Embed Size (px)

Citation preview

Republic of the Philippines COMMISSION ON AUDIT

Commonwealth Avenue, Quezon City, Philippines

CONSOLIDATED ANNUAL AUDIT REPORT

on the

NATIONAL CONCILIATION AND MEDIATION BOARD

For the Year Ended December 31, 2009

i

Executive Summary A. Introduction

The National Conciliation and Mediation Board (NCMB) is an attached agency and under the administrative supervision of the Secretary of the Department of Labor and Employment (DOLE). It serves as a machinery that shall ensure prompt response to all labor-management disputes that may arise and shall work towards their early and amicable settlement.

NCMB was created within the ambit of the DOLE on January 30, 1987, as enunciated in Section 22 of EO 126, as amended, to give more meaning to the constitutional and presidential orders of the Department and was tasked of ensuring the maintenance of industrial peace by promoting harmonious, equitable and stable employment relations that assure equal protection for the rights of all concerned parties.

The Board absorbs the conciliation, mediation, labor- management cooperation and voluntary arbitration functions of the Bureau of Labor Relations (BLR) and its counterparts in the regional offices of the Department in accordance with Section 29 (c) of Executive Order No. 126, with the following major functions:

Formulate policies, programs, standards, procedures, manuals of operations, and guidelines pertaining to effective mediation and conciliation of all labor disputes;

Perform preventive mediation and conciliation functions; Coordinate and maintain linkages with other sectors or institutions and other

government authorities concerned with matters relative to the prevention and settlement of labor disputes; and

Administer the voluntary arbitration program, maintain/update list of

voluntary arbitrators, compile arbitration awards and decisions.

The Board is headed by an Executive Director, assisted by two Deputy Executive Directors who are appointed by the President upon recommendation of the Secretary of Labor and Employment. It also maintains fifteen regional branches all over the country, each headed by an Executive Director II assisted by some technical and support staff. The personnel complement as of December 31, 2009 consisted of 51 permanent employees in NCMB-Main and 152 in the fifteen regional offices.

ii

B. Accomplishments vs Plans/Targets

For CY 2009, the NCMB reported number of accomplishments vis-á-vis its plans and targets.

Major Program/Activity/Project Target Accomplish-ment

Percentage of

Accomplish-ment

Remarks

I. PARTNERSHIP AND LABOR-MANAGEMENT EMPOWERMENT

A. WORKPLACE COOPERATION AND PARTNERSHIP (LMCS)

LMC Facilitation No. of LMCs facilitated

- Organized Establishment 96 86 90 - Unorganized Establishment 103 103 100

LMC Enhancement

No. of LMCs enhanced 593 619 104 - Organized Establishment 228 232 102 - Unorganized Establishment

Documentation of LMC Best Practices

No. of LMCs Best Practices documented

- Organized Establishment 45 48 107 - Unorganized Establishment 23 13 57

B. WORKPLACE DISPUTE PREVENTION AND SETTLEMENT (GMs)

Institutionalization of GMs in unorganized companies

No. of Companies covered 167 171 102 Operationalization of GMs

- Organized Establishment 209 204 98 Strengthening/Enhancement

No. of GMs strengthened - Organized Establishment 530 487 92 - Unorganized Establishment 244 239 98

Documentation of GMs No. of GMs documented

- Organized Establishment 40 38 95 - Unorganized Establishment 23 10 43

iii

Major Program/Activity/Project Target Accomplish-ment

Percentage of

Accomplish-ment

Remarks

C. ADVOCACY AND NETWORKING

Meetings/briefings/consultations conducted

No. of meetings/briefings/consultations conducted

284

387

136

Dissemination of IEC materials No. of IEC materials

disseminated 5,700 8,710 153

Meeting with social partners and various sectors

No. of MOAs forged 26 18 69 No. of training conducted 155 200 129

II. CONCILIATION AND MEDIATION PROGRAM

No. of new AS/L cases declared

20 4 20 Of the 327 total NS/L cases handled, only 4 0r 1% materialized into A/S, 5 percentage points lower than the target of 6%, which reflects the effectiveness of the conciliation-mediation services of the Board

No. of new NS/L cases filed 274 286 104 No. of new PM cases filed 460 482 105 Disposition Rate

Actual Strike/Lockouts 95% 100% 105 Notices of Strike/Lockout 93% 85% 91 Preventive Mediation 94% 89% 95

Settlement Rate Actual Strike/Lockouts 75% 75% 100 Notices of Strike/Lockout 78% 74% 95 Preventive Mediation 89% 81% 91

Duration to Dispose/Settle

iv

Major Program/Activity/Project Target Accomplish-ment

Percentage of

Accomplish-ment

Remarks

Actual Strike/Lockouts 23 20 3 days faster

Notices of Strike/Lockout 29 44 15 days longer

Preventive Mediation 22 34 12 days longer

SAGAP/FLAVAS CASE No. of new cases filed 740 995 134

III. ARBITRATION AND ADJUDICATION PROGRAM

Voluntary Arbitration Cases facilitated and monitored

No. of new voluntary arbitration cases

137 134 98

Disposition Rate Previous Cases 100% 80% 80 Current Cases 50% 50% 100 Combined Cases 60% 63% 105

Average Days to decide From Submission to Decision 20 74 54 days

longer -The delay could be explained by the difficulty of reconciling the schedule of the opposing parties and the Arbitrator.

- In some cases, the Arbitrator exerts efforts to convince the parties to settle, which necessary prolongs the proceedings.

- Holidays, cessation of work due to natural calamities

- Motions for postponements/extensions of time filed by either or both parties and approved by the VA.

v

Major Program/Activity/Project Target Accomplish-ment

Percentage of

Accomplish-ment

Remarks

From acceptance or Arbitrator 90 208 118 days longer

-Conflicting schedules/ commitments of the Arbitrator or Panel of Voluntary Arbitrators.

-Depends on the complexity of case which requires the Arbitrator to study the case and conduct research in order to come up with a very good decision.

SVAF Subsidy Utilization No. of Cases Subsidized 138 84 61 Amount of Subsidy (in pesos) P1,198,500.00

In 2009, the Board managed to reduce the incidence of work stoppages from five

in the previous year to only four, the lower strike incidence in Philippine labor relations history. The new strike cases comprise 1.22 of the 327 total notices of strike/lockouts handled during the period. Decisions of Accredited Voluntary Arbitrators continue to enjoy wide acceptance, hence a decline in the voluntary arbitration cases. Affirmation rate for the year is computed at 100 percent while reversal rate is placed at 0 percent. C. Financial Highlights

The NCMB sources and application of funds and its consolidated financial condition for the audit year 2009, with comparative figures for 2008, are summarized in the tables below.

Table 1 Sources and Application of Funds

Particulars 2009

(in millions) 2008

(in million) Annual Appropriations (RA No. 9498 and 9401)

P115.48

P122.91

Allotments Received Extended

MOOE 8.87 3.76 CO 1.82 1.92 Total P10.70 P5.68

vi

Particulars

2009 (in millions)

2008 (in million)

Current PS 61.40 67.51 MOOE 50.74 52.91 CO 1.50 2.49 Total P113.64 P122.91

Obligations PS 61.40 66.81 MOOE 45.86 45.84 CO .25 2.58 Total P107.51 P115.23

Major Sources of Funds Subsidy from Nat’l Government P115.73 P123.37

Notice of Cash Allocation 112.93 117.68 Remittance Advice 2.07 5.69

Application of Funds Expenses P124.51 P113.01

Personal Services 71.99 66.81 MOOE 52.52 46.20

Table 2

Financial Condition

Particulars 2009

(in millions) 2008

(in millions) Total Assets P 15.14 P 14.60 Cash .51 .62 Receivables .48 .27 Inventories 1.43 1.46 Prepayments 1.33 1.27 PPE 11.20 10.98 Other Assets .19 .00 Total Liabilities P 11.05 P.93 Current Liabilities 11.05 .93 Equity P 4.08 P 13.67

D. Scope of Audit

This consolidated audit report covers the results of audit of the Main Office and its 15 Regional Branches (RBs) including the National Capital Region for the year ended December 31, 2009.

E. Auditor’s Report

The Auditor rendered a qualified opinion on the fairness and reliability of the presentation of the financial statements as of December 31, 2009 for reasons cited in the attached State Auditor’s Report.

vii

F. Observations and Recommendations

The following audit observations and recommendations were discussed with management concerned during the exit conference conducted on May 19, 2010, the details of which are discussed in Part II of this report. Management comments were incorporated in this report, where appropriate.

1. Cash advances for salaries and other benefits under account “Payroll Fund”

were fully liquidated by the concerned accountable officers of NCMB Main and the regional branches as of December 31, 2009. (Par. 1)

We recommended that management continue its compliance by the concerned accountable officers with the requirements/regulations of COA Circular No. 97-002 dated February 10, 1997 and Accounting Circular No. 2006-001 dated November 9, 2006, as to the liquidation of paid payrolls.

2. Unliquidated cash advances for travel/project expenses increased the balance

of the account Advances to Officers and Employees by P106,994.38 or 152 percent while Petty Cash Fund totaling P113,600.00 remained unliquidated at year-end contrary to the rules and regulations of COA Circular No. 97-002 dated February 10, 1997, thus the pertinent accounts’ balances are overstated while the corresponding expenses accounts are understated. Likewise, the Subsidiary Ledger for said account not maintained in RCMB-VII. (Paras. 2-8) We recommended that management direct the concerned officers and employees to submit immediately the proper accounting of expenditures to settle the unliquidated cash advances for travel and project expenses as well as the Petty Cash Fund granted during the year. We also recommended the immediate refund of the unexpended balance particularly those pertaining to CY 2008 as required under COA Circular No. 97-002 dated February 10, 1997.

3. Loss of funds amounting to P10,000.00 due to the alleged estafa committed

by a former disbursing officer of RCMB-NCR was reclassified to Accounts Receivable instead of Other Receivables (149) as required in COA Circular No. 2003-002 dated August 1, 2003, causing the year-end balance of the former account of doubtful validity while the latter is understated of the same amount. (Paras. 13-17)

We recommended that management require the Accounting Analyst to re-evaluate the entries made and effect the necessary adjustments to reflect the correct balances of the affected accounts in the ensuing year.

viii

4. Miscellaneous trust receipts maintained/deposited to the agency’s depository bank totaling P88,981.44 were not yet remitted to the Bureau of the Treasury contrary to the regulations of Executive Order No. 338, thereby overstating the balance of account Cash-In-Bank, Local Currency Current Account of the same amount. (Paras. 20-24)

We recommended and management agreed to direct the Accountant and the Cashier to remit/deposit immediately the remaining balances of funds still maintained with the agency’s depository bank (LBP) in accordance with the requirements of Executive Order No. 338. Failure to do so shall subject the responsible official/s and employee/s to appropriate criminal and/or administrative action pursuant to Section 6 of the said EO.

5. Disallowances/charges totaling P239,915.19 remained unsettled as of

December 31, 2009, thus depriving the government the use of the funds for other priority projects and programs. (Paras. 27-28)

We recommended that management require all persons liable to fully settle their obligations to the government as of the end of year 2010. We also recommended that RCMB-VI management devise a reasonable scheme for the immediate settlement of the disallowances/charges pursuant to existing COA rules and regulations.

6. Unfunded obligations amounting to P7,104,408.00 earmarked as Accounts

Payable as of December 31, 2009 increased the negative balance of the Statement of Income and Expenses to P8,836,926.25. (Paras. 31-34)

We recommended that management advise the Budget Officer to coordinate with the Department of Budget and Management for the immediate release in the ensuing year of the National Cash Allocation (NCAs) to finance the unfunded obligations taken up as Accounts Payable as of December 31, 2009. We further recommended to require the Chief Accountant to closely coordinate with the Budget Officer and both will assess/compare the succeeding fund releases with the obligations incurred to avoid the recurrence of negative balances in the financial reports unless if the causes are non-cash transactions.

7. Funds amounting to P977,702.96 reportedly transferred to the NCMB-Main

Office from the Department of Labor and Employment-OSEC were not recorded/recognized in the agency books and not yet liquidated as at year-end thus, the accuracy of the reported account balance is unreliable. (Paras. 39-42)

ix

We recommended that management require the Accountant to take up in the books the remaining balance of the fund transfer and cause the immediate liquidation of the same in the ensuing year.

8. The reliability and accuracy of the year-end balance of account Cash, National Treasury-MDS amounting to P14,829.51 in RCMB-VIII books cannot be ascertained due to the failure of the Accountant-Designate to submit the bank reconciliation statements and its supporting documents as of December 31, 2009 in violation of Section 74 of P.D. 1445 and COA Circular No. 92-125A. (Paras. 45-49)

We recommended strict compliance to Section 74 of PD 1445 and COA Circular No. 92-125A to avoid the sanctions of automatic suspension of payment of salaries due to failure of the Accountant-Designate to comply with the submission of the Bank Reconciliation Statement pursuant to Section 122(2) and (3) of PD 1445.

Specifically, we suggested the following remedial steps:

a. Make arrangement with the depository bank to allow the Accountant to pick up the bank statements to ensure timely receipt of bank statements.

b. Require the Accountant to prepare and submit BRS for December 2009 and the previous months/years and to update the related accounting records.

9. Office supplies valued at P24,088.02 which were not found during the physical inventory count remained unaccounted for by the concerned supply official due to the issuance of supplies carried on stock without the required Requisition and Issue Slip pursuant to Section 53 of the Manual on the New Government Accounting System, Volume II, causing the overstatement of the year-end balance of Office Supplies Inventory account by P476,206.06. (Paras. 54-56)

We recommended that management instruct the new Storekeeper to adhere strictly to the COA rules and regulations and avoid the issuance of requested supplies in the absence of RIS; review the discrepancies noted and coordinate with the accounting personnel for the preparation of necessary adjustments to arrive at the correct cost of unused supplies carried on stock.

10. The balances of Property, Plant and Equipment accounts per accounting

records totaling P41.86 million and per property unit’s physical count of P37.66 million differed by P4.20 million, thus casting doubts on their reliability (Paras. 59-64).

x

The COA Audit Team of NCMB-Main recommended that management require the Inventory Committee to complete the reconciliation of the result of the inventory with the accounting records investigate the discrepancies noted, coordinate with the accounting personnel for the preparation of necessary adjustments to arrive at the correct value of existing properties and submit the reconciled report to the COA Audit Team in accordance with Section 490 of the GAAM, Volume I.

11. Unserviceable/obsolete properties in RCMB-II valued at P484,209.60 were

not yet disposed of during the year and not reclassified to Other Assets account in violation of Section 143 of the Manual on National Government Accounting System (NGAS), thus resulting in the overstatement of PPE accounts and the understatement of Other Assets account (Paras. 72).

The COA Audit Team in RCMB- II recommended and management agreed to instruct the Accountant-Designate to draw a journal entry voucher reclassifying the unserviceable properties to Other Assets account pursuant to Section 143 of the Manual on NGAS. The team further recommended that management require the property officer to prepare and submit to COA the prescribed Inventory & Inspection Report (I&I Report) of unserviceable properties indicating the management’s appraisal therein, for the conduct of necessary inspection and evaluation needed for their disposal pursuant to Section 64 of the Manual on NGAS.

12. Unserviceable furniture and IT equipment costing P39,542.00 in RCMB-

NCR were automatically dropped-off from the books at book value of P5,878.17 instead of the actual cost without the proper disposal required by existing laws, rules and regulations. (Paras. 74-79)

We recommended that management direct the Accounting Analyst to prepare immediately adjusting entries in the succeeding year to reflect the correct balances of the affected accounts and to follow strictly the accounting principles and standards in the recording of transactions to avoid misleading information found in the year-end financial reports.

13. Small tangible items with estimated useful life of more than a year in

RCMB-CAR totaling to P41,259.77 were not reclassified from Office Furniture and Fixtures to Inventory account contrary to COA Circular No. 2005-002 dated April 14, 2005, thus overstating the PPE account while understating the Inventory account. (Paras. 83-86)

xi

We recommended and management agreed that:

a) the Accountant-Designate prepare the adjusting entries and record the procured small tangible assets in accordance with COA Circular No. 2005-002; and

b) the Supply Officer issue Inventory and Custodian Slips for the

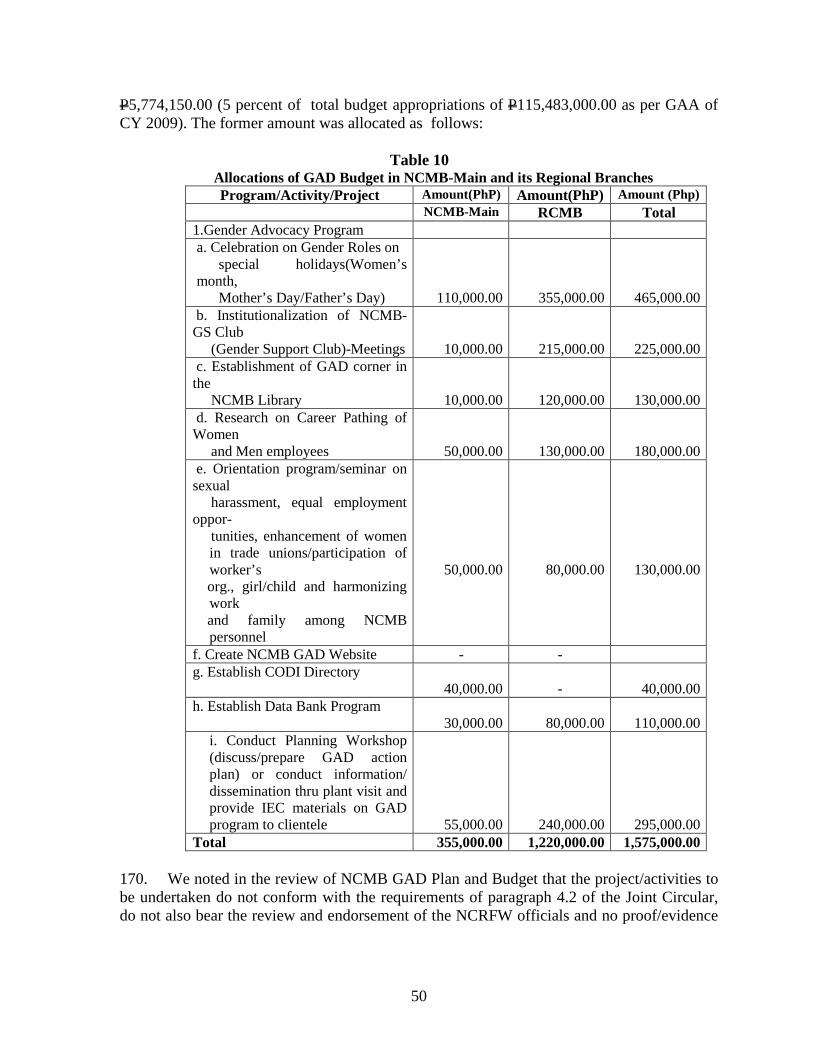

monobloc chairs and white boards for monitoring, control and accountability purposes

14. Several expenditure transactions of NCMB-Main and RCMB-NCR were not

yet properly classified to the pertinent appropriate accounts in accordance with COA Circular No. 2004-008 dated September 20, 2004 despite repeated reminders in last year’s audit report, thus affecting the accuracy of the reported operating expenses in the financial statements. (Paras. 84-90)

We recommended that management instruct the Accountant in NCMB-Main and the Accounting Analyst in the RCMB-NCR to be careful in the recording of entries in the journal reports and ledger books. Likewise, require the same officials to prepare adjusting entries in the succeeding year to reflect the correct balances of the affected accounts and to follow strictly the accounting principles and standards in the recording of transactions to avoid misleading information in the year-end financial reports.

15. A copy of the contract involving the outsourced Psychometric Assessment Services in NCMB-Main was not forwarded to the COA Office for review and evaluation of cost as required in COA Circular No. 87-278 and COA Memorandum No. 2005-027 while the procurement process/procedures were not conducted by NCMB but made use of the activity done by the Department of Labor and Employment (DOLE). (Paras. 96-99)

We recommended that management create a Bids and Awards Committee (BAC), separate and distinct from that of the DOLE as required by existing laws and regulations and to adhere strictly to the requirements of RA 9184 to address the procurement needs of NCMB-Main Office and its regional offices. We further recommend that the Accountant instructed to submit to the COA Auditor all contracts including Purchase Orders five days after perfection thereof.

16. The designated Accountant of RCMB-CAR also acts as the Supply Officer

contrary to the principle of sound internal control on the segregation of duties and functions. (Paras. 131-132) We recommended that management designate an employee other than the Accountant-Designate to perform the functions of a supply officer to separate the accounting from the custodial function and for a stronger internal control over agency assets.

xii

We further recommended that instead of the Budget Officer, assign an official as Supply Officer who has no access with the financial and procurement process to have a sound internal control. The Budget Officer is responsible for the obligations portion of the financial procedures of every transactions.

17. Traveling expenses incurred by an employee during the availment of family

visit privilege totaling P5,025.00 was reimbursed by RCMB-VII without legal basis and available funds for the purpose contrary to Section 4.1 of Presidential Decree No. 1445 resulting to irregular expenditures by the same amount. (Paras.147-153)

The COA Audit Team of RCMB-VII recommended that management require Mr. Hacelfeo T. Cuares to refund immediately the traveling expenses incurred amounting to P5,025.00 charged to the branch funds while the nine (9) working days used should be deducted from the earned vacation leave credits. Henceforth, the team further recommended to management to stop the practice of paying family visit expenses charged against government funds.

18. The CY 2009 Gender and Development Plan and Budget for the NCMB

Main and its regional offices was not reviewed and endorsed by the National Commission on the Role of Filipino Women (NCRFW), thus the allocation and utilization thereof are not in pursuance of the Joint Circular No. 2004-1 of the Department of Budget and Management (DBM), National Economic and Development Authority (NEDA) and the NCRFW. (Paras. 176-187

We recommended that management require the GAD Focal Point to prepare a Plan and Budget allocation that conforms with the guidelines/policies set forth in Joint Circular No. 2004-1 of the DBM, NEDA and NCRFW so that the activities/projects to be undertaken gear towards the objectives of equality and opportunity of gender treatment for men and most especially for women.

We further recommended that management require the NCMB GAD Focal person to resubmit the CY 2010 budget and have it stamped “received” and indicate the date of receipt. We also recommended that management require same official or his representative to follow up the action taken to the submitted GAD Plan and Budget until it is reviewed and endorsed by the NCRFW. We further recommended to re-evaluate the Office Order for the creation of Focal Person and include the regional branches for the proper and updated monitoring of the implementation and utilization of the distributed GAD funds in the succeeding years.

xiii

G. Implementation of Prior Years’ Audit Recommendations

The status of implementation of prior year’s recommendation is shown below:

Status Number Percentage

Fully Implemented 10 50% Partially Implemented 5 20 Net Implement 5 20

Total 20 100%

Table of Contents

Page No. Part I Financial Statements

• State Auditor’s Report 1 • Statement of Management’s

Responsibility for financial statements 3

• Detailed Balance Sheet 4 • Detailed Statement of Income and

Expenses 6

• Statement of Cash Flows 9 • Notes to Financial statements 10 Part II Observations and Recommendations 18 Part III Status of Implementation of Prior Year’s Audit

Recommendations 56

Part IV Annexes

State Auditor’s Report The Executive Director National Concilitaiton and Mediation Board Arcadia Bldg., Quezon Avenue Quezon City

Pursuant to Section 2, Article IX-D of the Philippine Constitution and Section 43 of the government Auditing Code of the Philippines (PD 1445), we have audited the accompanying Consolidated Balance sheet of the National Conciliation and Mediation Board (NCMB) as of December 31, 2009, and the related Consolidated Statement of Income and Expenses and Consolidated Cash Flows for the year ended. These financial statements are the responsibility of the Auditee. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with generally accepted state auditing standards. Those standards require that we plan and perform the audit to obtain reasonable assurance that the financial statements are free of material misstatement/s. Our audit also included examining, on a test basis, evidence supporting the amount and disclosures in the financial statements. It also included assessing, as well as, evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion.

As discussed in Part II – Audit Observations and Recommendations, we observed that:

1. Unliquidated cash advances for travel/project expenses increased the balance of the account Advances to Officers and Employees by P106,994.38 or 152 percent while Petty Cash Fund totaling P113,600.00 remained unliquidated at year-end contrary to the rules/regulations of COA Circular No. 97-002 dated February 10, 1997, thus the pertinent accounts’ balances are overstated while the corresponding expenses accounts are understated. Likewise, the Subsidiary Ledger for said account not maintained in RCMB-VII.

2. Loss of funds amounting to P10,000.00 due to the alleged estafa committed by the

former disbursing officer of RCMB-NCR was reclassified to Accounts Receivable instead of Other Receivables (149) as required in COA Circular No. 2003-002 dated August 1, 2003, causing the year-end balance of the former account of doubtful validity while the latter is understated by the same amount.

3. Miscellaneous trust receipts totaling P88,981.44 maintained/deposited to the agency’s

depository bank were not yet remitted to the National Treasury contrary to Executive Order No. 338, thereby overstating the balance of account Cash-In-Bank, Local Currency Current Account of the same amount.

Republic of the Philippines COMMISSION ON AUDIT

Commonwealth Avenue, Quezon City

2

4. Disallowances/ charges totaling P239,915.19 have remained unsettled as of December 31, 2009, thus depriving the government the use of the funds for other priority projects and programs.

5. Unfunded obligations totaling P7,104,408.00 earmarked as Accounts Payable as of

December 31, 2009 of NCMB-Main increased the negative balance of the Statement of Income and Expenses to P8,836,926.25.

6. Funds amounting to P977,702.96 reportedly transferred to the NCMB-Main Office

from the Department of Labor and Employment-OSEC were not recorded/recognized in the agency books and not yet liquidated as at year-end thus, the accuracy of the reported account balance is unreliable.

7. The balances of Property, Plant and Equipment accounts per accounting records

totaling P41.86 million and per property unit’s physical count of P37.66 million differed by P4.20 million, thus casting doubts as to their reliability.

8. Unserviceable/obsolete properties in RCMB-II valued at P484,209.60 were not yet

disposed of during the year and not reclassified to Other Assets account pursuant to Section 143 of the Manual on National Government Accounting System (NGAS), thus resulting in the overstatement of PPE accounts and the understatement of Other Assets account. On the other hand, unserviceable furniture and IT equipment costing P39,542.00 in RCMB-NCR were automatically dropped-off from the books at book value of P5,878.17 instead of the actual cost without the proper disposal required by existing laws, rules and regulations.

In our opinion, except for the effects of the deficiencies presented in the preceding paragraph, the financial statements referred to above, present fairly, in all material respects, the financial position of the National Conciliation and Mediation Board as of December 31, 2009 and the results of its operations and its cash flows for the year then ended in accordance with applicable laws, rules and regulations and in conformity with applicable generally accepted state accounting principles.

COMMISSION ON AUDIT

By:

31 May 2010

3

4

2009 2008

Current Assets

Cash (Note 5)Cash-Collecting Officer P P 9,621.25Payroll Fund 160,632.97Petty Cash Fund 113,600.00 125,900.00Cash-Local Currency, Current account 400,098.16 319,362.25 Total Cash 513,698.16 615,516.47

Receivable (Note 6)Accounts Receivable 10,000.00 16,680.00Advances From Officers and Employees 177,313.56 70,319.18Due from NGAs 38,531.42 129,448.37Due from GOCCs 7,500.00Receivable-Disallowances and Charges 239,915.19 29,989.75Other Receivable 15,000.00 15,568.13 Total Receivables 480,760.17 269,505.43

Inventories (Note 7)Office Supplies Inventory 1,308,034.42 1,348,644.98Other Supplies Inventory 114,525.30 114,525.30 Total Inventories 1,422,559.72 1,463,170.28

Prepaid Expenses (Note 8)Prepaid Insurance 41,101.43 10,955.51Prepaid Rent 1,223,172.48 1,195,632.48Guaranty Deposits 50,000.00 50,000.00Other Prepaid Expenses 17,696.67 14,480.00 Total Prepayments P 1,331,970.58 P 1,271,067.99

ASSETS

NATIONAL CONCILIATION AND MEDIATION BOARDConsolidated Detailed Balance Sheet

As of December 31, 2009(With Comparative Figures for CY 2008)

5

2009 2008

Property, Plant & Equipment (Note 9)Office Equipment 8,573,841.58 7,736,604.07Furniture and Fixtures 5,796,427.81 5,334,310.40IT Equipment and Software 15,074,566.56 15,352,913.62Communication Equipments 125,248.00 141,528.00Library Books 944,831.24 944,831.24Motor Vehicles 11,286,388.00 11,839,238.00Other Property, Plant and Equipment 55,210.69 0.00 Total Property, Plant & Equipment 41,856,513.88 41,349,425.33Less: Accumulated Depreciation 30,656,120.94 30,796,414.49 Property, Plant & Equipment, Net 11,200,392.94 10,553,010.84

Other Assets (Note 10) 193,499.05 430,317.93

Total Assets P 15,142,880.62 P 14,602,588.94

Current Liabilities (Note 11)Accounts Payable 10,267,370.40 745,459.64Due to Officers and Employees 3,303.00 Due to National Treasury 231,590.18 Other Payables 207,459.80 126,120.52Due to BIR 182,583.88 60,979.94Due to GSIS 31,023.45 974.58Due to PAG-IBIG 38,931.43 Due to PHILHEALTH 81,462.50 25.00Performance/Bidders/Bail Bonds Payable 15,849.41 Total Current Liabilities 11,059,574.05 933,559.68

EquityGovernment Equity, beginning 13,669,029.26 9,879,727.31Retained Operating Surplus Adjustments 2,040.58 205,174.79 Prior Year's Adjustments (750,837.02) (304,084.39) Current Operations (8,836,926.25) 3,888,211.55

(9,585,722.69) 3,789,301.95Government Equity, ending 4,083,306.57 13,669,029.26

Total Liabilities and Equity P 15,142,880.62 P 14,602,588.94

See Accompanying Notes to Financial Statements

LIABILITIES AND EQUITY

6

2009 2008

INCOMESubsidy Income from National Government (Note 13) P 119,333,137.77 P 123,373,169.22Less: Reversion of Unused NCA 3,599,412.45 6,415,642.50

Subsidy Income from NG, Net 115,733,725.32 116,957,526.72Seminar Fees 2,000.00Loss/Gain on Sale of Assets (60,288.39) (54,652.95)Other Fines and Penalties (Note 14) 1,554.57 39.50Miscellaneous Operating and Service Income(Note 14) 892.50 450.00

Total Income 115,675,884.00 116,905,363.27

EXPENSESPersonal Services

Salaries & Wages - Regular Pay 47,228,754.72 40,755,316.42Personnel Economic Relief Allowance (PERA) 2,322,690.68 1,138,568.71Additional Compensation (ADCOM) 2,316,075.23 3,413,705.91Representative Allowance 1,625,090.90 1,393,800.00Transportation Allowance 1,508,105.11 1,309,227.35Clothing Allowance 772,000.00 768,000.00Productivity Incentive Allowance 405,000.00 361,000.00Other Bonuses and Allowances 272,000.00 260,000.00Longevity Pay 180,000.00 269,083.00Cash Gift 975,250.00 947,250.00Year-end Bonus 4,220,169.80 3,540,362.33Life & Retirement Insurance Benefits 5,647,860.55 4,835,199.09PAG-IBIG Contributions 233,700.00 227,829.10PHILHEALTH Contributions 382,248.50 158,175.50ECC Contributions 231,668.86 229,308.63Terminal Leave Benefits 1,782,125.98 3,822,721.82Other Personnel Benefits 1,882,485.22 3,377,993.18Total Personal Services P 71,985,225.55 P 66,807,541.04

Maintenance and Other Operating ExpensesTraveling Expenses - Local 4,233,727.01 3,842,064.97Traveling Expenses - Foreign 1,500.00 10,515.36Training and Seminar Expenses 1,532,945.63 683,996.96

NATIONAL CONCILIATION AND MEDIATION BOARDConsolidated Detailed Statement of Income and Expenses

For the Year Ended December 31, 2009(With Comparative Figures for CY 2008)

7

2009 2008

Scholarship Expenses 23,478.00 18,000.00Office Supplies Expenses 2,992,355.57 3,269,740.15Accountable Forms Expenses 35,104.00 24,250.00Drugs and Medicine Expenses 479.75Gasoline, Oil and Lubricants 1,240,530.02 1,620,091.71Other Supplies Expenses 111,390.14Water Expenses 319,027.98 627,549.53Electricity Expenses 3,185,399.61 2,660,695.58Postage and Deliveries 391,720.28 345,192.20Telephone - Landline 1,569,166.84 1,748,820.40Telephone - Mobile 528,785.67 528,808.41Internet Expenses 418,806.84 349,589.61Advertising Expenses 1,410.00 18,032.00Printing and Binding Expenses 103,563.00 31,654.84Rent Expenses 9,134,658.07 5,140,605.77Representation Expenses 1,349,450.02 1,116,460.19Transportation and Delivery Expenses 25,075.00 26,000.00Auditing Services 173,672.82 17,222.00Subscription Expenses 146,411.34 63,094.60Legal Services 50,000.00General Services 122,124.72Janitorial Services 2,435,918.67 2,008,738.05Security Services 3,162,754.09 2,520,736.10Other Professional Services 2,582,267.21 2,222,181.57Repairs and Maintenance: Office Building 40,355.10 89,077.80 Other Leasehold Improvement 38,766.00 Office Equipment 259,876.73 381,171.50 Furnitures and Fixtures 141,371.65 211,973.50 IT Equipment and Software 332,215.03 215,559.14 Communications Equipment 200.00 Other Property, Plant and Equipment 500.00 Motor Vehicles 791,698.60 676,710.82Extraordinary Expenses 122,000.00 110,620.54Taxes, Duties and Licenses 2,229.06 4,398.12Fidelity Bond Premium 176,712.55 168,457.25Insurance Expenses 220,270.34 307,818.51Donation 30,000.00Depreciation Expenses: Office Equipment 315,851.90 159,555.49 Furniture and Fixtures 238,740.88 216,414.95

8

2009 2008

IT Equipment & Software 1,038,789.62 1,049,760.59 Books 12,208.88 3,328.84 Communication Equipment 3,987.00 11,351.91 Motor Vehicle 122,400.05 122,399.95 Other Property, Plant and Equipment 539.92Other Maintenance & Operating Expenses(Note 12) 12,965,024.83 13,379,947.05Total MOOE (Note 14) 52,523,335.70 46,204,710.68Financial Expenses

Bank Charges 4,249.00 4,900.00Total Financial Expenses 4,249.00 4,900.00Total Expenses (Note 12) 124,512,810.25 113,017,151.72

Net Income Over Expenses (Note 15) P (8,836,926.25) P 3,888,211.55

See Accompanying Notes to Financial Statements

9

2009 2008Cash Flow from Operating Activities:

Cash Inflows:Receipt of Notice of Cash Allocation (NCA) P 112,925,047.00 P 117,679,077.00Receipt of Notice of Transfer Allocation (NTA) 77,644,859.06 73,481,272.38

227,447.21Collection of Receivables (disallowances) 11,722.20 45,767.70

1,801,921.0921,130.14

Collection of Income/Revenues/fines and penalties 892.50 403,450.00Receipt of refund of cash advances 60,855.63 129,827.78Receipt of refund of overpayment of expenses 104,443.06

Total Cash Inflows 192,798,317.89 191,739,394.86

Cash Outflows:Cash payment of operating expenses 80,665,850.04 79,250,148.29Transfer of funds thru NTA 77,644,859.06 73,481,272.38Cash payment terminal leave 1,581,274.48 3,822,721.82Remittance of collections to BTR 351,784.86 229,905.54Reversion of unused NCA 3,599,412.45 6,415,642.50

1,801,921.09Grant of cash advances and petty cash funds 9,420,266.94 10,056,298.90Cash purchase of inventories 2,212,409.80 2,574,116.30

12,005.52Remittance of GSIS/PAGIBIG/PHILHEALTH payables 12,975,640.34 13,969,820.19Cash payment of accounts payables 870,539.89 2,137,543.37

Total Cash Outflows 191,135,964.47 191,937,469.29

Cash Provided by Operating Activities P 1,662,353.42 P (198,074.43)

Cash Flow from Investing Activities:Cash Inflows:

Receipt of Proceeds from sale of assets 2,500.00 5,627.05Cash Outflows:

Cash Purchase of Property, Plant and Equipment (1,766,671.73) (1,259,583.18)Cash Provided by Investing Activities (1,764,171.73) (1,253,956.13)

Total Cash provided by Operating and Investing Activities (101,818.31) (1,452,030.56)Add: Cash Balance, Beginning January 1 615,516.47 2,067,547.03Cash Balance, Ending December 31 P 513,698.16 P 615,516.47

NATIONAL CONCILIATION AND MEDIATION BOARDConsolidated Statement of Cash FlowsFor the Year Ended December 31, 2009

(With Comparative Figures for CY 2008)

Redemption/Return of Bidder's/Performance Bond

Cancellation of Checks Issued during the year

Collection of VA Award Held-In-TrustReceipt of Bidder's/Performance Bond

Payment/Deposit of VA Awards

10

NATIONAL CONCILIATION AND MEDIATION BOARD NOTES TO FINANCIAL STATEMENTS

As of December 31, 2009 1. General/Agency Profile

1.1 The National Conciliation and Mediation Board (NCMB) was created by virtue of Executive Order No. 126, reorganizing the Department of Labor and Employment.

1.2 The NCMB is mandated by the EO to serve as the lead government

agency for:

Formulation of policies, develop plans and programs and set standards and procedures relative to the promotion of conciliation and voluntary arbitration. Facilitation of labor-management cooperation through joint mechanisms for information sharing, effective communication and consultation and group problem solving.

2. Basis of Financial Statements Presentation

2.1 The financial statements herein show the financial condition, result of operations and cash activities of NCMB for the calendar year ended December 31, 2009. These financial statements have been prepared in accordance with generally accepted state accounting principles and standards.

3. Summary of Significant Accounting Policies

3.1 The Board uses the accrual basis of accounting. All expenses are

recognized when incurred and reported in the final statements in the period to which they relate. Revenues are recorded when realized, except for transactions where accrual basis is impractical or when, other methods are required by law.

3.2 The board adopts the system of One Fund Concept. It maintains General

Fund (101) and Special Account in the General Fund (151) for Collective Bargaining Agreement Registration fees.

3.3 The Decentralized Accounting System is adopted.

Notice of Cash Allocation (NCA) is recorded in the Regular Agency (RA) books upon receipt of the Advice of NCA Issued.

11

Notice of Transfer Allocation (NTA) is issued to the Regional Branches, and is recorded by the Branches upon receipt.

The Modified Obligation System is used to record allotments received and obligations incurred.

Income/receipts which the agency is not authorized to use and are required to be remitted to the National Treasury are recorded in the National Government (NG) Books.

3.4 Supplies and materials purchased for inventory purposes are recorded using perpetual inventory system.

3.5 Petty Cash Fund (PCF) account is maintained under the Imprest System.

All replenishments are directly charged to the expense account. Supplies and materials purchased out of the Petty Cash Fund for immediate use or emergency are taken up as outright expenses.

3.6 Property Plant and Equipment (PPE) are carried at cost less accumulated

depreciation and obsolescence. The Straight Line Method of depreciation is used to depreciate the PPE. A residual value computed at 10 percent of the cost of asset is set and depreciation starts on the second month after purchase. Regular maintenance, repair and minor replacements are charged against Maintenance and Other Operating Expenses (MOOE) as these were incurred.

3.7 Tangible assets with serviceable life of more than one year but small

enough to be considered as PPE are recorded as inventories upon acquisition and expense upon issuance.

3.8 Payable accounts are recognized and recorded in the books of accounts

only upon acceptance of the goods/inventory/other assets and rendition of services to the agency

3.9 Taxes withheld are remitted to the Bureau of Internal Revenue (BIR) thru

Tax Remittance Advice. 3.10 Accounts were reclassified to conform with the new Chart of Accounts

prescribed under the New Government System (NGAS) which was implemented effective January 1, 2002.

3.11 Financial expenses such as bank charges are separately classified from

MOOE.

3.12 Transactions in foreign currencies are recorded in Philippine Peso based on the BSP rate of exchange prevailing at the date of transactions.

12

4. Correction of Fundamental Errors

4.1 Fundamental errors of prior years are corrected by using the Prior Year’s Adjustments account. Errors affecting current year’s operation are charged to the current year’s accounts.

5. Cash and Other Cash Accounts

Petty Cash Fund P 113,600.00 Cash-In-Bank, Local Currency Current Account 400,098.16

TOTAL P 513,698.16 Petty Cash Fund balance of P 113,600.00, consists of cash advance

granted to Regular and Special Disbursing Officers in the Central Office and Regional Branches, maintained under the Imprest System, for payment of petty or miscellaneous authorized expenditures which cannot be immediately paid by check.

The account Cash in Bank – Local Currency, Current Account consists of: Central Office:

Bidder’s Bond P 67,307.71 GATT Fund 20,000.01 Sports & Cultural Activities 43,668.00 Seminar /Conference Fees 24,755.48 ATM Payroll Account ___26,987.92 TOTAL P 182,719.12

Regional Branch No. VI:

Voluntary Arbitration Award P 216,821.08 Regional Branch No. XIII:

Regular Current Account P 557.96 TOTAL P 400,098.16

========== 6. Receivables

This account consists of:

Accounts Receivable P 10,000.00 Due from NGAs 38,531.42 Receivable-Disallowances and Charges 239,915.19 Advances to Officers and Employees 177,313.56 Other Receivables 15,000.00

TOTAL P 432,228.75

13

The Accounts Receivable amounting to P10,000.00 was originally recorded in the Petty Cash Fund account but due to loss of funds through estafa by Ms. Adelfa Lacerna, former Cash Disbursing Officer of NCMB-NCR, the unliquidated cash advance was later reclassified to the said account at the start of the year.

The amount of P38,531.42 Due from NGAs consists of undelivered

supplies procured from the Procurement Service of the Department of Budget and Management during the last quarter of CY 2009.

The account Advances to Officers and Employees pertains to the

unliquidated cash advances granted for travel and for special purposes which have been liquidated early part of CY 2010.

The Receivable-Disallowances and Charges of P239,915.19 pertains to

the disallowances for the year 2004 and 2006 of NCMB-Main amounting to P2,661.54 and the Regional Branches VI and VIII in the amount of P233,179.44 and P4,074.21, respectively.

7. Inventories

This account consists of:

Office Supplies Inventory P 1,308,034.42 Other Supplies Inventory 114,525.30

TOTAL P 1,463,170.28

All purchases are coursed thru the inventory account and issuances are recorded as they take place except for purchases out of the petty cash fund which are charged directly to the appropriate expense account.

8. Prepayments and Other Current Assets

This account consists of:

Prepaid Rent P 1,223,172.48 Prepaid Insurance 41,101.43 Guaranty Deposits 50,000.00 Other Prepaid Expenses 17,696.67

TOTAL P 1,331,970.58

The account Prepaid Rent consists of P 1,195,632.48 for two months advance and security deposit for office space of the Central Office, and P 540.00 for advance rental for one unit lock box (P.O. Box 1604) in the Philippine Postal Office, while the P 27,000.00 represents payment for one month advance deposit for new office space of Regional Branch No. XII.

The Prepaid Insurance pertains to the unexpired portion of payment to

GSIS to cover insurance of supplies and motor vehicles.

14

The account Guaranty Deposits represents the security deposit for rental of office building of Regional Branch No. VII.

The account Other Prepaid Expenses pertains to the deposit of telephone

services of Central Office.

9. Property Plant and Equipment

This account consists of:

Particulars Acquisition Cost Accumulated Net Book Accounts Depreciation Value

Office Equipment P8,573,841.58 P6,077,658.99 P2,496,182.59 Furniture and Fixtures 5,796,427.81 3,964,066.26 1,832,361.55 IT Equipment and Software 15,074,566.56 10,606,394.94 4,468,171.62 Communication Equipment 125,248.00 101,974.25 23,273.75 Library Books 944,831.24 335,030.63 609,800.61 Motor Vehicle 11,286,388.00 9,569,106.25 1,717,281.75 Other Property, Plant & Equipment 55,210.69 1,889.62 53,321.07

TOTAL P41,856,513.88 P30,656,120.94 P11,200,392.94 =========== =========== ===========

The account Office Equipment included equipment worth P169,450.00, purchased from the Special Account in the General Fund (Fund 151).

10. Other Assets P 193,499.05

This account pertains to the cost of assets not used in the operation and those waiting for disposal.

11. Current Liabilities

This account includes the following:

Accounts Payable P 10,267,370.40 Due to Officers and Employees 3,303.00 Due to National Treasury 231,590.18 Due to GSIS 31,023.45 Due to PAG-IBIG 38,931.43 Due to BIR 182,583.88 Due to PHILHEALTH 81,462.50 Performance/Bidders/Bail Bonds Payable 15,849.41 Other Payables 207,459.80

TOTAL P 11,059,574.05

The Accounts Payable pertains to the unpaid obligations as of December 31, 2009 of the Central Office and the Regional Branches.

15

The account Other Payables represents the remaining balance of the Voluntary Arbitration Award/Decision of Regional Branch No. VI.

12. Other Maintenance and Operating Expenses

The total Other Maintenance and Operating Expenses for the year amounted to P 12,965,024.83. The account includes expenses incurred in the conduct of plant-level orientation seminars on grievance machinery, voluntary arbitration, area-wide seminars and skills training. Payment for Subsidy of Voluntary Arbitrators is charged to the account.

It also includes expenses incurred during the Mid-Year and Year-End

Performance Assessment and Corplanning Exercises, Labor Day Celebration, Independence Day, DOLE Sports fest, Search for Outstanding LMC Awards for Industrial Peace, GAD Programs, payment of Collective Negotiation Agreement (CNA) and other regular and special activities/programs of the Board which cannot be classified under the specific financial expense accounts.

13. Subsidy Income from National Government

This account includes the following:

NCA received from DBM for payment of expenses for agency operational expenses P112,925,047.00

Tax Remittance Advice (TRA) issued to BIR 6,468,946.40 Less: Refund of Unused Cash Advances, etc. (60,855.63) Total P119,333,137.77

============ The account consists of Notice of Cash Allocation (NCA) received from

the Department of Budget and Management and Tax Remittance Advice and cash refund remitted to the Bureau of Treasury.

For this year, Notice of Cash Allocation (NCA) amounting to

P 112,925,047.00 was received from the Department of Budget and Management for the current operating expenses, payment of prior year liabilities and terminal leave benefits of former employees.

The total amount of P 77,644,859.06 was released to the Regional

Branches to cover their budgetary requirements for Operating Expenses (Personal Services, Maintenance and Other Operating Expenses and Capital Outlay).

14. Receipt of Other Income

In addition to the Subsidy Income from the National Government, the

agency’s financial resources were augmented by Other Fines and Penalties of P1,554.57 and Miscellaneous Operating and Service Income of P892.50.

16

15. Expenses Expenses recorded in the books amounted to P124,512,810.25 which

include (a) non-cash expenses (depreciation) amounting to P1,732,518.25 and (bank charges) of P4,249.00 (b) Prior year adjustments amounting to P750,837.02 (c) Supplies expenses (prior year supplies inventories and issued during the year) amounting to P2,992,355.57 and (d) unpaid obligations for which goods and services have been delivered/rendered, and recognized during the year amounted to P10,267,370.40. Following the Matching Principle of Accounting, all expenses are recorded and reported in the period which they are incurred to reflect the actual expenses/utilization of the Board at year end. The unreleased cash allocation for the year amounted to P13,834,752.95, details shown in the table below:

Table 1

Summary of Allotment, Corresponding Released/Unreleased Cash Allocations

Allotment *Cash Allocation which should be

released by DBM

Actual Cash Released by

DBM

Unreleased Cash Allocation

RLIP P 5,924,977.00 P5,924,977.00 P5,924,977.00 - PS 66,352,365.00 61,044,175.80 59,690,307.90 1,353,867.90

MOOE 59,615,420.29 56,634,649.28 44,718,941.10 11,915,708.18 CO 3,322,103.03 3,155,997.88 2,590,821.00 565,176.88

TOTAL P135,214,865.32 P126,759,799.95 P112,925,047.00 P13,834,752.95

* Computed net of withholding of eight percent and five percent for PS and MOOE, respectively.

The reported expenses of P52,523,335.70 as of December 31, 2009

exceeded the reported income of P115,675,884.00 by P 8,836,926.25 due to unreleased cash allocation of P13,834,752.95. Of the latter amount, P10,267,370.40 was obligated and taken up as Accounts Payable as of December 31, 2009 causing an unfunded obligations of P7,104,408.00 ( negative balance of P8,836,926.25 less depreciation expenses of P1,732,518.25). The request for cash allocation to cover payment for the payable accounts of P10,267,370.40 has been submitted to the DBM early part of CY 2010.

16. Allotments, Obligations and Balances

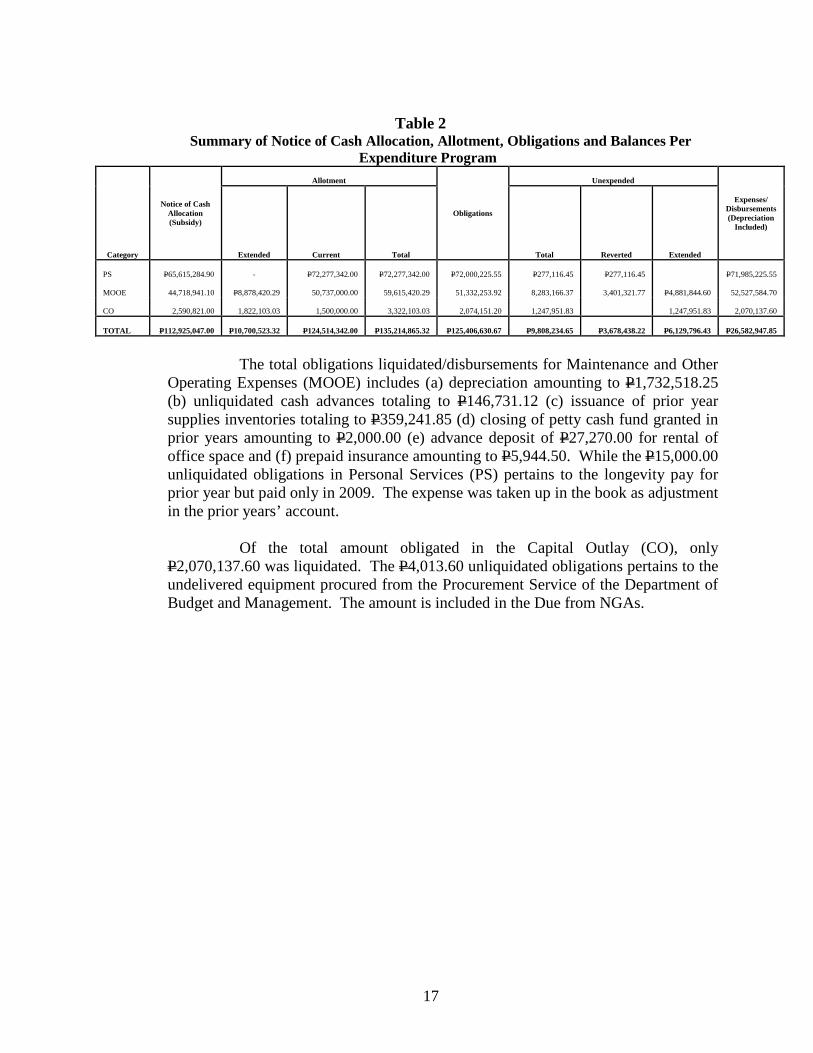

Total allotment available during the year amounted to P135,214,865.32,

including the continuing appropriations/allotment carried over from FY 2008 of P10,700,523.32. Of the amount, P3,401,321.77 was reverted to the General Fund pursuant to the Budget Circular No. 2006-1 dated February 1, 2006. The Summary of Notice of Cash Allocation, Allotment, Obligations and Balances as of December 31, 2009 per expenditure program was as follows:

17

Table 2

Summary of Notice of Cash Allocation, Allotment, Obligations and Balances Per Expenditure Program

Category

Notice of Cash Allocation (Subsidy)

Allotment

Obligations

Unexpended

Expenses/ Disbursements (Depreciation

Included)

Extended Current Total Total Reverted Extended

PS

P65,615,284.90 -

P72,277,342.00

P72,277,342.00

P72,000,225.55

P277,116.45

P277,116.45

P71,985,225.55

MOOE

44,718,941.10

P8,878,420.29

50,737,000.00

59,615,420.29

51,332,253.92

8,283,166.37

3,401,321.77

P4,881,844.60

52,527,584.70

CO

2,590,821.00

1,822,103.03

1,500,000.00

3,322,103.03

2,074,151.20

1,247,951.83

1,247,951.83

2,070,137.60

TOTAL

P112,925,047.00 P10,700,523.32 P124,514,342.00 P135,214,865.32 P125,406,630.67 P9,808,234.65 P3,678,438.22 P6,129,796.43 P26,582,947.85

The total obligations liquidated/disbursements for Maintenance and Other

Operating Expenses (MOOE) includes (a) depreciation amounting to P1,732,518.25 (b) unliquidated cash advances totaling to P146,731.12 (c) issuance of prior year supplies inventories totaling to P359,241.85 (d) closing of petty cash fund granted in prior years amounting to P2,000.00 (e) advance deposit of P27,270.00 for rental of office space and (f) prepaid insurance amounting to P5,944.50. While the P15,000.00 unliquidated obligations in Personal Services (PS) pertains to the longevity pay for prior year but paid only in 2009. The expense was taken up in the book as adjustment in the prior years’ account.

Of the total amount obligated in the Capital Outlay (CO), only

P2,070,137.60 was liquidated. The P4,013.60 unliquidated obligations pertains to the undelivered equipment procured from the Procurement Service of the Department of Budget and Management. The amount is included in the Due from NGAs.

18

PART II - OBSERVATIONS AND RECOMMENDATIONS Cash Advance Cash advances for salaries and other benefits under account “Payroll Fund” were fully liquidated by the concerned accountable officers of NCMB Main and the regional branches as of December 31, 2009.

1. We recommended that management continue its compliance by the concerned accountable officers with the requirements/regulations of COA Circular No. 97-002 dated February 10, 1997 and Accounting Circular No. 2006-001 dated November 9, 2006, as to the liquidation of paid payrolls. Unliquidated Cash Advances of Officers and Employees in NCMB-Main and RCMB- CAR to RCMB- XII Unliquidated cash advances for travel/project expenses increased the balance of the account Advances to Officers and Employees by P106,994.38 or 152% while Petty Cash Fund totaling P113,600.00 remained unliquidated at year-end contrary to the rules and regulations of COA Circular No. 97-002 dated February 10, 1997, thus the pertinent accounts’ balances are overstated while the corresponding expenses accounts are understated. Likewise, the Subsidiary Ledger for said account not maintained in RCMB-VII.

2. The granting, utilization and liquidation of cash advance is governed by COA Circular No. 97-002 dated February 10, 1997, pertinent provisions of which are quoted as follows:

2.a “No additional cash advances shall be allowed to any official or employee unless the previous cash advance given to him is first settled or a proper accounting thereof is made

2.b A cash advance shall be reported on as soon as the purpose for which it was

given has been served.

2.c When a cash advance is no longer needed or has not been used for a period of two (2) months, it must be returned to or refunded immediately to the collecting officer.

2.d All cash advances shall be fully liquidated at the end of each year. Xxxx.”

3. The year-end unliquidated cash advances were composed of the following:

Table 1 Schedule of Unliquidated Cash Advances Per Account and Per Office

Offices

Petty Cash

Fund

Advances to Officers and Employees

Amount

NCMB-Main P64,600.00 P64,600.00 Regional Branches - ( RB CAR, I, II, III,

19

- IV-A & B, V, VI,) 49,000.00 49,000.00 - (RB VII, VIII, X,

XI, XII)

177,313.56

177,313.56 Total for CY 2009 113,600.00 177,313.56 290,913.56 Total for CY 2008 P125,900.00 P70,319.18 P196,219.18 Increase (Decrease) P(12,300.00) P106,994.38 P94,694.38 Percentage of Inc./Dec. 9.77% 152.16% 48.26%

4. Very apparent in the above table is the significant increase of the year-end balance of account Advances to Officers and Employees by P106,994.38 or 152.16% as compared to last year, showing management’s failure to initiate control on the grants of cash advances for travels and project expenses. Verification of agency records also revealed that the purposes for which the cash advances were given have long been served but the unspent balances are yet to be refunded, as presented in the Aging of Unliquidated Cash Advances (Annex A).

5. The audit team also noted that the respective accountable officers in the Main Office and eight regional branches failed to liquidate the Petty Cash Fund (PCF) granted during the year totaling to P113,600.00 and allowed the PCF to remain in their safekeeping even in the ensuing year contrary to Paragraph 5.1.2 of COA Circular No. 97-002 dated February 10, 1997 which requires that “ The AO shall liquidate his cash advance for petty operating expenses and field operating expenses within twenty (20) days after the end of the year; subject to replenishment as frequently as necessary during the year.”

6. Moreover, the COA Audit Team of RCMB-VII noted that the Accountant-Designate failed to maintain a Subsidiary Ledger (SL) for the account Advances to Officers and Employees (148), thus immediate verification and review of the amount of cash advances granted and liquidated for each employee for a given time could not be facilitated, contrary to Section 12 of the New Government Accounting System (NGAS) Manual, Volume II.

Section 12 of the New Government Accounting System (NGAS) Manual, Volume II states that “ The Subsidiary Ledger (SL) is a book of final entry containing the details or breakdown of the balance of the controlling account appearing in the General ledger (GL). Postings to the SL generally come from the source documents. Examples of GL accounts which have SL are Cash Collecting Officers, Cash-Disbursing Officers, Cash in Bank-Local Currency, Current Account, Accounts Receivable, Notes Receivable, etc. The totals of the SL balances shall be reconciled with their respective control account regularly or at the end of each month. Schedules shall be prepared periodically to support the corresponding controlling GL accounts.”

7. Verification and review of the Trial Balance for calendar year 2009 revealed that the account Advances to officers and Employees (148) pertaining to the 12 agency personnel granted cash advances has no corresponding Subsidiary Ledger (SL), thus verification of their accountabilities for a given period could not be ascertained.

8. The continuous failure of the concerned accountable officers to liquidate the cash advances as soon as the purpose for which these were given has been served resulted to the

20

overstatement of the balances of accounts Advances to Officers and Employees and Petty Cash Fund while the pertinent expense accounts were understated.

9. We recommended that management:

direct all concerned officers and employees of NCMB-Main and its regional offices to submit immediately the proper accounting of expenditures to settle the unliquidated cash advances for travel and project expenses as well as the Petty Cash Fund granted during the year.

comply strictly with the regulations/requirements of COA Circular No. 97-

002 dated February 10, 1997. request the immediate refund of the unexpended balance particularly those

pertaining to CY 2008 as required under Require the Accountant –Designate of RCMB-VII to maintain a Subsidiary

Ledger (SL) for account Advances to Officers and Employees (148) for the year 2010.

10. The Chief Accountant assured the COA Audit Team that she will inform all concerned accountable officers in the NCMB-Main office and its regional branches to liquidate all Petty Cash Funds still in their safekeeping. The malpractice of holding the Petty Cash Fund beyond the period required by COA regulations will automatically be stopped in year 2010. She also informed the Auditors that the unliquidated balance of the account Advances to Officers and Employees as of December 31, 2009 was reduced to P31,388.56 because RCMB-VII management already liquidated the amount of P145,925.00 on February 9, 2010 and instructed the Accountant-Designate to maintain a Subsidiary Ledger for the account Advances to Officers and Employees (148) starting January 2010.

Misclassification of account/transaction Loss of funds amounting to P10,000.00 due to the alleged estafa committed by a former disbursing officer of NCMB-NCR was reclassified to Accounts Receivable instead of Other Receivables (149) as required in COA Circular No. 2003-002 dated August 1, 2003, causing the year-end balance of the former account of doubtful validity while the latter is understated by the same amount.

11. The account Other Receivables is defined as an “amount due from agency’s officers and employees for overpayment, cash shortages, loss of assets and other bills issued by the agency. It also includes advances for official travel.” (Emphasis applied) 12. On the other hand, the account Accounts Receivable is used to record the amount due from customers/clients resulting from services rendered, trading/business transactions, and sale of merchandise or property which are expected to be collected in the regular course of business or over a definite period of time.

21

13. Analysis of the Petty Cash Fund account disclosed that the prior year’s balance of P10,000.00 was reclassified to Accounts Receivable account as per Journal Entry Voucher Number 625 dated December 31, 2009 for the alleged loss of funds through estafa by Ms. Adelfa Lacerna, former Disbursing Officer of NCMB-NCR. Ms. Lacerna is no longer connected with POEA after a prolonged absence from work. This loss of funds was not reported to the Office of the COA Auditor.

14. The said loss of funds should have been recorded under the account Other Receivables instead of Accounts Receivable as required in COA Circular No. 2003-002 dated August 1, 2003.

15. Due to the erroneous classification of accounts/transactions by the Accounting Analyst, the year-end balance of Accounts Receivable was overstated while the account Other Receivables (149) is understated by P10,000.00.

16. We recommended that management require the Accounting Analyst to re-evaluate the entries made and effect the necessary adjustments to reflect the correct balances of the affected accounts in the ensuing year.

17. The Accounting Analyst clarified that the classification made is in accordance with the instruction/advice from the NCMB-Central Office (NCMB-CO). Nonetheless, they will strictly adhere to the audit findings and will make the necessary adjusting entry to reflect the correct balances of the affected accounts on the April 2010 financial report.

Unremitted trust receipts maintained in the depository bank

Miscellaneous trust receipts maintained/deposited to the agency’s depository bank totaling P88,981.44 were not yet remitted to the National Treasury contrary Executive Order No. 338, thereby overstating the balance of account Cash-In-Bank, Local Currency Current Account of the same amount.

18. Section 2 of Executive Order No. 338, as implemented by Joint Circular No. 1- 97, dated January 2, 1997 of the COA, DOF, and DBM, specifically requires “ All government offices to immediately transfer all public moneys deposited with depository banks and other institutions to the Bureau of the Treasury, regardless of income source.”

19. Section 6 of RA No. 9524, otherwise known as the General Appropriations Act for CY 2009 further provides that “Receipts from non-tax sources authorized by law for specific purpose which are collected/received by a government office or agency acting as a trustee, agent or administrator, or which have been received as guaranty for the fulfillment of an obligation, and all other collections classified by law or regulations as trust receipt shall be treated as trust liability of the agency concerned and deposited with the National Treasury in accordance with EO No. 338, s. 1996 xxxxxxxxxxxxxx.” 20. The balance of the account Cash-In-Bank-Local Currency Current Account (111) shown in the consolidated detailed Balance Sheet totaled P400,098.16. Analysis of the account revealed that the balance was composed of bidder’s bond receipts, excess/unutilized project funds and trust receipts (garnishment for award to aggrieved claimants)

22

21. Further analysis of the account also revealed that of the P400,098.16 cash in bank, P88,981.44 or 22.24 percent are due for remittance/transfer to the National Treasury in accordance with the requirements of Executive Order No. 338, particularly the unutilized balances of programs/projects, as presented in the Table below:

Table 2

Trust Receipts Due For Remittance to the National Treasury

Nature of Collections/Receipts Cash-In-Bank, LCCA Balance

Funds Due for Transfer to

the BTR NCMB-Main Office

Bidder’s Bond P67,307.71 GATT Fund 20,000.00 P20,000.00 Sports and Cultural Activities 43,668.00 43,668.00 Seminar/Conference fees 24,755.48 24,755.48 ATM Payroll Account 26,987.92 Sub- Total 182,719.12 88,423.48

RCMB-VI Garnishment/Award to Aggreived Claimants 216,821.08

RCMB-XIII Unspent Project Funds 557.96 557.96 Grand Total P 400,098.16 P 88,981.44 ========= ========

22. The continuous failure of the accounting official to remit/deposit to the account of the National Treasury the remaining balance of collections, the excess/unutilized project funds and, the balance of account Cash-In-Bank, Local Currency Current Account reported in the financial statements resulted in the overstatement of the said account.

23. We recommended and management agreed to direct the Accountant and the Cashier to remit/deposit immediately the remaining balances of funds still maintained with the agency’s depository bank (LBP) in accordance with the requirements of Executive Order No. 338. Failure to do so shall subject the responsible official/s and employee/s to appropriate criminal and/or administrative action pursuant to Section 6 of the said EO.

24. The Chief Accountant informed the COA Audit Team that all dormant trust receipts long maintained in the depository bank will be closed as of June 30, 2010 as per coordination made with the Land Bank of the Philippines.

Unfunded obligations/expenses Unfunded obligations amounting to P7,104,408.00 earmarked as Accounts Payable as of December 31, 2009 increased the negative balance of the Statement of Income and Expenses to P8,836,926.25. 25. The net income over expenses reported in the Statement of Income and Expenses as of December 31, 2009 showed a negative balance of P8,836,926.25 making it appear that the expenses incurred by NCMB exceeded the subsidy/other income received during the year.

23

26. The excess of expenses over income consists of depreciation expenses amounting to P1,732,518.25 and unfunded obligations amounting to P7,104,408.00 earmarked as Accounts Payable as of December 31, 2009.

27. The negative balance was disclosed by the agency Accountant in the Notes to the Financial Statements, under Note 15, indicating therein that the cause of the negative balance was the unreleased cash allocation amounting to P13,834,752.95.

28. Verification of agency reports and records showed that the total appropriations approved for NCMB as per General Appropriations Act for CY 2009 amounted to P115,483,000.00 while the actual special allotment released and received amounted to P19,731,865.32 as per Schedule of Special Release of Allotment(SARO) or a total allotment of P135,214,865.32. Of the latter amount, P125,406,630.67 was obligated during the year including those earmarked as Accounts Payable at year-end. However, the total cash allocation received as per Notice of Cash Allocation only amounted to P112,925,047.00, yielding an unfunded obligations of P12,481,583.67, of which P10,267,370.40 was taken up as Accounts Payable- Due and Demandable as of December 31, 2009. Total Accounts Payable for NCMB-Main amounted to P3,317,776.15 while the remaining balance of P6,949,594.25 was distributed to the regional branches nationwide.

29. We recommended that management:

advise the Budget Officer to coordinate with the Department of Budget and Management for the immediate release in the ensuing year of the National Cash Allocation (NCAs) to finance the unfunded obligations taken up as Accounts Payable as of December 31, 2009.

require the Chief Accountant to closely coordinate with the Budget Officer

and both will assess/compare the succeeding fund releases with the obligations incurred to avoid the recurrence of negative balances in the financial reports unless if the causes are non-cash transactions.

30. Management commented that the Accountant and Budget Officer were already instructed and have immediately conducted further review and analysis of the fund releases as well as the obligations incurred for the year. The total obligations of P125,406,630.67 included expenses incurred during the Mid-Year and Year-End Performance Assessment, Labor Day Independence Day Celebrations, DOLE Sports fest, Search for Outstanding LMC Awards for Industrial Peace, Voluntary Arbitrators fee, payment of Collective Negotiation Agreement (CNA) and other regular and special activities/programs of the Board which cannot be classified under any of the budgetary accounts. The above activities, programs and expenditures were charged against the available allotment/savings from the released MOOE of the Board. Revised Notes to Financial Statements, Statement of Allotment, Obligations and Balances, Cash Releases, and detailed computation of C.N.A. incentive were submitted for reference.

24

31. The negative balance reported in the Statement of Income and Expenses was incurred, as follows:

a. On Personal Services – Terminal Leave Benefits and Other Personnel Benefits

(Productivity Enhancement Bonus and Monetization of Leave Credits). These expenses were obligated even without available appropriation/allotment using the savings from the released PS allotment as authorized in Section 60 of the GAA of 2009 (RA 9524) and item no. 5.1.2.1 of Budget Circular No. 2009-5.

b. Maintenance and Other Operating Expenses – these are expenses incurred for

the activities enumerated in paragraph no.36.

32. The Statement of Income and Expenses showed a negative balance due to unfunded obligations. The total cash allocation that should be released by the DBM should be P126,759,799.95. According to the DBM, all obligations which cannot be backed up by cash shall be reported as Accounts Payable as of December 31, 2009. The agency concerned shall request the release of the same in the ensuing year.

Unrecorded and unliquidated interfund transfer Funds amounting to P977,702.96 reportedly transferred to the NCMB-Main Office from the Department of Labor and Employment-OSEC were not recorded/recognized in the agency books and not yet liquidated as at year-end thus, the accuracy of the reported account balance is unreliable.

33. Section 48 of the Government Accounting and Auditing Manual, Volume I, specifically requires that:

“ Transactions must be promptly recorded to maintain the relevance and value of the information to agency management in controlling operations and making decisions.”

34. Further, Section 158 of the Manual on the New Government Accounting System, defines Due to NGAs as “ an account used to record the amount of liabilities due to national government agencies including those inter-agency transferred funds received for the implementation of specific programs/projects.”

35. Review of the Trial Balances and general ledger entries showed that the account Due to NGAs was not maintained in the NCMB- Main books of accounts as of December 31, 2009. Verification of agency records to validate the confirmation letter dated February 15, 2010 sent by the Audit Team Leader of the Department of Labor and Employment (DOLE) showed that the interfund transfer from DOLE to NCMB-Main for GATT activities amounting to P1,088,064.46 was previously taken up as Trust Liabilities in the Board’s books of accounts under the Old Government Accounting System (OGAS). Liquidations submitted for the interfund transfer were credited by the Accountant to the latter account. Pursuant to the Manual on the New Government Accounting System, all old accounts should be closed to the new chart of accounts, thus the balances of trust liabilities accounts pertaining to funds transferred by other government agencies should have been closed to the

25

Due to NGAs account. On the other hand, the funds transferred were still existing in the DOLE books under the account Due from NGA’s showing an unliquidated balance of P977,702.96 as of December 31, 2009.

36. Interview made with the Chief, Financial Management Division, revealed that the liquidation papers are still in their custody since they are still awaiting for several supporting documents from the NCMB-Region IV.

37. We recommended that management require the Accountant to take up in the books the remaining balance of the fund transfer and cause the immediate liquidation of the same in the ensuing year.

38. Management commented that the Accountant averred that she recorded the amount transferred by DOLE for the GATT activities of NCMB-Main as Trust Liabilities (OGAS account). After the conduct of the approved training programs, the agency recorded the liquidation reports and submitted the same to DOLE thru the Office of then Undersecretary Felicisimo O. Joson, for their appropriate action. She later learned that the said reports were not taken in the books of DOLE when she received a confirmation from the COA-NCMB Audit Team. Concerned officials of the agency requested the Regional Branches to resubmit liquidation papers to the Central Office. As of date, all RBs’ have submitted their reports, except RV IV-A. The Accountant informed the Audit Team that she’s in the process of retrieving the liquidation papers with the assurance to submit the same report on or before April 30, 2010. She will also prepare Journal Entry Voucher (JEV) to restore the account Due to NGAs and will submit to DOLE the disbursement reports once completed. Non Submission of Bank Reconciliation Statements and its supporting documents The reliability and accuracy of the year-end balance of account Cash, National Treasury-MDS amounting to P14,829.51 in RCMB-VIII books cannot be ascertained due to the failure of the Accountant-Designate to submit the bank reconciliation statements and its supporting documents as of December 31, 2009 in violation of Section 74 of P.D. 1445 and COA Circular No. 92-125A. 39. Section 74 of P.D. 1445 states that:

“At the close of each month, depositories shall report to the agency head, in such form as he may direct, the condition of the agency account standing on the books. The head of the agency shall see to it that reconciliation is made between the balances shown in the reports and the balance found in the books of the agency.”

40. While COA Circular No. 92-125A dated March 04, 1992, Sec. 2.1, states: “The Chief Accountant/Head of Government Accounting Units of National Government Agencies shall: a. Prepare Monthly Treasury Reconciliation Statements (TRS) of Treasury

accounts and Bank Reconciliation of the general account based on the Treasury Statement (TS) and Bank Statement (BS) submitted by the BTr and the bank, respectively.

26

b. Prepare correcting/adjusting entries for discrepancies/errors or other reconciling items requiring corrections by the agency immediately after the Treasury/Bank Reconciliation Statements were made and after these items were properly analyzed and verified.

c. Submit the originals of the TRS within 15 days after receipt of TS together with

copies of the Journal Entry Vouchers taking the correcting/adjusting entries, to TARD, BTr and Accounting Office (AO) COA

d. Submit the original of the BRS for the general account within 15 days after the

end of the month to the COA Auditor, copy furnished the concerned Government Servicing Bank (GSB) and the Department of Budget and Management (DBM) and Accounting Finance Bureau (AFB).”

41. Section 5 of the same Circular states that, “failure on the part of the officials concerned to comply with the requirements of this Circular shall subject them to the sanctions imposed under Section 122(2) and (3) of PD 1445”. 42. The COA Audit Team in RCMB-VIII noted that the Accountant failed to submit Bank Reconciliation Statements from May 2008 to December 31, 2009 hence, the accuracy of the monthly bank transactions as shown in the bank statements remained unverified, thus, affecting the reliability of the reported year-end balance of the account Cash-In-National Treasury-MDS. 43. When asked, the Accountant-Designate reasoned out that the delay was due to the late submission of bank statements by the depository bank. The COA Audit team averred that she should take the initiative to obtain personally or follow up from the bank in writing the copies of bank statements as well as informing them of the delay or non-receipt of the bank statements. 44. We recommended strict compliance with Section 74 of PD 1445 and COA Circular No. 92-125A to avoid the sanctions of automatic suspension of payment of salaries due to failure of the Accountant-Designate to comply with the submission of the Bank Reconciliation Statement pursuant to Section 122(2) and (3) of PD 1445. 45. Specifically, we suggested the following remedial steps:

a. Make arrangement with the depository bank to allow the Accountant to pick up the bank statements to ensure timely receipt of bank statements.

b. Require the Accountant to prepare and submit BRS for December 2009 and

the previous months/years and to update the related accounting records. 46. In the exit conference, management acknowledged the audit recommendation and assured the audit team to submit the required reports. 47. The COA Audit Team also emphasized that the sanctions embodied in Section 122(2) and (3) of PD 1445 will be imposed should the designated Accountant still fail to submit the BRS at least, in the next calendar year.

27