Embed Size (px)

Citation preview

Report of the independent auditor

with the consolidated financial statements as of 31 December 2014 of

World ORT, Geneva

General Information World ORT

Contents

Page:

2 Report of the Trustees

7 Independent Auditors' Report

9 Consolidated Statement of Comprehensive Activities

10 Consolidated Statement of Financial Position

11 Consolidated Cash Flow Statement

12 Consolidated Statement of changes in Charitable Funds

13 Notes to the Consolidated Financial Statements

Company secretary and registered office

Stephen West, 1, Rue De Varembé, CH-1211 Genève 20, Switzerland.

Administration address

126 Albert Street, London, NW1 7NE, United Kingdom.

Auditors Ernst & Young, 59 Route de Chancy, P.O. Box 48, CH-1213 Petit Lancy 1,Switzerland.

Bankers UBS AG, case Postale 2770, CH-1211 Genève 2, Switzerland.

Solicitors Ming Halperin Burger et Inaudi, 5 Avenue Léon-Gaud, CH-1206 Genève,Switzerland.

1

Report of the Trustees World ORT

for the year ended 31 December 2014

The Trustees of World ORT present their annual report for the year ended 31 December 2014.

Trustees with specific functions are termed "officers".

Officers

Non-Executive

President Jean de Gunzburg

President Mauricio Merikanskas

Deputy President Conrad Giles

Chairman of the Board of Trustees Mauricio Merikanskas

Chairman of the Board of Trustees Jean de Gunzburg

Treasurer Shelley Fagel

Secretary Dario Wertheim

until 18-May-2014

from 19-May-2014

until 18-May-2014

from 19-May-2014

Executive

Director General & CEO Shmuel Sisso

The responsibility for the financial statements lies with the Board of Trustees.

Trustees' responsibilitiesThe Trustees of World ORT are responsible for the preparation of the financial statements for eachfinancial year which give a true and fair view of the organisation's income and expenditure duringthe year and of its state of affairs at the end of the year. In preparing these financial statementsthey are required to:

• select suitable accounting policies and then apply them consistently;

• make judgements and estimates that are reasonable and prudent;

• state whether applicable accounting standards and statements of recommended practice havebeen followed, subject to any material departures being disclosed and explained in the financialstatements; and

• prepare the financial statements on the going concern basis unless it is inappropriate to assumethat the organisation will continue in business.

The responsibilities of the Trustees include keeping proper accounting records which disclose, withreasonable accuracy, at any time, the financial position of the organisation. They are alsoresponsible for safeguarding the assets of the organisation and hence for taking reasonable stepsfor the prevention and detection of fraud and other breaches of laws and regulations.

Status of the World ORT groupWorld ORT is a not-for-profit organisation registered with the Registry of Commerce in Geneva anddomiciled in Switzerland. The registered address is:

1 Rue de Varembé, CH-1211 Genève 20, Switzerland.

Mission and objectivesThe mission of World ORT, a non-profit, non-political organisation whose aim is to work for theadvancement of Jewish people through training and education; to provide communities, whereverthey are, with the skills and knowledge necessary to cope with the complexities and uncertaintiesof their environment; to foster economic self-sufficiency, mobility and a sense of identity throughthe use of state-of-the-art technology.

ORT International Co-operation, a division created in 1960, implements projects at the request ofinternational agencies, local communities, host governments and private firms. ORT trainingprogrammes are designed to meet local needs and are particularly successful in overcomingeconomic, cultural and linguistic barriers. A key objective of ORT technical assistance is toestablish a self-sustaining, locally based training capacity.

2

Report of the Trustees (continued) World ORT

for the year ended 31 December 2014

World ORT's programmesImportant to the success of World ORT is the role of affiliated organisations in fundraising orimplementing programmes. Affiliates are autonomous national organisations forming part of theworldwide ORT network and using the "ORT" name. This network operates exclusively for educationalpurposes.

Fundraising is performed by World ORT and by the affiliate, national organisations in various countries.Fundraisers have a catalogue of World ORT projects to show potential donors. Their success dependson a number of factors including the economic environment and donor's life cycle.

During 2014, a property in Paris, which was no longer being used for teaching students, was sold byORT France. Some of the proceeds were remitted to World ORT and are included in revenue for theyear.

Projects are not commenced until funding has been secured and so project activity can be cyclical.World ORT has managed to smooth these effects by entering into partnerships with national and localgovernments where possible.

Each relationship with a government body is defined by the relevant contract and accounted foraccordingly.

World ORT's Education Department has continued its work of coordinating ORT's global community ofeducators, facilitating the exchange of ideas and practice, and running programmes to fosterexcellence in teaching and learning.

Specifically, the department has run the following activities and programmes over 2014:

- The 14th World ORT Wingate Seminar on "Serious Games and Gamification for Learning", hosted atORT House in London for teaching professionals.

- Four Naomi Prawer Kadar Seminars for Digital Technology in Jewish Education, hosted for localJewish Studies and Hebrew teachers in Argentina, Italy, Russia and the UK.

- "Chibur" — a regional competition involving students aged 12-16 in countries of the former Soviet Unionand Easter Europe researching their family's and community's Jewish heritage, and presenting thesestories through the design of blogs and websites.

"iJET" — a regional competition, supported by teacher training, involving students aged 14-16 fromLatin America researching the lives of key historical Jewish personalities and presenting their findingsvia a range of digital technologies.

The World ORT Future Leaders programme, a nine-month leadership training programme to nurturethe leadership potential of 16-18 year olds from Europe and the former Soviet Union. Seminars wereheld in Strasbourg and Israel, in addition to distance learning and local community work.

- The World ORT English and Science Summer School, hosted at ORT House in London, for 30 ORTstudents from around the world to benefit from two weeks of intensive English language tuition andscience exploration.World ORT continue further development of the "Music of the Holocaust" website project focusing oneducational components and translation to Russian and Spanish.

In the CIS and Baltic States (the former Soviet Union) World ORT operates formal education in 17schools . In these schools, Technology Centres are established. ORT has created an integrated e-learning system to deliver a unified educational methodology in the region. Teachers from Jewishschools in the region are provided with instruction in the most recent developments in teachinginformation and communications technology.

The QUEST initiative (Quality and Universal Education through Science and Technology) is allowingWorld ORT to upgrade and refresh our schools in the CIS and Baltic States. This is facilitated by anespecially generous donation.

World ORT provides adults training in the Jewish communities of the FSU through long-termprogrammes such as VTC - Yesod in St. Petersburg, 16 KesherNet centres in small communities andtraining for women in Kishinev, MoldovaAt the time of preparing the financial statements, there is political unrest in the region. World ORT'seducation activities continue to operate. World ORT's management and Trustees are monitoring thesituation.

3

Report of the Trustees (continued) World ORT

for the year ended 31 December 2014World ORT's programmes (continued)

World ORT activities in Eastern Europe include on-going projects in the ORT-Lauder Jewishschool in Sofia, Bulgaria and the Lauder school in Prague, Czech Republic.World ORT cooperates actively with the ORT school in Rome and the affiliated school in Milan,Italy. These projects are mostly aimed at individualised learning and ICT for teaching.

World ORT International Co-operation projects in 2014 took place in Liberia, Montenegro andMyanmar (run by IC Washington office) and in Haiti (run by IC Geneva office).The Heftsiba programme sends teachers from Israel to schools in CIS and Baltic States for anacademic year. This programme is sponsored by the Israel Ministry of the Diaspora.

World ORT in Israel, Kadima Mada, has 34 affiliated schools and towards the end of the yearwas preparing formally to bring into its network three schools and to forge partnerships withother organisations.Kadima Mada programmes in 2014, generously supported by donations from manyorganisations and private individuals have included the continued installation and operation ofSmart Classrooms in schools in the North and the South of the country; providing digitalteaching aids in co-operation with the Israel Ministry of Education and the Ministry for theDevelopment of the Negev and the Galilee.The Centres of Excellence programme was extended to Haredi and Arab students and continuesto extend opportunities to young people to enjoy science and technology based learning thatwould otherwise not be available to them.

The Kay-Or programme, in co-operation with the Israel Ministry of Education, operates 27schools within hospitals providing educational services to hospitalised children

Other programmes such as High Five, MABAT and a range initiatives have helped thousands ofyoung people through STEM education both as part of the school curriculum and by way of extra-curricular activitiesDuring the security emergency in the summer, Kadima Mada gratefully received assistance fromJFNA and other donors to run respite programmes for those affected by the conflict.

Investment PolicyThe trustees have unlimited powers of investment. The trustees delegate this responsibility tothe investment committee who meet approximately three times per annum.Details of the financial assets can be found in note 10.In summary, the investment policy has three main strands:

Ownership of freehold land and an office building, ORT House in London, which hosts theadministrative staff.ORT House comprises most of the value of the fixed assets. Some offices in the property are letto tenants all of whom are non-commercial organisations.The revenue from the letting activity in 2014 was $474,000 (2013: $342,000). The property'srunning costs in the year were $628,000 (2013: $691,000)

1

2 Investment in State of Israel bonds. About half of the investment in bonds is on behalf of a long-term project in Israel.

3 Placement of funds which are not required in the day-to-day running of World ORT in the handsof an investment manager of international standing. The investment committee gives theinvestment manager the overall asset allocation which is regularly reviewed.

4

Report of the Trustees (continued) World ORTfor the year ended 31 December 2014

Risk ManagementThe trustees examine the major risks that the charity faces each financial year when preparing and updatingthe strategic plan. Details of the financial risks faced by World ORT are in note 15.

Operational risks are identified as (1) the reliance on a small number of country organisations for a largeproportion of the voluntary income, (2) project management, (3) the defined benefit pension scheme and (4)not being able to let the excess space in ORT House, London.

1 There is a risk of World ORT having a concentration of only a few fundraising countries or organisations.This risk is managed as follows:

1.1 World ORT has direct access to certain major donors in agreement with their local country organisations.

1.2 Encouraging donor country organisations to diversify their fundraising base from major individuals and familytrusts to many individual small donors.

1.3 Helping the operational countries to raise funds. In the first instance they are attracting funds fromgovernment and municipalities. Secondly, they are seeking parental contributions. Thirdly, they are seekingthird-party donations hopefully including major donors. This last point has proved very difficult in countrieswhere there is not yet a culture of giving.

2 Project management risks mainly consist of (1) the deliverable benefit is not defined and then agreed by allparties, (2) projects start before adequate funding is secured, (3) the approved spending is exceeded and (4)that the benefit is not delivered within the agreed time. World ORT manages these risks using procedures,plans and reviews.

2.1 In the case of major donors or third party organisations, the tangible or intangible object to be delivered isagreed at the outset either by a project proposal document or a formal agreement.

2.2 Projects are not started until there is certainty as to the source of funds. The Director General and the ChiefFinance Officer authorise the project to start by signing a project initiation document.

