Embed Size (px)

Citation preview

Report on Issues Relating to the Potential Relocation of the Port Elizabeth Manganese Terminal and Tank Farm to the

Port of Ngqura

Compiled for the Port Elizabeth Regional Chamber of Commerce

Dr. Crispian Olver May 2008

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm i May 2008 _____________________________________________________________________ CONTENTS Tables ......................................................................................................................................... i Figures ....................................................................................................................................... ii Executive Summary.................................................................................................................. iii 1 Introduction....................................................................................................................... 1 2 Background to proposals for relocation and waterfront ................................................... 1 3 The Port Elizabeth Manganese Terminal.......................................................................... 2 4 The Port Elizabeth tank farm............................................................................................ 6 5 Environmental and health issues associated with manganese terminal and tank farm ..... 9 6 Legislative framework for ports in South Africa............................................................ 11 7 Restructuring within Transnet ........................................................................................ 12 8 Port Development Frameworks and port planning issues............................................... 15 9 The Coega IDZ and the Coega Development Corporation............................................. 20 10 Rail and freight planning issues...................................................................................... 23 11 Plans for the relocation of the manganese terminal to Ngqura ....................................... 25 12 The financial viability of relocating the manganese terminal......................................... 27 13 The Manganese industry in South Africa ....................................................................... 33 14 The future Manganese market ........................................................................................ 36 15 City plans for the development of a waterfront .............................................................. 38 16 Department of Public Enterprises Property Project ........................................................ 41 17 Valuation of the development of a Port Elizabeth waterfront ........................................ 42 18 Multiplier effects of a waterfront development .............................................................. 44 19 The Southernport Developments legal matter and its implications ................................ 46 20 Summary of the Pro’s and Con’s of relocation............................................................... 49 21 Suggested next steps ....................................................................................................... 51 22 References....................................................................................................................... 55

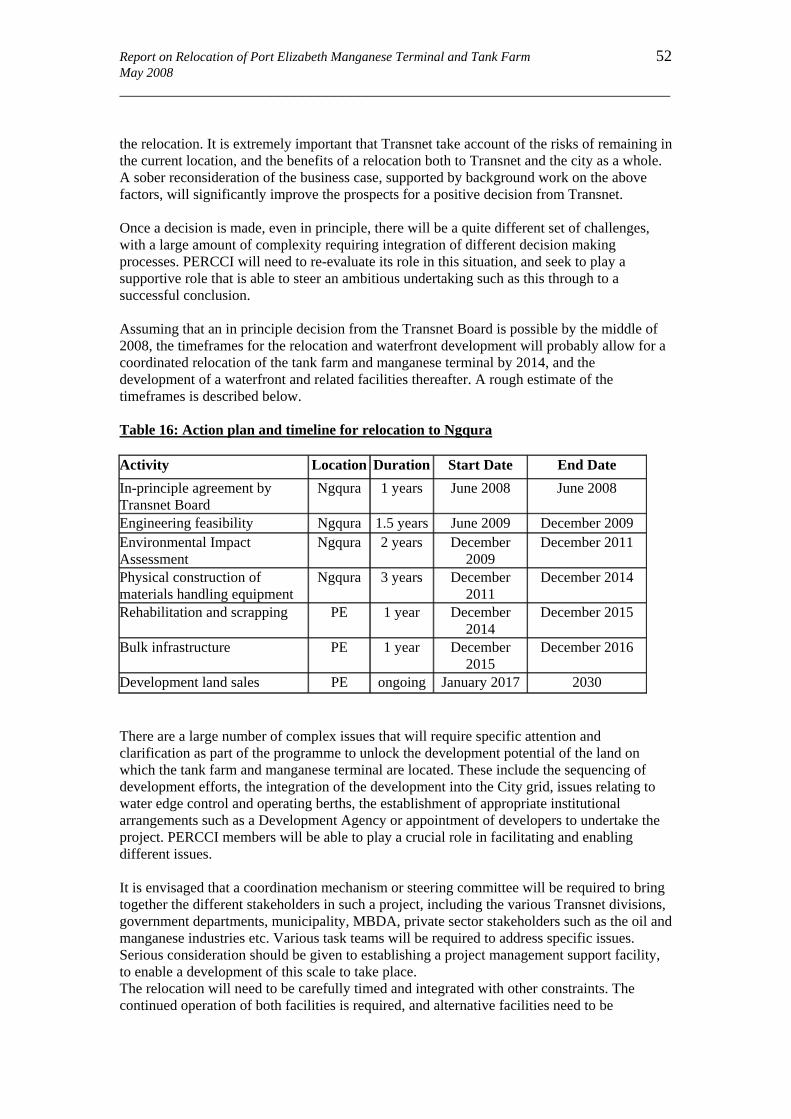

Tables Table 1: Volumes of ore exported through Port of Port Elizabeth, 1991/92 – 2006/07............ 4 Table 2: Projected volumes through Ngqura Port 2010 - 2050 ............................................... 16 Table 3: Summary of estimates of capex for relocation of manganese terminal..................... 28 Table 8: Estimate of total capital costs for upgrade to 6mtpa capacity ................................... 28 Table 4: Annual Capacity Demand and Supply for Port Elizabeth scenario........................... 30 Table 5: Annual Capacity Demand and Supply for Ngqura scenario...................................... 31 Table 6: Programme of capital expenditure for Ngqura and Port Elizabeth ........................... 31 Table 7: Financial viability of Ngqura and Port Elizabeth scenarios ...................................... 32 Table 9: World steel consumption and production by region.................................................. 36 Table 10: Growth rates and manganese content for different materials .................................. 37 Table 11: Current and future manganese ore exports.............................................................. 38 Table 12: Capitalised Property Income (in R’s billion)........................................................... 43 Table 13: Project Returns (in R’s billion) ............................................................................... 44 Table 14: Multipliers used for calculating economic impact of waterfront development....... 45 Table 15: Economic impact of a proposed waterfront development ....................................... 45 Table 16: Action plan and timeline for relocation to Ngqura.................................................. 52

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm ii May 2008 _____________________________________________________________________

Figures Figure 1: Aerial view of the Port Elizabeth manganese terminal and tank farm....................... 3 Figure 2: Port plan for first phase of Ngqura........................................................................... 17 Figure 3: 2050 scenario plan for Port of Ngqura..................................................................... 17 Figure 4: Current layout of Port of Port Elizabeth .................................................................. 18 Figure 5: Future plan for Port of Port Elizabeth with waterfront ............................................ 19 Figure 6: Port expansion plans for the Port of Port Elizabeth ................................................. 20 Figure 7: CDC plans for a ferro-metals cluster in Coega ........................................................ 22 Figure 8: Manganese ore rail line, Hotazel to Port Elizabeth.................................................. 23 Figure 9: Indicative schedule for trains on Hotazel - Port Elizabeth line................................ 24 Figure 10: Layout of manganese stockpile.............................................................................. 26 Figure 11: Schematic representation of manganese ore handling process .............................. 27 Figure 12: World Steel Demand 1945 – 2007......................................................................... 36 Figure 13: MBDA plan for area surrounding Port Elizabeth harbour ..................................... 40 Figure 14: Map of port showing Transnet land involved in Casino license application ......... 47

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm iii May 2008 _____________________________________________________________________ Executive Summary The Port Elizabeth Regional Chamber of Commerce and Industry (PERCCI) commissioned this report in order to analyse the pertinent issues relating to the relocation of the Port Elizabeth manganese ore terminal and tank farm. PERCCI views this relocation as a strategic intervention that will contribute to the overall development of the Ngqura port and the Coega Industrial Development Zone (IDZ), while at the same time enabling a waterfront development to the south of Port Elizabeth harbour. This will unlock the enormous development potential of this land, and significantly boost tourism and job creation in the region. The proposal for the development of a waterfront to the southern side of Port Elizabeth harbour has been the subject of many proposals and discussions over the years. It was mooted by the Burggraaf Committee in 1985 in their investigation into the potential for greater public use of South Africa’s harbours. It was subsequently taken up by Portnet in the 1990’s as a possible income generator to fund the Coega harbour development. More recently, it became the centre piece of the 2020 Vision that was championed by the Nelson Mandela Bay Metropolitan Municipality (NMBM) and the Mandela Bay Development Agency (MBDA). The MBDA prepared a " Master Plan" known as the Strategic Spatial and Implementation Framework (SSIF), which includes a waterfront development on the site of the manganese terminal and tank farm, and a linkage between the CBD and the waterfront. Various port plans have been drawn up by Transnet for Port Elizabeth harbour, some of which include the status quo, and some of which include the relocation of the manganese terminal and tank farm, and a port plan that dedicates the southern side of the port to a waterfront development and the fishing industry. The Department of Public Enterprises (DPE) has championed the use of strategic land adjacent to ports, and has done many of the feasibility studies that are used to motivate for the relocation.

The legal framework for the management of ports in South Africa is created by the National Ports Act, promulgated in 2005. Amongst others, the legislation provides for Port Developments Frameworks to be gazetted, which set out a long term plan for the use and functions of particular ports. The legislation also places a legal obligation on the National Ports Authority (NPA) to ensure that port services are provided equitably to users of the ports. It creates the legal basis for private operators and investors to take responsibility for operating port facilities, which could include the private operation of a manganese terminal. The case for relocating the tank farm once the leases expire in 2014 is overwhelming. There are very serious environmental and safety hazards associated with the current facility, and the costs of addressing these in the current location are prohibitive. The tank farm is inefficiently designed, out of date and beyond its safe lifespan. The oil industry is ready to plan and undertake relocation at their own cost, and this will not impact on Transnet’s balance sheet. They have various workable alternatives to consider, and the supply of petroleum products will not be compromised by relocation in 2014. Retaining the facility on the site opens both Transnet and the oil industry to serious risks of litigation, and exposes the CBD and city population to serious hazards. The relocation of the tank farm should also not be linked to the fate of the manganese terminal, as relocation is warranted in its own right. The Port Elizabeth manganese terminal is antiquated, and poses some serious environmental hazards. It has a capacity to handle 3,6 mtpa of manganese ore, and this capacity is currently being upgraded to 4,2 mtpa. There is a maximum capacity of 6 mtpa due to limitations on the

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm iv May 2008 _____________________________________________________________________ ore berth, and in terms of the original permit. Any growth in manganese ore export beyond this limit will require relocation to Ngqura or another port. The key issue in evaluating the financial viability of the relocation of the manganese terminal is the projected volumes of ore that will be processed by the terminal. The report analyses the manganese industry in South Africa, whose resources are estimated to be approximately 80 percent of total world manganese resources. However, South Africa produces less manganese ore than many other countries, partly due to its higher cost structure and long lines of transportation. The manganese industry in South Africa is dominated by Samancor and Assmang, but a number of new entrants to the market are pushing for increases in export volumes through Port Elizabeth. The overall outlook for manganese demand is good. Manganese is essential in steelmaking and demand for manganese has been rising faster than steel production in recent years. Steel demand is predicted to exceed 6% per annum for the next few years. Specific manganese consumption is growing again, and manganese intensive steel grades will grow faster than average. Non steel applications for manganese are also facing good growth prospects. In general, this means that there are limited downside risks for the next ten to fifteen years. Over the next few years local manganese players plan to increase their exports to 11mtpa, which is well in excess of the available capacity in Port Elizabeth. In order to expand the manganese ore export capacity, significant investments will be needed in upgrading the rail link from Kimberly to Ngqura, in rolling stock, and in the ore terminal. These investments will be needed regardless of whether the terminal remains in Port Elizabeth, or is relocated to Ngqura. The bulk of these costs relate to the rail upgrade and rolling stock. Transnet is currently finalising a feasibility study into the relocation of the Port Elizabeth manganese terminal. This was triggered by an earlier investigation done by DPE, which looked into the financial analysis of the relocation of the manganese terminal. Only the results of this earlier DPE study are available for analysis. The DPE study showed that, if Critical Infrastructure Funding was made available for Ngqura, there was not a significant difference from a commercial point of view between relocating to Ngqura and upgrading the facilities in the current location. A significant increase in the current tariffs was required in order to fund the investments in either scenario, and the industry has raised concerns that these tariffs will render South African exports uncompetitive. The key strategic difference between the two scenarios is that PE cannot realistically expand beyond 6 million tons per annum, making this a hard capacity constraint. The pro’s and con’s of the two scenarios are summarised below: Retention at Port Elizabeth The benefits of retaining the facilities in their current location are that this is business as usual, and no additional effort is required. There are limited capex requirements, and it is generally considered a ‘safe’ option. The risks associated with retention include the adverse environmental, safety and quality of life implications for the city and its population, and the fact that capacity expansion beyond 6mtpa is not possible in Port Elizabeth. The retention will also have the effect of freezing out the new players in the manganese industry, and compromise transformation initiatives in this regard. Ultimately the retention in Port Elizabeth will place a limit on the growth of the manganese ore export market. Relocation to Ngqura The benefits of relocating the terminal to Ngqura include significant economic and enterprise level benefits, and the overall catalytic effect that this will have on development in both Port

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm v May 2008 _____________________________________________________________________ Elizabeth and Ngqura. Ngqura is clearly also a more appropriate location for both the manganese terminal and tank farm. The risks associated with the relocation are that it requires complex integrated planning, and significant capital investment, which are subject to uncertainties about the future market for manganese ore. In addition there are property market risks associated with a very substantial waterfront development, although these will largely be borne by the private sector.

The poor condition of the current manganese ore export terminal is a major issue. The projected increase in manganese ore volumes for export and beneficiation suggests that government and Transnet should be planning on a more ambitious scale. The additional capex that will be required from the NPA and Spoornet for the relocation strategy is sufficiently compensated by the tariff increases paid by the manganese industry, and the net income derived from the released land. While this was estimated to be approximately R4 billion, the Southernport Developments arbitration will have resulted in this amount being reduced. There is also the issue of Transnet not wishing to engage in the property development business. Nevertheless with some careful planning and structuring it should be possible to Transnet to extract a significant portion of this value from a development. The overall benefits of enabling a waterfront development include the direct capital investment, accelerated growth in regional GDP, increased tourism, and the creation of both direct and indirect jobs. The combined tax revenue to Government from such a development further reinforces the economic returns to be derived from the relocation strategy. From the perspective of central government, any grant-based capital subsidy that may be required to place any single SOE in an equivalent economic position is therefore economically justified. The report concludes by exploring the actions and steps that will be required to facilitate the relocation and waterfront development. In order to effect a relocation by 2014, it will be necessary to carefully coordinate a number of complex decision making processes. The institutional arrangements that will be required to coordinate this are analysed.

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 1 May 2008 _____________________________________________________________________

1 Introduction The Port Elizabeth Regional Chamber of Commerce and Industry (PERCCI) has undertaken a strategic project to promote the transfer of the existing tank farm and manganese ore terminal from Port Elizabeth Harbour to the Coega IDZ. This will release the existing land, which is occupied by the tank farm and manganese terminal, for commercial development. This project is seen as strategic because it will unlock significant development potential, and massively stimulate the local economy for many decades to come. The relocation of the tank farm and manganese terminal, and the consequent redevelopment of the land as a waterfront, has enormous potential to:

• Boost employment, trade and investment within the NMBM area and adjacent regions.

• Build and enhance the tertiary sector within the region, including tourism and leisure. • Enhance the value of current land assets along the foreshore and adjacent land

holdings, thereby improving municipal rates and taxes and contributing to the municipality’s capacity.

• Enhance municipal infrastructure and the overall efficiency of the city. • Enhance the quality of life of Port Elizabeth’s citizens and improve environmental

quality. • Enhance the Port-City interface and create access for citizens to the unique character

and value of the port as a public asset. All major stakeholders in Port Elizabeth recognise the constraints imposed by the present location of the manganese ore handling facility and oil tank farm to unlocking the development potential of this land. The relocation will also have a positive economic impact on the Port of Ngqura, and the land released by this relocation will have considerably more value through an alternative use as a waterfront development. The purpose of this report is to investigate the issues relating to the relocation of the manganese terminal and tank farm, and in particular issues that will impact on the overall technical and financial viability of the relocation. The report also explores ways in which to release prime property for a mixed use waterfront development, thereby transforming the PE foreshore.

2 Background to proposals for relocation and waterfront The proposal for the development of a waterfront to the southern side of the Port Elizabeth harbour has been around for many years, and has been the dream of many planners within the municipality and the port. In 1985, the then Minister of Transport and Environmental Affairs established an inter-departmental commission of inquiry, known as the Burggraaf Committee, for the purposes of determining the potential for greater public use of South Africa’s harbours. It reported in 1987 that SATS (the predecessor of Transnet) should release land for leisure, recreational, commercial and residential purposes. The report identified the area around King’s Beach as developable, and suggested that a working harbour could be maintained in conjunction with a mixed use area, focussing on tourism, commercial and residential development. In the 1990’s, planners within Portnet and planners working on the Coega IDZ concept identified the development of a Port Elizabeth waterfront as a possible offset to the costs of building a deep water harbour at Ngqura. The proposal included relocating the Port Elizabeth

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 2 May 2008 _____________________________________________________________________ harbour's tanker berth and tank farm and manganese terminal facilities to Coega at a cost of R300-million, a move that would also boost the Coega project's industrial and commercial base and release prime land for the Port Elizabeth Waterfront development. Portnet MD at the time, Rob Childs, indicated that if the Ngqura project went ahead, they would seek to broaden the base of the project by spending an additional R300-million to move the tanker berth and tank farm and manganese terminal from Port Elizabeth to Ngqura. This would create critical mass at Coega and ensure Portnet was not reliant on only one "tenant". In support of the rationale, it was stated that "We would, of course, have to recoup the R300-mllion. By moving the berth, tank farm and terminal, we would not only get rid of an eyesore, but create a Waterfront on the 50ha of prime land which would be released on the Port Elizabeth harbour site." Portnet had developed plans for what it called the Algoa Marina, a waterfront development including commercial, residential, recreational and marina elements. However, these plans had not been developed in a holistic manner, taking account of the inner city development requirements. This project was taken up the previous Mayor of the metropolitan council, Cllr Nceba Faku, who championed an ambitious plan, known as Vision 2020, for the Metropole. Vision 2020 packaged together a number of inner city redevelopment projects with plans to grow the regional economy, boost tourism and create jobs. It included projects such as the Statue of Freedom, the Motherwell Urban Renewal Programme, the Port Elizabeth Harbour re-development and the relocation of the highways in Port Elizabeth. In 2002, the city council commissioned a number of planning studies including a Vision for the Inner City and The Downtown Study which focussed on the Central Business District. Amongst others these studies recommended that the city establish a development agency to champion the key projects identified by the city. The Mandela Bay Development Agency (MBDA) was accordingly established in 2004, and has operated within an inner city “Mandate Area” which covers approximately 1039 hectares. The MBDA commissioned a master plan for the 1039ha Mandate Area, and appointed a consortium including GAPP Architects, KPMG, Metroplan and Urban Dynamics to undertake market research to find out where investment gaps existed in Port Elizabeth’s property market. The master plan identified development potential and proposed a number of large capital projects such as a convention centre. The MBDA has championed these projects in order to revitalise Port Elizabeth’s deteriorating central business district and inner city. These projects have included the development of the southern part of Port Elizabeth’s harbour and the inner city’s Central Hill, Baakens River and Richmond Hill districts. The MBDA’s efforts have been directed to unlocking the southern part of the harbour for non-industrial development, and they have commissioned a number of studies and plans which will be reviewed in this report. These efforts have been given a significant boost through the work of the DPE, which established a property project to facilitate the strategic use of non-core land owned by SOE’s and promote the strategic development of land adjacent to inner cities and ports.

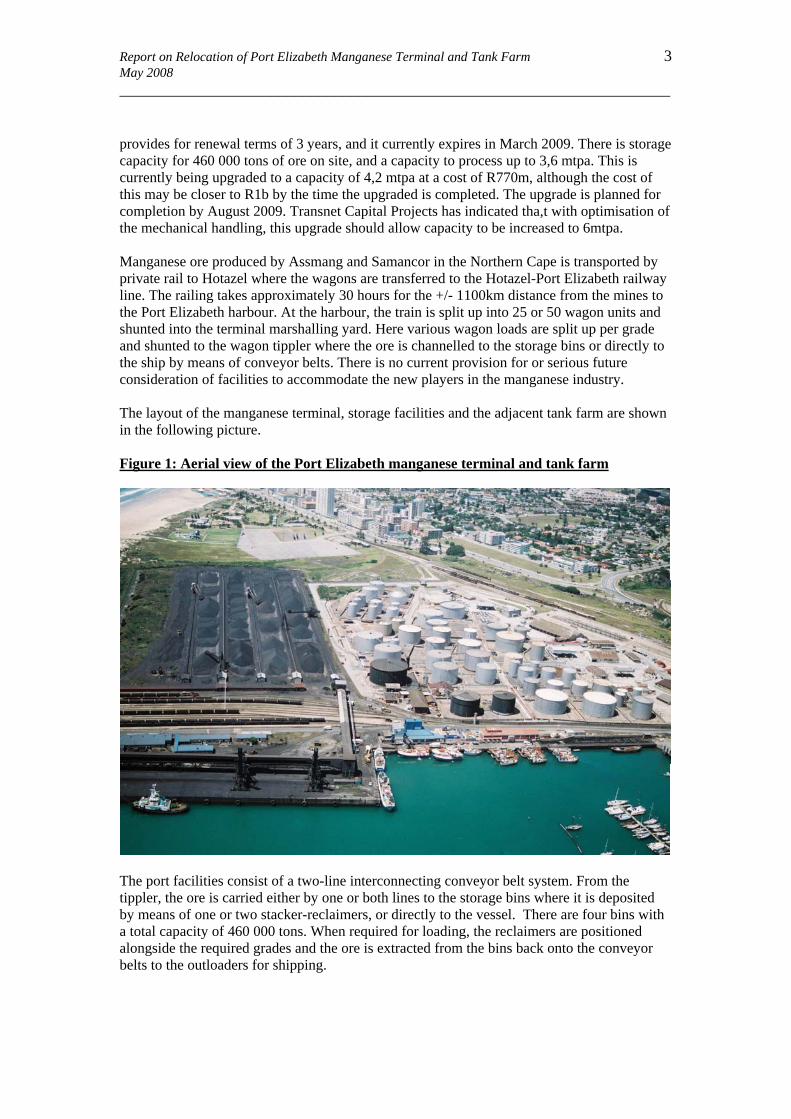

3 The Port Elizabeth Manganese Terminal The manganese ore terminal and storage facility at Port Elizabeth are the property of Transnet National Ports Authority (NPA), and they are operated by Transnet Port Terminals (previously known as South African Port Operations or SAPO). Together with the tank farm, they are situated on Erf 578 to the south of the harbour. The manganese terminal lease

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 3 May 2008 _____________________________________________________________________ provides for renewal terms of 3 years, and it currently expires in March 2009. There is storage capacity for 460 000 tons of ore on site, and a capacity to process up to 3,6 mtpa. This is currently being upgraded to a capacity of 4,2 mtpa at a cost of R770m, although the cost of this may be closer to R1b by the time the upgraded is completed. The upgrade is planned for completion by August 2009. Transnet Capital Projects has indicated tha,t with optimisation of the mechanical handling, this upgrade should allow capacity to be increased to 6mtpa. Manganese ore produced by Assmang and Samancor in the Northern Cape is transported by private rail to Hotazel where the wagons are transferred to the Hotazel-Port Elizabeth railway line. The railing takes approximately 30 hours for the +/- 1100km distance from the mines to the Port Elizabeth harbour. At the harbour, the train is split up into 25 or 50 wagon units and shunted into the terminal marshalling yard. Here various wagon loads are split up per grade and shunted to the wagon tippler where the ore is channelled to the storage bins or directly to the ship by means of conveyor belts. There is no current provision for or serious future consideration of facilities to accommodate the new players in the manganese industry. The layout of the manganese terminal, storage facilities and the adjacent tank farm are shown in the following picture. Figure 1: Aerial view of the Port Elizabeth manganese terminal and tank farm

The port facilities consist of a two-line interconnecting conveyor belt system. From the tippler, the ore is carried either by one or both lines to the storage bins where it is deposited by means of one or two stacker-reclaimers, or directly to the vessel. There are four bins with a total capacity of 460 000 tons. When required for loading, the reclaimers are positioned alongside the required grades and the ore is extracted from the bins back onto the conveyor belts to the outloaders for shipping.

