Embed Size (px)

Citation preview

Resources equities –

June 2011

An attractive way to play the commodity super cycle

For professional investors or advisers only

Sam Catalano

Portfolio Manager, Global Resources Equities

Gavin Marriott

Product Manager, Global and International Equities

2

Investing to maximise returnsLife in the New Normal

What is the New Normal

– Changes to the fundamental structure of the global economy

– An era of shifting geo-political power and influence

Implications for investors

– An era of lower returns on stocks and bonds

– Challenge to pre-conceived wisdom which will require investors to think differently

33

-

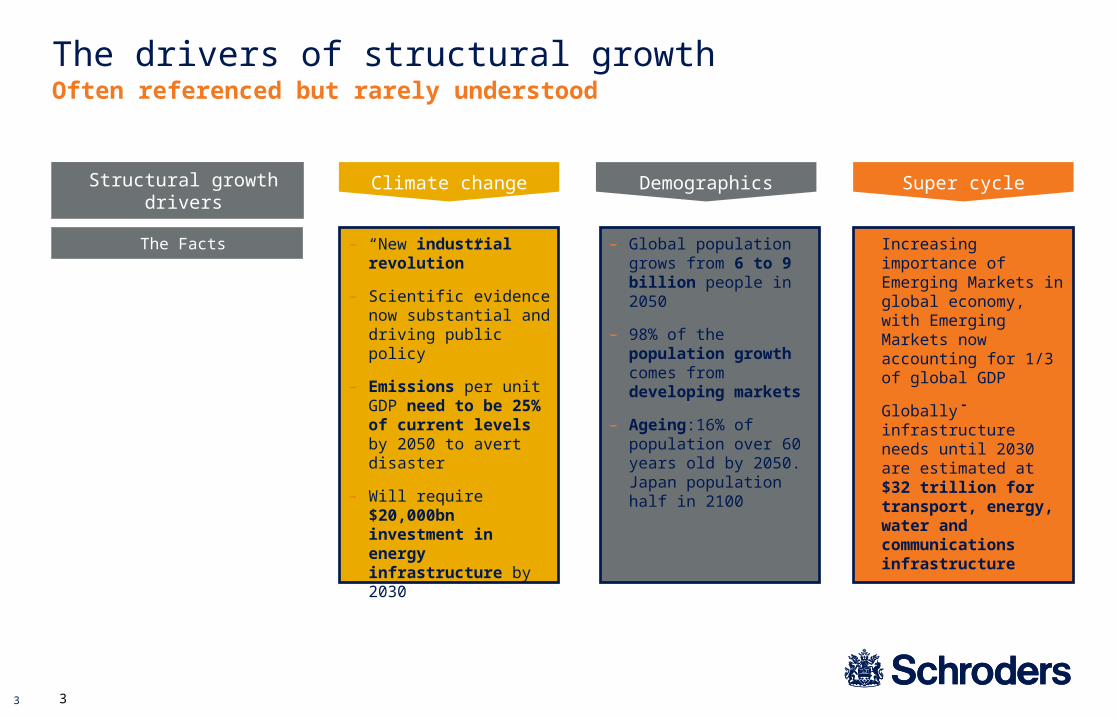

The drivers of structural growthOften referenced but rarely understood

Structural growth drivers

The Facts – Global population grows from 6 to 9 billion people in 2050

– 98% of the population growth comes from developing markets

– Ageing:16% of population over 60 years old by 2050. Japan population half in 2100

– “New industrial revolution”

– Scientific evidence now substantial and driving public policy

– Emissions per unit GDP need to be 25% of current levels by 2050 to avert disaster

– Will require $20,000bn investment in energy infrastructure by 2030

– Increasing importance of Emerging Markets in global economy, with Emerging Markets now accounting for 1/3 of global GDP

– Globally infrastructure needs until 2030 are estimated at $32 trillion for transport, energy, water and communications infrastructure

Climate change Demographics Super cycle

4

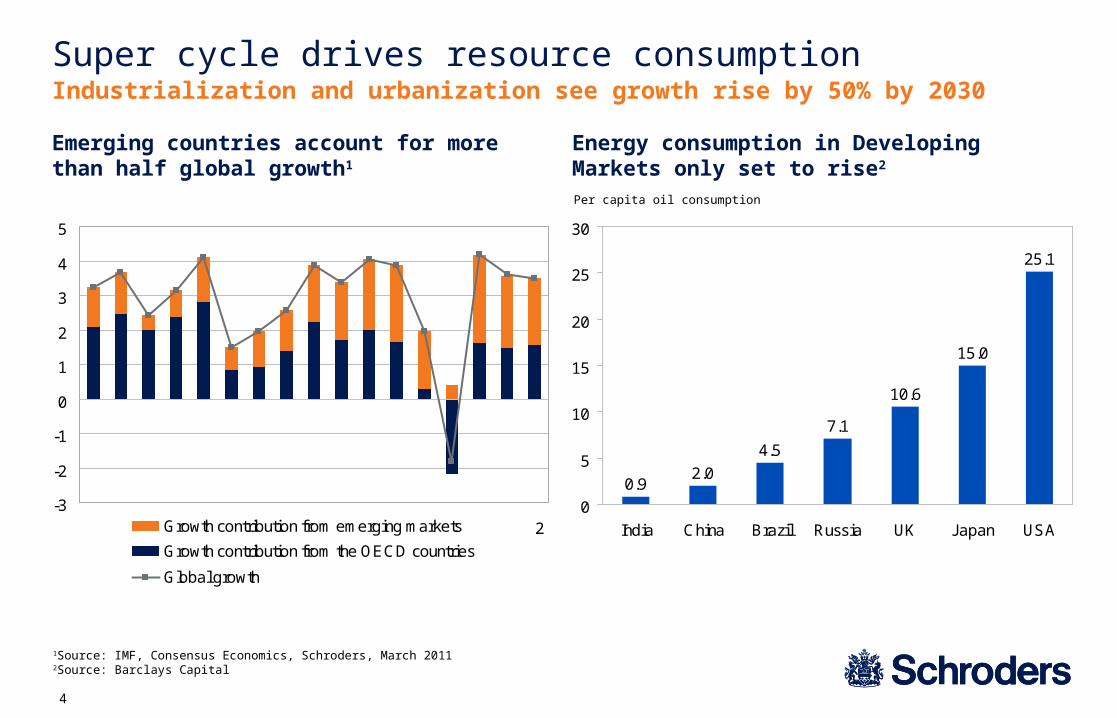

Super cycle drives resource consumptionIndustrialization and urbanization see growth rise by 50% by 2030

0.92.0

4.5

7.1

10.6

15.0

25.1

0

5

10

15

20

25

30

India China Brazil Russia UK Japan USA

Per capita oil consumption

Energy consumption in Developing Markets only set to rise2

-3

-2

-1

0

1

2

3

4

5

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12Growth contribution from emerging markets

Growth contribution from the OECD countries

Global growth

Emerging countries account for more than half global growth1

1Source: IMF, Consensus Economics, Schroders, March 20112Source: Barclays Capital

5

0

100

200

300

400

500

600

700

800

900

19

00

19

04

19

08

19

12

19

16

19

20

19

24

19

28

19

32

19

36

19

40

19

44

19

48

19

52

19

56

19

60

19

64

19

68

19

72

19

76

19

80

19

84

19

88

19

92

19

96

20

00

20

04

20

08

USA China

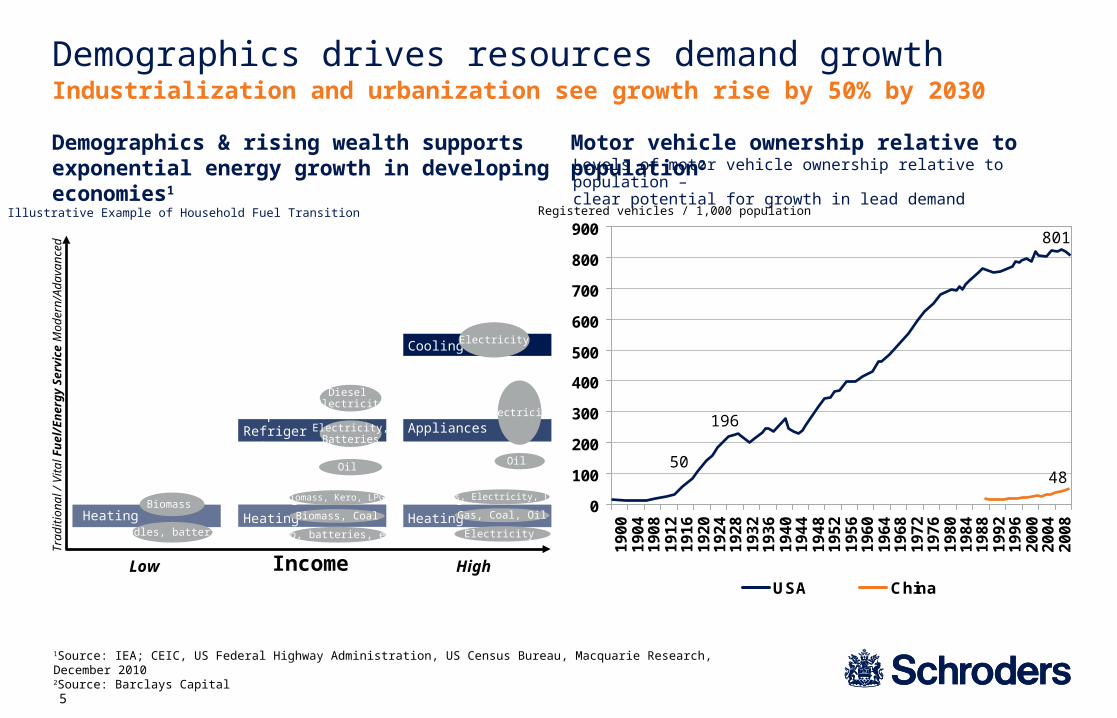

Demographics drives resources demand growth

Demographics & rising wealth supports exponential energy growth in developing economies1

Motor vehicle ownership relative to population2

1Source: IEA; CEIC, US Federal Highway Administration, US Census Bureau, Macquarie Research, December 20102Source: Barclays Capital

50

196

48

801

Registered vehicles / 1,000 population

Levels of motor vehicle ownership relative to population – clear potential for growth in lead demand

Tra

diti

on

al /

Vita

l Fu

el/

En

erg

y S

erv

ice

Mo

de

rn/A

da

van

ced

IncomeLow High

Cooking

Heating

Lighting

Biomass

Candles, batteries

Cooking

Heating

Lighting

Biomass, Kero, LPG

Biomass, Coal

Kero, batteries, elec

Water PumpRefrigerationBasic AppliancesTransport

Diesel Electricity

Electricity,Batteries

Oil

Cooking

Heating

Lighting

Gas, Electricity, LPG

Gas, Coal, Oil

Electricity

RefrigerationBasic Appliances

Transport

Other Appliances

Cooling

ICT

Electricity

Oil

Electricity

Illustrative Example of Household Fuel Transition

Industrialization and urbanization see growth rise by 50% by 2030

6

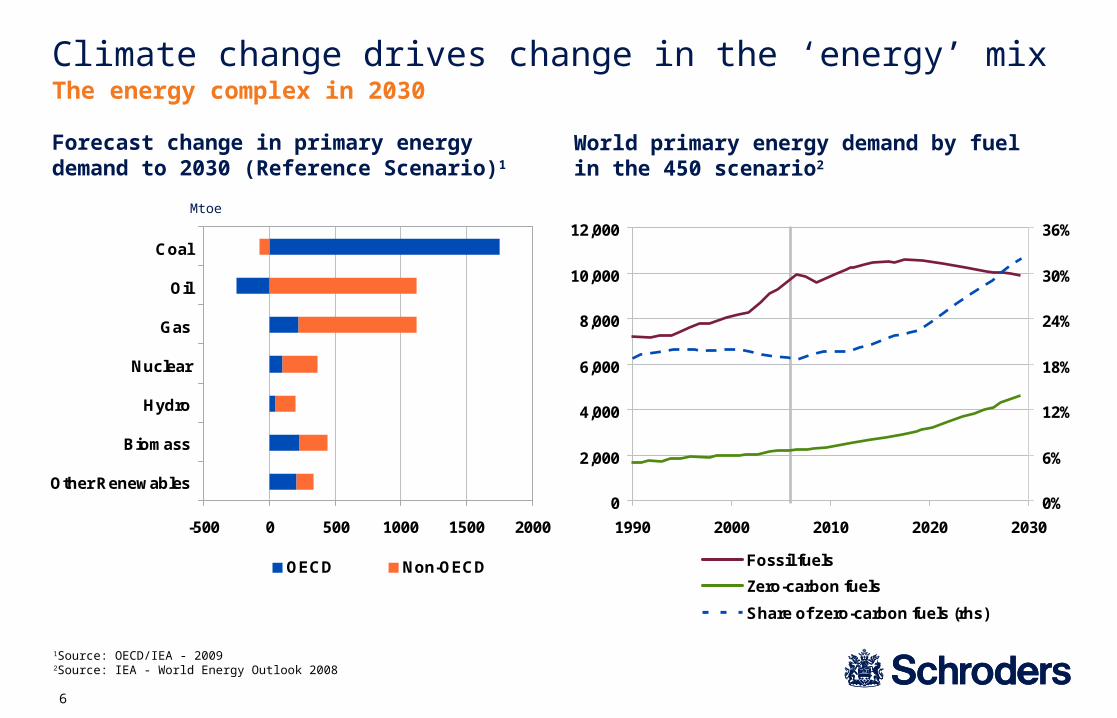

World primary energy demand by fuel in the 450 scenario2

Climate change drives change in the ‘energy’ mixThe energy complex in 2030

-500 0 500 1000 1500 2000

Other Renewables

Biomass

Hydro

Nuclear

Gas

Oil

Coal

OECD Non-OECD

Forecast change in primary energy demand to 2030 (Reference Scenario)1

Mtoe

1Source: OECD/IEA - 20092Source: IEA - World Energy Outlook 2008

0

2,000

4,000

6,000

8,000

10,000

12,000

1990 2000 2010 2020 2030

0%

6%

12%

18%

24%

30%

36%

Fossil fuels

Zero-carbon fuels

Share of zero-carbon fuels (rhs)

7

Demand is only one side of the equationSupply of resources are finite

Access

Quality of Resource Base

Depletion of reserves

Corporate responsibility

Structural supply constraints

8

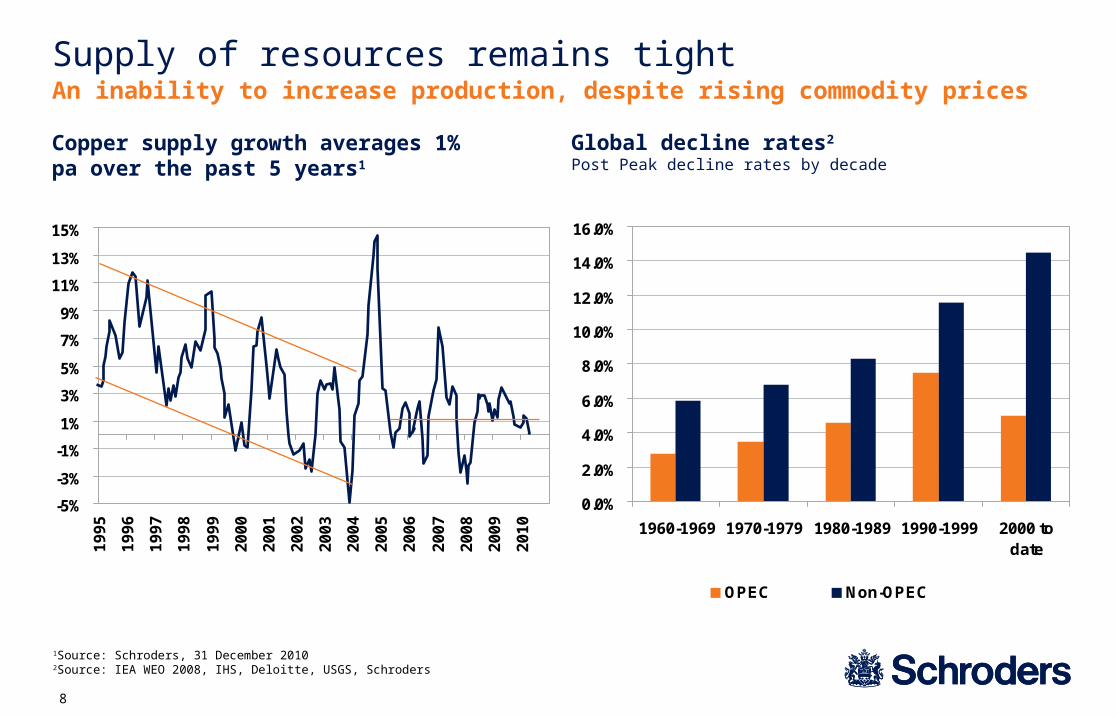

Supply of resources remains tightAn inability to increase production, despite rising commodity prices

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

13%

15%

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Copper supply growth averages 1% pa over the past 5 years1

1Source: Schroders, 31 December 20102Source: IEA WEO 2008, IHS, Deloitte, USGS, Schroders

Global decline rates2

Post Peak decline rates by decade

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

1960-1969 1970-1979 1980-1989 1990-1999 2000 todate

OPEC Non-OPEC

9

What this means in practiceResources are a key beneficiary of structural growth drivers

