Embed Size (px)

Citation preview

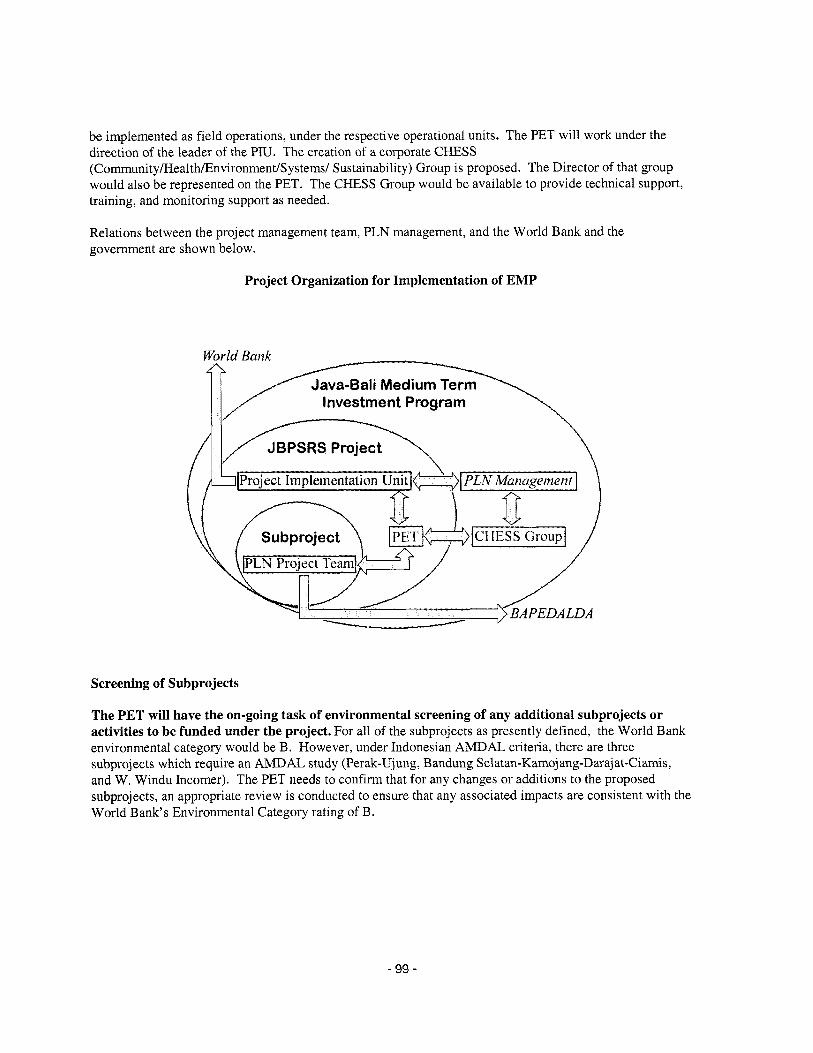

Document of The World Bank

FOR o m c u USE ONLY

Report No: 254144”

PROJECT APPRAISAL DOCUMENT

ON A

PROPOSED LOAN

IN THE AMOUNT OF US$141 MILLION

TO THE

REPUBLIC OF INDONESIA

FOR A

JAVA-BAL1 POWER SECTOR RESTRUCTURING AND STRENGTHENING PROJECT

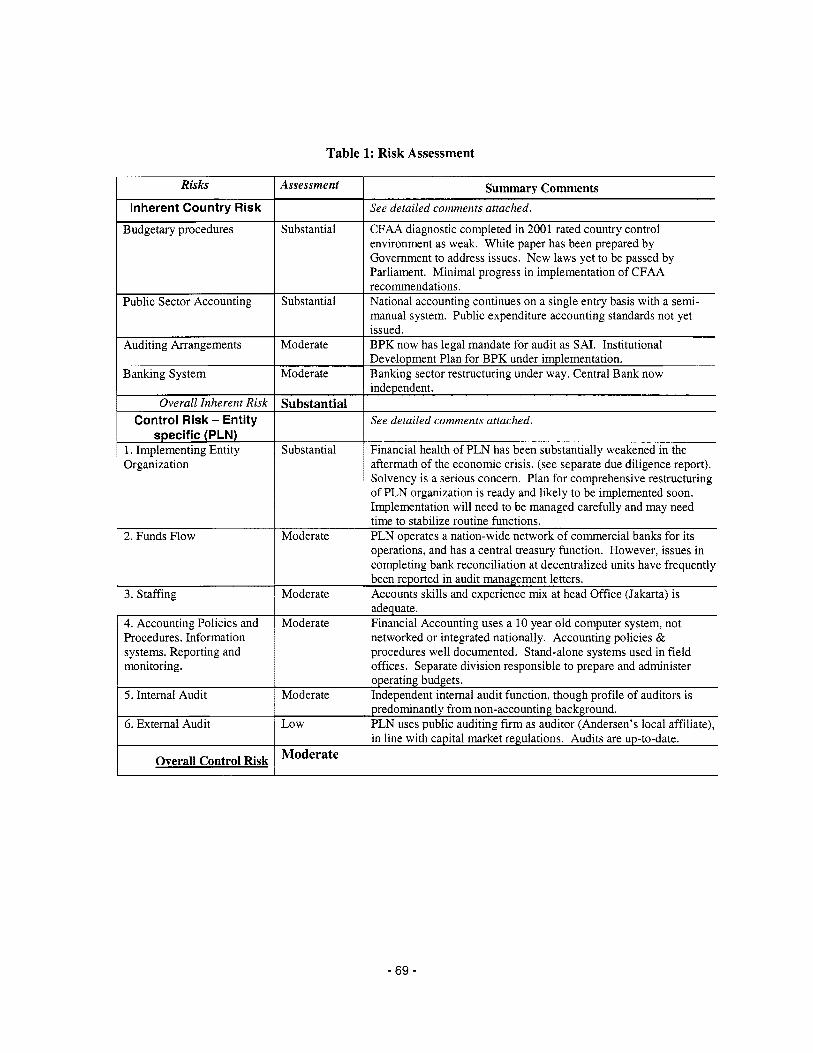

June 4,2003

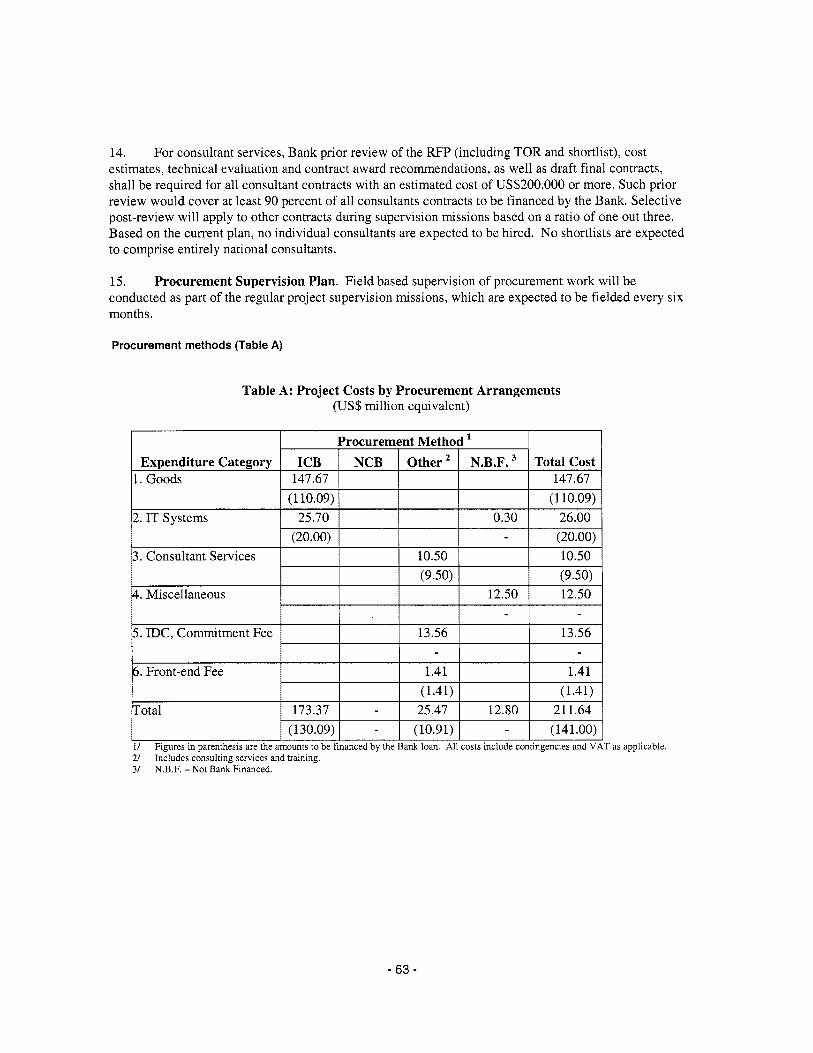

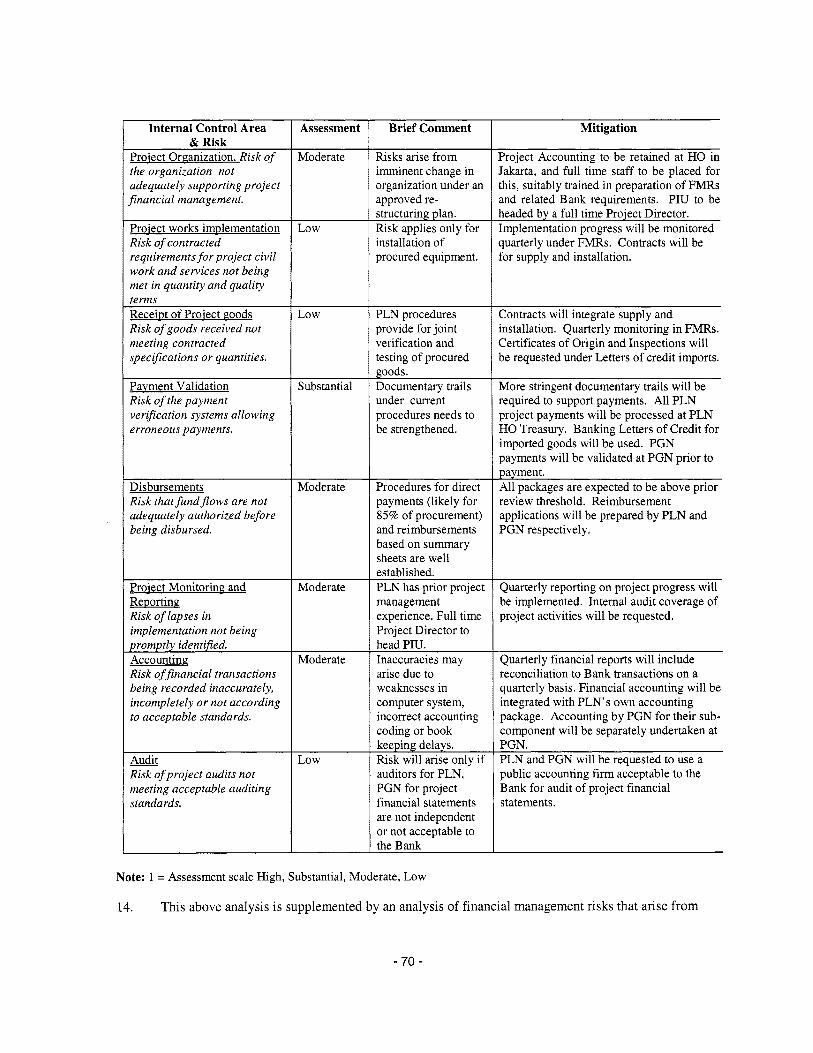

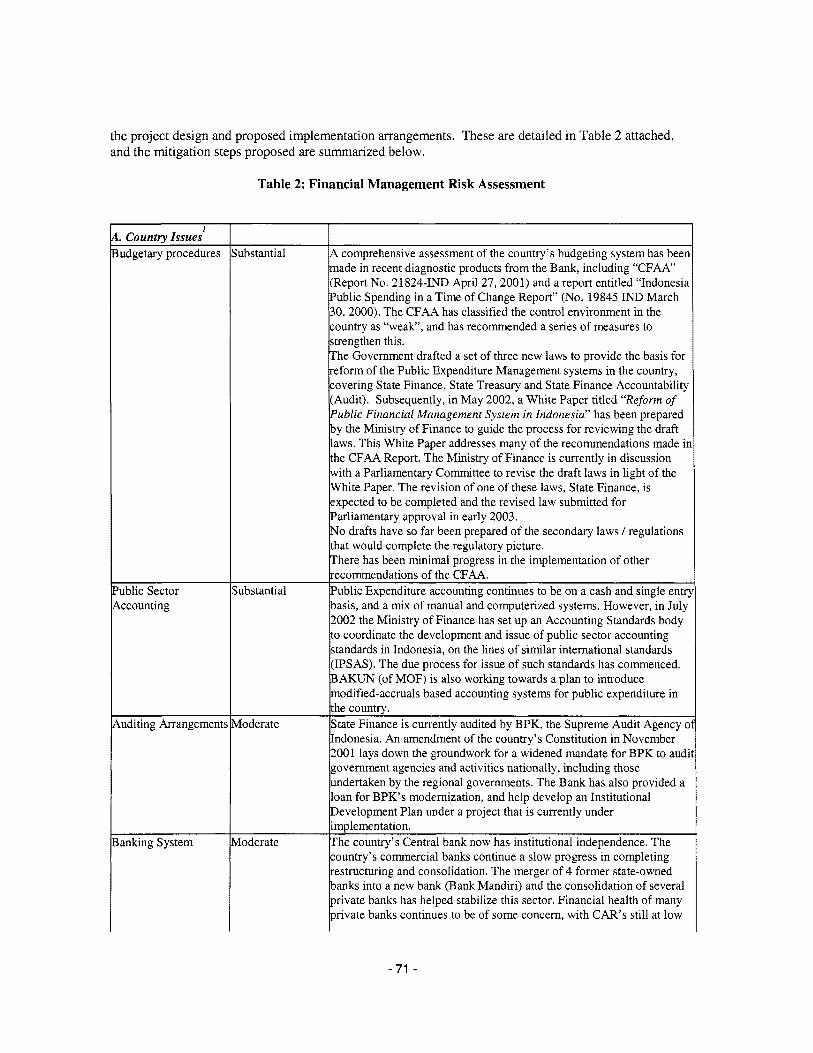

Energy and Mining Sector Unit East Asia and Pacific Region

This document has a restricted dfstribntion and may be used by ncipientr only in the performance of their official duties Its contenb may not otherwise be disclosed without World Bank aathorizatioa