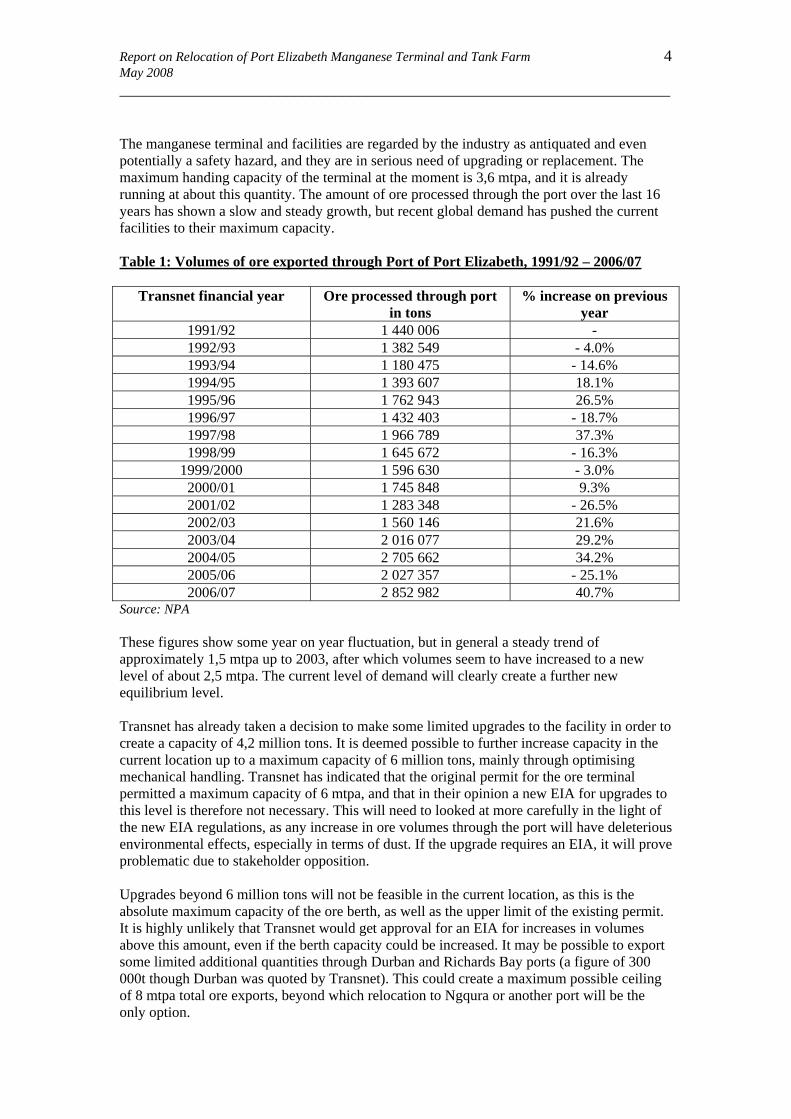

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 4 May 2008 _____________________________________________________________________ The manganese terminal and facilities are regarded by the industry as antiquated and even potentially a safety hazard, and they are in serious need of upgrading or replacement. The maximum handing capacity of the terminal at the moment is 3,6 mtpa, and it is already running at about this quantity. The amount of ore processed through the port over the last 16 years has shown a slow and steady growth, but recent global demand has pushed the current facilities to their maximum capacity. Table 1: Volumes of ore exported through Port of Port Elizabeth, 1991/92 – 2006/07

Transnet financial year Ore processed through port in tons

% increase on previous year

1991/92 1 440 006 - 1992/93 1 382 549 - 4.0% 1993/94 1 180 475 - 14.6% 1994/95 1 393 607 18.1% 1995/96 1 762 943 26.5% 1996/97 1 432 403 - 18.7% 1997/98 1 966 789 37.3% 1998/99 1 645 672 - 16.3%

1999/2000 1 596 630 - 3.0% 2000/01 1 745 848 9.3% 2001/02 1 283 348 - 26.5% 2002/03 1 560 146 21.6% 2003/04 2 016 077 29.2% 2004/05 2 705 662 34.2% 2005/06 2 027 357 - 25.1% 2006/07 2 852 982 40.7%

Source: NPA These figures show some year on year fluctuation, but in general a steady trend of approximately 1,5 mtpa up to 2003, after which volumes seem to have increased to a new level of about 2,5 mtpa. The current level of demand will clearly create a further new equilibrium level. Transnet has already taken a decision to make some limited upgrades to the facility in order to create a capacity of 4,2 million tons. It is deemed possible to further increase capacity in the current location up to a maximum capacity of 6 million tons, mainly through optimising mechanical handling. Transnet has indicated that the original permit for the ore terminal permitted a maximum capacity of 6 mtpa, and that in their opinion a new EIA for upgrades to this level is therefore not necessary. This will need to looked at more carefully in the light of the new EIA regulations, as any increase in ore volumes through the port will have deleterious environmental effects, especially in terms of dust. If the upgrade requires an EIA, it will prove problematic due to stakeholder opposition. Upgrades beyond 6 million tons will not be feasible in the current location, as this is the absolute maximum capacity of the ore berth, as well as the upper limit of the existing permit. It is highly unlikely that Transnet would get approval for an EIA for increases in volumes above this amount, even if the berth capacity could be increased. It may be possible to export some limited additional quantities through Durban and Richards Bay ports (a figure of 300 000t though Durban was quoted by Transnet). This could create a maximum possible ceiling of 8 mtpa total ore exports, beyond which relocation to Ngqura or another port will be the only option.

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 5 May 2008 _____________________________________________________________________ The NPA engages with Samancor and Assmang in a systematic way to plan future export volumes. They establish 6 year forecasts, which are used as the basis for planning. These forecasts are revised every three years. Transnet has indicated that the current contracts with exporters expire in 2008, and that these contracts are all under renegotiation. The NPA locks exporters into agreements based on these forecasts, with penalties for under-performance against forecast. It is notable that there is no recognition of the news players in the industry. The tariffs for the import and export of manganese through the harbour are set out in the Tariff Book published by the NPA. For manganese ore, these are set at R11.93 for both import and export of break bulk, and at R45.47 for the import and R5.67 for the export of dry bulk in the 2007/08 financial year. The revenues from these tariffs cover the operating costs of the terminal, but they do not cover the capital costs of the terminal, as these were written off many years ago. The tariffs also cover accruals for the future provision of new facilities. NPA has indicated that the manganese terminal is not a high revenue earner for them, especially compared to the adjacent tank farm, and they acknowledge that alternative land uses can produce far higher returns. Transnet and the industry use total channel tariffs as a basis for their negotations – these include tariffs for rail, terminal and port fees. From 1st April 2008 these have been increased to R220 per ton. Transnet has indicated to the industry that these tariffs will increase to R250 per ton to accommodate the upgrade to 4,2mtpa in Port Elizabeth. They estimate that these tariffs will need to increase further to R300 per ton for an upgrade to 6mt in Port Elizabeth. Transnet’s estimates of the tariffs to accommodate the Ngqura relocation are R380 per ton. Transnet has not been transparent about how these fees are calculated, and they seem excessive based the studies described in this document. McClintock and Skinner, based on their revised estimated of the rail and terminal costs, have indicated that in their view a more realistic tariff is R195 per ton for the total channel cost. The key issue for Transnet is whether the relocation of the manganese terminal to Ngqura is commercially viable, as it has implications for the Transnet balance sheet, and will impact on the financials of SAPO, NPA and Spoornet. There are high level capital expenditure estimates available for a relocated facility at Ngqura, which will be explored in further detail later in this document. The NPA has indicated that, in their opinion, there are a number of obstacles to relocating the manganese terminal to Ngqura, which are:

• The volumes of ore processed through the terminal do not yet justify relocation, and relocation should only be considered once predictable ore exports greater than 6 million tons per annum can be expected.

• Even at these volumes the move remains questionable financially, as there is a very limited ability within the manganese industry to accept higher tariffs. NPA estimates a funding gap of between R1b and R2b after factoring in some modest tariff increases.

• There is limited berth capacity at Ngqura, with the aluminium smelter taking up two additional berths. Consequently a manganese terminal will require the expansion of the port, will further capital costs.

• The rail link to Ngqura is also not adequate for moving the manganese ore to the port, and will to be upgraded, further adding to the costs.

• There is a concern that the location of the manganese terminal at Ngqura will lead to contamination of the aluminium smelter, and that the location of these facilities in the same port is not possible.

However, NPA also acknowledge that they face real problems in accommodating the new manganese exporters who are coming on stream, and that the NPA is under a legislative

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 6 May 2008 _____________________________________________________________________ obligation to provide services to these new players. They are also aware of the resistance from many role players to the current location of the facility, and are concerned that an EIA for an extensive upgrade in the PE harbour will be extremely difficult to negotiate.The NPA concerns will be addressed systematically later in the document, but a summary response to these issues is:

• Regarding the volumes of ore, if the new players are taken into account, then the 6 mtpa cut-off point has already been reached.

• Significant cost reductions can be obtained if a phased export facility based on the operations in Durban is constructed. Private operators have already made proposals for this, and are prepared to take the financial risk.

• The investment by Alcan appears to be no longer on the cards, and even if the investment goes ahead, there are ways in which to stagger the investment process so that new berth capacity can be constructed at a later date.

• The costs of upgrading the rail link will need to be incurred regardless of whether the ore is exported via Port Elizabeth or Ngqura. This is not a significant factor in choosing between the two scenarios.

• There is no evidence that contamination of the aluminium smelter is a risk, and the dust from the new ore terminal will be minimised with state of the art dust control measures.

4 The Port Elizabeth tank farm The Port Elizabeth tank farm is located on Erf 578, which is leased from NPA in terms of various lease agreements with the oil companies. These leases were concluded for periods of 20 years, and will expire on or before February 2014. The tank farm consists of 56 storage tanks with an average size of 1,5 to 1,6 million litres. There are two tanks with a capacity of 6 million litres, and one tank with a capacity of 13 million litres. The average height of the tanks is 16m. There are also two 1000m3 LPG gas spheres, which have been recently recommissioned by Easigas and Afrox. The fuel products stored at the tank farm are diesel (AGO), unleaded petrol (ULP95), jet fuel, illuminating paraffin, heavy fuel oil, feedstock and Aldorax. It is estimated that there is a total throughput of fuels within the tank farm in excess of 300 000 cmpa, which are transported out of the terminal by road and rail, and by pipeline to the airport. The tanker berth which serves the tank farm was constructed between 1936 and 1938, and the first fuel storage tanks were completed in 1939. In 1953 the berthing facilities were extended together with further fuel storage areas. There is a jet fuel pipeline which runs up to the airport from the tank farm. It is 4 inches in diameter and 5 km long, and pumps fuel approximately 8 hrs a day. The fuel line runs from the pump station at the North West corner of the tank farm, skirts the western boundary of the tank farm, and runs up the Baakens River valley to the airport. There are safety concerns with the jet fuel pipeline, and it has apparently failed the recent seismic tests. This pipeline is the one element of the tank farm that is not easily relocated to Ngqura, and a special solution will need to be found for it. The core elements of the system are the tanker berth for jet fuel, storage tanks, a pumping station, and fire control equipment. It is possible that jet fuel could be trucked or transported by rail from storage facilities at Ngqura, although there are dangers associated with the movement of such large quantities of fuel through an urban area.

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 7 May 2008 _____________________________________________________________________ The tank farm was previously divided up into segments each with their own storage facilities for different petroleum companies. Increasingly, the companies have shared storage capacity and load ramps, and they are now clustered into two groups. Shell and BP share facilities, and process about 800 000 litres per day of all fuel products. Engen, Caltex / Chevron and Total share facilities, and process about 1 million litres of all fuel products per day. There is approximately 21 days of stock available across all the fuel products – this is not deemed sufficient in the current context of fuel shortages and the impact on the economy. Other tank farms have a greater level of cooperation between the companies. For example, in Walvis Bay there is one operating company for the tank farm that manages it on behalf of all the petroleum industry. The most successful of the tank farms is the one in Mossel Bay, which runs at a profit. It is managed by 4 staff, and is supplied by PetroSA. It has a quick replenishment time and high volumes, which drives its profitability. The common-user tank farm concept has proposed in the original feasibility studies for a relocated facility at Coega, which is why a relatively small footprint is still shown in the CDC plans. By comparison the Port Elizabeth tank farm is run quite inefficiently. Shell has 12 staff, Caltex 26 and Total 5, which together with contractors makes for a total staff compliment of approximately 50 people. The use of storage space at the tank farm is also highly inefficient. The local engineers estimate that if an integrated approach to storage was adopted, the total number of tanks required to store the same volumes of fuel would be approximately 18, broken down as follows:

• Diesel 3 tanks • ULP95 4 tanks • Jet fuel 3 tanks • Illuminating paraffin 2 tanks • Heavy fuel oil 3 tanks • Feedstock & Aldorax 3 tanks

The lifespan of a fuel storage tank is estimated to be 35 years in the current environment. The marine environment is associated with much higher levels of corrosion, and this is exacerbated by the ship fed nature of the fuel, which inevitably includes some sea water. The first tanks were built in 1939, and they vary in dates, with the last tanks built in 1963. This means that the current life of the tanks is 45 years and older. The tanks are built with steel plate that varies in thickness from 10mm at the base of the tank to 6mm at the upper rim. Corrosion on the lower plates down to 6 to 8mm is highly likely in some instances, and this poses a serious threat of rupture. The tanks have a bund wall and floor as a secondary containment mechanism in the case of leakage. The SABS standard requires that this secondary containment is impervious and has the capacity to take the full volume of the tank plus 10%. However, most of the bund floors in Port Elizabeth are built with paving stones, and are not impervious. As a consequence, both the primary and secondary containment mechanisms for the tank farm do not meet modern safety and environmental standards. The end result of leakage will be that the fuel ends up in the harbour. The integrity of the tanker berth lines is also suspect. There are two lines of 250mm diameter stretching for approximately 1,5 km to the tank farm. The condition of these lines could be poor. A CIPS test of pipeline integrity has been done recently, but the results are not known.

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 8 May 2008 _____________________________________________________________________ Another area of concern is the integrity of the tank farm fire control systems. These are salt water based, and were installed by the predecessor of the Central Energy Fund over 20 years ago. The condition of the fire system is suspect. There has been extensive pollution arising from the tank farm over the years. This includes the following instances:

• The now disused pipeline from the tank farm to the bunkers was corroded and there are a number of points of leakage.

• Previously the sludge from the tanks was simply buried in holes in the ground dug next to the manholes. This practice was quite widespread. The sludge is from leaded fuel, and has a high heavy metals content.

• The load ramps for the tank farm are heavy spill areas, and there have been numerous incidents over the years.

• There are 5 to 6 sites of leakage on the Shell site alone, and probably similar amounts of leakage on the other sites.

It appears that historical estimates of leakage are also routinely underreported. This is partly due to fluctuations in the volume of the oil due to temperature changes – a 1O change in temperature can result in a 10 000 litre difference in volume, making losses as measured by the level in the tank very difficult to estimate. The tank farm leases specify that the improvement to the site will become the property of Transnet once the lease is terminated. Currently the lease for Total is set to expire in 2012, and the lease for the rest of the companies is set to expire in 2014. The industry has been informed by NPA that the lease is not renewable, and they have accordingly been considering their options for relocating. The oil industry has a policy of “product stewardship”, in terms of which they take responsibility for the environmental rehabilitation costs associated with the industry. The industry has therefore committed itself to the environmental rehabilitation of the tank farm on expiry of the lease. The experience of “greening” the Cape Town tank farm has demonstrated some of the difficulties associated with such rehabilitation, including the constant fight against the ingress of water during rehabilitation operations. It has been estimated that the costs in Port Elizabeth could be between 10 and 20 times the cost of the Cape Town rehabilitation. Estimates of the rehabilitation cost vary widely between R500m and R1billion. Kante and Templar consulting engineers have done a preliminary design and costing of a new tank farm on behalf of the industry. As a general guideline, it costs approximately R1 per litre of storage capacity to build a new tank farm. A cost estimate of R550 m was communicated in 2005, although it is not clear how accurate this is. The main issue is that the costs of relocation will be borne by the industry, and a new tank farm will be privately owned and operated. The relocation of the tank farm therefore has no implications for the Transnet balance sheet. The industry understands and accepts storage costs as an essential part of doing business, and has built these into the overall cost structure for petroleum. The industry norm for storage and handling costs is 0.4c per litre. This rate is meant to include provision for capital costs and depreciation, although industry players have indicated that in their view the capital element of this is understated.

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 9 May 2008 _____________________________________________________________________ The oil industry has established a relocation forum, which brings together the different companies. The forum is chaired by Mr Nic Titus from Engen, and it plays a facilitatory role with respect to decision making regarding the relocation. One alternative that has been considered by the industry is to do deliveries of fuel from East London, which has some spare storage capacity, and from Mossel Bay, where additional storage capacity can be easily built. However this is not optimal in terms of safety with the volumes of fuel on the road. Theoretically, there is no additional cost associated with this approach, due to compensation levies for inter-zonal transport, although there have been some difficulties associated with accessing this levy in recent years, which may be exacerbated by steadily rising fuel prices. Land for the construction of a new tank farm has been earmarked at Coega, although the distance of 22 km outside Port Elizabeth is not considered optimal. The industry looked at plans to locate the tank farm further inland outside the NPA and CDC areas, but the longer pipelines, booster pumps and additional servitudes made this option unviable. The recent announcement by PetroSA regarding plans to build a refinery on CDC land is significant, as there will inevitably be storage requirements that can be pooled with the industry’s needs. The main issue for the industry is to have adequate advance notice in order to plan for the relocation, and they would like to receive a firm decision from Transnet in this regard. The CDC has already developed plans to provide supporting infrastructure and utility services including electricity, but are concerned about the lack of an integrated approach to planning. There is certain key infrastructure that will need to be provided by NPA, including the liquid fuels berth and pipeline. NPA will need to have a project plan for this, which is coordinated with the project plan for the lessees on the construction of the tank farm, as well as with the plans of CDC, Sasol and PetroSA. The industry has indicated that these complexities mean that, if a new tank farm must be ready by 2014 to coincide with the expiry of the lease, the latest date for an investment decision on the new tank farm is 2009. However, a number of prior agreements will need to be put into place, so an in principle decision to relocate must be taken this year.

5 Environmental and health issues associated with the manganese terminal and tank farm

The environmental issues associated with the current tank farm and manganese terminal and storage facility have been documented in a study undertaken by Enviros Consulting in 2005. A State of the Environment study was commissioned by the MBDA as part of the Statue of Freedom initiative, and it highlighted the main environmental concerns associated with the current facilities. The environmental issues identified in the above report on the tank farm were largely confirmed by the Enviros study. In particular they highlighted the following major spills:

• Next to Tank 32 a spill of 30m3 of 93 octane unleaded fuel. • Tank 5 a spill of 8 m3 of JET A1 due to overfilling of tanks, also resulting in some

damage to the tanks. • Next to Tank 30, a spill of 5000 litres of White Spirit due to pipe corrosion. • Next to the LPG spheres, a seepage of various products including diesel, mogas and

White Spirit amounting to 3000 litres. • Product was also found to be leaking under the jetty at the fishing boat bunkering

jetty.

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 10 May 2008 _____________________________________________________________________ There have also been a large number of minor spills approximating 100 litres each, in areas such as the road loading gantry, the rail tank car loading gantry, the inlet discharge manifold number 1 and 2, the boiler house and next to the LPG spheres. The tank farm site and associated facilities are therefore quite considerably polluted. The site runoff currently drains into an underground drainage system, and flows into the harbour via a drain in the southern most part of the harbour. There is also a bund drainage berm and wetland to the south of the tank farm which collects waste water flowing from west to east. The ground water is also very shallow, and it is likely that contamination will remain on the site for considerable periods of time. The Enviros study noted that the tank farm site is in a sensitive location next to the CBD, and therefore that safety controls and emergency procedures need to be stringently adhered to. They recommend that the 1999 UK Control of Major Accident Hazards regulations should apply, and that an independent review and update of the risks associated with the installation should be undertaken. In particular they recommend a review of the external and internal emergency procedures, site security and the potential threat of terrorism, access and proximity control, and ongoing monitoring arrangements. To date these recommendations have not been acted upon, and the failure to do so opens the NPA and the oil companies to litigation. The main environmental hazard associated with the manganese terminal is a significant dust problem, which affects the general public in the direction of the prevailing winds (Summerstrand and suburbs). Particulate air pollution from manganese ore is now associated with a range of effects on health, including effects on respiratory, neurological and cardio-vascular systems. A wide range of medical research backs up these findings, and the research has been documented as part of this study. The WHO has issued guideline values which recognise an exposure limit of 0.15 micrograms per m3 averaged out over a year. The Medical Officer of Health carried out monitoring of the dust in the period 1985 to 1993, and concluded that the dust fall out from the operations was not significant. However, the standards that were being used at the time did not take account of the large body of research on the matter which has become available in the last decade. A spot sample of the dust from the ore terminal was analysed as part of the Enviros study, and it found the presence of trace elements including chromium, copper, nickel, lead, selenium, thallium and zinc. The report recommended that a proper system of monitoring be put in place, so that public health concerns can be allayed. The Enviros report concluded that contamination of the site by the tank farm and manganese terminal probably includes:

• Hydro-carbon contamination, including poly-aromatic hydrocarbons, of soil at the tank farm, with free product layers on the local water table, dissolved and emulsified hydrocarbons in the groundwater, a smear zone through tidal action, and the escape of volatile gases.

• Heavy metal contamination from the manganese ore storage facilities, which, while relatively immobile and low risk, will require physical isolation and coverage with clean material.

• Contamination of estuarine silts from both the above sources and discharged ballast. The Enviros report makes various recommendations regarding remediation of the site, which will involve quite extensive operations to deal with contaminated soil and groundwater. They indicate that an integrated approach to the whole site should be followed in order to reduce

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 11 May 2008 _____________________________________________________________________ costs. They also recommend a thorough risk based site assessment. The decommissioning process should be very carefully carried out, and a phased clean up run in parallel with the overall design and construction of the development. Lastly they recommend a careful system of validation monitoring in order to ensure that the risks arsing from residual contamination have been adequately addressed.

6 Legislative framework for ports in South Africa The new framework for the management of ports in South Africa is created by the National Ports Act, promulgated in 2005. In terms of the Act all the ports and their associated assets are transferred from the National Ports Authority of South Africa, a division of Transnet, to a newly created subsidiary company of Transnet known as the National Ports Authority (Pty) Ltd. This newly created subsidiary has its own Board and decision making structures, and is governed by its own legislation. In practice the NPA is the same organisation, although governed by a different legislative framework. The aim of the legislation was to update the regulatory framework for ports in South Africa, and create a clear delimitation of authority between the NPA, the Transport Minister and the Public Enterprises Minister. The Act aims to promote the development of an effective and productive South African ports industry. It also sets out to enhance transparency in the management of ports, and separate port operations from the landlord function within ports. Lastly the Act aims to facilitate private sector involvement and participation in port activities, which could be significant for the future operation of a manganese terminal at Ngqura. The main functions of the newly mandated National Ports Authority set out in the legislation are to own and manage ports to ensure their efficient and economic functioning. The Act specifies that the NPA must plan, provide, maintain and improve port infrastructure. It must also control land use within ports, and has the power to lease land under conditions that it may determine. The NPA must prepare a port development framework plan for each port, which must reflect the NPA’s policy for port development and land use within the port. The NPA is obliged to facilitate the building and exploitation of the infrastructure of ports, and regulate and control development within ports, in accordance with approved port development framework plans. The legislation places a number of obligations on the NPA which are significant for the purposes of this study. Firstly, it requires the NPA to remain financially autonomous, which means that the NPA will seek to ensure that new investment decisions are commercially viable. The Act also requires the NPA to ensure that port users have efficient access to the port system, and it must satisfy all reasonable demands for port services and facilities. In terms of port decisions, the Act requires the NPA to look at biophysical, social and economic issues in an integrated way in making decisions regarding port development and operations. The decision making authority in NPA is the Board, and amongst others the Board must approve all port reform measures, including concession agreements, and it must approve the sale, acquisition and long-term lease of property in ports. The Act specifically indicates that the NPA can encourage and facilitate private sector investments and participation in the provision of port services and facilities. This would allow, for example, a privately operated manganese terminal to be built at Ngqura. The Act provides for agreements with the private sector regarding port operations and services. The NPA can enter into agreements with private companies in order to design, construct, rehabilitate, develop, finance, maintain or operate a port terminal or port facility. These

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 12 May 2008 _____________________________________________________________________ agreements with private operators must allow the NPA to monitor and review performance with the operation of the terminal or facility. The agreements must also be awarded through a “procedure that is fair, equitable, transparent, competitive and cost-effective”. The Act provides for licenses to be issued by the NPA for private operators, and the terms and conditions of the license to be set out in the license. However Transnet are not obliged to bring in private port operators. In discussion with Transnet Capital Projects, it was clearly indicated that Transnet would not favour a privately operated ore terminal. The NPA is given the power to change the use to which immovable property may be put in order to improve the efficiency and effectiveness of the operations of the port, and it can direct the lessees and lawful occupiers of the property to alter the use to a new use. If the terms of a long-term lease which existed before this Act are substantially prejudicial to the operation of a port, the Authority can also direct that the applicable terms be renegotiated in order to remove the prejudice. These clauses may be significant if NPA needs to exit any arrangements relating the current tank farm and manganese terminal in Port Elizabeth. The Act includes provisions to boost the cooperation between NPA, municipalities and other government agencies (this would include, for example, the CDC). It obliges all organs of state to work together to ensure the effective management of all ports. It obliges the National Ports Authority to conclude a memorandum of understanding with the relevant organs of state to give effect to this co-operation, and it provides for the Minister to then publish this memorandum in the government gazette. The Act establishes a procedure for amending the boundaries of ports, which may be important for a potential waterfront development to the south of the PE harbour, as the port boundaries will undoubtedly need to be amended. The Minister of Transport can review, vary or extend the boundaries of ports after consulting the NPA and obtaining Cabinet approval. The Minister must consult with the municipality concerned if the amendment affects the municipal boundaries. The Minister is also obliged to follow an open and transparent process, which must include a viability study, and a strategic environmental impact assessment. There are implications of these provisions for Ngqura, where the NPA may require additional land currently owned by the CDC. The Act also establishes an independent ports regulatory body, known as the Ports Regulator, which exercises economic regulation of the ports system in line with government’s strategic objectives. The Ports Regulator is intended to promote equity of access to ports and their facilities and services. It can hear appeals and complaints and investigate complaints. It must also consider proposed tariffs of the Authority. This mechanism for approving tariffs will be important for the establishment of a new manganese terminal at Ngqura. Concerns have been raised regarding the ability of such a regulator to seriously challenge the current practices of Transnet.

7 Restructuring within Transnet The central decision maker with regard to the relocation of the manganese terminal and tank farm is Transnet, and it important to reflect briefly on some of the developments within Transnet, as this has implications for the outcome of a decision on relocation. Transnet has recently been through a major process of restructuring, designed to refocus the company on its core business of freight logistics. The main pillars of the Transnet corporate strategy have been stated as:

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 13 May 2008 _____________________________________________________________________

• Redirecting the business; • Restructuring the balance sheet; • Improving risk management and adherence to high standards of corporate

governance; and • Revitalising human capital.

Transnet intends playing a major role in enabling the economy to grow at 6%, in line with Government’s Accelerated and Shared Growth Initiative of SA (ASGISA). All the Transnet assets or businesses that do not support the strategy of building a world-class freight transport company are being sold, either to Government or the private sector. Transnet’s core or continuing businesses have been defined as:

• Transnet Freight Rail (previously known as Spoornet), the freight rail division; • Transnet National Ports Authority (NPA), which fulfils the landlord function for

South Africa’s port system; • Transnet Port Terminals (previously known as South African Port Operations or

SAPO), which operates the nation’s leading ports; • Transnet Pipelines (previously known as Petronet), the fuel and gas pipeline business;

Transnet Rail Engineering (previously known as Transwerk), the rolling stock maintenance division.

Transnet has undertaken a far-reaching business reengineering programme to build Transnet’s core business units into efficient, profitable and customer-oriented entities. The reengineering programme focused on unlocking synergies and improving interfaces between rail and ports, thereby growing Transnet’s market share and profitability. The programme is known as Vulindlela, and will run over several years. Vulindlela has consolidated all of Transnet’s internal reengineering and efficiency improvement initiatives, and has been focused on:

• The optimisation of Transnet Freight Rail’s iron ore line, the general freight business and the coal line;

• Improving maintenance practices and culture; • Containing costs, simplifying processes and improving service delivery; • Upgraded procurement processes; • Improving safety; and • Attention to Transnet Freight Rail’s National Operating Centre, which is focusing on

the scheduling of trains. Most of these initiatives have been concentrated in Transnet Freight Rail, because turning around the freight rail division is seen as key to Transnet’s future. Reengineering operations is also key to Transnet’s ability to make major infrastructure investments over the next five years. A major capital investment programme has been developed by Transnet in support of the broader economic growth that is expected to continue over the medium term. Transnet plans to commit R64,5 billion over the next five years to a capital expenditure programme. This programme is intended to address the significant investment backlog within Transnet, and lay the foundation in port, rail and pipeline capacity for future growth over the medium term. To ensure effective management and better coordination of this plan, Transnet has set up a central capital projects team within the Corporate Centre. This team oversees all capital projects above R300 million. The Capital Projects team is key to any investment decision relating to the relocation of the manganese terminal to the Port of Ngqura.

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 14 May 2008 _____________________________________________________________________ Centralising the major capital projects is designed to free up divisional managers to concentrate on managing their units, preventing cost and schedule overruns, and ensuring skills and technology transfers as a result of pairing experienced project professionals with less experienced ones. The major capital expenditure projects over the next five years include: Transnet Freight Rail (R31,5 billion)

• Iron ore corridor expansion (rail and Saldanha infrastructure); • Richards Bay coal line and infrastructure expansion; • Refurbishment/maintenance programme; and • General freight fleet renewal and upgrade programmes. • Transnet Rail Engineering (R2,6 billion) • Upgrade of equipment and facilities.

NPA (R18,6 billion)

• Completion of the Port of Ngqura; • Container terminal expansion – Cape Town and Durban; and • Durban port entrance channel project to enable growth and servicing of larger ships.

Transnet Port Terminals (R6,3 billion)

• Container terminals expansion – Durban, Cape Town and Ngqura; • Multi-purpose terminal expansion – Durban; • Iron ore terminal expansion; and • Richards Bay dry bulk terminal.

Transnet Pipelines (R4,9 billion)

• New multi-product pipeline; • Upgrade of the gas pipeline; and • Terminalling and logistics.

The costs of upgrading the manganese export facilities – both rail and ore terminal - need to be seen within the context of the overall capital expenditure programme. On the positive side, such upgrades fit within the overall vision and programme of Transnet, provided that Transnet can be convinced that they are integral to growing the South African manganese ore export market, and that they are commercially viable. It is useful to emphasize these broader strategies and objectives in opening up discussions with Transnet on this subject. Transnet NPA is a key player in the decision to relocate the manganese ore terminal, and it is important to note that this strategic division has itself been undergoing significant restructuring. NPA views its strategic objectives as growing a national port infrastructure by harnessing the opportunities of increased growth in international trade, while reducing the costs of port infrastructure management. It aims to position NPA as a competitive international ports management entity. In achieving this it will ensure that the respective coastal regions are assured of both bulk and general cargo port handling facilities. NPA is committed to creating capacity to meet current and future customer demand, and, applied to the manganese ore market, this means that NPA should be planning proactively to meet future demand. As will be demonstrated later, this has significant implications for the relocation strategy.

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 15 May 2008 _____________________________________________________________________ 8 Port Development Frameworks and port planning issues As indicated in the review of the new ports legislation, the NPA is required to prepare a port development framework for each port. Ideally this should be done in a consultative manner, including affected parties such as the NMBM and the CDC. The framework must reflect the NPA’s policy for port development and land use within the port. The framework then sets the context for all future work on port infrastructure and development. To date there have been no such frameworks published for either Port Elizabeth or Ngqura. A draft national ports plan was prepared by the Department of Transport and submitted to the Minister of Public Enterprises in 2006, but this plan has not been formally approved or published. Phase 1 of the Ports Master Plan, which details the strategy for each port, is being finalised by Transnet. The port planners within Transnet indicate that the port plans are at the moment being treated as flexible planning instruments, and that it may be premature, at least in the case of Port Elizabeth and Ngqura, to publish finished port plans. What is on the table at the moment are different options for development, rather than definitive port plans. Stakeholders have also indicated that in their opinion the current scenarios are not integrated plans, and they do not take account of local and regional imperatives. There should be a process of stakeholder involvement in the finalisation of the port plans. The main tasks of the national port planning process are to define the overall national economic objectives and their impact on the ports, and from there to define the responsibilities of the NPA. The port planning process enables Transnet and NPA to prepare a broad national traffic forecast, to assign traffic to individual ports, and thus enable NPA to prepare individual port plans and consequent investment plans. The port planners see a fourfold role for the port:

• To serve the international trading needs of the hinterland of the port. • To generate trade and regional development. • To capture an increasing share of international maritime traffic. • To capture an increasing share of distant hinterland traffic.

The Transnet port planners have made a number of presentations on port plans for Port Elizabeth and Ngqura over the last 2 years, and the following information has been gleaned from these presentations. It is important to understand the South African ports system as a complementary coupling of old and new ports in three regional nodes:

• Cape Town and Saldanha in the West • Port Elizabeth and Ngqura in the Centre • Durban and Richards Bay in the East.

These regional nodes service a global east – west flow of traffic, as well as the Gauteng and African hinterland. To a certain extent these regional nodes can be seen as competing for the hinterland traffic, but there is also a move towards a more rational distribution of port infrastructure, and a balanced inland transport corridor routing. Importantly within each regional node there is move towards a rational distribution of port functions. The older ports, located within cities, face serious constraints in terms of the movement of goods, as well as the environmental effects of heavy industry and certain cargo. There are also strong pressures from the cities for a more people friendly port – city interface, such as waterfront developments and access corridors. Port planners and managers tend to view these activities as interfering with port activities, and consider them as a serous constraint on the ports – however these views are portrayed as outdated by city planners and no longer appropriate in a changing global context.

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 16 May 2008 _____________________________________________________________________ Nevertheless the logic appears to suggest that the older city ports should be defined as “clean” ports, with a focus on fishing, foodstuffs, car terminals and waterfront developments, while the containers, break-bulk, dry bulk and liquid bulk are channelled through the newer “industrial” ports. However, local circumstances vary quite considerably, and there will be some residual industrial activities in each of the old ports for many years to come. The port of Ngqura is newest of all the ports, and is still under construction. The NPA is charged with developing the port to support new deep draft container traffic, as well as supporting industries that could locate at Coega. It will take over container, dry bulk and break bulk traffic from the Port of Port Elizabeth. The first phase of development comprises two dry bulk berths, two container berths and one bulk liquid berth. The dredged depth in the entrance channel and at the bulk liquid berth is 18 m, and alongside the inner berths 16.5 m. The harbour is designed to cater for future expansion depending on the increase in maritime traffic. In terms of the planning for the ports of Ngqura and Port Elizabeth, it is envisaged by the port planners that the containers, break-bulk, dry bulk and liquid bulk will largely move to Ngqura. The following projections of volumes through Ngqura have been used to inform port plans: Table 2: Projected volumes through Ngqura Port 2010 - 2050 2010 2020 2050 Containers (TEU) 428 000 999 069 4 312 047 Break-bulk (million tons) - 0.51 0.92 Dry bulk (million tons) 2.70 6.75 13.58 Liquid bulk (million tons) 1.10 1.25 1.69 Vehicles (units) - - - Source: Transnet NPA Based on these projections the port planners have prepared an indicative port plan for the first phase of Ngqura, which allocates 382 ha for containers, 526 ha for break-bulk, 448 ha for dry bulk, and 433 ha for liquid bulk. These volume projections do not include volumes arising from new manganese players, the ferro-manganese plants, the steel plant, the crude oil refinery and the Coega Power Station with an associated LNG Terminal. The port plan contains 7 berths, which may already prove to be inadequate to accommodate the above activities.

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 17 May 2008 _____________________________________________________________________ Figure 2: Port plan for first phase of Ngqura

Figure 3: 2050 scenario plan for Port of Ngqura

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 18 May 2008 _____________________________________________________________________ There are certain constraints that have arisen as a result of the Coega Aluminium Smelter (CAS) project, which has required two berths to be dedicated exclusively for its purposes. However latest developments bring into question the viability of this investment proceeding. The port managers have indicated that four berths will need to be assigned for containers, two for the CAS project and one for liquid bulk. This means that dry bulk and break-bulk will have to move through Port Elizabeth in the immediate term, and that these can only move over to Ngqura once the next phase has been completed. However the CDC has questioned this approach, indicating that in their opinion manganese ore exports can be commenced over the berth allocated for CAS, and switched if CAS does recommence later. The future expansion plans for Ngqura are shown in Figure 3, which gives an indication of how the port layout might look in 2050. Port expansion occurs in two directions - digging out berths inland of the current port (for which one of harbour walls was already built during construction) and adding additional container terminals to the west of the port. Importantly, these plans do indicate that if the CAS project goes ahead, accommodating the manganese ore export terminal will require an expansion of the current Ngqura port. If a phased approach as set out above is taken, revenue can be generated for a number of years to help improve the economics. Such a paradigm shift time towards enabling the relocation is now required. The plans for Port Elizabeth use as their departure point the current port layout, which is described in Figure 4. The main features of the current layout are well known, with containers and motor vehicles occupying the large No. 1 quay on the northern side of the port, break-bulk on the smaller No. 2 and 3 quays, ship repair and fishing on the western side of the port, and to the south in the yacht basin, the tank farm, the manganese terminal and the oil terminal. Figure 4: Current layout of Port of Port Elizabeth

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 19 May 2008 _____________________________________________________________________ Various scenarios have been drawn up by the port planners for Port Elizabeth, some of which include the status quo. The status quo option is based on retention of the manganese terminal and tank farm for the foreseeable future, largely because the current volumes of manganese through the port do not justify the investment in a new terminal. As will be shown later, the breakeven point in terms of volumes of manganese that justifies relocation is approximately 7 mtpa. However, some of the scenarios contemplated by the port planners include a relocation of the manganese terminal and tank farm, and a port plan that dedicates the southern side of the port to a waterfront development and the fishing industry. This plan is set out in figure 5 below. In the port planning process, there are also options that have been developed for the expansion of the Port Elizabeth harbour in a northwards direction. Such an expansion would be necessitated by an increase in movement of motor vehicles, which cannot be directed through the industrial port of Ngqura, as well as the retention and growth of a significant proportion of the container traffic. This does not seem to be a likely scenario at the moment, since the logic of building Ngqura was that it would accommodate the new deep water container vessels, and it requires the container traffic to be redirected through it to justify the investment in the port. However, this expansion scenario is included, because it remains an option to be considered. It is also significant in that it indicates that the port planners’ views on expansion are that it should take place in a northerly direction, and that the southern portion of the port can be used as a “softer” port – city interface. Figure 5: Future plan for Port of Port Elizabeth with waterfront

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 20 May 2008 _____________________________________________________________________ Figure 6: Port expansion plans for the Port of Port Elizabeth

9 The Coega IDZ and the Coega Development Corporation The Coega Industrial Development Zone (IDZ) is one of the incentive zones in South Africa for new industrial investments, and it is managed by the Coega Development Corporation (CDC) which is in charge of the IDZ, its infrastructure and the recruitment of investors. The logic behind the IDZ is that Coega is strategically located mid-way between the world’s major trade and supply zones. The new deep water port can accommodate the large container vessels that are the future of containerisation. Coega is equidistant from the main sources of the raw materials in the east and west, in addition to having access to South Africa’s mineral wealth. The IDZ covers 11 000 hectares of land adjacent to the Port of Ngqura, and is a phased development around industry clusters. The Coega IDZ aims to attract foreign and local investment in export orientated manufacturing industries. More recently a strong in-country demand has been recognised and the focus now includes local, regional and national industries. It has Custom Secure Areas dedicated for export oriented manufacturing companies located in the IDZ. The key priority investment sectors currently pursued by the CDC are in the following sectors:

• Metallurgical industries, including ferro-chrome, stainless steel, iron and steel slabs, and aluminium beneficiation

• Textiles, including industries related to flax, wool, mohair and agro-processing • Automotive industries such as automotive components and Original Equipment

Manufacturers • Services such as Financial Shared Services Centres and Call Centres • Chemicals such as Petrochemicals and Chlorine

Report on Relocation of Port Elizabeth Manganese Terminal and Tank Farm 21 May 2008 _____________________________________________________________________

• Alternative Energy Sources such as LNG • Crude oil refining.

One of the CDC’s main services is infrastructure provision, which is done in three phases or “tiers” – bulk services for the different industrial sectors (1st Tier), secondary distribution of services up to the site boundaries (2nd Tier) and finally site services (3rd Tier) for specific investor requirements. The first infrastructure investments in the Coega IDZ are focusing on areas where the first investors are locating. Zones 1 – 5 have been identified to locate the following activities: