Embed Size (px)

Citation preview

Journal of Multidisciplinary Studies Vol. 7, Issue No. 1, pp. 21-39, August 2018 ISSN 2350-7020 (Print) ISSN 2362-9436 (Online) doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

21

Resistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

Ringgold P. Atienza

College of Business and Management, Misamis University, Ozamiz City, Philippines

Corresponding author: Ringgold P. Atienza, email: [email protected]

Abstract Innovations, even the successful ones, face initial resistance from their users that hinders or slows down its adoption process. The mobile and internet banking innovation in the Philippines was not spared from this phenomenon. Initial resistance could become a barrier to adoption of this innovation. Since the innovation faces a widespread resistance among bank customers, concentrating on understanding the reasons for innovation resistance is helpful. This study used the innovation resistance framework that has five barriers namely: usage, value, risk, tradition and image barriers. This study explored the level of resistance to mobile and internet banking among bank clients in Ozamiz City. It also explored the significant effects of customer’s socio-economic profile to their resistance. This study employed the survey method using a questionnaire. Respondents were randomly selected from institutions and households in Ozamiz City. Mean, standard deviation, Pearson correlation, and t-test were the statistical tools used. Results showed that risk barrier was the strongest barrier while usage is the weakest barrier. This signifies that customers do not resist internet and mobile banking because they are not capable of using the platform but because they are afraid of any financial risks they might encounter when they are online. News concerning fraud on banking, whether using branch-based or mobile and internet banking increase the challenge for banks in the mainstreaming of this innovation. Banks must exert effort in communicating with their customers on the security issues of their platform to overcome the problem of resistance.

Keywords: barrier, customers, financial, mobile, risk

21

R. P. AtienzaResistance to Mobile and Internet Banking Innovation in Ozamiz City, PhilippinesJournal of Multidisciplinary StudiesVol. 7, Issue No. 1, pp. 21-39, August 2018ISSN 2350-7020 (Print)ISSN 2362-9436 (Online)doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

Resistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

R. P. Atienza

22

Introduction

In the Philippines, traditional branch-based banking remains the most widely adopted method of banking transaction (Medhi et al., 2009). In a traditional set-up, savers physically had to go to a bank branch to transfer, deposit or withdraw money in their account and get a bank statement over-the-counter. Cash dispensers and automated teller machines were introduced in late 60s to facilitate withdrawals, deposits and even payments or transfers accommodating mobility in much wider geographical areas. Afterwards, the introduction of tele-banking, phone-banking, and PC-banking paved the way to the revolutionary non-branched-based banking. Now, the recent innovation in banking technology is the use of mobile and internet banking (Chang, 2003; Consulting, 2008; Wilson & Goddard, 2016).

Mobile and internet banking using wireless technology provide customers with interactive retail banking transactions anytime, anywhere (Bamoriya & Singh, 2011). This banking innovation has enormous potential that immensely reduced the cost of transaction, increased the speed of service, improved the efficiency and productivity, and provided better customer satisfaction, convenience and flexibility (Lassar et al., 2005; Nasri & Charfeddine, 2012).

Mobile and internet banking can be characterized into two types of innovation, as a process innovation and as a product innovation. The new innovation has shifted from customer-to-bank teller process to customer-to-system process. The users can now handle their own banking without the need for human interaction at one end. Non-regular customers can also inquire with the banks via public websites. New products and services are also offered as mobile and internet banking proliferate. Through their websites, banks offer comprehensive personal financial management packages. For example, a package is tailor-made for each client combining commercial banking, investment in stockmarket, bondmarket, ETF, mutual funds, sales of insurance products and pension schemes (Chang, 2003).

The value-adding internet mobile services are important in gaining a competitive advantage among banks (Wang et al., 2006).

22

Journal of Multidisciplinary StudiesVol. 7, Issue No. 1, pp. 21-39, August 2018ISSN 2350-7020 (Print)ISSN 2362-9436 (Online)doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

Journal of Multidisciplinary Studies Vol. 7, Issue No. 1, pp. 21-39, August 2018 ISSN 2350-7020 (Print) ISSN 2362-9436 (Online) doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

23

Mobile banking represents an additional service for certain occasions adding the element of true mobility to internet banking. For example, customers find mobile banking valuable when being out of town, on the road, or in case of acute need for money transfer (Laukkanen & Louronen, 2005).

Banks are putting great efforts to take advantage of the business opportunities offered by wireless technology but still users resist innovations even though this innovation is necessary and desirable (Yu, 2012). Savers are still reluctant to adopt the innovation (Bradley & Stewart, 2002). This resistance to innovation is manifested by customers through postponement, opposition or rejection in the use of the system (Kleijnen et al., 2009). Resistance occurs even in case of successful innovation and before the adoption may begin, the initial resistance must first be overcome (Ram, 1987).

The resistance to innovation among consumers is one of the major causes of product or service failures faced by the organizations (Ram & Sheth, 1989). Since the vast majority of consumers do not have a priori desire to change, we could learn more by concentrating on understanding the reasons for innovation resistance rather than on the reasons for adoption. Thus, the interest in studying consumer resistance to innovations is to identify the reasons that prevent consumers from adopting an innovation (Laukkanen et al., 2007).

Resistance grew from the user’s habit or satisfaction with an existing behavior, and the perceived risk associated with the new system (Sheth, 1981). Satisfaction with the performance of the current system increases resistance to alternatives and reduces the likelihood of adoption. Perceived risks are derived from physical, social or economic consequences, performance uncertainty, and perceived side effects of innovation. The perceived self-efficacy or the ability to successfully perform to new system, has also an important role in the barriers in consumer resistance to technological innovations (Agarwal et al., 2000). Providing a more comprehensive view to this phenomenon, Ram and Sheth’s Innovation Resistance Theory indicated that the reason users resist innovation is because of the obstacles produced by change, and conflicts brought by innovation. These five obstacles or barriers are the

23

R. P. AtienzaResistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

Resistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

R. P. Atienza

24

usage barrier, value barrier, risk barrier, tradition barrier, and image barrier (Ram & Sheth, 1989).

Usage barrier comes into operation when an innovation is not well-suited to existing workflows, practices or habits. In case of technology-intensive services, the usage barrier could be connected to the usability of the service and the changes it requires from the customers (Laukkanen et al., 2007). It is the ease of use which an individual considers in an innovation to be free of effort (Davis, 1989).

Value barrier is derived from the performance and monetary value of an innovation in comparison to its substitute (Rogers, 2010). The greater the perceived advantage that mobile and internet banking offers over other ways of banking, the more likely mobile and internet banking is to be adopted (Brown et al., 2003). One such advantage is the option to check the transactions of an account wherever wanted, increasing customer’s feeling of control over financial affairs. However, if an innovation does not offer superior performance to existing alternatives, it is not worthwhile for customers to change their behavior. For example, in a study done by Luarn and Lin (2005), financial cost considerations showed to have a negative effect on the intention to use mobile and internet banking.

Risk barrier refers to the degree of risk inherent in an innovation. Initially, perceived risk was primarily related to fraud or product quality. Today, as people have engaged in online behavior, perceived risk is largely related to financial, psychological, physical, or social risks in online transaction (Forsythe & Shi, 2003). In mobile and internet banking, the personal and banking data input and output mechanisms may hinder the confidence of clients to use such system as they are afraid of having their information exposed somewhere else. Information hacking also posed a problem and it showed that perceived web security is also a significant and direct determinant of customer’s intention. Without a proper knowledge of the system, individuals are not interested to test the system (Amin, 2007). Moreover, mobile phones may be limited in computational power, memory capacity, and battery life, limiting the use of mobile services (Siau & Shen, 2003). Self-efficacy is also important since customers who are not so

24

Journal of Multidisciplinary StudiesVol. 7, Issue No. 1, pp. 21-39, August 2018ISSN 2350-7020 (Print)ISSN 2362-9436 (Online)doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

Journal of Multidisciplinary Studies Vol. 7, Issue No. 1, pp. 21-39, August 2018 ISSN 2350-7020 (Print) ISSN 2362-9436 (Online) doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

25

knowledgeable in the system may be anxious to make mistakes. Evidence of the relationship between self-efficacy and using a computer can be found in the study of Martocchio and Webster (1992).

Traditional barrier takes place when an innovation is incompatible with an individual’s existing values, norms and past experiences. The traits of the consumers are related to a broader discussion about technology readiness. Some consumers may indeed feel uncomfortable when faced with self-service technologies, resulting in frustration with technology-based systems (Parasuraman, 2000). Some cases fall into the category of technophobia (Meuter et al., 2003). In the banking context the tradition barrier may arise if an individual perceives mobile and online banking to be very different from the way one has been accustomed to in paying bills (Fain & Roberts, 1997). A strong desire to deal with human tellers may also discourage an individual from adopting self-service technologies (Marr & Prendergast, 1993). The preference for human tellers may be derived from a need for social interaction and chat with bank personnel (Heinonen, 2004). It may be that in mobile banking the tradition barrier takes place if consumers simply prefer to deal directly with the bank clerk instead of using new banking technologies. Information technology poses both opportunities and challenges. Even with Automated Teller Machines and Internet Banking, many consumers still prefer the personal touch of their neighborhood branch bank (Gopinath, 2005).

Image barrier arises when an innovation is associated with something that has formed negative image to the users. It could be the innovation’s identity as to its origin in product category where it belongs, the geographical and ethnical origin, or the company that created such innovation. If an individual dislikes such association of the innovation, a negative image will develop and so create a barrier to adoption. The image barrier of internet and mobile banking can be linked to the different types of anxiety towards computers or technology itself, referring to a consumer’s negative state of mind about technology tools (Meuter et al., 2003). It could also be the bad news about this technology a customer had heard from a verified or even an unverified source. In this case having a negative perception on

25

R. P. AtienzaResistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

Resistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

R. P. Atienza

26

technology such as internet and mobile banking instantly forms a barrier of the services relating to technology.

While the internet and mobile banking patronage in most Southeast Asian nations have been increasing rapidly, the Philippines showed a sluggish growth a decade ago (Sala-i-Martin et al., 2007). Recently, the Philippines has the fastest growing market for smartphones and leading users in internet, mobile, and social media among ASEAN countries (Igna, 2015; Medenilla, 2016), a status that should position the country to become potential users for this new innovation. Advanced and developing countries have been studying issues and challenges in the adoption and resistance of mobile and internet banking (AbuShanab et al., 2010; Alsajjan & Dennis, 2010; Hasan et al., 2010; Mbiti & Weil, 2011; Bamoriya & Singh, 2011; Foon & Fah, 2011; Kesharwani & Bisht, 2012; Maduku & Mpinganjira, 2012; Hanafizadeh & Khedmatgozar, 2012; Fox, 2013). Hence, an understanding to consumer behavior, specifically in Philippines where adoption is relatively low, is the baseline in increasing adoption of this innovation.

Specifically, the study is conducted in Ozamiz City, Philippines. The city is regarded as the center of commerce, health, transportation and education in Misamis Occidental province. Its financial industry is booming as evidenced by the existence of more than 25 financial institutions of different types, ranging from commercial banks to cooperatives (Atienza, 2014). However, based on casual conversations, a considerable number of people living in the area have expressed resistance to mobile and internet banking because of the risks they might encounter with the innovation. This study aimed to examine level of resistance to mobile and internet banking in Ozamiz City using the innovation resistance model of Ram and Sheth (1989).

Materials and Methods

The study employed the survey method in which the questionnaire was developed from the study of Laukkanen et al. (2008). It includes the six-point likert scale statements of the five barriers namely usage, value, risk, tradition and image barriers.

26

Journal of Multidisciplinary StudiesVol. 7, Issue No. 1, pp. 21-39, August 2018ISSN 2350-7020 (Print)ISSN 2362-9436 (Online)doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

Journal of Multidisciplinary Studies Vol. 7, Issue No. 1, pp. 21-39, August 2018 ISSN 2350-7020 (Print) ISSN 2362-9436 (Online) doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

27

The interpretation of the scale is as follows: 1.00–1.83, weak barrier; 1.84–2.67, moderately weak barrier; 2.68–3.51, slightly weak barrier; 3.52–4.35, slightly strong barrier; 4.36–5.15, moderately strong barrier; 5.16–6.00, strong barrier.

A reliability analysis using Cronbach’s alpha was run on a sample size of 50 to measure the internal consistency of the items in measuring the five barriers. The results showed strong internal consistency thus the questionnaire was highly reliable on all measures; 0.935, 0.810, 0.925, 0.875, 0.815, on usage, value, risk, tradition and image barrier, respectively. Survey questionnaires were personally distributed to the different institutions and households in Ozamiz City, Philippines. Selection of respondents was based on prior knowledge that they have been employed and regularly receiving their salary with active bank accounts. Respondents were asked first whether they casually do banking transaction using traditional branch-based banking and had not preferred or used mobile and internet banking. The informed consent was sought right after. The respondents were then shown the platform of one of the internet banking apps for them to assess the innovation. A total of 212 questionnaires, comprising of 84.8% of those distributed, were retrieved and analyzed. Descriptive statistics such as mean and standard deviation were used to determine the barrier levels of the users. Pearson correlation was also tested for the barriers, age, and monthly income. The independent sample t-test was used to test the mean difference of gender in terms of their perceived level of barriers on innovation. The R programming was used in data analysis (R Core Team, 2013), and Tableau Public 10.1 was used for data visualization. Results and Discussion

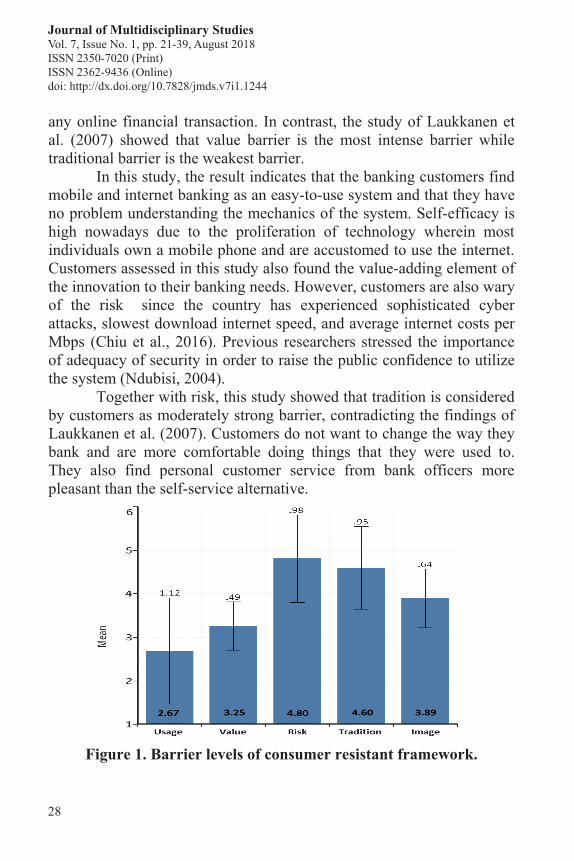

Figure 1 shows risk as the strongest among the five barriers and usage as the weakest barrier although it has the highest standard deviation of 1.12. The study of Tan and Teo (2000) also found risk barrier to be a very high significant factor. Lim et al. (2016) stated that value, risk, and image were barriers to non-user’s intentions to engage in

27

R. P. AtienzaResistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

Resistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

R. P. Atienza

28

any online financial transaction. In contrast, the study of Laukkanen et al. (2007) showed that value barrier is the most intense barrier while traditional barrier is the weakest barrier.

In this study, the result indicates that the banking customers find mobile and internet banking as an easy-to-use system and that they have no problem understanding the mechanics of the system. Self-efficacy is high nowadays due to the proliferation of technology wherein most individuals own a mobile phone and are accustomed to use the internet. Customers assessed in this study also found the value-adding element of the innovation to their banking needs. However, customers are also wary of the risk since the country has experienced sophisticated cyber attacks, slowest download internet speed, and average internet costs per Mbps (Chiu et al., 2016). Previous researchers stressed the importance of adequacy of security in order to raise the public confidence to utilize the system (Ndubisi, 2004).

Together with risk, this study showed that tradition is considered by customers as moderately strong barrier, contradicting the findings of Laukkanen et al. (2007). Customers do not want to change the way they bank and are more comfortable doing things that they were used to. They also find personal customer service from bank officers more pleasant than the self-service alternative.

Figure 1. Barrier levels of consumer resistant framework.

