Embed Size (px)

DESCRIPTION

report

Citation preview

A SUMMER TRAINING REPORTON

RECRUITMENT AND SELECTION OF LIFE ADVISORSIN

BHARTI AXA

Submitted in the partial fulfillment for the award of Degree of Bachelor in Business Administration

(2010-13)

UNDER THE GUIDANCE SUBMITTED BY

Mr. Miklesh Prasad yadav Sagar Gupta Faculty (Management), CPJCHS (07324201710)

CHANDERPRABHU JAIN COLLEGE OF HIGHER STUDIES & SCHOOL OF LAWAffiliated to Guru Gobind Singh Indraprastha University, Delhi

Plot No OCF Sector A-8, Narela New Delhi -40

DECLARATION

This is to certify that Thesis/Report entitled “recruitment and selection of life advisor” which is submitted by me in partial fulfillment of the requirement for the award of degree BBA to GGSIP University, Dwarka, Delhi comprises only my original work and due acknowledgement has been made in the text to all other material used.

Date: Sagar gupta

APPROVED BY \

Mr. Miklesh Prasad yadav

CERTIFICATE

This is to certify that Report entitled “recruitment and selection of life insurance agent” which is submitted by sagar gupta in partial fulfillment of the requirement for the award of degree BBA to GGSIP University, Dwarka, and Delhi is a record of the candidate’s own work carried out by him under my/our supervision. The matter embodied in this report is original and has not been submitted for the award of any other degree.

Date: Supervisor Signature

ACKNOWLEDGEMENT

I offer my sincere thanks and humble regards to Chanderprabhu Jain College of Higher S

tudies & School of Law, GGSIP University, New Delhi for imparting us very valuable pr

ofessional training in BBA.

I pay my gratitude and sincere regards to Mr.Miklesh Prasad yadav, my project Guide for

giving me the cream of his knowledge. I am thankful to him as he has been a constant sou

rce of advice, motivation and inspiration. I am also thankful to him for giving his suggesti

ons and encouragement throughout the project work.

I take the opportunity to express my gratitude and thanks to our computer Lab staff and li

brary staff for providing me opportunity to utilize their resources for the completion of th

e project.

I am also thankful to my family and friends for constantly motivating me to complete the

project and providing me an environment which enhanced my knowledge

Sagar Gupta

Executive summary

Introduction

A general term ‘insurance’ is related to service sector. Insurance is concerned with the pr

otection of economic value of assets. For example in case of a factory or a cow, the produ

ct generated by it is sold and income is generated. In this project the Bharti AXA Life Ins

urance Company is undertaken which is one of the popular sector insurance sectors. The

analysis of “Bharti AXA Life Insurance” is taken form different sectors.

For creating strong relationship and for a success full business every insurance company r

equired financial planner.

Objective of the study

How to recruit agents for Bharti-AXA life insurance.

To understand the process of recruitment and selection of agent in life insurance.

Why people are not willing to work as an agent in life insurance sector specially

with private companies.

Need of the study

The study is undertaken to know how many people are interested to work as life insuranc

e agent in Bharti AXA and their thinking about the Bharti AXA Life Insurance Company

or about private insurance company.

Table of Contentss.no topic Page

no1. CHAPTER- 1: INTRODUCTION

1.1 About the Industry 1.2 About Organization/ Company Profile 1.3 SWOT Analysis

1

2. CHAPTER– 2: Literature Review

2.1 Literature Review 2. 2 about the Topic

25

3. CHAPTER– 3: RESEARCH METHODOLOGY 3.1 Purpose of the study 3.2 Research Objectives of the study 3.3 Research Methodology of the study 3. 3.1 Research Design 3.3.2 Data Collection Techniques 3.3.3 Sample design 3.3.3.1 Population 3.3.3.2 Sample size 3.3.3.3 Sampling method 3.3.4 Method of data collection 3.3.4.1 Instrument for data collection 3.3.4.2 Drafting of a questionnaire 3.3.5 Limitations

48

4. CHAPTER –4: ANALYSIS& INTERPRETATION 4.1 INTERPRETATION

54

5. CHAPTER- 5: FINDINGS & SUGGESTIONS 5.1 Findings 5.2 Suggestions

58

6. CHAPTER- 6: CONCLUSION

61

7. CHAPTER-7: BIBLIOGRAPHY

63

Chapter 1

Introduction

INDUSTRY P ROFILE

W hat is insurance

Today insurance industry is growing fast. After coming the private players this industry is

becoming complex day to day and the competition is increasing very fast.

Insurance is basically a risk-sharing device. The losses to assets resulting from n

atural climates (life, fire, flood, earthquake, accident etc) are meet-out of common pool c

ontributes by large number of persons who are exposed to similar risk. This contribution

of money is used to pay the losses suffered by the unfortunate few. The basic principle is

that the loss should occur as a result of a natural calamity or an unexpected event beyond

human control and insured person should not making gains out of insurance

The business of insurance is related to the protection of the econom

ic values of assets. Every asset has a value. The asset would have been created through th

e efforts of the owner. Every asset is expected to last for a certain period of time during

which it will provide the benefits. After that, the benefit may not be available. Some of

the key characteristics of insurance are as follow-

.

1. Insurance is the method of the spreading and transfer to risk.

3. Loss of assets depriver the owner of the expected benefit.

4. Insurance is the content is a mechanism that helps to reduce the adverse conseque

nces due to loss of assets.

5. Insurance is assurance and protects the human life.

A bout insurance

The beginning of the insurance started to the city of London. It started with t

he marine business. Marine traders, who used to gather at Lloyd, are a coffee house in L

ondon, agreed to share losses to goods during transportation by ship. Marine related loss

es include:-

Loss of ship by sinking due to bad whether in high seas.

Goods in transit by ship robbed by ship pirates.

Loss of over damage to the goods in transit by ship due to bad whether in high sea

s.

The first insurance policy was issued in England in 1583.

L ife insurance in india

In India, insurance started in the early 19th century when the Britishers on thei

r postings in India felt the need of life insurance cover. It started with English companies

like, The European and the Albert”. The first Indian Insurance Company was the Bombay

Assurance Society Ltd. In 1870 .

By the mid 1950 there were around 170 insurance companies and 80 providen

t fund societies in the country life insurance scene. However, in the absence of regulator

y systems, scams and irregularities were almost a way of life at most of these companies.

As a result the government decided nationalizes the life assurance business in

India.The Life Insurance Corporation(LIC) of India was set up in 1956 to take over aroun

d 250 Life insurance companies. For years thereafter, insurance remained a monopoly of

the public sector. In 2000 have extensive powers to oversee the insurance business and re

gulate in a manner that will safeguard the interests of the insured.

Need of Life Insurance

Life insurance is a contract providing for payment of a sum of money to the person assure

d or, failing him, to the person entitled to receive the same, on the happening of certain ev

ent.

A family is generally dependent for its food, clothing and shelter on the income brought i

n at regular intervals by the bread winner of the family. So long as the he lives and the inc

ome is received steadily, that family is secure; but should death suddenly intervene the fa

mily may be left in a very difficult situation and sometimes, in stark poverty.

Uncertainty of death is inherent in human life. It is this uncertainty that is risk, which giv

es rise to the necessity for some form of protection against the financial loss arising from

death; insurance substitutes this uncertainty by certainty.

Advantages of Life Insurance.

1. It is superior to an ordinary savings plans

This is so because unlike other saving plans, it affords full protection against risk of death.

In case of death, the full sum assured is made available under a life assurance policy; wh

ereas under other savings schemes the total accumulated savings alone will be available.

The latter will be considerably less than the sum assured, if death occurs during early yea

rs.

2. Insurance encourages and forces thrift

A savings deposit can be too easily withdrawn. Many may not be able to resist the tempta

tion of using the balance for some less worthy purpose. On the other hand, the payment o

f life insurance premiums becomes a habit and comes to be viewed with the same serious

ness as the payment of interest on a mortgage. Thus insurance, in effect brings about com

pulsory saving.

3. Easy settlement and protection against creditors:

The life assured can name a person or persons to whom the policy moneys would be paya

ble in the event of his death. The proceeds of a life insurance policy can be protected agai

nst.The claims of the creditors of the life assured by effecting a valid assignment of the p

olicy. A married women’s property act policy constitutes a trust in favor of the wife and c

hildren and no separate assignment is necessary. The beneficiaries are fully protected fro

m creditors except to the extent of any interest in the policy retained by the assured.

4. Administering the legacy for beneficiaries:

It often happens that a provision which a husband or father has made through insurance is

quickly lost through speculative or unwise investment or by unnecessary expenditure on l

uxuries. These contingencies can be provided against in the case of insurance. The policy

holder can arrange that in the in the event of his death the beneficiary should receive, inst

ead of a single sum (a). payment of the net claim amount by equal installments over a spe

cified period of years, or (b).payment of the claim amount by smaller monthly installment

s over the selected period followed by a lump sum at the end thereof.

5. Ready marketability and suitability for quick borrowings:

After an initial period, if the policy holder finds himself unable to continue payment of pr

emiums he can surrender the policy for a cash sum. Alternatively he can tide over a temp

orary difficulty by taking loan on the sole security of the policy without delay. Further a l

ife insurance policy is sometimes acceptable as security for a commercial loan.

6. Tax relief:

For computing income tax (especially in India the Indian income tax act) follows deducti

on from income tax payable, a certain percentage of a portion of the taxable income of in

dividuals which is diverted to payment of insurance premiums. When this tax relief is tak

en into account it will be found that the assured is n effect paying a lower premium for hi

s insurance.

How Insurance Works

The mechanism of insurance is very simple. People who are exposed to the same risks co

me together and agree that, if any one of the members suffers a loss, the others will share

the loss and make good to the person who lost. All people who send goods by ship are ex

posed to the same risk related to water damage, ship sinking, piracy, etc. those owning fa

ctories are not exposed to these risks, but they are exposed to different kinds of risks like,

fire, hailstorms, earthquakes, lightening, burglary, etc. like this, different kinds of risks ca

n be identified and separate groups, made including those exposed to such risks. By this

method, the risk is spread among the community and the likely big impact on one is redu

ced to smaller manageable impacts on all.

If a Jumbo Jet with more than 350 passenger’s crashes, the loss would run into several cr

ores of rupees. No airline would be able to bear such a loss. It is unlikely that many Jumb

o Jets will crash at the same time. If 100 airline companies flying Jumbo Jets, come toget

her into an insurance pool, whenever one of the jumbo jets in the pool crashes, the loss to

be borne by each airline would come down to a few lakhs of rupees. Thus, insurance is a

business ‘sharing’.

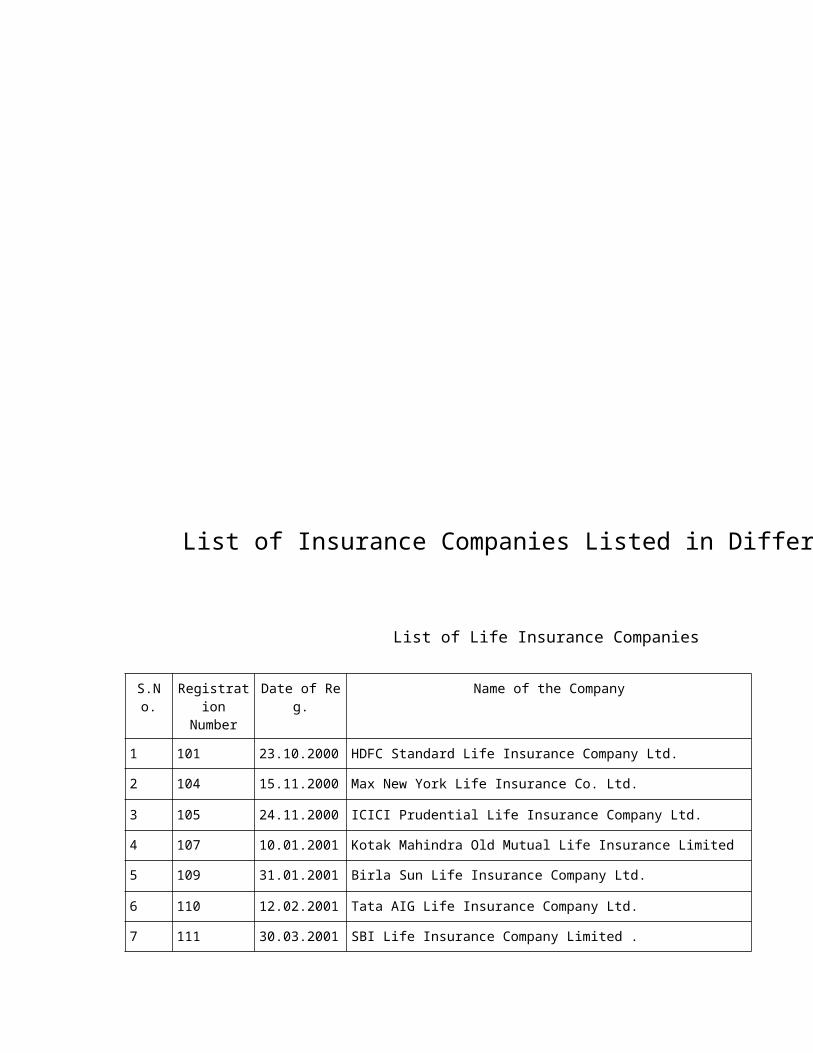

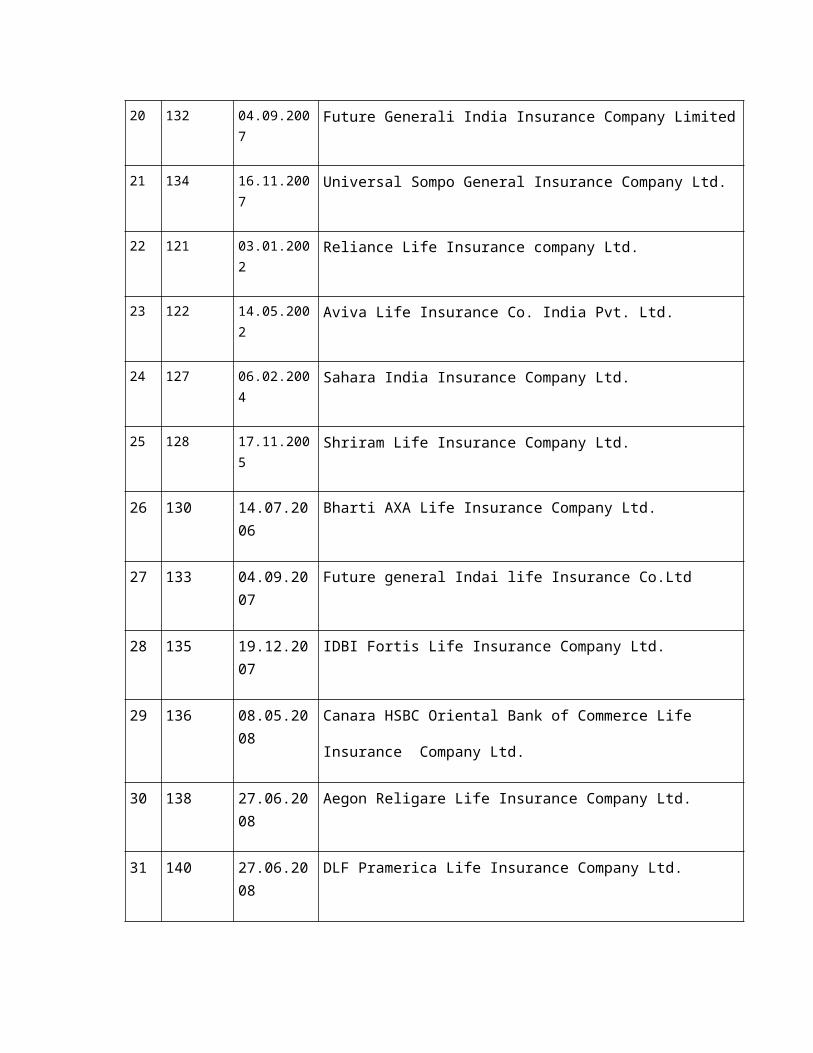

List of Insurance Companies Listed in Different Years

List of Life Insurance Companies

S.No. Registration

Number

Date of Reg. Name of the Company

1 101 23.10.2000 HDFC Standard Life Insurance Company Ltd.

2 104 15.11.2000 Max New York Life Insurance Co. Ltd.

3 105 24.11.2000 ICICI Prudential Life Insurance Company Ltd.

4 107 10.01.2001 Kotak Mahindra Old Mutual Life Insurance Limited

5 109 31.01.2001 Birla Sun Life Insurance Company Ltd.

6 110 12.02.2001 Tata AIG Life Insurance Company Ltd.

7 111 30.03.2001 SBI Life Insurance Company Limited .

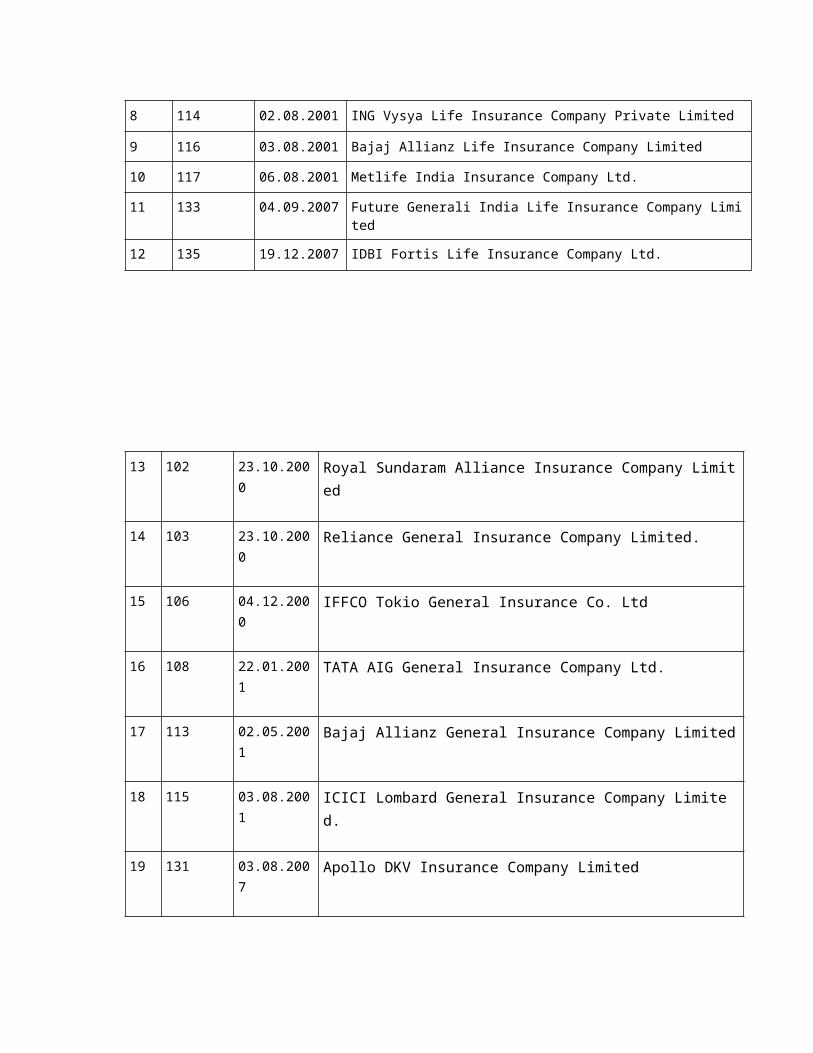

8 114 02.08.2001 ING Vysya Life Insurance Company Private Limited

9 116 03.08.2001 Bajaj Allianz Life Insurance Company Limited

10 117 06.08.2001 Metlife India Insurance Company Ltd.

11 133 04.09.2007 Future Generali India Life Insurance Company Limited

12 135 19.12.2007 IDBI Fortis Life Insurance Company Ltd.

13 102 23.10.2000 Royal Sundaram Alliance Insurance Company Limited

14 103 23.10.2000 Reliance General Insurance Company Limited.

15 106 04.12.2000 IFFCO Tokio General Insurance Co. Ltd

16 108 22.01.2001 TATA AIG General Insurance Company Ltd.

17 113 02.05.2001 Bajaj Allianz General Insurance Company Limited

18 115 03.08.2001 ICICI Lombard General Insurance Company Limited.

19 131 03.08.2007 Apollo DKV Insurance Company Limited

20 132 04.09.2007 Future Generali India Insurance Company Limited

21 134 16.11.2007 Universal Sompo General Insurance Company Ltd.

22 121 03.01.2002 Reliance Life Insurance company Ltd.

23 122 14.05.2002 Aviva Life Insurance Co. India Pvt. Ltd.

24 127 06.02.2004 Sahara India Insurance Company Ltd.

25 128 17.11.2005 Shriram Life Insurance Company Ltd.

26 130 14.07.2006 Bharti AXA Life Insurance Company Ltd.

27 133 04.09.2007 Future general Indai life Insurance Co.Ltd

28 135 19.12.2007 IDBI Fortis Life Insurance Company Ltd.

29 136 08.05.2008 Canara HSBC Oriental Bank of Commerce Life

Insurance Company Ltd.

30 138 27.06.2008 Aegon Religare Life Insurance Company Ltd.

31 140 27.06.2008 DLF Pramerica Life Insurance Company Ltd.

