Embed Size (px)

Citation preview

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

27 September 2016 Asia Pacific/Philippines

Equity Research Restaurants

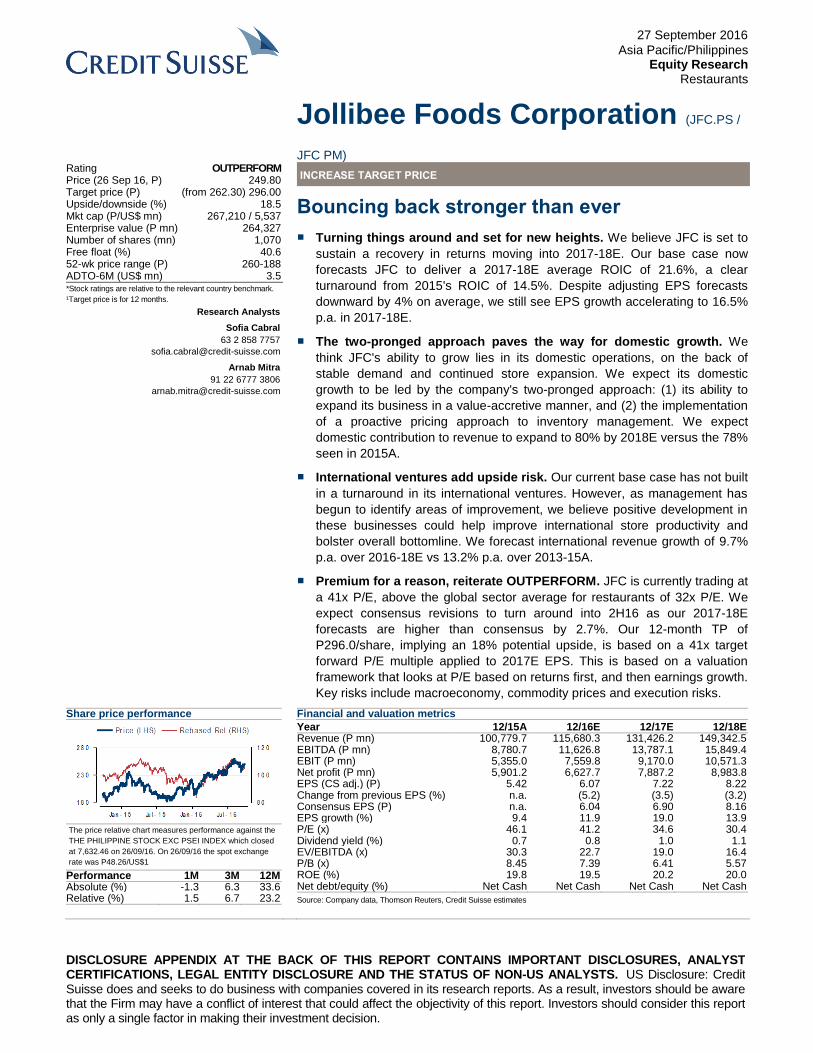

Jollibee Foods Corporation (JFC.PS /

JFC PM) Rating OUTPERFORM Price (26 Sep 16, P) 249.80 Target price (P) (from 262.30) 296.00 Upside/downside (%) 18.5 Mkt cap (P/US$ mn) 267,210 / 5,537 Enterprise value (P mn) 264,327 Number of shares (mn) 1,070 Free float (%) 40.6 52-wk price range (P) 260-188 ADTO-6M (US$ mn) 3.5 *Stock ratings are relative to the relevant country benchmark.

¹Target price is for 12 months.

Research Analysts

Sofia Cabral

63 2 858 7757

Arnab Mitra

91 22 6777 3806

INCREASE TARGET PRICE

Bouncing back stronger than ever

■ Turning things around and set for new heights. We believe JFC is set to

sustain a recovery in returns moving into 2017-18E. Our base case now

forecasts JFC to deliver a 2017-18E average ROIC of 21.6%, a clear

turnaround from 2015's ROIC of 14.5%. Despite adjusting EPS forecasts

downward by 4% on average, we still see EPS growth accelerating to 16.5%

p.a. in 2017-18E.

■ The two-pronged approach paves the way for domestic growth. We

think JFC's ability to grow lies in its domestic operations, on the back of

stable demand and continued store expansion. We expect its domestic

growth to be led by the company's two-pronged approach: (1) its ability to

expand its business in a value-accretive manner, and (2) the implementation

of a proactive pricing approach to inventory management. We expect

domestic contribution to revenue to expand to 80% by 2018E versus the 78%

seen in 2015A.

■ International ventures add upside risk. Our current base case has not built

in a turnaround in its international ventures. However, as management has

begun to identify areas of improvement, we believe positive development in

these businesses could help improve international store productivity and

bolster overall bottomline. We forecast international revenue growth of 9.7%

p.a. over 2016-18E vs 13.2% p.a. over 2013-15A.

■ Premium for a reason, reiterate OUTPERFORM. JFC is currently trading at

a 41x P/E, above the global sector average for restaurants of 32x P/E. We

expect consensus revisions to turn around into 2H16 as our 2017-18E

forecasts are higher than consensus by 2.7%. Our 12-month TP of

P296.0/share, implying an 18% potential upside, is based on a 41x target

forward P/E multiple applied to 2017E EPS. This is based on a valuation

framework that looks at P/E based on returns first, and then earnings growth.

Key risks include macroeconomy, commodity prices and execution risks.

Share price performance

The price relative chart measures performance against the

THE PHILIPPINE STOCK EXC PSEI INDEX which closed

at 7,632.46 on 26/09/16. On 26/09/16 the spot exchange

rate was P48.26/US$1

Performance 1M 3M 12M Absolute (%) -1.3 6.3 33.6 Relative (%) 1.5 6.7 23.2

Financial and valuation metrics

Year 12/15A 12/16E 12/17E 12/18E Revenue (P mn) 100,779.7 115,680.3 131,426.2 149,342.5 EBITDA (P mn) 8,780.7 11,626.8 13,787.1 15,849.4 EBIT (P mn) 5,355.0 7,559.8 9,170.0 10,571.3 Net profit (P mn) 5,901.2 6,627.7 7,887.2 8,983.8 EPS (CS adj.) (P) 5.42 6.07 7.22 8.22 Change from previous EPS (%) n.a. (5.2) (3.5) (3.2) Consensus EPS (P) n.a. 6.04 6.90 8.16 EPS growth (%) 9.4 11.9 19.0 13.9 P/E (x) 46.1 41.2 34.6 30.4 Dividend yield (%) 0.7 0.8 1.0 1.1 EV/EBITDA (x) 30.3 22.7 19.0 16.4 P/B (x) 8.45 7.39 6.41 5.57 ROE (%) 19.8 19.5 20.2 20.0 Net debt/equity (%) Net Cash Net Cash Net Cash Net Cash

Source: Company data, Thomson Reuters, Credit Suisse estimates

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 2

Focus charts Figure 1: JFC remains dominant in the Philippine

fast food industry…

Figure 2: …and implied QSR underpenetration gives

the market big growth opportunities

Source: Company data, Credit Suisse estimates Source: Euromonitor, World Bank, Credit Suisse estimates

Figure 3: Cost of inventory management, as a

percentage of revenue, could be the key…

Figure 4: …as well as the success of its

international operations, which lately constitute

19% of systemwide sales

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 5: We believe JFC's consistent double-digit

ROICs and clear runway for growth… Figure 6: …justify its forward P/E of 41x

Source: Company data, Credit Suisse estimates Source: Thomson Reuters Datastream, Credit Suisse estimates

JFC brands59%

McDonalds12%

Goldilocks10%

KFC6%

Shakey's4%

Pizza Hut4%

Others5%

1.30

1.19

0.71

0.23

0.09 0.08 0.070.02 0.01

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

KR CH JP TH VN PHL IN ID MY

45%

46%

48%

46%

47%

48% 48% 48%48%

49%

48%49% 49%

43%

44%

45%

46%

47%

48%

49%

50%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

E

2017

E

2018

E

Domestic 81%

Yonghe King8%

Other China brands

3%

Jollibee 5%

Chowking 2%

Red Ribbon 1%

22.9%

17.4% 17.4%

23.9%

21.4%

14.5%

19.1%

21.2%22.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

12/10A 12/11A 12/12A 12/13A 12/14A 12/15A 12/16E 12/17E 12/18E

17

22

27

32

37

42

47

Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Fwd PER Ave-2SD Ave-1SD

Average Ave+1SD Ave+2SD

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 3

Bouncing back stronger than ever JFC is turning around from its slip last year and, more importantly, its re-energised “two-

pronged” approach is set to deliver sustainable growth into FY17-18E. In our view, there's

potential not just for the company to recover from the previous year's cost side issues, but

to effectively expand its existing asset base and continue to deliver escalating returns in

the future.

Turning things around and set for new heights

We believe JFC is set to sustain a recovery in returns moving into 2017-18E. Our base

case now forecasts JFC to deliver a 2017-18E average ROIC of 21.6%, a clear turnaround

from 2015's ROIC of 14.5%. We believe that JFC's ability to continuously grow lies in a

two-pronged approach, namely, (1) its ability to expand its business domestically in a

value-accretive manner; and (2) the implementation of a proactive approach to inventory

management. Playing domestic defense. The bulk of JFC's business lies in its Philippine

operations which, as of 1H16, contributed roughly 80% to its revenue. In our view,

domestic operations will continue to drive the company's business on the back of

unabated domestic demand and implied QSR underpenetration compared to peers. A

more proactive approach to inventory management. Along with its expansion efforts, a

strategic pricing approach, which the company has committed to implementing proactively,

could work to offset unexpected increases in raw material prices and allow the company

room for GP margin expansion. We believe management will be able to bring down cost of

inventories as a percentage of revenue to 48.4%, on average, over 2016-18E from the

48.8% seen in 2015. Resultantly, we see GPM expanding to 22.1%, on average, from

2016-18E versus GPM of 21.5% reported, on average, over the past five years.

International ventures add upside risk

Our current base case has not built in a turnaround in its international ventures,

particularly its brand Yonghe King (8% of systemwide sales) and its recent acquisition of

Smashburger. However, as management has recently begun to identify areas of

improvement, we believe positive development in these businesses could provide possible

upside risk to earnings estimates. For 2016-18E, we see steady international revenue

growth of approximately 9.7% p.a., on average. This compares with the 13.2% p.a., on

average, international revenue growth recorded over 2013-15A.

Premium for a reason

JFC currently trades at a 41x P/E, above the global sector average for restaurants of 32x

P/E, which we justify based on JFC's clear medium-term growth story and its ability to

deliver escalating returns. Our 2017-18E EPS forecasts are 2.7% higher than consensus

on average. With a visible turnaround in FY16E and as both topline growth and margin

expansion gather pace into FY17-18E, we expect the stock to re-rate further.

Target P/E based TP of P296.0. We utilise a stylised model created by our Global

Financial Strategies team to guide our target P/E multiple. The model looks at P/Es, given

different scenarios for ROIC and earnings growth. Based on an average ROIC of 21.6%

from 2017-18E and EPS growth of 16.5% p.a. over the same period, we set a target P/E of

41x. Applying this to our 2017E EPS forecast of P7.22 yields a target price of P296.0.

Key risks: (i) a significant change in the macroeconomic environment which could

dampen consumer sentiment and impact earnings; (ii) commodity price volatility; and (iii)

execution risks related to its domestic and international expansion.

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 4

Jollibee Foods Corporation (JFC.PS / JFC PM)

Price (26 Sep 2016): P249.80; Rating: OUTPERFORM; Target Price: (from P262.30) P296.00; Analyst: Sofia Cabral

Income Statement (P mn) 12/15A 12/16E 12/17E 12/18E

Sales revenue 100,780 115,680 131,426 149,343 Cost of goods sold 79,808 90,441 102,322 116,096 EBITDA 8,781 11,627 13,787 15,849 EBIT 5,355 7,560 9,170 10,571 Net interest expense/(inc.) (32) 15 15 15 Recurring PBT 6,435 8,540 10,150 11,552 Profit after tax 5,046 6,784 8,072 9,194 Reported net profit 4,928 6,628 7,887 8,984 Net profit (Credit Suisse) 5,901 6,628 7,887 8,984

Balance Sheet (P mn) 12/15A 12/16E 12/17E 12/18E

Cash & cash equivalents 11,498 12,518 14,146 16,048 Current receivables 5,433 9,717 11,040 12,545 Inventories 5,478 6,202 7,075 16,577 Other current assets 4,760 5,437 6,177 7,019 Current assets 27,169 33,874 38,438 52,189 Property, plant & equip. 14,547 18,852 22,358 26,214 Investments 998 984 984 984 Intangibles 9,412 9,412 9,412 9,412 Other non-current assets 12,636 7,198 7,568 7,798 Total assets 64,763 70,320 78,760 96,598 Current liabilities 21,068 22,474 25,443 37,013 Total liabilities 33,006 34,386 37,488 49,245 Shareholders' equity 31,631 36,324 41,874 48,172 Minority interests 1,133 592 399 180 Total liabilities & equity 64,763 70,320 78,760 96,598

Cash Flow (P mn) 12/15A 12/16E 12/17E 12/18E

EBIT 5,355 7,560 9,170 10,571 Net interest 32 (15) (15) (15) Tax paid (2,002) (2,138) (2,363) (2,606) Working capital 5,913 (2,377) 715 513 Other cash & non-cash items (3,174) 11,815 5,141 5,660 Operating cash flow 6,124 14,844 12,647 14,123 Capex (3,922) (10,386) (8,470) (9,317) Free cash flow to the firm 2,202 4,458 4,177 4,806 Investing cash flow (3,922) (10,361) (8,489) (9,315) Equity raised 608 253 265 279 Dividends paid (1,887) (2,187) (2,603) (2,965) Financing cash flow 1,677 (3,464) (2,530) (2,905) Total cash flow 3,879 1,020 1,628 1,903 Adjustments 0 0 0 0 Net change in cash 3,879 1,020 1,628 1,903

Per share 12/15A 12/16E 12/17E 12/18E

Shares (wtd avg.) (mn) 1,088 1,093 1,093 1,093 EPS (Credit Suisse) (P) 5.42 6.07 7.22 8.22 DPS (P) 1.76 2.03 2.42 2.76 Operating CFPS (P) 5.63 13.59 11.57 12.93

Earnings 12/15A 12/16E 12/17E 12/18E

Growth (%) Sales revenue 11.1 14.8 13.6 13.6 EBIT (12.7) 41.2 21.3 15.3 EPS 9.4 11.9 19.0 13.9 Margins (%) EBITDA 8.7 10.1 10.5 10.6 EBIT 5.3 6.5 7.0 7.1

Valuation (x) 12/15A 12/16E 12/17E 12/18E

P/E 46.1 41.2 34.6 30.4 P/B 8.45 7.39 6.41 5.57 Dividend yield (%) 0.7 0.8 1.0 1.1 EV/sales 2.6 2.3 2.0 1.7 EV/EBITDA 30.3 22.7 19.0 16.4 EV/EBIT 49.6 34.9 28.6 24.6

ROE analysis (%) 12/15A 12/16E 12/17E 12/18E

ROE 19.8 19.5 20.2 20.0 ROIC 14.5 19.1 21.2 22.0

Credit ratios 12/15A 12/16E 12/17E 12/18E

Net debt/equity (%) (4.4) (9.5) (12.2) (14.7) Net debt/EBITDA (x) (0.16) (0.29) (0.37) (0.44)

Company Background

JFC is a multinational chain of fast food restaurants headquartered in the Philippines. As of 2014 it has a total of 2,913 restaurants in the Philippines and abroad, and owns the operating license for ten different fast food brands.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (P) (from 299.30) 330.70

Our Grey Sky Scenario (P) (from 198.00) 223.80

Share price performance

The price relative chart measures performance against the THE PHILIPPINE

STOCK EXC PSEI INDEX which closed at 7,632.46 on 26-Sep-2016

On 26-Sep-2016 the spot exchange rate was P48.26/US$1

Source: Company data, Thomson Reuters, Credit Suisse estimates

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 5

Turning things around and set for new heights We believe JFC is set to deliver a 2017-18E average ROIC of 21.6%, a clear turnaround

from 2015's ROIC of 14.5%. Contraction in 2015 average ROIC was due to one-time costs

related to its Smashburger acquisition and IT-related expenses. Overall GP margins were

also affected by domestic cost side issues beginning as early as 2014 related to port

congestion and a significant increase in raw material prices, particularly beef. In light of

this, we believe that the foregoing was one time occurrences and 2015 can serve as a

learned lesson for a stronger and better JFC as well as a springboard for, not only steady,

but sustainable growth moving forward.

In our view, JFC's ability to continuously grow lies in a two-pronged approach: (1) its ability

to expand and make value-accretive ventures domestically, and (2) the implementation of

a proactive approach to inventory management.

First engine: Playing domestic defense

JFC has a distinguished home court advantage

JFC continues to dominate its home court through its efficient and effective store rollout

over the years as, according to 1H16 company data, JFC outlets constituted 59% of the

Philippines' total store network (Figure 7). Additionally, according to Euromonitor, as of

2015 it constituted 56% of the Philippine fast food industry in terms of value. JFC's

dominance in the Philippines fast food market can further be underscored by its

comparison with other international markets. According to Euromonitor, in 2015, China's

top QSR player, Yum! Brands Inc., accounted for 4% of the Chinese fast food market in

terms of value while, in the US, the top player McDonald's constituted 16% of the total fast

food market over the same period of time. The bulk of JFC's business lies in its Philippine

operations which, as of 1H16, contributed roughly 80% to net sales. In our view, JFC's

domestic operations will continue to drive growth moving forward as the current

environment presents an array of available expansion opportunities for the market, such

as the industry's implied QSR underpenetration relative to peers (Figure 8).

Figure 7: Phils store network market share—2015 Figure 8: QSR outlets per capita ('000s)

Source: Company data, Credit Suisse estimates Source: Euromonitor, World Bank, Credit Suisse estimates

We note that the Philippines still holds one of the lowest QSR penetration rates in the

region, which we have measured by QSR outlets per 1000 persons. According to

Euromonitor, the average number of QSR outlets per person in the region was measured

at approximately 0.41, with the Philippines coming in at 0.08. The company has also

JFC brands59%

McDonalds12%

Goldilocks10%

KFC6%

Shakey's4%

Pizza Hut4%

Others5%

1.30

1.19

0.71

0.23

0.09 0.08 0.070.02 0.01

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

KR CH JP TH VN PHL IN ID MY

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 6

stated that JFC's penetration rate of Philippine cities, measured as the percentage of

areas in the country where JFC has store presence in, is approximated at 80%. In

municipalities, JFC store penetration rate is approximated at 8%, suggesting further room

for growth in these kinds of areas.

We also believe that there still lies upside on the domestic demand side. As seen in Figure

9, which charts the relationship between wealth per adult versus fast food service

spending per capita in the region, we observe that the Philippines sits in a 'sweet spot' of

the curve, where the slope begins to steepen and implies that relatively incremental

increases in wealth levels translate into a rapid increase in expenditures.

Figure 9: Wealth per adult vs fast food service spending/capita/annum (US$) –

2015

Source: Euromonitor, Credit Suisse estimates

Based on the data presented above regarding QSR penetration and fast food service

spending per capita, we expect JFC, as the market's biggest player, to effectively leverage

on available expansion opportunities, particularly in more rural areas. Considering their

undisputed dominance in the Philippine fast food industry, extensive experience in the

domestic market, and large scale operations, we believe that JFC has the advantage of

being a potent 'first mover' in newer areas and municipalities outside developed cities,

thus increasing demand through QSR outlet penetration. Newer entrants on the other

hand, without as much knowledge of the Philippine consumer, would likely be forced to

open their first outlets in the already developed areas, where demand is already present

and competition is likely more concentrated. According to management, approximately

70% of its store network expansion in the near term is set to take place in areas outside

Metro Manila (Figure 10).

VN

TH

KRSG

PHLMY

JP

IDIN

HK

CH

R² = 0.7523

-100

0

100

200

300

400

500

0 50000 100000 150000 200000 250000 300000Fas

t foo

d se

rvic

e sp

endi

ng p

er c

apita

/ann

um (

US

$)

Wealth per adult (US$)

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 7

Figure 10: Examples of planned store openings per geographical area

Region Province

Luzon (ex-Metro Manila) Quezon

Laguna

Bataan

Batangas

Cavite

Visayas Aklan

Romblon

Mindanao Davao

Zamboanga

Source: Company data

Additionally, according to management, JFC targets a minimum ROIC per store, which

lately has been pegged at 16%. According to JFC, however, newer stores in the

Philippines have been yielding higher ROICs at a range of 20-22%, which management

has attributed to unabated domestic demand. We believe that this provides evidence for

potential ROIC expansion and, additionally, acts as a further testament to the company's

discipline in expanding its footprint in value-accretive areas.

Considering this, we expect JFC's domestic operations to continue to grow on the back of

efficient store roll-out and continued store productivity. For 2016-18E, we expect domestic

revenue growth to accelerate and grow at an average of 15.2% p.a. compared with the

12.1% p.a. growth seen over 2013-15A.

Key revenue drivers

Based on the foregoing data, we forecast the following contributions to revenue growth

over 2016-18E (Figure 11):

■ Philippine sales. For 2016-18E, we forecast an average contribution of 11.4 pp. Over

2006-15A, average contribution was 9.2 pp.

■ International sales. For 2016-18E, we forecast an average contribution of 2.1 pp.

Over 2006-15A, average contribution was 3.7 pp.

■ Franchising. For 2016-18E, we forecast an average contribution of 0.6 pp. Over 2006-

15A, average contribution was 0.4 pp.

Figure 11: Revenue contribution to sales growth—2006A-18E

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

P mn

Net sales - domestic 27,377 33,155 35,931 37,284 40,937 47,186 52,247 58,339 65,996 73,586 85,901 98,407 112,939

Net sales - international 4,727 3,514 5,739 8,375 9,956 12,476 15,669 18,440 20,690 22,676 24,686 27,262 29,916

Franchising 1,808 2,025 2,221 2,299 2,478 2,893 3,144 3,504 3,986 4,518 5,093 5,757 6,488

Total 33,911 38,694 43,892 47,958 53,372 62,555 71,059 80,283 90,671 100,780 115,680 131,426 149,343

% YoY 16.8 14.1 13.4 9.3 11.3 17.2 13.6 13.0 12.9 11.1 14.8 13.6 13.6

Contribution to sales growth (pp)

Domestic 10.8 17.0 7.2 3.1 7.6 11.7 8.1 8.6 9.5 8.4 12.2 10.8 11.1

International 6.7 (3.6) 5.8 6.0 3.3 4.7 5.1 3.9 2.8 2.2 2.0 2.2 2.0

Franchising (0.7) 0.6 0.5 0.2 0.4 0.8 0.4 0.5 0.6 0.6 0.6 0.6 0.6

Total % YoY 16.8 14.1 13.4 9.3 11.3 17.2 13.6 13.0 12.9 11.1 14.8 13.6 13.6

Source: Company data, Credit Suisse estimates

We also forecast the average company-owned store network growth and revenue per

store growth as follows (Figure 12).

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 8

Figure 12: Revenue per store and avg. store network growth—2006A-18E

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

Philippines

Average co-owned stores %YoY 18.9% 8.0% 5.6% 3.1% 4.8% 4.5% 4.5% 5.8% 7.0% 10.5% 10.1% 8.1% 8.3%

Revenue per store %YoY -5.0% 12.1% 2.6% 0.7% 4.7% 10.2% 6.0% 5.5% 5.8% 0.9% 6.0% 6.0% 6.0%

International

Average co-owned stores %YoY 19.2% 7.3% 31.5% 31.5% 18.9% 20.6% 19.1% 11.4% 4.0% 2.4% 3.2% 4.6% 4.5%

Revenue per store %YoY 43.1% -30.7% 24.2% 10.9% 0.0% 3.9% 5.5% 5.7% 7.9% 7.0% 5.5% 5.5% 5.0%

Source: Company data, Credit Suisse estimates

Second engine: A more proactive approach to

inventory management

Management looking to neutralise input cost surprises

Management is now implementing an updated pricing policy that we believe could stand to

neutralise input costs. Up until 2013, management was mostly applying incremental price

hikes of less than 1%, at least twice or thrice a year, for its domestic brands. This proved

inadequate in 2014, however, as raw material prices rose at an unprecedented pace. In

4Q14, management was eventually required to implement a 4% YoY price hike with

disastrous results to topline, the effect of which trickled into 2015.

We believe management has since learned an invaluable lesson in terms of the

importance of proactive pricing, which is reiterated now more than ever as the company

acknowledges the risk of a rise in raw material costs in 2H16 or 2017. Its updated pricing

approach of more frequent, 1% price hikes (done every three or four months across more

of its brands) while input costs are still stable could effectively solve the problem of

potential cost surprises before they occur, without the consumer feeling the impact of a

material one-time price adjustment.

Cost of inventories the biggest cost component

A sizable portion of JFC's cost of sales is dedicated to its cost of inventories. Cost of

inventories as a percentage of total revenue was measured at an average of 47.9% over

2011-15A (Figure 13). Note that, within cost of inventories, raw materials constitute

roughly 20-25% of revenue, and imported beef constitutes the bulk of this.

We forecast the new pricing strategy can help bring down cost of inventories as a

percentage of revenue to 48.4%, on average, for 2016-18E from the 48.8% hike seen in

2015.

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 9

Figure 13: Cost of inventories as a percentage of revenue over 2006A-18E

Source: Company data, Credit Suisse estimates

Resultantly, we see GPM expanding to 22.1%, on average, over 2016-18E versus GPM of

21.5% reported, on average, over the past five years.

Take 2015 as a lesson

As previously mentioned, cost of inventories as a percentage of sales quickly rose to

48.8% in 2015. We note that cost side issues in 2015A can be traced back to as early as

2014 as, according to the company, raw material costs rose by an average of 5.4% YoY,

driven by a spike in the cost of beef (Figure 14). In order to try and offset this, JFC

resorted to quarterly 1% hikes in its Jollibee brand finished with a roughly 4% YoY

increase made in 4Q14. Note that in 1H16 the Jollibee brand constituted roughly 58% of

Philippine systemwide sales.

Figure 14: USDA ground beef retail prices index

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse estimates

The one-time price increase of 4% YoY backfired on two counts as (1) it failed to offset

already escalated input costs (Figure 15) and (2) negatively affected sales volume from

more price sensitive customers (Figure 16). The effect of which trickled into the first two

45%

46%

48%

46%

47%

48% 48% 48%48%

49%

48%49% 49%

43%

44%

45%

46%

47%

48%

49%

50%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

E

2017

E

2018

E

2.5

2.7

2.9

3.1

3.3

3.5

3.7

3.9

4.1

4.3

4.5

Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16

Oct 2014: Implemented

+4% price increase in

Jollibee brand

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 10

quarters of 2015. By April 2015, JFC decided to roll back the prices of Chickenjoy variants

and was able to revert to a higher topline momentum by 2H15.

Figure 15: Quarterly cost of inventories as a percent

of revenue—1Q14 to 2Q16 Figure 16: Quarterly revenue growth—1Q14 to 2Q16

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

2015 proved to be a difficult year for the company that underscored the importance of a

proactive approach to pricing. Moving forward, we believe that the successful and

consistent implementation of the company's pricing strategy in avoidance of another

material one-time price jump could translate into further potential upside.

Additional cost saving initiatives

We note that the company has also been making a conscious effort in reducing other cost

items, particularly in the salaries and wages item under cost of sales. Management has

stated that they have been making a conscious effort of shifting to more contracted

services, reflected in other cost of sales, as this would help the company save more on

training-related expenses in the future. Considering the low visibility on the impact of this

move however, we have not explicitly built this in to our other opex numbers, wherein

training-related expenses are classified. We forecast salaries and wages together with

other cost of sales items, as a percentage of revenue, at 18.9%, on average, over 2016-

18E, which is at the same level as in 2013-15A.

Electricity and utilities as a percentage of revenue has also been trending downwards over

the past few years, which management owed to a decline in power rates and company

initiatives regarding the installation and usage of LED lights. We expect this to stabilise at

around 3.5% as a percentage of revenue over 2016-18E, on average, from 3.8% in

2015A.

Cost of sales breakdown

We forecast the following breakdown for the company's cost of sales, as a percentage of

revenue, over 2016-18E (Figure 17):

■ Cost of inventories. 48.4% versus 2006-15A average of 47.1%.

■ Salaries and wages. 9.1% versus 2006-15A average of 11.0%.

■ Rent. 7.1% versus 2006-15A average of 7.0%.

■ Electricity and utilities. 3.5% versus 2006-15A average of 4.4%.

48%

47%

47%

48% 48%

48%48%

47%

49%

50%

48%

49%

48%

48%

46%

46%

47%

47%

48%

48%

49%

49%

50%

50%

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q

FY13 FY14 FY15 FY16

10%

13%

14%15%

15%14%

12%11% 10%

9%

14%

12%

13%14%

0%

2%

4%

6%

8%

10%

12%

14%

16%

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q

FY13 FY14 FY15 FY16

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 11

■ Other cost of sales items. 9.8% versus 2006-15A average of 8.1%.

Figure 17: Cost of sales breakdown

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

Cost of inventories 45.1% 46.2% 47.5% 46.2% 46.7% 47.7% 47.7% 47.6% 47.7% 48.8% 48.3% 48.5% 48.5%

Salaries and wages 11.0% 10.8% 11.5% 12.1% 12.2% 11.0% 10.9% 10.5% 10.2% 9.8% 9.3% 9.0% 8.9%

Rent 5.9% 5.7% 6.3% 7.0% 7.3% 7.7% 7.7% 7.4% 7.4% 7.4% 7.1% 7.1% 7.0%

Electricity & utilities 4.8% 4.5% 4.2% 4.3% 4.7% 4.4% 4.6% 4.3% 4.2% 3.8% 3.6% 3.5% 3.5%

Other cost of sales 8.6% 8.4% 8.4% 6.6% 6.8% 7.9% 7.8% 8.0% 8.8% 9.4% 9.8% 9.8% 9.8%

Total 75.4% 75.5% 77.9% 76.2% 77.7% 78.7% 78.7% 77.8% 78.2% 79.2% 78.2% 77.9% 77.7%

Source: Company data, Credit Suisse estimates

Further upside from cost of inventory management

As previously mentioned, we currently forecast cost of inventories as a percentage of

revenue at 48.4% (Figure 18), on average, over 2016-18E. For our upside case, we

assume raw material prices remain stable moving forward and the company manages to

bring down cost of inventories as a percentage of revenue to as low as 47.6% (Figure 19),

on average, over 2017-18E. This was the same level seen in 2013, when raw material

prices only rose marginally, by approximately 0.3% YoY. Assuming this, GP margins over

the same period of time could improve to an average of 23.1%. This is compared to the

GP margins of 22.2%, on average, we currently see for 2017-18E.