28

Journal of Multidisciplinary StudiesVol. 7, Issue No. 1, pp. 21-39, August 2018ISSN 2350-7020 (Print)ISSN 2362-9436 (Online)doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

Journal of Multidisciplinary Studies Vol. 7, Issue No. 1, pp. 21-39, August 2018 ISSN 2350-7020 (Print) ISSN 2362-9436 (Online) doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

29

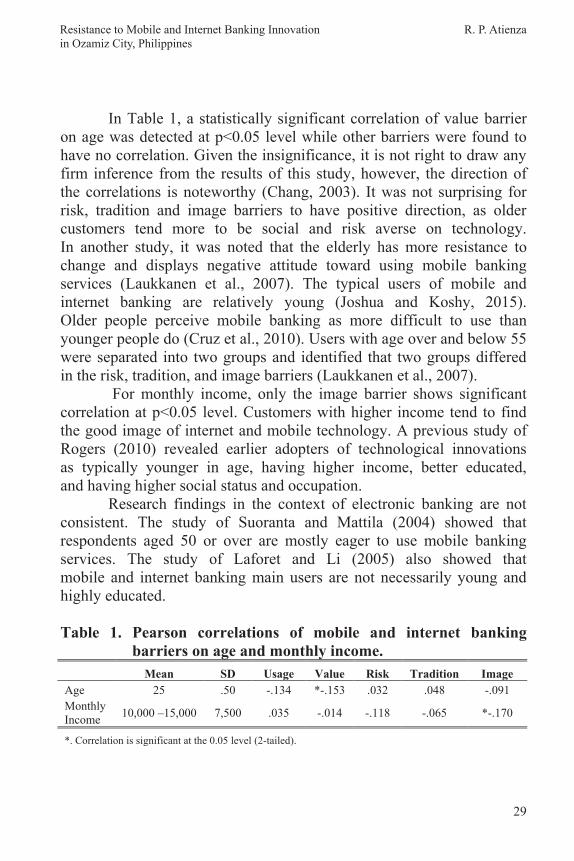

In Table 1, a statistically significant correlation of value barrier on age was detected at p<0.05 level while other barriers were found to have no correlation. Given the insignificance, it is not right to draw any firm inference from the results of this study, however, the direction of the correlations is noteworthy (Chang, 2003). It was not surprising for risk, tradition and image barriers to have positive direction, as older customers tend more to be social and risk averse on technology. In another study, it was noted that the elderly has more resistance to change and displays negative attitude toward using mobile banking services (Laukkanen et al., 2007). The typical users of mobile and internet banking are relatively young (Joshua and Koshy, 2015). Older people perceive mobile banking as more difficult to use than younger people do (Cruz et al., 2010). Users with age over and below 55 were separated into two groups and identified that two groups differed in the risk, tradition, and image barriers (Laukkanen et al., 2007).

For monthly income, only the image barrier shows significant correlation at p<0.05 level. Customers with higher income tend to find the good image of internet and mobile technology. A previous study of Rogers (2010) revealed earlier adopters of technological innovations as typically younger in age, having higher income, better educated, and having higher social status and occupation.

Research findings in the context of electronic banking are not consistent. The study of Suoranta and Mattila (2004) showed that respondents aged 50 or over are mostly eager to use mobile banking services. The study of Laforet and Li (2005) also showed that mobile and internet banking main users are not necessarily young and highly educated.

Table 1. Pearson correlations of mobile and internet banking

barriers on age and monthly income. Mean SD Usage Value Risk Tradition Image Age 25 .50 -.134 *-.153 .032 .048 -.091 Monthly Income 10,000 –15,000 7,500 .035 -.014 -.118 -.065 *-.170

*. Correlation is significant at the 0.05 level (2-tailed).

29

R. P. AtienzaResistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

Resistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

R. P. Atienza

30

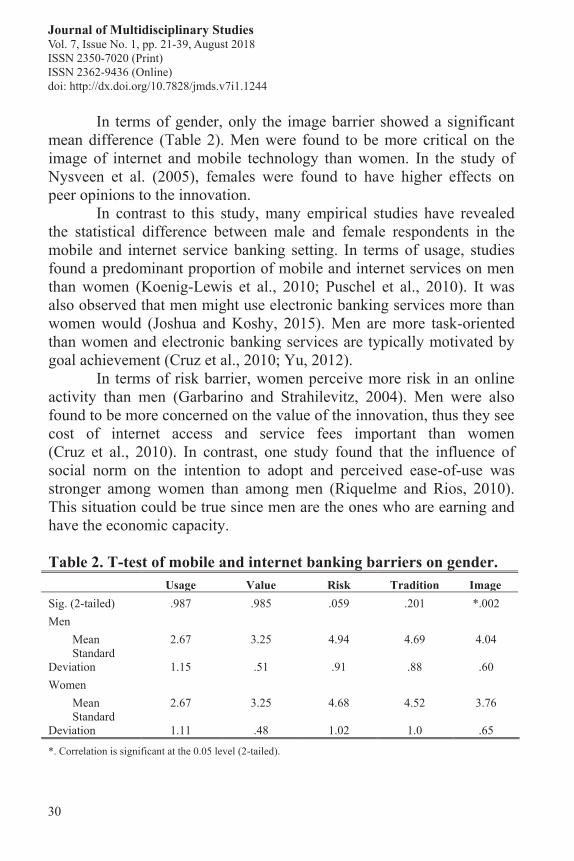

In terms of gender, only the image barrier showed a significant mean difference (Table 2). Men were found to be more critical on the image of internet and mobile technology than women. In the study of Nysveen et al. (2005), females were found to have higher effects on peer opinions to the innovation.

In contrast to this study, many empirical studies have revealed the statistical difference between male and female respondents in the mobile and internet service banking setting. In terms of usage, studies found a predominant proportion of mobile and internet services on men than women (Koenig-Lewis et al., 2010; Puschel et al., 2010). It was also observed that men might use electronic banking services more than women would (Joshua and Koshy, 2015). Men are more task-oriented than women and electronic banking services are typically motivated by goal achievement (Cruz et al., 2010; Yu, 2012).

In terms of risk barrier, women perceive more risk in an online activity than men (Garbarino and Strahilevitz, 2004). Men were also found to be more concerned on the value of the innovation, thus they see cost of internet access and service fees important than women (Cruz et al., 2010). In contrast, one study found that the influence of social norm on the intention to adopt and perceived ease-of-use was stronger among women than among men (Riquelme and Rios, 2010). This situation could be true since men are the ones who are earning and have the economic capacity.

Table 2. T-test of mobile and internet banking barriers on gender. Usage Value Risk Tradition Image Sig. (2-tailed) .987 .985 .059 .201 *.002 Men Mean 2.67 3.25 4.94 4.69 4.04 Standard Deviation 1.15 .51 .91 .88 .60 Women Mean 2.67 3.25 4.68 4.52 3.76 Standard Deviation 1.11 .48 1.02 1.0 .65

*. Correlation is significant at the 0.05 level (2-tailed).

30

Journal of Multidisciplinary StudiesVol. 7, Issue No. 1, pp. 21-39, August 2018ISSN 2350-7020 (Print)ISSN 2362-9436 (Online)doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

Journal of Multidisciplinary Studies Vol. 7, Issue No. 1, pp. 21-39, August 2018 ISSN 2350-7020 (Print) ISSN 2362-9436 (Online) doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

31

Almost all of the barriers in the framework, except image on usage and image on value, have significant correlation at P>0.01 level (Table 3). This shows high validity of the Ram and Sheth’s (1989) innovation resistance framework and was developed further by Laukkanen et al. (2008) into the resistance of using mobile and internet banking. Table 3. Pearson correlations of mobile and internet banking

barriers. Usage Value Risk Tradition Image Usage Value **.652 Risk **-.456 **-.312 Tradition **-.409 **-.281 **.745 Image .063 .083 **.451 **.462 **. Correlation is significant at the 0.01 level (2-tailed).

Conclusions and Recommendations Among the five barriers to the adoption of the internet and mobile banking, risk barrier shows to be the strongest while usage barrier is the weakest. This signifies that customers do not resist internet and mobile banking because they are not capable of using the platform but because they are afraid of any financial risks they might encounter when they are online. News in the Philippines concerning fraud on banking, whether using branch-based or mobile and internet banking appeared every now and then. This makes customers to be more risk-averse in every transaction they conduct, especially in the matters of money. To overcome the problem of resistance, banks must exert effort in communicating with their customers on the secureness of their platform. It is also important to take into consideration the socio-demographic profile of the customers in determining their target audiences. For example, the age is relevant in value barrier and monthly income on image barrier. There is also gender difference when it comes to image barrier, where banks may intensify awareness among men the image of mobile and internet banking.

31

R. P. AtienzaResistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

Resistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

R. P. Atienza

32

Acknowledgment

The author is thankful to Juvet A. Mahumok and Kimberly Saloritos for their assistance in all phases of this research.

Literature Cited

AbuShanab, E., Pearson, J. M., & Setterstrom, A. J. (2010). Internet banking and customers’ acceptance in Jordan: The unified model’s perspective. Communications of the Association for Information Systems, 26(1), 23.

Agarwal, R., Sambamurthy, V., & Stair, R. M. (2000). Research report:

The evolving relationship between general and specific computer self-efficacy—An empirical assessment. Information Systems Research, 11(4), 418-430. doi: 10.1287/isre.11.4.418.11876

Alsajjan, B., & Dennis, C. (2010). Internet banking acceptance model:

Cross-market examination. Journal of Business Research, 63(9), 957-963.

Amin, H. (2007). Internet banking adoption among young

intellectuals. Journal of Internet Banking and Commerce, 12(3), 1.

Atienza, R. P. (2014). Credit card usage pattern in Ozamiz City,

Philippines. Journal of Multidisciplinary Studies, 3(1), 60-85. doi: http://dx.doi.org/10.7828/jmds.v3i1.626.

Bamoriya, P. S., & Singh, P. (2011). Issues & challenges in mobile

banking in India: A customers’ perspective. Research Journal of Finance and Accounting, 2(2), 112-120.

Bradley, L., & Stewart, K. (2002). A Delphi study of the drivers and

inhibitors of Internet banking. International Journal of Bank Marketing, 20(6), 250-260. doi: 10.1108/02652320210446715

Journal of Multidisciplinary Studies Vol. 7, Issue No. 1, pp. 21-39, August 2018 ISSN 2350-7020 (Print) ISSN 2362-9436 (Online) doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

33

Brown, I., Cajee, Z., Davies, D., & Stroebel, S. (2003). Cell phone banking: Predictors of adoption in South Africa—An exploratory study. International Journal of Information Management, 23(5), 381-394.

Chang, Y. T. (2003). Dynamics of banking technology adoption:

An application to Internet banking (No. 2068-2018-1398). Chiu, C. L., Chiu, J. L., & Mansumitrchai, S. (2016). Privacy, security,

infrastructure and cost issues in internet banking in the Philippines: Initial trust formation. International Journal of Financial Services Management, 8(3), 240-271.

Consulting, G. (2008). Using technology to engage retail banking

customers. Why banks must carefully manage their digital touchpoints to create a seamless customer experience.

Cruz, P., Barretto Filgueiras Neto, L., Muñoz-Gallego, P., & Laukkanen,

T. (2010). Mobile banking rollout in emerging markets: Evidence from Brazil. International Journal of Bank Marketing, 28(5), 342-371.

Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and

user acceptance of information technology. MIS quarterly, 319-340.

Fain, D., & Roberts, M. L. (1997). Technology vs. consumer behavior:

The battle for the financial services customer. Journal of Interactive Marketing, 11(1), 44-54.

Foon, Y. S., & Fah, B. C. Y. (2011). Internet banking adoption in Kuala

Lumpur: An application of UTAUT model. International Journal of Business and Management, 6(4), 161-167.

32

Journal of Multidisciplinary StudiesVol. 7, Issue No. 1, pp. 21-39, August 2018ISSN 2350-7020 (Print)ISSN 2362-9436 (Online)doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

Journal of Multidisciplinary Studies Vol. 7, Issue No. 1, pp. 21-39, August 2018 ISSN 2350-7020 (Print) ISSN 2362-9436 (Online) doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

33

Brown, I., Cajee, Z., Davies, D., & Stroebel, S. (2003). Cell phone banking: Predictors of adoption in South Africa—An exploratory study. International Journal of Information Management, 23(5), 381-394.

Chang, Y. T. (2003). Dynamics of banking technology adoption:

An application to Internet banking (No. 2068-2018-1398). Chiu, C. L., Chiu, J. L., & Mansumitrchai, S. (2016). Privacy, security,

infrastructure and cost issues in internet banking in the Philippines: Initial trust formation. International Journal of Financial Services Management, 8(3), 240-271.

Consulting, G. (2008). Using technology to engage retail banking

customers. Why banks must carefully manage their digital touchpoints to create a seamless customer experience.

Cruz, P., Barretto Filgueiras Neto, L., Muñoz-Gallego, P., & Laukkanen,

T. (2010). Mobile banking rollout in emerging markets: Evidence from Brazil. International Journal of Bank Marketing, 28(5), 342-371.

Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and

user acceptance of information technology. MIS quarterly, 319-340.

Fain, D., & Roberts, M. L. (1997). Technology vs. consumer behavior:

The battle for the financial services customer. Journal of Interactive Marketing, 11(1), 44-54.

Foon, Y. S., & Fah, B. C. Y. (2011). Internet banking adoption in Kuala

Lumpur: An application of UTAUT model. International Journal of Business and Management, 6(4), 161-167.

33

R. P. AtienzaResistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

Resistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

R. P. Atienza

34

Forsythe, S. M., & Shi, B. (2003). Consumer patronage and risk perceptions in Internet shopping. Journal of Business Research, 56(11), 867-875.

Fox, S. (2013). 51% of US adults bank online. Pew Research Internet

Project. Retrieved from http://www.pewinternet.org/files/old-media/Files/Reports/2013/PIP_OnlineBanking.pdf

Garbarino, E., & Strahilevitz, M. (2004). Gender differences in the

perceived risk of buying online and the effects of receiving a site recommendation. Journal of Business Research, 57(7), 768-775.

Gopinath, S. (2005). Retail banking-opportunities and challenges. RBI

Bulletin, 59(6), 591-595. Retrieved at: https://www.rbi.org.in/ Upload/Speeches/Pdfs/63378.pdf

Hanafizadeh, P., & Khedmatgozar, H. R. (2012). The mediating role of

the dimensions of the perceived risk in the effect of customers’ awareness on the adoption of Internet banking in Iran. Electronic Commerce Research, 12(2), 151-175.

Hasan, A. S., Baten, M. A., Kamil, A. A., & Parveen, S. (2010).

Adoption of e-banking in Bangladesh: An exploratory study. African Journal of Business Management, 4(13), 2718.

Heinonen, K. (2004). Reconceptualizing customer perceived value:

The value of time and place. Managing Service Quality: An International Journal, 14(2/3), 205-215.

Igna, H. (2015). Internet, social media and mobile use of Filipinos

in 2015. National Teleheatlth Center. Retrieved from https://telehealth.ph/2015/03/26/internet-social-media-and-mobile-use-of-filipinos-in-2015/

Journal of Multidisciplinary Studies Vol. 7, Issue No. 1, pp. 21-39, August 2018 ISSN 2350-7020 (Print) ISSN 2362-9436 (Online) doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

35

Joshua, A. J., & Koshy, M. P. (2015). Usage patterns of electronic banking services by urban educated customers: Glimpses from India. The Journal of Internet Banking and Commerce, 2011.

Kesharwani, A., & Singh Bisht, S. (2012). The impact of trust and

perceived risk on internet banking adoption in India: An extension of technology acceptance model. International Journal of Bank Marketing, 30(4), 303-322.

Kleijnen, M., Lee, N., & Wetzels, M. (2009). An exploration of

consumer resistance to innovation and its antecedents. Journal of Economic Psychology, 30(3), 344-357.

Koenig-Lewis, N., Palmer, A., & Moll, A. (2010). Predicting young

consumers’ take up of mobile banking services. International Journal of Bank Marketing, 28(5), 410-432.

Laforet, S., & Li, X. (2005). Consumers’ attitudes towards online and

mobile banking in China. International Journal of Bank Marketing, 23(5), 362-380.

Lassar, W. M., Manolis, C., & Lassar, S. S. (2005). The relationship

between consumer innovativeness, personal characteristics, and online banking adoption. International Journal of Bank Marketing, 23(2), 176-199.

Laukkanen, P., Sinkkonen, S., & Laukkanen, T. (2008). Consumer

resistance to internet banking: Postponers, opponents and rejectors. International Journal of Bank Marketing, 26(6), 440-455.

Laukkanen, T., & Lauronen, J. (2005). Consumer value creation in mobile banking services. International Journal of Mobile Communications, 3(4), 325-338.

34

Journal of Multidisciplinary StudiesVol. 7, Issue No. 1, pp. 21-39, August 2018ISSN 2350-7020 (Print)ISSN 2362-9436 (Online)doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

Journal of Multidisciplinary Studies Vol. 7, Issue No. 1, pp. 21-39, August 2018 ISSN 2350-7020 (Print) ISSN 2362-9436 (Online) doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

35

Joshua, A. J., & Koshy, M. P. (2015). Usage patterns of electronic banking services by urban educated customers: Glimpses from India. The Journal of Internet Banking and Commerce, 2011.

Kesharwani, A., & Singh Bisht, S. (2012). The impact of trust and

perceived risk on internet banking adoption in India: An extension of technology acceptance model. International Journal of Bank Marketing, 30(4), 303-322.

Kleijnen, M., Lee, N., & Wetzels, M. (2009). An exploration of

consumer resistance to innovation and its antecedents. Journal of Economic Psychology, 30(3), 344-357.

Koenig-Lewis, N., Palmer, A., & Moll, A. (2010). Predicting young

consumers’ take up of mobile banking services. International Journal of Bank Marketing, 28(5), 410-432.

Laforet, S., & Li, X. (2005). Consumers’ attitudes towards online and

mobile banking in China. International Journal of Bank Marketing, 23(5), 362-380.

Lassar, W. M., Manolis, C., & Lassar, S. S. (2005). The relationship

between consumer innovativeness, personal characteristics, and online banking adoption. International Journal of Bank Marketing, 23(2), 176-199.

Laukkanen, P., Sinkkonen, S., & Laukkanen, T. (2008). Consumer

resistance to internet banking: Postponers, opponents and rejectors. International Journal of Bank Marketing, 26(6), 440-455.

Laukkanen, T., & Lauronen, J. (2005). Consumer value creation in mobile banking services. International Journal of Mobile Communications, 3(4), 325-338.

35

R. P. AtienzaResistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

Resistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

R. P. Atienza

36

Laukkanen, T., Sinkkonen, S., & Laukkanen, P. (2007, December). Information as a barrier to innovation adoption. In Proceedings of ANZMAC (Australian and New Zealand Marketing Academy) Conference, Dunedin, New Zealand (pp. 3062-3068).

Luarn, P., & Lin, H. H. (2005). Toward an understanding of the

behavioral intention to use mobile banking. Computers in Human Behavior, 21(6), 873-891.

Maduku, D. K., & Mpinganjira, M. (2012). An empirical investigation

into customers' attitude towards usage of cell phone banking in Gauteng, South Africa. Journal of Contemporary Management, 9(1), 172-189.

Marr, N. E., & Prendergast, G. P. (1993). Consumer adoption of self-

service technologies in retail banking: Is expert opinion supported by consumer research?. International Journal of Bank Marketing, 11(1), 3-10.

Martocchio, J. J., & Webster, J. (1992). Effects of feedback and

cognitive playfulness on performance in microcomputer software training. Personnel Psychology, 45(3), 553-578.

Mbiti, I., & Weil, D. N. (2011). Mobile banking: The impact of M-Pesa

in Kenya (No. w17129). National Bureau of Economic Research. Medenilla, K. (2016). Philippines: ‘Fastest-growing’ smartphone nation

in Southeast Asia. Asian Journal – The Filipino-American Community Newspaper. Retrieved from http://asianjournal. com/news/philippines-fastest-growing-smartphone-nation-in-southeast-asia/

Journal of Multidisciplinary Studies Vol. 7, Issue No. 1, pp. 21-39, August 2018 ISSN 2350-7020 (Print) ISSN 2362-9436 (Online) doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

37

Medhi, I., Ratan, A., & Toyama, K. (2009, July). Mobile-banking adoption and usage by low-literate, low-income users in the developing world. In International Conference on Internationalization, Design and Global Development (pp. 485-494). Springer Berlin Heidelberg.

Meuter, M. L., Ostrom, A. L., Bitner, M. J., & Roundtree, R. (2003).

The influence of technology anxiety on consumer use and experiences with self-service technologies. Journal of Business Research, 56(11), 899-906.

Nasri, W., & Charfeddine, L. (2012). Factors affecting the adoption of

internet banking in Tunisia: An integration theory of acceptance model and theory of planned behavior. The Journal of High Technology Management Research, 23(1), 1-14.

Ndubisi, N. O. (2004, July). Factors influencing e-learning adoption

intention: Examining the determinant structure of the decomposed theory of planned behaviour constructs. In In Proceedings of the 27th Annual Conference of HERDSA (pp. 252-262).

Nysveen, H., Pedersen, P. E., & Thorbjørnsen, H. (2005). Explaining

intention to use mobile chat services: Moderating effects of gender. Journal of Consumer Marketing, 22(5), 247-256.

Parasuraman, A. (2000). Technology readiness index (TRI) a multiple-

item scale to measure readiness to embrace new technologies. Journal of Service Research, 2(4), 307-320.

Puschel, J., Afonso Mazzon, J., & Mauro C. Hernandez, J. (2010).

Mobile banking: Proposition of an integrated adoption intention framework. International Journal of Bank Marketing, 28(5), 389-409.

36

Journal of Multidisciplinary StudiesVol. 7, Issue No. 1, pp. 21-39, August 2018ISSN 2350-7020 (Print)ISSN 2362-9436 (Online)doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

Journal of Multidisciplinary Studies Vol. 7, Issue No. 1, pp. 21-39, August 2018 ISSN 2350-7020 (Print) ISSN 2362-9436 (Online) doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

37

Medhi, I., Ratan, A., & Toyama, K. (2009, July). Mobile-banking adoption and usage by low-literate, low-income users in the developing world. In International Conference on Internationalization, Design and Global Development (pp. 485-494). Springer Berlin Heidelberg.

Meuter, M. L., Ostrom, A. L., Bitner, M. J., & Roundtree, R. (2003).

The influence of technology anxiety on consumer use and experiences with self-service technologies. Journal of Business Research, 56(11), 899-906.

Nasri, W., & Charfeddine, L. (2012). Factors affecting the adoption of

internet banking in Tunisia: An integration theory of acceptance model and theory of planned behavior. The Journal of High Technology Management Research, 23(1), 1-14.

Ndubisi, N. O. (2004, July). Factors influencing e-learning adoption

intention: Examining the determinant structure of the decomposed theory of planned behaviour constructs. In In Proceedings of the 27th Annual Conference of HERDSA (pp. 252-262).

Nysveen, H., Pedersen, P. E., & Thorbjørnsen, H. (2005). Explaining

intention to use mobile chat services: Moderating effects of gender. Journal of Consumer Marketing, 22(5), 247-256.

Parasuraman, A. (2000). Technology readiness index (TRI) a multiple-

item scale to measure readiness to embrace new technologies. Journal of Service Research, 2(4), 307-320.

Puschel, J., Afonso Mazzon, J., & Mauro C. Hernandez, J. (2010).

Mobile banking: Proposition of an integrated adoption intention framework. International Journal of Bank Marketing, 28(5), 389-409.

37

R. P. AtienzaResistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

Resistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines

R. P. Atienza

38

R Core Team (2013). R: A language and environment for statistical computing. R foundation for Statistical Computing, Vienna, Autria. URL http://www.R-project.org/

Ram, S. (1987). A model of innovation resistance. NA-Advances in

Consumer Research Volume 14. Ram, S., & Sheth, J. N. (1989). Consumer resistance to innovations:

The marketing problem and its solutions. Journal of Consumer Marketing, 6(2), 5-14.

Riquelme, H. E., & Rios, R. E. (2010). The moderating effect of gender

in the adoption of mobile banking. International Journal of Bank Marketing, 28(5), 328-341.

Rogers, E. M. (2010). Diffusion of innovations. Simon and Schuster.

Retrieved at: https://www.researchgate.net/profile/Anja_ Christinck/publication/225616414_Farmers_and_researchers_ How_can_collaborative_advantages_be_created_in_participatory_research_and_technology_development/links/00b4953a92931a6fae000000.pdf#page=37

Sala-i-Martin, X., Blanke, J., Hanouz, M. D., Geiger, T., Mia, I., &

Paua, F. (2007). The global competitiveness index: Measuring the productive potential of nations. The Global Competitiveness Report, 2008, 3-50.

Sheth, J. N. (1981). An integrative theory of patronage preference and

behavior (pp. 9-28). College of Commerce and Business Administration, Bureau of Economic and Business Research, University of Illinois, Urbana-Champaign.

Siau, K., & Shen, Z. (2003). Building customer trust in mobile

commerce. Communications of the ACM, 46(4), 91-94.

Journal of Multidisciplinary Studies Vol. 7, Issue No. 1, pp. 21-39, August 2018 ISSN 2350-7020 (Print) ISSN 2362-9436 (Online) doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

39

Suoranta, M., & Mattila, M. (2004). Mobile banking and consumer behaviour: New insights into the diffusion pattern. Journal of Financial Services Marketing, 8(4), 354-366.

Tan, M., & Teo, T. S. (2000). Factors influencing the adoption of

Internet banking. Journal of the AIS, 1(1es), 5. Wang, Y. S., Lin, H. H., & Luarn, P. (2006). Predicting consumer

intention to use mobile service. Information Systems Journal, 16(2), 157-179.

Wilson, J. O., & Goddard, J. (2016). Banking: A very short

introduction. OUP Catalogue. Yu, C. S. (2012). Factors affecting individuals to adopt mobile banking:

Empirical evidence from the UTAUT model. Journal of Electronic Commerce Research, 13(2), 104.

38

Journal of Multidisciplinary StudiesVol. 7, Issue No. 1, pp. 21-39, August 2018ISSN 2350-7020 (Print)ISSN 2362-9436 (Online)doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

Journal of Multidisciplinary Studies Vol. 7, Issue No. 1, pp. 21-39, August 2018 ISSN 2350-7020 (Print) ISSN 2362-9436 (Online) doi: http://dx.doi.org/10.7828/jmds.v7i1.1244

39

Suoranta, M., & Mattila, M. (2004). Mobile banking and consumer behaviour: New insights into the diffusion pattern. Journal of Financial Services Marketing, 8(4), 354-366.

Tan, M., & Teo, T. S. (2000). Factors influencing the adoption of

Internet banking. Journal of the AIS, 1(1es), 5. Wang, Y. S., Lin, H. H., & Luarn, P. (2006). Predicting consumer

intention to use mobile service. Information Systems Journal, 16(2), 157-179.

Wilson, J. O., & Goddard, J. (2016). Banking: A very short

introduction. OUP Catalogue. Yu, C. S. (2012). Factors affecting individuals to adopt mobile banking:

Empirical evidence from the UTAUT model. Journal of Electronic Commerce Research, 13(2), 104.

39

R. P. AtienzaResistance to Mobile and Internet Banking Innovation in Ozamiz City, Philippines