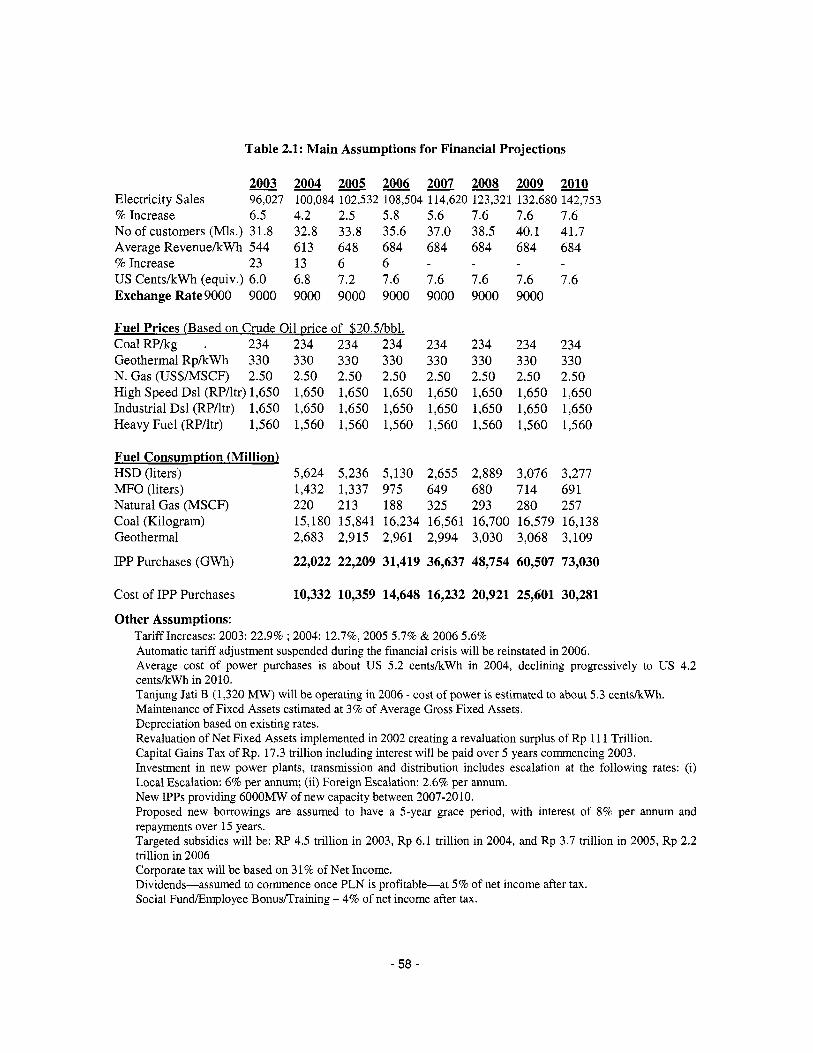

Pub

lic D

iscl

osur

e A

utho

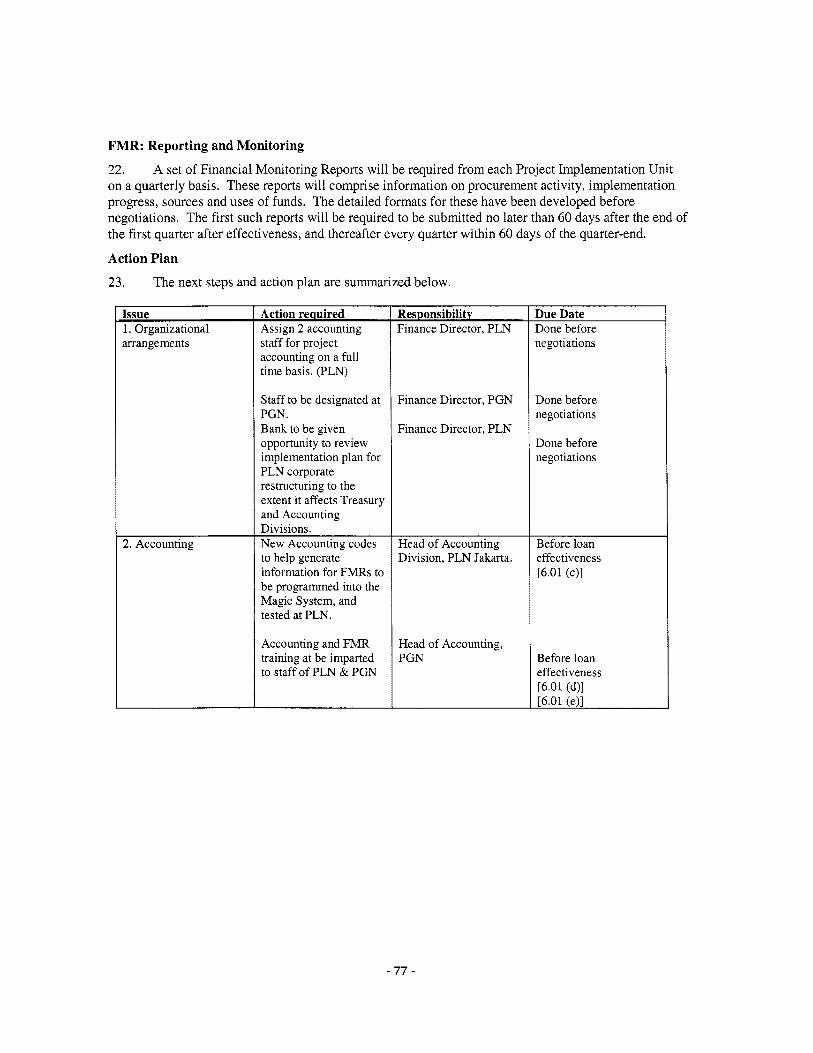

rized

Pub

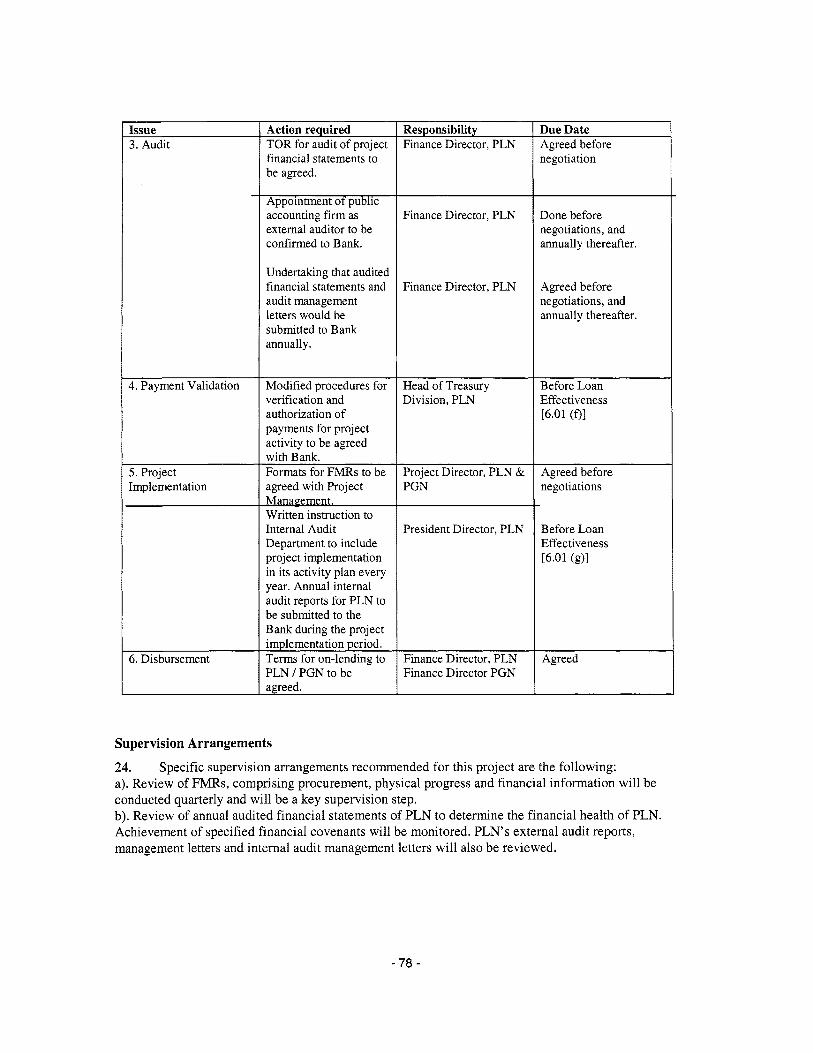

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective as of December 3 1,2002)

Currency Unit = Indonesia Rupiah (Rp) Rp = US$0.0001121

US$1 = 8,917.5

FISCAL YEAR Govemment of Indonesia -- January 1 - December 3 1

ABBREVIATIONS AND ACRONYMS ADB AMDAL ANDAL ATAM CIS DGEEU DSM EIRR EMP EMSA ERP GO1 ICB IDC IP IPO IPP IRP I T JBIC KEIII LARPF LNG LRMC MIGAS MOU NPV P3B PET PGN PIU PJB PLN PPA PTDII RKL/RPL UKLNPL USAID

Asian Development Bank Analysis of Impacts on the Living Environment Environmental Impact Analysis Automatic Tariff Adjustment Mechanism Customer Information System Directorate General of Electricity and Energy Utilization Demand Side Management Economic Intemal Rate of Return Environmental Management Plan Electricity Market Supervisory Agency Enterprise Resource Planning Govemment of Indonesia Intemational Competitive Bidding Interest During Construction Subsidiary generating company of PLN (Jakarta) Initial Public Offering Independent Power Producer Integrated Resource Planning Information Technology Japan Bank for Intemational Cooperation Export-credit loan package 111 Land Acquisition and Resettlement Policy Framework Liquefied Natural Gas Longmn Marginal Cost Directorate General of Oil and Gas Memorandum of Understanding Net Present Value PLN’s Java-Bali Ttransmission System Business Unit Project Environmental Team Indonesia’s State oi l and gas company Project Implementation Unit Subsidiary generating company of PLN (Surabaya) Indonesia’s State power company Power Purchase Agreement Second Power Transmission and Distribution Project Environmental ManagementlMonitoring Plan Environmental Managemenmonitoring Procedures United States Agency for Intemational Development

Vice President: Jemal-ud-din Kassum

Acting Sector Director: Mohammad Farhandi Task Team Leader: Mohammad Farhandi

Country Director: Andrew Steer

FOR OFFICIAL USE ONLY

INDONESIA JAVA-BAL1 POWER SECTOR RESTRUCTURING AND STRENGTHENING PROJECT

CONTENTS

A. Project Development Objective

1. Project development objective 2. Key performance indicators

B. Strategic Context

1. Sector-related Country Assistance Strategy (CAS) goal supported by the project 2. Main sector issues and Government strategy 3. Sector issues to be addressed by the project and strategic choices

C. Project Description Summary

1. Project components 2. Key policy and institutional reforms supported by the project 3. Benefits and target population 4. Institutional and implementation arrangements

Page

2 2 \

2 3 8

11 12 13 13

D. Project Rationale

. 1. Project alternatives considered and reasons for rejection 15 17 17 18 19

2. Major related projects financed by the Bank and/or other development agencies 3. Lessons learned and reflected in the project design

5. Value added of Bank support in this project 4. Indications of borrower commitment and ownership

E. Summary Project Analysis

1. Economic 2. Financial 3. Technical 4. Institutional 5. Environmental 6. Social 7. Safeguard Policies

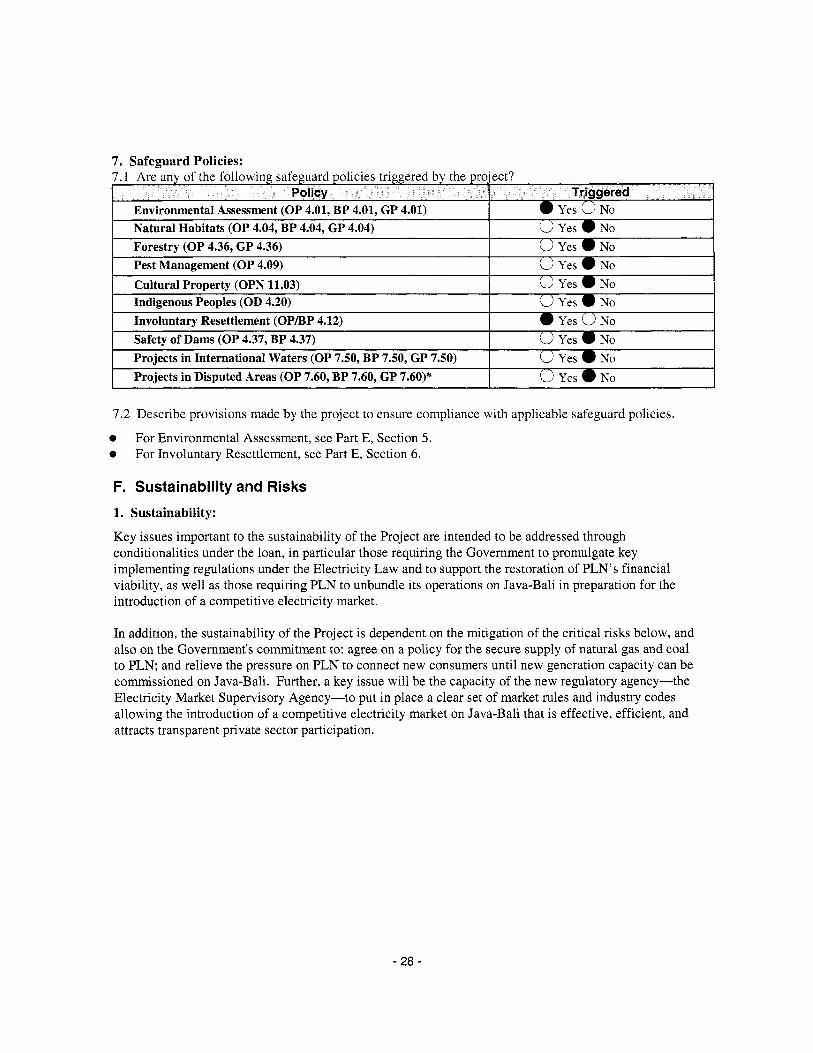

A .

20 20 22 22 24 26 28

This document has a restricted distribution and may be used by recipients only in the performance o f their official duties. I t s contents may not be otherwise disclosed without Wor ld Bank authorization.

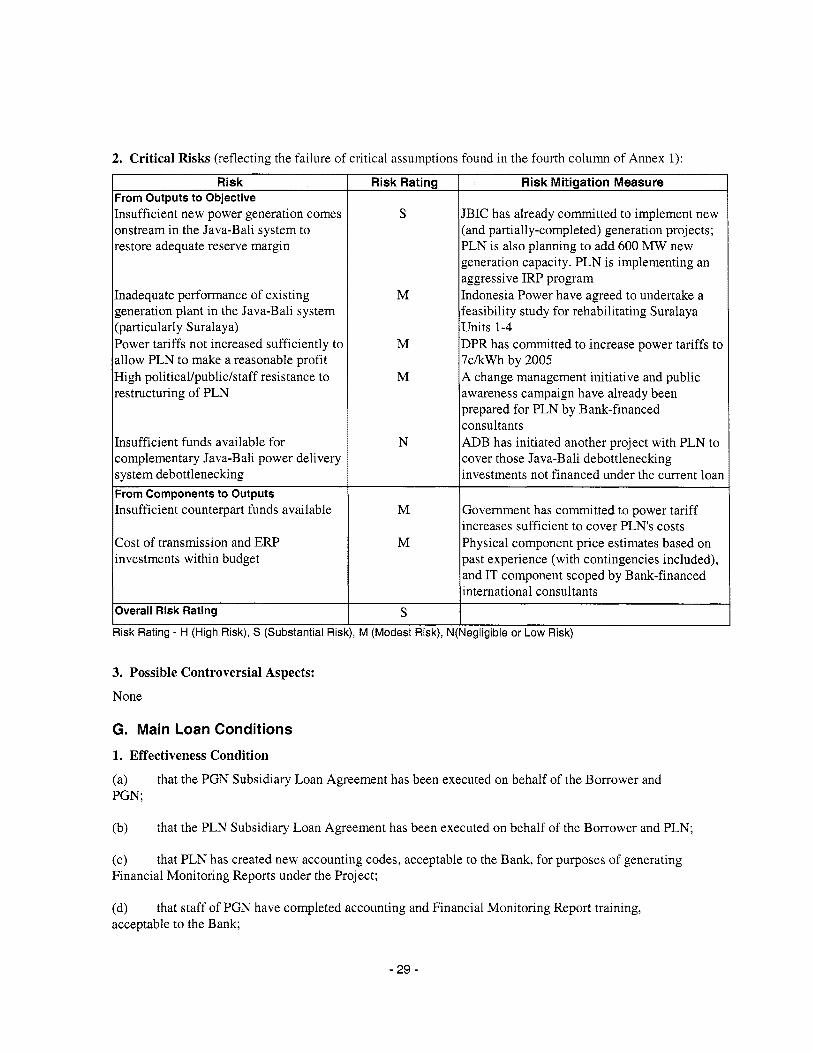

F. Sustainability and Risks

1. Sustainability 2. Critical r isks 3. Possible controversial aspects

G. Main Conditions

1. Effectiveness Condition 2. Other

H. Readiness for Implementation

I. Compliance with Bank Policies

Annexes

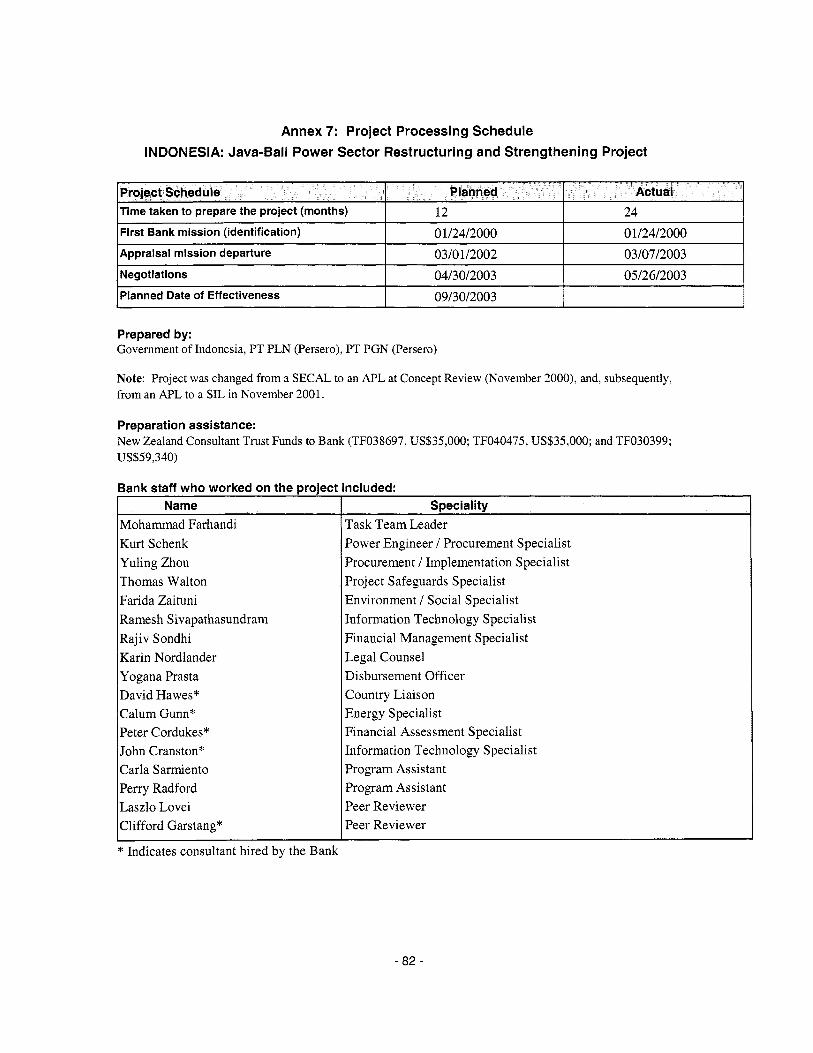

Annex 1: Project Design Summary Annex 2: Detailed Project Description Annex 3: Estimated Project Costs Annex 4: Cost Benefit Analysis Summary Annex 5: Financial Summary Annex 6: (A) Procurement Arrangements

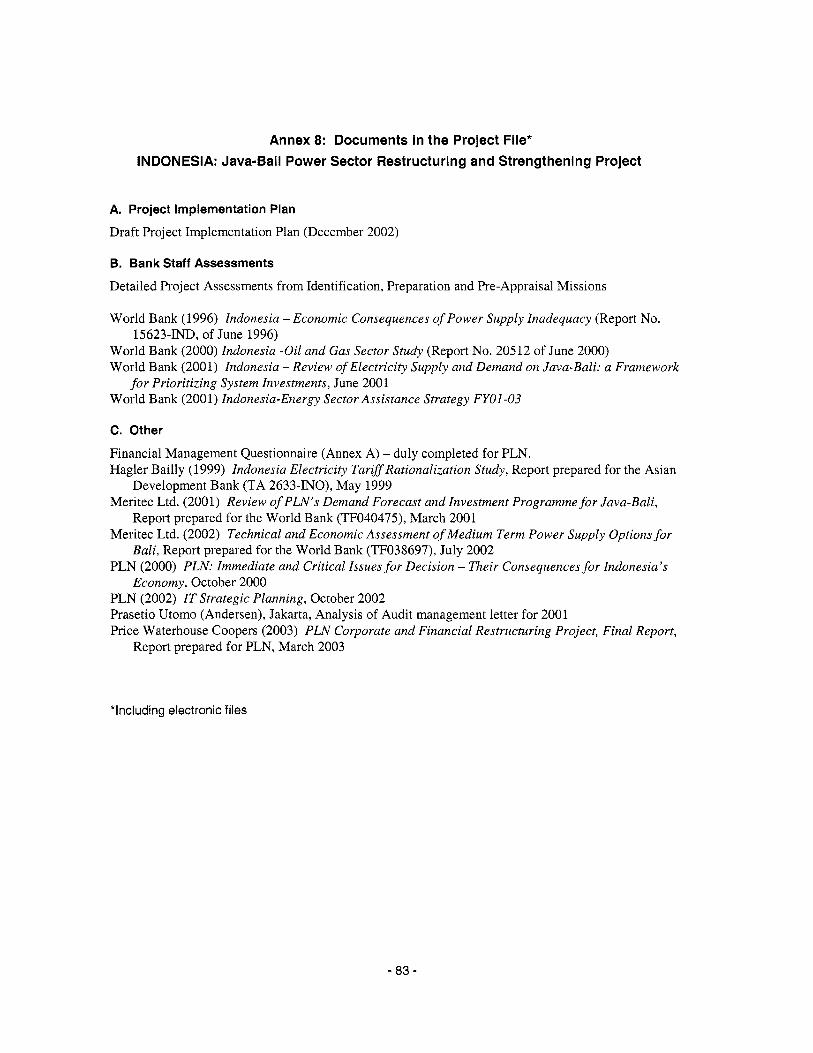

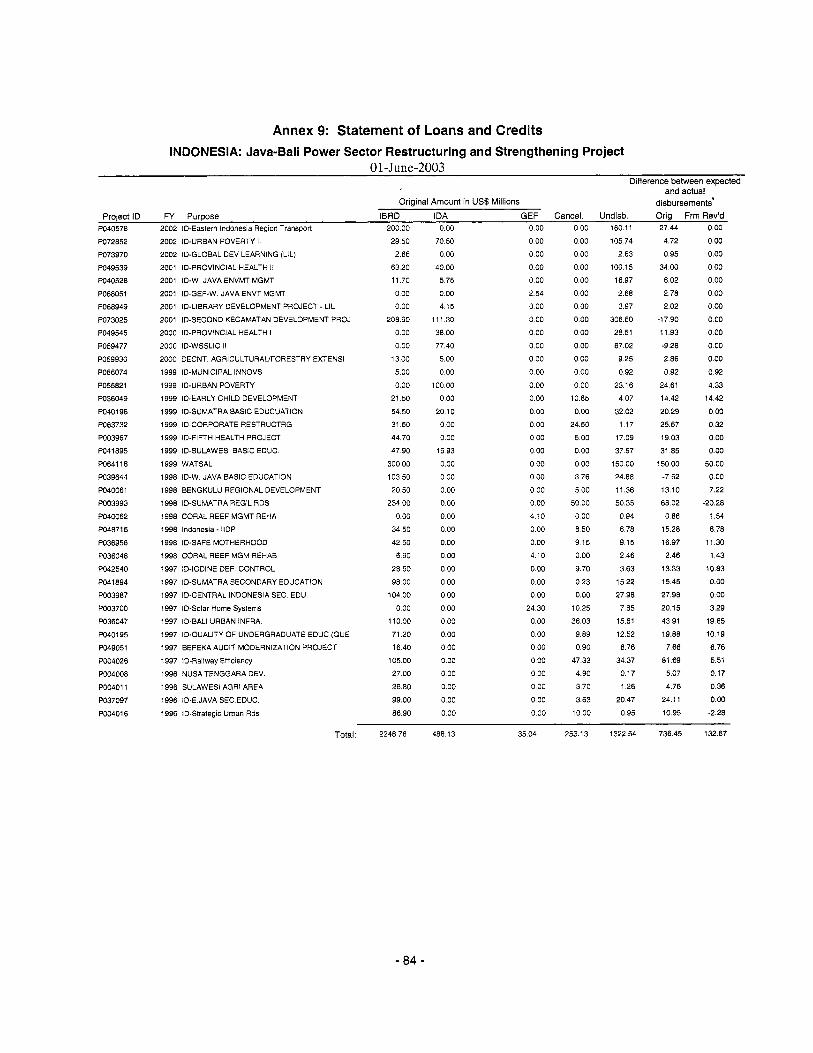

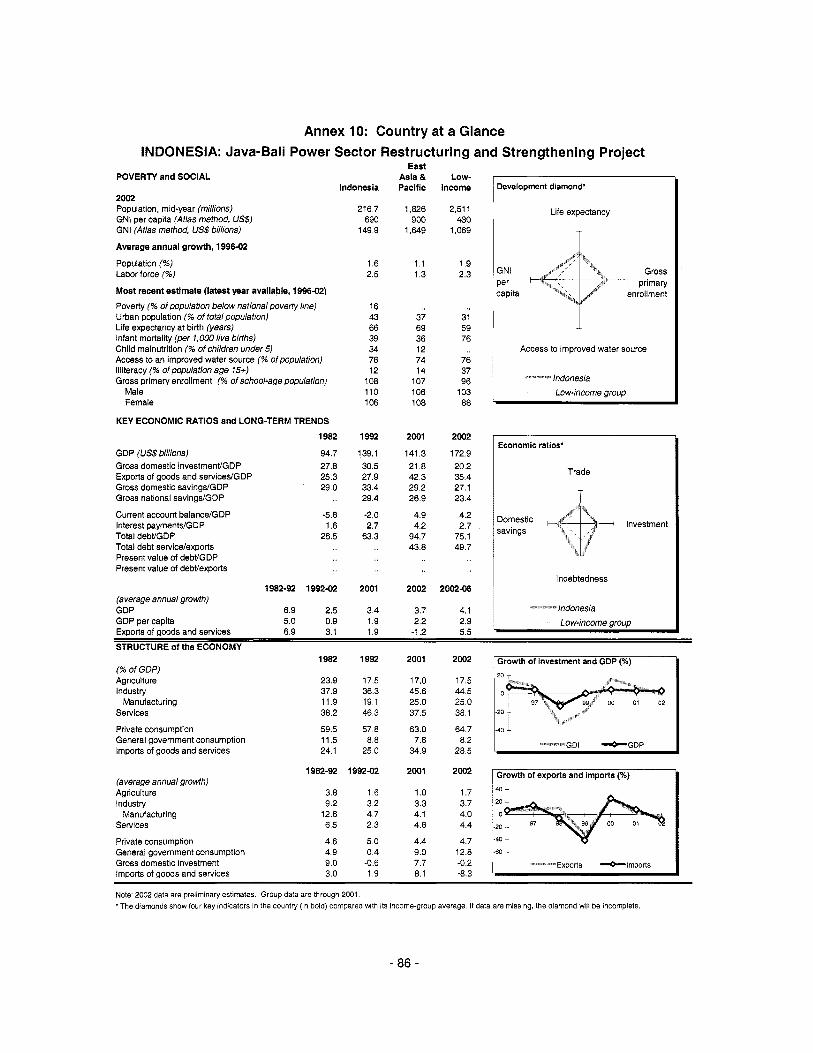

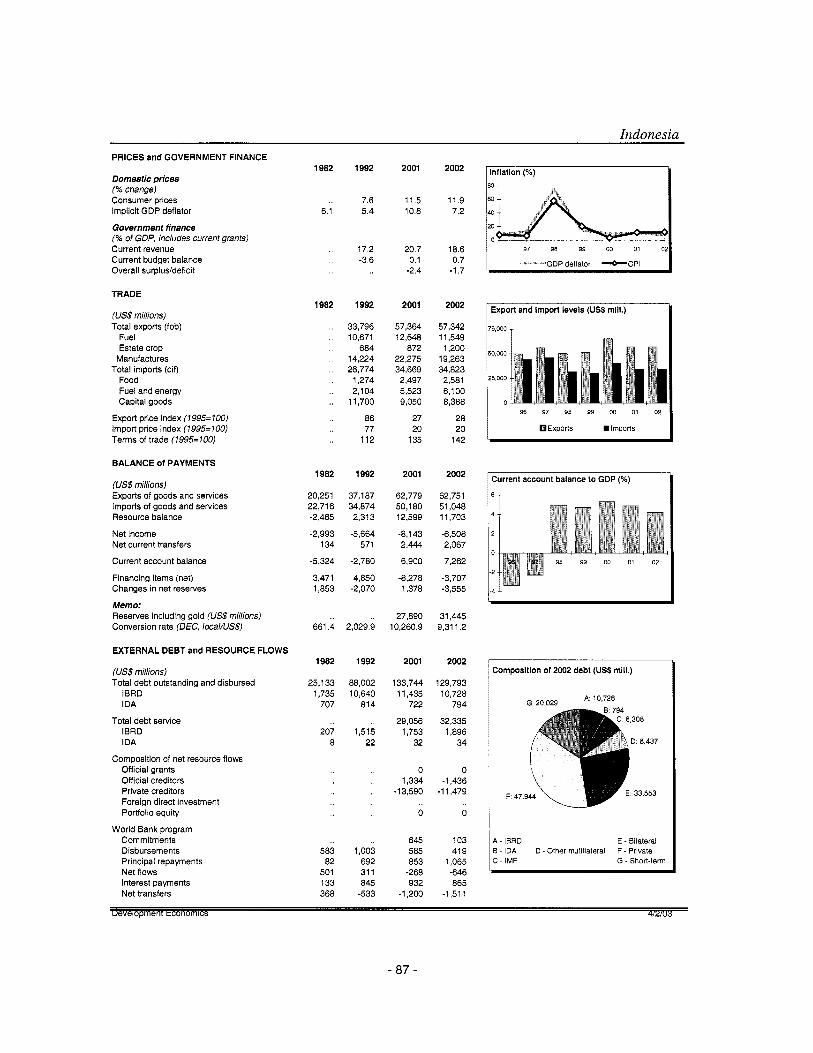

(B) Financial Management and Disbursement Arrangements Annex 7: Project Processing Schedule Annex 8: Documents in the Project File Annex 9: Statement o f Loans and Credits Annex 10: Country at a Glance Annex 11: PLN's Restructuring Program Annex 12: (A) Brief Summary o f Environmental and Social Assessment and Management Plan

(B) Brief Summary o f Land Acquisition and Resettlement Policy Framework

28 29 29

29 30

32

33

34 37 44 45 50 60 66 82 83 84 86 88 98

MAP(S) IBRD 32213

INDONESIA Java-Bali Power Sector Restructuring and Strengthening Project

Project Appraisal Document East Asia and Pacific Region

EASEG

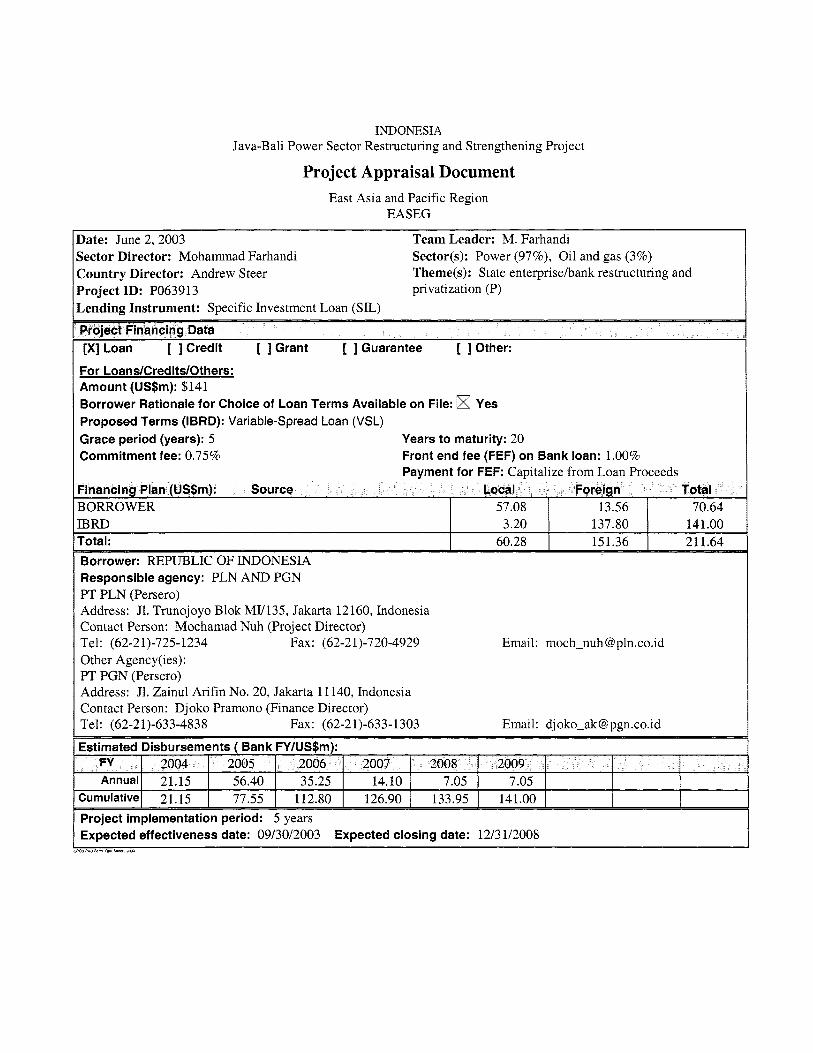

Date: June 2,2003 sector Director: Mohammad Farhandi Zountry Director: Andrew Steer Project ID: PO63913 privatization (P) Lending Instrument: Specific Investment Loan (SIL)

Team Leader: M. Farhandi Sector(s): Power (97%), O i l and gas (3%) Theme(s): State enterprisehank restructuring and

[XI Loan [ ] Credit [ ] Grant [ ] Guarantee [ ] Other: For Loans/Credits/Others: Amount (US$m): $141 Borrower Rationale for Choice of Loan Terms Available on File: Proposed Terms (IBRD): Variable-Spread Loan (VSL)

Yes

Grace period (years): 5 Commitment fee: 0.75%

Years to maturity: 20 Front end fee (FEF) on Bank loan: 1.00% Payment for FEF: Capitalize f rom Loan Proceeds

BORROWER 57.08 I 13.56 I 70.64

Borrower: REPUBLIC OF INDONESIA Responsible agency: P L N AND PGN PT PLN (Persero) Address: J1. Trunojoyo Blok MI/135, Jakarta 12160, Indonesia Contact Person: Mochamad Nuh (Project Director) Tel: (62-21)-725-1234 Fax: (62-21)-720-4929 Other Agency(ies): PT PGN (Persero) Address: J1. Zainul Arifin No. 20, Jakarta 11 140, Indonesia Contact Person: Djoko Pramono (Finance Director) Tel: (62-21)-633-4838 Fax: (62-2 1)-633- 1303

Emai 1: moc h-nuh 0 pln .co. id

Email: [email protected]

Estimated Disbursements ( Bank FY/US$m):

Annual1 21.15 I 56.40 1 35.25 I 14.10 1 7.05 1 7.05 I I I 77.55 I 112.80 I 126.90 I 133.95 I 141.00 I

Project implementation period: 5 years Expected effectiveness date: 09/30/2003 Expected closing date: 12/3 1/2008

caPAo*m e.” b.*m iam

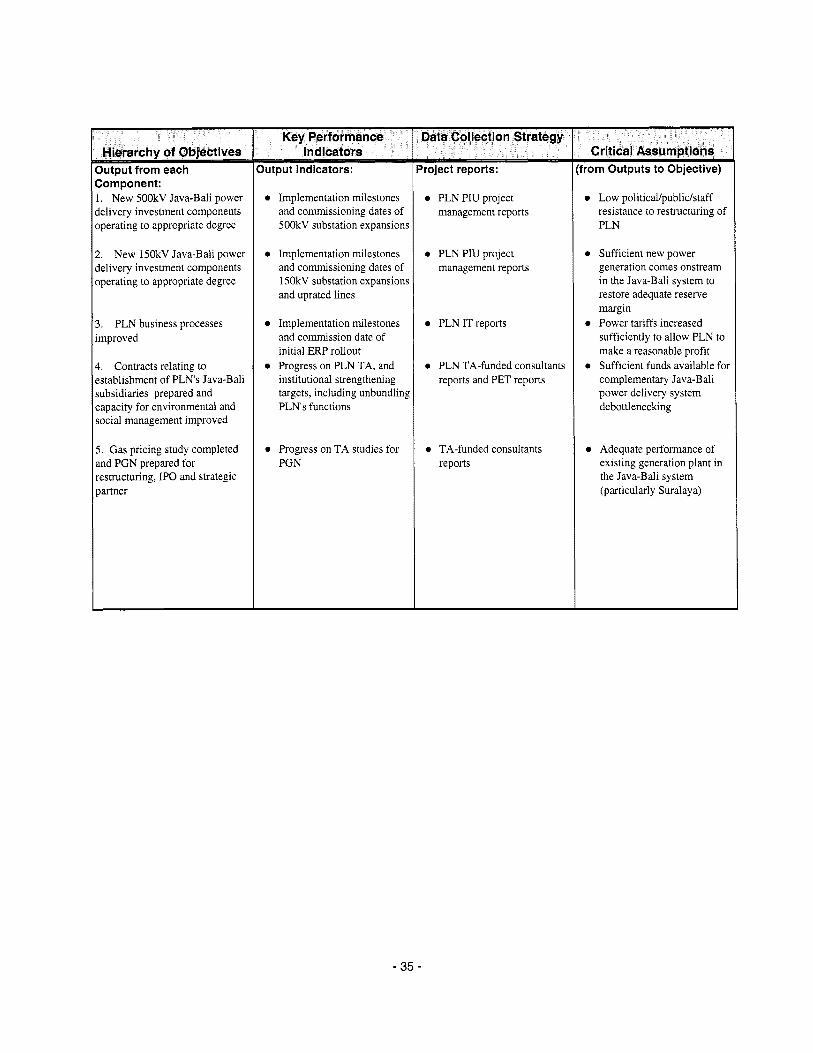

A. Project Development Objective

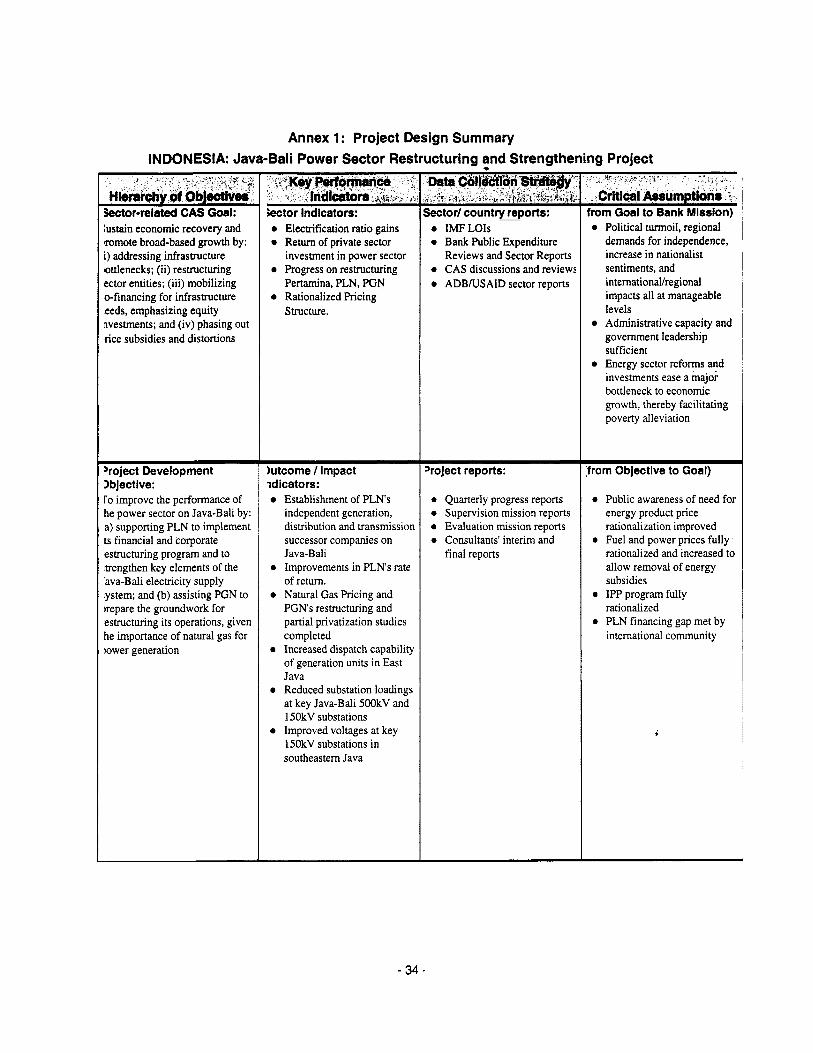

1. Project development objective: (see Annex 1)

The development objective o f the Project i s to improve the performance o f the power sector on Java-Bali by: (a) supporting the State power company (PLN) to implement i t s financial and corporate restructuring plan, and to strengthen key elements o f the Java-Bali electricity supply system; and (b) assisting the State gas company (PGN) to prepare the groundwork for restructuring i t s gas transmission and distribution operations, given the importance o f natural gas for power generation.

This objective i s to be achieved through the provision o f Bank financing toward priority investments and technical assistance for PLN, and technical assistance for PGN. In particular, project components for PLN will: (i) support PLN’s financial and corporate restructuring, b y providing technical assistance and b y enhancing the company’s information systems capabilities; (ii) achieve greater utilization o f existing generation capacity on East Java, b y relieving constraints in the bulk transmission grid; (iii) improve the reliability o f existing generation supply at the P L N and independent power producer (IPP) geothermal power plants on West Java, b y strengthening the associated local transmission system; and (iv) improve the reliability o f power supply at various locations throughout Java and Bali, b y strengthening and debottlenechng local transmission and subtransmission networks. Technical assistance to PGN w i l l enhance i t s capabilities for expanding gas utilization on Java.

2. Key performance indicators: (see Annex 1)

The key performance indicators o f the project are: (i) the establishment o f independent distribution, transmission and generation successor companies f rom PLN’s operations on Java-Bali; (ii) improvements in PLN’s rate o f return on revalued net fixed assets; (iii) increased dispatch capability o f generation units at the Paiton, Grati and Gresik complexes on East Java; (iv) reduced substation percentage loadings at Mandirancan, Krian, and Klaten 500kV substations on Java; (v) reduced substation percentage loadings at key 150kV substations throughout Java-Bali; and (vi) improved voltages at key 150kV substations in southeastern Java. In addition, PGN should have completed the documentation outlining the framework and implementation plans for: (i) unbundling i t s transmission and distribution functions to create an appropriate corporate structure; (ii) preparing for an IPO or some other form o f private equity participation of part o f i t s distribution operations; (iii) and attracting a strategic partner for i t s transmission operations.

B. Strategic Context 1. Sector-related Country Assistance Strategy (CAS) goal supported by the project: (see Annex 1) Document number: 24608-IND Date of latest CAS discussion: 09/16/02

The proposed Project, included in the FY03 Indonesia lending program, i s consistent with the most recent CAS Progress Report (No 24608-IND). This Project i s the first o f the two Specific Sector Loans (i.e., the Power project for FY03 and the Gas project for FY04), and as such, primarily relates to the power sector. The resolution o f several issues during FY02, including on-lending guidelines and the Government’s decision to go ahead with the proposed Power project (for about $140 mill ion instead o f $100 mill ion originally envisaged), has resulted in a larger program in FY03. Moreover, the Government i s on the verge o f meeting the high case triggers, which lends further support to the upward lending trend. The main reasons for increase in the loan amount o f the Power project are the need for Bank to help with additional financing for (a) PLN’s Enterprise Resource Planning (ERP) system to support i t s restructuring, which i s central to the development objective o f the Project; and (ii) expansion o f 115kV system to address additional localized constraints in power supply, and thus preempt future power

- 2 -

interruption.

The Project supports the objective in the CAS o f sustaining economic recovery and promoting broad-based growth through assistance to the GO1 to: 0

0

address infrastructural bottlenecks in power, by providing direct investment lending for the removal o f key power system delivery constraints on Java-Bali; restructure sector entities, by (a) supporting the implementation o f PLNs corporate restructuring through technical assistance and by providing direct investment lending for upgrading information systems, and (b) providing technical assistance (TA) to assess how PGNs operations can be restructured; mobilize co-financing for infrastructure needs, emphasizing equity investments, by (a) supporting the restructuring o f P L N and PGN, and (b) providing TA to evaluate options for greater private sector participation in the gas sector; phase out price subsidies and remove price distortions, by providing TA to develop a rational domestic gas pricing strategy.

0

0

2. Main sector issues and Government strategy:

Sector Background and Issues. The GO1 and the Bank have been discussing the key policy issues in the wider energy sector over the past few years-namely the need for: (i) revising the policy and legislative frameworks o f the power and hydrocarbon (Le., o i l and gas) sectors: (ii) rationalizing the prices o f energy products, and gradually phasing out the substantial subsidies for petroleum products and electricity; (iii) implementing the fundamental restructuring o f the key sector entities-namely the State power company (PLN), the State gas transportation and distribution company (PGN), and the State o i l (and gas) company (Pertamina); (iv) rationalizing the country’s independent power producer (IPP) program; (v) removing constraints to the development o f the domestic natural gas industry; and (vi) improving urban air quality, b y promoting the use o f cleaner fuels (including natural gas). A detailed analysis o f the issues, and options for addressing them, have been presented in Bank-prepared or supported studies, including: the Background Papers to the Power Sector Restructuring Workshop o f August 1998; the Indonesia - Oi l and Gas Sector Study (Report No. 205 12-IND) o f June 2000; a confidential report o f June 2000 on Indonesia’s IPP program; the Indonesia - Energy Sector Assistance Strategy FYOI-03; and the report Indonesia -Review of Electricity Supply and Demand on Java-Bali: a Framework for Prioritizing System Investments o f June 2001.

While the East Asian financial crisis had wide-ranging impacts on Indonesia’s economy, it had a more profound impact on Indonesia’s power sector than on those of other countries in the region. The substantial devaluation of the Rupiah caused by the crisis transformed P L N from a moderately profitable company into one unable to meet i t s obligations for foreign currency-denominated debt service payments, fuel costs, and power purchases from private independent power producers (IPPs). The crisis also exposed shortcomings in the sector’s governance structure which were already present prior to the crisis-particularly in terms o f PLN’s monopolistic organization, and the absence o f competitiveness and transparency in Indonesia’s IPP program (which primarily depended on unsolicited proposals). In addition, the lack o f funds flowing into the broader energy sector since the crisis means that there i s a urgent need for both substantial investment in new electricity infrastructure and rehabilitation o f existing power assets, as well as investment in the upstream infrastructure used to supply fuel for power generation, particularly natural gas.

Key Achievements to Date in the Power Sector. P L N was established under Government Regulation 18/1972 as a Perum (Le. government company), and the Electricity Act (Law No. 15/1985) assigned P L N both the right and obligation to supply power throughout Indonesia. Although in theory this law allowed

- 3 -

private sector participation in the sector, i t was not until Presidential Decree 37/1992 that Indonesia’s IPP program become a reality. In 1994, under Government Regulation 23/1994, P L N was converted from a Perum to a Persero (a limited liability corporation), and in 1995, two generation subsidiaries on Java-Bali were established (currently named Indonesia Power and PJB). Despite the difficult political and economic environment the country has been facing since the regional crisis, a number o f notable steps have already been taken by the GO1 to resolve some o f the key problems in the power sector that were reinforced by this legal and regulatory framework and exacerbated by the crisis.

Issuance of the Power Sector Restructuring Policy. The f i rs t publicly-launched Power Sector Restructuring Policy to provide a blueprint for the de-monopolization of the sector was issued by the Government in August 1998-prepared with assistance from the Bank, ADB and USAID. This Policy outlined that the key objectives for restructuring the sector were: restoration o f financial viability; competition; transparency; and more efficient private sector participation (Annex 11). The Policy recognized that, while power system operations in many areas outside Java w i l l require GO1 support for the foreseeable future, the electricity system on Java-Bali i s relatively well-developed, and over the medium to longer term can potentially be transformed into a commercially-viable and financially-independent operation. Transitional steps involved the geographical unbundling o f PLN’s outside Java operations f rom those on Java-Bali, which would in turn be functionally unbundled into Java-Bali generation, transmission and distribution units or successor companies. A new law with implementing regulations would allow for the establishment o f a fu l ly competitive multi-buyedmulti-seller power market on Java-Bali, via an intermediate transitional single buyer stage (with the option o f establishing a parallel bilateral contracts market), a l l to be governed b y an independent regulatory agency. In support o f the implementation o f this Policy, the Bank and ADB agreed to focus on complementary areas o f restructuring activities. ADB provided the Government with program and technical assistance loans (co-financed with JBIC) to deal with sectoral aspects o f reform, such as preparing the init ial drafts o f the new Electricity Law, implementing regulations, and market rules, while the Bank’s focus was on the financial and corporate restructuring o f PLN. Passage of the 2002 Electricity Law. The new Electricity Law envisaged by the 1998 Policy was eventually passed in September 2002. While i t s key objectives and outcomes remain broadly the same, the Law does differ in some important respects f rom the Policy, notably in that i t provides l itt le detail in regard to transitional provisions, or to the financing mechanisms for public service obligations and residual subsidies. Nevertheless, the Law does potentially pave the way for a competitive power market operation (at least on Java-Bali) over the medium to long term, as long as effective implementing rules and regulations in support o f the L a w are promulgated. Within five years o f the Law going into force, at least one region must be designated for competition in generation, and principles o f unbundling and transmission/distribution open access w i l l apply in al l regions designated by the Government as competitive (with competition possible down to the low voltage consumer level). Within one year o f the enactment o f the Law, a new regulatory body-the Electricity Market Supervisory Agency (EMSA)-must be established, and i t i s charged with issuing the market rules and industry codes governing competitive regions. In non-competitive off-grid areas, local and regional governments w i l l play a greater role in the sector, having authority to issue licenses for electricity supply functions and to regulate prices, whereas in non-competitive areas connected to the national transmission grid, the Government w i l l continue to play the role o f regulator and licensor (Annex 11). In addition to preparing the groundwork for the establishment o f EMSA, the Directorate General for Electricity and Energy Utilization (DGEEU) has already drafted the majority o f supporting regulations, rules, and codes. Design and Implementation of PLN’s Financial and Corporate Restructuring Program. A major Bank-funded technical assistance (TA) contract for supporting PLN to design and begin implementing i t s financial and corporate restructuring program commenced in M a y 2001, and the bulk of this work was completed in late 2002. (The final report was submitted in March 2003). Recommendations on financial restructuring have contributed to the recent improvement in PLN’s

0

- 4 -

finances (see below), and recommendations on corporate restructuring have provided the basic plan for the new organizational design, j ob descriptions, business procedures and performance indicators across PLN’s head office, as well as i t s generation, transmission and distribution subsidiaries and business units (Annex 11). However, the passage of the new Law has required that some o f the recommendations o f the TA be reviewed for consistency. Nevertheless, the key objectives and final outcomes o f the 1998 Policy are s t i l l valid and achievable, although there w i l l be delays to some aspects o f the implementation program, pending the establishment of EMSA, and the issuance by both the Government and EMSA o f the new regulatory framework. Increases in the Power Tariz. Following a number o f unsystematic tariff increases during 2000 and 2001, the GO1 agreed in principle-with endorsement f rom the DPR-that power tariffs would reach pre-crisis levels b y 2005 (Le., US7 centskwh). For 2002 and 2003, specific approval for increases o f 6% per quarter has been given, which means that as o f December 2002, PLN’s average revenue level i s about US5.3c/kWh, more than twice the level immediately after the crisis. Presidential Decree 89/2002 outlines per quarter tariff increases for 2003, which put tariffs on track for reaching US6.8ckWh by the end o f 2003. Debt Restructuring for PLN. In June 2001, the GO1 approved the conversion o f Rp29 tri l l ion o f PLN’s overdue interest (plus fines) to equity, and the unpaid principal of Rp5 tri l l ion was converted to a new 20 year loan. New Borrowing by PLN. Following the crisis, the GO1 froze new lending for PLN, partly as the result o f a reluctance to take on new exposures, but also over concerns that PLN’s system expansion plan was sound, wi th individual projects carefully prioritized and estimated costs soundly based. However, in June 2002, a limited Cabinet meeting agreed that PLN could proceed with discussions relating to 16 loans from multilateral and bilateral sources already in the pipeline (amounting to an envelope o f US$804 million), including the Bank’s proposed Project, and two loans which have since been approved b y ADB’s Board in December 2002. Payment of Targeted Subsidies for the Poorest Electricity Consumers. In December 2001, the GO1 paid Rp6.7 tri l l ion to PLN in order to cover three years (1999-2001) o f “targeted’ subsidies relating to the costs o f supplying PLN’s lowest consumption customers. Moreover, in October 2002, the GO1 formalized the future provision o f targeted subsidies to PLN for consumers with a connection capacity o f up to 450VA. Renegotiation of ZPP Contracts. P L N has now successfully renegotiated or closed out about 18 o f the 27 pre-crisis PPAs, and has reached agreement on the payment o f arrears to those IPPs with currently-operating power plants-amounting to about 3,100MW.

Short Term and Long Term Challenges Facing the Power Sector. Notwithstanding these significant achievements, Indonesia’s power sector s t i l l faces a number o f crucial short and long term challenges. As the Bank has been indicating to the GO1 for the past 24 months or so-init ially through the submission o f i t s June 2001 report on the Java-Bali power supply/demand balance, and reinforced through subsequent correspondence from the Bank as well as ongoing sector dialogue-over the short to medium term, the key challenge i s that o f burgeoning power shortages, because secure operation o f the power system, particularly on Java-Bali, i s vital to the entire Indonesian economy. Already, areas outside Java have been experiencing frequent power supply interruptions, and this situation i s likely to extend to the crucial Java-Bali power system over the next three years. The GO1 therefore needs to support P L N in mitigating the risk of power shortages. In addition, given the long lead times associated with major power infrastructure projects, the GO1 needs to take further actions in the short term to ensure that, in the medium to longer term, the viability o f the sector i s secured. These actions include helping to (a) continue restoring PLN’s financial viability, (b) attract the private sector to reinvest in the power sector, (c) secure supplies o f natural gas for power generation, and (d) manage the decentralization o f electricity supply*

- 5 -

Mitigating the Risk of Power Shortages. Before the regional crisis, the main concern was the prospect of a significant oversupply o f power generation, given that 11,000MW of new capacity was included in the IPP program (10,OOOMW o f which was intended for Java-Bali). Nevertheless, only 3,000MW of IPP capacity ended up being commissioned in the Java-Bali system. An additional power station on Java i s under construction-the Tanjung Jati B plant (1,32OMW)-but i t s f i r s t unit i s unlikely to be commissioned before 2006. On the other hand, demand for electricity on Java-Bali continues to be robust, despite the fallout from the crisis. After substantial efforts b y the GO1 and PLN to secure funding for new generation-which the Bank supported by presenting i t s analysis o f the need for additional generation capacity to donor partners-the Japan Bank for International Cooperation (JBIC) agreed at the January 2003 C G I Meeting to support the repowering o f the Muara Karang plant, as well as an extension to the Muara Tawar plant, both in the Jakarta area. These projects would add 420MW and 225MW to the Java-Bali system respectively. In addition, P L N has already received bids for about 600MW of fast track gas turbine plant (also at the Muara Karang site), and these should be commissioned before 2006. Nevertheless, 2004 and 2005 w i l l remain critical years for PLN in operating the Java-Bali system.

Hence, the Bank has advised the GO1 that i t needs to: (i) resolve outstanding financing issues relating to the Tanjung Jati B plant, the transmission line required to evacuate power f rom Tanjung Jati B into the Java-Bali bulk transmission grid, and the completion o f the southern section o f the Java-Bali grid; (ii) take into account that P L N has little alternative except to control the rate at which new customers are connected until the fast track gas turbines and other planned generation capacity can be commissioned; and (iii) finalize plans for securing financing for the additional generating capacity which w i l l be required in the medium to longer term-particularly the proposed capacity additions at Muara Karang and Muara Tawar, as well as Tanjung Priok-and ensure that natural gas supplies w i l l be secured for these gas-fired combined cycle plants. Furthermore, the Bank has encouraged P L N to continue: (i) maintaining and improving the availability and reliability o f existing power generation capacity, in particular by rehabilitating Units 1-4 at the Suralaya coal-fired plant (given that these 1,600MW are crucial for providing base load in the Java-Bali system); (ii) prioritizing new customer connections; and (iii) carefully managing electricity demand growth through integrated resource planning (IRP) initiatives. P L N has already begun implementing an IRP program o f supply and demand side management measures that includes: (i) increasing peak power tariffs relative to off-peak tariffs; (ii) offering interruptible tariffs to large consumers, as well as buyback tariffs f rom customers with their own captive power plants; and (iii) promoting the replacement o f existing commercial, household and street lighting with high efficiency bulbs.

Restoring PLN’s Financial Viability. As i s discussed below, the private sector i s unlikely to play a major role in Indonesia’s power sector for the next several years. Therefore, during the transition period until the introduction of competition, PLN w i l l s t i l l have a key investment role to play in the sector. Yet, despite the actions already taken to support PLN, the company’s current financial position s t i l l l i m i t s i t s ability to undertake that role. Even under a strictly limited rate o f electricity sales growth, P L N s t i l l needs to undertake a significant capital expenditure program. Moreover, apart f rom the impact o f the removal o f fuel subsidies on PLN’s operating expenditures, fuel costs are also set to increase significantly unless the company can secure new supplies o f natural gas. This i s because P L N w i l l be forced to run gas-fired units on considerably more expensive o i l (see below).

Therefore, to restore PLN’s creditworthiness and ability to raise financing itself, the Bank has advised the Government to: (i) continue to increase power tariffs, aiming for-at a minimum-a positive rate o f return on PLN’s revalued assets by 2004; (ii) reintroduce the Automatic Tariff Adjustment Mechanism (ATAM) to minimize PLN’s exposure to foreign exchange and fuel price fluctuation r isks; (iii) provide

- 6 -

approval for borrowing commensurate with PLN’s realistic capital expenditure program, over the short term until PLN’s financial health i s restored: (iv) explore options for reducing PLN’s capital gains tax burden from asset revaluation; (v) agree on a policy for the secure supply o f natural gas, coal and geothermal steam to PLN; and (vi) provide P L N with subsidies for any public service obligations imposed on i t s operations.

Attracting the Private Sector to Invest in the Power Sector. The new Electricity Law implicit ly acknowledges that, even if P L N were in a strong financial position, i t would be untenable for the company to provide the substantial levels o f new investment in generation, transmission and distribution required over the long term on i t s own, or to remain in i t s currently monopolistic form. As such, greater private sector participation wi l l be required to satisfy much o f the country’s future power supply needs. However, substantial new private investment i s unlikely to come to the sector before the next 5-6 years. Apart f rom Indonesia’s poor investment climate overall (which w i l l itself not be improved by the prospect o f power shortages), there i s a global concern regarding investment in the energy sector, stemming in part f rom the failure o f energy companies such as Enron. At present, even those existing IPP sponsors wi th successfully renegotiated contracts w i l l find i t difficult to convince lenders to support the expansion o f existing proven power projects without the provision of a government guarantee. Consequently, the groundwork needs to be laid now to ensure that new private power projects are able to come onstream even within this timeframe. Hence, although the passage o f the new Electricity L a w i s an important first step, the Bank has advised the GO1 to press on with: (i) promptly issuing implementing regulations: (ii) establishing and providing the new Supervisory Agency for the power sector with resources commensurate with i t s roles and responsibilities; and (iii) resolving the remaining issues associated with the existing IPP program.

Securing Supplies of Natural Gas for Power Generation. The existing gas supply contracts for PLN’s gas-fired plants on West Java terminate in 2004, and although the contracts relating to PLN’s East Java plants run until 2011, available gas i s declining at a rapid rate, with some units already switching to oil. Moreover, the viability of most current proposals for repowering or extending existing plants, or for constructing new combined-cycle plants, are dependent on the availability o f natural gas as a fuel. While Indonesia has substantial gas reserves, some o f which are on Java, the best long term prospects for supporting expanded gas utilization on Java-both for power generation and industrial purposes-appear to be by pipeline f rom fields in South Sumatra andor East Kalimantan, and LNG from the Tangguh field in West Papua. PGN would clearly be a key player in any significant gas transmission project, and discussions between PGN, JBIC, and the GOI, on the South Sumatera to West Java pipeline are already almost completed and the government o f Japan has committed to the project. However, to deal with the challenges o f implementing such major infrastructure projects-and to comply with the October 2001 Oil and Gas Law, which has clarified PGN’s role and future structure-PGN needs to restructure i t s operations by ful ly unbundling transmission from distribution, and to seek private sector financing and expertise in both i t s distribution and transmission functions. In addition, a key issue remains the need for a rationalized gas pricing structure, the lack o f which w i l l continue to act as a significant impediment to the expansion o f the domestic natural gas industry. These are areas for which PGN has asked the Bank’s assistance as part o f the proposed project.

Managing the Decentralization of Electricity Supply. Implementation o f the new Electricity Law w i l l transfer significant responsibilities for power supply to provincial governments, kabupatens, private companies, and even community-based cooperatives, since some licenses w i l l be able to be issued by local mayors (or governors). Therefore, these bodies w i l l have a crucial role in expanding access to electricity in poorer and remote regions. Consequently, the GO1 w i l l need to: (i) issue clear regulations under the new Law to outline how various financing mechanisms can be used to support decentralized

- f -

power provision in those areas where i t i s uneconomic for PLN, or i t s successor companies, to extend the existing national transmission grid; and (ii) determine how the substantial needs for institutional strengthening, which w i l l be required by those agencies with new responsibilities under the Law, can be met.

3. Sector issues to be addressed by the project and strategic choices:

I t i s not realistic to address all the above outstanding sector issues within the context o f a single operation. The current progress on the various issues, the level o f GO1 commitment, the Bank‘s comparative advantage and the existing involvement o f other donors (ADB, JBIC, USAID), as well as the amount o f additional analytical work required before some issues can be adequately addressed, have led to the decision to prepare a specific investment loan (SIL) operation, focusing primarily on: (i) supporting the implementation of PLN’s financial and corporate restructuring; (ii) preparing PGN for restructuring and partial privatization; and (iii) strengthening the power system on Java-Bali. The Project w i l l contain technical assistance components and conditionalities in support o f actions on these issues, as well as investment components for PLN.

For instance, while issues relating to Pertamina’s role and functions continue to be a major unresolved challenge for the energy sector as a whole (not least in terms of possible implications for domestic gas sector restructuring), additional analytical work i s required to assess alternatives for reforming Pertamina in a fundamental way-including the formation o f several true subsidiaries, as well as the initiation o f a major divestiture and/or partial privatization program. However, such analysis would only be effective with the co-operation o f Pertamina itself, a situation which currently i s not the case.

Power Sector Restructuring. Implementation of the GOI’s 1998 Power Sector Restructuring Policy has been supported by ADB, USAID, and the Bank. ADB (with co-financing from JBIC o f US$400 million) provided the GO1 with a program loan o f US$380 million, and a technical assistance loan o f US$20 mill ion to the Directorate General o f Electricity and Energy Utilization (DGEEU) in order to deal with the sectoral aspects of restructuring-particularly the initial drafting o f the new Electricity Law and associated regulations, as well as the market rules governing the creation o f a competitive electricity market. (USAID has been providing ongoing capacity building support to the Ministry o f Mines and Energy). While the Bank worked closely with ADB in providing feedback on the init ial drafts o f the Electricity Law, i t was agreed that the Bank’s subsequent focus be on the financial and corporate restructuring o f PLN. As such, the Bank (under the Second Power Transmission and Distribution Project) financed the technical assistance (TA) required to help P L N design and begin implementing i t s corporate restructuring program, and the bulk of this work was completed in late 2002 (Annex 11).

However, the passage o f the Electricity Law, and the yet-to-be promulgated implementing rules and regulations, w i l l require that some o f the recommendations o f this work be reviewed for consistency, and modified accordingly. Nevertheless, notwithstanding some differences between the 1998 Policy (which was the basis for Bank TA) and the 2002 Law, many o f the TA recommendations relating to PLN’s new organizational design, j ob descriptions, business procedures, and performance indicators, s t i l l remain valid. Consequently, the Bank considers that-on balance-the key objectives and final outcomes o f the 1998 Power Sector Restructuring Policy are s t i l l valid and achievable, although there w i l l be delays to some aspects o f the implementation program, pending the establishment o f the new regulator-namely the Electricity Market Supervisory Agency (EMSA)-and the issuance by both Government and E M S A o f the new regulatory framework.

To comply with the Law’s requirement that competitive regions must be functionally unbundled, PLN must continue preparing to spin o f f i t s Java-Bali operations as independent successor companies.

- 8 -

Initially, P L N can press on with carrying out i t s restructuring implementation plan as applicable to i t s existing subsidiaries and business units. Effective implementation o f subsequent steps, however, w i l l require key implementing regulations to be in place, and market rules and industry codes to have been issued b y EMSA. Once EMSA finalizes the new market rules, transmission charging methodology and open access tariffs, as well as decisions relating to generation market power, P L N can proceed with fu l ly unbundling i t s Java-Bali operations. This w i l l firstly involve the creation of four (or more)-subject to E M S A approval-new generation subsidiaries f rom Indonesia Power and PJB. In addition, five independent distribution companies and an independent transmission company w i l l be created from PLN’s operations on Java-Bali. All o f these new Java-Bali companies w i l l initially be established as subsidiaries under the P L N holding company, with a target date o f the end o f 2006. These companies w i l l subsequently be spun-off as independent companies before such time as the Government designates the Java-Bali system as competitive, which (by Law) must occur before the end o f September 2007. These measures w i l l be supported in the new Project through conditionalities and technical assistance. In addition, a key element o f PLN’s restructuring plan i s the further measures needed to improve PLN’s financial position, and these measures w i l l also be underpinned by financial covenants in the loan (Section G.).

The loan w i l l also include partial financing for the enhanced information systems capabilities needed by PLN to support the implementation o f i t s corporate restructuring program, notably a pilot rollout o f an Enterprise Resource Planning (ERP) System for core financial, materials management, human resources management and asset management. P L N w i l l itself-through a jo int venture arrangement (consistent with the company’s overall new IT Strategy)-finance the init ial rollout o f new customer information systems (CIS). (ADB intends to provide complementary financing for the development o f the information systems required to implement the competitive wholesale electricity market).

Power System Strengthening. While the new Electricity Law provides l itt le guidance on the transitional steps required to introduce competition in electricity supply, i t does outline a number o f realistic pre-conditions which must be met before competition can be designated for a particular region, including: (a) there should be competition in the supply o f primary energy, meaning that fuels used for power generation should receive no subsidies; (b) power tariffs must reach cost recovery plus a reasonable level o f profit; and (c) adequate generation reserves and an unconstrained transmission network should be present. The GO1 has been taking active measures to address the f i rs t two pre-conditions for competition, yet bottlenecks remain in the existing transmission system which would make i t diff icult to introduce a power market, even i f there were no prospect o f power shortages caused b y an insufficient level o f generation reserves.

Over the past few years, the Bank and ADB have taken a similar position in deciding not to become involved in the direct financing o f large-scale power generation plants in Indonesia. On the other hand, JBIC has become involved in the partially-completed Tanjung Jati B plant in Central Java (for which construction was halted as the result o f the crisis), and has recently committed to repowering and extending two existing plants near Jakarta (Muara Tawar and Muara Karang). While the Bank w i l l continue to explore options to support the GO1 in working with PLN to transparently and competitively bring new generation on-line in order to mitigate the risk o f power shortages, i t i s not intended that the currently-proposed Project include any generation components, and therefore the Project w i l l not directly address the most critical issue currently facing PLN-namely, the looming shortfall in generation capacity. Nevertheless, the Project w i l l contribute to alleviating actual and potential shortfalls in the overall electricity supply and demand balance on Java-Bali. The Project w i l l ensure greater utilization o f existing generation capacity on East Java by relieving bottlenecks in the bulk transmission grid, and w i l l also improve the reliability o f existing generation supply at PLN and IPP geothermal power plants on

- 9 -

West Java by strengthening the associated local subtransmission system. In addition, the Project w i l l include technical assistance for reviewing the design o f the proposed Upper Cisokan pumped storage hydro plant, which in the longer term, would provide complementary and efficient pealung service to gas-fired plant. Given the long lead time o f constructing hydro projects, i t i s timely to undertake such a review at the present time.

Apart f rom the need to undertake investments which w i l l support greater utilization and more secure operation o f existing generation in the Java system, there has been chronic underinvestment in al l elements o f the Java-Bali power system over the past few years. Even i f sufficient investments in generation capacity are made to restore an adequate system reserve margin on Java-Bali, unless existing substation capacity i s expanded at many locations throughout Java and Bali, localized electricity demand growth w i l l be severely constrained over the medium term. But o f immediate concern i s the fact that many existing transmissionhubtransmission lines and substations are already experiencing very high loading and/or extremely poor voltage, thus placing the security o f many localized parts o f the Java-Bali power system at risk. Consequently, significant investment to strengthen the system b y uprating existing lines and expanding existing substations would be required even if demand were to remain constant, and the Project directly supports PLN’s efforts in this regard, as does ADB’s complementary Power Transmission Improvement Sector Project (approved in December 2002). The Project focuses on the Java-Bali power system given the relative importance of i t s secure operation to the overall Indonesian economy, and i t s relative state o f readiness to make the transition to a commercially-viable and competitive operation. Furthermore, while the Bank has not undertaken recent analytical work on the outside Java power system, ADB has just approved a new loan to PLN for critical investment needs in the Outer Islands.

Preparation for Domestic Natural Gas Sector Restructuring. To take full advantage o f the economic and environmental benefits o f the greater utilization of domestic gas, the infrastructure constraints also need to be addressed. However, additional analytical work i s required to ensure that the sources o f natural gas supply are sufficient to meet demand (particularly for power generation), as well as to assess in which sectors the focus o f future gas market development should be. While ADB are providing technical assistance to MIGAS to prepare a gas development plan, and USTDA i s working with PGN on the feasibility o f bringing gas to Java from East Kalimantan, these studies do not address the question o f gas pricing in depth, and consequently the economic utilization o f gas. Therefore, the Project w i l l include complementary TA to PGN for a gas pricing study. In addition, the Ministry o f State Owned Enterprises’ SOE Masterplan for 2002-2006 refers to the intent to proceed with the further privatization o f PGN through the sale of interests in subsidiary companies, but provides no details. Consequently, the Project w i l l include TA to prepare PGN for the restructuring and unbundling o f i t s operations (particularly transmission from distribution) as well as for increasing private equity in the domestic gas sector, by identifying additional strategic partners for gas transmission, and by preparing for a limited IPO for gas distribution. I t i s envisaged that the implementation o f the framework developed through this preparatory work w i l l be supported under a new S I L to PGN in FY04.

- 1 0 -

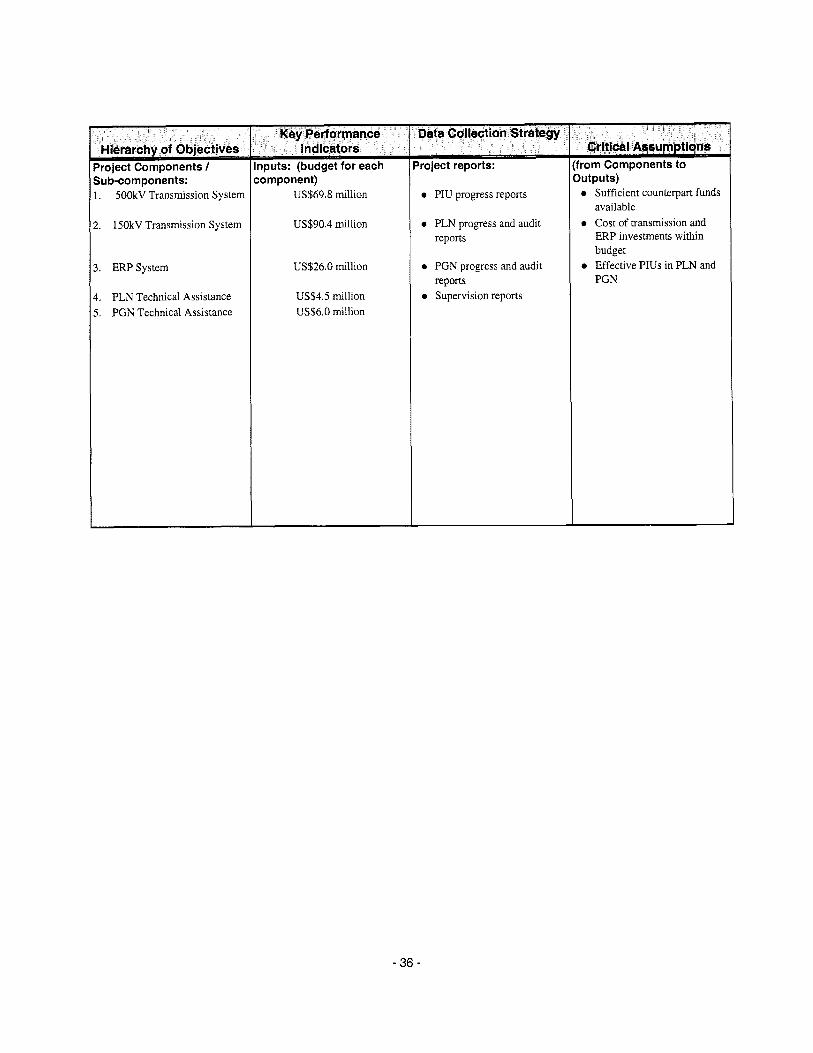

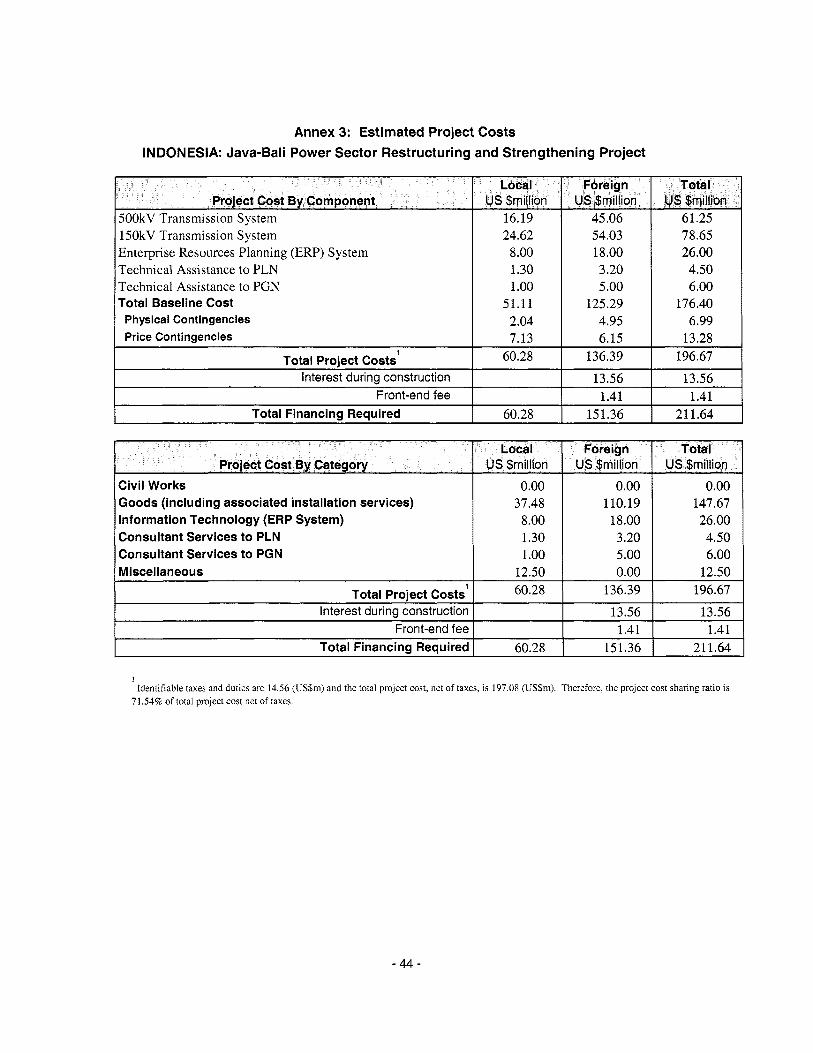

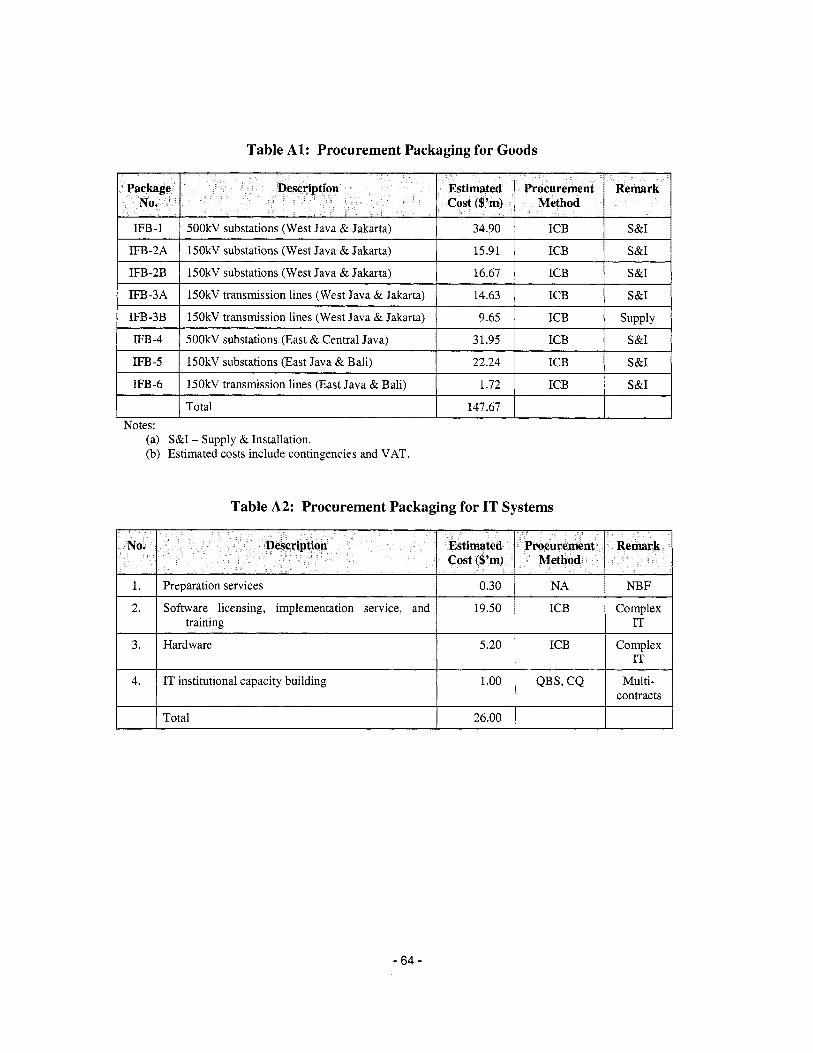

C. Project Description Summary 1. Project components (see Annex 2 for a detailed description and Annex 3 for a detailed cost breakdown) :

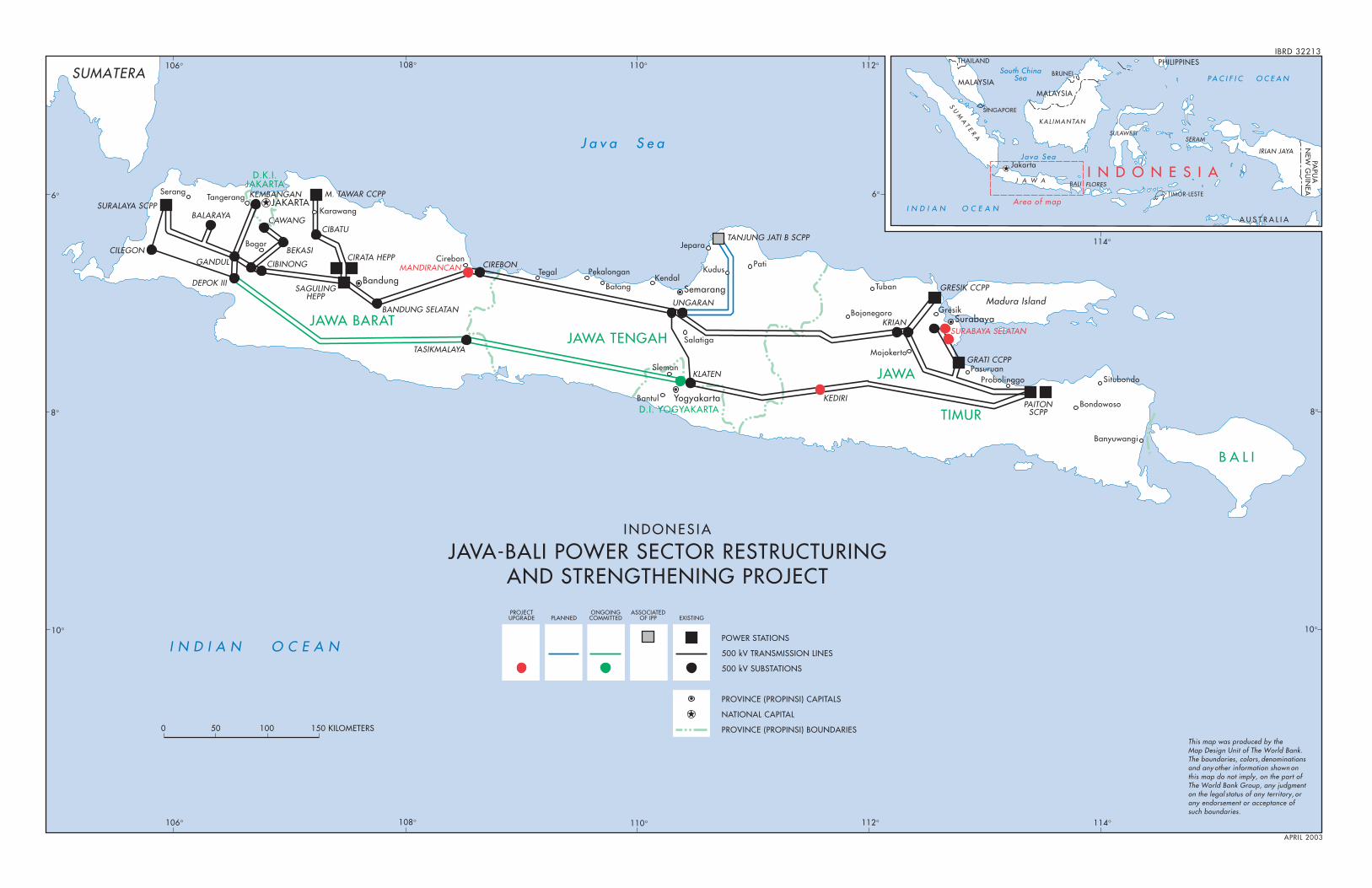

Component 1 - Power System Strengthening (500kV Transmission Svstem)

The Project w i l l support PLN’s initiatives to (a) achieve greater utilization o f existing generation capacity on Java-Bali, (b) improve the security o f supply to the cities o f Cirebon and Surabaya, and (c) debottleneck local interconnections between bulk transmission and subtransmission levels, by: (i) expanding existing 500kV substations; and (ii) installing new 500kV circuit breakers. Total cost o f this component i s US$69.8 mill ion (including contingencies and VAT), with IBRD financing o f US$50.0 million.

Component 2 - Power System Strengthening (150kV Subtransmission System)

The Project w i l l support PLN’s initiatives to (a) provide a level o f security commensurate with the existing and potential PLN and P P geothermal generation capacity evacuated through the West Java 150kV subtransmission network near Bandung, (b) improve security o f supply to Surabaya, and (c) relieve multiple localized overloading and voltage problems at subtransmission level-via PLN’s 150/70kV and 150/20kV transformer replacement and substation expansion program-by: (i) uprating existing 150kV subtransmission lines: (ii) expanding existing 150kV substations; and (iii) installing 150kV circuit breakers. Total cost of this component i s US$90.4 mi l l ion (including contingencies and VAT), with IBRD financing o f US$60.1 million.

Component 3 - P L N Enterprise Resource Planning System

The Project w i l l support P L N to implement a pilot rollout o f the company’s Enterprise Resource Planning (ERP) information system. The focus o f this pilot w i l l be core financial, materials management, human resources management and asset management in P L N Pusat and three representative subsidiary business units. This component w i l l help to facilitate PLN’s corporate and financial restructuring. Total cost o f this component i s US$26.0 million, with IBRD financing o f US$20.0 million. Activities under this component that are undertaken after appraisal completion (using IBRD procurement procedures), w i l l be eligible for retroactive financing under the loan.

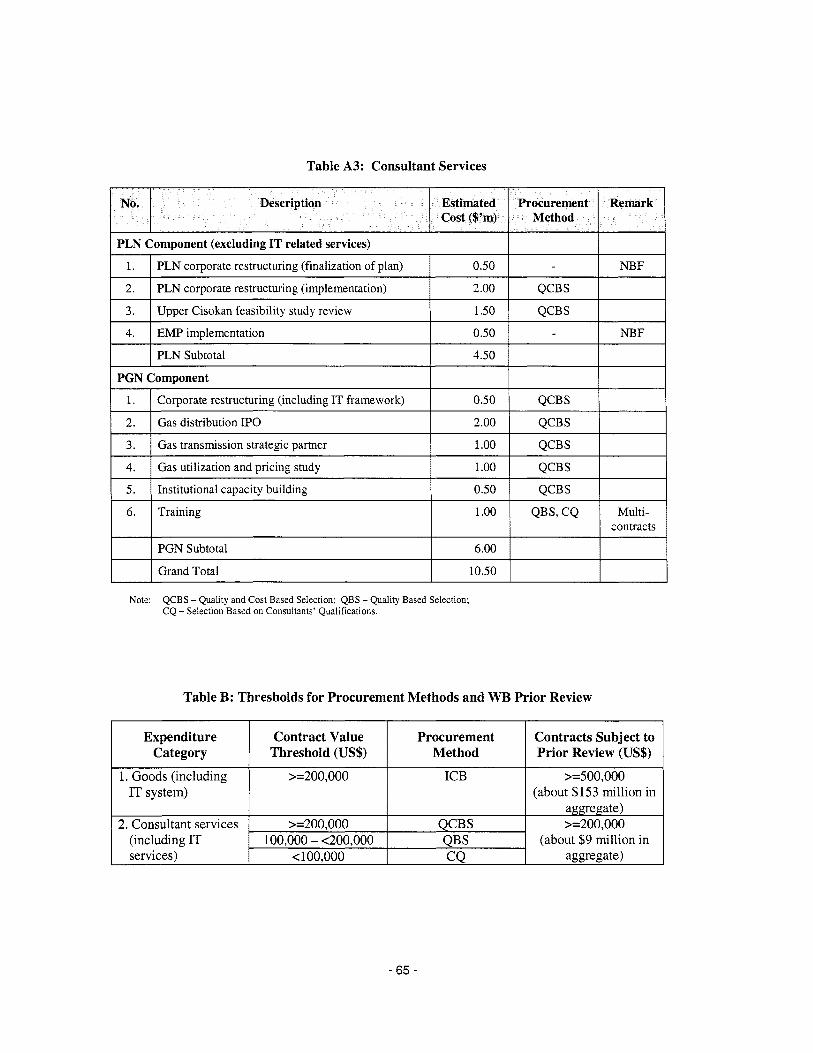

Component 4 - PLN Restructuring and Institutional Strengthening (Technical Assistance)

The Project w i l l also support PLN’s restructuring program-as well as i t s institutional strengthening initiatives-through technical assistance for: (i) finalizing an action plan for the business reorganization and corporate restructuring o f P L N (; (ii) facilitating the implementation o f that Plan: and (iii) strengthening PLN’s core capacity for environmental and social management. (Consultancy services for items (i) and (iii) wi l l be financed b y PLN). IBRD financing o f item (ii) i s $2 million. Additional TA (IBRD financing $1.5 million) w i l l be provided to PLN for reviewing the detailed design and cost estimate o f the Upper Cisokan pump storage generating plant on Java. Total cost o f this component i s US$4.5 million, with IBRD financing o f US$3.5 million.

- 1 1 -

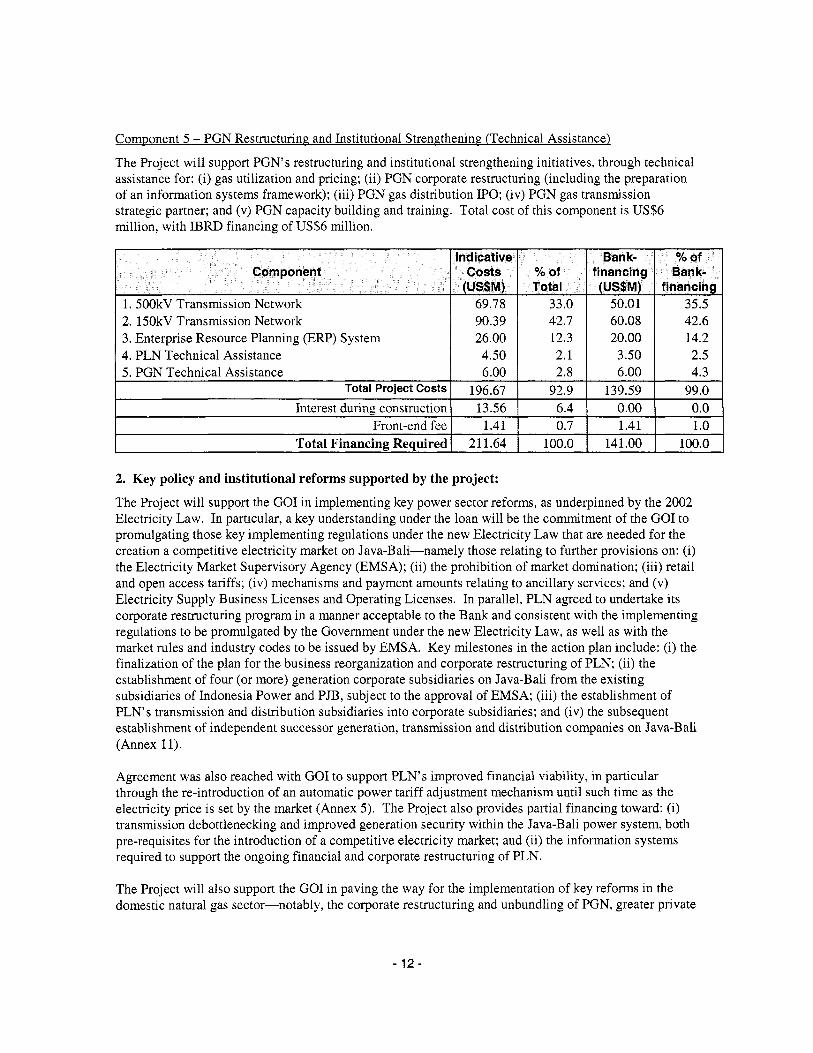

Component 5 - PGN Restructuring and Institutional Strengthening (Technical Assistance)

The Project w i l l support PGN’s restructuring and institutional strengthening initiatives, through technical assistance for: (i) gas utilization and pricing; (ii) PGN corporate restructuring (including the preparation o f an information systems framework); (iii) PGN gas distribution IPO; (iv) PGN gas transmission strategic partner; and (v) PGN capacity building and training. Total cost of this component i s US$6 million, wi th IBRD financing of US$6 million.

90.39 26.00 4.50 6.00

2. 150kV Transmission Network 3. Enterprise Resource Planning (ERP) System 4. PLN Technical Assistance 5. PGN Technical Assistance

42.7 60.08 42.6 12.3 20 * 00 14.2 2.1 3.50 2.5 2.8 6.00 4.3

Total Project Costs Interest during construction

196.67 92.9 139.59 99.0 13.56 6.4 0.00 0.0

I Front-end fee I 1.41 I 0.7 I 1.41 I 1.0 I Total Financing Required 1 21 1.64 1 100.0 I 141.00 I 100.0 I

2. Key policy and institutional reforms supported by the project:

The Project w i l l support the GO1 in implementing key power sector reforms, as underpinned b y the 2002 Electricity Law. In particular, a key understanding under the loan w i l l be the commitment o f the GO1 to promulgating those key implementing regulations under the new Electricity Law that are needed for the creation a competitive electricity market on Java-Bali-namely those relating to further provisions on: (i) the Electricity Market Supervisory Agency (EMSA); (ii) the prohibition o f market domination; (iii) retail and open access tariffs; (iv) mechanisms and payment amounts relating to ancillary services; and (v) Electricity Supply Business Licenses and Operating Licenses. In parallel, P L N agreed to undertake i t s corporate restructuring program in a manner acceptable to the Bank and consistent with the implementing regulations to be promulgated b y the Government under the new Electricity Law, as well as with the market rules and industry codes to be issued by EMSA. Key milestones in the action plan include: (i) the finalization o f the plan for the business reorganization and corporate restructuring o f PLN; (ii) the establishment o f four (or more) generation corporate subsidiaries on Java-Bali f rom the existing subsidiaries o f Indonesia Power and PJB, subject to the approval o f EMSA; (iii) the establishment o f PLN’s transmission and distribution subsidiaries into corporate subsidiaries; and (iv) the subsequent establishment o f independent successor generation, transmission and distribution companies on Java-Bali (Annex 11).

Agreement was also reached with GO1 to support PLN’s improved financial viability, in particular through the re-introduction o f an automatic power tariff adjustment mechanism until such time as the electricity price i s set by the market (Annex 5). The Project also provides partial financing toward: (i) transmission debottlenecking and improved generation security within the Java-Bali power system, both pre-requisites for the introduction o f a competitive electricity market; and (ii) the information systems required to support the ongoing financial and corporate restructuring o f PLN.

The Project w i l l also support the GO1 in paving the way for the implementation o f key reforms in the domestic natural gas sector-notably, the corporate restructuring and unbundling o f PGN, greater private

- 1 2 -

sector participation in both PGN’s gas transmission and distribution operations, as well as the establishment o f a rational natural gas pricing policy. These reforms in the domestic gas sector w i l l in tum support the greater utilization o f natural gas for power generation on Java-Bali. Technical assistance w i l l also be provided to PGN for the capacity building required to enable the company to undertake such major changes.

3. Benefits and target population:

The restructuring o f PLN’s operations on Java-Bali in line with the Electricity Law, and the physical investments under the loan, w i l l a l l contribute to the improved performance o f the electricity sector on Java-Bali. Investments in the Java-Bali transmission and subtransmission system w i l l improve: (i) overall and localized system efficiency, through less expensive generation dispatch, reduced losses and extended asset lifetimes; (ii) overall and localized system security, through lessened likelihood o f power outages due to an increase in generation reserve margin and expanded localized transmission/subtransmission; (iii) and localized system quality, through improved voltage levels-particularly important for industrial consumers o f electricity, and thus for the wider macroeconomic. Furthermore, even if sufficient investments in generation capacity are made to restore an adequate system reserve margin on Java-Bali, unless existing substation capacity i s expanded at many locations throughout Java and Bali, localized electricity demand growth w i l l be capped. Investments in information systems for PLN w i l l support the improved efficiency of PLN’s operations, and act as a catalyst for unbundling o f the company. This w i l l in tum allow the introduction o f competition, thus placing downward pressure on costs, benefiting al l electricity consumers on Java and Bali.

The blueprint for restructuring PGN w i l l pave the way for increased domestic utilization o f natural gas, thus leading to significant economic and environmental benefits for all group o f consumers.

4. Institutional and implementation arrangements:

Implementation Period. The Project w i l l be implemented over five years.

Executing Agencies. The executing agencies for the Project w i l l be P L N and PGN. P L N w i l l be responsible for implementing Components 1-4, and PGN for Component 5 (para. C-1).

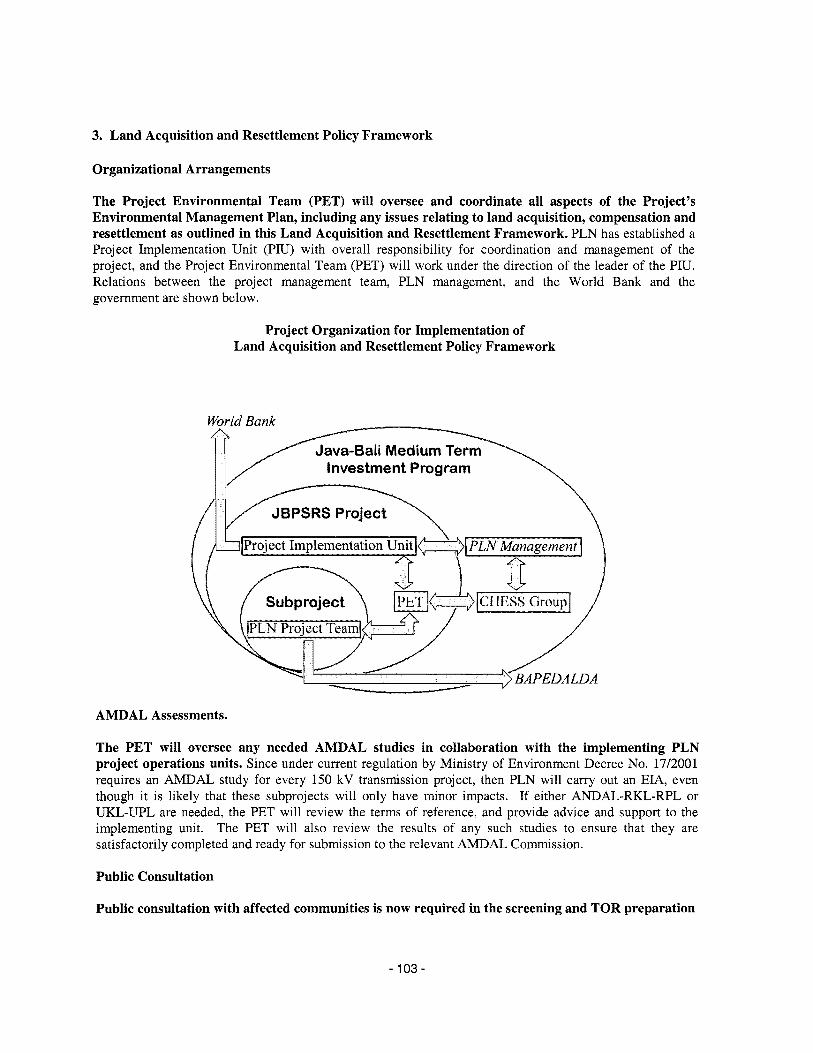

Project Implementation. Within PLN, three units w i l l have responsibilities for project implementation, they are: the Project Implementation Unit (PIU), P L N Project Java-Bali (PLN Proyek Induk Pembanglut dan Jaringan Jawa Bal i and Nusra), and PLN’s Java-Bali Transmission Business Unit (P3B). The P IU was established on September 18, 2002 b y P L N President Director Decree No. 134.K/OlO/DIR/2002 specifically for this Project. I t i s located at P L N head office in Jakarta and responsible to the President Director. Staffing includes one project director (full-time), assisted by five activity managers-respectively for procurement, environment/social and community development, supervision and monitoring, engineering and IT-plus an additional 20 part-time professional staff. A small PIU i s established within PGN to coordinate i t s technical assistance components. (Also see Section E.4.2).

Reporting, Monitoring and Evaluation Arrangements. The main tasks associated with monitoring and reporting during the implementation process w i l l be carried out by PLN Project Java-Bali, while the responsibility o f coordination among all the parties concerned lies with the PIU. A Master Implementation Schedule w i l l be prepared by PIU, which should comprise several modules covering site preparation, environmental management, procurement, design, supply, construction, test and commissioning. PLN Project Java-Bali w i l l be required to prepare detailed schedules for site survey and preparation, and to work out with each contractor/supplier a schedule covering equipment design, manufacturing, shipping and delivery, construction and installation, test and commissioning, in line with

- 1 3 -

the master schedule. The purpose of these scheduling activities i s to provide a continual assessment not only on the predicted completion date but also o f where schedule slippages are occurring so that remedial action can be taken in a timely manner.

The P IU w i l l prepare Project Progress Reports on a quarterly basis. Such reports w i l l cover al l aspects related to project implementation, including but not limited to: project implementation status, progress made in the last quarter, procurement, construction, installation, schedule and cost control, issues/problems and actions. Progress and status o f implementing the Environmental Management Plan (EMP) and the Land Acquisition and Resettlement Policy Framework (LARPF) w i l l also be included in the quarterly reports. Upon completion o f the Project, a completion report w i l l be prepared to assess the achievement o f project objectives, to assess the project design and implementation experience, to draw lessons learned, and to prepare plans for project operation.

