Embed Size (px)

Citation preview

Report No. 7269-PH

Philippines:Energy Sector StudySeptember 15, 1988

Industry and EnErgy DivisionCountry Department IIAsia Region

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit Philippine Peso (P)US$1.00 = P 21

WEIGHTS AND MEASURES

MMTOE = Million tons oil equivalentMMBOE = Million barrels oil equivalentBOPD = Barrels of oil per dayMW = Megawatt (1,000 kilowatts)lIWh = Terrawatt-hours (billion kilowatt-hours)kWh = Kilowatt-hours (1,000 watt-hours)kV = Kilovolt (1,000 volts)km = Kilometer (0.6214 mile)MWh = Megawatt hour (1,000 kilowatt-hours)

ABBREVIATIONS AND ACRONYMS

ADB - Asian Development BankBED - Bureau of Energy DevelopmentBEU - Bureau of Energy UtilizationEHV - Extra High VoltageERB - Energy Regulatory BoardHVDC - High Voltage Direct CurrentHVAC - High Voltage Alternate CurrentMERALCO - Manila Electric CompanyMOE - Ministry of EnergyNEA - National Electrification AdministrationNEDA - National Economic Development AuthorityNPC - National Power CorporationOEA - Office of Energy AffairsPCI - Philippine Geothermal Inc.PNOC - Philippine National Oil CompanyPNPC-EDC - PNOC-Energy Development CorporationPNOC-EDI - PNOC-Energy Drilling Inc.PNPP - Philippine Nuclear Power PlantSCC - Semirara Coal Corporation

FOR OFFICIAL USE ONLY

ENERGY SECTOR STUDY

Table of Contents

Page No.

Summary and Conclusionso................ e..... ..................... i

Part One: Energy Development Policy

I. AN OVz&¶IEW OF THE ENERGY SECTOR.......... .......... 1

A. The Macroeconomic Context ..................****.......... . IB. Energy Resources and Production...... . .... ....... 1

| ~~~~~C. Energy Demand .... .0....... . ....... 0........ .0-.000. .................. 3D. Institutional Framework ....... ..... . ............. .......o...o . 5

II. POWER SECTOR DEVELOPMENT PROGRAM ........... o ................ 7

A. Introduction..* .. 000 . 00000000..0-. 7B. Demand Forecast..o..r... ........ ... .. o.. .......... 7C. Present Generating l?acilities..*cit...ie.. ..... 9Do Least-Cost Expansion Plan..ooooo...o..o ... 10E. Sensitivity A sa l y s i s 15F. Other Giids 16Go Conclusionse.**..*.**oo*ea .. oo*oo* 17

III. COAL DEVELOPMENT AND UTILIZATION POLICY............... o.... 19

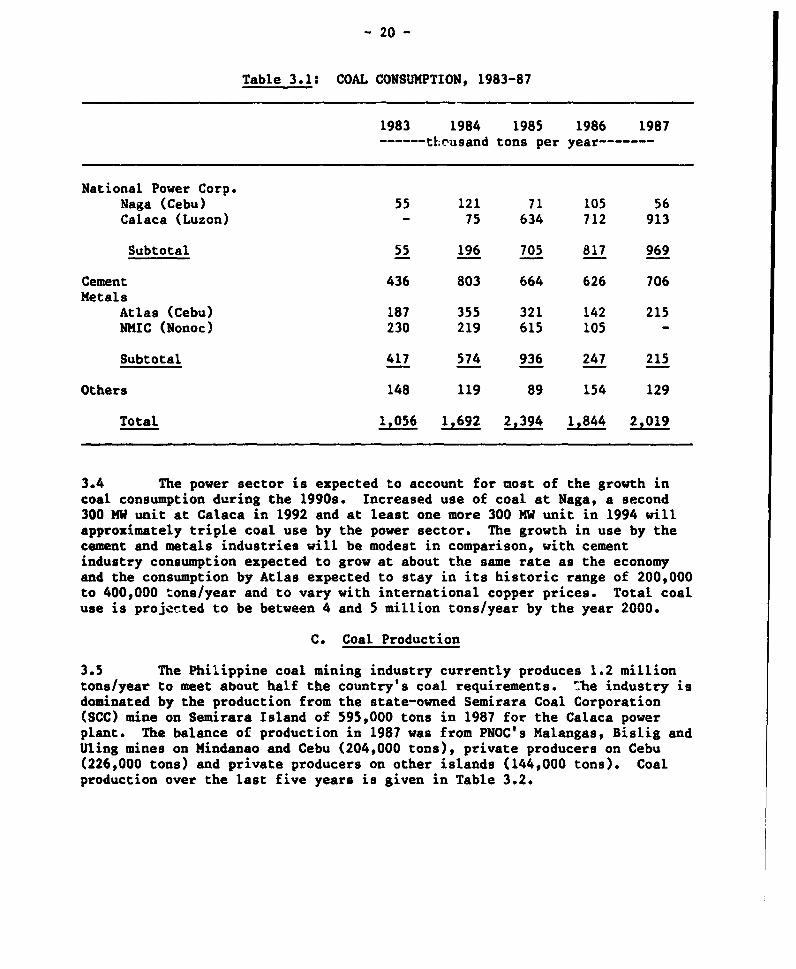

Ao Introduction ...... 19B. Coal Consumption* ...... .. .. .............. oooo.... 19C. Coal Productiono.. tu...oo.o n..... o.o ............... *oo. 20D. Major Policy Issues.**.e ..... s..ooo ........... oo.o.. 22E. Conclusions and Recommendations....................... 27

IV. GEOTHERMAL DEVELOPMENT AND UTILIZATION POLlCY... lCY......oo 29

Ao Intoutionuot i o n 29B. Organizational Structure. . o.o...... o.. . . o. ...... 29C. Assessment of Geothermal Resources.................... 30D. Cost of Geothermal Exploration and Development-om......nt 32E. The Tongonan Projecto.oj etoo.ovo. oo.. o.... ....... .... 34F. Major Issues in the Sectoroe ct.o.......o or.... o....or... 36G. Conclusions and Recommendations.m.....d t... o.....n.o.... 38

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Page No.

Part Two: Energy Pricing Policy

V. ENERGY PRICING .................. ................ ................... . 40

A. Introduction ... *.********* ............ *to ........... .* ........... 40B. Petroleum Product Prices. .. .......... t ............. . *... . 40C. Electricity Tariffs . ...................... .*. 42D. Steam Prices ....................... .... ... *.. .......... 46E. Coal Pricing Policy .. 48F. Recommendations ..................... ............. . 49

Part Three: Operational Issues

VI. TECHNICAL AND ECONOMIC ASPECTS OF POWER PLANTREHABILITATION ..................... **..* .................... #** .... 51

A. Introduction ....... .......... 51B. Technical Aspects of Plant Rehabilitation................ 51C. Economic Analysis of Plant Rehabilitation*................ 57D. Centralized Maintenance Capabilities&..................... 60E. Conclusions and Recommendations ............ .... .... 62

VII. TRANSMISSION AND DISTRIBUTION LOSSES ........................ 64

A. Introduction ... ................................... 64B. Technical Characterstics of the Distribution System ...... 64C. Technical Losses.*.*.**** ............... .... . . 67D. Non-Technical Losses* ....... * .... ...... **.s. 68E. Measures Taken by MERALCO.*.*. . .. ..... * . ..... ..... . 70"'. Conclusions ........ .0*0.... 000......................................... 71

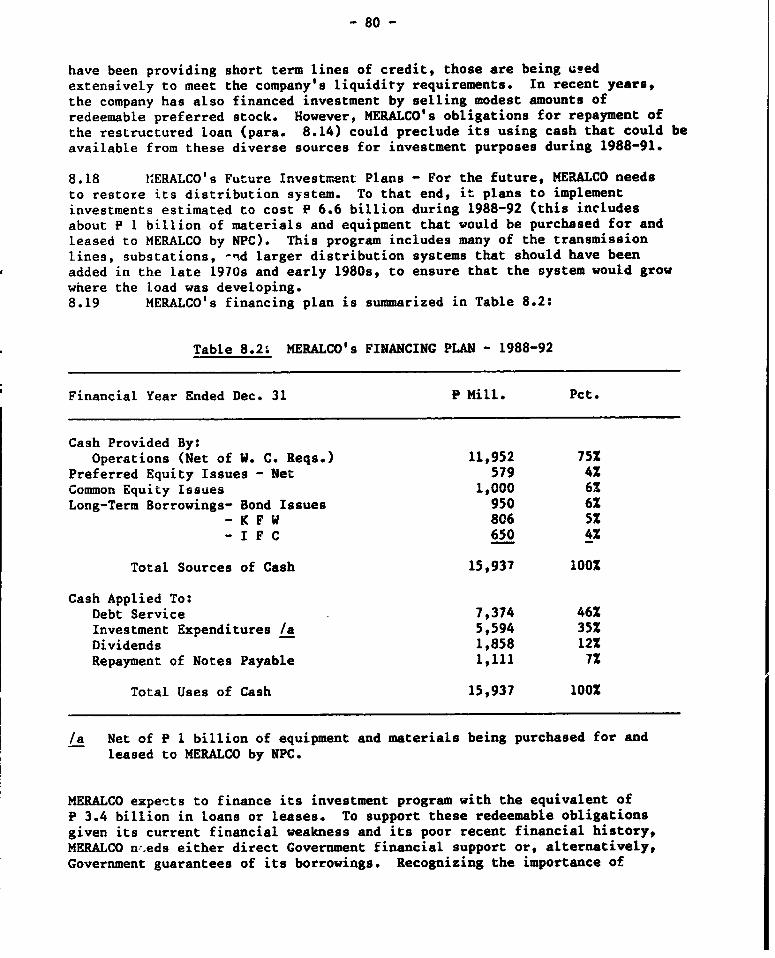

VIII. FINANCIAL ISSUES FACING THE POWER SECTOR . .......... 73

A. Introduction ..... 000 ... . ........................ .................. 73B. Local Currency Funding Constraints .......... ............... 74C. Shortages of Equity Capital.o ..................... 79D. Government Support for Electricity Retailing Activities.. 82E. Conclusions.. ....... #0...... 0 ........ 84

ANNEXES

Annex 1.1 - Commercial Energy Balance, 1987

Annex 2.1 - NPC's June 1987 Generation Expansion ProgramAnnex 2.2 - Calculation of Levli-eO Generation CostsAnnex 2.3 - Underlying Assumptios. " the Least Cost Development ProgramAnnex 2.4 - Results of Least-Cost De.c_opment Plan

Annex 3.1 - Coal Consumption by End UseAnnex 3.2 - Coal Production and ImportsAnnex 3.3 - Historical and Projected Prices of CoalAnnex 3.4 - Environmeuntal Effects of Power and Coal Sector Development

Annex 4.1 - General Characteristics of Operating Geothermal Fields in thePhilippines

Annex 4.2 - Analysis of Geothermal Exploration ActivitiesAnnexi 4.3 - The Cost of Exploration and DevelopmentAnnex 4.4 - The Cost of a 110 MW Field: A Typical Case Versus Historical

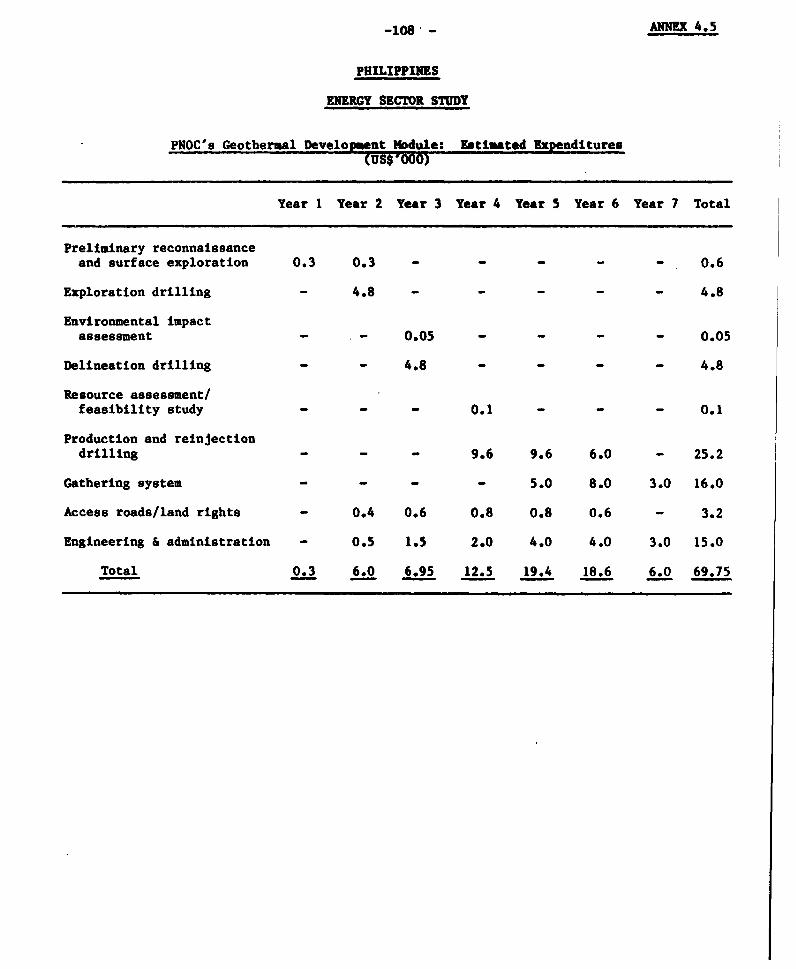

CostsAnnex 4.5 - PNOC's Geothermal Development Module: Estimated ExpendituresAnnex 4.6 - Historical Costs of Geothermal Exploration and DevelopmentAnnex 4.7 - Estimated Cost of Geothermal Exploration and Development at

PinatuboAnnex 4.8 - Estimated Cost of Geothermal Exploration and Development at LaboAnnex 4.9 - Annual Operating and Maintenance Cost of the Bacon-Manito PlantAnnex 4.10 - Estimated Cost of Tongonan Development

Annex 6.1 - Summary of Technical Data fcr NPC Oil Fired Power PlantsAnnex 6.2 - Data and Assumptions underlying Economic Analysis of Plant

RehabilitationAnnex 6.3 - Partial Rehabilitation of Sucat Units 1 and 4Annex 6.4 - Cost Estimates for Partial Rehabilitation of Sucat Units 2 and 3Annex 6.5 - Cost Estimates for Full Rehabilitation of Sucat Units 2 and 3Annex 6.6 - Rehabilitation Program: Unit Outage ScheduleAnnex 6.7 - Cost Estimates for Restoration Program of Bataan Units 1 and 2Annex 6.8 - Cost Estimates for Restoration Program of Manila Units 1 and 2Annex 6.9 - List of Equipment for Fabrication ShopAnnex 6.10 - NPC Training Courses

Annex 7.1 - Estimation of Technical LossesAnnex 7.2 - Manila Electric Company: Yearly System Losses

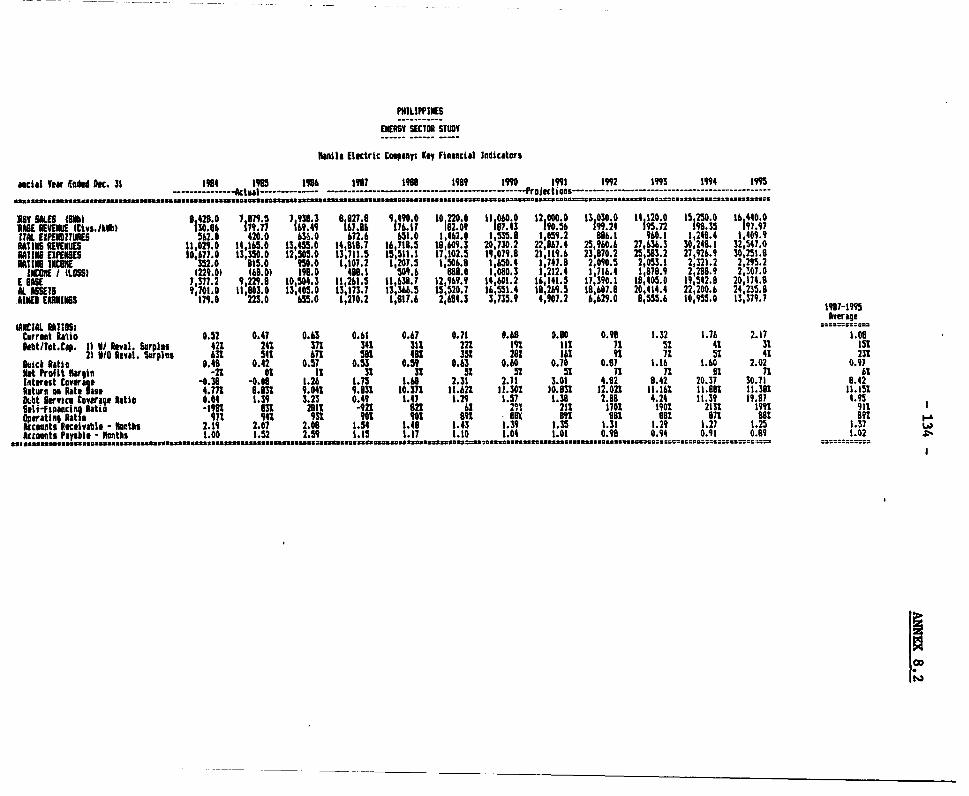

Annex 8.1 - National Power Corporation: Key Financial IndicatorsAnnex 8.2 - Manila Electric Company: Key Financial Indicators

This report was prepared by an energy sector mission that visitedPhilippines from January 24 to February 19, 1988. The mission comprised:

1. Hossein Razavi, Senior Economist/Mission Leader2. Anil Malhotra, Senior Energy Specialist3. Jamil Sopher, Senior Financial Analyst4. Paul Dyson, Senior Mining Engineer5. Mihir Mitra, Power Engineer6. DeAnne Julius, Energy Pricing Specialist7. Mudasar Imran, Economist8. William Berge, Geothermal Specialist9. Richard Buckland, Coal Specialist10. M. Rozali, System Planning Engineer11. Alfred Banks, Power Plant Engineer12. Miguel Diaz, Power System Engineer

The mission gratefully acknowledges very effective cooperation fromthe Office of Energy Affairs (OEA), the National Economic DevelopmentAuthority (NEDA), the National Power Corporation (NPC), the PhilippineNational Oil Company (PNOC), the Manila Electric Company (IWEBALCO), theSemirara Coal Corporation (SCC) and the Energy Regulatory Board (ERB). Themission also acknowledges very beneficial discussions with the chairmen andcertain members of the House Committee on Energy, the Senate Committee onPublic Utilities and the Senate Committee on Natural Resources*

SUMMARY AND CONCLUSIONS

Background and Objective

1. Throughout the period following the oil crisis of the mid 1970s, theenergy policy of the Philippines has focused on developing indigenous energyresources and promoting more efficient energy usage. Indigenous energyresource development involved heavy government participation in developingoil, geothermal, coal and hydro resources. Energy demand management initiallyfocused on direct intervention, with fuel allocation and rationing schemesused during periods of tight supply. However, energy pricing was soon recog-nized as a more permanent and effective policy tool for managing demand. Theresults of steps taken to meet the above energy policy objectives have beenimpressive. Imported oil's share of total energy use has declined from 95% in1973 to 56% in 1986, and energy consumption patterns indicate improvingefficiency in energy use.

2. Despite the notable past success in resource development and demandmanagement, the sector now faces a number of issues with regard to its medium-and long-term development strategy and efficient utilization of availableresources:

(a) Previously, increases in electricity demand in Luzon were expectedto be met by generation from the 620 MW Philippine Nuclear PowerPlant (PNPP). However, the Government's decision in 1986 tomothball PNPP along with the "downgrading of generating capacity i.the Tiwi geothermal power plant and the relatively ;..-p increase inpower demand in 1987 have created a sudden need to re-examine andoptimize energy choices in order to meet the expected demandincreases;

(b) The recent collapse in international energy prices has introducedconsiderable uncertainty regarding the economics of domestic energyproduction. In particular, the development of domestic coal andcertain hydro resources may no longer be viable alternatives toenergy imports;

(c) Pricing of geothermal steam and domestic coal has been continuouslydisputed among the concerned entities and has created a bottleneckin planning by the agencies responsible for developing theseresources;

(d) The Government's decision to abolish the Ministry of Energy has ledto a lack of coordination of energy sector activities and, inparticular, a lack of clear direction for energy resource develop-ment; and

(e) Certain problems in the operational efficiency of the power sectorhave created considerable concern: electricity losses haveincreased from about 8Z in 1980 to more than 20% in 1987; rehabili-tation of oil-fired power plants needs to be decided urgently; andfinancial issues facing the power sector need to be resolved.

- ii -

3. The purpose of this study is to review: (a) the prospects fordevelopment of the country's indigenous energy resources, including hydropower, geothermal and coal resources; (b) the pricing of geothermal steam,coal, electricity and petroleum products; and (c) selective operational issuesin the power sector including power plant rehabilitation, transmission/distribution losses and financial issues facing the major entities in thesector. Based on this review, a short-, medium- and long-term strategy fornational energy development is suggested.

Energy Demand

4. Energy consumption in the Philippines fell from a peak of 9.2 mil-lion tons of oil equivalent (MMTOE) in 1Q79 to 7.1 MMTOE in 1985 in responseto a program of demand managemuent and a slowdown in economic activity. Withthe resumption of economic growth in 1987, chis trend has been reversed,resulting in total energy consumption of 9.6 MMTOE in 1987. Demand isexpected to continue growing over the next five years by an estimated 4.7%p.a. In 1987, the industrial sector accounted for 51% of tot l energy demand,followed by the transport sector with 32% of demand and resid..tial/commercialuses with 14%. Over 80% of total energy demand is met by petroleum productsand 15% is met by electricity, mainly for residential/commercial uses andindustry.

5. Electricity demand is forecast to grow at an annual average rate of5.4% over the period 1988-2000. This "base-case" forecast assumes a GDPgrowth rate of 5.8% in 1988-92. and 6.3% for 1993-2000. Despite theassumption of an increasing GDP grow'h rate, growth in power demand isexpected to be relatively stable due to declining trends in electricity/GDPelasticities. The mission developed also high and low growth scenarios. Thehigh-growth scenario is based on a GDP g.owth rate of 7.5% p.a., and indicatesa power demand growth of 6.5% p.a. The low growth scenario is based on a GDPgrowth rate of 5.2% p.a. and results in electricity consumption increasing at4.8% p.a.

Domestic Sources of Energy

6. The Philippines has only modest amounts of indigenuus energysources. Proven petroleum reserves are estimated at 4 million tons, naturalgas deposits are considered subcommercial, probable uranium v-serves are esti-mated at 1.2 MMTOE, and total potential coal resources are estimated at about1,500 million tons, with the largest proven deposits located on the smallisland of Semirara and in the Cagayan Valley of northern Luzon. Hydropowerresources, by contrast, are quite substantial, with a theoretical power poten-tial of over 10,000 MW. However, development of these resources is relativelycostly due to the distance of the better sites from the main transmissiongrid.

7. The country's main potential domestic energy resource is geothermalsteam. While the geothermal reserves have not been fully evaluated, theycould exceed 8,000 MW. Based on current information, there are about 4,431 MWof probable reserves, 1,640 MW of which nave been tested, but only 894 MW of

- iii -

capacity has been installed. About 3,000 MW of total pJotential reserves areon Luzon, but only 700 MW is being utilized. Most of the remaining geothermalresources are on the island of Leyte, which has potential geothermal resourcesestimated at about 2,000 MW, of which 400 MW is available from the Tongonanfield. Utilization of the Tongonan reserves would require the construction ofan overland/submarine transmission line from Tongonan to Luzon Island.Depending on whether this line is high voltage direct current (HVDC) or highvoltage alternate current (HVAC), the line would cost between US$210 millionand UJS$370 million. Further development of Tongonan reserves will require adetailed feasibility study to (a) determine the exact routing of the line;(b) estimate the impact of the line on the stability of the Luzon grid; and(c) decide whether HVDC or HVAC is technically appropriate.

Institutional Framework, Coordination and Planning

8. Policy formulation and planning of the energy sector are theresponsibilities of the Office of Energy Affairs (OEA), a new agencyestablished in mid-1987 to take over the functions formerly carried out by thenow abolished Ministry of Energy. OEA reports to the Office of thePresident. Other key sectoral institutions are: the Philippine National OilCompany (PNOC), responsible for developing indigenous hydrocarbon andgeothermal resources; the National Power Corporation (NPC), responsible forpower generation and transmission; the Manila Electric Company (MERALCO), aprivate company supplying electricity to the Metro Manila area; the state-owned Semirara Coal Corporation (SCC), the major coal producer; and theNational Electrification Administration (NEA), responsib e for rural electri-fication.

9. PNOC and NPC were att&ched to MOE prior to its abolition, anarrangement which allowed effective coordination of sector policies andprograms and contributed to the Philippines' rapid and successful drive todevelop domestic resources and curtail consumption. Currently, however, OEAis organizationally distinct from PNOC and NPC (which are also under theOffice of the President) and lacks the authority to carry out its coordinationand decision-making functions for the sector. As a result, sectoral policiesand investment programs lack cohesion and reflect inadequate long-rangeplanning. The lack of a strong central agency in the sector has also alloweddisagreements between PNOC and NPC over critical issues like steam pricing toremain unresolved for a relatively long period of time, with consequent anddeleterious effects on sector development.

10. To relieve this situation, it is recommended that an EnergyCoordination Council be set up in the Office of the President to be headed bythe Executive Secretary, with the Presidents of NPC, PNOC and SCC and theExecutive Director of the OEA as members. The OEA should then prepare a long-term plan for energy deNelopment for the country, in consultation with thethree major public sector energy agencies and under the overall framework ofthe economic plans prepared by the National Economic and Development Authority(NEDA). This plan should be formally ratified by the Energy CoordinationCouncil on ar annual basis. All investments in the energy sector whichrequire the commitment of government funds should be in consonarce with theenergy plan approved by the Energy Coordination Council. It would be the

- iv -

responsibility of OEA to ensure this through appropriate intercessions in thedeliberations of the Investment Coordinating Committee, the government agencyresponsible for investment fund appropriations.

Economics of Various Sources of Energy

11. The development of Philippine's indigenous energy resources isclosely intertwined with that of the power sector. Just as geothermal steam,domestic coal and hydropower represent a large energy source fcr power genera-tion; so the power sector represents the major consumer of these resourceswithout which none of them is likely to experience substantial development inthe future. Thus, the development strategy of indigenous sources of energyneeds to be studied within a consolidated framework using the netback value tothe p.wer sector as a benchmark to assess the economics of these resources.

12. The mission carried out a least-cost analysis of the power sectordevelopment program for the Luzon power grid in order to establish a frameworkfor comparison of the economics of various sources of energy. The results ofthis analysis indicate that the average incremental cost (in 1987 dollars) ofenergy generated from alternative sources of energy is as follows:

US /kwh

Luzon geothermal 2.90Tongonan geothermalwith HVAC 2.72with HVDC 3.08

Imported coal 3.46Domestic coal 4.50Heavy fuel oil 4.32

13. The dynamic analysis using the investment programming package, WASP,resulted in the same economic ranking as the above. Thus the economicsequence of utilizing various sources of energy would be:

(a) to develop Luzen geothermal resources as much and as rapidly aspossible;

(b) to utilize Tongonan geothermal after a detailed feasibility studyproving its technical viability with HVDC line or with HVAC line ata reduced cost;

(c) to fill the gap between the growth in electricity demand and theavailable geothermal resources with power plants using importedcoal; and

(d) to replace imported coal with domestic coal as and if the relativeeconomic merits of domestic coal improves due to an unexpectedincrease in international energy prices.

14. Implications of the above sequence with regard to the developmentstrategy of each sector are described in the following paragraphs.

Geothermal Sector

15. Based on our review of existing assessments of geothermal resourcesin the Philippines, the following areas in Luzon show a good potential forexploitation: (a) the Bacon-Manito field probably has a much higher potentialthan the 110 MW committed for commissioning in 1991, but more drilling,testing and reservoir engineering work are needed before a commitment can bemade on subsequent plants; (b) the Mt. Labo field has estimated potentialreserves of 400 MW; (c) the Mt. Pinatubo has a 56% probability of resourcediscovery and a 40% probability of reserves of about 200 MW; and (d) theBatong-Huhay field has a high probability for success and may have reserves ofabout 150-200 MW. On Leyte, the Tongonan field has estimated reserves ofabout 800 MW, with a minimum of 480 MW and maximum of 1,200 MW. If it isdecided to connect the Tongonan field to the Luzon grid, 52 more wells wouldneed to be drilled to support an additional 440 MW of capacity. Moregenerally, substantial delineation and development work, as well as, a well-planned exploration program are needed in the geothermal sector.

16. Despite the economic advantages of geothermal resources over othersources of energy, a number of factors have impeded the development andutilization of geothermal steam:

(a) While overall geothermal production costs are not excessive comparedto those of other countries, exploratory drilling costs in thePhilippines range from US$1.2 to 1.8 million per well, significantlyhigher than the industry norm of US$0.8-1.0 million under similarconditions. The higher drilling costs need to be reduced by betterplanning and supervision, use of experienced contractor's crews withaccess to latest technology, higher rig utilization factors andreduced drilling times.

