Embed Size (px)

Citation preview

Restructuring BusinessAutumn 2015

Health and safetyWhat insolvency practitioners need to know…

Brief case reports, Horizon watch… and much more

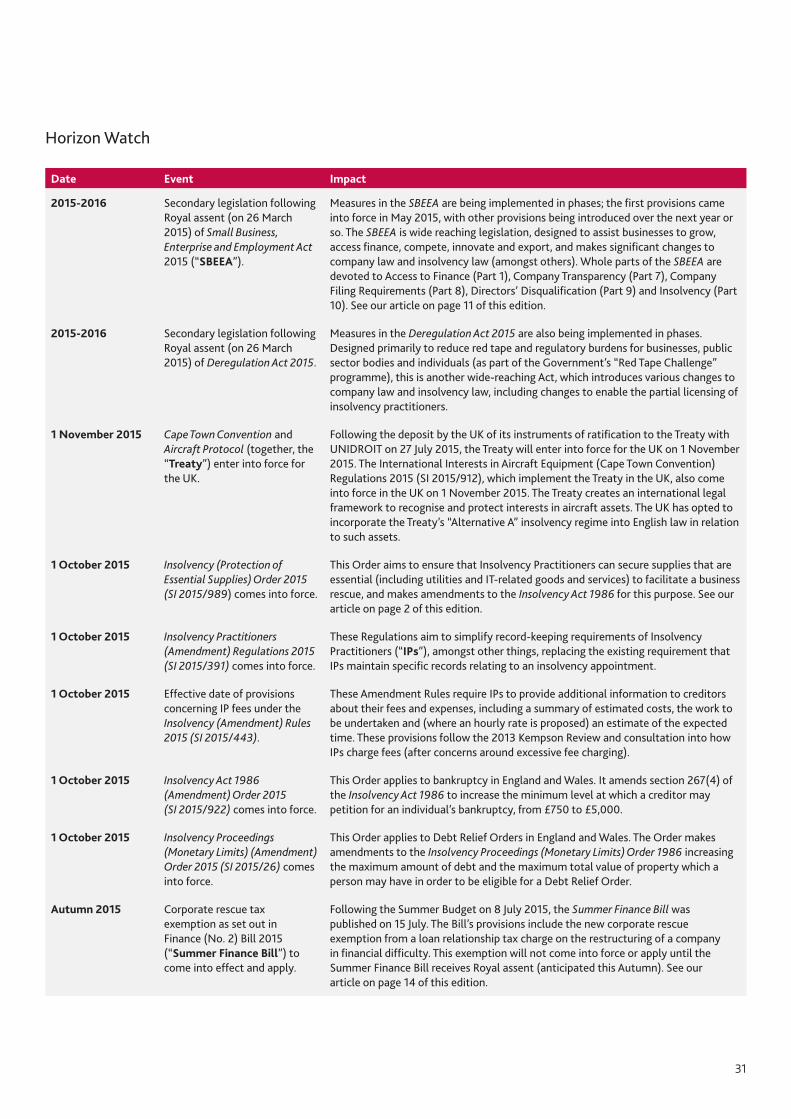

Greater protection of essential supplies

Distress in the oil and gas sector

Promoting good corporate behaviour

Corporate rescue tax exemption

Also inside this issue:

IFT Turnaround Legal Adviser of the Year

Foreword – Autumn 2015There is plenty on the legislative agenda for restructuring and insolvency professionals over the next 12 months (see Horizon watch). In this edition, we focus in particular on the implications of the new Insolvency (Protection of Essential Supplies) Order 2015 for insolvency practitioners (see Greater protection of essential supplies), as well as recent developments designed to make companies more transparent and directors more accountable (see Promoting good corporate behaviour), and we comment on the new corporate rescue tax exemption in the Summer Finance Bill (see Corporate rescue tax exemption not to apply until the autumn).

With the volatility in oil prices continuing, we continue to see businesses effected by distress in the oil and gas sector, and highlight some restructuring issues specific to this sector (see Distress in the oil and gas sector: an overview). We also include a feature on health and safety considerations for insolvency practitioners (see Wound up about health and safety?). Our Brief case section summarises some of the recent notable decisions by the courts.

It is still a very challenging market for restructuring and insolvency professionals and we are all having to evolve and refine our offerings to ensure that we remain relevant and offer value in the ever changing financial landscape that we currently find ourselves in.

We hope you enjoy this edition and, as ever, your support and feedback is welcomed and appreciated.

Steven CotteePartnerLondonT: +44 (0)20 7490 6940E: [email protected]

1

ContentsPinsent Masons | Restructuring Business | Autumn 2015

Magazine editor: Sharon Smith, Senior Practice Development Lawyer

While we take every care to confirm the accuracy of the content in this edition, it is not legal advice. Specific legal advice should be taken before acting on any of the topics covered.

02 Greater protection of essential supplies

Sharon Smith looks at the implications of the new Insolvency (Protection of Essential Supplies) Order 2015 for businesses and insolvency practitioners.

05 “Wound up” about health and safety?

What insolvency practitioners need to know about their legal health and safety responsibilities … By Kizzy Augustin and Oliver Brooks.

08 Distress in the oil and gas sector: an overview

Michael Thomson provides an overview of current funding issues in the sector and highlights some sector specific restructuring issues.

11 Promoting good corporate behaviour

Making companies more transparent and directors more accountable… Sharon Smith looks at some recent developments from Parliament and the courts.

14 Corporate rescue tax exemption not to apply until the autumn

Eloise Walker comments on the new exemption in the Summer Finance Bill.

15 Brief Case

Various team members summarise key cases over the past few months, focusing on the implications for restructuring professionals.

30 Horizon Watch

A look at upcoming dates involving legal developments.

33 Diary Room

Our latest guest to get quizzed is London based Senior Associate Bhal Mander.

35 Team News

Our usual round-up of team news across the UK.

2

Greater protection of essential suppliesThe Insolvency (Protection of Essential Supplies) Order 2015 (SI 2015/989) comes into force on 1 October 2015.

Sharon Smith looks at the implications of the Order for businesses and insolvency practitioners.

3

IntroductionThe Insolvency (Protection of Essential Supplies) Order 2015 (SI 2015/989) (the “Order”) comes into force on 1 October 2015. Its purpose is to amend the Insolvency Act 1986 (the “Act”) to provide greater protection to businesses (including companies and businesses run by individuals) to ensure that suppliers of essential supplies:

• continue to provide such supplies to insolvent businesses at a time when an insolvency practitioner is working to find a viable solution to restructure or rescue them; and

• do not (i) use the critical nature of their supplies to negotiate an unfair advantage when a business enters administration or a voluntary arrangement, and / or (ii) compel payment of charges incurred before commencement of an insolvency event, by threatening to terminate the supply on the grounds of non-payment of outstanding charges.

The Order gives effect to provisions contained in the Enterprise and Regulatory Reform Act 2013, and supports the UK’s general “business rescue” culture.

Protections before 1 October 2015The Act already includes some protections to insolvent businesses to ensure the continuation of certain kinds of essential supplies; these are set out in section 233 (as to corporate insolvency) and section 372 (as to individual insolvency).

Sections 233 and 372 prohibit a supplier of utilities (including gas, electricity, water and communication services) from compelling the payment of charges incurred before the commencement of an insolvency event by threatening to terminate the supply of the utilities on the grounds of non-payment. Sections 233 and 372 provide that, if a request is made by or with the concurrence of the officeholder for essential supplies to be provided after an insolvency event, the supplier may make it a condition of the supply that the officeholder personally guarantees the payment of any charges in respect of such supply. However, the supplier is not entitled to make it a condition of such supply that any outstanding charges incurred before the insolvency are paid.

The scope of section 233 and 372 is confined to a limited list of suppliers including statutory undertakers and similar bodies.

