Embed Size (px)

Citation preview

- 1 -

Report of Bank of China (Hungária) Zrt.

Compliant with the disclosure requirements contained in Regulation 575/2013/EU of the European Parliament and of the

Council on prudential requirements for credit institutions and investment firms (CRR)

In respect of 31 December 2016

This report follows the structure of the CRR.

Scope of the disclosure requirements (CRR Article 431)

Pursuant to the provisions of Act CCXXXVII of 2013 on Credit institutions and financial enterprises, Bank of China (Hungária) Zrt., (hereinafter: the Bank) shall fulfill the reporting requirements contained in Regulation 575/2013/EU of the European Parliament and of the Council on prudential requirements for credit institutions and investment firms (hereinafter: CRR or Regulation), part eight, on an individual basis, once a year.

Declaration of the Board of Directors of Bank of China (Hungária) Zrt., pursuant to Article 435 section (1) of the Regulation:

The general risk profile of the Bank

The Bank follows the guidelines of Bank of China Limited (hereinafter: Head Office or Owner or BOC), which are characterized by a conservative approach to risk-taking. The aim of the Bank is to implement its strategic objective, under which it shall find the correct ratio between risk-taking and profit. The Bank focuses its business activities for the purpose of earning a profit, on lending to large corporations and on trade financing, in order to promote economic relations between China and Central Eastern Europe.

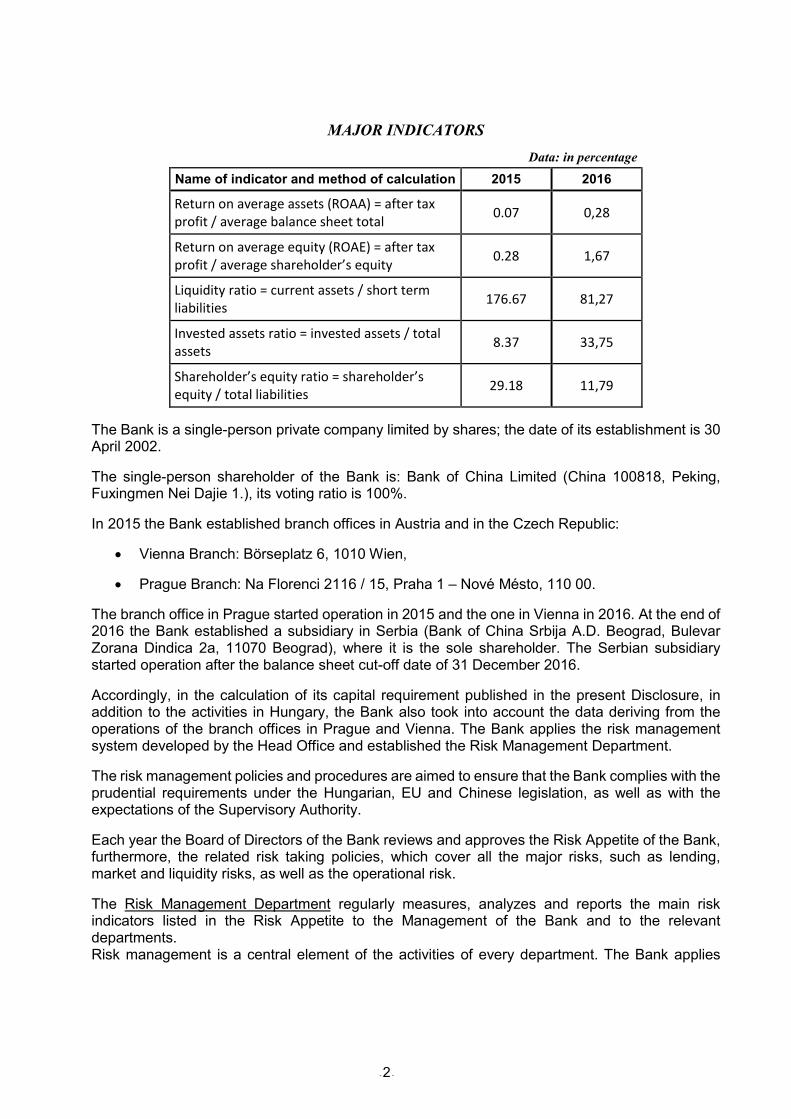

The activities of the Bank in 2016 were implemented in accordance with its business strategy, it operated profitably and all its assets are problem-free. Expressed as the after tax profit divided by total assets, the return on assets stood at 0.20% according to data as of the end of 2016. Additional indicators characteristic of the activity of the Bank are provided in the following table:

- 2 -

MAJOR INDICATORS

Data: in percentage

Name of indicator and method of calculation 2015 2016

Return on average assets (ROAA) = after tax profit / average balance sheet total

0.07 0,28

Return on average equity (ROAE) = after tax profit / average shareholder’s equity

0.28 1,67

Liquidity ratio = current assets / short term liabilities

176.67 81,27

Invested assets ratio = invested assets / total assets

8.37 33,75

Shareholder’s equity ratio = shareholder’s equity / total liabilities

29.18 11,79

The Bank is a single-person private company limited by shares; the date of its establishment is 30 April 2002.

The single-person shareholder of the Bank is: Bank of China Limited (China 100818, Peking, Fuxingmen Nei Dajie 1.), its voting ratio is 100%.

In 2015 the Bank established branch offices in Austria and in the Czech Republic:

Vienna Branch: Börseplatz 6, 1010 Wien,

Prague Branch: Na Florenci 2116 / 15, Praha 1 – Nové Mésto, 110 00.

The branch office in Prague started operation in 2015 and the one in Vienna in 2016. At the end of 2016 the Bank established a subsidiary in Serbia (Bank of China Srbija A.D. Beograd, Bulevar Zorana Dindica 2a, 11070 Beograd), where it is the sole shareholder. The Serbian subsidiary started operation after the balance sheet cut-off date of 31 December 2016.

Accordingly, in the calculation of its capital requirement published in the present Disclosure, in addition to the activities in Hungary, the Bank also took into account the data deriving from the operations of the branch offices in Prague and Vienna. The Bank applies the risk management system developed by the Head Office and established the Risk Management Department.

The risk management policies and procedures are aimed to ensure that the Bank complies with the prudential requirements under the Hungarian, EU and Chinese legislation, as well as with the expectations of the Supervisory Authority.

Each year the Board of Directors of the Bank reviews and approves the Risk Appetite of the Bank, furthermore, the related risk taking policies, which cover all the major risks, such as lending, market and liquidity risks, as well as the operational risk.

The Risk Management Department regularly measures, analyzes and reports the main risk indicators listed in the Risk Appetite to the Management of the Bank and to the relevant departments. Risk management is a central element of the activities of every department. The Bank applies

- 3 -

various tools: it sets limits for the clients and transactions, applies qualifications and also involves collaterals. The regulation of the risk assumption process is an important element of risk management. Head Office developed a complex regulation concerning the entire Group on the risk profile and the Bank prepares its own Risk Policy in that framework, properly applying the aims formulated therein. In the field of risk management the Bank follows its own internal rules regulating the processes of risk assumption and management, the rules of decision-making and levels of approval, the eligible collaterals and securities upon the establishment of a business relationship, then the debt rating procedures during the existence of the business relationship. Management of the credit risk The purpose of the process of credit approval is to reduce the credit risk. The system of limits is an important element to control credit risks. The Bank has introduced limits on countries, industries, products, partners and clients. It has established a limit on large exposures and on the group of associated enterprises. It is a further aim of these limits to enable the control of concentration risk (as well). The Bank prefers those exposures, where the transaction is supported by a strong collateral and accepts bank guarantees (including guarantees received from the sister institutions of BoC), cash collateral, mortgage, pledge and suretyship. The Bank worked out in detail the policies applying to the evaluation of risks and the collaterals, which take into account the characteristics, availability and enforceability of the asset. This procedure is an important part of the risk taking process. Regular risk monitoring evaluates not only the financial and commercial position of the debtor, but also the developments concerning the given transaction and the collaterals during the entire term of the assets. The Bank does not participate in credit derivative transactions. In order to record and update the data concerning its exposures, the Bank adopted the procedures elaborated by the Head Office, furthermore, it uses the IT application developed for this purpose by the Head Office.

Market risk The Bank takes a conservative approach to market risks: basically, it does not engage in any FX transactions on its own account (proprietary trading) and also minimizes the interest risks. The Bank does not provide investment services. Head Office introduced limits for banking book and trading book transactions. In 2016 the Bank observed every limit applying to market risks. The Risk Management Department of the Bank is responsible for the management of the market risks. The Middle Office continuously reports to the Management of the Bank on exposures related to market risks and any development that affect these. The Bank applies a method and a limit system for the measurement of market risks. In 2014 Head Office implemented a new core accounting system, in order to further strengthen general risk management. Specially developed subsystems are available to monitor market risks as well. During 2016 the Bank continued to tightly cooperate with the developers of the system. In order to make optimal use of the opportunities provided by the system, the employees of the Bank participate in continuous training. These systems provide sufficient information for every person and unit responsible for risk management, within the framework of their scope of decision-making. The Head Office and the Bank keep developing the relevant IT systems, so they comply with the regulatory requirements of the Basel Convention, the EU, Hungary and China related to the risks of the Treasury transactions

- 4 -

as well. The Bank introduced a strict regulation on the Treasury partner and transaction limits, which are also monitored at Group level. Senior Management of the Bank regularly receives reports on assets exposed to market risk. The Bank allocates additional capital under Pillar II on its portfolio exposed to market risk, as prescribed by the Supervisory Authority.

Counterparty risk Head Office established a global counterparty risk limit regime, and the Bank operates in compliance with that. At the same time, the Bank may introduce a local limit while adhering to the guideline of the Head Office, following the assessment of the possible counterparty’s financial position. Concerning treasury transactions, in most cases the Bank uses the services of other members of the BoC Group, thereby minimizing any undesirable risks that may come with the wrong-way counterparty risk. The Bank did not conclude any netting agreements in the year of the disclosure. As at 31 December 2016 the Bank had no transaction that would have required any counterparty risk calculation under the CRR.

Operational risk The Bank uses the basic indicator approach to define the capital requirements of the operational risks. The capital set aside for this purpose was always significantly higher than the losses related to the operational risks borne by the Bank. The Bank obtained several types of insurances in order to reduce its operational risks (asset insurance, third party liability insurance, etc.).

Statement Pursuant to Article 435 (1) of the Regulation, the Board of Directors of Bank of China (Hungária) Zrt., states by approving the present Report that its risk management system is appropriate, which guarantees that the applied risk management system is appropriate in terms of the profile and strategy of the Bank and the risk profile of the Bank is within the framework approved by the Board of Directors.

Non-material, proprietary or confidential information (CRR Article 432).

Pursuant to Article 432 (1) of CRR, institutions may omit one or more of the disclosures listed in CRR. However, the Bank did not take this opportunity concerning the reporting year. The Bank publishes information that is relevant for its activity.

Frequency and means of disclosure (CRR Articles 433. and 434)

The Bank publishes the information required by the CRR annually and provides it on its web site.

Risk management objectives and policies (CRR Article 435)

Major risk types affecting the Bank are the following:

1. Credit risk (default risk) 2. Operational risks 3. Market risk

- 5 -

4. Residual risk 5. Concentration risk 6. Country risk 7. Counterparty risk 8. Banking book interest rate risk 9. Liquidity risk

The highest risk of the activity of the Bank is connected with the lending to the clients; therefore management of the relevant risks needs special attention.

1. Credit risks related to clients

1.1. Strategy of credit risk management

The Bank uses the “standard” method to quantify the capital requirement of the lending risk.

In order to ensure safe and profitable operation, the Bank has developed its client lending and risk assumption conditions, which it amends, as necessary, on the basis of the applicable rules of law, the business concepts and requirements of the Owner and the recommendations of the Supervisory Authority. Client lending includes every case of risk-taking that will result in the commitment of the Bank to make a payment related to its client with the probability that the client will not fulfill its obligation as per the contract.

The Bank may extend the loan or provide suretyship, bank guarantee or other banker’s obligation if its full return seems certain based on the business and financial plans of the transaction and the available collaterals. The Bank extends loans in the local market primarily when either real estate, or bank guarantee or cash collateral is available. The Bank takes part in international syndicated loans and mainly participates in transactions assessed and preferred by the Owner. The debtors repaid their loans immaculately in the reporting year as well. The Bank extended short-term loans to companies registered in China in 2016 as well, under a cooperation agreement concluded with the Owner, which provides also for the collaterals of the repayment of the loans. In accordance with the practice of former years, in 2016 the Bank continued its cooperation in the field of trade financing with other units of the Bank of China Group. The deals were completed in various forms, however, it was a common feature that the individual claims were guaranteed by a branch office of Bank of China.

The decision-makers are the competent deputy general manager, or the Credit Approval Officer and the Credit Risk Committee together, or the Owner, who make their decisions according to value limits or type of business. The Chief Executive Officer of the Bank has veto right on risk-taking. The decision-maker defines the conditions of risk-taking in a resolution. Organizational units independent of the business function will give their opinion on the proposals on risk-taking.

Monitoring of the risks is based on the decision approving the risk-taking. When the contracts on risk-taking are concluded and the loans are to be disbursed, the relevant departments of the Bank verify compliance with the stipulations of the contracts regulating the disbursement. The Bank regularly verifies whether the clients fulfill their payment and data reporting obligations. The Bank may impose sanctions in the case of failure to do so. Since until now each debtor has fulfilled all the payment obligations according to schedule, the Bank has not yet imposed any sanctions.

- 6 -

1.2. Process of credit risk management

1.2.1. Client and transaction rating

Corporate Banking Department (CBD) prepares the risk-taking proposals in case of large corporate clients for the decision-making bodies of the Bank and the proposal is assessed by Risk Management Department, which is independent from CBD and

a) verifies whether the proposal complies with the regulations of the Bank; b) analyzes the risks of the client, the risks of the transaction and the offered collaterals, securities, assesses the risk classification of the client according to its balance sheet and the client’s limit; c) forms a summary of the analysis and provides an opinion on what contractual conditions Risk Management Department would support the deal.

Corporate Banking Department manages also the deals financing companies registered in China. These deals are subject to the cooperation within the BOC Group. The approval of such transactions takes place in a simplified framework: when Risk Management Department is satisfied that the Bank has received the necessary data on the transaction and that the transaction is covered by the commitment of the BOC Group or other financial institutions (or by cash collateral), then the competent Deputy General Manager will approve it.

1.2.2. Steps before signing the contract and loan disbursement

Both Legal & Compliance Department and Risk Management Department examines the contracts to be concluded with the clients of the Bank before signing, according to the following criteria:

i) whether the contractual conditions are met under the valid resolution necessary for signing the contract, ii) whether every contract for the given deal has been prepared compliant with the relevant resolution, iii) whether the data of the contract(s) are comprehensive, true and consistent, iv) whether the contracts contain correctly all the data, provisions and conditions included

in the resolution.

If the contract or any of the related contracts is not qualified impeccable, Legal & Compliance Department and/or Risk Management Department will notify Corporate Banking Department on the remarks and initiate the necessary amendments.

1.2.3. Submission of a proposal on classification of the assets

It is primarily the task of Corporate Banking Department to submit a proposal to the decision-makers of the Bank on the quarterly and extraordinary classification of the client-related assets and off-balance-sheet items. Also Corporate Banking Department will submit a proposal to the decision-makers on the rate of impairment and provisions if needed, after Risk Management Department and the Credit Approval Officer have checked and counter-signed it.

Ever since the Bank was established so far each client has fulfilled all his/her obligations to the Bank in time, therefore no impairment has been formed and no work-out activity has taken place.

The Bank monitors its client-related exposures and compliance with the contractual payment

- 7 -

conditions on a monthly basis and notifies the competent personnel of the Bank accordingly. This evaluation covers the entire client portfolio and filters the actual and expected risks in time. Prior to the maturity date Corporate Banking Department notifies the debtors requesting them to secure the cover for interest payment and capital installment in time.

Should it become necessary, Corporate Banking Department and Risk Management Department would make the arrangements related to late payments. In case the delay and/or the anticipated loss would justify that the Bank should reclassify its exposure and recognize impairment or create provision, Corporate Banking Department will submit a proposal on the actions related to collection and on the rate of the impairment/provision to the Credit Approval Officer after obtaining the opinion of Risk Management Department.

The approval of the Owner is required to create an impairment/provision exceeding USD 2 million.

Following the completion of the quarterly asset classification process, based on the opinion of Risk Management Department and the Credit Approval Officer, Corporate Banking Department will submit a report to the Management, if reclassification and creating a provision become necessary.

Client and client group limit

The Bank applies a client and client group limit system in order to define the maximum risk acceptable in respect of one client or one group of clients. The limit of the individual clients or client groups is determined by the client classification category, by the economic situation of the sector of the client/client group and by their system of collaterals. The Bank will not assume any risk higher than the client limit in respect of the client/client group.

1.2.4. Collateral valuation

In addition to the assessment of risks, the Bank regularly evaluates, both in the course of decision making and in monitoring, the credit risk mitigating tools (collaterals) offered by the client or a third party or the covenants ensured in the contract.

Further information is provided on collateral evaluation and credit risk mitigating techniques in section “Use of credit risk mitigation techniques” (CRR Article 453)

1.2.5. Lending to small enterprises and retail customers

Considering the fact that the Bank only operates two branch offices in Hungary, lending to retail customers and to small enterprises is performed only in a moderate volume. This activity is also performed according to the above principles: Banking Department accepts and evaluates the application of the client. In case of SME loans the approval procedure is identical with the one followed in case of large corporate customers. In case of retail lending Risk Management Department evaluates the proposals and submits them to the Credit Approval Officer for approval.

2. Operational risks

See the chapter on “Operational risk” (CRR Article 446) for detailed information on operational risk.

3. Market risk

At the end of the year 2016 the Bank had open positions in euro, pound sterling, Japanese yen, US dollar, Chinese yuan and Czech koruna. The position in Czech koruna was related to the Prague Branch of the Bank opened during 2015. The capital requirement calculated on market risks and

- 8 -

further details are contained in the chapter “Exposure to market risk (CRR Article 445)”

4. Residual risk

One of the methods applied by the Bank to mitigate the risks concerning exposures to clients is to apply a conservative definition of the scope and value of collaterals when the collaterals and securities are accepted.

Proposals will be submitted to the decision makers on risk taking related to clients by presenting the fair market value of the collaterals, furthermore, any factors that may have an impact on the expenses that would be incurred in a collection procedure, and a higher collateral multiplier may be proposed on the basis of client rating and the coverage requirements to be determined depending on the transaction.

In case of real estate collaterals securing assets with a long-term maturity the properties must be regularly reappraised in accordance with the legal requirements.

The Bank regularly examines the collaterals of risk-taking transactions as part of its credit monitoring activity and identifies the residual risks in the framework of the quarterly asset classification.

5. Concentration risk

The concentration risk can be defined as any individual (direct and/or indirect) exposure or group of exposures that is capable of causing a loss that would jeopardize the continuous operation or the continuation of the activities of the Bank.

Concentration risk may derive from the following:

1) large individual (or possibly related) exposures (the definition of "related" must be broad

enough to include, for example, exposures related through joint

ownership/management/guarantee providers); and

2) significant exposures existing in respect of such groups of partners where the likelihood of

a default is determined by common reasons, for example:

- economic sector;

- geographical location;

- currency;

- product;

- credit risk mitigating measures (including, among others, risks existing in respect of

one single security provider, related to indirect credit exposure).

The fundamental tools for concentration risks management are the limit systems. The regulations on the limit systems are subject to approval by the Board of Directors of the Bank. In the case of assuming a large risk concerning one client or client group, the Bank follows the legal requirements. The Bank continuously monitors the concentration of its exposures to client groups and sectors. Possible exposures to foreign enterprises may be converted to risks related to financial institutions for the Bank through individual commitments of the BOC Group or Chinese financial institutions. The Bank pays special attention to observe the limits of large exposures.

The Bank does not apply regional limits within the country.

- 9 -

6. Country risk

The Bank defines country limits for its international operations applying to every country where it has a one-time or continuous exposure (e.g. a branch office of Bank of China, or a subsidiary bank, a counterparty bank or borrower is located there, who is involved in a transaction resulting an exposure). The country limit is the summarized measure of the risks allowed to be accepted by the Bank concerning financial institutions and clients registered in the given country.

In 2016 again the Bank relied on the country ratings of Moody's to define the country limits. In addition to the above, the Bank has taken into account

- the requirements of Head Office, - the information, macro-economic data published in the press on the given country, - other information, e.g. analyses of economic research institutions, other banks/companies.

The Bank has managed its foreign exposures in such a manner that the country risk should not increase the capital requirement of the Bank.

7. Counterparty risk

From time to time the Bank places its liquid sources with other banks, partly within the BoC Group. In its placements and derivative transactions - short-term FX swaps - the Bank minimizes its counterparty risks primarily through the limit system. The capital requirement of these transactions does not affect significantly the capital adequacy ratio of the Bank.

8. Banking book interest rate risk

For detailed information see chapter “Exposure to interest rate risk on positions not included in the trading book” (CRR Article 448)

9. Liquidity risk

The liquidity risks of the Bank can be primarily assigned to two categories: a) Maturity: a liquidity risk related to a mismatch in maturity dates; b) Structural: a risk related to the opportunity to renew the funds or the change in funding costs.

The fundamental purpose of the Bank is to observe the requirements and guidelines related to its liquidity management, the assurance of the ability to pay at all times (solvency and liquidity). Efficient liquidity management ensures that the Bank has sufficient liquid assets or appropriate access to such assets, in order to fulfill its due payment obligations. In order to ensure the harmony of maturity dates at all times, the Bank applies the limits approved by the Board of Directors.

As a result of a conservative lending policy, the own funds of the Bank provide coverage for a majority of the medium and long-term loans, furthermore, for the investments (a small shareholding in Garantiqa Hitelgarancia Zrt., as well as fixed assets used in the banking operation and welfare assets).

The specific conditions of fund raising are defined by the Asset - Liability Committee of the Bank, in accordance with the development of market conditions.

The purpose of liquidity reserve policy is to ensure that liquid assets of appropriate level should be available for the Bank at all times to cover any unexpected outflow of funds. The Bank is prepared for the appropriate and safe handling of any extraordinary liquidity situation.

- 10 -

II. Identification and measurement of risks, description of the organizational units and functions ensuring their monitoring

The exploration and identification of risks extends to every employee, organizational unit and executive officer of the Bank. If the employees or organizational units of the Bank detect and identify a risk, they are required to start handling it immediately, according to the internal policies.

Corporate Banking Department

In the risk-taking proposals the Department presents the risks of the client, transaction and the system of collaterals, makes proposals for the management and business conditions of the risks. It makes proposals on the rating of the transactions and the recognition of the pertinent impairment/provision, if any in the framework of the monthly and the quarterly reports and qualifications, in coordination with the Risk Management Department

Risk Management Department

Its function is the assessment of proposals and draft contracts on loans, investments and other forms of risk-taking from the aspect of risk management. The Department will submit its findings to the decision-making bodies of the Bank including assessment of the debtor rating, collateral valuation and assessment of transaction rating. It makes proposals on client limits and the financial conditions to be applied in contracts resulting in exposures, for the purpose of risk mitigation. It gives opinion on the risk taking contracts comparing them to the decisions approving the related transactions and validates the contracts after Legal & Compliance Department approved them. It provides opinion for the quarterly and extraordinary ratings of assets and off-balance-sheet items for the decision-making bodies of the Bank, as well as proposals on the measure of impairment and provisions. Should it become necessary, - together with Corporate Banking Department - it would submit proposals for the collection of claims rated doubtful or bad. It would submit proposals for the change of the rating of the related transaction, client, collateral, on the amount of impairment and provision.

It will input the loan agreements into the IT systems after they are signed properly and in line with the internal regulations. It will check and approve the disbursement requests.

It gives its opinion on the establishment of country limits and monitors their utilization.

Banking Department

Ensures that the data of the clients are registered accurately in a timely manner, manages the transactions related to the accounts of the clients and supports the activity of the Compliance Officer.

Internal Audit

It supports the efforts of the Management aimed at risk mitigation by continuously auditing the activities of the Bank.

Administration

Manages any reputational risks, it is involved in the organization of the PR activity of the Bank and the establishment of the technical (non-IT) conditions necessary for the operation of the Bank.

- 11 -

Financial Department

It is among the tasks of the Department to record any losses suffered by the Bank deriving from operational risk (default interest, penalty, fine imposed for failure of compliance, etc.), notifying the relevant managers on any errors, mistakes, so that similar errors could be avoided in the future. Keeping separate records of these data enables the monitoring of the annual changes in operational losses.

Operations Department / Loan Administration

The Department will execute the monetary transactions (bank transfers in HUF and foreign currency) based on the orders of the clients, furthermore, execution of banking - including Treasury - transactions and the prevention of the related risks as best as possible, minimizing the impact of any errors that may have occurred.

Concerning lending operations, it checks and manages the loan disbursements. The Department monitors whether the borrowers comply with the conditions of the loan contract and manages payments between the borrower and the lenders when the Bank is the “Paying Agent”. It is an additional task of the Department to monitor the maturing payment obligations of the debtors, to dispatch the appropriate payment reminders, furthermore, to mail the advices on the completed payments and interest fixing.

IT Department

The Department ensures the operation of the IT systems of the Bank. It has a key role in the measurement of operational risks related to IT applications and in the development of the IT risk management.

Treasury

Treasury manages the liquidity of the Bank and the market risks that may occur.

III. Scope of application of risk measurement and reporting systems

1. Client rating The Bank performs client rating for every client with whom it concludes a risk assumption contract, or who secures risk assumption partially or fully, e.g. by guarantee. The rating may be based on the classification of international credit rating agencies recognized by the Supervisory Authority, or on the rating of the Head Office, or on the internal rating system used by the Bank. The rating category of the client affects the eligibility of the client for lending, his limit, the collateral requirements and the price of risk assumption.

2. Collateral valuation In decision making and then in monitoring the Bank constantly evaluates the collateral provided by the client. The applied coverage ratio takes into account the legal and collection costs that would be incurred in a collection procedure.

3. Rating of the transaction and recognition of impairment, formation of provisions The Bank takes into account the lending, investment and country risks related to the assets by recognizing impairment on the assets and by the reversal thereof, and creates risk provision in order to cover the incurred interest and exchange rate risks, the risks related to off balance sheet liabilities and all other risks.

- 12 -

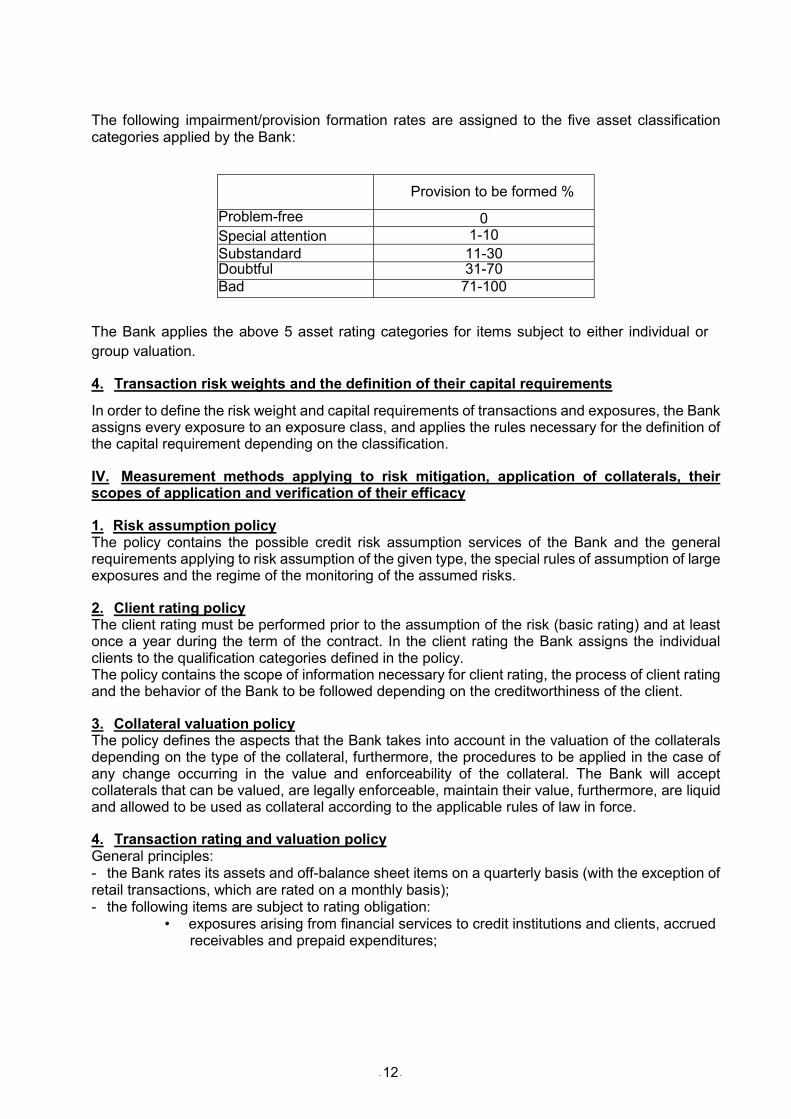

The following impairment/provision formation rates are assigned to the five asset classification categories applied by the Bank:

The Bank applies the above 5 asset rating categories for items subject to either individual or

group valuation.

4. Transaction risk weights and the definition of their capital requirements

In order to define the risk weight and capital requirements of transactions and exposures, the Bank assigns every exposure to an exposure class, and applies the rules necessary for the definition of the capital requirement depending on the classification.

IV. Measurement methods applying to risk mitigation, application of collaterals, their scopes of application and verification of their efficacy

1. Risk assumption policy The policy contains the possible credit risk assumption services of the Bank and the general requirements applying to risk assumption of the given type, the special rules of assumption of large exposures and the regime of the monitoring of the assumed risks.

2. Client rating policy The client rating must be performed prior to the assumption of the risk (basic rating) and at least once a year during the term of the contract. In the client rating the Bank assigns the individual clients to the qualification categories defined in the policy. The policy contains the scope of information necessary for client rating, the process of client rating and the behavior of the Bank to be followed depending on the creditworthiness of the client.

3. Collateral valuation policy The policy defines the aspects that the Bank takes into account in the valuation of the collaterals depending on the type of the collateral, furthermore, the procedures to be applied in the case of any change occurring in the value and enforceability of the collateral. The Bank will accept collaterals that can be valued, are legally enforceable, maintain their value, furthermore, are liquid and allowed to be used as collateral according to the applicable rules of law in force.

4. Transaction rating and valuation policy General principles: - the Bank rates its assets and off-balance sheet items on a quarterly basis (with the exception of retail transactions, which are rated on a monthly basis); - the following items are subject to rating obligation:

• exposures arising from financial services to credit institutions and clients, accrued receivables and prepaid expenditures;

Provision to be formed %

Problem-free 0 Special attention 1-10

Substandard 11-30 Doubtful 31-70 Bad 71-100

- 13 -

• investments, securities (hereinafter: investments), • contingent and certain (future) liabilities (hereinafter: off-balance-sheet liabilities).

5. Impairment recognition and provision calculation policy Based on the rating of the transaction and the assets, by assigning to the appropriate asset rating category and rating group, impairment must be recognized on securities, investments, receivables and other assets. Provisions must also be formed on the contingent and future obligations listed in legal stipulations regulating the bookkeeping of credit institutions. If it becomes necessary, the Bank will determine the recognition of the impairment or reversal based on individual or group assessment, as well as the formation, reversal or use of the provision.

V. Application of prudential rules

Taking into account that Bank of China Srbija started its operation in January 2017 only, therefore the Bank doesn’t prepare consolidated financial statements for year 2016, because its standalone financial statements give a true and fair view of the equity and financial position of the Bank.

The Bank does not apply credit derivatives. The Bank does not apply netting arrangements. The Bank has no items with particularly high risk within the meaning of Article 128 of CRR,

at the same time, according to the recommendation of the National Bank of Hungary, in the calculation of the capital requirement for Pillar II it has set aside additional capital on bullet type transactions and FX loans.

The Bank is not engaged in securitization or security-based transactions (with the exception of the purchase of government securities in HUF).

Information regarding governance arrangements (CRR Article 435 section 2)

At the end of 2016 the governing body of the Bank (the Board of Directors) consisted of 5 persons. One of them was member of the board at another joint stock company and was managing director of a limited liability company however these positions do not result in conflict of interest. Other two Board members are in management position in Bank of China Limited Hungarian Branch.

The policy on the selection of members of the governing body is based on the skills, talents and experiences of the members, i.e. at least one university degree, 15 years of relevant experiences in the banking sector or at an appropriate financial institution are required, the candidate must be familiar with risk management at banks, understand and be capable of implementing the business strategy of the Bank, a good command of the English language and advanced user level computer skills are also required.

In the selection of members of the governing body, apart from the professional aspects the following circumstances are also important: the Board of Directors should have both Chinese and non-Chinese members, furthermore, external and internal members are also required in order to ensure diversity among members of the body. At the end of year 2016 the Board of Directors had two Chinese and three Hungarian members, while the number of internal directors was two and the number of external members was three.

A risk management committee is operating in the Bank, which assesses matters of strategic importance and this committee met four times in 2016.

- 14 -

The Board of Directors had four meetings in 2016 and the Supervisory Board had five.

Proposals are made for such meetings related to the items on the agenda. The various organizational units (Corporate Banking Department, Risk Management Department, Financial Department, etc.) keep the internal members of the Board of Directors informed - on a daily, weekly, monthly basis - in tabular and textual form, in addition to the reports sent to the Supervisory Authority and to the Owner. Scopes of application (CRR article 436)

The Bank is under no obligation of consolidation for prudential purposes. There is only one company where the Bank has an investment (HUF 10 Million) subject to accounting consolidation: Garantiqa Hitelgarancia Zrt. Data disclosed herewith contain information on both the Bank’s activity in Hungary and data on the activity of Prague Branch and Vienna Branch.

The Bank deducted capital equal to 10 % of CET1 of the investment into the Serbian subsidiary from the own funds.

There are no significant practical or legal, current or predictable impediments to the instant transfer of own funds or to the repayment of the liabilities between the mother company and the subsidiaries.

- 15 -

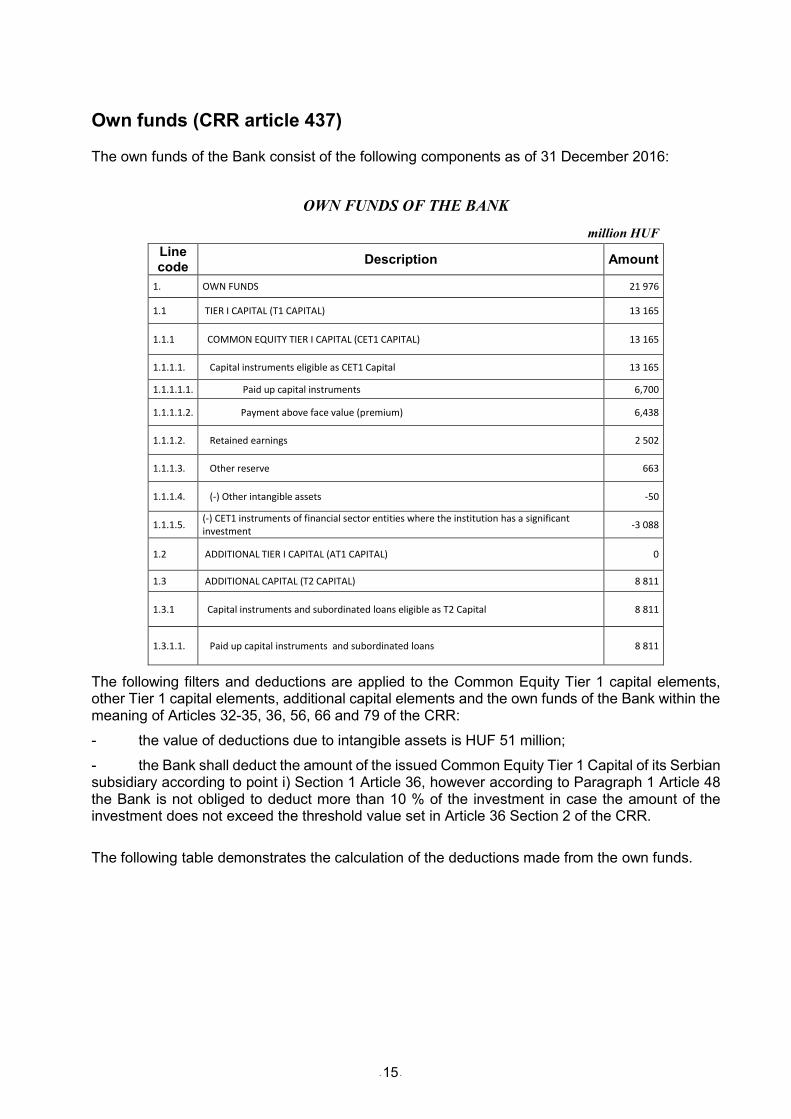

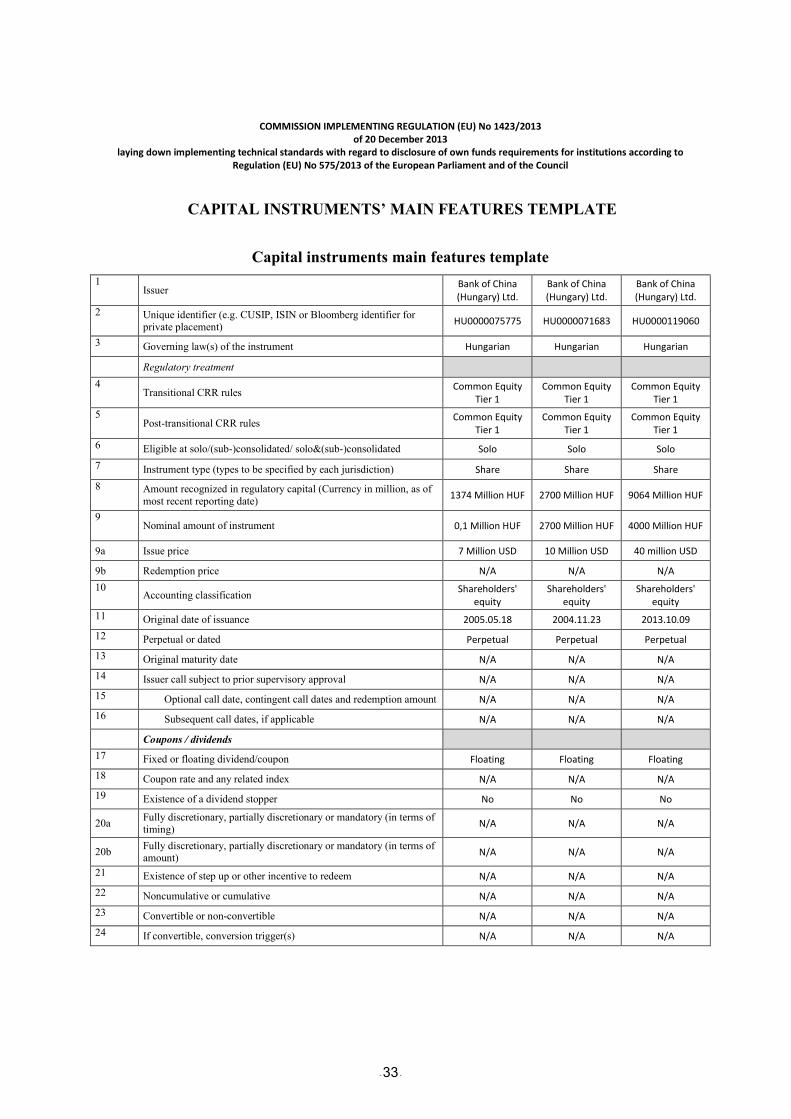

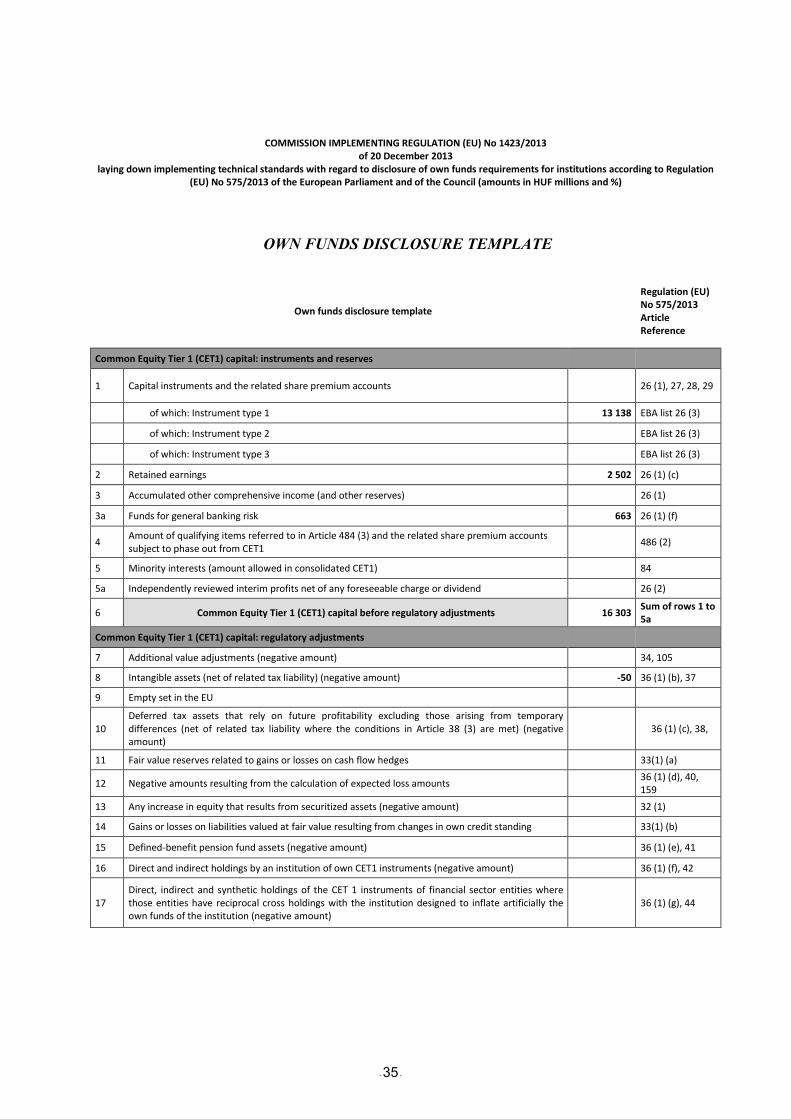

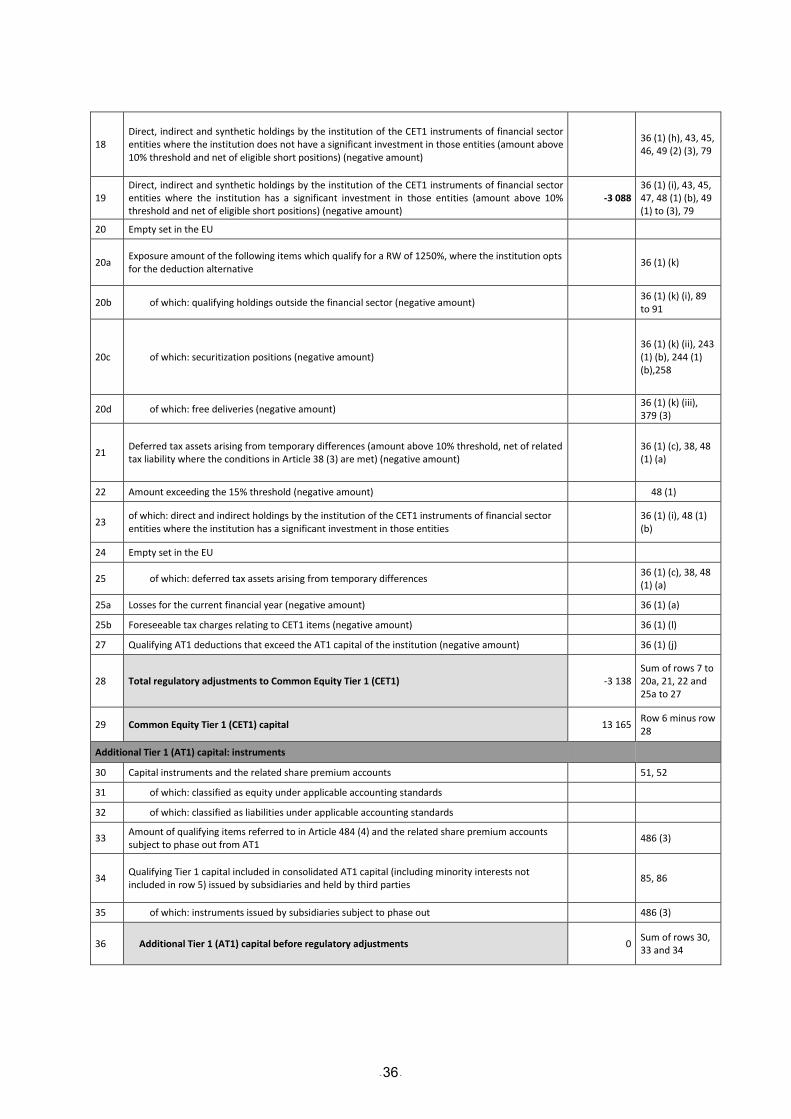

Own funds (CRR article 437)

The own funds of the Bank consist of the following components as of 31 December 2016:

OWN FUNDS OF THE BANK

million HUF

Line code

Description Amount

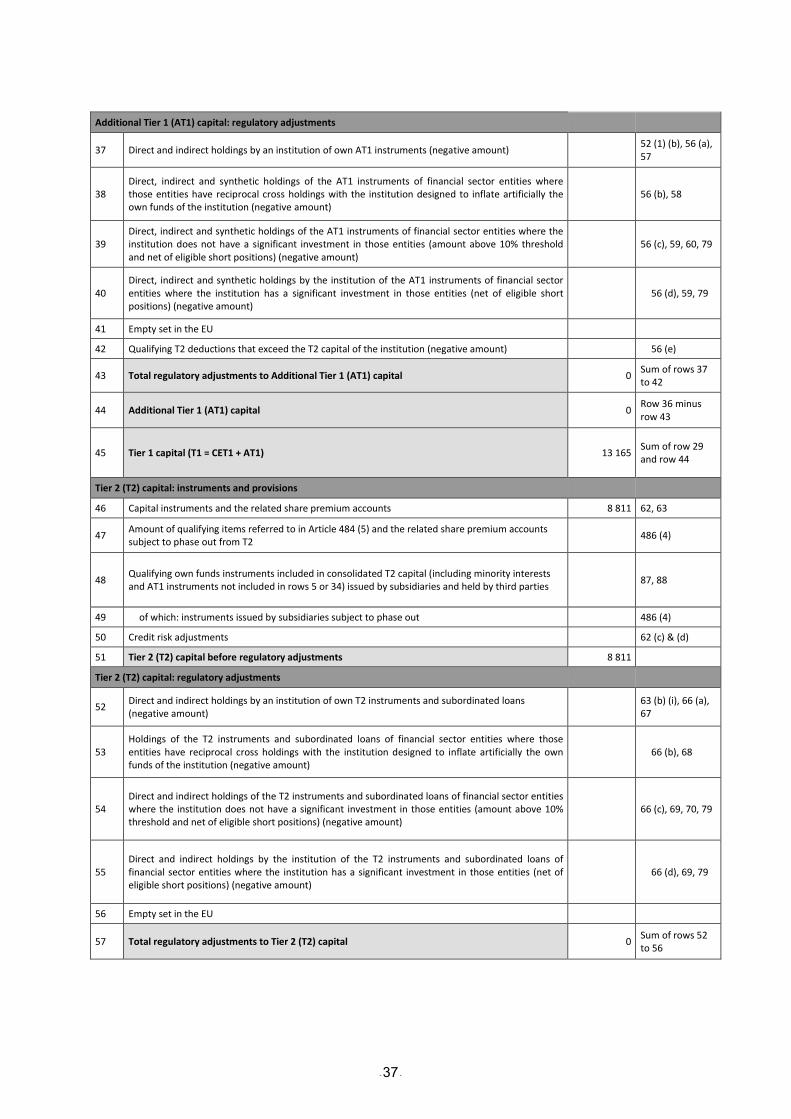

1. OWN FUNDS 21 976

1.1 TIER I CAPITAL (T1 CAPITAL) 13 165

1.1.1 COMMON EQUITY TIER I CAPITAL (CET1 CAPITAL) 13 165

1.1.1.1. Capital instruments eligible as CET1 Capital 13 165

1.1.1.1.1. Paid up capital instruments 6,700

1.1.1.1.2. Payment above face value (premium) 6,438

1.1.1.2. Retained earnings 2 502

1.1.1.3. Other reserve 663

1.1.1.4. (-) Other intangible assets -50

1.1.1.5. (-) CET1 instruments of financial sector entities where the institution has a significant investment

-3 088

1.2 ADDITIONAL TIER I CAPITAL (AT1 CAPITAL) 0

1.3 ADDITIONAL CAPITAL (T2 CAPITAL) 8 811

1.3.1 Capital instruments and subordinated loans eligible as T2 Capital 8 811

1.3.1.1. Paid up capital instruments and subordinated loans 8 811

The following filters and deductions are applied to the Common Equity Tier 1 capital elements, other Tier 1 capital elements, additional capital elements and the own funds of the Bank within the meaning of Articles 32-35, 36, 56, 66 and 79 of the CRR:

- the value of deductions due to intangible assets is HUF 51 million;

- the Bank shall deduct the amount of the issued Common Equity Tier 1 Capital of its Serbian subsidiary according to point i) Section 1 Article 36, however according to Paragraph 1 Article 48 the Bank is not obliged to deduct more than 10 % of the investment in case the amount of the investment does not exceed the threshold value set in Article 36 Section 2 of the CRR.

The following table demonstrates the calculation of the deductions made from the own funds.

- 16 -

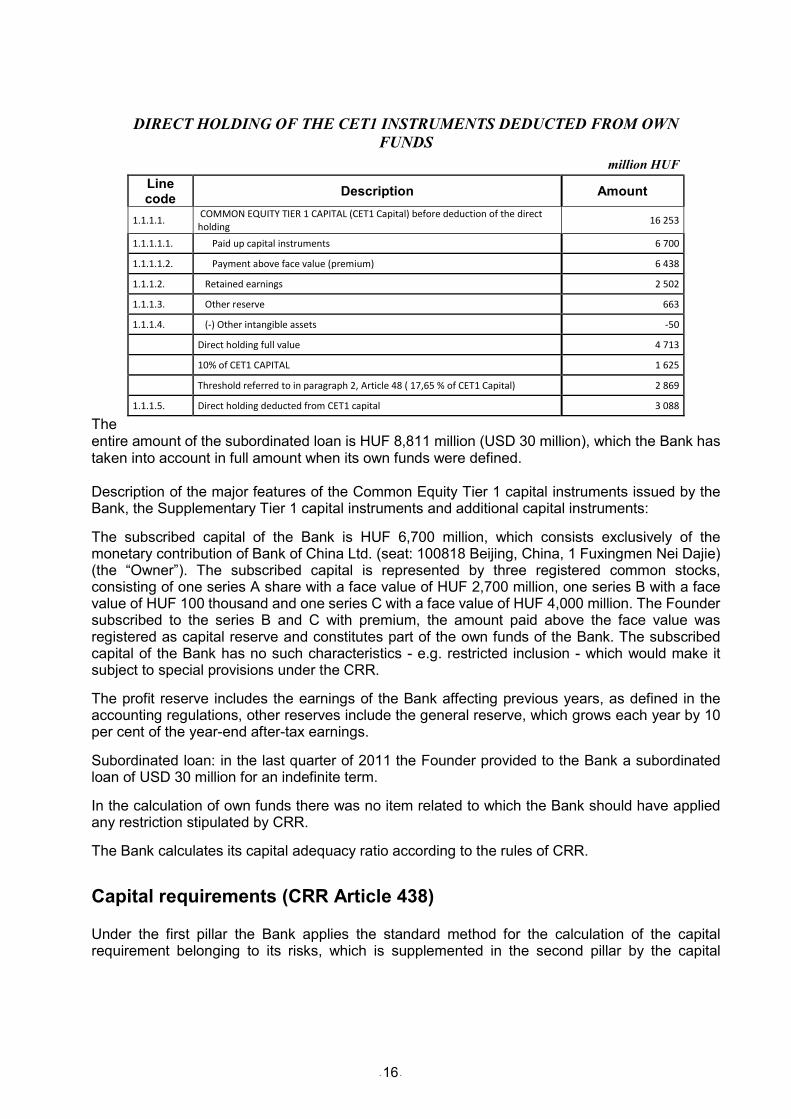

The entire amount of the subordinated loan is HUF 8,811 million (USD 30 million), which the Bank has taken into account in full amount when its own funds were defined. Description of the major features of the Common Equity Tier 1 capital instruments issued by the Bank, the Supplementary Tier 1 capital instruments and additional capital instruments:

The subscribed capital of the Bank is HUF 6,700 million, which consists exclusively of the monetary contribution of Bank of China Ltd. (seat: 100818 Beijing, China, 1 Fuxingmen Nei Dajie) (the “Owner”). The subscribed capital is represented by three registered common stocks, consisting of one series A share with a face value of HUF 2,700 million, one series B with a face value of HUF 100 thousand and one series C with a face value of HUF 4,000 million. The Founder subscribed to the series B and C with premium, the amount paid above the face value was registered as capital reserve and constitutes part of the own funds of the Bank. The subscribed capital of the Bank has no such characteristics - e.g. restricted inclusion - which would make it subject to special provisions under the CRR.

The profit reserve includes the earnings of the Bank affecting previous years, as defined in the accounting regulations, other reserves include the general reserve, which grows each year by 10 per cent of the year-end after-tax earnings.

Subordinated loan: in the last quarter of 2011 the Founder provided to the Bank a subordinated loan of USD 30 million for an indefinite term.

In the calculation of own funds there was no item related to which the Bank should have applied any restriction stipulated by CRR.

The Bank calculates its capital adequacy ratio according to the rules of CRR.

Capital requirements (CRR Article 438)

Under the first pillar the Bank applies the standard method for the calculation of the capital requirement belonging to its risks, which is supplemented in the second pillar by the capital

DIRECT HOLDING OF THE CET1 INSTRUMENTS DEDUCTED FROM OWN FUNDS

million HUF

Line code

Description Amount

1.1.1.1. COMMON EQUITY TIER 1 CAPITAL (CET1 Capital) before deduction of the direct holding

16 253

1.1.1.1.1. Paid up capital instruments 6 700

1.1.1.1.2. Payment above face value (premium) 6 438

1.1.1.2. Retained earnings 2 502

1.1.1.3. Other reserve 663

1.1.1.4. (-) Other intangible assets -50

Direct holding full value 4 713

10% of CET1 CAPITAL 1 625

Threshold referred to in paragraph 2, Article 48 ( 17,65 % of CET1 Capital) 2 869

1.1.1.5. Direct holding deducted from CET1 capital 3 088

- 17 -

requirement calculated for additional risks according to the principle of building blocks. In that framework it provides sufficient capital for the country risks. Generally, the Bank assumes significant risks in countries belonging to investment category. The concentration risk is relatively significant, however, settlement risk and reputation risk are low. Since its establishment, the Bank has not obtained actual figures for the measurement of the residual risks, since each debtor has fulfilled the obligations according to schedule, therefore no collateral had to be enforced. When performing its fund raising and lending activities, the Bank strives to keep the applied interest bases and re-pricing periods in harmony, therefore at the Bank it is sufficient to set aside only a small amount of additional capital to cover interest rate risks. Thanks to the short re-pricing periods, the stress tests quantify a low risk exposure. The Bank keeps its open FX positions low and by the application of the stress tests developed and prescribed by the Supervisory Authority it continuously measures the losses to be anticipated in the case of any extreme movement of FX rates. Owing to the low open positions, the stress tests imply low potential losses. With regard to the characteristics of the Bank, i.e.:

- its own funds constitute 16% of the balance sheet total, and

- the liquidity position of the parent bank is extremely strong,

the liquidity risk of the Bank is negligible, therefore at the Bank it would not be justified to set aside

a significant amount of additional capital to cover this risk.

The strategic decisions are approved by the Owner therefore the Bank does not set aside any

separate additional capital for strategic risks.

The Bank generates a capital buffer for the risks, which are difficult to quantify (e.g. reputational risk), among others.

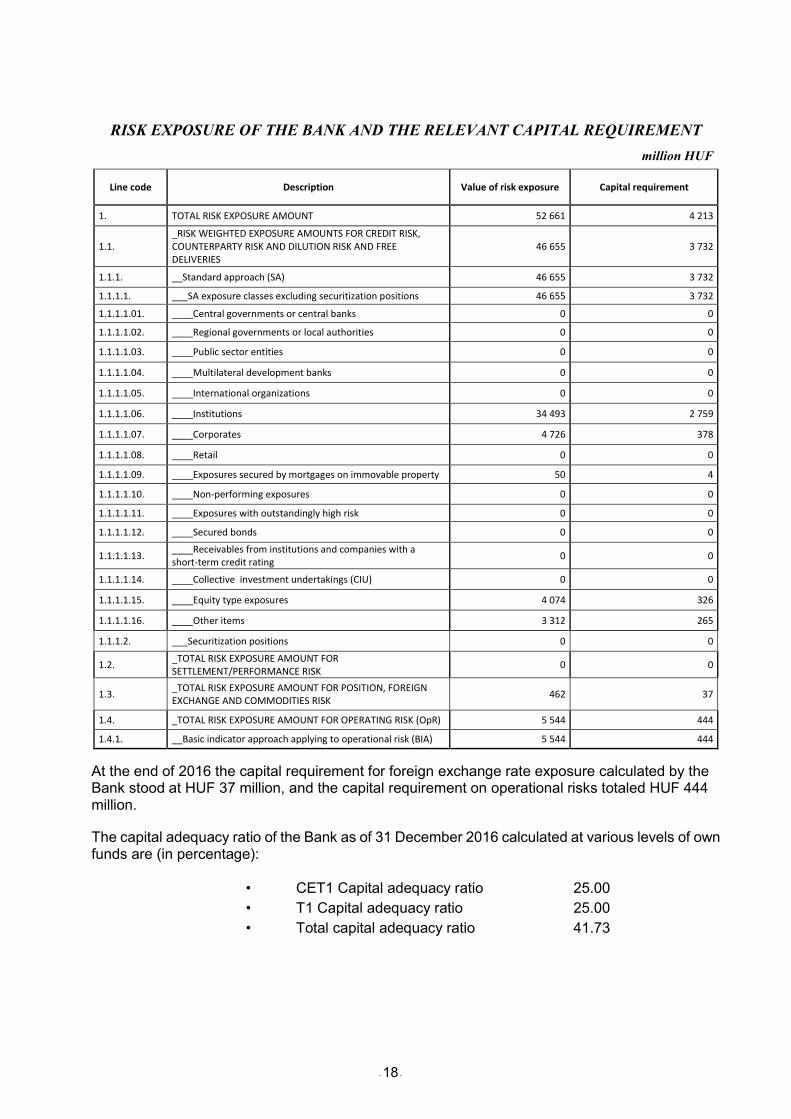

The risk management system applied by the Bank is suitable and appropriate for the definition, quantification, management and monitoring of all the major risks. The exposure values belonging to the individual exposure classes defined in Article 112 of CRR, weighted by risk and the appropriate capital requirement calculated at 8 per cent are illustrated by the following table:

- 18 -

RISK EXPOSURE OF THE BANK AND THE RELEVANT CAPITAL REQUIREMENT

million HUF

Line code Description Value of risk exposure Capital requirement

1. TOTAL RISK EXPOSURE AMOUNT 52 661 4 213

1.1. _RISK WEIGHTED EXPOSURE AMOUNTS FOR CREDIT RISK, COUNTERPARTY RISK AND DILUTION RISK AND FREE DELIVERIES

46 655 3 732

1.1.1. __Standard approach (SA) 46 655 3 732

1.1.1.1. ___SA exposure classes excluding securitization positions 46 655 3 732

1.1.1.1.01. ____Central governments or central banks 0 0

1.1.1.1.02. ____Regional governments or local authorities 0 0

1.1.1.1.03. ____Public sector entities 0 0

1.1.1.1.04. ____Multilateral development banks 0 0

1.1.1.1.05. ____International organizations 0 0

1.1.1.1.06. ____Institutions 34 493 2 759

1.1.1.1.07. ____Corporates 4 726 378

1.1.1.1.08. ____Retail 0 0

1.1.1.1.09. ____Exposures secured by mortgages on immovable property 50 4

1.1.1.1.10. ____Non-performing exposures 0 0

1.1.1.1.11. ____Exposures with outstandingly high risk 0 0

1.1.1.1.12. ____Secured bonds 0 0

1.1.1.1.13. ____Receivables from institutions and companies with a short-term credit rating

0 0

1.1.1.1.14. ____Collective investment undertakings (CIU) 0 0

1.1.1.1.15. ____Equity type exposures 4 074 326

1.1.1.1.16. ____Other items 3 312 265

1.1.1.2. ___Securitization positions 0 0

1.2. _TOTAL RISK EXPOSURE AMOUNT FOR SETTLEMENT/PERFORMANCE RISK

0 0

1.3. _TOTAL RISK EXPOSURE AMOUNT FOR POSITION, FOREIGN EXCHANGE AND COMMODITIES RISK

462 37

1.4. _TOTAL RISK EXPOSURE AMOUNT FOR OPERATING RISK (OpR) 5 544 444

1.4.1. __Basic indicator approach applying to operational risk (BIA) 5 544 444

At the end of 2016 the capital requirement for foreign exchange rate exposure calculated by the Bank stood at HUF 37 million, and the capital requirement on operational risks totaled HUF 444 million.

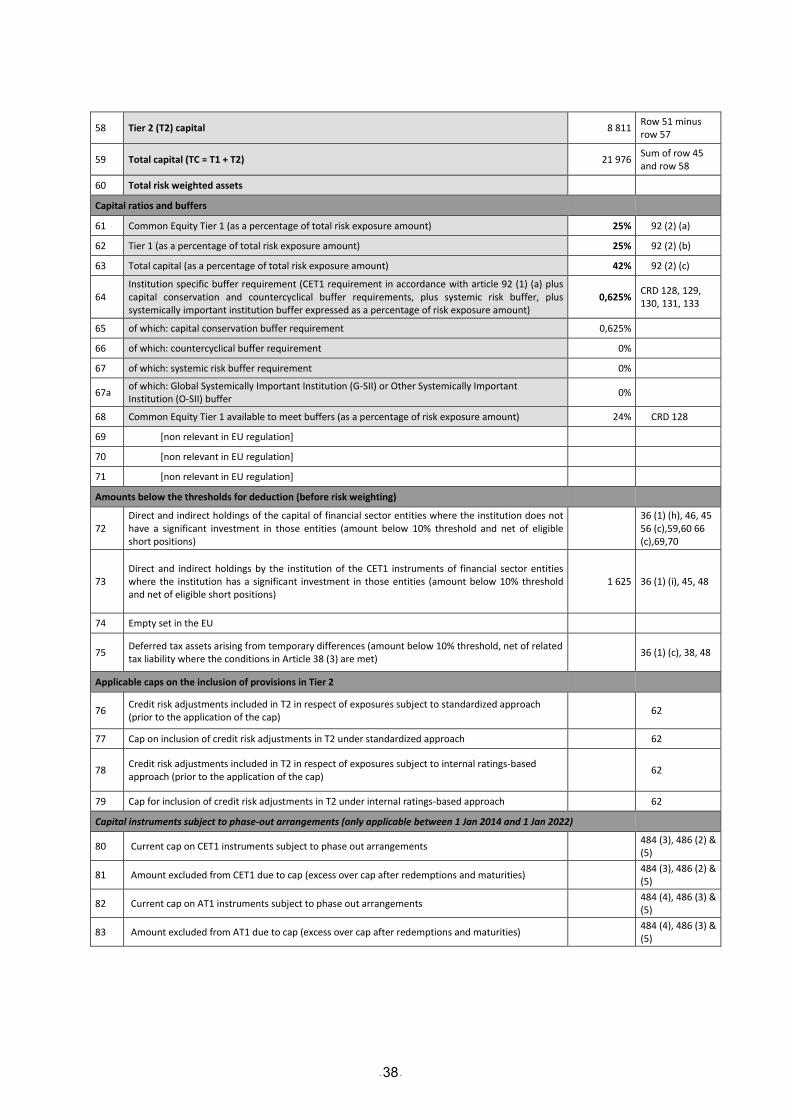

The capital adequacy ratio of the Bank as of 31 December 2016 calculated at various levels of own funds are (in percentage):

• CET1 Capital adequacy ratio 25.00

• T1 Capital adequacy ratio 25.00

• Total capital adequacy ratio 41.73

- 19 -

Exposure to counterparty credit risk (CRR Article 439)

As at 31 December 2016 the Bank did not have any transactions for which the counterparty risk within the meaning of the CRR would have to be calculated.

From time to time the Bank places its liquid sources for short periods with other banks, partly within

the BoC Group. In its placements and derivative transactions - short-term FX swaps - the Bank

minimizes its counterparty risks primarily through the limit system. The capital requirement of these

transactions does not significantly affect the capital adequacy ratio of the Bank.

Capital buffers (CRR Article 440)

As at 31 December 2015 the Bank had no such exposure for which it would have created capital buffer due to its geographical location. The Bank was not qualified as significant financial institution neither globally, nor otherwise therefore it was not required to meet capital buffer requirements under the applicable rules of law in force.

The Bank created a capital conservation being 0.625 % of its total risk exposures amounting to HUF 329 M.

Indicators of global systemic importance (CRR 441)

The Bank was not qualified as a significant institution at global systemic level.

Credit risk adjustments, past due and impaired exposures (CRR Article 442)

The loan portfolio of the Bank is problem-free, the clients have had no overdue obligations to the Bank so far and therefore the Bank did not recognize any impairment concerning its exposures in 2016 either, similarly to previous years.

The Bank regulates in its internal policies the handling of any problems related to possible late

payment by the client and deterioration of the quality of the exposures.

Based on the applicable rules of law in force, the Bank considers the non-performance of the client

a fact if either or both of the following events have taken place:

• Based on its information, the Bank believes that the client will not fully meet its loan obligations to the Bank, unless the Bank applies recourse in order to enforce the collateral.

• The client is in delay with meeting a material loan obligation to the Bank continuously for 90 days.

In the case of corporate customers the Bank considers the higher of the following two values as the

threshold value of materiality:

• the HUF equivalent of CNY 5,500, • 2% of the exposure.

Although the Bank is primarily involved in corporate lending, in case of retail clients the Bank

- 20 -

considers the higher of the following two values as the threshold value of materiality:

• the lowest monthly minimum wage applicable at the time of falling in delay, • the installment for one month.

Based on the quarterly rating of the debtor, impairment must be recognized between the book

value of the exposure and the expected return on it, as a loss type outstanding amount (impaired

receivable).

The Bank takes into account in the profit and loss account the lending, investment and country

risks events related to the assets by the impairment recognized on the assets and by the reversal

thereof, and forms a risk provision in order to cover the incurred interest and exchange rate risks,

the risks related to off balance sheet liabilities and all other risks.

The Bank applies, for items both subject to individual and group assessment, the five

asset-rating categories (problem-free, special mention, substandard, doubtful, bad) mentioned in

the Risk management objectives and policies (CRR Article 435), Part III section 3.

In individual assessment the Bank primarily considers the following aspects:

• client rating: the financial situation, stability, revenue-generating capability of the client • adherence to the repayment schedule: any delays that occurred in the repayment of the

outstanding debt • the country risk related to the client • value and availability of the collaterals and how easily they can be mobilized • the opportunity to resell, mobilize the item • future payment obligations arising from the item and generating losses and changes of the

above.

As mentioned earlier, the Bank is primarily involved in corporate lending. The Bank rates the

retail loans in groups, provided they are rated as small amount exposures according to the

accounting policy of the Bank. Exposures subject to group rating are classified by a simplified

rating process into rating groups, the basis of which is compliance with the repayment schedule.

The Bank has no purchased receivables deriving from expired exposures therefore it does not assess any dilution risk.

- 21 -

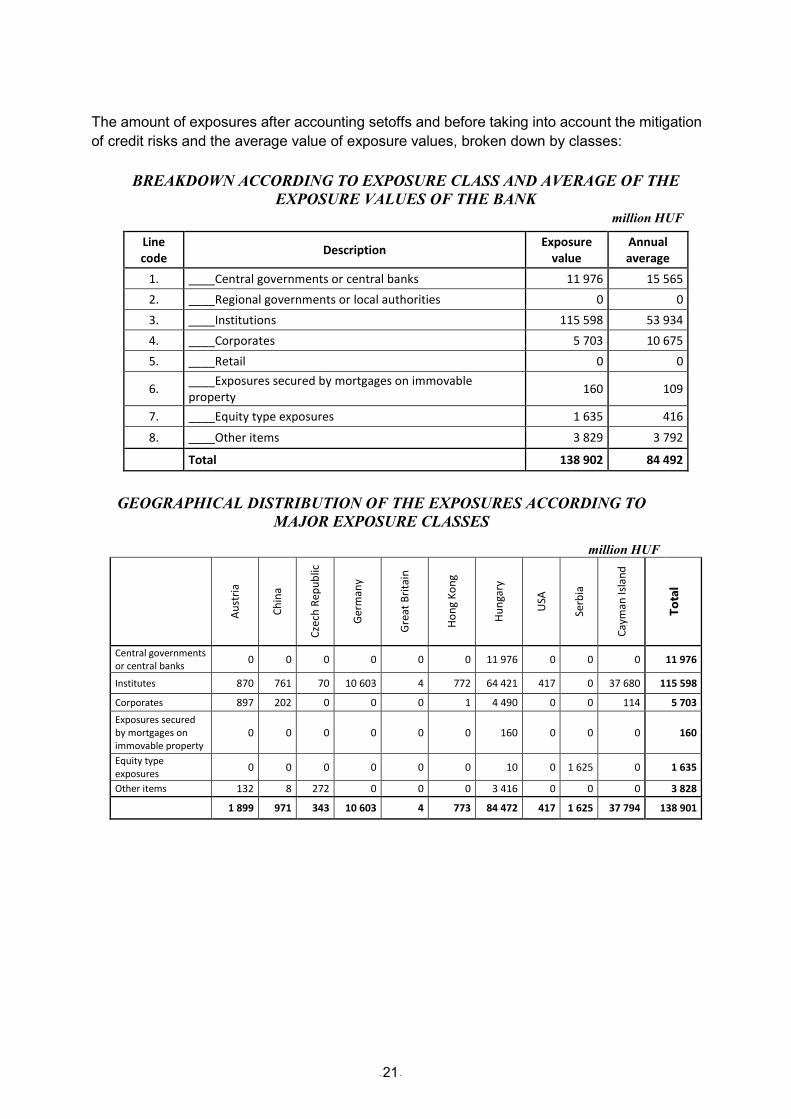

The amount of exposures after accounting setoffs and before taking into account the mitigation

of credit risks and the average value of exposure values, broken down by classes:

BREAKDOWN ACCORDING TO EXPOSURE CLASS AND AVERAGE OF THE EXPOSURE VALUES OF THE BANK

million HUF

Line code

Description Exposure

value Annual average

1. ____Central governments or central banks 11 976 15 565

2. ____Regional governments or local authorities 0 0

3. ____Institutions 115 598 53 934

4. ____Corporates 5 703 10 675

5. ____Retail 0 0

6. ____Exposures secured by mortgages on immovable property

160 109

7. ____Equity type exposures 1 635 416

8. ____Other items 3 829 3 792

Total 138 902 84 492

GEOGRAPHICAL DISTRIBUTION OF THE EXPOSURES ACCORDING TO MAJOR EXPOSURE CLASSES

million HUF

Au

stri

a

Ch

ina

Cze

ch R

epu

blic

Ger

man

y

Gre

at B

rita

in

Ho

ng

Ko

ng

Hu

nga

ry

USA

Serb

ia

Cay

man

Isla

nd

To

tal

Central governments or central banks

0 0 0 0 0 0 11 976 0 0 0 11 976

Institutes 870 761 70 10 603 4 772 64 421 417 0 37 680 115 598

Corporates 897 202 0 0 0 1 4 490 0 0 114 5 703

Exposures secured by mortgages on immovable property

0 0 0 0 0 0 160 0 0 0 160

Equity type exposures

0 0 0 0 0 0 10 0 1 625 0 1 635

Other items 132 8 272 0 0 0 3 416 0 0 0 3 828

1 899 971 343 10 603 4 773 84 472 417 1 625 37 794 138 901

- 22 -

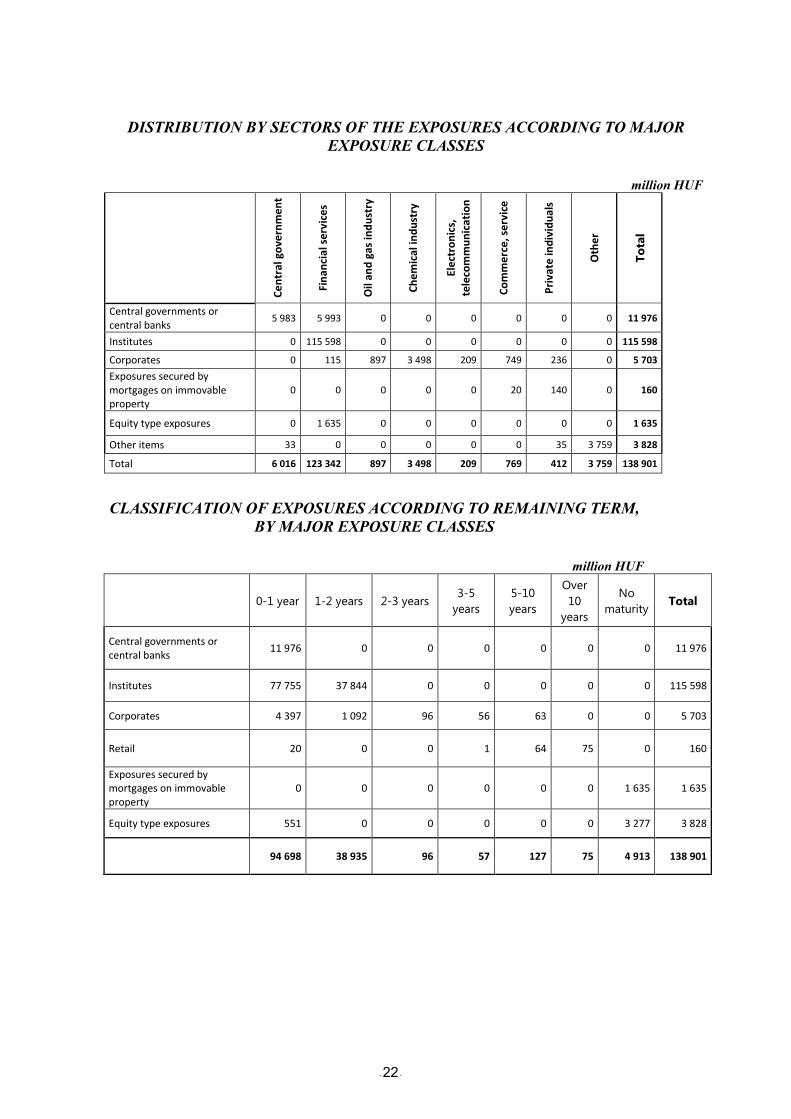

DISTRIBUTION BY SECTORS OF THE EXPOSURES ACCORDING TO MAJOR EXPOSURE CLASSES

million HUF

Ce

ntr

al g

ove

rnm

en

t

Fin

anci

al s

erv

ice

s

Oil

and

gas

ind

ust

ry

Ch

em

ical

ind

ust

ry

Ele

ctro

nic

s,

tele

com

mu

nic

atio

n

Co

mm

erc

e, s

erv

ice

Pri

vate

ind

ivid

ual

s

Oth

er

To

tal

Central governments or central banks

5 983 5 993 0 0 0 0 0 0 11 976

Institutes 0 115 598 0 0 0 0 0 0 115 598

Corporates 0 115 897 3 498 209 749 236 0 5 703

Exposures secured by mortgages on immovable property

0 0 0 0 0 20 140 0 160

Equity type exposures 0 1 635 0 0 0 0 0 0 1 635

Other items 33 0 0 0 0 0 35 3 759 3 828

Total 6 016 123 342 897 3 498 209 769 412 3 759 138 901

CLASSIFICATION OF EXPOSURES ACCORDING TO REMAINING TERM, BY MAJOR EXPOSURE CLASSES

million HUF

0-1 year 1-2 years 2-3 years 3-5

years

5-10

years

Over

10

years

No

maturity Total

Central governments or central banks

11 976 0 0 0 0 0 0 11 976

Institutes 77 755 37 844 0 0 0 0 0 115 598

Corporates 4 397 1 092 96 56 63 0 0 5 703

Retail 20 0 0 1 64 75 0 160

Exposures secured by mortgages on immovable property

0 0 0 0 0 0 1 635 1 635

Equity type exposures 551 0 0 0 0 0 3 277 3 828

94 698 38 935 96 57 127 75 4 913 138 901

- 23 -

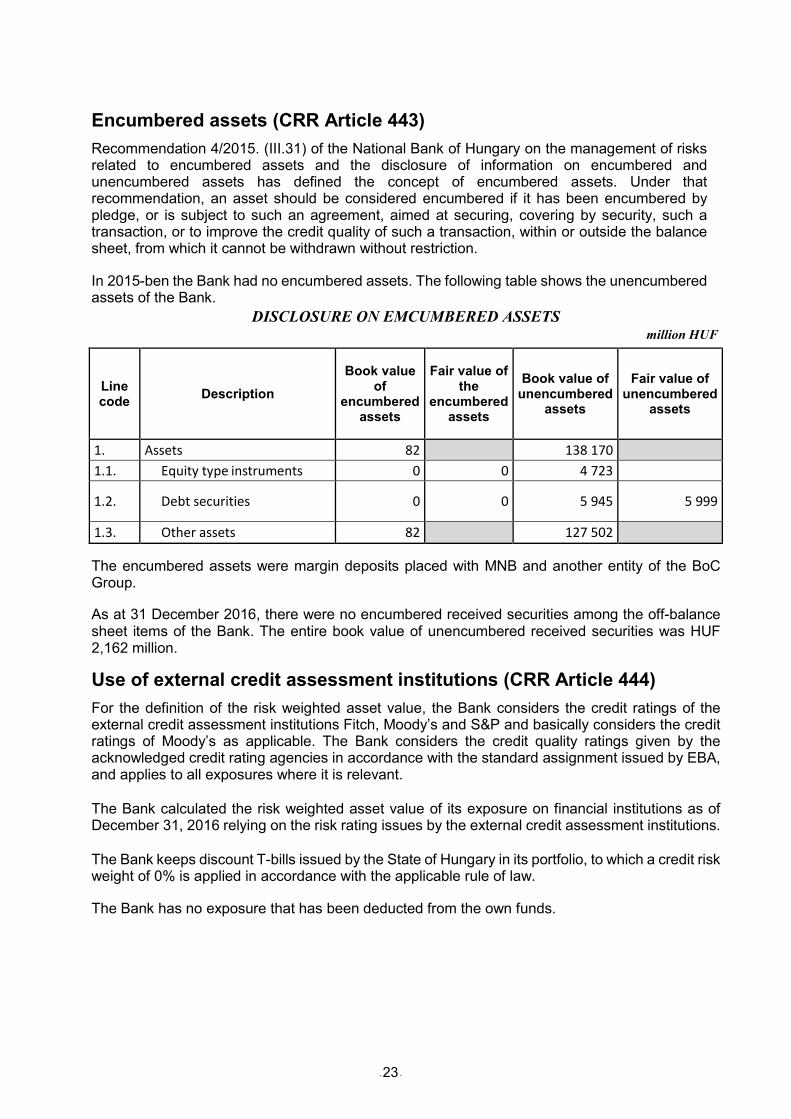

Encumbered assets (CRR Article 443)

Recommendation 4/2015. (III.31) of the National Bank of Hungary on the management of risks related to encumbered assets and the disclosure of information on encumbered and unencumbered assets has defined the concept of encumbered assets. Under that recommendation, an asset should be considered encumbered if it has been encumbered by pledge, or is subject to such an agreement, aimed at securing, covering by security, such a transaction, or to improve the credit quality of such a transaction, within or outside the balance sheet, from which it cannot be withdrawn without restriction.

In 2015-ben the Bank had no encumbered assets. The following table shows the unencumbered assets of the Bank.

DISCLOSURE ON EMCUMBERED ASSETS million HUF

Line code

Description

Book value of

encumbered assets

Fair value of the

encumbered assets

Book value of unencumbered

assets

Fair value of unencumbered

assets

1. Assets 82 138 170

1.1. Equity type instruments 0 0 4 723

1.2. Debt securities 0 0 5 945 5 999

1.3. Other assets 82 127 502

The encumbered assets were margin deposits placed with MNB and another entity of the BoC Group.

As at 31 December 2016, there were no encumbered received securities among the off-balance sheet items of the Bank. The entire book value of unencumbered received securities was HUF 2,162 million.

Use of external credit assessment institutions (CRR Article 444)

For the definition of the risk weighted asset value, the Bank considers the credit ratings of the external credit assessment institutions Fitch, Moody’s and S&P and basically considers the credit ratings of Moody’s as applicable. The Bank considers the credit quality ratings given by the acknowledged credit rating agencies in accordance with the standard assignment issued by EBA, and applies to all exposures where it is relevant.

The Bank calculated the risk weighted asset value of its exposure on financial institutions as of December 31, 2016 relying on the risk rating issues by the external credit assessment institutions.

The Bank keeps discount T-bills issued by the State of Hungary in its portfolio, to which a credit risk weight of 0% is applied in accordance with the applicable rule of law.

The Bank has no exposure that has been deducted from the own funds.

- 24 -

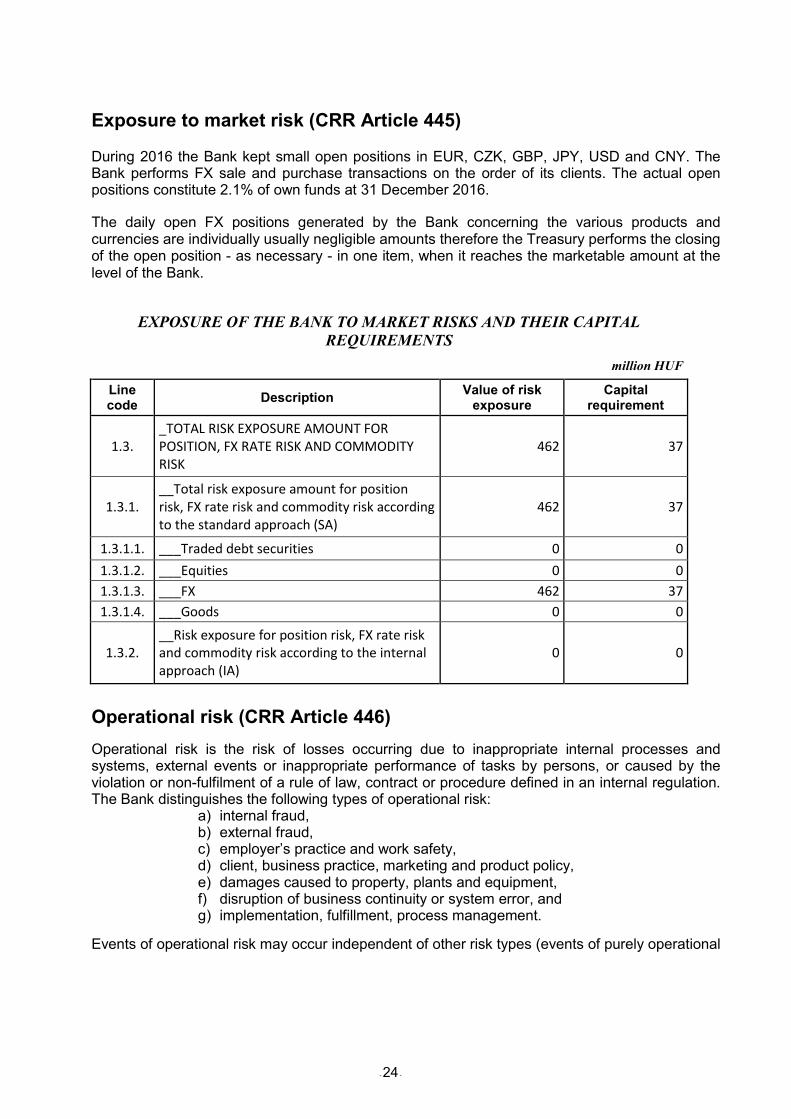

Exposure to market risk (CRR Article 445)

During 2016 the Bank kept small open positions in EUR, CZK, GBP, JPY, USD and CNY. The Bank performs FX sale and purchase transactions on the order of its clients. The actual open positions constitute 2.1% of own funds at 31 December 2016.

The daily open FX positions generated by the Bank concerning the various products and currencies are individually usually negligible amounts therefore the Treasury performs the closing of the open position - as necessary - in one item, when it reaches the marketable amount at the level of the Bank.

EXPOSURE OF THE BANK TO MARKET RISKS AND THEIR CAPITAL REQUIREMENTS

million HUF

Line code

Description Value of risk

exposure Capital

requirement

1.3. _TOTAL RISK EXPOSURE AMOUNT FOR POSITION, FX RATE RISK AND COMMODITY RISK

462 37

1.3.1. __Total risk exposure amount for position risk, FX rate risk and commodity risk according to the standard approach (SA)

462 37

1.3.1.1. ___Traded debt securities 0 0

1.3.1.2. ___Equities 0 0

1.3.1.3. ___FX 462 37

1.3.1.4. ___Goods 0 0

1.3.2. __Risk exposure for position risk, FX rate risk and commodity risk according to the internal approach (IA)

0 0

Operational risk (CRR Article 446)

Operational risk is the risk of losses occurring due to inappropriate internal processes and systems, external events or inappropriate performance of tasks by persons, or caused by the violation or non-fulfilment of a rule of law, contract or procedure defined in an internal regulation. The Bank distinguishes the following types of operational risk:

a) internal fraud, b) external fraud, c) employer’s practice and work safety, d) client, business practice, marketing and product policy, e) damages caused to property, plants and equipment, f) disruption of business continuity or system error, and g) implementation, fulfillment, process management.

Events of operational risk may occur independent of other risk types (events of purely operational

- 25 -

risk) or related to these. In respect of operational risks the Bank defines the capital requirement according to the basic indicator approach, for the coverage of which it set aside HUF 444 million on 31 December 2016.

The operative risk management of the Bank follows the principle of comprehensive control, adjustment in time, cost-benefit and accountability.

- Comprehensive control: in an effort to minimize the losses deriving from operational risks, operational risk management must cover every business process, department and function of the Bank, and its implementation is the obligation of every employee.

- Adjustment in time: in the case of changes in the internal environment (changes in the business strategy and policies of the Bank) or in the external environment (laws, directives, policies), the management of operational risk must be simultaneously adjusted appropriately, or developed.

- Cost – benefit principle: the steps of operational risk management must be determined according to the size of business operations, their complexity and functions, and they must be optimized in order to make the business aims reachable with reasonable amount of risk management costs and tolerable operational risk losses.

- Accountability: an appointed person is responsible for every phase of the operating processes. Primarily the managers of the organizational units are responsible for the management of the operational risks belonging to their departments, and they are entitled to investigate whether the person responsible for the violation of the rules on operational risks can be called to account and they will report every problem case to the general manager.

Every organizational unit of the Bank monitors, evaluates and manages any disturbances, operational risks occurring within its own scope of activities and prepares and updates the process regulations, administrative rules and internal policies. The accounting function of the Bank collects, records and evaluates operational risks, data on losses in the entire the Bank.

By assessing the risk levels of the processes, the Bank defines what are the risks carried by any given process and what are the quantified losses of that might be caused by the possible deficiencies in the given process. The Bank will also define to what extent the embedded controls into the processes or any other checks and measures may prevent or mitigate those losses.

It is an important feature of operational risks that they only partially derive from contracts concluded by the Bank (among others for procurements), to a large extent exposure to such risks is a fact, so the Bank also identifies them and makes an effort to manage them. However, where the source of the operational risk is a contract concluded by the Bank, the possible risks must be identified already in the stage of preparing the contract, and they must be excluded in the contract in consideration of the cost-benefit principle. The means for that is the accurate specification of the requirements prior to signing the contract. The definition and implementation of minimum service levels promotes the application of the cost-benefit principle.

This principle must be applied in the preparation of every major contract, including procurement processes, as well. Tendering and asking for offers from several suppliers will help to find the one who meets best the demand specification. The means to mitigate the risks inherent in procured assets is to agree on warranty and damage compensation obligations concerning the suppliers in the procurement agreements.

Business continuity plans are prepared for the most important processes.

- 26 -

The process of data collection related to operational risk

If any organizational unit detects operational deficiencies, disturbances, losses, it is required to record these and report them in an ad hoc note addressed to the general manager. The Accounting function will check and summarize the data on the quantifiable losses. If necessary, the general manager will notify the Board of Directors of the Bank on any losses related to operational risk and the steps that have been taken or are to be taken.

In the reporting period the Bank did not suffer any meaningful operating losses.

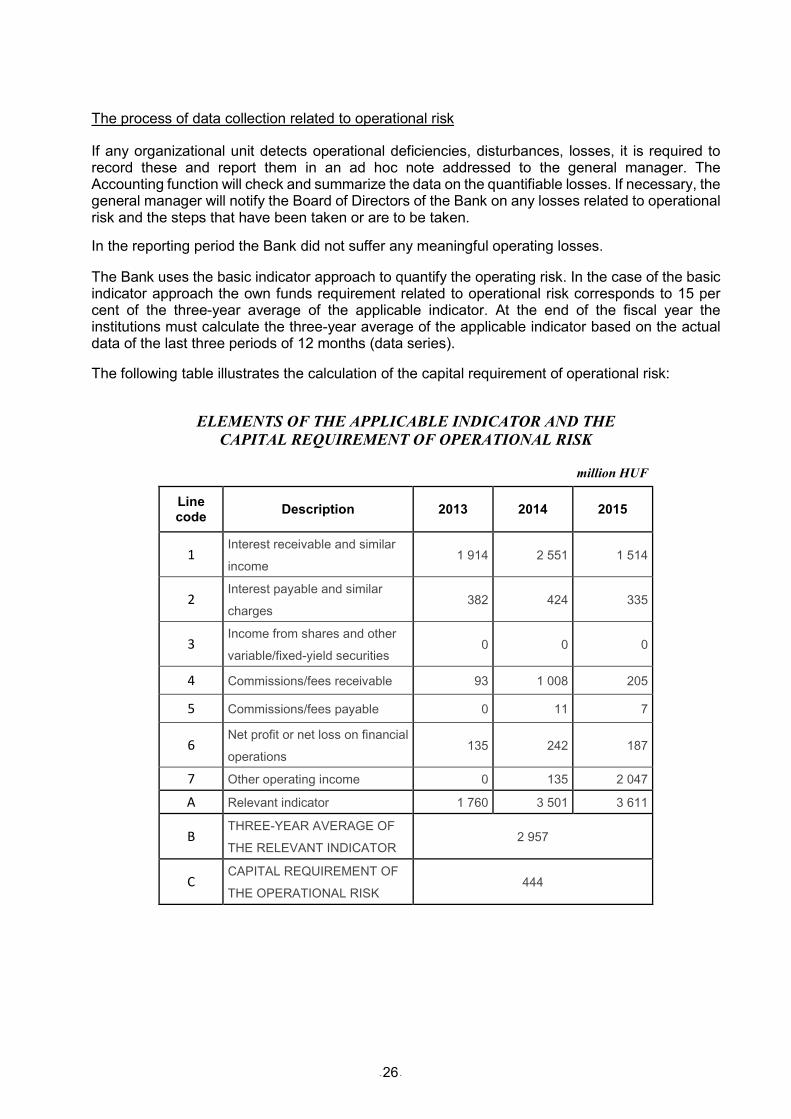

The Bank uses the basic indicator approach to quantify the operating risk. In the case of the basic indicator approach the own funds requirement related to operational risk corresponds to 15 per cent of the three-year average of the applicable indicator. At the end of the fiscal year the institutions must calculate the three-year average of the applicable indicator based on the actual data of the last three periods of 12 months (data series).

The following table illustrates the calculation of the capital requirement of operational risk:

ELEMENTS OF THE APPLICABLE INDICATOR AND THE CAPITAL REQUIREMENT OF OPERATIONAL RISK

million HUF

Line code

Description 2013 2014 2015

1 Interest receivable and similar

income 1 914 2 551 1 514

2 Interest payable and similar

charges 382 424 335

3 Income from shares and other

variable/fixed-yield securities 0 0 0

4 Commissions/fees receivable 93 1 008 205

5 Commissions/fees payable 0 11 7

6 Net profit or net loss on financial

operations 135 242 187

7 Other operating income 0 135 2 047

A Relevant indicator 1 760 3 501 3 611

B THREE-YEAR AVERAGE OF

THE RELEVANT INDICATOR 2 957

C CAPITAL REQUIREMENT OF

THE OPERATIONAL RISK 444

- 27 -

Exposures in equities not included in the trading book (CRR Article 447)

During the year 2016 the Bank did not purchase or sell investments, accordingly, it did not have any profit or loss realized from its investments.

At the end of the year 2016 the Bank had equity exposure in Garantiqa Hitelgarancia Zrt., -, the book value of which is HUF 10 million. The share of the Bank in the subscriber capital of Garantiqa Hitelgarancia Zrt., is 0.1276%. The shareholding of the Bank in the equity of Garantiqa Hitelgarancia Zrt. - according to its audited balance sheet of 31 December 2016 - is HUF 39 million, which exceeds the book value of the investment. The Bank classified its investment as problem-free.

The book value of the investments of the Bank into its Serbian subsidiary were HUF 4,713 Million as of December 31, 2016.

Exposure to interest rate risk on positions not included in the trading book (CRR Article 448)

The liabilities of the Bank in addition to its shareholder’s equity and subordinated loan capital received from the Owner consist mainly of short-term client deposits or short-term loans borrowed from members of the BOC Group, therefore it is a basic principle of the interest risk management policy of the Bank that the Bank manages its interest rate risks in a preventive manner, in general it does not engage in placements with a fixed interest for any term longer than three months, unless it can finance such placements with a source that has the same term and also bears a fixed interest rate. The Bank usually applies an interest base that follows market movements (HUF: BUBOR, EUR: EURIBOR, USD: LIBOR, CNY: HIBOR). The Bank measures its interest rate risk on an annual basis in the framework of ICAAP. With regard to the fact that the clients place their deposits for a very short term (often payment is only made to the current account, without a term deposit), therefore in 2016 the Bank continuously kept a significant volume of liquid assets in liquid securities (e.g. discount treasury bills). The Bank accepts if its clients prepay their outstanding loans, the negative interest impact of which is mitigated by reducing the funds raised by it from members of the BoC Group, i.e. it pays less interest for the liabilities.

Following the recommendation of the Supervisory Authority, the calculation of the internal capital requirement of the interest rate risk is based on a presumed interest shock of 200 basis points in the case of exposures denominated in the currency of G10 countries. The stress test applies the same method to the HUF positions, but in consideration of the Hungarian processes the Bank applies 300 basis points to measure of the interest rate shock.

If the standard interest rate shock on the interest rate risk of the banking book indicates a potential decrease of over 20% of the own funds of the Bank, then the Bank will take the necessary actions in order to reduce its interest rate risk exposure.

Exposure to securitization positions (CRR Article 449)

The Bank does not have any securitized positions therefore it has no obligation of disclosure concerning CRR Article 449.

- 28 -

Remuneration policy (CRR Article 450)

The Board of Directors approved the remuneration policy of the Bank for 2016, as proposed by the senior management. At least once a year the remuneration policy is assessed and decision is taken on the remuneration policy of the given year. The Bank did not reach those indicators that would have made it obligatory to set up a remuneration committee, therefore the Bank did not establish such a committee.

At Bank of China (Hungária) Zrt., the members of the Board of Directors and the members of the Supervisory Board, the managing directors, furthermore, the chief accountant, the head of risk management and the internal auditor are considered Specified Persons Importance from remuneration point of view.

Members of the Board of Directors and Supervisory Board do not receive any performance based remuneration for their activities in this capacity.

All five members of Senior Management are simultaneously managing directors of Bank of China (Hungária) Zrt., and Bank of China Limited Hungarian Branch under multiple employment as permitted by Article 195 of the Hungarian Labor Code. The related labor contracts the parties agreed that Bank of China Limited Hungarian Branch will make the salary payments for the members of the Senior Management.

The Bank wishes to apply its remuneration policy as well to encourage the Management and employees of the Bank to refrain from taking excessive risks. The components of the remuneration policy (base salary, benefits and performance dependent wage/bonus) are known to each employee of the Bank, as well as the principle of the Head Office stating that the bonus shall not exceed 50% of the yearly base salary and shall only be disbursed, as a main rule, if the Bank is profitable.

For the year 2016 the Bank’s Remuneration Policy determined the following targets as conditions for bonus payment for the Specified Persons:

- the ratio of non-performing loans must not exceed 5% (25%) - the Bank must comply with the legal provisions on capital requirements (25%) - the liquidity of the Bank must be stable (25%)

Liquidity ratio: not lower than 25% and monitored on a monthly basis;

Liquidity ratio: = liquid assets/liquid liabilities.

Liquid assets and liabilities mean the assets or liabilities of which the remaining maturity is less than 1 month.

- the Bank should be profitable (25 %) (25%). Performance is measured at Bank, department and individual level. The Head Office has not introduced stock option for the employees anywhere and owing to the size of the Bank and the possible amounts of the bonuses, the bonus can be paid in cash within the framework set by the relevant Government decree.

The Bank provides various benefits to its employees (e.g. tickets for local travel in Budapest, lunch vouchers, use of automobile), several of which are contained in the employment contracts, others are provided by the Bank according to employee groups.

- 29 -

In the year 2016 the Bank spent a total of HUF 1 456 million on wages and other staff related expenditures, within which wages and bonuses totaled HUF 1 149 million and other personal related payments HUF 307 million. The eight Specified Persons received a total of HUF 137 million of this amount.

In the year 2016 a total of HUF 89 494 thousand bonus was paid to employees of the Bank, of this amount the payment of HUF 2 192 thousand was deferred - in the case of the Person(s) of Special Importance - for the years 2017 and 2018.

According to the relevant internal policy, in the case of the Specified Persons at least 40% of the bonus must be withheld, which amount may be paid in a deferred manner.

HUF 848 thousand was paid as deferred payment to Specified Person(s).

No acquired entitlement was subsequently adjusted.

In the year 2016 the Bank did not pay any amounts (e.g. hire-in fee) related to new employment contracts or severance.

No person received any remuneration at the Bank that would equal or exceed the amount of one million euros.

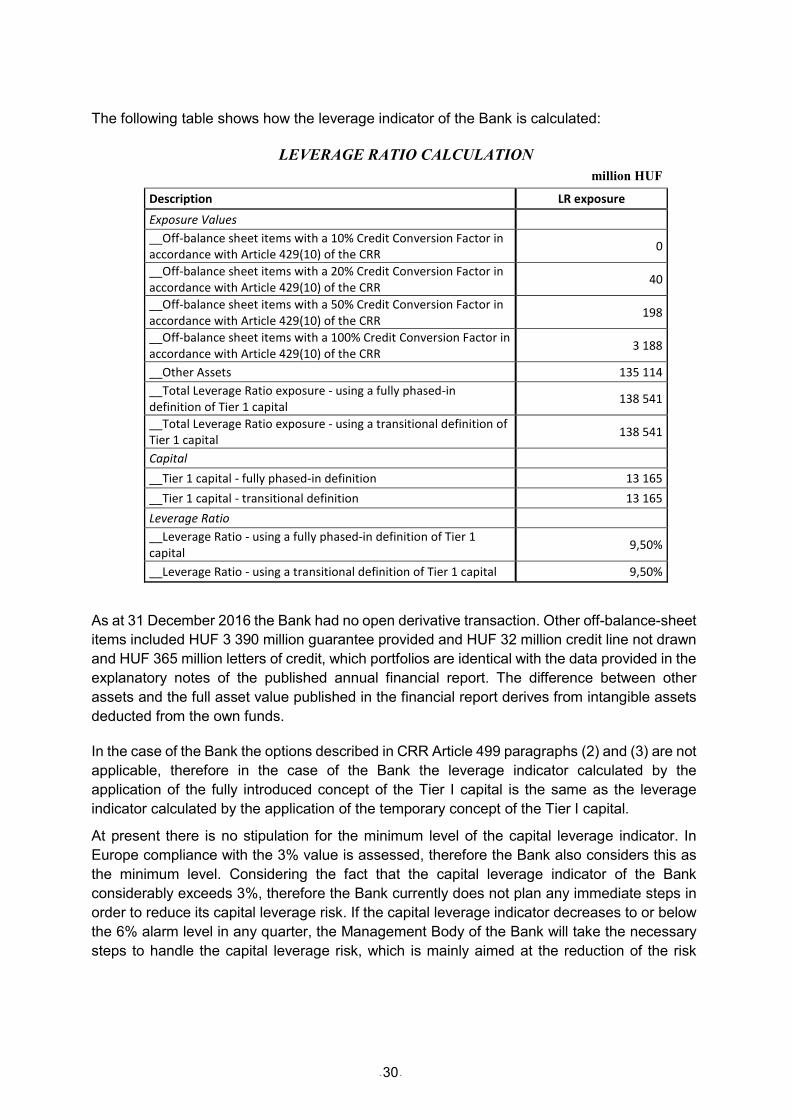

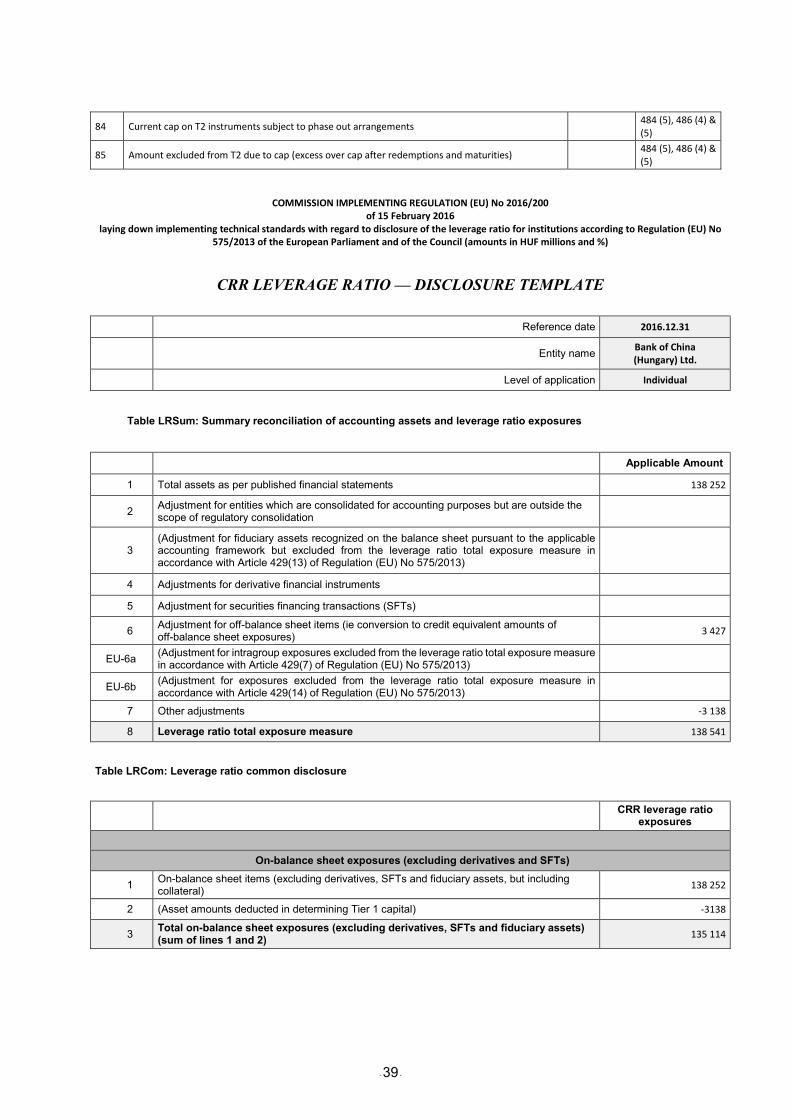

Leverage (CRR Article 451)

Pursuant to CRR Article 429, the leverage ratio shall be calculated as an institution's capital

divided by that institution's total exposures and shall be expressed as a percentage. The capital

measure shall be the Tier 1 capital. Total exposure is the sum of the exposure values of all assets

and off-balance sheet items not deducted from Tier I capital.

- 30 -

The following table shows how the leverage indicator of the Bank is calculated:

LEVERAGE RATIO CALCULATION

million HUF

Description LR exposure

Exposure Values

__Off-balance sheet items with a 10% Credit Conversion Factor in accordance with Article 429(10) of the CRR

0

__Off-balance sheet items with a 20% Credit Conversion Factor in accordance with Article 429(10) of the CRR

40

__Off-balance sheet items with a 50% Credit Conversion Factor in accordance with Article 429(10) of the CRR

198

__Off-balance sheet items with a 100% Credit Conversion Factor in accordance with Article 429(10) of the CRR

3 188

__Other Assets 135 114

__Total Leverage Ratio exposure - using a fully phased-in definition of Tier 1 capital

138 541

__Total Leverage Ratio exposure - using a transitional definition of Tier 1 capital

138 541

Capital

__Tier 1 capital - fully phased-in definition 13 165

__Tier 1 capital - transitional definition 13 165

Leverage Ratio

__Leverage Ratio - using a fully phased-in definition of Tier 1 capital

9,50%

__Leverage Ratio - using a transitional definition of Tier 1 capital 9,50%

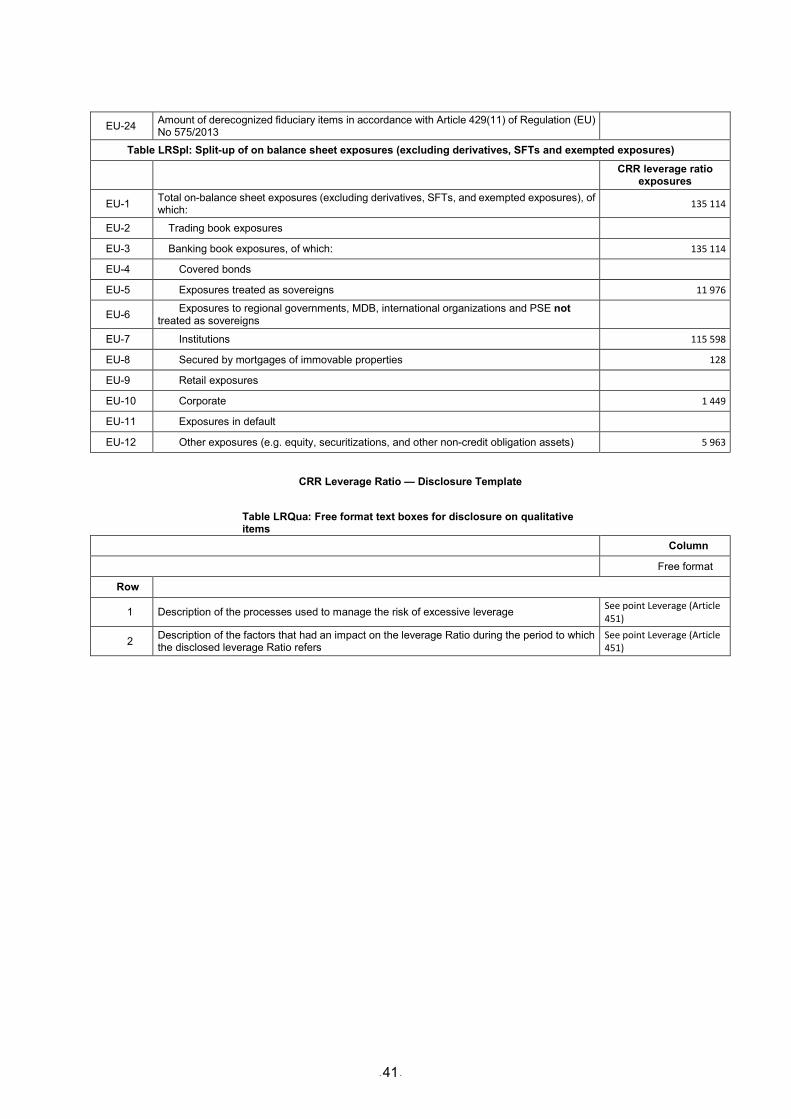

As at 31 December 2016 the Bank had no open derivative transaction. Other off-balance-sheet

items included HUF 3 390 million guarantee provided and HUF 32 million credit line not drawn

and HUF 365 million letters of credit, which portfolios are identical with the data provided in the

explanatory notes of the published annual financial report. The difference between other

assets and the full asset value published in the financial report derives from intangible assets

deducted from the own funds.

In the case of the Bank the options described in CRR Article 499 paragraphs (2) and (3) are not

applicable, therefore in the case of the Bank the leverage indicator calculated by the

application of the fully introduced concept of the Tier I capital is the same as the leverage

indicator calculated by the application of the temporary concept of the Tier I capital.

At present there is no stipulation for the minimum level of the capital leverage indicator. In

Europe compliance with the 3% value is assessed, therefore the Bank also considers this as

the minimum level. Considering the fact that the capital leverage indicator of the Bank

considerably exceeds 3%, therefore the Bank currently does not plan any immediate steps in

order to reduce its capital leverage risk. If the capital leverage indicator decreases to or below

the 6% alarm level in any quarter, the Management Body of the Bank will take the necessary

steps to handle the capital leverage risk, which is mainly aimed at the reduction of the risk

- 31 -

exposures by the sale of assets.

In 2016 the following had impact on the leverage indicator:

• we have considered the value of the exposures without intangible assets and

the investment into the Serbian subsidiary, since their value was deducted in the

calculation of the Tier I capital;

• the amount of the Tier I capital was increased by the audited profit and the

general reserve formed at the end of the year.

Use of the IRB Approach to credit risk (CRR Article 451)

The Bank does not calculate the risk-weighted exposure amounts under the IRB Approach

therefore it has no disclosure obligation in respect of Article 452 of the CRR.

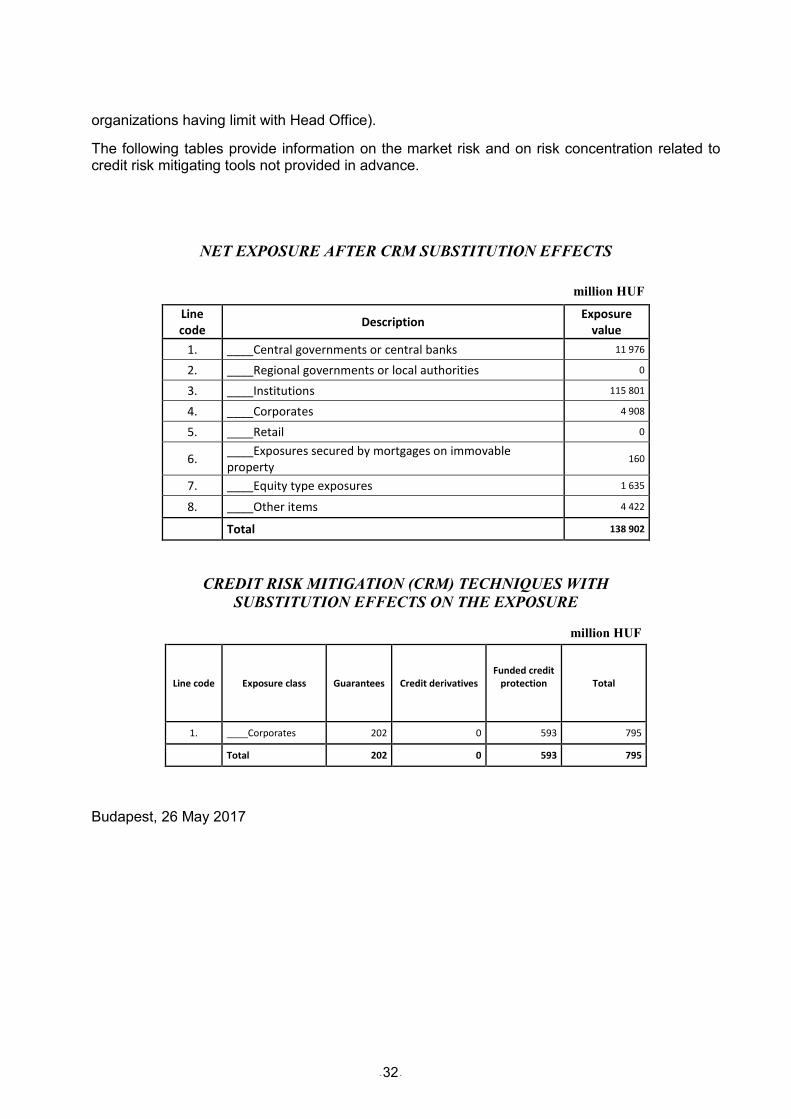

Use of credit risk mitigation techniques (CRR Article 453)

The Bank does not apply netting. The Bank regularly evaluates the assets offered or stipulated (in the contracts) assets serving the purpose of risk mitigation, whether in the decision making process or during monitoring whether the collaterals were offered by the customer or by third parties.

In case of mortgages the bases of the collateral evaluation is the evaluation made by an independent expert within the previous 90 days. The Bank is entitled to revise the market value provided by the independent expert. The Bank will establish the collateral value of the asset serving to mitigate the risk based on the market value and applying a multiplier, which is also considering the effects of the FX rate modifications. The Bank will pay attention also to the liquidation value of the asset given by the independent expert.

The Bank regularly checks if the collaterals supporting the deal are available, keep their value, are they enforceable, if these were changed and if the answer is yes, the Bank will reconsider the collateral value of the asset or in the applied multiplier.