Embed Size (px)

Citation preview

1

REQUEST FOR PROPOSAL (RFP)

National Bidding

DATE: November 4, 2014

REFERENCE: RFP/UNDP/INDIA/2014/045

Dear Sir / Madam: We request you to submit your Proposal for a “National Study on Financial Cooperatives in the context of financial inclusion”.

Please be guided by the form attached hereto as Annex 1 & 2, in preparing your Proposal. Annexure 1 – Description of Requirements Annexure 2 – Terms of Reference

Annexure 3 – Form for submitting service provider’s Technical proposal Annexure 4 – Form for submitting service provider’s financial proposal

Annexure 5 – General Terms and Conditions of the Contract Your proposal comprising of technical proposal and financial proposal, in separate sealed

envelopes, should reach on or before 18th November, 2014, 1730 hrs. (IST) at the address below:

United Nations Development Programme 55, Lodi Estate, New Delhi – 110 003

Mr. Surjit Singh Fax: 91-11-24627612

If the technical and financial proposals are not submitted in separate sealed envelopes, the

proposal will be rejected.

Please also provide the technical proposal and its annexures (scanned copies in ONE PDF FILE) in a CD/DVD, which can be kept in the envelope containing the hard copy of the technical proposal. PLEASE NOTE THAT CD/DVD should not contain the Financial Proposal.

Your Proposal must be expressed in the English language, and be valid for a minimum period of One Hundred and Twenty (120) days.

In the course of preparing your Proposal, it shall remain your responsibility to ensure that it reaches the address above on or before the deadline. Proposals that are received by UNDP after the deadline indicated above, for whatever reason, shall not be considered for evaluation.

2

Services proposed shall be reviewed and evaluated based on completeness and compliance of the Proposal and responsiveness with the requirements of the RFP and all other annexes providing details of UNDP requirements.

The Proposal that complies with all of the requirements, meets all the evaluation criteria, and offers the best value for money shall be selected and awarded the contract. Any offer that does not meet the requirements shall be rejected.

Any discrepancy between the unit price and the total price shall be re-computed by UNDP, and the unit price shall prevail and the total price shall be corrected. If the Service Provider does not accept the final price based on UNDP’s re-computation and correction of errors, its Proposal will be rejected.

No price variation due to escalation, inflation, fluctuation in exchange rates, or any other market factors shall be accepted by UNDP after it has received the Proposal. At the time of Award of Contract or Purchase Order, UNDP reserves the right to vary (increase or decrease) the quantity of services and/or goods, by up to a maximum of twenty five per cent (25%) of the total offer, without any change in the unit price or other terms and conditions.

Any Contract or Purchase Order that will be issued as a result of this RFP shall be subject to the General Terms and Conditions attached hereto. The mere act of submission of a Proposal implies that the Service Provider accepts without question the General Terms and Conditions of UNDP, herein attached as Annex 3.

Please be advised that UNDP is not bound to accept any Proposal, nor award a contract or

Purchase Order, nor be responsible for any costs associated with a Service Provider’s preparation and submission of a Proposal, regardless of the outcome or the manner of conducting the selection process.

UNDP’s vendor protest procedure is intended to afford an opportunity to appeal for persons

or firms not awarded a Purchase Order or Contract in a competitive procurement process. In the event that you believe you have not been fairly treated, you can find detailed information about vendor protest procedures in the following link: http://www.undp.org/content/undp/en/home/operations/procurement/protestandsanctions

UNDP encourages every prospective Service Provider to prevent and avoid conflicts of interest, by disclosing to UNDP if you, or any of your affiliates or personnel, were involved in the preparation of the requirements, design, cost estimates, and other information used in this RFP.

UNDP implements a zero tolerance on fraud and other proscribed practices, and is committed to preventing, identifying and addressing all such acts and practices against UNDP, as well as third parties involved in UNDP activities. UNDP expects its Service Providers to adhere to the UN Supplier Code of Conduct found in this link: http://www.un.org/depts/ptd/pdf/conduct_english.pdf

Thank you and we look forward to receiving your Proposal.

Yours sincerely,

Irenee Dabare Deputy Country Director (Operations)

UNDP, India

3

Annex 1

Description of Requirements

Context of the Requirement

In various fora, including Microfinance India Summit 2013, it is being realized that there is a need to do an in-depth study of financial cooperatives in India, in order to; a) identify the regulatory gaps that exist in different cooperative Acts in the context of financial inclusion; b) document the successful financial cooperatives including Primary Agriculture Cooperative Societies (PACS), Cooperatives functioning as federations of SHGs and also cooperative Banks (traditional as well as new age); c) analyse the value chains of various microfinance services (savings, credit, insurance/micro-pensions, remittances and Micro leasing) as well as financial management and governance related issues of cooperatives.

The outputs of the study undertaken by UNDP will facilitate decision-making towards changes in policy and regulatory environment for financial cooperatives and towards undertaking innovations required in products and services and delivery mechanism, and adopt strategies to strengthen financial cooperatives so that they better contribute towards financial inclusion.

Implementing Partner Direct implementation by UNDP

Brief Description of the Required Services

National Study on Financial Cooperatives in the context of financial inclusion

List and Description of Expected Outputs to be Delivered

1. Inception report with detailed plan of action and timelines

2. Preliminary report based on secondary data analysis

3. Draft report of the study after completion of field work

4. Final project completion report addressing all the comments and suggestions received from UNDP

Person to Supervise the Work/Performance of the Service Provider

Programme Analyst, UNDP India Resource Person and Moderator, Microfinance Community of Practice, Solution Exchange

Frequency of Reporting As mentioned below

Progress Reporting Requirements

1. Inception report with detailed plan of action and timelines within one week of award of contract based upon the contents of the existing TOR.

2. Preliminary report based on secondary data analysis

3. Draft report of the study

4. Presentation of draft report at least 30 days before the end date of contract.

5. Submission of final project completion report addressing all the comments and suggestions received from UNDP

Location of work Four sample states

Expected duration of work Six (6) months

Target start date 25th November 2014

Latest completion date 24th May 2015

Travels Expected The assignment would include travel to the States for the field study

4

Special Security Requirements

☐ Security Clearance from UN prior to travelling

☐ Completion of UN’s Basic and Advanced Security Training

☐ Comprehensive Travel Insurance

☒ Others [Not Applicable]

Facilities to be Provided by UNDP (i.e., must be excluded from Price Proposal)

☐ Office space and facilities

☐ Land Transportation

☒ Others [Not Applicable]

Implementation Schedule indicating breakdown and timing of activities/sub-activities

☒ Required

☐ Not Required

Names and curriculum vitae of individuals who will be involved in completing the services

☒ Required

☐ Not Required

Currency of Proposal ☐ United States Dollars

☐ Euro

☒ Indian Rupees (INR)

Value Added Tax on Price Proposal

☐ must be inclusive of VAT and other applicable indirect taxes

☒ must be exclusive of VAT and other applicable indirect taxes

Validity Period of Proposals (Counting for the last day of submission of quotes)

☐ 60 days

☐ 90 days

☒ 120 days In exceptional circumstances, UNDP may request the Proposer to extend the validity of the Proposal beyond what has been initially indicated in this RFP. The Proposal shall then confirm the extension in writing, without any modification whatsoever on the Proposal.

Partial Quotes ☒ Not permitted

☐ Permitted

Payment Terms Condition for Payment Release : After satisfactory acceptance and approval of outputs / deliverables/ report by UNDP

Outputs Percentage

Timing

Submission of Inception report and work plan

20% Within 7 days after award of contract.

Submission of Preliminary Report 30% Within 1 month from the date of award of contract.

Submission of draft of the study report

20% Within 5 months from the date of award of contract.

Submission of final report on completion of all activities as per the ToR

30% Within 6 months from the date of award of contract.

5

Person(s) to review/inspect/ approve outputs/completed services and authorize the disbursement of payment

Programme Analyst, UNDP India Resource Person and Moderator, Microfinance Community of Practice, Solution Exchange

Type of Contract to be Signed

☐ Purchase Order

☐ Institutional Contract

☒ Contract for Professional Services

Criteria for Contract Award

☒Compliance on Preliminary Examination of Proposals

☒Compliance on Essential Eligibility/Qualification requirements

☒Highest Combined Score (based on the 70% technical offer and 30% price weight distribution)

☒ Full acceptance of the UNDP Contract General Terms and Conditions (GTC). This is a mandatory criteria and cannot be deleted regardless of the nature of services required. Non acceptance of the GTC may be grounds for the rejection of the Proposal.

Criteria for Preliminary Examination of Proposals

1. Bid was received on or before the date and time specified 2. Technical Offer separately sealed from Financial Offer 3. Details of Personnel to be engaged in the Contract Submitted 4. Implementation Timetable submitted 5. Latest Certificate of Registration of Business submitted 6. Latest Audited Financial Statements submitted 7. Is the Offeror, or any of its joint venture member, included in UN

Security Council 1267 List, Suspended and Removed vendors list 8. Is the performance of the offeror, any of its Joint Venture Member,

or any of the proposed key personnel found satisfactory in previous assignments with UNDP

Criteria for Essential Eligibility/Qualification

Not-for-profit institutions/ cooperatives / private or public limited companies/ Government institutions, having a minimum of 5 years of experience of working/ supporting/ training/ research and consultancy in the area of cooperatives/ Financial inclusion/Financing

Team Leader having minimum experience of 5 years in financial cooperatives / financial inclusion / undertaking research and consultancy at the national level

The team members having minimum 2 years of knowledge and experience of working on microfinance issues, cooperatives - especially financial cooperatives, governance and management of community based institutions/ cooperatives; and understanding of cooperative Acts and laws.

