Embed Size (px)

Citation preview

HSEHealth & Safety

Executive

An evidence based evaluation of how best tosecure compliance with health and safety law

Prepared by Greenstreet Berman Ltdfor the Health and Safety Executive 2005

RESEARCH REPORT 334

HSEHealth & Safety

Executive

An evidence based evaluation of how best tosecure compliance with health and safety law

Michael Wright, Ali Antonelli, John Norton Doyle,Mark Bendig and Richard Genna

Greenstreet Berman LtdFulcrum House

5 Southern CourtSouth Street

ReadingBerkshireRG1 4QS

This research builds on previous studies by delineating companies into discrete groups and mappingonto each type of organisation “levers” which influence compliance with health and safety law. It alsoacquires evidence about the likely degree of influence that each lever might have. It providesconclusions on the targeting of interventions and the potential role of new levers to motivatecompliance with health and safety law.

This main report is accompanied by a summary report.

This report and the work it describes were funded by the Health and Safety Executive (HSE). Itscontents, including any opinions and/or conclusions expressed, are those of the authors alone and donot necessarily reflect HSE policy.

HSE BOOKS

ii

© Crown copyright 2005

First published 2005

ISBN 0 7176 2989 9

All rights reserved. No part of this publication may bereproduced, stored in a retrieval system, or transmitted inany form or by any means (electronic, mechanical,photocopying, recording or otherwise) without the priorwritten permission of the copyright owner.

Applications for reproduction should be made in writing to: Licensing Division, Her Majesty's Stationery Office, St Clements House, 2-16 Colegate, Norwich NR3 1BQ or by e-mail to [email protected]

Executive summary

The Revitalising Health and Safety (RHS) Action Plan incorporates many ideas suggested in consultation on how to achieve targets, such as fewer injuries. These ideas aim to build on the HSE’s existing strategy of encouragement, persuasion, assistance and enforcement. Whilst past research has identified key drivers for health and safety there are examples of conflicting findings. Against a background of mixed and incomplete research findings, it is important to understand the interaction between motivational “levers” in order to:

• Understand how the influence of motivational factors co-vary and interact;

• Understand how the attitudes and behaviours of organisations vary according to their type, whilst also mapping out how other organisational characteristics / types vary as organisational attitudes to health and safety vary;

• Seek evidence of the importance of each factor and the case for “new levers”.

Therefore, this research built on previous studies by delineating companies into discrete groups and mapping “levers” onto each type of organisation. We acquired evidence about the likely degree of influence that each lever might have.

After completing a literature review, thirty-nine exploratory discussions were run with employers and key stakeholders, such as the CBI and trade associations, selected from a representative range of sectors and sizes of organisations. Next, two different questionnaire based surveys were developed to assess what motivates organisations to comply with health and safety; one for employers and one for intermediaries. The content was the same apart from the addition of a separate section within the intermediary version, which was incorporated to establish their willingness to take a more active role.

The list of motivational factors remains largely unchanged from previous research, namely enforcement/regulation, reputational risk, the moral case, avoiding cost of accidents and business incentives. However, it is apparent that:

• The financial incentive provided by insurance premiums has grown;

• The fear of enforcement is intertwined with the fear of reputational damage as well as business disruption;

• There is also evidence that the moral case remains a driver, especially in SMEs where you may know or be related to your colleagues. In larger firms the moral case is expressed in terms of societal values, and;

• It is also clear that understanding and awareness remain key precursors.

iii

It is clear that organisational attitudes and the influence of “levers” varies between organisations, primarily according to their size and sector. It is also apparent that a link can be made between the current attitude of organisations towards health and safety, their size/sector and their recommendation of new incentives for health and safety. This suggests that it is not only possible, but also more effective, to match compliance tactics to the attitudes of the organisations, rather than adopt a “one size fits all approach”. The inference that can be drawn from this is that no single “lever” will be equally needed nor effective for all organisations.

These findings also support the notion of targeting interventions and communications according to the expressed attitude of organisations. This can be considered in the context of both national initiatives, such as media campaigns, and inspection tactics.

It is important not to dismiss relatively low rated ‘incentives’. It is legitimate to argue that the moderate rating assigned to some as yet untested incentives is actually strong evidence because (1) with greater awareness and experience they may offer potential and (2) the effect of more established incentives may have already been realised. Thus, whilst enforcement and the business case remain important, established incentives, other as yet untried incentives such as earned autonomy, adverse publicity, greater investor/worker pressure and restorative justice have scope for increased impact. Clearly, as these levers are relatively untested in the UK health and safety arena, the way in which they may operate and the actions needed to increase their influence require further research, piloting and evaluation. Insurance is a prime example of how the role of an incentive can change, as well as being a lever that the HSE could make more use.

iv

CONTENTS

EXECUTIVE SUMMARY

1 INTRODUCTION ............................................................................................................................1

1.1 BACKGROUND............................................................................................................................1

1.2 MODELS AND EVIDENCE OF ORGANISATIONAL H&S ATTITUDES AND BEHAVIOURS ...................5

1.2.1 A decision making model ......................................................................................................5

1.2.2 Restorative justice...............................................................................................................14

1.2.3 Adverse publicity ................................................................................................................15

1.2.4 Internalising costs of poor performance.............................................................................18

1.2.5 Reducing compliance costs.................................................................................................19

1.2.6 Raising awareness of hazards, risks and costs ...................................................................19

1.2.7 Inter-company variations ...................................................................................................23

1.2.8 Concluding points...............................................................................................................25

2 EXPLORATORY DISCUSSIONS................................................................................................26

2.1 INTRODUCTION ........................................................................................................................26

2.2 CONCLUSIONS FROM RESEARCH AND DISCUSSIONS ..................................................................27

2.2.1 Networking, partnering and amplifying impact of the HSE................................................27

2.2.2 Drivers for health and safety ..............................................................................................29

2.2.3 Costs and benefits of health and safety...............................................................................31

2.2.4 Potential implications.........................................................................................................31

3 POSTAL SURVEY .........................................................................................................................33

3.1 INTRODUCTION ........................................................................................................................33

3.2 PILOTING..................................................................................................................................33

3.2.1 Overview.............................................................................................................................33

3.2.2 Draft questionnaire.............................................................................................................33

3.2.3 Pilot study...........................................................................................................................34

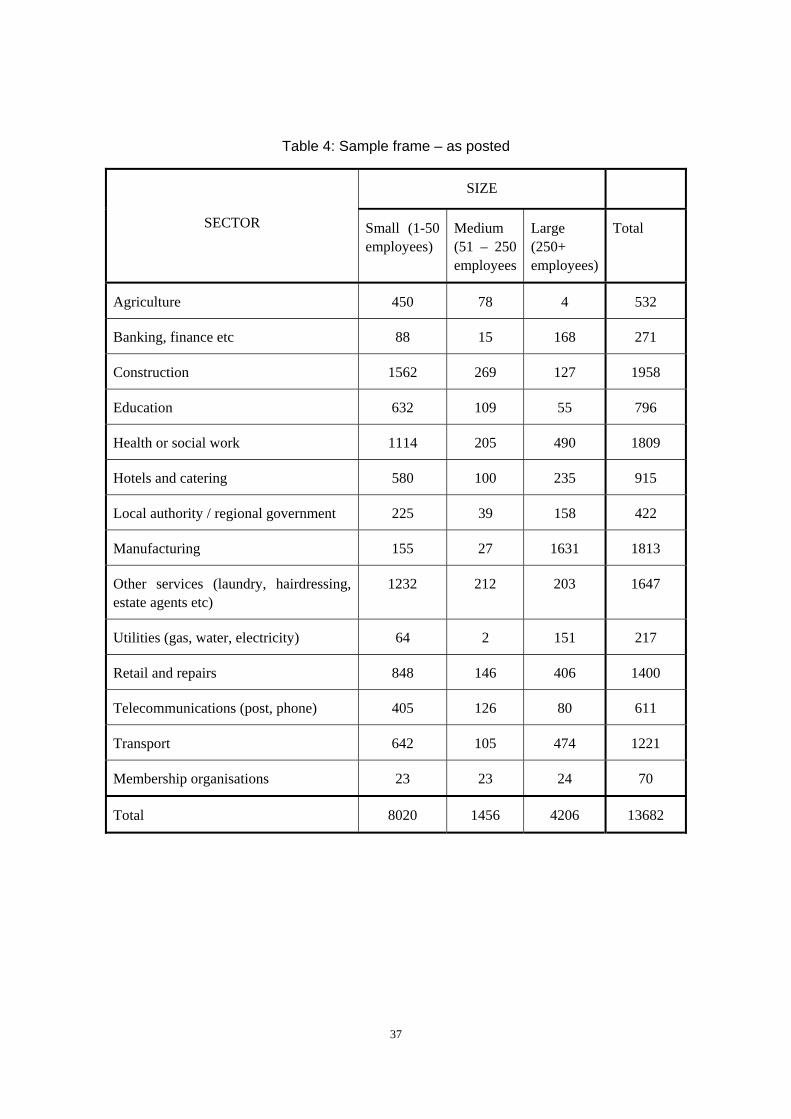

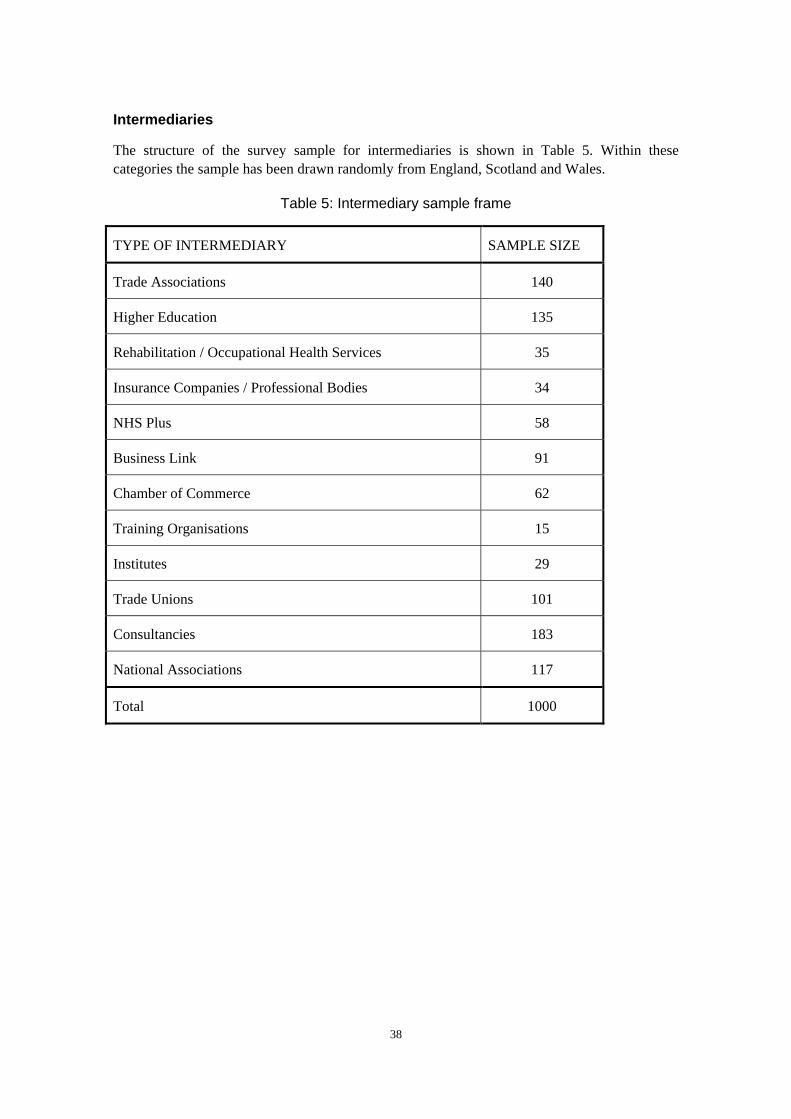

3.3 SAMPLE FRAME AND SIZE.........................................................................................................35

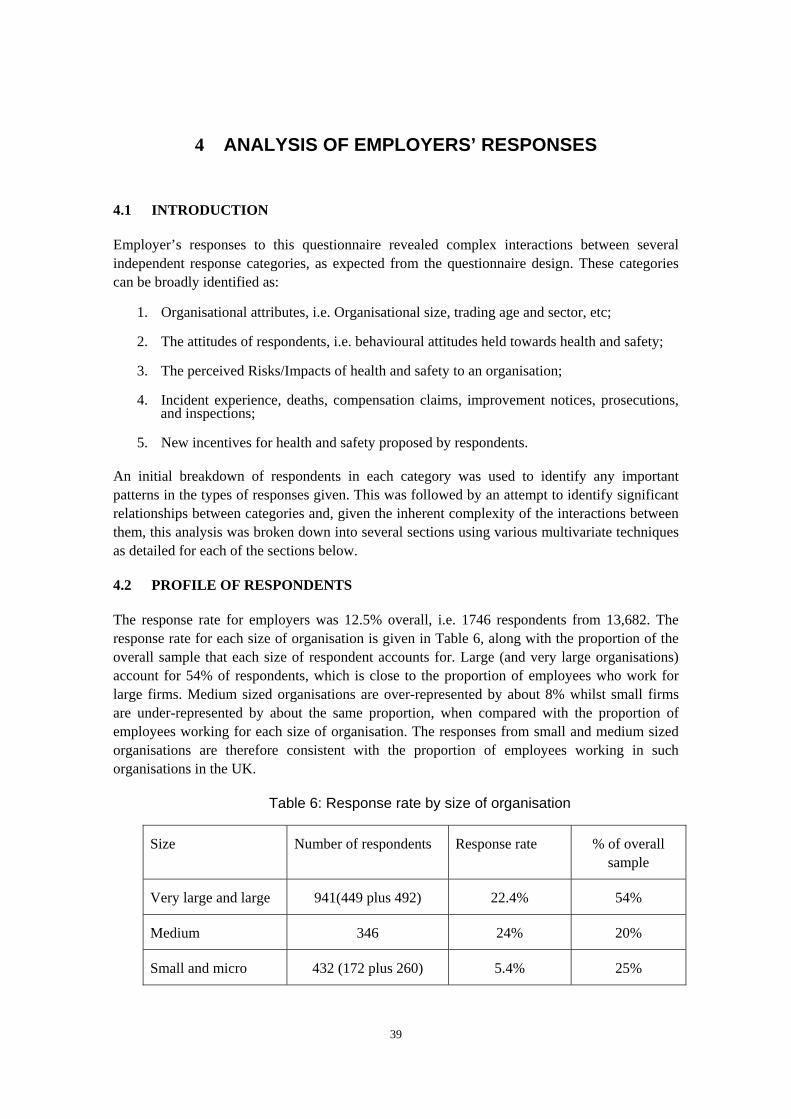

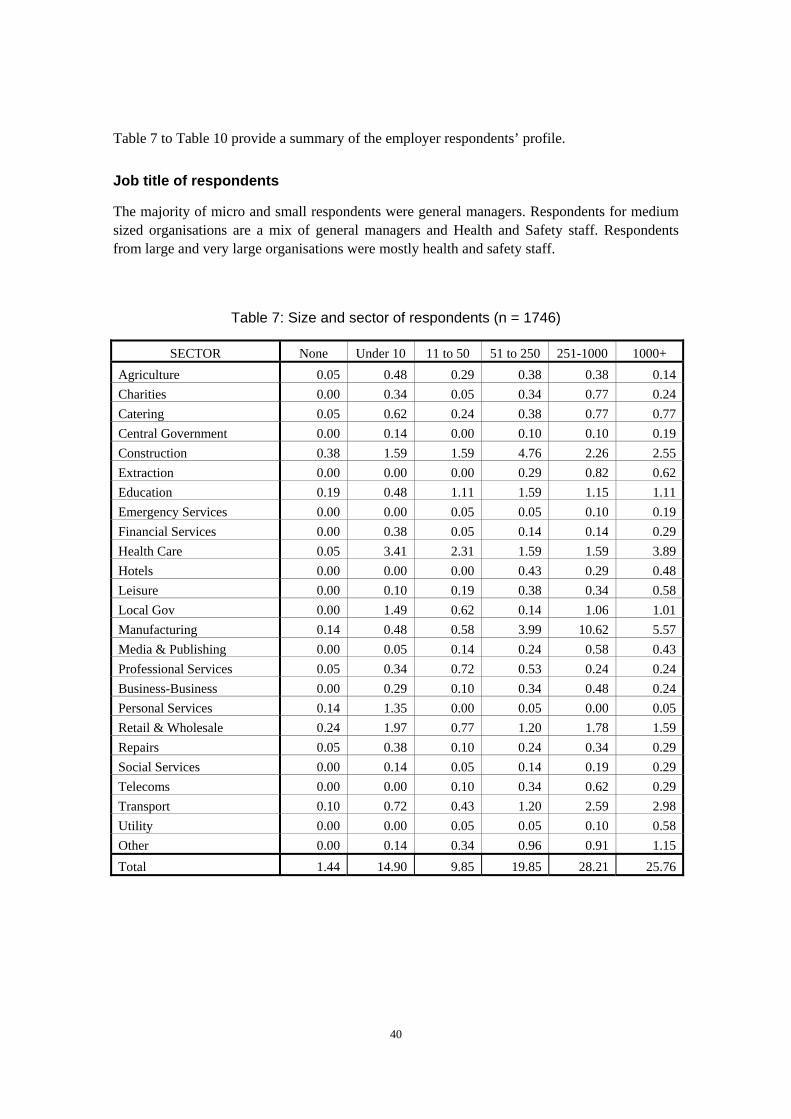

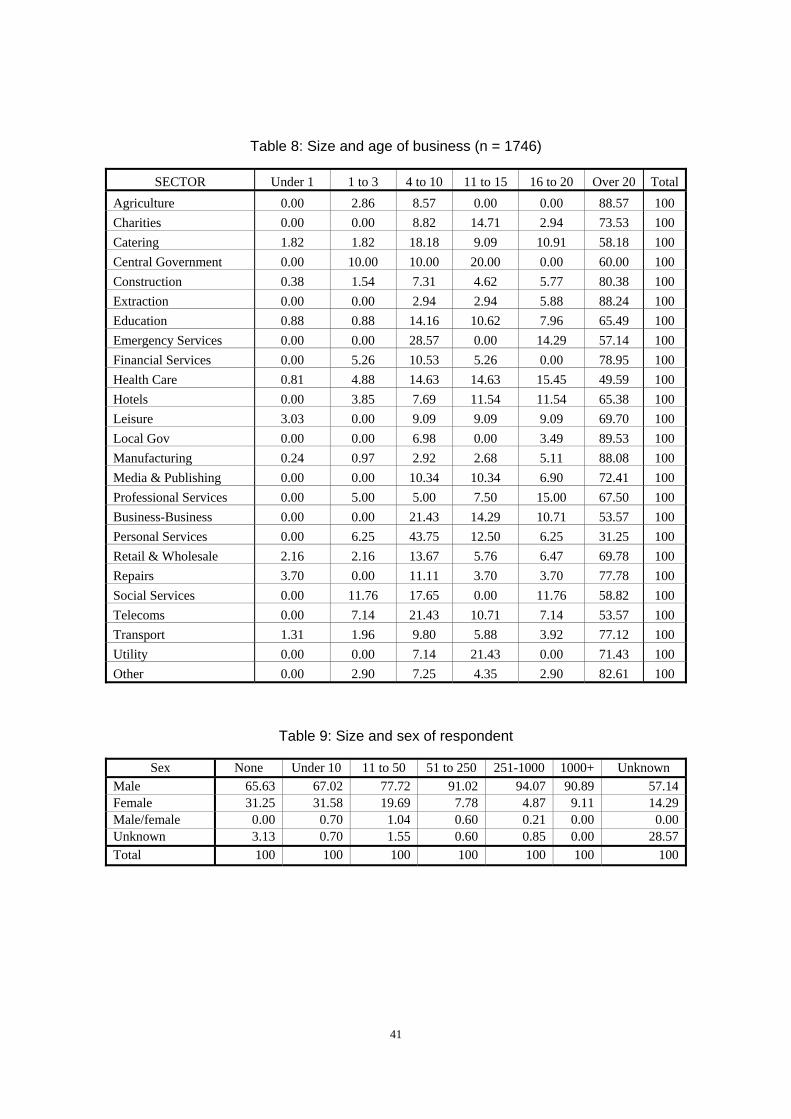

4 ANALYSIS OF EMPLOYERS’ RESPONSES ............................................................................39

4.1 INTRODUCTION ........................................................................................................................39

4.2 PROFILE OF RESPONDENTS .......................................................................................................39

