Embed Size (px)

Citation preview

Reserves – Release or Forever?

Jeffrey A. Friedman, Partner Michele Borens, Partner Leah Robinson, Partner TEI/IPT SALT Day December 9, 2014

©2014 Sutherland Asbill & Brennan LLP

Agenda

• Overview of issues and concerns with reserves • FIN 48 Standards

• FAS 5 Standards

• Disclosures

Brief discussion regarding required disclosures

2

©2014 Sutherland Asbill & Brennan LLP 3

Background

• “In principle, the validity of a tax position is a matter of tax law. It is not controversial to recognize the benefit of a tax position in an enterprise’s financial statements when the degree of confidence is high that the tax position will be sustained upon examination by a taxing authority. However, in some cases, the law is subject to varied interpretation, and whether a tax position will ultimately be sustained may be uncertain.” FASB Interpretation No. 48 (pg. 4). For these uncertain tax positions, under FAS 5 or FIN 48, a

taxpayer may be required to book a reserve.

©2014 Sutherland Asbill & Brennan LLP

Reserves – Are they forever?

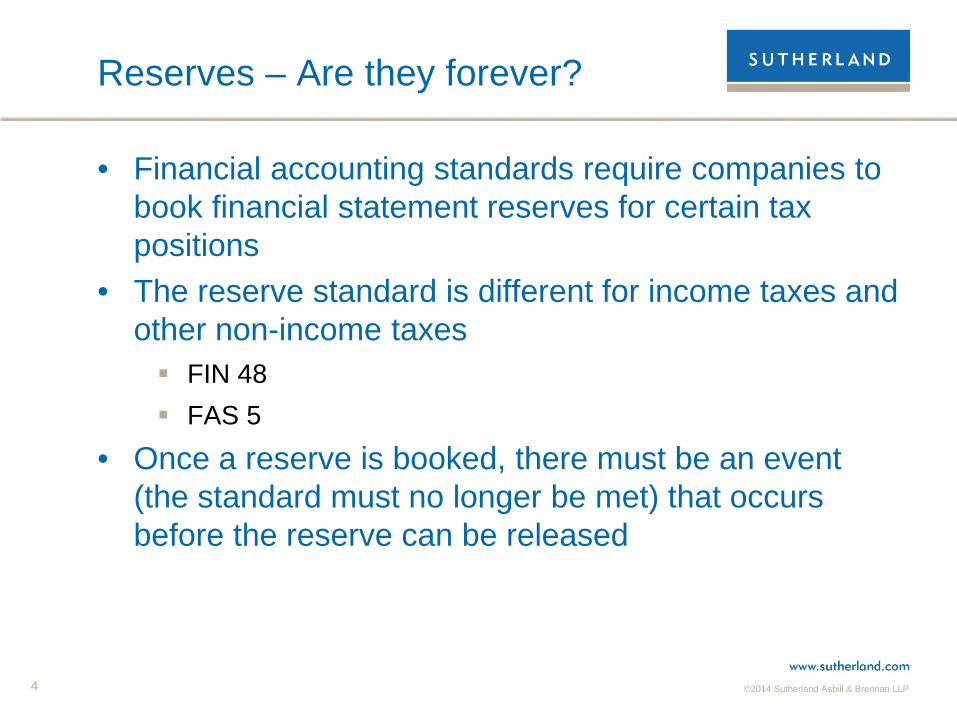

• Financial accounting standards require companies to book financial statement reserves for certain tax positions

• The reserve standard is different for income taxes and other non-income taxes FIN 48 FAS 5

• Once a reserve is booked, there must be an event (the standard must no longer be met) that occurs before the reserve can be released