Note: 1. If bidders do not meet any of the above listed criteria, their proposal will not be considered for further evaluation. 2. Bidders meeting above listed criteria are required to submit evidences (details / documents) in support – otherwise proposal may be disqualified.

6

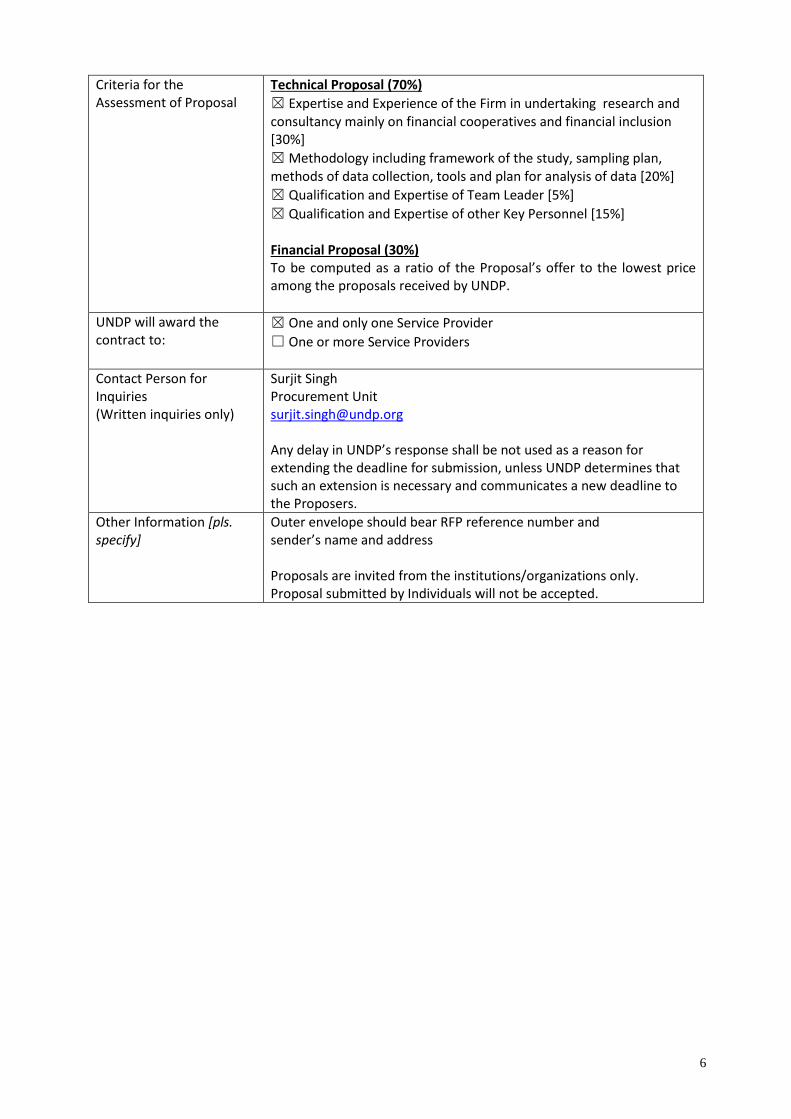

Criteria for the Assessment of Proposal

Technical Proposal (70%)

☒ Expertise and Experience of the Firm in undertaking research and consultancy mainly on financial cooperatives and financial inclusion [30%]

☒ Methodology including framework of the study, sampling plan, methods of data collection, tools and plan for analysis of data [20%]

☒ Qualification and Expertise of Team Leader [5%]

☒ Qualification and Expertise of other Key Personnel [15%] Financial Proposal (30%) To be computed as a ratio of the Proposal’s offer to the lowest price among the proposals received by UNDP.

UNDP will award the contract to:

☒ One and only one Service Provider

☐ One or more Service Providers

Contact Person for Inquiries (Written inquiries only)

Surjit Singh Procurement Unit [email protected] Any delay in UNDP’s response shall be not used as a reason for extending the deadline for submission, unless UNDP determines that such an extension is necessary and communicates a new deadline to the Proposers.

Other Information [pls. specify]

Outer envelope should bear RFP reference number and sender’s name and address Proposals are invited from the institutions/organizations only. Proposal submitted by Individuals will not be accepted.

7

Annex 2

Terms of Reference

Study of Financial Cooperatives in the context of Financial Inclusion in India

Global and Indian Scenario of Financial Cooperatives

Global Scenario: Financial cooperatives are important players in the world banking system, reaching the poorest people and having a substantial economic impact. Worldwide, they serve over 857 million people, including 78 million living on less than $2 a day, and represent 23 per cent of all bank branches. Financial cooperatives include both cooperative banks (based mainly in Europe) and credit unions (set up originally in North America and developing countries), as well as banks owned by agricultural or consumer cooperatives. Cooperative banks, although member-owned, can have non-members as customers, whereas credit unions are licensed to serve members only.1 In Europe, there are 4,000 cooperative banks active in 20 countries, with 50 million members, 780,000 employees, €5.65 billion in assets and an average market share of 20 per cent.2 Worldwide, there are over 51,000 credit unions that operate in 100 countries, with 196 million members and $1.56 billion in assets. It is a fact that financial cooperatives including Credit Unions are the first and original microfinance institutions in the world. The present financial cooperatives existing in the form of credit unions, thrift and credit cooperatives, Primary Agriculture Credit Cooperatives (PACS), rural and urban cooperative banks etc. are in one way or the other based on the lessons drawn from the well-known models promoted by Raiffeisen, Shultze – Delitzsch, Dr. Wollemborg, Desjardins and Rochdale pioneers. In the context of inclusive development, cooperatives are critical institutions for both social and financial inclusion. Whereas the social inclusion issue is addressed by sub-sectoral and service cooperatives, savings and credit cooperatives function as intermediaries of inclusive finance. Cooperatives play a significant role in the provision of microfinance services to the poor, globally. Some of the largest banks in the world are cooperatives: Rabo Bank, for instance, has 50% Dutch citizens in membership. It is rated as the world’s third-safest bank.3 A comprehensive report of ILO (2009) “Resilience of cooperative Business Model in Times of Crisis” informs that saving and credit cooperatives (also known as credit unions or SACCOs), building societies and cooperative banks all over the world are reporting that they are still financially sound, and that customers are flocking to bank with them because they are highly trusted4. Financial inclusion and role of financial cooperatives in India The CRISIL report considers that the cooperative movement was the first effort towards financial inclusion. As per the CRISIL Report on Financial Inclusion - “Financial inclusion is certainly not just a recent phenomenon. In India, the earliest effort at financial inclusion can be traced back to 1904, when the co-operative movement began in the country5.”

1 Report of the Secretary-General Cooperatives in social development and the observance of the International Year of Cooperatives, 22 July, 2013 (http://daccess-dds-ny.un.org/doc/UNDOC/GEN/N13/402/80/PDF/N1340280.pdf) 2 International Labour Organization, Resilience in a downturn: The power of financial cooperatives (Geneva,

International Labour Office, 2013). 3 DFID and UK Aid. 2010. Briefing notes - Working with cooperative for poverty reduction. DFID,UK

4 ILO, Resilience of cooperative Business Model in times of crisis. 2009 pp.2

5 http://indiamicrofinance.com/wp-content/uploads/2013/08/CRISIL-Inclusix-financial-inclusion-india-report.pdf

8

The Indian financial cooperative system is complex in nature but it is the largest financial cooperative system in the world, in terms of people served. An article by Dave Grace (2008) informs - “Together, the urban sector, three tiered short-term rural sector and credit societies serve an estimated 267 to 390 million people. This compares to the second largest financial cooperative movement in the world in China which serves approximately 200 million people6.”

Present Scenario of Financial Cooperatives in India

Financial Cooperatives in India

Credit Cooperatives (95156)

Rural Cooperatives (93550) Urban Banks ( 1606)

Short Term ( 92833) Long Term ( 717)

Scheduled ( 51) Non-Scheduled (1555)

State Cooperative Banks (31)

State Cooperative Agriculture and Rural Development Banks ( 20)

Multi State (25) Multi State (21)

District Cooperative banks (370)

Primary Cooperative Agriculture and Rural Development Banks (697)

Single State (26) Single State ( 1534)

Primary Agriculture Cooperative Societies ( 92432)

Figures in Parentheses indicate the number of institutions at end March 2013 for UCBs

and at end March 2012 for rural cooperatives

For rural cooperatives, the number of cooperatives refer to reporting cooperatives Source: RBI Report – “Developments in Cooperative Banking” 2013

It is important to note here that the RBI data covers only those financial cooperatives that are reporting to RBI. The new age or self-reliant cooperatives that have emerged in the recent past are not included in this data. Hence it is pertinent to have a glimpse of the financial cooperatives registered under self-reliant or Multi state cooperative Act that are undertaking financial inclusion initiatives. The first primary level agriculture cooperatives in India were Primary Agriculture Cooperative Societies (PACS). These cooperatives are multipurpose in nature as they provide credit as well as also conduct business in input supply ( fertilizers, seeds and pesticides etc.) andconsumer services. Many PACS are also functioning as Mini banks with the support of District Cooperative Banks (DCCBs). As per the RBI data of 2013, there exist 92432 PACS and 370 DCCBs. Agribusiness Financial Cooperatives In the recent past several good initiatives have been taken up in terms of establishing agribusiness cooperatives in India especially after introduction of Self-reliant Cooperative Societies Act. Organisations like Mulkanoor Co-operative Rural Bank and Marketing Society Ltd., Andhra Pradesh have annual turnovers of INR 15.68 million and the products of the society includes financial services, input supply services, marketing services, consumer services, and welfare services. Buldana Urban Cooperative society Ltd. is an urban-based cooperative but provides a lot of services to farmers.

