Embed Size (px)

Citation preview

Restoring Trust in Finance: Moral Obligation meets Econ 101

Gordon Menzies Thomas Simpson

Donald Hay David Vines

Outline

1. What I didn't understand about finance 2. Financial firms have a bad reputation 3. The departure of the ‘gentlemen bankers’ 4. Is losing moral restraint costly? 5. Does competition policy work for banking? 6. Addressing banker trustworthiness

Logic of Argument

1. What I didn't understand about finance 2. Financial firms have a bad reputation 3. The departure of the gentlemen bankers 4. Is losing moral restraint costly? 5. Does competition policy work for banking? 6. Addressing banker trustworthiness

Logic of Argument

1. What I didn't understand about finance 2. Financial firms have a bad reputation 3. The departure of the gentlemen bankers 4. Is losing moral restraint costly? yes 5. Does competition policy work for banking? no 6. Addressing banker trustworthiness is desirable … and maybe some of us have a role to play

Outline

1. What I didn't understand about finance 2. Financial firms have a bad reputation 3. The departure of the gentlemen bankers 4. Is losing moral restraint costly? 5. Does competition policy work for banking? 6. Addressing banker trustworthiness

1. What I didn't understand about finance

• RBA experience forced my simple theories aside…

Uncovered Interest Parity (UIP) and the carry trade

• On average you can earn foreign exchange returns by chasing high interest rates (you shouldn’t be able to: failure of UIP)

• “on average”

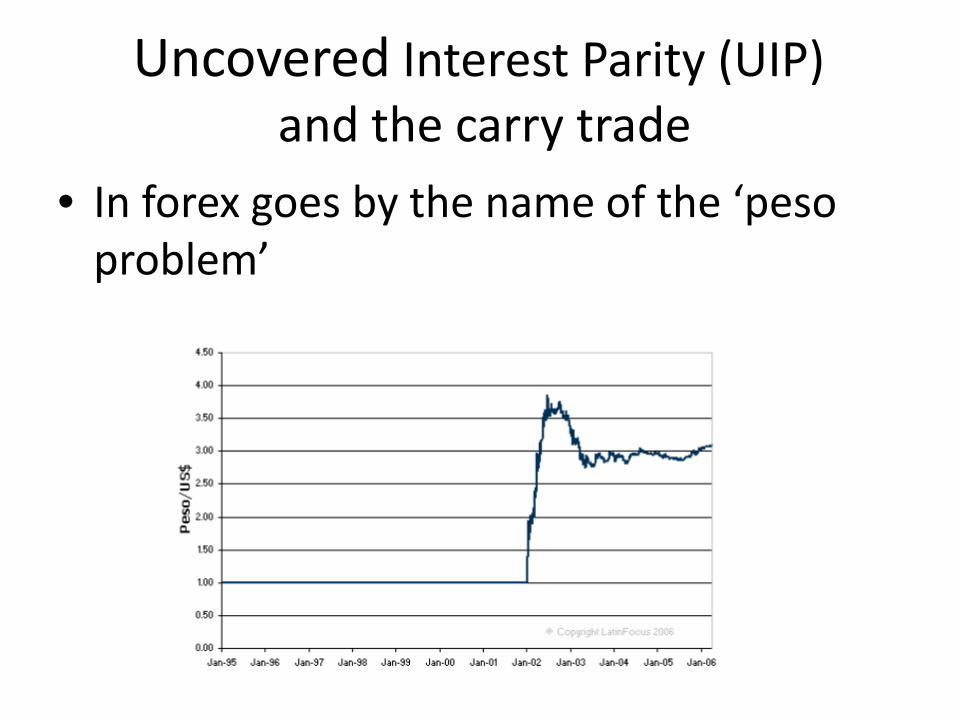

Uncovered Interest Parity (UIP) and the carry trade

• In forex goes by the name of the ‘peso problem’

1. What I didn't understand about finance

• The real world throws up strange ways of making money inconsistent with theory

• Some of these ways involve making small amounts of money for a long time but being subject to a risk of losing a lot of money without warning

• There are temptation for financial firms to mislead clients

Outline

1. What I didn't understand about finance 2. Financial firms have a bad reputation 3. The departure of the gentlemen bankers 4. Is losing moral restraint costly? 5. Does competition policy work for banking? 6. Addressing banker trustworthiness

Bad enough to film …

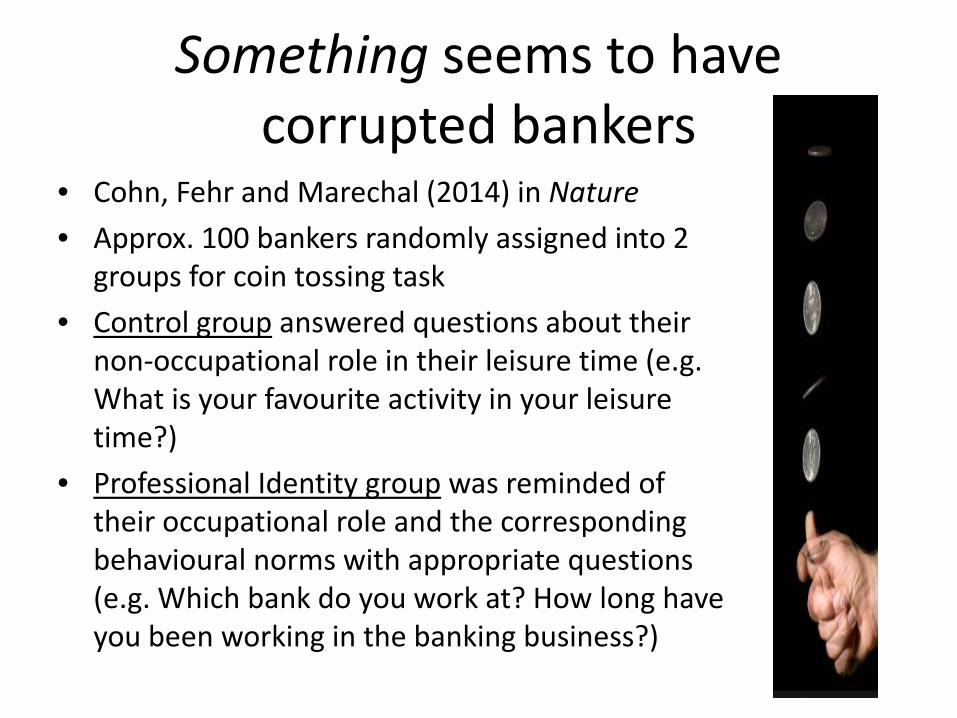

Something seems to have corrupted bankers

• Cohn, Fehr and Marechal (2014) in Nature • Approx. 100 bankers randomly assigned into 2

groups for coin tossing task • Control group answered questions about their

non-occupational role in their leisure time (e.g. What is your favourite activity in your leisure time?)

• Professional Identity group was reminded of their occupational role and the corresponding behavioural norms with appropriate questions (e.g. Which bank do you work at? How long have you been working in the banking business?)

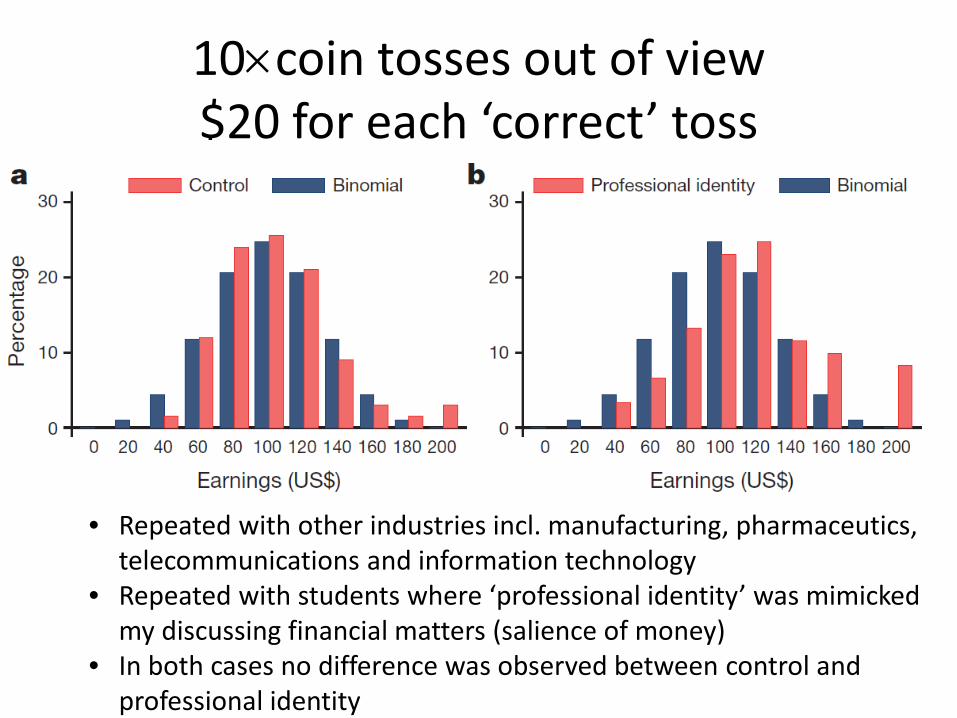

10×coin tosses out of view $20 for each ‘correct’ toss

• Repeated with other industries incl. manufacturing, pharmaceutics, telecommunications and information technology

• Repeated with students where ‘professional identity’ was mimicked my discussing financial matters (salience of money)

• In both cases no difference was observed between control and professional identity

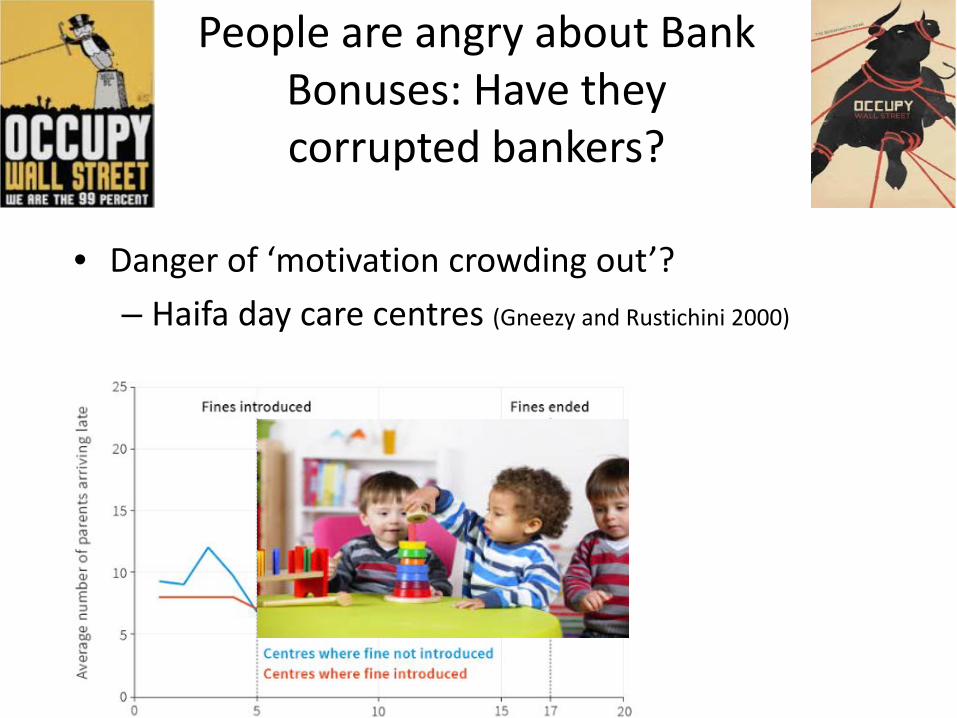

People are angry about Bank Bonuses: Have they corrupted bankers?

• Danger of ‘motivation crowding out’? – Haifa day care centres (Gneezy and Rustichini 2000)

Outline

1. What I didn't understand about finance 2. Financial firms have a bad reputation 3. The departure of the gentlemen bankers 4. Is losing moral restraint costly? 5. Does competition policy work for banking? 6. Addressing banker trustworthiness

3. The Departure of Gentlemen Bankers

In the UK Banking was once a gentlemen’s club where the members monitored themselves and were risk averse. Firms and partnerships not ‘fit and proper’ suffered penalties and even exclusion from the club

They had financed the Empire

• ‘The City’ (of London) supported economy for centuries. By the C20th : – running worldwide sterling payments mechanism – attracting and investing funds – markets for securities, derivatives and commodities – financing projects worldwide – insurance

What was banking doing during the ‘Atlee era’?

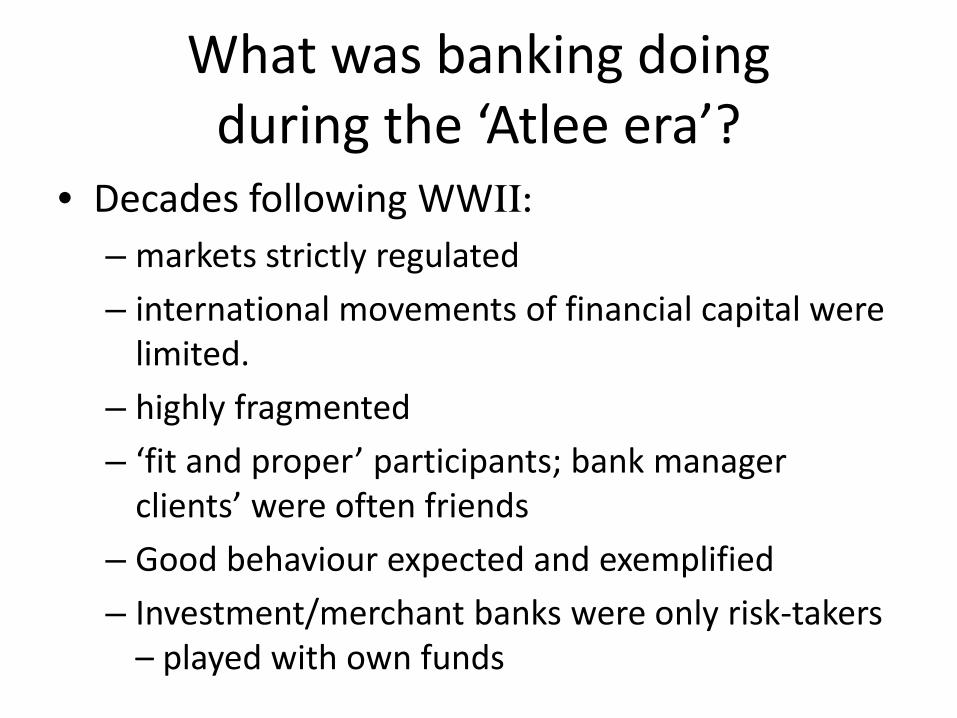

• Decades following WWII: – markets strictly regulated – international movements of financial capital were

limited. – highly fragmented – ‘fit and proper’ participants; bank manager

clients’ were often friends – Good behaviour expected and exemplified – Investment/merchant banks were only risk-takers

– played with own funds

The end of an era

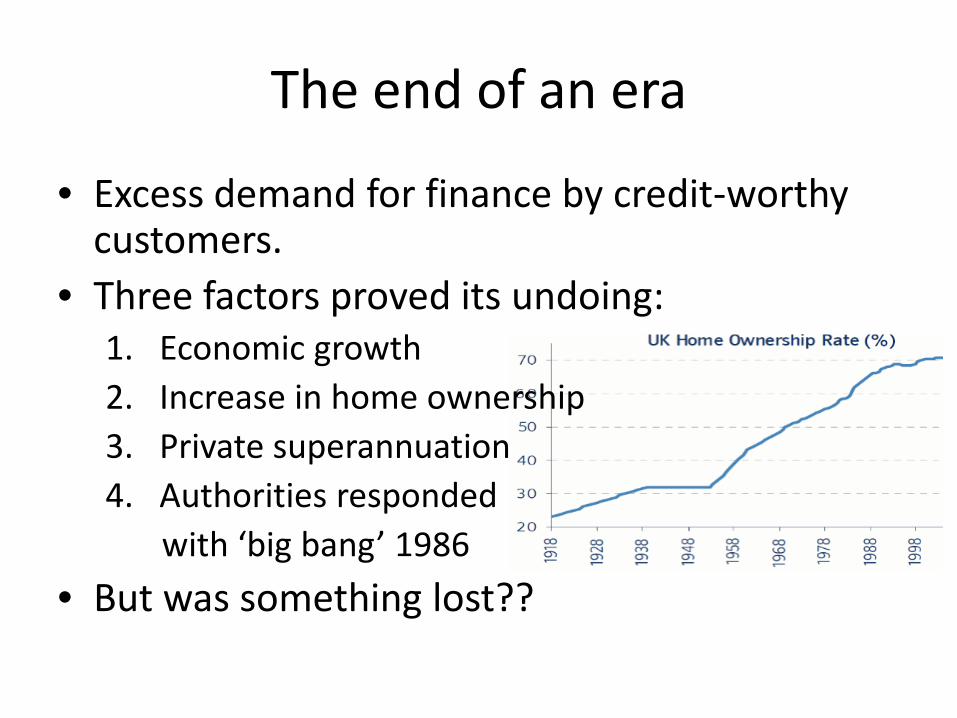

• Excess demand for finance by credit-worthy customers.

• Three factors proved its undoing: 1. Economic growth 2. Increase in home ownership 3. Private superannuation 4. Authorities responded with ‘big bang’ 1986

• But was something lost??

• Maybe motivation crowding out through bonuses

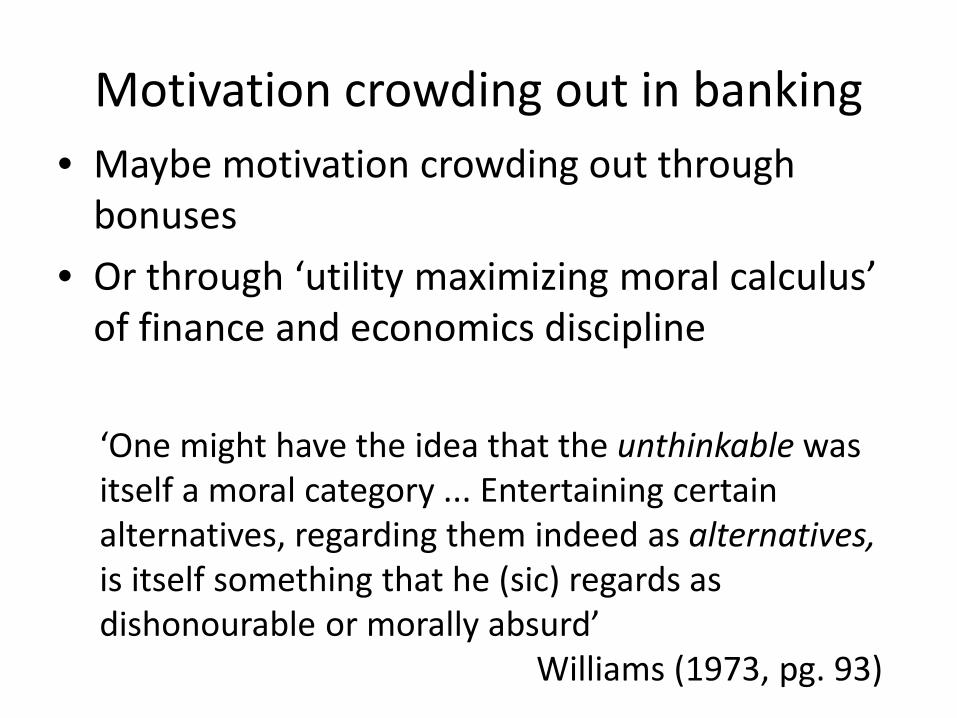

• Or through ‘utility maximizing moral calculus’ of finance and economics discipline

‘One might have the idea that the unthinkable was itself a moral category ... Entertaining certain alternatives, regarding them indeed as alternatives, is itself something that he (sic) regards as dishonourable or morally absurd’ Williams (1973, pg. 93)

Motivation crowding out in banking

Thinking the Unthinkable?

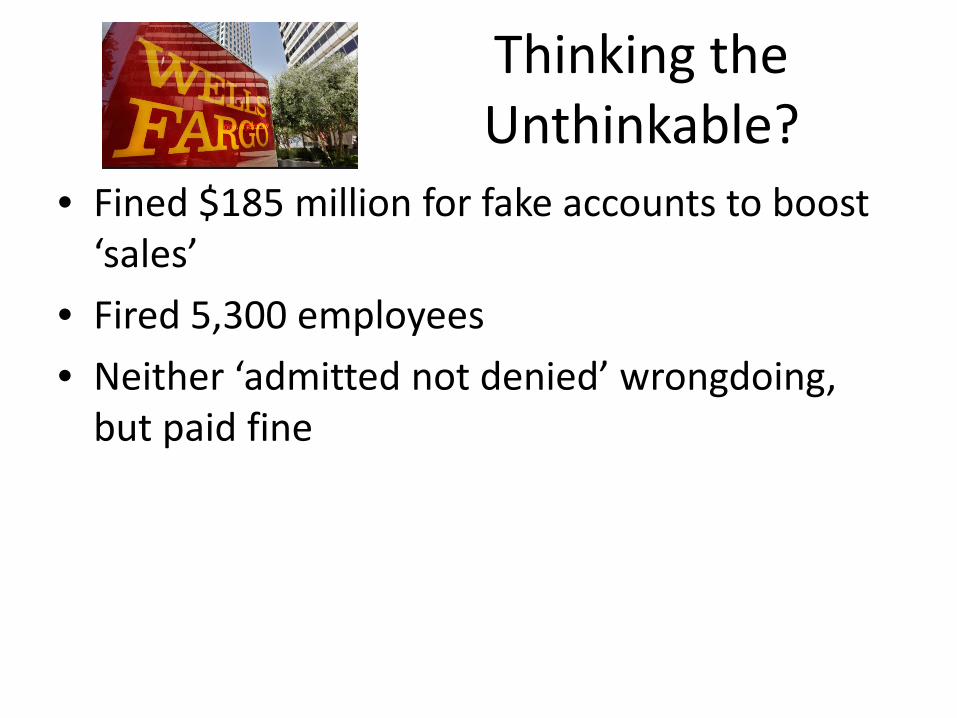

• Fined $185 million for fake accounts to boost ‘sales’

• Fired 5,300 employees • Neither ‘admitted not denied’ wrongdoing,

but paid fine

How could the management of such a firm fail to resign immediately as a matter of a moral principle? – only by doing an instrumental calculation and deciding they could ‘ride it out’.

Thinking the Unthinkable?

• Such a calculation is itself a reprehensible moral

act, according to Williams, even if they had resigned

• The calculation arises from ‘cost benefit’ thinking applied to morality courtesy of an economics or finance training, which encourages the idea that everything boils down to a cost benefit calculation

Thinking the Unthinkable?

Outline

1. What I didn't understand about finance 2. Financial firms have a bad reputation 3. The departure of the gentlemen bankers 4. Is losing moral restraint costly? 5. Does competition policy work for banking? 6. Addressing banker trustworthiness

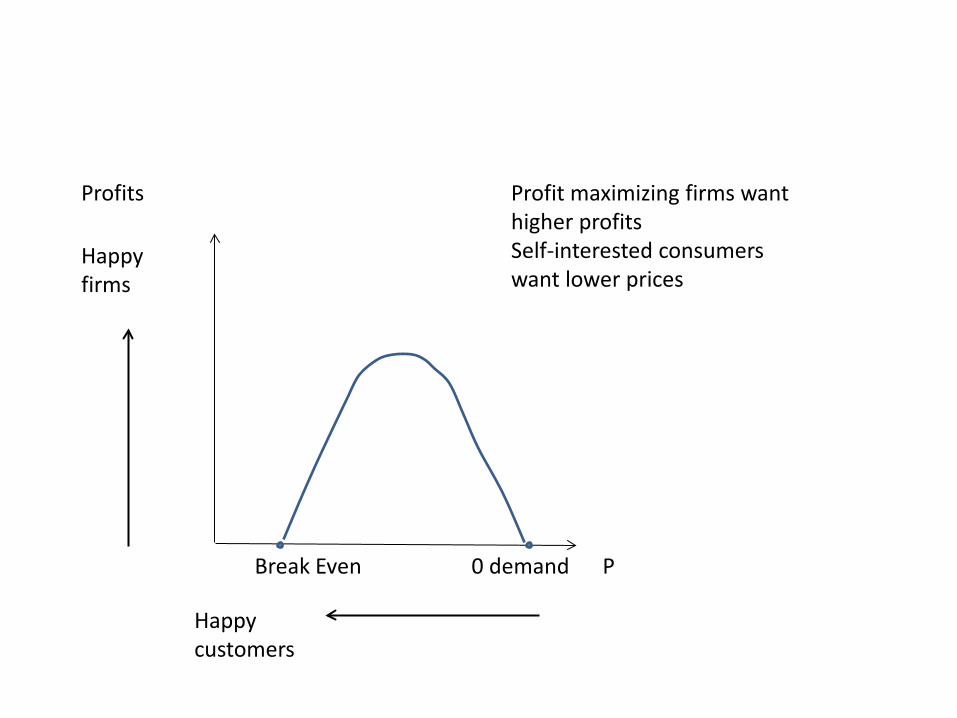

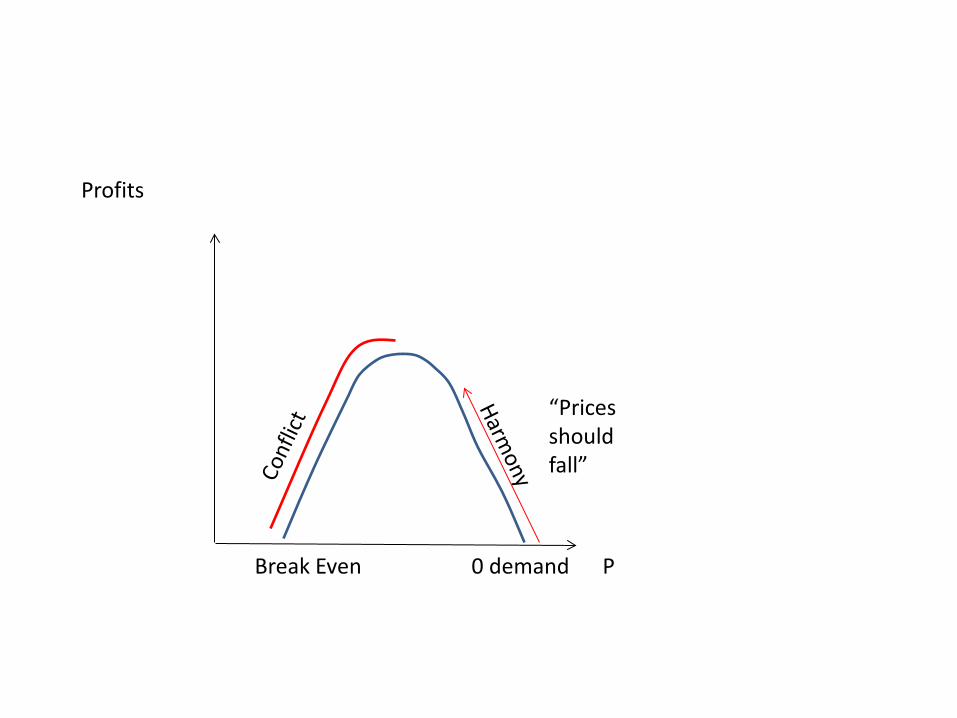

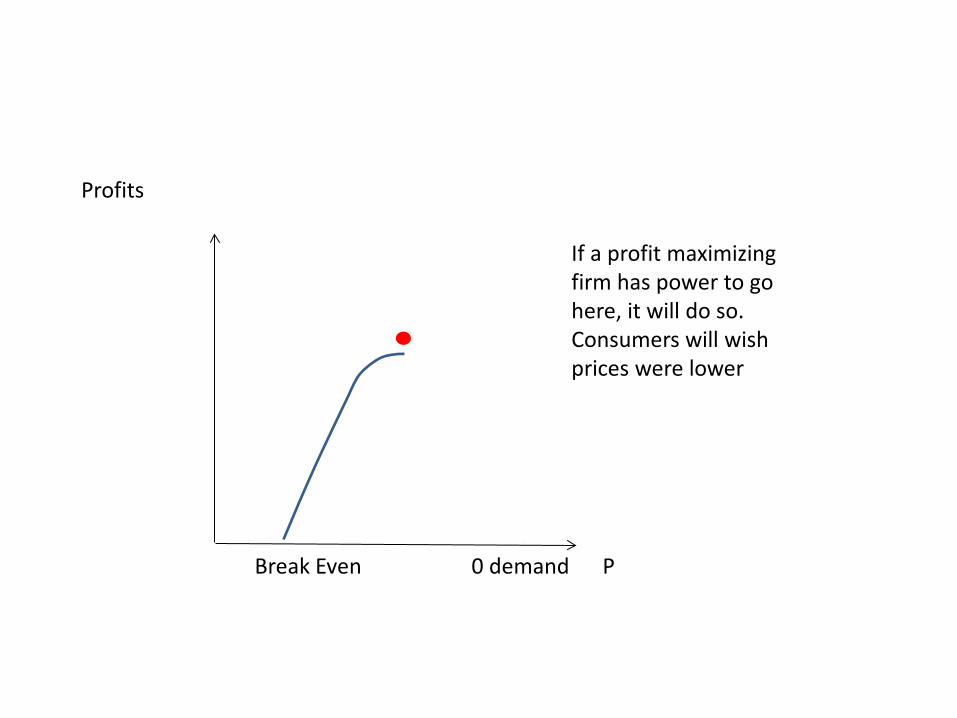

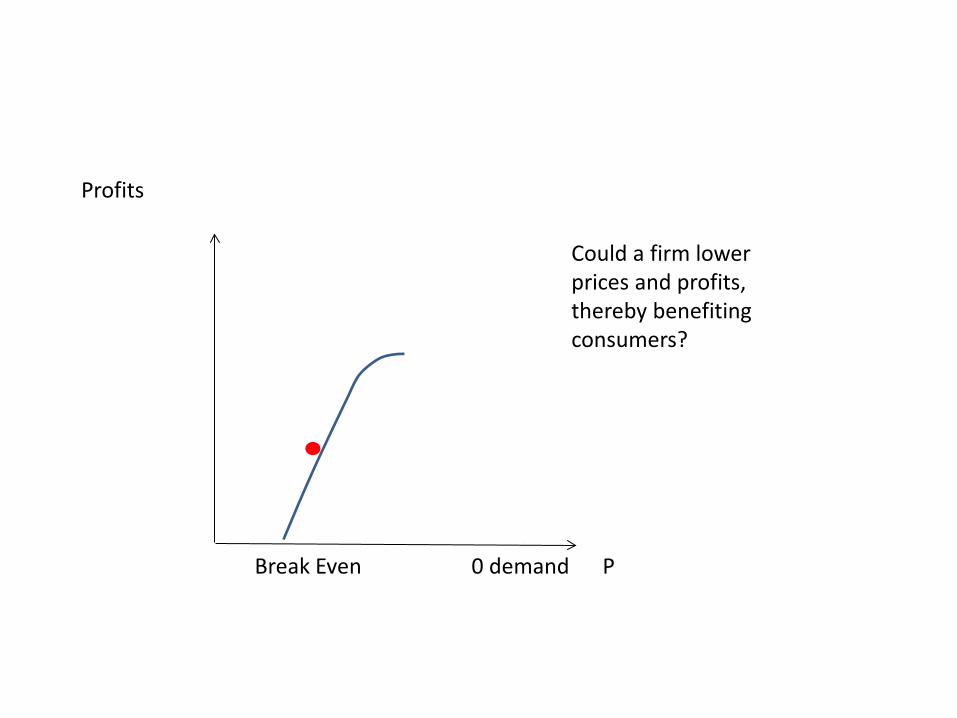

Case Study: A monopolist who doesn’t maximize profits

• The gentlemen’s banker club was an oligopoly that exploited market power to some extent

• But probably not as much as current generation immediately before 2008

• Let’s describe the club as a monopolist that shows restraint by not fully exploiting monopoly power

• This helps us think about moral restraint and to introduce a new idea

Profits

Break Even 0 demand P

Profit maximizing firms want higher profits Self-interested consumers want lower prices

Happy firms

Happy customers

Profits

Break Even 0 demand P

“Prices should fall”

Profits

If a profit maximizing firm has power to go here, it will do so. Consumers will wish prices were lower

Break Even 0 demand P

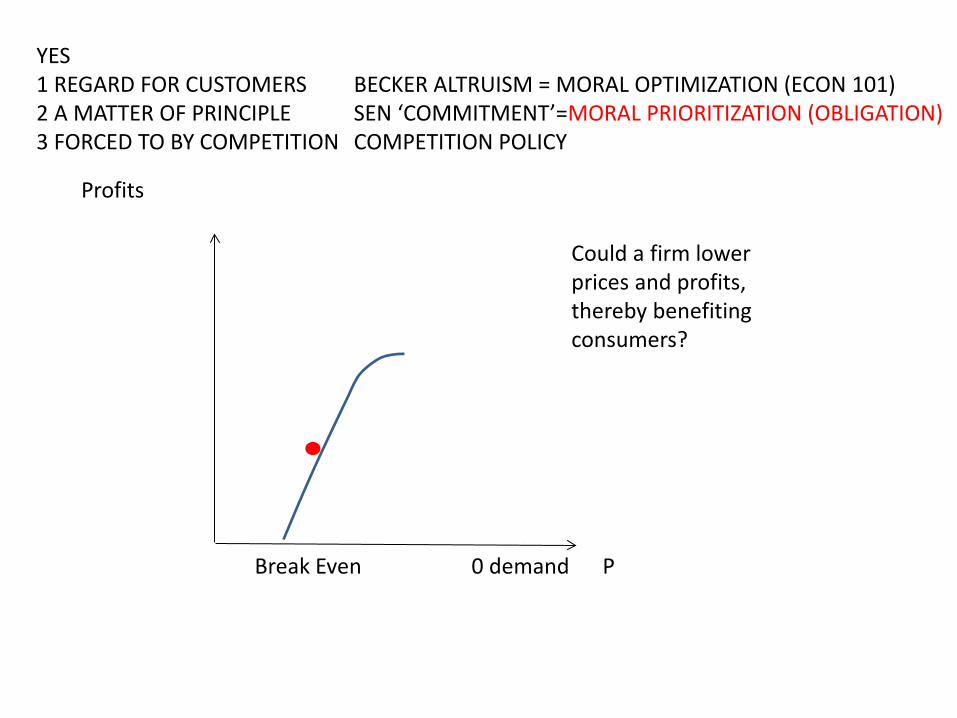

Profits

Could a firm lower prices and profits, thereby benefiting consumers?

Break Even 0 demand P

Profits

Could a firm lower prices and profits, thereby benefiting consumers?

YES 1 REGARD FOR CUSTOMERS 2 A MATTER OF PRINCIPLE 3 FORCED TO BY COMPETITION

BECKER ALTRUISM = MORAL OPTIMIZATION (ECON 101) SEN ‘COMMITMENT’=MORAL PRIORITIZATION (OBLIGATION) COMPETITION POLICY

Break Even 0 demand P

Profits

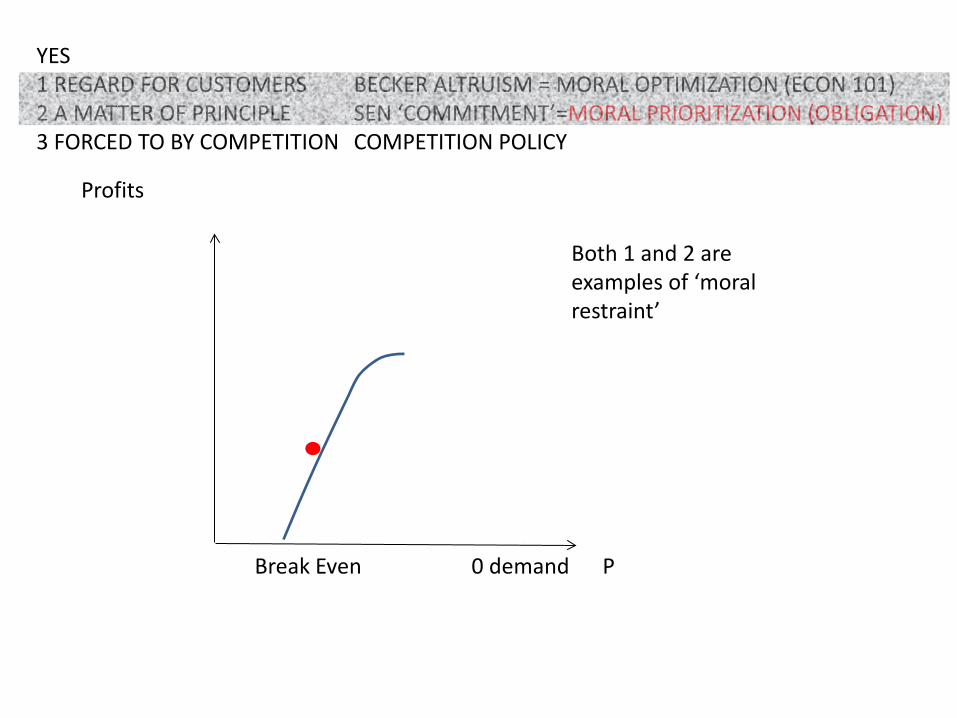

Both 1 and 2 are examples of ‘moral restraint’

YES 1 REGARD FOR CUSTOMERS 2 A MATTER OF PRINCIPLE 3 FORCED TO BY COMPETITION

BECKER ALTRUISM = MORAL OPTIMIZATION (ECON 101) SEN ‘COMMITMENT’=MORAL PRIORITIZATION (OBLIGATION) COMPETITION POLICY

Break Even 0 demand P

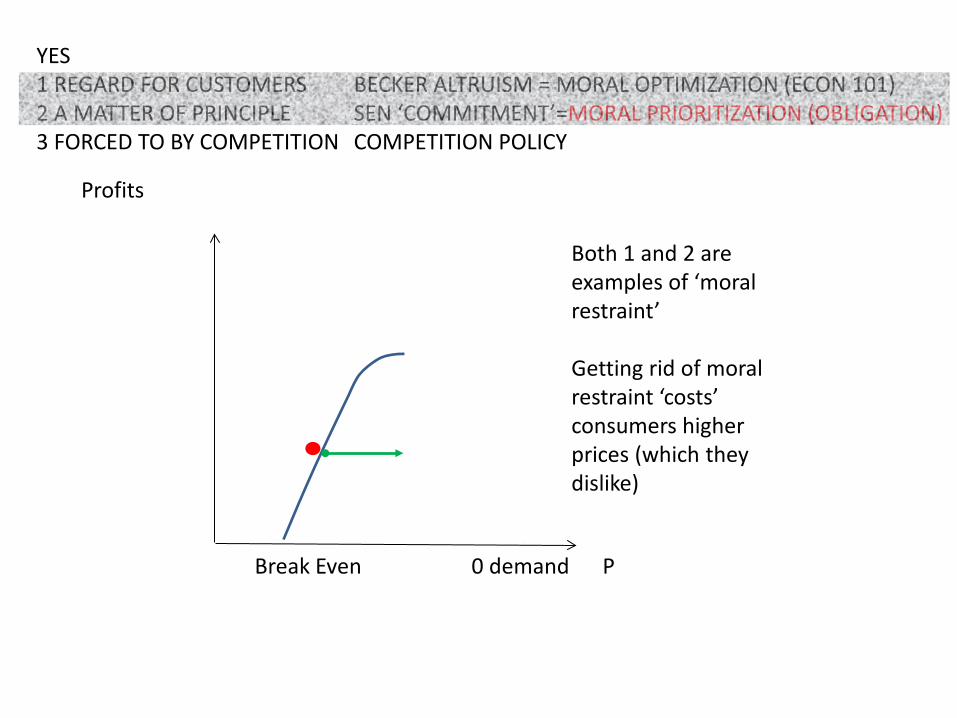

Profits

Both 1 and 2 are examples of ‘moral restraint’ Getting rid of moral restraint ‘costs’ consumers higher prices (which they dislike)

Break Even 0 demand P

YES 1 REGARD FOR CUSTOMERS 2 A MATTER OF PRINCIPLE 3 FORCED TO BY COMPETITION

BECKER ALTRUISM = MORAL OPTIMIZATION (ECON 101) SEN ‘COMMITMENT’=MORAL PRIORITIZATION (OBLIGATION) COMPETITION POLICY

Moral Obligation meets Econ 101

• ‘Moral prioritization’ is our contribution • It is the vehicle for moral obligation to find its

way into decisions • In this example both sorts of moral restraint

can lead to the same outcome • But this is not always so… • Two examples to make the distinction clearer

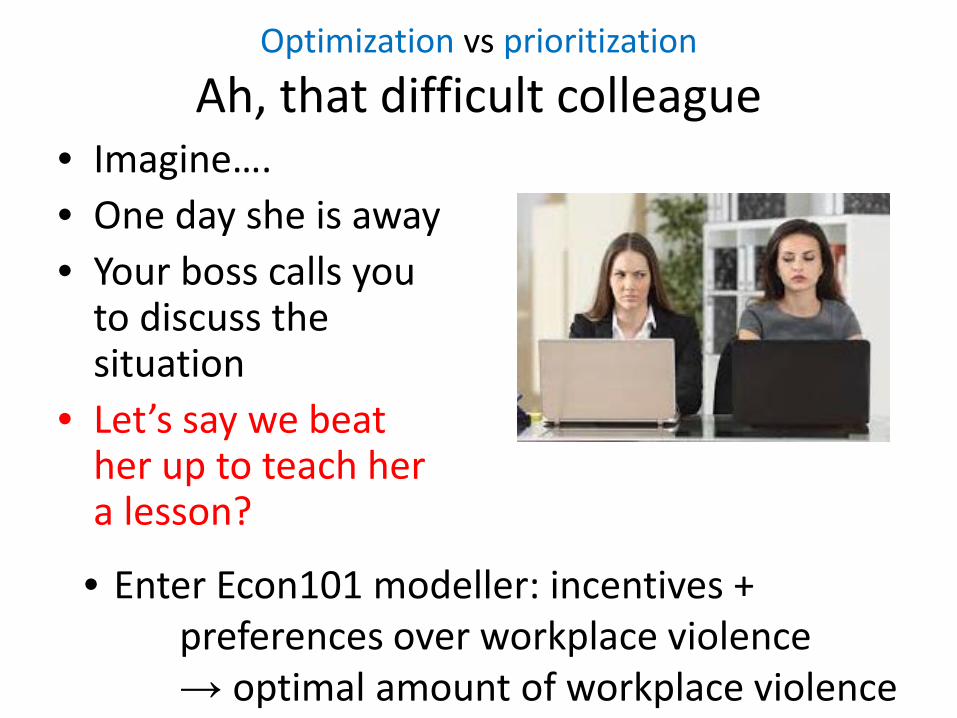

Optimization vs prioritization

Ah, that difficult colleague • Imagine…. • One day she is away • Your boss calls you

to discuss the situation

• Let’s say we beat her up to teach her a lesson?

• Enter Econ101 modeller: incentives + preferences over workplace violence → optimal amount of workplace violence

‘Optimal workplace violence’ is not how most people think

• Most people regard certain actions as ‘unthinkable’ for moral decisions. ‘no violence’ is moral prioritization

• ‘One might have the idea that the unthinkable was itself a moral category ... Entertaining certain alternatives, regarding them indeed as alternatives, is itself something that he (sic) regards as dishonourable or morally absurd’ Williams (1973, pg. 93)

• Moral optimization, on the other hand, might be about choosing a ‘low’ amount of optimal workplace violence out of concern for your colleague.

Optimization vs prioritization

Ah, those caring fund managers • Fund manager is advising a client about a

favourable investment opportunity which nonetheless has a 5% chance of a very bad outcome

• The client enjoys ‘gets utility’ from feeling she is a smart investor who chooses good fund managers and she really enjoys looking forward to earning high returns

Optimization vs Prioritization • Moral optimization makes the stated probability of a

bad outcome a choice variable to optimize • It may be ‘optimal’ for the manager to lie and state a

lower probability of failure. In the most likely state of affairs (the investment earns a good return) everyone is very happy. A ‘moral’ fund manager will weigh the client’s desire to look forward to a good return very heavily, and may say the probability is much lower than 5 per cent!

• Moral prioritization says the manager owes the client his best estimate of the probability of failure.

Is moral restraint worth thinking about?

• If moral restraint of either sort is hard to come by, maybe there is a shortcut through more competition (bank example)

• Competition is also an attractive solution to things like lying – if there are plenty of firms to choose from, a reputation for dishonesty could spell disaster for the dishonest firm

• Does competition policy work for banking?

Outline

1. What I didn't understand about finance 2. Financial firms have a bad reputation 3. The departure of the gentlemen bankers 4. Is losing moral restraint costly? 5. Does competition policy work for banking? 6. Addressing banker trustworthiness

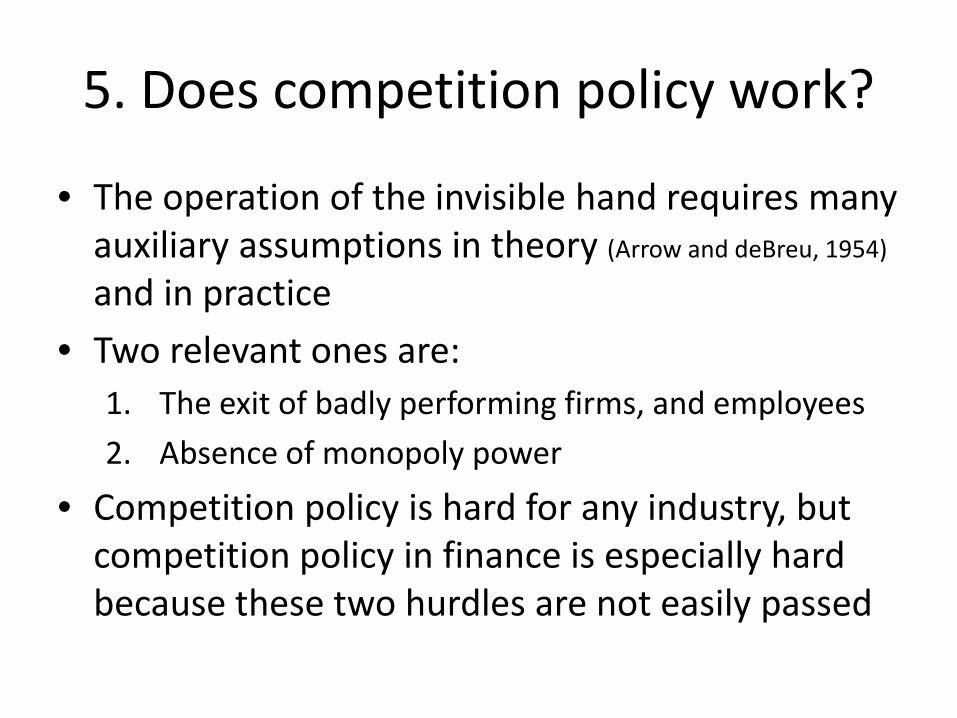

5. Does competition policy work?

• The operation of the invisible hand requires many auxiliary assumptions in theory (Arrow and deBreu, 1954)

and in practice • Two relevant ones are:

1. The exit of badly performing firms, and employees 2. Absence of monopoly power

• Competition policy is hard for any industry, but competition policy in finance is especially hard because these two hurdles are not easily passed

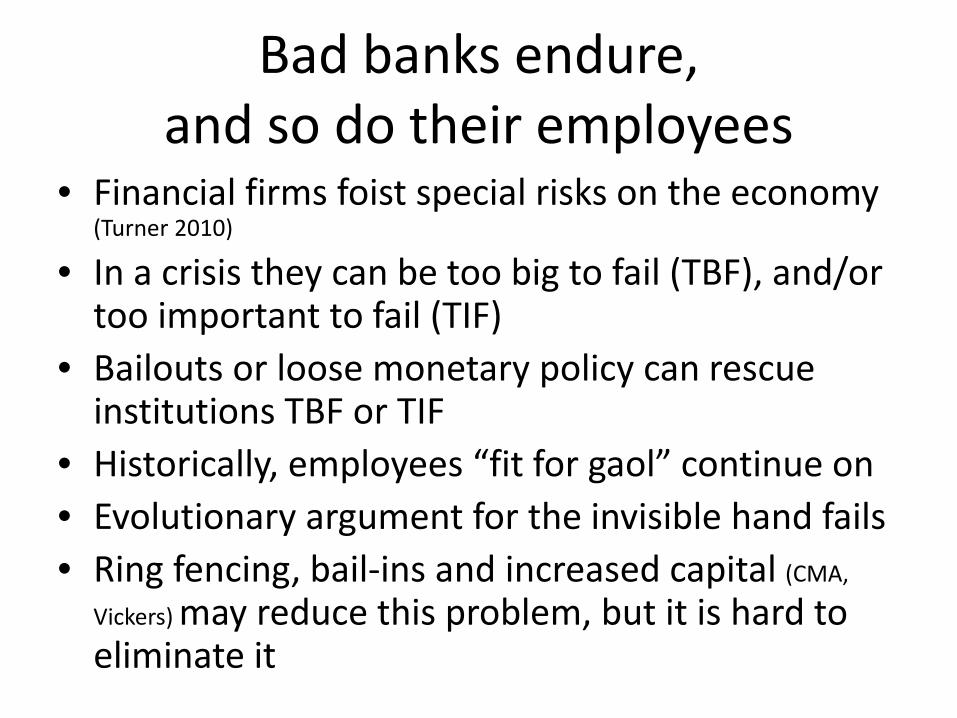

Bad banks endure, and so do their employees

• Financial firms foist special risks on the economy (Turner 2010)

• In a crisis they can be too big to fail (TBF), and/or too important to fail (TIF)

• Bailouts or loose monetary policy can rescue institutions TBF or TIF

• Historically, employees “fit for gaol” continue on • Evolutionary argument for the invisible hand fails • Ring fencing, bail-ins and increased capital (CMA,

Vickers) may reduce this problem, but it is hard to eliminate it

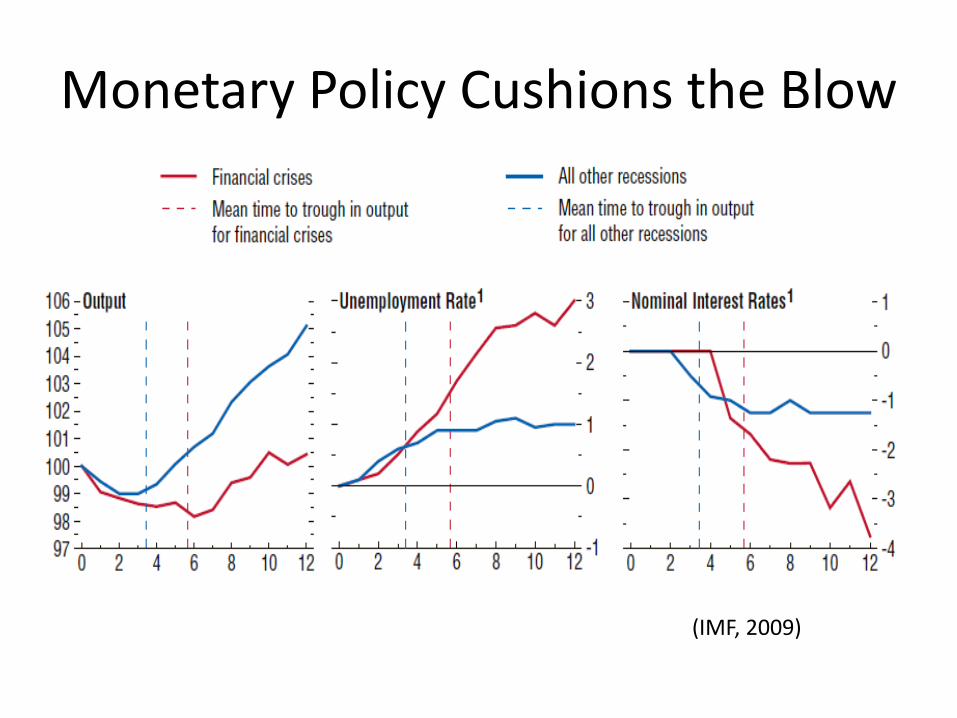

Monetary Policy Cushions the Blow

(IMF, 2009)

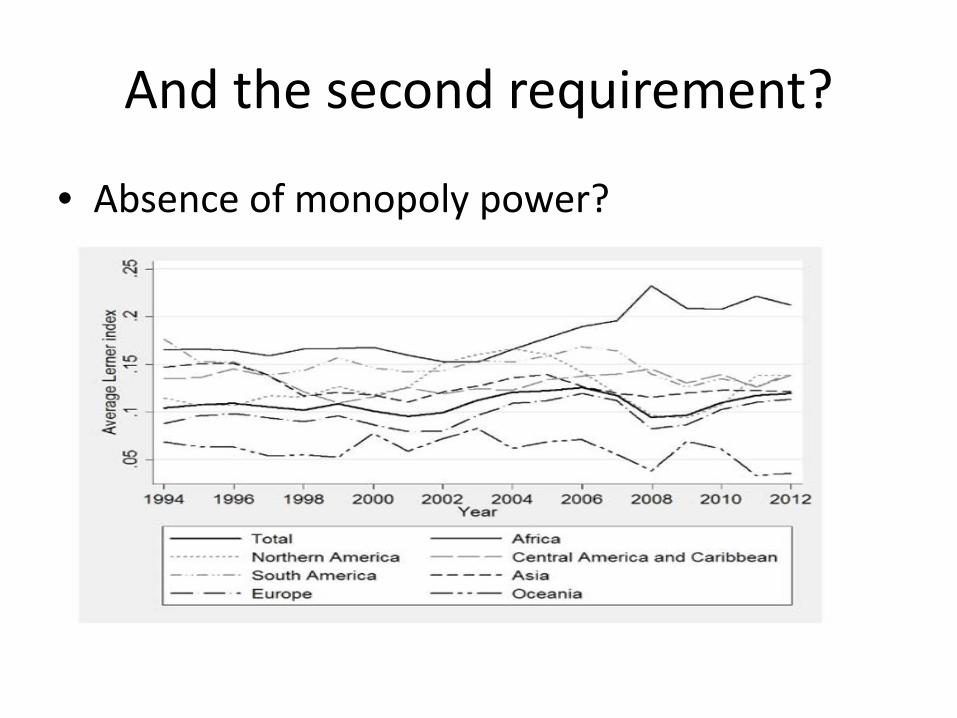

And the second requirement?

• Absence of monopoly power?

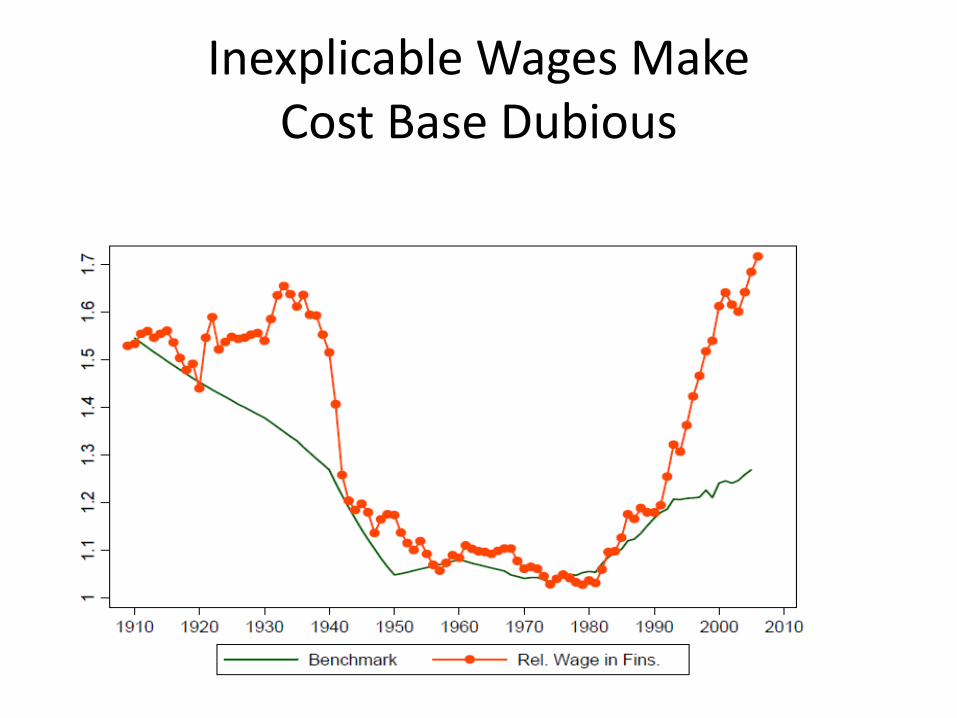

Inexplicable Wages Make Cost Base Dubious

• Remember the carry trade? • It stands as an instance of a whole range of

strategies which are profitable in the short term by piling up risk in ‘the tails’

• Noe & Peyton Young (2014) outline some examples of these strategies

• When the tail event happens, the investor loses everything, but the fund manager merely fails to get his or her bonus

How do we interpret profits anyway?

• a regulator may choose to not pursue a complex competition case against a bank

• This could lead to a higher bar of misbehaviour that triggers court action for banking vis a vis other industries and a greater degree of monopoly power in practice

• This may also help explain the lack of litigation against managers after 2008

And try taking a bank to court….

Competition policy has been hard in the UK

• Vickers (2011) noted high concentration and switching costs

• Promoted challenger banks • Comp and Markets Authority (2016) noted

continued high concentration but integration of investment and banking meant it couldn’t conclude monopoly power existed in retail banking

• Consumers (for whom banking fees are a tiny fraction of budget) display inertia

5. Does competition policy work? No

• The operation of the invisible hand requires many auxiliary assumptions in theory (Arrow and

deBreu, 1954) and in practice • Two relevant ones are:

1. Badly performing firms, and employees, exit 2. Absence of monopoly power

• All competition policy is hard, but competition policy in finance is especially hard because these two hurdles are not easily passed

Outline

1. What I didn't understand about finance 2. Financial firms have a bad reputation 3. The departure of the gentlemen bankers 4. Is losing moral restraint costly? 5. Does competition policy work for banking? 6. Addressing banker trustworthiness

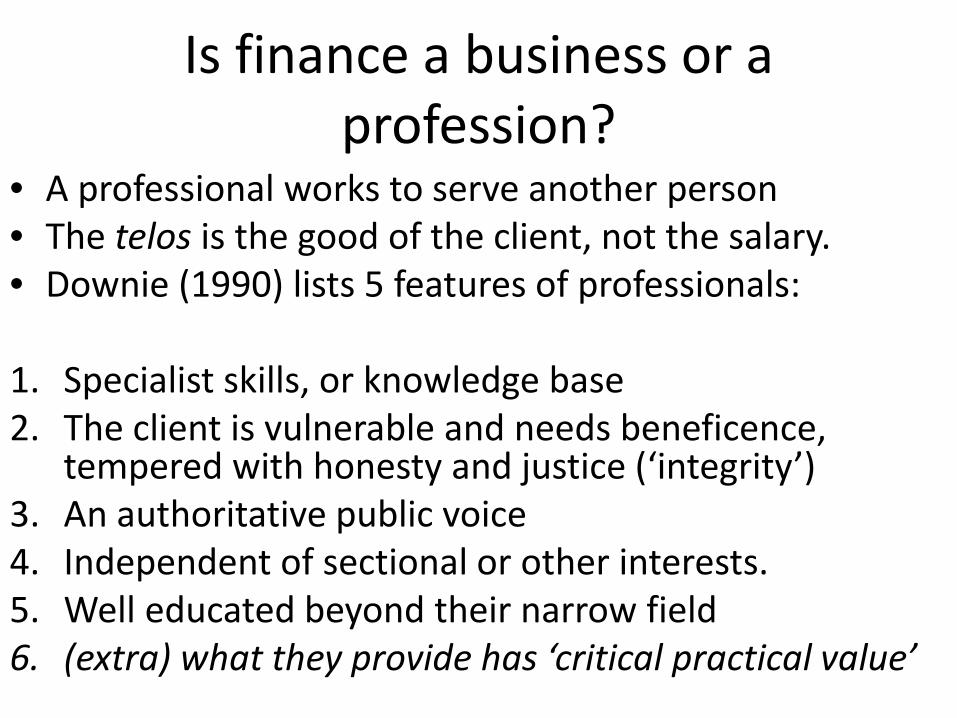

Is finance a business or a profession?