2.3 The finance system is designed around project management. Reports are available by project to showprogress in funding, expenditure, the current project balance and the timeline to completion.

2.4 Project managers turn the initial project plan into purchase orders which are then authorised by theirmanager.

2.5 Project managers regularly review their data in the financial planning system and then any revised projecttimeline is authorised by their manager.

2.6 When a project completes, a project completion certificate is obtained, signed by the recipient.

2.7 Where agreed with the donors or third-party organisations, a report is submitted to them confirming that theproject has been delivered and to the recipient's satisfaction.

3 The defined benefit pension scheme has a deficit of $709,000 as set out in note 16. The actuaries haveadvised the trustees of a recovery plan which has been put into effect. This commits World ORT to additionalpayments to the pension fund of about $100,000 each year.

The trustees closed the scheme to new members in 1999. It had three active members at the end of 2014.The next retirement is expected in 2018. The last member is due to retire in 2028.

The trustees explored the option to fix the liability with a third party. This mainly involves paying-up the deficitimmediately plus an amount for future risk. At the moment, the trustees believe it is more cost-effective tomanage the risk internally.The trustees appointed a professional trustee in early 2013 with the remit to identify plan risk andrecommend ways to minimise it. Further considerations of the plan risk are in note 16.

4 The risk of not letting space in ORT House is managed by4.1 Maintaining the building to a commercially attractive standard.4.2 A large space is occupied with a conferencing activity which has a diverse set of clients in the public and

charity sectors.

4.3 Dividing the rest of the excess space into smaller units to achieve a diversity of tenants.Rental and licence fee revenue Number of tenants

Actual Plan Plan2014 2015 2016

under $50,000 per annum 9 9 9$51,000 - $100,000 per annum 1 1 1 Total number of tenants 10 10 10

5

Report of the Trustees (continued) World ORTfor the year ended 31 December 2014

Results for the yearTotal revenue for the year was US$47.5 million, compared with US$43.8 million in 2013.Revenue for restricted projects was US$38.5 million for the year (2013: US$37.8 million).

During 2014, a property in Paris, which was no longer used for teaching students, was soldby ORT France. Some of the proceeds, about $2.6 million, were remitted to World ORT andare included in unrestricted revenue for the year. Of this, $1.5 million was transferred to anendowment fund to be used at trustees discretion to foster best educational practice.

World ORT International Co-operation projects in 2014 took place in Liberia, Montenegroand Myanmar (run by IC Washington office) and in Haiti (run by IC Geneva office).Unrestricted activities showed a surplus of $525,000 for the year. Restricted projectsshowed a deficit of $60,000 for the year due to timing differences of project revenue toexpenditure.

There was a net total surplus of $465,000 for the year (2013: surplus of $3,180,000).

Review of financial transactionsGains on investments, including re-invested income, were $268,000 compared with a gainon investments of $1,001,000 in 2013.

Property and fixed assetsMovements on fixed assets are set out in note 9 to the financial statements. The Trusteesare of the opinion that the market value of freehold land and buildings is at least equal to thevalue shown in these financial statements.

The financial statements, together with explanatory notes set out on pages 13 to 34,summarise the transactions of the organisation during the year ended 31 December 2014.The financial statements comply with International Accounting Standards.

Signed in terms of the Constitution of World ORT by:

Ste hen _ estChief Financial Officer

■

6

Peter KlauberChair, Finance Committee

25 August 2015

EYBuilding a betterworking world

Ernst & Young Ltd Phone +41 58 286 56 56Route de Chancy 59P.O. Box

Fax +41www.ey.com/ch

58 286 56 57

CH-1213 Geneva

To the Board of Trustees of

World ORT, Geneva

Lancy, 16 September 2015

Report of the independent auditor on the consolidated financialstatements

As independent auditor and in accordance with your instructions, we have audited the accompanyingconsolidated financial statements of World ORT (consolidated statements of comprehensive activities,consolidated statement of financial position, consolidated cash flow statement, consolidated statement ofchanges in charitable funds and notes) on pages 9 to 34 for the year ended 31 December 2014.

Responsibility of the President, the Director General, the CFO and the Chair of the FinanceCommitteeThe President, the Director General, the CFO and the Chair of the Finance Committee are responsiblefor the preparation of the financial statements in accordance with the requirements of InternationalFinancial Reporting Standards (IFRS). This responsibility includes designing, implementing andmaintaining an internal control system relevant to the preparation of consolidated financial statementsthat are free from material misstatement, whether due to fraud or error. The President, the DirectorGeneral, the CFO and the Chair of the Finance Committee are further responsible for selecting andapplying appropriate accounting policies and making accounting estimates that are reasonable in thecircumstances.

Auditor's responsibilityOur responsibility is to express an opinion on these consolidated financial statements based on ouraudit. We conducted our audit in accordance with International Standards on Auditing. Those standardsrequire that we plan and perform the audit to obtain reasonable assurance whether the financialstatements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosuresin the consolidated financial statements. The procedures selected depend on the auditor's judgment,including the assessment of the risks of material misstatement of the consolidated financial statements,whether due to fraud or error. In making those risk assessments, the auditor considers the internalcontrol system relevant to the entity's preparation of the consolidated financial statements in order todesign audit procedures that are appropriate in the circumstances, but not for the purpose of expressingan opinion on the effectiveness of the entity's internal control system. An audit also includes evaluatingthe appropriateness of the accounting policies used and the reasonableness of accounting estimatesmade, as well as evaluating the overall presentation of the consolidated financial statements. We believethat the audit evidence we have obtained is sufficient and appropriate to provide a basis for our auditopinion.

OpinionIn our opinion, the consolidated financial statements for the year ended 31 December 2014 give a trueand fair view of the financial position, the results of operations and the cash flows in accordance with

!FRS.

Ernst & Young Ltd

Ph ip e StöckliLicensed audit expert(Auditor in charge)

Thomas MadoeryLicensed audit expert

8

Consolidated statement of comprehensive activities

for the year ended 31 December 2014

World ORT

Note

Unrestrictedfunds

ÚS$'000

Restrictedfunds

US$'000

2014Total

ÚS$'000

2013Total

ÚS$'000

Revenue

Donations and grants 3a 8,408 38,493 46,901 43,347

Property 3b 474 474 342

Meetings and other revenue 121 - 121 138

Total revenue 9,003 38,493 47,496 43,827

Expenditure

Direct project and charitable expenditure:

Grants and project costs 2,835 38,602 41,437 35,527

Delivery costs 2,561 2,561 2,497

Property costs 3b 628 628 691

Other direct costs 333 333 382

Total 6,357 38,602 44,959 39,097

Other expenditure:

Fundraising and publicity 1,019 - 1,019 1,294

Management and administration 1,367 - 1,367 1,305

Total 4 2,386 2,386 2,599

Total expenditure 8,743 38,602 47,345 41,696

Surplus/(deficit) before financial items 260 (109) 151 2,131

Financial income

Interest earned 5 5 4

Investment income 23 18 41 44

Gains on investments, realised andunrealised 10 237 31 268 1,001

Total 265 49 314 1,049

Surplus/(deficit) for the year 525 (60) 465 3,180

Other recognised gains and losses

Actuarial loss on defined benefit pension 16

scheme(200) (200) (98)

Net movement in funds 325 (60) 265 3,082

The notes on pages 13 to 34 form part of these Financial Statements

9

Consolidated statement of financial position

at 31 December 2014

World ORT

ASSETSNon-current assets

Note

2014US$'000

2013US$'000

Property, fixtures and equipment 9 3,605 3,602

Financial assets 10 11,305 11,195

14,910 14,797

Current assets

Accounts receivable 11 3,608 3,772

Cash and cash equivalents 12 12,577 13,293

16,185 17,065

TOTAL ASSETS 31,095 31,862

CHARITABLE FUNDS AND LIABILITIES

Charitable fundsRestricted funds

Restricted endowment funds 17 (a) 2,727 1,356

Restricted project funds 17 (b) 18,499 19,930

21,226 21,286

Unrestricted funds

General reserves 5,844 5,519

5,844 5,519

Total Charitable funds 27,070 26,805

Non-current liabilities

Employee benefit liability 16 709 697

Current liabilities

Accounts payable 13 3,316 4,360

Total Liabilities 4,025 5,057

TOTAL CHARITABLE FUNDS AND LIABILITIES 31,095 31,862

The notes on pages 13 to 34 form part of these Financial Statements

10

Cons•lidated Cash Flow statementfor the year ended 31 December 2014

World ORT

Cash flows from operating activitiesNote

2014US$'000

2013US$'000

Receipts from donations and other income 47,660 43,575

Payments to grant recipients, suppliers and employees (48,306) (41,754)

Net cash flows from operating activities (646) 1,821

Cash flows from investing activities

Purchase of tangible fixed assets 9 (94) (36)

Interest received 5 4

Investment income 41 44

Investment added 10 - (300)

Investment capital returned 10 160 27

Net cash flows from investing activities 112 (261)

Unrealised foreign exchange loss on cash and cashequivalents

(182) (16)

Net (decrease)/increase in cash and cash equivalents (716) 1,544

Cash and cash equivalents at 1 January 13,293 11,749

Cash and cash equivalents at 31 December 12,577 13,293

The notes on pages 13 to 34 form part of these Financial Statements

11

Consolidated statement of changes in charitable funds World ORTfor the year ended 31 December 2014

Restrictedfunds

Unrestrictedfunds

GeneralReservesÚS$'000

Totalfunds

ÚS$'000Endowment

ÚS$'000ProjectsÚS$'000

At 1 January 2013 1,223 16,005 6,495 23,723

Surplus/(deficit) for the year 2013 133 3,925 (878) 3,180

Pension actuarial loss (98) (98)

At 31 December 2013 1,356 19,930 5,519 26,805

Surplus/(deficit) for the year 2014 1,531 (1,591) 525 465

Grant from restricted fund (160) 160

Pension actuarial loss (200) (200)

At 31 December 2014 2,727 18,499 5,844 27,070

An explanation of the pension loss is set out in note 16.

An explanation of the Charitable Funds is set out in note 17.

12

Notes to the Consolidated Financial Statements World ORTat 31 December 2014

1 Authorisation of financial statements and statement of compliance with IFRSs

The consolidated financial statements of World ORT for the year ended 31 December 2014 wereauthorised for issue by the Trustees of World ORT on 03 May 2015. The consolidated financial

statements of World ORT have been prepared in accordance with International Financial ReportingStandards (IFRS) as issued by the International Accounting Standards Board.

2 Accounting policiesa. Basis of preparation

The consolidated financial statements have been prepared on a historical cost basis, except forfinancial instruments that have been measured at fair value. The accounting policies that follow set outthose policies which apply in preparing the financial statements for the year ended 31 December 2014.

The consolidated financial statements have been prepared in US Dollars as this is the functional andpresentational currency of the World ORT group. All values have been rounded to the nearestthousand (US$'000) except when otherwise indicated.

Judgements and key sources of estimation and uncertaintyThe preparation of financial statements requires the Trustees to make judgements, estimates and

assumptions that affect the amounts reported for assets and liabilities at the financial position date andthe amounts reported for revenues and expenses during the year. However, the nature of estimation

means that actual outcomes could differ from those estimates.

In the process of applying World ORT's accounting policies, the Trustees have made the following

judgements, assumptions and estimations which have the most significant effect on the amountsrecognised in the financial statements.

• Legal claimIn October 2007 ORT Israel brought a claim of US$4.7 million against World ORT and ORT America

jointly. See note 19.Trustees have to judge if it is possible to estimate with any certainty the amount, if any, that may needto be paid, whether to make a provision for the future legal cost of the dispute and, with advice fromlegal counsel, whether to make provision in these financial statements for any liability arising out of the

claims.

• Non-financial assetsWorld ORT assesses whether there are any indicators of impairment for all non-financial assets ateach reporting date.When value in use calculations are undertaken Trustees must estimate future cash flows from theasset or cash generating unit and choose a suitable discount rate in order to reflect the present value of

those cash flows.The current carrying value of non-financial assets of $3.6 million (2013: $3.6 million) is not considered

impaired.

• Defined benefit pension schemeThe valuation of the scheme assets and liabilities is subject to assumptions about discount rates,expected rates of return on assets, future salary increases, mortality rates and future pension

increases.World ORT retains the services of qualified actuaries to advise the Trustees when making these

assumptions and the current applied assumptions are in line with prevailing market benchmarks.

• Fair value of financial instrumentsState of Israel bonds are valued at their nominal value as they will be held to maturity. Other financial

assets are held in a portfolio. World ORT retains a fund manager to manage the portfolio and submit a

period-end valuation. The liquid nature of the portfolio's assets leads the manager to apply their marketvalue at the financial position date (also see notes 2i and 2j).

13

Notes to the Consolidated Financial Statements World ORTat 31 December 2014

Accounting policies (continued)

b. Jurisdictions

World ORT and its subsidiaries are registered in Switzerland, United States of America, Israeland the United Kingdom and are therefore subject to tax law in these jurisdictions respectively.As each entity is exempt from paying tax, no IAS 12 disclosures have to be made.

c. Basis of consolidation

The consolidated financial statements of World ORT for the year ended 31 December 2014include three subsidiary undertakings, consolidated in full, as follows:

Subsidiary Country Status

World ORT Inc. United States of America Wholly ownedWorld ORT Trust United Kingdom Wholly ownedWorld ORT Kadima Mada Israel Effective control *

Sasa Setton Kay Or Israel Effective control *

* World ORT owns 49% of World ORT Kadima Mada. The remaining 51% of the shares are heldin trusteeship equally by seven independent, unrelated shareholders. The shares weretransferred to the trustees on 04 May 2011. World ORT considers that it has effective controlwith this share structure and benefits from an independent oversight. The World ORT KadimaMada senior staff are appointed by World ORT. The World ORT Kadima Mada budgets arecontrolled and approved by World ORT.

There is no minority interest in World ORT Kadima Mada as there are no permanent assetsand no free reserves. The ownership represented by the shares is non-beneficial.

* World ORT Kadima Mada owns 49% of Sasa Setton Kay Or. The remaining 51% of the sharesare held in trusteeship equally by seven independent, unrelated shareholders. The shares weretransferred to the trustees on 1 July 2014. World ORT Kadima Mada considers that it haseffective control with this share structure and benefits from an independent oversight. The SasaSetton Kay Or senior staff are appointed by World ORT Kadima Mada. The Sasa Setton KayOr budgets are controlled and approved by World ORT Kadima Mada.

There is no minority interest in Sasa Setton Kay Or as there are no permanent assets and nofree reserves. The ownership represented by the shares is non-beneficial.

The consolidated financial statements contain revenue and expenses of schools in the formerSoviet Union and Baltic States. These are schools for which World ORT has effective controlby appointing the school principal and providing additional funds.

All inter-entity transactions, including unrealised gains and losses, have been eliminated.

The financial statements of the subsidiaries are prepared for the same reporting period asWorld ORT, using consistent accounting policies.

14

Notes to the Consolidated Financial Statements World ORTat 31 December 2014

Accounting policies (continued)

d. Foreign currency translationThe functional and presentation currency of the World ORT group and its subsidiaries is the US

Dollar. It is the functional currency because most income is due in US Dollars and, in turn, the

group matches as much of its commitments as possible in that currency.

Transactions in non-dollar currencies are initially recorded in the functional currency rate ruling at

the date of the transaction.

Monetary assets and liabilities denominated in foreign currencies are retranslated at the

functional currency exchange rate ruling at the financial position date. Fixed assets are

translated at the rate of the initial transaction.

Exchange differences are recognised in profit or loss in the period in which they arise.

e. RevenueRevenue, including donations, is recognised in the period in which World ORT is entitled to

receipt and where the revenue can be reliably measured.Revenue from government bodies is recognised either according to contracts or where World

ORT exercises control of the school.

Unrestricted funds are available for use at the Trustees' discretion in furtherance of the

objectives of World ORT.

Restricted funds are subject to specific restrictions imposed by the donor.

Gifts in kind are included in restricted income at their fair value when received.

International Co-operation projects are included in restricted funds and are accounted for under

the same policies.Property income and other revenue is recognised on the accruals basis.

f. ProvisionsProvisions are recognised when World ORT or a subsidiary has a present obligation (legal or

constructive) as a result of a past event and it is probable that an outflow of resources

embodying economic benefits will be required to settle the obligation and a reliable estimate can

be made of the amount of the obligation.

g. Property, fixtures and equipmentProperty, fixtures and equipment are stated at cost less accumulated depreciation and

accumulated impairment losses. Such costs include costs directly attributable to making the

asset capable of operating as intended.

Depreciation is provided on all tangible fixed assets, other than freehold land, at rates calculated

to write off the cost or valuation, less estimated residual value, based on prices prevailing at the

date of acquisition or revaluation, of each asset evenly over its expected useful life. The rates

applied are as follows:

Freehold buildings: 2% per annum on cost

Building improvements: 20% per annum on cost

Fixtures and equipment: 20% per annum on cost

Computer equipment: 33.33% per annum on cost

The carrying values of tangible fixed assets are reviewed for impairment in periods if events or

changes in circumstances indicate carrying values may not be recoverable. If any such

indication exists and where the carrying values exceed the estimated recoverable amounts, the

assets are written down to their estimated recoverable amounts.

An asset's recoverable amount is the higher of an asset's fair value less costs to sell and its

value in use. In assessing value in use, the estimated future cash flows are discounted to their

present value using a pre-tax discount rate that reflects the current market assessments of the

time value of money and the risks specific to the asset.

Expenditure on fixed assets to be used on projects is charged to project costs in profit or loss in

the period in which it is incurred.

15

Notes to the Consolidated Financial Statements World ORTat 31 December 2014

Accounting policies (continued)

h. LeasesLeases where the lessor retains substantially all the risks and benefits of ownership of the asset areclassified as operating leases. Operating lease payments are recognised as an expense in profit orloss on a straight line basis over the lease term.

i. Financial assets: initial recognition and measurementFinancial assets within the scope of IAS 39 are classified as financial assets at fair value through theprofit and loss account, loans and receivables, held-to-maturity investments, available-for-salefinancial assets, or as derivatives designated as hedging instruments in an effective hedge, asappropriate.

State of Israel bonds are held-to-maturity investments. The other financial assets are held-for-trading subject to the overall asset-allocation policy set by the World ORT investment committee tothe fund manager.

Financial assets at fair value through the profit and loss accountFinancial assets are initially recognised at fair value plus transaction costs, except in the case offinancial assets recorded at fair value through the profit and loss account. All financial assets at fairvalue through the profit and loss account are traded in active markets and so subsequentmeasurement of fair value of these financial assets is determined with reference to the quotedmarket bid price at the close of business on the financial position date.Any gains or losses are included with gains or loss on investments in the profit and loss account.

The type of financial assets held by the Group is listed in note 10.

k. Cash and cash equivalentsCash and cash equivalents comprise cash at bank and in hand and short-term deposits with anoriginal maturity of three months or less.Their carrying values equate to fair value by reason of their short term nature.

I. ReceivablesReceivables, which have terms according to their individual contracts, are recognised and carried atthe lower of their original invoice amount and their recoverable amount. Where the time value ofmoney is material, receivables are carried at amortised cost. Provision is made when there isobjective evidence that the Group will not be able to recover balances in full. Balances are writtenoff when the probability of recovery is assessed as being remote.

m. Accounts payable• Accounts payable are recognised and carried at the original invoiced amount or, in the case of

accruals, the anticipated amount to be invoiced. Where the time value of money is material,payables are carried at amortised cost.

n. Pensions and other post employment benefitsA subsidiary undertaking operates a defined benefit pension scheme and a defined contributionscheme. Both schemes require contributions to be made to separately administered funds.

• The defined benefit plan was established on 14 February 1974 and was closed to new memberswith effect from 1 November 1999.The cost of providing benefits under the defined benefit plans is determined using the projected unitcredit method.Re-measurements, comprising of actuarial gains and losses, the effect of the asset ceiling,excluding net interest (not applicable to the Group) and the return on plan assets (excluding netinterest), are recognised immediately in the statement of financial position with a correspondingdebit or credit to retained earnings through OCI in the period in which they occur. Re-measurementsare not reclassified to profit or loss in subsequent periods.

16

Notes to the Consolidated Financial Statements World ORTat 31 December 2014

Accounting policies (continued)

n. Pensions and other post employment benefits (continued)

Past service costs are recognised in profit or loss on the earlier of:The date of the plan amendment or curtailment, and

- The date that the Group recognises restructuring-related costs

Net interest is calculated by applying the discount rate to the net defined benefit liability or asset.

World ORT recognises the following changes in the net defined benefit obligation under Other

Expenditure in consolidated statement of comprehensive activities.Service costs comprising current service costs, past-service costs, gains and losses on curtailments

and non-routine settlementsNet interest expense or incomeThe defined benefit asset or liability comprises the present value of the defined benefit obligation

(using a discount rate based on high quality corporate bonds), less past service costs not yetrecognised and less the fair value of plan assets out of which the obligations are to be settled. Plan

assets are assets that are held by a long-term employee benefit fund or qualifying insurance

policies. The value of any plan asset recognised is restricted to the sum of any past service costs

not yet recognised and the present value of any economic benefits available in the form of refunds

from the plan or reductions in the future contributions to the plan.

The net defined benefit employee liability at 31 December 2014 is $709,000 (2013: $697,000).Further details, including the principal assumptions agreed with the actuary, are given in note 16.

• The defined contribution scheme was started from 1 April 2001 and is open to all employees who

have been in employment for at least three months. The assets of the scheme are held separately

from those of World ORT. Contributions are charged to the statement of comprehensive activities as

they become payable in accordance with the scheme rules. Differences between contributions

payable in the year and the contributions actually paid are shown as either prepayments or accruals

in the financial position.

o. Ex-gratia benefitsIn the past, World ORT agreed to provide benefits to a group of former employees and benefits to

some persons with links to World ORT. No funding for the post-employment portion of the benefits

was made during that group's employment. Due to the ages of the individuals concerned which

range from 78 to 95 years old and the amounts involved, the Trustees determined that the related

employee liability would not be material. World ORT have therefore decided that no further

provisions will be made and that the cost of the benefits will be borne in the year that the benefit is

paid. The cost is currently running at $34,000 per annum. but as most of the payments are in Swiss

Francs, the US Dollar value is uncertain. (See note 16).

p. Fund accountingEndowment funds are set aside for future purposes and form part of the restricted funds.

q• ReservesWorld ORT will maintain general funds to an amount equalling at least one year's expenditureexcluding direct project expenditure. The Trustees have established this policy in order to protect the

organisation's charitable programme in the event of a reduction in World ORT's revenue or an

unexpected need for additional expenditure.

r. Project fundsProject funds are monies received from donors and partners in advance of the financial needs of the

project (see note 17).Fundraising for projects is performed up to the value of the plan set out in the

project proposal.Occasionally the circumstances of a project change so that the funds received are in excess of the

revised needs of the project. In these cases the policy is to offer the donor(s) an alternative project

to make use of their funds.

17

Notes to the Consolidated Financial Statements World ORTat 31 December 2014

Accounting policies (continued)

s. Derecognition of financial assets and liabilitiesFinancial assetsA financial asset is derecognised where the rights to receive cash flows from the asset have expired;or the rights to receive cash flows from the asset have been transferred together with substantiallyall the risks and rewards of the asset, or where control of the asset has been transferred.

Financial liabilitiesA financial liability is derecognised when the obligation under the liability is discharged, cancelled orexpires.

t. Derivative financial instrumentsWorld ORT uses derivative financial instruments in the form of foreign currency contracts to hedgeits risks associated with foreign currency fluctuations as stated in note 15.

Such derivative financial instruments are initially recognised at fair value on the date on which aderivative contract is entered into and subsequently re-measured at fair value and classified at fairvalue through profit and loss.Derivatives are carried as financial assets when the fair value is positive and as financial liabilitieswhen the fair value is negative.

Unrealised gains and losses are booked directly in profit or loss as the conditions for hedgeaccounting have not been met.

The fair value of forward exchange contracts is calculated by using the forward exchange rates atthe financial position date for contracts with similar maturity profiles.

u. New and amended standards and interpretationsThe Group applied for the first time certain standards and amendments, which are effective forannual periods beginning on or after 1January 2014. The nature and the impact of each newstandard and amendment is described below.This list is not exhaustive but only discloses thechanges relevant to the Group.Investment Entities (Amendments to IFRS 10, IFRS 12 and IAS 27)These amendments provide an exception to the consolidation requirement for entities that meet thedefinition of an investment entity under IFRS 10 Consolidated Financial Statements and must beapplied retrospectively, subject to certain transition relief. The exception to consolidation requiresinvestment entities to account for subsidiaries at fair value through profit or loss. Theseamendments have no impact on the Group, since none of the entities in the Group qualifies to be aninvestment entity under IFRS 10.

Offsetting Financial Assets and Financial Liabilities - Amendments to IAS 32These amendments clarify the meaning of 'currently has a legally enforceable right to set-off andthe criteria for non- simultaneous settlement mechanisms of clearing houses to qualify for offsettingand are applied retrospectively. These amendments have no impact on the Group, since none of theentities in the Group has any offsetting arrangementsNovation of Derivatives and Continuation of Hedge Accounting - Amendments to IAS 39These amendments provide relief from discontinuing hedge accounting when novation of aderivative designated as a hedging instrument meets certain criteria and retrospective application isrequired. These amendments have no impact on the Group as the Group has not novated itsderivatives during the current or prior periods.IFRIC 21 LeviesIFRIC 21 clarifies that an entity recognises a liability for a levy when the activity that triggerspayment, as identified by the relevant legislation, occurs. For a levy that is triggered upon reaching aminimum threshold, the interpretation clarifies that no liability should be anticipated before thespecified minimum threshold is reached. Retrospective application is required for IFRIC 21. Thisinterpretation has no impact on the Group as it has applied the recognition principles under IAS 37Provisions, Contingent Liabilities and Contingent Assets consistent with the requirements of IFRIC21 in prior years.

18

Notes to the Consolidated Financial Statements World ORT

at 31 December 2014

Accounting policies (continued)

u. New and amended standards and interpretations (continued)

Annual Improvements 2010-2012 CycleIn the 2010 - 2012 annual improvements cycle, the IASB issud seven amendments to six standards,which included an amendment to IFRS 13 Fair Value Measurement. The amendment to IFRS 13 is

effective immediately and, thus, for periods beginning at 1 January 2014, and it clarifies in the Basisfor Conclusions that short-term receivables and payables with no stated interest rates can be

measured at invoice amounts when the effect of discounting is immaterial. This amendment to IFRS

13 has no impact on the Group.

Annual Improvements 2011-2013 CycleIn the 2011-2013 annual improvements cycle, the IASB issued four amendments to four standards,which included an amendment to IFRS 1 First-time Adoption of International Financial Reporting

Standards. The amendment to IFRS 1 is effective immediately and, thus, for periods beginning at 1

January 2014, and clarifies in the Basis for Conclusions that an entity may choose to apply either acurrent standard or a new standard that is not yet mandatory, but permits early application, provided

either standard is applied consistently throughout the periods presented in the entity's f first IFRSfinancial statements. This amendment to IFRS 1 has no impact on the Group since the Group is an

existing IFRS preparer.

v. Standards issued but not yet effective

The standards and interpretations issued, but not yet effective, up to the date of issuance of the

Group's financial statements are shown below. This list is not exhaustive but only discloses the

changes relevant to the Group. The Group intends to adopt these standards, if applicable, when

they become effective.IFRS 9 Financial Instruments

In July 2014, the IASB issued the final version of IFRS 9 Financial Instruments which reflects allphases of the financial instruments project and replaces IAS 39 Financial Instruments: Recognition

and Measurement and all previous versions of IFRS 9. The standard introduces new requirementsfor classification and measurement, impairment, and hedge accounting. IFRS 9 is effective for

annual periods beginning on or after 1January 2018, with early application permitted. Retrospective

application is required, but comparative information is not compulsory. Early application of previous

versions of IFRS 9 (2009, 2010 and 2013) is permitted if the date of initial application is before1 February 2015. The adoption of IFRS 9 will have an effect on the classification and measurement

of the Group's financial assets, but no impact on the classification and measurement of the Group'sfinancial liabilities.

IFRS 14 Regulatory Deferral Accounts

IFRS 14 is an optional standard that allows an entity, whose activities are subject to rate-regulation,

to continue applying most of its existing accounting policies for regulatory deferral account balances

upon its first-time adoption of IFRS. Entities that adopt IFRS 14 must present the regulatory deferral

accounts as separate line items on the statement of financial position and present movements in

these account balances as separate line items in the statement of profit or loss and other

comprehensive income. The standard requires disclosures on the nature of, and risks associated

with, the entity's rate-regulation and the effects of that rate-regulation on its financial statements.

IFRS 14 is effective for annual periods beginning on or after 1 January 2016. Since the Group is an

existing IFRS preparer, this standard would not apply.

Amendments to IAS 19 Defined Benefit Plans: Employee Contributions

IAS 19 requires an entity to consider contributions from employees or third parties when accounting

for defined benefit plans. Where the contributions are linked to service, they should be attributed to

periods of service as a negative benefit. These amendments clarify that, if the amount of the

contributions is independent of the number of years of service, an entity is permitted to recognisesuch contributions as a reduction in the service cost in the period in which the service is rendered,instead of allocating the contributions to the periods of service. This amendment is effective for

annual periods beginning on or after 1 July 2014. It is expected that this amendment is relevant tothe Group, since one of the entities within the Group has a defined benefit plans with contributions

from employees, but not third parties.19

Notes to the Consolidated Financial Statements World ORTat 31 December 2014

Accounting policies (continued)v. Standards issued but not yet effective (continued)

IFRS 3 Business CombinationsThe amendment is applied prospectively and clarifies that all contingent consideration arrangementsclassified as liabilities (or assets) arising from a business combination should be subsequentlymeasured at fair value through profit or loss whether or not they fall within the scope of IFRS 9 (orIAS 39, as applicable).IFRS 8 Operating SegmentsThe amendments are applied retrospectively and clarify that:An entity must disclose the judgements made by management in applying the aggregation criteria inparagraph 12 of IFRS 8, including a brief description of operating segments that have beenaggregated and the economic characteristics (e.g. sales and gross margins) used to assesswhether the segments are 'similar'.The reconciliation of segment assets to total assets is only required to be disclosed if thereconciliation is reported to the chief operating decision maker, similar to the required disclosure forsegment liabilities.

IAS 16 Property, Plant and Equipment and IAS 38 Intangible AssetsThe amendment is applied retrospectively and clarifies in IAS 16 and IAS 38 that the asset may berevalued by reference to observable data on either the gross or the net carrying amount. In addition,the accumulated depreciation or amortisation is the difference between the gross and carryingamounts of the asset.IAS 24 Related Party DisclosuresThe amendment is applied retrospectively and clarifies that a management entity (an entity thatprovides key management personnel services) is a related party subject to the related partydisclosures. In addition, an entity that uses a management entity is required to disclose theexpenses incurred for management services.IFRS 3 Business CombinationsThe amendment is applied prospectively and clarifies for the scope exceptions within IFRS 3 that:Joint arrangements, not just joint ventures, are outside the scope of IFRS 3This scope exception applies only to the accounting in the financial statements of the jointarrangement itselfIFRS 13 Fair Value MeasurementThe amendment is applied prospectively and clarifies that the portfolio exception in IFRS 13 can beapplied not only to financial assets and financial liabilities, but also to other contracts within thescope of IFRS 9 (or IAS 39, as applicable).IAS 40 Investment PropertyThe description of ancillary services in IAS 40 differentiates between investment property and owner-occupied property (i.e., property, plant and equipment). The amendment is applied prospectivelyand clarifies that IFRS 3, and not the description of ancillary services in IAS 40, is used to determineif the transaction is the purchase of an asset or business combination.

IFRS 15 Revenue from Contracts with CustomersIFRS 15 was issued in May 2014 and establishes a new five-step model that will apply to revenuearising from contracts with customers. Under IFRS 15 revenue is recognised at an amount thatreflects the consideration to which an entity expects to be entitled in exchange for transferring goodsor services to a customer.The principles in IFRS 15 provide a more structured approach to measuring and recognisingrevenue.The new revenue standard is applicable to all entities and will supersede all current revenuerecognition requirements under IFRS. Either a full or modified retrospective application is requiredfor annual periods beginning on or after 1 January 2017 with early adoption permitted. The Group iscurrently assessing the impact of IFRS 15 and plans to adopt the new standard on the requiredeffective date

20

Notes to the Consolidated Financial Statements World ORT

at 31 December 2014

Accounting policies (continued)v. Standards issued but not yet effective (continued)

Amendments to IFRS 11Joint Arrangements: Accounting for Acquisitions of Interests

The amendments to IFRS 11 require that a joint operator accounting for the acquisition of an

interest in a joint operation, in which the activity of the joint operation constitutes a business must

apply the relevant IFRS 3 principles for business combinations accounting. The amendments alsoclarify that a previously held interest in a joint operation is not remeasured on the acquisition of an

additional interest in the same joint operation while joint control is retained. In addition, a scope

exclusion has been added to IFRS 11to specify that the amendments do not apply when the parties

sharing joint control, including the reporting entity, are under common control of the same ultimate

controlling party.

The amendments apply to both the acquisition of the initial interest in a joint operation and the

acquisition of any additional interests in the same joint operation and are prospectively effective for

annual periods beginning onor after 1 January 2016, with early adoption permitted. These amendments are not expected to have

any impact to the Group.

Amendments to IAS 16 and IAS 38: Clarification of Acceptable Methods of Depreciation and

AmortisationThe amendments clarify the principle in IAS 16 and IAS 38 that revenue reflects a pattern of

economic benefits that are generated from operating a business (of which the asset is part) rather

than the economic benefits that are consumed through use of the asset. As a result, a revenue-

based method cannot be used to depreciate property, plant and equipment and may only be used in

very limited circumstances to amortise intangible assets. The amendments are effectiveprospectively for annual periods beginning on or after 1January 2016, with early adoption permitted.

These amendments are not expected to have any impact to the Group given that the Group has not

used a revenue-based method to depreciate its non-current assets.

Amendments to IAS 27: Equity Method in Separate Financial Statements

The amendments will allow entities to use the equity method to account for investments in

subsidiaries, joint ventures and associates in their separate financial statements. Entities already

applying IFRS and electing to change to the equity method in its separate financial statements will

have to apply that change retrospectively. For first-time adopters of IFRS electing to use the equity

method in its separate financial statements, they will be required to apply this method from the date

of transition to IFRS. The amendments are effective for annual periods beginning on or after 1

January 2016, with early adoption permitted

21

Notes to the Consolidated Financial Statementsat 31 December 2014

World ORT

3a Donations and grants

2014ÚS$'000

2013ÚS$'000

Donations restricted to specific projects 38,179 36,129

International Co-operation grants 314 1,691

38,493 37,820

Unrestricted donations 8,408 5,527

46,901 43,347

3b Property

Rents and tenant recharges

Property costs

4 Other Expenditure

2014US$'000

474

(628)

2013US$'000

342

(691)

(154) (349)

2014ÚS$'000

2013ÚS$'000

Personnel 1,258 1,365Defined contribution pension - benefits expense 96 177Defined benefit pension - contributions and recovery plan 209 132Defined benefit pension - service cost and interest (155) (182)Office 95 70Travel and meetings 219 176Premises and insurance 230 236Operating lease rentals 26 34Audit and consultancy fees 98 191Legal fees 146 166Other professional fees 61 222Depreciation 20 25Currency exchange gains/(losses) 83 (13)

2,386 2,599

22

Notes to the Consolidated Financial Statementsat 31 December 2014

World ORT

5 Employee benefit expense

Included in project costs:

2014US$'000

2013ÚS$'000

Salaries 4,719 4,082

Social security costs 176 181

Pension costs 2

Included in delivery costs:Salaries 986 950

Social security costs 777 646

Pension costs 25 143

Included in property costs:Salaries 157 133

Social security costs 16 5

Pension costs * 93

Included in fundraising and publicity costs:Salaries 530 478

Social security costs 110 93

Pension costs 68 151

Included in administration costs:Salaries 484 461

Social security costs 55 52

Pension costs * 82 (24)

Total employee benefit expense 8,187 7,444

* The cost of the defined benefit pension scheme for 2014 are includedin administration costs

6 Depreciation, leasing and foreign exchange differences included

in the consolidated statement of comprehensive activities2014 2013

Included in project costs: US$'000 ÚS$'000

Buildings and equipment - overseas so not capitalised 1,577 239

Leases 321 199

Foreign exchange differences (net) 131 179

Included in delivery costs:Equipment - overseas so not capitalised (2013: car sold) 15

Depreciation 16 14

Leases 148 180

Foreign exchange differences (net) 5 (33)

Included in property costs:Equipment - conferencing items of low individual value 2Depreciation 40 103

Foreign exchange differences (net) 23

Included in fundraising and publicity costs:Depreciation 1 3

Leases 12 3

Foreign exchange differences (net) (1)

Included in administration costs:Depreciation 19 22

Leases 14 31

Foreign exchange differences (net) 84 (13)

23

Notes to the Consolidated Financial Statementsat 31 December 2014

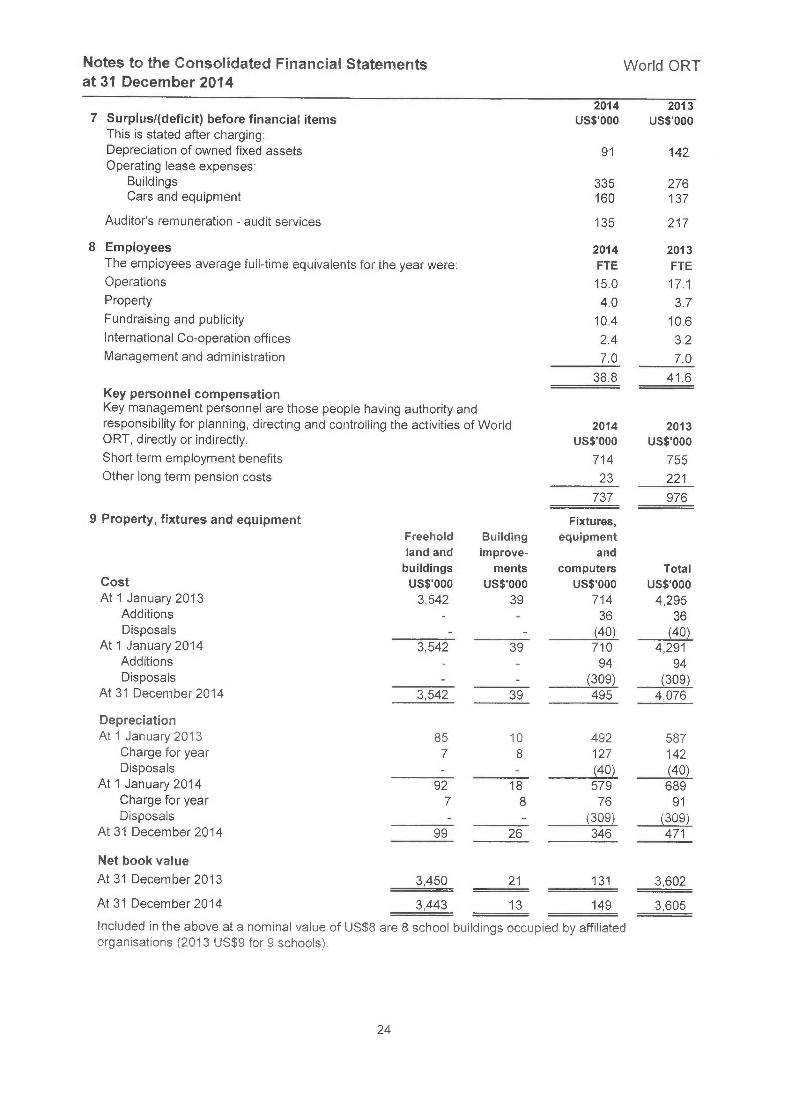

World ORT

7 Surplus/(deficit) before financial itemsThis is stated after charging:

2014US$'000

2013US$'000

Depreciation of owned fixed assets 91 142Operating lease expenses:

Buildings 335 276Cars and equipment 160 137

Auditor's remuneration - audit services 135 217

8 Employees 2014 2013The employees average full-time equivalents for the year were: FTE FTE

Operations 15.0 17.1Property 4.0 3.7Fundraising and publicity 10.4 10.6International Co-operation offices 2.4 3.2Management and administration 7.0 7.0

38.8 41.6Key personnel compensationKey management personnel are those people having authority andresponsibility for planning, directing and controlling the activities of World 2014 2013ORT, directly or indirectly. US$'000 US$'000Short term employment benefits 714 755Other long term pension costs 23 221

737 976

9 Property, fixtures and equipment Fixtures,Freehold Building equipmentland and improve- andbuildings ments computers Total

Cost US$'000 US$'000 US$'000 US$'000At 1 January 2013 3,542 39 714 4,295

Additions - 36 36Disposals (40) (40)

At 1 January 2014 3,542 39 710 4,291Additions 94 94Disposals - (309) (309)

At 31 December 2014 3,542 39 495 4,076

DepreciationAt 1 January 2013 85 10 492 587

Charge for year 7 8 127 142Disposals - (40) (40)

At 1 January 2014 92 18 579 689Charge for year 7 8 76 91Disposals - (309) (309)

At 31 December 2014 99 26 346 471

Net book value

At 31 December 2013 3,450 21 131 3,602

At 31 December 2014 3,443 13 149 3,605

Included in the above at a nominal value of US$8 are 8 school buildings occupied by affiliatedorganisations (2013 US$9 for 9 schools).

24

Notes to the Consolidated Financial Statementsat 31 December 2014

World ORT

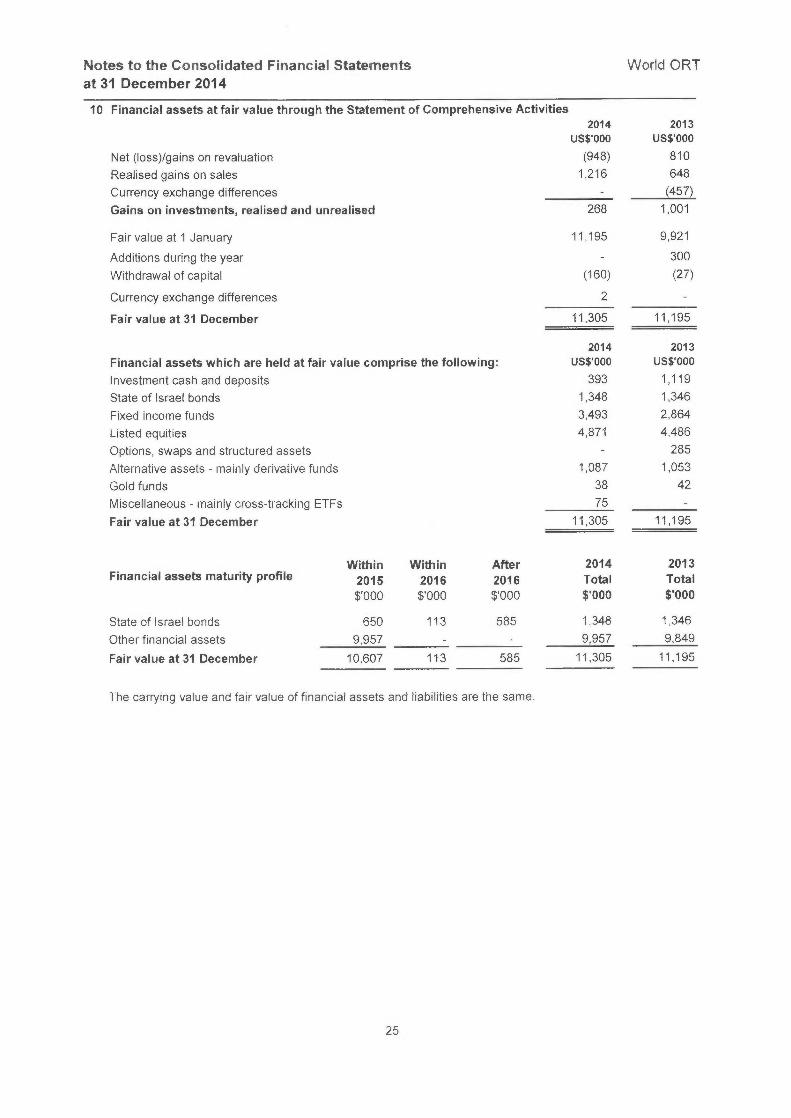

10 Financial assets at fair value through the Statement of Comprehensive Activities2014

ÚS$'000

2013

ÚS$'000

Net (loss)/gains on revaluation (948) 810

Realised gains on sales 1,216 648

Currency exchange differences - (457)

Gains on investments, realised and unrealised 268 1,001

Fair value at 1 January 11,195 9,921

Additions during the year - 300

Withdrawal of capital (160) (27)

Currency exchange differences 2 -

Fair value at 31 December 11,305 11,195

2014 2013

Financial assets which are held at fair value comprise the following: US$'000 US$'000

Investment cash and deposits 393 1,119

State of Israel bonds 1,348 1,346

Fixed income funds 3,493 2,864

Listed equities 4,871 4,486

Options, swaps and structured assets - 285

Alternative assets - mainly derivative funds 1,087 1,053

Gold funds 38 42

Miscellaneous - mainly cross-tracking ETFs 75

Fair value at 31 December 11,305 11,195

Within Within After 2014 2013Financial assets maturity profile 2015 2016 2016 Total Total

$'000 $'000 $'000 5'000 $'000

State of Israel bonds 650 113 585 1,348 1,346

Other financial assets 9,957 - - 9,957 9,849

Fair value at 31 December 10,607 113 585 11,305 11,195

The carrying value and fair value of financial assets and liabilities are the same.

25

Notes to the Consolidated Financial Statementsat 31 December 2014

World ORT

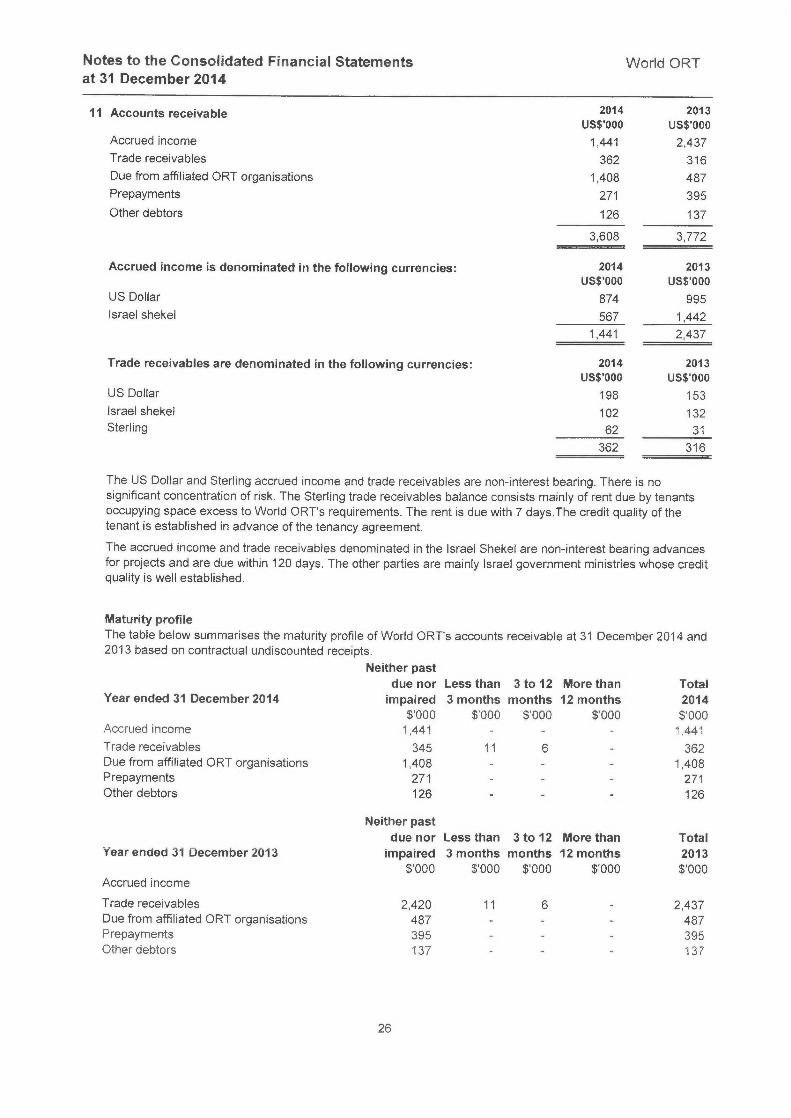

11 Accounts receivable 2014 2013ÚS$'000 ÚS$'000

Accrued income 1,441 2,437Trade receivables 362 316Due from affiliated ORT organisations 1,408 487Prepayments 271 395

Other debtors 126 137

3,608 3,772

Accrued income is denominated in the following currencies: 2014 2013ÚS$'000 ÚS$'000

US Dollar 874 995Israel shekel 567 1,442

1,441 2,437

Trade receivables are denominated in the following currencies: 2014 2013ÚS$'000 ÚS$'000

US Dollar 198 153Israel shekel 102 132Sterling 62 31

362 316

The US Dollar and Sterling accrued income and trade receivables are non-interest bearing. There is nosignificant concentration of risk. The Sterling trade receivables balance consists mainly of rent due by tenantsoccupying space excess to World ORT's requirements. The rent is due with 7 days.The credit quality of thetenant is established in advance of the tenancy agreement.

The accrued income and trade receivables denominated in the Israel Shekel are non-interest bearing advancesfor projects and are due within 120 days. The other parties are mainly Israel government ministries whose creditquality is well established.

Maturity profileThe table below summarises the maturity profile of World ORT's accounts receivable at 31 December 2014 and2013 based on contractual undiscounted receipts.

Neither pastdue nor Less than 3 to 12 More than Total

Year ended 31 December 2014 impaired 3 months months 12 months 2014$'000 $'000 $'000 $'000 $'000

Accrued income 1,441- 1,441

Trade receivables 345 11 6 362Due from affiliated ORT organisations 1,408 1,408Prepayments 271 271Other debtors 126 126

Neither pastdue nor Less than 3 to 12 More than Total

Year ended 31 December 2013 impaired 3 months months 12 months 2013$'000 $'000 $'000 $'000 $'000

Accrued income

Trade receivables 2,420 11 6 2,437Due from affiliated ORT organisations 487

- 487Prepayments 395

- 395Other debtors 137

-

-

137

26

Notes to the Consolidated Financial Statements World ORT

at 31 December 2014

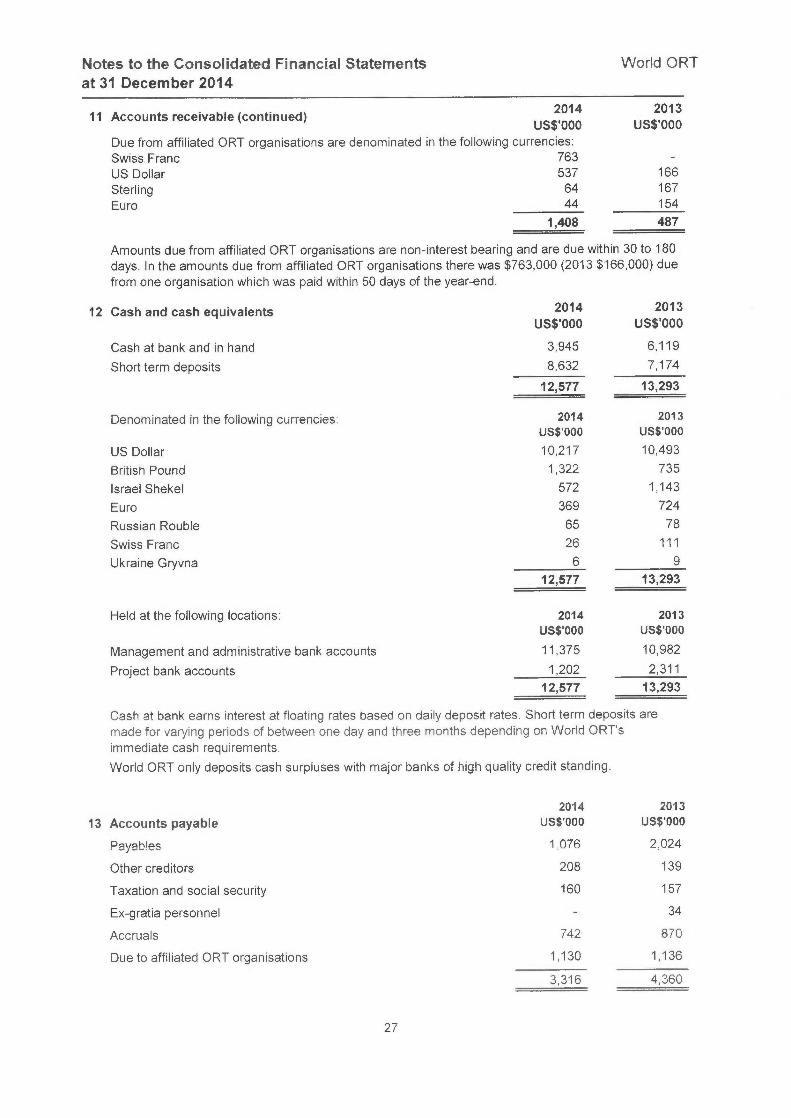

11 Accounts receivable (continued) 2014

ÚS$'000

Due from affiliated ORT organisations are denominated in the following currencies:

Swiss Franc 763

2013ÚS$'000

-

US Dollar 537 166

Sterling 64 167

Euro 44 154

1,408 487

Amounts due from affiliated ORT organisations are non-interest bearing and are due within 30 to 180

days. In the amounts due from affiliated ORT organisations there was $763,000 (2013 $166,000) due

from one organisation which was paid within 50 days of the year-end.

12 Cash and cash equivalents 2014 2013ÚS$'000 ÚS$'000

Cash at bank and in hand 3,945 6,119

Short term deposits 8,632 7,174

12,577 13,293

Denominated in the following currencies: 2014 2013

US$'000 US$'000

US Dollar 10,217 10,493

British Pound 1,322 735

Israel Shekel 572 1,143

Euro 369 724

Russian Rouble 65 78

Swiss Franc 26 111

Ukraine Gryvna 6 9

12,577 13,293

Held at the following locations: 2014 2013

ÚS$'000 US$'000

Management and administrative bank accounts 11,375 10,982

Project bank accounts 1,202 2,311

12,577 13,293

Cash at bank earns interest at floating rates based on daily deposit rates. Short term deposits are

made for varying periods of between one day and three months depending on World ORT's

immediate cash requirements.

World ORT only deposits cash surpluses with major banks of high quality credit standing.

13 Accounts payable

2014

ÚS$'0002013

US$'000

Payables 1076 2.024

Other creditors 208 139

Taxation and social security 160 157

Ex-gratia personnel - 34

Accruals 742 870

Due to affiliated ORT organisations 1,130 1,136

3,316 4,360

27

Notes to the Consolidated Financial Statements World ORTat 31 December 2014

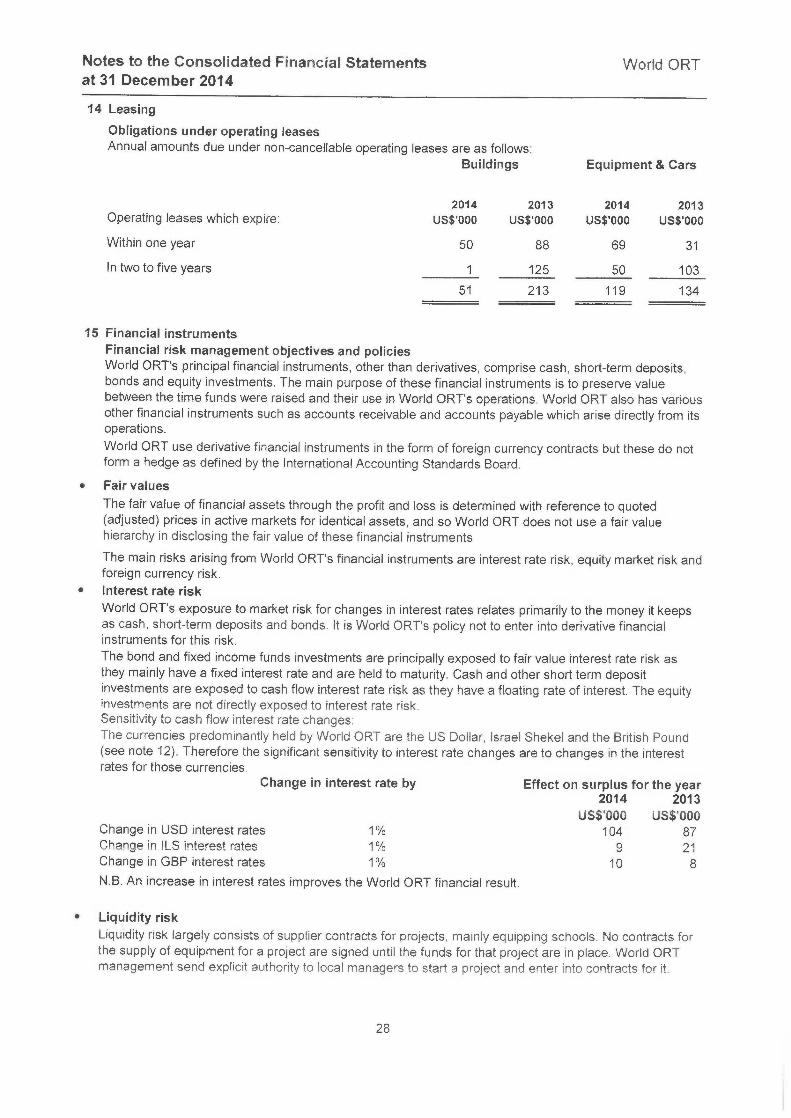

14 Leasing

Obligations under operating leasesAnnual amounts due under non-cancellable operating leases are as follows:

Buildings Equipment & Cars

2014 2013 2014 2013Operating leases which expire: US$'000 US$'000 US$'000 US$'000

Within one year 50 88 69 31

In two to five years 1 125 50 103

51 213 119 134

15 Financial instrumentsFinancial risk management objectives and policiesWorld ORT's principal financial instruments, other than derivatives, comprise cash, short-term deposits,bonds and equity investments. The main purpose of these financial instruments is to preserve valuebetween the time funds were raised and their use in World ORT's operations. World ORT also has variousother financial instruments such as accounts receivable and accounts payable which arise directly from itsoperations.World ORT use derivative financial instruments in the form of foreign currency contracts but these do notform a hedge as defined by the International Accounting Standards Board.

• Fair values

The fair value of financial assets through the profit and loss is determined with reference to quoted(adjusted) prices in active markets for identical assets, and so World ORT does not use a fair valuehierarchy in disclosing the fair value of these financial instruments

The main risks arising from World ORT's financial instruments are interest rate risk, equity market risk andforeign currency risk.

• Interest rate riskWorld ORT's exposure to market risk for changes in interest rates relates primarily to the money it keepsas cash, short-term deposits and bonds. It is World ORT's policy not to enter into derivative financialinstruments for this risk.The bond and fixed income funds investments are principally exposed to fair value interest rate risk asthey mainly have a fixed interest rate and are held to maturity. Cash and other short term depositinvestments are exposed to cash flow interest rate risk as they have a floating rate of interest. The equityinvestments are not directly exposed to interest rate risk.Sensitivity to cash flow interest rate changes:The currencies predominantly held by World ORT are the US Dollar, Israel Shekel and the British Pound(see note 12). Therefore the significant sensitivity to interest rate changes are to changes in the interestrates for those currencies.

Change in interest rate by Effect on surplus for the year2014 2013

ÚS$'000 ÚS$'000Change in USD interest rates 1% 104 87Change in ILS interest rates 1% 9 21Change in GBP interest rates 1% 10 8N.B. An increase in interest rates improves the World ORT financial result.

• Liquidity riskLiquidity risk largely consists of supplier contracts for projects, mainly equipping schools. No contracts forthe supply of equipment for a project are signed until the funds for that project are in place. World ORTmanagement send explicit authority to local managers to start a project and enter into contracts for it.

28

Notes to the Consolidated Financial Statements World ORTat 31 December 2014

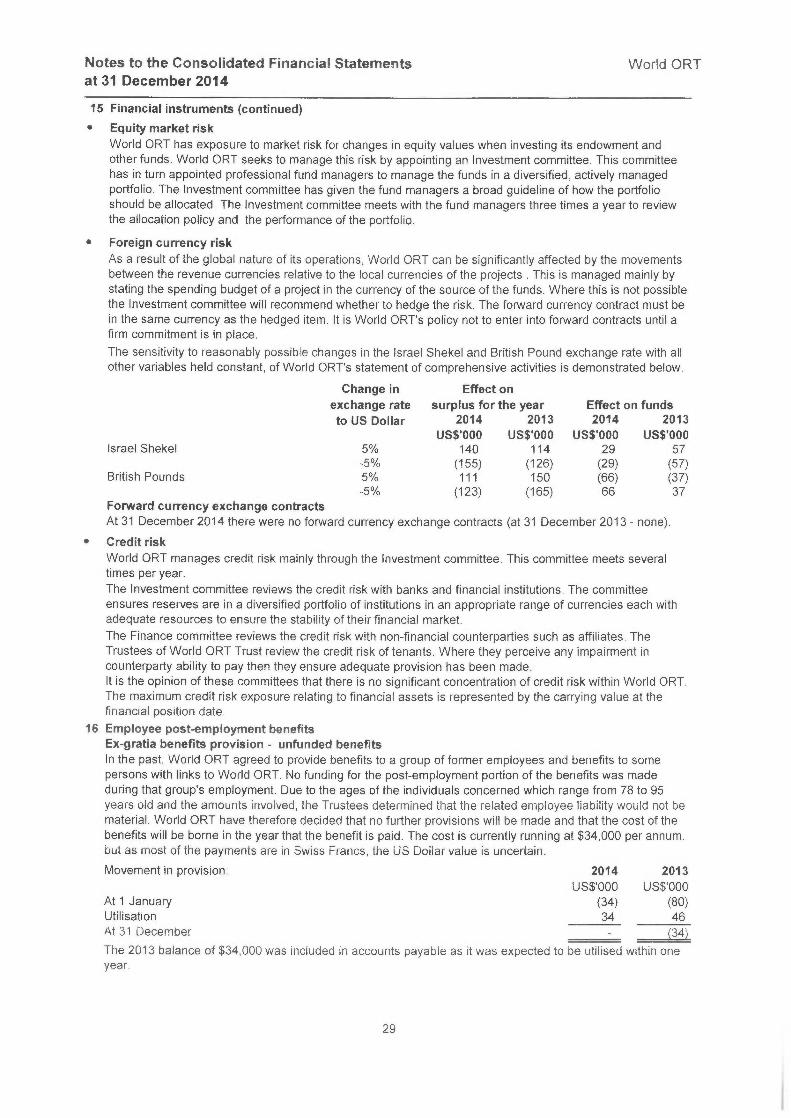

15 Financial instruments (continued)

• Equity market riskWorld ORT has exposure to market risk for changes in equity values when investing its endowment andother funds. World ORT seeks to manage this risk by appointing an Investment committee. This committeehas in turn appointed professional fund managers to manage the funds in a diversified, actively managedportfolio. The Investment committee has given the fund managers a broad guideline of how the portfolioshould be allocated. The Investment committee meets with the fund managers three times a year to reviewthe allocation policy and the performance of the portfolio.

• Foreign currency risk

As a result of the global nature of its operations, World ORT can be significantly affected by the movementsbetween the revenue currencies relative to the local currencies of the projects . This is managed mainly bystating the spending budget of a project in the currency of the source of the funds. Where this is not possiblethe Investment committee will recommend whether to hedge the risk. The forward currency contract must bein the same currency as the hedged item. It is World ORT's policy not to enter into forward contracts until afirm commitment is in place.

The sensitivity to reasonably possible changes in the Israel Shekel and British Pound exchange rate with allother variables held constant, of World ORT's statement of comprehensive activities is demonstrated below.

Change in

exchange rate

to US Dollar

Effect on

surplus for the year2014 2013

US$'000 US$'000

Effect on funds2014 2013

US$'000 US$'000Israel Shekel 5% 140 114 29 57

-5% (155) (126) (29) (57)British Pounds 5% 111 150 (66) (37)

-5% (123) (165) 66 37Forward currency exchange contractsAt 31 December 2014 there were no forward currency exchange contracts (at 31 December 2013 - none).

• Credit risk

World ORT manages credit risk mainly through the Investment committee. This committee meets severaltimes per year.The Investment committee reviews the credit risk with banks and financial institutions. The committeeensures reserves are in a diversified portfolio of institutions in an appropriate range of currencies each withadequate resources to ensure the stability of their financial market.The Finance committee reviews the credit risk with non-financial counterparties such as affiliates. TheTrustees of World ORT Trust review the credit risk of tenants. Where they perceive any impairment incounterparty ability to pay then they ensure adequate provision has been made.It is the opinion of these committees that there is no significant concentration of credit risk within World ORT.The maximum credit risk exposure relating to financial assets is represented by the carrying value at thefinancial position date.

16 Employee post-employment benefitsEx-gratia benefits provision - unfunded benefitsIn the past, World ORT agreed to provide benefits to a group of former employees and benefits to somepersons with links to World ORT. No funding for the post-employment portion of the benefits was madeduring that group's employment. Due to the ages of the individuals concerned which range from 78 to 95years old and the amounts involved, the Trustees determined that the related employee liability would not bematerial. World ORT have therefore decided that no further provisions will be made and that the cost of thebenefits will be borne in the year that the benefit is paid. The cost is currently running at $34,000 per annum.but as most of the payments are in Swiss Francs, the US Dollar value is uncertain.

Movement in provision:

At 1 JanuaryUtilisationAt 31 December

2014

US$'000(34)34

2013

US$'000(80)46 (34)

The 2013 balance of $34,000 was included in accounts payable as it was expected to be utilised within oneyear.

29

Notes to the Consolidated Financial Statements World ORTat 31 December 2014

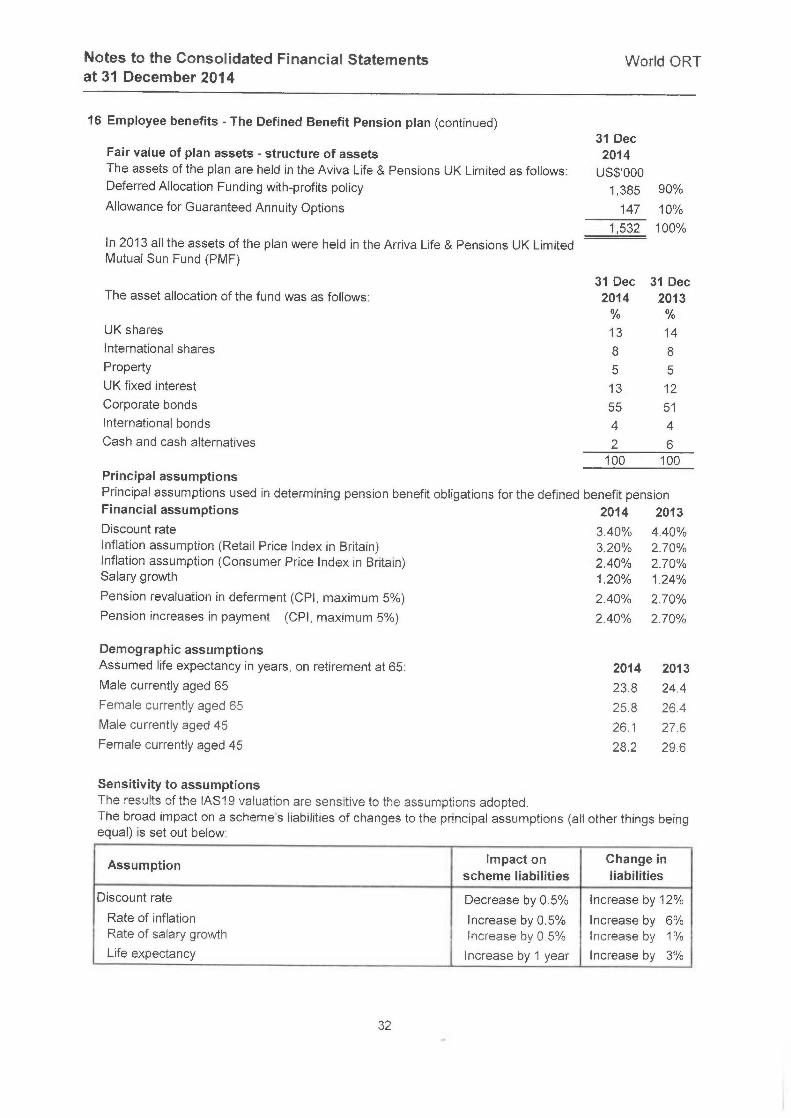

16 Employee post-employment benefits

World ORT has a subsidiary which operates the following pension plans:• The Defined Contribution Pension scheme

The assets of the defined contribution pension scheme are held separately from those of World ORT in anindependently administered fund. World ORT contributes up to 11% (mainly 5%). The cost to World ORT ofcontributions to the scheme was $88,000 (2013: $259,000).The reason for the year-on-year decrease was that two staff who left during 2013 opted for certain moniesdue to them to be paid into their pension fund accounts.

Unpaid contributions at the end of the year were $9,000, paid in January 2015 (2013: $6,664 paid inJanuary 2014).

• Employee benefits - The Defined Benefit Pension planThis scheme is known as the ORT Retirement Benefit Plan (ORBP) which is based in Great Britain andadministered by a third party. The assets of the scheme are held separately to those of World ORT. Theplan assets are 100% invested in a with-profit fund.The plan closed to new entrants in 1999. The plan has an independent professional trustee.

Periodically, the trustee reviews the level of funding in the ORBP as required by UK pension law. Such areview includes the asset-liability matching strategy and investmentrisk management policy. The board of trustees adjusts its contribution based on the results of the triennialactuarial review.Since the pension liability is adjusted to consumer price index, the pension plan is exposed to UK's inflation,interest rate risks and changes in the life expectancy for pensioners. As the plan assets include significantinvestments in corporate bonds and quoted equity shares of entities, World ORT is also exposed to marketrisk arising in the corporate bonds and equity sectors.A full actuarial valuation was carried out at 1 January 2012 and the process has started for the full valuationat 1 January 2015. A calculation was done to 31 December 2014 by a qualified actuary, independent of thescheme's sponsoring employer. The major assumptions used by the actuary are shown below.World ORT currently pays contributions at the rate of 38.8% of pensionable pay (2013: 27.6%).Contributory members pay their employee contributions at the rate of 7% of pensionable salary. Theemployer makes a special payment for the contributions of the non-contributory members at the same rate.Membership of the defined benefit pension plan

2014 2013Active members at 31 December 3 4Preserved and deferred members at 31 December 42 42Of the active members, the average time to the plan's normal retirement age of 65 is 6.5 years with theyoungest having 13.5 years to serve.

Based on the existing schedule of contributions, World ORT expects to contribute US$136,000 plus 38.8%of total pensionable salaries to The ORT Retirement Benefit Plan in the next accounting year.

The expected contributions to the defined benefit plan obligation in future years are:

2014 2013ß!S$'000 US$'000

Within the next 12 months 186 1950 615 546Between 6 and 10 years 172 264Beyond 10 years 65 25Total expected payments 1,038 1,030

The expected duration of the plan is 13.5 years (2013: 14.5 years).

30

Notes to the Consolidated Financial Statements

at 31 December 2014

World ORT

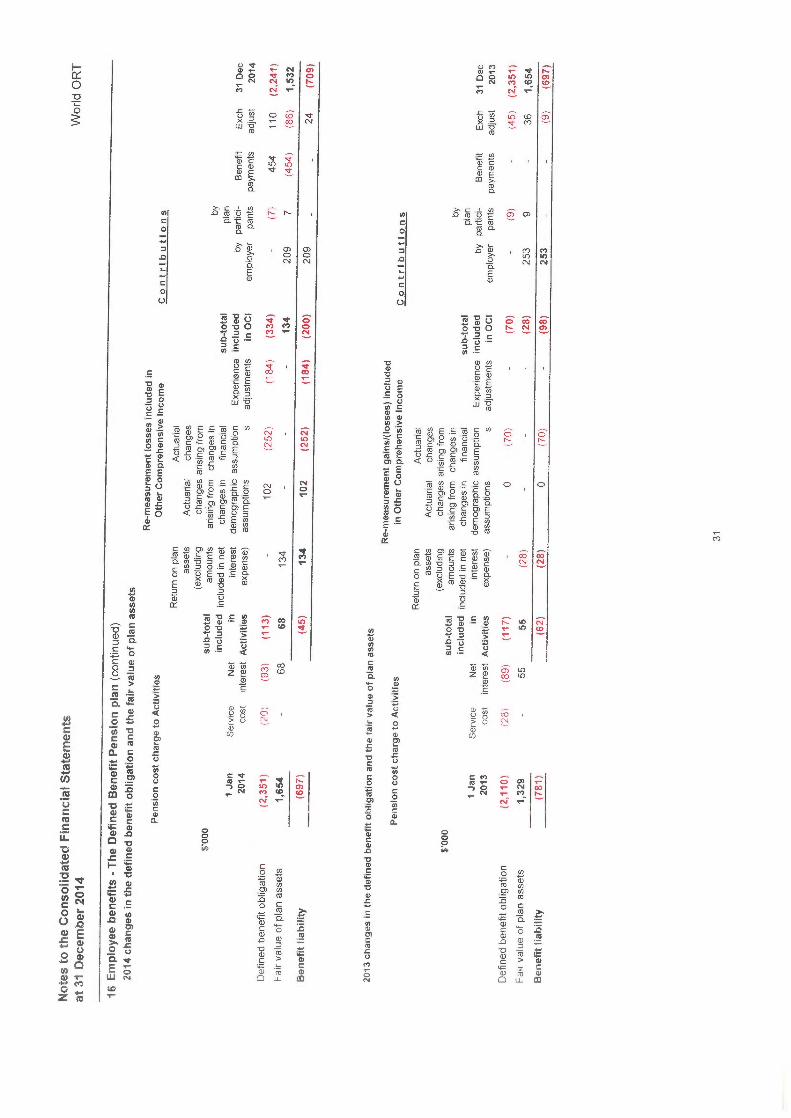

16 Employee benefits - The Defined Benefit Pension plan (continued)

2014 changes in the defined benefit obligation and the fair value of plan assets

Re-measurement losses included in