4

©2014 Sutherland Asbill & Brennan LLP

Background

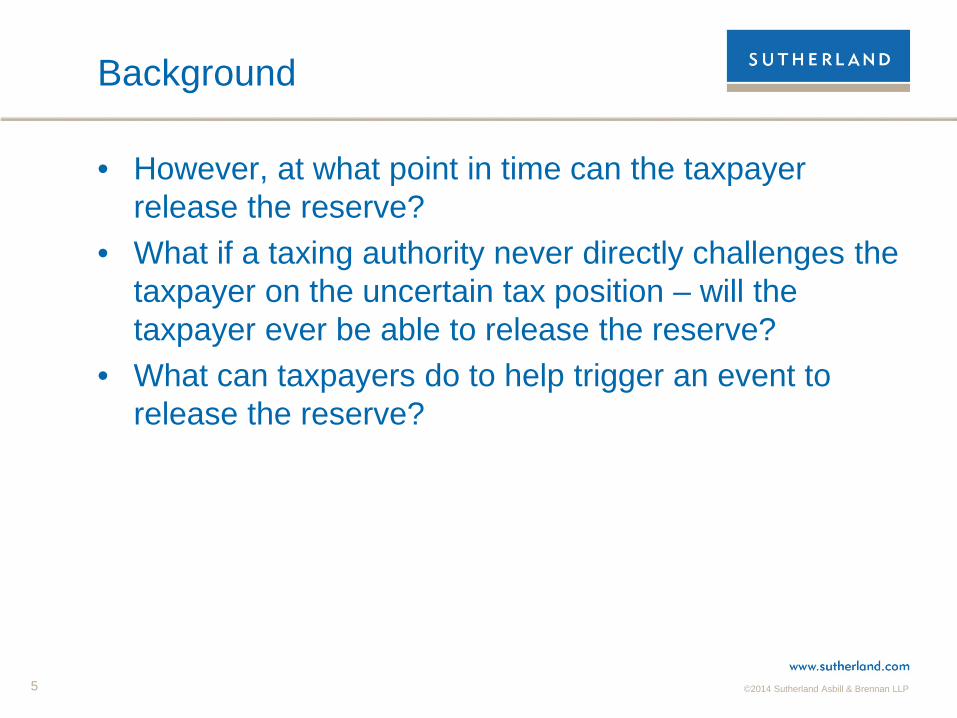

• However, at what point in time can the taxpayer release the reserve?

• What if a taxing authority never directly challenges the taxpayer on the uncertain tax position – will the taxpayer ever be able to release the reserve?

• What can taxpayers do to help trigger an event to release the reserve?

5

©2014 Sutherland Asbill & Brennan LLP 6

FIN 48

©2014 Sutherland Asbill & Brennan LLP 7

FIN 48

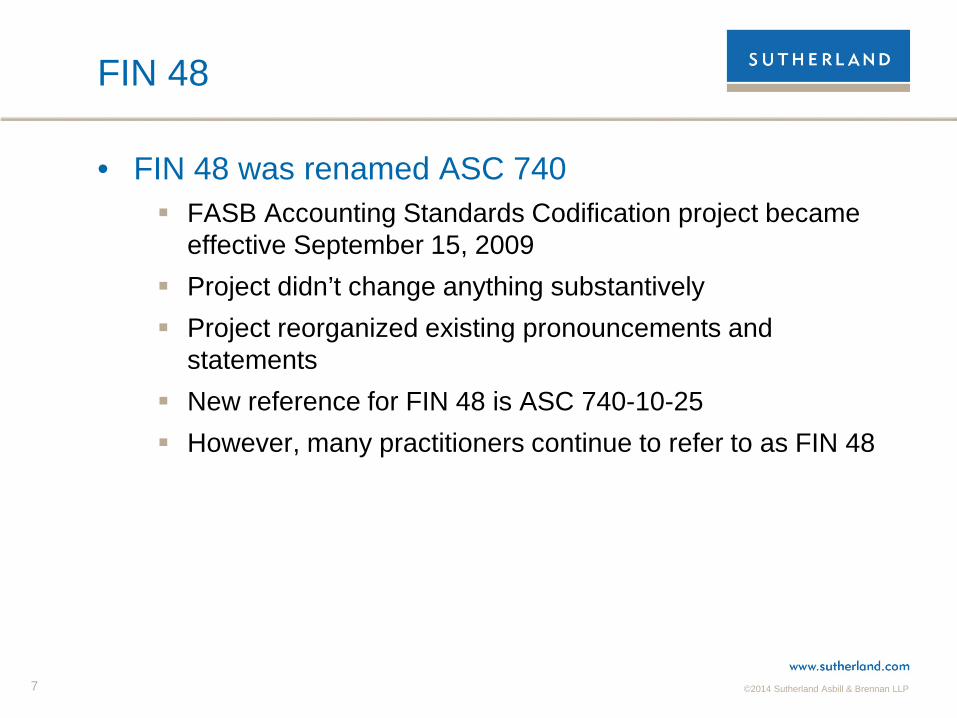

• FIN 48 was renamed ASC 740 FASB Accounting Standards Codification project became

effective September 15, 2009 Project didn’t change anything substantively Project reorganized existing pronouncements and

statements New reference for FIN 48 is ASC 740-10-25 However, many practitioners continue to refer to as FIN 48