• A professional works to serve another person • The telos is the good of the client, not the salary. • Downie (1990) lists 5 features of professionals:

1. Specialist skills, or knowledge base 2. The client is vulnerable and needs beneficence,

tempered with honesty and justice (‘integrity’) 3. An authoritative public voice 4. Independent of sectional or other interests. 5. Well educated beyond their narrow field 6. (extra) what they provide has ‘critical practical value’

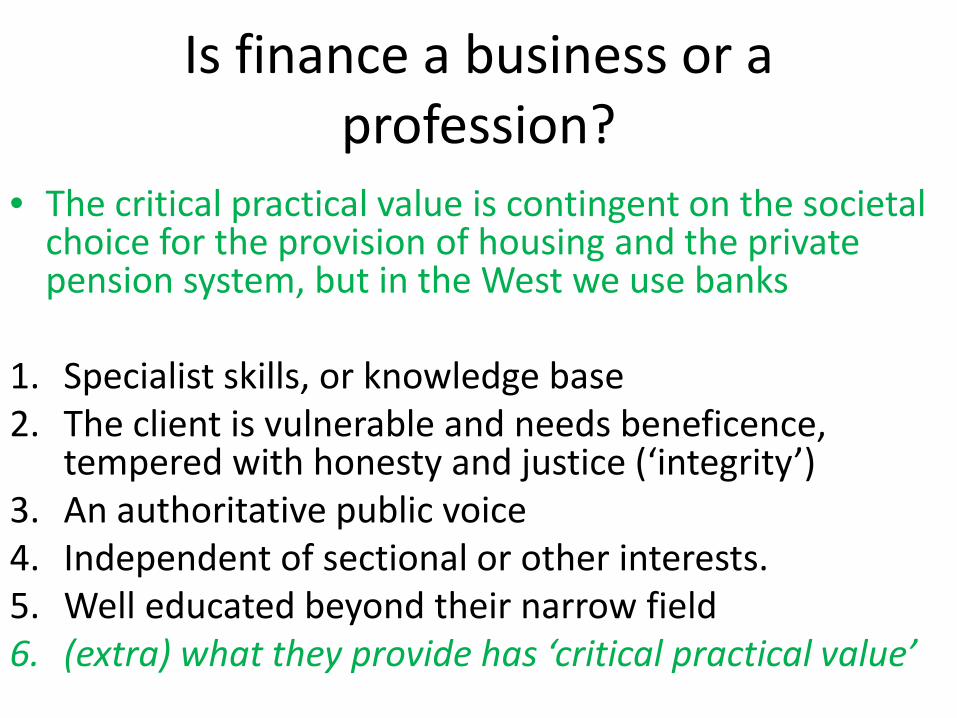

Is finance a business or a profession?

• The critical practical value is contingent on the societal choice for the provision of housing and the private pension system, but in the West we use banks

1. Specialist skills, or knowledge base 2. The client is vulnerable and needs beneficence,

tempered with honesty and justice (‘integrity’) 3. An authoritative public voice 4. Independent of sectional or other interests. 5. Well educated beyond their narrow field 6. (extra) what they provide has ‘critical practical value’

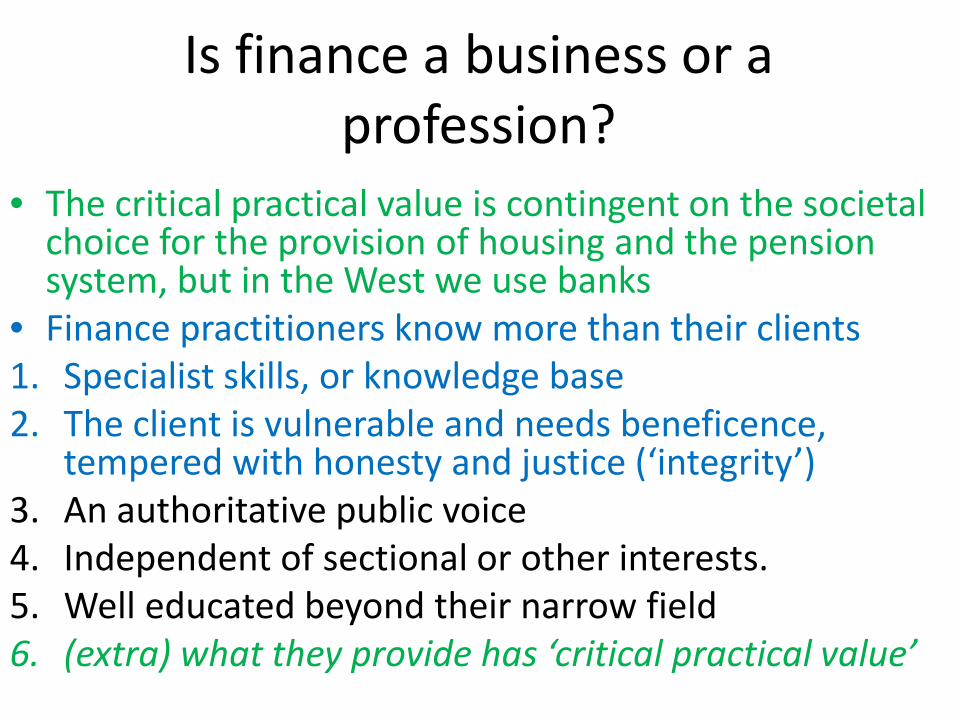

Is finance a business or a profession?

• The critical practical value is contingent on the societal choice for the provision of housing and the pension system, but in the West we use banks

• Finance practitioners know more than their clients 1. Specialist skills, or knowledge base 2. The client is vulnerable and needs beneficence,

tempered with honesty and justice (‘integrity’) 3. An authoritative public voice 4. Independent of sectional or other interests. 5. Well educated beyond their narrow field 6. (extra) what they provide has ‘critical practical value’

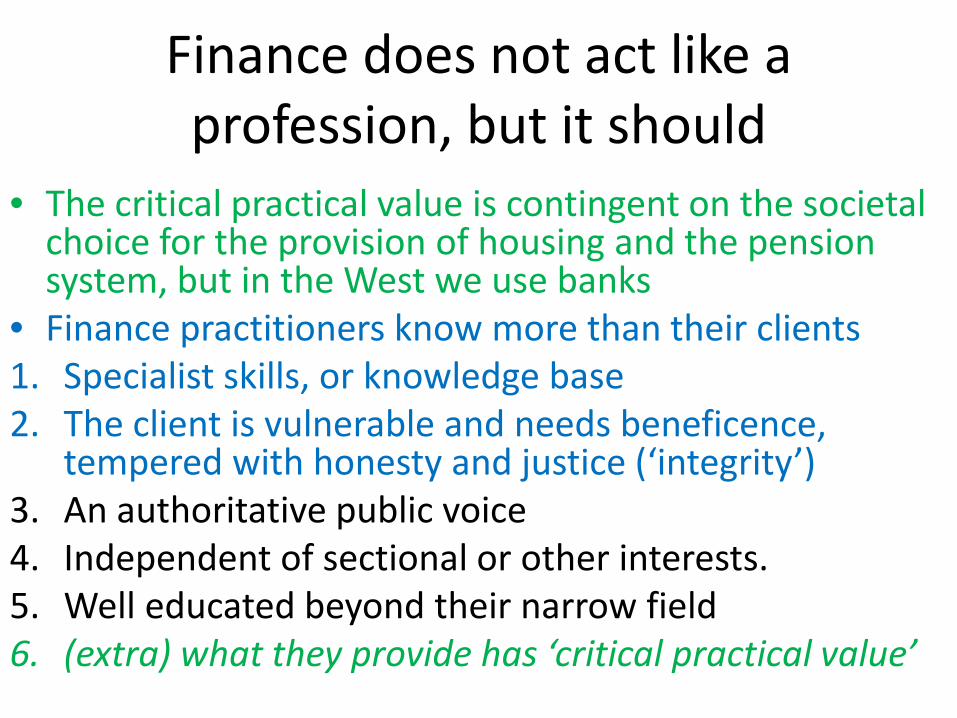

Finance does not act like a profession, but it should

• The critical practical value is contingent on the societal choice for the provision of housing and the pension system, but in the West we use banks

• Finance practitioners know more than their clients 1. Specialist skills, or knowledge base 2. The client is vulnerable and needs beneficence,

tempered with honesty and justice (‘integrity’) 3. An authoritative public voice 4. Independent of sectional or other interests. 5. Well educated beyond their narrow field 6. (extra) what they provide has ‘critical practical value’

How to achieve professionalisation

• Self certification eg. General Medical Council – A swifter path to strike someone off than formal law

• Non-performance related pay signals trust (Bowles 2016)

Education

• Ethics education is another path for professionalisation – This can be general ethics training which focuses

on applying rules or standards to situations in the workplace (eg. identify and resolve conflict of interest ethically).

– More ambitiously, it could seek to uncover corrosive elements of the feeder discipline’s training (evidenced by studies that show economists are more anti-social than others)

What are the Morally Corrosive Elements in Economics Training?

• Invisible hand • Maths is valuable, but conventions imply extra

things, such as nonzero optimal quantities • Stable preferences cramps the description of

motivation crowding out: problem is always ‘out there’ in incentives, not ‘in here’ in character

Misunderstandings? • The ‘big lie’ i.e. often-repeated Utility = U($) • ‘Preferences’ ignores motives and trivializes

moral choice ‘preferences over workplace violence’

Conclusion

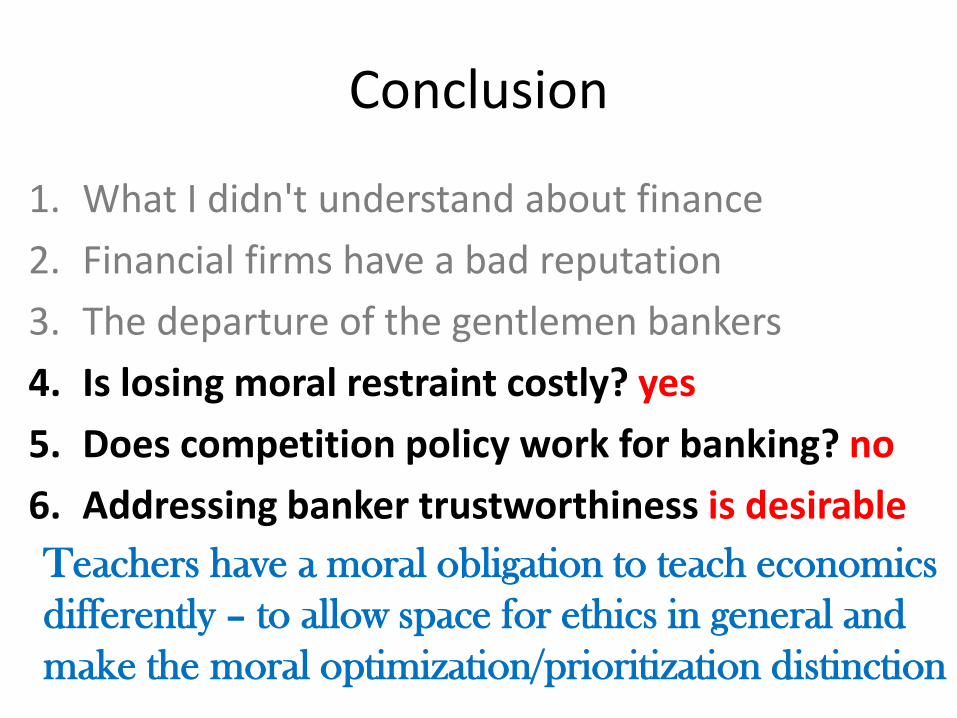

1. What I didn't understand about finance 2. Financial firms have a bad reputation 3. The departure of the gentlemen bankers 4. Is losing moral restraint costly? yes 5. Does competition policy work for banking? no 6. Addressing banker trustworthiness is desirable

Teachers have a moral obligation to teach economics differently – to allow space for ethics in general and make the moral optimization/prioritization distinction

thanks

Spares

How to achieve professionalisation

• Labour markets will do part of the job • Increased regulation makes finance less profitable

and perhaps less mathematically interesting • This may see a decline in self-selection by financial

motivation and extreme quantitative skill • If these characteristics and concern for ‘soft’

concepts associated with professionalisation are negatively correlated, this may prepare the ground for cultural change

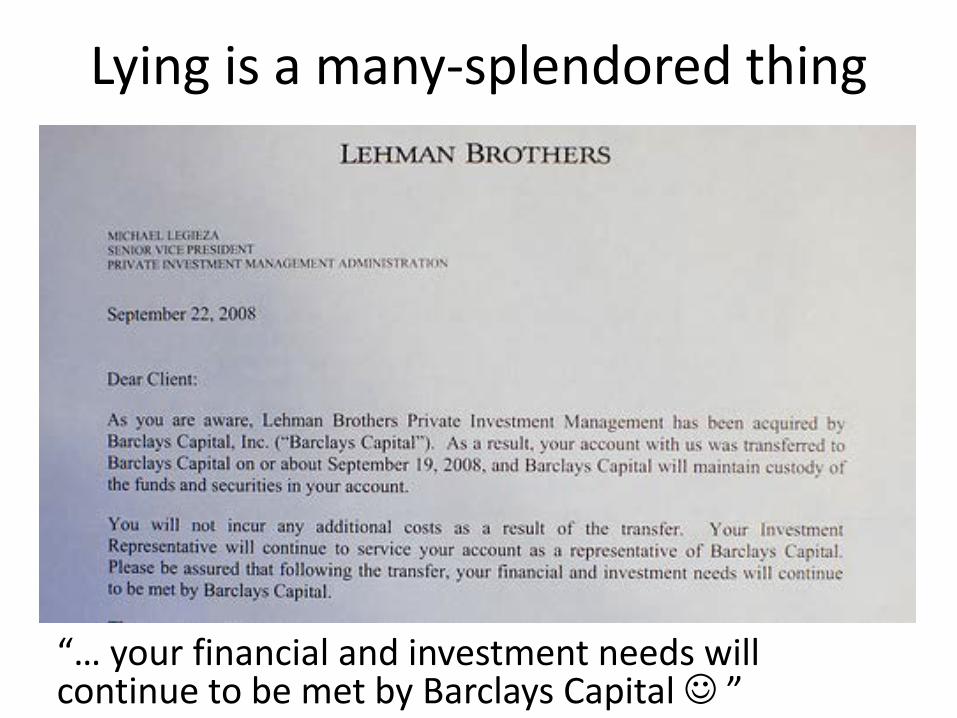

Lying is a many-splendored thing

“… your financial and investment needs will continue to be met by Barclays Capital ”

Two other features of Sen’s approach

• It is intellectually humble – it doesn’t require that all actions have to be explained by economistic reasoning

• It builds a narrative where moral restraint is costly, and we can measure that cost in lumps - whereas the cost is marginal for Becker

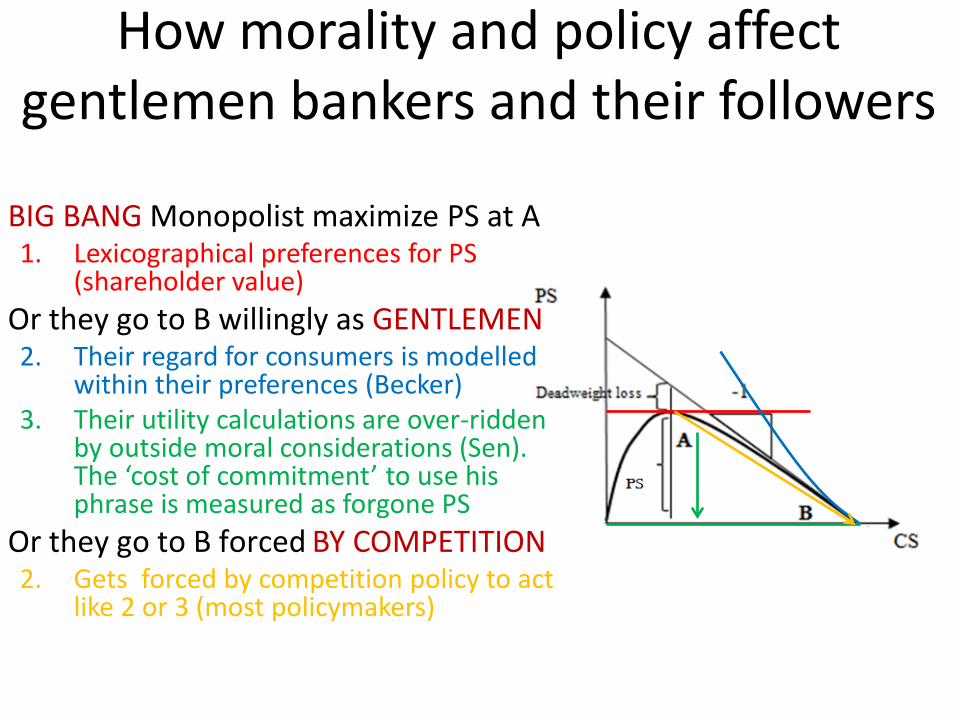

How morality and policy affect gentlemen bankers and their followers

BIG BANG Monopolist maximize PS at A 1. Lexicographical preferences for PS

(shareholder value) Or they go to B willingly as GENTLEMEN 2. Their regard for consumers is modelled

within their preferences (Becker) 3. Their utility calculations are over-ridden

by outside moral considerations (Sen). The ‘cost of commitment’ to use his phrase is measured as forgone PS

Or they go to B forced BY COMPETITION 2. Gets forced by competition policy to act

like 2 or 3 (most policymakers)

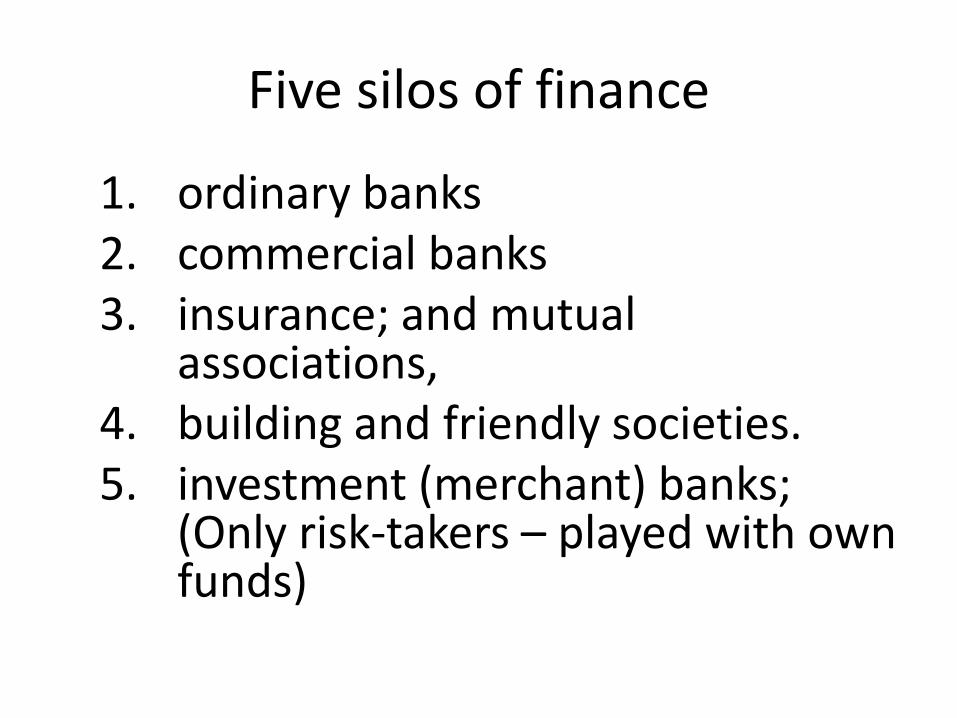

Five silos of finance

1. ordinary banks 2. commercial banks 3. insurance; and mutual

associations, 4. building and friendly societies. 5. investment (merchant) banks;

(Only risk-takers – played with own funds)

Bankers themselves were boring • Typical 1960s bank manager

– Conservative – Personal – No cross selling, and

conflicts of interest – Low remuneration & no

performance-related pay Never wore a mac

• Bank of England managed by moral suasion

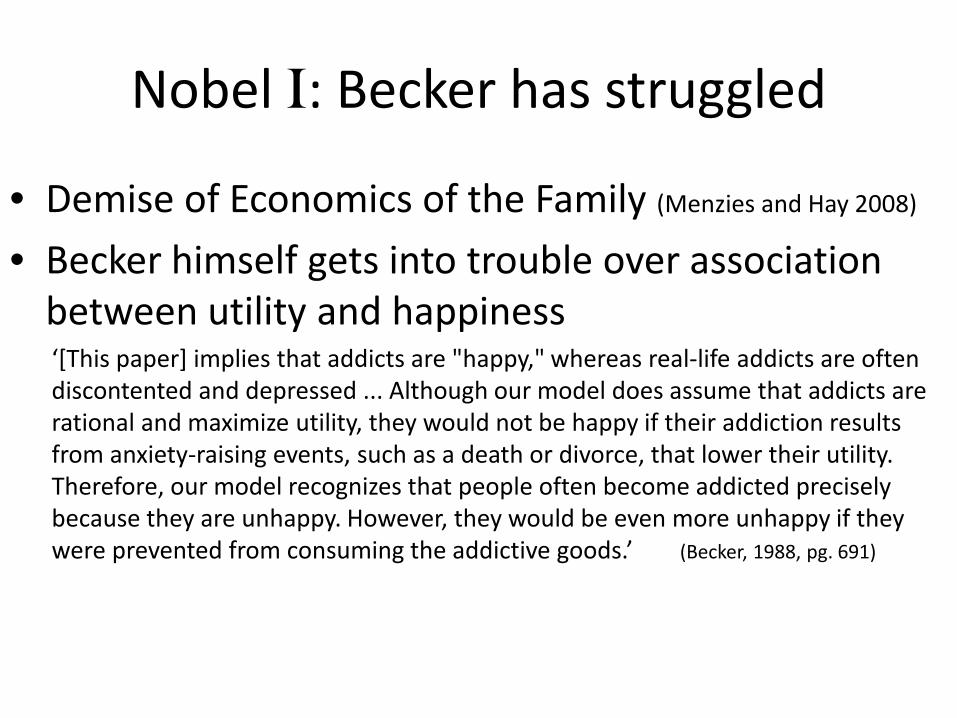

Nobel I: Becker has struggled

• Demise of Economics of the Family (Menzies and Hay 2008) • Becker himself gets into trouble over association

between utility and happiness ‘[This paper] implies that addicts are "happy," whereas real-life addicts are often discontented and depressed ... Although our model does assume that addicts are rational and maximize utility, they would not be happy if their addiction results from anxiety-raising events, such as a death or divorce, that lower their utility. Therefore, our model recognizes that people often become addicted precisely because they are unhappy. However, they would be even more unhappy if they were prevented from consuming the addictive goods.’ (Becker, 1988, pg. 691)

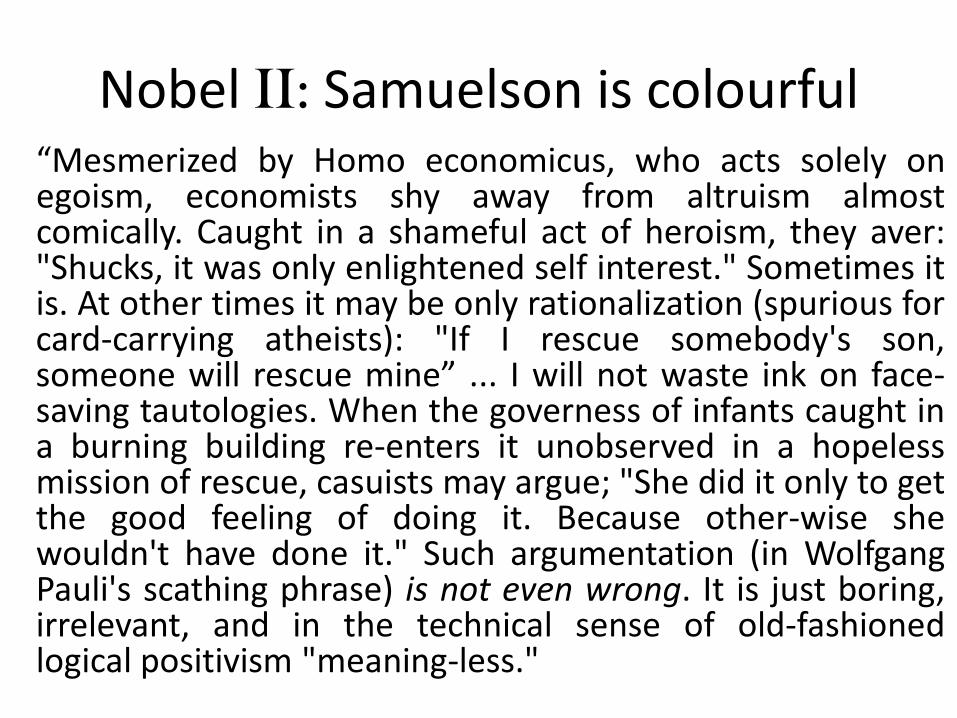

Nobel II: Samuelson is colourful “Mesmerized by Homo economicus, who acts solely on egoism, economists shy away from altruism almost comically. Caught in a shameful act of heroism, they aver: "Shucks, it was only enlightened self interest." Sometimes it is. At other times it may be only rationalization (spurious for card-carrying atheists): "If I rescue somebody's son, someone will rescue mine” ... I will not waste ink on face-saving tautologies. When the governess of infants caught in a burning building re-enters it unobserved in a hopeless mission of rescue, casuists may argue; "She did it only to get the good feeling of doing it. Because other-wise she wouldn't have done it." Such argumentation (in Wolfgang Pauli's scathing phrase) is not even wrong. It is just boring, irrelevant, and in the technical sense of old-fashioned logical positivism "meaning-less."

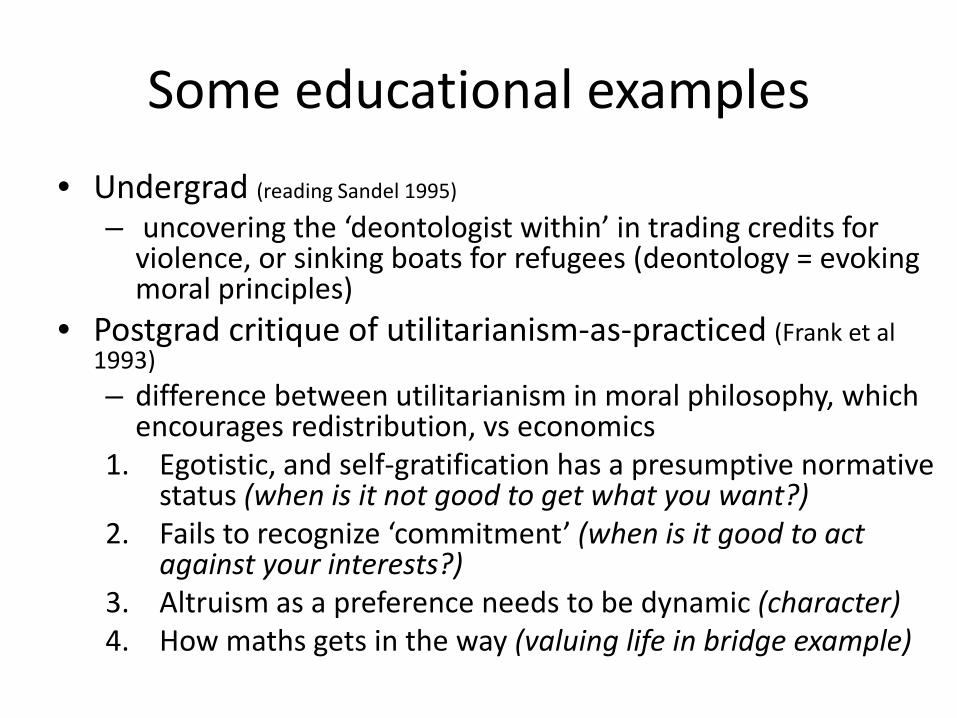

Some educational examples • Undergrad (reading Sandel 1995)

– uncovering the ‘deontologist within’ in trading credits for violence, or sinking boats for refugees (deontology = evoking moral principles)

• Postgrad critique of utilitarianism-as-practiced (Frank et al 1993) – difference between utilitarianism in moral philosophy, which

encourages redistribution, vs economics 1. Egotistic, and self-gratification has a presumptive normative

status (when is it not good to get what you want?) 2. Fails to recognize ‘commitment’ (when is it good to act

against your interests?) 3. Altruism as a preference needs to be dynamic (character) 4. How maths gets in the way (valuing life in bridge example)

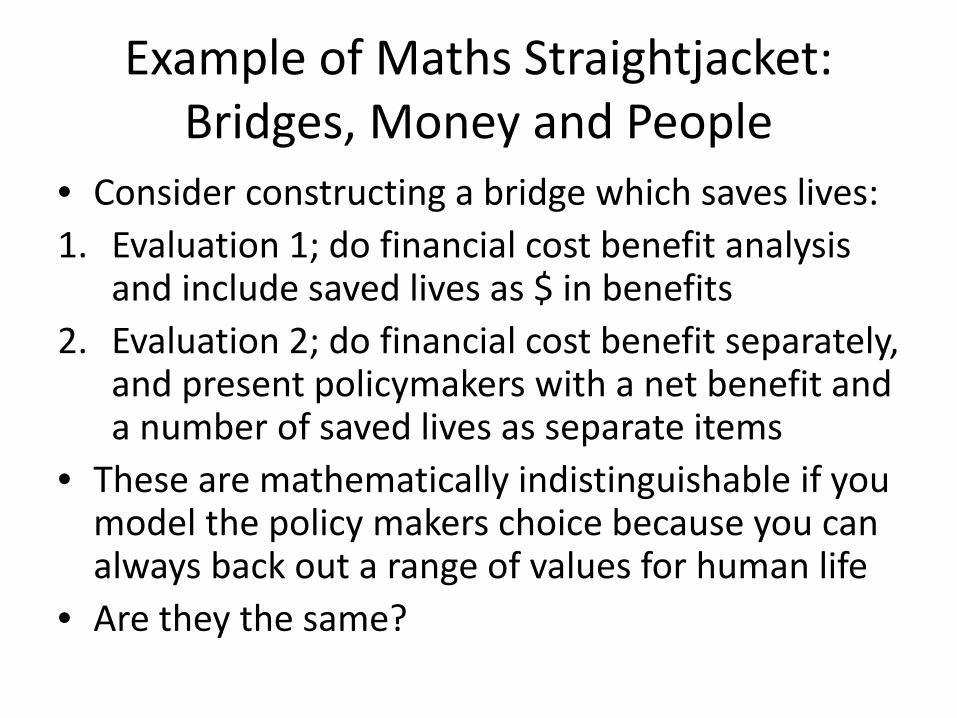

Example of Maths Straightjacket: Bridges, Money and People

• Consider constructing a bridge which saves lives: 1. Evaluation 1; do financial cost benefit analysis

and include saved lives as $ in benefits 2. Evaluation 2; do financial cost benefit separately,

and present policymakers with a net benefit and a number of saved lives as separate items

• These are mathematically indistinguishable if you model the policy makers choice because you can always back out a range of values for human life

• Are they the same?

Moral reasoning is ‘sacred’

• ‘Sacred forces are not to be distinguished from profane ones simply by their greater intensity, they are different – they have special qualities which others do not have’ (Durkheim, 1915, pg. 85)

• ‘insofar as instrumental rationality offers a good account of what people typically do, to the same extent it is incapable of explaining those aspects of their behaviour which they take most seriously’ Goodin (1982)

Utilitarianism means lots of things

• Utility began as a ‘pleasure minus pain’ measure with Bernoulli and then Bentham

• In moral philosophy it is a theory which says ‘everyone matters’ and which promotes redistribution and justice (foot vs fire)

• In economics interpersonal comparisons of utility have been avoided, making redistribution problematic (foot vs fire)

Utilitarianism means lots of things in Economics

• It can mean as little as ‘consistent preferences’

‘no matter whether you are a single-minded egoist or a raving altruist or a class-conscious militant, you will appear to be maximizing your own utility in this enchanted world of definitions’ Sen (1977)

• but it can also mean a cluster of auxiliary assumptions

Utilitarianism means lots of things in Economics

• Let’s take these seriously so that the combined theory is falsifiable (unusual) 1. Egotistic, and self-gratification has a presumptive

normative status 2. About happiness 3. About ‘preference’ satisfaction 4. Preferences are fixed 5. Utility functions are ‘smooth’ (cont. and twice differentiable)

mathematical functions

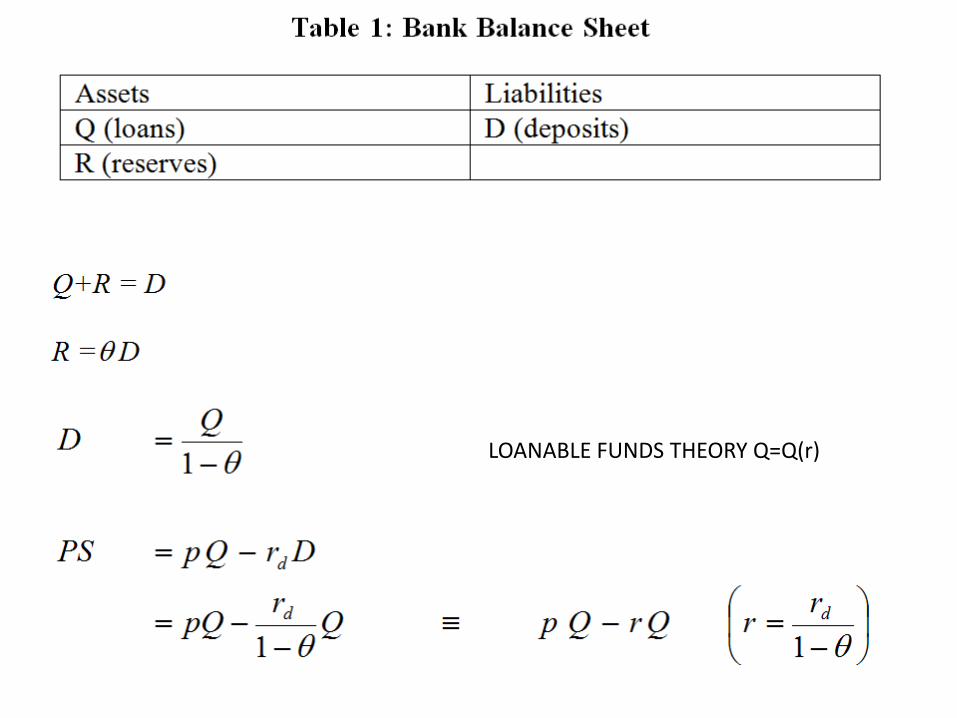

LOANABLE FUNDS THEORY Q=Q(r)

![DNSSEC Restoring trust in DNS Roland van Rijswijk roland.vanrijswijk [at] surfnet.nl](https://img.pdfslide.us/doc/110x75/56814a56550346895db779d7/dnssec-restoring-trust-in-dns-roland-van-rijswijk-rolandvanrijswijk-at-surfnetnl.jpg)