Embed Size (px)

Citation preview

1

SYNOPSIS

� The Housing Development Finance

Corporation Ltd. (HDFC) was

amongst the first to receive an ‘in

principle’ approval from the RBI to set

up a bank in the private sector.

� Bank’s Capital Adequacy Ratio

registered at 16.50% as on 31.03.12.

� Net Income and PAT of the company

are expected to grow at a CAGR of

25% and 22% over 2011 to 2014E

respectively.

� HDFC Bank Ltd has recommended a

dividend of Rs. 4.30 per equity share

of Rs. 2/- each (i.e. 215%) out of the

net profits for the year ended March

31, 2012.

� HDFC Bank has approved sub-

division (split) of one equity share of

the Bank from nominal value of Rs.

10/- each into five equity shares of

nominal value of Rs. 2/- each.

Years Net Income Operating profit Net Profit EPS P/E

FY 12 272863.50 175404.60 51670.70 22.02 24.75

FY 13E 330164.84 205846.88 62004.01 26.42 20.63

FY 14E 389594.51 238548.62 71808.00 30.60 17.81

Stock Data:

Sector: Banking

Face Value Rs. 10.00

52 wk. High/Low (Rs.) 557.70/400.45

Volume (2 wk. Avg.) 159000

BSE Code 500180

Market Cap (Rs.In mn) 1278951.50

Share Holding Pattern

1 Year Comparative Graph

HDFC Bank BSE SENSEX

C.M.P: Rs. 545.00 Target Price: Rs. 606.00 Date: June 15th, 2012 BUY

HDFC Bank Ltd. Result Update: Q4 FY 12

2

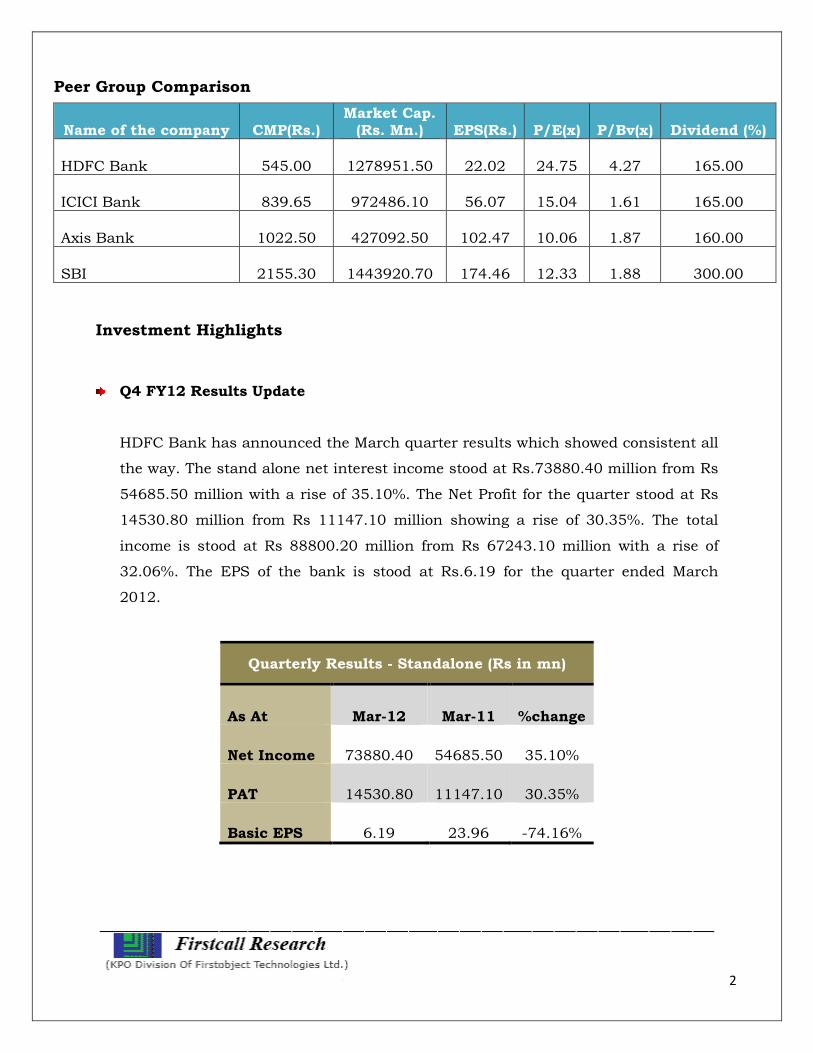

Peer Group Comparison

Name of the company CMP(Rs.) Market Cap.

