Embed Size (px)

Citation preview

R E S U L T S2 0 1 1

R E S U L T S 2 0 1 1

1.

2.

3.

4.

5.

Corporate Bodies

Letter to the Shareholders

Interpump Group’s Structure

Financial highlights

Consolidated statement offinancial position

Consolidated income statement

Comprehensive consolidatedincome statement

Consolidated cash flow statement

Statement of changes inconsolidated shareholders’ equity

Directors’ remarks onperformance in 2011

Companies in the Group

Business sector information

Independent Auditor’s report

Pag. 5

Pag. 6

Pag. 9

Pag. 11

Pag. 15

Pag. 17

Pag. 19

Pag. 20

Pag. 22

Pag. 25

Pag. 32

Pag. 35

Pag. 42

Annex 1 Pag. 45

6.

7.

8.

9.

10.

11.

12.

13.

3

INDEX

Chairman

Deputy Chairmanand Executive Director

Executive Director

Independent Director

Independent Director

Non-executive Director

Non-executive Director

Non-executive Director

Independent Director

Non-executive Director

Giovanni Cavallini

Fulvio Montipò

Paolo Marinsek

Salvatore Bragantini

Sergio Erede

Giuseppe Ferrero

Marco Reboa (a), (b)

Giovanni Tamburi (b)

Franco Cattaneo (a), (b)

Giancarlo Mocchi (a)

Chairman

Statutory Auditor

Statutory Auditor

Enrico Cervellera

Achille Delmonte

Paolo Scarioni

(a) Member of the Audit Committee(b) Member of the Remuneration Committee

PricewaterhouseCoopers S.p.A.

5

Board of Directors

Board of Statutory Auditors

Independent Auditors

Interpump Group S.p.A.Head Office: 42049 Sant’Ilario d’Enza (RE) - Via E. Fermi, 25Share Capital: Euro 50,787,787.44 wolly paid up - Court of Reggio EmiliaCompanies Register R.E.- Tax Code 11666900151Vat Number IT 01682900350

CORPORATE BOD I ES 1.

Dear Shareholders,

In 2011 the Interpump Group reached a historic record for EBITDA, recording earnings of €95.0 million. Despite differences betweenbusiness activities and geographical areas, we can consider that the 2009 crisis is now behind us, even though reasons for uncertaintyin the global macroeconomic scenario persist. In relation to sales, the Industrial Sector far exceeded pre-crisis levels, while the HydraulicSector reached approximately 80% of pre-crisis levels. Highly encouraging signals were received from North America and EmergingCountries (BRIC) with significant growth percentages (respectively +20.5% and +48.2%). Contrasting signals were recorded in Europe(including Italy), which anyway returned average growth of 16.2%, although results country by country varied widely. The driving rolewas played by Germany (+35.3%).

The Interpump Group achieved the following consolidated results in 2011:- sales rose by 16.1% to €493.3 million (€472.3 million, excluding the sales of Unielectric, which was sold in September 2011),

compared to the €424.9 million of 2010;- as already mentioned, EBITDA rose to €95.0 million, equivalent to 19.3% of sales (€94.7 million without Unielectric or 20.0% of sales)

compared to €74.1 million in 2010 (equivalent to 17.4% of sales), representing growth of 28.2%;- EBIT reached €75.8 million, equivalent to 15.4% of sales (€54.7 million in 2010), reflecting an increase of 38.5%;- net profit rose by 55.5% to reach €42.6 million, compared to the €27.4 million of 2010;- earnings per share were €0.439 versus €0.284 for 2010 (+54.6%);- ROCE reached 16.4% versus 12.5% of 2010 and ROE rose to 13.5% compared to the 9.5% of 2010;- Net financial indebtedness, including debts for the acquisition of the minority interests of already controlled companies (equivalent to

€19.0 million) was €146.0 million at 31 December 2011 (€147.8 million at 31 December 2010). The €28.8 million free cash flow was entirely utilised for the acquisition of investments, treasury stock and dividends.

Performance by sector

Sales of the Hydraulic Sector totalled €229.9 million compared to the €190.3 million for 2010 and were therefore up by 20.8% (+18.1%on a like for like basis). Sales of US companies increased by 38.3% in dollar on dollar terms (+27.8% on a like for like basis); translatedinto euro the increase was 31.6% (+21.7% on a like for like basis). Sales of the other companies in the Hydraulic Sector rose by 16.7%with respect to the figure for 2010.

EBITDA for the Hydraulic Sector was €32.9 million or 14.3% of sales (€23.6 million in 2010, equivalent to 12.4% of sales), reflectinggrowth of 39.2% and improving by 1.9 percentage points both due to increase in volumes and the control of costs.

Industrial Sector turnover was up by 15.5% at €242.4 million compared to the €209.8 million of 2010. Sales of very-high pressuresystems reached €148.4 million, with growth of 21.3% compared to the €122.4 million in 2010. Sales of high pressure water pumpsreached €82.1 million and were up by 8.8% compared to the €75.4 million of 2010.

Industrial Sector EBITDA totalled €60.7 million (25.0% of sales) compared to the figure of €50.3 million recorded in 2010 (23.9% ofsales), reflecting growth of 20.5%.

External growth

2011 saw an increase in the Group’s rate of external growth. In April 2011 the Group acquired American Mobile Power (AMP)headquartered in Fairmont (Indiana - USA), one of the main US manufacturers of aluminium and steel tanks for industrial vehicle hydraulicsystems. The Company's sales from 1 April to 31 December 2011 (nine months) totalled $7.7 million with EBITDA of $1.5 million, equivalentto 19.6% of sales. The Group acquired 80% of American Mobile's shares for the overall price of $6.8 million, paid in cash. AMP’soperations are highly synergistic with respect to the business of the Interpump Group's Hydraulic Division. In this context, Muncie PowerProducts, which is a wholly owned subsidiary of Interpump Group, is the US leader in power take-offs for industrial vehicles and it hasstrengthened its position on the US market thanks to the acquisition of American Mobile, expanding its product offering with AMP's tanks.

In addition, preliminary contracts were signed in 2011 for the acquisition of Takarada, Galtech and MTC: the deals were closed in Januaryand February of 2012 so these companies were excluded from the 2011 consolidated financial statements, although they will feature inthe 2012 report.

Takarada, with registered office in Caxias do Sul (state of Rio Grande do Sul - Brazil), is a leading manufacturer and seller of powertake-offs and related hydraulic components for industrial vehicles in Brazil. In 2011 the company recorded sales of 17.9 million Reais(€8.0 million) and EBITDA of 3.3 million Reais (€1.5 million), equivalent to 18.6% of sales. A total of 29.0 million Reais (€12.9 million)was paid for 100% of Takarada's capital, inclusive of the company's financial debt. Also Takarada’s operations are highly synergisticwith respect to the business of the Interpump Group's Hydraulic Division. With the acquisition of Takarada, the Interpump Group lays thegroundwork for substantial growth of the Hydraulic Sector in Brazil, currently on the verge of allocating significant funds to the developmentof infrastructure in the coming years, also thanks to its selection as the host of forthcoming top international sporting events (Football WorldCup and the Olympics).

R E S U LT S 2 0 1 1

Galtech and MTC, both headquartered in Reggio Emilia, Italy, are engaged in the manufacture and sale of directional control valves,hydraulic valves and accessories, gear pumps and gear motors. The companies recorded combined sales of € 20.7 million in 2011, withEBITDA of €1.1 million. The net financial indebtedness of the two companies at 31 December 2011 was €1.1 million. 53% of Galtech'sshare capital and 60% of the capital of MTC was acquired for €6.3 million, of which €4.7 million paid in cash and the remaining amountsettled with 300,831 Interpump Group S.p.A. treasury shares.

Also the operations of Galtech and MTC are highly synergistic with respect to the business of the Interpump Group's Hydraulic Sector. Inthis context, it should be noted that Interpump Hydraulics S.p.A., a 100% owned subsidiary of Interpump Group S.p.A, is world leaderin power take-offs for industrial vehicles and through the acquisitions of Galtech and MTC it has strengthened its market position bybroadening its product offering.

Treasury stock

In 2011 the Group acquired 3,548,594 treasury shares at an average price of €4.6468; the shares can be used for the acquisition ofequity investments or to service stock option plans. In the same period, 1,074,286 treasury shares were sold for €4.3 million to pay forinvestments, and 50,000 for the exercise of stock options. At 31 December 2011 Interpump Group held 5,484,280 treasury shares,equivalent to 5.6% of the share capital, with an average unit cost of €4.449.

Dividends

The Board of Directors made a proposal to the shareholders' meeting to distribute a dividend of 12 euro cents per share. If approved,the dividend will be distributed as from 10 May with coupon clipping date of 7 May.From the share listing date (16 December 1996) to 8 March 2012 (share reference price of €6.35), the total return for shareholders hasbeen 11% annually for more than 15 consecutive years, considering the increase in value of the share, the dividends, the purchase oftreasury stock and the capital increase.

Warrants

October 2011 saw the end of the second exercise period of Interpump Group warrants; 10,464 warrants were exercised during theperiod, and consequently 6,431 newly issued shares were subscribed for an equivalent value of €31 thousand. There are therefore18,446,168 outstanding warrants exercisable in October 2012 by underwriting 59 newly issued shares for each 96 warrants at a priceof €5.10 per share.

Strategy for 2012 and coming years

For 2012 and future years the Interpump Group will focus a significant amount of resources on development in countries with fast-growingeconomies. In this context, the Group considers that structured growth in the future will be achieved above all through surging businessin emerging economies. In this regard we draw your attention to an additional initiative undertaken in 2011: December saw the incorporationof the Dubai based Interpump Hydraulics Middle East FZCO, founded in order to provide a local branch to penetrate the Middle Easternmarket more effectively.

As in the past, much importance will be awarded to North America, which is currently the most important market for the Group and whichis displaying highly encouraging signs of recovery. With regard to Europe, Interpump Group plans to consolidate its competitive positionsand improve them wherever possible.

Special attention will be devoted to controlling costs and to finance management, in order to maximise the generation of free cash flowto be allocated to structured external growth and the remuneration of shareholders.

I thank you for your confidence in Interpump Group S.p.A. . With the unwavering commitment of all our staff and that of myself, it is mybelief that the Group will continue to generate adequate resources for growth and for increased value of the Group for the benefit of allour shareholders.

Yours sincerely

Sant’Ilario d’Enza (RE), 13 March 2012 Giovanni Cavallini Chairman

The manager responsible for drafting company accounting documents, Carlo Banci, declares, pursuant to the terms of section 2 article 154(2) of the FinancialServices Act, that the accounting disclosures in the present document correspond to the contents of documents, the account books and the accounting entries

Sant’Ilario d’Enza (RE), 13 March 2012Carlo Banci

Manager responsible for draftingcompany accounting documents

L E T T ER TO THE SHAREHOLDERS 2.

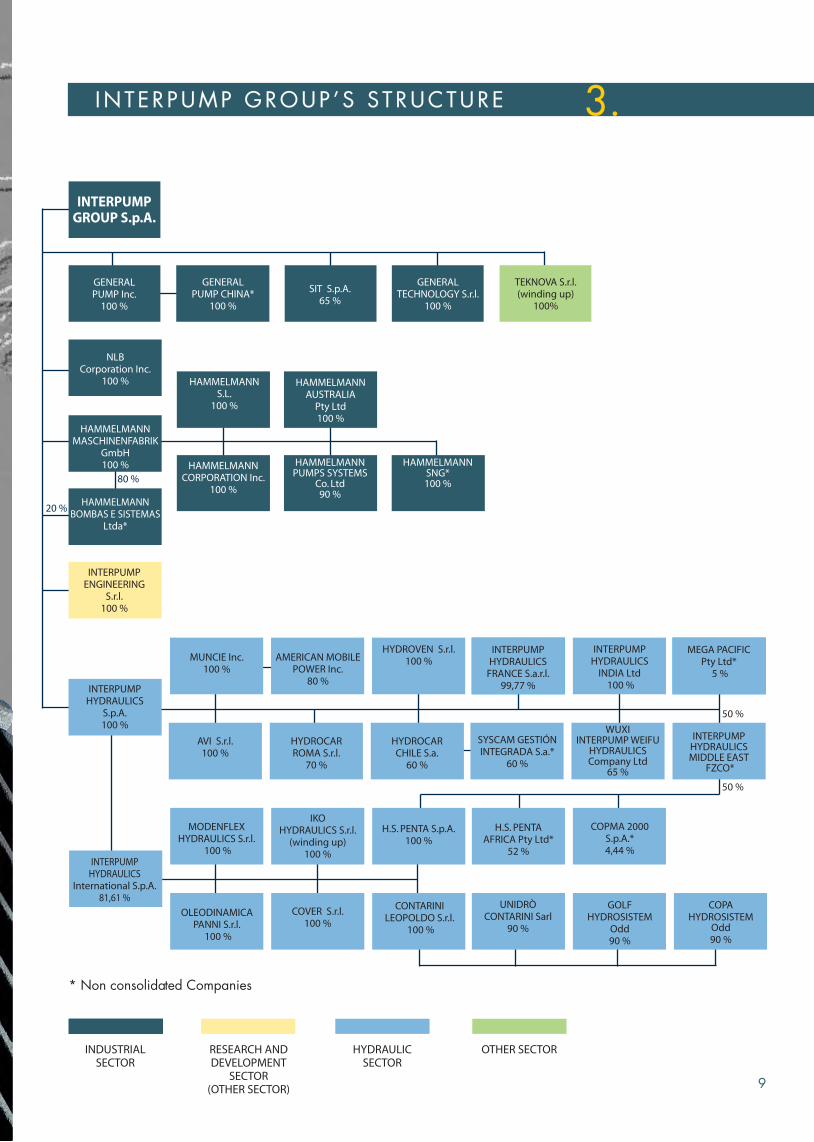

INDUSTRIALSECTOR

RESEARCH ANDDEVELOPMENT

SECTOR(OTHER SECTOR)

HYDRAULICSECTOR

* Non consolidated Companies

OTHER SECTOR

COPMA 2000S.p.A.*4,44 %

OLEODINAMICAPANNI S.r.l.

100 %

MODENFLEXHYDRAULICS S.r.l.

100 %

IKOHYDRAULICS S.r.l.

(winding up)100 %

H.S. PENTAAFRICA Pty Ltd*

52 %

COVER S.r.l.100 %

CONTARINILEOPOLDO S.r.l.

100 %

H.S. PENTA S.p.A.100 %

UNIDRÒCONTARINI Sarl

90 %

GOLFHYDROSISTEM

Odd90 %

INTERPUMPHYDRAULICS

International S.p.A.81,61 %

INTERPUMPENGINEERING

S.r.l.100 %

INTERPUMPHYDRAULICS

S.p.A.100 %

MUNCIE Inc.100 %

AMERICAN MOBILEPOWER Inc.

80 %

HYDROVEN S.r.l.100 %

HYDROCARCHILE S.a.

60 %

HYDROCARROMA S.r.l.

70 %

AVI S.r.l.100 %

SYSCAM GESTIÓNINTEGRADA S.a.*

60 %

INTERPUMPHYDRAULICS

FRANCE S.a.r.l.99,77 %

WUXIINTERPUMP WEIFU

HYDRAULICSCompany Ltd

65 %

GENERALPUMP Inc.

100 %

GENERALPUMP CHINA*

100 %

SIT S.p.A.65 %

GENERALTECHNOLOGY S.r.l.

100 %

HAMMELMANNS.L.

100 %

HAMMELMANNCORPORATION Inc.

100 %

HAMMELMANNMASCHINENFABRIK

GmbH100 %

HAMMELMANNAUSTRALIA

Pty Ltd100 %

HAMMELMANNPUMPS SYSTEMS

Co. Ltd90 %

NLBCorporation Inc.

100 %

TEKNOVA S.r.l.(winding up)

100%

INTERPUMPGROUP S.p.A.

HAMMELMANNBOMBAS E SISTEMAS

Ltda*

20 %

80 %

INTERPUMP GROUP ’S S TRUCTURE 3.

HAMMELMANNSNG*100 %

INTERPUMPHYDRAULICS

INDIA Ltd 100 %

MEGA PACIFICPty Ltd*

5 %

INTERPUMPHYDRAULICSMIDDLE EAST

FZCO*

COPAHYDROSISTEM

Odd90 %

9

50 %

50 %

2011 confirmed the recovery in sales and profitability that began in March2010. Sales of continuing operations rose by 18.0% to €472.3 million.The Industrial Sector surpassed the highest levels of the pre-recession periodwith 15.5% growth, while the Hydraulic Sector, which had suffered a farmore significant downturn, rose to around 80% of the sales recorded priorto the economic crisis. The reason for this difference is connected with thefact that the Hydraulic Sector is mainly driven by the sale of industrialvehicles in a market that has been particularly hard-hit by the slump in thebuilding construction sector, which has yet to display any significant signsof growth – at least on European markets – after the crisis. Despite thisbackground, in 2011 the Hydraulic Sector grew by 20.8% on the heelsof the promising performance in 2010, when the sector achieved growthof 27.1%.

A major contribution to recovery came from BRIC countries (Brazil, Russia,India and China), which together recorded growth of 48.2%. Althoughvolumes remain modest (sales in 2011 totalled €43.5 million), the overallincidence on consolidated sales rose from 7.3% to 9.2%. We can thereforesee that the initiatives undertaken in India, and especially in China in recentyears, are starting to generate rewards. In addition, to strengthen itscompetitive position in Brazil, on 15 February 2012 the Group acquired100% of Takarada, a Brazilian manufacture of power take-offs and otherhydraulic components, as illustrated in greater detail below.

The Group retained all the initiatives undertaken in 2009 and 2010 aimedat cutting back on costs and ensuring rigorous control of working capitaland expenditure, as described in the Board of Directors' Report accompanyingthe consolidated financial statements at 31/12/2010. Thanks also to allthe initiatives undertaken, EBITDA of continuing operations was up by28.0% versus 2010, reaching €94.7 million (20.0% of sales), reflectinga rise of 1.5 percentage points. Comprehensive EBITDA (inclusive of theElectric Motors Sector) totalled €95.0 million. This is a record in the historyof the Interpump Group, higher than the prior record of 2007 when thefigure was €94.3 million, thus confirming the solidity of the Group'scompetitive positions, which have made it possible to achieve this resultin a period like the present, in which the macroeconomic outlook is uncertainin the extreme.

From the standpoint of liquidity management we continued to focus attentionon the control of working capital; this said, the significant level of growthrecorded in sales volumes resulted in absorption of liquidity of continuingoperations in the measure of €21.4 million, after the actions taken in 2009and 2010 had served to generate liquidity from the management ofworking capital, respectively, of €44.7 million and €5.5 million.

Since April, 2011 data also include American Mobile Power, which wasacquired on 15 April 2011. American Mobile Power (AMP), headquarteredin Fairmount (Indiana), is among the primary US manufacturers and sellersof tanks for industrial vehicle hydraulic systems, mainly constructed ofaluminium and steel. The company's sales from 1 April to 31 December2011 (nine months) totalled $7.7 million, while EBITDA totalled $1.5million, equivalent to 19.6% of sales. The Group acquired 80% of AmericanMobile's shares for a total of $6.8 million, paid in cash. The remaining20% will be acquired in April 2016 for a price based on the resultsachieved by the company in the two preceding years. The operations ofAMP are highly synergistic with respect to the business of the InterpumpGroup's Hydraulic Division. In this context, Muncie Power Products, whichis a wholly owned subsidiary of Interpump Group, is the US leader inpower take-offs for industrial vehicles, and through the acquisition ofAmerican Mobile it has strengthened its position on the US market, expandingits product offering with AMP’s tanks.

The Group accentuated initiatives for external growth during the financialperiod.

An outline agreement was signed on 11 July 2011 for the acquisition ofGaltech. This transaction was closed on 31 January 2012. Headquarteredin Reggio Emilia, Galtech is active in the production and sale of gearpumps and motors, directional control valves, hydraulic accessories, andgeneral components. In 2011 company sales were €15.0 million, whileadjusted EBITDA was negative in the amount of €0.3 million. The netfinancial indebtedness of the company as at 31 December 2011 was €1.7million. The acquisition of 53% of Galtech's share capital was achievedfor a total price of €3.3 million, paid half in cash and half with 300,831Interpump Group S.p.A. treasury shares. The sellers are entitled to divestthe remaining 47% from the date of approval of the 2014 financialstatements until the date of approval of the 2025 financial statements.

An outline agreement was signed on 28 November 2011 for the acquisitionof MTC. This transaction was closed on 18 January 2012. Headquarteredin the province of Reggio Emilia, MTC is active in the production and saleof directional control valves and a range of other hydraulic valves. In 2011the company recorded sales of €5.7 million and EBITDA of €1.4 million,equivalent to 23.9% of sales. At 31 December 2011 the company heldcash totalling €0.6 million. The acquisition of 60% of the share capital ofMTC took place for a total cash payment of €3.0 million. The sellers areentitled to dispose of the remaining 40% from the date of approval of the2014 financial statements until the date of approval of the 2025 financialstatements.

The operations of Galtech and MTC are highly synergic with respect to thebusiness of the Interpump Group's Hydraulic Division. In this context, itshould be noted that Interpump Hydraulics S.p.A., a 100% owned subsidiaryof Interpump Group S.p.A, is the world leader in power take-offs for industrialvehicles and through the acquisitions of Galtech and MTC, it has strengthenedits market position, broadening its product offering.

On 2 November 2011 the Group acquired the remaining 49% of thesubsidiary AVI S.r.l. for €1,350 thousand, of which €270 thousand paidat the same time as the acquisition of the holdings with the remainder tobe settled in four annual instalments of €270 thousand each. Thereforesince that date the Group has held 100% of AVI s.r.l..

An outline agreement was signed on 21 December 2011 for the acquisitionof Takarada. This transaction was closed on 15 February 2012. Takarada,with registered office in Caxias do Sul (Brazil – the state of Rio Grande doSul ), is a leading manufacturer and seller of power take-offs and relatedhydraulic components for industrial vehicles. In 2011 the company recordedsales of 17.9 million Reais (€8.0 million) and EBITDA of 3.3 million Reais(€1.5 million), equivalent to 18.6% of sales. Acquisition of 100% of theshare capital of Takarada occurred for a total cash payment of 29.0 millionReais (€12.9 million), including received financial indebtedness. The businessof Takarada is highly synergic with respect to the business of the InterpumpGroup's Hydraulic Division. With the acquisition of Takarada, the InterpumpGroup lays the groundwork for substantial growth of the Hydraulic Sectorin Brazil, currently on the verge of allocating significant funds to thedevelopment of infrastructure in the coming years, also thanks to its selectionas the host of forthcoming top international sporting events (Football WorldCup and the Olympics).

In addition, a new company, Interpump Hydraulics Middle East FZCO withregistered office in Dubai, was incorporated on 19 December 2011. Thecompany, which is held in the measure of 50% by Interpump HydraulicsS.p.A. and 50% by HS Penta S.p.A., was created with the aim of obtaininga local distributor able to achieve more effective market penetration. Theincorporation of this company forms part of the Group's strategy of growthin areas with the greatest potential and fastest rate of development.

On 26 September 2011 Interpump Group divested its 70% stake inUnielectric, a company active in the production of windings and electricmotors for a price of €3.5 million. This amount was paid in cash on theexecution date in the quantity of one third (€1.2 million) while a furtherthird will be paid within 15 December 2012 and the final third will besettled within 15 December 2013. The extended payments are secured bybank guarantees. Unielectric was sold because Interpump Group no longerconsidered the investment to be strategic in the framework of the businesssectors of the Group, which is currently focused in the Industrial Sector (highand very high-pressure water pumps) and the Hydraulic Sector (power take-offs, hydraulic pumps, cylinders and other hydraulic components). With thesale of Unielectric the Interpump Group has therefore withdrawn from theElectric Motors Sector. The sale, which complied with the requirements ofIFRS 5 and the most recent orientations of international accounting principles,has been represented in this report as a Discontinued Operation and itis the only one of its kind in the period.

11

Main events of the year

F INANC IA L H IGHL IGHTS 4.

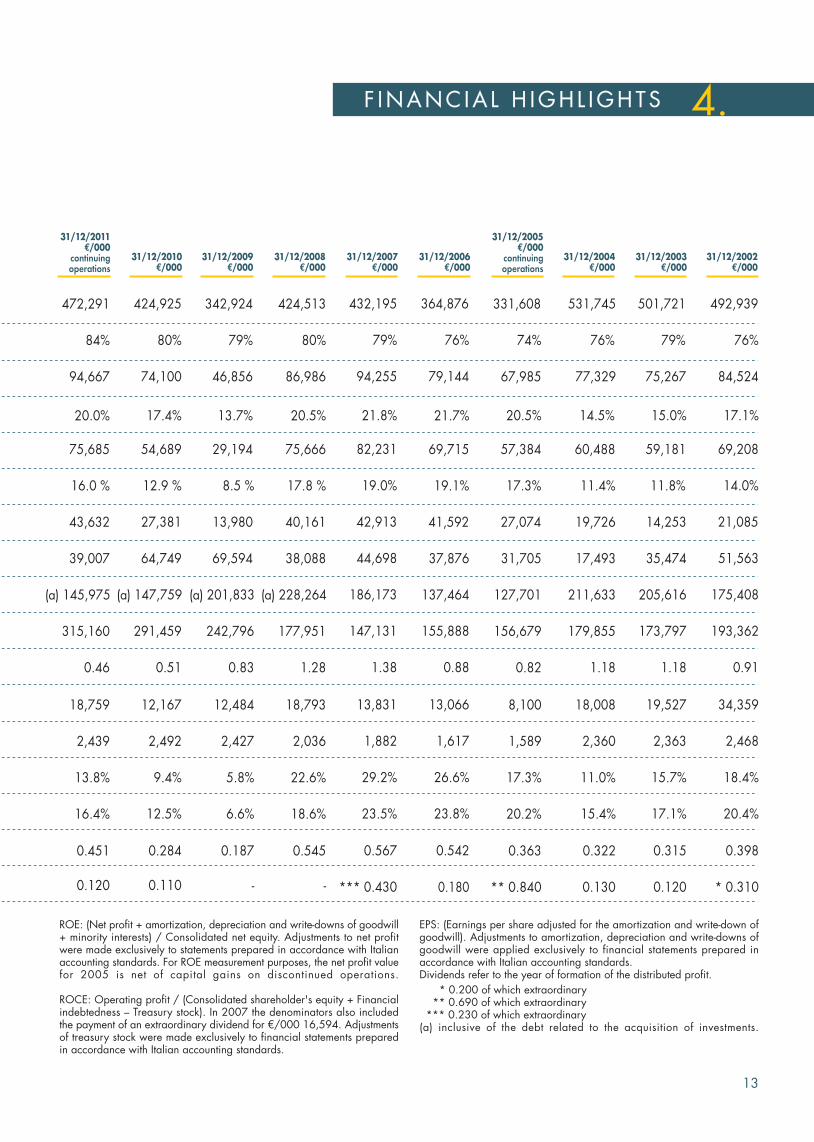

Consolidated net revenues

Foreign sales

EBITDA(Earnings before interest, tax, depreciation and amortization)

Consolidated operating profit

Operating profit %

Consolidated net profit

Cash flow from operations

Net financial indebtedness

Consolidated shareholders' equity

Debt/Equity ratio

Net capital expenditure for the year in tangibleand intangible fixed assets

Average number of employees

ROE

EPS -

Dividend per share -

ROCE

The results illustrated in the table above arebased on the consolidated accounts preparedin accordance with international accountingstandards ( IFRS) for the years ending31/12/2004 up to and including 31/12/2011,while figures for the other years are based onconsolidated accounts prepared according toItalian accounting standards.

EBITDA %

12

EPS: (Earnings per share adjusted for the amortization and write-down ofgoodwill). Adjustments to amortization, depreciation and write-downs ofgoodwill were applied exclusively to financial statements prepared inaccordance with Italian accounting standards.Dividends refer to the year of formation of the distributed profit.

* 0.200 of which extraordinary ** 0.690 of which extraordinary *** 0.230 of which extraordinary(a) inclusive of the debt related to the acquisition of investments.

331,608

74%

67,985

156,679

0.82

8,100

1,589

17.3%

20.2%

0.363

** 0.840

57,384

27,074

31,705

127,701

17.3%

60,488

11.4%

19,726

17,493

211,633

179,855

1.18

18,008

2,360

11.0%

15.4%

0.322

0.130

531,745

77,329

76%

501,721

79%

75,267

59,181

11.8%

14,253

35,474

205,616

173,797

1.18

19,527

2,363

15.7%

17.1%

0.315

0.120

492,939

76%

84,524

193,362

0.91

34,359

2,468

18.4%

20.4%

0.398

* 0.310

69,208

21,085

51,563

175,408

14.0%

432,195

79%

94,255

147,131

1.38

13,831

1,882

29.2%

23.5%

0.567

*** 0.430

82,231

42,913

44,698

186,173

19.0%

20.5% 14.5% 15.0% 17.1%21.8%

364,876

76%

79,144

155,888

0.88

13,066

1,617

26.6%

23.8%

0.542

0.180

69,715

41,592

37,876

137,464

19.1%

21.7%

424,513

80%

86,986

177,951

1.28

18,793

2,036

22.6%

18.6%

0.545

75,666

40,161

38,088

(a) 228,264

17.8 %

20.5%

-

342,924

79%

46,856

242,796

0.83

12,484

2,427

5.8%

6.6%

0.187

29,194

13,980

69,594

(a) 201,833

8.5 %

13.7%

-

424,925

80%

74,100

291,459

0.51

12,167

2,492

9.4%

12.5%

0.284

54,689

27,381

64,749

(a) 147,759

12.9 %

17.4%

0.110

31/12/2011€/000

continuingoperations

31/12/2009€/000

31/12/2008€/000

31/12/2007€/000

31/12/2005€/000

continuingoperations

31/12/2006€/000

31/12/2004€/000

31/12/2003€/000

31/12/2002€/000

ROE: (Net profit + amortization, depreciation and write-downs of goodwill+ minority interests) / Consolidated net equity. Adjustments to net profitwere made exclusively to statements prepared in accordance with Italianaccounting standards. For ROE measurement purposes, the net profit valuefor 2005 is net of capital gains on discontinued operations.