©2014 Sutherland Asbill & Brennan LLP

FIN 48

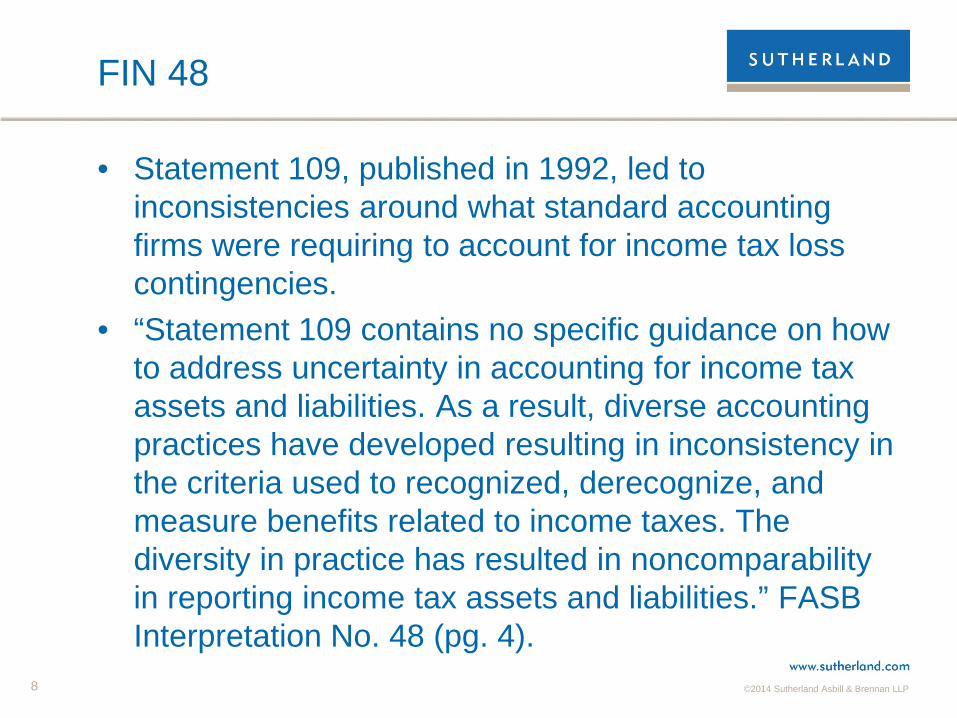

• Statement 109, published in 1992, led to inconsistencies around what standard accounting firms were requiring to account for income tax loss contingencies.

• “Statement 109 contains no specific guidance on how to address uncertainty in accounting for income tax assets and liabilities. As a result, diverse accounting practices have developed resulting in inconsistency in the criteria used to recognized, derecognize, and measure benefits related to income taxes. The diversity in practice has resulted in noncomparability in reporting income tax assets and liabilities.” FASB Interpretation No. 48 (pg. 4). 8