6 Dave Grace, Financial Cooperatives in India: Where Are the members.CAB Calling, pp.10, Jan-March2008,

9

Ware-House Receipt Loan and Gold Loan are two good examples. It was established in 1986 with a small capital of INR 12,000 and has crossed an unbelievable sum of INR 25820 million. It has 14 types of deposit schemes available with the society. There are several all-women banks such as SEWA bank, Bhagini Nivedita Cooperative Bank, Mann Deshi Cooperative Bank and agriculture cooperatives like Rawain Women’s Multipurpose Autonomous Cooperative Society Ltd. (RWMACS), Uttarkashi, Uttarakhand and Apni Shakari Sewa Samiti Ltd. Jaipur, Rajasthan that are successfully functioning and providing support to farmers. It is important to mention here that there are large number of Farmers Producer organisations in India which are predominantly functioning as producer companies, however in terms of providing financial services to their members they are unable to do so, and depend largely on external sources. Multipurpose agriculture cooperatives can be a good option for them but due to weakness of various state Acts farmer opt for producer company mode. The proposed study will also be useful in terms of suggesting changes in Cooperative Acts so that farmers opt for creating agribusiness cooperatives for their benefit. Purpose of Undertaking the Study On various forums, including Microfinance India Summit 2013, it is being realized that there is a need to do an in-depth study of financial cooperatives in India to - identify the regulatory gaps that are existing in different cooperative Acts in context of financial inclusion; Document the successful financial cooperatives including Primary Agriculture Cooperative Societies (PACS), Cooperatives functioning as federations of SHGs and also cooperative Banks (traditional as well as new age); and also to analyse the value chains of various microfinance services (savings, credit, insurance/micro-pensions, remittances and Micro leasing) as well as financial management and governance related issues of cooperatives. Keeping in view of the same, Microfinance Community of Practice conducted an e-discussion on the issue of undertaking a study and also a small group workshop. The outputs of the two initiatives will facilitate in developing methodology, selecting the sample and also in conduct of the study. The links to access the final outputs are given for reference: E - Discussion: http://in.one.un.org/img/uploads/SolEx_FTP/MF/cr-se-mf-07071401_Cooperatives.pdf Small Group Workshop: http://in.one.un.org/img/uploads/SolEx_FTP/MF/Report-of-Small-Group-Workshop-Financial-Cooperative.pdf There have been several initiatives taken up by Microfinance Community of Practice, Solution Exchange on financial cooperatives. The outputs of the initiatives are given at Annexure -1. The summary of the latest discussion on the need and methodology of the study is also given at Annexure -2) Result of the study: As a result of the study, it is envisaged that the recommendations of the study will facilitate in making changes in policy and regulatory environment for financial cooperatives, undertaking innovations required in products and services and delivery mechanism, and adopt strategies to strengthen financial cooperatives so that they better contribute for financial inclusion.

10

Framework showing various constituencies and results of the study

Gaps/ Needs of various subsets of

Cooperatives engaged or going to be

undertake Microfinance Activities/ Financial

Inclusion

Identification of Policy

Issues requiring legal/ Regulatory Changes

Implementation Gaps/

Gaps in the Value chains

requiring regulatory changes or implementation

of policy decisions

Cooperative Acts, Rules and Regulations requiring changes in the provisions

Multi State Cooperative Societies Act

MACS/ Self-Reliant Cooperative Acts

Cooperative Societies Acts of Different

States (Old Acts) Banking Regulation Act

Changes in different Acts Bylaws of Cooperatives

Key Constituencies/ Stakeholders

Government of India/ State

Government ( Department of

Cooperation) and Other Relevant

Ministries Registrar Offices of Various

States

Reserve Bank of India, NABARD,

UN Organizations, Donor

agencies, International Organizations

International Cooperative

Alliance NCDC,

Training/ Academic institutions

NGOs, Research Organizations,

Activities to be taken up under the project

National Level Study on Policy, Regulations issues/Acts and MF operational issues

Dissemination of the Outputs of the studies

in the form of report/ Publication

Policy and Advocacy – Through a small

groups

Relevant MF subsectors/

Activities and their value chains Savings,

Credit,

Micro - insurance,

Remittance / Payment Services Micro Leasing

Streamlined Policies and regulations related to cooperatives

More Autonomy in Cooperatives and clarity of operations

Clear Legal and Regulatory Scenario

More effective Governance, Management and operational environment of cooperatives in

context of MF

Strengthened Cooperative Institutions in Terms of Business, Governance and management Improved Financial Inclusion and MF Services for the Poor

Financial Cooperatives functioning at various levels

11

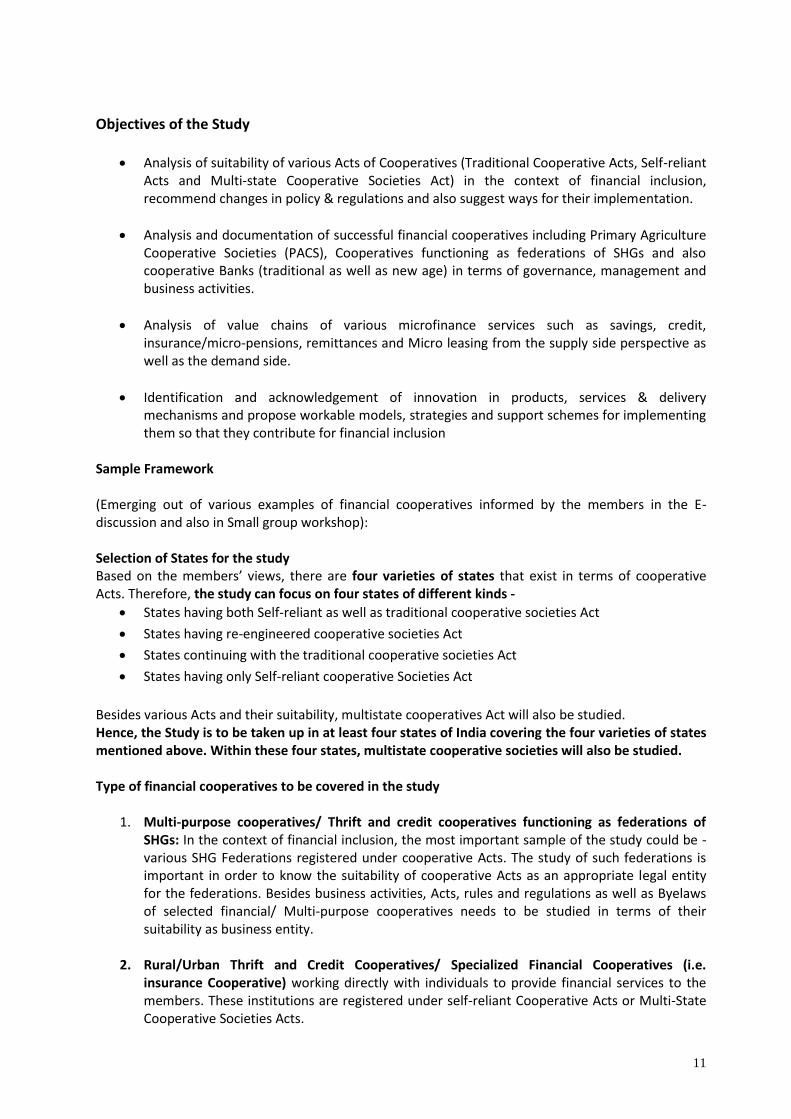

Objectives of the Study

Analysis of suitability of various Acts of Cooperatives (Traditional Cooperative Acts, Self-reliant Acts and Multi-state Cooperative Societies Act) in the context of financial inclusion, recommend changes in policy & regulations and also suggest ways for their implementation.

Analysis and documentation of successful financial cooperatives including Primary Agriculture Cooperative Societies (PACS), Cooperatives functioning as federations of SHGs and also cooperative Banks (traditional as well as new age) in terms of governance, management and business activities.

Analysis of value chains of various microfinance services such as savings, credit, insurance/micro-pensions, remittances and Micro leasing from the supply side perspective as well as the demand side.