ROCE: Operating profit / (Consolidated shareholder's equity + Financialindebtedness – Treasury stock). In 2007 the denominators also includedthe payment of an extraordinary dividend for €/000 16,594. Adjustmentsof treasury stock were made exclusively to financial statements preparedin accordance with Italian accounting standards.

472,291

84%

94,667

315,160

0.46

18,759

2,439

13.8%

16.4%

0.451

75,685

43,632

39,007

(a) 145,975

16.0 %

20.0%

0.120

31/12/2010€/000

13

F INANC IA L H IGHL IGHTS 4.

EBITDA (Euro /millions)Net revenues (Euro/millions)

Cash Flow from operations (Euro /millions) Dividends (Euro)

The graphic shows only the ordinary dividends.In addiction the company has distributed special dividends:0.439 Euro in1999, 0.200 Euro in 2002,0.690 Euro in 2005 and 0.230 Euro in 2007.

‘02 ‘03 ‘04 ‘0584

.5

75.3

77.3

68.0

‘02 ‘03 ‘04 ‘05

492.

9

501.

7

531.

7

331.

6

‘06

79.1

‘06

364.

9

‘02 ‘03 ‘04 ‘05

51.6

35.5

17.5

31.7

‘02 ‘03 ‘04 ‘05

0.11

0

0.12

0

0.13

0 0.15

0

‘06

0.18

0

‘06

37.9

* *

*

* Continuing operations

* Continuing operations * Continuing operations

‘07

432.

2

‘07

44.7

‘07

94.3

‘07

0.20

0

‘08

424.

5

‘08

87.0

‘08

38.9

‘09

342.

9

‘09

46.9

‘09

70.0

‘10

424.

9

‘10

74.1

‘10

64.7

‘08 ‘09 ‘10

0.11

0

‘11

472.

3

‘11

94.7

‘11

40.8

‘11

0.12

0

* *

*

14

R E S U LT S 2 0 1 1

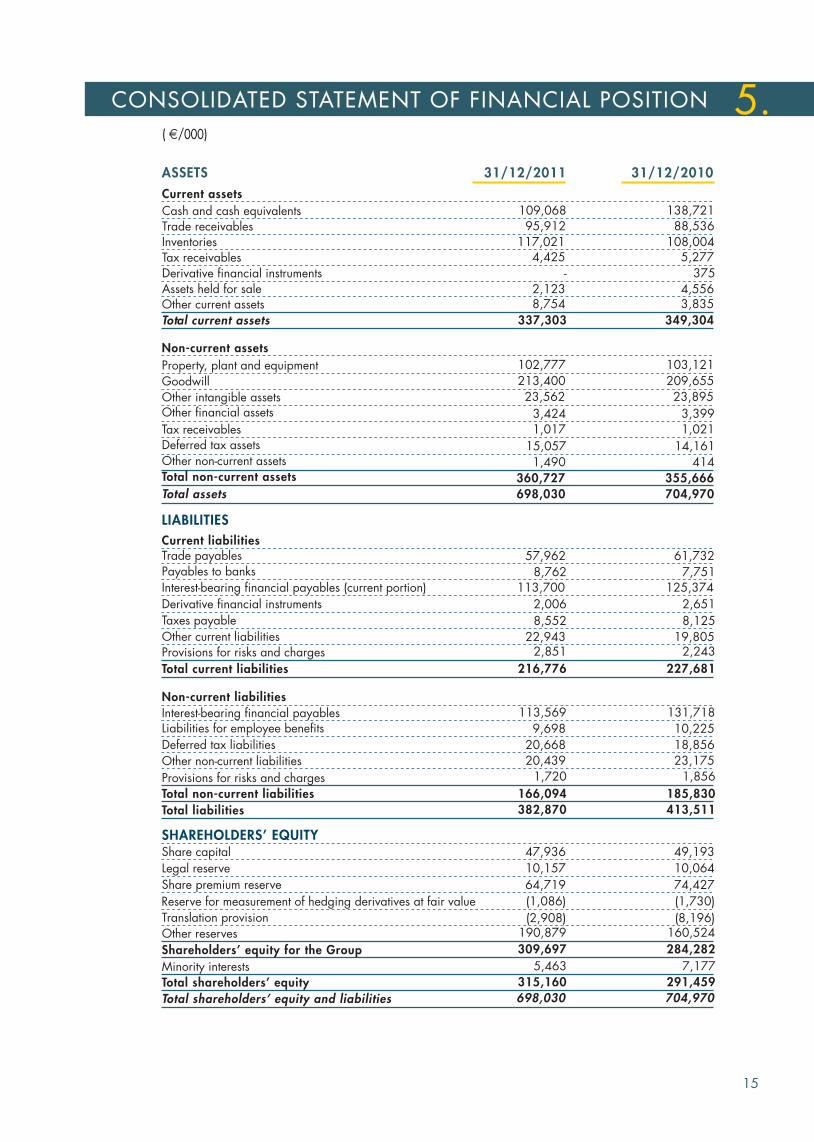

( /000)

ASSETSCurrent assetsCash and cash equivalentsTrade receivablesInventoriesTax receivablesDerivative financial instrumentsAssets held for saleOther current assetsTotal current assets

LIABILITIESCurrent liabilitiesTrade payablesPayables to banks

Interest-bearing financial payables (current portion)

Derivative financial instruments

Taxes payable

Other current liabilitiesProvisions for risks and charges

Total current liabilities

Non-current liabilitiesInterest-bearing financial payablesLiabilities for employee benefits

Deferred tax liabilities

Other non-current liabilities

Provisions for risks and chargesTotal non-current liabilitiesTotal liabilities

SHAREHOLDERS’ EQUITYShare capital

Legal reserve

Share premium reserve

Reserve for measurement of hedging derivatives at fair valueTranslation provisionOther reserves

Shareholders’ equity for the GroupMinority interestsTotal shareholders’ equityTotal shareholders’ equity and liabilities

Non-current assetsProperty, plant and equipmentGoodwillOther intangible assetsOther financial assets

Tax receivablesDeferred tax assetsOther non-current assetsTotal non-current assetsTotal assets

31/12/2011 31/12/2010

109,06895,912

117,0214,425

-2,1238,754

337,303

57,9628,762

113,700

2,006

8,55222,943

2,851

216,776

113,569

9,698

20,66820,439

1,720

47,936

10,157

64,719

(1,086)

(2,908)190,879

309,6975,463

166,094382,870

315,160698,030

102,777

360,727

213,40023,562

3,4241,017

15,0571,490

698,030

138,72188,536

108,0045,277

3754,5563,835

349,304

61,7327,751

125,374

2,651

8,12519,805

2,243

227,681

131,718

10,225

18,85623,175

1,856

49,193

10,064

74,427

(1,730)

(8,196)160,524

284,2827,177

185,830413,511

291,459704,970

103,121

355,666

209,65523,895

3,3991,021

14,161414

704,970

15

CONSOLIDATED STATEMENT OF FINANCIAL POSITION 5.

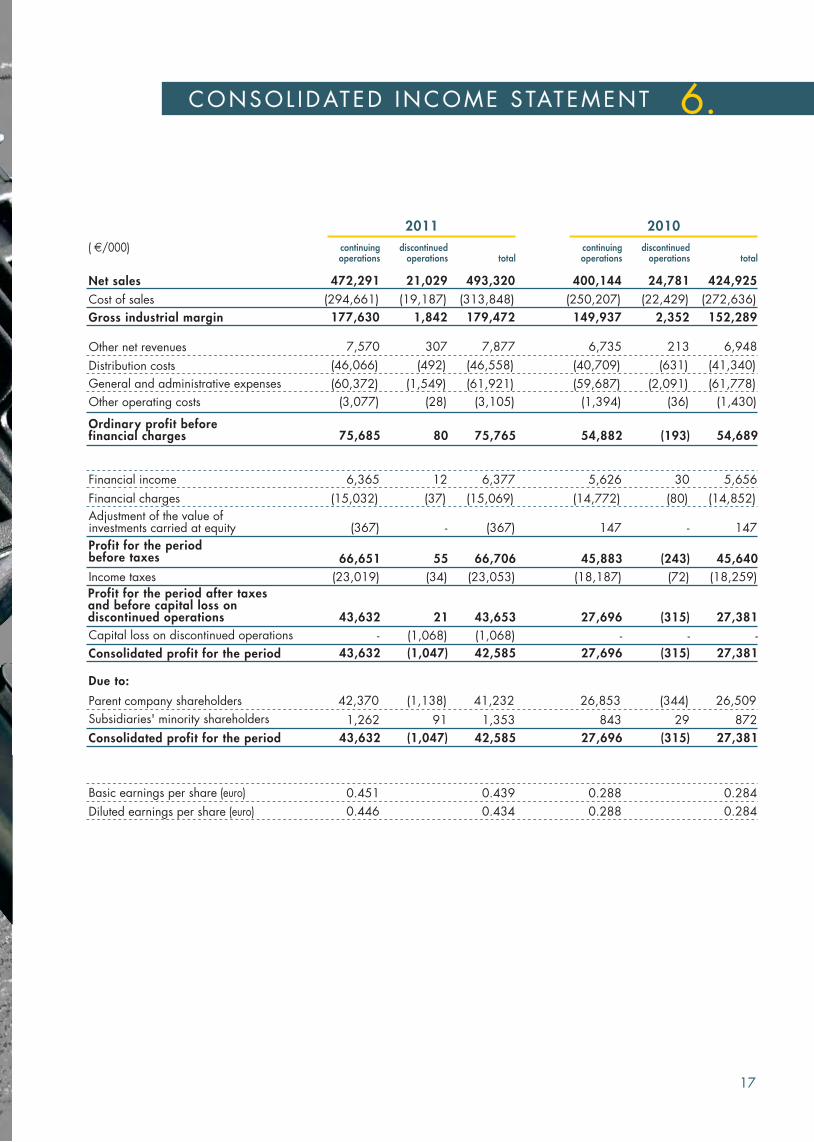

Net salesCost of sales

Gross industrial margin

Other net revenues

Distribution costs

General and administrative expenses

Other operating costs

Financial income

Financial charges

Adjustment of the value ofinvestments carried at equity

Profit for the periodbefore taxes

Income taxes

Consolidated profit for the period

Due to:

Parent company shareholders

Subsidiaries' minority shareholders

Consolidated profit for the period

Basic earnings per share (euro)

Diluted earnings per share (euro)

Ordinary profit beforefinancial charges

( /000)

424,925(272,636)

152,289

6,948

(41,340)

(61,778)

(1,430)

5,656

(14,852)

147

45,640(18,259)

27,381

26,509

872

27,381

0.284

0.284

54,689

Profit for the period after taxesand before capital loss ondiscontinued operationsCapital loss on discontinued operations -

27,381

472,291(294,661)

177,630

7,570

(46,066)

(60,372)

(3,077)

6,365

(15,032)

(367)

66,651(23,019)

43,632

42,370

1,262

43,632

0.451

0.446

75,685

43,632-

21,029(19,187)

1,842

307

(492)

(1,549)

(28)

12

(37)

-

55(34)

(1,047)

(1,138)

91

(1,047)

80

21(1,068)

493,320(313,848)

179,472

7,877

(46,558)

(61,921)

(3,105)

6,377

(15,069)

(367)

66,706(23,053)

42,585

41,232

1,353

42,585

0.439

0.434

75,765

43,653(1,068)

400,144(250,207)

149,937

6,735

(40,709)

(59,687)

(1,394)

5,626

(14,772)

147

45,883(18,187)

27,696

26,853

843

27,696

0.288

0.288

54,882

-

27,696

24,781(22,429)

2,352

213

(631)

(2,091)

(36)

30

(80)

-

(243)(72)

(315)

(344)

29

(315)

(193)

-

(315)

17

CONSOL IDATED INCOME S TATEMENT 6.

continuingoperations

discontinuedoperations total

continuingoperations

discontinuedoperations total

2011 2010

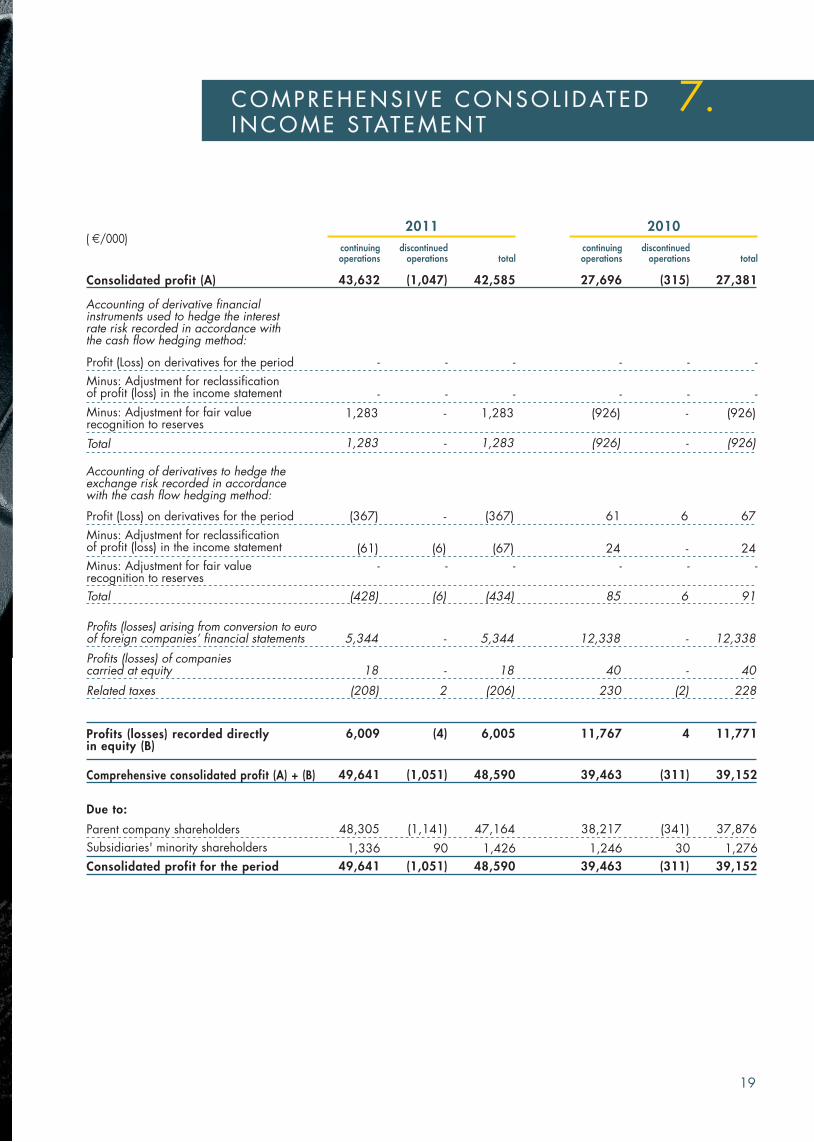

Consolidated profit (A)

Profit (Loss) on derivatives for the period

Minus: Adjustment for reclassificationof profit (loss) in the income statement

Minus: Adjustment for fair valuerecognition to reserves

Total

Profit (Loss) on derivatives for the period

Minus: Adjustment for reclassificationof profit (loss) in the income statement

Minus: Adjustment for fair valuerecognition to reserves

Total

Profits (losses) recorded directlyin equity (B)

Due to:

Parent company shareholders

Subsidiaries' minority shareholders

Consolidated profit for the period

42,585

-

1,283

(367)

(67)

-

(434)

6,005

47,164

1,426

48,590

( /000)

Accounting of derivative financialinstruments used to hedge the interestrate risk recorded in accordance withthe cash flow hedging method:

Accounting of derivatives to hedge theexchange risk recorded in accordancewith the cash flow hedging method:

Profits (losses) arising from conversion to euroof foreign companies’ financial statements

Related taxes

5,344

(206)

Profits (losses) of companiescarried at equity 18

Comprehensive consolidated profit (A) + (B) 48,590

-

1,283

27,381

-

(926)

67

24

-

91

11,771

37,876

1,276

39,152

12,338

228

40

39,152

-

(926)

continuingoperations

43,632

-

1,283

(367)

(61)

-

(428)

6,009

48,305

1,336

49,641

5,344

(208)

18

49,641

-

1,283

discontinuedoperations

(1,047)

-

-

-

(6)

-

(6)

(4)

(1,141)

90

(1,051)

-

2

-

(1,051)

-

-

totalcontinuingoperations

discontinuedoperations total

(315)

-

-

6

-

-

6

4

(341)

30

(311)

-

(2)

-

(311)

-

-

27,696

-

(926)

61

24

-

85

11,767

38,217

1,246

39,463

12,338

230

40

39,463

-

(926)

19

2011

COMPREHENS IVE CONSOL IDATEDINCOME S TATEMENT

7.