©2014 Sutherland Asbill & Brennan LLP 9

FIN 48

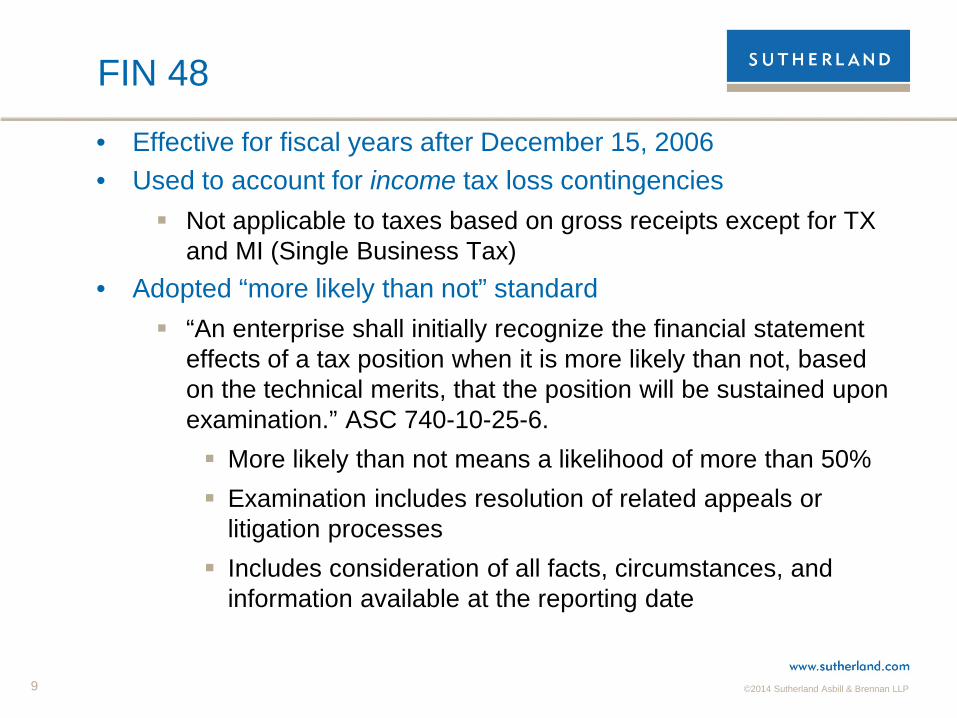

• Effective for fiscal years after December 15, 2006 • Used to account for income tax loss contingencies

Not applicable to taxes based on gross receipts except for TX and MI (Single Business Tax)

• Adopted “more likely than not” standard “An enterprise shall initially recognize the financial statement

effects of a tax position when it is more likely than not, based on the technical merits, that the position will be sustained upon examination.” ASC 740-10-25-6. More likely than not means a likelihood of more than 50% Examination includes resolution of related appeals or

litigation processes Includes consideration of all facts, circumstances, and

information available at the reporting date

©2014 Sutherland Asbill & Brennan LLP 10

FIN 48

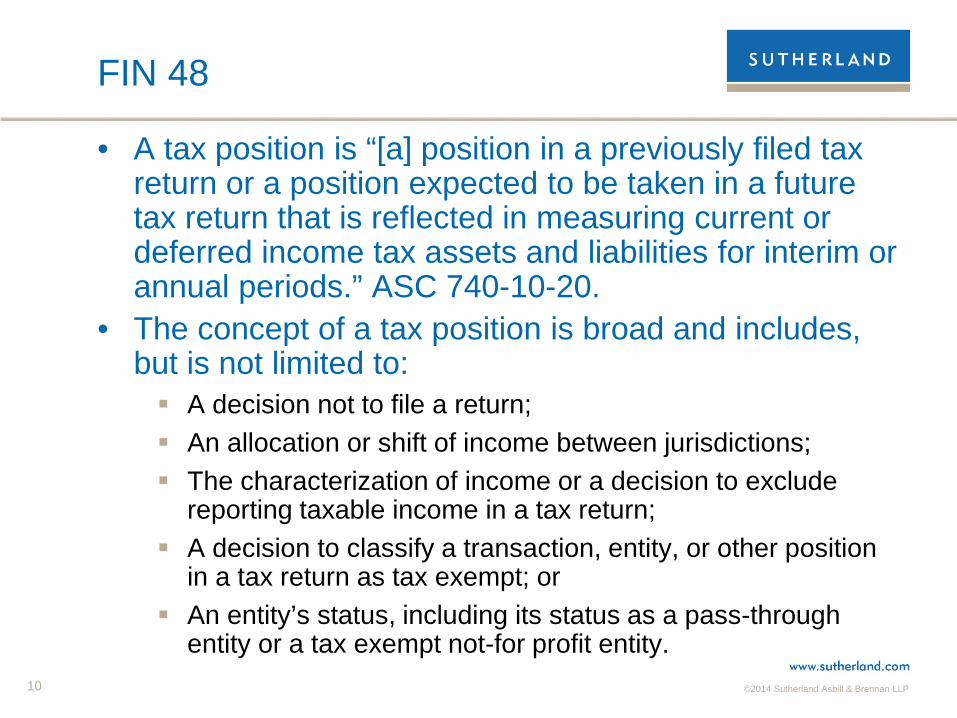

• A tax position is “[a] position in a previously filed tax return or a position expected to be taken in a future tax return that is reflected in measuring current or deferred income tax assets and liabilities for interim or annual periods.” ASC 740-10-20.

• The concept of a tax position is broad and includes, but is not limited to: A decision not to file a return; An allocation or shift of income between jurisdictions; The characterization of income or a decision to exclude

reporting taxable income in a tax return; A decision to classify a transaction, entity, or other position

in a tax return as tax exempt; or An entity’s status, including its status as a pass-through

entity or a tax exempt not-for profit entity.

©2014 Sutherland Asbill & Brennan LLP 11

FIN 48

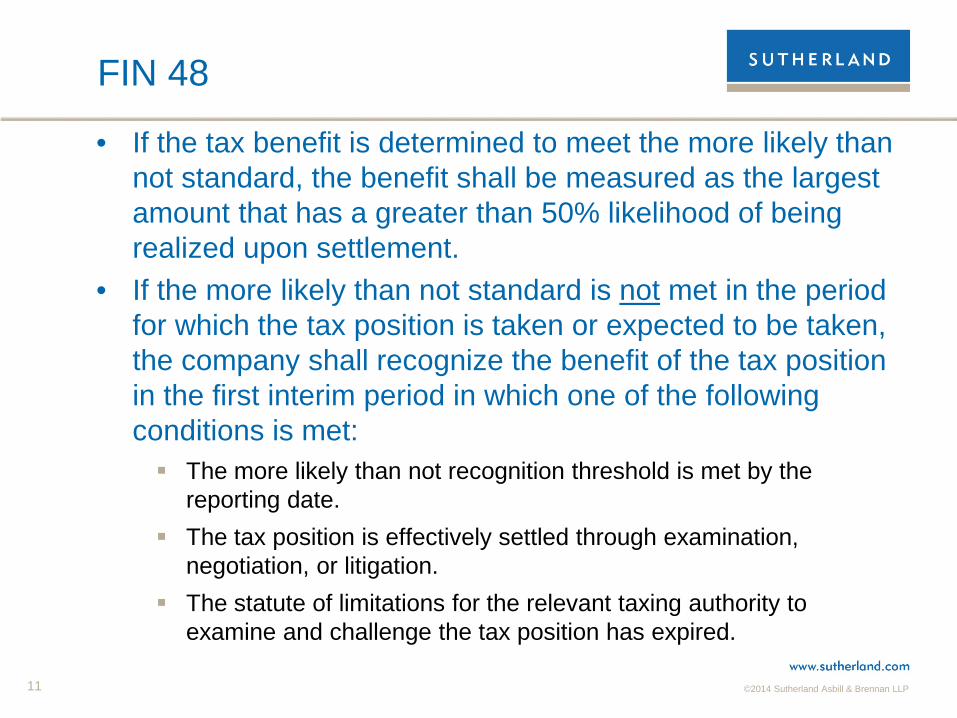

• If the tax benefit is determined to meet the more likely than not standard, the benefit shall be measured as the largest amount that has a greater than 50% likelihood of being realized upon settlement.

• If the more likely than not standard is not met in the period for which the tax position is taken or expected to be taken, the company shall recognize the benefit of the tax position in the first interim period in which one of the following conditions is met: The more likely than not recognition threshold is met by the

reporting date. The tax position is effectively settled through examination,

negotiation, or litigation. The statute of limitations for the relevant taxing authority to

examine and challenge the tax position has expired.

©2014 Sutherland Asbill & Brennan LLP 12

FIN 48

• Example Company has been filing income tax returns in State A in

2005. However, before 2005, it is not sure when it first had nexus with or was doing business in State A.

Because no tax returns were filed before 2005, the statute of limitations for those years never began running.

State A has provided no guidance on how far back it will look in determining if there is a tax return due and if a tax deficiency is owed.

How long must State A continue to book a reserve for?

©2014 Sutherland Asbill & Brennan LLP 13

FIN 48

• This example highlights the dilemma for taxpayers • Once the reserve gets booked, can the taxpayer ever

release it? • This issues comes up most frequently with respect to

nexus Taxpayers and taxing authorities often have widely

disparate ideas regarding what establishes nexus with a state such that the state can impose its income tax on the taxpayer

This problem has only been exacerbated in recent years by the development of economic nexus, affiliate nexus, factor nexus, etc.

©2014 Sutherland Asbill & Brennan LLP 14

FIN 48

• What if a state has a published look-back period? Does the taxpayer need to accrue a reserve for only the

look-back period or book a reserve for years beyond the state’s published look-back period?

• Other possible solutions? Could participation in a state’s voluntary disclosure program

allow the taxpayer to release the reserve? Could taxpayer seek guidance from the taxing authority on

its position? Letter ruling?

Binding or non-binding Legislative change? Regulations?

©2014 Sutherland Asbill & Brennan LLP

FIN 48

• Other possible solutions? Informal guidance regarding state’s look back policy

Documented conversation with state Another similar case that strengthens position Registration with the state and expiration of the SOL for

periods after registration Audit

15

©2014 Sutherland Asbill & Brennan LLP 16

FAS 5

©2014 Sutherland Asbill & Brennan LLP

FAS 5

• FAS 5 was renamed ASC 450 New reference for FAS 5 is ASC 450 However, many practitioners continue to refer to as FAS 5

• FAS 5 is applicable to non-income taxes, including: employment taxes, sales and use taxes, abandoned and unclaimed property, property taxes, franchise/net worth taxes, and gross receipts taxes.

17

©2014 Sutherland Asbill & Brennan LLP 18

FAS 5

• FAS 5 requires companies to accrue a reserve for a loss contingency if both of the following conditions are met:

• It is probable that an asset had been impaired or a liability had been incurred at the date of the financial statement.

• This amount of the liability is reasonably estimable.

• Probable is defined as “the future events are likely to occur.”

• If no accrual is made for a loss contingency because one or both of the conditions are not met, disclosure of the contingency shall be made when there is at least a reasonable possibility that a loss or an additional loss may have been incurred.

©2014 Sutherland Asbill & Brennan LLP 19

FAS 5

• Example Company claimed a credit against its gross receipts taxes in

State A. However, it is unclear whether the conditions required to be met to claim the credit were in fact met before the deadline to claim the credit.

If Company determines that it is not “probable” that a loss will occur upon audit, then No loss contingency reserve would have to be accrued Financial statement benefit of the deduction is fully

recognized

©2014 Sutherland Asbill & Brennan LLP 20

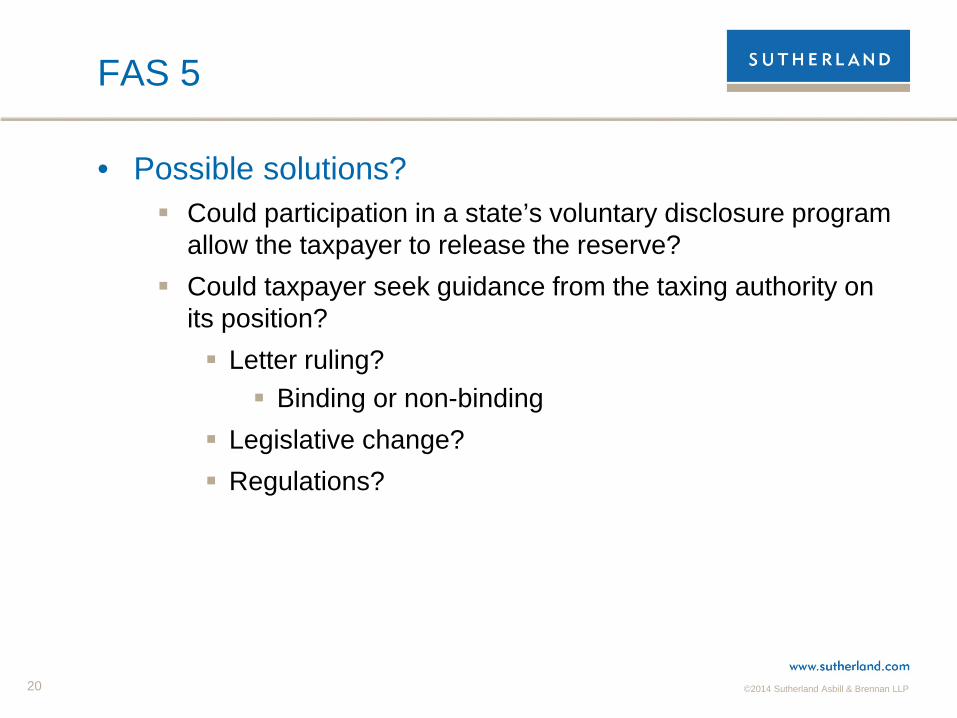

FAS 5

• Possible solutions? Could participation in a state’s voluntary disclosure program

allow the taxpayer to release the reserve? Could taxpayer seek guidance from the taxing authority on

its position? Letter ruling?

Binding or non-binding Legislative change? Regulations?

©2014 Sutherland Asbill & Brennan LLP 21

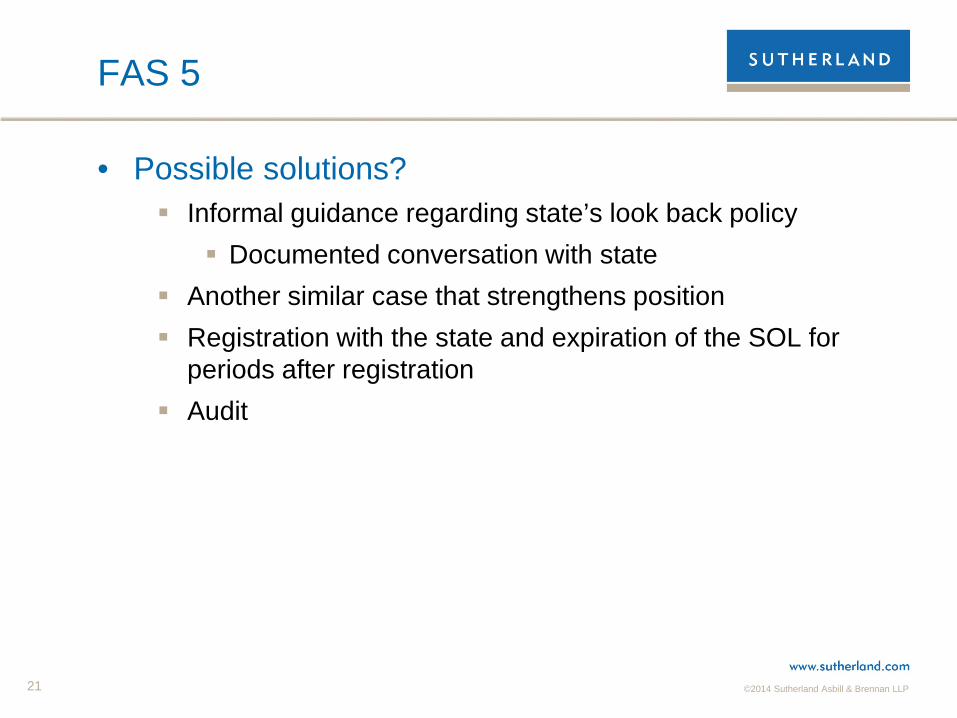

FAS 5

• Possible solutions? Informal guidance regarding state’s look back policy

Documented conversation with state Another similar case that strengthens position Registration with the state and expiration of the SOL for

periods after registration Audit

©2014 Sutherland Asbill & Brennan LLP 22

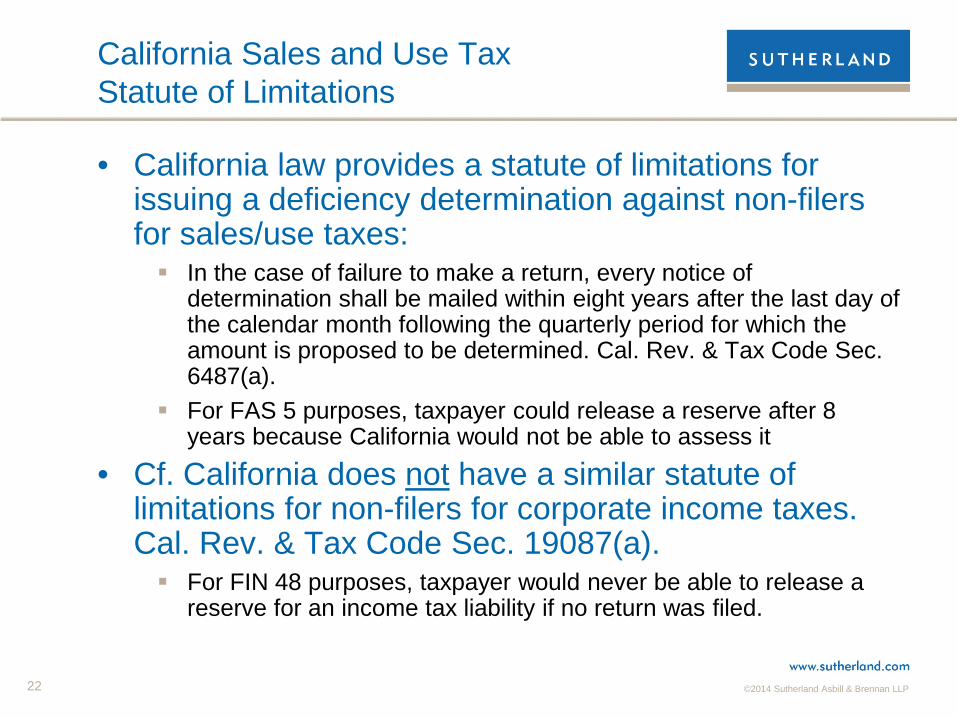

California Sales and Use Tax Statute of Limitations

• California law provides a statute of limitations for issuing a deficiency determination against non-filers for sales/use taxes: In the case of failure to make a return, every notice of

determination shall be mailed within eight years after the last day of the calendar month following the quarterly period for which the amount is proposed to be determined. Cal. Rev. & Tax Code Sec. 6487(a).

For FAS 5 purposes, taxpayer could release a reserve after 8 years because California would not be able to assess it

• Cf. California does not have a similar statute of limitations for non-filers for corporate income taxes. Cal. Rev. & Tax Code Sec. 19087(a). For FIN 48 purposes, taxpayer would never be able to release a

reserve for an income tax liability if no return was filed.

©2014 Sutherland Asbill & Brennan LLP

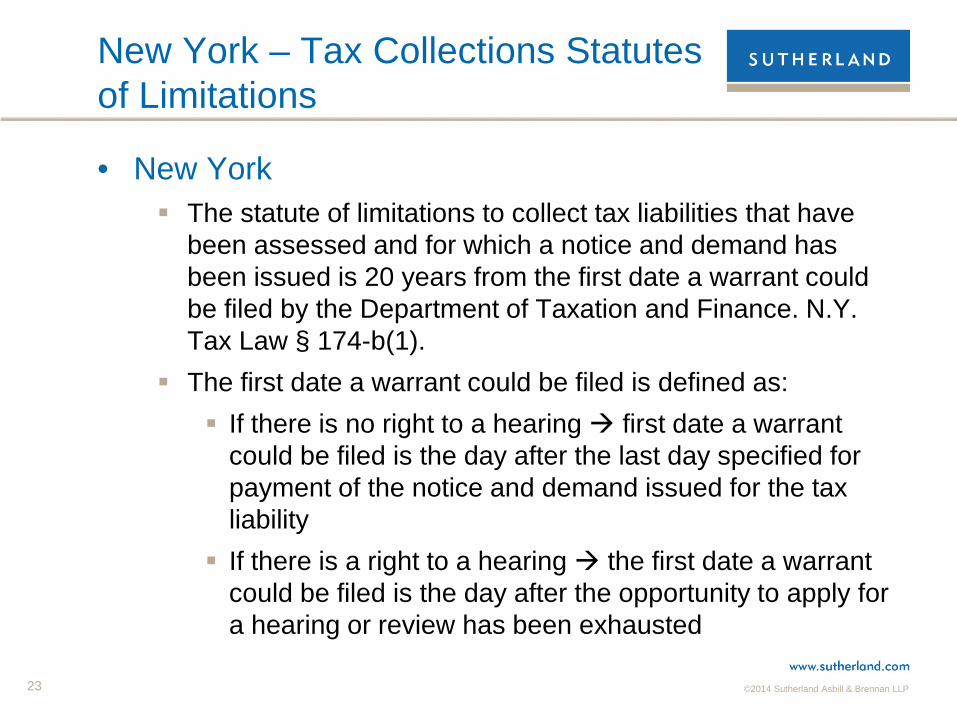

New York – Tax Collections Statutes of Limitations

• New York The statute of limitations to collect tax liabilities that have

been assessed and for which a notice and demand has been issued is 20 years from the first date a warrant could be filed by the Department of Taxation and Finance. N.Y. Tax Law § 174-b(1).

The first date a warrant could be filed is defined as: If there is no right to a hearing first date a warrant

could be filed is the day after the last day specified for payment of the notice and demand issued for the tax liability

If there is a right to a hearing the first date a warrant could be filed is the day after the opportunity to apply for a hearing or review has been exhausted

23

©2014 Sutherland Asbill & Brennan LLP

Missouri – Sales and Use Tax Statutes of Limitation

• Missouri can assess sales and use tax at any time in the case of “a fraudulent return or neglect or refusal to make a return…” Mo. Rev. Stat. Sec. 144.220(1). What is neglect or refusal to make a return? If taxpayer has reasonable position that it is not required to

collect and remit sales and use tax under Missouri law, may only be subject to 3 year statute of limitation.

• “In other cases, every notice of additional amount proposed to be assessed under this chapter shall be mailed to the person within 3 years after the return was filed or required to be filed.” Mo. Rev. Stat. Sec. 144.220(3).

24

©2014 Sutherland Asbill & Brennan LLP

Questions?

Jeffrey A. Friedman [email protected]

202.383.0718

Michele Borens [email protected]

202.383.0936

Leah Robinson [email protected]

212.389.5043

25

©2014 Sutherland Asbill & Brennan LLP

Connect with us!

The Sutherland SALT Shaker mobile app is now available. Download today from the: Windows Phone Store iTunes App Store Google Play Amazon Appstore for Android

Visit us at www.stateandlocaltax.com

@Sutherland_SALT Sutherland SALT Group

26