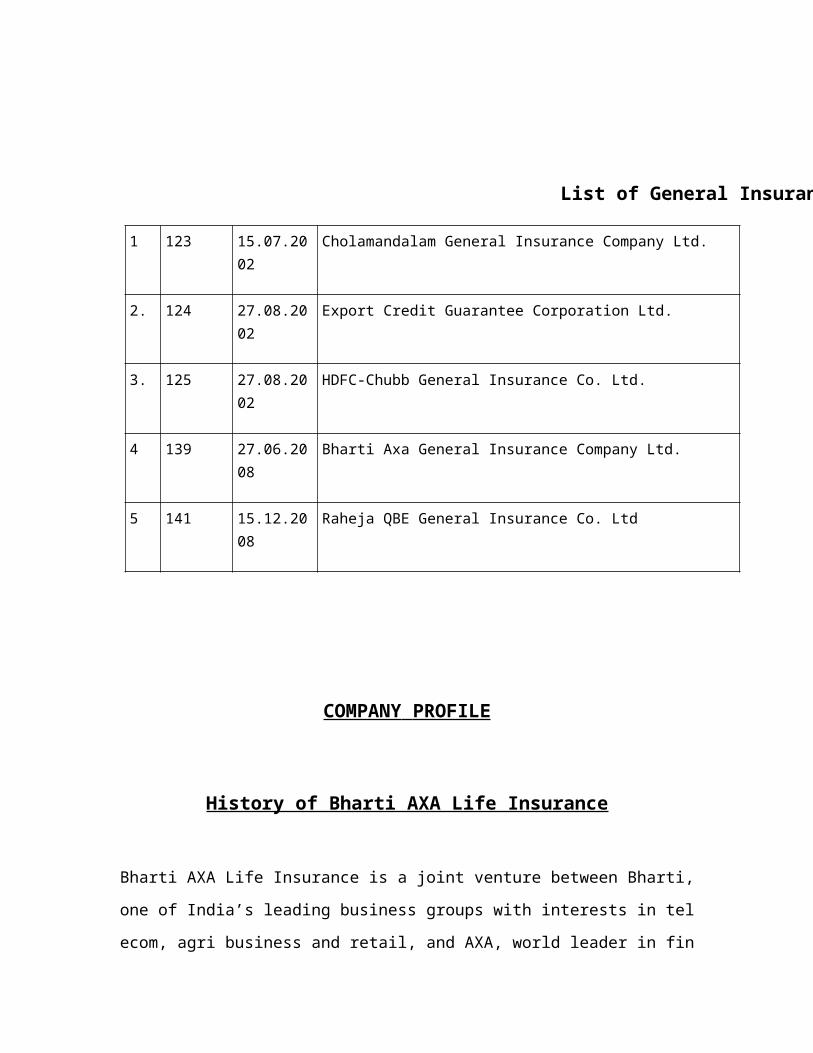

List of General Insurance Companies

1 123 15.07.2002 Cholamandalam General Insurance Company Ltd.

2. 124 27.08.2002 Export Credit Guarantee Corporation Ltd.

3. 125 27.08.2002 HDFC-Chubb General Insurance Co. Ltd.

4 139 27.06.2008 Bharti Axa General Insurance Company Ltd.

5 141 15.12.2008 Raheja QBE General Insurance Co. Ltd

COMPANY PROFILE

History of Bharti AXA Life Insurance

Bharti AXA Life Insurance is a joint venture between Bharti, one of India’s leading busin

ess groups with interests in telecom, agri business and retail, and AXA, world leader in fi

nancial protection and wealth management. The joint venture company has a 74% stake f

rom Bharti and 26%stake of AXA.

The company launched national operations in December 2006. Today, company have ove

r 8000 employees across over 12 states in the country and a national footprint of distribut

ors trained to provide quality financial advice and insurance solutions to the large Indian

customer base. Open first branch office in Hyderabad. Introduces 2 unit linked products-

“future confident’ and ‘wealth confident’

As we further expand our presence across the country with a large network of distributors,

we continue to provide innovative product and service offerings to cater to specific insur

ance and wealth management needs of customers. Whatever your plans in life, you can be

confident that Bharti AXA Life will offer the right financial solutions to help you achieve

them.

VisionTo be a leader and the preferred company for financial protection and wealth managemen

t in India

Values

1. Professionalism :-A professional is a collegial discipline that regulates itself by m

eans of mandatory, systematic training. It has a base in a body of technical and sp

ecialized knowledge that it both teaches and advances it sets and enforces its own

standards and it has a service rather than a profit orientation, enshrined in a code o

f ethics.

2. Innovation: - Innovation . . . is generally understood as the successful introduction of a new thing or method . . . Innovation is the embodiment, combination, or synthesis of knowledge in original, relevant, valued new products, processes, or services.

3. Team Spirit :-team spirit is the spirit of a group that makes the members want the

group to succeed

4. Pragmatism :-Pragmatism is the philosophy of considering practical consequence

s and real effects to be vital components of meaning and truth.

5. Integrity : - Integrity is consistency of actions, values, methods, measures, princip

les, expectations and outcome. As a holistic concept, it judges the quality of a syst

em in terms of its ability to achieve its own goals.

Bharti AXA Life Insurance – Growing Presence

Number of cities - 111 Number of offices - 163 Number of Agents - 30,000 PLUS.

Strategy

To achieve a top 5 market position in India through a multi-distribution, multi-pro

duct platform

To adapt AXA's best practice blueprints as a sound platform for profitable growth

To leverage Bharti's local knowledge, infrastructure and customer base

To deliver high levels of shareholder return

To build long term value with our business partners by enhancing the proposition

to their customers

To be the employer of choice to attract and retain the best talent in India

To be recognised as being close and qualified by our customers

Bharti group

Milestones of bharti group

In 1976, the foundation of bharti group was laid.

In 1981, started the business of importing the generators.

In 1984, introduced the push button phones in India.

In 1995, set up airtel to enter mobile telephone service.

In 2006, entered into the JV with wal-mart.

In 2006, set up bharti comtel.

In 2006, entered in to insurance business through a joint venture with AX

A Asia pacific holdings Ltd.

In 2010, acquires zain telecom’s business in 15africa countries.

Bharti group facts

Bharti group operates in 21 countries across the globe.

Bharti group has 19 different countries.

Bharti group was founded in year 1995

5th largest telecom company worldwide.

In India, airtel holds 30% market share.

airtel has revenue of $7.8 billion

Bharti enterprises

Bharti Airtel Ltd

Bharti Airtel Ltd is one of Asia's leading telecommunications service provider. The Com

pany is India’s largest integrated telecom company in terms of customer base and offers

Mobile Services, Fixed Line services, Broadband & IPTV, DTH, Long Distance and Ente

rprise services. Airtel also offers mobile services in Sri Lanka on a state-of-the art 3.5 G n

etwork.

Bharti TeleTech Ltd

Bharti Teletech is India’s leading telecom & allied products company. It is one of the larg

est manufacturers of landline telephones in the world. With a strong distribution network

across the country, the company is also the primary distributor of IT and Telecom produc

ts from interntional brands such as Motorola, Blackberry, Thomson, Polycom, Transcend,

and Logitech.

Telecom Seychelles Ltd

A subsidiary of Bharti, Telecom Seychelles Ltd provides comprehensive telecom services

including 3G mobile services in Seychelles, under the ‘Airtel’ brand.

Comviva Technologies Ltd

Comviva is the leading provider of integrated VAS solutions for mobile operators in eme

rging markets. Among the top 3 global providers of integrated VAS solutions in rapidly g

rowing markets, Comviva has deployed solutions for over 100 mobile operator customers

in over 80 countries worldwide.

FieldFresh Foods Pvt. Ltd.

FieldFresh Foods Pvt. Ltd., is a venture between Bharti Enterprises and Del Monte Pacifi

c Limited, to offer fresh and processed fruits and vegetables in the domestic as well as int

ernational markets, including Europe and the Middle East.

Bharti Retail Pvt Ltd

Bharti Retail is a wholly owned subsidiary of Bharti Enterprises. Bharti Retail operates a

chain of multiple format stores that offer consumers affordable prices, great quality and w

ider choice. The company’s neighbourhood format stores operate under the "Easyday" br

and and the compact hypermarket format under the “Easyday market” brand.

Bharti AXA General Insurance Company

Bharti AXA General Insurance is a joint venture between Bharti Enterprises and AXA, w

orld leader in financial protection and wealth management. The company was incorporate

d in July 2007 and offers a full suite of general insurance solutions to meet the needs of b

usinesses and individuals alike.

Bharti AXA Life Insurance Company

Bharti AXA Life Insurance Company Ltd is a joint venture between Bharti Enterprises an

d AXA, world leader in financial protection and wealth management. The company offer

s a range of life insurance and wealth management products with an endeavour to help cu

stomers lead a confident life.

Bharti AXA Investment Managers Pvt. Ltd.

Bharti AXA Investment Managers Pvt. Ltd., an asset management company in India, is a

joint venture between Bharti Enterprises, AXA Investment Managers (AXA IM) and AX

A Asia Pacific Holdings (AXA APH).

Centum Learning Limited

Centum Learning Limited provides end-to-end learning and skill-building solutions to se

veral large corporates. It provides solutions that impact business performance through en

hanced employee productivity, customer profitability and effective talent transformation.

Jersey Airtel Ltd

Jersey Airtel, a subsidiary of Bharti, offers world-class mobile services in Jersey (Channe

l Islands) over its full 2G, 3G and HSDPA enhanced network. The Company brings mark

et-leading products and services to its customers under Airtel-Vodafone brand.

Bharti Foundation

Bharti Foundation was set up in 2000, with the vision, “To help underprivileged children

and young people of our country realize their potential”. It aims to create and support pro

grams that bring about sustainable changes through education and the use of technology a

nd information.

Bharti Realty

Bharti Realty Limited is a young, vibrant and dynamic realty company with expanding in

terests in commercial, retail and residential real estate. Bharti Realty aims to be amongst t

he most admired real estate players in India and aspires to attain highest degree of custom

er trust through superior product design and maintaining an uncompromising stand towar

ds environmental responsibility, ethics and safety

Bharti Infratel

Bharti Infratel, a wholly owned subsidiary of Bharti Airtel, provides passive infrastructur

e services on a non-discriminatory basis to all telecom operators in India. Bharti Infratel a

lso holds approximately 42% stake in Indus Towers, a joint venture between Bharti, Vod

afone and Idea to offer passive infrastructure services.

AXA GROUP

AXA Group is a worldwide leader in Financial Protection. AXA's operations are diverse

geographically, with major operations in Western Europe, North America and the Asia/P

acific area. AXA had Euro 1,315 billion in assets under management as of December 31,

2006. For full year 2006, IFRS revenues amounted to Euro 79 billion, IFRS underlying e

arnings amounted to Euro 4,010 million and IFRS adjusted earnings to Euro 5,140 millio

n

Axa group was originally founded in 1816.axa is world’s leading financial service

provider with across 5 continents in 57 countries.

France , china , Australia , new Zealand , Hong Kong , Singapore , Thailand , Ind

onesia , Philippines and major countries across Europe , north America and Asia

pacific.

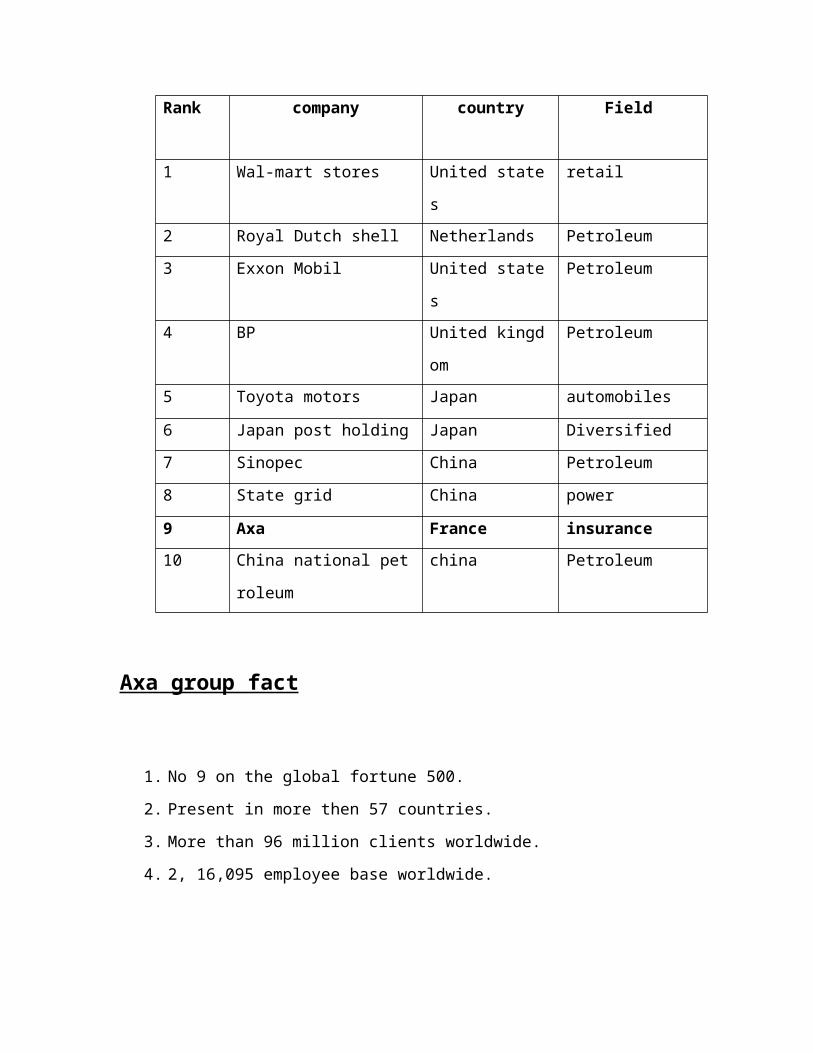

Fortune global 500

Rank company country Field

1 Wal-mart stores United states retail

2 Royal Dutch shell Netherlands Petroleum

3 Exxon Mobil United states Petroleum

4 BP United kingdom Petroleum

5 Toyota motors Japan automobiles

6 Japan post holding Japan Diversified

7 Sinopec China Petroleum

8 State grid China power

9 Axa France insurance

10 China national petroleum china Petroleum

Axa group fact

1. No 9 on the global fortune 500.

2. Present in more then 57 countries.

3. More than 96 million clients worldwide.

4. 2, 16,095 employee base worldwide.

Products of Bharti-AXA Life Insurance

Bharti AXA Life Insurance offers a suite of flexible products. It has 7 life insurance prod

ucts and 8 riders that can be customized to over 400 combinations enabling customers to

choose the policy that best fits their need. Some important product offered by bharti AXA

are-

1. Future confident- This product is designed to meet the long term needs of the custom

ers like meeting the educational need of the children

2. Wealth confident scheme-This is the flagship product of Bharti AXA life insurance. I

t is a unit linked investment and protection product which is providing risk cover for 10 y

ear but the customer has to pay premium only for 5 years, it also provide customer the fle

xibility in premium payments .

3. Invest Confident– This policy is designed for those people who want to invest throug

h a single larger premium.

4. Secure confident– This product is designed to meet the need of those customers who only want to take risk cover and not taking policy as an investment.

5. Save confident– This product is a traditional money back insurance product. It offers a combination of benefits like liquidity, long term saving and risk cover.

6. Aspire life – This is an ULIP product, designed to meet the needs of those customers who want to invest money for a longer period of time.

SWOT ANALYSIS

Strength

Bharti AXA Life Insurance Company India’s Most Respected Company in the ins

urance industry of India.

Excellent services

Customized of product as per customer needs

Brand image

Business experience

Strong financial base

Innovative product technology, organization culture and environment.

Weakness

Lot of the competitions is in the market offers some product difference in the pre

mium and offerings.

Target only bigger income group where other companies are trying to catch middl

e lower level people.

Higher premium as compared to the other companies.

Client face problem to get insured due to large number of formalities.

High target of financial advisor and for the sales development.

Opportunity

Huge market is literally untapped out of estimated 320 million is usable markets

only 20% of the population is insured.

In the pension field where people want good life after their retirement.

Indian people are more emotional towards their children that are why children pl

an are selling like hot cakes.

Health insurance and pension schemes and estimated market potential of approxi

mately $ 10 billion.

Threats

Weak perception of private players in the minds of Indian people due to frequent f

inancial schemes.

Large number of insurance players.

Current government policies do not encourage gross domestic savings.

Of the tax liabilities of the service rises the customers will have little money to in

vest.

And change rules day by day more rigid which is very difficult for the company.

Chapter 2

Literature Review

LITERATURE REVIEW

Objectives of the study

To understand the process of recruitment and selection of agent in Bharti AXA lif

e insurance.

How to recruits agent for Bharti-AXA life insurance

To know about the view of general public about the job of agent

Why people are not willing to work with as an agent, especially with private playe

r.

Meaning of Recruitment

Finding the right people is a make-or-break factor for success in business today. Recruitin

g the top talent for a job takes time and you have to attract quality candidates who have th

e knowledge and skills needed to help your company grow.

The fact is, your success with recruitment depends on how well you prepare your job ad,

and use source of recruitment, and your interviewing skills.

Prepare a job ad that works to start, you want to be sure that your potential candidate trul

y understands the job. The clearer you are with the task description, working conditions a

nd advantages, the less time you will waste examining and rejecting applications

The essentials of any job description are:

A brief description of your company

Detailed outline of the tasks involved

Qualifications and experience required

Equipment and resources used to do the work

Skills required using them.

However, you should also include work benefits (e.g., vacation, travel and perks), general

working conditions (e.g., scheduling, outside work) and the specific traits required (e.g.,

teambuilding and communications skills). Ultimately, you want to be perceived as an attr

active employer in a competitive market.

Find the right recruitment vehicle choose the vehicle that best works for your company, d

epending on your budget and resources.

Word of mouth, or simply telling your employees, friends and colleagues about a job ope

ning, is a less expensive strategy but generates fewer candidates. The advantage is that yo

u already know something about your recruiters and their skills, knowledge and achievem

ents. This is a preferred method with companies that have a finder's fee program for their

employees.

Advertising is a toss of the dice. If it goes well, it can help you find ideal candidates in a r

egional, national, or international pool. If not, it's a costly investment yielding few results.

Make sure to factor in the time it takes to go through a large number of resumes.

Employment agencies cost more but generally provide a good range of candidates. The e

mployment advisors look at your needs, screen a number of candidates, and only send yo

u the applications that meet your requirements. Bear in mind that the largest employment

agencies do not necessarily offer the best choice of candidates. There are numerous agenc

ies that specialize in recruitment in specific sectors.

Recruiting online such as monster.ca, workopolis.com, and jobboom.com. These can pro

vide inexpensive, worldwide access to employees. In fact, 65% of job seekers now have a

ccess to these types of services.

Using the Internet for recruiting usually involves regular visits to specialized recruitment

sites, joining newsgroups, and posting your job openings on recruitment sites, electronic

publications and on your own Web site.

Sources of Recruitment

Controlled sources

Natural market

Your family

Your friends

People at job/business

Neighbors

Extended Natural market

The following are sources of names:

People know through children.

People know through spouse.

People know through hobbies/ games.

People known through social groups

People known through public service.

People you do business with.

Friends of friends.

C enter of influence

People with influence and prestige, other member of society believe and faith on t

hem.

People who have a big circle of relationships: like secretary in societies, president

of an association.

People who are known to you and are wiling to help you.

People who have contacts with the class of people you want to deals with

People who have faith in your leadership.

A centre of influence is a person who is in contact with many people through soci

al, political, religious or business angulations

Usually a respected individual with influence over the people with he/she is in co

ntact.

Uncontrolled Sources

Job Ads/Inserts

This program should be on regular long range basis.

Example: Navajeevan sharma who is a relationship officer in bhrati AXA Life Ins

urance company put an ad in the newspaper, in which he called for the reader to p

hone him during a specified 2 to 4 hours period on Monday or Sunday morning

From those who called Navjeevan Sharma was able to eliminate more misfits (wh

o are not qualified) and arrange for two to six personal visits.

Placement consultants

MOA can recruit a placement consultant or register him self in internet job search sites to

get list of prospects.

Seminars/job fairs

Manager of agency can also organized seminars at

management institutes and colleges.

OR

Bharti AXA life insurance company participate in the job fairs and then short list

prospects and then look for further opportunities for them.

Cold Prospecting

MOA can use the telephone directory.

MOA and telecaller can use the directories of various business and social organiza

tions.

Database

Primary data: Direct collection of data of from the source of information, techno

logy including personal interviewing, survey etc.

Secondary Data: Indirect collection of data from sources can be purchased from t

he open market and various kind of database are available such as telephone datab

ases of various surveys.

Point to be noted while recruiting the Agents

Mature and responsible family person.

Ambitious, hungry for recognition, challenges.

Occupation.

Experience and current designation.

For how many years he is living in the city.

Greedy person.

Occupation of parent.

Family income.

Any experience in life insurance sector.

Leadership qualities.

Social and amiable.

Recruitment and selection Process

↓

↓

↓

↓

Recruitment and S election of best candidates

Develop a Profile

Approaching the Targeted recruits

Initial screening and Interviews

Reality check

Develop sources of recruitment

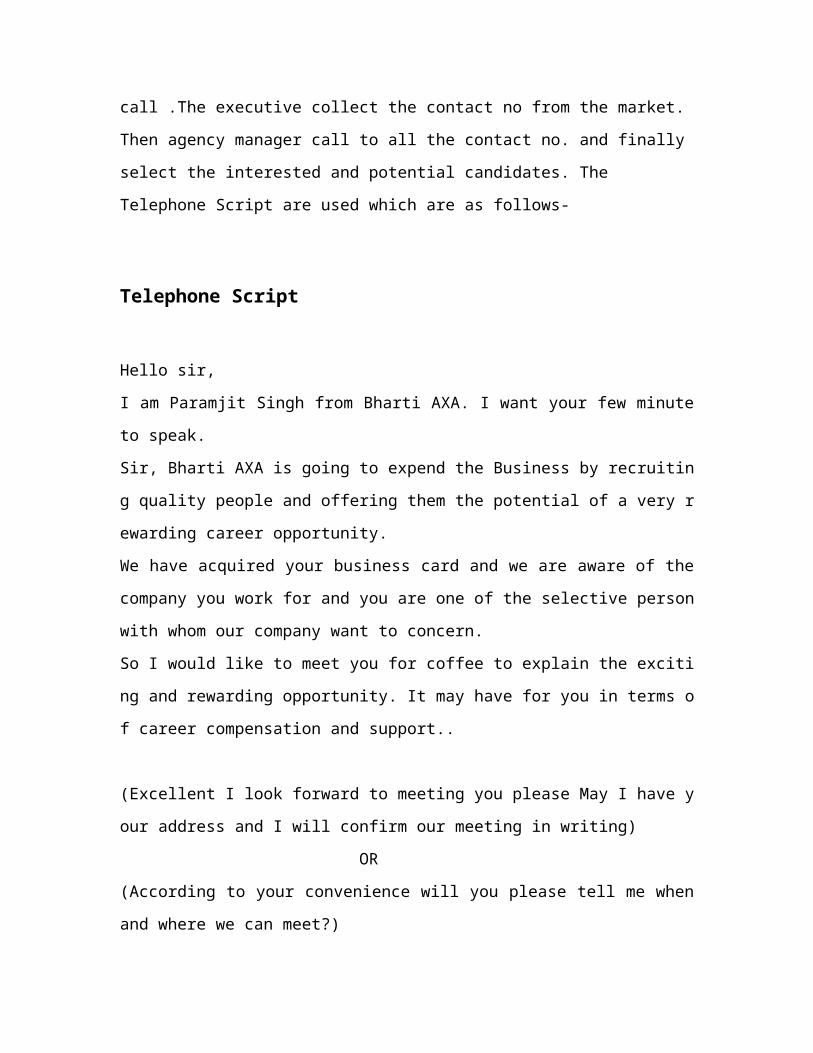

Recruitment of the advisors starts from the telephone call .The executive collect the

contact no from the market. Then agency manager call to all the contact no. and finally

select the interested and potential candidates. The Telephone Script are used which are as

follows-

Telephone Script

Hello sir,

I am Paramjit Singh from Bharti AXA. I want your few minute to speak.

Sir, Bharti AXA is going to expend the Business by recruiting quality people and offering

them the potential of a very rewarding career opportunity.

We have acquired your business card and we are aware of the company you work for and

you are one of the selective person with whom our company want to concern.

So I would like to meet you for coffee to explain the exciting and rewarding opportunity.

It may have for you in terms of career compensation and support..

(Excellent I look forward to meeting you please May I have your address and I will confir

m our meeting in writing)

OR

(According to your convenience will you please tell me when and where we can meet?)

Thank You Sir.

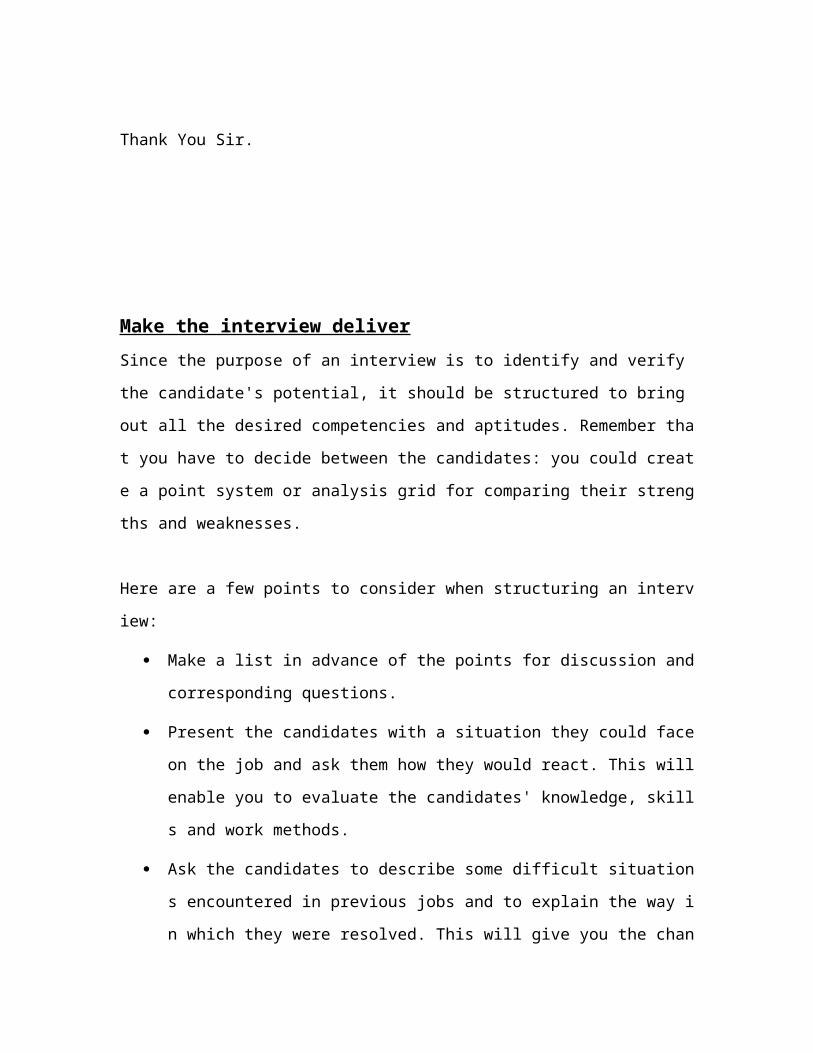

Make the interview deliver

Since the purpose of an interview is to identify and verify the candidate's potential, it sho

uld be structured to bring out all the desired competencies and aptitudes. Remember that

you have to decide between the candidates: you could create a point system or analysis gr

id for comparing their strengths and weaknesses.

Here are a few points to consider when structuring an interview:

Make a list in advance of the points for discussion and corresponding questions.

Present the candidates with a situation they could face on the job and ask them ho

w they would react. This will enable you to evaluate the candidates' knowledge, s

kills and work methods.

Ask the candidates to describe some difficult situations encountered in previous jo

bs and to explain the way in which they were resolved. This will give you the cha

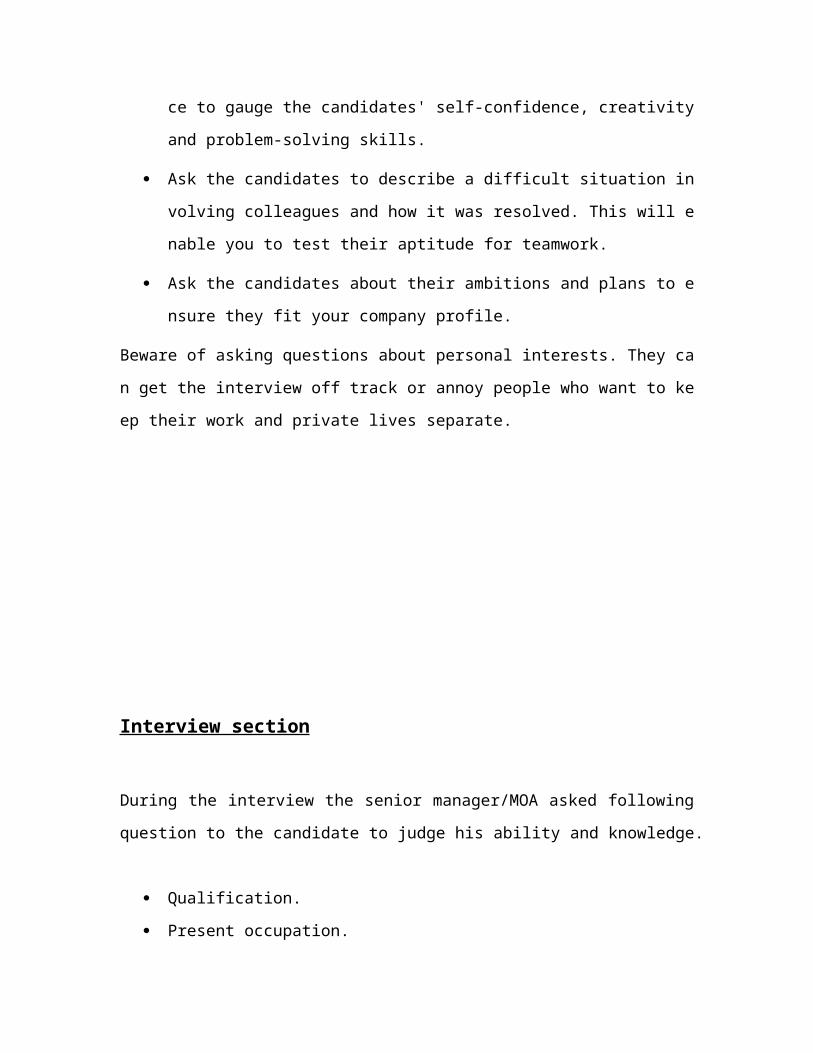

nce to gauge the candidates' self-confidence, creativity and problem-solving skills.

Ask the candidates to describe a difficult situation involving colleagues and how i

t was resolved. This will enable you to test their aptitude for teamwork.

Ask the candidates about their ambitions and plans to ensure they fit your compan

y profile.

Beware of asking questions about personal interests. They can get the interview off track

or annoy people who want to keep their work and private lives separate.

Interview section

During the interview the senior manager/MOA asked following question to the candidate

to judge his ability and knowledge.

Qualification.

Present occupation.

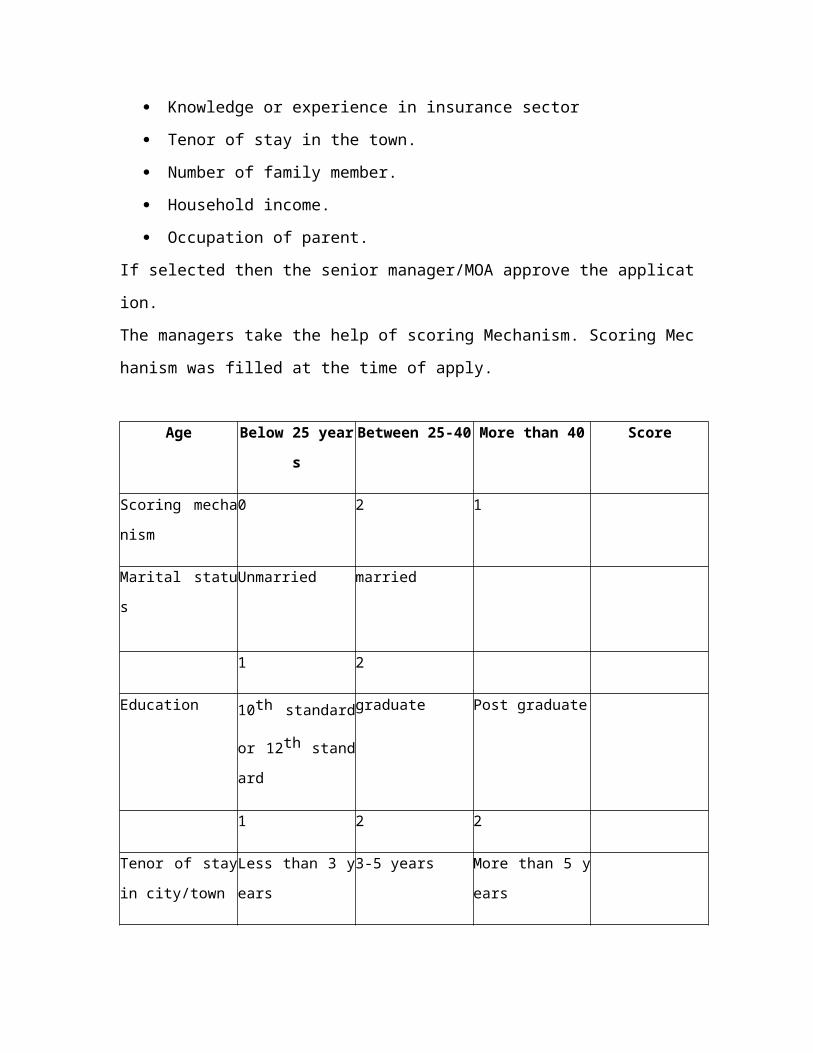

Knowledge or experience in insurance sector

Tenor of stay in the town.

Number of family member.

Household income.

Occupation of parent.

If selected then the senior manager/MOA approve the application.

The managers take the help of scoring Mechanism. Scoring Mechanism was filled at the t

ime of apply.

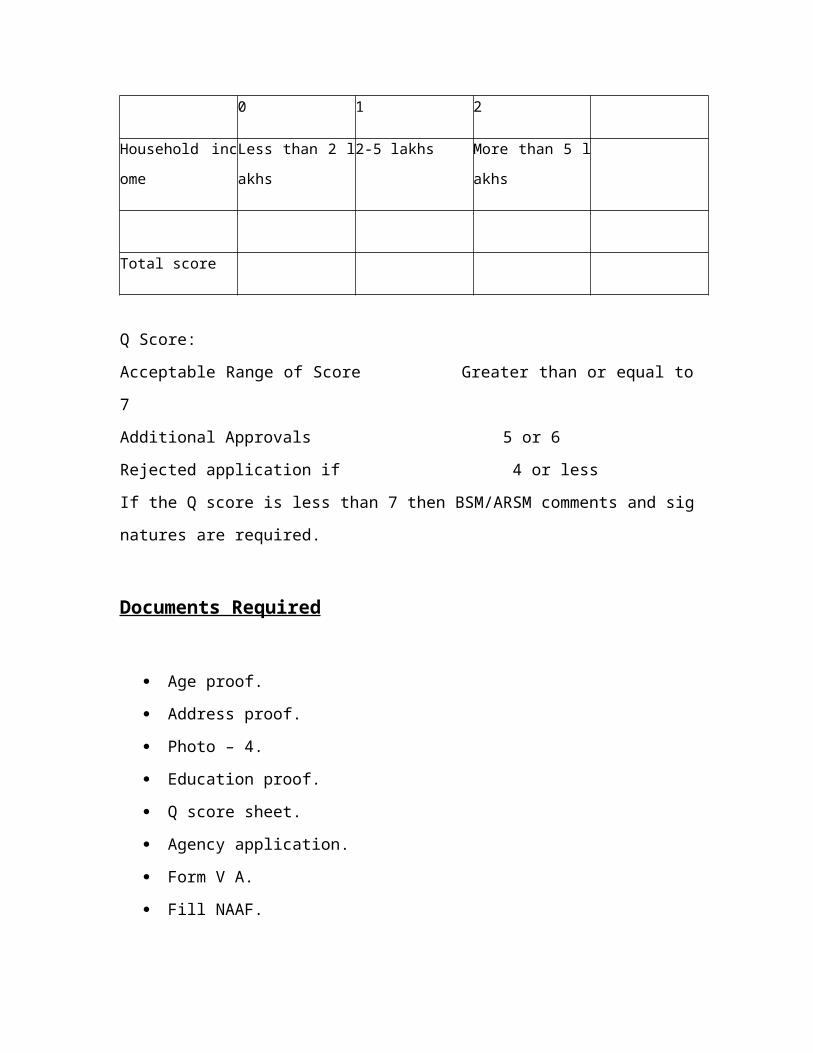

Age Below 25 years Between 25-40 More than 40 Score

Scoring mechanis

m

0 2 1

Marital status Unmarried married

1 2

Education 10th standard or

12th standard

graduate Post graduate

1 2 2

Tenor of stay in ci

ty/town

Less than 3 years 3-5 years More than 5 year

s

0 1 2

Household incom

e

Less than 2 lakhs 2-5 lakhs More than 5 lakhs

Total score

Q Score:

Acceptable Range of Score Greater than or equal to 7

Additional Approvals 5 or 6

Rejected application if 4 or less

If the Q score is less than 7 then BSM/ARSM comments and signatures are required.

Documents Required

Age proof.

Address proof.

Photo – 4.

Education proof.

Q score sheet.

Agency application.

Form V A.

Fill NAAF.

Training

7 DAYS Training and also provide a text book (IC-33 life insurance) for pre-recruitment

Examination for Life Insurance Agents, which is based on syllabus prescribed by insuran

ce Regulatory & Development Authority.

IRDA for short, has laid down that those who wish to become insurance agents will be gi

ven licenses only after they complete a course of study, training and pass an examination

prescribed by it.

During this training the knowledge about the entire essential concept related to life insura

nce is provided to agent. Insurers will have different practices and offer different benefits

in their plans. All of them will be based on these concepts. The details of the practices an

d the plans of each insurer will have to be learnt from the respective insures.

During training following things will be teaches.

What is insurance

Principles of life Assurance

Premiums and Bonuses

Life Insurance products

Underwriting

Insurance Documents

Policy conditions

Claims

Linked life insurance products

Insurance agency

Laws and Regulations

IRDA Regulation 2000.

IRDA Regulation 2002.

Examination and Code

Examination is the second last part of the recruitment and selection process.

It include one hour test under, which contain 50 objective questions, one marks each,

Pass marks are 25.

There are two method of examination.

Online

Manual

In case of online the result is declared on the spot and in the case of manual result is decla

red within one month.

After clearing the exam, ULIP training of two days will be given to the advisor about the

product of company and then agency code is generated.

Definition of Agent

According to section 182 of Indian contracts Act, an “agent” is a person employ

ed to do any act for another or to represent another in dealing with a third perso

n. In the insurance industry, the term “agent” is ordinarily applied to a person en

gaged by the insurer to procure new business. The insurance Act definers and in

surance agent as one who is licensed under Section 42 of that Act and is paid by

way of commission or otherwise, in consideration of his soliciting of procuring i

nsurance business, including business relating to the continuance, renewal or re

vival of policies of insurance. He is, for all purposes, an authorized salesman for

insurance and needs a license.

An agent is one who acts on behalf of another. The “another” on whose behalf t

he agent acts, is called the principal in this case. The insurance company is the p

rincipal in this case. The lawyer is the agent of the client, when he argues the ca

se in court. An ambassador is an agent of his country. The agent represents the p

rincipal and acts on his behalf. Some insurers designate their agents as ‘adviser

s”,” consultants” etc. as if they are independent advisor or consultant would not

be appointed by an insurance company. He would be knowledgeable enough as

a person to be approached for advice or consultation. Some insurance agents ma

y acquire that status. All insurance agents should strive to attain that status.

Procedure for becoming an Agent

The insurance Act, 1938 lays down that an insurance agent must possess a licence

under Section 42 of that Act. The licence is to be issued by the IRDA. The IRDA

has authorized designated persons, in each insurance company, to issue the licenc

es on behalf of the IRDA.

In terms of the Insurance Act, a licences will not be given if the person is

(a) minor,

(b) found to be of unsound mind,

(c) found guilty of criminal misappropriation or criminal misappropriation or

criminal breach of trust or cheating or forgery or an abetment of or attempt to

commit any such offence

(d) found guilty of or knowingly participation in or conniving at any fraud, dis

honesty or misrepresentation against an insurer or an insured,

(e)not possessing the requisite qualifications and specified training,

(f) Found violating the code of conduct as specified in the regulations.

(g) The fee for a licence is Rs.825 for individual. A licence is granted for 3 ye

ars. It may be renewed after 3 years and again valid for 3 years.

A licence issued by the IRDA may be to act as an agent for a life insurer, for a ge

neral insurer or as a composite insurance agent working for a life insurer as sell as

a general insurer. No agent is allowed to work for more than one life insurer or m

ore than one general insurer.

The Qualifications necessary before a licence can be given are that the person

must be

(a) Not a minor.

(b) Have passed at least the 12th standard or equivalent examination, if he is t

o be appointed in a place with a population of 5,000 or more.

(c) Have undergone practical training for at least 50 hours in life or general in

surance business, as the case may be, form an institution, approved and notifie

d by the IRDA. IN the case of a person wanting to become a composite insura

nce agent, the applicant should have completed at least 75 hours practical train

ing in life and general insurance business, which may be spread over six to eig

ht weeks.

d) Have passed the pre-recruitment examination conducted by the insurance

institute of India or any other examination body authorized

by the IRDA.

The licence once issued, can be cancelled whenever the person acquires a disqualification.

Applications for renewal have to make at least thirty days before the expiry of the licenc

e, along either the renewal fee of Rs.250. If the application is not made at least thirty days

before the expiry, but is made before the date of expiry of licence, an additional fee of Rs.

100 is payable . If the application is made after the date of expiry, it would be normally b

eing refused.

Prior to renewal of the licence, the agent should have completed at least 25 hours practica

l training in life or general insurance business or at least 50 hours practical training in life

and general insurance business in the case of a composite insurance agent.

Insures who select agents for appointment, make arrangements for training, for appearing

in the prescribed examinations, and obtaining the licence.

NOTE

The insurance Act provides, In Section 44, for payment of commission on renewal premi

um even after termination of the agency. The commission will be limited to a rate not exc

eeding 4%, to be eligible for this; the agent should have been an agent with that insurer fo

r at least

(1) five years and policies for at least Rs50,000 are in force one year before termi

nation of agency or,

(2) 10 year.

This commission will be payable to the heirs of the agent after the agent’s death.

Facility provided to Life adviser

+

+

+

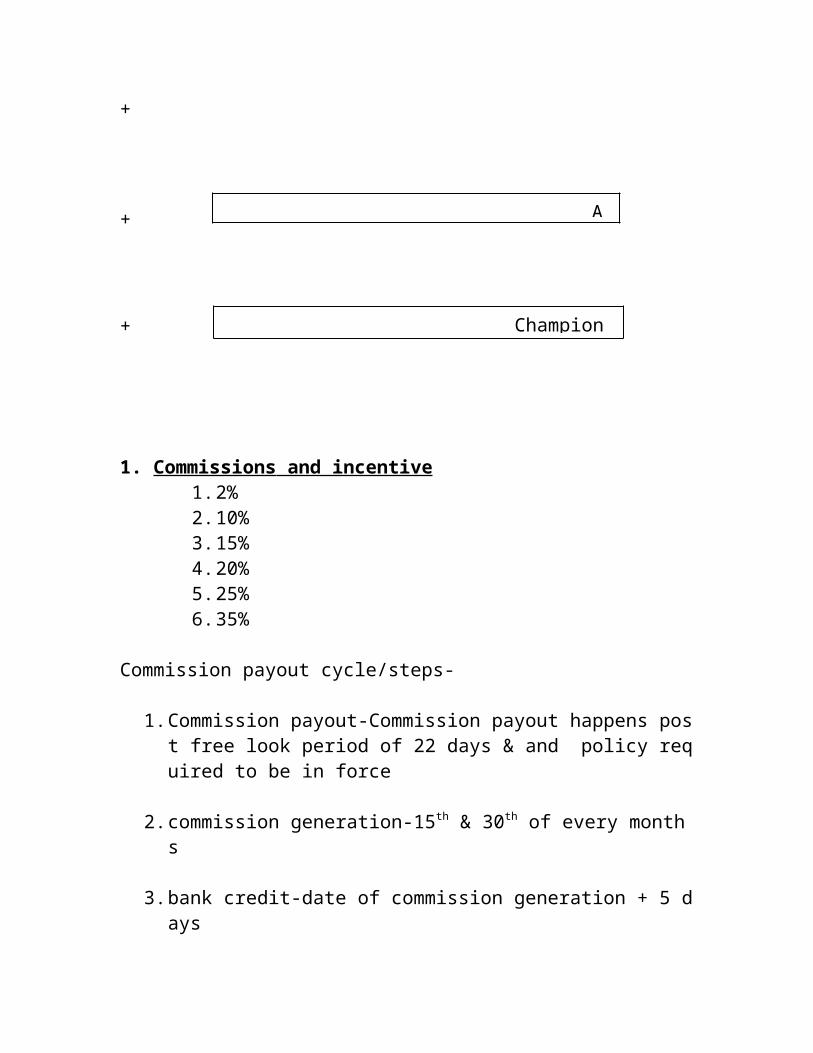

1. Commissions and incentive 1. 2%2. 10%3. 15%4. 20%5. 25%6. 35%

Commission payout cycle/steps-

1. Commission payout-Commission payout happens post free look period of 22 days & and policy required to be in force

2. commission generation-15th & 30th of every months

3. bank credit-date of commission generation + 5 days

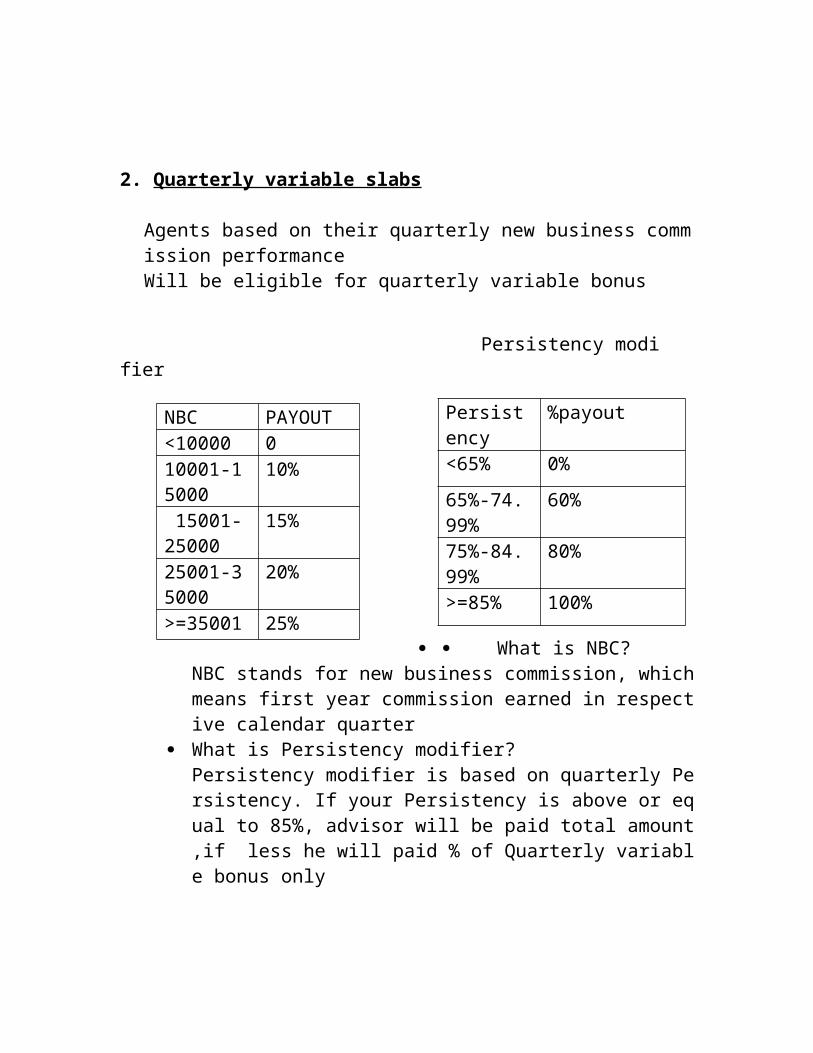

2. Quarterly variable slabs

Agents based on their quarterly new business commission performance Will be eligible for quarterly variable bonus

Commissions and incentives

Quarterly variable bonus

Acers club

Champion league

Persistency modifier

What is NBC?

NBC stands for new business commission, which means first year commission earned in respective calendar quarter

What is Persistency modifier?Persistency modifier is based on quarterly Persistency. If your Persistency is above or equal to 85%, advisor will be paid total amount ,if less he will paid % of Quarterly variable bonus only

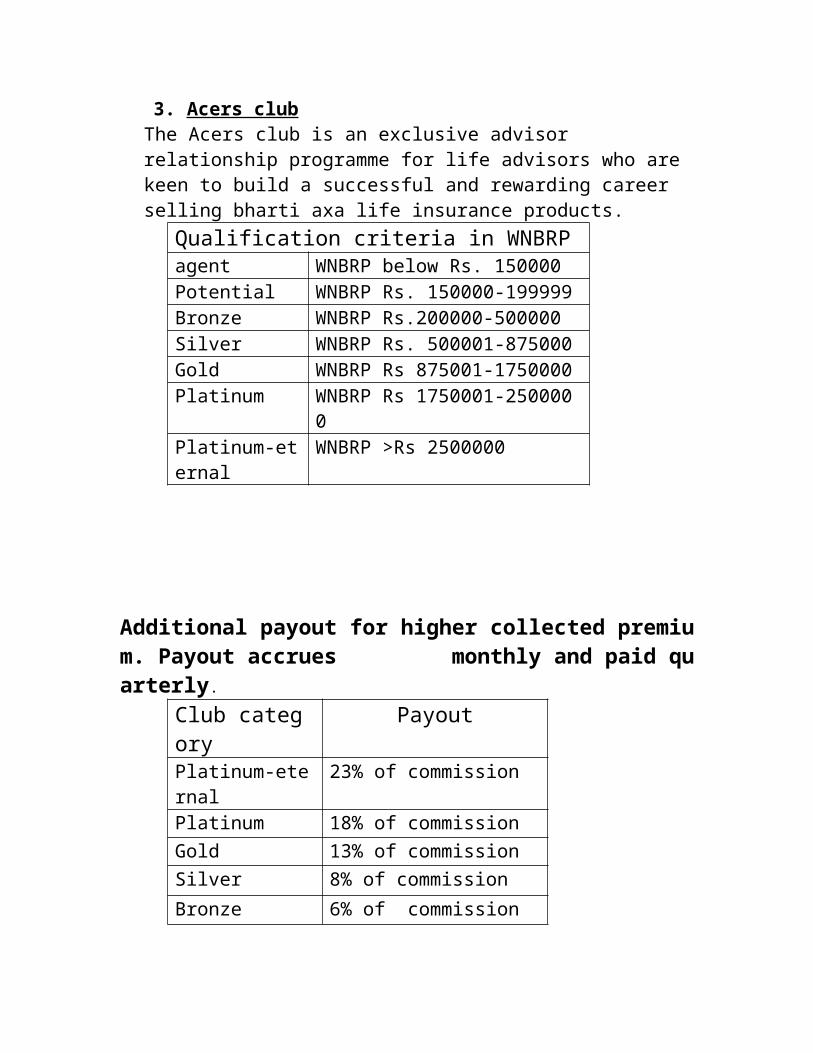

3. Acers club

The Acers club is an exclusive advisor relationship programme for life advisors who are keen to build a successful and rewarding career selling bharti axa life insurance products.

Qualification criteria in WNBRPagent WNBRP below Rs. 150000Potential WNBRP Rs. 150000-199999Bronze WNBRP Rs.200000-500000Silver WNBRP Rs. 500001-875000Gold WNBRP Rs 875001-1750000Platinum WNBRP Rs 1750001-2500000Platinum-eternal WNBRP >Rs 2500000

Additional payout for higher collected premium. Payout accru

Persistency %payout<65% 0%

65%-74.99%

60%

75%-84.99%

80%

>=85% 100%

NBC PAYOUT<10000 010001-15000

10%

15001-25000

15%

25001-35000

20%

>=35001 25%

es monthly and paid quarterly.

Club category PayoutPlatinum-eternal 23% of commission

Platinum 18% of commission

Gold 13% of commission

Silver 8% of commission

Bronze 6% of commission

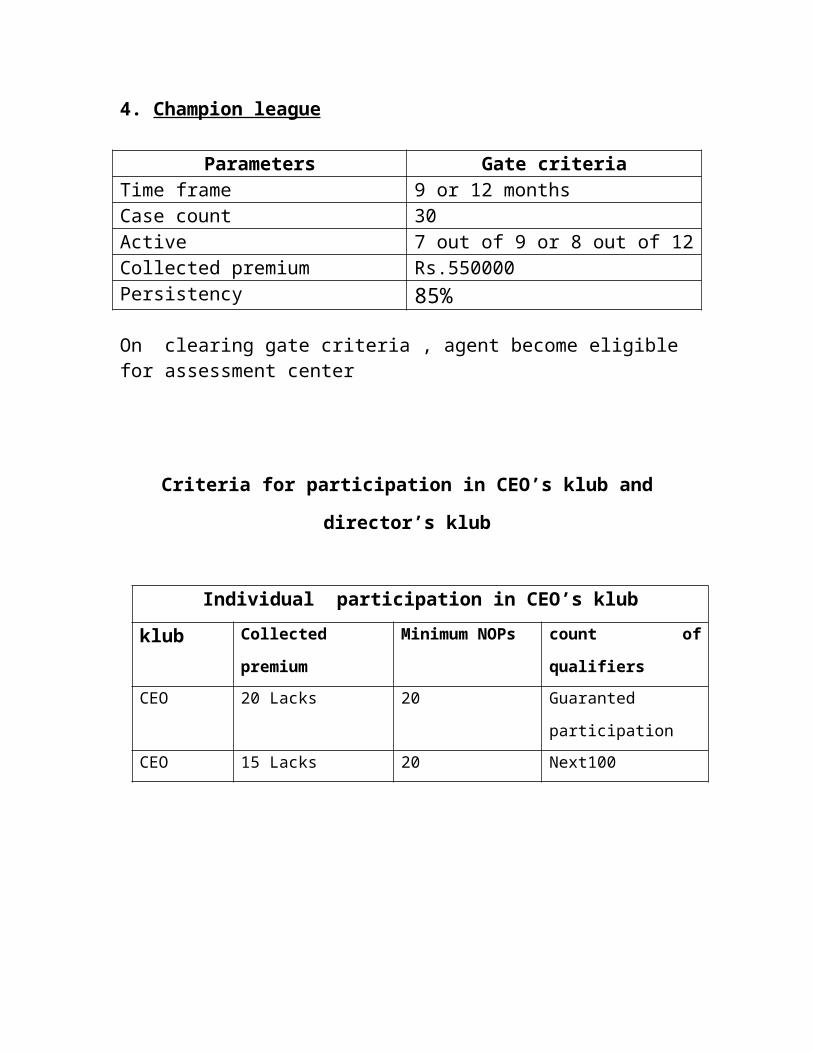

4. Champion league

Parameters Gate criteria Time frame 9 or 12 monthsCase count 30Active 7 out of 9 or 8 out of 12Collected premium Rs.550000Persistency 85%

On clearing gate criteria , agent become eligible for assessment center

Criteria for participation in CEO’s klub and director’s klub

Individual participation in CEO’s klub

klub Collected

premium

Minimum NOPs count of qualifiers

CEO 20 Lacks 20 Guaranted participation

CEO 15 Lacks 20 Next100

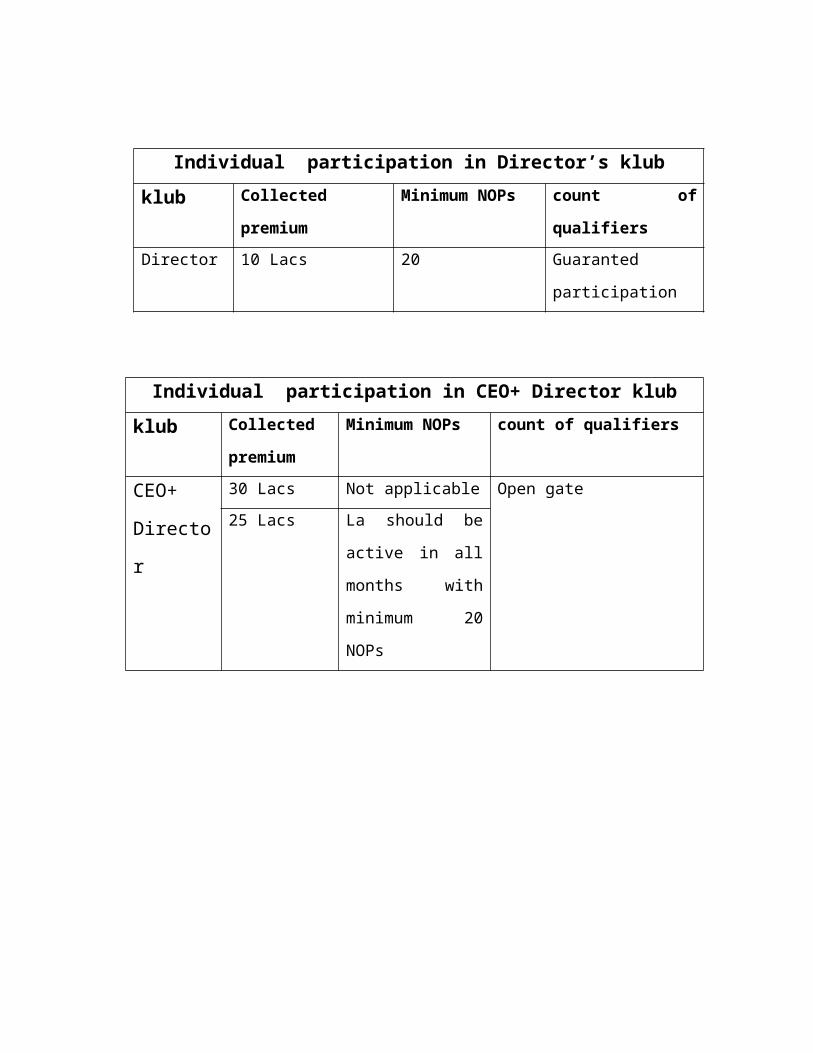

Individual participation in Director’s klub

klub Collected

premium

Minimum NOPs count of qualifiers

Director 10 Lacs 20 Guaranted

participation

Individual participation in CEO+ Director klub

klub Collected

premium

Minimum NOPs count of qualifiers

CEO+

Director

30 Lacs Not applicable Open gate

25 Lacs La should be active

in all months with

minimum 20 NOPs

Function of life Life Advisor

Understanding the prospect’s needs and persuade him to buy a plan of life insuran

ce that suits his interests best.

Complete the formalities:- paper work, medical examination, which are necessary

to get the policy expeditiously.

Keep in touch to ensure that changing circumstances are reflected in the arrangem

ents relating to premium payments, nomination and other necessary alterations.

Facilitate quick settlement of claims.

Be totally honest with both the prospect and the insurer.

Not to induce prospects to submit wrong information.

Career with Bharti AXA

Opportunity to earn unlimited income.

Career Growth.

Be your own boss.

High quality training & Support to improve productivity.

Compensation amongst the best.

Club member benefits.

Payout structured to facilitate your cash flows better.

Best in class & competitive products.

Pension for life.

Chapter -3

Rresearch methodology

Research Methodology

Purpose of the study

To understand the process of recruitment and selection of agent in Bharti AXA life insurance.

How to recruits agent for Bharti-AXA life insurance To know about the view of general public about the job of agent Why people are not willing to work with as an agent, especially with private playe

r.

Research Methodology is the investigation of specific problem in detail. At first problem

is defined carefully for conducting research. There should be a good research plan for con

ducting research. No research can be done without data collection. After all this analyze i

s made for getting solution for problem.

Defining the problem

Defining the sampling plan

Collection of data

Analyze and interpretation

Defining the problem

Defining the research problem is first necessary step for any research. This work should b

e done carefully. Here research problem is to know wiliness of general public to work as

an agent with private player or Bharti-AXA life insurance.

Sampling plan

The sampling plan calls for three decisions.

A) Sampling Unit: I have completed my survey in DELHI.

B) Sample Size: The selection of 20 respondents. The sample was drawn from shopkeep

ers. The selection of the respondent was done on the basis of simple random sampling.

C) Contact methods

I have conduct the respondent through personal interviews

Research Instrument

A questionnaire was constructed for my survey. Questionnaire consisting of a set of quest

ions made to filled by various respondents.

Collecting the Information

After this, I have collected the information from the respondent with the help of question

naire.format of questionnaire

QUESTIONNAIRE

1. Name-

2. Occupation

Govt

Pvt

Student

Proprietor

Others

3. Years present in the city

<1

1-2

2-3

4-5

4. Married

Yes

No

5. Contact no

6. Address

7. Do you leave in joint family?

Yes

No

1. Would you be interested in taking up this business opportunity with B

harti?

Yes

No

2. How much time can you dedicate per day for this activity? (For gettin

g

Appointments)

½ hr

1-2 hrs

3-5 hrs

5 hrs or more

3. Do you have any knowledge of or experience in Insurance?

Knowledge

Yes

No

Experience

Yes

No

If yes, then please specify the name of the company.

4. Can you spare ½ day on training to understand the product and how ca

n introduce it to your customer?

Yes

No

5. How many people do you know in this city?

Under 50

51-100

101-300

301-600

Above 600

Analyze the Information

The next step is to extract the pertinent finding from the collected data. I have tabulated t

he collected data & developed frequency distributions.

Thus the whole data was grouped aspect wise and was presented in tabular from. Thus, fr

equencies & percentages were to reder impact of the study.

Presentations of Findings

This was the last stop of the survey.

Limitation

I didn’t get complete feed from the shopkeepers about the question as they are bus

y in there work and had less time to fill questioned.

Sincerity of answering the questions cannot be judged.

Time was the major constraint for me to understand the long process of recruitme

nt and selection.

Limited money available for project.

Chapter 4

Analysis and interpretation

Data Presentation and Interpretation

Analysis 1 Occupation of individuals surveyed

Govt. Employee Pvt. Employee Students Unemployed Housewife17 86 50 06 04

Here in this chart it shows that maximum numbers of people surveyed come from Pvt.Employee and student community.Interpretation: Sample which has been surveyed is dominated by younger individual like student and recently joined private employee.

Analysis 2 Qualification of individuals

Qualification 10th or below Intermediate Graduate P.G.No. of individual 18 15 80 50

Govt. Employee10%

Pvt. Employee53%

Student31%

Unemployed4%

Housewife2%

Interpretation :- The majority people surveyed came form graduate and post graduate groups and they fulfils our requirement.

Analysis 3 Biggest concern for future

Career Income Job50 64 49

Interpretation:- Though all the three choices were equally preferred but the income was most preferred.

Analysis 4were they prepared for there future planning

Result YES NO

No. of individual 77 86

Interpretation: - It shows that majority was still having no planning for future.

Analysis 5 Interested for extra income

RESULT YES NONO. OF INDIVIDUAL 116 46

Interpretation: - A very high response was shown for earning extra income. The people who were interested for more income is the one who show more interest towards insurance.

Analysis 6Preferred amount as extra income by different people.

Result 0k-5k 5k-10k 10k-20k >20k No AnswerNo. of individual

28 51 29 7 48

Interpretation: -Most people needed in around 5-10 thousand in the form of extra income.

Chapter 5

Finding

And

Suggestions

Finding

Why people are not ready to work with private players in life insurance?

Or

Why people are not ready to work as an agent in any company?

In these days LIC created a very well image in the mind of General public becaus

e it is semi Government Company and also an oldest company. In short most peop

le of Indian believe upon the LIC only.

During the training period we felt that most of people who are already working in

insurance sector think that it is easy to sell the product of LIC than to sell the prod

uct of other life insurance company.

Most of people say that this job affects upon there social relation with other and al

so effect upon there business.

Most of people believe that private insurance companies carried out fraud activity

that’s why they never believe upon the private players.

People think that it is a time consuming activity and also required huge market ski

lls.

Some people said that only greedy people like to work in insurance sector.

Suggestions

Bharti-AXA life insurance company must give more advertisements on electr

onic media and print media, as it help in enhance its goodwill and more peopl

e are willing to work with reputed companies, through proper advertisement it

become easy to sell the product.

An insurance company must work with honesty to win the confident of its age

nt and general public.

Duration of training must be reducing as in these day people have no extra tim

e.

Fees charged by companies from candidate for IRDA exam and training shoul

d reduce.

Many other extra facilities must be provide to agent to attract them such local

and foreign trips, special price on achieving a target, open bank account at fre

e of cost,

Bharti-AXA Life Insurance Company must organize more and more seminars

and also participate in the job trade fairs to find out more candidates.

Increase the commission of agents.

The duration of the process of recruitment and selection is too long (one and h

alf month), during this process mostly candidate loss there interest, so there is

an urgent need to reduce the duration of this period.

Reduce the minimum premium amount it will help company to attract the age

nt of other company, as it increases the scope of market of its agent.

Chapter 6

Conclusion

Conclusion

In India, there is throat cut competition in the market of life insurance that brand service

which adopt new strategies for sales. I concluding the whole story it can be said that peop

le are much more aware about the aspects of life insurance and also have knowledge abou

t the role and act of agent but mostly people unwilling to work as life insurance agent and

mostly people prefer to work with LIC because it is a semi government corporation.

Chapter 7

Bibliography

BIBLIOGRAPHY

www.irdaindia.org

www.bhart-axalife.com

www.wikipedia.org

www.ibef.org

www.insuranceguide.com

market research,naresh malohtra

S. Balachandran, (2009), IC-33 Life Insurance, Shri S.J Gidwani Publishers,

Mumbai