(b) PNOC, or any other entity which may wish to develop geothermalresources, is required to pay 60% of its net revenues as royalty tothe C vernment while its recovery of costs is limited to 90% oftotal avenue. This requirement has, at current energy prices, madesteam exploration and exploitation appear economically unattrac-tive. In order to remove this constraint, the Government shoulddesignate PNOC as its "implementor" for geothermal development,wntich would exempt PNOC from royalty payments but require PNOC tocontinue paying corporate income tax to insure that Governmentcaptures its part of net revenues. PNOC may also consider enteringinto joint venture agreements with other local and foreign partiesin order to share the risk of exploration. Over the long-term,however, the Government will need to alter the royalty legislationin order to encourage other local and foreign parties to undertakegeothermal exploration and production.

(c) The price of steam has long been in contention since it has noobservable international price or independently determined value. A

- vi -

recent study has, however, proposed the principle of "avoided cost"to determine the price of steam in the Philippines and this has beenaccepted by both PNOC and NPC. In the case of a geothermal field onLuzon, th._ avoided cost is the break-even price of electricitygenerated from imported coal. This would enable NPC to generateelectricity from geothermal steam at the same cost as from a coal-powered plant, which is NPC's next best alternative. The missionhas estimated the avoided economic cost at USC2.4/kWh and theavoided f.nancial cost (after including duties on imported coal) atUS¢2.75/kWh. It is proposed that the steam price in Luzon be set atUSC2.7/kWh with the condition that PNOC absorb the exploration riskof resource development. This price would be appropriate for thenext four fields to be developed in Luzon and for the perceivedarrangement that two public entities (PNOC and NPC) produce and usethe geothermal steam. It is important to note that if a privatesector entity enters either or both of these activities, then aseparate pricing scheme would be needed to ensure that Gcvernmentwould capture the economic rent on geothermal resources.

(d) Coordination between PNOC as the geothermal producer and NPC as thesteam user needs to be improved and a mechanism established toassure the geothermal producer that the steam will be utilized whendeveloped and the power company that the steam will be availablewhen power plant construction is completed. Establishment of theproposed Energy Coordination Council (para. 10) would help resolvethis problem.

Coal Sector

17. Philippine coal resources, comprising thin seams of high qualitycoal and more accessible low quality coal, are considerably more expensive to

* mine than the resourc- q",ailable in the coal exporting countries, eveni allowing for the freight C differential. Domestic resources are currently

used to meet about half the 2._: million tons per annum of coal consumed by thecountry's power, cement and metal industries. There are two conflictingconsiderations in devising the future strategy for the coal sector. First,domestic coal is more expensive than imported coal. Thus, the mandated use ofdomestic coal imposes a significant burden on coal consumers in particular thepower and cement industry which may, in turn, hurt the internationalcompetitiveness of the industrial sector. Second, strategically, it is notunreasonable for the Philippines to have a domestic coal industry,particularly in view of fluctuating price of imported coal, lead time requiredfor mine development, and perhaps social considerations. The governmentstrategy should, therefore, allow for the financial survival of the existingcoal industry at its current stage of operation, but at the same time aim at(a) reducing the burden on coal users by narrowing the gap betweeninternational and domestic prices; and (b) preventing misallocation ofresources by limiting the expansion of the coal industry until and unlessinternational coal prices increase significantly.

18. In early 1988, the domestic price was about 15% above the purchasedprice (inclusive of duties) and 40% above the CIF price of imported coal. It

- vii -

is recommended that the domestic price of coal be maintained in nominalterms. Given the present projection of a relatively rapid increase in theinternational price of coal, the gap between the domestic and the import pricewill narrow substantially in the next few years. A fixed domestic price wouldresult in a parity with the purchased price of imported coal by 1990; there-after the duty on imported coal can be reduced gradually. The CIF price ofimported coal is expected to reach the level of domestic price by 1993-94.

19. With the above pricing policy, domestic coal will becomeeconomically cost effective within the next five years when the domestic pricewould give appropriate signals regarding economic viability of new investmentsin the sector. In the interim, however, the Government should limit theexpansion of the industry which might be triggered by the present prices.Candidates for major expansion in the coal industry are the Semirara andIsabela mines both of which are considered for supplying fuel to the powersector. NPC plans include a second 300 MW unit at Calaca, using Semirara coalas the fuel source, and a 300 MW mine mouth plant at Isabela in NorthernLuzon. With regard to Calaca, NPC's understanding was that the power plantshould be designed to use 100% Semirara coal and that the coal would beavailable by 1992 when the power plant will be commissioned. The missionreviewed the economic viability as well as the implementation constraints ofthe Calaca/Semirara development scheme. With the heat content of 7,200 BTU/lband the average cost of $40/ton, the cost of new coal on Semirara would bealmost twice the current CIF price of imported coal (on a BTU basis) and wouldstay 65% to 70% higher than the CIF price of $40/ton (12,000 BTU) projectedfor the early 1990s.

20. The mission reviewed the economic cost of the following alterna-tives: (a) to design Calaca II for imported coal and to use imported coal;(b) to design the plant for Semirara coal and to use Semirara coal; and (c) todesign the unit with the flexibility of using either imported or Semirara coalbut to use imported coal for the first five years (1992-1997) and Semiraracoal afterwards. The results indicate that the total discounted (investmentand fuel) cost of alternative (a) for a 300 MW power plant is US$568 millioncompared with a discounted cost of US$734 million for alternative (b), i.e.the additional cost to the country to use the Semirara coal is US$166 mil-lion. From this additional cost about US$22 million is due to the capitalcost differential of the power plant and about US$144 million to the coalprice differential. Alternative (c) reduces the additional cost imposed onthe economy from US$166 million to US$89 million. In view of the uncertaintyof international energy prices and the Government's desire to develop theindigenous resources, it is recommended that the Calaca plant be designed touse either domestic or imported coal, the premium paid for preserving thisflexibility being about US$20 million. NPC should use imported coal when thepower plant is commissioned in 1992 and switch to domestic coal in the late1990s if international coal prices increase beyond the current projections.On this basis, development of new Semirara deposits should be postponed untilthe late 1990s.

21. With regard to the proposed Isabela plant, analysis of this invest-ment scheme indicates that: (a) Isabela coal expansion is more costly thanthat of Semirara; (b) the Isabela plant would need a 400-km transmission line

- viii -

to connect with the main load center in southern Luzon, and (c) the Isabelaplant would have no flexibility to be able to use imported coal because of itsinland location. It is, therefore, recommended that the Isabela plant and itscorresponding transmission line be dropped from the NPC development plan.

22. By implementing the above pricing and investment policy, theGovernment would (a) allow the domestic coal industry to continue operatingexisting mines; (b) reduce the burden on coal consumers; and (c) provide aflexibility to expand the industry in the late 1990s if international pricesincrease substantially.

Power Sector

23. Based on current projections of power demand (base scenario,para. 5), the least-cost development program for the Luzon grid is as follows:

Year Plant Capacity (MW)

1989 Gas turbines 2001991 Bacon-Manito I geothermal 1101992 Bacon-Manito II geothermal 110

Calaca II coal 3001993 Luzon geothermal (Imported Coal*) 3301995 Tongonan geothermal I (Imported Coal*) 4501996 Kalayaan pumped storages 2 x 1501997 Tongonan geothermal II (Imported Coal*) 4501998 Imported Coal 3001999 Imported coal 2 x 3002000 Imported coal 2 x 3002001 Coal (imported/domestic) 2 x 300

* Fall back alternatives which need to be prepared for the eventthat geothermal resources cannot be committed on time.

24. This investment program is radically different from NPC's latestpublished investment program, which is heavily dependent on domestic coal andhydropower. Our least-cost analysis indicates that NPC should:

(a) defer its plans to construct the San Roque (390 MW), Casecnan (268MW) and Binongan (175 MW) hyrdo projects until and unless furtherstudies show substantial reduction in the estimated cost of theseplants; only installation of Kalayaan pump storage appearseconomical in conjunction with and complementary to the Tongonanplant;

(b) cancel its plan to construct the Isabela coal units (300 MW);

(c) cancel plans for construction of the Northern Luzon EHV (extra highvoltage) line which would have been needed in conjunction withIsabela and the hydro units;

- ix -

(d) change the design of Calaca II from dependence on domestic coal tothe use of either imported or domestic coal, but plan to useimported coal at least until the late 1990s;

(e) include the Tungonan geothermal project in its development plan; and

(f) continue to carry out preparation studies of plants using importedcoal to be implemented if (i) the demand grows faster than assumedhere, (ii) Luzon geothermal is not available in full capacity forcommissioning in 1993, or the Tongonan plant cannot be constructedfor commissioning in 1995.

25. It is very important to note that the main thrust of the least-costplan is the composition of the program based on the viability of thecandidates included in the program (Luzon geothermal, Tongonon geothermal andimported coal) and the non-viability of candidates excluded from the p-ogram(further domestic coal, and hydro power plants). The commissioning dates forthe included candidates can and should be adjusted based on growth in demandand practical constrainLs in implementation. In particular, the commissioningdates indicated in the program are based on full availability of Luzongeothermal resources. If PNOC cannot commit the timely availability of 330 MWfor commissioning in 1993, a 110 MW of Luzon geothermal should be constructedfor commissioning in 1993 and a 300 MW coal unit should bie built forcommissioning in 1994. As stated earlier, the development strategy for thepower sector should be (a) to commission Luzon geothermal plants as much andas early as possible (b) to develop Tongonan geothermal as soon as possibleafter the feasibility study is completed and (c) to supplement the gap betweenthe demand and geothermal supply, with thermal plants using imported coal. Inaddition, the short-term shortages in generating capacicy have to be met byinstalling gas turbines. The total capital cost of this investment programwill be US$337.3 million compared with US$3,373 million of the NPC'sdevelopment plan. Taking account of price escalations, the financingrequirements of the mission's proposed program will be about $4,700 million ofwhich US$2,980 million will be in foreign exchange. The mission carried out asensitivity analysis of the least-cost program with respect to assumptions onload growth, fuel prices and capital costs of various plants. This analysisindicates that the above least-cost sequence remains unchanged within areasonable range of variation in underlying assumptions (para. 2.20).However, it is noted that the least-cost development plan should becontinually updated as the underlying parameters change over time.

Key Issues In the Power Sector

26. Aside from the institutional and investment issues discussed above,several critical pricing, operational and financial issues in the sector needto be addressed and resolved for efficient development and operations of thepower sector.

27. Electricity Tariffs. Despite the prevailing perception, electricityprices in the Philippines are not excessively high ccmpared with average ratesin other ASEAN countries. However, the structure of tariffs is noteconomically efficient and leads to inefficient use of power and cross-subsidy

x

among various users. In particular, industrial customers are paying tariffshigher than cost of service in order to subsidize smaller users. The currenttariff structure should be revised to reflect the real cost of supplyingenergy and capacity to different consumers, perhaps even at different times ofday. This task should begin by NPC in cooperation with MERALCO so that long-run marginal cost (LRMC) pricing signals can be provided first to the indus-trial and other large electricity consumers in and around Manila. Over timethis may lead to a better dispersion of energy-intensive industry to otherareas and islands. In the meantime, it will provide a fair basis for chargingand a benchmark against which to measure the need for future tariff changes.

28. Our analysis indicates that a move towards LRMC pricing would notrequire a significant increase in average tariffs. Only after 1991 is a realincrease required. This provides ample time for a revenue-neutral restructur-ing of NPC's and MERALCO's tariffs and for implementation of a trial programof time-of-day metering. The mission's proposal for the capacity and energycharges of an LRMC-based tariff structure is presented in para. 5.12.Implementation of this proposal would reduce the cross-subsidy by .argeindustrial consumers of other customer groups and increase the economicefficiency of electricity use.

29. Power Plant Rehabilitation. Metro Manila has five major fuel oil-fired thermal plants: NPC's Malaya (600 MW), Sucat (850 MW), Manila (200 MW)and Bataan (225 MW) stations and MERALCO's Rockwell station (225 MW). Two ofthese plants (Sucat and Rockwell) are in very poor operating condition andwould need major repairs to remain in service. The Manila and Bataan.stationsare essentially at nameplate rating but need major overhaul work. Malaya hasrecently been rehabilitated and is operating at full capacity at an acceptableheat rate. Analysis carried out by the mission indicates that it is tech-nically feasible to rehabilitate all the derated units but it is noteconomically attractive to proceed with a full unit rehabilitation program inone step because: (a) the cost of full rehabilitation as presently estimatedis, for most of the units, excessively high; (b) the rehabilitated units wouldbe used at low plant factors after 1992-93 when base generation will shiftfrom oil to coal and geothermal energy; and (c) partially rehabilitating theunits to recover lost capacity will permit NPC to evaluate the full rehabili-tation program after the 1990-93 capacity shortage is over.

30. Considering the capacity requirements of the Luzon grid and the costof rehabilitating various plants, it is recommended that:

(a) the Rockwell power plant be retired in due course since its rehab-ilitation is not economically viable and its return to full loadingis likely to face serious environmental objections. The levelizedcost of operating a rehabilitated Rockwell plant is USC5.1/kWh,compared with USC4.8/kWh for a new oil-fired power station;

(b) an action program be prepared immediately for the partial rehabili-tation of Sucat units which, after a two-stage rehabilitation, wouldhave a lev.zlized cost of USC3.6 to USC3.8/kWh, which is the least-cost option compared to the alternatives af full rehabilitation orinstallation of new units;

- xi -

(c) the Bataan and Manila plants have been operating satisfactorily buttheir thermal efficiencies have deteriorated. Bataan unit 1 hassuffered a derating of 3-4 MW. After essential repairs, these unitscould operate at a levelized cost of USC3.1-3.3/kWh while withoutthe repairs the levelized cost would reach about USC4.0/kWh. It istherefore recommended that NPC allocate sufficient funds to purchasethe required spare parts and undertake essential repairs, and

(d) the two-stage rehabilitation of oil-fired power plants, particularlyof the Sucat un5ts, would provide NPC with an opportunity to savesubstantial resources by carrying out most of the rehabilitation in-house and to develop advanced maintenance capabilities through checlose involvement of its staff in all aspects of rehabilitation.However, to develop the capabilty for in-house rehabilitation, NPCwould need to: (i) establish fabrication shops to produce some ofthe spare parts which are presently bought at high prices from theoriginal manufacturers; (ii) augment NPC's central maintenancedepartment to perform the major portion of rehabilitation workscheduled over the next two to three years; and (iii) design acomprehensive training program coordinated with (i) and (ii).

31. MERALCO Transmission/Distribution Losses. In 1986, MERALCO hadsystem losses equivalent to about 21% of net generation. This level of lossesis extremely high and should, based on the technical characteristics of thesystem, be reduced to around 9%. MERALCO did, in fact, reduce its losses frommore than 20% in the 1950s to about 8%, which it maintained during the1970s.

32. Mission's analysis indicate that technical losses are about 9.5Znotably less than MERALCO's own estimate of 11%. Thus, there is only amoderate opportunity to reduce technical losses, a long-term target for theselosses would be about 8%. The first step towards reducing technical losseswould be to identify problem areas through improving the Transformer LoadMonitoring System; surveying serviced areas to establish priorities for systemrehabilitation; and updating computerized distribution records to include newload conditions.

33. Non-technical losses are primarily due to meter tampering by some ofthe large industrial and commercial consumers of electricity. Mission'sanalysis indicates that non-technical losses are about 11.5%, notably higherthan MERALCO's own estimate of 10%. To curb nontechnical losses, MERALCO hasbeen implementing an action program since 1985 which includes investigationand billing recourse, analysis of billing data, monitoring of consumers'monthly consumption and demands, enclosure of meters in steel boxes to preventreoccurance of tampering, advertisement, and elimination of interventions byMERALCO employees and others in the settlement of pilfered electricity ofrelatives and friends. This action program is satisfactory and a reversal intrends has already started. However, the long-term success of the loss reduc-tion program can be achieved only if appropriate legislation is passed toenable electricity distributers to prosecute pilferers more effectively andlevy heavy penalties on consumers involved in pilferage.

- xii -

34. Financial Issues. The power sector represents the largest share ofcapital expenditures in the country and, thus, requires a very effective meansof internal resource mobilization. Currently, the sector faces several struc-tural problems which have created financial constraints in optimizing invest-ment decisions and in allocating sufficient funds for maintenance of plant andequipment. The three major structural problems identified and recommendationsto address them are as follows:

(a) NPC. A chronic shortage of counterpairt funds has hampered NPC'sability to implement its projects in a least-cost manner by causingimplementation delays resulting in cost over-runs and by introducinga bias in favor of investments with large foreign exchange com-ponents which can be financed externally. During 1988-95, NPC'sinvestment requirements envision a local cost content that exceedsits capacity to generate cash from operations by P 26.4 billion; itsoverall financing gap is expected to be considerably larger as thecost and redemption requirements for local currency financing areadded to the investment shortfall. Thus, the overall financing gapis too large to be financed by the government through budgetaryallocations and the short term financing instruments that have beenused in the past are inadequate to meet the large projectedrequirements. In the short term, while its financing requirementsare modest and it is arranging to tap alternative domestic sourcesof long term funds, NPC should make the best use of instrumentsavailable internally through government, including: (a) maintainingits tariff at levels that enable it to realize the 10% maximum rateof return allowed under its statute; (b) auctioning five year bondsthrough the Government's securities auction facility; and(c) seeking some modest additional equity capital from thegovernment. For the medium to long term, NPC needs to cooperatewith financial institutions, institutional investors and privatesyndicates so that they can shoulder some of NPC's capitalrequirements either through the sale of long term financialinstruments or by independent investments in generation facilitiesthrough Build, Operate and Transfer schemes.

(b) MERALCO. Shortages of equity capital have engaged MERALCO to followa pattern of underinvestment in distribution facilities, preventingthe system from expanding in parallel with growth in demand.Because MERALCO tariffs are already set at levels yielding themaximum rates of return permitted under its charter, MERALCO too hasonly limited capacity to increase local currency generated fromoperations. It cannot obtain the credit it currently needs forinvestment without direct government financial support or, alterna-tively, government guarantees of its borrowings. MERAI.CCO plans toraise about P 1.6 billion in new equity capital during 1989-92.Still, its long-term financial health depends on the Government'sabolishing the current practice of allowing the financing of thetotal cost of public utility stock purchases by loans that depend onthe company's dividends for debt service, using the shares them-selves for collateral. Instead, the Government should require thatall purchases of shares in MERALCO and other providers of essential

- xiii -

services, even those transacted between principals, conform tomargin requirements similar to those of the Makati Stock Exchange,which currently requires a margin of at least 50%.

(c) Retailing Constraints. Weak commercial practices at the retaillevel have prevented both NPC and MERALCO from realizing their fullcapacity to generate cash from operations. In addition to theextremely high levels of nontechnical losses incurred by MERALCO,both NPC and MERALCO have experienced difficulty in collectingconsumer charges. When MERALCO and other electricity retailerscould not collect from government sector consurwers, they in turnwere not able to pay NPC. In 1987, the Governm'ent instituted pro-cedures to help the retailers collect the amounts due and encouragedNPC to use all available remedies to enforce its billings. Thesemeasures appear well conceived and comprehensive, but it is stilltoo early to judge their effectiveness.

National Energy Development Strategy

35. Based on the above analysis of sector development potential andoperational issues, the following strategy for energy development isrecommended.

36. In the short-run (1989-90), the power sector will face a shortage ofcapacity due to the rapid recovery of electricity demand, mothballing of thenuclear plant and the downgrading of the Tiwi geothermal plant. To forestallthis shortage, the following options are available to the economy: rehabili-tation of power plants at Sucat and Rockwell; reduction of transmission/distribution losses; management of power demand; and installation of gasturbines. Our analysis indicates that (a) rehabilitation of the Rockwellstation is not viable (para. 26); (b) rehabilitation of the Sucat station isadvisable with a phased program of works (para. 27); and (c) demand managementand loss reduction, though important from an efficiency point of view, willnot significantly affect the capacity requirements of the grid. Thus, themajor source of additional capacity in the short term has to be the installa-tion of gas turbines. Gas turbines are not necessarily wasteful investmentsbecause they can be relocated to serve other grids when they are not needed onLuzon and, as the system increasingly moves towards using coal and geothermalfor base-generation, gas turbines can provide complementary peaking capacity.

37. In the medium-term (1991-93), the new generating capacity should bebased on Luzon geothermal and imported coal. Commissioning of the Bacon-Manito I geothermal power plant is planned for 1991. The other three identi-fied geothermal sites on Luzon--Bacon-Manito II, Pinatubo, and Mt. Labo--havethe potential of supplying at least an additional 330 MW of power. However,assessment and delineation work on these sites needs to be accelerated. Aminimum of 9-12 geothermal wells should be drilled during the next 18-24months so that the steam fields at one or more of these sites can be committedfor development by the end of 1989. The least-cost development plan includesBacon-Manita II and at least one more site to be commissioned in 1992 and1993, respectively.

38. In the long-term (1994-2000) the options to increase generatingcapacity are Tongonan geothermal, imported coal, domestic coal, and, possibly,

- xiv -

further geothermal resources on Luzon. In view of the long lead timesinvolved in development and utilization of indigenous energy resources,several immediate actions are necessary if timely policy decisions are to bemade. In particular, (a) the feasibility study of the Tongonan project shouldbe commissioned immediately so that the results are available by the middle of1989 in order for NPC and the Government to decide between Tongonan and thefurther use of imported coal; (b) the program of geothermal exploration shouldbe corninued on Luzon with a minimum of three to five wells drilled per year;and (c) the Government should announce a policy that any geothermal steam thatcan be provided by a company, private or public, will be used in the powersector if it is available at a price lower than the power company's avoidedcost. However, the complementary component, as well as, the fall-backalternative to geothermal energy is imported coal. Thus, NPC should continueits preparation of coal power plants for implementation in the medium- and thelong-term.

I. AN OVERVIEW OF THE ENERGY SECTOR

A. The Macroeconomic Context

1.1 Most of the problems of the Philippines' energy sector today are abyproduct of the political and economic turbulance that the country hasexperienced since the beginning of the 1980s. This makes planning especiallydifficult. After growing faster than 6% per year during the last half of the1970s, GNP stagnated and then fell by more than 10% during 1984-85. It nowshown signs of recovering with an encouraging growth of 5.1% in 1987. Energydemand followed a similar pattern, but peaked in 1979, fell by nearly aquarter by 1985 and then recovered strongly to surpass its 1979 peak in 1987.

1.2 During the last half of the 1970s, investment averaged 30% of GNPand energy accounted for nearly half of total public sector investment. Underthe macroeconomic stabilization program of the mid 1980s, overall investmentwas cut back sharply to around 14% of GNP. This could not have been achievedwithout a significant cut in energy investment. In constant prices, the 1986level of energy sector investment was only 30% of its 1979 level. The declinehas been particularly pronounced in the geothermal subsector. In addition, amajor product of the earlier investment--the nuclear power plant--is notavailable for use following the Government's decision to mothball it.

1.3 The new legal and institutional structures being developed through-out the Government have had a major impact on the energy sector. The Ministryof Energy (MOE) has been abolished, and new people have been appointed to headthe major agencies involved in the sector. Legislative ccLmittees now take anactive interest in energy pricing and investment decisions. But the coordina-ting machinery is not yet in place to permit the input of all these bodies andstill enable prompt and lasting decisions to be made.

1.4 Thus the energy sector faces a number of challenges as thePhilippines emerges from its successful stabilization program and refocusesits efforts on economic recovery and growth. The remainder of this chapterprovides an overview of energy resources and production, demand patterns andgrowth, institutional developments and policy priorities. Subsequent chaptersdiscuss each of the energy sabsectors in greater detail.

B. Energy Resources and Production

1.5 Unlike many of its ASEAN neighbors, the Philippines is not wellendowed with indigenous energy that can be economically developed. After theenergy price increases of the early 1970s, a major effort was made to exploreand develop the available resources and, as a result, the country became aproducer of geothermal steam (1978) and oil (1979), in addition to coal andhydropower. However, proven oil reserves amount to only 4 million tons andproduction has been declining since 1983. Geothermal reserves are not yetfully evaluated, but could exceed 8,000 MW. Only 1,640 MW has been proven sofar. The total potential coal resource is estimated at about 1,500 milliontons but most of it is low grade and expensive to mine. Hydro resources arequite substantial, with a theoretical power potential in excess of 10,000

- 2 -

MW. However, the better sites are distant from the gria and thus expensive to

use. Non-conventional energy sources sucli as agricultural wastes and bio-

masses are plentiful, and the Philippines has beer in the forefront of inter-

national efforts to develop them. By 1926 non-conventional energy supplied

18.5% of the Philippines' total energy use.

1.6 Despite its relatively modest commercial energy endowment, the

Philippines has made great efforts to reduce dependence on imports. As shown

in Table 1.1, the country moved from a position of 6Z self-supply of commer-

cial energy in 1975 to over 30% by 1984. The mid-1980s was probably a turning

point for that ratio due to a combination of factors: (a) technical

constraints on expanding oil production, (b) economic constraints on expanding

coal and hydro based on the likelihood of continued weakness in imported coal

prices, and (c) a revival of energy demand growth. As discussed inChapter II, the only indigenous energy resource that merits significant new

investment is geothermal steam.

Table 1.1: ENERGY PRODUCTION('000 TOE)

Self-supplyCoal Oil Hydro Geothermal Total Ratio /a

1975 36 - 560 - 596 6

1980 23 490 877 517 1,861 15

1981 22 252 932 690 1,896 16

1982 102 483 939 881 2,406 20

1983 377 657 739 1,015 2,788 23

1984 571 524 1,314 1,128 3,537 32

1985 554 358 1,383 1,227 3,521 32

1986 593 423 1,498 1,140 3,654 33

1987 573 274 1,300 1,128 3,275 27

Z of total 17.5 8.4 39.7 34.4 100

Average Annual Growth Rates

1982-87 41.2 -10.7 6.7 5.1 6.4

/a Total indigenous production as a percent of commercial primary energy

requirements (i.e., including losses in transformation and distribution).

- 3 -

C. Energy Demand

1.7 During the 1970s the Philippines was one of the first oil-importingdeveloping countries to adopt a comprehensive program of energy conservationand demand management. Through both price increases and targetted energyaudits, a sustained effort was made to check the growth in consumption. Thesuccess of this effort is shown in Table 1.2. From a peak of 9.2 million TOEin 1979, commercial energy consumption fell to a trough of 7.1 million TOE in1985. At the same time, the proportion accounted for by oil was reduced from88% to 74%. With the resumption of economic growth in the Philippines in1986, these trends have been reversed.

1.8 Such a reversal does not indicate a relaxation of the conservationprogram; petroleum consumption remains heavily taxed and the energy auditprogram continues to expand to reach more industries. However, with inter-national energy prices below their levels of the late 1970s, and with theconsiderable progress already achieved in cutting excessive energy use, it isappropriate that energy demand management be redirected. The Office of EnergyAffairs (OEA) is well placed to undertake the coordination and strategicplanning roles which will be needed as sector objectives change to permitresumption of demand growth and increased imports where fc-eign sources areclearly cheaper than indigenous ones (para. 1.11).

Table 1.2: ENERGY CONSUMPTION /a('000 TOE)

Coal Oil Electricity Total Z Oil

1975 25 6,979 732 7,736 90

1979 66 8,130 1,052 9,248 881980 89 7,371 1,110 8,57Cj 861981 87 6,979 1,171 8,227 851982 91 6,869 1,263 8,223 841983 320 6,769 1,474 8,563 791984 390 5,465 1,470 7,325 751985 319 5,229 1,554 7,102 74

1986 305 5,860 1,366 7,530 781987 343 7,816 1,452 9,611 81

Average AnnualGrowth Rates

1982-87 30.4 2.6 2.8 3.2

1987-92 11.0 4.2 5.5 4.7

/a Net domestic consumption, after transformation and distribution losses.

- 4 -

1.9 Annex 1.1 presents the 1987 energy balance for the Philippines. Assummarized below in Table 1.3, it shows that the industrial sector accountsfor 51% of total energy demand, followed by transport with 32%. Electricityprovides over half the commercial energy used by the residential/commercialsector and llX of that used by industry. Over 80% of total energy demand ismet by petroleum products, of which the transport sector consumes only 40%.As economic growth is diversified away from heavy industry, it is likely thatthe share of energy used for transport and by the residential/commercialsectors will increase. Much of this increase can only be met by petroleumproducts. Thus, diversification away from oil in the power sector (seeChapter V) will be the only significant way to keep oil imports from growingrapidly.

Table 1.3: DISTRIBUTION OF ENERGY DEMAND, 1987('000 TOE)

Residential &commercial Industrial Transport Other Total Percent

Coal - 343 - - 343 3.6

Oil 604 4,022 3,030 160 7,816 81.3

Electricity 771 542 - 139 1,452 15.1

Total 1,375 4,907 3,030 299 9,611 100.0

Percent 14.3 51.1 31.5 3.1 100.0

D. Institutional Framework

1.10 There have been a number of major changes in the institutionalframework of the energy sector since it came into prominence in the mid-1970s. The basic organization of the sector was established by a PresidentialDecree in 1977 which created the Ministry of Energy (MOE) as the centralpolicy, planning and regulatory body for energy. The MOE had two major parts:a Bureau for Energy Development (BED) and a Bureau for Energy Utilization(BEU). In addition to the creation of the new Ministry, the responsibilitiesof the Philippine National Oil Company (PNOC) were extended to include thedevelopment of indigneous hydrocarbon and geothermal resources. The NationalPower Corporation (NPC), which is responsible for power generation and trans-mission, and the National Electricification Administration (NEA), which isresponsible for rural electricification, were also strengthened. PNOC and NFCwere attached to MOE for program and policy coordination which was handled byan internal committee chaired by the Minister of Energy. The Minister alsoserved as chairman of the boards of PNOC and NPC. This centralized structure

- 5 -

contributed to the Philippines' rapid and successful drive to develop indige-nous resources and to curtail consumption, yet it also suffered from a lack ofindependent oversight and accountability.

1.11 With the change in government in 1986, the MOE was abolished and itsfunctions were temporarily assumed by the Office of the President. The twomain bureaux of the MOE were placed under a Deputy Executive Secretary forEnergy in the President's Office pending the report of the President'sCommission on Government Reform. Through the issuance of Executive Order(E.O.) No. 193 in July 1987, the Office of Energy Affairs was mandated to takeover the bulk of the functions of the former MOE, but to be organizationallydistinct from PNOC and NPC and to remain under the Office of the President.In addition, the regulatory, environmental and watershed management functionsof MOE were reallocated, respectively, to the Energy Regulatory Board (E.O.172) and the Department of Environment and Natural Resources (E.O. 131).

1.12 This new organization of the sector is consistent with theGovernment's policy of decentralized decision-making and eventual privatiza-tion of the commercially viable public enterprises. However, there is a needfor closer coordination and a central focus for decision-making by those partsof the sector which represent natural monopolies and whose investments areinterdependent. In particular, the development policies for the geothermal,coal and power subsectors are largely interwined and none of the three canpursue an efficient strategy without close coordination with the other two.The OEA has a mandate to play this coordinating role but lacks the authorityto enforce its decisions.

1.13 An immediate action to relive the situation is to create acoordinated planning mechanism across the various sub-sectors. In the absenceof a separate department of energy, it is suggested that an EnergyCoordination Council be set up in the Office of the President to be headed bythe Executive Secretary, with the Presidents of NPC, PNOC and SCC and theExecutive Director of the OEA as members. The OEA should prepare a long-termplan for energy development for the country, in consultation with the threemajor public sector agencies involved and under the overall framework ofeconomic plans prepared by NEDA. This plan should be formally ratified by theEnergy Coordination Council on an annual basis. All investments in the energysector which require the commitment of government funds should be inconsonance with the energy plan approved by the Energy Coordination Council.It should be the responsibility of the OEA to ensure this through appropriateintercessions in the deliberations of the Investment Coordinating Committee(ICC). It should also be the responsibility of OEA to carry out studies ofvarious energy issues and ensure implementation of government policy regardinginvestment planning, pricing and operational performance of the energy sector.

- 6 -

II. THE POWER SECTOR DEVELOPMENT PROGRAP'

A. Introduction

2.1 The National Power Corporation (NPC) is responsible for the planningand operation of seven separate grids in the Philippines. These may be div-ided into three regions: the Luzon power grid (installed capacity 4,111 MW),five island grids in the Visayas islands (agaregate installed capacity 600MW), and the Mindanao grid (installed capacity 1,067 MW). Luzon is the mostimportant of these regions, accounting in 1986 for 114,756 CWh or 77% of totalelectricity generation, compared to Mindanao (3,040 GWh, 16%), and the Visayasgrids (collectively accounting for 1,467 GWh, or 8%).

2.2 The grids exhibit significantly different characteristics in theirgeneration plant mix; the Mindanao grid is heavily dependent (83%) on hydrocapacity. In the Visoyas, on the other hand, the individual grids on theislands of Leyte and Negros are similarly dependent (approximately 84%) ongeothermal capacity, with a mix of oil and coal plant in the remaininggrids. The Luzon power grid is the most diversified, with oil, coal,geothermal and hydro plant.

2.3 Because of its size and importance, the major issues for powerdevelopment arise in connection with the future development of the Luzon powergrid. Accordingly, the major part of this chapter focusses on the least-costdevelopment plan for Luzon, including an analysis of load forecasts, presentgenerating facilities, the least-cost expansion plan developed by the missionand sensitivity analysis.

B. Demand Forecasts

2.4 Growth of electricity sales for the Luzon power grid over the. period1971-80 averaged around 6.9% p.a., but dropped sharply in the first half ofthe 1980s, to an average growth rate of 1.7% p.a., and to negative grow-thrates in 1984 and 1985 (Table 2.1). The last two years, however, have wit-nessed a significant recovery, with a demand growth for sales of 2.4% in 1986,and over 10% in 1987. Energy sales in 1987 totalled 14,967 GWh, with a systempeak demand of 2,592 MW. Losses in generation and transmission are currentlyof the order of 9%, and the annual system load factor is around 70%.

Table 2.1: HISTORICAL ELECTRICITY DEMANDS

Sales Generation PeakGWh X p.a. GWh MW Load factor

1970 6,047 - 6,400 n.a. n.a.1971 6,688 10.60Z 7,569 n.a. n.a.1973 7,725 8.15% 8,227 1,335 70.35%1974 7,805 10.04% 8,262 1,379 68.39%1975 8,506 8.98Z 9,037 1,513 68.18%1976 9,200 8.16% 9,652 1,659 66.42%1977 9,813 6.66% 10,380 1,729 69.33%1978 10,749 9.54% 11,222 1,780 71.97%1979 11,645 8.34% 12,504 1,926 74.11%1980 12,163 4.45% 13,115 2,074 72.19%1981 12,690 4.33% 13,666 2,225 70.11%1982 13,125 3.43% 14,398 2,364 69.53%1983 13,907 5.96% 15,294 2,478 70.46%1984 13,243 -4.77% 14,655 2,374 70.47%1985 13,221 -0.17% 14,449 2,311 71.37%1986 13,542 2.43% 14,756 2,435 69.18%1987 14,967 10.52X n.a. 2,592 n.a.

2.5 NPC's load forecasts are based on analysis of sectoral demands usingdemographic and economic data. The latest (February 1988) forecast of elec-tricity generation for the Luzon power grid reflects the recent increase indemand, and is somewhat higher than the previous (September 1986) forecast.This forecast is based on GDP growth rates of 5.81 in 1988-92, and 6.3X for1993-2000 and is considered reasonable to be used as the normal scenario forleast-cost analysis. The mission developed also High and Low growthscenarios. The High-growth scenario is based on a GDP growth rate of 7.5%p.a. The Low-growth scenario is based on a GDP growth rate of 5.2% p.a. Theresultant demand projections are summarized in Table 2.2. Overall growthrates of electricity generation for the period 1987-2000 are 6.5% p.a. for thehigh growth scenario and 4.8% p.a. for the low growth scenario, compared to5.4% for the normal scenario. Under the normal scenario, electricity genera-tion in the year 2000 is predicted at 32,472 GWh, under the high scenario37,121 GWh (141 higher), and under the Low scenario 29,996 GWh (8% lower).

- 8 -

Table 2.2: SCENARIOS FOR GROWTH IN DEMAND(Average Growth Rate per Annum)

Period Base High Low

1987-90 6.15% 7.16% 6.09%1990-95 5.47% 6.92% 4.64%1995-2000 4.97% 5.76% 4.19%

1987-2000 5.44% 6.53% 4.8%

C. Present Generating Facilities

2.6 The current total installed capacity of the Luzon interconnectedsystem is around 4,111 MW, comprising 47% oil, 30% hydro, 16% geothermal, and7% coal fired capacity. For the oil-fired units, rehabilitation programs havebeen recently completed or are planned. In addition to NPC's units, a pro-posal is under consideration for rehabilitation of MERALCO's Rockwell powerstation, which has an installed capacity of five 25 MW and three 60 MWunits. Although the plant was retired in 1984, the 60 MW units were laterbrought back into limiLed service to augment supply to the Metro Manilaarea. The technical and economic assessment of this proposal is given inChapter VI. NPC's hydro capacity totals 1,226 MW, which includes a 300 MWpumped storage plant at Kalayaan. Seasonal variations in hydro flows restrictthe output of hydro stations significantly during the dry season. Geothermalplants are located at two sites in Luzon, Makiling-Banahaw and Tiwi, each ofwhich has six units of 55 MW nominally rated capacity. Owing to anticipatedreduction of steam output at Tiwi, a program has been drawn up to prematurelyretire two units at that site in 1988/89 and one more in 1992/93. NPC alsooperates a single 300 MW coal-fired unit at Calaca, which was commissioned in1984. This unit, though intended to burn local (Semirara) coal, cannot attainfull capacity with that coal, and currently operates on a blend of imported(Australian) and local coal. The 620 MW nuclear plant at Bataan reached anadvanced state of construction, but has for several years been mothballed. Itis not envisaged for the purposes of this study that this plant will be com-pleted and commissioned.

2.7 The major components of NPC's current generation expansion programare two 55 MW units at a new geothermal site at Bacon-Manito (1991), and a 300MW coal-fired unit as an expansion to Calaca (1992). In addition, at least200 MW of gas turbines are to be installed around 1989/90. This, togetherwith the rehabilitation program for Sucat Units 1 and 4 (recovering a total of120 MW), will add 730 MW of capacity through 1992. In view of the anticipatedrapid load growth up to the mid 1990s, however, some concern has beenexpressed as to the possibility of a capacity shortfall up to the date of com-missioning of the 300 MW coal unit in 1992. Consideration of the existing andcommitted plant complement in relation to the demand growth would seem to

- 9 -

indicate that there will be sufficient capacity over the period. This is con-tingent upon sufficient capacity being available from hydro during the dryseason (despite an installed conventional hydro capacity of 926 MW, NPCconsiders the guaranteed capacity during dry periods to be only about 200 MW).Furthermore, the Tiwi geothermal plant suffers from gradual derating inbetween scheduled outages owing to build-up of deposits, and this wouldfurther erode the capacity margins. Several measures can be contemplated toalleviate the shortfall, should it materialize. These include acceleratingthe current planting-up program, increasing the rated capacity of committedplant, introducing new plant such as additional geothermal and gas turbines,reducing losses, and demand management. Of these options, perhaps the mostrealistic at this point is the installation of additional gas turbines, asthese can be commissioned within a comparatively short lead time. Accord-ingly, should a continued high rate of demand growth increase the likelihoodof this capacity shortfall, or if the current expansion program is delayed,then the installation of additional gas turbines will be necessary in themedium term, and NPC should take appropriate steps to allow for this.

D. Least Cost Expansion Plan

2.8 NPC's current (June 1987) generation expansion plan for the Luzonpower grid is shown in Annex 2.1. Apart from the ongoing committed develop-ment program, post-1992 installations include further expansions to the geo-thermal complement (totalling 550 MW through the year 2000), a local coalplant (Isabela) of 300 MW in 1995, further hydro plants at San Roque,Casecnan, and Binongan (totalling 833 MW), and additional 300 MW coal units in1999 and 2000 (coal source not identified). The mission undertook an indepen-dent assessment of the least-cost development plan, based on the revised loadforecast and the latest available data on the capital and fuel costs ofvarious alternatives.

Options for Future Expansion

2.9 Apart from the two Luzon geothermal fields which are currently pro-ducing, further geothermal resources have been identified in Luzon with aproven reserve of around 530 MW, and a total probable reserve of over 1,300MW. The Tongonan geothermal fields in Leyte (Visayas) have a resource baseestimated at between 480-1,200 MW. The mission assessed the economic cost ofgeothermal steam (production cost for future wells plus an exploration riskpremium) to be USC1.63/kWh generated, while that of Tongonan was estimated atUS1.O07/kWh. Transmission from Leyte to Luzon, however, requires high-voltagelines and cables over a distance of around 480 km, including a submarineportion of around 25 km; this will substantially increase the delivered costsof power.

2.10 For indigenous coal, the source of particular interest for Luzonpower development is Semirara, a small island to the south, where the existingmine serves part of the needs of NPC's 300 MW coal station at Calaca, and canbe expanded to meet future local coal needs for power generation. With acalorific value of 7,200 BTU/lb, the economic delivered cost of futuresupplies of Semirara coal has been estimated at US$40/ton CIF or US$2.53/MBTU.The Isabela coal deposits in Luzon which feature in the June 1987 development

- 10 -

plan have been assessed to be uneconomic for the purposes of generation expan-sion in the foreseeable future (Chapter III). Imported coal is also an optionfor future thermal plant. This is currently available on the internationalmarket from Australia, China and other sources. Current prices of importedcoal are fairly low, of the order of US$30/ton for a calorific value of 12,000BTU/lb; they are, however, expected to increase in the future fromUS$1.21/MBTU in 1988 to around US$1.52/MBTU by 1992, and to escalate by 1%p.a. from 1995 onwards, reaching a level of US$1.59/MBTU by the year 2000.

2.11 Several hydro sites in Luzon have been identified by NPC as candi-dates for future system development, some of them being multi-purposeschemes. Feasibility or prefeasibility studies have been conducted for mostof these sites and provide sufficient data at the planning level for anassessment of the economics of this option. NPC's pumped storage plant atKalayaan, currently consisting of 2 x 150 MW pump-generators, can also beexpanded further to an additional 300 MW.

Levelized Generation Costs

2.12 The lifetime levelized generation costs (LGC) for the thermal andgeothermal base-load options, as estimated by the mission, are given inTable 2.3. Annex 2.2 details the methodology, data, and results of the LGCanalysis. The lowest-cost alternatives are Tongonan geothermal with HVACtransmission and Luzon geothermal--relative to the imported coal option, theLGCs for these candidates are 21Z and 16% cheaper, respectively. Othercandidates, in increasing order of cost, are Tongonan/HVDC (11% lower thanimported coal), oil (252 higher) and Semirara coal (30Z higher). Therefore,the most promising options for thermal and geothermal expansion are Luzon geo-thermal, Tongonan geothermal, and imported coal. Oil and domestic coal, onthe the other hand, are significantly more expensive and not competitive.

i

- 11 -

Table 2.3: LEVELIZED GENERATION COSTS

Plant Capacity LGC

ThermalImported coal 300 MW 3.46 cts/kWhSemirara coal 300 MW 4.50 cts/kWhFuel oil 300 MW 4.32 cts/kWh

GeothermalLuzon geothermal 55 MW 2.90 cts/kWhTongonan geothermal- HVAC transmission 450 MW 2.72 cts/kWh- HVDC transmission 450 MW 3.10 cts/kWh

HydroPantay 23 MW 7.09 cts/kWhSan Roque 390 MW 6.61 cts/kWhCasecnan 268 MW 5.54 cts/kWhAbra 174 MW 7.96 cts/kWhDiduyon 352 MW 5.83 cts/kWhBalogBalog 33 MW 9.74 cts/kWhAgos (Kaliwa) 140 MW 12.72 cts/kWhMatuno 180 MW 9.11 cts/kWhGened 600 MW 9.69 cts/kWh

2.13 As a comparison to the thermal and geothermal alternatives, theLGCs for hydro candidates are also summArized in Table 2.3. This shows thatcompared to the thermal and geothermal options, hydro candidates are notcompetitive-the lowest-cost (Casecnan) at 5.54 cts/kWh is 23X higher thaneven a domestic coal plant.

2.14 As the economic generation cost from Luzon geothermal issignificantly lower than that for imported coal, which is the next candidatefor development in lieu of geothermal, there is some latitude in price-settingfor geothermal steam. The break-even fuel price (i.e., the steam price whichyields the same cost per kWh generated as imported coal) is the "avoided cost"for the system. This was computed to be 2.40 cts/kWh in relation to the nextplanting-up, with imported coal priced at its economic cost (i.e., excludingduties and taxes). If imported coal is priced at financial cost, the break-even price for Luzon steam is 2.75 cts/kWh.

WASP Analysis

2.15 Based on the normal scenario of load growth (para. 2.5), and capitaland fuel costs of various candidate plants (Annex 2.3), a least-cost expansionplan was derived for the Luzon power grid over the period 1987-2001, using theWASP computer program. Details are given in Annex 2.4. The results (Table

- 12 -

2.4) confirm that Luzon geothermal and imported coal are clearly prioritycandidates--a total 495 MW Luzon geothermal capacity and 2,100 KW importedcoal capacity are in the least-cost plan over the period 1991-2001. Inaddition, the first stage of Tongonan geothermal (450 MW), with the assumptionof an HVAC line, is selected in 1995, followed by the second stage in 1997.Apart from these thermal/geothermal plants, the Kalayaan pumped storage plant(300 MW) features in the optimal solution from 1996. Local coal plant, gasturbines, and hydro candidates are not selected before 2000; this confirms theprevious LGC analysis. The capital cost of new capacity additions is $3,373million, and capital cost disbursements for this program reach a peak ataround $440 million in 1995/97. The objective function (total discountedoperation and capital cost, plus allowance for salvage value of new plant atthe planning horizon) amounts to $3,899 million over the fifteen-year period1987-2001. The underlying assumption regarding the interconnection from Leyteto Luzon is an HVAC line with the current estimated cost of $210 million. Incase the transmission requirement dictates an HVDC line, the strict least-costsolution would be to construct the Tongonan interlink in 1997-98. However,the additional cost of bringing the implementation forward to 1995-1998 wouldbe less than 1Z of the total discounted cost.

Table 2.4: LEAST-COST DEVELOPMENT PROGRAM

Year Plant Capacity (MW)

1989 Gas turbines 2001991 Bacon-Manito I geothermal 1101992 Bacon-Manito II geothermal 110

Calaca II coal 3001993 Luzon geothermal (Imported Coal*) 3301995 Tongonan geothermal I (Imported Coal*) 4501996 Kalayaan pumped storage 2 x 1501997 Tongonan geothermal II (Imported Coal*) 4501998 Imported Coal 3001999 Imported coal 2 x 3002000 Imported coal 2 x 3002001 Coal (imported/domestic) 2 x 300

* Fall back alternatives which need to be prepared for the eventthat geothermal resources cannot be committed on time.

2.16 In light of the above least-cost development plan, the followingrecommiendations can be made:

(a) In view of the important position of geothermal resources, effortsshould be made to prove and undertake necessary preparatory activi-ties for the timely exploitation of these indigenous resources bothin Luzon and in Leyte (Tongonan).

- 13 -

(b) NPC should take steps to prepare for a program of investment incoal-fired plant. Should the demand grow faster than assumed here,NPC would need to construct coal plants. In addition NPC may needto use imported coal as a fall-back alternative in case Luzongeothermal cannot be fully committed or the Tongonan plant does nctprove viable or if its implementation tak'i longer than expected.

(c) The viability of transmission of Tongonan geothermal power to Luzonneeds to be carefully studied to narrow down the alternatives avail-able (e.g. choice of DC or AC, routing), to establish reliableupdated cost estimates, to assess the impact of the interconnectionon the development of the existing transmission system, and toaddress operational aspects, including system reliability andsecurity.

(d) The identification of the expansion of Kalayaan pumped storage aspart of the optimal development sequence will necessitate anupdating study of this project so that it can proceed on schedulewhen required.

(e) Luzon transmission development as a whole will have to be assessedin light of the above development sequence. In particular, thecurrently planned transmission development north of Manila toaccommodate Isabela and the hydro plants should be deferred to alater stage.