2010

Cash flow from operating activities

Earnings before taxes and capital losseson discontinued operations

Adjustments for non-cash items:

Capital losses (Capital gains) from thesale of fixed assets

Amortization and depreciation ofintangible and tangible fixed assets

(Profit) losses from investments

Net liquidity generated byoperating activities

Net Capital losses (Capital gains)from the sale of investments

Costs ascribed to the income statementrelative to stock options that do not involvemonetary outflows for the Group

Net change of risk funds andallocations to provisions for employeebenefits

Net financial charges

Other

(Increase) decrease in trade receivablesand other current assets

(Increase) decrease in inventories

Increase (decrease) in trade payablesand other current liabilities

Interest paid

Currency exchange gains realized

Income taxes paid

Cash flows from investmentactivitiesOutlay for the acquisition of investments,net of received cash and including thetreasury shares transferred for payment

Proceeds from the sale of investments

Proceeds from sales oftangible fixed assets

Received financial income

18,316

996

367

581

8,692

180

92,459

(14,373)

(12,118)

4,713

(8,720)

(267)

(22,687)

39,007

(1,929)

(10,986)

Increase in intangible fixed assets (2,770)

Portion of capital increase of asubsidiary paid by the minorityshareholder

Capital expenditure in property,plant and equipment

1,603

2,899

Outlays for tangible fixed assetsdestined for hire (3,700)

Proceeds from the sale of fixedassets granted for hire 2,250

Other 106

Net liquidity generated (used) byinvesting activities

-

(9,102)

1,551

-

( /000)

45,640

18,893

2,280

(147)

(353)

9,196

(8)

74,130

(12,106)

(3,321)

25,556

(8,956)

590

(11,144)

64,749

(539)

(6,808)

(2,300)

360

1,089

(2,225)

1,426

(102)

(14,535)

(33)

(7,117)

43

300

(16,699)

-

66,706

18,077

962

367

612

8,667

180

92,138

(14,452)

(11,113)

5,887

(8,702)

(264)

(22,687)

40,807

(1,928)

(10,644)

(2,763)

1,591

2,896

(3,700)

2,250

139

-

(9,102)

1,551

-

66,651

(16,332)

-

239

34

-

(31)

25

-

321

79

(1,005)

(1,174)

(18)

(3)

-

(1,800)

(342)

(7)

12

3

-

-

(33)

-

-

55

(1)

(367)

-

-

-

(243)

354

104

-

(4)

50

-

250

(2,951)

51

3,179

(46)

(6)

(23)

454

(11)

(164)

(21)

29

22

-

-

(102)

(236)

-

-

-

-

45,883

18,539

2,176

(147)

(349)

9,146

(8)

73,880

(9,155)

(3,372)

22,377

(8,910)

596

(11,121)

64,295

(528)

(6,644)

(2,279)

331

1,067

(2,225)

1,426

-

(14,299)

(33)

(7,117)

43

300

20

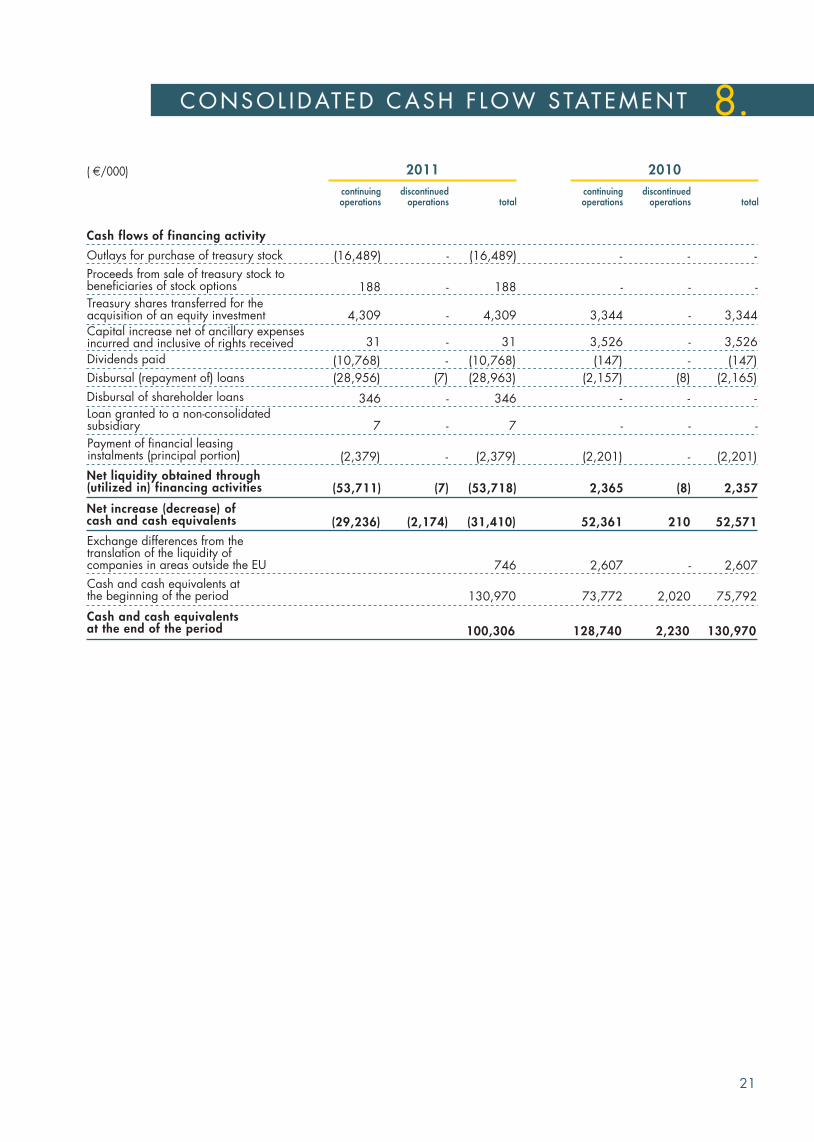

8.

continuingoperations

discontinuedoperations total

continuingoperations

discontinuedoperations total

2011 2010

Cash flows of financing activity

Outlays for purchase of treasury stock

Proceeds from sale of treasury stock tobeneficiaries of stock options

Disbursal of shareholder loans

Net liquidity obtained through(utilized in) financing activities

Net increase (decrease) ofcash and cash equivalents

Cash and cash equivalents atthe beginning of the period

Disbursal (repayment of) loans

Exchange differences from thetranslation of the liquidity ofcompanies in areas outside the EU

-

(7)

(2,174)

Cash and cash equivalentsat the end of the period

Payment of financial leasinginstalments (principal portion) -

(7)

Capital increase net of ancillary expensesincurred and inclusive of rights received -

( /000)

Treasury shares transferred for theacquisition of an equity investment -

Dividends paid -

Loan granted to a non-consolidatedsubsidiary -

-

-

2,357

52,571

130,970

(2,201)

-

(2,165)

3,526

3,344

(147)

-

75,792

2,607

-

-

188

(53,711)

(29,236)

(2,379)

(28,956)

31

4,309

(10,768)

7

(16,489)

346

188

(53,718)

(31,410)

100,306

(2,379)

(28,963)

31

4,309

(10,768)

7

130,970

746

(16,489)

346

-

-

2,365

52,361

128,740

(2,201)

-

(2,157)

3,526

3,344

(147)

-

73,772

2,607

-

-

(8)

210

2,230

-

-

(8)

-

-

-

-

2,020

-

21

CONSOL IDATED CASH F LOW STATEMENT 8.

continuingoperations

discontinuedoperations total

continuingoperations

discontinuedoperations total

2011 2010

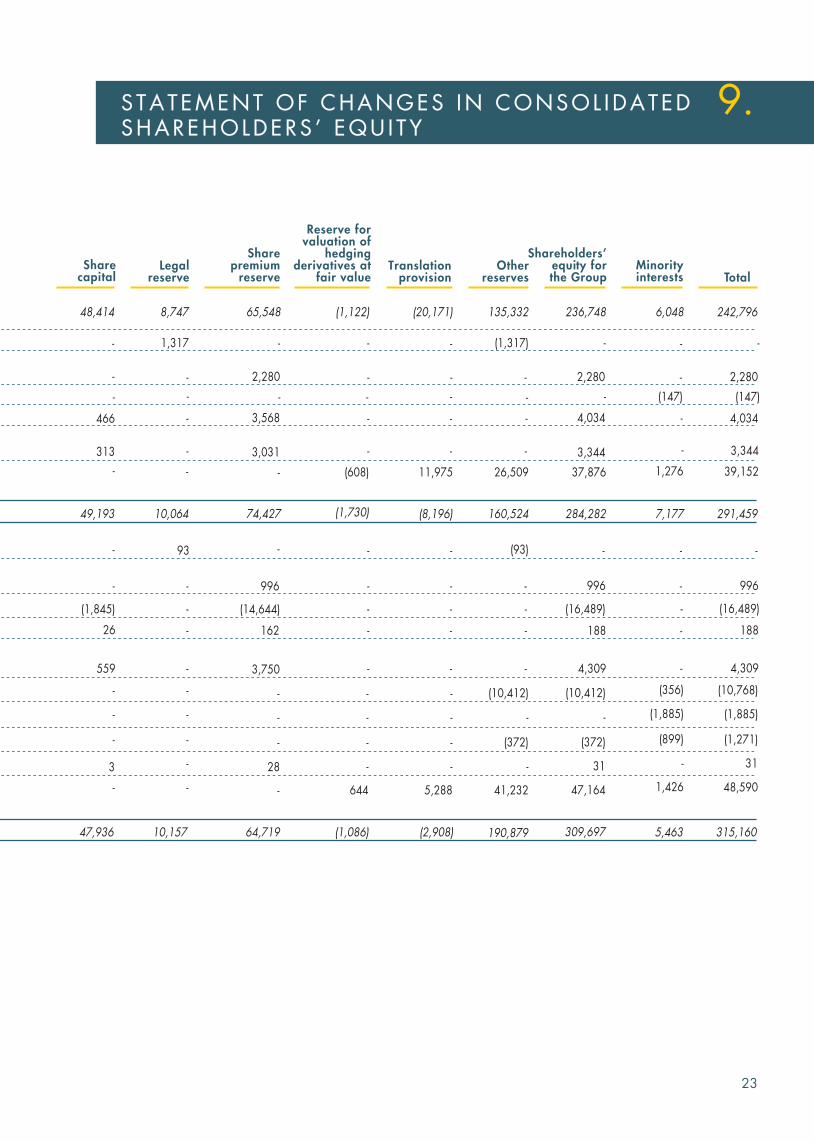

Balances as at 1 January 2010

Capital increase following exercise of warrants

Disposal of treasury stock to pay debts forthe acquisition of equity investments

Balances at 31 December 2010

Sale of treasury stock to the beneficiaries of stock options

Purchase of treasury stock

Balances at 31 December 2011

Recording in the income statement of the fair value of the stock options assigned and exercisable

Allocation of 2010 residual profit

Recording in the income statement of the fair valueof the stock options assigned and exercisable

Dividends paid

Allocation of 2009 profit

Comprehensive profit (loss) for 2010

Dividends paid

Transfer of treasury stock to support the acquisition of the additional11% of Interpump Hydraulics International

( /000)

Disposal of investment in Unielectric

Acquisition of additional 49% of AVI

Capital increase following exercise of warrants

Comprehensive profit (loss) for 2011

22

9.

Sharecapital

Legalreserve

Sharepremium

reserveOther

reserves

Shareholders’equity forthe Group

Minorityinterests Total

242,796

Translationprovision

Reserve forvaluation of

hedgingderivatives at

fair value

2,280

291,459

-

996

(16,489)

188

4,309

(10,768)

315,160

6,048

-

7,177

-

-

5,463

236,748

2,280

284,282

-

996

190,879

135,332

-

-

160,524

-

-

-

-

309,697

(20,171)

-

-

-

(8,196)

-

-

-

-

-

(2,908)

65,548

74,427

64,719

(1,122)

-

-

-

-

-

-

-

-

(1,086)

8,747

-

-

-

10,064

-

-

-

-

-

10,157

48,414

49,193

-

-

47,936

- -

-

-

-

-

-

-

-

-

(147)

4,034

3,344

39,152

(356)

-

2,280

-

996

- - - (10,412)

-

-

(10,412)

-

-

1,276

-

-

-

-

-

26

559

93

-

-

-

162

3,750

(608)

(1,730)

11,975 26,509

(93)

37,876

188

4,309

-

-

(1,885)-- (1,885)- - - - -

(1,271)-- (899)- - - (372) (372)

31- -- - - 31

48,590-- 1,426- 644 5,288 41,232 47,164

466

313

(1,845)

3

1,317

3,568

3,031

(14,644)

28

(1,317)

4,034

3,344

(16,489)

(147)

23

S TATEMENT OF CHANGES IN CONSOL IDATEDSHAREHOLDERS ’ EQU I TY

9.

The "other" item refers to cleaning machinery and machinery for sheet metal drawing, blanking and pressing.

Discontinued operations

The income statement for discontinued operations represents exclusively the contribution of the Electric Motors Sector to the consolidatedtotal; indeed, sales made by the Electric Motors Sector to Interpump Group S.p.A. and its subsidiaries are not shown among discontinuedoperations because the aim of the income statement is to represent the situation of the Interpump Group after the divestment of Unielectric.Therefore the discontinued operations column does not present pro forma figures, and nor is it representative of the marginality of theElectric Motors Sector.