Demand

– Demand for resources continues to rise

– Although cyclical in nature, structural drivers dominate

Supply

– Resources increasingly constrained

– Limited capacity to deal with demand shocks

Implications for investors

– Resource prices set to rise in the long term

– Demand/supply imbalance creates opportunities for investors

– A source of visible growth underpinning a strategic allocation

– An efficient hedge against inflation

10

10

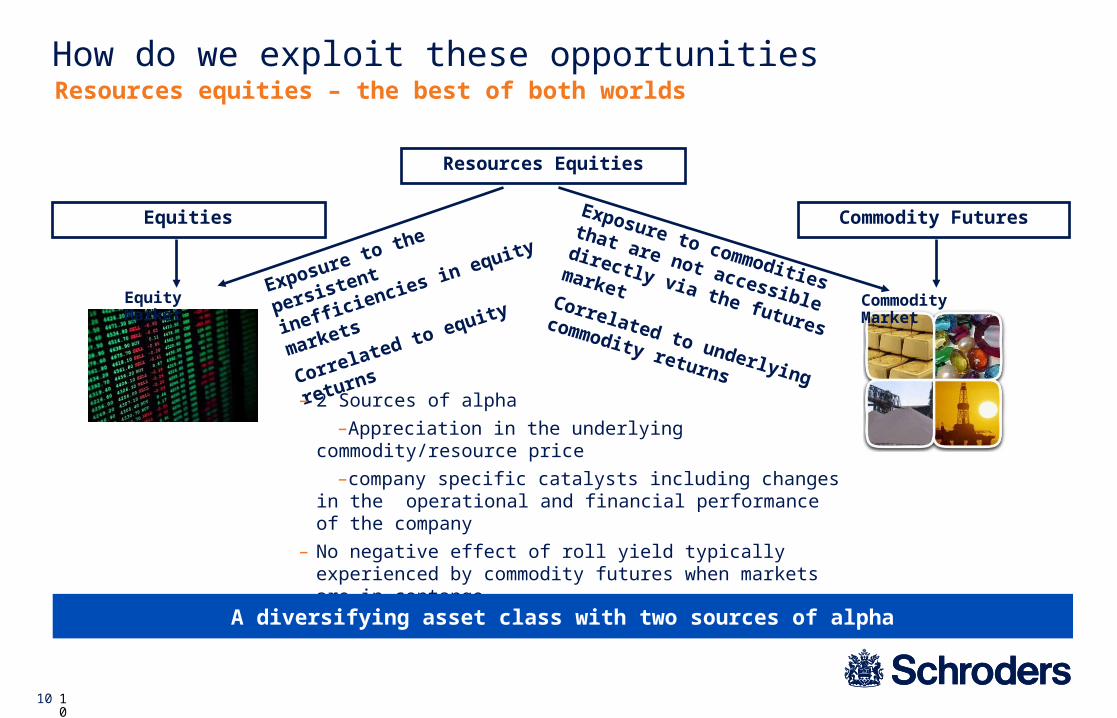

How do we exploit these opportunitiesResources equities – the best of both worlds

Equities

Resources Equities

Commodity Futures

Exposure to the persistent

inefficiencies in equity

markets

Correlated to equity returns

Exposure to commodities that

are not accessible directly via

the futures marketCorrelated to underlying

commodity returns

– 2 Sources of alpha

–Appreciation in the underlying commodity/resource price

–company specific catalysts including changes in the operational and financial performance of the company

– No negative effect of roll yield typically experienced by commodity futures when markets are in contango

– Can accommodate long term strategic positions

Equity Market Commodity Market

A diversifying asset class with two sources of alpha

11

Copper Price compared to First Quantum Minerals

100

120

140

160

180

200

220

240

Sep-10 Nov-10 Jan-11 Mar-11

Copper First Quantum Minerals

For illustrative purposes only and not a recommendation to buy or sell sharesSource: Datastream, USD, 14 April 2011

Why resources equitiesThe best of all worlds – 2 sources of alpha

Rebased to 100

12

The importance of the growth gapForward growth – an indicator of share price performance

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Mar 02 Jun 03 Sep 04 Dec 05 Mar 07 Jun 08 Sep 09

0

5

10

15

20

25

30

35

40

45

Fwd EPS (rhs) Price

Xstrata share price

(£,x) (£/ps)

Source: Macquarie Research, December 2010

13

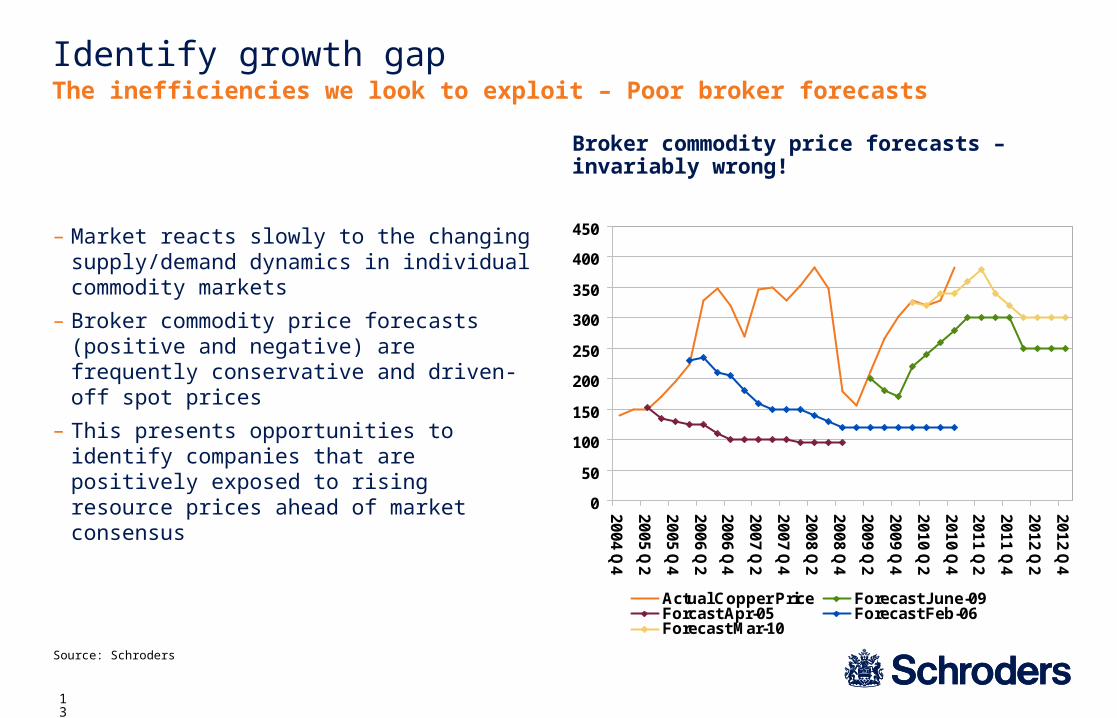

Identify growth gapThe inefficiencies we look to exploit – Poor broker forecasts

– Market reacts slowly to the changing supply/demand dynamics in individual commodity markets

– Broker commodity price forecasts (positive and negative) are frequently conservative and driven-off spot prices

– This presents opportunities to identify companies that are positively exposed to rising resource prices ahead of market consensus

Broker commodity price forecasts – invariably wrong!

0

50

100

150

200

250

300

350

400

450

20

04

Q4

20

05

Q2

20

05

Q4

20

06

Q2

20

06

Q4

20

07

Q2

20

07

Q4

20

08

Q2

20

08

Q4

20

09

Q2

20

09

Q4

20

10

Q2

20

10

Q4

20

11

Q2

20

11

Q4

20

12

Q2

20

12

Q4

Actual Copper Price Forecast June-09Forcast Apr-05 Forecast Feb-06Forecast Mar-10

Source: Schroders

14

0

200

400

600

800

1,000

1,200

1,400

Mar 10 May 10 Jul 10 Sep 10 Nov 10

100

150

200

250

300

350

400

450

This year

Identify growth gapPoor broker forecasts – Stock example

Walter Energy WLT

– Adverse weather affecting a number of regions & starting to have significant effect on supply

– Floods in Queensland have major impact on coking & thermal coal supplies. The state supplies two thirds of the world’s coking coal and 8% of the world’s thermal coal

– Approximately 75% of Queensland mines are not operating because of flooding

– In 2008, flooding reduced coal production by roughly 8-10 million tonnes. The recent flood appears to be worse. Market slow to recognise the impact of unseasonal weather & price forecasts for coking coal fail to keep pace with deteriorating supply outlook

For illustrative purposes only and not a recommendation to buy or sell sharesSource: Datastream, USD, 31 December 2010, Australian Bureau of Meteorology (Comet Post Office Station)

Market slow to anticipate supply constraintsRainfall Accumulation (mm)

Rainfall Accumulation (mm) RHS

♦♦♦

♦

2011 consensus forecasts for Hard Coking Coal♦

Coking Coal Price in USD LHS

Current Coking Coal Price (Jan 2011)♦

15

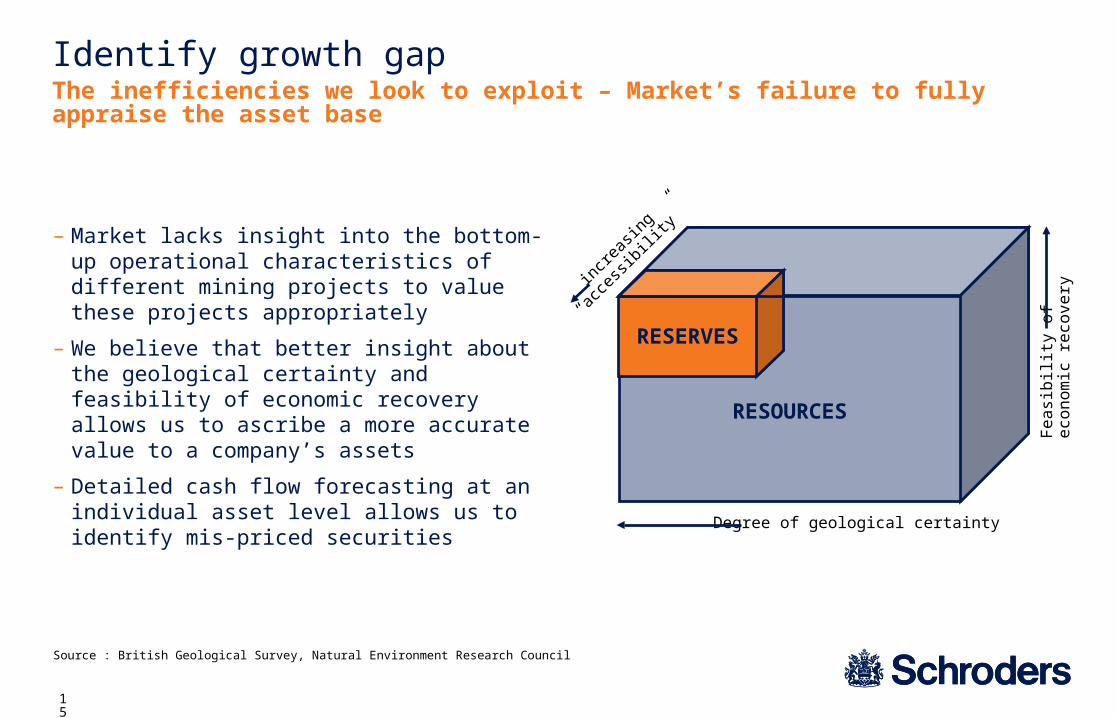

Identify growth gapThe inefficiencies we look to exploit – Market’s failure to fully appraise the asset base

– Market lacks insight into the bottom-up operational characteristics of different mining projects to value these projects appropriately

– We believe that better insight about the geological certainty and feasibility of economic recovery allows us to ascribe a more accurate value to a company’s assets

– Detailed cash flow forecasting at an individual asset level allows us to identify mis-priced securities

Source : British Geological Survey, Natural Environment Research Council

RESOURCES

RESERVES

Degree of geological certainty

Fe

asi

bili

ty o

f e

con

om

ic r

eco

very

incre

asing

“acc

essib

ility”

16

0

25

50

75

100

125

150

Dec-07

Apr-08

Aug-08

Dec-08

Apr-09

Aug-09

Dec-09

Apr-10

Aug-10

Dec-10

Apr-11

First Quantum Share Price

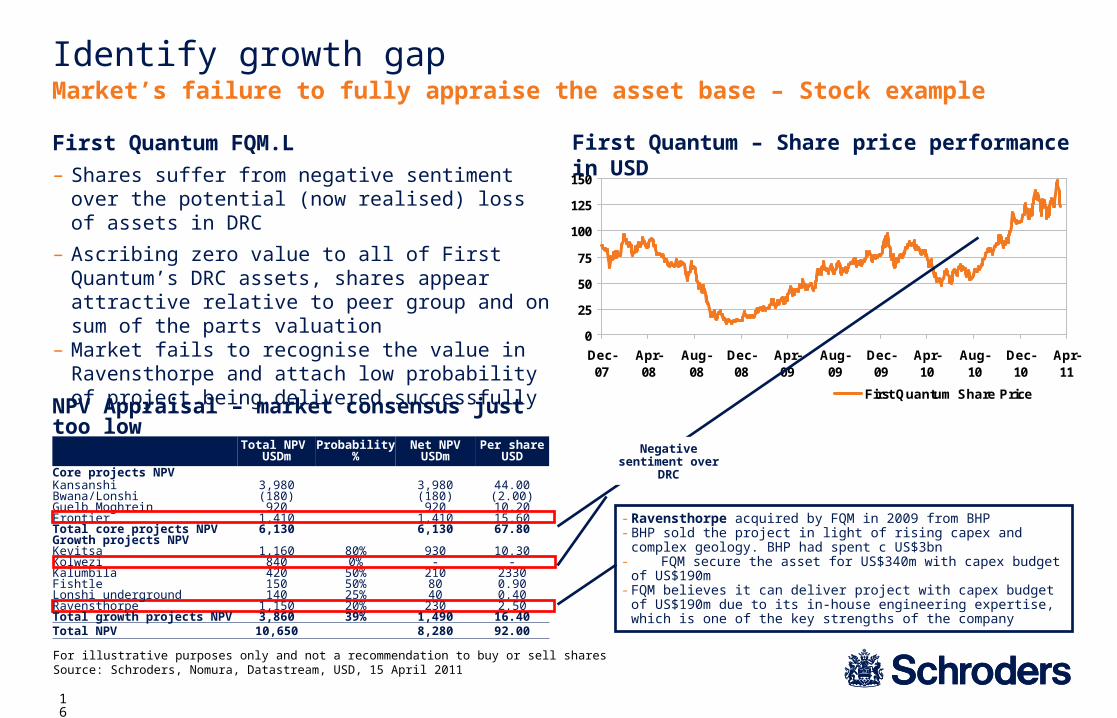

Identify growth gapMarket’s failure to fully appraise the asset base – Stock example

For illustrative purposes only and not a recommendation to buy or sell sharesSource: Schroders, Nomura, Datastream, USD, 15 April 2011

NPV Appraisal – market consensus just too low

Total NPV USDm Probability % Net NPV

USDmPer share

USDCore projects NPVKansanshi 3,980 3,980 44.00Bwana/Lonshi (180) (180) (2.00)Guelb Moghrein 920 920 10.20Frontier 1,410 1,410 15.60Total core projects NPV 6,130 6,130 67.80Growth projects NPVKevitsa 1,160 80% 930 10.30Kolwezi 840 0% - -Kalumbila 420 50% 210 2330Fishtle 150 50% 80 0.90Lonshi underground 140 25% 40 0.40Ravensthorpe 1,150 20% 230 2.50Total growth projects NPV 3,860 39% 1,490 16.40Total NPV 10,650 8,280 92.00

First Quantum – Share price performance in USDFirst Quantum FQM.L

– Shares suffer from negative sentiment over the potential (now realised) loss of assets in DRC

– Ascribing zero value to all of First Quantum’s DRC assets, shares appear attractive relative to peer group and on sum of the parts valuation

– Market fails to recognise the value in Ravensthorpe and attach low probability of project being delivered successfully

Negative sentiment over DRC

- Ravensthorpe acquired by FQM in 2009 from BHP- BHP sold the project in light of rising capex and complex geology. BHP

had spent c US$3bn - FQM secure the asset for US$340m with capex budget of US$190m- FQM believes it can deliver project with capex budget of US$190m due to

its in-house engineering expertise, which is one of the key strengths of the company

17

Global Resources – Near term outlookShort term positive – Waiting for the Chinese Rebound

Demand

– Underlying demand drivers remains robust. Data remains solid (i.e. PMI indices, IP)

– Strong restock in China expected Q2 2011. Significant destocking seen through 2010

– Commodity prices have remained at historically elevated levels (and in some cases record levels), despite mass Chinese destocking during 2010 and with anaemic demand in the developed world

– Western world (specifically US) recovery has been largely ex-construction based to date. Lead indicators suggest this might be turning

Supply

– Supply side will continue to disappoint. Supply disruption risk remains – there is limited flexibility in the supply chain

Valuation

– Sentiment has been very weak in recent months given caution over MENA activity and Chinese tightening activity

– We stick to the fundamentals. When sentiment turns, significant upside for many resources equities. We are well positioned

18

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2008 2009 2010

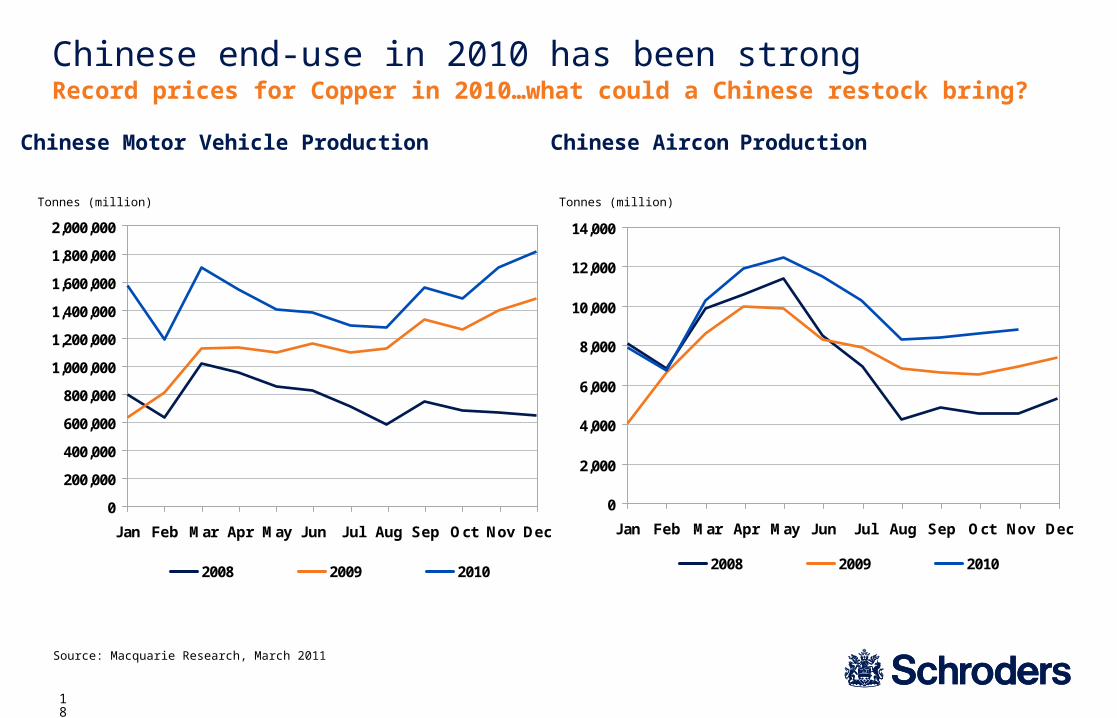

Chinese end-use in 2010 has been strong

Source: Macquarie Research, March 2011

Record prices for Copper in 2010…what could a Chinese restock bring?

Chinese Motor Vehicle Production

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2008 2009 2010

Chinese Aircon Production

Tonnes (million)Tonnes (million)

19

25.0

27.0

29.0

31.0

33.0

35.0

37.0

39.0

41.0

43.0

45.0

Sep-10 Sep-10 Oct-10 Oct-10 Oct-10 Nov-10 Nov-10 Dec-10 Dec-10 Jan-11 Jan-11 Feb-11 Feb-11 Mar-11

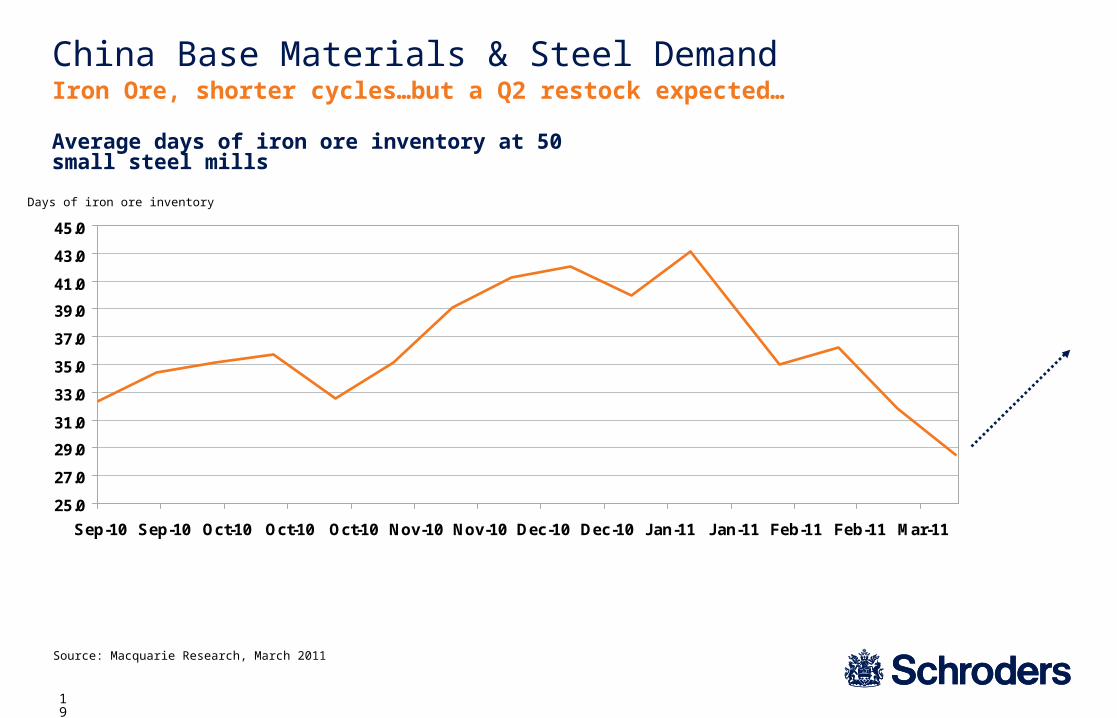

China Base Materials & Steel Demand

Source: Macquarie Research, March 2011

Iron Ore, shorter cycles…but a Q2 restock expected…

Days of iron ore inventory

Average days of iron ore inventory at 50 small steel mills

20

35

40

45

50

55

60

65

Nov-95 May-97 Nov-98 May-00 Nov-01 May-03 Nov-04 May-06 Nov-07 May-09 Nov-10

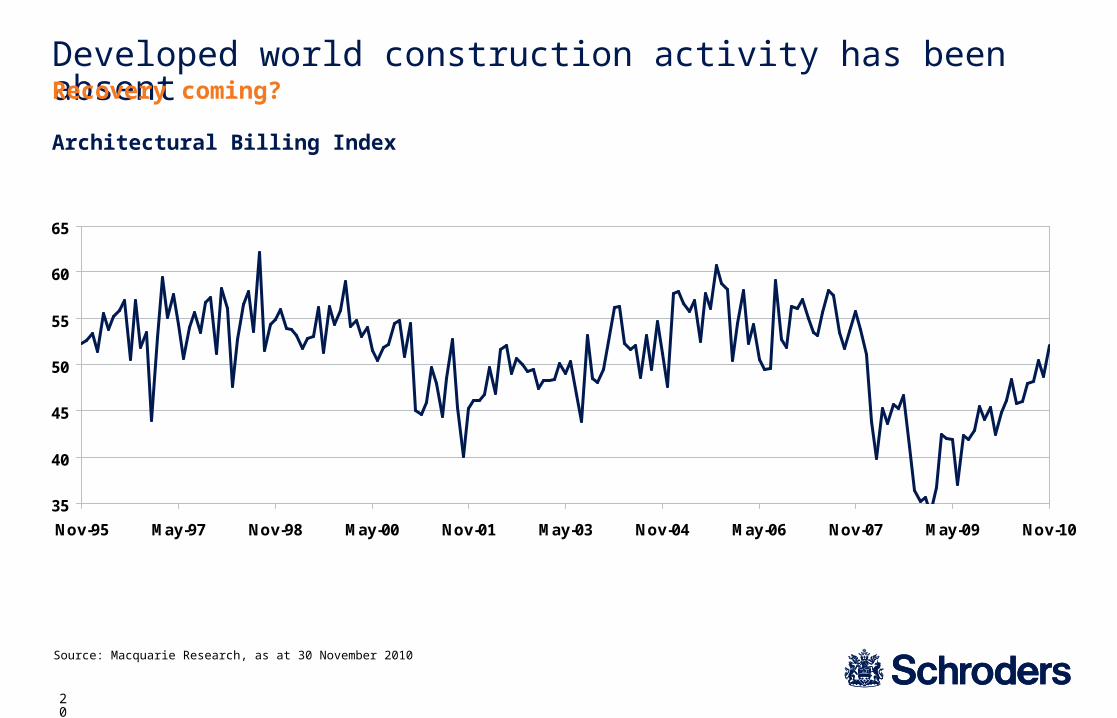

Developed world construction activity has been absent

Architectural Billing Index

Source: Macquarie Research, as at 30 November 2010

Recovery coming?

21

4

8

12

16

20

Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11

Mining 12m Fwd PE Average

Resources equity valuations attractiveUpside is material

Mining Sector Forward PE Multiples – a discounted sector

Source: Datastream

22

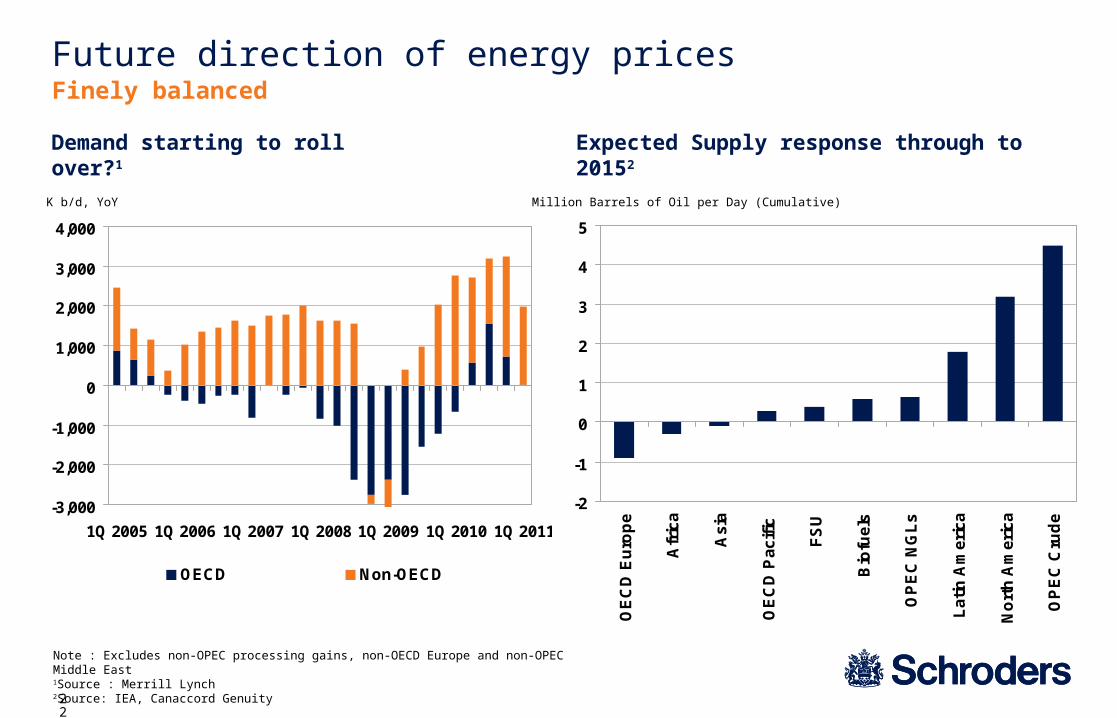

Future direction of energy pricesFinely balanced

Demand starting to roll over?1 Expected Supply response through to 20152

-2

-1

0

1

2

3

4

5

OE

CD

Eu

rop

e

Afr

ica

As

ia

OE

CD

Pa

cif

ic

FS

U

Bio

fue

ls

OP

EC

NG

Ls

La

tin

Am

eri

ca

No

rth

Am

eri

ca

OP

EC

Cru

de

Note : Excludes non-OPEC processing gains, non-OECD Europe and non-OPEC Middle East1Source : Merrill Lynch2Source: IEA, Canaccord Genuity

Million Barrels of Oil per Day (Cumulative)

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

1Q 2005 1Q 2006 1Q 2007 1Q 2008 1Q 2009 1Q 2010 1Q 2011

OECD Non-OECD

K b/d, YoY

23

25

30

35

40

45

50

55

Se

p-0

4

Se

p-0

5

Se

p-0

6

Se

p-0

7

Se

p-0

8

Se

p-0

9

Se

p-1

0

OPEC Supply Non-OPEC Supply

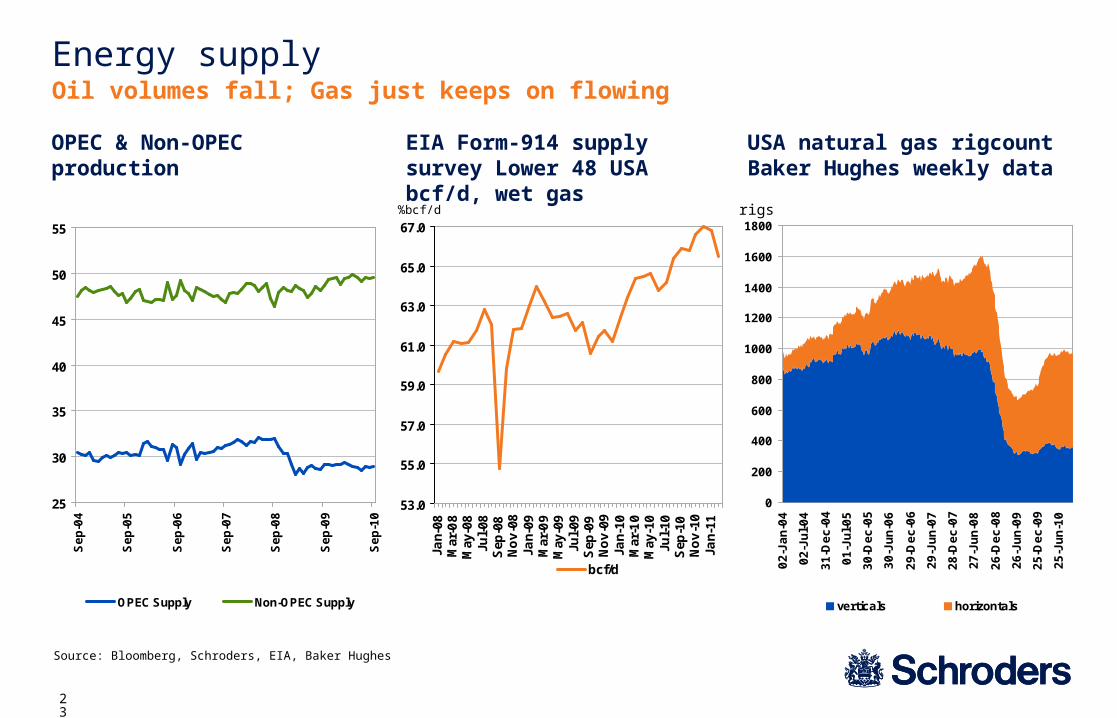

Oil volumes fall; Gas just keeps on flowing

Source: Bloomberg, Schroders, EIA, Baker Hughes

USA natural gas rigcountBaker Hughes weekly data

0

200

400

600

800

1000

1200

1400

1600

1800

02

-Ja

n-0

4

02

-Ju

l-0

4

31

-De

c-0

4

01

-Ju

l-0

5

30

-De

c-0

5

30

-Ju

n-0

6

29

-De

c-0

6

29

-Ju

n-0

7

28

-De

c-0

7

27

-Ju

n-0

8

26

-De

c-0

8

26

-Ju

n-0

9

25

-De

c-0

9

25

-Ju

n-1

0

verticals horizontals

rigs

OPEC & Non-OPEC production EIA Form-914 supply survey Lower 48 USA bcf/d, wet gas

53.0

55.0

57.0

59.0

61.0

63.0

65.0

67.0

Jan-

08M

ar-0

8M

ay-0

8Ju

l-08

Sep

-08

No

v-0

8Ja

n-09

Mar

-09

May

-09

Jul-

09S

ep-0

9N

ov

-09

Jan-

10M

ar-1

0M

ay-1

0Ju

l-10

Sep

-10

No

v-1

0Ja

n-11

bcf/d

%bcf/d

Energy supply

24

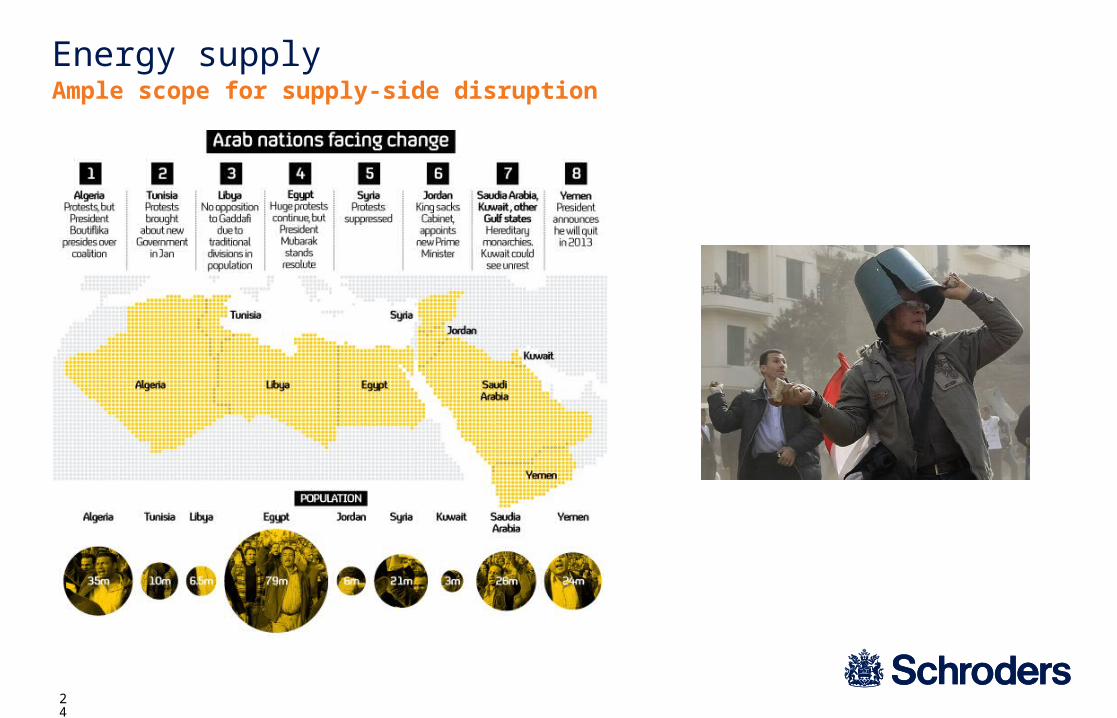

Energy supplyAmple scope for supply-side disruption

25

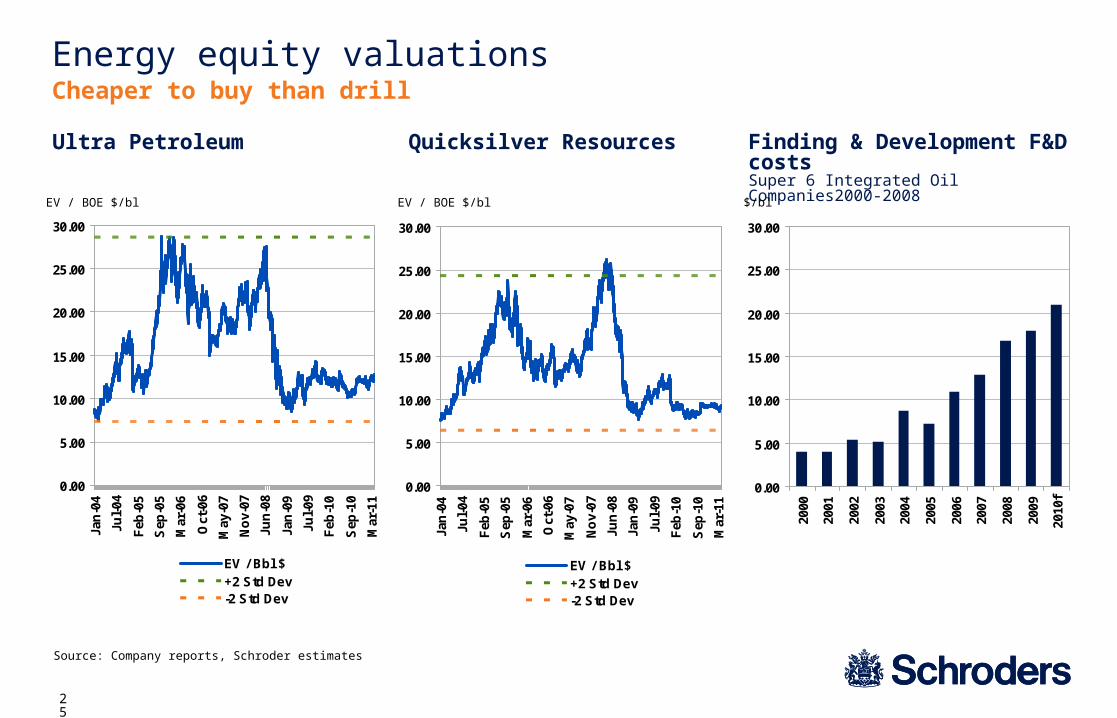

Energy equity valuationsCheaper to buy than drill

Finding & Development F&D costs Super 6 Integrated Oil Companies2000-2008$/bl

Ultra Petroleum

EV / BOE $/bl

Quicksilver Resources

EV / BOE $/bl

Source: Company reports, Schroder estimates

0.00

5.00

10.00

15.00

20.00

25.00

30.00

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

f

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Jan

-04

Jul-

04

Feb

-05

Sep

-05

Mar

-06

Oct

-06

May

-07

No

v-07

Jun

-08

Jan

-09

Jul-

09

Feb

-10

Sep

-10

Mar

-11

EV / Bbl $+2 Std Dev-2 Std Dev

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Jan

-04

Jul-

04

Feb

-05

Sep

-05

Mar

-06

Oct

-06

May

-07

No

v-07

Jun

-08

Jan

-09

Jul-

09

Feb

-10

Sep

-10

Mar

-11

EV / Bbl $+2 Std Dev-2 Std Dev

26

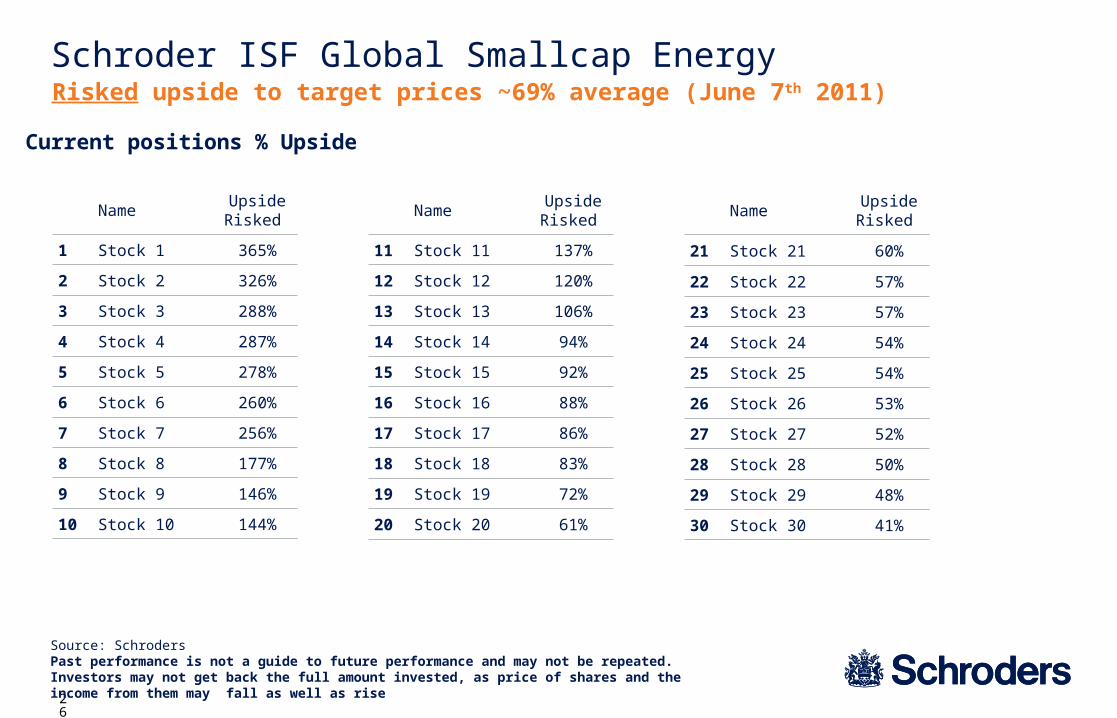

NameUpside Risked

1 Stock 1 365%

2 Stock 2 326%

3 Stock 3 288%

4 Stock 4 287%

5 Stock 5 278%

6 Stock 6 260%

7 Stock 7 256%

8 Stock 8 177%

9 Stock 9 146%

10 Stock 10 144%

Current positions % Upside

Schroder ISF Global Smallcap EnergyRisked upside to target prices ~69% average (June 7th 2011)

Source: SchrodersPast performance is not a guide to future performance and may not be repeated. Investors may not get back the full amount invested, as price of shares and the income from them may fall as well as rise

NameUpside Risked

11 Stock 11 137%

12 Stock 12 120%

13 Stock 13 106%

14 Stock 14 94%

15 Stock 15 92%

16 Stock 16 88%

17 Stock 17 86%

18 Stock 18 83%

19 Stock 19 72%

20 Stock 20 61%

NameUpside Risked

21 Stock 21 60%

22 Stock 22 57%

23 Stock 23 57%

24 Stock 24 54%

25 Stock 25 54%

26 Stock 26 53%

27 Stock 27 52%

28 Stock 28 50%

29 Stock 29 48%

30 Stock 30 41%

27

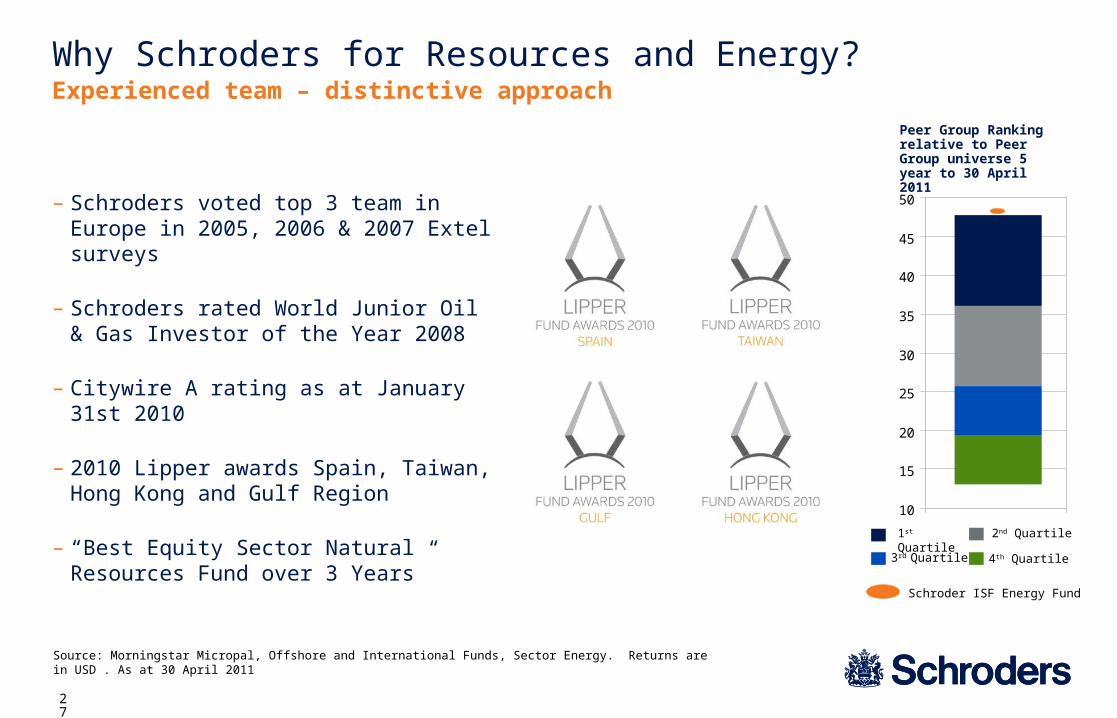

Why Schroders for Resources and Energy?

Source: Morningstar Micropal, Offshore and International Funds, Sector Energy. Returns are in USD . As at 30 April 2011

Experienced team – distinctive approach

1st Quartile 2nd Quartile

3rd Quartile 4th Quartile

Schroder ISF Energy Fund

– Schroders voted top 3 team in Europe in 2005, 2006 & 2007 Extel surveys

– Schroders rated World Junior Oil & Gas Investor of the Year 2008

– Citywire A rating as at January 31st 2010

– 2010 Lipper awards Spain, Taiwan, Hong Kong and Gulf Region

– “Best Equity Sector Natural Resources Fund over 3 Years” 10

15

20

25

30

35

40

45

50

Peer Group Ranking relative to Peer Group universe 5 year to 30 April 2011

28

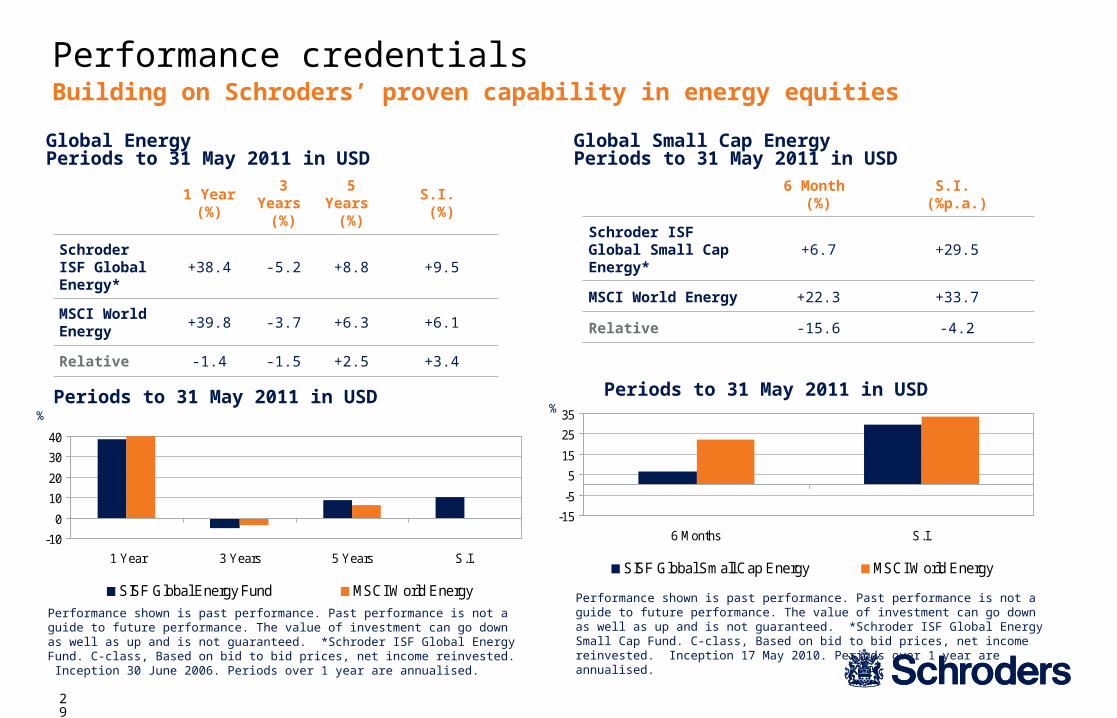

Performance credentialsBuilding on Schroders’ proven capability in commodities & energy equities

0

10

20

30

40

50

3 months 6 months Since Inception**

Schroder ISF Global Resources Equity Benchmark***

%

Global Resources EquitiesPeriods to 31 May 2011 in USD

3 Months(%)

6 Months (%)

Since Inception** (%)

Schroder ISF Global Resources Equity * +2.0 +17.4 +39.6

Benchmark*** +0.3 +16.3 +34.6

Relative +1.7 +1.1 +5.0

Performance shown is past performance. Past performance is not a guide to future performance. The value of investment can go down as well as up and is not guaranteed. *Schroder ISF Global Resources Equity Fund. Acc C-class, Based on bid to bid prices, net income reinvested. ** Inception 17 May 2010. ***MSCI AC World 35% Energy and 65% Materials. Fund is benchmark unconstrained and that the benchmark is shown for performance comparison.

Periods to 31 May 2011 in USD

29

Performance credentialsBuilding on Schroders’ proven capability in energy equities

-10

0

10

20

30

40

1 Year 3 Years 5 Years S.I.

SISF Global Energy Fund MSCI World Energy

%

Global EnergyPeriods to 31 May 2011 in USD

1 Year(%)

3 Years (%)

5 Years (%)

S.I. (%)

Schroder ISF Global Energy*

+38.4 -5.2 +8.8 +9.5

MSCI World Energy

+39.8 -3.7 +6.3 +6.1

Relative -1.4 -1.5 +2.5 +3.4

Performance shown is past performance. Past performance is not a guide to future performance. The value of investment can go down as well as up and is not guaranteed. *Schroder ISF Global Energy Fund. C-class, Based on bid to bid prices, net income reinvested. Inception 30 June 2006. Periods over 1 year are annualised.

Periods to 31 May 2011 in USD

-15

-5

5

15

25

35

6 Months S.I.

SISF Global Small Cap Energy MSCI World Energy

Global Small Cap EnergyPeriods to 31 May 2011 in USD

6 Month (%)

S.I. (%p.a.)

Schroder ISF Global Small Cap Energy*

+6.7 +29.5

MSCI World Energy +22.3 +33.7

Relative -15.6 -4.2

Performance shown is past performance. Past performance is not a guide to future performance. The value of investment can go down as well as up and is not guaranteed. *Schroder ISF Global Energy Small Cap Fund. C-class, Based on bid to bid prices, net income reinvested. Inception 17 May 2010. Periods over 1 year are annualised.

Periods to 31 May 2011 in USD%

30

Investing to maximise returnsConclusion

– Structural growth increases certainty of long term returns

– Resources are key beneficiaries of structural growth drivers

– Resource related equities are an attractive way to exploit the opportunities

– Strong argument for making a strategic allocation

31

Important information

Risk warning: Investments in equities are subject to market risk and, potentially, to currency exchange rate risk. This fund may use financial derivative instruments as a part of the investment process. This may increase the fund’s price volatility by amplifying market events.

Important Information: This presentation does not constitute an offer to anyone, or a solicitation by anyone, to subscribe for shares of Schroder International Selection Fund (the “Company”). Nothing in this presentation should be construed as advice and is therefore not a recommendation to buy or sell shares.

Subscriptions for shares of the Company can only be made on the basis of its latest prospectus together with the latest audited annual report (and subsequent unaudited semi-annual report, if published), copies of which can be obtained, free of charge, from Schroder Investment Management (Luxembourg) S.A.

An investment in the Company entails risks, which are fully described in the prospectus.

Past performance is not a reliable indicator of future results, prices of shares and the income from them may fall as well as rise and investors may not get the amount originally invested.

Third party data is owned or licensed by the data provider and may not be reproduced or extracted and used for any other purpose without the data provider's consent. Third party data is provided without any warranties of any kind. The data provider and issuer of the document shall have no liability in connection with the third party data. The Prospectus and/or www.schroders.com contains additional disclaimers which apply to the third party data.

This presentation is issued by Schroder Investment Management Limited, 31, Gresham Street, EC2V 7QA, who is authorised and regulated by the Financial Services Authority. For your security, all telephone calls are recorded.