Embed Size (px)

Citation preview

RESULTS FOR Q3 2016 ANALYSTTELECONFERENCE

02 Operation

03Financials

01Market

2

3

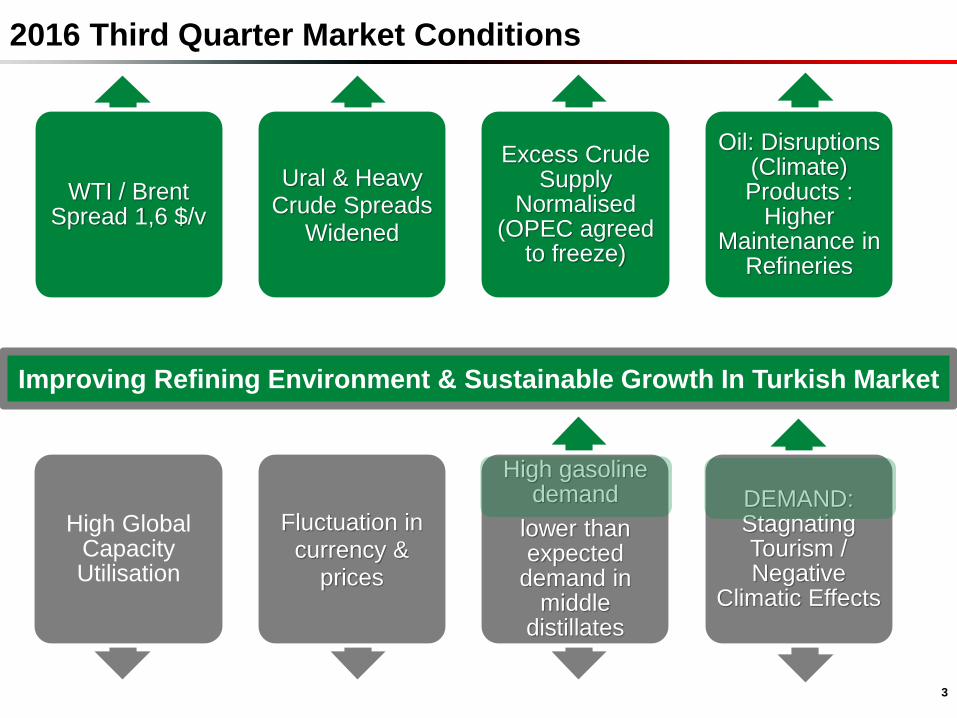

2016 Third Quarter Market Conditions

WTI / Brent Spread 1,6 $/v

Ural & HeavyCrude Spreads

Widened

Excess Crude Supply

Normalised(OPEC agreed

to freeze)

Oil: Disruptions (Climate) Products :

HigherMaintenance in

Refineries

High Global Capacity Utilisation

Fluctuation in currency &

prices

High gasolinedemand

lower than expected

demand in middle

distillates

DEMAND: StagnatingTourism / Negative

Climatic Effects

Improving Refining Environment & Sustainable Growth In Turkish Market

17,114,0 14,4

22,7

19,7

14,3

9,1511,4 12,3

4

8

12

16

20

24

Jul Aug Sep

Gasoline Cracks

2014 2015 2016

2016 vs 2015

Key Data Effecting Refining in Q3

4

106,6101,6

97,3

56,546,6 47,6

45,1 41,046,7

30

48

66

84

102

120

Jul Aug Sep

Crude Oil Prices

2014 2015 2016

-1,06

-0,26

-1,56

-0,61

-0,94-0,66

-1,3

-1,7

-2,2-2,5

-2,0

-1,5

-1,0

-0,5

0,0

Jul Aug Sep

Ural-Brent Difference

2014 2015 2016

2016 vs 2015

-1,54

$/bbl

14,7

17,017,0

12,315,7

15,03

8,9 8,69,4

6

10

14

18

Jul Aug Sep

Diesel Cracks

2014 2015 2016

58% 62%

2016 vs 2015

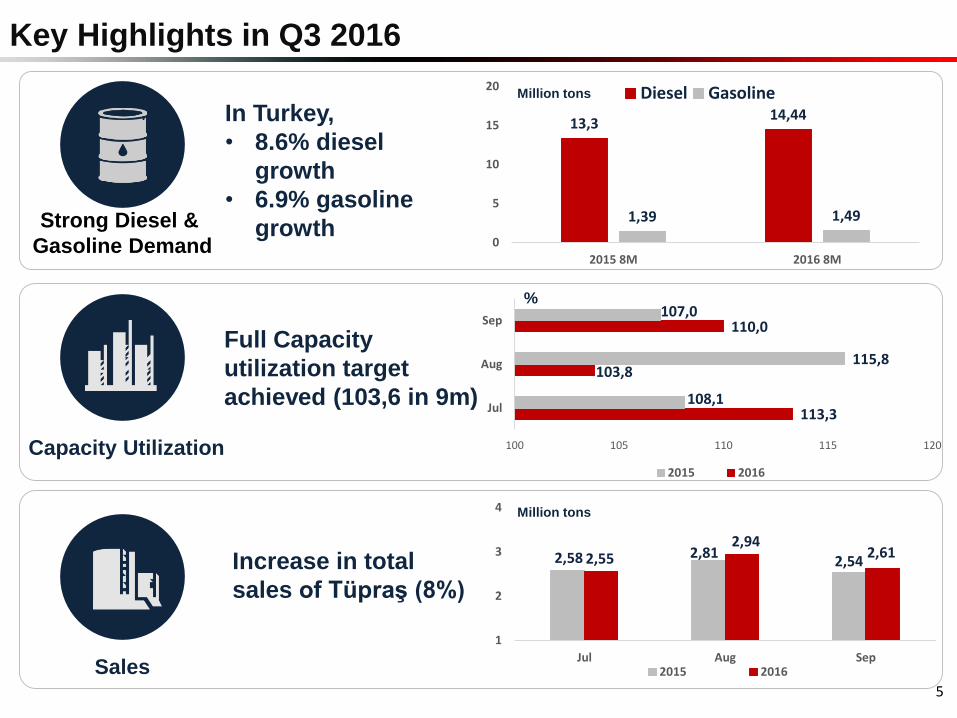

Key Highlights in Q3 2016

5

2,58 2,812,542,55

2,942,61

1

2

3

4

Jul Aug Sep2015 2016

Increase in total

sales of Tüpraş (8%)

In Turkey,

• 8.6% diesel

growth

• 6.9% gasoline

growth

Million tons

Million tons

Sales

Strong Diesel &

Gasoline Demand

%

13,314,44

1,39 1,49

0

5

10

15

20

2015 8M 2016 8M

Diesel Gasoline

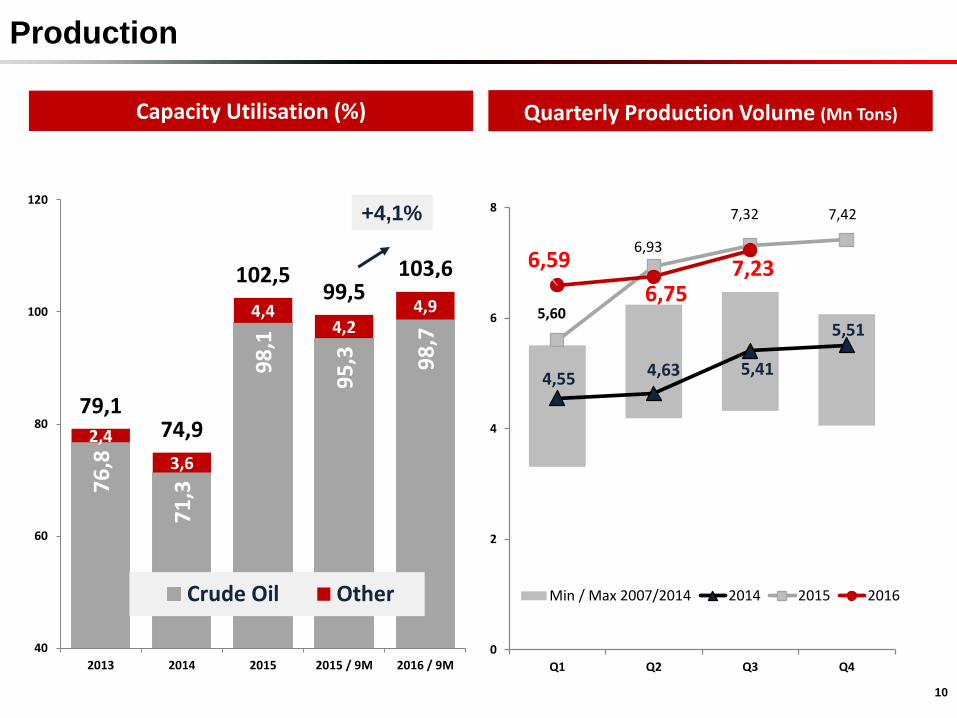

Full Capacity

utilization target

achieved (103,6 in 9m)