(Rs. Mn.) EPS(Rs.) P/E(x) P/Bv(x) Dividend (%)

HDFC Bank 545.00 1278951.50 22.02 24.75 4.27 165.00

ICICI Bank 839.65 972486.10 56.07 15.04 1.61 165.00

Axis Bank 1022.50 427092.50 102.47 10.06 1.87 160.00

SBI 2155.30 1443920.70 174.46 12.33 1.88 300.00

Investment Highlights

Q4 FY12 Results Update

HDFC Bank has announced the March quarter results which showed consistent all

the way. The stand alone net interest income stood at Rs.73880.40 million from Rs

54685.50 million with a rise of 35.10%. The Net Profit for the quarter stood at Rs

14530.80 million from Rs 11147.10 million showing a rise of 30.35%. The total

income is stood at Rs 88800.20 million from Rs 67243.10 million with a rise of

32.06%. The EPS of the bank is stood at Rs.6.19 for the quarter ended March

2012.

Quarterly Results - Standalone (Rs in mn)

As At Mar-12 Mar-11 %change

Net Income 73880.40 54685.50 35.10%

PAT 14530.80 11147.10 30.35%

Basic EPS 6.19 23.96 -74.16%

3

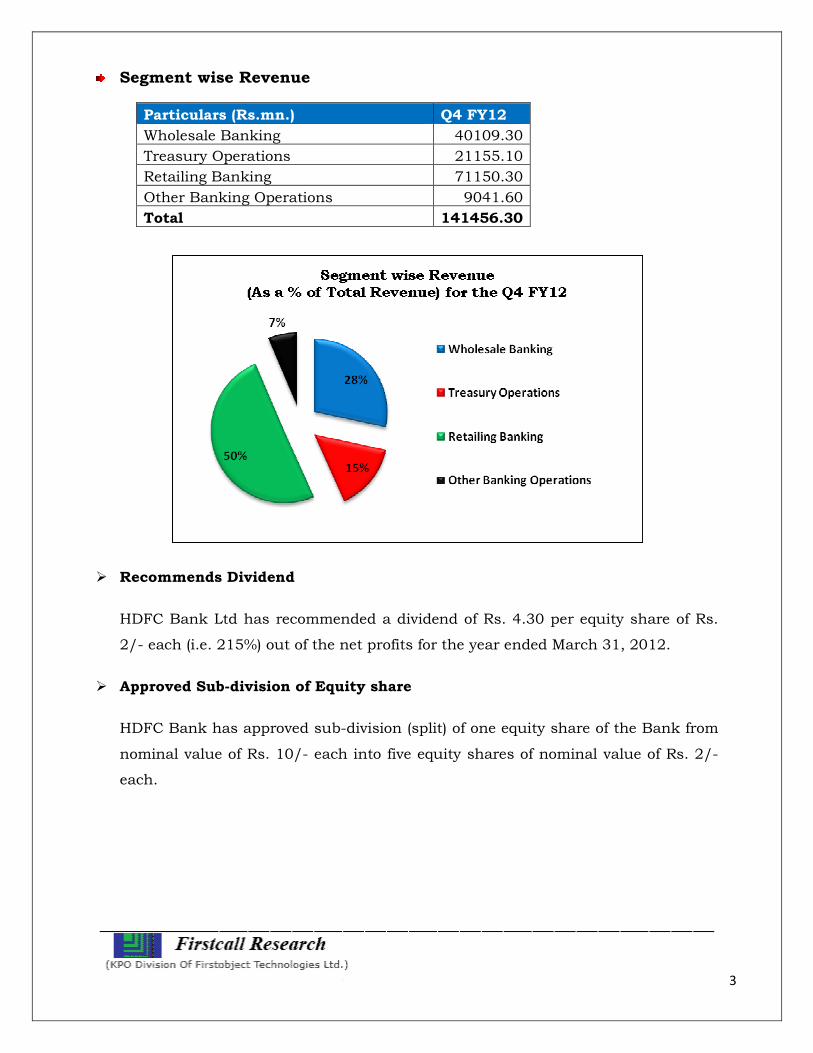

Segment wise Revenue

Particulars (Rs.mn.) Q4 FY12

Wholesale Banking 40109.30

Treasury Operations 21155.10

Retailing Banking 71150.30

Other Banking Operations 9041.60

Total 141456.30

� Recommends Dividend

HDFC Bank Ltd has recommended a dividend of Rs. 4.30 per equity share of Rs.

2/- each (i.e. 215%) out of the net profits for the year ended March 31, 2012.

� Approved Sub-division of Equity share

HDFC Bank has approved sub-division (split) of one equity share of the Bank from

nominal value of Rs. 10/- each into five equity shares of nominal value of Rs. 2/-

each.