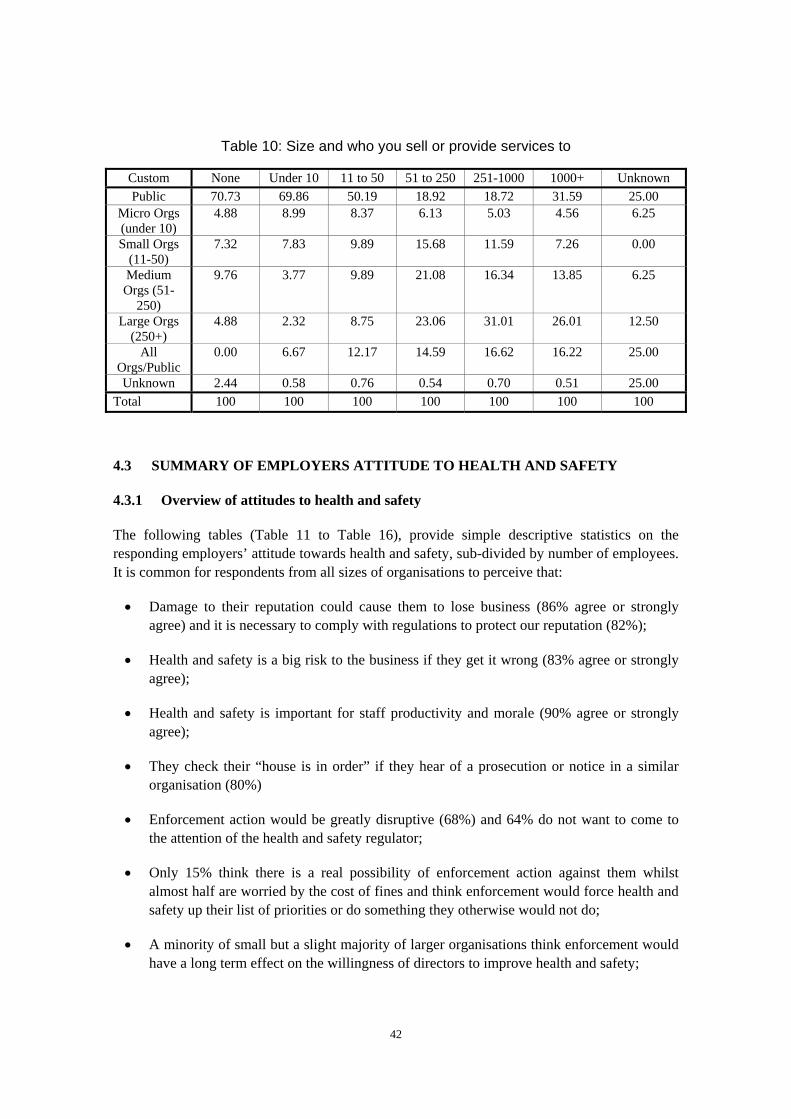

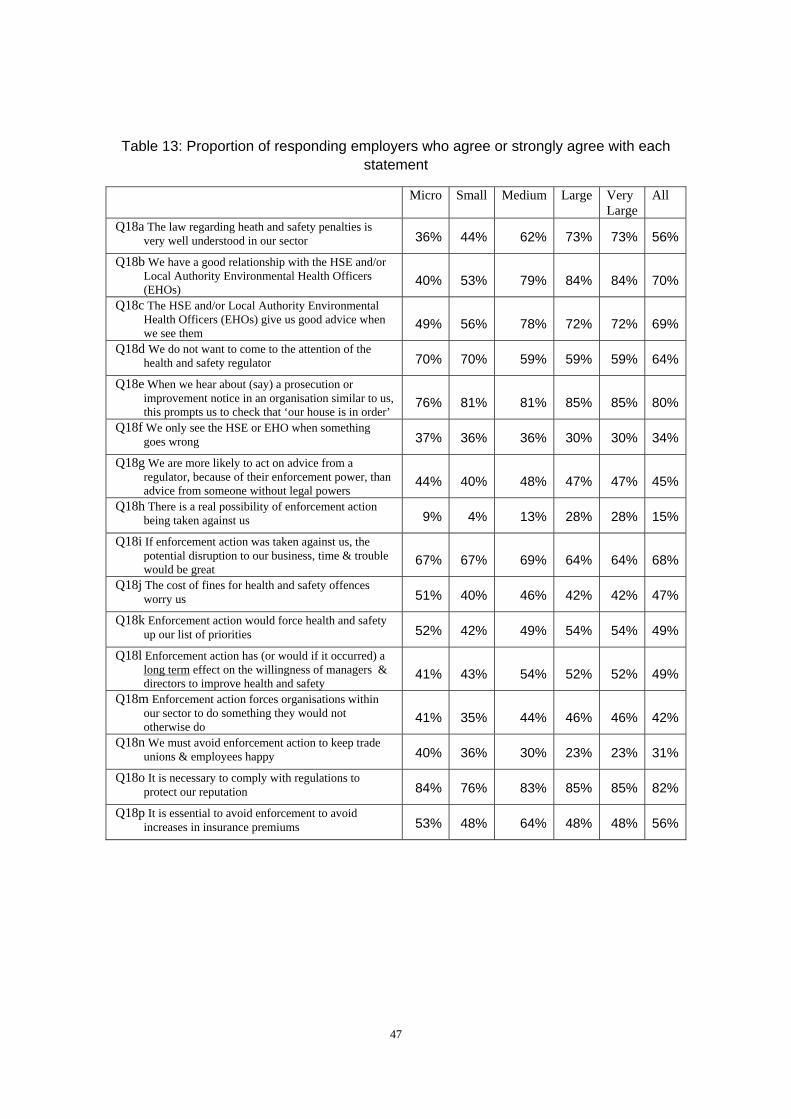

4.3 SUMMARY OF EMPLOYERS ATTITUDE TO HEALTH AND SAFETY................................................42

v

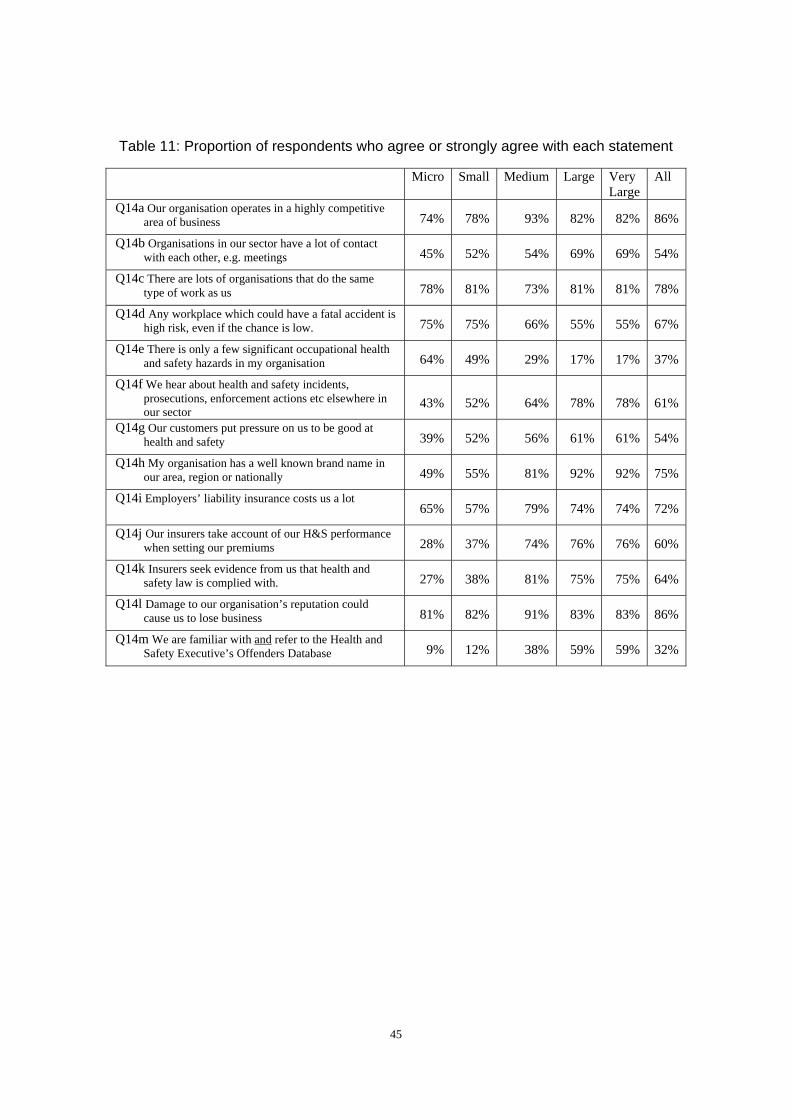

4.3.1 Overview of attitudes to health and safety..........................................................................42

4.3.2 Differences in attitudes between small and larger organisations.......................................43

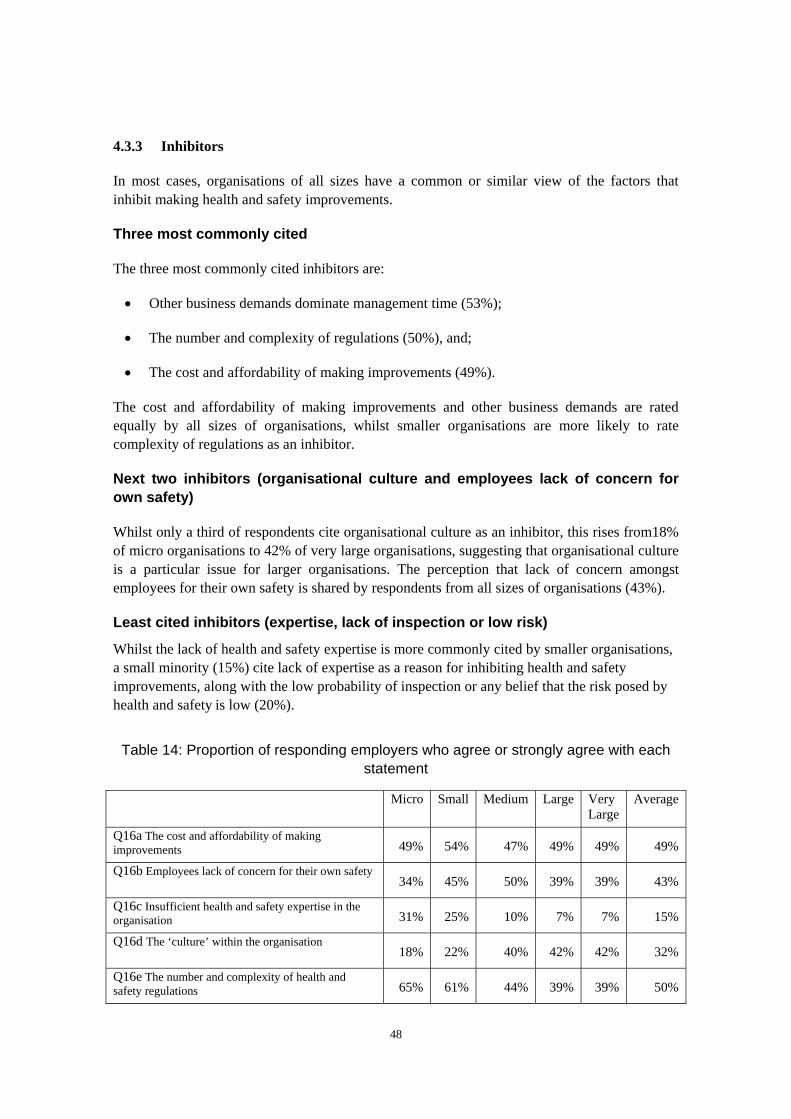

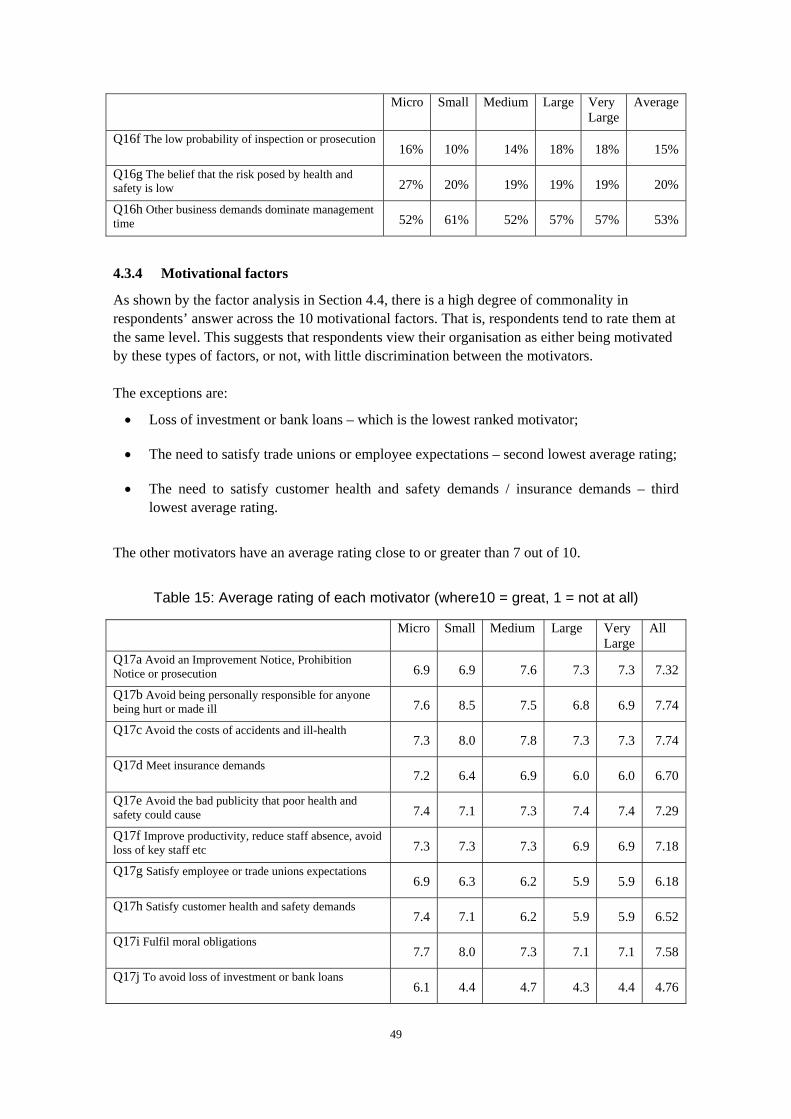

4.3.3 Inhibitors ............................................................................................................................48

4.3.4 Motivational factors ...........................................................................................................49

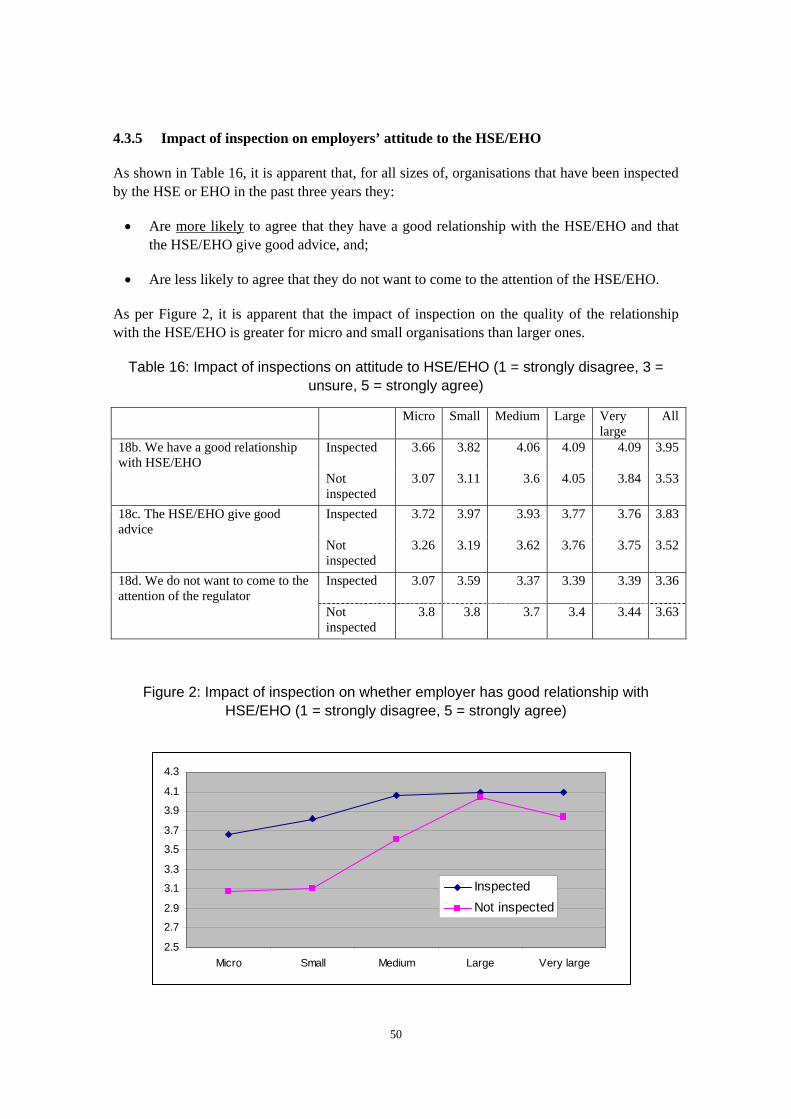

4.3.5 Impact of inspection on employers’ attitude to the HSE/EHO ...........................................50

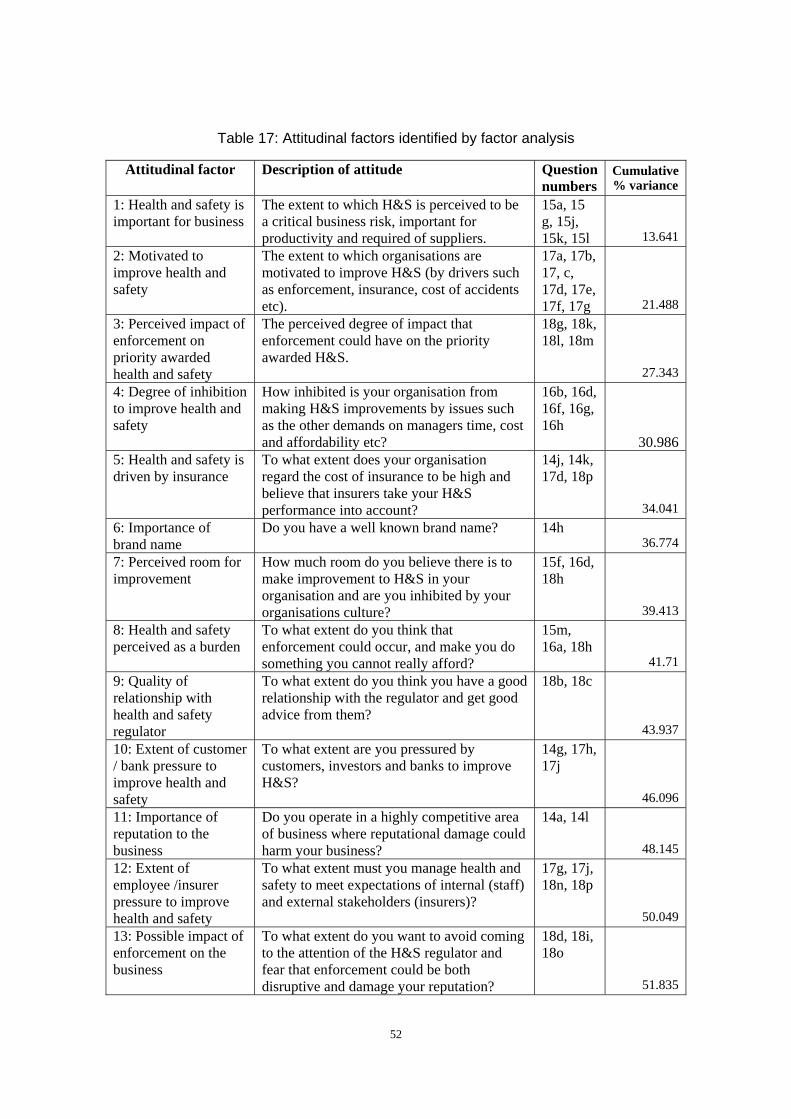

4.4 FACTORS ANALYSIS OF EMPLOYERS’ ATTITUDES TO HEALTH AND SAFETY ..............................51

4.5 ASSOCIATION OF ATTITUDES WITH OTHER FACTORS ................................................................53

4.5.1 Overview.............................................................................................................................53

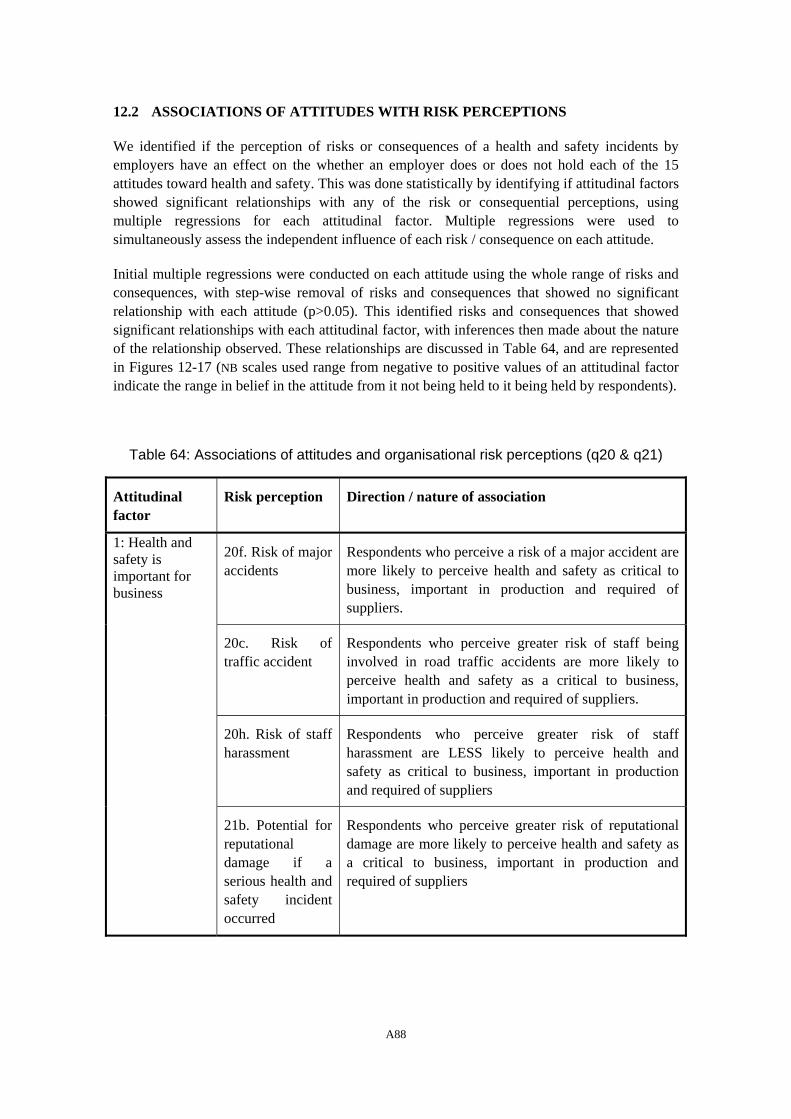

4.5.2 Association of attitudes with organisational attributes, risk perceptions, incident experience and new incentives..........................................................................................................53

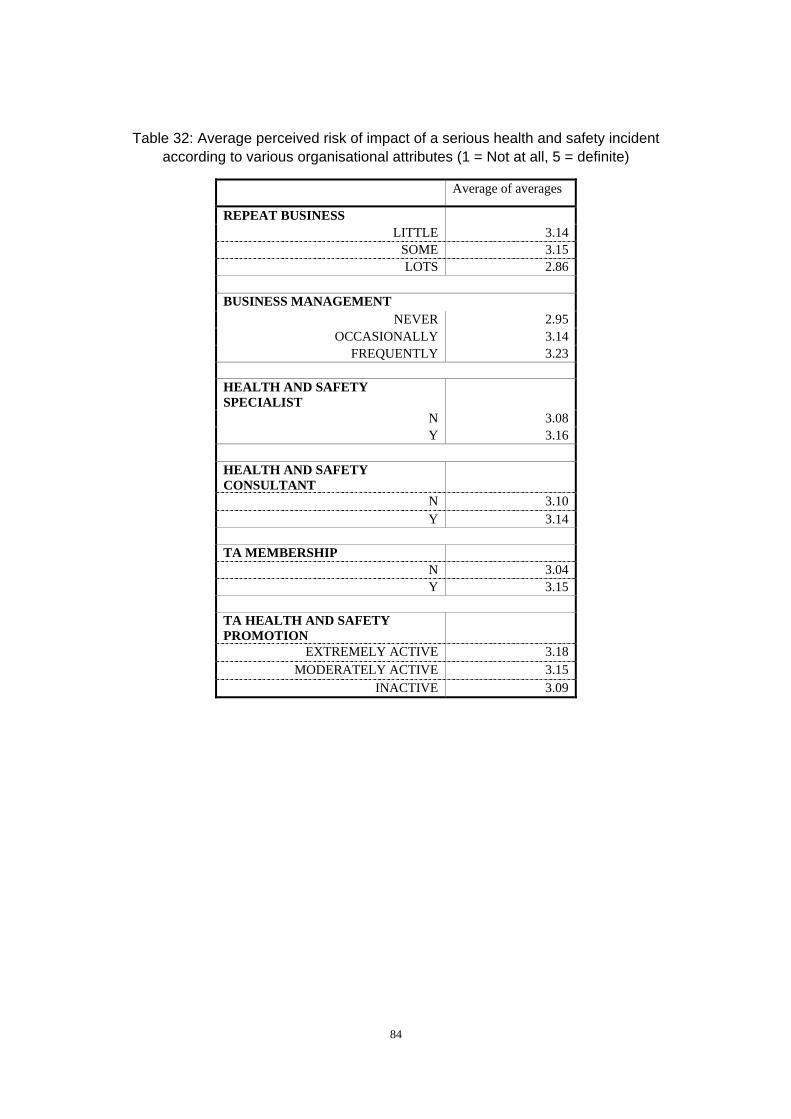

4.6 ASSOCIATION OF RISK PERCEPTIONS WITH ORGANISATIONAL ATTRIBUTES ..............................73

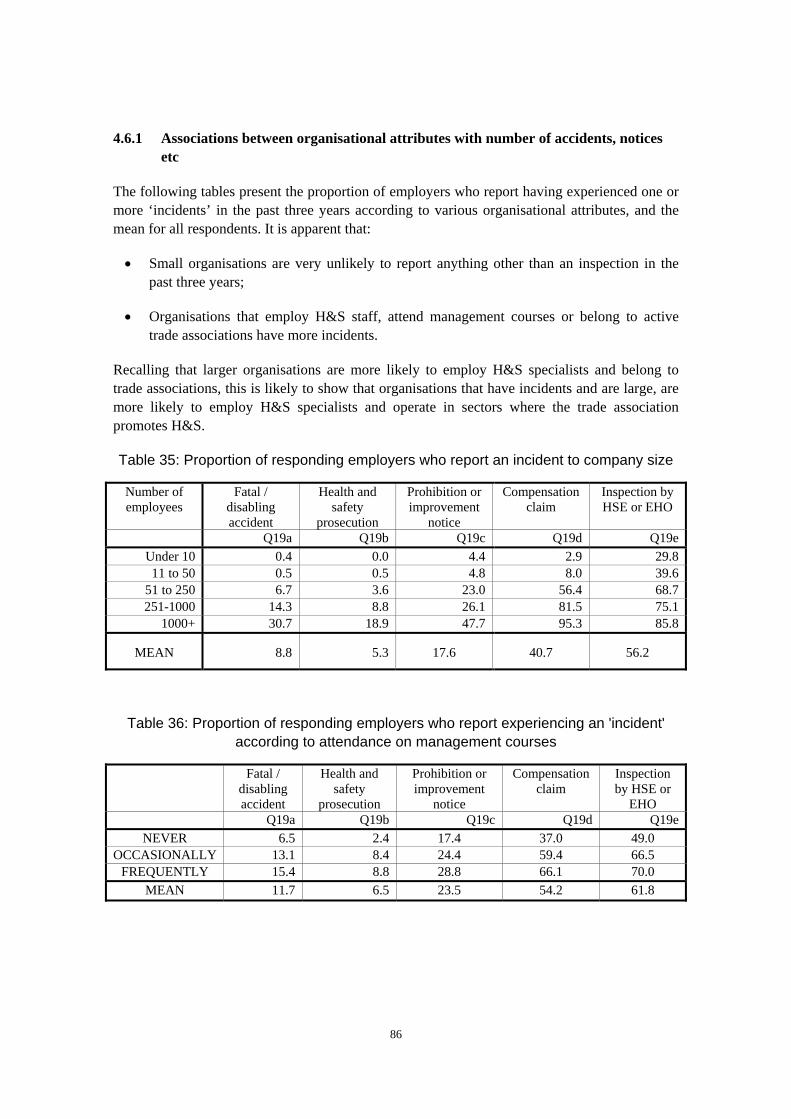

4.6.1 Associations between organisational attributes with number of accidents, notices etc .....86

4.7 EMPLOYERS VIEW OF NEW INCENTIVES ....................................................................................89

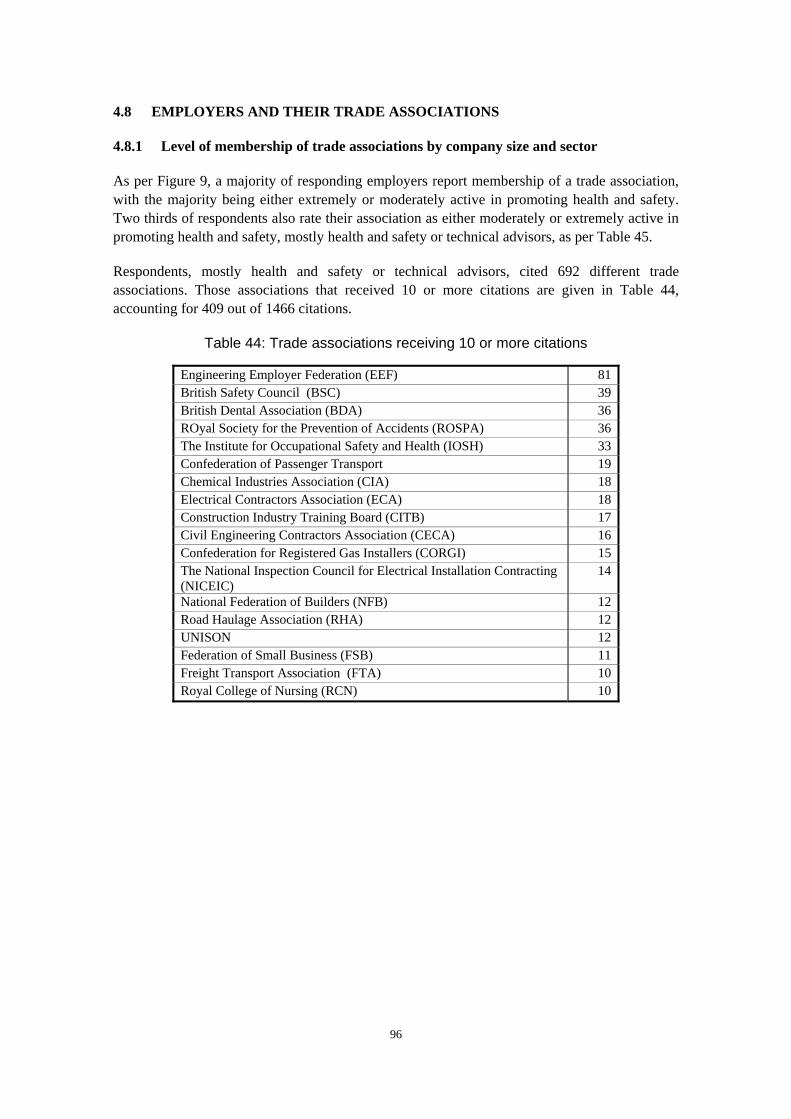

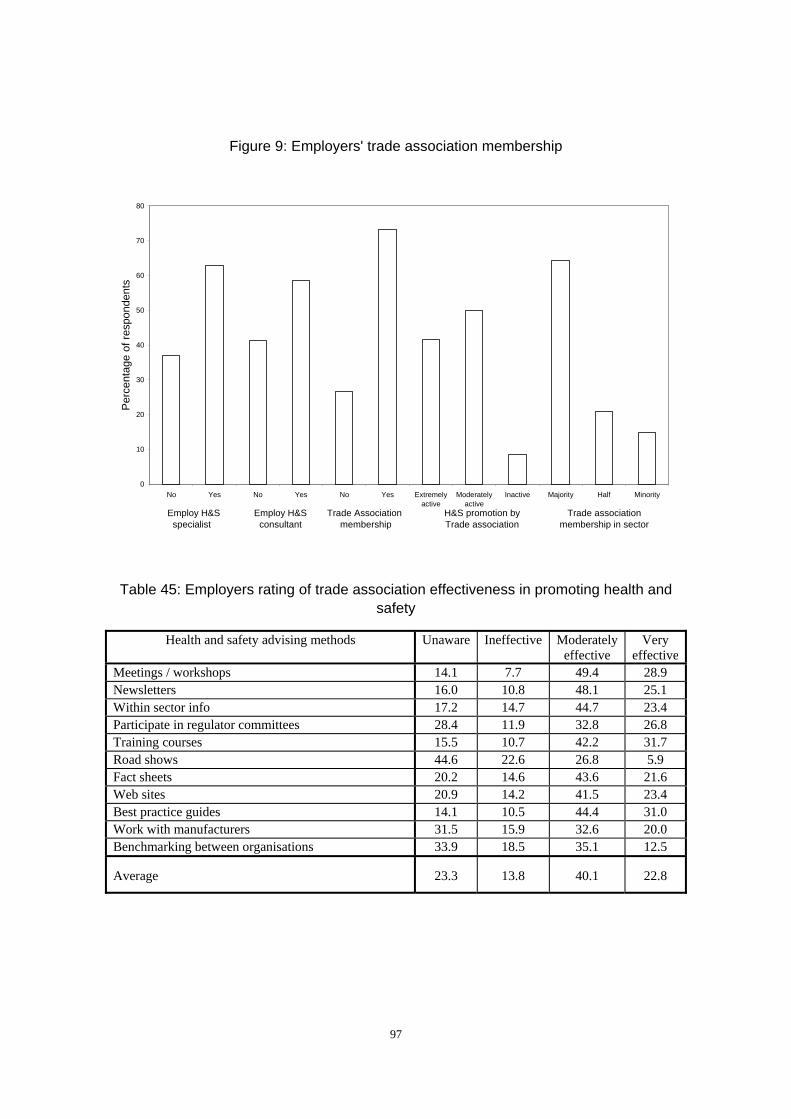

4.8 EMPLOYERS AND THEIR TRADE ASSOCIATIONS........................................................................96

4.8.1 Level of membership of trade associations by company size and sector ............................96

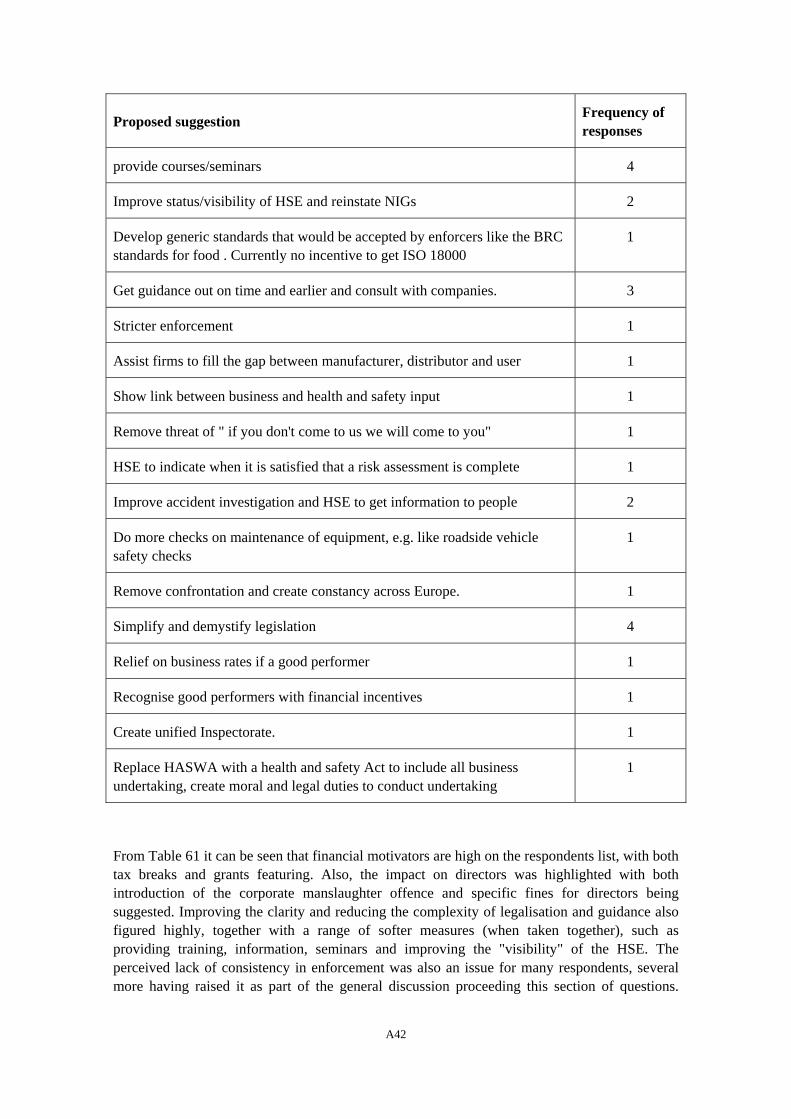

4.9 FREE TEXT SUGGESTIONS AND COMMENTS...............................................................................98

4.9.1 Introduction ........................................................................................................................98

4.9.2 HSE under resourcing ........................................................................................................98

4.9.3 The number of HSE regulations and complexity ................................................................98

4.9.4 Directors being qualified in health and safety....................................................................99

4.9.5 Availability of H&S resource materials, publications and services ...................................99

4.9.6 International occupational health and safety standards.....................................................99

4.9.7 Guidance.............................................................................................................................99

4.9.8 Whistle blowers ................................................................................................................100

5 ANALYSIS OF INTERMEDIARIES’ RESPONSES................................................................101

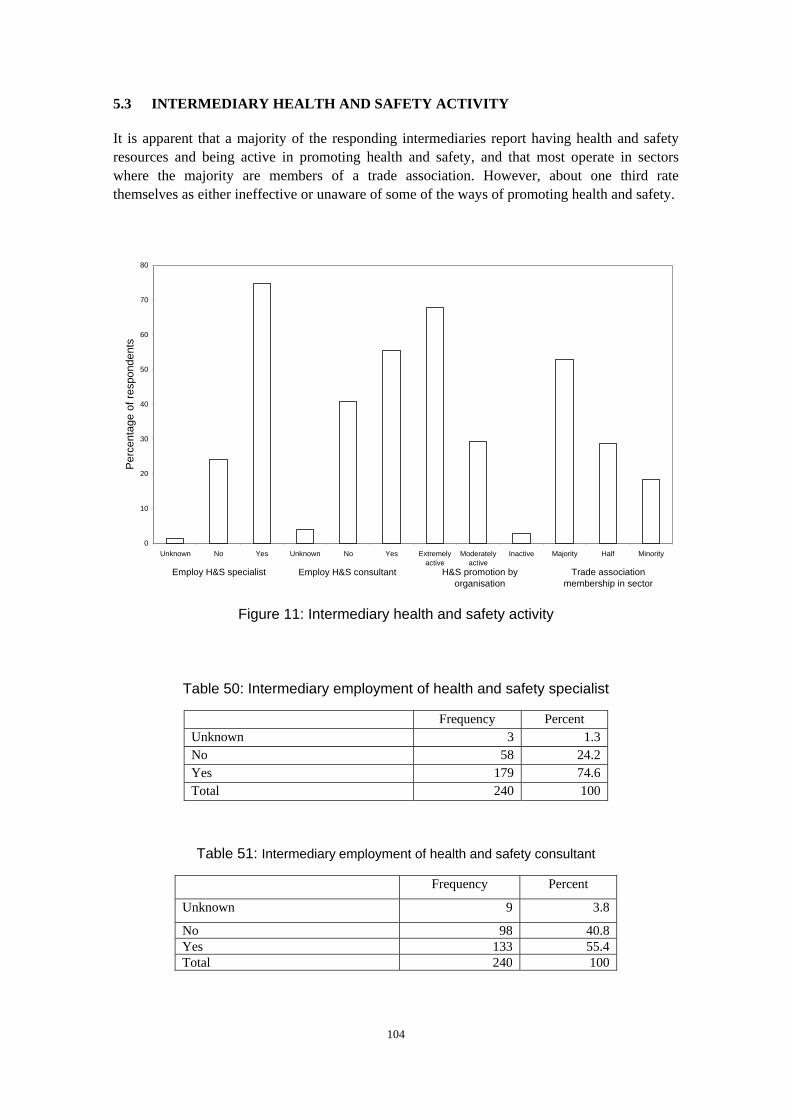

5.1 OVERVIEW .............................................................................................................................101

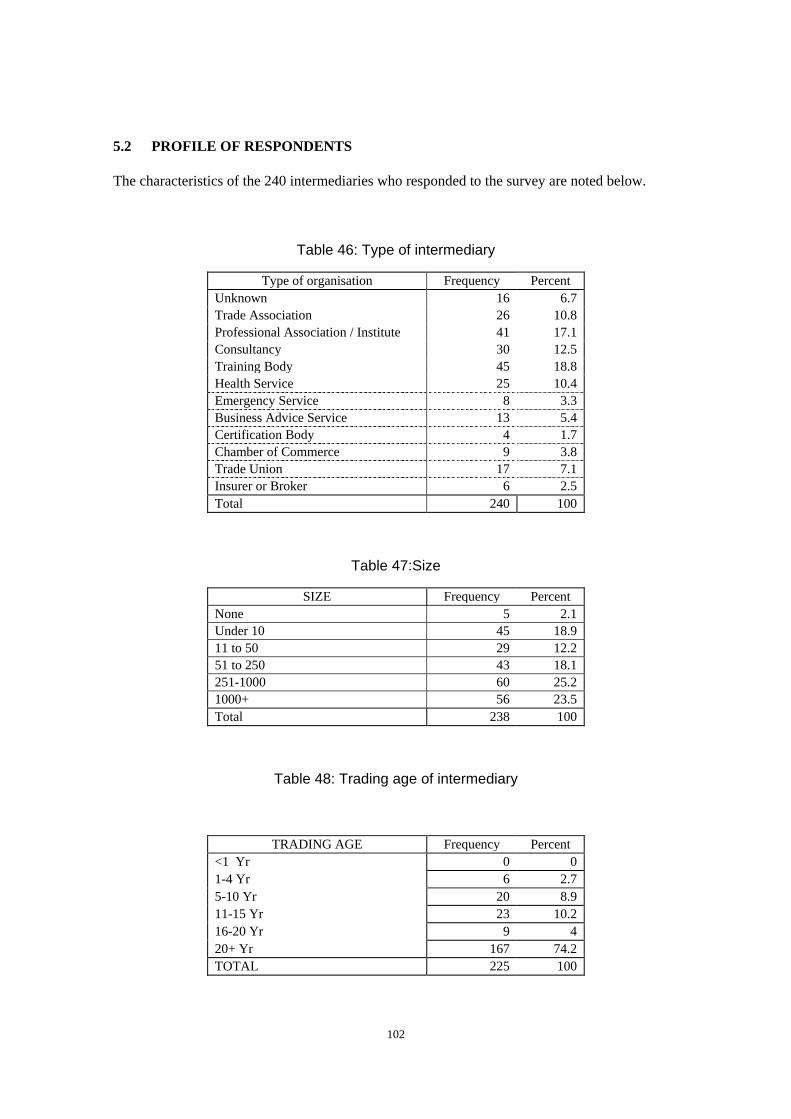

5.2 PROFILE OF RESPONDENTS .....................................................................................................102

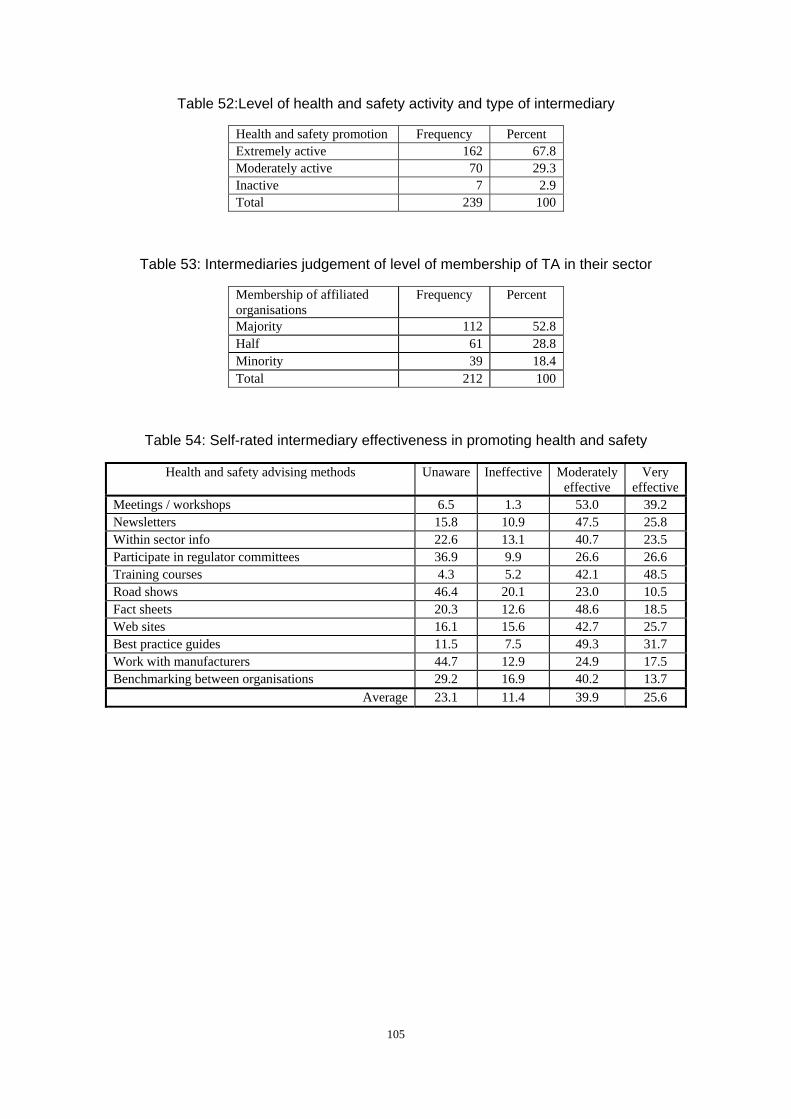

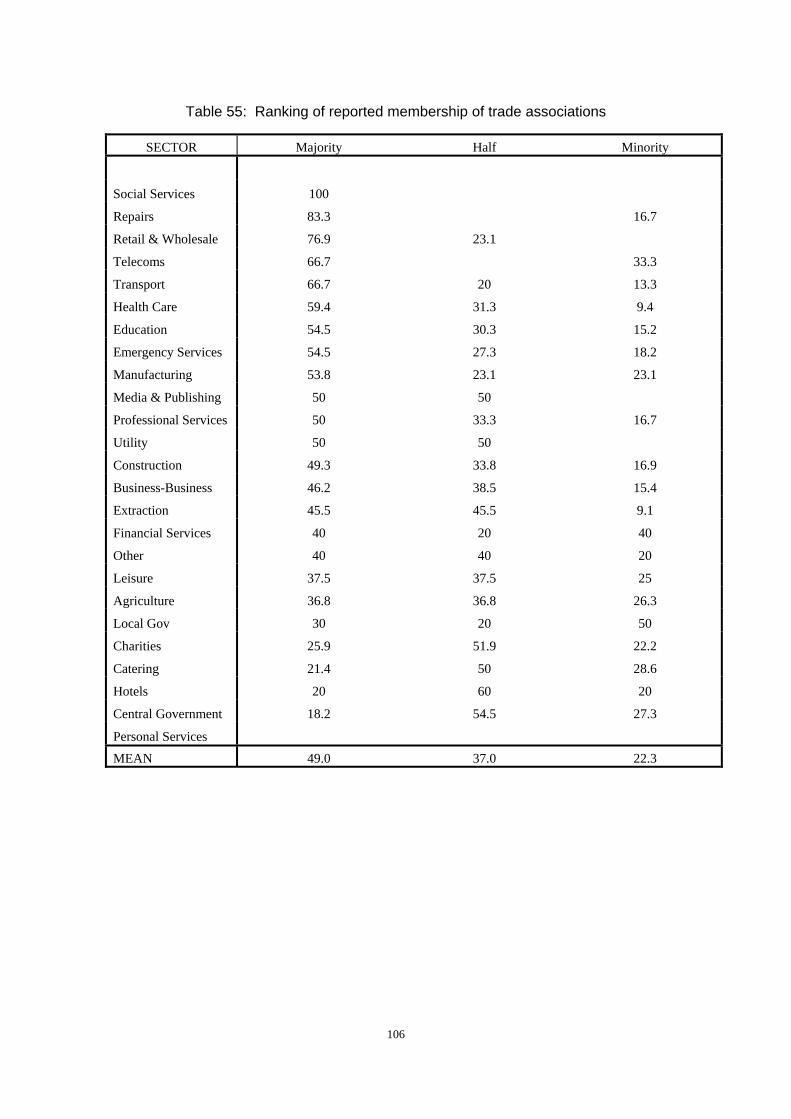

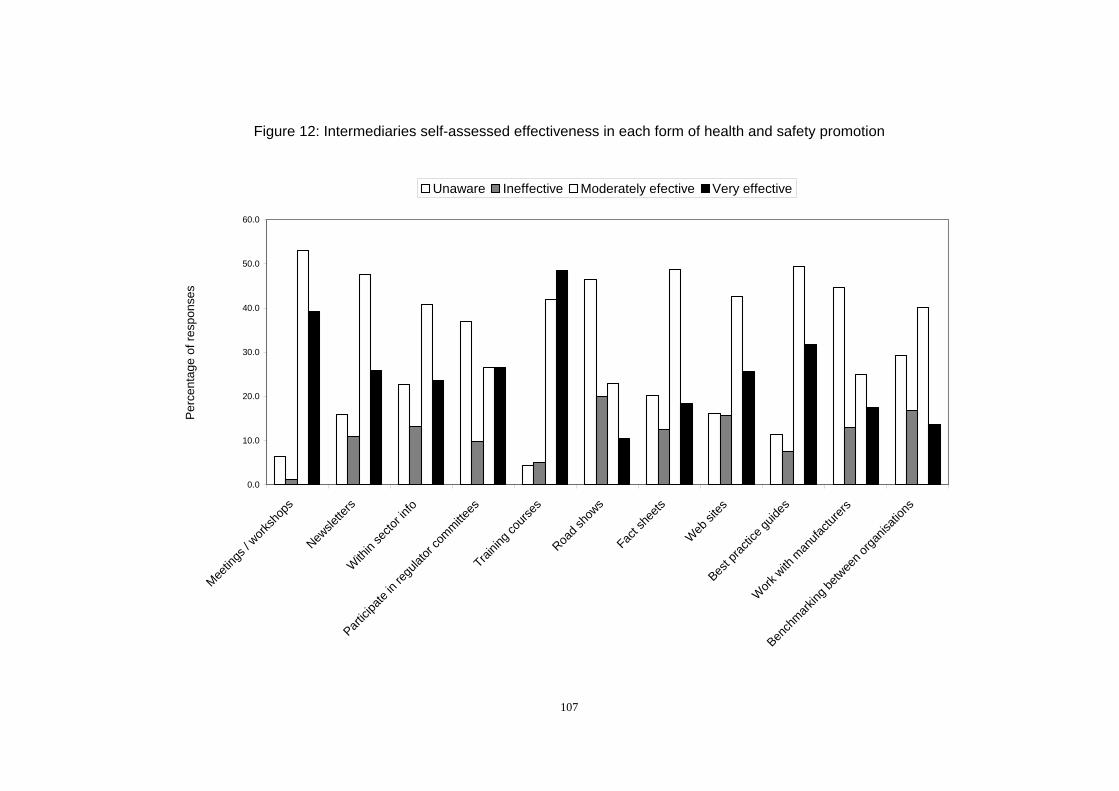

5.3 INTERMEDIARY HEALTH AND SAFETY ACTIVITY ....................................................................104

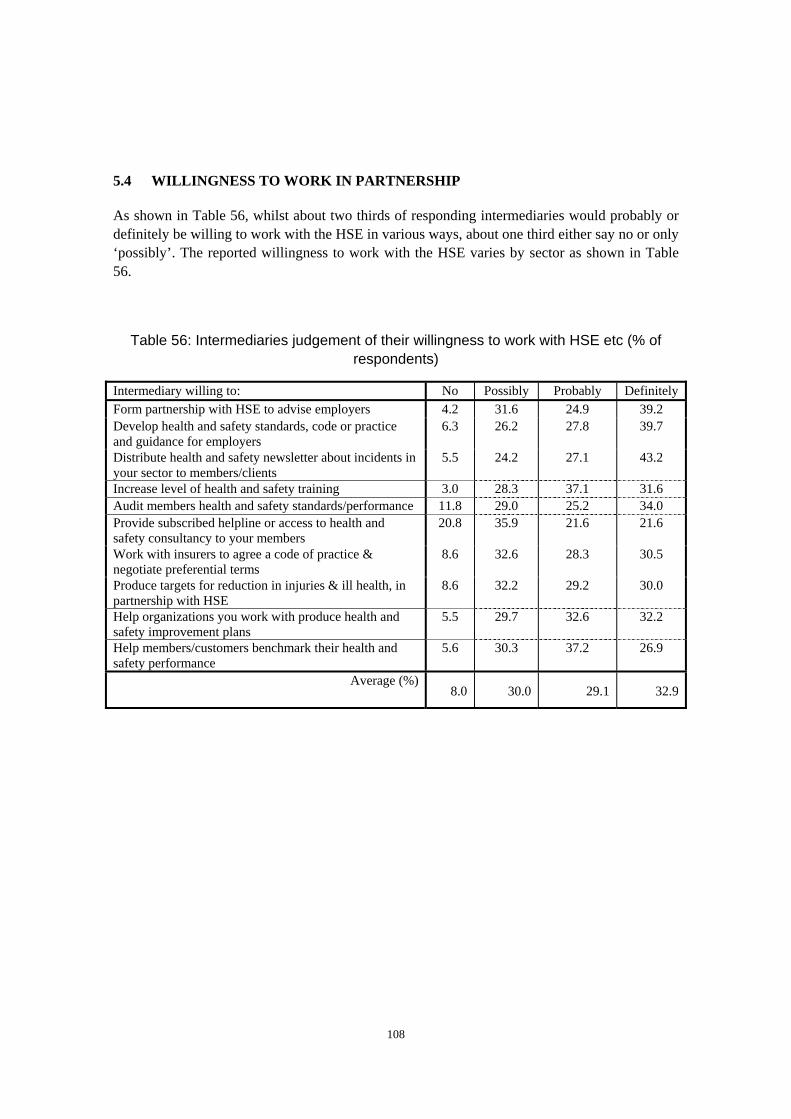

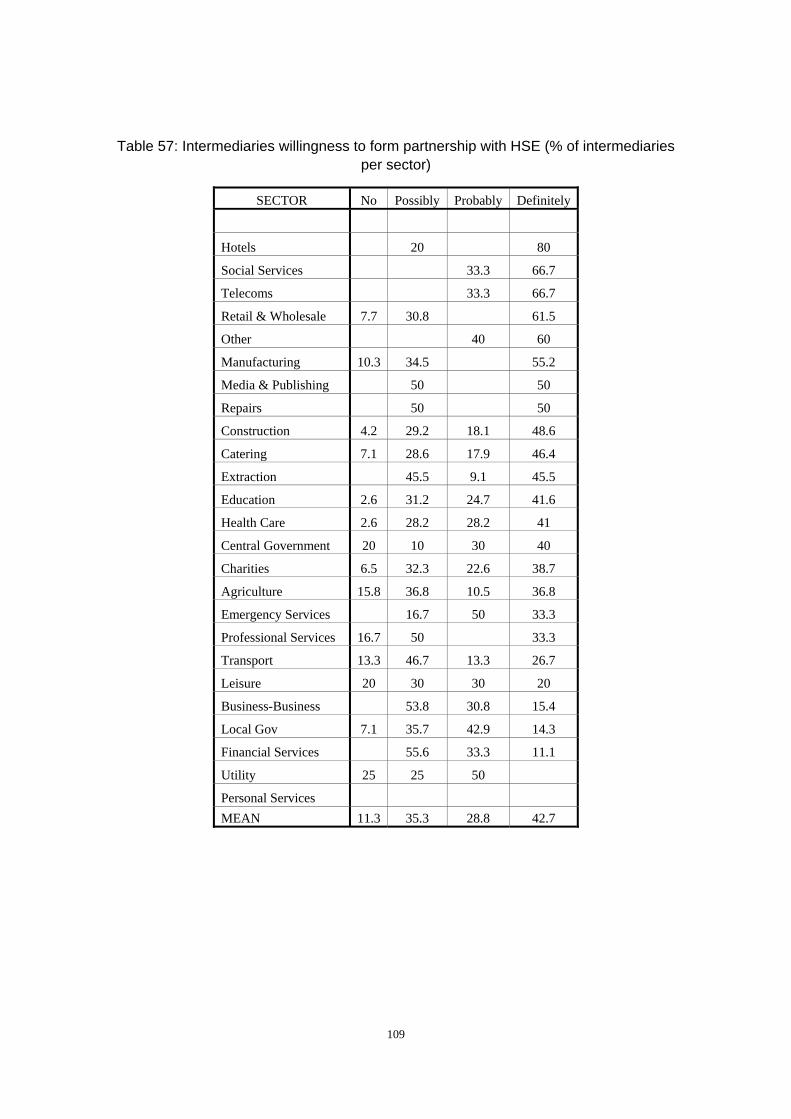

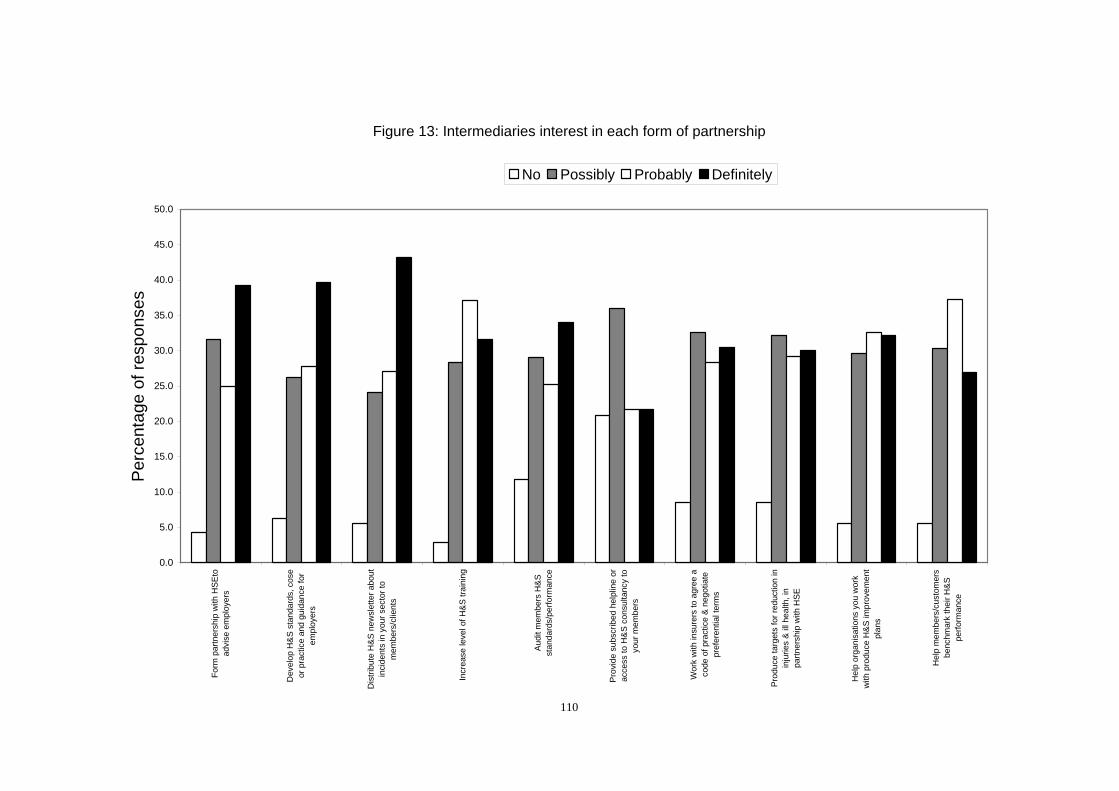

5.4 WILLINGNESS TO WORK IN PARTNERSHIP...............................................................................108

5.5 FREE TEXT COMMENTS AND SUGGESTIONS.............................................................................111

6 DISCUSSION OF FINDINGS .....................................................................................................112

6.1 OVERVIEW .............................................................................................................................112

6.2 ASSOCIATION OF ATTITUDES WITH PREFERRED INTERVENTIONS ............................................112

6.2.1 Associations......................................................................................................................112

vi

6.2.2 Implications for targeting.................................................................................................114

6.3 STRATEGY FOR COMPLIANCE .................................................................................................117

6.3.1 Advice and guidance: the role of the HSE........................................................................117

6.3.2 Advice and guidance: the role of intermediaries..............................................................118

6.3.3 The business case for health and safety............................................................................119

6.3.4 Enforcement......................................................................................................................121

6.3.5 Encouraging rehabilitation ..............................................................................................122

6.4 DISPARITIES IN THE PERCEPTION OF HEALTH AND SAFETY .....................................................122

6.5 CONCLUSIONS ........................................................................................................................123

6.5.1 Factors motivating health and safety improvements ........................................................123

6.5.2 New levers for health and safety.......................................................................................123

6.5.3 Segmenting organisations.................................................................................................124

7 REFERENCES..............................................................................................................................125

8 APPENDIX A: PROFORMA FOR EXPLORATORY DISCUSSIONS......................................1

9 APPENDIX B: OVERVIEW OF EXPLORATORY DISCUSSIONS FEEDBACK ..................8

9.1 TRADE ASSOCIATION AND SECTOR BASED ACTIVITY ..................................................................8

9.1.1 Profile ...................................................................................................................................8

9.1.2 Health and safety activity .....................................................................................................9

9.1.3 Current health and safety issues.........................................................................................10

9.2 RELATIONSHIPS WITH REGULATORS.........................................................................................10

9.3 RESPONSE TO NEWS OF SAFETY ISSUES ....................................................................................12

9.3.1 Hearing about incidents .....................................................................................................12

9.3.2 Response to hearing about prosecution / improvement notices..........................................13

9.4 UNDERSTANDING AND PERCEPTION OF HEALTH AND SAFETY RISKS.........................................15

9.4.1 Level of understanding of health and safety between sectors .............................................15

9.4.2 Perception of risk................................................................................................................16

9.4.3 Overall risk.........................................................................................................................17

9.5 UNDERLYING DRIVERS FOR HEALTH AND SAFETY ....................................................................18

9.5.1 Good for business ...............................................................................................................18

9.5.2 A critical business success factor .......................................................................................18

9.5.3 An important aspect of ensuring staff productivity and morale..........................................19

9.5.4 A moral duty .......................................................................................................................19

9.5.5 Something you do just because of regulations....................................................................19

vii

9.6 THE COSTS AND BENEFITS OF HEALTH AND SAFETY .................................................................20

9.6.1 Value or burden?................................................................................................................20

9.6.2 The business case................................................................................................................21

9.7 IMPACT OF THE INSURANCE MARKET/INDUSTRY ......................................................................21

9.8 REPUTATIONAL RISK ................................................................................................................22

9.9 FEAR OF ENFORCEMENT ACTION ..............................................................................................27

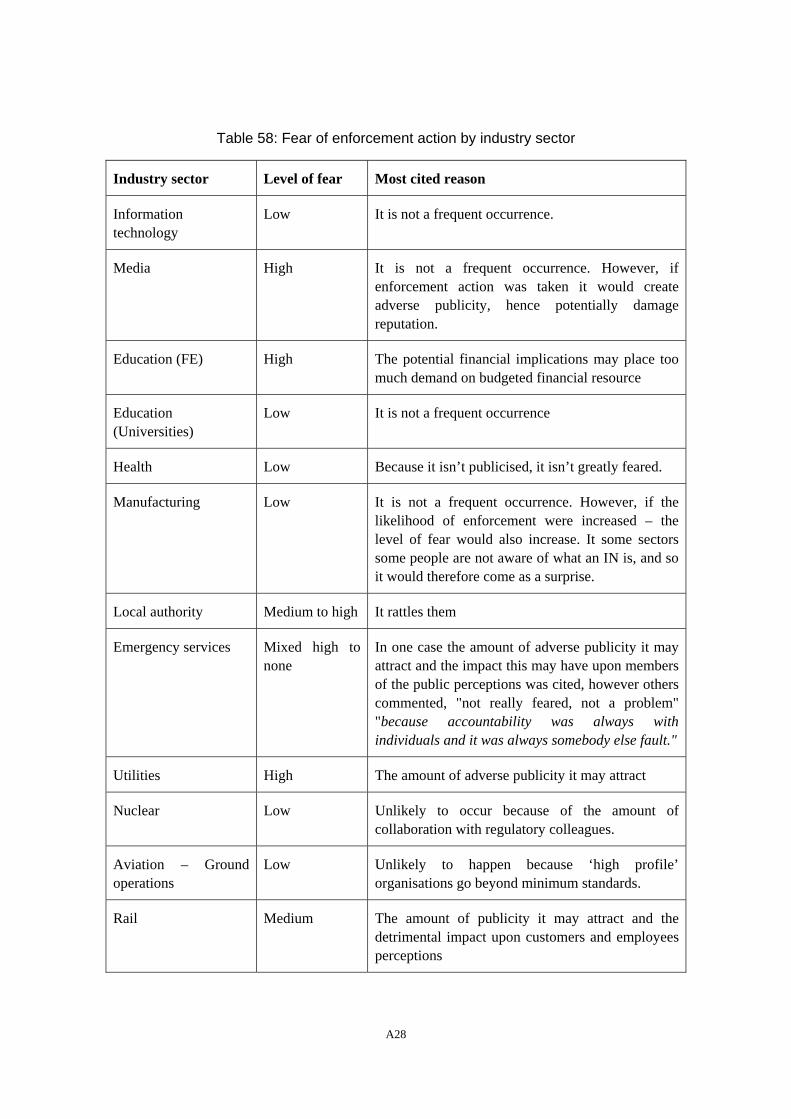

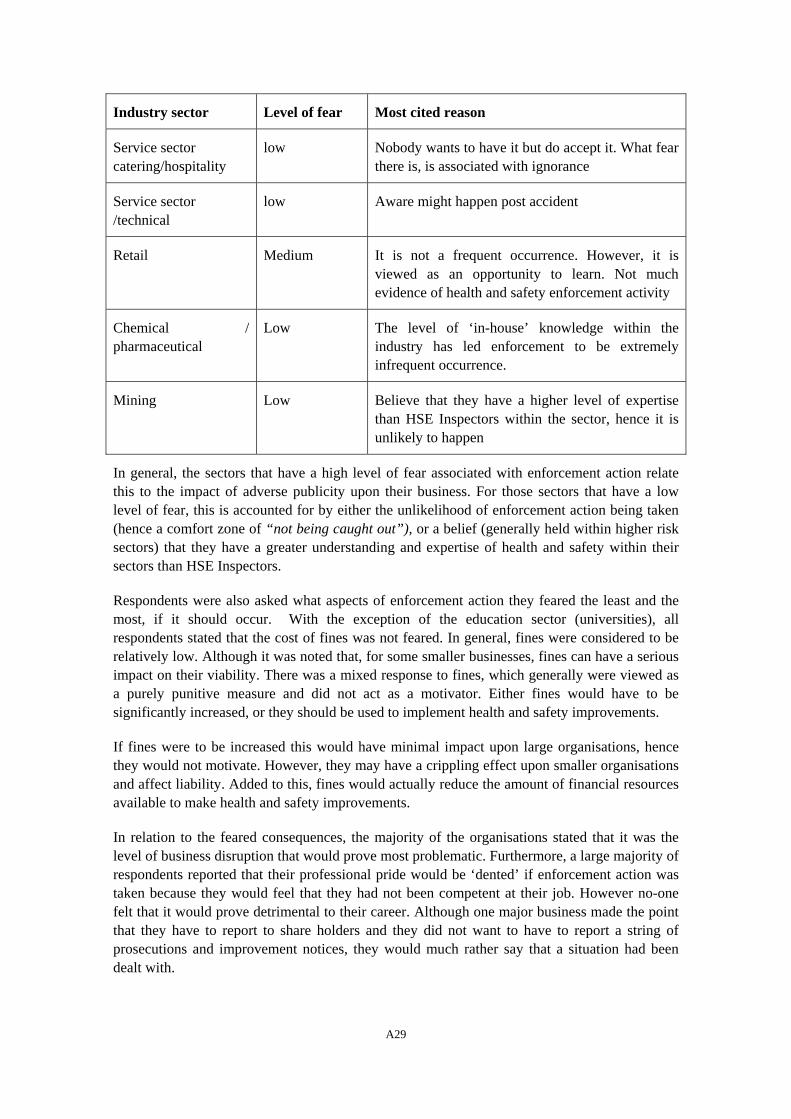

9.9.1 Fear of enforcement............................................................................................................27

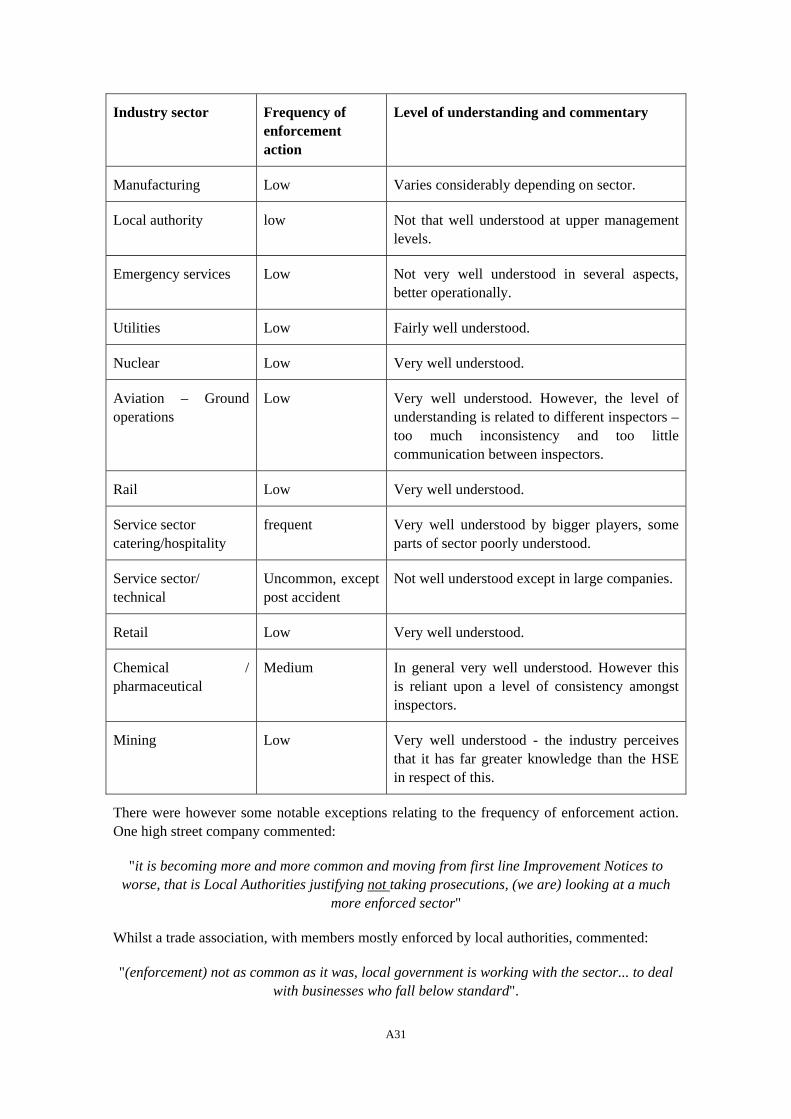

9.9.2 Frequency and level of understanding of enforcement action ............................................30

9.9.3 Effectiveness of enforcement action....................................................................................32

9.9.4 Enforcement action as a yard stick.....................................................................................33

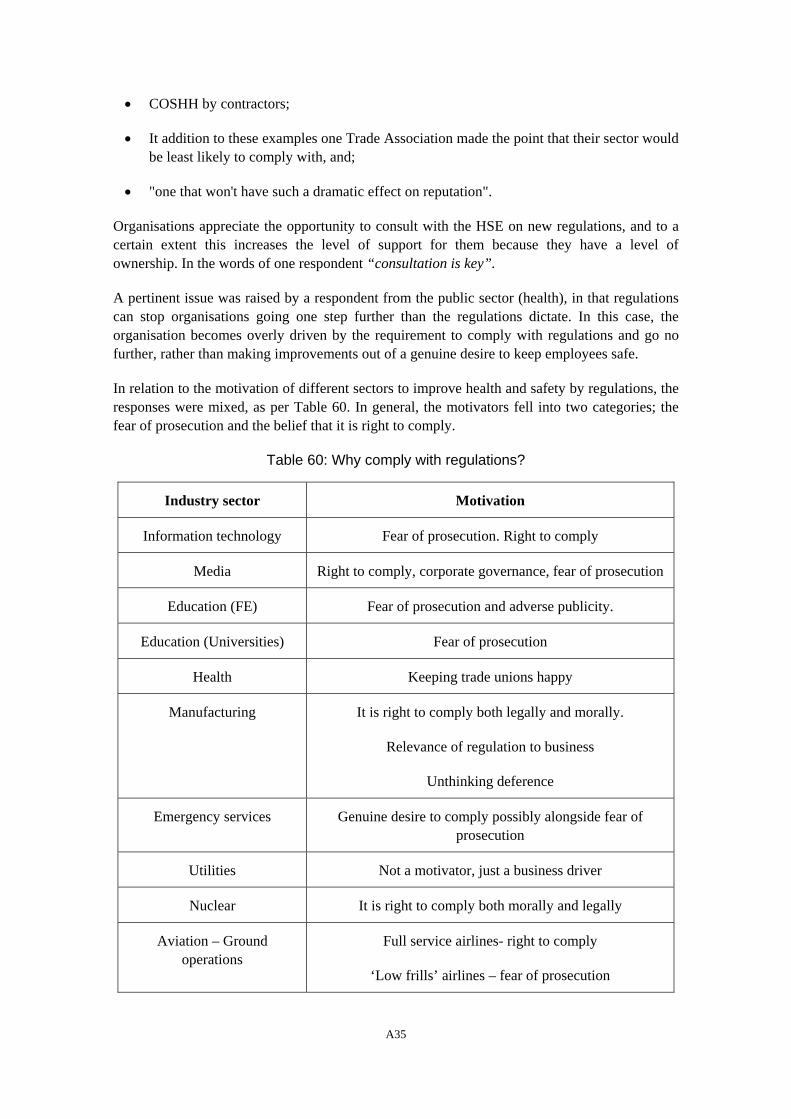

9.10 THE ROLE OF REGULATIONS .....................................................................................................34

9.11 THE MORAL CASE.....................................................................................................................37

9.12 WHY DO ORGANISATIONS AND SECTORS DIFFER IN THEIR VIEWS OF HEALTH AND SAFETY?.....38

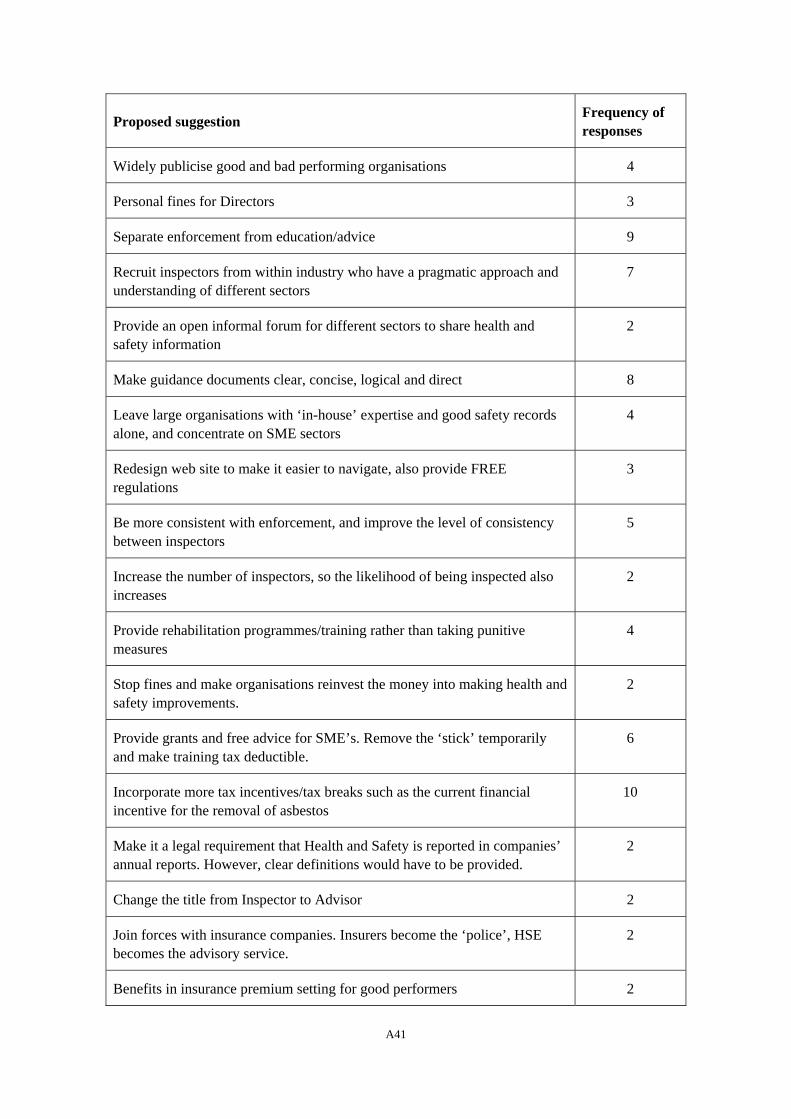

9.13 HOW FIRMS COULD BE BETTER MOTIVATED TO MANAGE HEALTH AND SAFETY .......................40

10 APPENDIX C: FINAL INTERMEDIARIES’ POSTAL QUESTIONNAIRES........................44

11 APPENDIX D: FINAL EMPLOYERS’ POSTAL QUESTIONNAIRES..................................56

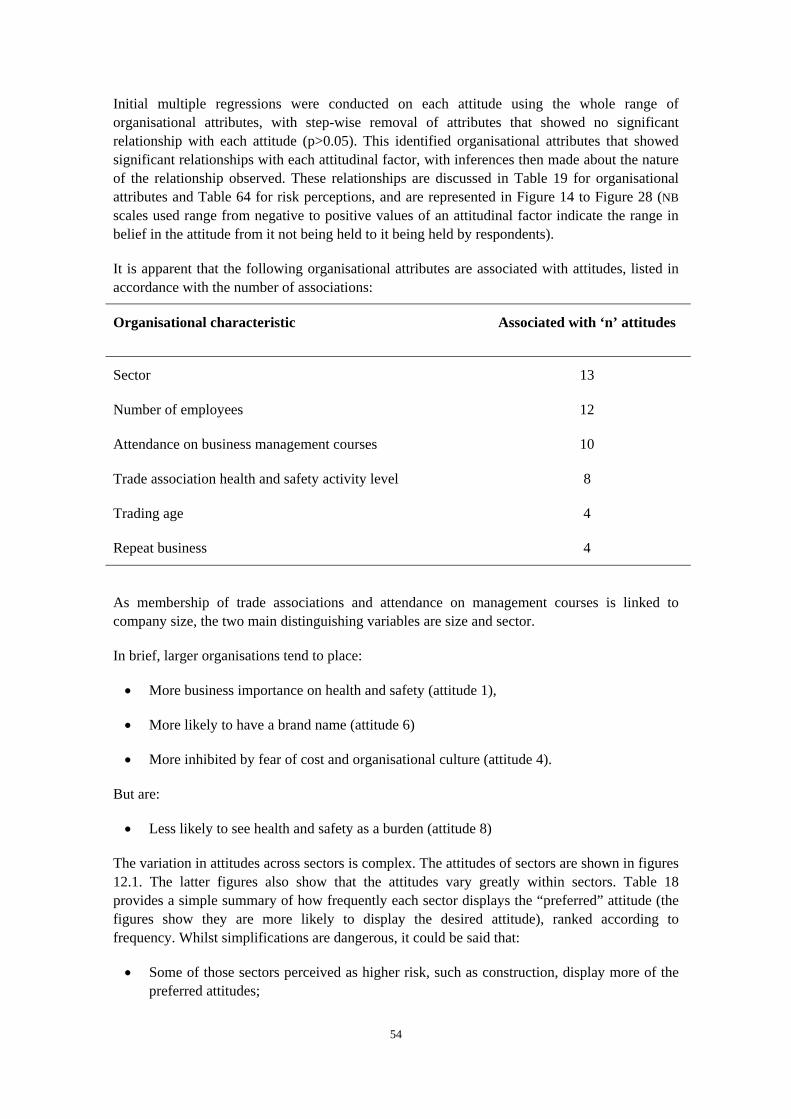

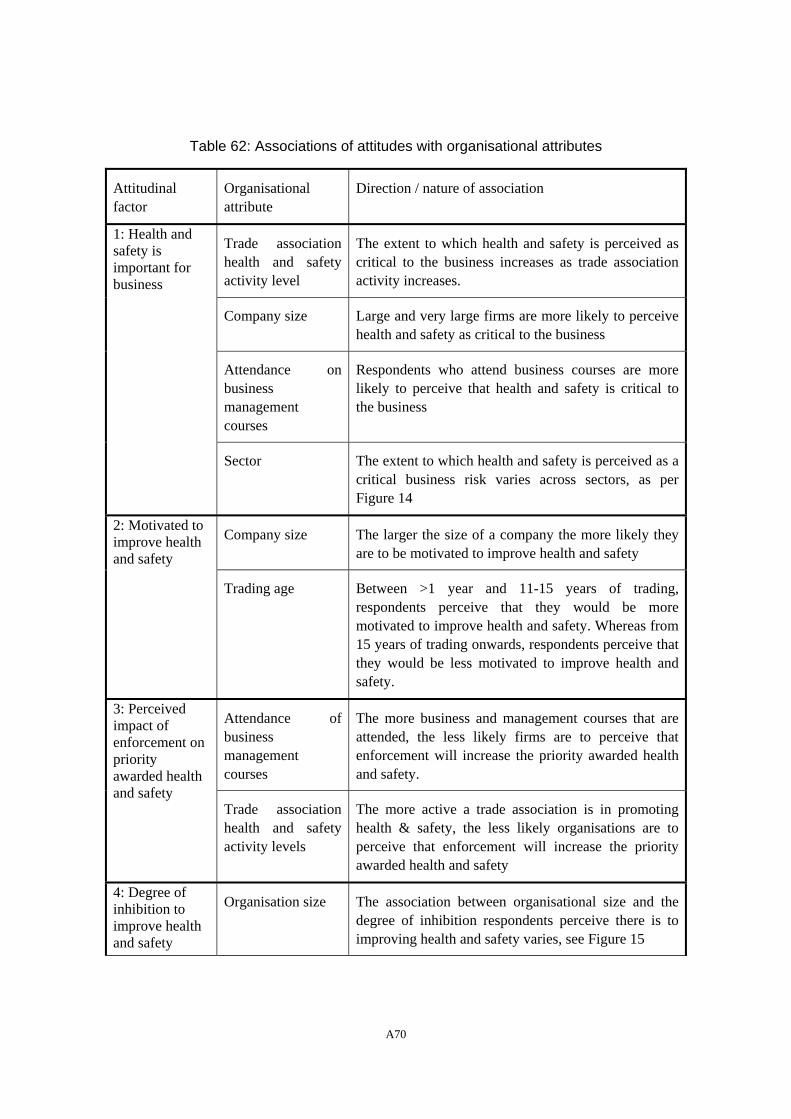

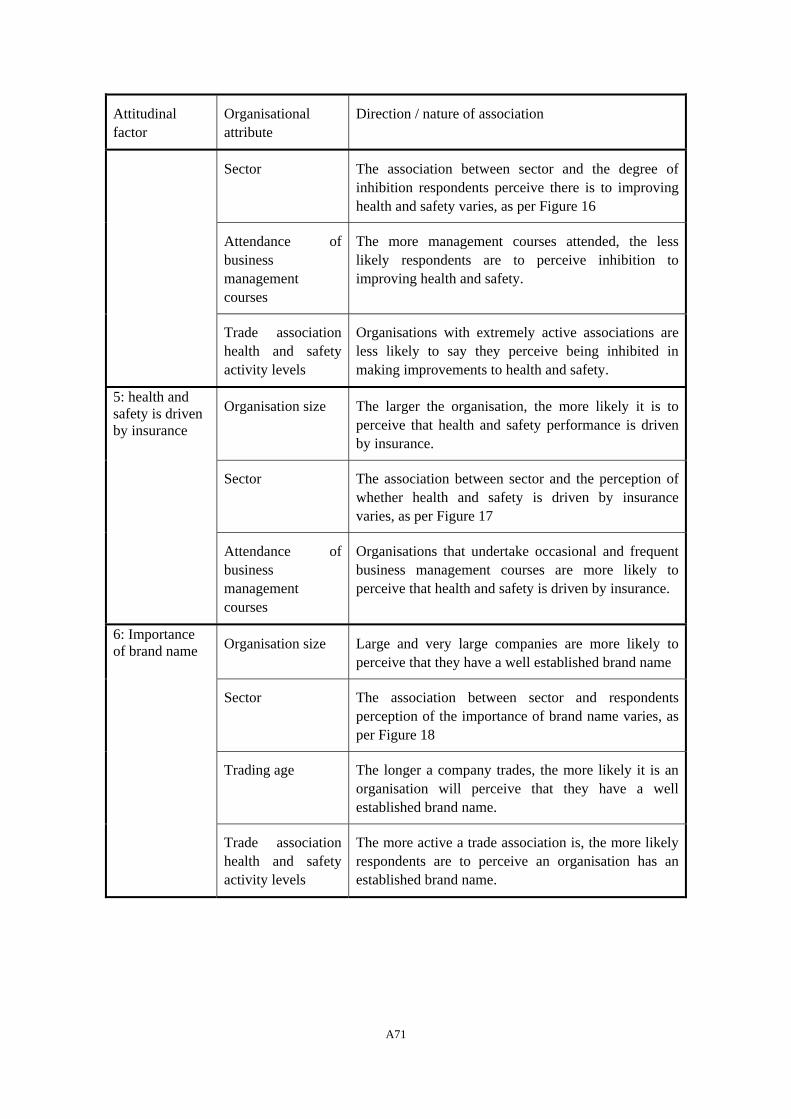

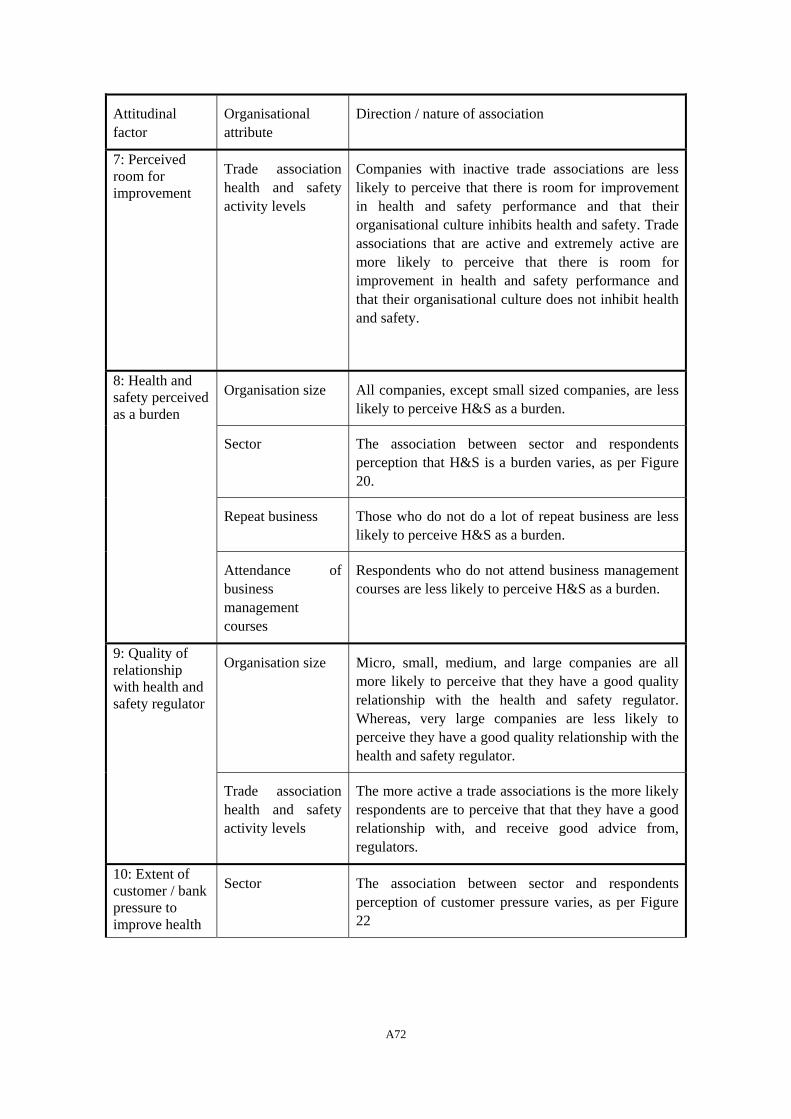

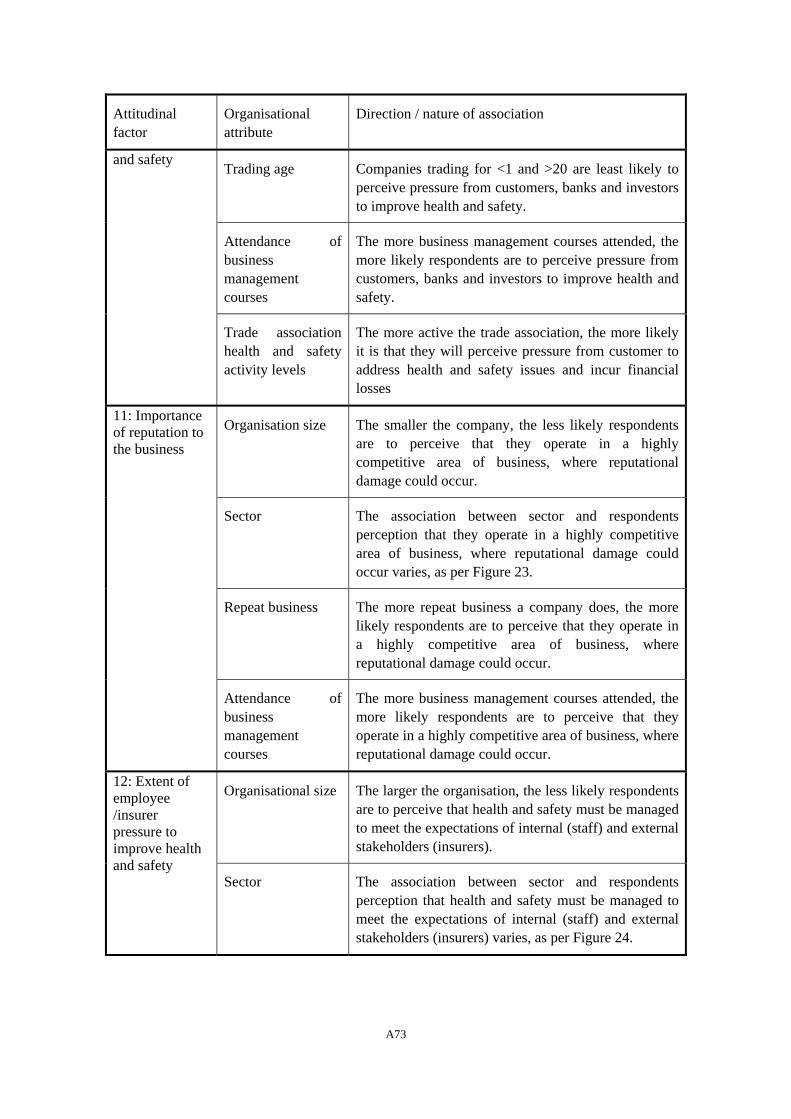

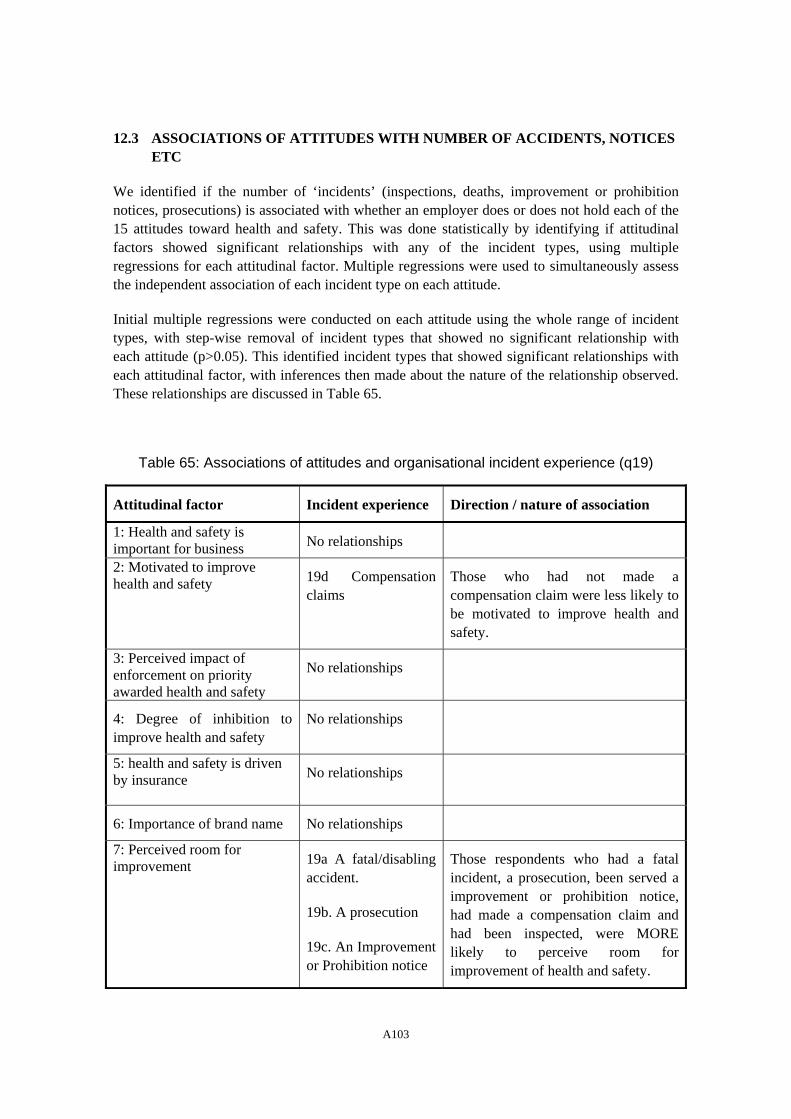

12 APPENDIX E: ASSOCIATION OF ATTITUDINAL FACTORS WITH OTHER FACTORS & ISSUES..................................................................................................................................................68

12.1 ASSOCIATIONS OF ATTITUDES WITH ORGANISATIONAL ATTRIBUTES........................................69

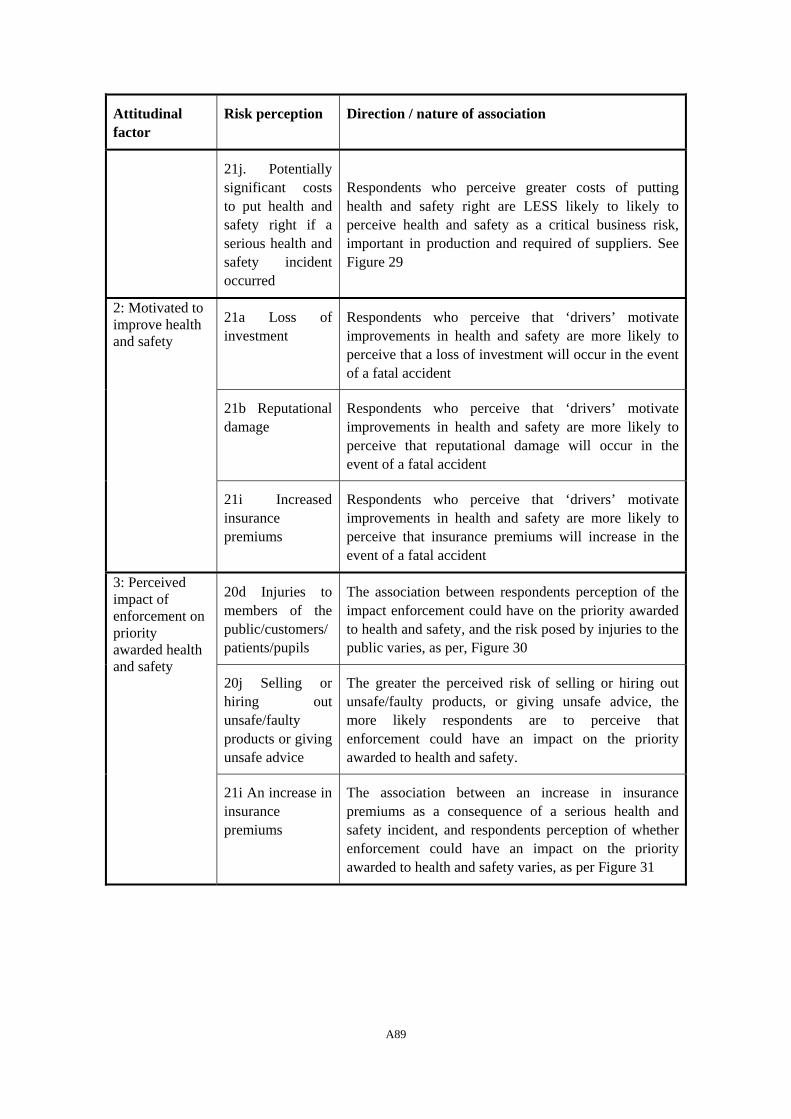

12.2 ASSOCIATIONS OF ATTITUDES WITH RISK PERCEPTIONS ...........................................................88

12.3 ASSOCIATIONS OF ATTITUDES WITH NUMBER OF ACCIDENTS, NOTICES ETC ...........................103

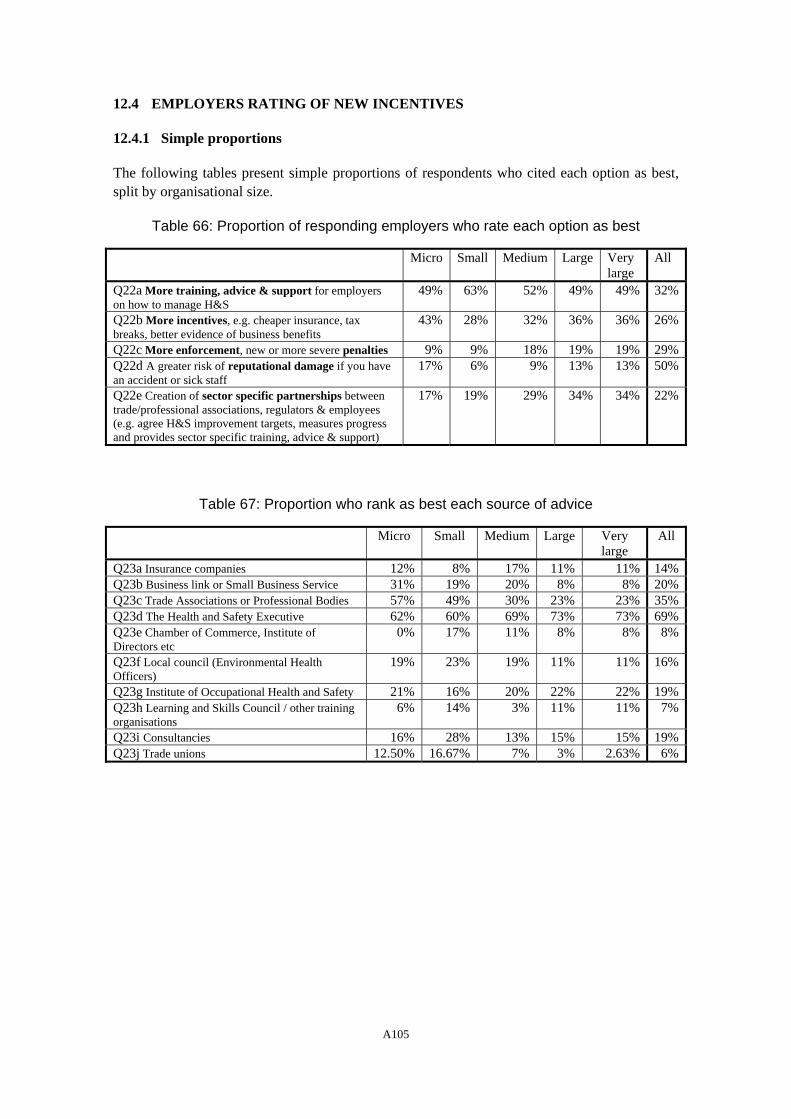

12.4 EMPLOYERS RATING OF NEW INCENTIVES ..............................................................................105

12.4.1 Simple proportions ...........................................................................................................105

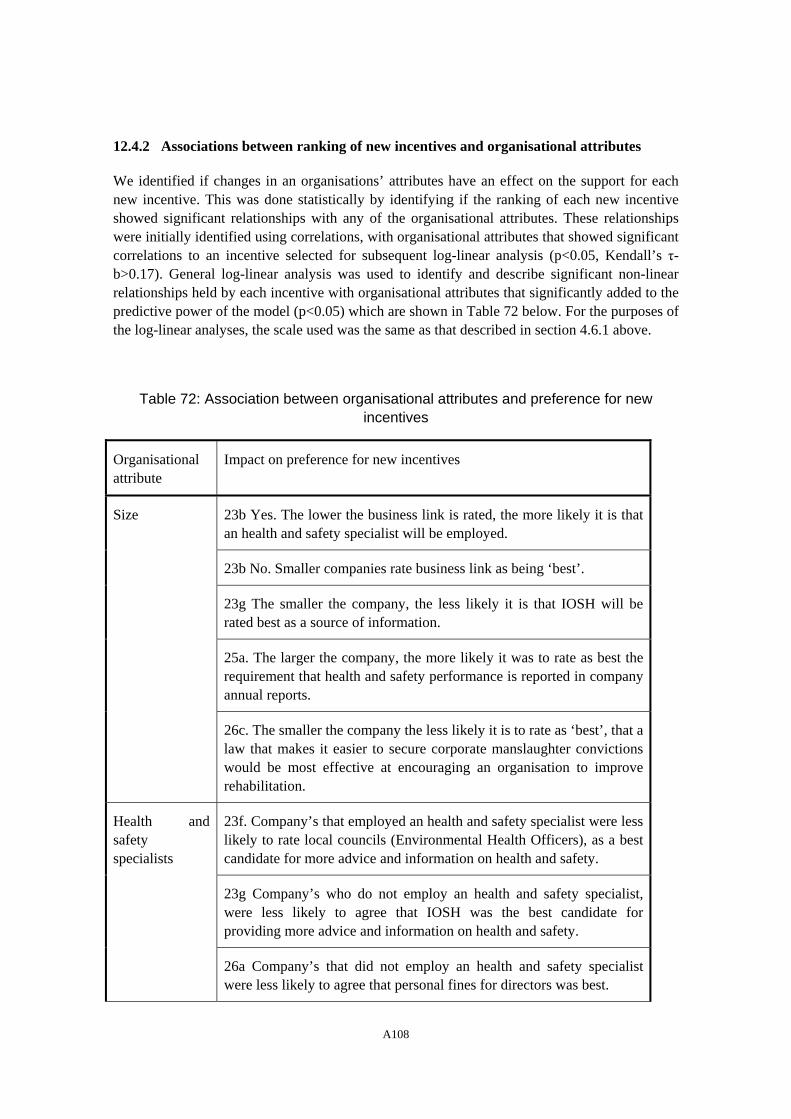

12.4.2 Associations between ranking of new incentives and organisational attributes...............108

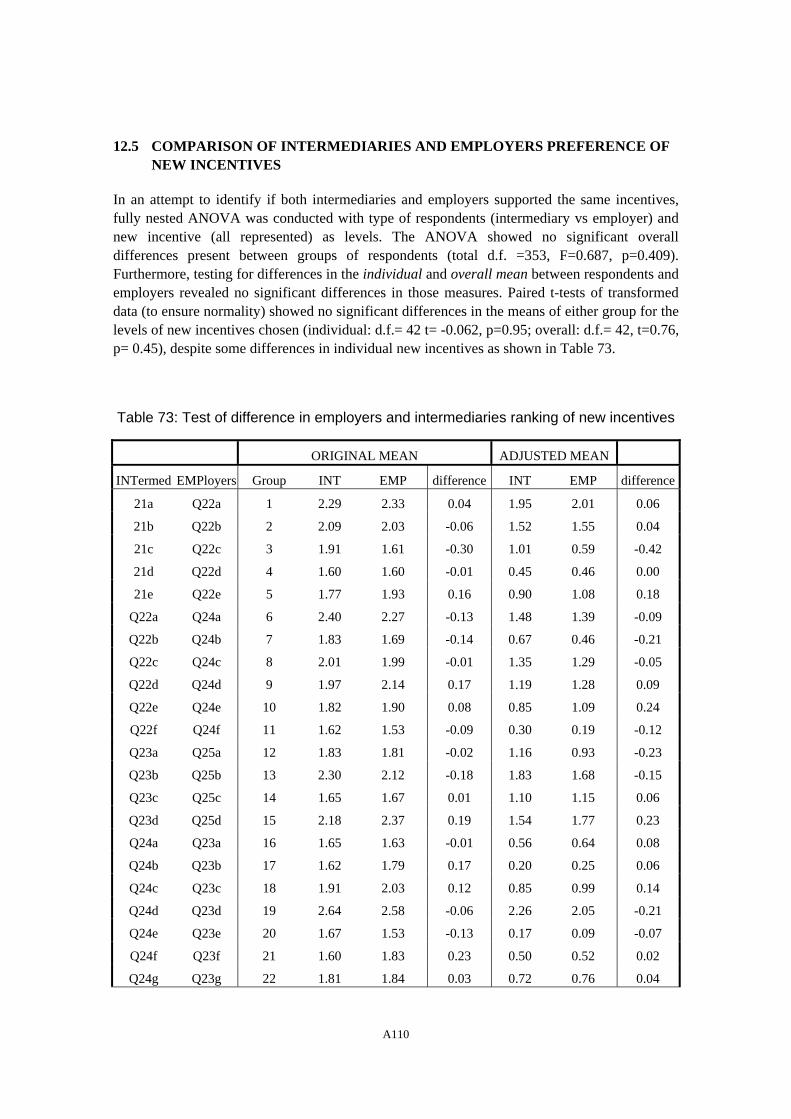

12.5 COMPARISON OF INTERMEDIARIES AND EMPLOYERS PREFERENCE OF NEW INCENTIVES.........110

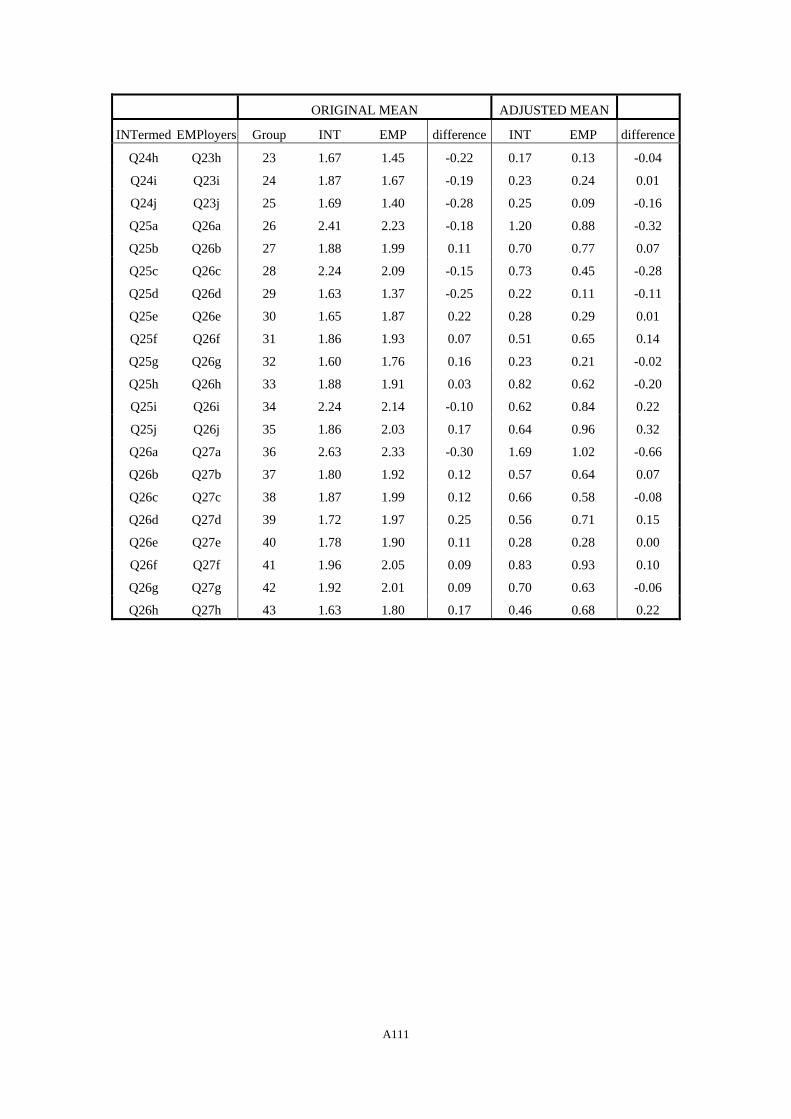

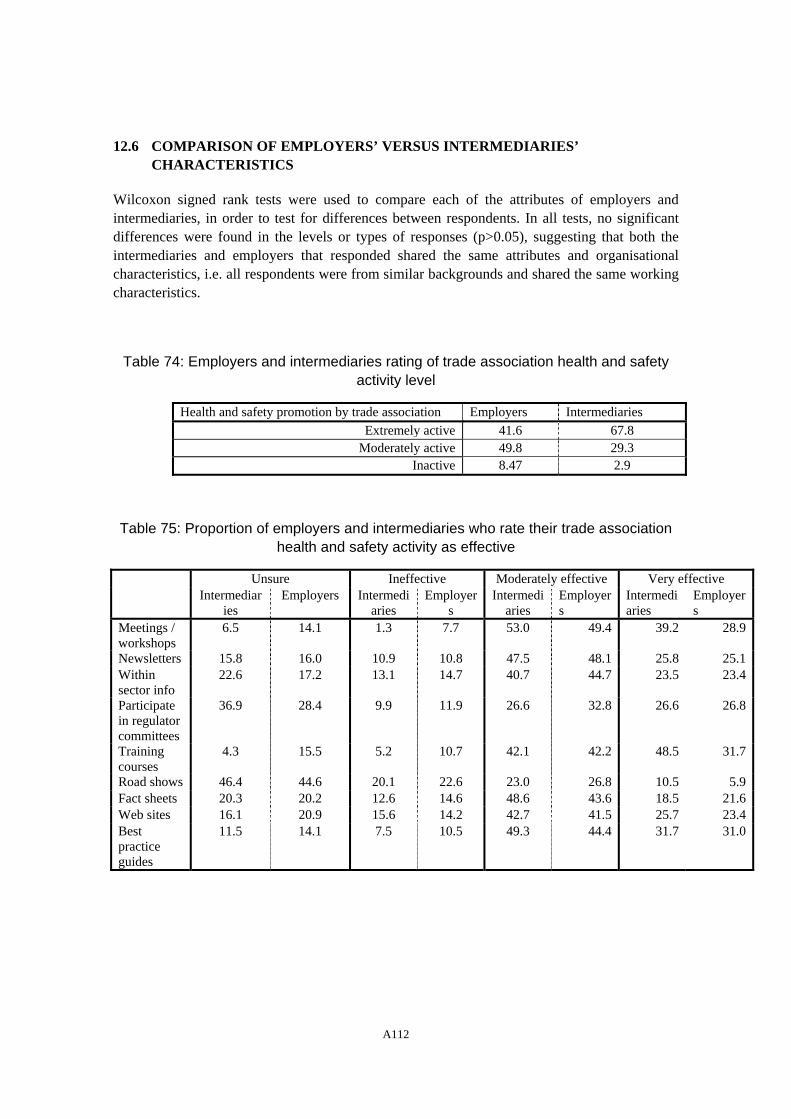

12.6 COMPARISON OF EMPLOYERS’ VERSUS INTERMEDIARIES’ CHARACTERISTICS........................112

viii

1 INTRODUCTION

1.1 BACKGROUND

The Revitalising Health and Safety (RHS) Action Plan incorporates many ideas suggested in consultation on how to achieve targets, such as fewer injuries. These ideas aim to build on the HSE’s existing strategy of encouragement, persuasion, assistance and enforcement. As discussed in Wright, Marsden and Antonelli (2004) past research lends support to many of the ideas laid out in RHS and elsewhere, particularly the idea of increasing access to advice and help, increasing concern for health and safety and reducing inhibitory factors.

Examples of new ideas about advice include:

• Help lines – low cost advisory service for SMEs;

• Working with partners, e.g. trade associations, business links and TECs;

• Working with other government departments, such as the Department of Health on occupational health;

• Increasing the role and reach of employee representatives, such as via roving workplace advisors;

• Developing more sector specific advice;

• Increasing the role of internet based advice and information;

• Education regarding health and safety in schools and colleges.

Examples of ideas to increase concern for health and safety include:

• Increasing supply chain pressure, such as including health and safety to a higher level in government procurement;

• Insurance & other financial incentives;

• Naming and shaming;

• Court mandated publicity of prosecutions;

• Novel penalties and restorative justice, such as court ordered administrative orders;

• Corporate manslaughter law;

• Higher levels of accident investigation and post-accident enforcement;

• Higher levels of inspection;

1

• More effective inspection, such as through the Enforcement Policy Statement aimed at achieving consistent enforcement practices amongst other things;

• Requiring company health and safety external reporting;

• Regulating Directors’ health and safety responsibilities.

Examples of ideas to reduce inhibitors include:

• Subsidies;

• Improving the presentation of economic argument by creating company specific examples of the costs and benefits of health and safety, and;

• The study into provision of an OH service for SMEs highlighted the possibility of considering tax breaks to encourage uptake of OH.

The study provides:

• An up to date review of research on the factors motivating compliance with health and safety;

• Empirical evidence on employers’ view of the HSE’s current approach, particularly the economic argument for compliance and the role of regulations and sanctions;

• Evidence about the relative merits of levers in different contexts, sectors, sizes of firms etc;

• New ideas on how to motivate compliance in the context of RHS and Securing Health Together.

The research provides an evidence base on which to propose “levers” in different contexts and to consider the likely impact of ideas within RHS and Securing Health Together.

Past research

Previous research on the factors that motivate employers to comply or not comply with health and safety was compiled and reviewed in 1998 (Wright 1998) and more recently by Wright, Marsden and Antonelli (2004). These reviews, particularly the latter one provide an overview of motivational factors. They indicate that the main drivers for health and safety in the 1990’s have included:

• Regulations and enforcement;

• Financial and business benefits;

• Reputational risk;

• The moral case.

Recent research (Wright, Marsden and Antonelli, 2004) on motivational factors indicate, on balance, that:

2

• The incentive created by Employers’ Liability insurance premiums has grown due to the cost increases;

• There is mixed evidence about the extent to which employers believe that the business benefits of health and safety outweigh the costs;

• It is also clear from past research that the perceived cost and affordability of health and safety can inhibit improvements;

• The general perception of occupational health and safety as being something that boards need to manage as a potential risk to the organisation has grown, due to general increase in pressure from the regulator and other stakeholders;

• There is mixed evidence about whether there has been an increase in supply chain pressure for health and safety;

• The ‘compliance’ oriented and regulation driven attitude of organisations remains significant, and;

• The need for increased education and awareness remains significant.

Thus, motivational factors can be split into (1) factors that prompt concern, (2) mediating factors that moderate action especially affordability of health and safety, and (3) factors that enable action including awareness and knowledge of health and safety.

At times research has provided what at first appears to be conflicting findings, where for example, studies alternately report reputational risk or regulatory compliance as the main drivers, whilst others report that employers are not driven by the business case to manage H&S but nonetheless recommend that the business case is demonstrated in order to provide a “self-interest” for compliance. For example, loss of credibility (Hillage et al 2001) is reported to be the most influential factor together with the idea of moral necessity (belief in), which promotes a need to comply with the law. On the other hand it is reported that reviews of specific legislation generally concluded that compliance with the law was the most important reason that employers took actions to improve their health and safety practices and procedures (e.g. Honey et al., 1996b, Lancaster et al. 2001).

Other studies have suggested that enforcement has a specific deterrence effect on the firm acted upon but that enforcement does not have an industry wide preventive impact (McCaffrey, 1983, Ruser and Smith, 1991 and Smith, 1979 – quoted in Johnstone 2003). More recently Baggs etc al (2003) report (quoted in Johnstone 2003) that “enforcement visits may trigger a re-shuffling of managerial priorities and a greater attention to safety...”, suggesting specific deterrence goes beyond the narrow focus of the inspection. Johnstone (2003) suggests that the “rather confusing empirical evidence suggests that deterrence has some effect in the case of corporate, although it does not work across the board..”(p14).

Also, whilst previous reviews have indicated that many employers are motivated by the need to comply with regulations and the prospect of enforcement action, it was unclear what underlay the perceived need to comply and avoid enforcement. Hillage et al (2001) found that:

3

“among SMEs the threat of prosecution can raise awareness and understanding of workplace risks and can lead to the adoption of better health and safety practices. ….. The evidence therefore seems to suggest that there are at least two related factors at work here:

• the fear of being taken to court and/or receiving claims for compensation if found to be in breach of the law;

• the acceptance that the law is an expression of what should be done and that there is a moral duty to meet it.”

(quoted from Hillage et al 2001).

However, there was little hard evidence to clarify these points. Also, in this context the perceived seriousness of the hazard is important. If employers accept that a hazard poses a serious risk they appear more likely to respond to new health and safety requirements and guidance on the grounds that there is a substantive moral case to safeguard employees’ health and safety. It is unclear whether employers are motivated to comply with regulations for fear of the immediate costs arising from sanctions such as fines, especially given the perceived low probability of prosecution and (usually) low cost of a fine.

The differences in research findings may arise for a number of reasons. First, it is possible that the importance of various factors has changed over time due to changes in socio-economic and regulatory processes. For example, there is some evidence that the importance of insurance as a driver for H&S has changed since the 1990s. Whilst earlier studies rarely cited insurers or the desire to reduce employers’ liability premiums as a driver for H&S, studies completed since the 2002 price rises present a very different picture.

Secondly, it is possible that some factors are intertwined. If any one study focuses on (say) the role of regulation, the study may report regulation as the main driver. Another study may focus on reputational risk and report this to be the main driver. If reputational risk and regulation compliance are intertwined, both studies would “validly” report that the factor focused on is the main driver.

Thirdly, it is possible the influence of various factors varies according to the type of organisation. For example, governmental and charitable organisations may be driven by a different set of factors than (say) large private corporations. Similarly, large and small companies may differ in their attitudes and behaviours. Hence the conclusions of various studies may differ according to the type of organisation consulted.

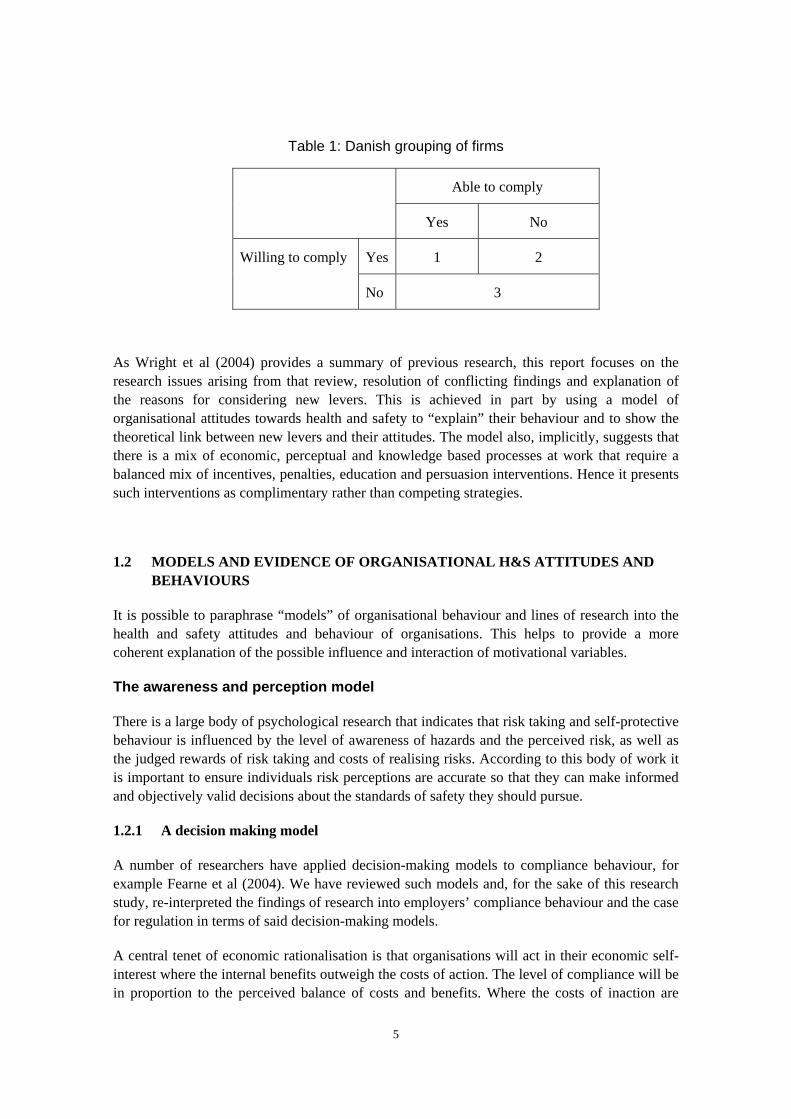

The latter concept has been elaborated by Jensen and Jensen in relation to Danish inspection strategies, where they characterise enterprises as per Table 1. The idea is that firms vary in their nature and hence the influence of motivational drivers, such as enforcement or self-interest, will vary. The Danish grouping, if applied to UK research findings, might place small firms in box 2 or 3, with larger firms in box 1 or 3.

4

Table 1: Danish grouping of firms

Able to comply

Yes No

Yes 1 2 Willing to comply

No 3

As Wright et al (2004) provides a summary of previous research, this report focuses on the research issues arising from that review, resolution of conflicting findings and explanation of the reasons for considering new levers. This is achieved in part by using a model of organisational attitudes towards health and safety to “explain” their behaviour and to show the theoretical link between new levers and their attitudes. The model also, implicitly, suggests that there is a mix of economic, perceptual and knowledge based processes at work that require a balanced mix of incentives, penalties, education and persuasion interventions. Hence it presents such interventions as complimentary rather than competing strategies.

1.2 MODELS AND EVIDENCE OF ORGANISATIONAL H&S ATTITUDES AND BEHAVIOURS

It is possible to paraphrase “models” of organisational behaviour and lines of research into the health and safety attitudes and behaviour of organisations. This helps to provide a more coherent explanation of the possible influence and interaction of motivational variables.

The awareness and perception model

There is a large body of psychological research that indicates that risk taking and self-protective behaviour is influenced by the level of awareness of hazards and the perceived risk, as well as the judged rewards of risk taking and costs of realising risks. According to this body of work it is important to ensure individuals risk perceptions are accurate so that they can make informed and objectively valid decisions about the standards of safety they should pursue.

1.2.1 A decision making model

A number of researchers have applied decision-making models to compliance behaviour, for example Fearne et al (2004). We have reviewed such models and, for the sake of this research study, re-interpreted the findings of research into employers’ compliance behaviour and the case for regulation in terms of said decision-making models.

A central tenet of economic rationalisation is that organisations will act in their economic self-interest where the internal benefits outweigh the costs of action. The level of compliance will be in proportion to the perceived balance of costs and benefits. Where the costs of inaction are

5

external to the organisation, regulation is required to ensure that the organisation that benefits from the activity that creates the external costs manages those risks in a proportionate and effective way. In this situation, the level of compliance would be in proportion to the perceived balance of internal costs and external benefits.

Such economic rationalisation provides a classic justification for regulating health and safety, rather than relying on economic self-interest, where the costs of poor health and safety performance are borne outwith the organisation that creates the risk and benefits from the activities that create the risk.

There is a large body of research that indicates that this has, and may remain, the position in the UK, although recent events in insurance and reputational risk may be changing this position. Indeed, the case for UK health and safety regulation is often framed in terms of the benefits to society, measured in terms of the subjective value of those deaths, injuries and ill-health that would be averted by the mandated duties. Indeed, many Regulatory Impact Assessments of health and safety regulations are based on a comparison of the compliance costs borne by organisations and the benefits accrued to society in the form of averted injury and ill-health. Such comparisons are completed to demonstrate and ensure that the mandated duties are proportionate.

It is possible to interpret many of the findings of previous research into employer behaviour in these terms. Many studies have indicated that employers’ compliance behaviour is influenced by the perception that the regulations address a real risk and that there are moral and ethical reasons to manage health and safety. It is possible to suggest that employers are, either consciously or implicitly, recognising that regulations exist to ensure that they do not “profit” at others expense. Indeed, many studies have indicated that whilst few firms quantify the costs of compliance and many do not believe there are tangible financial benefits of compliance, they nonetheless regard the costs and benefits of compliance to be reasonable. These paradoxical findings may well reflect the recognition that the costs are borne by organisations and the benefits are borne by wider society.

Following on from this line of reasoning, it is essential for the regulator to demonstrate the mandated duties are justified by the level of harm posed by the regulated activities and that the mandated duties are proportionate to the risk and effective.

However, it is possible to interpret these findings in another light. That is, it is possible to argue that, if the costs are currently external to the organisation, one way forward would be to transfer some or all of these costs into the organisation that creates the risk. Indeed, there are examples of this strategy being explicitly pursued, such as with the reform of the United States workers’ compensation system in the 1970’s. The reform had an explicit objective of creating a financial incentive for health and safety by transferring the largest possible proportion of the costs of injury and ill-health to employers via insurance. Hence it is perhaps unsurprising that the research in some countries has indicated that organisations bear a higher proportion of the costs of injury and ill-health, and that these internalised costs play a greater role in employers behavior. In contrast, the UK’s employers’ liability system was designed to ensure employers have funds to fulfill compensation settlements if they are sued, on grounds of negligence, by employees. That is. The imperative was to ensure funds were available for the employee. Employers’ liability was not designed to ensue all of the costs of injury and ill-health were borne by employers. Costs such as the NHS treatment of injuries have been excluded.

6

Following on from this line of reasoning, it could be argued that the UK, where costs of injury and ill-health have traditionally been external to organisations, should seek ways of transferring them to organisations. Indeed, more recent UK research can be interpreted as indicating that there has been some movement in this direction already. First, the very recent increases in employers’ liability insurance premiums have increased employers’ concern for health and safety and led to action to make improvements. It is also possible to see at least two other emerging developments. First, there is some evidence that supply chain pressure has created an “internal” driver for health and safety in some sectors. That is, where clients and customers place demands on suppliers/contractors to meet certain health and safety standards, this has the effect of “internalising” the cost of poor health and safety, i.e. organisation risk the loss of trade if they display poor health and safety. Secondly, there is some evidence that the fear of reputational damage is a driver for health and safety in some sectors. Again, in the event of poor health and safety performance the organisation incurs “internalised” costs in the form of loss of brand value for example.

However, even where the costs of injury and ill-health are internalised, this does not necessarily lead to a proportionate response. There is evidence that compliance, and general organisational commitment to health and safety, is highly influenced by awareness and perception of risks. It is possible to explain the role of these factors in terms of “imperfect knowledge” and perceptual bias. If an organisation is unaware of the full risk or costs of harm, internal or external to the organisation, arising from an activity or hazard, the rational decision would be against taking preventive measures. Indeed, there is a large body of evidence that indicates that awareness of a risk is often a pre-requisite to taking action, and that media attention about a “new” (or newly recognised hazard” such as stress can lead to an increase in preventive actions. There is also evidence that the presence of health and safety specialists in an organisation is associated with higher levels of awareness and action.

Similarly, if the cost and practicality of preventing a risk are overestimated, this may again sway an organisation against preventative action on the grounds that it is not proportionate to the risk. Following on from this line of evidence it is reasonable to suggest that it is essential to ensure organisations have a valid and accurate understanding of the risks posed by an activity or hazard, the costs and practicality of risk management, and the internal benefits of compliance.

As the time and cost involved in understanding regulations and planning actions is part of the compliance cost, this raises the issue of the “transaction” cost aspect of compliance. The importance of this factor can be seen in the often-reported request from small firms, in particular, for specific guidance. This can be interpreted as a wish to minimize the cost of compliance. That is, smaller organisations which typically lack in-house health and safety expertise may believe that they incur (or at least perceive that they incur) a high cost if they have to interpret a “flexible” non-prescriptive regulation, and translate general requirements into the specific actions they need to take. The wish to reduce the cost of compliance is evidenced by the perception that it is easier, less time consuming and hence cheaper for a small firm to be presented with a simple set of requirements that are specific to their business, and which hence require no interpretation.

It is also possible to interpret the expressed desire (from employers) for advisory site visits from inspectors in economic terms. Such visits are desired on the presumption that they will lead to specific advice on how to manage risks posed by the organisations own activities. Such advice, being specific, would entail little interpretation cost by the employer, and would avoid

7

unnecessary or inappropriate (and hence wasteful) actions. Also, with the inspector coming to the workplace, this avoids the time and cost of the employer seeking advice.

However, there is some evidence that even where the compliance costs are outweighed by the benefits, this may not lead to proportionate action. First, employers may not be economic optimisers. Some organisations, such as public sector organisations may lack a true profit optimisation philosophy. Also, if the costs of poor performance (and the benefits of improvements) are held centrally within an organisation, there is evidence of the economic self-interest being diluted, i.e. if your department fails to benefit from improvement local management will lack self-interest. On the other hand, profit motive may not lead to proportionate action. If other lines of business development offer a better return on investment (of time and money), such as increasing profit through greater sales rather than greater productivity, employers may focus their efforts on alternative ways of profit maximisation. Finally, if an organisation believes it can pass on the costs (i.e. externalise them) of harm, such as by increasing product costs, recognition of the internal costs of poor performance may not provide economic self-interest.

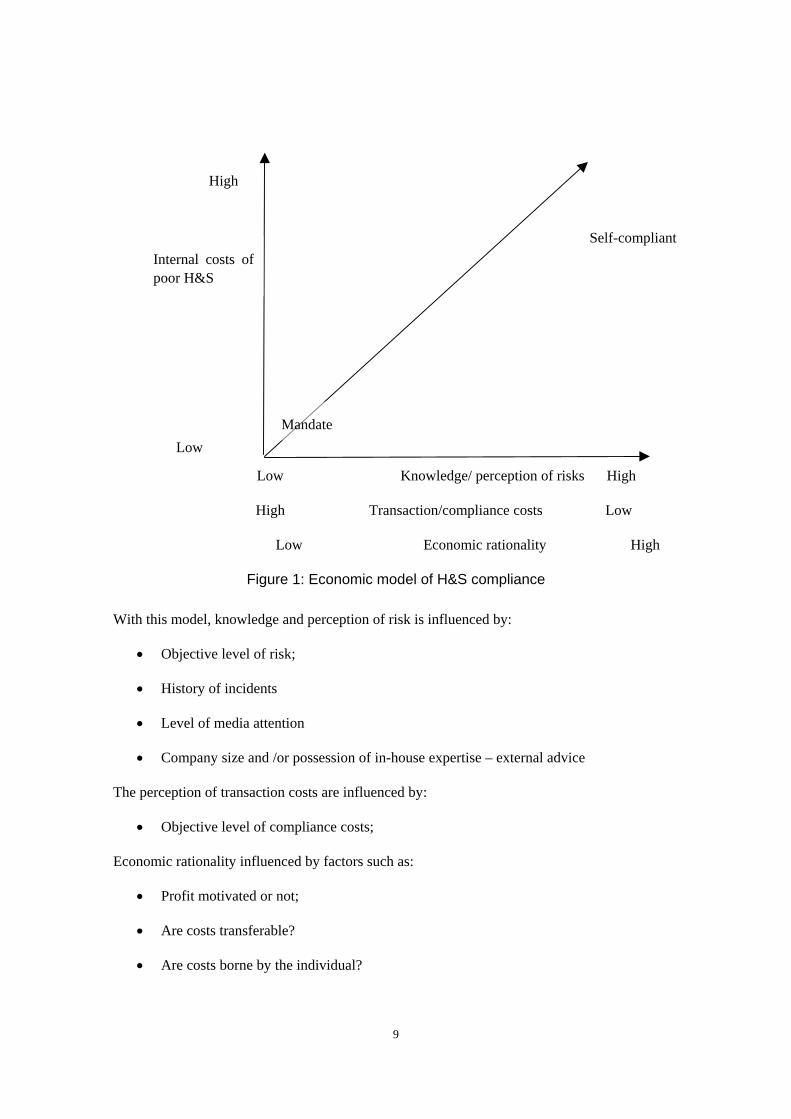

8

High

e

t

Low Knowledge/ perception of risks

High Transaction/compliance costs

Low Economic rationality

Figure 1: Economic model of H&S compliance

With this model, knowledge and perception of risk is influenced by:

• Objective level of risk;

• History of incidents

• Level of media attention

• Company size and /or possession of in-house expertise – external advice

The perception of transaction costs are influenced by:

• Objective level of compliance costs;

Economic rationality influenced by factors such as:

• Profit motivated or not;

• Are costs transferable?

• Are costs borne by the individual?

9

Self-complian

Mandat

Internal costs ofpoor H&S

Low

High

Low

High

The level of internal cost is influenced by:

• Objective level of internal costs, e.g. cost of insurance

• Perceived risk of reputational damage – which in turn is influenced by extent to which firm has a public image/brand value, whether demand is elastic, whether H&S is perceived as important by customers etc, possibility of detection and degree of publicity awarded wrong doing;

• Position in the supply chain and level of customer pressure.

The role of education, regulation and enforcement

A central tenet of economic rationalisation is that organisations will act in their economic self-interest where the internal benefits outweigh the costs of action. This model would argue for (1) ensuring organisations have a correct understanding of the costs and benefits of compliance, (2) costs are internalised where possible and (3) regulation is applied where cost internalisation is not possible or where an imperfect market exists. Therefore, in the context of the economic model of compliance behaviour, regulation and enforcement can be said to have a number of roles:

• Where the costs of poor health and safety are external to the organisation, regulation is required to ensure the organisation manages these risk in proportion to the external costs;

• If regulations exist to ensure all organisations manage risks that create external harm (social costs), for such enforcement to be seen as socially just it must be consistent across all organisations, otherwise the social case for regulation is undermined;

• Where lack of knowledge and/or skewed perceptions of risk cause organisation to under-rate the importance of a specific aspect of risk management, enforcement is required to force the organization to manage a risk in proportion to its importance (as judged by the regulator);

• Where compliance is due to lack of awareness of (for example) appropriate risk management practices, enforcement may have the effect of raising awareness. In this respect, the publicity of enforcement action may have an impact on other organizations, by raising their awareness;

• Where the costs of interpreting general regulations is seen as high by an employer, enforcement may be seen as a way of translating general requirements into specific ones;

• Where the employer is unwilling to incur the transaction costs involved in understanding and interpreting regulations, enforcement involves the regulator making the judgement for the employer;

• Where an employer does not follow a rationale model of decision making, enforcement applies an external view of rational and proportionate behaviour.

10

In this context, enforcement can be seen to:

• Have a deterrent effect beyond the enforced organization by generating a fear of reputational damage (where they are perceived by society to have acted unethically or negligently, as shown by a prosecution for example);

• Have a narrow effect within organisations by forcing them to act on risks they either did not recognise or which they would not act on due to their belief that the costs of compliance were disproportionate;

• Have an educational effect beyond the enforced organisation by increasing awareness of the risks and appropriate preventive actions;

• Help internalise the costs of poor health and safety, by generating reputational damage, leading to customer dissatisfaction (if they have H&S demands) and by levying fines.

The economic analysis of crime assumes that commercial organisations will breach the law if the benefits exceed its expected costs. This interpretation of the economic model leads to a “detect and punish” approach where the regulator must police organisations to detect intentional and purposeful non-compliance. It assumes that the costs of poor H&S are either not internalised by organisations or are insufficient to lead to appropriate H&S standards, and that organisations consciously act in a criminal manner.

In a more general paper looking at challenges for regulatory compliance (across all aspects of legislation) the OECD (2001) address a number of points about how enforcement may influence behaviour:

• They refer to the need for regulation to be simple so that it can be easily understood with lower costs of compliance;

• They also highlight the need to ensure that there is fairness in regulation, otherwise rule breaking will occur where the regulation and its application is perceived to be unfair, and this in turn requires a high level of detection of rule breaking.;

• The studies quoted by the OECD seem to indicate that both the nature and extent of enforcement action are important with purely negative and punitive approaches actually reducing compliance;

• The OECD also points to the failures in monitoring of compliance with regulations as being a factor, an issue also highlighted by Hopkins (1995). As pointed out by the OECD paper, any form of justice is only effective if there is a high likelihood of being caught - as without being detected the impact of any penalty is non-existent.

Hopkins (1995) addresses the impact of on the spot fines as being effective and it would appear that it is the shock of the penalty itself, rather than the size of the penalty, that has the impact. This was a factor also cited by Mendaloff (in Sullivan and Frank 2003). Although, once this shock is overcome it may tend to have an opposite effect. Mendalof, again, refers to the increase in inspection related penalties in US from 35% (inspections resulting in penalties) between 1979-87 to 75% between 1992-8, inferring that as managers could now expect a penalty with each inspection the motivating effect of surprise is lost.

11

Whilst there are many studies, which report that employers cite regulation and enforcement as key drivers for health and safety, few studies have demonstrated the link with performance. Evidence, mostly from North America and cited in both; Sullivan and Frank (2003) and Hopkins (1995), seems to indicate that the nature and intensity of inspection, including the issue of fixed penalty notices has a direct bearing on safety performance.

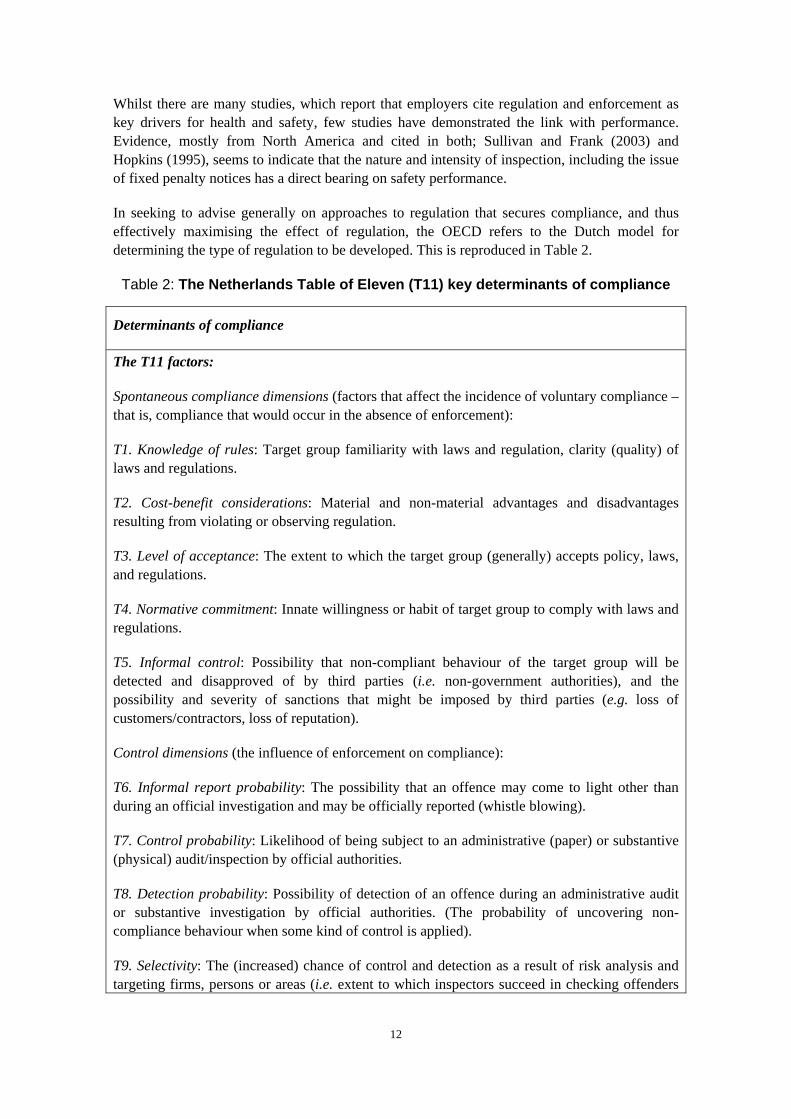

In seeking to advise generally on approaches to regulation that secures compliance, and thus effectively maximising the effect of regulation, the OECD refers to the Dutch model for determining the type of regulation to be developed. This is reproduced in Table 2.

Table 2: The Netherlands Table of Eleven (T11) key determinants of compliance

Determinants of compliance

The T11 factors:

Spontaneous compliance dimensions (factors that affect the incidence of voluntary compliance – that is, compliance that would occur in the absence of enforcement):

T1. Knowledge of rules: Target group familiarity with laws and regulation, clarity (quality) of laws and regulations.

T2. Cost-benefit considerations: Material and non-material advantages and disadvantages resulting from violating or observing regulation.

T3. Level of acceptance: The extent to which the target group (generally) accepts policy, laws, and regulations.

T4. Normative commitment: Innate willingness or habit of target group to comply with laws and regulations.

T5. Informal control: Possibility that non-compliant behaviour of the target group will be detected and disapproved of by third parties (i.e. non-government authorities), and the possibility and severity of sanctions that might be imposed by third parties (e.g. loss of customers/contractors, loss of reputation).

Control dimensions (the influence of enforcement on compliance):

T6. Informal report probability: The possibility that an offence may come to light other than during an official investigation and may be officially reported (whistle blowing).

T7. Control probability: Likelihood of being subject to an administrative (paper) or substantive (physical) audit/inspection by official authorities.

T8. Detection probability: Possibility of detection of an offence during an administrative audit or substantive investigation by official authorities. (The probability of uncovering non-compliance behaviour when some kind of control is applied).

T9. Selectivity: The (increased) chance of control and detection as a result of risk analysis and targeting firms, persons or areas (i.e. extent to which inspectors succeed in checking offenders

12

Determinants of compliance

more often than those who abide by the law).

Sanctions dimensions (the influence of sanctions on compliance):

T10. Sanction probability: Possibility of a sanction being imposed if an offence has been detected through controls and criminal investigation.

T11. Sanction severity: Severity and type of sanction and associated adverse effects caused by imposing sanctions e.g. loss of respect and reputation.

Source: Dick Ruimschotel, Compliance Methodology Consultants, Amsterdam and But Klaasen, Ministry of Justice, The Hague.

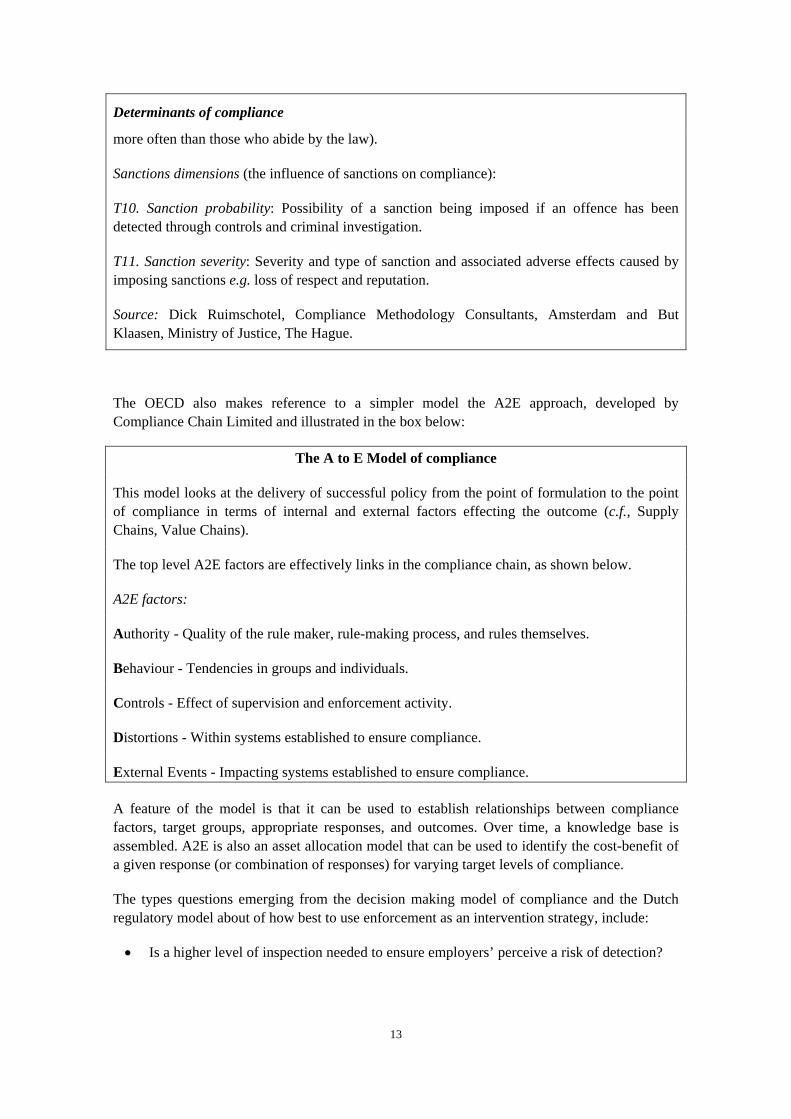

The OECD also makes reference to a simpler model the A2E approach, developed by Compliance Chain Limited and illustrated in the box below:

The A to E Model of compliance

This model looks at the delivery of successful policy from the point of formulation to the point of compliance in terms of internal and external factors effecting the outcome (c.f., Supply Chains, Value Chains).

The top level A2E factors are effectively links in the compliance chain, as shown below.

A2E factors:

Authority - Quality of the rule maker, rule-making process, and rules themselves.

Behaviour - Tendencies in groups and individuals.

Controls - Effect of supervision and enforcement activity.

Distortions - Within systems established to ensure compliance.

External Events - Impacting systems established to ensure compliance.

A feature of the model is that it can be used to establish relationships between compliance factors, target groups, appropriate responses, and outcomes. Over time, a knowledge base is assembled. A2E is also an asset allocation model that can be used to identify the cost-benefit of a given response (or combination of responses) for varying target levels of compliance.

The types questions emerging from the decision making model of compliance and the Dutch regulatory model about of how best to use enforcement as an intervention strategy, include:

• Is a higher level of inspection needed to ensure employers’ perceive a risk of detection?

13

• Would higher penalties increase the internalised costs of poor performance or would it lead to a perception of enforcement as unfair/ disproportionate and hence undermine the perceived legitimacy of regulations?

• Should prosecutions focus on the corporate body rather than the individual?

• Should employers’ be offered greater incentives in reward for better performance (such as earned autonomy or targeted inspection) to help internalise and increase the benefits (less inspection) of good performance?

• Are there alternative penalties that would help to internalise costs of poor performance and / or provide a more positive incentive to organisations (see 1.2.2 and 1.2.3 for two examples)?

• Should the law be changed to increase the possibility and consequence of prosecution?

• Should the actual or perceived cost of compliance be reduced?

It is also the case that the relevance of the economic argument at the organisational level is questioned by a number of theorists. For example, Cutler and James (1996) criticize the HSE for painting an overly simplistic picture of the ‘safety pays’ argument, and points out three flaws with it, namely:

• It encourages the notion that employers should prioritise the avoidance of accidents by reference to potential financial returns;

• It is estimated that the average costs of non-injury accidents are nearly three times those of injury accidents;

• At some point further investment in the safety programme will not give a net return. Thus, based on a purely financial argument, safety expenditure should be increased up to the point where the marginal cost of safety equals its marginal benefit, and no further (Ashby & Diacon, 1996).

In addition, Hopkins (1999) believes that managers’ thinking about expenditure on health and safety may in fact be essentially flawed. He points to ‘Institutionalized irrationality’ in which managers’ focus on the costs of complying with health and safety legislation, over too short a period of time. As a result, the costs of compliance are identified as a financial burden. Next he points to ‘Bounded rationality’ in which managers lack access to all relevant information. Such failures to fully weigh up the economic arguments are thought to lead to faulty decision making by managers.

This leads to the further issue of whether there is evidence that employers are influenced by the costs and benefits of H&S.

1.2.2 Restorative justice

The concept of restorative justice (OECD, 2001) has been expressed as a more familial social control mechanism involving the identification of wrongdoing, the creation of shame, and then reintegration (back into the family). To quote the OECD paper:

14

“a number of business regulators have experimented with adopting innovative mechanisms for restorative justice when compliance fails, in order to remedy the wrong

and ensure compliance in the future. While the evidence on the effectiveness and fairness of restorative justice for individual offenders is still being evaluated, there is good evidence that the restorative justice is effective for corporate law breaking. The

aim of restorative justice is to restore enterprises to a position where they have both the capacity and willingness to comply after they have committed a violation.”

Whereas the use of restorative justice approaches increased compliance – this is attributed in part to the point that whilst the enforcers disapproved of the original non-compliance, they provided approval/ praise for the actions taken once the non-compliance was identified.

1.2.3 Adverse publicity

The role of reputation risk in securing compliance

There is a large body of research in the UK that indicates organisations are prompted to manage H&S to avoid the reputational damage of incidents, as summarised in Wright et al 2004. In the context of the economic model of behaviour, reputational damage (arising from H&S incidents or enforcement) is a way in which external costs are internalised, through loss of brand value. In this sense, enforcement may also play a role in internalising costs if it causes reputational damage.

Following on from this line of thinking, it is important to publicize enforcement actions to ensure its role in internalising costs is maximised. This may have the effect of increasing other organisations perception of the possibility of reputational damage, and hence have a deterrent effect beyond the enforced organisation. Such publicity is also needed for the enforcement to be known, such as publicity via mass media, and hence for it to create reputation damage. For this to be achieved, the enforcement action must be needed to be perceived by wider society (or at least customers) as an indication of unethical behaviour by the organisation, or in some way create a loss of brand value. If stakeholders perceive the enforcement to be disproportionate or unjust, such enforcement is less likely to create reputational damage.

Indeed, there has been a body of research summarised and reviewed by Yeung (Yeung, 200?) completed on the role of adverse publicity in securing regulatory compliance. This work has been awarded greater interest in Australia recently due to the introduction of Adverse Publicity Orders. Similarly, the OECD (2001) refers to the effect of negative publicity and the associated loss of corporate prestige. In brief, it is suggested by Yeung that reputational risk has grown in importance for a number of reasons, including:

• Growth in information technology and media – leading to rapid transmission of information directly to general public on a, low cost and instantaneous basis;

• A professionalisation of communications where society actively engages media;

• A greater public (and company) interest in corporate misconduct due to (1) a recognition of the impact of shares value on pension funds as well as the wider share ownership in some countries and (2) growing impact of brand values on commercial performance (due to consumer sensitivity towards brand image and values).

15

It is suggested that these trends have led to a growth in media attention towards reporting of corporate misconduct and a growth in the impact of “misconduct” on commercial performance. Indeed, Yeung concludes that:

“There appears to be verifiable evidence that firms are sensitive to adverse publicity.” (p11)

“In these studies, a statistically significant negative impact between adverse publicity and firm performance is typically observed.” (p11)

“..firms fear the sting of adverse publicity attacks on their reputations more than they fear the law itself.” (p12)

Accordingly it is argued that regardless of whether brand values really do impact commercial performance, organisations are increasingly motivated to manage their reputations and image.

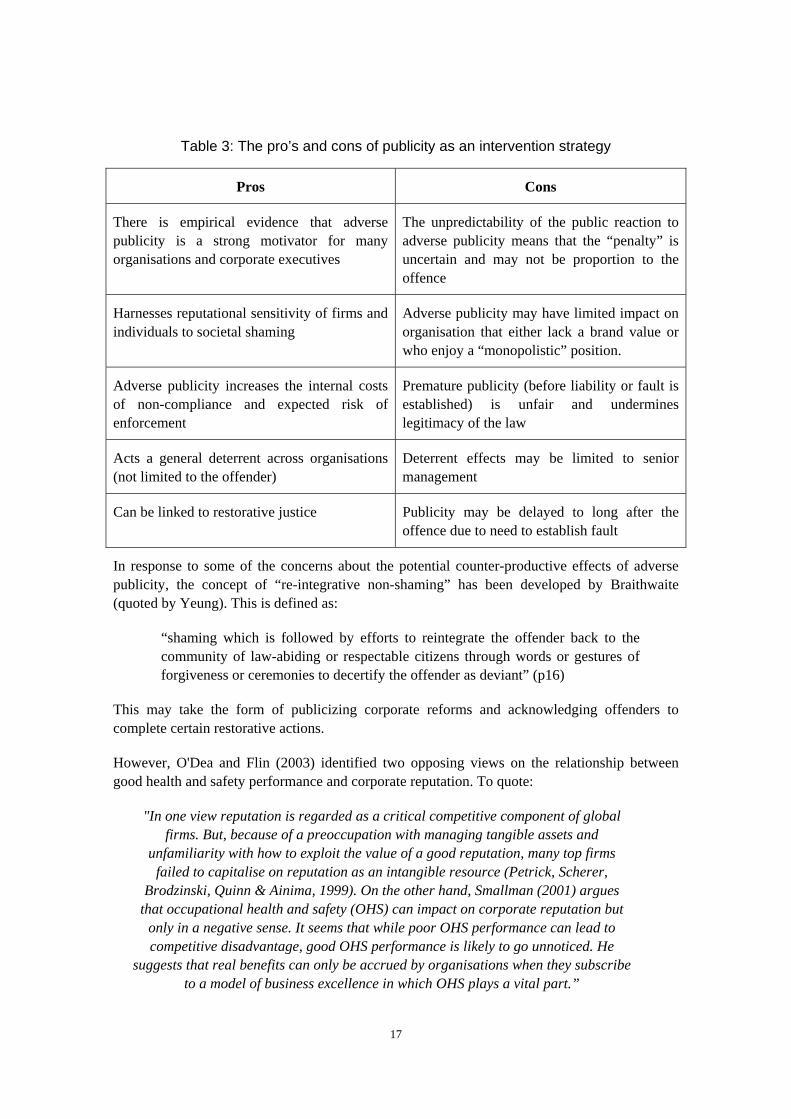

These observations formed the context for the introduction of adverse publicity orders in Australia, the pros and cons of which are summarised in Table 3. They also form the context for recent HSE proposals and initiatives such as:

• Encourage corporate firms to publicly report their health and safety standards / performance, and;

• Operate an Offenders Database.

Recent research, as reviewed by Wright, Marsden and Antonelli (2004), suggests that it is apparent that enforcement is important in respect of:

• Creating a deterrent for large and small firms alike, including a fear of reputational damage;

• The HSE is an active actor in the creation of reputational risk for organisations, including its enforcement work and the published findings of audits and reviews.

This lends support to the idea of better publicising the outcome of enforcement action.

16

Table 3: The pro’s and cons of publicity as an intervention strategy

Pros Cons

There is empirical evidence that adverse publicity is a strong motivator for many organisations and corporate executives

The unpredictability of the public reaction to adverse publicity means that the “penalty” is uncertain and may not be proportion to the offence

Harnesses reputational sensitivity of firms and individuals to societal shaming

Adverse publicity may have limited impact on organisation that either lack a brand value or who enjoy a “monopolistic” position.

Adverse publicity increases the internal costs of non-compliance and expected risk of enforcement

Premature publicity (before liability or fault is established) is unfair and undermines legitimacy of the law

Acts a general deterrent across organisations (not limited to the offender)

Deterrent effects may be limited to senior management

Can be linked to restorative justice Publicity may be delayed to long after the offence due to need to establish fault

In response to some of the concerns about the potential counter-productive effects of adverse publicity, the concept of “re-integrative non-shaming” has been developed by Braithwaite (quoted by Yeung). This is defined as:

“shaming which is followed by efforts to reintegrate the offender back to the community of law-abiding or respectable citizens through words or gestures of forgiveness or ceremonies to decertify the offender as deviant” (p16)

This may take the form of publicizing corporate reforms and acknowledging offenders to complete certain restorative actions.

However, O'Dea and Flin (2003) identified two opposing views on the relationship between good health and safety performance and corporate reputation. To quote:

"In one view reputation is regarded as a critical competitive component of global firms. But, because of a preoccupation with managing tangible assets and

unfamiliarity with how to exploit the value of a good reputation, many top firms failed to capitalise on reputation as an intangible resource (Petrick, Scherer,

Brodzinski, Quinn & Ainima, 1999). On the other hand, Smallman (2001) argues that occupational health and safety (OHS) can impact on corporate reputation but

only in a negative sense. It seems that while poor OHS performance can lead to competitive disadvantage, good OHS performance is likely to go unnoticed. He

suggests that real benefits can only be accrued by organisations when they subscribe to a model of business excellence in which OHS plays a vital part.”

17

The findings of Yeung and others indicate that there are some issues to be addressed, including:

• How can adverse publicity be applied in a fair and proportionate way?

• Can adverse publicity be designed to provide a positive “restorative” penalty?

• What are the best routes for such publicity?

• In which sectors may adverse publicity have an effect?

1.2.4 Internalising costs of poor performance

The economic model of H&S behaviour would also prompt the questions:

• Should and how can the proportion of costs borne internally by organisations be changed?

• How can a clear link between H&S performance on their costs/benefits be improved?

Outside of enforcement and penalties, two further options have been the subject of research, namely:

• Supply chain pressure, and;

• Insurance

Supply chain

Customers’ pressures have been identified as another way of “internalising” costs of poor H&S. As concluded in Wright at al (2004) “when exercised, supply chain pressure can have a significant effect on suppliers and contractors”(pvi). This is supported by Vickers et al (2003) who found a range of pressures, including those from insurers, of customers and suppliers including customer reinforced pressure regarding environmental legislation together with a need to create or maintain competitive advantage.

Of interest, there appears to be a common thread through much of the research indicating that, for food safety, there is a marked degree of "pressure" through the supply chain related to food quality standards. For example, in the contractorisation study (2003), the authors identify that in the catering sector there are demands by business on their suppliers for food safety reasons.

The PWC report of a small firms project for HSE and Belfast Council identified that one of the reasons health and safety was identified as a priority was the extent to which customers or standard bodies exerted pressure on a business.

However, it is unclear how common supply chain pressure is applied.

Insurance

The Wright (2002) study found from a review of experience in other countries that insurance is a significant motivator where a greater proportion of the costs of injury and ill-health are borne by the insured. It was suggested that the role of insurance could develop if the proportion of injury and ill-health costs borne by UK employers via employers’ liability insurance were to

18

rise. Subsequent to the prices rises in 2002-2003, the review of evidence for the HSE Strategy (Wright, Marsden and Antonelli, 2004) concluded that:

“Whilst earlier research provided mixed messages on the effectiveness of financial incentives, there is emerging evidence that with the increased cost of insurance that some organisations are starting to respond to insurance premiums by trying to improve health

and safety. Research has also found that small firms would be more likely to be incentivised if they saw a clearer link between their premiums and their health and safety performance. This provides support for the idea of developing a more risk based method of setting SMEs insurance premiums, and for further developing the role of insurance as

an incentive for better health and safety.”

This finding that the cost of insurance, and hence the prospect of discounts, suggests that insurance has the potential to become a particularly effective incentive for SMEs.

1.2.5 Reducing compliance costs

A number of options for reducing compliance costs have been suggested. The first and simplest idea has been to simplify and/or reduce the level of regulation. Other suggestions include:

• Reward good performance through “Earned autonomy” and / or “targeted inspection”, wherein good firms are the subject of less inspection;

• Create sector specific standards, which require less interpretation and hence lower compliance costs, and;

• Provision of tax incentives for health and safety expenditures, or grants for small firms.

1.2.6 Raising awareness of hazards, risks and costs

A series of HSE projects have indicated that raising employers’ awareness of hazards and how to control them is an essential pre-requisite for compliance. It is also commonly reported that the a priori level of awareness of hazards and the perceived risk posed by H&S hazards has a major influence on compliance. This is particularly so in the case of SMEs which tend to lack in-house health and safety specialists. In the context of the economic model of behaviour, awareness and knowledge of hazards are essential elements of rationale decision-making and judgement of the proportionality of risk controls and associated regulations. Recognition of the information needs of firms and the difficulty that is reported in accessing some firms leads to the notion of “relationship” building, as opposed to enforcement, as well as drawing on concepts of public information campaigns and marketing.

One study by Hillage, et al (2001) found that, overall, some 20-30% of employers are not aware of the law that affects them; the least understanding being amongst SMEs. Another study (Vickers et al 2003) confirmed this view identifying that h&s legislation specific to their business was not identified by 50% of SMEs. This latter study identified that the larger SMEs were better, in terms of their knowledge of health and safety legislation, although they were still described as poor in this respect. Of interest here was the finding that a recent visit by an inspector was not a factor in the business knowing specific legislation.

19

In the context of the economic model of behaviour, the perceived affordability and benefits of compliance are important variables. The relevance of this to health and safety behaviour is indicated by many research studies. First, there is some evidence from previous research to suggest that employers are sensitive to the “affordability” of health and safety management. That is, they appear to judge the “reasonableness” of health and safety in terms of whether the costs of compliance are in proportion to the seriousness of the risk and whether the health and safety controls are affordable in absolute terms. Highlighting the costs of injury and ill-health to the employer is important, in so far that it helps to offset some of employers’ direct compliance costs, and hence makes compliance more affordable. These “costs” can include intangibles elements, such as reputational damage, industrial relations problems and loss of customers. Reputational damage can come in the form of a high-profile accident, prosecution, adverse inspection report and so on (namely anything that castes doubt on the ethical behaviour or competence of the company). Indeed, there is anecdotal evidence that the value of a fine is seen as a measure of censure.

At the same time, education and awareness raising is important, in the context of enforcement, in order to:

• Demonstrate the fairness of the regulation and its proportionately, and;

• Enable organisations to manage the risk by raising awareness of suitable and effective risk controls.

O'Dea and Flin (2003) also found evidence from several studies supporting the view that companies have imperfect cost information. In a review of whether “cost of accident” and “business case” publicity has worked Wright et al (2004) concluded that “Whilst it appears that progress has been made in convincing organisations of the business case, the results are mixed and hence further work in promoting the business case is needed.” (pvi)

There is also mixed evidence that organisations see a link between productivity and health and safety. O'Dea and Flin (2003) in their review report Warrack and Sinah (1999) found that among the most sophisticated firms in their sample, this is in fact the case. They also report that Petrick et al (1999) found that excellent global leaders are capable of balancing four competing criteria of performance:

i) Profitability and productivity;

ii) Continuity and efficiency;

iii) Commitment and morale, and;

iv) Adaptability and innovation.

However, there is little evidence that other firms, such as SMEs, recognise this link.

These types of findings have led to a focus on how best to communicate with employers, especially the large number of small employers, with the goals of:

• Improving awareness of hazards and increasing their perception of the risk such that they accept the need to implement risk controls;

20

• Advising them of how best to manage the risk as well as their regulatory duties.

Working with intermediaries

Hillage et al (2001) identified that an improved understanding of health and safety and how to manage risks was a strong driver, although the link between information provision and improvement in performance is not strong. In concurrence with a number of studies the major source of information was from HSE/LA inspectors, although the absence of any link between an inspectors visit and knowledge of health and safety legislation should be noted. Although two thirds of respondents would use LA/HSE, 1 in 10 of respondents did not know how to get health and safety information. Whereas, some SMEs use other sources of information e.g. insurance companies, financial services and consultants. The indications are that these are actually little used.

A paper by John Kingston Associates (quoted in Atkins, 2003) recognised the overall problem of information handling within small firms, which may impact upon the effectiveness of health and safety information. This is an issue raised in other studies. In a 1999 consultation document it was found that SMEs had a lack of understanding /knowledge of health and safety with poorer training and employee competence. This view was reiterated by a HSL consultation draft in 2000 (quoted in Atkins).

One de-motivator to information handling may be related to literacy within organisations, especially small firms and EMB’s. A study by Wiseman et al (2002) of chemical information in small firms identified that health and safety issues were usually communicated verbally and a very low level of reading skills predominates. Thus suggesting that for some sectors there is possibly an issue relating to how information needs to be presented to reflect the regulatory driver. Safety information centres (Loughborough, 2000) appear to offer an approach to assisting in safety information provision to small firms, particularly in relation to establishing management systems.

On a somewhat different note, another study in 2000 conducted by Norwich Enterprise Agency trust (quoted in Atkins 2003) found that SMEs saw HSE as the enemy and a source of red tape. In Contractorisation aspects of health and safety in the supply chain, Partnership Sourcing Ltd (2000), the authors found that SMEs have difficulty in coping with the sheer volume of legislation.

These, and other concerns about how best to raise awareness and advise firms, have led to the suggestion that the HSE needs to work with other stakeholders to reach employers, especially SMEs, as well as set up an advisory service that is seen as independent of the enforcement side of the HSE. The review of evidence for the HSE (Wright, Marsden and Antonelli, 2004) strategy noted that:

“It is clear that working with intermediaries can effectively amplify the impact of the HSE and that this is particularly needed amongst the large number of SMEs. It is also clear that there is a range of intermediaries that the HSE could work with, but the relative effectiveness of each type

of intermediaries is less well researched. The effectiveness of some intermediaries has been subject to limited research and / or a single pilot. Whilst this provides an initial indication of

their potential role uncertainties remain.”

21

Thus, whilst the need for partnering and education is generally accepted and many alternative routes for education have been identified, they have yet to be subjected to full-scale evaluation.

The suggestion is that a collaborative approach involving all relevant stakeholders has a better chance of succeeding in achieving improvement than a single agency or stakeholder operating alone. This idea is supported by the OECD (2001), particularly with reference to success in other areas of policy regulation such as environmental controls. Additional support comes from Mootz, Franklin and Wickizer (2003) citing a study of inter-agency/stakeholder co-operation and community systems in Washington state relating to musculoskeletal injury management. However, what this study identified was that the area is fraught with difficulties. And, whilst such an approach may be effective it may not have an impact (J Hillage, et al 2001), in terms of reducing injury per se. Mootz et al (2003) argue that, on the basis of the evidence available, it is necessary to adopt a multiple attack approach, securing collaboration from and mobilising stakeholders with interventions that are synergistic.

Use of IT also seems to be an important area, particularly (as might be expected) with SMEs. For example, EMBs with IT felt less over regulated (Vickers et al 2003). However, other researchers cited in Atkins (2003) found that 25% of SMEs have no access to PC’s or web sites. Although an HSL report (quoted in Atkins 2003) showed that 50% of SMEs did have access to internet (major areas being manufacturing and financial sector) across all sectors (lowest in retail, hotels and restaurants), less than 30% of business used Government internet services. Overall, less than 2% of respondents had accessed HSE internet services. Indications are that small businesses prefer to talk (face/face). The Atkins (2003) review identifies a number of areas where IT has been found to be useful, including the relative success of COSHH although the precise impact of this is not clear.

Amplifying impact of accidents