompose the regional estimate, indicate retail businesses in the largest and mid-sized communities adjust totally in one period, but that retail businesses in the smallest communities do not. The faster rates of adjustment by retail businesses in the larger communities to changing consumer spending patterns may augment the development of regional growth centers in rural areas.

Retail Business Adjustment in Rural Hierarchies HE EARLY 1980’s WERE A PERIOD of extensive adjustment in the T economy as the country moved increasingly away from a production based

economy towards a trade and service economy. Inherent in the restructuring of the economy was a shift in the employment base away from production jobs towards retail and service occupations. One out of every three new jobs created during the early 1980’s was in the retail sector and the recent trade expansion has important spatial implications for both metropolitan and nonmetropolitan retail markets’.

David Henderson is an economist with The Ohio State University Piketon Research & Extension Center, 45661 and George Wallace is an economist in the Agriculture and Rural Economy Division of the Economic Research Service, Washington DC 20005-4788.

RETAIL BUSINESS ADJUSTMENT 81

The 1970s were a period of deconcentration of retail trade, with the smaller metropolitan and nonmetropolitan areas of the country gaining retail sales (Morrill 1982). The deconcentration of retail activity reverted to the longer run trend of concentration in the higher end of the city hierarchy during the early 1980’s. The recent rural to urban turnaround is evidenced by the fact that 2.5 million, or 85 percent, of the new retail jobs were created in the metropolitan counties.

One of the primary concerns of an expanding retail sector in metropolitan areas is the spatial impact that retail development projects have on the economic health of the various shopping districts. Retail growth in any one of the shopping districts in a metropolitan area affects the vitality of the adjacent shopping districts by changing their ability to generate sales. Reinvestment in older shopping centers or the development of new commercial prqjects affects the ability of the central business district, malls, strip developments, and other competing retail shopping districts, to draw customers (James 1985).

The same interrelationship between retail development projects in different shopping districts exists in the nonmetropolitan counties’. But the rural nature of nonmetropolitan counties causes much of the interdependence between shopping centers to occur among spatially separate communities. Retail developments in one community affect the ability of adjacent communities to draw customers; and the positive impacts of the recent retail expansion were probably concentrated in the larger regional growth centers of the nonmetropo- litan counties (Walzer and Stablein 1981).

The spatial aspects of developments in the retail structure of an area are partially determined by investment patterns (Buckwalter 1990). The role of private banks in the retail development of rural areas is important because the community bank is often the primary supplier of local retail investment funds3. Even though the significance of bank investment is generally recognized, there is little agreement on its role in the retail development of rural areas. (Dreese 1974; Ho 1979; Barkley and Helander 1985: Rogers et al. 1990). The purpose of this paper is to estimate the adjustment in the retail sector from changes in consumer spending patterns in order to test the hypothesis that the retail businesses’ adjustment process is identical across different ordered communities in a rural hierarchy.

The Data The Minnesota Department of Revenue provided data on retail businesses in

a ten county area of Southwest Minnesota. The data included the annual number of retail businesses and sales by community over the 1980-86 period. This study used information on 49 of the communities, 2 of which averaged 229 retail

82 GROWTH AND CHANGE, WINTER 1992

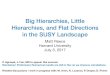

North = Large comrnuniry

= Mid-sized community

1 inch = 16 miles

-----A-

\ \ / /\

FIGURE 1. A Minnesota Community Hierarchy

RETAIL BUSINESS ADJUSTMENT 83

businesses per year over the period. 10 averaged 91. and the remaining 37 averaged 2 1.

Data on bank investment in the retail sector by community was collected from the Report of Condition and Income of the Board of Governors of the Federal Reserve System (ref). The bank data is reported by individual bank and contains annual information on deposits, securities, and commercial investment loans4. The individual bank data was aggregated up to the community level to match the retail data at the community level when more than one bank was located in a community.

Figure 1 shows the spatial distribution of the communities in Southwest Minnesota. The 10 mid-sized communities encircle the 2 highest ordered communities and the remaining 37 lowest ordered communities are dispersed throughout the area. The population in the 37 smallest communities has been stable since 1940 at about 500 residents per community. Population in the 10 mid-sized communities increased until 1960 and then stabilized at about 3,000 residents per community. Population in the 2 largest communities steadily increased until 1970 and then stabilized at about 10,000 residents per community.

Retailing in a Rural Minnesota Hierarchy Central place theory provides a behavioral framework for explaining

consumer spending patterns in a rural hierarchy. Retail businesses in lower ordered communities sell a smaller variety of goods; and their local customers import the remainder of their consumer items from businesses in higher ordered communities (Seninger 1978). In a static model, shopping in a larger community for higher ordered goods which are not offered in a smaller community should not adversely affect the level of sales in the smaller community.

Rural spending patterns also have a dynamic aspect which occurs when small town consumers travel to a larger community to purchase higher ordered goods and while there purchase lower ordered goods which are offered in the smaller community. This kind of shopping behavior represents competitive retail imports of lower ordered goods into the market of the smaller community from businesses located in the larger community. Rural consumers minimize shopping time and transportation costs by purchasing as many goods as possible during the one shopping trip to the larger community (Fotheringham 1983).

Inevitably, when consumer purchases of lower ordered goods in a larger community are directly substituted for consumer purchases of lower ordered goods in a smaller community, the relative market shares of the different ordered communities change. Consumer spending decreases in the smaller communities and increases in the larger communities because rural consumers are spending an increasing proportion of their consumer dollar in the larger community

84 GROWTH AND CHANGE, WINTER 1992

045

(Henderson 1990). Figure 2 shows how this process has affected consumer spending in the Southwest Minnesota hierarchy between 1981 and 1986.

------- - ~

-c--.- ------- ---XI* _ _ _ *----- _- ”-- --4------ I_-

0 47295 47519 0 46853 .~ 0.45658 0.45332

0.44336

Average Spending by Community Size

0’5 T Deflated 1982 Dollars

0.25 1 0.2413 0.23574

0 2145 0 21293 0.21619

0.20698

0.15

81 82 83 Year 84 85 86 W Largest E Mid-sized Smallest

FIGURE 2. Average Spending by Community Size

RETAIL BUSINESS ADJUSTMENT 85

Spending at retail businesses in the largest communities increased from 29 cents of every dollar spent in 1981 to 36 cents of every dollar spent in the area in 1986, while per dollar spending decreased by 3 cents per dollar in the mid-sized communities and by 4 cents per dollar in the smallest communities over the same period.

The retail businesses in the different ordered communities are expected to adjust to the changing consumer spending patterns. The businesses located in the largest communities are probably increasing their inventory purchases to meet the increased buying of the local consumers. On the other hand, the businesses in the mid-sized and smallest communities are probably decreasing their inventory purchasing to adjust to the decreased spending of the local consumers at their stores. The adjusting of the amount of purchases from the wholesale sector by the retail businesses is the short run investment the operators are making in their businesses.

Bank Activity in Southwest Minnesota Community bankers help retail businesses adjust to the changes in consumer

spending patterns by providing debt financing to the retail businesses. Research in the midwest indicates most commercial banks currently use local demand and time deposits as primary sources of debt financing for local small business development (Shaffer and Pulver 1990). Historical studies in the upper Midwest also suggest rural retail businesses tend to borrow funds from the bank in the community in which they are located (Federal Reserve Bank of Chicago 1956; Pike 1964; Shaffer 1978). Current research indicates 86 percent of total bank lending activity is within 10 miles of the bank location because local bankers recognize community market boundaries and tend to service their own perceived market (Taff et al. 1984; Rogers et al. 1988).

The general relationship between the community retail and banking sectors in the area was influenced by the general conditions in the national economy over the period. In particular, the changing real interest rate of the period may have affected the local financial markets. The real interest rate, as measured by the nominal interest rate minus the inflation rate, increased 25 percent over the period from 9.8 percent in 1981 to 12.4 percent in 1986; and local savers, bankers, and retail investors adjusted to the new financial market equilibrium.

Total real deposits by local savers in the area increased by 6.2 percent between 1981 and 1986, indicating that the total supply of local funds to the banks increased over the period. Total demand deposits decreased by 24 percent while total time deposits increased by 12 perceut over the period. Local savers were apparently shifting local financial resources away from non interest bearing demand deposits towards interest bearing time deposits’.

86 GROWTH AND CHANGE, WINTER 1992

The community bank is itself a business which maximizes its own profits while serving as a financial intermediary in the community. Bank portfolio theory postulates that as the real interest rate available on nonlocal securities rises, banks will shift their portfolios toward nonlocal securities and away from local commercial loans (Bernake 1988). Real commercial loans in the area did, in fact, decrease by 27.7 percent and the real value of nonlocal securities increased by 18.4 percent over the period6. Part of the decrease in local commercial loans may have occurred because higher real interest rates would have decreased the number of retail investment projects with an internal rate of return high enough to be financially feasible for local businesses’.

A Model of the Community Retail and Bank Sectors The bringing together of local savers and retail investors to form a

community retail funds market is one of the principal functions that a bank performs in a community. The bank allocates part of the supply of local demand deposits, within a portfolio of retail loans, to individual retail investors at the prevailing interest rate. The locus of the internal rates of return for all approved retail loans (investment projects) represents the retail sector’s demand for funds in the community retail investment market. Community retail businesses continue to invest in individual projects until the internal rate of return to a project equals the real interest rate paid to local savers.

The empirical community retail output function should have a variable that accounts for the larger variety of retail businesses located in the higher ordered communities. A community hierarchy variable should be included because the larger set of different retail enterprises in the higher ordered communities offers more retail investment opportunities. A community retail output function, with a community hierarchy, was identified as follows:

where 0 is aggregate retail output for the retail sector in community i, I is retail investment in community i, O,, is last periods retail output in community i, D is a variable that accounts for the relative effect of different sets of retail investment opportunities in the different ordered communities.

The model employs the flexible accelerator investment theory which identifies the desired amount of retail output as a linear function of last period’s retail output plus some adjustment in the current period. Previous research in the upper Midwest indicates that the greatest proportion of local bank commercial loans are for short run business expansion and operating loans (Shaffer and Pulver 1990). The relationship between retail output and loans in the current

RETAIL BUSINESS ADJUSTMENT 87

period is the short run partial adjustment businesses are making between actual retail output in the last period and their desired level of retail output in the current period.

The estimated magnitude of the short run coefficient of adjustment is an empirical question, but it is theoretically bounded between 0 and 1. An estimated coefficient of 1 means the retail businesses are adjusting their purchases in the current period to the actual level of retail sales they will have in that year. On the other hand, an estimated coefficient of 0 means nothing changes since retail sales in the current year are the same as in the previous year. The estimated coefficient is usually somewhere between 0 and 1, indicating only a "partial adjustment" to the desired level of output in the current period.

The following equation was specified to estimate an elasticity of retail output with respect to retail investment by community size:

0, = a + PIi, + PDjIit + PO,,., + PDjOit., + ei, [21

where 0 is total retail output (deflated gross retail sales) by community (i = 1...49), a is an intercept term, p are the coefficients of adjustment to be estimated, I is commercial investment loans, and Ot., is retail output in the previous period, D (0 or 1) is a dummy variable used to stratify the communities by size (j = 3), t refers to year (198 1-1 986), e is a random error termR. The commercial loan variable is an instrumental variable used as a proxy for investment in the retail sector by banks'. The number of businesses in the previous period was used as the instrumental variable for retail output in the previous period'".

A regional regression was calculated without the community dummy variable to estimate a regional coefficient of adjustment for the whole hierarchy. The regional coefficient of adjustment represents the average coefficient of adjustment across all three tiers of the local hierarchy. The results of the regional regression are used to test hypotheses about the adjustment process within the whole hierarchy and to establish an example of how to decompose regional estimates into more accurate community estimates.

The community regression facilitates the estimation of the retail coefficient of adjustment by community size, while holding output in the previous period constant. The procedure allows the coefficient of adjustment to vary by community size within the local hierarchy. Allowing the coefficient of adjustment to vary by community size facilitates hypothesis testing to discern if the coefficient of adjustment is equal across the different ordered communities in the local hierarchy".

88 GROWTH AND CHANGE, WINTER 1992

TABLE 1. ESTIMATED RETAIL OUTPUT EQUATIONS

VARIABLES Retail Mean Sales Elasticity

co EFF IC I E NTS’

Intercept

Regional adjustment

Largest community adjustment

Mid-sized community adjustment

Smallest community adjustment

Largest community lagged output

Mid-sized community lagged output

Smallest community lagged output

F

R2

N

-964,915.1 5* (381 ,I 87.43)

.82669* .21 (.06771) .93244* .22

(.09372) 1.10439* .24 (. 1 2256) .25658** .10 (.13648)

325,961.32* (9,823.59)

236,455.71 * (11,153.24)

200,136.46* (1 8,675.94)

21 45.92

.9782

.. 294

1. * **

Standard errors are in parenthesis. Significant at the 1 percent level. Significant at the 5 percent level.

RETAIL BUSINESS ADJUSTMENT 89

Results and Hypotheses Tests The estimated coefficients of adjustment, calculated mean elasticities, and

other statistical information from the regressions are provided in Table 1. All of the estimated coefficients of adjustment have the right sign and are of the expected magnitude. The estimated coefficient of adjustment for the whole hierarchy was 3 2 and the community level coefficients ranged from 1 for the largest and mid-sized communities to .25 for the smallest communities.

The estimated regional coefficient of adjustment is an average of the community coefficients of adjustment”. The spatially aggregated regional coefficient is less than the estimated coefficient for the largest and mid-sized communities, but greater than the estimated coefficient for the smallest communities. The regional estimate is less accurate than the community estimates because it is a spatial average which over estimates the adjustment for retail businesses in the smallest communities and underestimates the adjustment of retail businesses in the larger communities.

The results of the hypothesis tests are presented in Table 2. The results of the hypotheses tests provide a statistical basis for inferences about the adjustment of the retail sector to changes in consumer spending patterns in a rural hierarchy. Tested were two sets of hypotheses that increase the understanding of the adjustment processes occurring in the rural hierarchy during the retail expansion of the 1980’s.

The first set of hypotheses are based on the estimated regional coefficient of adjustment. The estimated coefficient is significantly greater than 0 and significantly less than 1. This result indicates that there was only a “partial adjustment” within the whole hierarchy to the changes in consumer spending patterns. While this result indicates that, as a whole, retail businesses in the hierarchy did not totally adjust in the short run, it does not indicate which part of the hierarchy is characterized by short run inflexibility.

The second set of hypotheses are based on the estimated community coefficients of adjustment and are designed to test for where in the hierarchy the short run rigidity exists. All three community level coefficients of adjustment are significantly greater than 0. The estimated coefficients for the largest and mid-sized communities are not significantly different from 1, but the estimated coefficient of adjustment for the smallest communities is significantly less than 1. These results imply that there was total short run adjustment to the shifts in consumer spending over the period by retail businesses in the largest and mid- sized communities, but only partial short run adjustment by retail businesses in the smallest communities

The estimated coefficient of adjustment for the smallest communities is statistically less than the estimated coefficients for the largest and mid-sized

90 GROWTH AND CHANGE, WINTER 1992

TABLE 2. HYPOTHESES TESTS’

Hypotheses Result

Regional Hypotheses

H,: Adjustment occurred between the years.

Estimated coefficient of adjustment (.82669) is greater than 0.

H,: Total adjustment occurs within one year.

Estimated coefficient of adjustment (.82669) is equal to 1.

Hypotheses by Community Size

Largest Communities

H,: Adjustment occurred between the years.

Estimated coefficient of adjustment (.93244) is greater than 0.

H,: Total adjustment occurs within one year.

Estimated coefficient of adjustment (.93244) is equal to 1.

Mid-sized Communities

H,: Adjustment occurred between the years.

Estimated coefficient of adjustment (1.1 0439) is greater than 0.

H,: Total adjustment occurs within one year.

Estimated coefficient of adjustment (1,10439) is equal to 1.

Smallest Communities

H,: Adjustment occurred between the years.

Estimated coefficient of adjustment (.25658) is greater than 0.

H,: Total adjustment occurs within one year.

Estimated coefficient of adiustment (.25658) is equal to 1.

Accept

Reject

Accept

Accept

Accept

Accept

Accept

Reject

1. One tailed hypotheses tests.

RETAIL BUSINESS ADJUSTMENT 91

communities”. This result confirms that the short run rigidity in the hierarchy is concentrated in the smallest communities. Retail businesses in the smallest communities are apparently not totally adjusting during the year and it is this short run rigidity which causes the regional coefficient of adjustment for the whole hierarchy to be less than 1. This result implies that retail businesses in the lower end of the hierarchy need more time to adjust to the changes in consumer spending than do their counterparts in the larger communities.

Conversely, the speed at which retail businesses in the largest communities can adjust allows them to alter their supply more efficiently to meet the new market demand within one year. The faster speed of adjustment to the change in demand from the shifting consumer spending patterns in the largest communi- ties could increase the their relative growth. A faster growth rate in the largest communities may augment the development of larger regional centers in rural hierarchies.

Conclusions The short-run rate of adjustment in the retail sector is slower in smaller rural

communities than in larger rural communities. The relatively faster rate of adjustment in the larger communities augments the ability of their retail sector to alter their supply and adjust to the changing demand caused by the spatial shifts in consumer spending patterns within the hierarchy. The synergistic affect of a relatively faster rate of adjustment on the supply side and the changing consumer spending patterns on the demand side may augment each other, furthering the development of regional growth centers in rural hierarchies.

NOTES 1. Total wage and salary employment in the U.S. increased by 9,128,792 jobs between

1980 and 1986. Retail employment increased by 2,913,755 and accounted for 32 percent of the increase in total employment.

2. Total nonmetropolitan wage and salary employment increased by 520.635 jobs between 1980 and 1986. Retail employment increased by 434,485 and accounted for 85 percent of the total increase in nonmetropolitan employment.

3. Between 1980 and 1986. total real commercial loans from all lending institutions increased 347 billion dollars and grew at an annual rate of about 16 percent a year. Nationally, real commercial loans by banks grew from 96 billion in 1980 to 259 billion in 1986, at a rate of 24 percent a year.

4. The commercial loans data included loans to business enterprises (proprietors, partnerships, and corporations) whether secured or unsecured, single payment or installment. Minnesota was a unit banking state until 1980 and then became a very limited branching state in 1981. The data indicated no significant bank branching activity between the communities in the area.

92 GROWTH AND CHANGE, WINTER 1992

5. The time deposit data includes interest bearing NOW accounts, certificates of deposit (CD's), and other interest bearing financial instruments.

6. The quantity of commercial loans for all three sizes of community leveled off while nationally they continued to increase at a rate of 17 percent per year after 1986 when real interest rates began to decline.

7. The internal rate of return to an investment project equals the maximum interest rate that can be paid by the businesses after the investment recovers all the costs of the project including a residual profit for the investor. Increases in the real interest rate decreases the number of feasible projects by increasing the finance costs of the investment projects for businesses.

8. Each of the 49 community time series equations were tested for first order serial correlation. The hypothesis of no autocorrelation was accepted for 35 equations and inconclusive for the other 14 equations. Each of the 6 cross-sectional annual equations was tested for homoskedasticity. The hypothesis of homoskedasticity was accepted at the 10 percent level in 5 of the 6 years. The tests indicate that the ordinary least squares (OLS) estimates are unbiased and as efficient as estimates from more restric- tive generalized least squares (GLS) procedures.

9. While loans to the service profession and industrial projects are included in the commercial loans variable, previous research indicates most commercial loans in communities of the size in Southwest Minnesota are to retail businesses for operating and expansion purposes.

10. Ordinary least squares estimates from equation [2] are unbiased only if O,, is stochastic or independent of the error tern. To correct for the potential bias in the disturbance term, output in the previous period is measured with an instrumental variable. The Pearson correlation coefficient between real retail sales (0,) in the current period and the number of businesses (Ol.,) in the previous period was .97205 and the correlation between the error term of the equation and the instrumental variable (0, ,) was zero.

1 1 . The interaction term between the dummy variable and bank loans for each size of community was rotated so that the a standard error could be estimated for each investment coefficient. The standard errors could then be used in formal hypothesis testing about the magnitude of the estimated coefficient of adjustment across the different community sizes in the local hierarchy.

12. The share of total retail sales by community size was; largest communities = (.31681), mid-sized communities = (.46213), smallest communities = (.22 106). The sum of the estimated community coefficients of adjustment weighted by the percentage of total retail sales by community size equaled the estimated regional coefficient of adjustment for the whole hierarchy (.82669) with a rounding error at the second decimal point. (.93244)(.31680) + (1.10439)(.46213) + (.25658)(.22106) = .86248.

13. The estimaled coefficient of adjustment for the lowest ordered communities was - 25658 with a standard error of .13648. Using a two tailed test, the estimated coeffi- cient of adjustment for the lowest ordered community was statistically less than the estimated coefficients of adjustment for the mid-sized and highest ordered communities at the 1 percent level.

RETAIL BUSINESS ADJUSTMENT 93

REFERENCES

Barkley, D. and P. Helander. 1985. Commercial bank loans and non-metropolitan

Bemake, B. and A. Blinder. 1988. Credit, money, and aggregate demand. American

Buckwalter, D. 1990. Diverse retail structure and Christaller’s separation principle in

Dreese, G. 1974. Banks and regional economic development. Review of Regional Studies

Federal Reserve Bank of Chicago. 1956. Bank loans to businesses. Chicago. Fotheringham, A. 1983. A new set of spatial interaction models: The theory of competing

destinations, Environment and Planning A 15, 15-36. Henderson, D. 1990. Retail sales and consumer expenditure functions. The Journul of

Agricultural Research 42, 27-34. Ho, Y. 1979. Commercial banking and regional growth: The case of Wisconsin.

Unpublished Ph.D.dissertation. School of Business, University of Wisconsin--Madison. James, F. 1985. Economic impacts of private reinvestment in older regional shopping

centers. Growth and Change 16, 3:11-24. Morrill, R. 1982. Continuing deconcentration trends in trade. Growth and Change 13,

Pike, J. 1964. The structure and adequacy of Wisconsin commercial banking. Unpublished Ph.D. dissertation. Department of Agricultural Economics, University of Wisconsin-- Madison.

Rogers, G . , R. Shaffer, and G . Pulver. 1988. Identification of local capital markets for policy research. Review of Regional Studies 18, 55-66.

, 1990. The adequacy of capital markets for rural nonfarm businesses. Review of Regional Studies 20, 23-32.

Seninger, S. 1978. Expenditure diffusion in central place hierarchies: Regional policy and planning aspects. Journal of Regional Science 18, 243-61.

Shaffer, R. 1978 Commercial banking activity in West Central Wisconsin: 1969 and 1974. Research Report 2912. College of Agriculture and Life Science. University of Wisconsin-Madison.

Shaffer, R. and G . Pulver. 1990. Rural nonfarm businesses’ access to debt and equity capital. Staff Report AGES9070. Economic Research Service.

Taff, S., G . Pulver, and S. Staniforth. 1984. Are small community banks prepared to make complex business loans? Research Reporr 3263. College of Agriculture and Life Sciences., University of Wisconsin--Madison.

Walzer, N. and Ralph Stablein. 1981. Small towns and regional centers. Growrh and Change 12, 3:2-8.

economic activity: A question of causality. Review of Regional Studies 15, 26-32.

Economic Review 78 (May, Papers and Proceedings), 435-39.

medium-sized metropolitan areas. Growth and Change 2 1, 2: 15-33.

40, 647-56.

1 :46-48.