Extension of provisions to more private utility suppliers and suppliers of IT servicesThe Order extends the scope of sections 233 and 372 to include:

• a wider list of private suppliers of gas, electricity, water or communication services, including the supply of utilities from a landlord to tenant; and

• the supply of goods or services that are for the purpose of enabling or facilitating anything done by electronic means (i.e. IT services). These include the supply of point of sale terminals; computer hardware and software; information, advice and technical assistance in connection with the use of IT; data storage and processing; and website hosting.

There are still limitations to the scope of the legislative provisions. An arts and crafts retailer might argue that its most essential supplies are those of paints and wool. However, the legislation does not provide for an assessment of which supplies are essential for any particular business. Even so, the extension of the scope of these legislative provisions, particularly to include suppliers of IT services, is significant.

Insolvency-related terms in essential supply contracts to be invalidated in administration and voluntary arrangementsThe Order also inserts new sections 233A (as to companies) and 372A (as to individuals) into the Act. These new sections cause certain “insolvency-related terms” in contracts to cease to have effect (thereby preventing a supplier from terminating a supply or contract, altering the terms of the contract, or compelling higher payments for the supply) when a company enters administration, or when a voluntary arrangement is approved in respect of a company or individual respectively.

The insolvency-related terms cease to have effect only in a contract for those utility and IT supplies listed in sections 233 and 372 (as amended).

The insolvency-related terms may continue to be relied upon in respect of other insolvency procedures, thereby enabling a supplier to terminate a contract when a company goes into liquidation or a bankruptcy order is made against an individual.

Sections 233A and 372A only apply to contracts entered into after 1 October 2015.

When may a supplier terminate a contract or supply?

The Order provides certain safeguards for suppliers. If an insolvency-related term in an essential supply contract ceases to have effect, a supplier may terminate the contract or the supply if certain conditions are met, as follows.

A supplier may terminate the contract if:

• the officeholder, or supervisor of the voluntary arrangement, consents to termination of the contract; or

• the court grants permission for the termination of the contract; or

• any charges in respect of the supply that are incurred after the company entered administration, or the voluntary arrangement took effect, are not paid within the period of 28 days beginning with the day on which payment is due.

The court may grant permission under the second bullet above only if it is satisfied that continuation of the contract would cause the supplier hardship.

4

A supplier may terminate the supply if:

• the supplier gives written notice to the officeholder, or supervisor of the voluntary arrangement, that the supply will be terminated, unless the officeholder personally guarantees the payment of any charges for the continuation of the supply after the company entered administration, or the voluntary arrangement took effect; and

• the officeholder or supervisor does not give that guarantee within 14 days (beginning with the day the notice is received).

Clearly, it is therefore important that the officeholder or supervisor gives a personal guarantee within the fortnight of any such request to ensure continuation of the supply. Insolvency practitioners may be reluctant to give personal guarantees, and in some cases (particularly in voluntary arrangements, where they have limited control of the business) may not feel in a position to give them (particularly in respect of so many different essential supplies). It is likely that such concerns will result in a degree of negotiations with suppliers, however it is to be hoped that these do not hinder the purpose of the Order, which is generally to assist insolvency practitioners in the rescue of businesses for the benefit of all creditors and employees.

Suppliers of utilities and IT services should review their supply contracts, and terms and conditions (particularly their termination provisions), to consider what (if any)

amendments are necessary as a result of the Order. Although the Order does not set out sanctions for breach of the new rules, it is likely that an insolvency practitioner could apply for an injunction to ensure the continuation of services and obtain damages in the event of breach.

Suppliers should take comfort from the safeguards that they will continue to be paid for supplies provided during administration and voluntary arrangements. In the case of administration, payments incurred after the business enters administration are treated as an administration expense, and thus payable high up the insolvency waterfall ahead of preferential creditors and most other creditors (except fixed charge holders). The new rules are not meant to punish suppliers, but to prevent them from using the critical nature of their services from exploiting financially distressed businesses looking to recover.

Conclusion

Generally, the Order will be welcomed by employees and creditors of businesses

entering administration or voluntary arrangements, as well as insolvency practitioners seeking a viable rescue solution for them. The extension of the rules to include supplies of IT services is vitally important. With the increasing reliance by businesses on IT, it is frequently not possible for businesses to continue to trade without a fully operative system.

The invalidation of insolvency-related terms in utility and IT supply contracts on businesses entering administration or voluntary arrangements is also a huge step forward. Insolvency trade body R3 had previously described termination clauses which took effect on insolvency as “one of the biggest obstacles to business rescue that insolvency practitioners come across”. By effectively banning such clauses in such situations, the Order will help insolvency practitioners ensure that businesses continue to receive many of the crucial supplies they need during rescue, so as to deliver the best outcome for creditors and employees.

The new rules should make it easier for insolvency practitioners to restructure and continue to trade a business, whilst seeking purchasers for it as a going concern, since they should not be subjected to unreasonable demands made of them by utility and IT suppliers going forwards. As well as making the task of rescuing businesses easier, the Order should increase the likelihood that those businesses will survive and jobs will be saved, which is good news for creditors and employees of those businesses, as well as insolvency practitioners.

Sharon SmithSenior Practice Development LawyerManchesterT: +44 (0)161 234 8422E: [email protected]

5

“Wound up” about health and safety?What Insolvency Practitioners need to know about their legal health and safety responsibilities…

By Kizzy Augustin and Oliver Brooks

6

IntroductionAlthough there has been a recent downward trend in the number of company insolvencies in England and Wales, over four thousand companies still entered into formal insolvency in the first quarter of 2015. And those who are “in control” of insolvent companies have various health and safety responsibilities, often without realising that to be the case.

The specialist regulatory team at Pinsent Masons has advised a significant number of insolvency practitioners (“IPs”) and managing agents facing criminal investigation and personal prosecution relating to allegations arising out of the management of health and safety (including issues relating to fire safety), whether acting as administrators, liquidators or LPA receivers. Any failure by IPs to consider health and safety issues properly – whether such issues arise from the operations of the business, the control of premises or the sale of work equipment – could have a significant impact on the IP’s appointment in a variety of ways:

• additional time and resources may be required to address specialist health and safety issues that were not anticipated at the outset of the appointment;

• the insolvency process may be unnecessarily prolonged by an ongoing health and safety investigation, as the insolvency process cannot be completed until the conclusion of such an investigation;

• the realisable assets of a company may be devalued in the event of a prosecution;

• the company may attract adverse publicity, affecting both the value of an insolvent company and the reputation of the IP concerned; and

• any resultant criminal conviction for a health and safety offence could result in the IP losing their ability to practice as well as their liberty in the event of a custodial sentence.

The message is clear: IPs must have an awareness of health and safety law and the responsibilities that they owe in order to best protect themselves against criminal liability and reputational damage.

The Health and Safety regime

The Health and Safety at Work etc. Act 1974 (“HSWA”) and related regulations apply to all workplaces – whether a company is solvent or not, and irrespective of it being managed by a board of directors or an appointed IP.

The HSWA imposes various general duties on employers, employees, and those who are “in control” of business premises or those who manage business operations. Some or all of those duties could apply in circumstances where an IP has been appointed to control, manage and direct the operations of an insolvent business. In the event of any breach of those duties, the company itself and/or an IP in their individual capacity (due to their personal acceptance of the IP appointment) could attract potential criminal liability. The penalties for breaches by individuals of the health and safety regime can be significant – the Crown Court can impose unlimited fines and/or up to 2 years’ imprisonment.

In the event of the most serious work-related incidents where a death has occurred, an IP could also face the prospect of being investigated in their individual capacity for gross negligence manslaughter in addition to any action against the insolvent business for corporate manslaughter.