4

Company Profile

The Housing Development Finance Corporation Ltd. (HDFC) was amongst the first to

receive an ‘in principle’ approval from the RBI to set up a bank in the private sector, as

part of the RBI’s liberalisation of the Indian Banking Indian Banking Industry in 1994.

The bank was incorporated in August 1994 in the name of “HDFC Bank Ltd with its

registered office in Mumbai, India. HDFC Bank commenced operations as a Scheduled

Commercial Bank in January 1995. The bank has a network of 2,544 branches and

8,913 ATMs in 1,399 cities as on March 31, 2012.

Products & services

� Personal Banking

� Accounts & deposits:

Savings Accounts, Salary Accounts, Current Accounts, Deposits, Demat Account,

Safe Deposit Locker & Rural Accounts.

� Loans:

Personal Loans, Home Loan, Car Loans, Two wheeler loans, Loans against Assets,

Educational Loan, Government Sponsored Programs & Rural Loans.

� Cards:

Business Platinum Credit Card and Business Gold Credit Card

� Investments:

Wealth Services and Investment Products.

� Insurance:

Life Insurance, Health Insurance, Motor Insurance, Travel Insurance and Home

Insurance.

� FOREX:

Travel solutions, Remittance Products and Other Forex Services.

5

� Premium Banking:

Imperia Banking, Preferred Banking & Classic Banking

� Private Banking

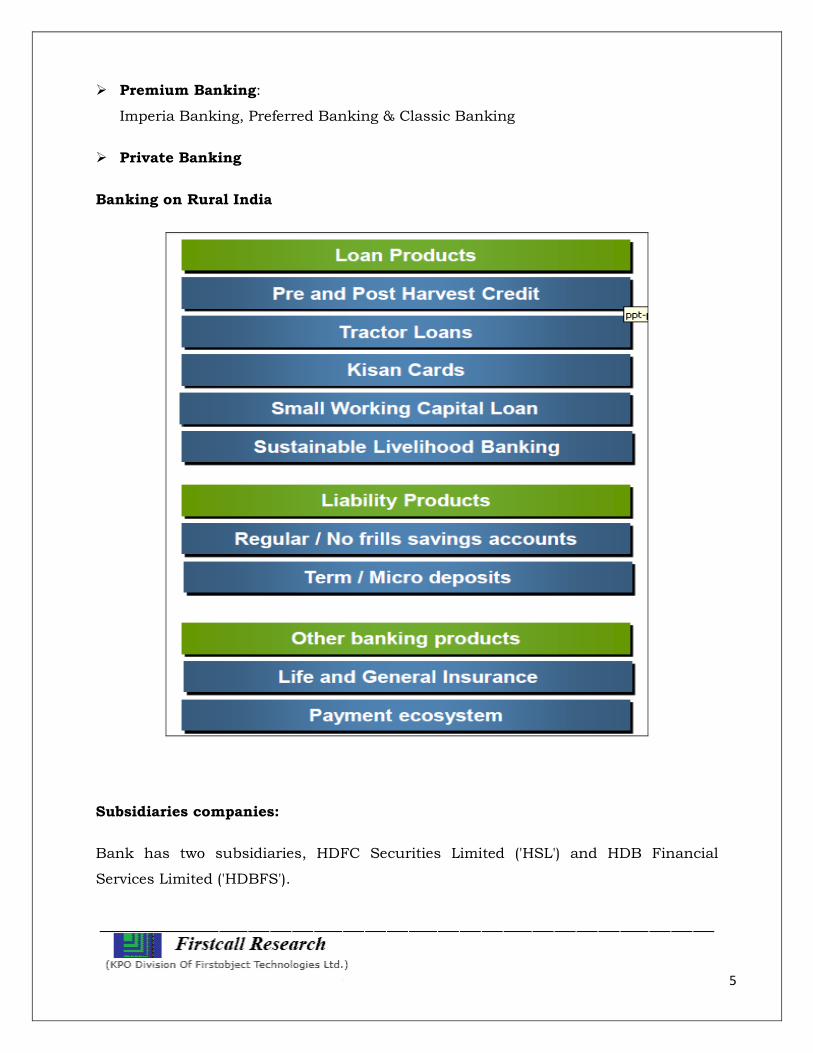

Banking on Rural India

Subsidiaries companies:

Bank has two subsidiaries, HDFC Securities Limited ('HSL') and HDB Financial

Services Limited ('HDBFS').

6

� HDFC Securities Limited ('HSL')

HSL is primarily in the business of providing brokerage services through the

internet and other channels with a focus to emerge as a full-fledged financial

services provider offering a bouquet of financial services along with the core

broking product. The company continued to strengthen its distribution franchise

and as on March 31, 2012 has a network of 180 branches across the country

catering to the needs of its 1.4 million customers.

� HDB Financial Services Limited ('HDBFS')

HDBFS is a non-deposit taking non-bank finance company ('NBFC'); the customer

segments being addressed by HDBFS are typically underserviced by the larger

commercial banks, and thus create a profitable niche for the company to operate.

Apart from lending to individuals, the company grants loans to small and medium

business enterprises and micro small and medium enterprises.

7

Financial Results

12 Months Ended Profit & Loss Account (Standalone)

Value(Rs.in.mn) FY11 FY12 FY13E FY 14E

Description 12m 12m 12m 12m

Net Income 199282.10 272863.50 330164.84 389594.51

Other Income 43351.50 52436.90 59253.70 65179.07

Total income 242633.60 325300.40 389418.53 454773.57

Interest Expended -93850.80 -149895.80 -183571.65 -216224.95

Net Interest Income 148782.80 175404.60 205846.88 238548.62

Operating Expenses -71529.20 -85900.60 -102351.10 -120189.90

Operating Profit 77253.60 89504.00 103495.78 118358.72

Provisions & Contingencies -19067.10 -14372.50 -13764.94 -14439.76

Profit Before Tax 58186.50 75131.50 89730.85 103918.95

Tax -18922.60 -23460.80 -27726.83 -32110.96

Profit After Tax 39263.90 51670.70 62004.01 71808.00

Equity Capital 4652.30 4693.40 4693.40 4693.40

Reserves 249111.30 294550.40 356554.41 428362.41

Face Value (Rs.) 10.00 2.00 2.00 2.00

EPS 84.40 22.02 26.42 30.60

8

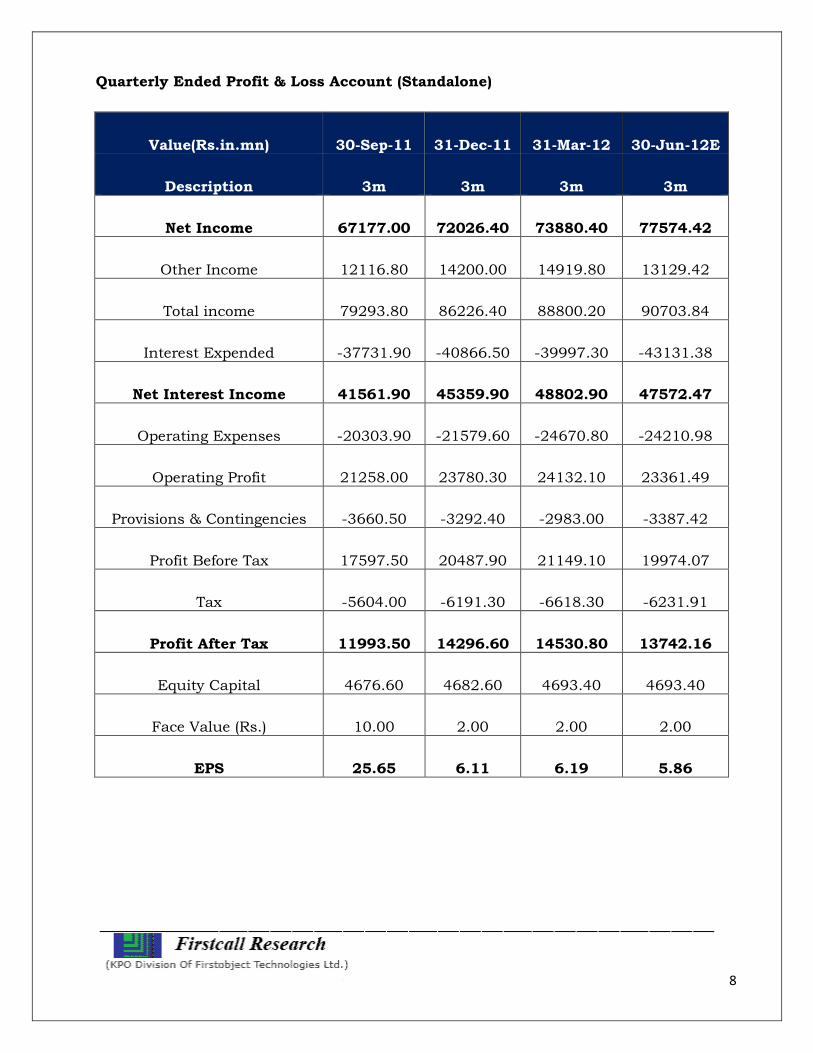

Quarterly Ended Profit & Loss Account (Standalone)

Value(Rs.in.mn) 30-Sep-11 31-Dec-11 31-Mar-12 30-Jun-12E

Description 3m 3m 3m 3m

Net Income 67177.00 72026.40 73880.40 77574.42

Other Income 12116.80 14200.00 14919.80 13129.42

Total income 79293.80 86226.40 88800.20 90703.84

Interest Expended -37731.90 -40866.50 -39997.30 -43131.38

Net Interest Income 41561.90 45359.90 48802.90 47572.47

Operating Expenses -20303.90 -21579.60 -24670.80 -24210.98

Operating Profit 21258.00 23780.30 24132.10 23361.49

Provisions & Contingencies -3660.50 -3292.40 -2983.00 -3387.42

Profit Before Tax 17597.50 20487.90 21149.10 19974.07

Tax -5604.00 -6191.30 -6618.30 -6231.91

Profit After Tax 11993.50 14296.60 14530.80 13742.16

Equity Capital 4676.60 4682.60 4693.40 4693.40

Face Value (Rs.) 10.00 2.00 2.00 2.00

EPS 25.65 6.11 6.19 5.86

9

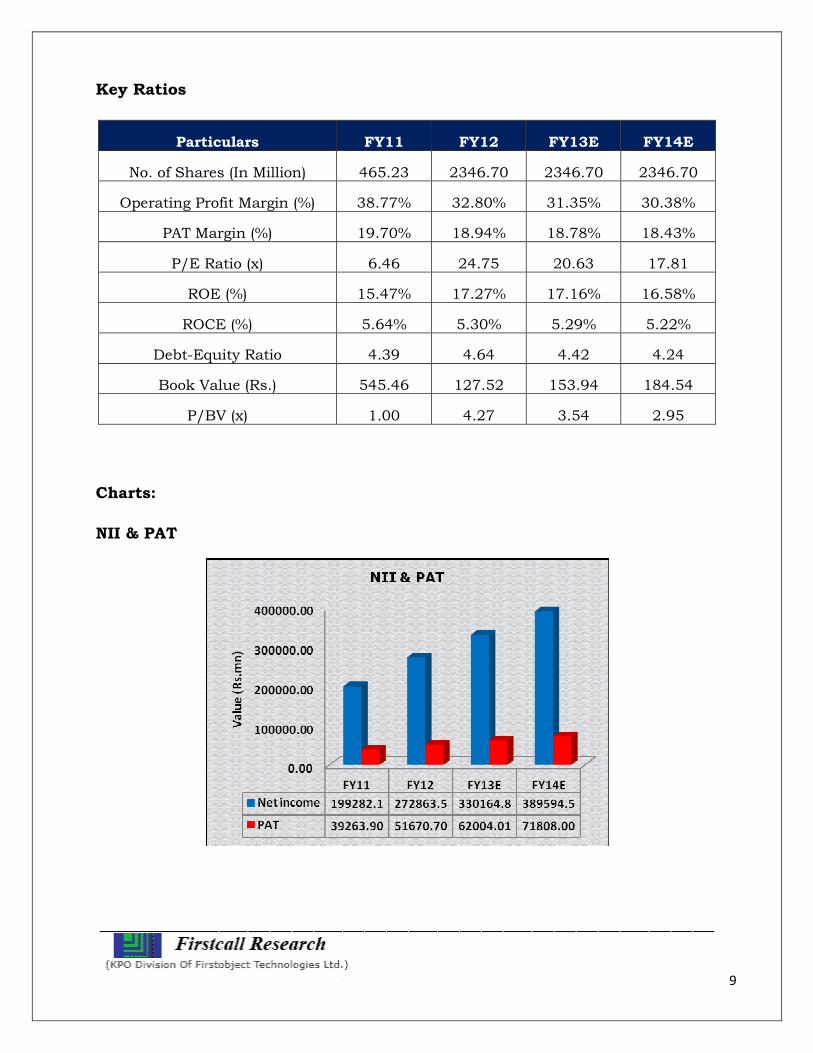

Key Ratios

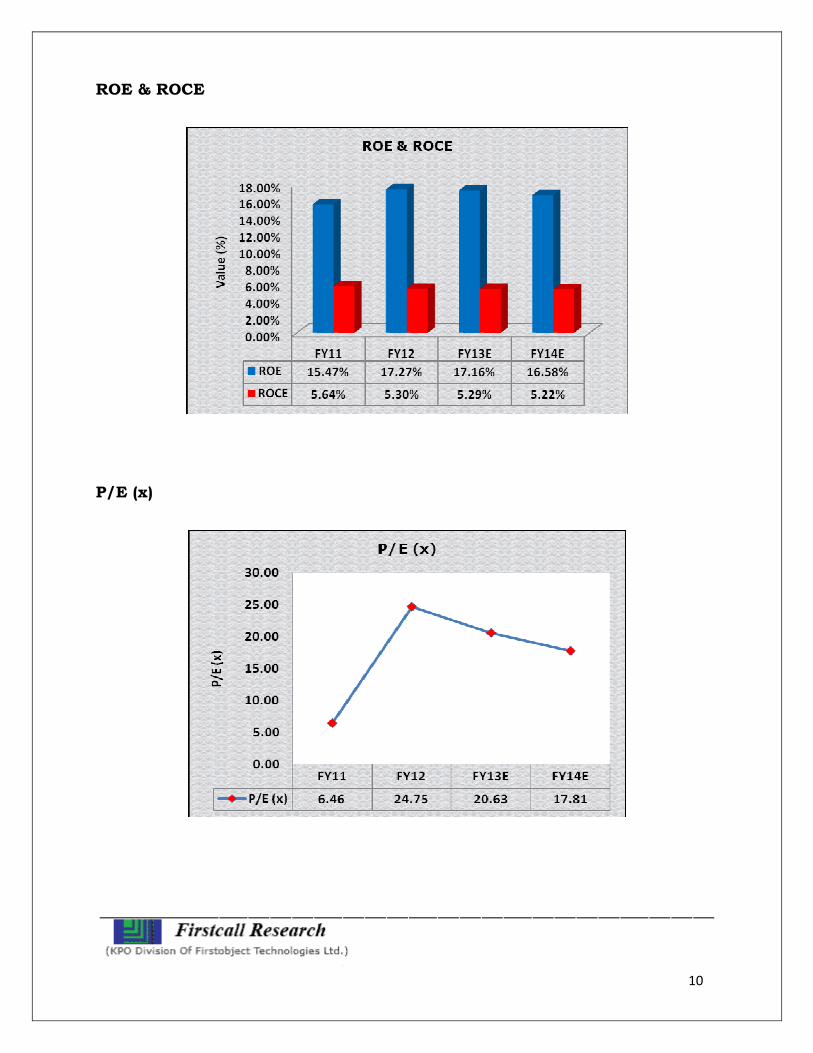

Particulars FY11 FY12 FY13E FY14E

No. of Shares (In Million) 465.23 2346.70 2346.70 2346.70

Operating Profit Margin (%) 38.77% 32.80% 31.35% 30.38%

PAT Margin (%) 19.70% 18.94% 18.78% 18.43%

P/E Ratio (x) 6.46 24.75 20.63 17.81

ROE (%) 15.47% 17.27% 17.16% 16.58%

ROCE (%) 5.64% 5.30% 5.29% 5.22%

Debt-Equity Ratio 4.39 4.64 4.42 4.24

Book Value (Rs.) 545.46 127.52 153.94 184.54

P/BV (x) 1.00 4.27 3.54 2.95

Charts:

NII & PAT

10

ROE & ROCE

P/E (x)

11

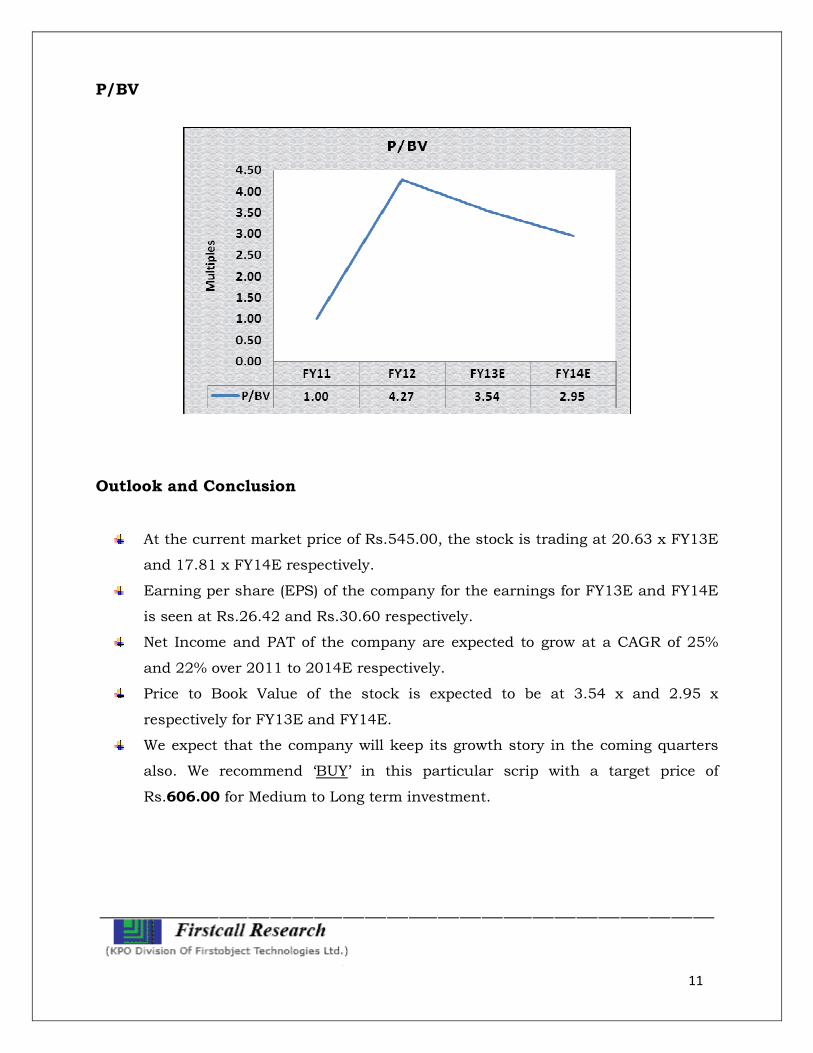

P/BV

Outlook and Conclusion

At the current market price of Rs.545.00, the stock is trading at 20.63 x FY13E

and 17.81 x FY14E respectively.

Earning per share (EPS) of the company for the earnings for FY13E and FY14E

is seen at Rs.26.42 and Rs.30.60 respectively.

Net Income and PAT of the company are expected to grow at a CAGR of 25%

and 22% over 2011 to 2014E respectively.

Price to Book Value of the stock is expected to be at 3.54 x and 2.95 x

respectively for FY13E and FY14E.

We expect that the company will keep its growth story in the coming quarters

also. We recommend ‘BUY’ in this particular scrip with a target price of

Rs.606.00 for Medium to Long term investment.

12

Industry Overview

With India experiencing a cycle of growth, the Rs 64 trillion (US$ 1.25 trillion)-Indian

Banking industry is poised to grow exponentially as the sector reflects the health of an

economy. Indian banks have proved their mettle time and again as their regulations

align with international standards, while they remain conventional in their approach.

The Reserve Bank of India (RBI), the regulator, continuously monitors the

macroeconomic environment to formulate its policies and directions.

According to the world's largest rating agency, Standard & Poor (S&P)'s Ratings

Services, India's banking system has a high level of stable, core customer deposits

supported by the system's good franchise, extensive branch networks, and large, yet

growing, domestic savings.

In fact, the next three decades are highly crucial and opportunity-oriented for the

Indian banking industry, which is primarily driven by demographics and reforms, said

Mr M V Nair, Former CMD, Union Bank.

Key Statistics

According to the RBI's 'Quarterly Statistics on Deposits and Credit of Scheduled

Commercial Banks', September 2011, Nationalised Banks, as a group, accounted for

52.2 per cent of the aggregate deposits, while State Bank of India (SBI) and its

associates accounted for 21.8 per cent. The share of New private sector banks, Old

private sector banks, Foreign banks and Regional Rural banks in aggregate deposits

was 13.7 per cent, 4.8 per cent, 4.6 per cent and 2.9 per cent, respectively.

With respect to gross bank credit also, nationalised banks hold the highest share of

51.6 per cent in the total bank credit, with SBI and its associates at 22.1 per cent and

New Private sector banks at 13.8 per cent. Foreign banks, Old private sector banks

and Regional Rural banks held a share of 5.2 per cent, 4.8 per cent and 2.5 per cent,

respectively.

13

• Another statement released by the RBI stated that bank deposits grew 13.4 per

cent to Rs 60.72 trillion (US$ 1.19 trillion) in the fiscal 2011-12 (the year to

March 23, 2011), while loans and advances grew 17.08 per cent to Rs 47.54

trillion (US$ 930 billion).

• The RBI data reveals that India Inc raised US$ 2.7 billion through external

commercial borrowings (ECBs) and foreign currency convertible bonds (FCCBs)

in January 2012.

• Owing to a rise in core foreign currency assets (FCAs), India's foreign exchange

reserves increased by US$ 862 million to US$ 294.82 billion for the week ended

March 16, 2012.

Indian Banking Sector: Recent Developments the Indian banking sector has come a

long way from serving through traditional approach to the online genre. According to a

survey by online survey company Ipsos, 57 per cent of Indians prefer to use the

Internet for banking and other financial holdings rather than shopping online. Things

have been made much easier by eliminating hefty paper processes and introducing

customer-friendly online banking facility with robust security features. Such changes

have not only facilitated access to several banking products, but have also improved

customer loyalty and money transfer mechanism.

Transactions in mobile banking are also on an upsurge as more than 2,800,000

transactions (worth about Rs 196.12 crore [US$ 38.37 million]) were conducted during

February 2012. The figure indicated a 300 per cent increase in terms of volume and

over 200 per cent increase in terms of value.

At present, the RBI has allowed 65 banks to conduct mobile banking out of which 47

banks have commenced offering these services.

National Australia Bank has recently opened its branch in Mumbai, India. The bank

would not only support existing institutional corporate and business banking

customers operating or trading with India but would also act as a mediator for Indian

clients who want to expand or invest in Australia or New Zealand.

Meanwhile, Development Bank of Singapore has expressed its keenness to operate as

a wholly-owned subsidiary (WoS) in India, while it infused Rs 500 crore (US$ 97.82

14

million) into its local branch operations. The entity is committed to establish a

universal banking franchise in India and looking forward to become a WoS to achieve

the same.

HDFC Bank is planning to set up kiosks that would allow employees to apply for loans

without stepping out of their offices. Initially the kiosks would be set up in offices of

the companies that already have a banking relationship with HDFC. The bank would

set up 1,500 priority desks across 500 companies in nine cities by August 2012.

Launch of RuPay

India has launched the country's first domestic payment card network, RuPay, to

compete with multinational Visa Inc. and Mastercard Inc. The new development will

not only help banks reduce cost of issuing a debit card but will also lead to expansion

of payment network in rural areas. National Payments Corp of India Ltd (NPCI), jointly

owned by banks, is the nodal agency to manage and promote RuPay.

NPCI has stated that 200,000 RuPay cards have already been issued and the target is

to have 10 million debit cards under the brand by March 2013. The system is expected

to be used for credit cards by March 2015 and all public sector banks are expected to

join the system by the end of 2012. RuPay based debit cards can be used by the

consumers on the Internet from September 2012.

Currently, India has around 260 million debit cards in use.

Government Initiatives

In its Budget for 2012-13, the Government has earmarked a capital of Rs 15,888 crore

(US$ 3.11 billion) to be infused in public sector banks, regional rural banks and other

financial institutions, including Nabard (National Bank for Agriculture and Rural

Development). Apart from this, the Government is also planning to set up a financial

holding company that will raise funds for public sector banks.

Taking a step closer towards mobile banking, the RBI has allowed banks to facilitate

cross-border remittance between bank accounts through mobiles, subject to clearance

15

from the local regulator. Banks will stand responsible for ensuring quality of funds,

adherence to know-your-customer (KYC) and other standards during the process.

Furthermore, the RBI has liberalised regulations pertaining to FCAs to provide

operational flexibility to Indian entities making overseas direct investments. After

satisfying stipulated requirements and conditions, Indian entities can open, hold and

maintain FCAs abroad that would simplify the process of making overseas direct

investments.

Road Ahead

According to a report by the Boston Consulting Group (BCG) India, prepared in

association with a leading industry organisation and Indian Banks Associations (IBA),

Indian banking industry would be the world's third largest in asset size by 2025 and

mobile banking would become the second largest banking mode after ATMs.

Furthermore, owing to the positive eco-system of the industry and regulatory and

Government initiatives, mobile banking is anticipated to enhance from 0.1 per cent of

transactions in a 45 per cent financial inclusion base in 2010 to 34 per cent of the

transactions with 80 per cent rural inclusion base by 2020, as per the report.

________________ ____ _________________________ Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation

for the purchase or sale of any financial instrument or as an official confirmation of any

transaction. The information contained herein is from publicly available data or other

sources believed to be reliable but do not represent that it is accurate or complete and it

should not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s

affiliates shall not be in any way responsible for any loss or damage that may arise to any

person from any inadvertent error in the information contained in this report. This document

is provide for assistance only and is not intended to be and must not alone be taken as the

basis for an investment decision.

16

Firstcall India Equity Research: Email – [email protected]

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

Ashish.Kushwaha Oil & Gas

A.Nagaraju Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s,Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions(domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

other international stock exchanges.

For Further Details Contact:

3rd Floor,Sankalp,The Bureau,Dr.R.C.Marg,Chembur,Mumbai 400 071

Tel. : 022-2527 2510/2527 6077/25276089 Telefax : 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com