Embed Size (px)

Citation preview

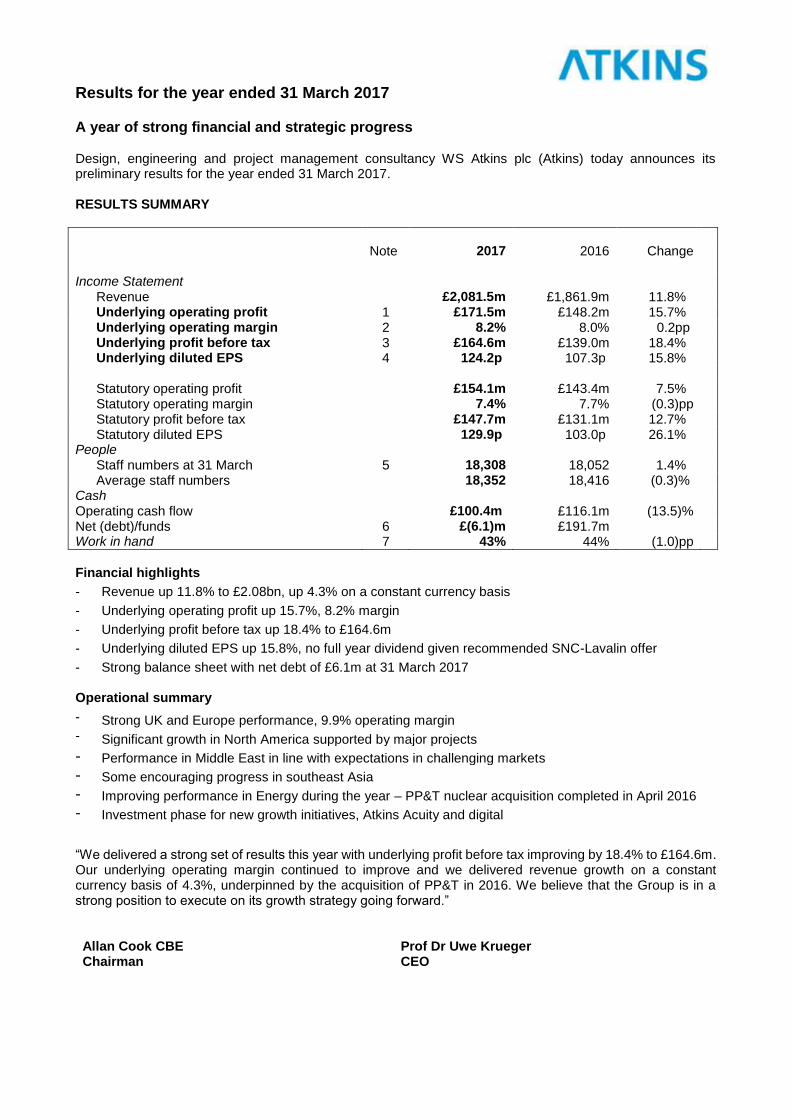

Results for the year ended 31 March 2017 A year of strong financial and strategic progress Design, engineering and project management consultancy WS Atkins plc (Atkins) today announces its preliminary results for the year ended 31 March 2017. RESULTS SUMMARY

Note

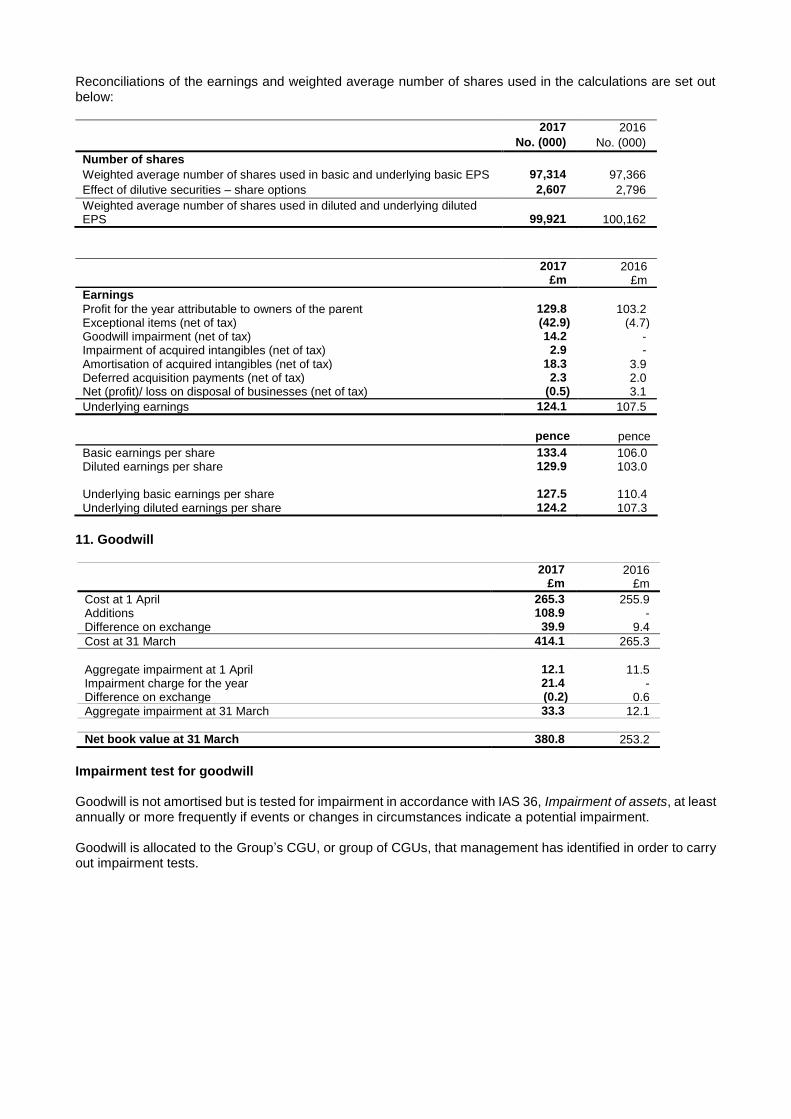

2017

2016

Change

Income Statement Revenue £2,081.5m £1,861.9m 11.8% Underlying operating profit 1 £171.5m £148.2m 15.7% Underlying operating margin 2 8.2% 8.0% 0.2pp Underlying profit before tax 3 £164.6m £139.0m 18.4% Underlying diluted EPS 4 124.2p 107.3p 15.8% Statutory operating profit £154.1m £143.4m 7.5% Statutory operating margin 7.4% 7.7% (0.3)pp Statutory profit before tax £147.7m £131.1m 12.7% Statutory diluted EPS 129.9p 103.0p 26.1% People Staff numbers at 31 March 5 18,308 18,052 1.4% Average staff numbers 18,352 18,416 (0.3)% Cash Operating cash flow £100.4m £116.1m (13.5)% Net (debt)/funds 6 £(6.1)m £191.7m Work in hand 7 43% 44% (1.0)pp

Financial highlights

- Revenue up 11.8% to £2.08bn, up 4.3% on a constant currency basis

- Underlying operating profit up 15.7%, 8.2% margin

- Underlying profit before tax up 18.4% to £164.6m

- Underlying diluted EPS up 15.8%, no full year dividend given recommended SNC-Lavalin offer

-

Strong balance sheet with net debt of £6.1m at 31 March 2017

Operational summary

- Strong UK and Europe performance, 9.9% operating margin - Significant growth in North America supported by major projects

- Performance in Middle East in line with expectations in challenging markets

- Some encouraging progress in southeast Asia

- Improving performance in Energy during the year – PP&T nuclear acquisition completed in April 2016

- Investment phase for new growth initiatives, Atkins Acuity and digital

“We delivered a strong set of results this year with underlying profit before tax improving by 18.4% to £164.6m. Our underlying operating margin continued to improve and we delivered revenue growth on a constant currency basis of 4.3%, underpinned by the acquisition of PP&T in 2016. We believe that the Group is in a strong position to execute on its growth strategy going forward.” Allan Cook CBE Chairman

Prof Dr Uwe Krueger CEO

On 20 April 2017 the boards of directors of WS Atkins plc (Atkins) and SNC-Lavalin Group Inc. (SNC-Lavalin) announced that they had reached agreement on the terms and conditions of a recommended offer for the entire issued and to be issued share capital of Atkins by SNC-Lavalin of 2,080 pence in cash per ordinary share of Atkins. Subject to the approval of shareholders and the Court, and to the satisfaction or (where applicable) waiver of the other conditions, the transaction is expected to become effective on 3 July 2017. As set out in the scheme document published by Atkins on 18 May 2017, the Kenya and the United States merger control conditions to the offer have been satisfied. In addition, the Botswana Competition Authority has, pursuant to the provisions of section 60 of the Competition Act 2009, unconditionally approved the proposed acquisition. Accordingly, the Botswana merger control condition in respect of the offer is satisfied. Notes:

1. Underlying operating profit is profit before exceptional items, impairment of goodwill and intangibles, amortisation of acquired intangibles and deferred acquisition payments.

2. Underlying operating margin is the value of underlying operating profit expressed as a percentage of revenue.

3. Underlying profit before tax additionally excludes net profit on disposal of businesses of £0.5m (2016: loss £3.1m).

4. Underlying diluted EPS is based on underlying profit after tax and allows for the dilutive effect of share options.

5. Staff numbers are shown on a full-time equivalent basis, including agency staff.

6. Net (debt)/funds comprise cash and cash equivalents plus financial assets and loan notes receivable less borrowings.

7. Work in hand is the value of contracted and committed work as at 31 March that is scheduled for the following financial year, expressed as a percentage of budgeted revenue for the year.

Enquiries Heath Drewett, Group finance director +44 (0) 20 7121 2000 Kate Moy, Group investor relations director +44 (0) 20 7121 2000 Matt Graydon, Group PR director +44 (0) 20 7121 2000

Notes to editors 1. Atkins Atkins (www.atkinsglobal.com) is one of the world’s most respected design, engineering and project management consultancies, employing over 18,300 people across the UK, North America, Middle East and Africa, Asia Pacific and Europe. We build long term trusted partnerships to create a world where lives are enriched through the implementation of our ideas. You can view Atkins’ recent projects on our website. 2. Alternative performance measures When explaining the Group’s performance, we make reference to a variety of performance measures. A large number of these are defined under International Financial Reporting Standards (IFRS). We also use measures that are not defined under IFRS and these are referred to as alternative performance measures (APMs). We believe they help provide the reader with a balanced view and clearer insight into the performance of the business, removing the items that may give a distorted view of performance. A breakdown of the items that we adjust for to calculate underlying profit is given in the Financial review. 3. Attachments Attached to this news release are the overview of the year, business review, financial review, statement of going concern, statement of directors’ responsibilities, the consolidated income statement, consolidated statement of comprehensive income, consolidated balance sheet, consolidated cash flow statement, consolidated statement of changes in equity and notes to the preliminary financial information for the year. 4. Analyst webcast at 0800 Dial-in details are available from +44 (0) 20 7353 4200 for those wishing to join the conference call. A webcast of the presentation will be available via the Company’s website, www.atkinsglobal.com. 5. Cautionary Statement This announcement has been prepared for the shareholders of Atkins as a whole and its sole purpose and use is to assist shareholders of Atkins to exercise their governance rights. Atkins and its directors and the Group’s employees are not responsible for any other purpose or use or to any other person in relation to this announcement and their responsibility to shareholders of Atkins shall be limited to that which is imposed by statute. This announcement contains indications of likely future developments and other statements which are, or may be deemed to be, ‘forward looking statements’. Forward looking statements are prospective in nature and are not based

on historical or current facts, but rather on current expectations and projections of the management of Atkins about future events, and are therefore subject to risk factors associated with, among other things, the economic and business circumstances occurring from time to time in the countries, sectors and business segments in which the Group operates. These and other factors could adversely affect the Group’s results, strategy and prospects. Forward looking statements involve risks, uncertainties and assumptions. They relate to events and/or depend on circumstances in the future which could cause actual results and outcomes to differ materially from the future results expressed or implied by the forward-looking statements. You are cautioned not to place any reliance on these forward looking statements. No obligation is assumed to update or revise any forward looking statements, whether as a result of new information, future events or otherwise. Nothing in this announcement should be construed as a profit forecast. All persons, wherever located, should consult any additional disclosures that Atkins may make in any regulatory announcements or documents which it publishes. All persons, wherever located, should take note of these disclosures. The information in this announcement does not constitute an offer to sell or an invitation to buy shares in Atkins or an invitation or inducement to engage in any other investment activities. Past performance cannot be relied upon as a guide to future performance. 6. Publication on a website A copy of this announcement and the preliminary results video are available on Atkins’ website at www.investors.atkinsglobal.com/results-centre.