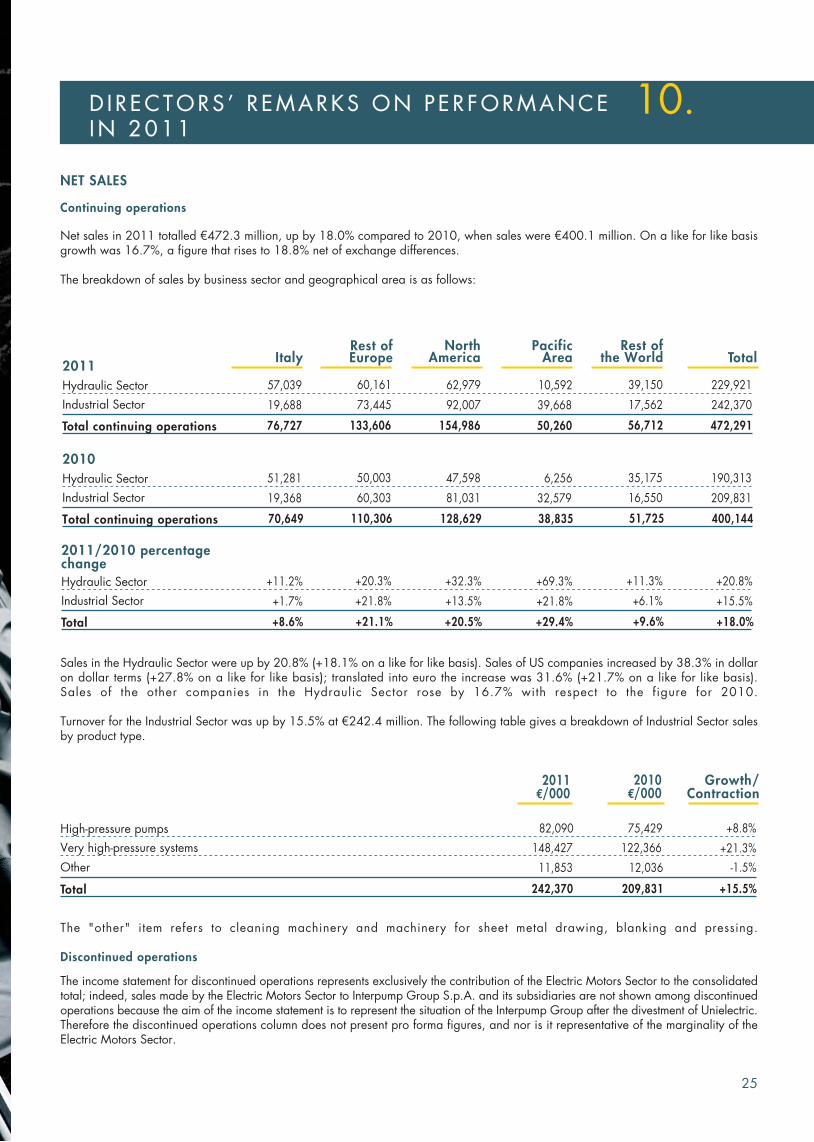

NET SALES

Continuing operations

Net sales in 2011 totalled €472.3 million, up by 18.0% compared to 2010, when sales were €400.1 million. On a like for like basisgrowth was 16.7%, a figure that rises to 18.8% net of exchange differences.

The breakdown of sales by business sector and geographical area is as follows:

+69.3% +11.3%Hydraulic Sector

+29.4%

+20.8%+11.2% +20.3%

+21.8%

+8.6%

+32.3%

Industrial Sector

Total

+1.7%

+21.1%

+13.5%

+20.5%

+21.8% +6.1%

+9.6%

+15.5%

+18.0%

2011/2010 percentagechange

PacificArea Total

Rest of the WorldItaly

Rest ofEurope

North America

10,592 39,150Hydraulic Sector

50,260

229,92157,039 60,161

73,445

76,727

62,979

Industrial Sector

Total continuing operations

19,688

133,606

92,007

154,986

39,668 17,562

56,712

242,370

472,291

2011

Sales in the Hydraulic Sector were up by 20.8% (+18.1% on a like for like basis). Sales of US companies increased by 38.3% in dollaron dollar terms (+27.8% on a like for like basis); translated into euro the increase was 31.6% (+21.7% on a like for like basis).Sales of the other companies in the Hydraulic Sector rose by 16.7% with respect to the figure for 2010.

Turnover for the Industrial Sector was up by 15.5% at €242.4 million. The following table gives a breakdown of Industrial Sector salesby product type.

Hydraulic Sector

Industrial Sector

Total continuing operations

2010

38,83570,649 110,306 128,629 51,725 400,144

82,090High-pressure pumps

11,853

242,370

+8.8%

Very high-pressure systems

Other

Total

148,427 +21.3%

-1.5%

+15.5%

Growth/ Contraction

2010€/000

75,429

12,036

209,831

122,366

2011€/000

6,256 35,175 190,31351,281 50,003

60,303

47,598

19,368 81,031 32,579 16,550 209,831

25

D I R ECTORS ’ R EMARKS ON PERFORMANCEIN 2011

10.

PROFITABILITY

Continuing operations

It should be noted that the income statement for 2011 reflects various non-recurring revenues and costs which largely offset each otherso EBITDA and EBIT were unaffected. Non-recurring income took the form of a capital gain of €1.2 million included under OtherOperating Revenues and related to the sale of a building classified under assets held for sale. Non-recurring costs were composed ofallocations of extraordinary amount although not of exceptional nature, made to the allowance for inventories and to the bad debtprovision on the basis of prudential evaluations of certain specific contingencies. The allocations to the allowance for inventories howeverhad a negative impact on the gross industrial margin in the measure of 0.2 percentage points, which were subsequently recovered interms of EBIT and EBITDA.

The cost of sales accounted for 62.4% of turnover (62.5% in 2010). Production costs totalled €102.3 million (€90.1 million in 2010),equivalent to 21.7% of sales (22.7% in 2010). The purchase costs of raw materials and components sourced on the market, includingchanges in inventories, totalled €192.4 million (€159.4 million in 2010). The incidence of purchase costs, including changes ininventories, was 40.7% compared to 39.8% in 2010. The effects of the consolidation of American Mobile are not significant.

On a like for like basis distribution costs rose by 12.3% with respect to 2010, while the relative incidence on sales fell by 0.4 percentagepoints.

General and administrative expenses rose by 0.5% like for like with respect to 2010, although their incidence on sales fell by 2.1percentage points. In 2010 general and administrative expenses were influenced by the recognition of costs for stock options relativeto the fourth tranche of the 2006/2009 plan (allocation of 1,100,000 options exercisable from 1 July 2010) and the recalculation ofthe exercise prices of options already allocated in prior years and not yet exercised, further to the share capital increase. The foregoingcosts of a one-off basis totalled €1.2 million. General and administrative expenses, net of the said non-recurring one-off amount were2.4% higher than in 2010, like for like.

Overall payroll costs of continuing operations were €106.7 million (€98.1 million in 2010) for an average headcount is 2,439 (therewere 2,349 employees of companies within continuing operations, hence excluding Unielectric, in 2010; the figure rises to 2,492 ifUnielectric is included). The increase in the average number of employees is due, in the number of 38, to the consolidation of AmericanMobile, which was not present in 2010. For calculation of the average number we draw your attention to the fact that the employeesof American Mobile were considered only for the period of consolidation and hence by three quarters. On a like for like basis payrollcosts were up by 7.4%, with an increase of 53 in the number of personnel (+2.2%) and a 5.0% increase in the average per-capitacost. The increase in the average headcount can be broken down as follows: -17 in Europe, +63 in the US (of which 38 due to theconsolidation of American Mobile, so the increase was 25 staff on a like for like basis) and +45 in the Rest of the World (China, India,Chile and Australia). The increase in the per-capita cost is due to the reduced recourse to social shock absorbers, the greater use ofovertime to cope with higher sales volumes, and also contractual salary raises and bonus awards for the achievement of targets.

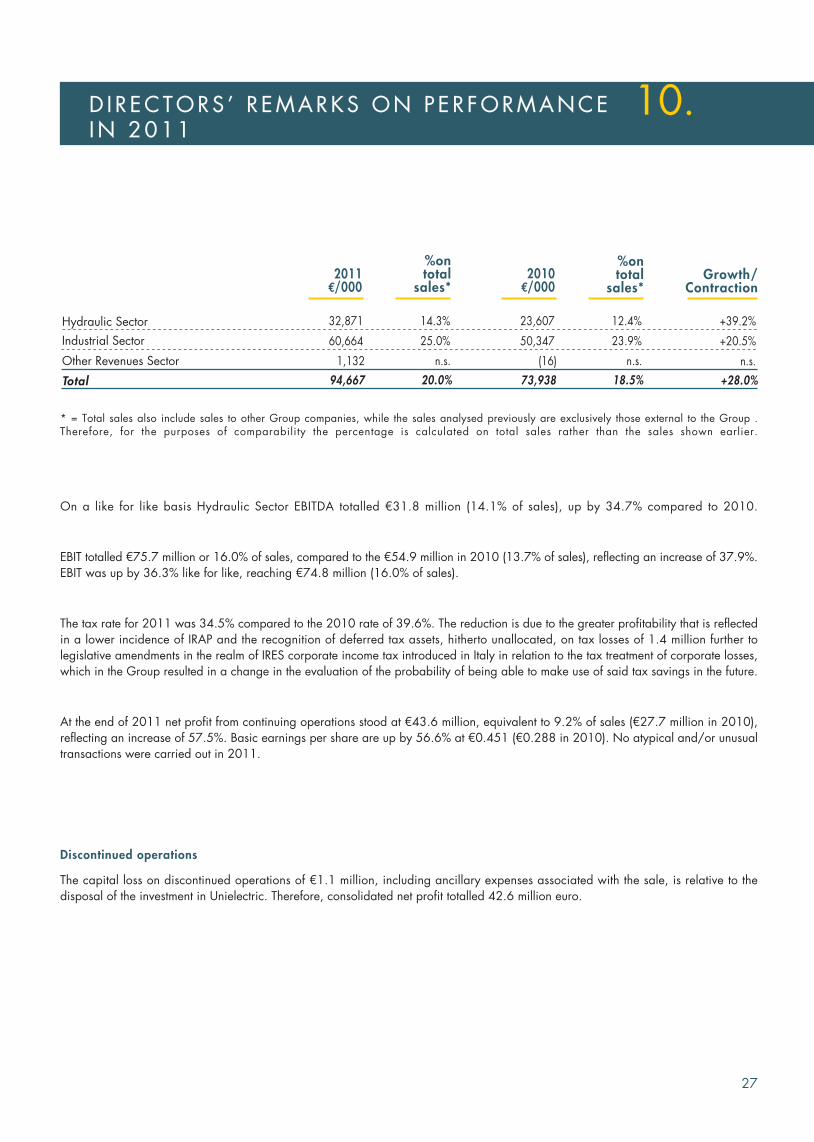

EBITDA stood at €94.7 million or 20.0% of sales, compared to the €73.9 million of 2010 which accounted for 18.5% of sales (+28.0%and +26.6% on a like for like basis). The following table shows EBITDA for each business sector:

26

10.

On a like for like basis Hydraulic Sector EBITDA totalled €31.8 million (14.1% of sales), up by 34.7% compared to 2010.

EBIT totalled €75.7 million or 16.0% of sales, compared to the €54.9 million in 2010 (13.7% of sales), reflecting an increase of 37.9%.EBIT was up by 36.3% like for like, reaching €74.8 million (16.0% of sales).

The tax rate for 2011 was 34.5% compared to the 2010 rate of 39.6%. The reduction is due to the greater profitability that is reflectedin a lower incidence of IRAP and the recognition of deferred tax assets, hitherto unallocated, on tax losses of 1.4 million further tolegislative amendments in the realm of IRES corporate income tax introduced in Italy in relation to the tax treatment of corporate losses,which in the Group resulted in a change in the evaluation of the probability of being able to make use of said tax savings in the future.

At the end of 2011 net profit from continuing operations stood at €43.6 million, equivalent to 9.2% of sales (€27.7 million in 2010),reflecting an increase of 57.5%. Basic earnings per share are up by 56.6% at €0.451 (€0.288 in 2010). No atypical and/or unusualtransactions were carried out in 2011.

Discontinued operations

The capital loss on discontinued operations of €1.1 million, including ancillary expenses associated with the sale, is relative to thedisposal of the investment in Unielectric. Therefore, consolidated net profit totalled 42.6 million euro.

Hydraulic Sector +39.2%32,871

60,664

1,132

Industrial Sector

Other Revenues Sector

Total 94,667

+20.5%

n.s.

+28.0%

14.3%

25.0%

n.s.

20.0%

%ontotal

sales*

* = Total sales also include sales to other Group companies, while the sales analysed previously are exclusively those external to the Group .Therefore, for the purposes of comparability the percentage is calculated on total sales rather than the sales shown earlier.

%ontotal

sales*Growth/

Contraction

23,607

50,347

(16)

73,938

12.4%

23.9%

n.s.

18.5%

2011€/000

2010€/000

27

D I R ECTORS ’ R EMARKS ON PERFORMANCEIN 2011

10.

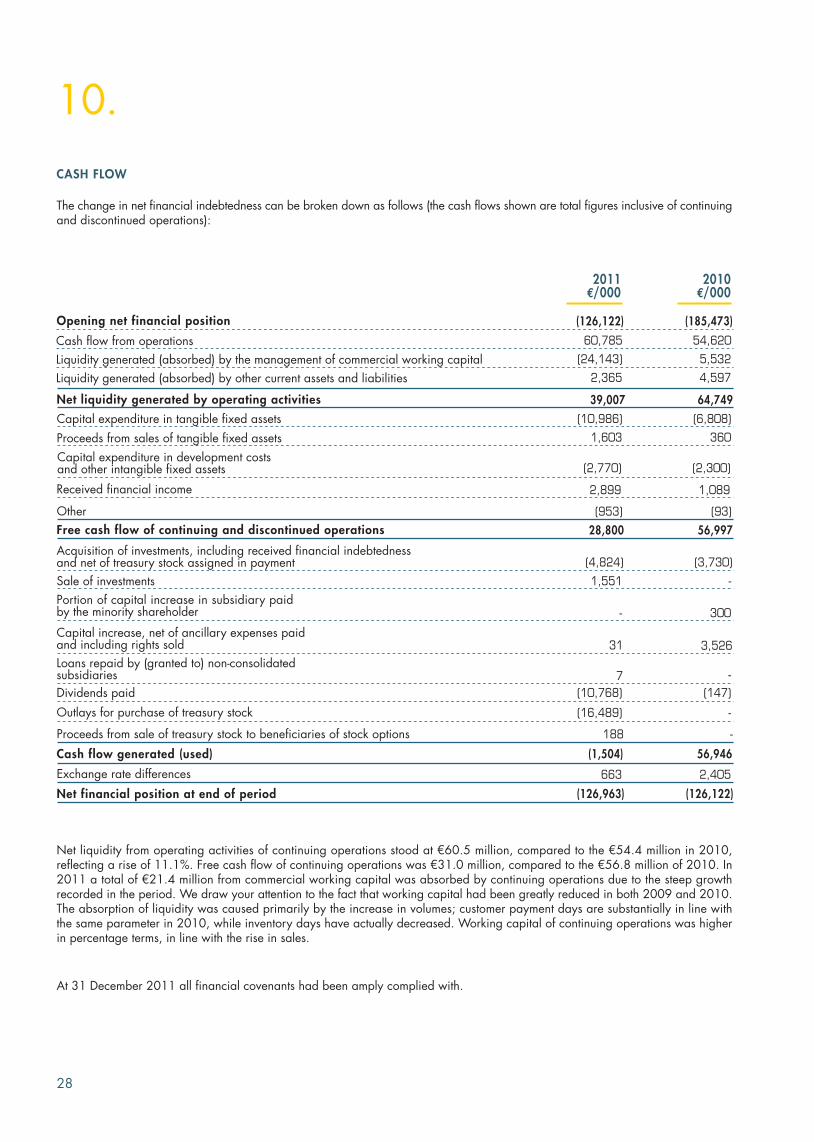

The change in net financial indebtedness can be broken down as follows (the cash flows shown are total figures inclusive of continuingand discontinued operations):

(126,122)Opening net financial position

Capital expenditure in tangible fixed assets

Proceeds from sales of tangible fixed assets

Received financial income

(10,986)

1,603

(2,770)

2,899

Other

Free cash flow of continuing and discontinued operations

Acquisition of investments, including received financial indebtednessand net of treasury stock assigned in payment

Portion of capital increase in subsidiary paidby the minority shareholder

Loans repaid by (granted to) non-consolidatedsubsidiaries

-

(10,768)

Capital expenditure in development costsand other intangible fixed assets

Outlays for purchase of treasury stock

Proceeds from sale of treasury stock to beneficiaries of stock options

Cash flow generated (used)

Exchange rate differences

(1,504)

663

Net financial position at end of period (126,963)

(953)

28,800

188

60,785Cash flow from operations

(24,143)Liquidity generated (absorbed) by the management of commercial working capital

2,365Liquidity generated (absorbed) by other current assets and liabilities

Net liquidity generated by operating activities 39,007

CASH FLOW

(4,824)

2011€/000

2010€/000

Sale of investments 1,551

Capital increase, net of ancillary expenses paidand including rights sold

Dividends paid

(16,489)

(185,473)

(6,808)

360

(2,300)

1,089

300

-

(147)

56,946

2,405

(126,122)

(93)

56,997

-

54,620

5,532

4,597

64,749

(3,730)

-

-

3,52631

7

28

Net liquidity from operating activities of continuing operations stood at €60.5 million, compared to the €54.4 million in 2010,reflecting a rise of 11.1%. Free cash flow of continuing operations was €31.0 million, compared to the €56.8 million of 2010. In2011 a total of €21.4 million from commercial working capital was absorbed by continuing operations due to the steep growthrecorded in the period. We draw your attention to the fact that working capital had been greatly reduced in both 2009 and 2010.The absorption of liquidity was caused primarily by the increase in volumes; customer payment days are substantially in line withthe same parameter in 2010, while inventory days have actually decreased. Working capital of continuing operations was higherin percentage terms, in line with the rise in sales.

At 31 December 2011 all financial covenants had been amply complied with.

10.

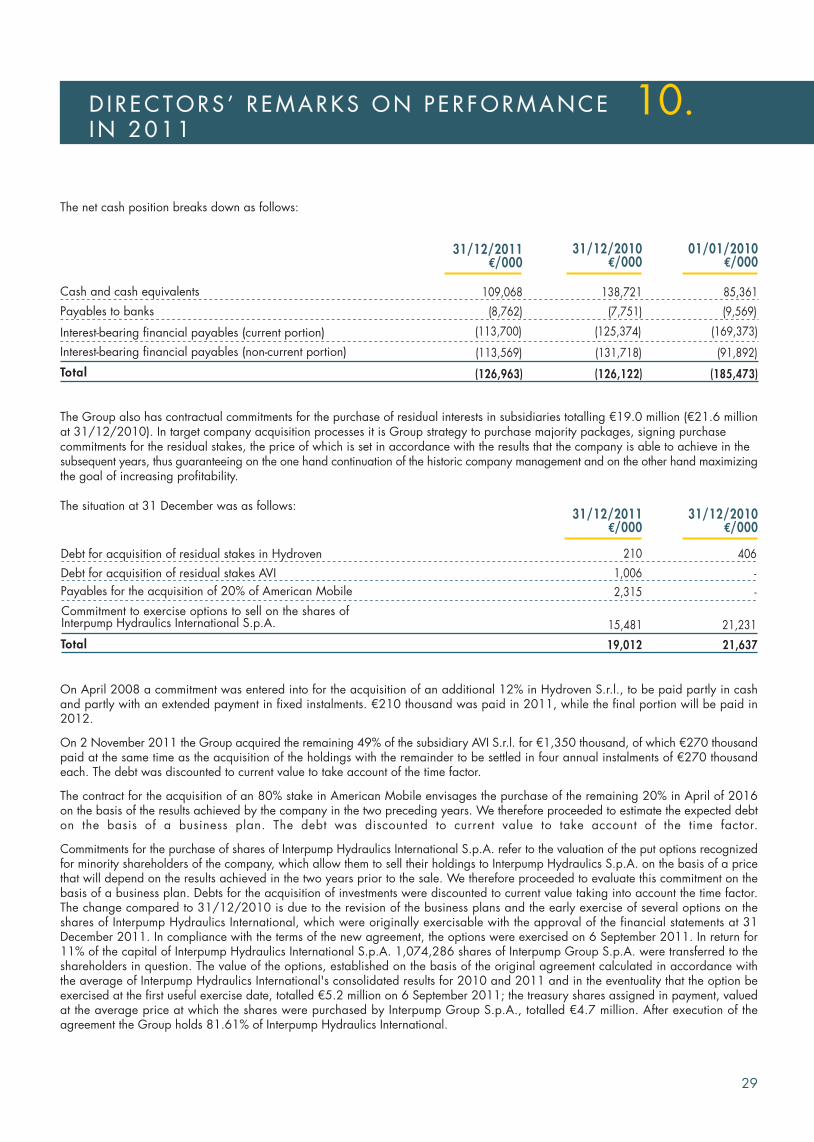

Cash and cash equivalents 109,068

(8,762)

(113,700)

(113,569)

(126,963)

The net cash position breaks down as follows:

The Group also has contractual commitments for the purchase of residual interests in subsidiaries totalling €19.0 million (€21.6 millionat 31/12/2010). In target company acquisition processes it is Group strategy to purchase majority packages, signing purchasecommitments for the residual stakes, the price of which is set in accordance with the results that the company is able to achieve in thesubsequent years, thus guaranteeing on the one hand continuation of the historic company management and on the other hand maximizingthe goal of increasing profitability.

The situation at 31 December was as follows:

On April 2008 a commitment was entered into for the acquisition of an additional 12% in Hydroven S.r.l., to be paid partly in cashand partly with an extended payment in fixed instalments. €210 thousand was paid in 2011, while the final portion will be paid in2012.

On 2 November 2011 the Group acquired the remaining 49% of the subsidiary AVI S.r.l. for €1,350 thousand, of which €270 thousandpaid at the same time as the acquisition of the holdings with the remainder to be settled in four annual instalments of €270 thousandeach. The debt was discounted to current value to take account of the time factor.

The contract for the acquisition of an 80% stake in American Mobile envisages the purchase of the remaining 20% in April of 2016on the basis of the results achieved by the company in the two preceding years. We therefore proceeded to estimate the expected debton the basis of a business plan. The debt was discounted to current value to take account of the time factor.

Commitments for the purchase of shares of Interpump Hydraulics International S.p.A. refer to the valuation of the put options recognizedfor minority shareholders of the company, which allow them to sell their holdings to Interpump Hydraulics S.p.A. on the basis of a pricethat will depend on the results achieved in the two years prior to the sale. We therefore proceeded to evaluate this commitment on thebasis of a business plan. Debts for the acquisition of investments were discounted to current value taking into account the time factor.The change compared to 31/12/2010 is due to the revision of the business plans and the early exercise of several options on theshares of Interpump Hydraulics International, which were originally exercisable with the approval of the financial statements at 31December 2011. In compliance with the terms of the new agreement, the options were exercised on 6 September 2011. In return for11% of the capital of Interpump Hydraulics International S.p.A. 1,074,286 shares of Interpump Group S.p.A. were transferred to theshareholders in question. The value of the options, established on the basis of the original agreement calculated in accordance withthe average of Interpump Hydraulics International's consolidated results for 2010 and 2011 and in the eventuality that the option beexercised at the first useful exercise date, totalled €5.2 million on 6 September 2011; the treasury shares assigned in payment, valuedat the average price at which the shares were purchased by Interpump Group S.p.A., totalled €4.7 million. After execution of theagreement the Group holds 81.61% of Interpump Hydraulics International.

Debt for acquisition of residual stakes in Hydroven

Debt for acquisition of residual stakes AVI

Payables for the acquisition of 20% of American Mobile

Commitment to exercise options to sell on the shares ofInterpump Hydraulics International S.p.A.

Total

1,006

15,481

19,012

406

-

-

21,231

21,637

31/12/2011€/000

85,361

(9,569)

(169,373)

(91,892)

(185,473)

31/12/2010€/000

01/01/2010€/000

138,721

(7,751)

(125,374)

(131,718)

(126,122)

31/12/2011€/000

31/12/2010€/000

210

2,315

Payables to banks

Interest-bearing financial payables (current portion)

Interest-bearing financial payables (non-current portion)

Total

29

D I R ECTORS ’ R EMARKS ON PERFORMANCEIN 2011

10.

Milan, 13 March 2012 For the Board of Directors

Mr. Giovanni Cavallini

Chairman

CAPITAL EXPENDITURE

Expenditure in property, plant and equipment totalled €16.5 million, of which €0.6 million through the acquisition of American Mobile(€9.8 million in 2010). We point out that the companies belonging to the very-high pressure systems segment record machinerymanufactured and hired out to customers under tangible fixed assets (€3.7 million at 31/12/2011 and €2.2 million at 31/12/2010).Net of these latter amounts and expenditure related to the acquisition of equity investments, actual capital expenditure stood at €12.2million in 2011 (€7.6 million at 31/12/2010) and refers to the normal renewal and modernization of plant, machinery and equipment.The difference with respect to the expenditure recorded in the cash flow statement is due to the dynamics of payments.

Increases in intangible fixed assets were €3.8 million, of which €1.0 million through the acquisition of American Mobile (€2.3 millionin 2010), and they mainly refer to expenditure for the development of new products, while the increases of American Mobile are mainlyrelated to the enhancement of the trademark deriving from the acquisition of a line of business.

RESEARCH AND DEVELOPMENT

The Research and Design Centre (Interpump Engineering S.r.l.), set up to centralize design and development of new products in highpressure pumps, hydraulic pumps and hydraulic components, completed a new family of high pressure pumps and a new family ofhydraulic pumps in 2011, in addition to two new valves. There are also several projects currently underway to design new high andvery-high pressure pumps, valves for the industrial sector, and hydraulic pumps. Research and development was conducted primarilywithin Interpump Hydraulics for the Hydraulic Sector and in Hammelmann for very high pressure pumps and systems.

Group strategy over the next few years is to continue with high levels of expenditure in the area of research and development in orderto impart renewed impetus to structured growth. Research costs have been capitalized in accordance with their multi-annual usefulness.The development costs capitalized in 2011 amount to €/000 2,434 (€/000 2,044 in 2010), while the costs charged to the incomestatement were €/000 6,846 (€/000 6,825 in 2010).

31

D I R ECTORS ’ R EMARKS ON PERFORMANCEIN 2011

10.

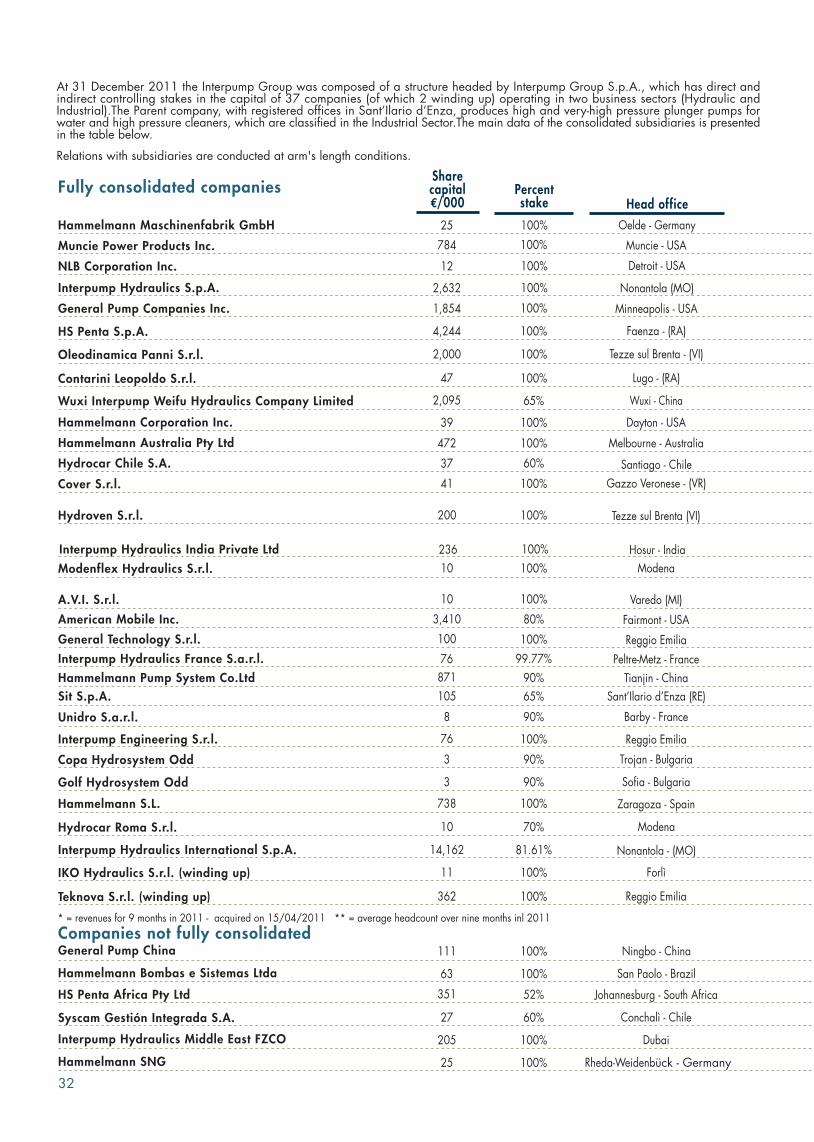

At 31 December 2011 the Interpump Group was composed of a structure headed by Interpump Group S.p.A., which has direct andindirect controlling stakes in the capital of 37 companies (of which 2 winding up) operating in two business sectors (Hydraulic andIndustrial).The Parent company, with registered offices in Sant’Ilario d’Enza, produces high and very-high pressure plunger pumps forwater and high pressure cleaners, which are classified in the Industrial Sector.The main data of the consolidated subsidiaries is presentedin the table below.

Relations with subsidiaries are conducted at arm's length conditions.

100%Muncie Power Products Inc. 784 Muncie - USA

General Pump Companies Inc.

Hammelmann Maschinenfabrik GmbH

Hydroven S.r.l.

Hammelmann Australia Pty Ltd

A.V.I. S.r.l.

Sit S.p.A.

Wuxi Interpump Weifu Hydraulics Company Limited

Hydrocar Chile S.A.

Interpump Hydraulics France S.a.r.l.

Contarini Leopoldo S.r.l.

Interpump Hydraulics International S.p.A.

Hammelmann S.L.

General Technology S.r.l.

Unidro S.a.r.l.

Interpump Engineering S.r.l.

25

1,854

200

472

10

37

2,095

105

76

14,162

47

738

100

76

8

100%

100%

100%

100%

100%

60%

65%

65%

99.77%

81.61%

100%

100%

100%

100%

90%

Minneapolis - USA

Oelde - Germany

Tezze sul Brenta (VI)

Melbourne - Australia

Varedo (MI)

Sant’Ilario d’Enza (RE)

Wuxi - China

Santiago - Chile

Peltre-Metz - France

Lugo - (RA)

Nonantola - (MO)

Zaragoza - Spain

Reggio Emilia

Reggio Emilia

Barby - France

* = revenues for 9 months in 2011 - acquired on 15/04/2011 ** = average headcount over nine months inl 2011

100%Interpump Hydraulics S.p.A. 2,632 Nonantola (MO)

Hammelmann Corporation Inc. 39 100% Dayton - USA

Interpump Hydraulics India Private Ltd 236 100% Hosur - India

Fully consolidated companies

Hydrocar Roma S.r.l. 10 70% Modena

NLB Corporation Inc. 12 100% Detroit - USA

Hammelmann Pump System Co.Ltd 871 90% Tianjin - China

Copa Hydrosystem Odd 3 90% Trojan - Bulgaria

Modenflex Hydraulics S.r.l. 10 100% Modena

IKO Hydraulics S.r.l. (winding up) 11 100% Forlì

Companies not fully consolidated

Syscam Gestión Integrada S.A.

HS Penta Africa Pty Ltd 351

27

52%

60%

Johannesburg - South Africa

Conchalì - Chile

Hammelmann Bombas e Sistemas Ltda 63 100% San Paolo - Brazil

Interpump Hydraulics Middle East FZCO 205 100% Dubai

HS Penta S.p.A. 4,244 100% Faenza - (RA)

Cover S.r.l. 41 100% Gazzo Veronese - (VR)

Oleodinamica Panni S.r.l. 2,000 100% Tezze sul Brenta - (VI)

Golf Hydrosystem Odd 3 90% Sofia - Bulgaria

General Pump China 111 100% Ningbo - China

Sharecapital€/000

Percentstake Head office

American Mobile Inc. 3,410 80% Fairmont - USA

Teknova S.r.l. (winding up) 362 100% Reggio Emilia

Hammelmann SNG 25 100% Rheda-Weidenbück - Germany

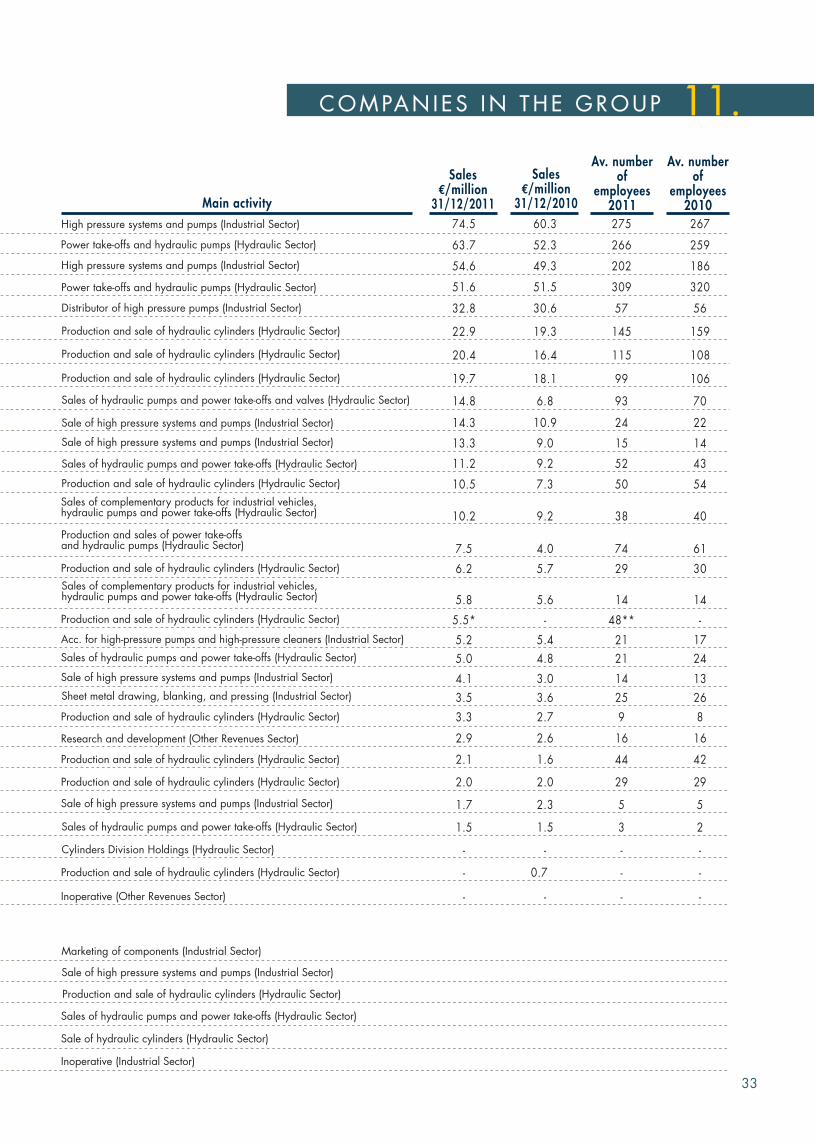

32

266

202

309

145

115

99

93

52

50

74

14

21

29

15

25

16

63.7

54.6

51.6

22.9

20.4

19.7

14.8

11.2

10.5

7.5

5.8

5.2

6.2

13.3

3.5

2.9

Power take-offs and hydraulic pumps (Hydraulic Sector)

Distributor of high pressure pumps (Industrial Sector)

High pressure systems and pumps (Industrial Sector)

Sales of complementary products for industrial vehicles,hydraulic pumps and power take-offs (Hydraulic Sector)

Sale of high pressure systems and pumps (Industrial Sector)

Sales of complementary products for industrial vehicles,hydraulic pumps and power take-offs (Hydraulic Sector)

Sheet metal drawing, blanking, and pressing (Industrial Sector)

Sales of hydraulic pumps and power take-offs (Hydraulic Sector)

Sales of hydraulic pumps and power take-offs and valves (Hydraulic Sector)

Sales of hydraulic pumps and power take-offs (Hydraulic Sector)

Production and sale of hydraulic cylinders (Hydraulic Sector)

Cylinders Division Holdings (Hydraulic Sector)

Sale of high pressure systems and pumps (Industrial Sector)

Acc. for high-pressure pumps and high-pressure cleaners (Industrial Sector)

Research and development (Other Revenues Sector)

Production and sale of hydraulic cylinders (Hydraulic Sector)

27574.5

Power take-offs and hydraulic pumps (Hydraulic Sector)

2414.3Sale of high pressure systems and pumps (Industrial Sector)

Production and sales of power take-offsand hydraulic pumps (Hydraulic Sector)

3810.2

144.1

Sales of hydraulic pumps and power take-offs (Hydraulic Sector)

5732.8

High pressure systems and pumps (Industrial Sector)

93.3

Sale of high pressure systems and pumps (Industrial Sector)

442.1Production and sale of hydraulic cylinders (Hydraulic Sector)

51.7

Production and sale of hydraulic cylinders (Hydraulic Sector)

31.5

Production and sale of hydraulic cylinders (Hydraulic Sector)

--

Production and sale of hydraulic cylinders (Hydraulic Sector)

Sales of hydraulic pumps and power take-offs (Hydraulic Sector)

Sale of high pressure systems and pumps (Industrial Sector)

Sale of hydraulic cylinders (Hydraulic Sector)

48**5.5*

Production and sale of hydraulic cylinders (Hydraulic Sector)

215.0

Production and sale of hydraulic cylinders (Hydraulic Sector)

Production and sale of hydraulic cylinders (Hydraulic Sector)

292.0Production and sale of hydraulic cylinders (Hydraulic Sector)

259

186

320

159

108

106

70

43

54

61

14

17

30

14

26

16

267

22

40

13

56

8

42

5

2

-

-

24

29

52.3

49.3

51.5

19.3

16.4

18.1

6.8

9.2

7.3

4.0

5.6

5.4

5.7

9.0

3.6

2.6

60.3

10.9

9.2

3.0

30.6

2.7

1.6

2.3

1.5

-

-

4.8

2.0

Marketing of components (Industrial Sector)

Main activity

Sales€/million

31/12/2011

Av. numberof

employees2011

Av. numberof

employees2010

Production and sale of hydraulic cylinders (Hydraulic Sector)

--

Inoperative (Other Revenues Sector)

-

Inoperative (Industrial Sector)

Sales€/million

31/12/2010

--- -

0.7

33

COMPAN IES IN THE GROUP 11.

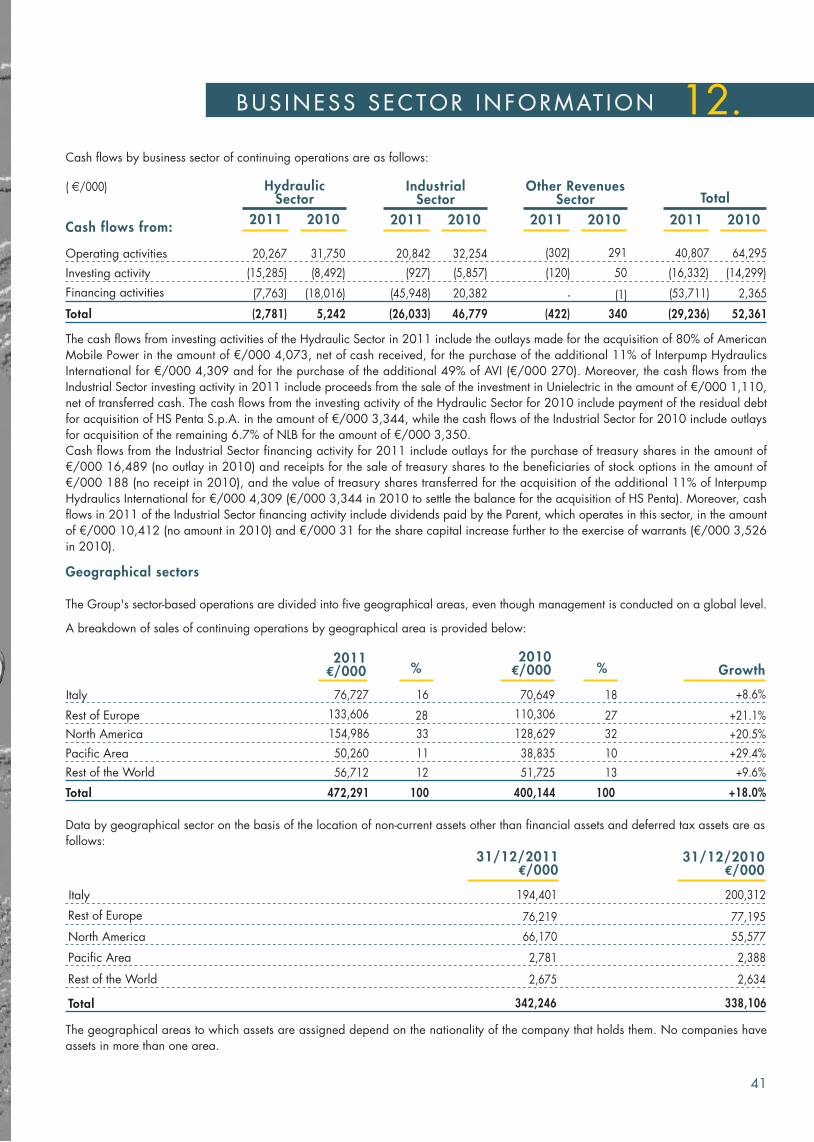

Business sector information is supplied with reference to operating sectors. We also present the information required by IFRS bygeographical area. Information on operating sectors reflects the Group’s internal reporting structure.

The value of components and products transferred between sectors is generally the effective sales price between Group companiesand corresponds to the best customer sale prices.

Sector information includes directly attributable costs and costs allocated on the basis of reasonable estimates. The holding costs(remuneration of directors, auditors and functions of the Group's financial management, control and internal auditing, and also consultancycosts and other related costs) were ascribed to the sectors on the basis of sales.

BUSINESS SECTORS

The Group is composed of the following business sectors:

Hydraulic Sector

. Mainly composed of high and very high-pressure pumps and pumping systems used in a wide range of industrial sectors for theconveyance of fluids. High-pressure plunger pumps are the main component of professional high-pressure washers. These pumps arealso utilized for a broad range of industrial applications including car wash installations, forced lubrication systems for machine tools,and inverse osmosis systems for water desalination plants. Very high-pressure pumps and systems are used for cleaning surfaces, ships,various types of pipes, and also for removing machining burr, cutting and removing cement, asphalt, and paint coatings from stone,cement and metal surfaces, and for cutting solid materials. Marginally, this sector also includes operations of drawing, shearing andpressing sheet metal and the manufacture and sale of cleaning machinery.

Industrial Sector

Includes the production and sale of power take-offs, hydraulic cylinders, pumps, and other hydraulic components. Power take-offs aremechanical devices designed to transmit drive from an industrial vehicle engine or transmission to power a range of ancillary servicesthrough hydraulic components. These products, combined with other hydraulic components (spool valves, controls, etc.) allow theexecution of special functions such as lifting tipping bodies, moving truck-mounted cranes, operating mixer truck drums, and so forth.Hydraulic cylinders are components of the hydraulic system of various vehicle types, utilized in a wide range of applications dependingon the type. Front-end and underbody cylinders (single acting) are utilized mainly on industrial vehicles in the construction sector, whiledouble acting cylinders are utilized in a range of applications: earthmoving machinery, agricultural machinery, cranes and truck cranes,waste compactors, etc.

35

BUS INESS SECTOR INFORMAT ION 12.

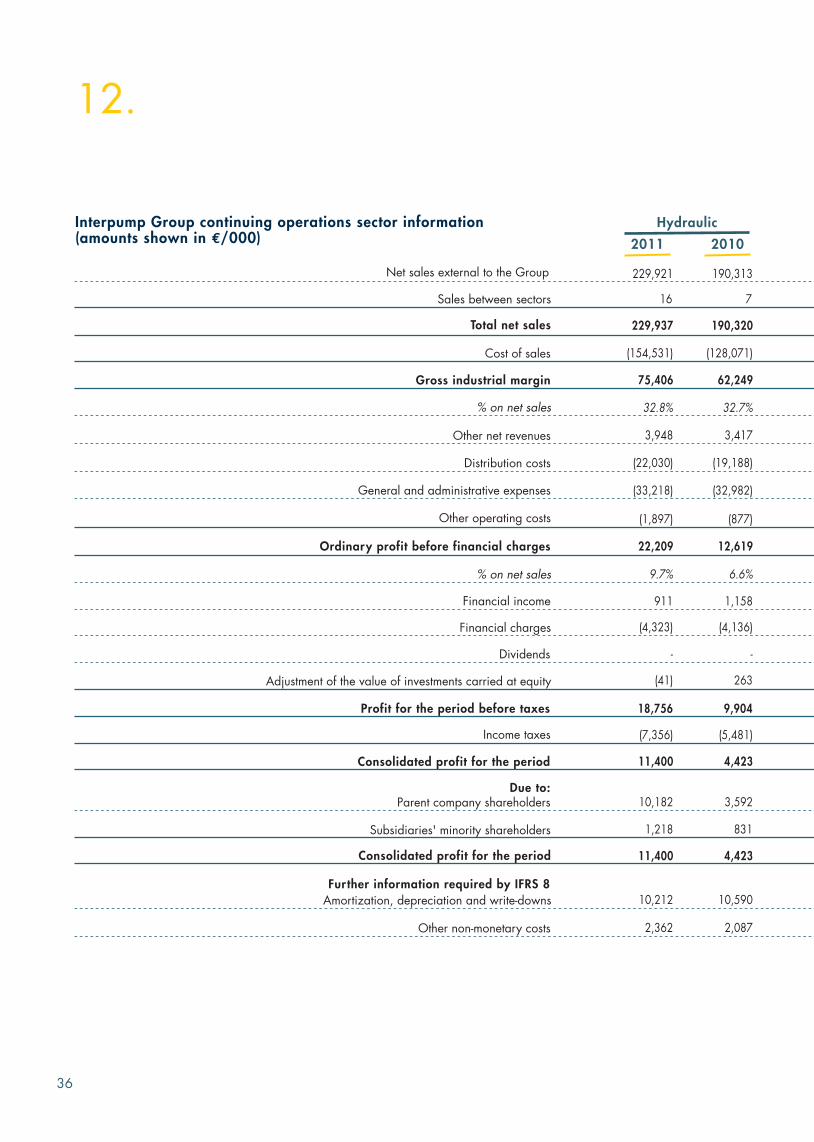

Net sales external to the Group

Sales between sectors

Total net sales

% on net sales

Cost of sales

Gross industrial margin

Other net revenues

Distribution costs

Other operating costs

Ordinary profit before financial charges

% on net sales

Financial income

Dividends

Adjustment of the value of investments carried at equity

Profit for the period before taxes

Income taxes

Consolidated profit for the period

Due to:Parent company shareholders

Subsidiaries' minority shareholders

Consolidated profit for the period

General and administrative expenses

229,921

229,937

(154,531)

75,406

32.8%

3,948

(22,030)

(33,218)

(1,897)

22,209

(41)

18,756

9.7%

Hydraulic

2011 2010

Financial charges

Further information required by IFRS 8Amortization, depreciation and write-downs

Other non-monetary costs

16

911

(4,323)

-

(7,356)

11,400

10,182

1,218

11,400

10,212

2,362

190,313

190,320

(128,071)

62,249

32.7%

3,417

(19,188)

(32,982)

(877)

12,619

263

9,904

6.6%

7

1,158

(4,136)

-

(5,481)

4,423

3,592

831

4,423

10,590

2,087

36

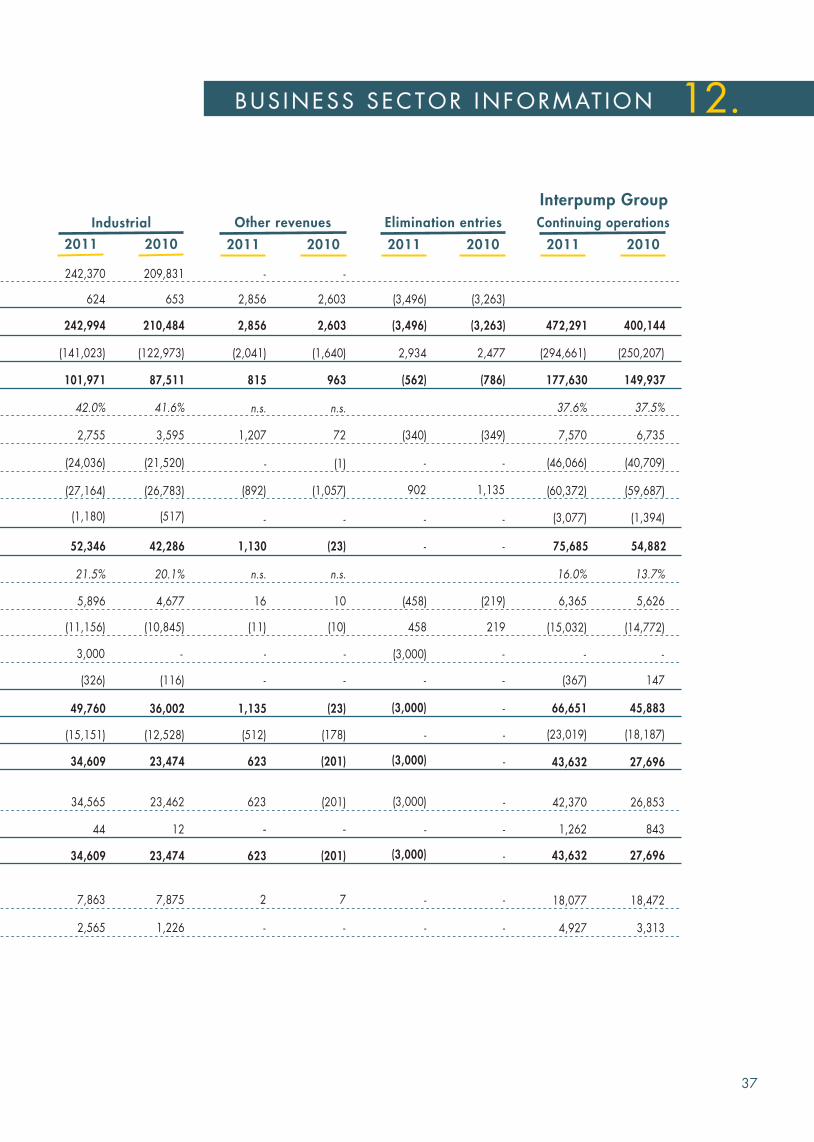

Interpump Group continuing operations sector information(amounts shown in €/000)

12.

472,291

(294,661)

177,630

37.6%

7,570

(46,066)

(3,077)

75,685

(367)

16.0%

6,365

-

66,651

(23,019)

43,632

42,370

1,262

43,632

(60,372)

(3,496)

(3,496)

2,934

(562)

(340)

-

-

-

-

902

-

2,856

2,856

(2,041)

815

n.s.

1,207

-

1,130

-

1,135

n.s.

(892)

242,370

624

242,994

(141,023)

101,971

42.0%

2,755

(24,036)

(1,180)

52,346

(326)

49,760

21.5%

(27,164)

Industrial

2011 2010 2011 2010

Other revenues

2011 2010

Elimination entries

2011 2010

Interpump Group

(15,032)

18,077

4,927

5,896

(11,156)

3,000

16

(11)

-

(458)

458

(15,151)

34,609

34,565

44

34,609

7,863

2,565

(512)

623

623

-

623

2

-

-

-

-

-

-

209,831

653

210,484

(122,973)

87,511

41.6%

3,595

(21,520)

(517)

42,286

(116)

36,002

20.1%

(26,783)

4,677

(10,845)

-

(12,528)

23,474

23,462

12

23,474

7,875

1,226

-

2,603

2,603

(1,640)

963

n.s.

72

-

(23)

-

(23)

n.s.

(1,057)

10

(10)

-

(178)

(201)

(201)

-

(201)

7

-

(1)

(3,263)

(3,263)

2,477

(786)

(349)

-

-

-

-

1,135

(219)

219

-

-

-

-

-

-

-

-

-

(3,000)

(3,000)

(3,000)

(3,000)

(3,000)

400,144

(250,207)

149,937

37.5%

6,735

(40,709)

(1,394)

54,882

147

13.7%

5,626

-

45,883

(18,187)

27,696

26,853

843

27,696

(59,687)

(14,772)

18,472

3,313

Continuing operations

37

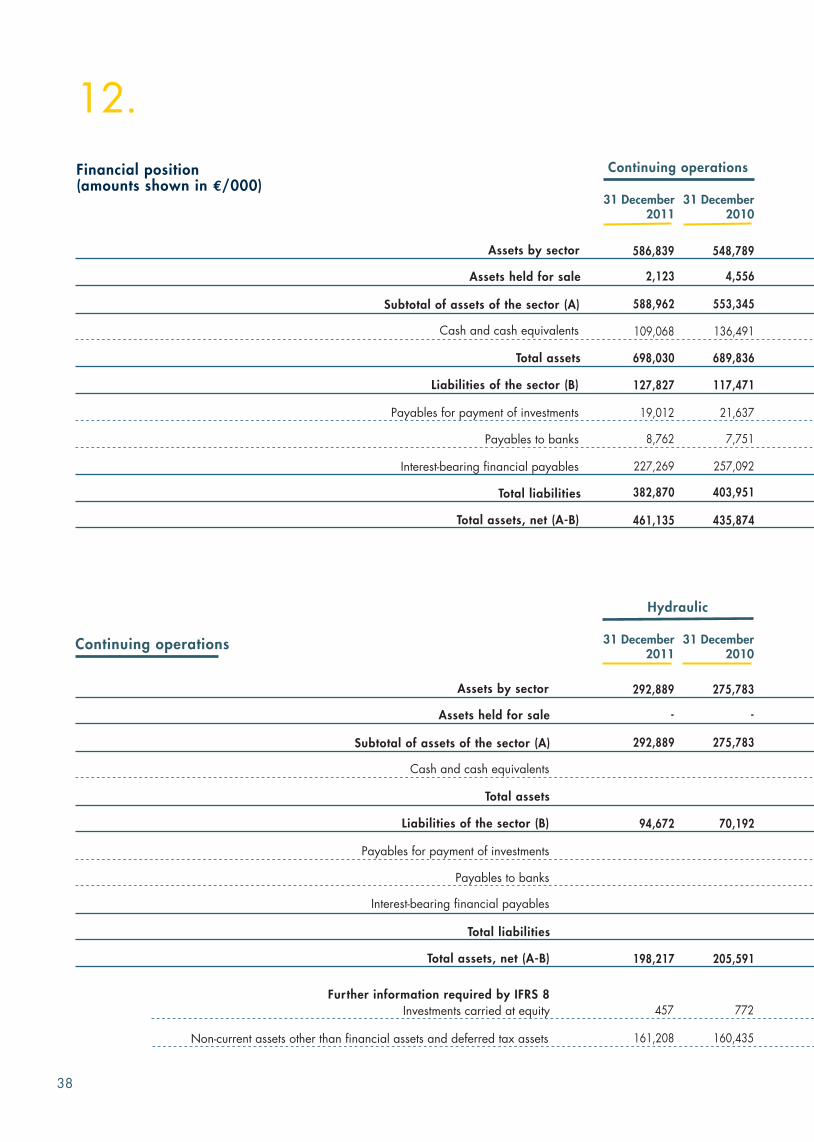

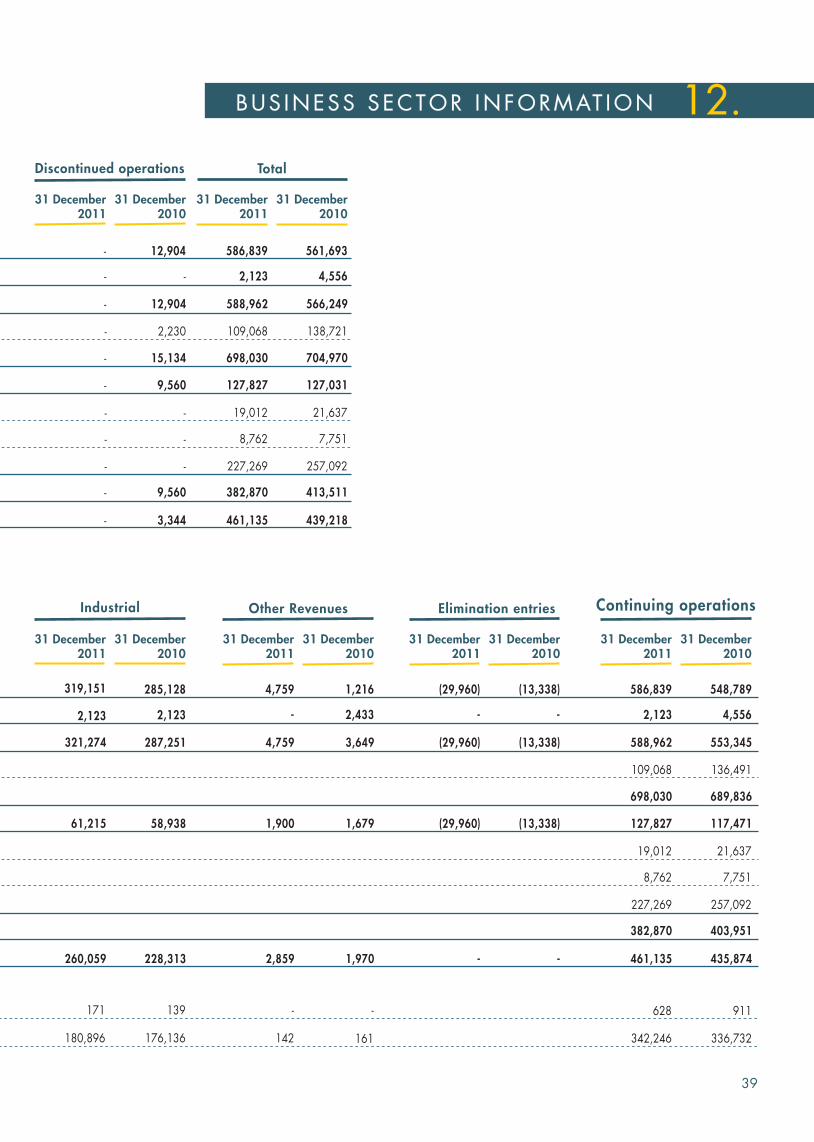

BUS INESS SECTOR INFORMAT ION 12.

Hydraulic

31 December2011

Assets by sector

Assets held for sale

Cash and cash equivalents

Liabilities of the sector (B)

Total assets

Payables to banks

Total liabilities

Interest-bearing financial payables

-

94,672

Payables for payment of investments

Subtotal of assets of the sector (A)

Total assets, net (A-B)

292,889

198,217

31 December2010

292,889

-

70,192

275,783

205,591

275,783

Further information required by IFRS 8Investments carried at equity

Non-current assets other than financial assets and deferred tax assets

457

161,208

772

160,435

Continuing operations

31 December2011

Assets by sector

Assets held for sale

Cash and cash equivalents

Liabilities of the sector (B)

Total assets

Payables to banks

Total liabilities

Interest-bearing financial payables

2,123

127,827

Payables for payment of investments

Subtotal of assets of the sector (A)

Total assets, net (A-B)

588,962

461,135

31 December2010

586,839

698,030

109,068

19,012

8,762

227,269

382,870

4,556

117,471

553,345

435,874

548,789

689,836

136,491

21,637

7,751

257,092

403,951

12.

Continuing operations

38

Financial position(amounts shown in €/000)

Other RevenuesIndustrial

31 December2011

31 December2010

31 December2011

31 December2010

58,938

287,251

228,313

285,128

-

1,900

4,759

2,859

4,759

2,433

1,679

3,649

1,970

1,216

Elimination entries

31 December2011

31 December2010