Capacity Utilization

113,3

103,8

110,0

108,1

115,8

107,0

100 105 110 115 120

Jul

Aug

Sep

2015 2016

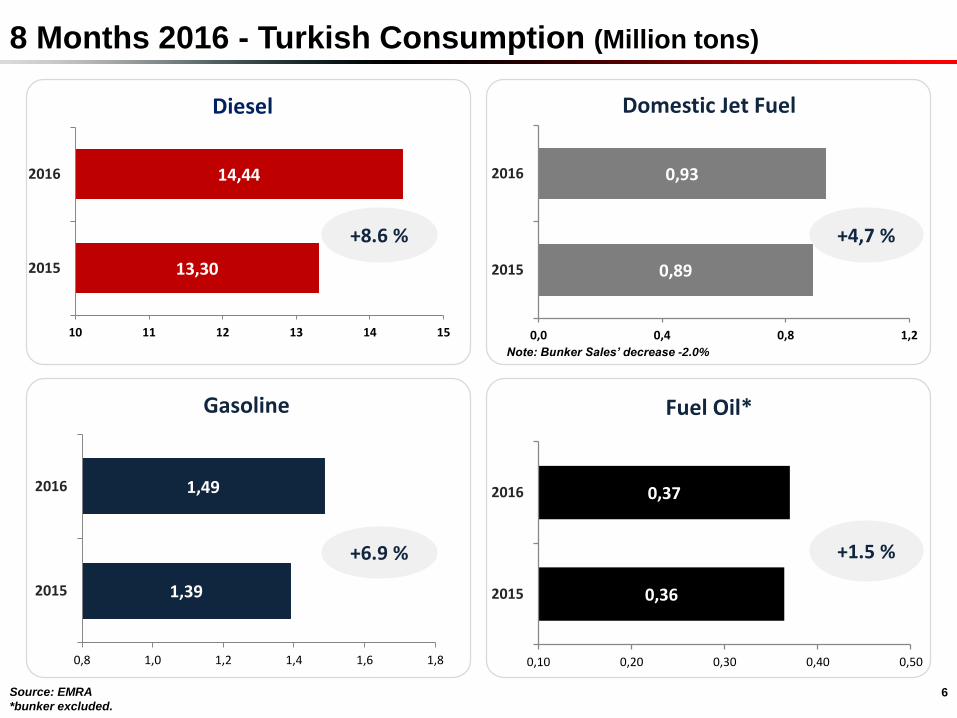

8 Months 2016 - Turkish Consumption (Million tons)

13,30

14,44

10 11 12 13 14 15

2015

2016

Diesel

0,89

0,93

0,0 0,4 0,8 1,2

2015

2016

Domestic Jet Fuel

1,39

1,49

0,8 1,0 1,2 1,4 1,6 1,8

2015

2016

Gasoline

0,36

0,37

0,10 0,20 0,30 0,40 0,50

2015

2016

Fuel Oil*

Source: EMRA

*bunker excluded.

+8.6 %

+1.5 %+6.9 %

+4,7 %

Note: Bunker Sales’ decrease -2.0%

6

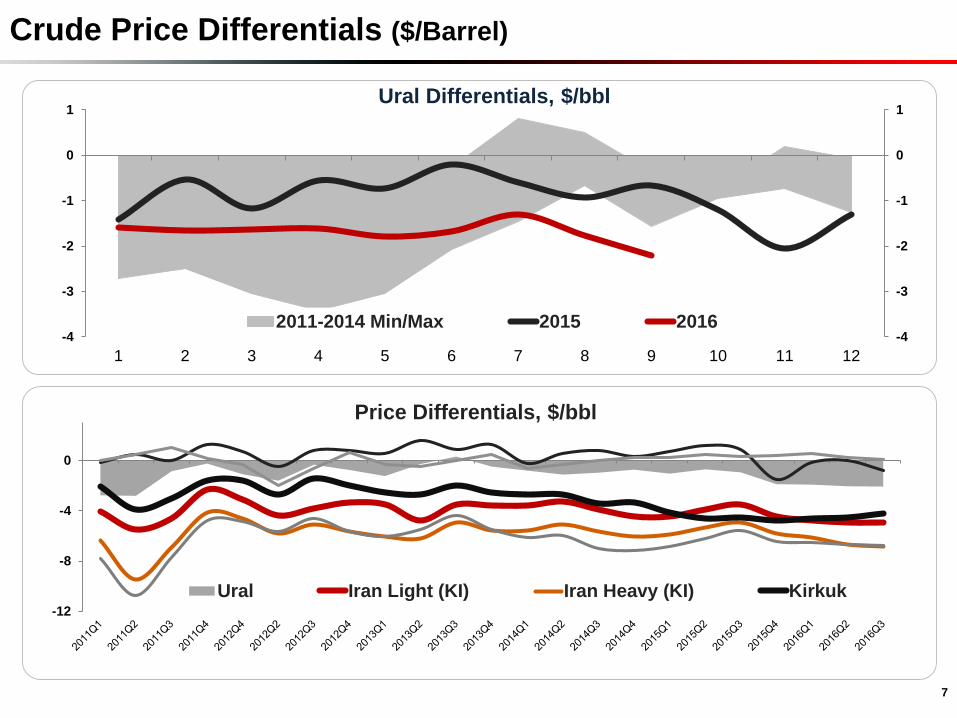

Crude Price Differentials ($/Barrel)

7

-12

-8

-4

0

Price Differentials, $/bbl

Ural Iran Light (KI) Iran Heavy (KI) Kirkuk

-4

-3

-2

-1

0

1

-4

-3

-2

-1

0

1

1 2 3 4 5 6 7 8 9 10 11 12

2011-2014 Min/Max 2015 2016

Ural Differentials, $/bbl

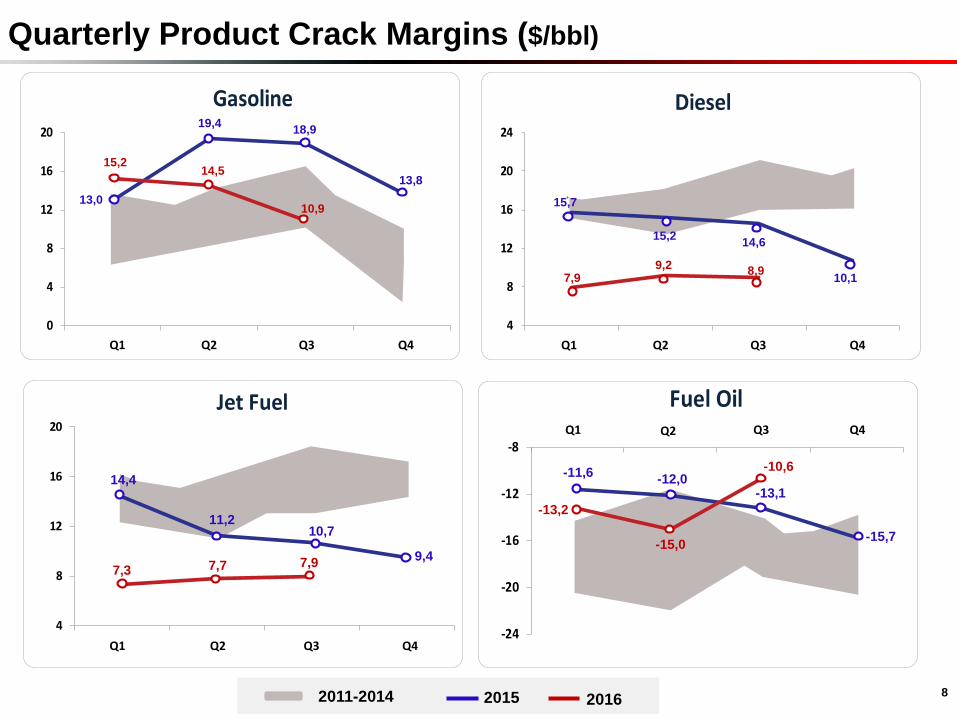

Quarterly Product Crack Margins ($/bbl)

82015 20162011-2014

15,214,5

10,913,0

19,418,9

13,8

Q1 Q4Q3Q2

-13,2

-15,0

-10,6

-15,7

-13,1-12,0

-11,6

Q1 Q4Q3Q2

7,3 7,7 7,99,4

11,210,7

14,4

Q1 Q4Q3Q2

15,7

15,214,6

10,18,9

9,27,9

Q1 Q4Q3Q2

Market Operations Financials

Capacity Utilisation (%)7

6,8

71

,3

98

,1

95

,3 98

,72,4

3,6

4,44,2

4,9

79,174,9

102,599,5

40

60

80

100

120

2013 2014 2015 2015 / 9M 2016 / 9M

Crude Oil Other

103,6

Quarterly Production Volume (Mn Tons)

4,55 4,63 5,41

5,515,60

6,93

7,32 7,42

6,59

6,757,23

0

2

4

6

8

Q1 Q2 Q3 Q4

Min / Max 2007/2014 2014 2015 2016

Production

10

+4,1%

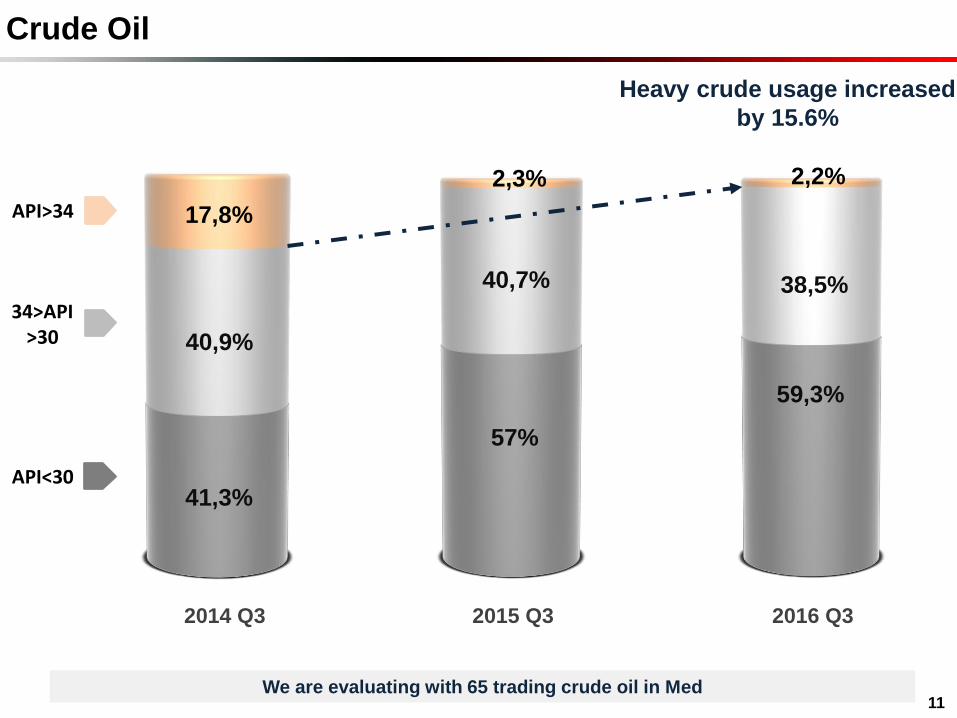

59,3%

38,5%

57%

40,7%

Crude Oil

11

2015 Q3 2016 Q3

We are evaluating with 65 trading crude oil in Med

41,3%

40,9%

2014 Q3

API<30

34>API>30

API>34 17,8%

2,3% 2,2%

Heavy crude usage increased

by 15.6%

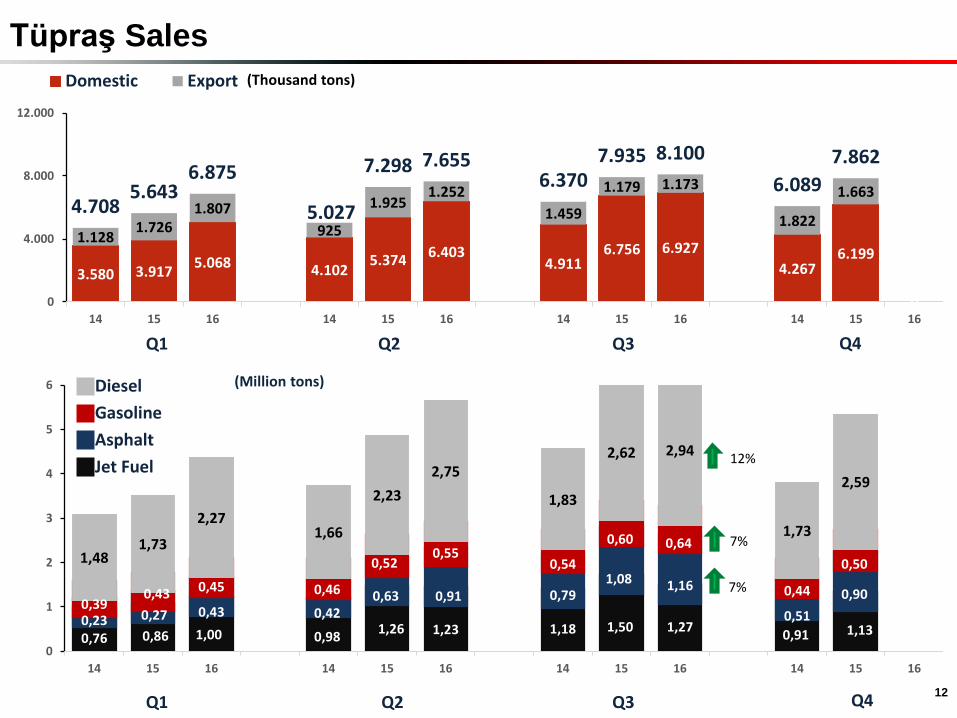

Tüpraş Sales

12

3.580 3.9175.068 4.102

5.3746.403

4.9116.756 6.927

4.2676.199

0

1.1281.726

1.807

925

1.9251.252

1.459

1.179 1.173

1.822

1.6634.708

5.6436.875

5.027

7.298 7.6556.370

7.935 8.100

6.089

7.862

0

4.000

8.000

12.000

14 15 16 14 15 16 14 15 16 14 15 16

Domestic Export (Thousand tons)

Q1 Q2 Q3 Q4

0,76 0,86 1,00 0,981,26 1,23 1,18 1,50 1,27

0,91 1,130,23 0,27 0,43 0,42

0,63 0,91 0,791,08 1,16

0,51

0,900,39

0,43 0,45 0,46

0,520,55

0,54

0,60 0,64

0,44

0,501,481,73

2,271,66

2,23

2,75

1,83

2,62 2,94

1,73

2,59

0

1

2

3

4

5

6

14 15 16 14 15 16 14 15 16 14 15 16

Diesel

Gasoline

Asphalt

Jet Fuel12%

7%

7%

Q1 Q2 Q3 Q4

(Million tons)

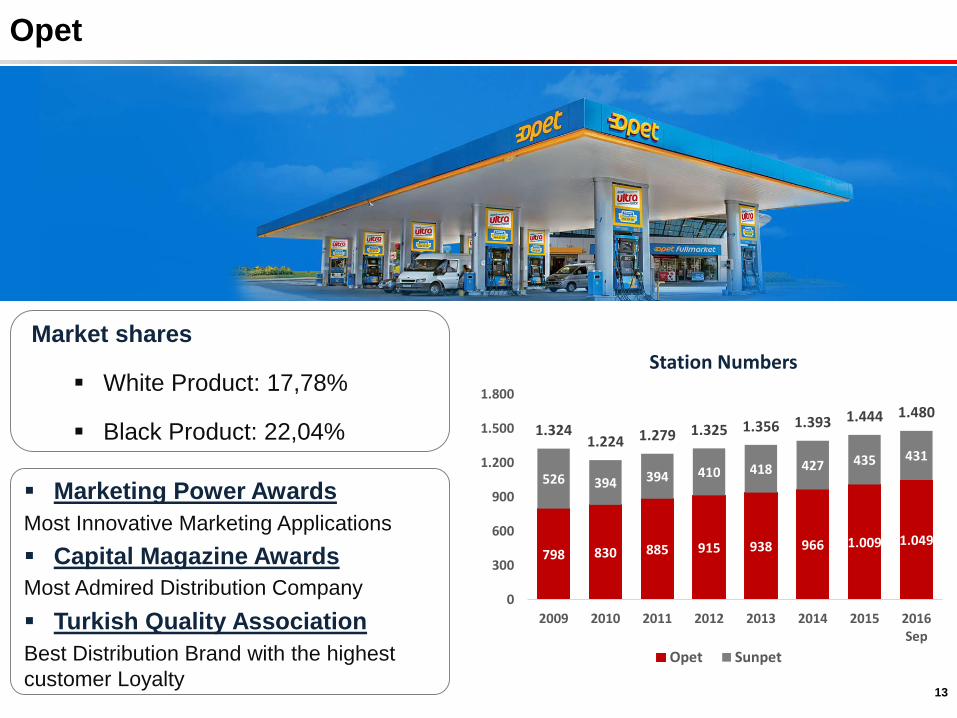

Opet

798 830 885 915 938 966 1.009 1.049

526 394 394 410 418 427 435 431

1.3241.224 1.279 1.325 1.356 1.393 1.444 1.480

0

300

600

900

1.200

1.500

1.800

2009 2010 2011 2012 2013 2014 2015 2016Sep

Station Numbers

Opet Sunpet

Market shares

White Product: 17,78%

Black Product: 22,04%

13

Marketing Power Awards

Most Innovative Marketing Applications

Capital Magazine Awards

Most Admired Distribution Company

Turkish Quality Association

Best Distribution Brand with the highest

customer Loyalty

Market Operations Financials

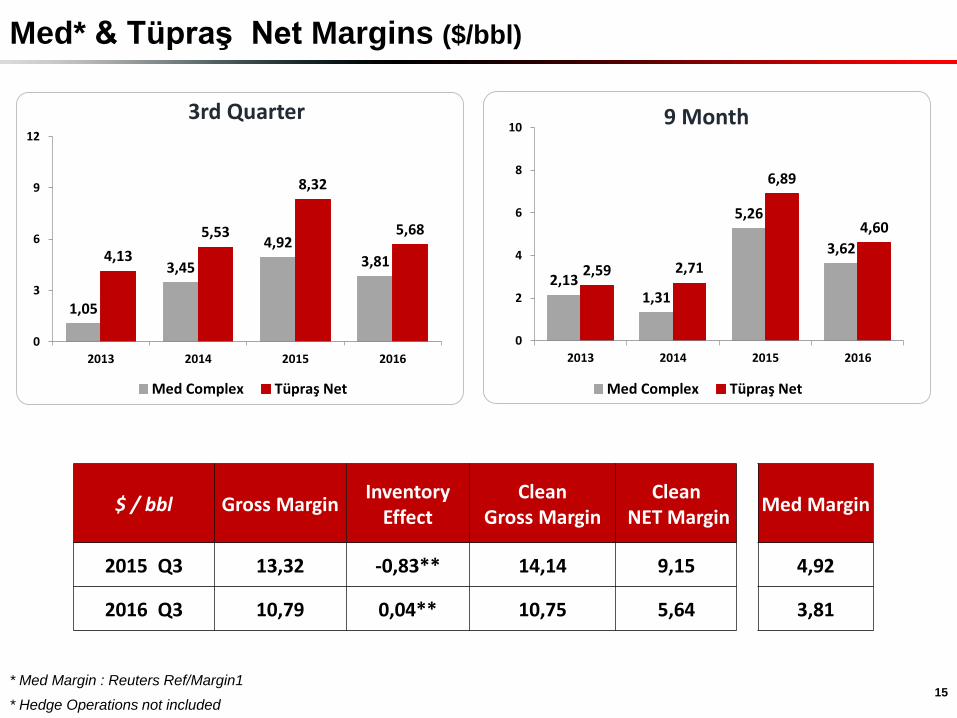

Med* & Tüpraş Net Margins ($/bbl)

15

2,131,31

5,26

3,62

2,59 2,71

6,89

4,60

0

2

4

6

8

10

2013 2014 2015 2016

9 Month

Med Complex Tüpraş Net

1,05

3,45

4,923,814,13

5,53

8,32

5,68

0

3

6

9

12

2013 2014 2015 2016

3rd Quarter

Med Complex Tüpraş Net

$ / bbl Gross MarginInventory

EffectClean

Gross MarginClean

NET MarginMed Margin

2015 Q3 13,32 -0,83** 14,14 9,15 4,92

2016 Q3 10,79 0,04** 10,75 5,64 3,81

* Hedge Operations not included

* Med Margin : Reuters Ref/Margin1

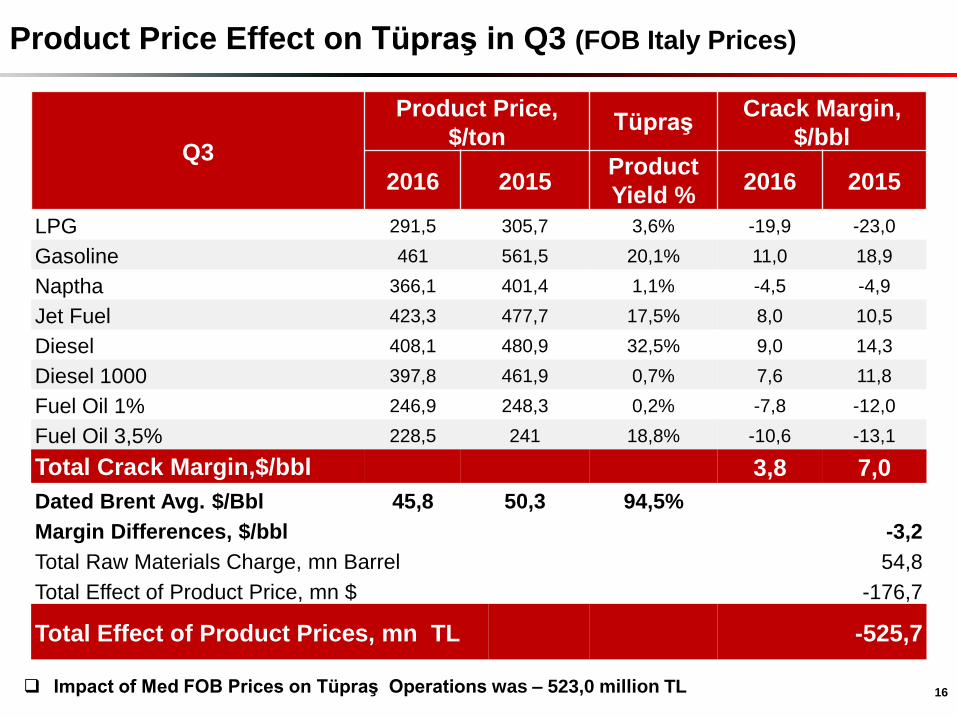

Product Price Effect on Tüpraş in Q3 (FOB Italy Prices)

Impact of Med FOB Prices on Tüpraş Operations was – 523,0 million TL

Q3

Product Price,

$/tonTüpraş

Crack Margin,

$/bbl

2016 2015Product

Yield %2016 2015

LPG 291,5 305,7 3,6% -19,9 -23,0

Gasoline 461 561,5 20,1% 11,0 18,9

Naptha 366,1 401,4 1,1% -4,5 -4,9

Jet Fuel 423,3 477,7 17,5% 8,0 10,5

Diesel 408,1 480,9 32,5% 9,0 14,3

Diesel 1000 397,8 461,9 0,7% 7,6 11,8

Fuel Oil 1% 246,9 248,3 0,2% -7,8 -12,0

Fuel Oil 3,5% 228,5 241 18,8% -10,6 -13,1

Total Crack Margin,$/bbl 3,8 7,0

Dated Brent Avg. $/Bbl 45,8 50,3 94,5%

Margin Differences, $/bbl -3,2

Total Raw Materials Charge, mn Barrel 54,8

Total Effect of Product Price, mn $ -176,7

Total Effect of Product Prices, mn TL -525,7

16

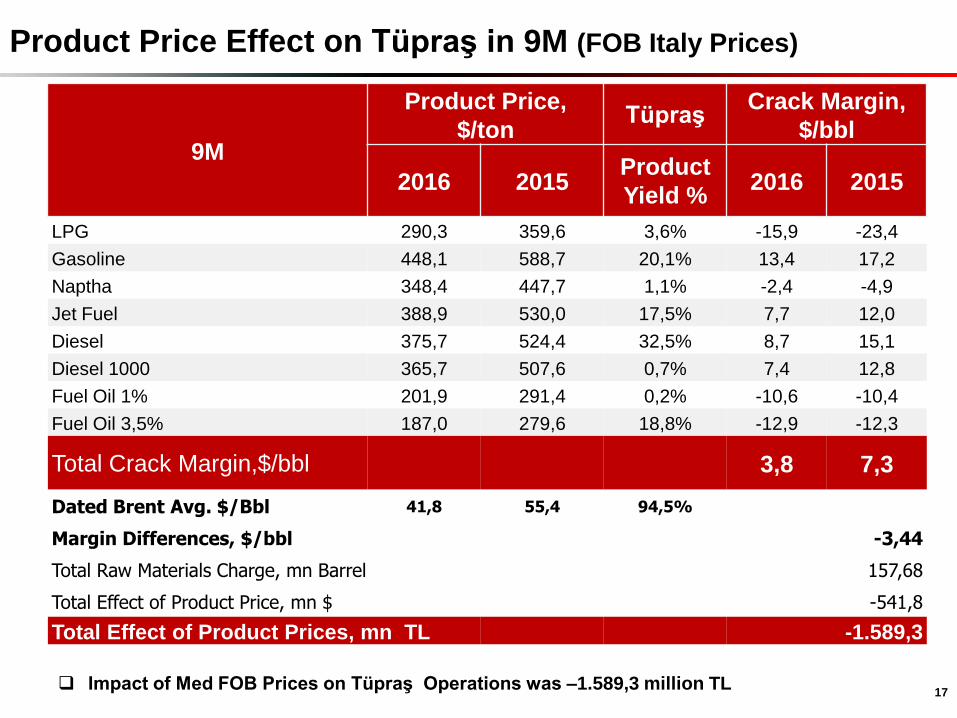

Product Price Effect on Tüpraş in 9M (FOB Italy Prices)

Impact of Med FOB Prices on Tüpraş Operations was –1.589,3 million TL

9M

Product Price,

$/tonTüpraş

Crack Margin,

$/bbl

2016 2015Product

Yield %2016 2015

LPG 290,3 359,6 3,6% -15,9 -23,4

Gasoline 448,1 588,7 20,1% 13,4 17,2

Naptha 348,4 447,7 1,1% -2,4 -4,9

Jet Fuel 388,9 530,0 17,5% 7,7 12,0

Diesel 375,7 524,4 32,5% 8,7 15,1

Diesel 1000 365,7 507,6 0,7% 7,4 12,8

Fuel Oil 1% 201,9 291,4 0,2% -10,6 -10,4

Fuel Oil 3,5% 187,0 279,6 18,8% -12,9 -12,3

Total Crack Margin,$/bbl 3,8 7,3

Dated Brent Avg. $/Bbl 41,8 55,4 94,5%

Margin Differences, $/bbl -3,44

Total Raw Materials Charge, mn Barrel 157,68

Total Effect of Product Price, mn $ -541,8

Total Effect of Product Prices, mn TL -1.589,3

17

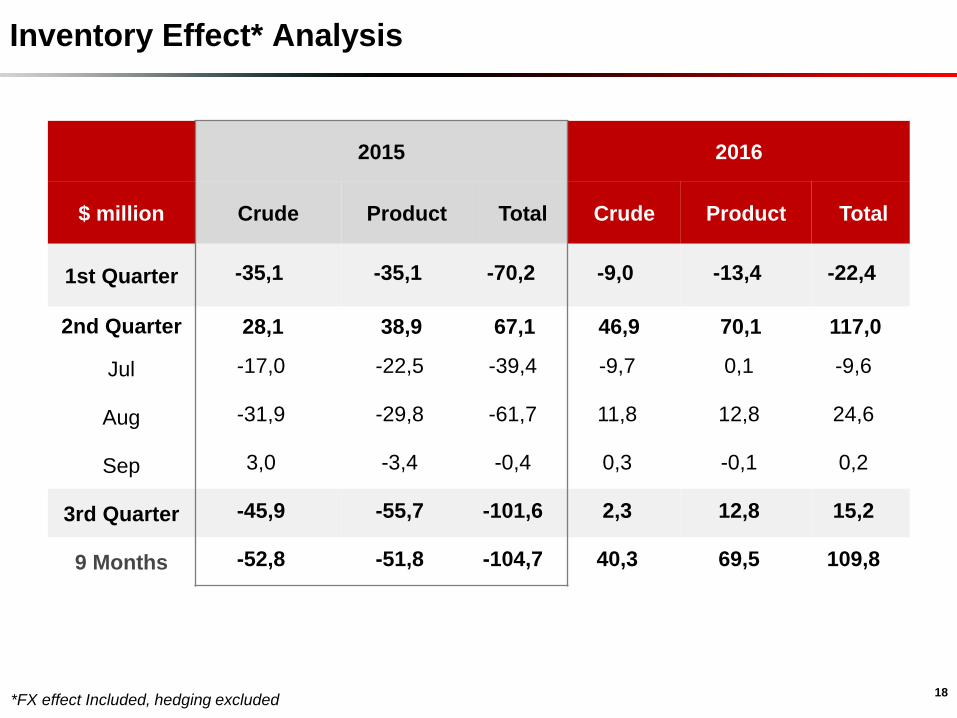

Inventory Effect* Analysis

18*FX effect Included, hedging excluded

2015 2016

$ million Crude Product Total Crude Product Total

1st Quarter -35,1 -35,1 -70,2 -9,0 -13,4 -22,4

2nd Quarter 28,1 38,9 67,1 46,9 70,1 117,0

Jul -17,0 -22,5 -39,4 -9,7 0,1 -9,6

Aug -31,9 -29,8 -61,7 11,8 12,8 24,6

Sep 3,0 -3,4 -0,4 0,3 -0,1 0,2

3rd Quarter -45,9 -55,7 -101,6 2,3 12,8 15,2

9 Months -52,8 -51,8 -104,7 40,3 69,5 109,8

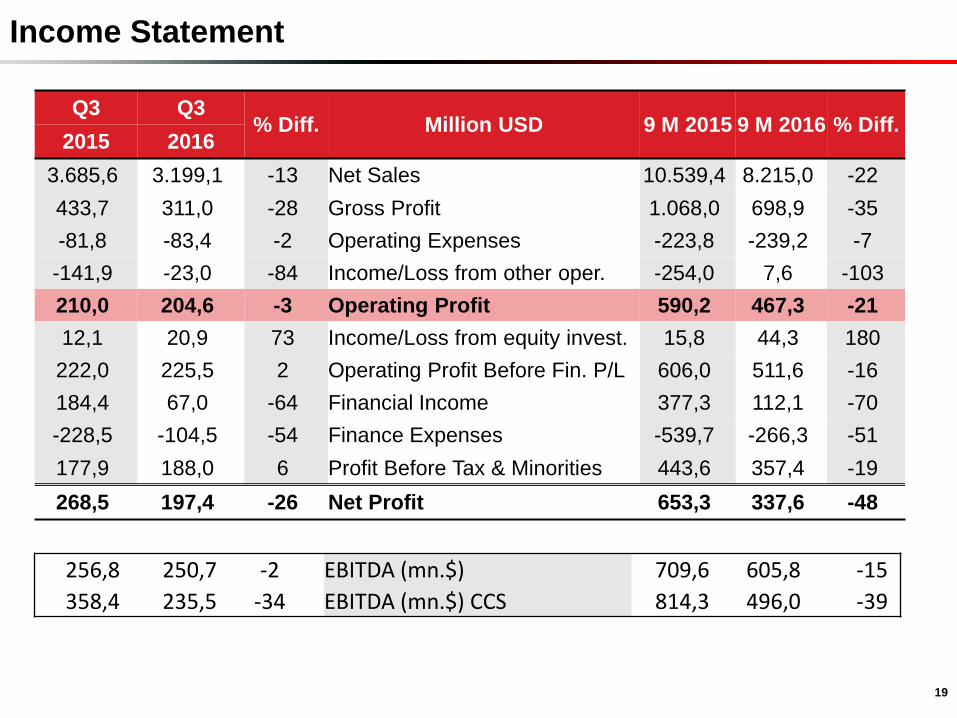

Income Statement

Q3 Q3% Diff. Million USD 9 M 2015 9 M 2016 % Diff.

2015 2016

3.685,6 3.199,1 -13 Net Sales 10.539,4 8.215,0 -22

433,7 311,0 -28 Gross Profit 1.068,0 698,9 -35

-81,8 -83,4 -2 Operating Expenses -223,8 -239,2 -7

-141,9 -23,0 -84 Income/Loss from other oper. -254,0 7,6 -103

210,0 204,6 -3 Operating Profit 590,2 467,3 -21

12,1 20,9 73 Income/Loss from equity invest. 15,8 44,3 180

222,0 225,5 2 Operating Profit Before Fin. P/L 606,0 511,6 -16

184,4 67,0 -64 Financial Income 377,3 112,1 -70

-228,5 -104,5 -54 Finance Expenses -539,7 -266,3 -51

177,9 188,0 6 Profit Before Tax & Minorities 443,6 357,4 -19

268,5 197,4 -26 Net Profit 653,3 337,6 -48

19

256,8 250,7 -2 EBITDA (mn.$) 709,6 605,8 -15

358,4 235,5 -34 EBITDA (mn.$) CCS 814,3 496,0 -39

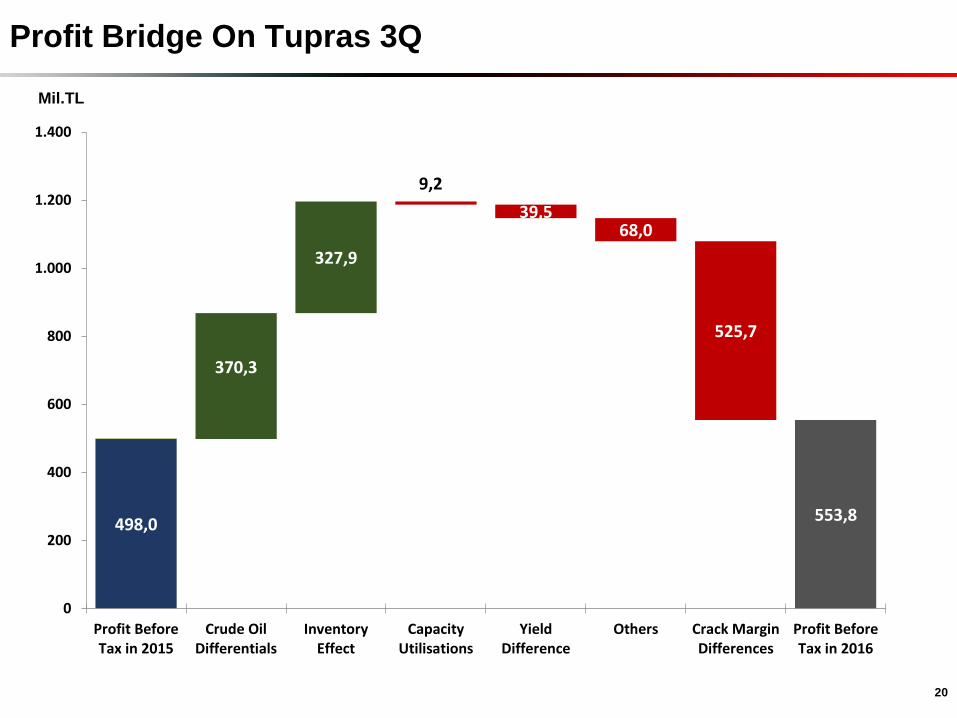

Profit Bridge On Tupras 3Q

20

Mil.TL

498,0553,8

370,3

327,9

9,2

39,568,0

525,7

0

200

400

600

800

1.000

1.200

1.400

Profit BeforeTax in 2015

Crude OilDifferentials

InventoryEffect

CapacityUtilisations

YieldDifference

Others Crack MarginDifferences

Profit BeforeTax in 2016

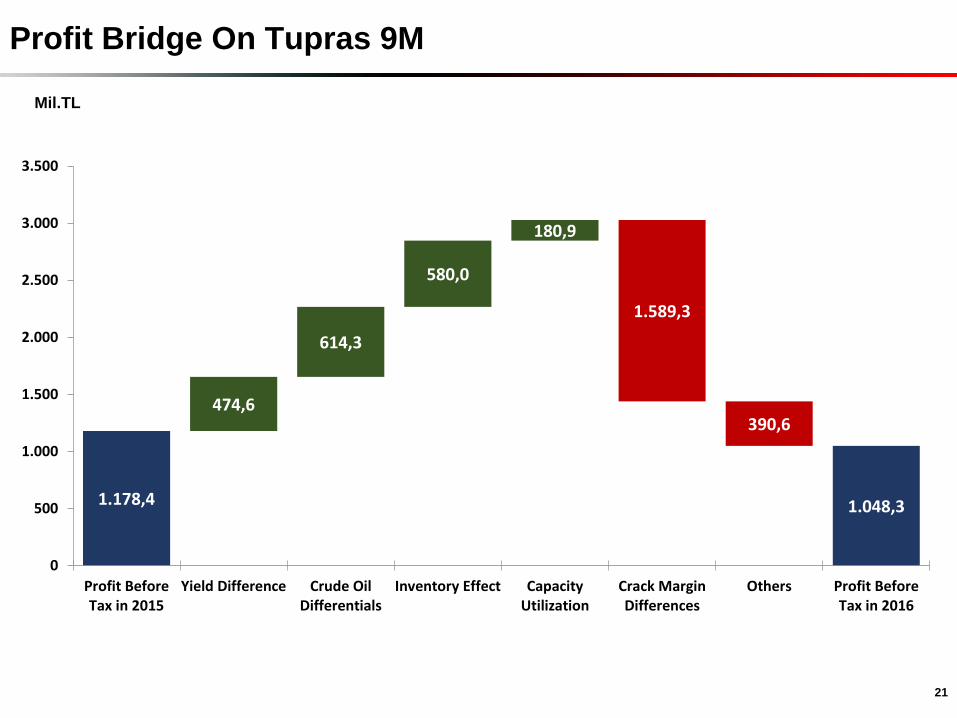

Profit Bridge On Tupras 9M

21

Mil.TL

1.178,4 1.048,3

474,6

614,3

580,0

180,9

1.589,3

390,6

0

500

1.000

1.500

2.000

2.500

3.000

3.500

Profit BeforeTax in 2015

Yield Difference Crude OilDifferentials

Inventory Effect CapacityUtilization

Crack MarginDifferences

Others Profit BeforeTax in 2016

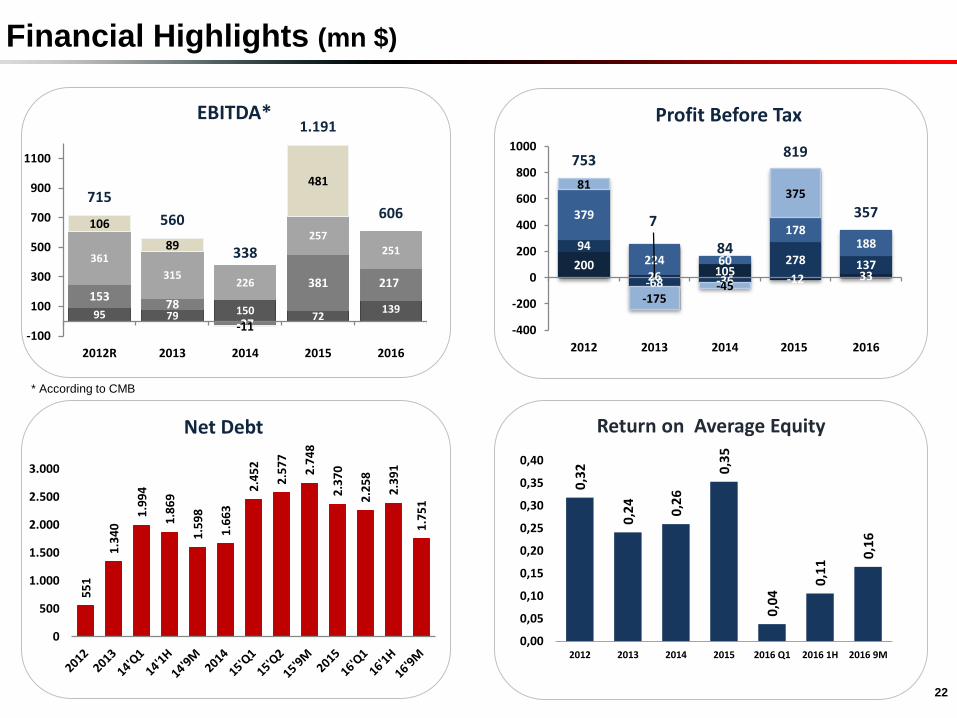

22

95 79 150 72139

15378

-27

381 217

361

315226

257251

106

89

-11

481

715

560

338

1.191

606

-100

100

300

500

700

900

1100

2012R 2013 2014 2015 2016

EBITDA*

20026 105

-12 33

94

-68 -36

278 137

379

224 60

178188

81

-175-45

375

753

7

84

819

357

-400

-200

0

200

400

600

800

1000

2012 2013 2014 2015 2016

Profit Before Tax

55

1

1.3

40

1.9

94

1.8

69

1.5

98

1.6

63

2.4

52

2.5

77

2.7

48

2.3

70

2.2

58

2.3

91

1.7

51

0

500

1.000

1.500

2.000

2.500

3.000

Net Debt

0,3

2

0,2

4

0,2

6

0,3

5

0,0

4

0,1

1

0,1

6

0,00

0,05

0,10

0,15

0,20

0,25

0,30

0,35

0,40

2012 2013 2014 2015 2016 Q1 2016 1H 2016 9M

Return on Average Equity

* According to CMB

Financial Highlights (mn $)

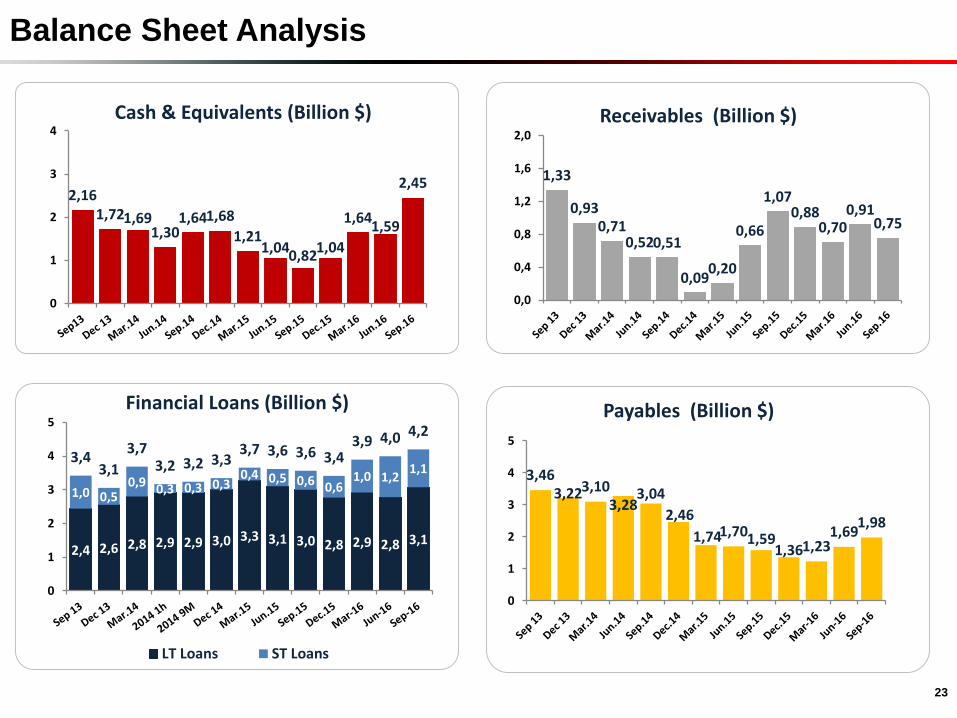

Balance Sheet Analysis

23

2,161,721,69

1,301,641,68

1,211,04

0,821,04

1,641,59

2,45

0

1

2

3

4Cash & Equivalents (Billion $)

1,33

0,930,71

0,520,51

0,090,20

0,66

1,070,88

0,700,91

0,75

0,0

0,4

0,8

1,2

1,6

2,0

Receivables (Billion $)

2,4 2,6 2,8 2,9 2,9 3,0 3,3 3,1 3,0 2,8 2,9 2,8 3,1

1,0 0,50,9 0,3 0,3 0,3

0,4 0,5 0,6 0,61,0 1,2

1,13,4

3,1

3,73,2 3,2 3,3

3,7 3,6 3,6 3,43,9 4,0 4,2

0

1

2

3

4

5

Financial Loans (Billion $)

LT Loans ST Loans

3,463,223,10

3,283,04

2,46

1,741,701,591,361,23

1,691,98

0

1

2

3

4

5

Payables (Billion $)

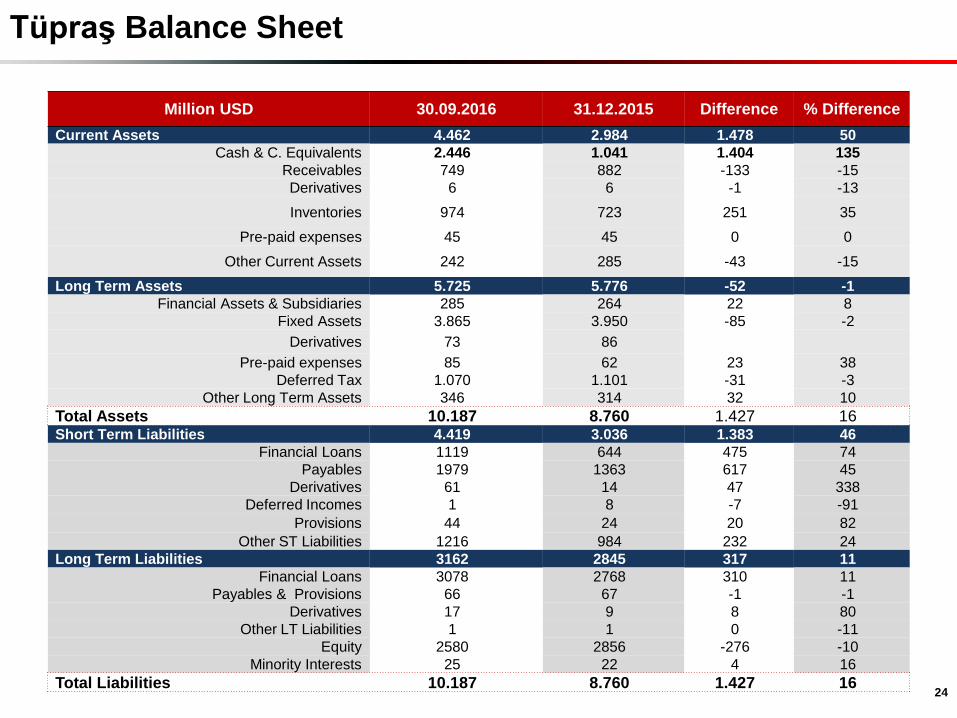

Tüpraş Balance Sheet

Million USD 30.09.2016 31.12.2015 Difference % Difference

Current Assets 4.462 2.984 1.478 50

Cash & C. Equivalents 2.446 1.041 1.404 135

Receivables 749 882 -133 -15

Derivatives 6 6 -1 -13

Inventories 974 723 251 35

Pre-paid expenses 45 45 0 0

Other Current Assets 242 285 -43 -15

Long Term Assets 5.725 5.776 -52 -1

Financial Assets & Subsidiaries 285 264 22 8

Fixed Assets 3.865 3.950 -85 -2

Derivatives 73 86

Pre-paid expenses 85 62 23 38

Deferred Tax 1.070 1.101 -31 -3

Other Long Term Assets 346 314 32 10

Total Assets 10.187 8.760 1.427 16Short Term Liabilities 4.419 3.036 1.383 46

Financial Loans 1119 644 475 74

Payables 1979 1363 617 45

Derivatives 61 14 47 338

Deferred Incomes 1 8 -7 -91

Provisions 44 24 20 82

Other ST Liabilities 1216 984 232 24

Long Term Liabilities 3162 2845 317 11

Financial Loans 3078 2768 310 11

Payables & Provisions 66 67 -1 -1

Derivatives 17 9 8 80

Other LT Liabilities 1 1 0 -11

Equity 2580 2856 -276 -10

Minority Interests 25 22 4 16

Total Liabilities 10.187 8.760 1.427 1624

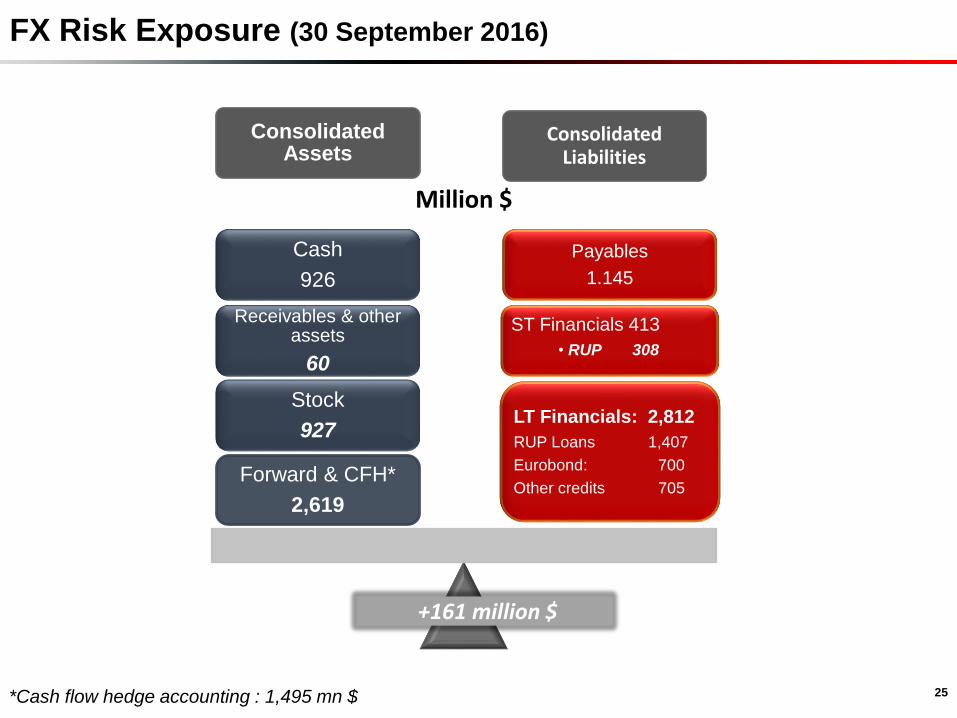

FX Risk Exposure (30 September 2016)

25*Cash flow hedge accounting : 1,495 mn $

ConsolidatedAssets

ConsolidatedLiabilities

LT Financials: 2,812

RUP Loans: 1,407

Eurobond: 700

Other credits 705

ST Financials 413

• RUP 308

Payables

1.145

Forward & CFH*

2,619

Stock

927

Receivables & otherassets

60

Cash

926

Million $

+161 million $

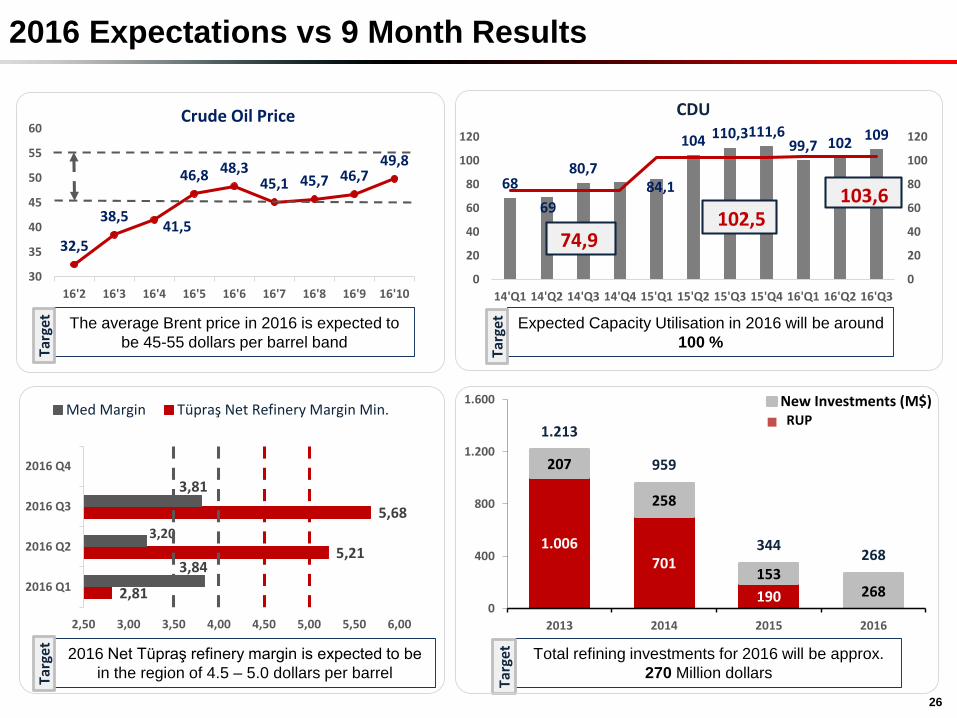

2016 Expectations vs 9 Month Results

26

32,5

38,541,5

46,8 48,345,1 45,7 46,7

49,8

30

35

40

45

50

55

60

16'2 16'3 16'4 16'5 16'6 16'7 16'8 16'9 16'10

Crude Oil Price

68

69

80,784,1

104 110,3111,699,7 102

109

0

20

40

60

80

100

120

0

20

40

60

80

100

120

14'Q1 14'Q2 14'Q3 14'Q4 15'Q1 15'Q2 15'Q3 15'Q4 16'Q1 16'Q2 16'Q3

CDU

74,9

The average Brent price in 2016 is expected to

be 45-55 dollars per barrel band

Expected Capacity Utilisation in 2016 will be around

100 %

2,81

5,21

5,68

3,84

3,20

3,81

2,50 3,00 3,50 4,00 4,50 5,00 5,50 6,00

2016 Q1

2016 Q2

2016 Q3

2016 Q4

Med Margin Tüpraş Net Refinery Margin Min.

Targ

et

Targ

et

103,6102,5

2016 Net Tüpraş refinery margin is expected to be

in the region of 4.5 – 5.0 dollars per barrelTarg

et

1.006701

190

207

258

153268

1.213

959

344268

0

400

800

1.200

1.600

2013 2014 2015 2016

New Investments (M$)RUP

Total refining investments for 2016 will be approx.

270 Million dollars

Targ

et

Disclaimer

This presentation contains forward-looking statements that reflect the Company

management’s current views with respect to certain future events. Although it is

believed that the expectations reflected in these statements are reasonable, they may

be affected by a variety of variables and changes in underlying assumptions that could

cause actual results to differ materially.

Neither Tüpraş nor any of its directors, managers or employees nor any other person

shall have any liability whatsoever for any loss arising from use of this presentation.

Thank You