Allegations of manslaughter are reserved for the most serious cases and require evidence of failings so serious that they amount either to “gross” negligence or a “gross” breach of duty. Although these prosecutions are uncommon, they do occur and are far more than a hypothetical risk. IPs should be aware that the number of prosecutions for corporate manslaughter has increased significantly over the last two years and those cases have often involved associated

allegations of individual liability for manslaughter and health and safety offences against the senior management of the organisations involved.

This rise in temperature has also resulted in increasing fines for serious breaches of the health and safety regime, particularly in respect of fatal incidents. Those levels are set to increase considerably with the introduction of proposed new sentencing guidelines which are anticipated to be in force within the coming months. It is important to note that fines for breaches of health and safety law and corporate manslaughter will not be assessed against the profitability of a company but rather its turnover, against which it is not possible to be indemnified or insured against.

Legal risks posed to IPsThe degree to which an IP is exposed to criminal liability for breaches of health and safety law will vary from appointment to appointment. For example, an IP will likely face greater risks if appointed to manage an insolvent company that operates within an inherently dangerous sector, such as construction, manufacturing or agriculture. Similarly, an appointment involving the management of old business premises may lead to an increased risk of maintenance and asbestos issues. In all circumstances, IPs need to be aware of the risks that they are exposed to and they must have in place control measures to guard against them.

IPs do not benefit from any special dispensation under health and safety legislation – they can be held personally responsible. In some circumstances, the enforcing authorities may find IPs a more attractive target for prosecution than the former directors (who may have since distanced themselves from the company) or an insolvent company.

Although insurance can be provided to cover against civil compensation claims brought by individuals for death or injury at the workplace, it is not possible to insure against the criminal penalties that may result from a successful prosecution for a breach of health and safety law – including fines, mandatory court charges and victim surcharge fees.

7

Key areas of risk

The Pinsent Masons team has advised a number of IPs during investigations and prosecutions by enforcing authorities. That experience has identified a number of commonly recurring themes. In particular, these have included:

• the adequacy of fire precautions and fire risk assessments under the control of the IP;

• risks posed by the sale of defective work equipment and machinery, and the extent to which the use of “waivers” can transfer liability to purchasers;

• the application of the Construction (Design & Management) Regulations 2015 to remedial construction works or the dismantling of structures following asset sales; and

• arrangements relating to the control of asbestos in premises.

‘Winding Up’It is plain that IPs must have at least a basic understanding of the various responsibilities that they owe under the health and safety regime. In addition, they must be alert to the risks that may be posed during any appointment – starting with an assessment of the nature of the insolvent company’s operations and the premises that it controls.

If an IP fails to understand the relevance of health and safety law to their appointments, the consequences could be grave – reputational damage, disqualification from the profession, substantial fines and even a loss of liberty.

This is not a “wind up”…

Kizzy AugustinSenior AssociateLondonT: +44 (0)20 7418 9573E: [email protected]

Oliver BrooksSolicitorLondonT: +44 (0)20 7054 2591 E: [email protected]

8

Distress in the oil and gas sector: an overviewFollowing a dramatic and sustained depression in oil prices, restructuring teams across banks and insolvency practitioner firms are building specialisms in a sector where distress has not been prevalent for a number of years.

Michael Thomson provides a high level overview of current funding issues in the oil and gas sector and highlights some sector specific restructuring issues.

9

Sector overviewActivity in the oil and gas sector can be categorised into three major areas: upstream, midstream and downstream.

• “Upstream” is often referred to as exploration and production (or “E&P”) and involves searching for hydrocarbons, drilling to explore for hydrocarbons and developing and operating wells to bring hydrocarbons to the surface.

• “Midstream” involves the transportation, storage, and marketing of hydrocarbons to downstream operators.

• “Downstream” refers to the refining of hydrocarbons and the marketing and distribution to consumers of products derived from hydrocarbons.

In the upstream sector, a number of E&P companies – ranging in size from the oil “majors” to smaller independents – commonly participate jointly in licences by entering as co-venturers into joint operating agreements (“JOAs”). Each JOA appoints one of the co-venturers as “operator”. The operator then contracts on behalf of the joint venture and invoices or “cash calls” the other co-venturers for their respective shares of expenditure.

These activities are supported by a profusion of specialist service providers. Such service companies form a vital part of the supply chain to the E&P companies. They range in scale from very large cash heavy corporates to very small, highly-geared entities.

Regulation of the sectorThe regulatory body that oversees upstream operations on the UK Continental Shelf is the Department of Energy and Climate Change (“DECC”). DECC grants licences to exploit the UK’s hydrocarbon resources. The Oil and Gas Authority (“OGA”), an executive agency of DECC, considers applications for licences and grants licences periodically in “licensing rounds”. The most recent 28th offshore licensing round granted 134 offshore licences. The most recent 14th onshore licensing will grant a round of licences by the end of 2015.

The OGA launched on 1 April 2015, following a government-instructed review by Sir Ian Wood into maximising the recovery of oil and gas from the UK Continental Shelf. One of the recommendations of the Wood Review was the creation of the OGA, as an independent economic regulator for the sector.

Part of DECC’s role is to oversee “decommissioning” i.e. the restoration of the seabed to its former condition once operations on an oil field have finished. A wide range of parties can be liable for decommissioning, including licence holders, former licence holders and parties associated to these companies. DECC can notify some or all of these parties that it requires them to submit a decommissioning programme for approval. The parties submitting the programme must then implement it and are jointly and severally liable to do so. Parties will enter into arrangements for the provision of security to cover the cost of decommissioning, commonly in the form of decommissioning security agreements (“DSAs”) in order to protect themselves, granting security for their share of decommissioning costs. Under the Petroleum Act, owning an interest in an offshore installation as security for a loan is specifically excluded as an interest which gives rise to a decommissioning liability.

DECC may take enforcement proceedings against licence holders and withdraw licences if the terms of a licence are not observed. Crucially for lenders, the terms of the licences allow DECC to revoke the licence if a co-venturer is insolvent or if, for example, there is a change of control following enforcement of security, in which case DECC may require a further change of control.

The oil price fall and consequential distressOil prices have plummeted during 2014 and, despite brief periods of stability, have continued to fall throughout 2015. The fall in oil prices rapidly caused cashflow and loan covenant issues for many companies operating in the oil sector. Oil companies reacted by slashing spending on assets, cutting day-to-day operating costs and re-negotiating lending terms so as to avoid defaulting on their loans. Upstream, midstream, and downstream companies began taking steps to restructure, either pre-emptively, or necessarily, if they were already in distress.

E&P companies have reassessed their capital expenditure and cut back on exploration and development. The consequential change to planned expenditure programmes reverberated down the supply chain. Service companies and rig operators are being asked to accept lower prices for their services and/or extended payment terms, to deal with

non-payment, and are experiencing a drop in overall demand.

Insolvency statistics suggest that the stakeholders most vulnerable to insolvency are small E&P companies and oil service companies. In the case of oil service companies, reports suggest that insolvencies trebled during 2014 and that “significant distress” throughout the sector increased by 69% in the last quarter of 2014, compared to the last quarter of 2013. The latest high profile E&P insolvency is the African focused Afren, which entered administration at the end of July 2015.

Sector specific restructuring issuesAs well as the usual host of issues to consider in any restructuring (including, for example, reduction of costs and employees, directors’ duties, and cross-border considerations), there are a number of sector specific issues. These include:

1. Funding, refinancing and debt restructuring

Smaller E&P companies often utilise reserves based lending, where the lender provides a loan against security over identified reserves yet to be extracted. The lender applies a series of assumptions as to forward oil prices (“price decks”) and extraction costs so as to determine ability to repay and loan amounts. Proceeds of the sale of hydrocarbons, once extracted, repay the lending.

Oil price therefore has a direct impact on the amount which companies can borrow through their reserves based lending. At twice-yearly “redetermination” dates, the amount of lending the company’s reserves can support is revalued using the lender’s current price deck. Whilst lenders’ price decks were traditionally always more conservative than the oil price, the oil price assumption used in redeterminations has reduced significantly.

The effects have been mitigated for those companies which entered into oil price hedging when prices were at their peak but those hedging instruments already in place are expiring and a sustained low price environment means these are not a solution in the long term. There have already been a number of covenant waivers over the first half of 2015. In some cases, lenders have looked for additional information and monitoring as a condition of consenting to the covenant waivers. Conditions attached to

10

such waivers include forcing E&P companies to reassess their spending plans, to look to sell assets or even to put themselves up for sale. In the case of oil service companies, we have seen that many borrowers are pre-emptively approaching their lenders in advance of covenant test dates, so as to avoid breach and agree covenant resets.

2. Licensing

Lenders must consider the impact that enforcement action would have on their borrowers’ licences and, in consequence, the value of their borrowers’ assets. DECC may revoke a licence entirely if any one of the licence holders becomes insolvent, or the licencees fail to make a payment under the licence. A change in ownership of a licencee also gives DECC grounds to terminate a licence, including where this is a result of enforcement of a security. We anticipate lenders will always wish to engage with DECC prior to taking enforcement action against a borrower to obtain comfort from DECC on how DECC will respond.

3. Defaults under JOAs

If (as will be the case with most fields) more than one company participates in the licence, the participants will have entered as co-venturers under the relevant JOA. The JOA (which sets out the contractual framework for the joint venture) will contain default provisions that ultimately result in forfeit of the defaulting party’s rights under the JOA and licence. The rights of lenders are always

subject to the terms of the JOA and, to preserve value in their borrowers, lenders need to avoid their borrowers defaulting under their JOAs. Co-venturers need to ensure that the JOA allows them to take pre-emptive action to avoid revocation of their licence, should the co-venturer be in default.

4. Defaults under DSAs

DSAs (which provide for the grant of security to cover decommissioning liabilities of oil field developments) include provisions which trigger upon the insolvency of a licence holder and other similar events of default. Such agreements will often provide, upon an event of default, for the provision of security to cover the decommissioning sums for which the defaulting party is liable, so as to meet that party’s share of decommissioning costs.

As it is not unusual to see DSAs entered into by smaller E&P companies being backed by letters of credit (or similar instruments), lenders should be especially cautious to ensure any action by them does not crystallise such a contingent liability and result in a further cash out-flow.

It is important for parties experiencing signs of distress to conduct a contract review at the earliest opportunity to assess potential default and termination provisions and to consider their re-negotiation and restructuring opportunities.

On the horizonThe world’s biggest oil companies have shelved spending on many new projects. Predictions are therefore that the impact of operators’ spending cuts on oil service companies will increase further in 2015 and during 2016 and beyond.

Merger & acquisition activity in the sector (that has already begun) will likely continue, with consolidation in the market and increased investment in distressed oil businesses or assets at reduced prices. The market has already seen service companies announcing intentions to acquire suppliers to avoid adverse impact on their business, and we expect further consolidation between service companies.

Given the further fall in oil prices, it is likely that the next redetermination to ascertain the amount of lending the company’s reserves can support will crystallise covenant breaches as well as highlighting near-term liquidity issues for the E&P companies. This is likely to trigger further asset and company sales to pre-empt solvency issues wherever possible.

Michael Thomson is a Senior Associate based between our Glasgow and Aberdeen offices, and has advised on numerous restructuring transactions in the oil and gas sector.

Michael ThomsonSenior AssociateGlasgowT: +44 (0)141 249 5599E: [email protected]

11

Promoting good corporate behaviour Making companies more transparent and directors more accountable…

Sharon Smith looks at some recent developments from Parliament and the courts.

12

Amongst the many diverse provisions of the Small Business, Enterprise and Employment Act 2015 (“SBEEA”) are significant changes to increase transparency surrounding company control in the UK, and increase directors’ accountability. Alongside these, there are signs that the courts are increasing pressure on directors who trade wrongfully or fraudulently when companies approach insolvency. Legislators and judges are sending a clear and consistent message: the structure and management of companies must be transparent, and directors (and those influencing them) must be held accountable for their actions. Here are some of the recent developments from Parliament and the courts.

Small Business, Enterprise and Employment Act 2015

The SBEEA (which received Royal assent on 26 March 2015) introduces various changes to company law and insolvency law, which are being implemented in phases over the next year or so. Amongst these are changes set out in Part 7 of the SBEEA (relating to the transparency of companies), Part 9 (relating to director disqualifications) and Part 10 (relating to insolvency), including the following:

New register of People with Significant ControlTo increase transparency around whom ultimately owns and controls UK companies, the SBEEA requires UK companies to hold and keep available for inspection a register of people with significant control over the company (a “PSC register”). A “person with significant control” (“PSC”) is an individual who ultimately owns or controls more than 25% of a company’s shares or voting rights, or who otherwise exercises control over a company or its management.

Companies will be required to take reasonable steps to identify people they know or suspect to have significant control, including by giving notice to PSCs and others to obtain information. The PSC register will include information on an individual’s name, date of birth, nationality, address, and details of their interest in the company. Companies will need to provide an initial statement about their PSCs to the Registrar of Companies (Companies House) on incorporation and maintain their PSC register going forwards, updating the information where necessary and at least once every 12 months. The information at Companies House will be publicly accessible in the same way as other corporate filings.

Under the current implementation schedule, the requirement to keep the PSC register will enter force from April 2016, with the obligation to file information at Companies House taking effect from June 2016.

Companies, particularly those with complex corporate structures, should begin (if they haven’t already) to identify their PSCs and adjust their internal procedures (and, if necessary, structures) so that they are prepared for compliance with the new registration requirements when they come into force. Although imposing an additional registration burden on companies (as well as on Companies House), the new requirements will be welcomed by creditors, investors and advisers who need to look through corporate structures in order to meet their own KYC requirements.

Abolition of bearer sharesTo assist in combatting fraud and ensure compliance with international standards, UK companies are prohibited (as from 26 May 2015) from issuing bearer shares, which by their nature are freely transferable and title to which passes by delivery. Existing bearer shareholders must surrender their shares to the company and have them exchanged for registered shares before 26 February 2016 (the transitional 9 month period); otherwise existing bearer shares must be cancelled.

Abolition of corporate entities as directorsTo deter opaque arrangements involving company directors, the SBEEA prohibits the use of corporate entities as directors (where one company acts as the director of another) going forwards; directors will need to be natural persons who can be held to account individually, with limited exceptions (to be set out in secondary regulations). Companies will need to consider the position with respect to the exceptions, and adjust their arrangements where necessary, to ensure compliance.

This provision is currently scheduled to enter force in October 2016. There will be a transitional period of one year, after which existing corporate entity directors will automatically cease to be directors (i.e. currently October 2017).

Statutory duties of directors apply to shadow directorsTo improve standards of shadow director conduct, and increase the accountability of shadow directors, who are involved in the company’s management and decision making and often influential to the board, the SBEEA makes clear that the general statutory duties that apply to directors under the Companies Act 2006 apply to shadow directors to the extent they are capable of applying (effective as from 26 May 2015).

Extensions to director disqualification regimePart 9 of the SBEEA includes changes which strengthen the rules on director disqualifications, widen the matters of misconduct courts must take into account when making disqualification orders against directors, and otherwise help creditors recoup losses resulting from director misconduct. The director disqualification regime under the Company Directors Disqualification Act 1986 (“CDDA”) is being extended for this purpose, with changes to be implemented including:

13

Disqualification orders• In an application for a disqualification order,

courts may take into account the conduct of directors in relation to overseas insolvency companies;

• Courts may make disqualification orders against persons who influence the conduct of a disqualified director; and

• The period in which the Secretary of State may apply for a disqualification order against a director of an insolvent company is being extended to three years (from two years).

New requirements for insolvency officeholders reporting on directors’ conduct Officeholders must prepare a report about the conduct of each person who was a director of the company (a) on the insolvency date, or (b) at any time during the period of three years ending with that date. Such reports must be filed within three months of insolvency commencing (unless the Secretary of State agrees to extend).

New powers for courts to make compensation orders against directorsThe courts may make a compensation order against a person (on application of the Secretary of State) where the court is satisfied that (1) the person is subject to a disqualification order or undertaking under the CDDA and (2) the conduct (for which the person is subject to the order or undertaking) has caused loss to one or more creditors of an insolvent company of which the person has at any time been a director.

New insolvency officeholder powersAmongst the insolvency law changes in Part 10 of the SBEEA are two provisions giving new powers to insolvency officeholders (which take effect on a date still to be confirmed at the time of writing):

• Section 117 SBEEA amends the Insolvency Act 1986 (the “Insolvency Act”) to permit

an administrator to bring an action for wrongful or fraudulent trading where a director (or, in the case of fraudulent trading, any person) has caused the business of an insolvent company to trade wrongfully or fraudulently. Giving administrators the same rights as liquidators in this respect should enable more actions to be brought against delinquent directors, as well as reduce costs (with no need for companies to be put into liquidation in order for such actions to be brought going forwards).

• Under Section 118 SBEEA, administrators and liquidators will be able to assign to third parties certain causes of action which only they can currently bring under the Insolvency Act. Such causes of action include wrongful trading, fraudulent trading, transactions at an undervalue and preferences. The officeholder will be able to assign not only the right to bring the action itself but also the proceeds of such an action.

Directors’ duties on approaching company insolvency – attitude of the courtsThe courts have shown little sympathy recently for directors accused of wrongful trading or fraudulent trading under the Insolvency Act.

In Jetivia v Bilta [2015] UKSC 23, a cross-border case involving allegations of fraudulent trading under section 213 of the Insolvency Act, the Supreme Court declared that where a company has been the victim of wrong-doing by its directors, that wrong-doing cannot be attributed to the company so as to afford the directors an illegality defence. The Supreme Court also ruled that fraudulent trading claims under section 213 have extra-territorial effect (i.e. the court can make remedial orders over persons outside the UK). In so deciding, the Supreme Court has put the legislative requirements of section 213 back squarely on the shoulders of directors and third parties who have

committed a fraud against the company, including in situations where such directors or third parties may reside abroad.

In Brooks v Armstrong [2015] EWHC 2289 (Ch), the High Court ruled that, in establishing a defence to wrongful trading allegations under section 214 of the Insolvency Act, the burden of proof is on the directors (not liquidators) to prove that the directors took “every step” to minimise the potential loss to creditors as soon as they knew that the company could not reasonably avoid liquidation. This decision increases the pressure on directors who continue trading on approaching insolvency, and will make it easier for liquidators to prove wrongful trading claims going forwards.

ConclusionThere is an increasing focus by Parliament and the courts in ensuring that companies are transparent and the individuals involved in the management of companies, particularly directors, are held accountable for their actions.

Enhancing transparency and accountability helps promote good corporate behaviour and encourages public trust, and Parliament is keen to improve the reputation of the UK as a trusted and fair place to do business. The new legislative changes are designed to help deter and sanction those who hide their interest in UK companies to facilitate illegal activities, and will generally be welcomed by creditors and investors of companies, as well as insolvency officeholders, who need to look through corporate structures, and hold individual directors to account.

Recent decisions by the courts should further assist insolvency officeholders in bringing claims against delinquent directors, and put pressure on directors to ensure they abide by their statutory duties, including their duty to act in the best interest of creditors on approaching company insolvency.

Sharon SmithSenior Practice Development LawyerManchesterT: +44 (0)161 234 8422E: [email protected]

14

Summer Budget 2015: Corporate rescue tax exemption not to apply until the autumnThe corporate rescue exemption from a loan relationship tax charge on the restructuring of a company in financial difficulty is in the Finance (No. 2) Bill, but will not come into force until that Bill receives Royal assent.

The new provisions were originally intended to apply to the release, modification or replacement of a debtor relationship of a company on or after 1 January 2015. However, they were not included in the pre-election Finance Bill (which became law in March 2015).

It is good to see the corporate rescue tax exemption will finally be coming into law, but anyone who has already acted on the back of its expected enactment will be shocked and disappointed to see that it does not apply to arrangements pre-Royal assent, which is poor form.

The omission of the provisions from the previous Finance Bill had left companies hoping to restructure in an extremely difficult position.

The loan relationship or corporate debt rules set out how debt is treated for corporation tax purposes. Tax liabilities and deductions are calculated broadly by reference to the accounting treatment of the debt. Without special rules wherever debts are released, tax charges could arise, even if the release is as a result of a restructuring of a company in financial distress. The changes will extend the current rules which apply where debt is exchanged for equity.

The draft legislation is contained in the Finance (No. 2) Bill 2015, which was published on 15 July. The legislation excludes taxable amounts which would otherwise arise where arrangements are made to restructure the debts of a company in financial distress with a view to ensuring its continued solvency. This will cover situations where debt is released, or where the terms are modified, supplementing and extending the existing rule which exempts credits arising in debtor companies when creditors exchange debt investment for an equity stake.

The new relief will be available to debtor companies on release from a debt if it is reasonable to assume that there would be a material risk that at some point within the

next 12 months the company would be unable to pay its debts without the release.

It is expected that the Finance (No. 2) Bill 2015 will not receive Royal assent until sometime in October. Unfortunately, companies in financial difficulty are not necessarily going to be in a position to hold off on restructuring until then. Anyone who restructured earlier this year, hoping that the new rules would come into force retrospectively (as the Government promised) could have a tax charge as a result of the delay in introducing the rules. We hope the Government will listen to lobbying and change its mind on the effective date of this provision.

Eloise Walker is a Partner specialising in corporate tax, structured and asset finance and investment funds. Eloise’s focus is on advising corporate and financial institutions on UK and cross-border acquisitions and re-constructions, corporate finance, joint ventures and tax structuring for offshore funds. Her areas of expertise also include structured leasing transactions, where she enjoys finding commercial solutions to the challenges facing the players in today’s market.

Eloise WalkerPartnerLondonT: +44 (0)20 7490 6169E: [email protected]

15While we take every care to confirm the accuracy of the content in this edition, it is not legal advice. Specific legal advice should be taken before acting on any of the topics covered.

Brief CaseVarious members of the team look at key cases from the past few months and consider the implications for restructuring and insolvency professionals

16

Contents

17 It wasn’t me directors’ misconduct • fraudulent trading claims • illegality defenceJetivia SA and another (Appellants) v Bilta (UK) Limited and others (Respondents) [2015] UKSC 23

18 Section 75 pension debt – implied implications section 75 pension debt • implied contract • indemnityRe Heis & Others (as joint administrators of MF Global UK Limited) v M F Global UK Services Limited [2015] EWHC 883 (Ch)

19 Arbitration clauses survive insolvency arbitration clause • construction contract • insolvencyPhilpott and another v Lycée Français Charles de Gaulle School [2015] EWHC 1065 (Ch)

20 Olympic establishment decision cross-border • winding-up • “establishment” • EC Insolvency RegulationThe Trustees of the Olympic Airlines SA Pension and Life Assurance Scheme (Appellants) v Olympic Airlines SA (Respondent) [2015] UKSC 27

21 Validation of property dispositions after a winding-up petition validation order • winding-up • section 127 Insolvency ActWilson v SMC Properties Ltd [2015] EWHC 870 (Ch)

23 Administrators’ fees: You get nothing in life for free! creditors’ challenge • administrators’ feesRandhawa and another v Turpin and another [2015] EWHC 517 (Ch)

24 Sanction of scheme of arrangement debt restructuring • overseas companiesRe Van Gansewinkel Groep BV and others [2015] EWHC 2151 (Ch)

26 Special administrators denied insolvency litigation funding possibilities special administration • conditional fee arrangementHartmann Capital Ltd & Ors, Re Investment Bank Special Administration Regulations 2011 [2015] EWHC 1514 (Ch)

27 Restoration man restoration to register • backdated winding-up petitionDavy v Pickering and others [2015] EWHC 380 (Ch)

28 The availability of bankruptcy for foreign debtors bankruptcy • foreign debtor • annulment applicationJSC Bank of Moscow v Kekhman & Ors [2015] EWHC 396 (Ch)

17

It wasn’t me

Jetivia SA and another (Appellants) v Bilta (UK) Limited and others (Respondents) [2015] UKSC 23Bhal Mander reviews an important decision by the Supreme Court on the scope of the illegality defence, in a case concerning directors’ misconduct.

What has happened?The Supreme Court has declared that where a company has been the victim of wrong-doing by its directors, that wrong-doing cannot be attributed to the company so as to afford the directors an illegality defence.

The Supreme Court also found that fraudulent trading claims under section 213 of the Insolvency Act 1986 have extra-territorial effect (i.e. the court can make remedial orders over persons outside the UK).

Whom does this affect and how?The case is relevant to all corporate insolvency officeholders bringing claims against directors and third parties that have committed a fraud against the company.

Next steps?The Supreme Court did not deal conclusively with the illegality defence as the issue was not determinative of the case. They did however say that “the proper approach to the defence of illegality needs to be addressed by this court (certainly with a panel of seven and conceivably with a panel of nine justices) as soon as appropriately possible”. The door to these types of defences is therefore not yet shut and there are likely to be further developments in this area in the future.

Relevant background

The liquidators of Bilta (UK) Limited brought proceedings against the company’s two former directors (amongst others) for breaches of their fiduciary duties to the company. Amongst the allegations, it was claimed that the directors had caused the company to enter into a number of transactions relating to European Emissions Trading Scheme Allowances and that these transactions constituted a VAT carousel fraud. The company had been compulsorily wound up by HM Revenue & Customs in November 2009.

The directors applied to strike out the claim relying on the illegality defence arguing that the company could not recover losses caused by its own illegal actions. The application was

dismissed by the High Court and that decision was upheld both by the Court of Appeal and the Supreme Court.

The Supreme Court decided that a company was not barred from suing its directors for losses caused by the directors’ breach of fiduciary duty in circumstances where those directors involved the company in a fraud.

Whilst the decision was unanimous, the Justices disagreed as to the reasons. Lords Toulson and Hodge considered that the illegality defence is a public policy rule and its application would depend on the facts of the particular case. Lord Sumption, on the other hand, considered that the defence was a rule of law. His view was that the acts of directors should always be attributed to the company, except where there has been a breach of duty owed to the company (such as fraud).

Bhaljinder ManderSenior AssociateLondonT: +44(0)20 7490 6670E: [email protected]

18

Section 75 pension debt – implied implications

Re Heis & Others (as joint administrators of MF Global UK Limited) v M F Global UK Services Limited [2015] EWHC 883 (Ch)Serena McAllister reviews this High Court case in which an implied contract between two group companies was found to include an indemnity for section 75 pension debt.

What has happened?The High Court decision found that an implied contract between a service company and the recipient of its seconded employees included an indemnity (by the recipient to the service company) for any section 75 debt in respect of those employees.

Under Section 75 of the Pensions Act 1995, an employer who participates in a defined benefit occupational pension scheme can, in specified circumstances, become liable for some or all of the shortfall in the pension scheme’s funding.

There were two main issues to be decided by the court:

(1) was there an implied contract between two group companies, MF Services (the service company and employer of seconded staff) and MF UK (the recipient of the seconded staff), in the absence of a written contract, to reimburse the costs of the seconded employees including pensions costs?; and

(2) if such a contract existed, did its terms extend to cover an indemnity by MF UK to MF Global for the section 75 debt?

The court found that:

(1) despite no written agreement, there was an implied contract between MF UK in favour of MF Services, on similar terms to the express contract MF UK had with group parent company, MF Holdings. Using established contract law principles, the court

held that MF Services had offered to provide MF UK with staff on the condition that MF UK would reimburse it with all associated costs in respect of the secondees. As evidence of acceptance, MF UK had reimbursed MF Services for these secondee costs directly.

(2) due to the way arrangements for seconded employees had operated, references in the contract to an obligation in respect of “pension contributions” and “aggregate costs” in respect of employees were considered wide enough to include an indemnity from MF UK to MF Services for all costs of MF Services as employer of the seconded staff.

Therefore, the judge declared that MF UK was obliged to indemnify MF Services in respect of the section 75 debt.

Whom does this affect and how?This decision very much turns on its facts, however the scenario where a service company exists without income and another group company is responsible for the liability of the employees seconded to it, is a common one. It is clear that, in these circumstances, the court was willing to take a wider view approach to “pension costs” in implying terms into the service agreement to cover the section 75 debt, and to hold group companies (other than the statutory employer) liable.

Officeholders dealing with group companies who have similar arrangements and which have a defined benefit occupational pension scheme may be well advised to investigate the

terms of any service agreements to see exactly where the section 75 debt liabilities lie.

Next steps?While helpful, this case could have been avoided by careful drafting and it is advisable to those drafting service agreements to address the responsibility for any pension scheme deficit explicitly to avoid terms being implied.

Relevant backgroundCompanies in the MF Global group carried on business as broker-dealers in financial markets. On 31 October 2011, the main group companies entered administration, including MF Global UK Limited (“MF UK”) and Global UK Services Ltd (“MF Services”). MF UK had been the main recipient of seconded employees from its service company, MF Services. No written contract existed between them, although one did exist between MF Services and MF Global Holdings Europe Limited (“MF Holdings”). MF UK had paid to MF Services the employees’ payroll costs including pension contributions. MF UK had also made payments direct to MF Services’ pension scheme trustees.

On administration, this triggered Section 75 of the Pensions Act 1995 and a pension scheme debt of just over £35m arose. Although settlement was reached with the Pension Protection Fund and the pension scheme trustees in respect of the section 75 debt to be paid to the pension scheme trustees, the parties disagreed which of them should fund this. The administrators of MF UK made an application for the court to determine this issue.

Serena McAllisterSenior AssociateLondonT: +44 (0)20 7490 6394E: [email protected]

19

Arbitration clauses survive insolvency

Philpott and another v Lycée Français Charles de Gaulle School [2015] EWHC 1065 (Ch)Tom Pringle looks at a High Court decision which highlights the primacy of arbitration clauses in contractual documents, including after insolvency.

What has happened?The High Court has ruled that an arbitration clause in a construction contract survives insolvency, and that the insolvency set-off rules cannot be used to circumvent this. The ruling was given in an application for directions by the liquidators of a construction company in creditors’ voluntary liquidation, where there was a dispute as to monies due (by both parties) under the construction contract in question.

Whom does this affect and how?This decision will impact officeholders in insolvency proceedings, where there is a dispute (particularly between an insolvent debtor and creditor) surrounding a contract containing an arbitration clause.

The court ruled that the mandatory stay under the Arbitration Act 1996 effectively ‘trumped’ the set-off provisions of insolvency legislation. The taking of an account of sums due from each party to the other pursuant to Rule 4.90 of the Insolvency Rules 1986 required resolution of the dispute, which was subject to the arbitration clause.

It is now clear that officeholders cannot circumvent (potentially costly) arbitration proceedings provided for in certain contracts by seeking directions under the set-off provisions of insolvency legislation prior to resolution of the dispute by arbitration. This is likely to affect in particular those taking

appointments over insolvent construction companies, an industry where such clauses are common.

Next steps?This decision makes clear the supremacy of arbitration clauses in contractual documentation, regardless of insolvency proceedings. There will be limited scope for officeholders to attempt to circumvent arbitration clauses and arbitration legislation by pointing to insolvency proceedings and insolvency legislation instead.

Relevant background

A construction company (the “Company”) and a school (the “School”) were parties to a construction contract (the “Contract”) in a Joint Contracts Tribunal standard form. The School submitted a proof of debt in the insolvency of the Company for £270,000. The Company’s position was that it was in fact owed £615,000 by the School.

The liquidators had not yet decided whether to accept or reject the proof. As a result of the competing claims, their position was that they could not do so until the account of mutual dealings and set off under Insolvency Rule 4.90 had taken place.

The Contract contained an arbitration clause that applied to the dispute. The School’s position was that the arbitration clause remained binding after the Company’s administration and liquidation.

Where a dispute is subject to a valid arbitration clause, and a party brings legal proceedings in respect of that dispute, section 9 of the Arbitration Act 1996 applies. Under section 9(4) a court should grant a stay of those legal proceedings unless “the arbitration agreement is null and void, inoperative, or incapable of being performed”.

The High Court decided that any claim by the liquidators against the School for monies due would be subject to the arbitration clause. Therefore, the School could apply for such proceedings brought by the liquidator to be mandatorily stayed under section 9 of the Arbitration Act.

Tom PringleAssociateLondonT: +44 (0)20 7490 6971E: [email protected]

20

Olympic establishment decision

The Trustees of the Olympic Airlines SA Pension and Life Assurance Scheme (Appellants) v Olympic Airlines SA (Respondent) [2015] UKSC 27Rebecca James looks at this Supreme Court decision on what connection a foreign company must have with the UK to entitle an English court to wind it up, if its centre of main interests (“COMI”) is in another EU Member State.

What has happened?In October 2009, the Greek courts placed Olympic Airlines SA (“Airline”) into liquidation proceedings (which are still on-going in Greece). The trustees of the Airline’s pension scheme presented a petition to wind-up the Airline in the UK (in secondary proceedings) on 20 July 2010. However, the Airline argued that the English courts did not have jurisdiction to wind it up, because it no longer had an “establishment” in the UK, which was required by the EC Regulation (1346/2000) on Insolvency Proceedings (“EC Insolvency Regulation”). “Establishment” is defined in the EC Insolvency Regulation as “any place of operations where the debtor carries out a non-transitory economic activity with human means and goods”.

The Supreme Court dismissed the appeal by the pension scheme trustees, finding that the Airline did not have an “establishment” in the UK (within the meaning of the EC Insolvency Regulation) at the date of the trustees’ winding-up petition (which the parties had accepted was the relevant date). At this date, the Airline’s business activities had ceased and only three employees in England remained to carry out internal administration in connection with the Greek liquidation. The court found that, in order to show such an “establishment”, it was necessary to demonstrate some external business activities with third parties; internal administration, a brass plate on a door or the payment of outgoings were insufficient.

Whom does this affect and how?

This decision will affect parties (and in particular, pension scheme trustees) seeking to wind up the UK business of an insolvent employer whose COMI is in another EU Member State.

In order for (a) a pension scheme to qualify for entry into the Pension Protection Fund (“PPF”) pursuant to section 127 of the Pensions Act 2004, and (b) employees to claim their guaranteed debts from the National Insurance Fund (“NIF”), a qualifying “insolvency event” must have occurred. The trustees of the Airline pension scheme had petitioned for the winding-up of the Airline in the UK, in order to qualify for entry into the PPF.

This case demonstrates that, where an employer based in another EU Member State is in financial distress, UK pension scheme trustees need to act quickly to ensure that UK insolvency proceedings are opened whilst external business economic activities are still continuing in the UK.

Next steps?The race to open secondary insolvency proceedings in the UK in these situations will be removed by the new recast EC Regulation on Insolvency Proceedings (the “Recast Regulation”). The Recast Regulation provides a new definition of “establishment”, meaning “any place of operations where a debtor carries out or has carried out in the 3-month period prior to the request to open main insolvency proceedings a non-transitory economic activity with human means and assets;”

This 3 month look-back period will increase the likelihood of creditors being able to demonstrate the external business activity required for an “establishment” in the UK. These provisions in the Recast Regulation do not apply, however, until 26 June 2017.

More broadly, this case supports the argument for change to the underlying UK pensions and employment legislation to allow claims under the PPF and the NIF where there are main insolvency proceedings in another EU member state. This would simplify similar cross-border insolvency situations by avoiding multiple insolvency proceedings, which can be costly and disruptive.

Relevant backgroundThe Olympic Airlines’ pension scheme had a deficit of £16 million. The Airline is liable for the deficit pursuant to section 75 of the Pensions Act 1995, but the return in the Greek liquidation will be minimal. On 20 July 2010, the trustees presented a winding-up petition against the Airline in England, so that the scheme could qualify for entry into the PPF.

21

The English court’s jurisdiction to wind up the Airline in England was restricted by the EC Insolvency Regulation. This provides that main insolvency proceedings may only be opened in the EU Member State where a debtor’s COMI is situated (i.e. Greece, in this case). The courts of another member state may only open secondary proceedings in respect of a debtor if that debtor has an “establishment” (as defined in the EC Insolvency Regulation) within that Member State. Therefore, the English courts could only wind up the Airline if it had an “establishment” in the UK. It was accepted by the parties that the relevant time for this

assessment was at the date of the winding-up petition.

The Supreme Court found that the definition of “establishment” must be read as a whole, and envisages a fixed place of business from which a business activity, consisting in dealings with third parties, is carried out. The last of the Airline’s business had ceased some time before the presentation of the winding-up petition, and the remaining English employees were carrying out only internal administration for the Greek liquidator at the date of that petition. This was insufficient to show the external economic activity required

for there to be an “establishment” in the UK at the petition date. Therefore, the English courts did not have jurisdiction to open secondary insolvency proceedings in the UK.

The Olympic Airlines pension scheme was given relief outside of the courts by an amendment to the underlying pensions legislation specifically to allow the entry of the Olympic Airlines pension scheme into the PPF. The amending legislation was very narrowly drafted, however, and so is unlikely to assist in similar cases in the future without further legislative intervention.

Rebecca JamesAssociateLondonT: +44 (0)20 7667 7155E: [email protected]

Validation of property dispositions after a winding‑up petition

Wilson v SMC Properties Ltd [2015] EWHC 870 (Ch)Emily Walker reviews this High Court decision, which provides a useful summary on the court’s approach to granting validation orders under section 127 of the Insolvency Act.

What has happened?The High Court has set out its approach to granting validation orders, in considering an application to validate a transaction under section 127 of the Insolvency Act 1986. Section 127 provides that in a winding-up by the court, any disposition of the company’s property made after the commencement of the winding-up is void, unless the court otherwise orders.

Focusing on the principles behind section 127, the court validated the transaction (in circumstances where the sale of a property had taken place after a winding-up petition had been issued against a company, but before the winding-up order was made). The principles concerned are the fundamental insolvency principles to provide for a pari passu distribution of a company’s assets and prevent dissipation of assets to the detriment of unsecured creditors.

The court also considered the interaction between the requirements of good faith and the role of market value in the context of section 127. The court’s view was that good faith does not relate solely to knowledge of the winding-up petition, but also extends to the value of the transaction. The judge said that the court “would be slow to validate a transaction if there were a significant reduction in the Company’s assets”.

22

Whom does this affect and how?

This decision impacts on all relevant parties in the context of an application for a validation order under section 127, including officeholders, creditors and purchasers of assets from insolvent entities.

The case clarifies that, in considering applications for validation orders, the court will have regard to the fundamental insolvency principles behind validation orders, as well as whether (in its view) the particular disposition of property was made in good faith and at market value.

Purchasers need to be aware that the further away from market value a transaction is (or was), the less likely it is that the court will find that it is (or was) made in good faith.

Next steps?The court emphasised how such applications will be dealt with on a case by case basis and that the perspectives of both the general body of creditors and the innocent third party need to be considered.

The decision highlights that good faith alone is not enough for a purchaser to rely on; purchasers must bear in mind that they need to be able to justify the price paid for an asset and keep a record of any negotiations and formal valuations obtained in order to prove that the price paid was close to, if not, market value.

Purchasers are also advised to carry out insolvency searches prior to entering into a transaction with a company in order to establish whether the company is the subject of a winding-up petition. If necessary, the purchaser can then consider making an application for a validation order before the transaction is completed, as opposed to after the event.

Relevant backgroundThe purchaser bought a commercial property from a company that subsequently went into liquidation. The purchaser sought a validation order on the grounds that he had purchased the property in good faith, on arm’s length commercial terms and at fair market value. The liquidator resisted the application, arguing that the property had been sold at an undervalue.

In reaching its decision, the court considered earlier case, Denney v John Hudson & Co Ltd [1992] BCLC 901. The judge there found that a disposition made in good faith in the ordinary course of business when the parties were unaware that a winding-up petition had been presented would normally be validated, unless there are grounds for supposing that the payment was intended to prefer the recipient above other unsecured creditors. However, although good faith was a powerful factor in favour of validation, it must be weighed against the consequences of validating the payment and the extent to which validation would contradict the pari passu principle.

On the facts of this case, the court found that the purchaser had not known about the winding-up petition and had therefore acted in good faith. The court also determined that the value of the property was fair and, in doing so, had taken into account the fact that the sale was within the context of a tight time frame, imposed by a concerned and pressing secured creditor, who would have taken possession and sold the property as mortgagee in possession if not paid.

The transaction did not undermine the policy behind section 127, as it had not favoured a pre-liquidation creditor and there had been no loss to the creditors as a whole.

Emily WalkerSolicitorLeedsT: +44 (0)113 368 7794E: [email protected]

23

Administrators’ fees: You get nothing in life for free!

Randhawa and another v Turpin and another [2015] EWHC 517 (Ch)Andrew Robertson looks at a recent case in which the High Court rejected a challenge by creditors to the level of administrators’ fees, based on the creditors’ argument that the company should never have entered into administration.

What has happened?The High Court has rejected an application by two creditors (the “Applicants”) for an order that:

1. the remuneration of the administrators of BW Estates Limited (the “Company”) was excessive and should be disallowed entirely or reduced to the extent the court felt appropriate; and

2. the administrators pay the costs of the application personally, as opposed to being an expense of the administration.

The Applicants argued that the administrators were never in a position to confirm that one of the statutory purposes of administration could be achieved because there was no good reason for the Company to go into administration, and the administrators were therefore not entitled to their fees for the work they had undertaken as administrators. The court rejected this argument and ordered that (in the first instance) the costs of the application should be paid by the Applicants.

Whom does this affect and how?The judgment is relevant to all insolvency practitioners when considering whether to make the statutory declaration that the purposes of administration could be achieved.

It is clear that, unless bad faith or breach of duty by the directors can be shown, the motive for appointing an administrator will be treated entirely separately to the

proposed administrator’s decision for making the statement that the purposes of administration could be achieved.

Administrators should be reassured that courts will look to respect administrators’ reasoning for making such a statement. The court will be unlikely to find that an administrator had no basis whatsoever to make a statement that the statutory purpose of an administration could be achieved.

Next steps?The ruling highlights the court’s reluctance to order that administration fees should be disallowed, unless they are entirely certain that the administration should not have been entered into. Creditors considering this type of application should bear this in mind.

Relevant backgroundIn a separate earlier dispute, the Applicants had secured a charging order against a shareholder and former director of the Company, providing the Applicants with an interest in the Company. Missed mortgage payments by the Company relating to their properties prompted the lending bank to appoint a receiver. It was then decided by a director of the Company to appoint administrators.

The Applicants’ overall contention was that there was no good reason for the Company to go into administration, and that the administration was deployed as a means to deplete the Company’s assets, rendering the charging order less valuable. The Applicants

therefore bought (at full value) a debt owed by the Company to its former solicitors, enabling the Applicants to bring a challenge to the administration as creditors of the Company.

The Applicants sought to rely on rule 2.109 of the Insolvency Rules 1986, which enables creditors of a Company in administration to challenge the level of administrators’ fees. The Applicants contended that the administrators were never in a position to confirm that one of the statutory purposes of administration could be achieved, so were not entitled to remuneration. They argued that the Company was in exactly the same position coming out of administration as it was entering administration, except that the Company’s assets had been reduced.

The court ruled that the director’s reasoning for making the administration appointment was not relevant to considering whether the administrators should have made the statement as to the purpose of the administration. The court indicated that it is not necessarily wrong to appoint an administrator where a bolder director may have taken some other course of action.

As to the costs of the application, the judge felt there was no reason to depart from the convention that the applicant pays the cost of the application it has brought. However, the court indicated that this matter would be revisited at a later hearing, which would be listed to determine the level of remuneration which the administrators should receive.

Andrew Robertson AssociateLondonT: +44 (0)20 7490 6172E: [email protected]

24

Sanction of scheme of arrangement

Re Van Gansewinkel Groep BV and others [2015] EWHC 2151 (Ch)Rebecca James reviews this decision by the High Court, which sanctioned a scheme of arrangement where creditors were domiciled in England, however cautioned that English law and one-way English jurisdiction clauses may not be enough to establish jurisdiction of the English courts.

What has happened?The High Court has sanctioned schemes of arrangement proposed by a group of five Dutch companies and one Belgian company, which have their centre of main interests in the Netherlands and Belgium, and no establishment or significant assets within England and Wales. The schemes are part of a restructuring of the group’s financial indebtedness, the terms of which are governed by English law, and several of the creditors are domiciled in England.

The case gives rise to three main points of note:

1. The High Court found that, following Re Rodenstock [2011] EWHC 1104 (Ch), the English courts had jurisdiction to sanction the schemes under the Recast Judgments Regulation (defined below) as a result of a number of the company’s creditors being domiciled in England.

Interestingly, in this case, a much smaller proportion of the scheme creditors were domiciled in England than in Re Rodenstock (where more than 50%, by value, of the scheme creditors were domiciled here). The court found that there was no requirement for a certain number or value of a company’s creditors to be in England and Wales to establish jurisdiction and indeed the domicile of a single creditor in England and Wales could be sufficient.

2. The High Court rejected the companies’ arguments that the English governing law and jurisdiction clauses in the facility agreements subject to the scheme were sufficient to establish the jurisdiction of the English courts. The High Court found that the jurisdiction clauses were

one-way, binding the companies only and not the relevant scheme creditors. Therefore, the jurisdiction clauses could not be used to establish the jurisdiction of the English courts over the scheme creditors for the purposes of the scheme.

3. In reaching its decision, the court was at pains to emphasise that the court does not rubber stamp schemes of arrangement, even where the scheme has the support of an overwhelming majority of creditors. The court considered that the procedure adopted in the case, and the level of evidence provided, was not satisfactory – see the ‘Next steps’ section below for further details.

Whom does this affect and how?

This decision affects overseas companies who are considering seeking a scheme of arrangement under Part 26 of the Companies Act 2006, and their creditors (whether supporting or objecting).

The decision shows the continuing willingness of the English courts to sanction schemes of arrangement, even where only a small number of a company’s creditors are based in England.

However, if the court’s ruling on one-way jurisdiction clauses is followed, this could present difficulties for overseas companies in establishing scheme jurisdiction where they do not have any creditors based in England. One-way jurisdiction clauses are commonly found in English law facility agreements.

Next steps?The court gave some useful procedural guidance for foreign companies seeking sanction for schemes of arrangement in the future, which included the following: