Embed Size (px)

Citation preview

For professional investors and advisers only. This material is not suitable for retail clients

Responding to the DC

investment challenge Schroders Defined Contribution

Conference 2016

Peter Weidner, Head of Advanced Beta

Remi Olu-Pitan, Fund Manager Multi-Asset

Ugo Montrucchio, Fund Manager Multi-Asset

@SchroderPension

Value of savings

The DC journey Gradual transition from working life to retirement

1

Source: Schroders, for illustration only

20/05/2016 10:39:31

Stable

growth Transition

to retirement

Time

Late retirement Growth

Normal retirement age

Early in retirement

Members can afford to take

on more risk

Investment returns and

risk become the dominant

factor

Focus on protecting

value

Responding to the DC

investment challenge

Growth phase

Peter Weidner, Head of Advanced Beta

What is ‘smart beta’? Many names…

Smart beta Alternative beta

Scientific beta

Alternative Beta Advanced beta Factor investing

3

What attracts investors to smart beta?

4

Source: MSCI, Morningstar. Gross total return in USD for the period of 31 December 1995 to 31 December 2015

20/05/2016 10:39:31

MSCI World

Minimum volatility

Value

Quality

Risk-weighted

Equal-weighted

Momentum

6.0%

9.0%

12.0%

11.0% 15.0% 19.0%

Annualised risk

Annualised return

High return and low risk

Low return and low risk

High return and high risk

Low return and high risk

Common pitfalls with smart beta investing Issues to watch out for

5

Source: Schroders, for illustration only

20/05/2016 10:39:31

Individual factor returns can be

highly cyclical

Uncontrolled scale may lead to poor

factor exposure and

uncompensated risks

Risk management

Products are designed for mass

market appeal

Investment guidelines are seldom

revised once they are in the public

domain

Implementation

Onus is placed on investors to

choose which factor(s) resonate

with their own investment views

Governance

A given factor can be implemented in many

different ways

– Fama-French factors are not investible and rely

heavily on small cap stocks

– Leading index factors are massively investible and

rely heavily on large cap stocks

“Value” portfolios can contain more or less value

depending on construction and intended capacity

– Three MSCI value indices: moderately correlated

active returns, very different cumulative returns

Not all factor portfolios are created equal Factors can be generic; however, investments are specific

6

Source: Schroders, Bloomberg, 31 December 2015

0

50

100

150

200

250

300

Dec-9

7

Oct-

98

Aug

-99

Ju

n-0

0

Apr-

01

Feb-0

2

Dec-0

2

Oct-

03

Aug

-04

Ju

n-0

5

Apr-

06

Feb-0

7

Dec-0

7

Oct-

08

Aug

-09

Ju

n-1

0

Apr-

11

Feb-1

2

Dec-1

2

Oct-

13

Aug

-14

Ju

n-1

5

ACWI ENHANCED VALUE Standard (Large+Mid Cap) Enhanced Value

ACWI PRIME VALUE Standard (Large+Mid Cap) Prime Value

ACWI VALUE WEIGHTED Standard (Large+Mid Cap) Value Weighted

Total active returns compared to MSCI ACWI

EVOLUTION

Incorporate latest academic and

proprietary research to ensure

strategies evolve with markets

Continuously monitor factors to

ensure portfolios reflect best ideas

ACCESS

Utilise style investing insights to

manage market risks

Minimise unintended risk

exposures to enhance risk-adjusted

returns

SOLUTIONS

Use advanced beta strategies as

building blocks within portfolios or

for the creation of new, stand-alone

solutions for client

Schroders advanced beta Our core competencies

7

Source: Schroders

Putting it all together Designing a solution to achieve equity-like returns, but with lower risk

Source: Schroders, 31 March 2016. For illustration only. *Inception date of sample portfolio is 21 November 2014. ‘Since inception’ performance data is for the period 21 November 2014 to 31 March

2016 and is stated in GBP. Benchmark MSCI AC World (NDR) TL. Portfolio is a segregated multi-factor portfolio managed for a UK Insurance client

8

Asset allocation

Value Quality Low Volatility Size

Performance (since inception) Portfolio* Benchmark

Annualised return 7.1% 3.5%

Volatility 12.0% 14.6%

Maximum drawdown -9.3% -10.9%

Portfolio characteristics Portfolio* Benchmark

Dividend yield 3.0% 2.7%

Return on equity 26.6% 20.7%

Price to earnings 16.8 18.5

Price to book 2.2 2.0

Responding to the DC

investment challenge

Stable growth phase

Remi Olu-Pitan, Fund Manager Multi-Asset

Returns matter in the stable growth phase Investment returns and risk become the dominant factor

Source: Schroders, for illustration only. 40 year contributions at base contribution rate of 10% of salary. Salary increases assumed to be 3% p.a. Starting salary is £25,000. Base annual investment

returns are estimated expected returns of a lifestyling strategy switching from equities to bonds and cash in the 10 years prior to retirement

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

First 20 years Second 20 years

1% increase in contribution rate 1% increase in investment return

% Increase in final pot

Early years: Increasing contributions and

investment returns have similar effect

Later years: Investment returns much

more important

10

Equities Deliver the returns…but beware of the adverse outcomes

11

Source: Schroders, Robert Shiller. Data shows 20 year rolling annualised returns from 1871 to 2016. Equities represent the S&P 500 Index

0

2

4

6

8

10

12

14

16

18

20

1891 1899 1908 1916 1924 1933 1941 1949 1958 1966 1974 1983 1991 1999 2008 2016

Rolling annualised 20Y return to equities

145-year average: 9% per annum

Best 20 year period: 18% per annum

Worst 20 year period: 2% per annum

Diversify Asset classes perform at different times…but correlations are unstable

12

Source: Schroders, Datastream, 31 December 2015. Equity: MSCI AC World Total Return Index, Property: UK IPD Index, Hedge Funds: HFRI Funds of Funds Composite Total Return Index,

Cash: 3 month Sterling LIBOR, Credit: Barclays Global High Yield Index, Govts: Barclays Global Treasury Index; Property: UK IPD Index; Commods: Bloomberg Commodity Index; EMD:

JPM GBI-EM Composite Index; ILS: Swiss Re Cat Bond Index. All show total return either in local currency or currency of denomination

20/05/2016 10:39:31

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Equity

26.40% Property

18.90%

Commods

21.40%

Property

18.10%

Commods

16.20%

Govts

10.20%

Credit

46.80%

Commods

16.80%

Property

8.10%

Equity

16.50%

Equity

26.20%

Property

19.30%

Property

7.59%

Credit

24.10% Equity

12.00%

Property

18.80%

Equity

17.00%

ILS

15.70%

EMD

10.20%

Equity

30.00%

Property

14.50%

EMD

6.40%

EMD

14.10%

ILS

11.40%

Equity

9.90% ILS

4.45%

Commods

23.90% Govts

10.30%

Equity

17.40%

ILS

12.30%

Govts

10.60%

Cash

5.50%

Commods

18.90%

Credit

12.30%

Govts

6.30%

ILS

10.50%

Property

10.90%

EMD

8.70%

EMD

3.39%

Govts

14.80% EMD

10.20% EMD

10.00%

Hedge

Funds

10.40%

Hedge

Funds

10.30%

ILS

2.30%

ILS

13.90%

ILS

11.30%

ILS

3.30% Credit

9.60%

Hedge

Funds

9.00%

ILS

6.30% Cash

0.50%

Hedge Funds

11.60%

Commods

9.10%

Hedge

Funds

7.50%

EMD

7.40%

Equity

7.70%

Hedge

Funds

-21.40%

Hedge

Funds

11.50%

Equity

11.10%

Cash

0.90%

Hedge

Funds

4.80%

EMD

0.90%

Hedge

Funds

3.40%

Equity

0.15%

Property

11.20%

Hedge

Funds

6.90%

Cash

4.70%

Govts

6.40%

Cash

6.00%

Property

-22.50%

EMD

6.70%

EMD

9.70%

Credit

-5.00% Property

2.40%

Cash

0.50% Cash

0.50%

Hedge

Funds

-0.23%

EMD

7.20% ILS

6.40%

ILS

1.50%

Cash

4.90%

EMD

5.50% Credit

-35.10% Govts

2.60%

Govts

5.90%

Hedge

Funds

-5.70%

Govts

1.80% Credit

-2.00%

Govts

-0.80%

Govts

-2.13%

ILS

7.10% Cash

4.70%

Credit

-3.90%

Credit

2.70%

Property

-5.50%

Commods

-35.60%

Property

2.20%

Hedge

Funds

5.70%

Equity

-6.00%

Cash

0.80% Govts

-4.30% Credit

-3.90% Credit

-7.62%

Cash

3.70% Credit

2.70%

Govts

-6.70%

Commods

2.10%

Credit

-7.60%

Equity

-39.20%

Cash

1.20%

Cash

0.70%

Commods

-13.30%

Commods

-1.10%

Commods

-9.50%

Commods

-17.00%

Commods

-24.66%

Best performing asset class

Worse performing asset class

Recovery

Output below trend,

Growth accelerating,

Inflation falling

Expansion

Output above trend,

Growth accelerating,

Inflation rising

Slow-down

Output above trend,

Growth decelerating,

Inflation rising

Recession

Output below trend,

Growth decelerating,

Inflation falling

Our approach to dynamic asset allocation Different assets to cope with different economic environments

13

Source: Schroders, for illustration only. Average length of full cycle is about 5 – 6 years

20/05/2016 10:39:31

Adjust asset class exposure over the economic cycle

Equity

Property

Infrastructure

Private Equity

High Yield

Equity Long Short

Hedge Funds

Commodities

Private Equity

Property

Equity

Event Driven Hedge Funds

Cash

Government Bonds

Commodities

CTA Hedge Funds

High Yield

Private Equity

Equity

Investment Grade

Global Macro Hedge Funds

Output (GDP)

50

100

150

200

250

300

350

1991 1994 1997 2000 2003 2006 2009 2012 2015

Real commodity prices

Our approach to dynamic asset allocation Valuations matter

14

Source: Bloomberg, Schroders, 31 March 2016. DJUBS Commodities Total Return deflated by US Core CPI, rebased to 31 January 1991 = 100. Sectors and securities are mentioned for illustrative

purposes only and should not be viewed as a recommendation to buy/sell

Real price, 31 January 1991 = 100

Valuations became stretched

-50 to -40 -40 to -30 -30 to -20 -20 to -10 -10 to 0 0 to 10 10 to 20 20 to 30 30 to 40 40 to 50 50 to 60

2015

2013

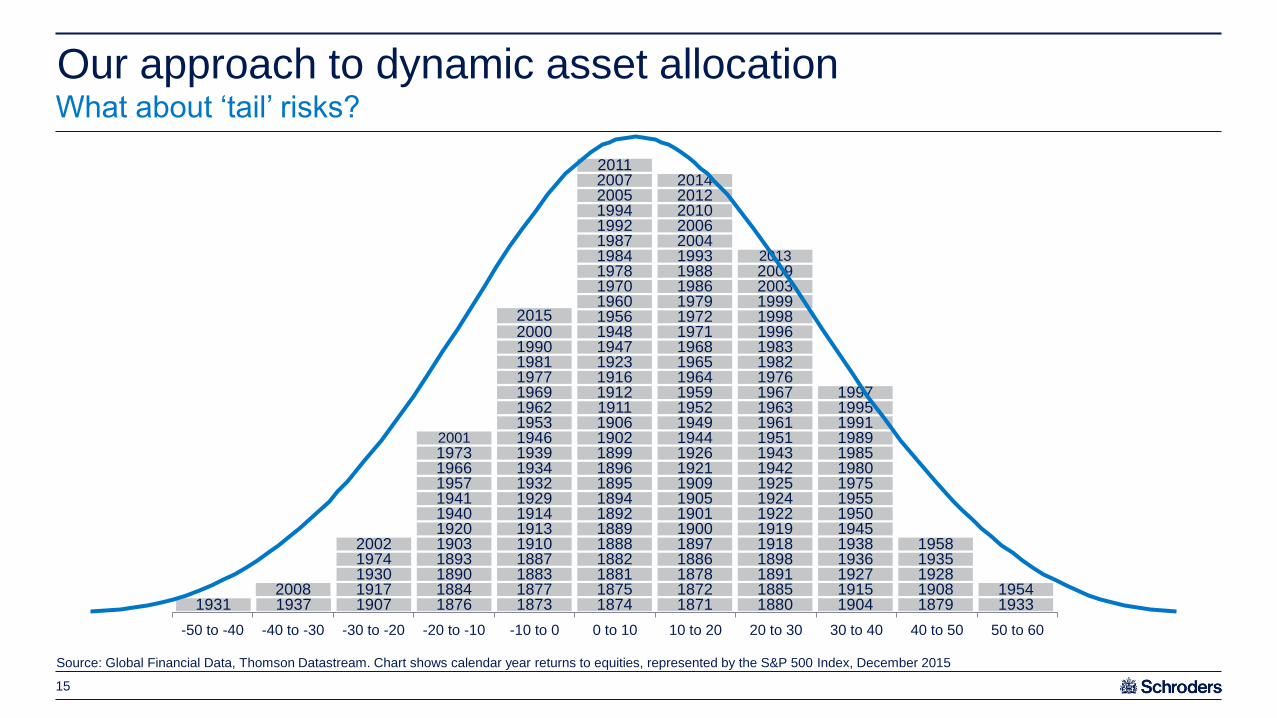

Our approach to dynamic asset allocation

1931 1937 1907 1876 1873 1874 1871 1880 1904 1879 1933 2008 1917 1884 1877 1875 1872 1885 1915 1908 1954

1930 1890 1883 1881 1878 1891 1927 1928 1974 1893 1887 1882 1886 1898 1936 1935 2002 1903 1910 1888 1897 1918 1938 1958

1920 1913 1889 1900 1919 1945 1940 1914 1892 1901 1922 1950 1941 1929 1894 1905 1924 1955 1957 1932 1895 1909 1925 1975 1966 1934 1896 1921 1942 1980 1973 1939 1899 1926 1943 1985 2001 1946 1902 1944 1951 1989

1953 1906 1949 1961 1991 1962 1911 1952 1963 1995 1969 1912 1959 1967 1997 1977 1916 1964 1976 1981 1923 1965 1982 1990 1947 1968 1983 2000 1948 1971 1996

1956 1972 1998 1960 1979 1999 1970 1986 2003 1978 1988 2009 1984 1993 1987 2004 1992 2006 1994 2010 2005 2012 2007 2014 2011

Source: Global Financial Data, Thomson Datastream. Chart shows calendar year returns to equities, represented by the S&P 500 Index, December 2015

What about ‘tail’ risks?

15

Our approach to dynamic asset allocation Consider a range of scenarios and their respective probabilities

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

US recession

China hard landing

EM defaults

emerge

US wages accelerate

Global reflation Baseline

Currency wars return

Source: Schroders. 29 February 2016 forecast. Baseline 2016 forecast 2.4% growth and 3.9% inflation. The opinions stated in this document include some forecasted views. We believe that we are

basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee that any forecasts or opinions will be realised

Stagflationary Reflationary

Productivity boost Deflationary

2016 inflation vs baseline forecast

2016 growth vs baseline forecast

16

OPEC cuts oil production

Our investment objective has two key

elements

A target return objective – UK inflation

(CPI) + 4% per annum

A volatility objective – 1/2 to 2/3 volatility

of global equities

We aim to achieve this objective through:

Diversification

Dynamic asset allocation

Downside risk management

Schroder Life Dynamic Multi-Asset Fund An alternative to equities for the stable growth phase

17

Source: Schroders, May 2016. *The return and maximum loss targets are investment objectives only and not guaranteed

Return target

Cash

Fixed income

Schroder Life

Dynamic

Multi-Asset Fund

“Balanced” fund

Superior risk adjusted returns

Equities

Responding to the DC

investment challenge

Transition into retirement

Ugo Montrucchio, Fund Manager Multi-Asset

‘There is no free lunch, but diversification offers a cheap one’. Financial Times (February 2015)

The case for diversification A precious tool when approaching retirement

19

Source: Bank of America, Schroders, May 2016

20/05/2016 10:39:31

Diversification can experience drawbacks:

Limited by the restrictive nature of asset classes

Value agnostic and may not protect against systemic shocks

Diversified … … not so diversified

BoA UK Gilt Index FTSE 100 Index BoA UK Gilt Index FTSE 100 Index

Capital weight Risk weight

Investors approaching retirement are confronted with two key challenges:

Increasingly challenging to assess safety Asset classes may be deceptive

Hunt for yield: The ongoing financial repression has modified investors’ risk preferences

Volatility: The steady rise blurs the defensive appeal provided by certain asset classes

20

Source: Barclays Capital, Schroders, 3 May 2016. Volatility is calculated using a 1Y rolling window, Nominal yield uses semi-annual convention

20/05/2016 10:39:29

1%

2%

3%

4%

5%

6%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Apr-

01

Apr-

02

Apr-

03

Apr-

04

Apr-

05

Apr-

06

Apr-

07

Apr-

08

Apr-

09

Apr-

10

Apr-

11

Apr-

12

Apr-

13

Apr-

14

Apr-

15

Apr-

16

Gilts volatility [LHS] Nominal Yield [RHS]

Better to think in terms of regimes Identify key sources of return

Focus on the drivers of risk and performance - from asset classes to risk premia

21

Source: Schroders, for illustration only

20/05/2016 10:39:31

Slowdown Growth Inflation

Government bonds

Low yielding currencies

Equities

Credit spreads

Commodities

Inflation-linked bonds

Property

When diversification fails… … a likely scenario?

Years of accommodative monetary policies may have increased the likelihood of tail events moving forward

22

Source: Schroders, BoA, Bloomberg, 3 May 2016. 160 day rolling correlation is calculated using FTSE 100 and BoA UK gilt index returns

20/05/2016 10:39:29

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

May-0

6

De

c-0

6

Ju

l-0

7

Fe

b-0

8

Se

p-0

8

Ap

r-0

9

No

v-0

9

Ju

n-1

0

Ja

n-1

1

Au

g-1

1

Ma

r-1

2

Oct-

12

Ma

y-1

3

De

c-1

3

Ju

l-1

4

Fe

b-1

5

Se

p-1

5

Ap

r-1

6

60 day equity/bonds correlation1

Rely on the ability of a talented manager to

navigate through the evolving phases of a

business cycle

At which point should insurance be

considered?

How can we protect against a ‘diversification failure’? We can’t fully, but tools exist to help us manage it better

23

Source: Schroders, for illustration only. 1Simulations is based on constant return assumptions for equities/bonds/cash and a glide-path designed to completely disinvest from equities by age 65

20/05/2016 10:39:31

Impact of capital loss is more severe for investors approaching

retirement and rebuilding savings is challenging

Time can help mitigate the incidence of losses to capital

accumulation1

Use a long-term approach to investing Skill

Buy some form of protection

0

50

100

150

200

250

300

350

400

450

25 29 33 37 41 45 49 53 57 61 65

Age

Scenario B: 20% capital loss realised at 55 years

Scenario A: 20% capital loss realised at 35 years

Account size (£,000)

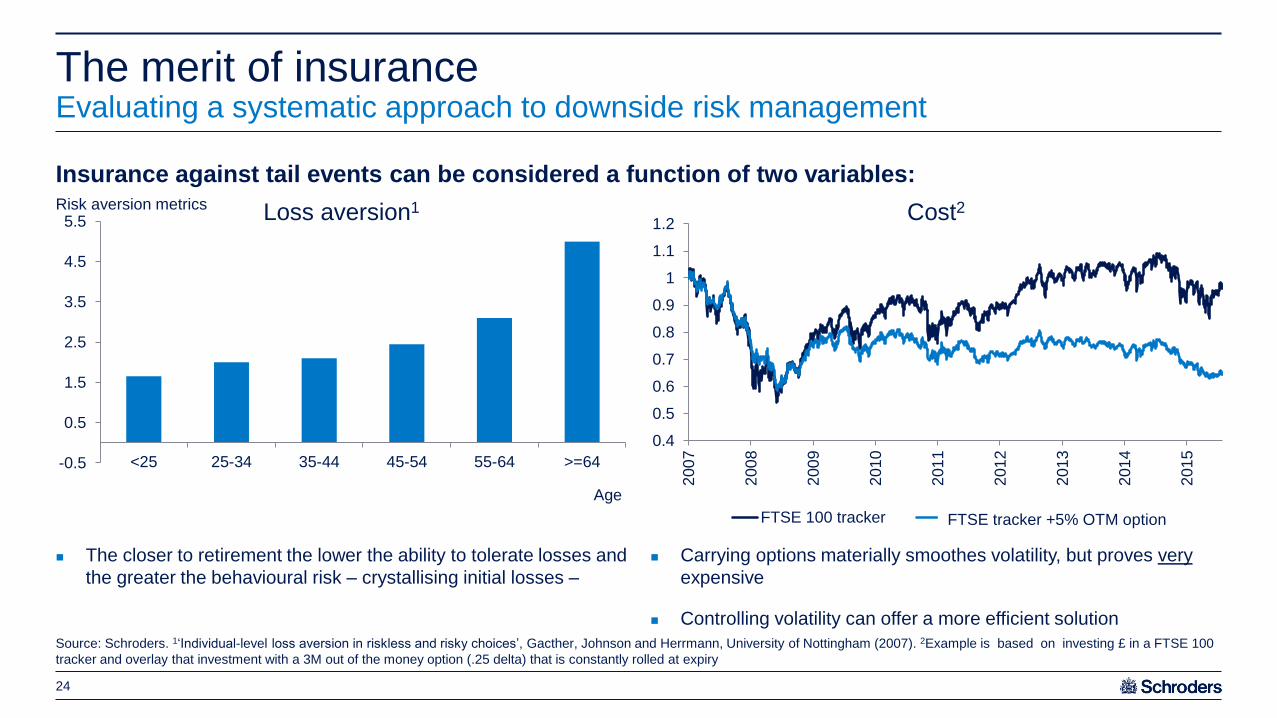

The closer to retirement the lower the ability to tolerate losses and

the greater the behavioural risk – crystallising initial losses –

Carrying options materially smoothes volatility, but proves very

expensive

Controlling volatility can offer a more efficient solution

Loss aversion1 Cost2

The merit of insurance Evaluating a systematic approach to downside risk management

24

Source: Schroders. 1‘Individual-level loss aversion in riskless and risky choices’, Gacther, Johnson and Herrmann, University of Nottingham (2007). 2Example is based on investing £ in a FTSE 100

tracker and overlay that investment with a 3M out of the money option (.25 delta) that is constantly rolled at expiry

20/05/2016 10:39:29

Insurance against tail events can be considered a function of two variables:

-0.5

0.5

1.5

2.5

3.5

4.5

5.5

<25 25-34 35-44 45-54 55-64 >=64

Age

0.4

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

FTSE 100 tracker Ftse tracker + 5% OTM optionFTSE tracker +5% OTM option

Risk aversion metrics

Conclusion Factors to keep in mind as we approach retirement

20/

05/

20

16

10:

39:

31

Diversification remains important – irrespective of the stage of our journey

to retirement

A critical evaluation of asset classes is key – think of how our

investments will evolve through the cycle

Downside risk management can be valuable – sensible implementation

can make a difference

25

For professional investors and advisers only. This material is not suitable for retail clients.

Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as

up and investors may not get back the amount originally invested.

This presentation is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or

solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or

investment recommendations. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. No responsibility can be accepted

for errors of fact or opinion. The data has been sourced by Schroders and should be independently verified before further publication or use. No responsibility can be

accepted for error of fact or opinion. This does not exclude or restrict any duty or liability that Schroders has to its customers under the Financial Services and Markets Act

2000 (as amended from time to time) or any other regulatory system.

The forecasts included in this presentation should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our forecasts are based on our own

assumptions which may change. We accept no responsibility for any errors of fact or opinion and assume no obligation to provide you with any changes to our assumptions

or forecasts. Forecasts and assumptions may be affected by external economic or other factors.

Schroder Life Dynamic Multi-Asset Fund: Where a fund holds investments denominated in currencies other than sterling investors should note that exchange rates may

cause the value of these investments, and the income from them, to rise or fall. Investors should be aware that the fund may invest in derivatives and in alternative

investments (hedge funds, property funds and private equity) which involve an above-average degree of risk and can be more volatile than investment in equities or bonds.

The fund is not tied to replicating a benchmark and holdings can therefore vary from those in the index quoted. For this reason the comparison index should be used for

reference only. Funds which invest in a smaller number of stocks can carry more risk than funds spread across a larger number of companies.

Third party data is owned or licensed by the data provider and may not be reproduced or extracted and used for any other purpose without the data provider's consent.

Third party data is provided without any warranties of any kind. The data provider and issuer of the document shall have no liability in connection with the third party data.

The Prospectus and/or www.schroders.com contains additional disclaimers which apply to the third party data. Exchange Plc and The Financial Times Limited and is used

by FTSE International Limited under licence. All rights in the FTSE indices and / or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any

liability for any errors or omissions in the FTSE indices and / or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express

written consent.

Issued in May 2016 by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registered No: 1893220 England. Authorised and regulated by

the Financial Conduct Authority. INS04828

Important information

26

20/05/2016 10:39:32