Figure 18: Cost of inventories as a percentage of

revenue over 2006A-18E (current forecast)

Figure 19: Cost of inventories as a percentage of

revenue over 2006A-18E (upside case)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Under our upside case for inventory cost management, EPS growth over 2017-18E would

also accelerate to 23.4% p.a. versus the current EPS growth forecast of 16.5% p.a. over

the same period of time. This would bring our 2017-18E EPS forecasts versus consensus

to increase to 14.7%, on average, from 2.7%, on average, under our current forecasts.

45%

46%

48%

46%

47%

48% 48% 48%48%

49%

48%49% 49%

43%

44%

45%

46%

47%

48%

49%

50%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

E

2017

E

2018

E

45%

46%

48%

46%

47%

48% 48% 48%48%

49%

48%

48% 48%

43%

44%

45%

46%

47%

48%

49%

50%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

E

2017

E

2018

E

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 12

International ventures add upside risk We believe that additional upside potential lies in JFC's international operations. Note that

our current base case has not built in a turnaround in JFC's international ventures,

particularly its brand Yonghe King and its recent acquisition of Smashburger.

Management, however, has recently begun to identify areas of improvements in these

ventures, such as a renewed focus on diversifying their menu offerings, new price

promotions and a sharper expansion strategy. We believe that positive development in

these businesses, in addition to continued growth on the international front, could provide

upside risk to earnings estimates.

Firming up the international front

The Bee goes global

While growing its domestic business, we note that the company has been keeping busy on

the global front through a number of acquisitions and joint ventures made every two years

or so in different markets (Figure 20). JFC generally has two methods in going about its

international strategy, wherein (1) it acquires or partners with a local brand in order to

penetrate the mainstream fast food market or (2) it brings its domestic brands to areas

with a large concentration of OFWs.

For 2016-18E, we see steady international revenue growth of approximately 9.7% p.a., on

average. This is compared to the 13.2% p.a., on average, international revenue growth

recorded over 2013-15A. Note, however, that 2013A international revenue numbers were

boosted by the company's acquisition of a majority stake in San Ping Wang in March

2012.

Figure 20: JFC acquisition history over 2004-15A

Company name Year acquired % stake Price paid Country Description

Smashburger 2015 40% US$99.5 mn USA Smashburger: Premium burger chain based in Denver,

Colorado

Dunkin' Donuts 2014 60% US$180.0 mn China Dunkin' Donuts: Franchisee of the brand in China

SuperFoods Group 2012 50% US$25 mn Vietnam Highlands Coffee: Coffee shop chain in Vietnam; Hard Rock

Café: franchisee in Macau, Hong Kong and Vietnam; Pho 24

brand in Vietnam, Indonesia, Philippines, Korea, Cambodia,

Macau

Wowprime 2012 48% P98.0 mn Taiwan 12 Sabu: Hotpot restaurant based in Taiwan specializing in

low-priced dishes

San Ping Wang 2012 55% P196.0 mn China San Ping Wang: Beef noodle business in South China

BK Group 2011 54% P66.0 mn Philippines Burger King: Sole franchisee of the brand in the Philippines

Chow Fun Holdings 2011 81% P140.0 mn USA Jinja Bar and Bistro: Asian-fusion casual chain based in

New Mexico

Mang Inasal 2010 70% P2,976 mn Philippines Mang Inasal: Filipino fast food chain specializing in grilled

chicken

Hong Zhuang Yuan 2008 100% P2,648 mn China Hong Zhuang Yuan: China-based chain specializing in

congee and hot dishes

Yonghe King 2004 85% US$22.5 mn China Yonghe King: China-based chain specializing in noodles,

rice, you tiao and soybean milk

Source: Company data

We expect topline growth from international operations to be buoyed by stable revenue

per average no. of international store growth. Over 2011-15A, revenue per average no. of

international stores grew, on average, 6.0% p.a. We subsequently forecast revenue per

average no. of international store growth at 5.3% p.a. over 2016-18E.

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 13

New approach to competition could turn the game around in China

As of 1H16, JFC's China operations (11% of total systemwide sales, as seen in Figure 21)

have been feeling downward pressure coming from the aggressive efforts of Western

brands such as McDonald's and KFC on the matters of pricing, a continued roll-out in

promotions, and location. Yonghe King, the brand primarily affected by this, accounts for

roughly 73% of JFC's China operations. We believe, however, that with the successful

execution of management's new strategy in counteracting competition, JFC could very

well turn things around in the medium term.

Figure 21: JFC systemwide sales split between

foreign brands—1H16 Figure 22: China fast food value market share—2015

Source: Company data, Credit Suisse estimates Source: Euromonitor, Credit Suisse estimates

JFC has already initiated new approaches in addressing the competition issue for Yonghe

King. The company, for example, has begun diversifying its menu offerings by introducing

new items diverging from its typical noodle offerings (Figure 23).

JFC has also started introducing price promotions in certain areas of China, which are

supposedly more price sensitive. With management noting a slight improvement in

transaction count recently, the company hopes to see a turnaround for its Yonghe King

brand by 2017. We have not priced this in to our numbers, but assuming the company's

efforts to counteract competition are successful, this could translate into a potential upside

for JFC's international revenue numbers.

Despite more aggressive competition in China, we also note that the Asian fast food

segment continues to dominate consumer preferences as it accounted for 86%, on

average, of the Chinese fast food market (in terms of value) over 2011-15A. This implies

room for JFC's China brands to continue to grow as the data suggests a certain degree of

insulation for the Asian fast food segment in terms of demand and preference.

Domestic 81%

Yonghe King8%

Other China brands

3%

Jollibee 5%

Chowking 2%

Red Ribbon 1%

Asian 86%

Bakery Products

1%

Burger3%

Chicken8% Other

2%

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 14

Figure 23: Signature and new dishes of Yonghe King

Signature dishes Additional

Non-alum fritters

Sweet and sour pork

Brewed soy milk

Crispy chicken thigh

Noodle soup

Dessert

Rice toppings

Source: Company data, Yonghe King company website

Efforts to keep Smashburger a smash hit

JFC has recently conceded that SSSG in its latest international venture, Smashburger, has

been lower than company's expectation. Management has attributed this to both intensifying

competition and weakening consumption in the US of late. In response, JFC has recently

identified areas of improvement in Smashburger operations to upper management and

corresponding ideas to correct them, such as introducing new products as well as streamlining

store expansion to more value-accretive areas moving forward. Note that, while these

proposals have yet to be implemented, a successful enactment of this strategy and a reversion

to normal SSSG levels can serve as a further push to JFC's bottomline. Historically, SSSG for

the chain has been seen at high single to double-digit growth.

Behind the Smashburger acquisition

Recall that in 2015 JFC, through its wholly-owned subsidiary Bee Good! Inc. (BGI),

entered into an agreement with Smashburger Master LLC to acquire a 40% stake in SJBF

LLC for the operations and management of the US-based better-burger chain,

Smashburger. The agreement also included a clause that states BGI is entitled to acquire

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 15

an additional 35% in Smashburger between 2018 and 2021 and the balance of 25%

between 2019 and 2026, at the latest.

The acquisition was a landmark one over the company's history as it marked JFC's first

move to tap into the US burger market by serving its mainstream customers. Note that the

acquisition is also a strategic one as Smashburger, characterised by its 100% certified

Angus beef burgers, more gourmet ingredients, and higher price points, sits well within the

fast casual segment.

A small but fast-growing player in fast casual

As a chunk of the top 20 fast casual market players' system sales share in the US,

Smashburger constituted roughly 2% as of 2015 (Figure 24). It, however, recorded one of

the fastest growths in the fast casual market over 2010-15A as it reported a CAGR of

roughly 35% p.a. (Figure 25). 2015 system-wide sales for the chain were approximated at

US$339 mn (roughly 12% of JFC's system-wide sales or comparable to JFC's domestic

brand Chowking) while store network has also been increasing annually by roughly 20%.

As of 1H16, Smashburger had 366 outlets, mostly in the US (present in 35 states and

seven foreign markets). Over the next 3-5 years, the company looks to increase its store

network by 60 to 80 stores (gross) annually.

Figure 24: US fast casual system sales market

share—Top 20 (2015A)

Figure 25: US fast casual players historical CAGR—

(2010-15A)

Source: Technomic, Credit Suisse estimates Source: Technomic, Credit Suisse estimates

Still a number of possibilities to be explored

For a giant like JFC, with its dominance among QSR peers in the market and a number of

resources at hand, we believe that there are a number of options for expansion that have

yet to be considered.

More value-accretive acquisitions

JFC has managed to maintain its dominance as a QSR player largely due to its ability to

make value-accretive acquisitions and grow these companies effectively. According to the

company, Greenwich, for example, had 50 stores in its network upon acquisition. As of

1H16, it had 237 stores. Similarly, Chowking too upon acquisition had just roughly 150

stores in its network which lately JFC has managed to grow to 501, including international

branches. According to the company, in making an acquisition, it prioritises (1) product

taste; (2) a favourable following and customer loyalty; (3) three major flagship products

that account for 50-60% of total revenue; (4) profitability; and (5) attractive valuations. As

of the moment, JFC has stated that it is already domestically well-placed and, should it

Panera Bread27%

Chipotle25%

Zaxby's8%

Five Guys8%

Qdoba4%

Others28%

-6.6%

5.4%

5.8%

8.8%

9.4%

9.8%

11.1%

13.0%

13.7%

14.1%

14.7%

18.2%

19.2%

34.7%

43.2%

45.8%

-10.0% 0.0% 10.0% 20.0% 30.0% 40.0% 50.0%

Baja Fresh

In-N-Out Burger

Schlotzsky's

Potbelly

Qdoba

Panera Bread

Moe's Southwest Grill

Five Guys

Zaxby's

Pollo Tropical

Noodles & Co.

Wingstop

Chipotle

Smashburger

Habit Burger

Zoe's Kitchen

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 16

make another acquisition, it would be in the international market, preferably in the fast

casual segment.

Jollibee in the USA (more OFW areas that the chain hasn't penetrated yet)

As of June, JFC had 85 stores in the US, 33 of which were Jollibee stores. The company

notes that its US-based stores have been recording high-single-digit SSSG with its

Jollibee stores posting double-digit SSSG. Existing Jollibee stores in the US are situated

predominantly on the West Coast with recent openings in Chicago, Queens and New

Jersey. The company plans to open more in Manhattan and Chicago as well as in

Canada.

Development of a mobile app like McDonald's, further IT enhancements

In order to more effectively reach their customers, it is not unlikely that JFC will launch a

mobile app or other varied online platforms which consumers can access through their

smartphones to order food more conveniently. McDonald's launched their mobile

application in 2014, followed shortly by Krispy Kreme which released its version in 2015.

We expect the emerging trend of online platforms in the Philippine fast food industry to

continue to grow, considering the Filipinos' increasing dependence on technology and

need for convenience. Additionally, in our view, chained players like Jollibee are more

likely to leverage on this development as their wider access to resources would allow them

to keep up more easily with the fast-changing lifestyles and preferences of Filipinos.

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 17

Premium for a reason; reiterate OUTPERFORM JFC currently trades at a 41x P/E, above the global sector average for restaurants of 32x

P/E, which we justify based on JFC's clear medium-term growth story and its ability to

deliver escalating returns. Over 2017-18E, we see average ROIC expanding to 21.6% and

EPS growth at 16.5% p.a. Our 2017-18E EPS forecasts are 2.7% higher than consensus

on average.

Attractive risk-reward profile

Consistent financial track record no accident

We base a great deal of our confidence in JFC's future growth on its execution capability,

which can be evidenced by its historical financial track record. Over 2010-15A, JFC

recorded double-digit ROICs ranging from 14.5% to 23.9% (Figure 26), despite the

company's consistent expansion efforts over the past few years and a steady rise in

invested capital. Over 2011-15A, the overall company-owned store network grew 7.9%

p.a. while the franchise store network grew 4.2% p.a. Note that in the midst of this, the

company has also managed a steady net cash position.

Healthy ROICs are supported by relatively stable margins. Over 2011-15A, EBITDA

margins came in at 10.0% on average. Over 2016-18E, we forecast EBITDA margins at

10.4%, on average, as margins should be supported by improving store productivity

(Figure 27).

Figure 26: Ave. ROIC over 2010A-18E Figure 27: EBITDA/average store over 2006A-18E

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

We have also noted consistent bottomline growth over the company's history. Over 2011-

15A, JFC's EPS grew at 13.3% p.a (Figure 28). This has been boosted by a solid topline,

which recorded growth of 13.6% p.a. over the same period (Figure 29).

22.9%

17.4% 17.4%

23.9%

21.4%

14.5%

19.1%

21.2%22.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

12/10A 12/11A 12/12A 12/13A 12/14A 12/15A 12/16E 12/17E 12/18E

2.70 2.85

2.57

2.92

2.66 2.63 2.77

3.34 3.28

2.91

3.63

4.08

4.44

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

2006 2008 2010 2012 2014 2016E 2018E

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 18

Figure 28: Net income growth—2006A-18E Figure 29: Topline growth—2006A-18E

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

For 2017-18E, we expect bottomline growth of 16.5% p.a. to be supported by topline

growth of 13.6% p.a., on average, over the same period of time.

Valuation relative to peers

We think JFC's premium valuations can also be justified on a peer comparison (Figure 30).

Within our Philipines consumer sector coverage, JFC records the second-highest market

cap, second only to URC. It, however, is expected to record one of the highest average

ROICs under our coverage over 2017-18E at 21.6%, surpassing the Philipines consumer

sector weighted average ROIC of 19.8%, over the same period. 2017-18E EPS growth of

16.5% p.a. is also expected to exceed the estimated weighted average of 15.4% for the

Philipines consumer sector.

Figure 30: CS Phils consumer valuation summary

Company ticker TP (P) CS rating MktCap

(US$mn)

ROIC (%) P/E (x) EPS growth (%)

2015 2016E 2017E 2018E 2015 2016E 2017E 2018E 2015 2016E 2017E 2018E

JFC.PS 295.5 O 5,537 14.5 19.1 21.2 22.0 46.1 41.2 34.6 30.4 9.4 11.9 19.0 13.9

URC.PS 238.5 O 8,363 21.4 20.0 21.6 23.5 32.0 28.7 24.5 21.1 9.7 11.6 17.1 16.0

DNL.PS 13.6 O 1,687 15.9 18.9 20.9 22.1 37.1 31.0 26.0 23.2 24.9 19.7 19.1 12.0

EMP.PS 7.6 N 2,405 15.8 12.5 12.0 13.0 16.7 17.1 15.8 14.4 5.0 (2.7) 8.7 9.7

RRHI.PS 80.1 N 2,250 10.6 10.8 12.2 13.7 25.0 22.5 19.4 17.2 20.4 11.0 15.9 13.0

SSI.PS 4.0 N 200 7.9 7.2 8.1 10.1 10.1 12.1 11.0 8.0 (36.1) (16.7) 9.9 37.5

Average 14.3 14.7 16.0 17.4 27.8 25.4 21.9 19.1 5.6 5.8 15.0 17.0

Weighted average 17.1 17.6 19.1 20.5 33.5 30.1 25.6 22.4 11.1 10.3 16.6 14.2

Source: Company data, Credit Suisse estimates

On a more global scale, we also note that in terms of P/E, Jollibee trades relatively in line

with other emerging QSR stocks, segregated in the first half of the matrix, while

simultaneously delivering healthy EPS growth (Figure 31).

29%

11%

-3%

15%

20%

1%

15%

25%

15%

10%

12%

19%

14%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

E

2017

E

2018

E

17%

14%

13%

9%

11%

17%

14%13% 13%

11%

15%

14% 14%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

E

2017

E

2018

E

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 19

Figure 31: JFC P/E and EPS CAGR versus peers

Company Ticker P/E EPS CAGR Remarks

IMC Alimentacao MEAL3.SA 70.7 (180.9) Bloomberg based; 2017E P/E, 2015-18E CAGR

Jollibee Foods Corporation JFC.PS 34.6 14.9 2017 P/E, 2015-18E CAGR

Arcos Dorados Holdings Inc. ARCO.N 34.3 (135.0) Bloomberg based; 2017E P/E, 2015-18E CAGR

Central Plaza Hotel PCL CENTEL.BK 25.1 12.0 2017 P/E, 2015-18E CAGR

PT Fast Food Indonesia Tbk FAST.JK 18.8 15.1 Bloomberg based; 2017E P/E, 2015-18E CAGR

Chipotle Mexican Grill, Inc. CMG.N 40.0 (1.3) 2017E P/E, 2015-18E CAGR

Jubilant Foodworks JUBI.BO 37.4 27.3 2018E P/E, 2016-19E CAGR

Domino's Pizza Group DOM.L 21.2 18.7 2017E P/E, 2015-18E CAGR

McDonald's Corp MCD.N 18.9 10.1 2017E P/E, 2015-18E CAGR

Wendy's Company WEN.OQ 22.9 18.7 2017E P/E, 2015-18E CAGR

Yum! Brands, Inc. YUM.N 21.7 14.0 2017E P/E, 2015-18E CAGR

Domino's Pizza Enterprises Ltd. DMP.AX 51.5 36.9 Bloomberg based; 2017E P/E, 2015-18E CAGR

Source: Company data, the BLOOMBERG PROFESSIONAL™ service, Credit Suisse estimates

Target P/E based TP of P296.0

With a turnaround in FY16E and as both topline growth and margin expansion are

expected to quicken into FY17-18E, we believe there is room for the stock to re-rate

further.

As discussed in our consumer sector initiation report (Value creating growth, 7 December,

2015), in our view, a more robust valuation framework is one that focuses on incremental

returns since a company can grow its EPS without creating shareholder value. We utilise a

stylised model created by our Global Financial Strategies team to guide our target P/E

multiple. The model looks at P/Es, given different scenarios for ROIC and earnings growth.

For 2017E-18E, we forecast an average ROIC of 21.6% and EPS growth of 16.5% p.a.

Therefore, we set a target P/E of 41x (Figure 32). Applying this to our 2017E EPS forecast

of P7.22 yields a target price of P296.0.

Figure 32: Graph of P/E and ROIC given different

scenarios for growth; WACC held constant (x) Figure 33: Past five-year P/E band

Source: Credit Suisse estimates Source: Thomson Reuters Datastream, Credit Suisse estimates

Our target P/E is at a 33% premium to the stock's past five-year average of 30.9x. The

stock currently trades at a forward P/E of 41x. We note that over the past three years, JFC

10

15

20

25

30

35

40

45

50

0.1 0.125 0.15 0.175 0.2 0.225

P/E (x)

ROIC

12.5% growth 15.0% growth 17.5% growth

17

22

27

32

37

42

47

Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Fwd PER Ave-2SD Ave-1SD

Average Ave+1SD Ave+2SD

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 20

has traded, on average, at a 123% premium to the market. This could be the inherent

scarcity premium placed on the stock as it is one of two pure consumer plays available in

the index. According to Bloomberg, the stock currently trades slightly below historical

levels at a 118% premium to the market.

Figure 34: JFC premium to market

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E

PCOMP 16.0 12.3 14.0 13.5 15.7 18.1 17.3 20.5 20.6 19.4

JFC 22.0 18.3 21.1 29.5 28.8 28.5 38.9 42.4 48.6 42.2

Premium to market 37.7% 49.3% 50.7% 119.2% 83.1% 57.6% 124.7% 106.8% 136.2% 117.6%

Source: Bloomberg, Credit Suisse estimates

Investment risks

Macroeconomic risks

As the Philippines continues to provide the bulk of JFC's business at 80% of revenue

recently, any adverse change in the current economic and political environment that could

prove negative to consumer sentiment could also potentially act as a definite downside

risk to our numbers. The current proposal being discussed regarding the implementation

of a soft drinks tax, for example, looks to impose an extra charge of P10 for every liter of

sugary drinks with a mandatory increase of 4% every year effective January 2017. While

the company states that this kind of measure would be passed on to customers, a material

change in price could again deter more price-sensitive customers and dampen consumer

demand. Current end-of-contract scheme talks also imply upside risks to costs and

operating expenses. As of 2016, approximately 72% of JFC's employees are employed on

a contractual basis.

Commodity price risk

The company has observed that commodity prices normally increase after elections as

inflation picks up. While the company is looking to proactively manage this with its

standard pricing policy, a significant increase in inventory cost that the company would be

unable to offset could again reduce our current earnings estimates. As of 1H16, cost of

inventories as a percentage of revenue stood at 48.3%.

Execution risks

The success of JFC's future growth lies in its ability to expand successfully, organically or

through M&As. Risks regarding overexpansion of its store network, unprofitable business

ventures, or entry into crowded fast food markets could serve as potential downside risks

to our numbers. Increased competition, particularly in its businesses abroad, could also

weaken topline growth.

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 21

Companies Mentioned (Price as of 26-Sep-2016) Arcos Dorados (ARCO.N, $5.39) Central Plaza Hotel PCL (CENTEL.BK, Bt40.0) Chipotle Mexican Grill, Inc. (CMG.N, $419.88) D&L Industries, Inc. (DNL.PS, P11.4) Domino's Pizza (DMP.AX, A$71.49) Domino's Pizza Group (DOM.L, 358.2p) Emperador Inc. (EMP.PS, P7.2) Fast Food ID (FAST.JK, Rp1,370) International Meal Company Holdings (MEAL3.SA, R$5.3) Jollibee Foods Corporation (JFC.PS, P249.8, OUTPERFORM, TP P296.0) Jubilant Foodworks (JUBI.BO, Rs958.6) McDonald's Corp (MCD.N, $116.53) Robinsons Retail Holdings, Inc. (RRHI.PS, P78.4) SSI Group, Inc. (SSI.PS, P2.92) Universal Robina Corporation (URC.PS, P185.0) Wendy's Company (WEN.OQ, $10.8) Yum! Brands, Inc. (YUM.N, $89.52)

Disclosure Appendix

Important Global Disclosures Sofia Cabral and Arnab Mitra each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

3-Year Price and Rating History for Jollibee Foods Corporation (JFC.PS)

JFC.PS Closing Price Target Price

Date (P) (P) Rating

06-Dec-13 170.00 205.00 O *

24-Feb-15 219.60 202.00 N

07-Dec-15 206.00 261.90 O *

19-May-16 233.60 262.30

10-Aug-16 252.20 262.30 *

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows: Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark* over the next 12 months. Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months. Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months. *Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S . and Canadian as well as European ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin American and non -Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or region al benchmark; prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiv eness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand stocks, the expected total return (ETR) calculation includes 12 -month rolling dividend yield. An Outperform rating is assigned where an ETR is greater than or equal to 7.5%; Underperform where an ETR less than or equa l to 5%. A Neutral may be assigned where the ETR is between -5% and 15%. The overlapping rating range allows analysts to assign a rating that puts ETR in the context of associated risks. Prior to 18 May 2015, ETR ranges for Outperform and Underperform ratings did not overlap with Neutral thresholds between 15% and 7.5%, which was in operation from 7 July 2011. Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances. Not Rated (NR) : Credit Suisse Equity Research does not have an investment rating or view on the stock or any other securities related to the company at this time. Not Covered (NC) : Credit Suisse Equity Research does not provide ongoing coverage of the company or offer an investment rating or investment view on the equity security of the company or related products.

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 22

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation: Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months. Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months. Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months. *An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cover multiple sectors.

Credit Suisse's distribution of stock ratings (and banking clients) is:

Global Ratings Distribution

Rating Versus universe (%) Of which banking clients (%) Outperform/Buy* 53% (50% banking clients) Neutral/Hold* 29% (24% banking clients) Underperform/Sell* 18% (44% banking clients) Restricted 0% *For purposes of the NYSE and NASD ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, an d Underperform most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy or sell a security should be based on investment objectives, current holdin gs, and other individual factors.

Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein. Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: http://www.csfb.com/research-and-analytics/disclaimer/managing_conflicts_disclaimer.html Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties.

Target Price and Rating Valuation Methodology and Risks: (12 months) for Jollibee Foods Corporation (JFC.PS)

Method: Utilising the stylised model from our CS Global Financial Strategies team, 2017E-18E average forecasts for ROIC of 21.6% and EPS growth of 16.5% p.a., we set a target P/E of 41.0x. Applying this to our 2017E EPS forecast yields a target price of P296.0. Our OUTPERFORM rating for Jollibee Foods Corporation reflects our positive view on the fundamentals of consumption growth in the Philippines and execution ability of the company.

Risk: Risks to our P296.0 target price and OUTPERFORM for Jollibee Foods Corporation include downward EPS revisions and lower-than-expected ROIC.

Please refer to the firm's disclosure website at https://rave.credit-suisse.com/disclosures for the definitions of abbreviations typically used in the target price method and risk sections.

See the Companies Mentioned section for full company names Please visit https://credit-suisse.com/in/researchdisclosure for additional disclosures mandated vide Securities And Exchange Board of India (Research Analysts) Regulations, 2014 Credit Suisse may have interest in (JUBI.BO)

For date and time of production, dissemination and history of recommendation for the subject company(ies) featured in this report, disseminated within the past 12 months, please refer to the link: https://rave.credit-suisse.com/disclosures/view/report?i=260190&v=-1nb8tlmy49otdl2l3spunc9my .

Important Regional Disclosures Singapore recipients should contact Credit Suisse AG, Singapore Branch for any matters arising from this research report. The analyst(s) involved in the preparation of this report may participate in events hosted by the subject company, including site visits. Credit Suisse does not accept or permit analysts to accept payment or reimbursement for travel expenses associated with these events. Restrictions on certain Canadian securities are indicated by the following abbreviations: NVS--Non-Voting shares; RVS--Restricted Voting Shares; SVS--Subordinate Voting Shares. Individuals receiving this report from a Canadian investment dealer that is not affiliated with Credit Suisse should be advised that this report may not contain regulatory disclosures the non-affiliated Canadian investment dealer would be required to make if this were its own report. For Credit Suisse Securities (Canada), Inc.'s policies and procedures regarding the dissemination of equity research, please visit https://www.credit-suisse.com/sites/disclaimers-ib/en/canada-research-policy.html. Principal is not guaranteed in the case of equities because equity prices are variable. Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that. This research report is authored by: Credit Suisse Securities (Philippines) Inc. ........................................................................................................................................... Sofia Cabral Credit Suisse Securities (India) Private Limited .................................................................................................................................... Arnab Mitra To the extent this is a report authored in whole or in part by a non-U.S. analyst and is made available in the U.S., the following are important disclosures regarding any non-U.S. analyst contributors: The non-U.S. research analysts listed below (if any) are not registered/qualified as research

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 23

analysts with FINRA. The non-U.S. research analysts listed below may not be associated persons of CSSU and therefore may not be subject to the NASD Rule 2711 and NYSE Rule 472 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account. Credit Suisse Securities (Philippines) Inc. ........................................................................................................................................... Sofia Cabral Credit Suisse Securities (India) Private Limited .................................................................................................................................... Arnab Mitra

For Credit Suisse disclosure information on other companies mentioned in this report, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

27 September 2016

Jollibee Foods Corporation (JFC.PS / JFC PM) 24

This report is produced by subsidiaries and affiliates of Credit Suisse operating under its Global Markets Division. For more information on our structure, please use the following link: https://www.credit-suisse.com/who-we-are This report may contain material that is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Credit Suisse or its affiliates ("CS") to any registration or licensing requirement within such jurisdiction. All material presented in this report, unless specifically indicated otherwise, is under copyright to CS. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of CS. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of CS or its affiliates.The information, tools and material presented in this report are provided to you for information purposes only and are not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. CS may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. CS will not treat recipients of this report as its customers by virtue of their receiving this report. The investments and services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about such investments or investment services. Nothing in this report constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. CS does not advise on the tax consequences of investments and you are advised to contact an independent tax adviser. Please note in particular that the bases and levels of taxation may change. Information and opinions presented in this report have been obtained or derived from sources believed by CS to be reliable, but CS makes no representation as to their accuracy or completeness. CS accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to CS. This report is not to be relied upon in substitution for the exercise of independent judgment. CS may have issued, and may in the future issue, other communications that are inconsistent with, and reach different conclusions from, the information presented in this report. Those communications reflect the different assumptions, views and analytical methods of the analysts who prepared them and CS is under no obligation to ensure that such other communications are brought to the attention of any recipient of this report. Some investments referred to in this report will be offered solely by a single entity and in the case of some investments solely by CS, or an associate of CS or CS may be the only market maker in such investments. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment at its original date of publication by CS and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. Investors in securities such as ADR's, the values of which are influenced by currency volatility, effectively assume this risk. Structured securities are complex instruments, typically involve a high degree of risk and are intended for sale only to sophisticated investors who are capable of understanding and assuming the risks involved. The market value of any structured security may be affected by changes in economic, financial and political factors (including, but not limited to, spot and forward interest and exchange rates), time to maturity, market conditions and volatility, and the credit quality of any issuer or reference issuer. Any investor interested in purchasing a structured product should conduct their own investigation and analysis of the product and consult with their own professional advisers as to the risks involved in making such a purchase. Some investments discussed in this report may have a high level of volatility. High volatility investments may experience sudden and large falls in their value causing losses when that investment is realised. Those losses may equal your original investment. Indeed, in the case of some investments the potential losses may exceed the amount of initial investment and, in such circumstances, you may be required to pay more money to support those losses. Income yields from investments may fluctuate and, in consequence, initial capital paid to make the investment may be used as part of that income yield. Some investments may not be readily realisable and it may be difficult to sell or realise those investments, similarly it may prove difficult for you to obtain reliable information about the value, or risks, to which such an investment is exposed. This report may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the report refers to website material of CS, CS has not reviewed any such site and takes no responsibility for the content contained therein. Such address or hyperlink (including addresses or hyperlinks to CS's own website material) is provided solely for your convenience and information and the content of any such website does not in any way form part of this document. Accessing such website or following such link through this report or CS's website shall be at your own risk.