Identification and acknowledgement of innovation in products, services & delivery mechanisms and propose workable models, strategies and support schemes for implementing them so that they contribute for financial inclusion

Sample Framework (Emerging out of various examples of financial cooperatives informed by the members in the E-discussion and also in Small group workshop): Selection of States for the study Based on the members’ views, there are four varieties of states that exist in terms of cooperative Acts. Therefore, the study can focus on four states of different kinds -

States having both Self-reliant as well as traditional cooperative societies Act

States having re-engineered cooperative societies Act

States continuing with the traditional cooperative societies Act

States having only Self-reliant cooperative Societies Act

Besides various Acts and their suitability, multistate cooperatives Act will also be studied. Hence, the Study is to be taken up in at least four states of India covering the four varieties of states mentioned above. Within these four states, multistate cooperative societies will also be studied. Type of financial cooperatives to be covered in the study

1. Multi-purpose cooperatives/ Thrift and credit cooperatives functioning as federations of SHGs: In the context of financial inclusion, the most important sample of the study could be - various SHG Federations registered under cooperative Acts. The study of such federations is important in order to know the suitability of cooperative Acts as an appropriate legal entity for the federations. Besides business activities, Acts, rules and regulations as well as Byelaws of selected financial/ Multi-purpose cooperatives needs to be studied in terms of their suitability as business entity.

2. Rural/Urban Thrift and Credit Cooperatives/ Specialized Financial Cooperatives (i.e. insurance Cooperative) working directly with individuals to provide financial services to the members. These institutions are registered under self-reliant Cooperative Acts or Multi-State Cooperative Societies Acts.

12

3. Primary Agriculture Cooperative Societies that are functioning as Self-help Promotion Institutions or as Business Correspondents of banks and catering to the needs of the poor.

4. Cooperative banks registered under traditional cooperative Acts at the rural levels - State

cooperative Banks, District cooperative Banks, State Agriculture and rural development Banks, Primary Cooperative Agriculture and Rural Development Bank (PCARDBs), having special focus on Micro financing and functioning as Self-Help Promotion Institution.

5. Urban Cooperative Banks registered under traditional Acts or Self-Reliant Cooperative Acts or Multi-state Cooperative Societies Act - All-women as well as general Urban Cooperative Banks

Scope of work

1. Sample-based Study: The study will focus on four states selected as sample for the study. It needs to be ensured that all the four varieties mentioned above are covered while selecting the states.

2. It is a systematic study to be done at two levels – Macro and Micro – At the Macro level the issues related to policy and regulations are to be covered whereas at the micro level case studies of financial cooperative needs to be undertaken in terms of financial inclusion and providing of MF services to their members.

3. Study on Regulatory scenario of cooperatives: This Study will be holistic in nature and will focus on the legal framework, Structure, various cooperative Acts to assess the gaps /Provisions to be changed focusing on each subset/type of cooperatives. The study will look into other relevant Acts which are influencing the MF activities taken up by cooperative Banks/ institutions.

4. Value Chains of Financial Services through Cooperatives: This Study will look into the operational (including management) and Governance related issues by undertaking case studies of various experiments of micro financing through cooperatives. The focus will be on the value chains of different microfinance products and services considering economic, operational and management related issues/ activities.

Submission of Proposals Interested agencies should submit their proposals clearly, mentioning the following points in not more than 15 pages (excluding Annexures):

Organizational strengths to undertake the task, particularly highlighting their strengths in conducting studies on cooperatives, especially financial cooperatives

Clear methodology for undertaking the study – Sample frame, sampling process, data collection methods and tools, process of analyzing data and report format

Details of core team members with requisite knowledge and experience

Justification for each team member, with clearly defined roles and responsibilities Action plan

to demonstrate and assure that task will be completed within the given timeline

Expected Outcomes and Steps to be followed: Immediately after the award of the assignment/signing of the contract, the selected agency will be invited to an inception meeting to make a presentation and obtain necessary inputs regarding the study approach, methodology, study samples, report structure and the action plan.

13

The expected outputs of the study are as follows: 1. Inception Report:

Based on the inputs received in the inception meeting, the agency should submit the inception report including understanding of the assignment, scope of the agreed work, detailed methodology, study samples, criteria to identify cases, indicative format for case-documentation, indicative structure of the final report, and time-bound action plan.

2. Preliminary Report – Phase 1 report:

In the first Phase of the study, following are expected to be completed –

Report of the analysis of various studies and reports of committees on cooperatives especially related to financing/ Financial inclusion

Report of macro-level environment of financial cooperatives - International regulatory norms, with clear and relevant examples of regulations; summary of different policies, relevant to the Indian situation, regulations and Acts in context of financial inclusion in India; gaps in policy and Acts that are inhibiting progress of financial inclusion through cooperatives; policy/regulatory changes required to streamline the working of financial cooperatives in India.

This will entail desk research and if required telephonic interviews can be taken by the study team to understand the practice part. Various clauses of different Acts of the states will be analyzed in this phase. 3. Field study and Submission of First draft of the study report with Case Studies, Second phase:

The second phase will involve extensive field study. At least four states will be covered in the context of applicability of various Acts relating to financial inclusion. Within these four states, 15 case studies will be taken up as per the sample plans. Six case studies will be undertaken in the sample state(s) having two Acts functional whereas two case studies each (Six Case Studies) will be done in the remaining states wherein only one Act is applicable. Besides case studies of the societies registered under state Acts, three case studies of Multi-State Cooperatives will also be undertaken in the selected states of the study. These case studies will preferably be taken up in the selected states only. If there are one or two multistate cooperatives that are functioning in the state other than four selected states, the study can be done in the context of assessing the particular sample cooperatives. Hence, a range of financial cooperatives will be covered in the study. The focus will not be on number of states but variety of cases; therefore the number of case studies to be undertaken can be increased. First Draft Report will be prepared after completing the field work in at least four sample states and also case studies of multi-State cooperatives. The agency is expected to present the first draft report in order to obtain necessary feedback and fill the gaps, wherever required. 4. Submission of Final report: Final Report to be submitted within one month of the presentation of

draft report

14

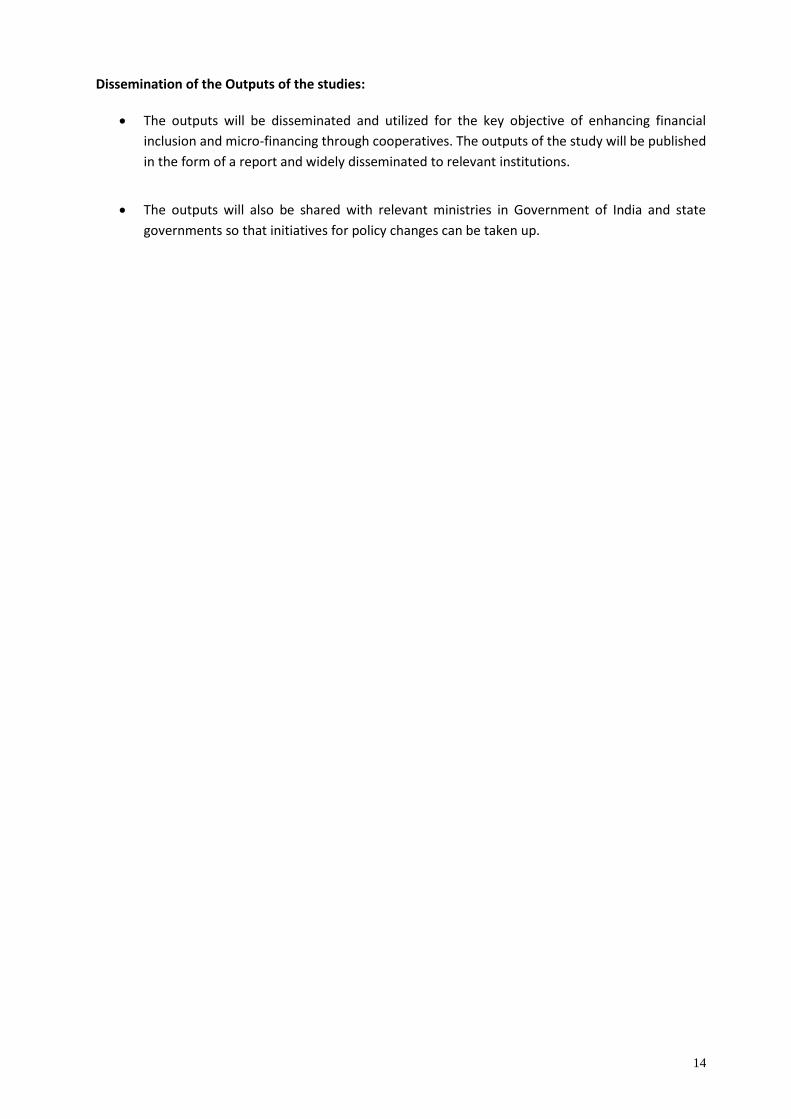

Dissemination of the Outputs of the studies:

The outputs will be disseminated and utilized for the key objective of enhancing financial

inclusion and micro-financing through cooperatives. The outputs of the study will be published

in the form of a report and widely disseminated to relevant institutions.

The outputs will also be shared with relevant ministries in Government of India and state

governments so that initiatives for policy changes can be taken up.

15

Annexure – 2.1

Initiatives on Cooperatives taken up by Microfinance Community of Practice from (2009 – 2013) Discussions conducted in the Microfinance Community on Cooperatives

Documentation of Case Studies on Microfinance through Cooperatives. Available at: ftp://ftp.solutionexchange.net.in/public/mf/cr-public/cr-se-mf-11021001-public.pdf

Enabling Cooperative Societies Acts for Fast Tracking Microfinance and Financial Inclusion in India. Available at: ftp://ftp.solutionexchange.net.in/public/mf/cr-public/cr-se-mf-11090901-public.pdf

Microfinance for Small Farmers through Exclusive Agriculture Credit Cooperatives and JLGs. Available at: ftp://ftp.solutionexchange.net.in/public/mf/cr/cr-se-mf-food-13020901-public.pdf

Action Group on Cooperatives Reports related to Action Group on Strengthening Cooperative Acts in Context of Financial Inclusion and Micro Financing Concept Note of the Action Group - ftp://ftp.solutionexchange.net.in/public/mf/resource/res_info_14100902.pdf Minutes of the Meeting of Action Group on ‘Strengthening Cooperative Acts in the Context of Financial Inclusion and Micro Finance: ftp://ftp.solutionexchange.net.in/public/mf/resource/res_info_29100901.pdf Report of the National workshop including Action Group Meeting Report - ftp://ftp.solutionexchange.net.in/public/mf/resource/res_info_261109.pdf Recent initiatives - E-discussion and small group workshop on the study (2014)

E – Discussion on conducting a national study of Financial Cooperatives in context of Financial Inclusion in India The Consolidated Reply is Available at: http://in.one.un.org/img/uploads/SolEx_FTP/MF/cr-se-mf-07071401_Cooperatives.pdf Small Group Workshop on Study of Financial Cooperatives in context of Financial Inclusion in India. The report of Small group workshop is available at: http://in.one.un.org/img/uploads/SolEx_FTP/MF/Report-of-Small-Group-Workshop-Financial-Cooperative.pdf

16

Annexure –2.2

Summary of the e-discussion in Solution Exchange on Study of Financial Cooperatives in context of Financial Inclusion in India

(Summary provides several successful examples of financial cooperatives and suggestions related to

the study. For accessing complete Consolidated reply please visit: http://in.one.un.org/img/uploads/SolEx_FTP/MF/cr-se-mf-07071401_Cooperatives.pdf

In the last two decades, there have been several important developments in the cooperative sector that have influenced the agenda of financial inclusion. These developments include - emergence of Model Cooperatives Societies Act; enactment of MACS / Self-Reliant Cooperative Societies Acts in different states; re-engineering of old Cooperative Societies Acts through amendments in various provisions; reduction in Government’s equity and their control; application of revival package for rural cooperative credit institutions; and legal reforms/amendments in cooperative credit structure/societies as a result of acceptance of revival package for short term cooperative credit structure. These reforms were results of the recommendations made by various important committees headed by Chaudhry Brahm Prakash, Jagdish Capoor, Vikhe Patil, V S Vyas and Prof. Vaidyanathan. In the context of financial inclusion, enactment of the Mutually Aided Cooperative Societies Act by the Andhra Pradesh government in 1995, was a significant step towards cooperative reforms. Following the example of Andhra Pradesh, eight other States (viz., Bihar 1996, Jharkhand 1996, Chhattisgarh 1999, Jammu and Kashmir 1999, Madhya Pradesh 1999, Karnataka 2001, Odisha 2002 and Uttaranchal 2003) have also passed similar legislations to liberalise cooperatives and provide more autonomy to the members. Moreover, in context of 97th Constitutional Amendment, liberal cooperative laws that are existing in several states are either amended or deemed to be amended. Unfortunately, two state governments - MP and Odisha repealed the liberal cooperative laws in their states. Reforms in financial cooperatives are carried out to a large extent by National Bank for Agriculture and Rural Development (NABARD) especially in context of recommendations of Vaidyanathan committee. Besides de-bureaucratization and de-politicization, reforms were also intended to bring changes in accounting system, skills in manpower and technology introduction. NABARD had supported an evaluation in three states, viz., Andhra Pradesh, Bihar and Madhya Pradesh. The outcome of the reforms was encouraging in MP as well as Bihar. In Bihar, changes in the Act brought more inclusion. Such evaluation reports will be useful for literature review in the proposed study. Members also informed that the recent report of Dr. Nachiket Mor Committee on Financial Inclusion acknowledges the efforts made by Financial Cooperatives in enhancing access to finance and therefore it can be referred. Changed scenario of financial cooperatives Historically, financial inclusion through cooperatives was taken up more in rural areas through District cooperative banks (DCCBs) and Primary Agriculture Cooperative Societies (PACS). Gradually, urban cooperative banks and urban thrift and credit cooperatives also started contributing for the financial inclusion keeping their focus primarily in urban areas. After introduction of Mutually Aided Cooperative Societies Act popularly known as Self-Reliant Cooperative Act, the scenario of financial cooperatives has further widened. The existing legal and regulatory structure of cooperatives in India is quite complex as different states are have different cooperative societies Acts. More precisely, based on the legal scenario, states in India can be classified into four categories:

States having both Self-reliant as well as the traditional cooperative societies Act

States having re-engineered cooperative societies Act

States continuing with the traditional cooperative societies Act

17

States having only Self-reliant cooperative Societies Act

Presently, the Indian financial cooperative system consists of:

Primary Agricultural Cooperatives (PACS) and their federal bodies – District Cooperative Banks and State Cooperative Banks (The three tier short term credit structure)

Agriculture and Rural Development Banks (varying structures in different states)

Urban Cooperative Banks ( registered under old state level cooperative Acts and also Multistate Cooperative Society Act)

Financial cooperatives registered under the old state level cooperatives Acts

Financial cooperatives including Multipurpose cooperatives, Salary earner’s cooperative societies and insurance cooperatives registered under the Multi State Cooperatives Act

Thrift and credit cooperatives registered under Self-reliant cooperative Acts applicable in several states

Self-Reliant Cooperatives: The self-reliant financial cooperatives are often promoted by Self- Help Promotion Institutions. These cooperatives are having the potential of managing financial systems and their own organization democratically. Several cooperatives extend services such as provision of small to large size credit, insurance and pension services through partnering with other agencies and savings accounts to encourage members to save money. A number of such cooperatives also provide livelihood support services including marketing linkages and social services in terms of accessing government schemes, addressing women’s issues and taking up community development activities. Traditional financial cooperatives that are engaged in banking activities come under the preview of RBI regulations and therefore these cooperatives are reporting regularly and being monitored. The reported data is available with RBI and being utilised for preparation of various reports. The data of self-reliant cooperatives is not being collated at one place and therefore there are information gaps related to the data on such cooperatives at state and national level. Financial Cooperatives registered under self-reliant cooperative Act face capital constraints to meet the required large size loan demands from their members as their members are from the poor economic category and can only pool capital of a certain amount. These cooperatives are neglected by the banks and other financial agencies to provide capital despite their good quality and governance. The Government needs to provide enabling environment for them to operate as small but significant niche player servicing limited geographies and specialized clientele. In the context of self-reliant cooperatives, members also shared the initiatives taken up by a Karnataka based leading NGO – ‘Sampark’ that has federated its SHGs and got the federations registered under the self-reliant cooperatives (SRC) Act of Karnataka. The external loans to these cooperatives are mostly provided through NABARD Financial Services Limited (NABFINS) and repayment percentage ranges from 98 to 100 percent. As banks in Karnataka are not extending loans to self-reliant cooperatives, their information does not enter district and state level bankers’ committees’ reports. Within the microfinance sector, Self-reliant cooperatives therefore remain unrecognized and unreported. Members also shared about ILO/CIDA pilot project - “Testing a Cooperative Approach to Poverty Alleviation among Tribals in Bihar". Rabo bank provided support in the form of a Revolving Loan Fund to provide seed money for purchase of raw material, agricultural inputs, retail business, etc. At the end of project period, the RLF component was formalized as the "RLF Swavalambi Sehkari Samiti Ltd" under the new Self Supporting Coop Societies Act. Even years after the project phased out, the RLF cooperative is sustaining well in terms of business and linkages. Members quoted another example of a SHG-federation in Pithoragarh, Uttarakhand. This was formed with the support from the Canadian Center for International Studies and Cooperation. After the project phased out, the federation is on its own. Both the examples are of self-reliant cooperatives which are operational and working successfully.

18

International Experience: Stressing on the issue of assessing the regulation and supervision in financial cooperatives, members quoted the example of credit unions in the countries like Germany, Canada and Ireland wherein the main reason of success has been strong regulation and supervision. Robust regulations seem to be important ingredient for the success of Credit Unions. In India, contradictory and multiple regulatory provisions, combined with the fact that those provisions allow bureaucrats and politicians to interfere and control such institutions, is one of the key reasons for less than optimal performance of financial cooperatives in India. Referring to the regulations and supervision guide book of World Council of Credit Unions (WOCCU’s), members shared core principles underlying credit unions supervision. While these principles convey that cooperative unions should operate free of government interference with management, it also stresses on supervision of credit unions by a government agency. Need of a National level Study The need of having a national level study on financial cooperatives is strongly realised by the members. They suggest to keep the focus of the study on those cooperatives which are having financial inclusion or financing for low incomes households as their primary objective. The study at a national level is required to do analysis at two levels – Macro and Micro. At the macro level, analysis needs to be done in context of the regulatory and management scenario of financial cooperatives and support available from various sources including NABARD and Government of India/state governments. Further, at the micro level, various financial cooperatives are to be studied in context of their governance, management, products and services, delivery mechanism and coverage so as to know the success factors as well as gaps that are existing at the society level. This will help in identifying the policy as well as operational and systemic gaps that require urgent attention at various levels and by different stakeholders. The study can also look into sustainability aspects in respect to SHG linkages with the financial cooperatives. The study should also give due emphasis on the problems related to loaning, tracking system of delinquencies and reasons of increasing Non-Performing Assets. Sample Frame of the study In terms of sample frame, members suggested following options to classify and select samples organisations for the study:

Multi-purpose cooperatives/ Thrift and credit cooperatives functioning as federations of SHGs: In context of financial inclusion, the most important sample of the study could be - various SHG Federations registered under cooperative Acts. The study of such federations is important to know the suitability of cooperative Acts as an appropriate legal entity for the federations. Besides business activities, it will be good to analyse the Acts, rules and regulations, and Byelaws of selected financial/ Multi-purpose cooperatives in terms of their suitability as business entity.

Rural/Urban Thrift and Credit Cooperatives/ Specialised Financial Cooperatives (i.e. insurance Cooperative) working directly with individuals to provide financial services to the members. These institutions are registered under self-reliant Cooperative Acts or Multi-state Cooperative Societies Acts.

Primary Agriculture Cooperative Societies that are functioning as Self-help Promotion Institutions or as Business Correspondents of banks and catering to the needs of the poor.

Cooperative banks registered under traditional cooperative Acts at the rural levels - State cooperative Banks, District cooperative Banks, State Agriculture and rural development Banks, Primary Cooperative Agriculture and Rural Development Bank (PCARDBs), having special focus on Micro financing and functioning as Self-Help Promotion Institution.

19

Urban Cooperative Banks registered under traditional Acts or Self-Reliant Cooperative Acts or Multistate Cooperative Societies Act - All women as well as general Urban Cooperative Banks

Suggested parameters for selecting a range of sample cooperatives:

Location (Geographical area) of the cooperative: proximity to and remoteness from town

Age of the cooperatives; <=5 years and more than 5 years;

Size of the cooperative

Cooperatives that are registered legally with self-reliant act and normal state cooperative act

Member’s composition (mixed, women, men, socially excluded categories, etc.)

Activities of the cooperative - financial and non-financial services

Donor/NGOs promoted and government programme promoted

Cooperatives linked with banks and government schemes and cooperatives not linked Sample Size: On the sample size, members have given different views – while some members suggested to cover 25-30 cooperatives using above criteria from 5 regions (South, North, East, West, North-East) in order to get a complete sample representation across the country and get comparative perspectives on the quality of cooperatives; others suggested to study 8 financial cooperatives in 4 states. Out of these four states, at least two states needs to be those where self-reliant cooperative Act is in operation. Another group of members suggested for a more comprehensive study. They proposed for 10 case studies of cooperatives that are internationally known, Assessment of 500 cooperatives using rapid assessment tool, and 10 consultations at state and national level with leaders, civil society organizations, academic institutions, government officers and donor organizations. Some of the Financial Cooperatives suggested by members for the proposed study

Rural Cooperative Banks - District Cooperative Bank, Bidar, Karnataka

Primary Agriculture Cooperative Societies (PACS) of Salem and Thanjavur districts that promote SHGs in their area

Urban Cooperative banks - Cuttack Urban Cooperative Bank – (urban cooperative bank having innovative products/ mechanism to deliver services)

Women Cooperative Banks -Shri Mahila SEWA Sahakari Bank Ltd. (SEWA Bank), Mann Deshi Mahila Sahakari Bank , Maharastra and Bhagini Nivedita Sahakari Bank Limited, Pune

Specialised cooperative - National Insurance Vimosewa Cooperative Ltd.- a financial cooperative providing insurance services only

Members also suggested a number of Thrift and Credit/ Multipurpose Cooperative institutions that are working well. These cooperatives include - Al-Khair Cooperative Credit Society, Patna (A cooperative model of ‘Interest-free’ Micro financing); Annapurna Mahila Cooperative Credit Society, Mumbai; Rawain Women’s Multipurpose Autonomous Cooperative Society Ltd., Uttarkashi (A multipurpose cooperative promoted by Himalayan Action Research Centre, Uttarakhand); Marwar Sharia Co-operative Credit and Savings Society, Jodhpur (A thrift and credit cooperative of minorities established by the Marwar Muslim Educational and Welfare Society); Indian Cooperative Network for Women (A unique multipurpose women cooperative registered under multi state cooperative Societies Act - promoted by Working Women’s Forum, Chennai) ; and Ankuram Sangamam Poram, Hyderabad Some more examples of successful financial cooperatives given by the members: CAMEL , Nellur, Andhra Pradesh; Eshwara, Bhumika, Gavisiddeshwara Souharda cooperatives (Self-reliant cooperatives promoted by Sampark, Karnataka); Apani Sahakari Sewa Samiti ltd, Jaipur (promoted by Centre for Community Economics and Development Consultants Society - CECOEDECON); Cooperatives promoted by GRAM, Andhra Pradesh; Cooperatives promoted by Cooperative

20

Development Foundation; Stree Nidhi Credit Cooperative Federation Ltd, Andhra Pradesh; Sewani multi-purpose society – A cooperative society near Surat. Some Additional suggestions of members about the study

Study Financial cooperatives in Uttar Pradesh and U.P. Co-operative Societies Act, 1965 in context of financial inclusion

Take Samples from North East, Hilly areas and Tribal areas for the study - At least one district cooperative bank of mountain region needs to be studied

Study not only “successful” but also “unsuccessful” cooperatives to identify factors of failure

Do comparative analysis of Cooperatives registered under the traditional Act, and those registered under the self-reliant Acts

Study financial inclusion through cooperatives in rural and urban areas separately

In addition to cooperatives, study Kshetriya Gramin Financial Services - a rural financial services delivery model designed and owned by IFMR Rural Finance and promoted by IFMR Trust.

Enumerate the challenges that financial cooperatives encounter in context of providing microfinance services to their members.

Sampling Methods: As far as sampling methods are concerned a group of members suggested using Multi Stage Random Sampling Method for selecting cooperative institutions. Another group of members suggested to utilise purposive sampling method for selecting the samples at various levels. Methods of data collection: A mix of quantitative and qualitative methods are suggested for data collection for the study. These methods include Focus Group Discussions (FGDs) with Board members, staff, members of the cooperative; Case studies of cooperative, leaders, member households; Interviews/ FDGs with various stakeholders and Key informants interviews. Members also suggested for having discussions with RBI, NABARD, donors, SCBs/DCCBs and also National Rural Livelihood Mission and their State Rural Livelihood Missions on their perceptions, policies and practices in recognising, lending and giving development grants to and through Self-reliant cooperatives. Tools: Questionnaire survey for Cooperatives; Schedules for members of cooperatives, PRA: Venn diagram, Rating Tool etc. Macro level review and analysis – Views and Suggestions of the members The study should review and assess the current regulatory regime. It can focus on the policy framework in different states, analyse whether the policy enables smooth functioning of cooperatives with due respect to their autonomy and conducive for the growth of financial cooperatives. It is important to document the experiences of cooperative structures (both state promoted and self-reliant) and consolidate them for maximising the potential to contribute to financial inclusion. It will also be important to understand and study the external ecosystem factors which are impeding the growth of self-reliant, self-sufficient cooperative movement to emerge. External factors include - economic, socio-cultural, gender, technological, political, legal and other factors. Member felt importance of enumerating the internal design features which will help emergence of true cooperatives - member owned and controlled entities - governance, member alliance and operating systems including product features and design. At the macro level it is also essential to review contribution of cooperatives to financial inclusion, difference in the cost of services by cooperatives compared to other mainstream banks, efficiency, productivity, profitability, sustainability of financial cooperatives and their social relevance. It will be useful to do analysis of a single-purpose institutions with that of multi-purpose institutions. Assessing Policy Constraints: An important component of the study should be the policy constraints in promoting and strengthening different types of financial cooperatives.

21

Data base of self-reliant cooperatives: An important issues of self-reliant cooperatives is that there is no data available on how many self-reliant cooperatives exist in the country, how many do well and do not do well and what are the issues faced by these cooperative, etc. Developing a database on financial cooperatives including multi-purpose ones prevalent across India, an institution should be assigned to update such database on a periodic basis and it can also be portrayed on the map of India. Members raised question marks on viability issues of financial cooperatives. Some of the important issues are – Focus on loans and recovery and not on full financial intermediation: The focus in financial cooperatives have been merely on issue of loans and recovery and never on full financial intermediation. This has resulted in aggressive pushing of credit without appropriate risk management system for the financial cooperatives. Application of Income Recognition, Asset Classification (IRAC) norms has only accentuated the issue and made it more transparent. Low risks for the higher tiers of the cooperatives: Cooperatives depend on refinance as a source of funding. Since long the approach has been one of pushing credit through the financial cooperatives through a ‘without risk’ refinance support. Refinance policies were designed such that higher financing agencies sustain. Thus it was the DCCB (partially) and the PACS (Fully) that met the risk of default. Members feel that PACS will not be viable if they are not part of the payment system and unless they are allowed to access low cost deposits. Moreover refinance cannot be an unlimited source. The revenue recovery Act: The Act enabled the cooperatives to recover but soon proved ineffective. It will be interesting to study who mooted the idea that revenue recovery which was applied to Taccavi loans could be used in cooperatives. Risk Management: There are no risk management tools for rural lending. Stabilization fund is too complex a product for risk management. At best it is useful for liquidity management with DCCB and PACS. The fund has not been fully utilized. In the absence of good ‘crop loss’ insurance policy, funding the crop failure through a loan is not appropriate. The current crop insurance scheme is therefore not at all sufficient. There needs to be an insurance product covering the entire income loss due to crop loss. Thus non availability of risk management products comes in the way of sustainability of financial cooperatives. Maintenance of SLR: The recent decision that scheduled Urban cooperative banks need to keep 25 per cent of their Statutory Liquidity Ratio (SLR) holdings in Government’s securities has also affected the deposit volumes of cooperatives. Micro level Review and Analysis – View and Suggestions of the members Governance Issues: Governance of financial cooperatives is an important issue that needs to be analysed in the study. Successful models where managing committees have played good role and innovative systems of governance can be captured under the study. Documenting Best Practices and Technology Innovations: While it will be good to list out and detail out some of the best practices adopted by cooperatives in India and abroad, it is equally important to know that - Why are they relevant and What should be done to disseminate learnings from best practices observed. Further, the study can recommend practices that can be standardized at provincial and national level and steps required for their implementation. Use of Technology – Bringing Cooperatives in Core Banking: There is a need to provide professional services to the clients by introduction of core banking system, SMS alert, ATMs, immediate disposal of loan proposals etc. Several Urban cooperative banks and even District cooperative banks have already started using various technology based services, including ATM services. Studying the use of technology by various cooperatives and its results in mobilising more members, will be useful. The

22

possibilities of financial cooperatives to incorporate mobile financial services and branchless banking to enhance their service offering also need to be analysed. SWOT analysis of the financial cooperatives: If our focus is to strengthen the financial services through cooperative system, it is important to do an in-depth analysis of financial cooperatives utilising SWOT analysis (strengths, weaknesses, opportunities and threats) to assess their capacities and potential available for them. Learning from the earlier studies and reports: While review of past studies is needed to know the recommendations made by various committees, it is also suggested to review the extent to which the actions are taken up on the recommendations. Members shared important studies such as Report of the Study Team on Self- Reliant Cooperative Laws – December 2005 (A study Commissioned by Canadian centre For International Studies And Cooperation, Delhi); Status of Self-reliant Cooperatives – A study in furtherance of the resurgence of a Vibrant Cooperative Movement Across India (Study sponsored by Watershed Support Services and Activities Network, Hyderabad and undertaken by Access Livelihoods Consulting India). Assessing a Financial cooperative – Specific aspects to be covered

Vision, mission and activities of the cooperative - how were these formulated and by whom

Capacity building requirements; capacity building needs of cooperatives and service providers; key organisations that can deliver the required support

Governance: Strengths of board members; Leadership role change; number of leaders trained and experienced at the cooperative level; How continued leadership is implemented; system of providing training to the new leaders; sub-committees in operation

Staff and capacity Building: Staff strength, technically qualified staff and the second level staff in place; Capacity building system for staff and board members

Product and Services: Products and services including the financial inclusion services (savings, credit, insurance, pension, financial literacy and education) and social and livelihood services provided by the cooperative

Organisational operational policies and systems: By-law, HR policies, accounting policies and systems, MIS, programme monitoring systems, External Linkages of the cooperative

Financial planning and fund management: Development of Annual plan of action, & implementation mechanism; sources of funding; percentage of required funds mobilized independently by the cooperative ; Level of operational and financial self-sufficiency; cash flow preparation and usage; transparency in sharing financial information

Support from SHPIs: SHPIs support to cooperatives; benefits of the support received; needs of cooperatives that are not fulfilled through SHPI

Value Chain of various services : Range of products; Process of delivery of products and services by cooperative; Customers’ satisfaction; system of tracking; support or guidance mechanism available for the clients

Suggestions on demand side aspects to be covered in the study: The issues to be covered from the client’s perspective include - Clients perception about the value proposition of the cooperatives; products and services required by the clients want and availability of products at the cooperative; Use of savings Accounts by the clients; dependency on other financial service providers by the members and reasons for the same; Changes clients would like to see in their financial cooperatives viz. services, product offerings, pricing, governance, ownership etc. Overall, members recommended for a national level study on financial cooperatives, suggested to keep focus on financial inclusion and proposed to cover a variety of financial cooperatives so that policy and implementation related changes can be made holistically.

23

Annex 3

FORM FOR SUBMITTING SERVICE PROVIDER’S

TECHNICAL PROPOSAL

(This Form must be submitted only using the Service Provider’s Official Letterhead/Stationery7)

[insert: Location].

[insert: Date] To: [insert: Name and Address of UNDP focal point] Dear Sir/Madam:

We, the undersigned, hereby offer to render the following services to UNDP in conformity with the requirements defined in the RFP dated [specify date], and all of its attachments, as well as the provisions of the UNDP General Contract Terms and Conditions:

A. Qualifications of the Service Provider

The Service Provider must describe and explain how and why they are the best entity that can deliver the requirements of UNDP by indicating the following:

a) Profile – describing the nature of business, field of expertise, licenses, certifications, accreditations; b) Business Licenses – Registration Papers, Tax Payment Certification, etc. c) Latest Audited Financial Statement – income statement and balance sheet to indicate Its financial

stability, liquidity, credit standing, and market reputation, etc. ; d) Track Record – list of clients for similar services as those required by UNDP, indicating description of

contract scope, contract duration, contract value, contact references; e) Certificates and Accreditation – including Quality Certificates, Patent Registrations, Environmental

Sustainability Certificates, etc. f) Written Self-Declaration that the company is not in the UN Security Council 1267/1989 List, UN

Procurement Division List or Other UN Ineligibility List.

B. Proposed Methodology for the Completion of Services

The Service Provider must describe how it will address/deliver the demands of the RFP; providing a detailed description of the essential performance characteristics, reporting conditions and quality assurance mechanisms that will be put in place, while demonstrating that the proposed methodology will be appropriate to the local conditions and context of the work.

7 Official Letterhead/Stationery must indicate contact details – addresses, email, phone and fax numbers – for

verification purposes

24

C. Qualifications of Key Personnel

If required by the RFP, the Service Provider must provide: a) Names and qualifications of the key personnel that will perform the services indicating who is Team

Leader, who are supporting, etc.; b) CVs demonstrating qualifications must be submitted if required by the RFP; and c) Written confirmation from each personnel that they are available for the entire duration of the

contract.

[Name and Signature of the Service Provider’s Authorized Person] [Designation] [Date]

25

Annex 4

FORM FOR SUBMITTING SERVICE PROVIDER’S FINANCIAL PROPOSAL

A. Cost Breakdown per Deliverable*

Deliverables [list them as referred to in the RFP]

Percentage of Total Price (Weight for

payment)

Price (Lump Sum, All

Inclusive)

1 Submission of Inception report and work plan 20%

2 Submission of Preliminary Report 30%

3 Submission of First draft of the Study Report 20%

4 Submission of final report 30%

Total 100% INR……

*This shall be the basis of the payment tranches

B. Cost Breakdown by Cost Component: Bidders are requested to quote for all components

including all costs associated with the study.

Description of Activity Remuneration per Unit of

Time

Total Period of Engagement

No. of Personnel

Total Amount

I. Personnel Services

1. Cost of Hiring Experts/ Field Investigators

II. Out of Pocket Expenses

1. Cost of Field Study - Cost of travel Including Boarding and lodging of the study team

2. Cost of Communication , Overheads and contingencies

4. Any other Costs, if any ( please specify)

TOTAL

INR…

Note:- 1. Study will be undertaken in at least 4 states selected as sample for the study 2. Additional sheets may please be attached for detailed break-up of the cost

[Name and Signature of the Service Provider’s Authorized Person] [Designation] [Date]

26

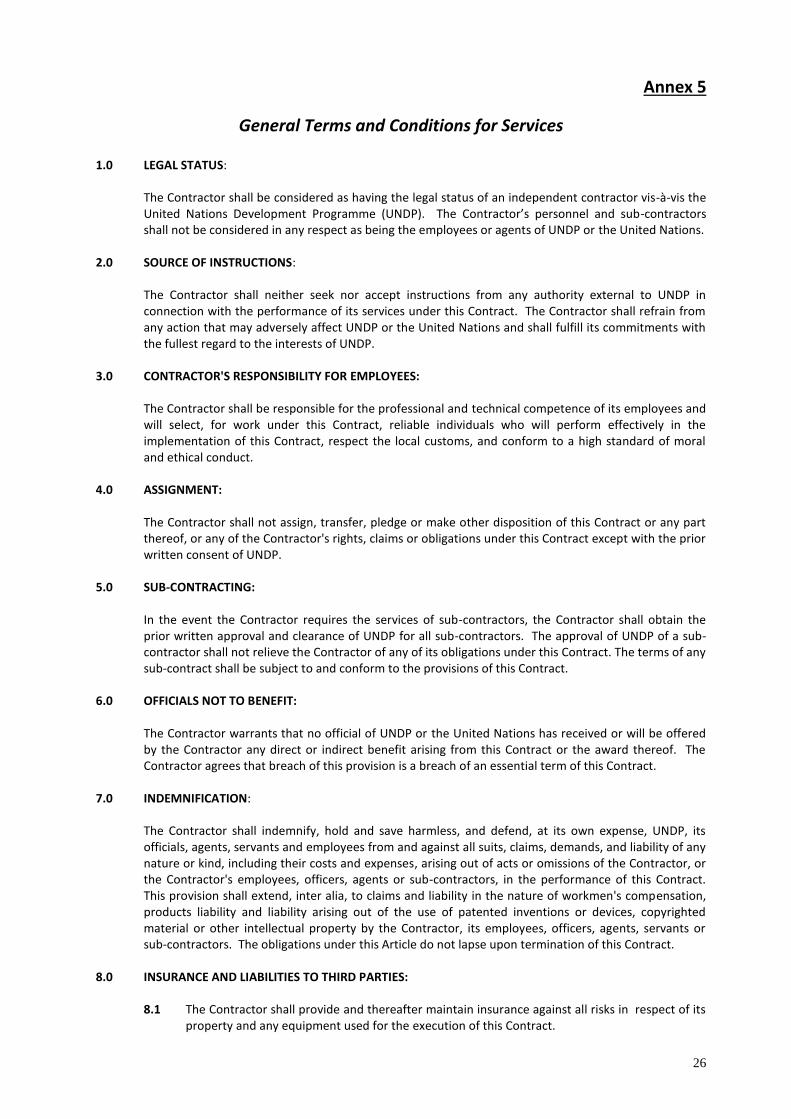

Annex 5

General Terms and Conditions for Services 1.0 LEGAL STATUS:

The Contractor shall be considered as having the legal status of an independent contractor vis-à-vis the United Nations Development Programme (UNDP). The Contractor’s personnel and sub-contractors shall not be considered in any respect as being the employees or agents of UNDP or the United Nations.

2.0 SOURCE OF INSTRUCTIONS:

The Contractor shall neither seek nor accept instructions from any authority external to UNDP in connection with the performance of its services under this Contract. The Contractor shall refrain from any action that may adversely affect UNDP or the United Nations and shall fulfill its commitments with the fullest regard to the interests of UNDP.

3.0 CONTRACTOR'S RESPONSIBILITY FOR EMPLOYEES:

The Contractor shall be responsible for the professional and technical competence of its employees and will select, for work under this Contract, reliable individuals who will perform effectively in the implementation of this Contract, respect the local customs, and conform to a high standard of moral and ethical conduct.

4.0 ASSIGNMENT:

The Contractor shall not assign, transfer, pledge or make other disposition of this Contract or any part thereof, or any of the Contractor's rights, claims or obligations under this Contract except with the prior written consent of UNDP.

5.0 SUB-CONTRACTING:

In the event the Contractor requires the services of sub-contractors, the Contractor shall obtain the prior written approval and clearance of UNDP for all sub-contractors. The approval of UNDP of a sub-contractor shall not relieve the Contractor of any of its obligations under this Contract. The terms of any sub-contract shall be subject to and conform to the provisions of this Contract.

6.0 OFFICIALS NOT TO BENEFIT:

The Contractor warrants that no official of UNDP or the United Nations has received or will be offered by the Contractor any direct or indirect benefit arising from this Contract or the award thereof. The Contractor agrees that breach of this provision is a breach of an essential term of this Contract.

7.0 INDEMNIFICATION:

The Contractor shall indemnify, hold and save harmless, and defend, at its own expense, UNDP, its officials, agents, servants and employees from and against all suits, claims, demands, and liability of any nature or kind, including their costs and expenses, arising out of acts or omissions of the Contractor, or the Contractor's employees, officers, agents or sub-contractors, in the performance of this Contract. This provision shall extend, inter alia, to claims and liability in the nature of workmen's compensation, products liability and liability arising out of the use of patented inventions or devices, copyrighted material or other intellectual property by the Contractor, its employees, officers, agents, servants or sub-contractors. The obligations under this Article do not lapse upon termination of this Contract.

8.0 INSURANCE AND LIABILITIES TO THIRD PARTIES:

8.1 The Contractor shall provide and thereafter maintain insurance against all risks in respect of its property and any equipment used for the execution of this Contract.

27

8.2 The Contractor shall provide and thereafter maintain all appropriate workmen's compensation insurance, or the equivalent, with respect to its employees to cover claims for personal injury or death in connection with this Contract.

8.3 The Contractor shall also provide and thereafter maintain liability insurance in an adequate

amount to cover third party claims for death or bodily injury, or loss of or damage to property, arising from or in connection with the provision of services under this Contract or the operation of any vehicles, boats, airplanes or other equipment owned or leased by the Contractor or its agents, servants, employees or sub-contractors performing work or services in connection with this Contract.

8.4 Except for the workmen's compensation insurance, the insurance policies under this Article

shall:

8.4.1 Name UNDP as additional insured; 8.4.2 Include a waiver of subrogation of the Contractor's rights to the insurance carrier

against the UNDP; 8.4.3 Provide that the UNDP shall receive thirty (30) days written notice from the insurers

prior to any cancellation or change of coverage. 8.5 The Contractor shall, upon request, provide the UNDP with satisfactory evidence of the

insurance required under this Article. 9.0 ENCUMBRANCES/LIENS:

The Contractor shall not cause or permit any lien, attachment or other encumbrance by any person to be placed on file or to remain on file in any public office or on file with the UNDP against any monies due or to become due for any work done or materials furnished under this Contract, or by reason of any other claim or demand against the Contractor.

10.0 TITLE TO EQUIPMENT:

Title to any equipment and supplies that may be furnished by UNDP shall rest with UNDP and any such equipment shall be returned to UNDP at the conclusion of this Contract or when no longer needed by the Contractor. Such equipment, when returned to UNDP, shall be in the same condition as when delivered to the Contractor, subject to normal wear and tear. The Contractor shall be liable to compensate UNDP for equipment determined to be damaged or degraded beyond normal wear and tear.

11.0 COPYRIGHT, PATENTS AND OTHER PROPRIETARY RIGHTS:

11.1 Except as is otherwise expressly provided in writing in the Contract, the UNDP shall be entitled to all intellectual property and other proprietary rights including, but not limited to, patents, copyrights, and trademarks, with regard to products, processes, inventions, ideas, know-how, or documents and other materials which the Contractor has developed for the UNDP under the Contract and which bear a direct relation to or are produced or prepared or collected in consequence of, or during the course of, the performance of the Contract, and the Contractor acknowledges and agrees that such products, documents and other materials constitute works made for hire for the UNDP.

11.2 To the extent that any such intellectual property or other proprietary rights consist of any

intellectual property or other proprietary rights of the Contractor: (i) that pre-existed the performance by the Contractor of its obligations under the Contract, or (ii) that the Contractor may develop or acquire, or may have developed or acquired, independently of the performance of its obligations under the Contract, the UNDP does not and shall not claim any ownership interest thereto, and the Contractor grants to the UNDP a perpetual license to use such intellectual property or other proprietary right solely for the purposes of and in accordance with the requirements of the Contract.

11.3 At the request of the UNDP; the Contractor shall take all necessary steps, execute all necessary

documents and generally assist in securing such proprietary rights and transferring or licensing

28

them to the UNDP in compliance with the requirements of the applicable law and of the Contract.

11.4 Subject to the foregoing provisions, all maps, drawings, photographs, mosaics, plans, reports,

estimates, recommendations, documents, and all other data compiled by or received by the Contractor under the Contract shall be the property of the UNDP, shall be made available for use or inspection by the UNDP at reasonable times and in reasonable places, shall be treated as confidential, and shall be delivered only to UNDP authorized officials on completion of work under the Contract.

12.0 USE OF NAME, EMBLEM OR OFFICIAL SEAL OF UNDP OR THE UNITED NATIONS:

The Contractor shall not advertise or otherwise make public the fact that it is a Contractor with UNDP, nor shall the Contractor, in any manner whatsoever use the name, emblem or official seal of UNDP or THE United Nations, or any abbreviation of the name of UNDP or United Nations in connection with its business or otherwise.

13.0 CONFIDENTIAL NATURE OF DOCUMENTS AND INFORMATION:

Information and data that is considered proprietary by either Party and that is delivered or disclosed by one Party (“Discloser”) to the other Party (“Recipient”) during the course of performance of the Contract, and that is designated as confidential (“Information”), shall be held in confidence by that Party and shall be handled as follows:

13.1 The recipient (“Recipient”) of such information shall:

13.1.1 use the same care and discretion to avoid disclosure, publication or dissemination of

the Discloser’s Information as it uses with its own similar information that it does not wish to disclose, publish or disseminate; and,

13.1.2 use the Discloser’s Information solely for the purpose for which it was disclosed.

13.2 Provided that the Recipient has a written agreement with the following persons or entities requiring them to treat the Information confidential in accordance with the Contract and this Article 13, the Recipient may disclose Information to:

13.2.1 any other party with the Discloser’s prior written consent; and, 13.2.2 the Recipient’s employees, officials, representatives and agents who have a need to

know such Information for purposes of performing obligations under the Contract, and employees officials, representatives and agents of any legal entity that it controls controls it, or with which it is under common control, who have a need to know such Information for purposes of performing obligations under the Contract, provided that, for these purposes a controlled legal entity means:

13.2.2.1 a corporate entity in which the Party owns or otherwise controls, whether

directly or indirectly, over fifty percent (50%) of voting shares thereof; or, 13.2.2.2 any entity over which the Party exercises effective managerial control; or, 13.2.2.3 for the UNDP, an affiliated Fund such as UNCDF, UNIFEM and UNV.

13.3 The Contractor may disclose Information to the extent required by law, provided that, subject