OVERVIEW OF THE YEAR We delivered a strong set of results this year. We have continued to improve our underlying operating margin along with revenue that rose 11.8% to £2.08bn (2016: £1.86bn) up 4.3% on a constant currency basis. Underlying operating profit increased 15.7% to £171.5m (2016: £148.2m), at an improved underlying operating margin of 8.2% (2016: 8.0%). In October 2016, we were pleased to complete the acquisition of Howard Humphreys, a multidisciplinary consultancy based in Kenya and Tanzania which provides engineering consultancy and project management services in the transportation, water and property markets. The acquisition will provide an important catalyst to develop our presence within East Africa’s rapidly growing infrastructure market. On 20 April 2017, the boards of directors of SNC-Lavalin and Atkins announced that they had reached agreement on the terms and conditions of a recommended all cash offer for the Company. The board of directors of SNC-Lavalin expects the acquisition to enhance SNC-Lavalin’s global position and addressable market in infrastructure, rail & transit and nuclear, combine two highly complementary businesses and increase both geographic reach and customer diversification globally. Underlying profit before tax of £164.6m (2016: £139.0m) is arrived at after adjusting for exceptional income totalling £41.7m (2016: exceptional income £4.7m), amortisation of acquired intangible assets of £29.2m (2016: £6.3m), deferred acquisition payments of £3.7m (2016: £3.2m), impairment of goodwill in both our Energy business in North America and our aerospace business in the Netherlands, which total £21.4m (2016: £nil), impairment of acquired intangibles of £4.8m (2016: £nil) and a residual gain of £0.5m on the sale of our Highway Services business in 2013 (2016: £3.1m loss on sale of Portuguese business). Profit is arrived at after reflecting realised and unrealised foreign exchange gains of £9.6m. Underlying diluted earnings per share rose 15.8% to 124.2p (2016: 107.3p). Operating cash flow in the year was £100.4m (2016: £116.1m), representing 65.2% (2016: 81.0%) of operating profit on a reported basis. The Group’s balance sheet remains strong with closing net debt of £6.1m (2016: net funds £191.7m). The Group pension schemes have seen the net IAS 19 pension liability reduce to £235.7m (2016: £265.3m). Closing staff numbers were 18,308 (2016: 18,052). This primarily reflects the acquisition of PP&T and Howard Humphreys, offset in part by reductions in oil and gas, as well as the Middle East, as we focused on improving productivity. Our UK and Europe business delivered another set of strong results with a 22.5% increase in operating profit to £90.4m (2016: £73.8m). While revenue reduced 3.4% to £911.1m, primarily as a result of a reduction in rail signalling revenue, margin improved to 9.9% (2016: 7.8%), helped by overhead efficiency savings. During the period, as part of our ongoing portfolio optimisation, we were pleased to complete the sale of our minority PFI investment in the M25 motorway to Edge Orbital Holdings 2 Limited, for a cash consideration of £66.3m. This has been adjusted for when arriving at underlying earnings and is not included in the segmental operating profit referred to above. Our North America business delivered significant growth this year. Revenue rose 32.5% (14.0% on a constant currency basis) due to increased major project volume in our department of transportation and intermodal businesses. Operating profit rose 64.2% (43.6% on a constant currency basis) at a much improved margin of 7.0% (2016: 5.6%). In addition, our technical professional organisation is seeing improved productivity and we have been able to utilise the Group’s global design centre capabilities in India on major projects including Purple Line and project NEON. Despite the overall challenging market environment in the region, our Middle East and Africa business has traded in line with our expectations. Revenue was down 6.5% at £232.2m at an operating margin of 9.4% (2016: 11.9%). The market liquidity situation continues to put pressure on working capital and debt collection, which remains a key focus across the region. The integration of Howard Humphreys is progressing well and already generating opportunities. Our Asia Pacific business has traded in line with our expectations this year. Revenue increased 11.4% to £118.2m (2016: £106.1m), a 1.4% reduction on a constant currency basis, at an operating margin of 7.9% (2016: 8.0%). During the year we secured a number of architectural projects including the iconic Cocobay Towers in Danang, Vietnam and we were particularly pleased to be awarded the advance engineering study for a key section of the proposed Cross Island Line in Singapore.

Market conditions for our Energy business improved in the second half, particularly in oil and gas. Nuclear performed well during the year and power and renewables remain in line with our expectations. The challenges in some oil and gas markets reduced in the second half as oil prices stabilised. Revenue and operating profit rose to £327.0m and £30.3m respectively (2016: £201.3m and £16.7m respectively), reflecting the acquisition of PP&T which completed in April 2016 and contributed revenue of £142.8m in the year. Our margin improved to 9.3% (2016: 8.3%). We are making headway into the Chinese renewables market with a recent appointment to design the offshore substation platform for the Binhai South Phase3 offshore windfarm in the Yellow Sea, our first offshore wind project in China. People We continue our work to attract more people into pursuing a career in the engineering sector. During the year, we welcomed over 300 new graduates across the Group and accelerated our apprentice programme by recruiting 60 apprentices within our UK business. We are a member of the ‘5% Club’, an industry-led campaign whose member organisations make a public commitment to have at least 5% of their UK workforce on formal graduate and apprenticeship schemes. Our current proportion is 11.9% (2016: 12.3%) of UK headcount. A more diverse and inclusive workforce is required to address the critical skills shortage in our industry and we are committed to building a more diverse and inclusive organisation globally. A women’s professional network is now well established in all our major office locations and we continue to roll out our flexible working practices across the Group. Dividend An interim dividend of 12.5p per share was paid on 6 January 2017 to all shareholders on the register on 25 November 2016. On 20 April 2017 the boards of directors of Atkins and SNC-Lavalin announced they had reached agreement on the terms and conditions of a recommended all cash offer for the entire issued and to be issued share capital of Atkins by SNC-Lavalin of 2,080 pence in cash per ordinary share of Atkins. The offer price has been agreed on the basis that no final dividend for the financial year ended 31 March 2017 will be paid by Atkins to its shareholders. If Atkins announces, declares, makes or pays any dividend or other distribution prior to the acquisition becoming effective, SNC-Lavalin reserves the right to reduce the offer price by an amount equal to the amount of such dividend or distribution. Outlook We are successfully delivering on our three strategic growth priorities. Despite an uncertain macroeconomic environment, our focused strategy and execution has supported total shareholder returns (TSR) of 144% over the five years to 31 March 2017. Our strategy to position the business in end-markets with favourable long-term trends, together with specific growth initiatives such as our Acuity advisory business, our expansion in nuclear engineering and our focus on digital and technology, position us well for future growth.

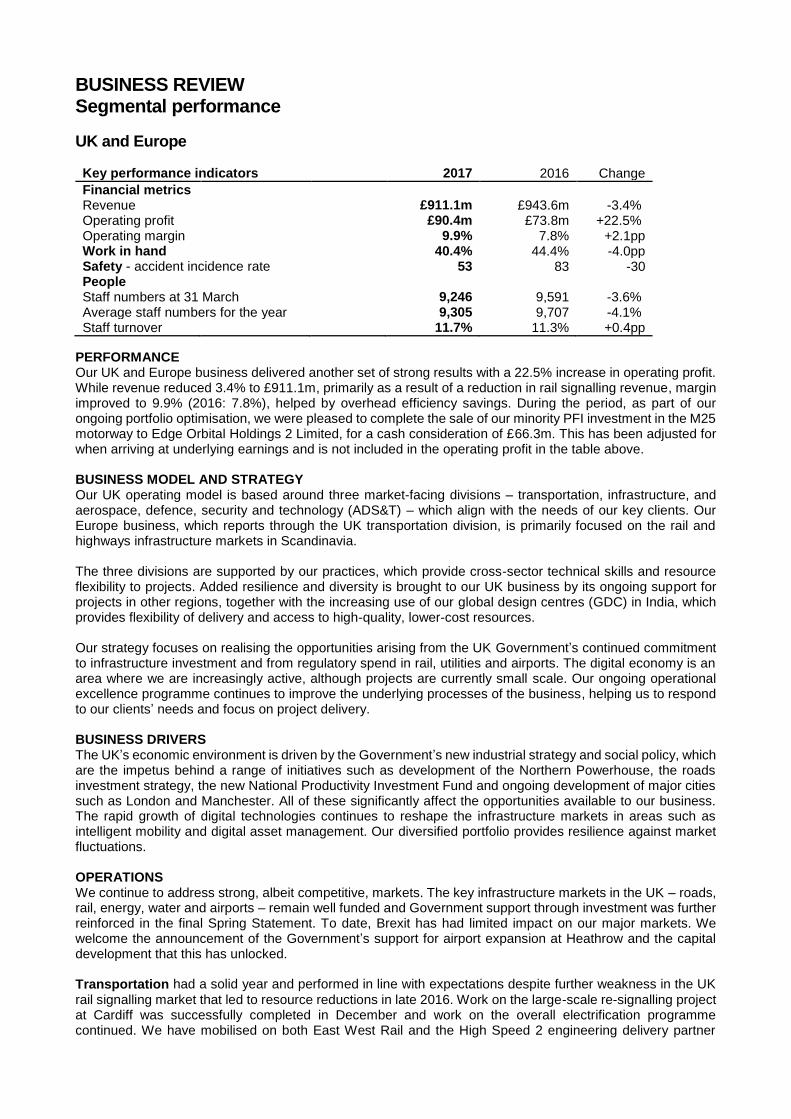

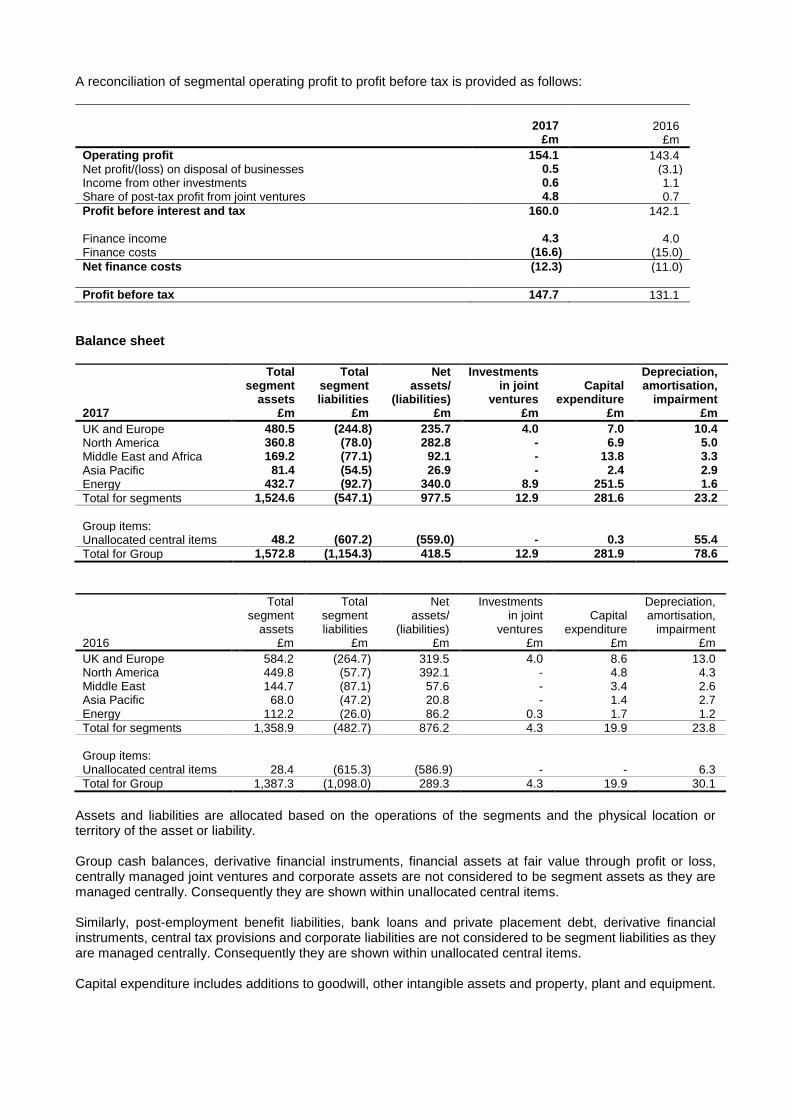

BUSINESS REVIEW Segmental performance

UK and Europe Key performance indicators 2017 2016 Change

Financial metrics Revenue £911.1m £943.6m -3.4% Operating profit £90.4m £73.8m +22.5% Operating margin 9.9% 7.8% +2.1pp Work in hand 40.4% 44.4% -4.0pp Safety - accident incidence rate 53 83 -30 People Staff numbers at 31 March 9,246 9,591 -3.6% Average staff numbers for the year 9,305 9,707 -4.1% Staff turnover 11.7% 11.3% +0.4pp

PERFORMANCE Our UK and Europe business delivered another set of strong results with a 22.5% increase in operating profit. While revenue reduced 3.4% to £911.1m, primarily as a result of a reduction in rail signalling revenue, margin improved to 9.9% (2016: 7.8%), helped by overhead efficiency savings. During the period, as part of our ongoing portfolio optimisation, we were pleased to complete the sale of our minority PFI investment in the M25 motorway to Edge Orbital Holdings 2 Limited, for a cash consideration of £66.3m. This has been adjusted for when arriving at underlying earnings and is not included in the operating profit in the table above. BUSINESS MODEL AND STRATEGY Our UK operating model is based around three market-facing divisions – transportation, infrastructure, and aerospace, defence, security and technology (ADS&T) – which align with the needs of our key clients. Our Europe business, which reports through the UK transportation division, is primarily focused on the rail and highways infrastructure markets in Scandinavia. The three divisions are supported by our practices, which provide cross-sector technical skills and resource flexibility to projects. Added resilience and diversity is brought to our UK business by its ongoing support for projects in other regions, together with the increasing use of our global design centres (GDC) in India, which provides flexibility of delivery and access to high-quality, lower-cost resources. Our strategy focuses on realising the opportunities arising from the UK Government’s continued commitment to infrastructure investment and from regulatory spend in rail, utilities and airports. The digital economy is an area where we are increasingly active, although projects are currently small scale. Our ongoing operational excellence programme continues to improve the underlying processes of the business, helping us to respond to our clients’ needs and focus on project delivery. BUSINESS DRIVERS The UK’s economic environment is driven by the Government’s new industrial strategy and social policy, which are the impetus behind a range of initiatives such as development of the Northern Powerhouse, the roads investment strategy, the new National Productivity Investment Fund and ongoing development of major cities such as London and Manchester. All of these significantly affect the opportunities available to our business. The rapid growth of digital technologies continues to reshape the infrastructure markets in areas such as intelligent mobility and digital asset management. Our diversified portfolio provides resilience against market fluctuations. OPERATIONS We continue to address strong, albeit competitive, markets. The key infrastructure markets in the UK – roads, rail, energy, water and airports – remain well funded and Government support through investment was further reinforced in the final Spring Statement. To date, Brexit has had limited impact on our major markets. We welcome the announcement of the Government’s support for airport expansion at Heathrow and the capital development that this has unlocked. Transportation had a solid year and performed in line with expectations despite further weakness in the UK

rail signalling market that led to resource reductions in late 2016. Work on the large-scale re-signalling project at Cardiff was successfully completed in December and work on the overall electrification programme continued. We have mobilised on both East West Rail and the High Speed 2 engineering delivery partner

contract, where our joint venture with CH2M is seeing good volumes. We are also leading on the business case development and preliminary design work for Crossrail 2 for Transport for London (TfL) and Network Rail respectively. In the second half, positions were re-secured on frameworks for TfL and Transport for Greater Manchester. Work on the A14 and smart motorways programme continues and several small wins on autonomous vehicle projects were also achieved. Infrastructure delivered a good performance in a competitive market. Our pipeline of work from water utility clients remains strong with our appointment to the Thames Water Professional Services Framework and a strengthened position in water consultancy services through other framework wins. Work on the Thames Tideway Tunnel is progressing well. We are developing a new digital solution for Thames Water to help it achieve significant operational savings. At Heathrow we secured a role, as part of an integrated team, to support planning and early design for the expansion programme. We have also won a contract for the design work on a major new college for Ealing and Hammersmith. ADS&T performed well this year. Its defence and security sectors enjoy strong markets with good wins in year

and a solid pipeline for both. However, the aerospace market remains challenging resulting in the decision to close our aerospace office in the Netherlands. This resulted in an impairment of goodwill of £2.9m, which does not form part of underlying earnings and therefore is not shown in the table above. Faithful+Gould had a good first half but began to see a slowdown in the UK market in the commercial property

sector in the South East in the second half. Although unsuccessful on the rebid of the SCAPE framework, we continue to deliver on our pipeline of work for the education sector, local government and in support of EDF on Hinkley Point C. We have been successful in a joint bid with the infrastructure division to deliver a large programme of school surveys. PEOPLE Closing staff numbers reduced to 9,246 (2016: 9,591) - UK: 8,465 (2016: 8,873), Europe: 781 (2016: 757). Staff turnover increased to 11.7% from 11.3%. In the UK, we continue to implement programmes to assist with the attraction, engagement and retention of talented people and are recognised by a number of independent organisations as a great place to work. We retained a place in The Sunday Times 30 Best Big Companies to Work For. The ongoing promotion of science, technology, engineering and mathematics (STEM) careers to young people continues to be a focus. Over 500 STEM ambassadors took part in more than 450 STEM activities with schools, colleges and community groups, engaging with thousands of students. During the year, over 300 people including 60 apprentices joined the UK business on formal education and development programmes. Focus on increasing the proportion of female employees continues and a range of flexible working options has been developed to help us both recruit and retain staff. We recruited 67 female graduates in the September 2016 intake, 26% of the total. In line with the rest of the Group, employee engagement is measured through our Viewpoint employee opinion survey. Across the region, our results in 2016 were down two points compared with the previous year, an understandable result given the continued reshaping of our UK business and the difficult conditions in aerospace and rail signalling. The result continued to outperform the global norm for the professional services sector. Following the survey, action plans have been developed to focus on recognition, wellbeing and career paths. SAFETY Workplace health, safety and wellbeing continue to be a high priority. In the UK the number of reportable accidents reduced to five while in Europe there were no reportable accidents during the year. RISKS SPECIFIC TO THE UK AND EUROPE Atkins’ corporate position on Brexit is fully aligned with that of the Institution of Civil Engineers and the CBI. We will continue to monitor developments closely following the triggering of Article 50 and seek to position ourselves to take advantage of the opportunities that emerge. Following the result of the recent UK election, infrastructure continues to have strong cross-party support and we anticipate that investment will remain a priority.

There is a risk in the medium to long term of a shortage of professional technical staff in our industry and our research has highlighted apprenticeships as one of the most effective ways to solve this. The majority of the Group’s post-employment benefit liability sits within the UK business and is comprised of defined benefit pension obligations, the largest of which is within the Atkins Pension Plan, which is closed to the future accrual of benefits (see note 14 for more details). The pension obligations are recognised as a risk due to their size and the fact that the ongoing liability is a function of a number of assumptions, not least the life expectancy of members. This risk is mitigated by ongoing cash contributions to the pension fund, which have been agreed recently with the pension trustee as part of the 2016 triennial valuation, along with measures to manage ongoing volatility.

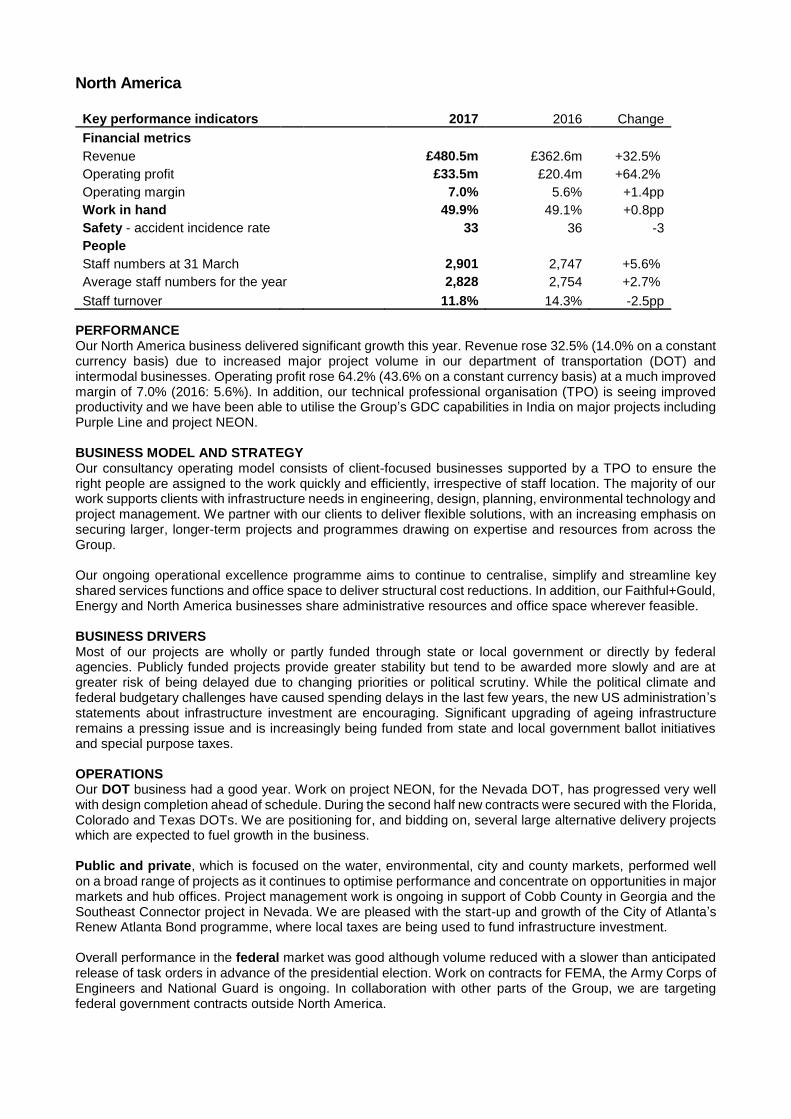

North America

Key performance indicators 2017 2016 Change

Financial metrics Revenue £480.5m £362.6m +32.5%

Operating profit £33.5m £20.4m +64.2%

Operating margin 7.0% 5.6% +1.4pp

Work in hand 49.9% 49.1% +0.8pp

Safety - accident incidence rate 33 36 -3

People Staff numbers at 31 March 2,901 2,747 +5.6%

Average staff numbers for the year 2,828 2,754 +2.7%

Staff turnover 11.8% 14.3% -2.5pp

PERFORMANCE Our North America business delivered significant growth this year. Revenue rose 32.5% (14.0% on a constant currency basis) due to increased major project volume in our department of transportation (DOT) and intermodal businesses. Operating profit rose 64.2% (43.6% on a constant currency basis) at a much improved margin of 7.0% (2016: 5.6%). In addition, our technical professional organisation (TPO) is seeing improved productivity and we have been able to utilise the Group’s GDC capabilities in India on major projects including Purple Line and project NEON. BUSINESS MODEL AND STRATEGY Our consultancy operating model consists of client-focused businesses supported by a TPO to ensure the right people are assigned to the work quickly and efficiently, irrespective of staff location. The majority of our work supports clients with infrastructure needs in engineering, design, planning, environmental technology and project management. We partner with our clients to deliver flexible solutions, with an increasing emphasis on securing larger, longer-term projects and programmes drawing on expertise and resources from across the Group. Our ongoing operational excellence programme aims to continue to centralise, simplify and streamline key shared services functions and office space to deliver structural cost reductions. In addition, our Faithful+Gould, Energy and North America businesses share administrative resources and office space wherever feasible. BUSINESS DRIVERS Most of our projects are wholly or partly funded through state or local government or directly by federal agencies. Publicly funded projects provide greater stability but tend to be awarded more slowly and are at greater risk of being delayed due to changing priorities or political scrutiny. While the political climate and federal budgetary challenges have caused spending delays in the last few years, the new US administration’s statements about infrastructure investment are encouraging. Significant upgrading of ageing infrastructure remains a pressing issue and is increasingly being funded from state and local government ballot initiatives and special purpose taxes. OPERATIONS Our DOT business had a good year. Work on project NEON, for the Nevada DOT, has progressed very well with design completion ahead of schedule. During the second half new contracts were secured with the Florida, Colorado and Texas DOTs. We are positioning for, and bidding on, several large alternative delivery projects which are expected to fuel growth in the business. Public and private, which is focused on the water, environmental, city and county markets, performed well on a broad range of projects as it continues to optimise performance and concentrate on opportunities in major markets and hub offices. Project management work is ongoing in support of Cobb County in Georgia and the Southeast Connector project in Nevada. We are pleased with the start-up and growth of the City of Atlanta’s Renew Atlanta Bond programme, where local taxes are being used to fund infrastructure investment. Overall performance in the federal market was good although volume reduced with a slower than anticipated release of task orders in advance of the presidential election. Work on contracts for FEMA, the Army Corps of Engineers and National Guard is ongoing. In collaboration with other parts of the Group, we are targeting federal government contracts outside North America.

We achieved significant growth in intermodal over the year. Purple Line work saw a slower start than anticipated, however improved volume and new wins in aviation resulted in positive momentum to finish the year. Collaboration with our GDC, and the broad depth of resources and capabilities available across the Group, helped establish a stronger position as we build on Purple Line to pursue larger projects and expand into the North America rail market going forward. Overall Faithful+Gould delivered a stable performance in its focus markets of aviation, manufacturing and pharmaceuticals. Following the successful renewal of the Bruce Power framework we continue to see opportunities in the energy sector. Manufacturing remains important with increased workload in the second half. We secured contracts for United at Houston and Newark airports and for the City and County of Denver at Denver Airport. We also secured a new three-year framework with BP and continue our work with Google. PEOPLE Headcount increased to 2,901 (2016: 2,747), reflecting the overall growth of the business. Focus remains on attracting and retaining key staff and, encouragingly, staff turnover fell to 11.8% from 14.3%. We are committed to recruiting, retaining, developing, and elevating minority and women professionals at every level of the organisation. We are using technology to reach diverse pools of candidates that are often not accessible via traditional job advertising. Our Atkins Minority Scholarship programme funds scholarships for deserving minority students in STEM majors. Our overall employee engagement score improved two points, although the response rate declined. Our goal is to be viewed as the employer of choice within the architecture, engineering and construction industry. SAFETY Our safety culture plays a central role in how we deliver work. The slight improvement in the accident incidence rate arose as a result of the increase in staff numbers, with no increase in the number of accidents this year. RISKS SPECIFIC TO NORTH AMERICA Most of our work is government funded and political uncertainty may lead to delays in federal programmes and funding. We monitor Congress’s activities for continued programme funding, particularly around transportation and highways, where delays would most significantly affect our workload. Support for federal funding of military and civilian programmes is also an area of risk for our task order based contracts.

Middle East and Africa

Key performance indicators 2017 2016 Change

Financial metrics Revenue £232.2m £248.3m -6.5%

Operating profit £21.8m £29.5m -26.1%

Operating margin 9.4% 11.9% -2.5pp

Work in hand 51.0% 48.0% +3.0pp

Safety - accident incidence rate 40 39 +1

People Staff numbers at 31 March 2,469 2,459 +0.4%

Average staff numbers for the year 2,453 2,580 -4.9%

Staff turnover 10.5% 10.7% -0.2pp

PERFORMANCE Despite the overall challenging market environment in the region, our Middle East and Africa (MEA) business has traded in line with our expectations. Revenue was down 6.5% at £232.2m (20.8% reduction on a constant currency basis) at an operating margin of 9.4% (2016: 11.9%). The market liquidity situation continues to put pressure on working capital and debt collection, which remains a key focus across the region. BUSINESS MODEL AND STRATEGY Our business model is to maintain strong, local resources in our chosen markets complemented by the increasing use of our GDC. This provides agility and efficiency by maximising our ability to mobilise for major projects, while minimising exposure to individual market resource demands and constraints. We focus on transportation, infrastructure and property in the United Arab Emirates (UAE), the Kingdom of Saudi Arabia (KSA) and Qatar. Despite recent slowdowns, we believe the region continues to offer opportunities linked to the drive for economic diversification and the need to invest in social infrastructure. Our strategy is aimed at carefully selecting and securing critical, complex projects and programmes with established key clients who need a long-term partner. In addition, local resources support our Energy business in the region. BUSINESS DRIVERS The economic climate in the Middle East is primarily driven by the global oil price. This affects demand for our services since regional spending ultimately flows through to capital investment in infrastructure, transportation and property. The prolonged low oil price has caused client decision-making to slow, with increased uncertainty around the award of projects. We believe the longer term need to invest in strategically important infrastructure that supports economic growth and diversification will continue to drive demand for our services. However, short-term project timing, scale and phasing are increasingly subject to review. Africa is seeing major investment in transportation, infrastructure and energy, presenting strong demand for world-class multidisciplinary design and consultancy services. OPERATIONS Our business delivered a good performance overall this year with a much improved second half, further reinforcing our position among the Middle East’s leading design, engineering and project management consultancies. Delivery of design packages on major projects and programmes in rail across the region continued, including our design work on Doha Metro in Qatar. The majority of originally contracted work on the Riyadh Metro project in KSA has now been successfully completed. We were pleased to secure a number of strategic contracts in the property market at the end of the year, although some of these have been a little slow to be initiated by our clients. In KSA we are seeing some early signs of an improvement as the oil price has stabilised. Property sector activity in the UAE remains buoyant, driven by its hosting of Expo 2020, and the Dubai Opera was successfully opened in August 2016. Transport and infrastructure markets remain challenging, with a number of significant award delays.

The integration of Howard Humphreys in East Africa is progressing well, following completion of the acquisition in October 2016, and the business is already generating diversification opportunities. Our Faithful+Gould business had a mixed year with property wins in KSA, Dubai and Abu Dhabi, while market

liquidity increased client caution on investment in new projects. In conjunction with site operations colleagues, we have secured a significant programme management office and supervision role on a major defence sector programme in KSA. PEOPLE Closing headcount was flat at 2,469 (2016: 2,459). Some 160 staff joined from Howard Humphreys but this was offset by restructuring to reflect more challenging conditions in the Middle East transportation and infrastructure markets in particular. Staff turnover was stable at 10.5% (2016: 10.7%). The overall employee engagement score reduced by two points but remains both the highest in the Group and ahead of industry norms. The response rate increased to 82% (2016: 66%) a significant improvement considering the challenging context in which the business was operating. In the Middle East and Africa, our aim is to be the employer of choice for women and our women’s business network played a leading role in the review of our maternity policy, which is now one of the most progressive in our industry in the region. SAFETY Although the number of major accidents was unchanged, the accident incidence rate deteriorated very slightly due to the reduction in average headcount. RISKS SPECIFIC TO MEA Certain countries within MEA have greater potential for political change. It is also a region with an increased risk of payment delays. We have been operating in the Middle East since 1967, giving us insight into the political environment and helping us to mitigate political and commercial risks. Further uncertainty around the oil price presents a major risk because of the impact on government spending and the knock-on effect on private sector confidence. Our focus on strategically important projects and programmes gives us some insulation from short-term changes, which partially mitigates this risk. Construction safety remains an elevated risk in MEA. We are mitigating this wherever possible and have been instrumental in creating improved standards for the industry through initiatives such as the Atkins Minimum Requirements.

Asia Pacific

Key performance indicators 2017 2016 Change

Financial metrics Revenue £118.2m £106.1m +11.4%

Operating profit £9.3m £8.5m +9.4%

Operating margin 7.9% 8.0% -0.1pp

Work in hand 47.6% 46.1% +1.5pp

Safety - accident incidence rate 86 209 -123

People Staff numbers at 31 March 1,275 1,354 -5.8%

Average staff numbers for the year 1,289 1,448 -11.0%

Staff turnover 18.6% 18.7% -0.1pp

PERFORMANCE Our Asia Pacific business has traded in line with our expectations this year. Revenue increased 11.4% to £118.2m (2016: £106.1m) (1.4% reduction on a constant currency basis) at an operating margin of 7.9% (2016: 8.0%). Our profitability and cash flow performance were again impacted by delays to the start of opportunities and cash receipts from some clients extending beyond agreed contract terms. BUSINESS MODEL AND STRATEGY We operate predominantly in Hong Kong and mainland China, supplemented by a network of offices across southeast Asia including Malaysia, Vietnam and Singapore, as well as India and Australia, offering our clients a range of services throughout the entire cycle of urban development. We work in partnership with chosen Chinese contractors on their domestic and international projects. Our strategy of geographic and market diversification continues, supported by our new Acuity advisory business. The focus is on urban planning, transport, infrastructure and property in the southeast Asian markets. Our multidisciplinary offering with Faithful+Gould provides a more integrated service for private sector clients in the region. In Hong Kong, we continue to expand our service offering and project portfolio in the infrastructure sector. In mainland China, property market conditions have led to the restructuring and right-sizing of our teams, but we see a more stable market looking forward. We will increasingly target state-owned enterprises and larger developers who have the financial capability to take major projects forward. BUSINESS DRIVERS Our growth potential in the region is underpinned by the scale of urbanisation driving both government spending and the rate of private sector investment. Outside Asia Pacific, good business opportunities exist for the Group as a whole as major Chinese companies invest in large scale infrastructure development projects outside their domestic market. OPERATIONS In Hong Kong, we secured additional design packages of work on the third runway at Hong Kong International Airport as we expanded our project portfolio. We remain cautious about the strength and sustainability of the recovery in the mainland China property market. Our overseas work with Chinese contractors continues with new project wins secured during the year in the Philippines, Africa and the Middle East in the property, transport and infrastructure sectors. We are also supporting Chinese developers in outbound investments in urban development. We have been appointed by CHEC Port City Colombo (Private) Limited to provide consultancy services in relation to the design of infrastructure and landscape works for the proposed Colombo Port City Development Project in Sri Lanka. The proposed city will be built on 269 hectares of reclaimed land and expects a future population of 250,000 people.

In southeast Asia, we secured a number of architectural project wins including the iconic Cocobay Towers in

Danang, Vietnam, consisting of twin towers rising to a height of approximately 200 metres. We worked with a major Malaysian industrial firm on a masterplan for a 348 hectare mixed-use, high-value manufacturing park, enabling it to move into new sectors and contribute to national industrial development. Our work to support Prasarana in a client advisory role on the delivery of its LRT3 light railway project in Malaysia continues. We are working with the Land Transport Authority (LTA) on the Jurong Regional Line in Singapore, a 20km new line that is expected to be completed by around 2025. We were particularly pleased to be awarded the advance engineering study for a key section of the proposed Cross Island Line in Singapore by the LTA. Our Faithful+Gould business had a mixed year. Activity in mainland China slowed in the first half, due to

reduced direct investment there by international clients. However, in the second half, we were pleased to be awarded a number of smaller retail, data centre, manufacturing and leisure contracts in China, Hong Kong and India and saw continued growth overall in the rest of Asia. PEOPLE Overall headcount in our Asia Pacific region decreased in the year to 1,275 (2016: 1,354) as we streamlined our businesses in mainland China and Hong Kong. Staff turnover has remained broadly unchanged at 18.6% (2016: 18.7%). The Asia Pacific Women’s Professional Network, which was launched last year, has gained momentum and is focusing on initiatives around facilitating the return to work and flexible working of staff, as well as enhanced maternity benefits. SAFETY The accident incidence rate has decreased significantly in Asia Pacific with only one reportable accident in the year. RISKS SPECIFIC TO ASIA PACIFIC Expanding our footprint across the region brings increased risks such as lack of commercial transparency, political instability and risks associated with operating within unfamiliar regulatory, tax and employment regimes. We undertake due diligence into both the market and specific clients, as well as using professional advisors to assist with legal and regulatory compliance.

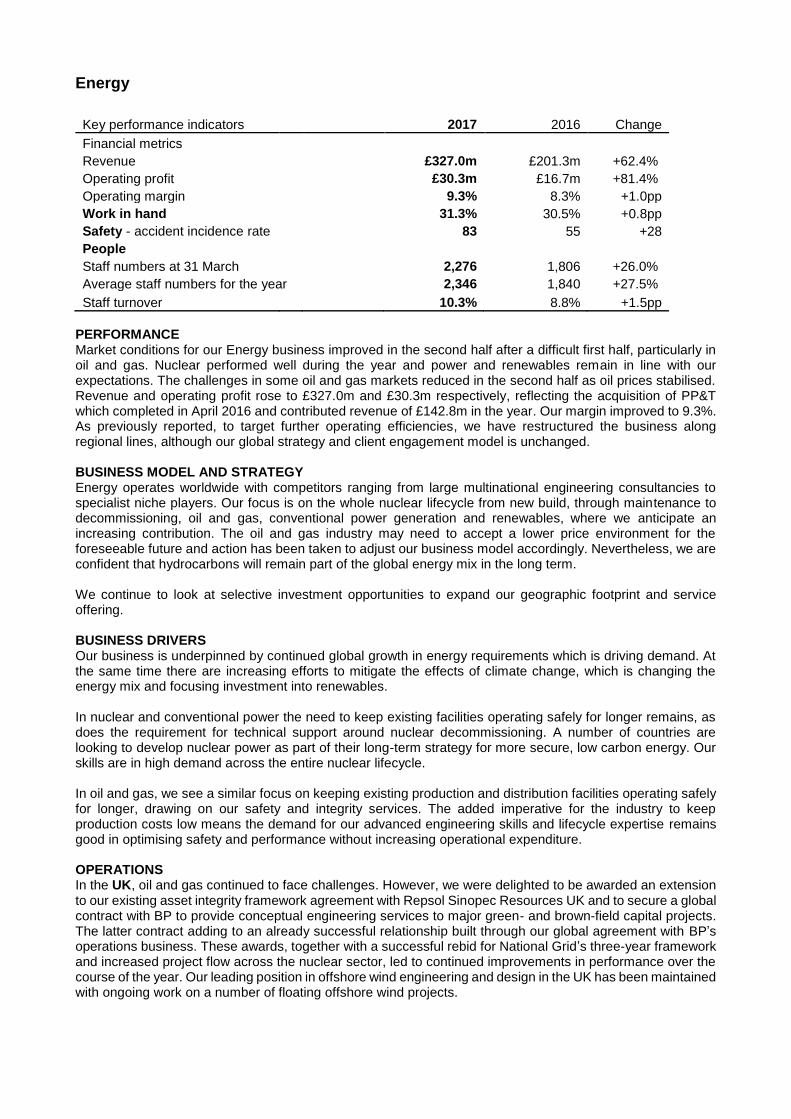

Energy

Key performance indicators 2017 2016 Change

Financial metrics Revenue £327.0m £201.3m +62.4%

Operating profit £30.3m £16.7m +81.4%

Operating margin 9.3% 8.3% +1.0pp

Work in hand 31.3% 30.5% +0.8pp

Safety - accident incidence rate 83 55 +28

People Staff numbers at 31 March 2,276 1,806 +26.0%

Average staff numbers for the year 2,346 1,840 +27.5%

Staff turnover 10.3% 8.8% +1.5pp

PERFORMANCE Market conditions for our Energy business improved in the second half after a difficult first half, particularly in oil and gas. Nuclear performed well during the year and power and renewables remain in line with our expectations. The challenges in some oil and gas markets reduced in the second half as oil prices stabilised. Revenue and operating profit rose to £327.0m and £30.3m respectively, reflecting the acquisition of PP&T which completed in April 2016 and contributed revenue of £142.8m in the year. Our margin improved to 9.3%. As previously reported, to target further operating efficiencies, we have restructured the business along regional lines, although our global strategy and client engagement model is unchanged. BUSINESS MODEL AND STRATEGY Energy operates worldwide with competitors ranging from large multinational engineering consultancies to specialist niche players. Our focus is on the whole nuclear lifecycle from new build, through maintenance to decommissioning, oil and gas, conventional power generation and renewables, where we anticipate an increasing contribution. The oil and gas industry may need to accept a lower price environment for the foreseeable future and action has been taken to adjust our business model accordingly. Nevertheless, we are confident that hydrocarbons will remain part of the global energy mix in the long term. We continue to look at selective investment opportunities to expand our geographic footprint and service offering. BUSINESS DRIVERS Our business is underpinned by continued global growth in energy requirements which is driving demand. At the same time there are increasing efforts to mitigate the effects of climate change, which is changing the energy mix and focusing investment into renewables. In nuclear and conventional power the need to keep existing facilities operating safely for longer remains, as does the requirement for technical support around nuclear decommissioning. A number of countries are looking to develop nuclear power as part of their long-term strategy for more secure, low carbon energy. Our skills are in high demand across the entire nuclear lifecycle. In oil and gas, we see a similar focus on keeping existing production and distribution facilities operating safely for longer, drawing on our safety and integrity services. The added imperative for the industry to keep production costs low means the demand for our advanced engineering skills and lifecycle expertise remains good in optimising safety and performance without increasing operational expenditure. OPERATIONS In the UK, oil and gas continued to face challenges. However, we were delighted to be awarded an extension to our existing asset integrity framework agreement with Repsol Sinopec Resources UK and to secure a global contract with BP to provide conceptual engineering services to major green- and brown-field capital projects. The latter contract adding to an already successful relationship built through our global agreement with BP’s operations business. These awards, together with a successful rebid for National Grid’s three-year framework and increased project flow across the nuclear sector, led to continued improvements in performance over the course of the year. Our leading position in offshore wind engineering and design in the UK has been maintained with ongoing work on a number of floating offshore wind projects.

In North America, the trading environment for our largely offshore-focused oil and gas businesses remained very challenging in the first half of the year resulting in the review and impairment of the carrying value of goodwill and acquired intangible assets in its oil and gas business by £23.3m. The US Tier 1 nuclear decommissioning market is developing well for us, following the acquisition of PP&T. In September 2016, we were delighted to win a contract to operate depleted uranium hexafluoride (DUF6) conversion over a five-year period at facilities in Kentucky and Ohio – our first major nuclear contract in North America since completing the acquisition of PP&T in April 2016. In the Middle East, nuclear continued to trade well, although there has been a slowdown in the pipeline of work for our power business and headcount has been reduced. Our oil and gas business performance, while starting to slow, remained good in the year and we continue to work with Abu Dhabi Marine Operating Company to help extend the life of Abu Dhabi’s oil and gas facilities. In the second half of the year, product sales to Asia associated with the treatment of decontaminated water at the Fukushima site have made good progress. We are making headway into the Chinese renewables market with a recent appointment by PowerChina Huadong Engineering Co. Ltd to design the offshore substation platform at State Power Investment Corporation’s 300MW Binhai SouthPhase3 offshore wind farm in the Yellow Sea. The contract win represents a landmark achievement as the first offshore wind project for Atkins in China. PEOPLE Headcount increased 26.0% to 2,276 (2016: 1,806). Some 600 colleagues joined from PP&T, although this was partially offset by rationalisation in our oil and gas business. Staff turnover has increased to 10.3% (2016: 8.8%). Career development for our mid-career staff continued to be an important focus via our Energising Your Career programme. This year we made particular efforts to ensure staff on the programme connected with a career mentor to help them progress with their plans. During the year we have increasingly focused on improving our provision for the apprentices who join the business, with the UK Apprenticeship Levy offering us an increased opportunity to take on and develop staff through apprenticeship programmes. We measure employee engagement through our Group wide Viewpoint employee opinion survey. Our overall engagement score for Energy reduced by two points this year, particularly reflecting lower job security following the headcount reductions during the year. However, it remains better than the benchmark for our industry sector. SAFETY During the year, there were two reportable accidents compared with one last year. RISKS SPECIFIC TO ENERGY Oil price volatility is a major risk for our Energy business. Mitigating action has been taken by reducing headcount and our overall cost base. We continue to address productivity and rebalance the business to meet demand. The safety, environmental and reputational consequences of an error in our work, given the high hazard nature of the facilities on which we work, is another significant risk. Our plans for growth are potentially affected by the availability of skills in the right locations. To help to mitigate this risk, we continue to invest in our in-house nuclear training academy that now provides externally recognised courses.

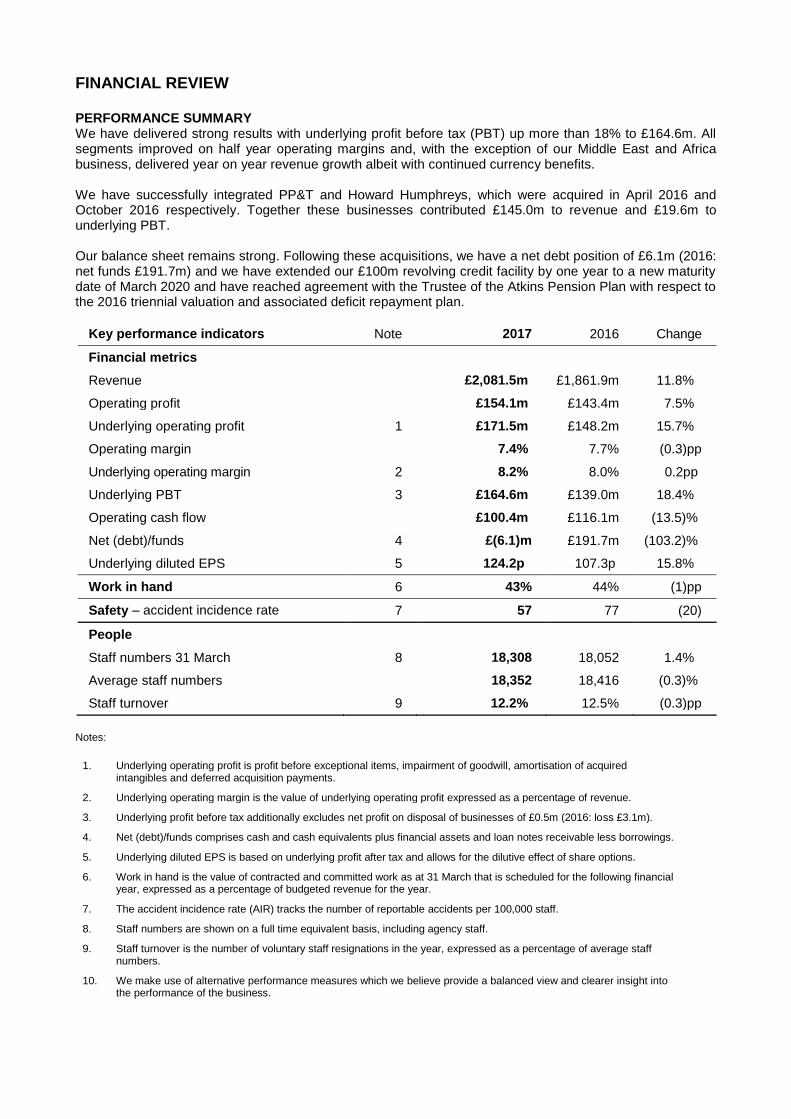

FINANCIAL REVIEW PERFORMANCE SUMMARY We have delivered strong results with underlying profit before tax (PBT) up more than 18% to £164.6m. All segments improved on half year operating margins and, with the exception of our Middle East and Africa business, delivered year on year revenue growth albeit with continued currency benefits. We have successfully integrated PP&T and Howard Humphreys, which were acquired in April 2016 and October 2016 respectively. Together these businesses contributed £145.0m to revenue and £19.6m to underlying PBT. Our balance sheet remains strong. Following these acquisitions, we have a net debt position of £6.1m (2016: net funds £191.7m) and we have extended our £100m revolving credit facility by one year to a new maturity date of March 2020 and have reached agreement with the Trustee of the Atkins Pension Plan with respect to the 2016 triennial valuation and associated deficit repayment plan.

Key performance indicators Note 2017 2016 Change

Financial metrics

Revenue £2,081.5m £1,861.9m 11.8%

Operating profit £154.1m £143.4m 7.5%

Underlying operating profit 1 £171.5m £148.2m 15.7%

Operating margin 7.4% 7.7% (0.3)pp

Underlying operating margin 2 8.2% 8.0% 0.2pp

Underlying PBT 3 £164.6m £139.0m 18.4%

Operating cash flow £100.4m £116.1m (13.5)%

Net (debt)/funds 4 £(6.1)m £191.7m (103.2)%

Underlying diluted EPS 5 124.2p 107.3p 15.8%

Work in hand 6 43% 44% (1)pp

Safety – accident incidence rate 7 57 77 (20)

People

Staff numbers 31 March 8 18,308 18,052 1.4%

Average staff numbers 18,352 18,416 (0.3)%

Staff turnover 9 12.2% 12.5% (0.3)pp

Notes:

1. Underlying operating profit is profit before exceptional items, impairment of goodwill, amortisation of acquired intangibles and deferred acquisition payments.

2. Underlying operating margin is the value of underlying operating profit expressed as a percentage of revenue.

3. Underlying profit before tax additionally excludes net profit on disposal of businesses of £0.5m (2016: loss £3.1m).

4. Net (debt)/funds comprises cash and cash equivalents plus financial assets and loan notes receivable less borrowings.

5. Underlying diluted EPS is based on underlying profit after tax and allows for the dilutive effect of share options.

6. Work in hand is the value of contracted and committed work as at 31 March that is scheduled for the following financial year, expressed as a percentage of budgeted revenue for the year.

7. The accident incidence rate (AIR) tracks the number of reportable accidents per 100,000 staff.

8. Staff numbers are shown on a full time equivalent basis, including agency staff.

9. Staff turnover is the number of voluntary staff resignations in the year, expressed as a percentage of average staff numbers.

10. We make use of alternative performance measures which we believe provide a balanced view and clearer insight into the performance of the business.

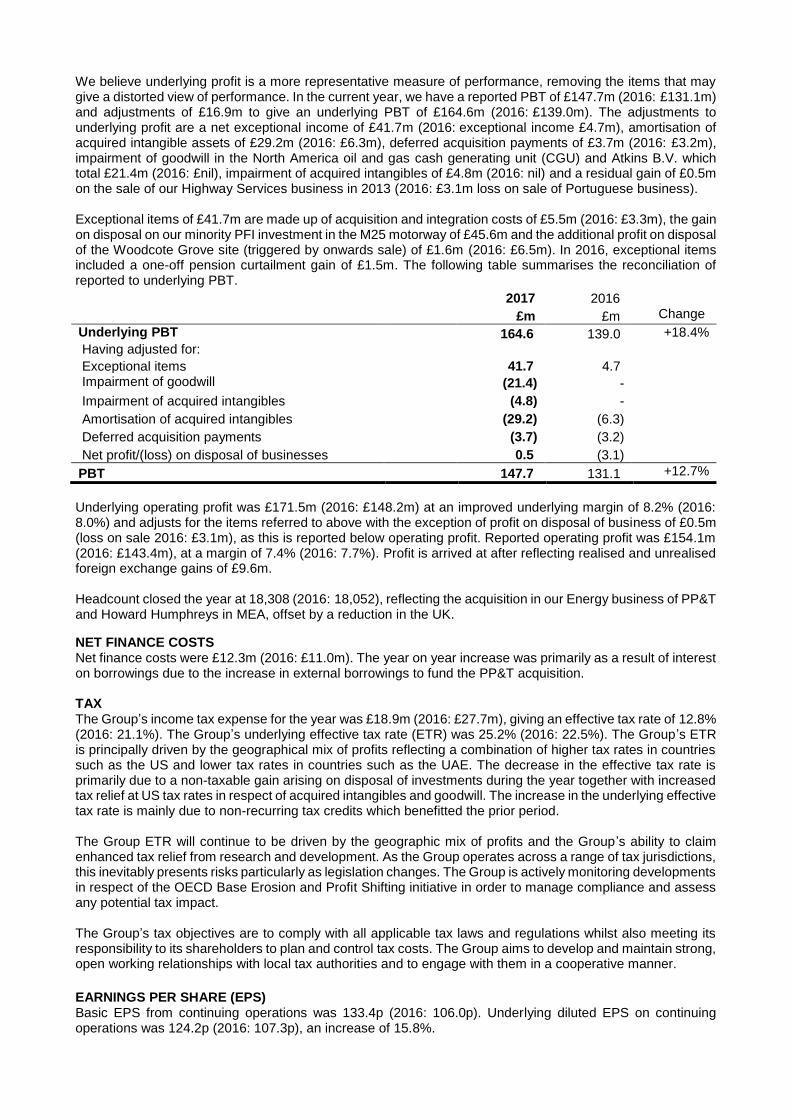

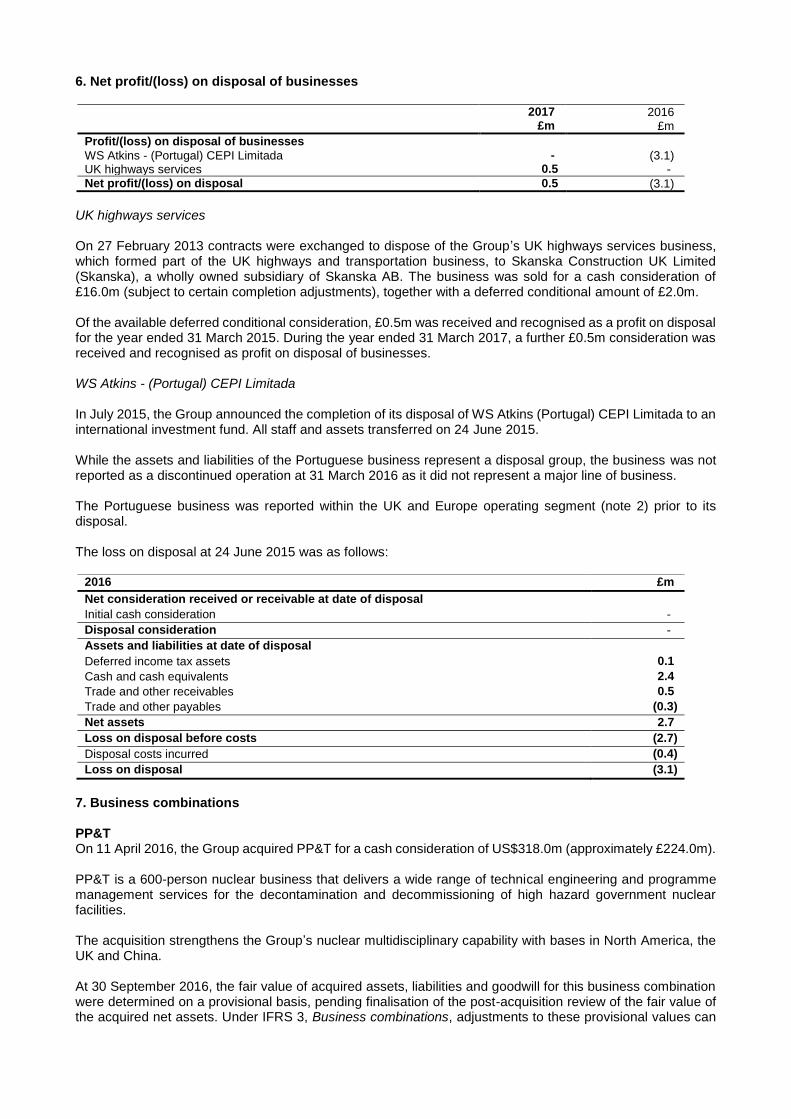

We believe underlying profit is a more representative measure of performance, removing the items that may give a distorted view of performance. In the current year, we have a reported PBT of £147.7m (2016: £131.1m) and adjustments of £16.9m to give an underlying PBT of £164.6m (2016: £139.0m). The adjustments to underlying profit are a net exceptional income of £41.7m (2016: exceptional income £4.7m), amortisation of acquired intangible assets of £29.2m (2016: £6.3m), deferred acquisition payments of £3.7m (2016: £3.2m), impairment of goodwill in the North America oil and gas cash generating unit (CGU) and Atkins B.V. which total £21.4m (2016: £nil), impairment of acquired intangibles of £4.8m (2016: nil) and a residual gain of £0.5m on the sale of our Highway Services business in 2013 (2016: £3.1m loss on sale of Portuguese business). Exceptional items of £41.7m are made up of acquisition and integration costs of £5.5m (2016: £3.3m), the gain on disposal on our minority PFI investment in the M25 motorway of £45.6m and the additional profit on disposal of the Woodcote Grove site (triggered by onwards sale) of £1.6m (2016: £6.5m). In 2016, exceptional items included a one-off pension curtailment gain of £1.5m. The following table summarises the reconciliation of reported to underlying PBT.

2017 2016

£m £m Change

Underlying PBT 164.6 139.0 +18.4%

Having adjusted for:

Exceptional items 41.7 4.7 Impairment of goodwill (21.4) -

Impairment of acquired intangibles (4.8) -

Amortisation of acquired intangibles (29.2) (6.3)

Deferred acquisition payments (3.7) (3.2)

Net profit/(loss) on disposal of businesses 0.5 (3.1)

PBT 147.7 131.1 +12.7%

Underlying operating profit was £171.5m (2016: £148.2m) at an improved underlying margin of 8.2% (2016: 8.0%) and adjusts for the items referred to above with the exception of profit on disposal of business of £0.5m (loss on sale 2016: £3.1m), as this is reported below operating profit. Reported operating profit was £154.1m (2016: £143.4m), at a margin of 7.4% (2016: 7.7%). Profit is arrived at after reflecting realised and unrealised foreign exchange gains of £9.6m. Headcount closed the year at 18,308 (2016: 18,052), reflecting the acquisition in our Energy business of PP&T and Howard Humphreys in MEA, offset by a reduction in the UK.

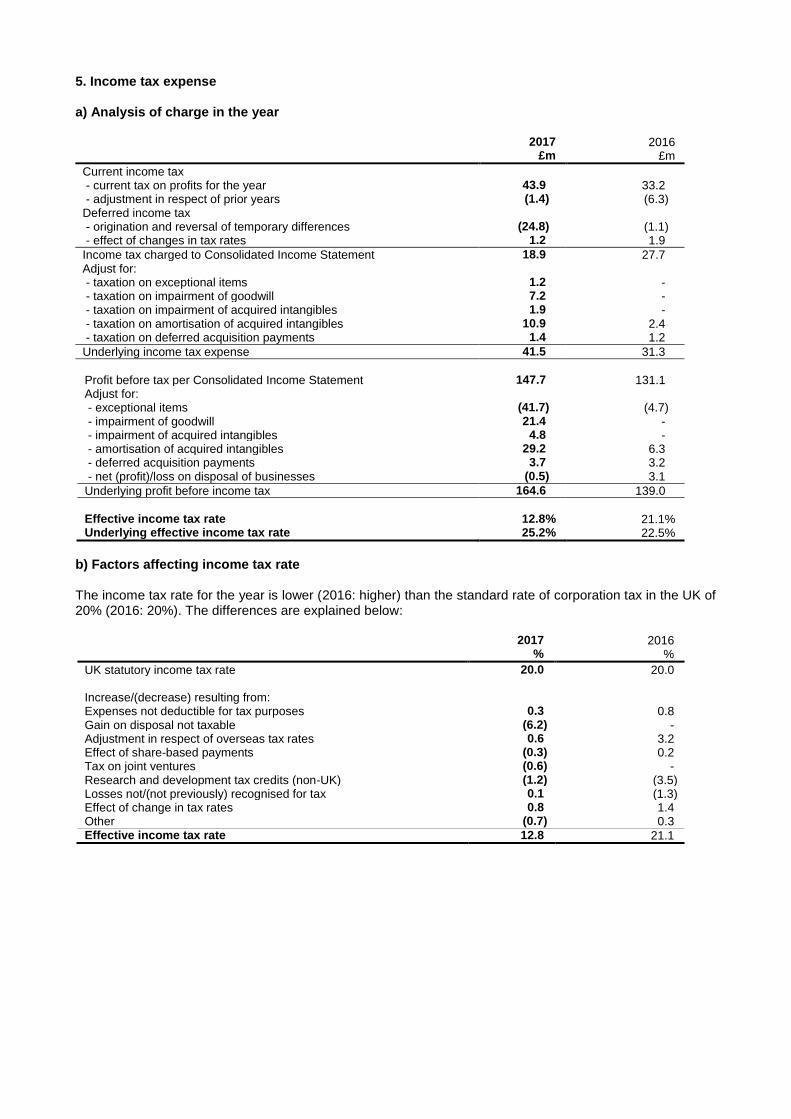

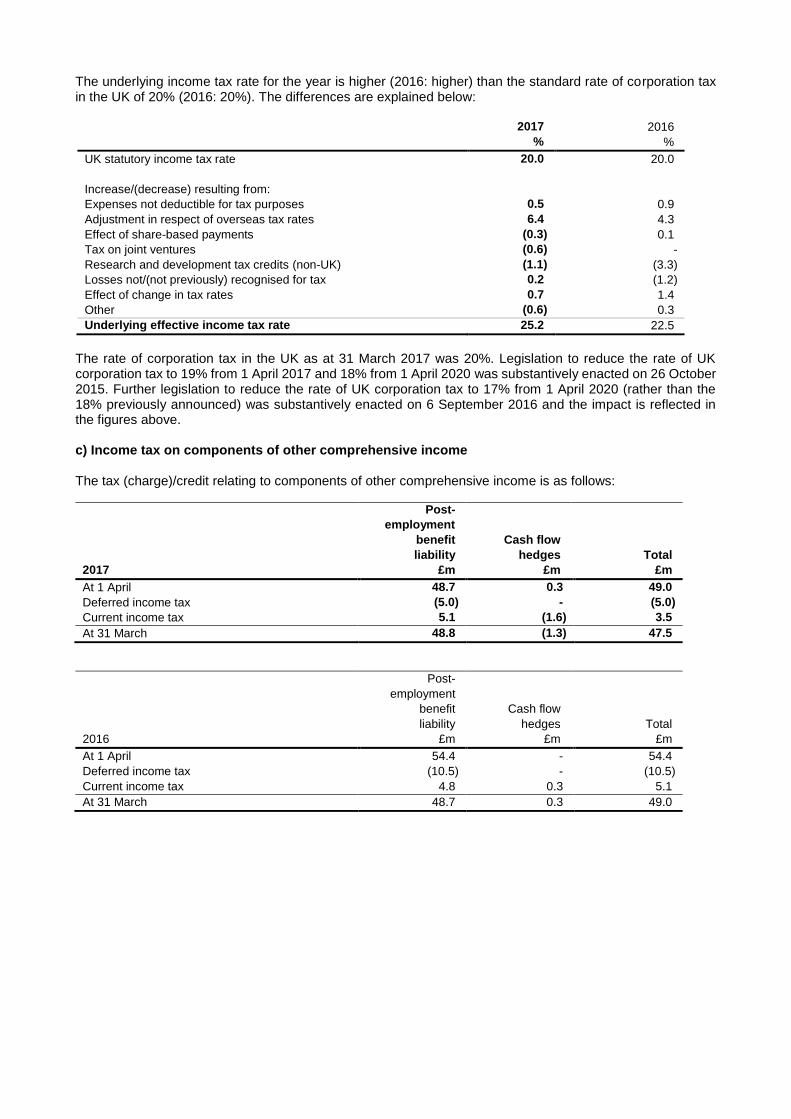

NET FINANCE COSTS Net finance costs were £12.3m (2016: £11.0m). The year on year increase was primarily as a result of interest on borrowings due to the increase in external borrowings to fund the PP&T acquisition. TAX The Group’s income tax expense for the year was £18.9m (2016: £27.7m), giving an effective tax rate of 12.8% (2016: 21.1%). The Group’s underlying effective tax rate (ETR) was 25.2% (2016: 22.5%). The Group’s ETR is principally driven by the geographical mix of profits reflecting a combination of higher tax rates in countries such as the US and lower tax rates in countries such as the UAE. The decrease in the effective tax rate is primarily due to a non-taxable gain arising on disposal of investments during the year together with increased tax relief at US tax rates in respect of acquired intangibles and goodwill. The increase in the underlying effective tax rate is mainly due to non-recurring tax credits which benefitted the prior period. The Group ETR will continue to be driven by the geographic mix of profits and the Group ’s ability to claim enhanced tax relief from research and development. As the Group operates across a range of tax jurisdictions, this inevitably presents risks particularly as legislation changes. The Group is actively monitoring developments in respect of the OECD Base Erosion and Profit Shifting initiative in order to manage compliance and assess any potential tax impact. The Group’s tax objectives are to comply with all applicable tax laws and regulations whilst also meeting its responsibility to its shareholders to plan and control tax costs. The Group aims to develop and maintain strong, open working relationships with local tax authorities and to engage with them in a cooperative manner.

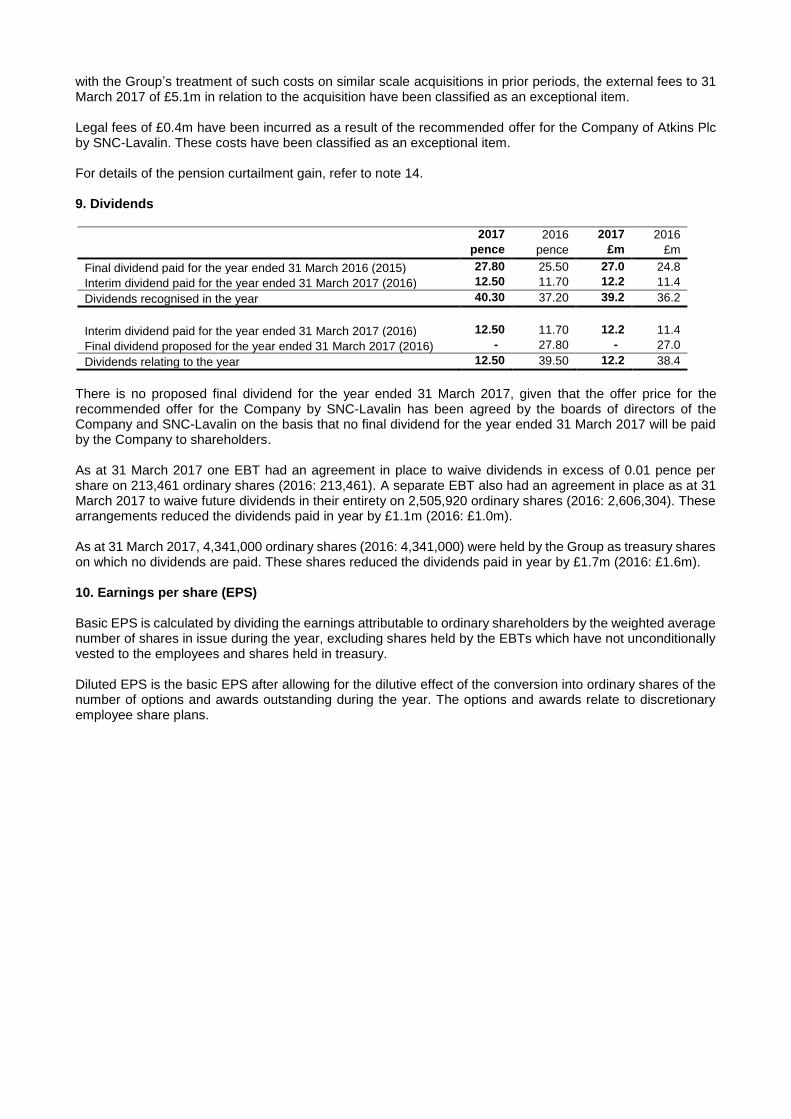

EARNINGS PER SHARE (EPS) Basic EPS from continuing operations was 133.4p (2016: 106.0p). Underlying diluted EPS on continuing operations was 124.2p (2016: 107.3p), an increase of 15.8%.

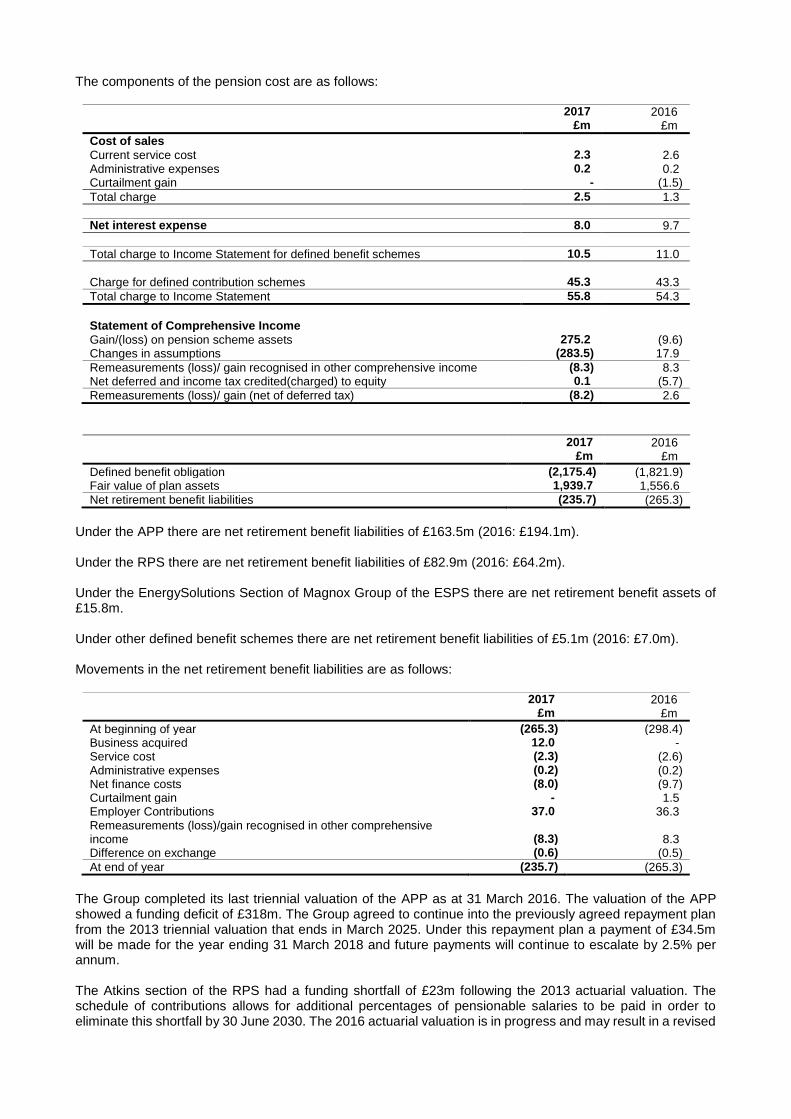

PENSIONS Funding and charges We reported in early April 2017 that we had reached agreement with the Trustee of the Atkins Pension Plan with respect to the 2016 triennial valuation, with the associated repayment plan unchanged from the previous valuation exercise in 2013. The agreed funding deficit at 31 March 2016 is £318m (31 March 2013: £430m). The agreed deficit repayment plan will see the Group pay £34.5m in the financial year to 31 March 2018, with payments in the following years escalating at 2.5% per annum. The total charge to the Consolidated Income Statement in respect of defined benefit schemes was £10.5m (2016: £11.0m), comprising current service cost of £2.3m (2016: £2.6m), administrative expenses of £0.2m (2016: £0.2m), a net interest expense of £8.0m (2016: £9.7m) and a curtailment gain in the prior year of £1.5m in the Railways Pension Scheme. The charge relating to defined contribution schemes increased to £45.3m (2016: £43.3m). IAS 19 (revised 2011) – valuation and accounting treatment The Group determines pension scheme funding with reference to actuarial valuations, but for reporting purposes uses IAS 19 (revised 2011) under which the Group recognised a reduced net retirement benefit liability of £235.7m at 31 March 2017 (2016: £265.3m). CASH Net debt as at 31 March 2017 was £6.1m (2016: net funds £191.7m), made up as follows:

2017 2016

£m £m

Cash and cash equivalents 224.5 419.3 Loan notes receivable 0.9 20.1 Financial assets at fair value through profit or loss 31.6 32.9 Borrowings due no later than one year - (7.0)

Borrowings due later than one year (263.0) (273.5)

Finance leases (0.1) (0.1)

Net (debt)/funds (6.1) 191.7

The Group’s financial position remains strong. Operating cash flow in the year was £100.4m (2016: £116.1m), representing 65.2% (2016: 81.0%) of operating profit on a reported basis or free cash flow of 69.4% (2016: 93.5%), which includes net capital expenditure and excludes the cash impact of non underlying items and pension deficit contributions and is summarised below. The move to a net debt position reflects the acquisitions in year, partially offset by the sale of our minority PFI investment in the M25 motorway. Reconciliation of profit before interest and tax to operating cash flow

2017 2016 £m £m

Profit before interest and tax 160.0 142.1 Add: depreciation 19.7 18.2 Add: amortisation and impairment 58.9 11.9

EBITDA 238.6 172.2

Comprising: - Underlying EBITDA 200.1 173.8 - Exceptional items 41.7 4.7 - Deferred acquisition payments (3.7) (3.2) - Net profit/(loss) on disposal of businesses 0.5 (3.1)

238.6 172.2

Pensions deficit funding (33.6) (32.8) Movement in working capital (54.1) (26.5) Movement in non-current payables - 0.1 Movement in provisions 0.3 0.5 Income from other investments (0.6) (1.1) Profit on sale of investments (45.6) - Other non-cash items (4.6) 3.7

Operating cash flow 100.4 116.1

The movement in non-cash items of £4.6m (2016: £3.7m) consists primarily of foreign exchange costs and share based payments. The increase in working capital is due to the timing of major projects in both our Energy and UK and Europe businesses. Net tax paid amounted to £21.5m (2016: £36.8m) with the decrease due primarily to a one-off payment for consortium loss relief and overpayments in prior periods now largely utilised. Net capital expenditure in the year, including the purchase of computer software licences, amounted to £20.7m (2016: £17.3m). CAPITAL STRUCTURE As at 31 March 2017, the Group had shareholders ’ funds of £418.5m (2016: £289.3m). The Company had shareholders’ funds of £310.4m (2016: £224.4m) and 104.5m fully paid ordinary shares in issue at 31 March 2017 (2016: 104.5m).

TREASURY POLICY AND OBJECTIVES The Group’s treasury function manages and monitors external funding and investment requirements and financial risks in support of the Group’s corporate objectives. The Board reviews and agrees procedures, requirements and authority levels for treasury activities. The Board delegates responsibility for the detailed review of the policies to the Audit Committee. The Group’s financial instruments, other than derivatives, comprise borrowings, cash and liquid resources and various items, such as trade receivables and trade payables, which arise directly from its operations. The main purpose of these financial instruments is to finance the Group’s activities. The Group also enters into derivative transactions, principally forward foreign currency contracts to manage foreign exchange risk on material commercial transactions undertaken in currencies other than the local functional currency. The main risks arising from the Group’s financial instruments are market risk (including foreign exchange risk, interest rate risk and price risk), credit risk and liquidity risk. The Group funds its ongoing activities through cash generated from its operations and, where necessary, borrowings and finance leases. Utilisation of the Group’s facilities is a consequence of prior and current year acquisitions and ongoing organic growth. As at 31 March 2017, the Group had £96.7m of undrawn committed borrowing facilities available (2016: £71.9m). There have been no significant changes to the Group’s treasury procedures, requirements and authority levels during the year. CRITICAL ACCOUNTING POLICIES The Group’s principal accounting policies are described in note 1 to the Financial Statements in the Annual Report and Accounts. The Financial Statements are prepared under International Financial Reporting Standards (IFRSs) as adopted by the European Union. The preparation of financial statements in conformity with generally accepted accounting principles requires the use of estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Although these estimates are based on management’s best knowledge of the amount, event or actions, actual results may ultimately differ from those estimates. Material estimates applied across the Group’s businesses and joint ventures are reviewed to a common standard and adjusted where appropriate to ensure that consistent treatment of similar and related issues that require judgement is achieved upon consolidation. Any revisions to estimates are recognised prospectively. The accounting policies and areas that require the most significant estimates and judgements to be used in the preparation of the Financial Statements are in relation to contract accounting, including recoverability of receivables, goodwill impairment, defined benefit pension schemes, tax, research and development, acquisition accounting and joint arrangements. Contract accounting The Group’s contract accounting policy is central to how the Group values the work it has carried out in each financial year. This policy requires forecasts to be made on the projected outcomes of projects. These forecasts require assessments and judgements to be made on changes in, for example, work scope, changes in costs and costs to completion. While the assumptions made are based on professional judgements, subsequent events may mean that estimates calculated prove to be inaccurate, with a consequent effect on the reported results.

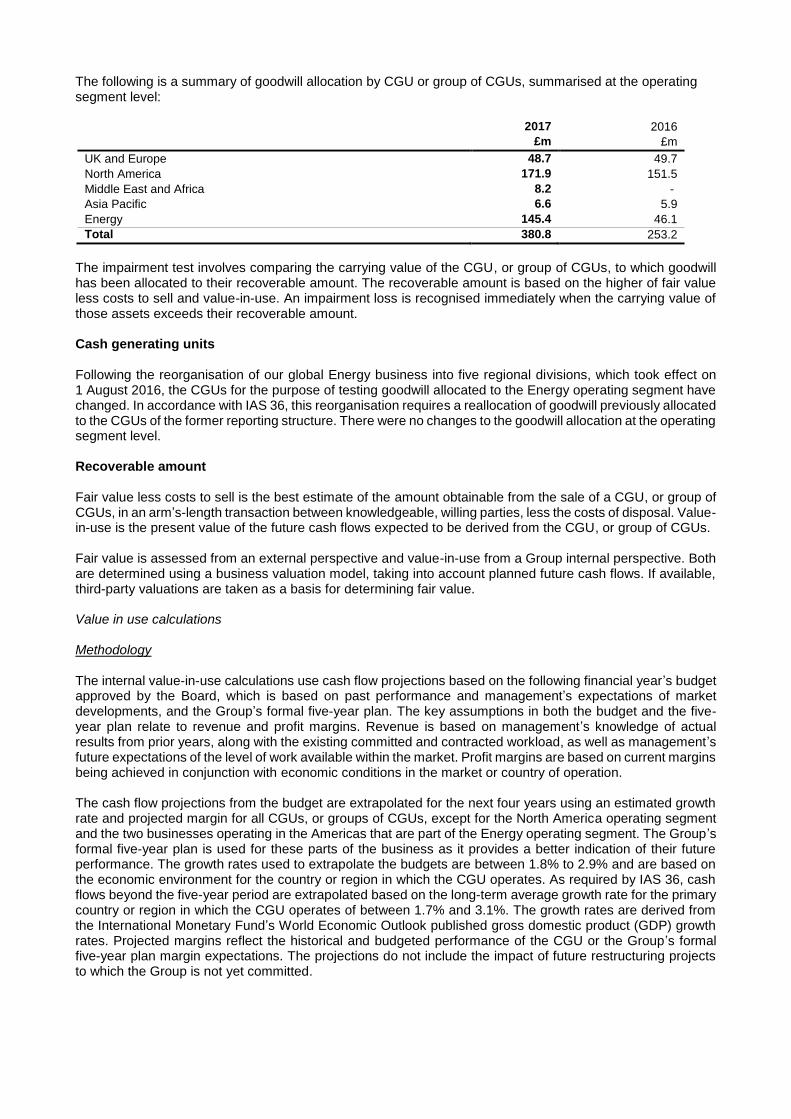

Goodwill impairment Goodwill is subject to impairment review both annually and when there are indications that the carrying value may not be recoverable. The carrying value of goodwill is compared to the recoverable amount, which is the higher of the value in use and fair value less costs to sell. For the purpose of impairment testing, goodwill acquired in a business combination is allocated to each of the cash-generating units (CGUs), or groups of CGUs, that is expected to benefit from the synergies of the combination. Each CGU or group of CGUs to which the goodwill is allocated represents the lowest level within the entity at which goodwill is monitored for internal management purposes. Determining whether goodwill is impaired requires an estimation of the value in use of CGUs to which the goodwill has been allocated. The value in use calculation requires an estimate to be made of the timing and amount of future cash flows expected to arise from the CGU and the application of a suitable discount rate to calculate the present value. The discount rates used are based on the Group’s weighted average cost of capital adjusted to reflect the specific economic environment of the relevant CGU. Defined benefit pension schemes Accounting for pensions involves judgement about uncertain events in the future such as inflation, salary levels at retirement, longevity rates, rates of return on plan assets and discount rates. Assumptions in respect of pensions and post-employment benefits are set after consultation with independent qualified actuaries. Management believes the assumptions are appropriate. However, a change in the assumptions used would have an impact on the Group’s results and net assets. Any differences between the assumptions and the actual outcome will affect results in future years. An estimate of the sensitivity to changes in key assumptions is disclosed in note 14. Tax The Group is subject to tax in a number of jurisdictions and judgement is required in determining the Group wide provision for income taxes. The Group provides for potential liabilities in respect of uncertain tax positions where additional tax may become payable in future periods and such provisions are based on management’s assessment of exposures. Deferred tax is accounted for on temporary differences using the liability method, with deferred tax liabilities being provided for in full and deferred tax assets being recognised only to the extent that it is probable that future taxable profits will be available against which the temporary differences can be utilised. Research and development (R&D) All R&D expenditure is written off to the Consolidated Income Statement as incurred. In the UK, the Group adopted the R&D expenditure credit regime with effect from 1 April 2013. These credits have characteristics more akin to government grants than income taxes and therefore are offset against the relevant expenditure in the income statement rather than via the tax charge. The credits are recognised to the extent that there is reasonable assurance that they will be received, albeit that the claim process takes place sometime after the original expenditure was incurred. Joint arrangements The Group applies IFRS 11 to all joint arrangements. Under IFRS 11 a joint arrangement is an arrangement over which two or more parties have joint control. Joint control is the contractually agreed sharing of control of an arrangement, which exists only when decisions about the relevant activities require the unanimous consent of the parties sharing control. The Group classifies its interests in joint arrangements as either joint ventures or joint operations. The Group holds 50% of the voting rights in some of its joint arrangements. However, the Group has joint control over these arrangements as under the respective contractual agreements unanimous consent is required from all parties to the agreements for all relevant activities. These joint arrangements are not structured through separate legal entities and the terms of the arrangements provide the Group and the other parties to the arrangements with the rights to the assets and obligations for the liabilities, or other facts and circumstances indicate this is the case. Therefore, these arrangements are classified as joint operations of the Group.

Acquisition accounting The Group applies the acquisition method to account for business combinations. The cost of an acquisition is measured as the fair value of the assets, equity instruments issued and liabilities incurred or assumed at the date of exchange. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values at the acquisition date irrespective of any non-controlling interest. Acquisition-related costs are expensed as incurred. Any contingent consideration is recognised at fair value at the acquisition date. The excess of the consideration transferred over the fair value of the identifiable net assets acquired is recorded as goodwill. Goodwill is reviewed on finalisation of fair values and any adjustments required to the accounting are recorded within 12 months of the acquisition date. GOING CONCERN The directors are required to consider the appropriateness of the going concern assertion in the preparation of the Group’s financial information for the year ended 31 March 2017. The Group meets its day-to-day working capital requirements through cash generated from operations and the use of its banking facilities. The Group has delivered good results and progressed its strategic objectives, not least through the acquisition of PP&T and Howard Humphreys. Following these acquisitions it has net borrowings at 31 March 2017 of £6.1m. The Group had cash and cash equivalents of £224.5m and access to undrawn committed borrowing facilities of £96.7m at 31 March 2017. On 30 January 2016 the Group amended and extended its five year revolving credit facility (RCF). This £200m facility matures on 30 January 2021. On 11 March 2016 the Group signed a new RCF of £100m, with a maturity of three years. On 23 February 2017, the Group exercised an option to extend the facility by an additional year. This £100m facility now matures on 11 March 2020. The total letters of credit in issue under the committed facilities at 31 March 2017 was £0.2m (31 March 2016: £0.2m). The Group has a good level of work in hand at 31 March 2017 representing 43% of forecast revenue for the year (2016: 44%). After making enquiries and having considered the Group’s results, the strength of its balance sheet and near-term outlook, the directors have a reasonable expectation that the Group has adequate resources to continue in operational existence for the foreseeable future. It is therefore deemed appropriate to continue to apply the going concern principle in the preparation of its consolidated financial information for the year ended 31 March 2017.

STATEMENT OF DIRECTORS’ RESPONSIBILITIES The directors are responsible for preparing the Annual Report, the Remuneration report and the Financial Statements in accordance with applicable law and regulations. Detailed below are statements made by the directors in relation to their responsibilities, disclosure of information to the Company’s independent auditor and going concern.

Company law requires the directors to prepare financial statements for each financial year. Under that law, the directors have prepared the Group and Company Financial Statements in accordance with International Financial Reporting Standards as adopted by the European Union. Under company law the directors must not approve the Financial Statements unless they are satisfied that they give a true and fair view of the state of affairs of the Company and the Group and of the profit or loss of the Company and Group for that period. In preparing these Financial Statements, the directors are required to:

- select suitable accounting policies and then apply them consistently - make judgements and accounting estimates that are reasonable and prudent - state whether applicable IFRSs as adopted by the EU have been followed, subject to any material

departures disclosed and explained in the Financial Statements - prepare the Financial Statements on the going concern basis unless it is inappropriate to presume that

the Company and the Group will continue in business

The directors are responsible for:

- keeping adequate accounting records that are sufficient to show and explain the Company’s transactions and disclose with reasonable accuracy at any time the financial position of the Company and the Group and enable them to ensure that the Financial Statements and the Remuneration report comply with the Act and, as regards the Group Financial Statements, Article 4 of the International Accounting Standard Regulation

- safeguarding the assets of the Company and the Group and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities

- the maintenance and integrity of the corporate and financial information included on the Company’s website. Legislation in the UK governing the preparation and dissemination of financial statements may differ from legislation in other jurisdictions

The directors consider that the Annual Report, taken as a whole, is fair, balanced and understandable and provides the information necessary for shareholders to assess the Group’s position and performance, business model and strategy.

Each of the directors, confirms that, to the best of their knowledge:

- the Group Financial Statements, which have been prepared in accordance with IFRSs as adopted by the EU, give a true and fair view of the assets, liabilities, financial position and profit of the Group

- the Directors’ report contained in the Annual Report includes a fair review of the development and performance of the business and the position of the Group, together with a description of the principal risks and uncertainties that it faces.

Going concern The directors have a reasonable expectation that the Company and the Group have adequate resources to continue in operational existence for the foreseeable future and therefore continue to adopt the going concern basis in preparing the Financial Statements.

Disclosure of audit information Each of the directors, whose names and functions are listed in the Annual Report, confirms that, to the best of his/her knowledge no relevant audit information of which the Company’s independent auditor is unaware and that he or she has taken all reasonable steps that he or she ought to have taken as a director in order to make himself or herself aware of any relevant audit information and to ensure that the Company’s independent auditor is aware of that information.

Approved by the Board and signed on its behalf by

Richard Webster Company secretary 14 June 2017

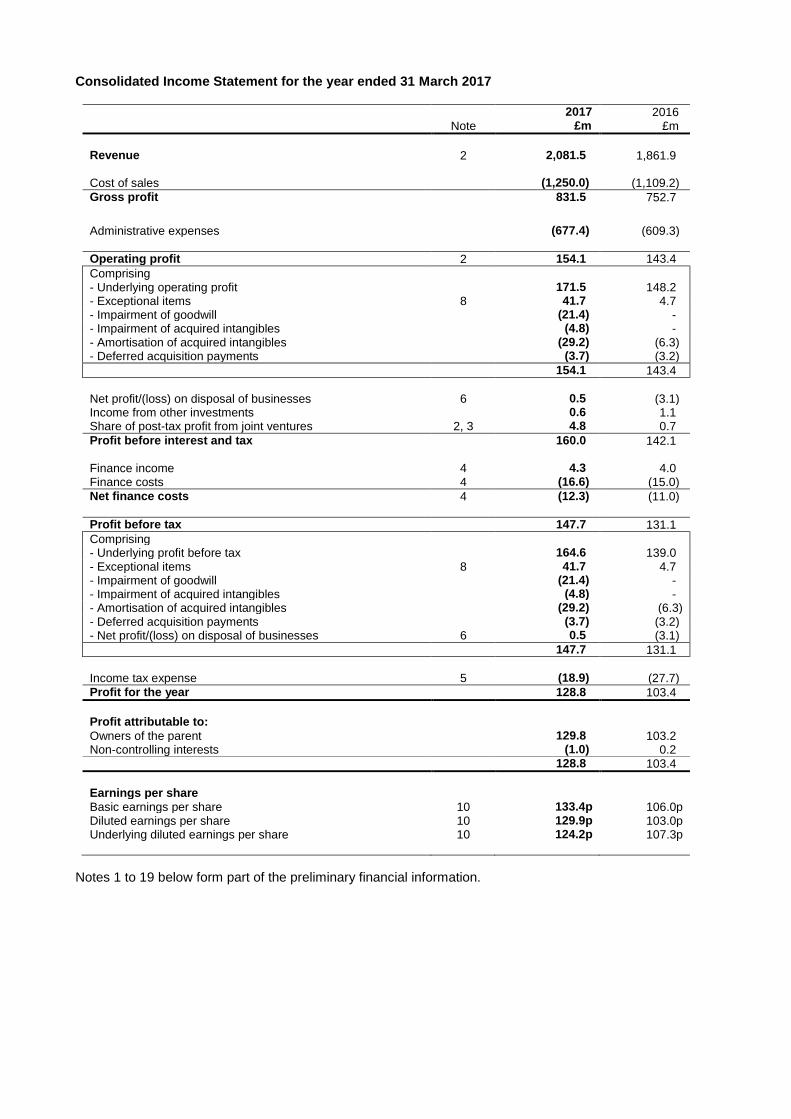

Consolidated Income Statement for the year ended 31 March 2017

2017 2016 Note £m £m

Revenue 2 2,081.5 1,861.9 Cost of sales (1,250.0) (1,109.2)

Gross profit 831.5 752.7

Administrative expenses (677.4) (609.3)

Operating profit 2 154.1 143.4

Comprising - Underlying operating profit 171.5 148.2 - Exceptional items 8 41.7 4.7 - Impairment of goodwill (21.4) - - Impairment of acquired intangibles (4.8) - - Amortisation of acquired intangibles (29.2) (6.3) - Deferred acquisition payments (3.7) (3.2)

154.1 143.4

Net profit/(loss) on disposal of businesses 6 0.5 (3.1) Income from other investments 0.6 1.1 Share of post-tax profit from joint ventures 2, 3 4.8 0.7

Profit before interest and tax 160.0 142.1 Finance income 4 4.3 4.0 Finance costs 4 (16.6) (15.0)

Net finance costs 4 (12.3) (11.0)

Profit before tax 147.7 131.1

Comprising - Underlying profit before tax 164.6 139.0 - Exceptional items 8 41.7 4.7 - Impairment of goodwill (21.4) - - Impairment of acquired intangibles (4.8) - - Amortisation of acquired intangibles (29.2) (6.3) - Deferred acquisition payments (3.7) (3.2) - Net profit/(loss) on disposal of businesses 6 0.5 (3.1)

147.7 131.1

Income tax expense 5 (18.9) (27.7)

Profit for the year 128.8 103.4

Profit attributable to: Owners of the parent 129.8 103.2 Non-controlling interests (1.0) 0.2 128.8 103.4

Earnings per share Basic earnings per share 10 133.4p 106.0p Diluted earnings per share 10 129.9p 103.0p Underlying diluted earnings per share 10 124.2p 107.3p

Notes 1 to 19 below form part of the preliminary financial information.

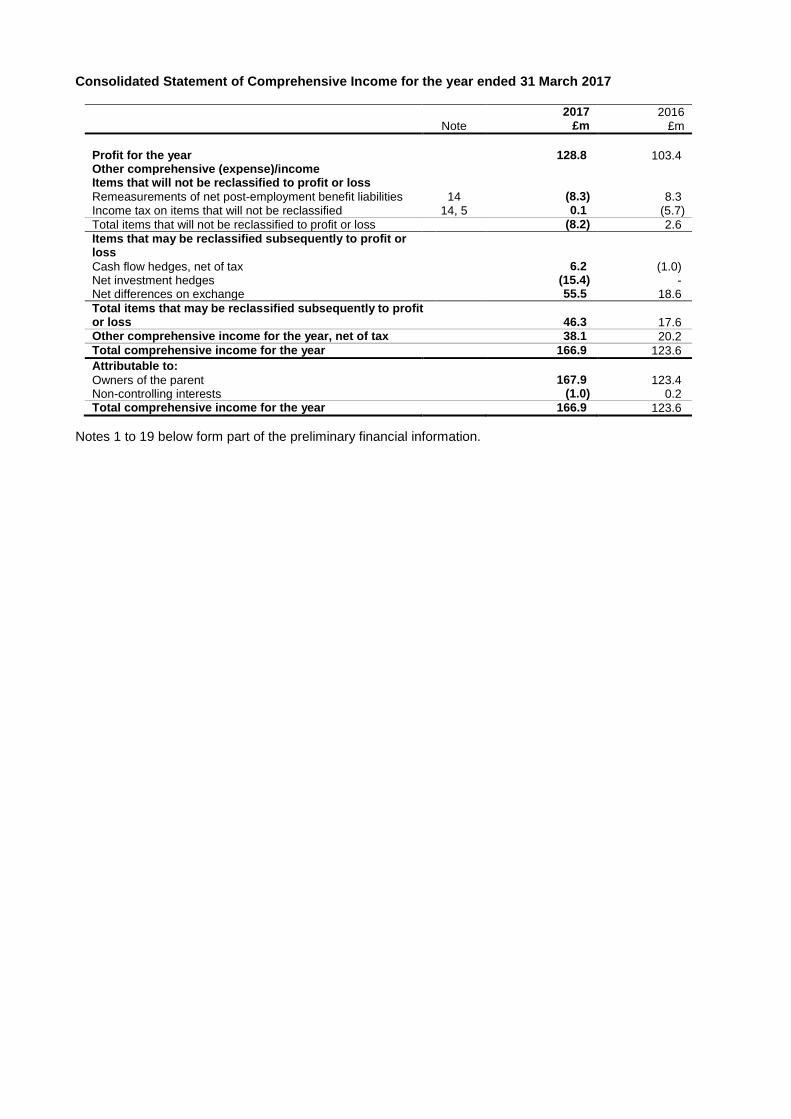

Consolidated Statement of Comprehensive Income for the year ended 31 March 2017

2017 2016 Note £m £m

Profit for the year 128.8 103.4 Other comprehensive (expense)/income Items that will not be reclassified to profit or loss Remeasurements of net post-employment benefit liabilities 14 (8.3) 8.3 Income tax on items that will not be reclassified 14, 5 0.1 (5.7)

Total items that will not be reclassified to profit or loss (8.2) 2.6

Items that may be reclassified subsequently to profit or loss Cash flow hedges, net of tax 6.2 (1.0) Net investment hedges (15.4) - Net differences on exchange 55.5 18.6

Total items that may be reclassified subsequently to profit or loss 46.3 17.6 Other comprehensive income for the year, net of tax 38.1 20.2 Total comprehensive income for the year 166.9 123.6

Attributable to: Owners of the parent 167.9 123.4 Non-controlling interests (1.0) 0.2 Total comprehensive income for the year 166.9 123.6

Notes 1 to 19 below form part of the preliminary financial information.

Consolidated Balance Sheet as at 31 March 2017

2017 2016 Note £m £m

Assets Non-current assets Goodwill 11 380.8 253.2 Other intangible assets 12 186.8 46.8 Property, plant and equipment 55.4 51.9 Investments in joint ventures 3 12.9 4.3 Deferred income tax assets 58.4 66.5 Derivative financial instruments 8.0 2.0 Other receivables 3.1 29.1 Post-employment benefit assets 14 15.8 -

721.2 453.8