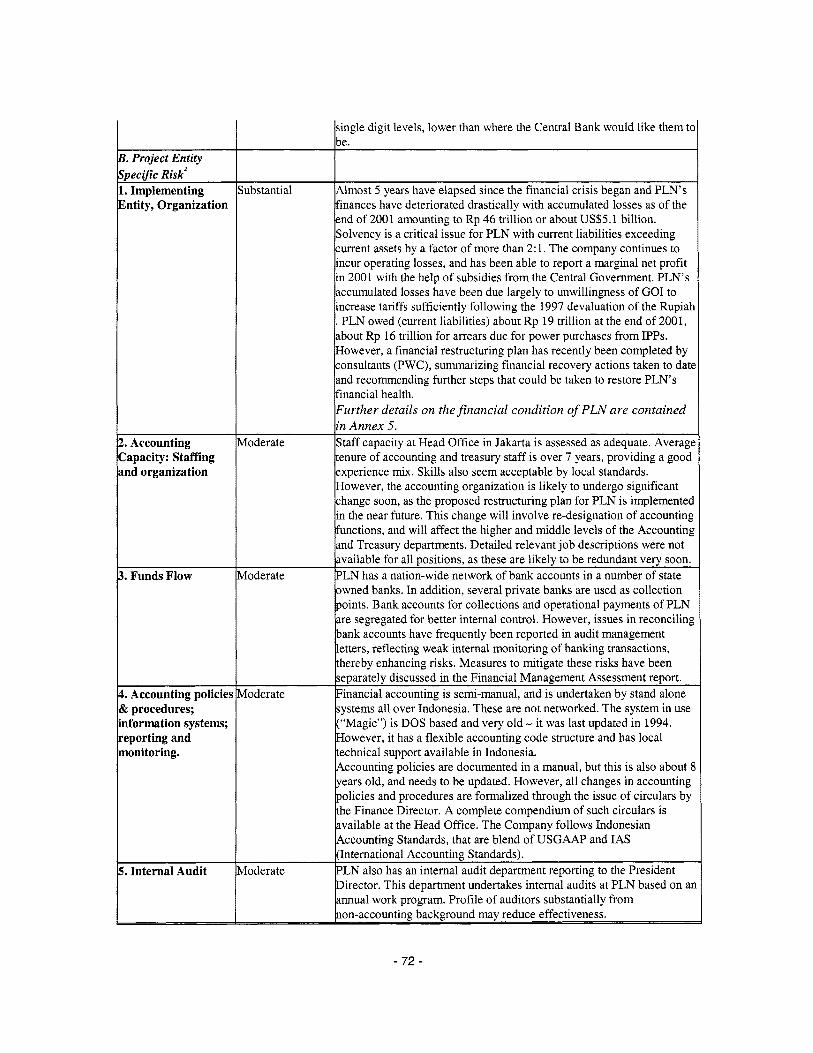

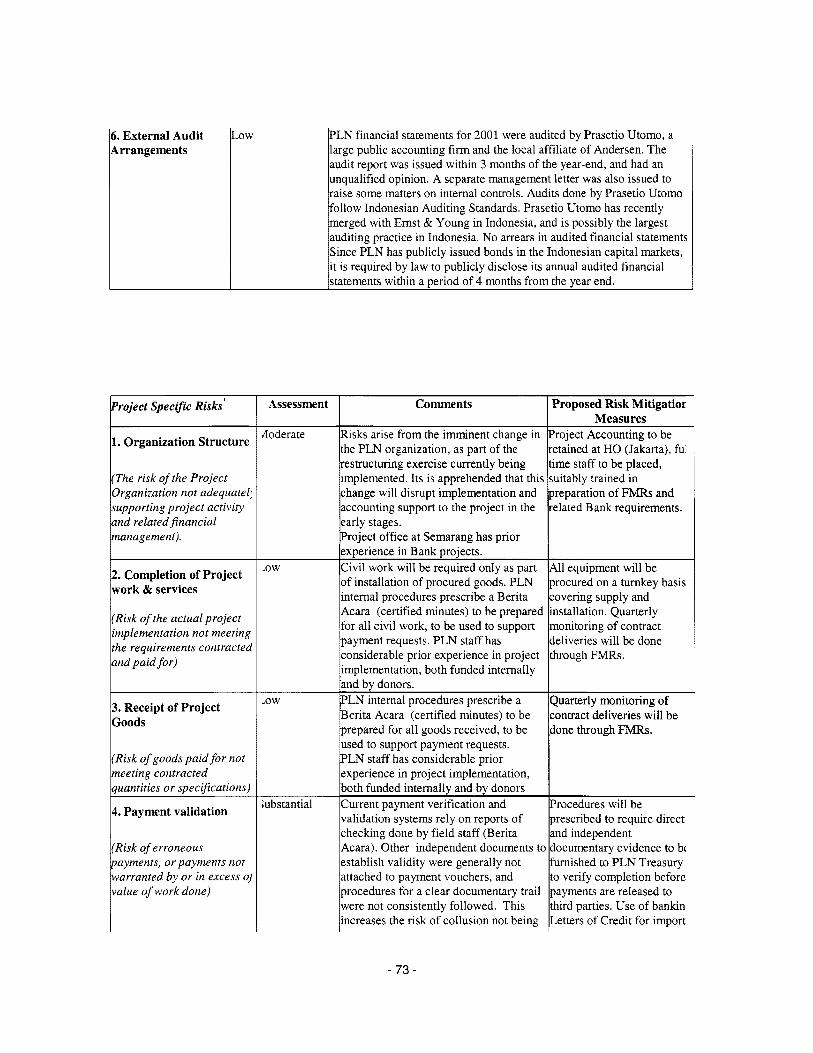

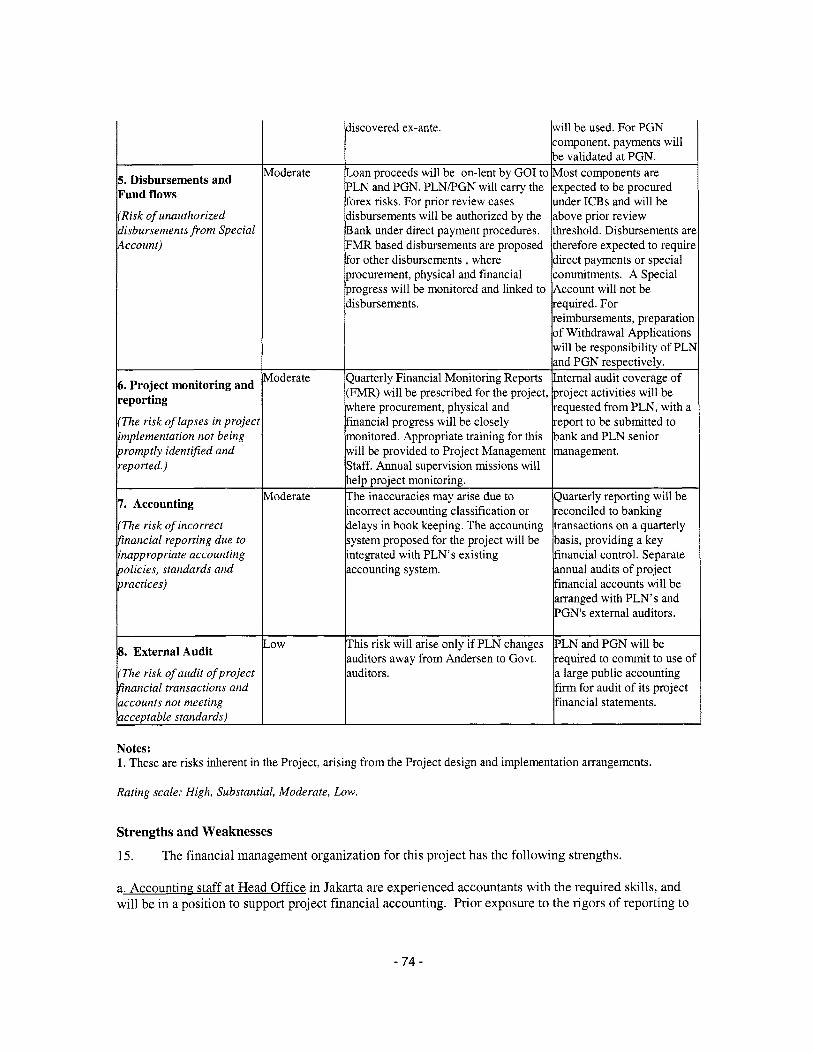

Accounting, Financial Reporting and Auditing Arrangements. A financial management assessment o f P L N was conducted by a Bank financial management specialist during the pre-appraisal mission in September 2002. (Given the relatively small size o f PGN’s portion o f the loan, comprising only a few TA activities which w i l l a l l subject to the Bank prior-review, the financial management capacity assessment has focused on P L N as the primary implementing agency). As a part o f this assessment, an evaluation was conducted o f the r isks inherent in the choice o f P L N as primary project implementing entity, as well as specific r isks arising from the proposed project design and implementation arrangements. In addition, consideration was given to the overall control environment in the country, as determined b y the Country Financial Accountability Assessment Report, a diagnostic study undertaken by the Bank in the year 2001.

The financial management assessment has concluded that while the overall country risks were substantial, arising f rom the continued weaknesses in public expenditure management, r isks arising f rom PLN as a project entity were rated moderate. PLN’s long prior experience in managing donor funds for their projects and the company’s exposure to local capital market accounting and auditing regulations arising out of the public issue o f bonds imparts some strengths to i t s financial management capacity. However, some weaknesses remain in accounting systems and payment validation procedures. Measures have been proposed to mitigate these r isks for purposes o f this Project.

Currently PLN’s financial accounts are audited b y a private sector accounting firm, Prasetio Utomo (previously the local affiliate o f Andersen). This firm has recently merged with the local affiliate o f Ernst & Young, public accountants. I t has been proposed that the Andersen-Emst & Young merged entity w i l l also be appointed as the auditor for project financial accounts. N o incremental cost for this w i l l be charged to the loan. The expenditure at PGN, being relatively small, w i l l also be audited by the same auditor so that consolidated project accounts can be audited and presented. More details o f the financial management assessment, as well as on accounting, financial reporting and auditing arrangements, are provided in Annex 6B.

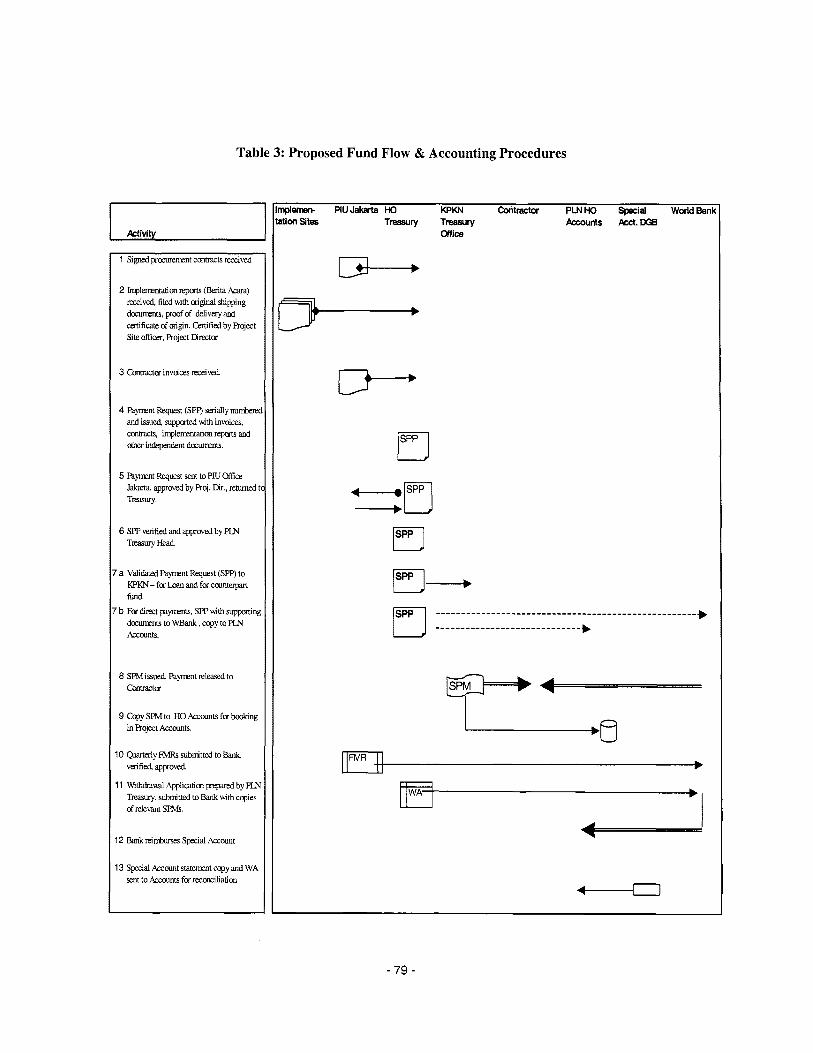

Disbursement Arrangements. I t i s proposed that about 85% o f the project expenditure w i l l be on goods that are likely to be subject to prior review procedures, and w i l l involve direct payments or special commitments. Some smaller payments would be reimbursed by the Bank to PLN at consolidated amounts of at least $200,000 per withdrawal application. A Special Account w i l l not be required for this project.

The Ministry o f Finance w i l l on-lend the funds associated with Components 1-4 to PLN, and the funds associated with Component 5 to PGN. This w i l l be achieved through Subsidiary Loan Agreements,

- 1 4 -

which would pass on all r isks and costs-including foreign exchange risk-incurred by the Government to PLN and PGN, on terms agreed with the Bank. More details of disbursement arrangements are provided in Annex 6B.

D. Project Rationale 1, Project alternatives considered and reasons for rejection:

The original project design-which reached Concept Review stage in November 2000-was for a hybrid-SECAL operation, given the perceived need o f the Government at that time for budgetary support, with physical components relating to both the power and domestic gas sectors. When the need for a balance-of-payments component reduced, the operation was reformulated as an APL. However, the importance o f the power sector issues, and the state o f readiness o f the power sector components as opposed to those intended for the domestic gas sector, led to the GO1 deciding to narrow the scope o f the operation to a Specific Investment Loan (SIL) focusing on the power sector.

The Project w i l l finance critically needed investments for strengthening the electricity supply system on Java-Bali, as well as investments in the information systems needed to support PLN’s financial and corporate restructuring. The Project i s intended to extend the support already being provided b y the Bank under the Second Power Transmission and Distribution project to help P L N implement i t s financial and corporate restructuring program. B y reaching agreements with the Government and P L N on key actions needed to be taken over the short to medium term, the Project w i l l help to restore PLN’s financial viability and result in an appropriately-designed corporate structure consistent with the new Electricity Law.

The proposed financing amount i s relatively minimal in the context o f the sector’s overall investment needs, involving only the most urgently-needed transmission and subtransmission investments for strengthening the existing power delivery system, based on the current level o f generation capacity and irrespective o f the completion time o f the remaining components o f the transmission system. Nevertheless, with looming generation shortfalls in the short to medium term, the existing electricity delivery system needs to be more effectively utilized, with measures taken to maintain and improve current levels o f system reliability and service quality. Furthermore, over the medium to longer term, a competitive power market with increased private sector participation w i l l not be able to be introduced even in a restructured power sector, should constraints and bottlenecks s t i l l exist in the bulk transmission network. On the other hand, even once an adequate generation reserve margin i s restored and geographic transmission constraints have been removed, numerous localized constraints w i l l s t i l l remain between transmission and subtransmission levels, and between subtransmission and distribution levels, unless actions are taken now to begin debottleneclung such constraints.

The choice o f the Project’s physical subcomponents was made after a full assessment o f the Java-Bali supply and demand balance, along with PLN’s corresponding investment program, in conjunction with other donors. Subcomponents were chosen based on their ability to: (i) achieve greater utilization o f existing generation capacity on East Java, by relieving constraints in the bulk transmission grid; (ii) improve the reliability o f existing generation supply at the West Java P L N and IPP geothermal power plants, b y strengthening the associated local transmission system: and (iii) improve the reliability and quality o f power supply at various poorly-performing locations throughout Java and Bali, b y strengthening and debottlenecking local subtransmission networks-in turn allowing for increased localized demand growth. All o f the selected subcomponents are incremental investments that w i l l provide more cost effective improvements in supply efficiency, reliability and quality than would be the case with constructing entirely new lines and substations.

- 1 5 -

Not undertaking these investments would result in continued system bottlenecks and inefficiencies, in tum creating an artificial demand for new power generation capacity, which-if such capacity were constructed-would be constrained by the same bottlenecks. One alternative might be to utilize the same level of funds on demand side measures. However, the Java-Bali system has suffered from chronic underinvestment for the past 5-6 years, and the level o f system loadings in many localized areas are far in excess o f levels which could be efficiently mitigated by local demand side initiatives. Nevertheless, P L N i s not neglecting the demand side, having already initiated a comprehensive Integrated Resource Planning (IRP) Program o f both supply-side and demand-side measures, including: (i) increasing peak power tariffs relative to off-peak tariffs; (ii) offering interruptible tariffs to large consumers, as well as buyback tariffs from customers with their own captive power plants; and (iii) promoting the replacement o f existing street lighting with high efficiency bulbs. (This Program i s being supported through grant financing from USAID).

The feasibility o f financing rehabilitation needs o f existing power plant in the Java-Bali system, particular for the Suralaya coal-fired plant was also assessed. Given the capacity o f the Suralaya coal-fired plant and i t s importance to the Java-Bali power system (almost 20% o f capacity, located close to Jakarta), maintaining plant availability i s o f paramount importance. However, this option was rejected b y PLN, as including a rehabilitation o f Suralaya in the scope would delay the Project because more detailed feasibility studies s t i l l need to be undertaken.

As for the proposed support to PLN’s information systems renewal program, PLN’s existing IT hardware and software i s outdated, fragmented and geared to i t s present monolithic structure. Upgrading information systems i s a prerequisite for effective implementation o f corporate (and financial) restructuring, and for improving management and operational efficiencies.

- 1 6 -

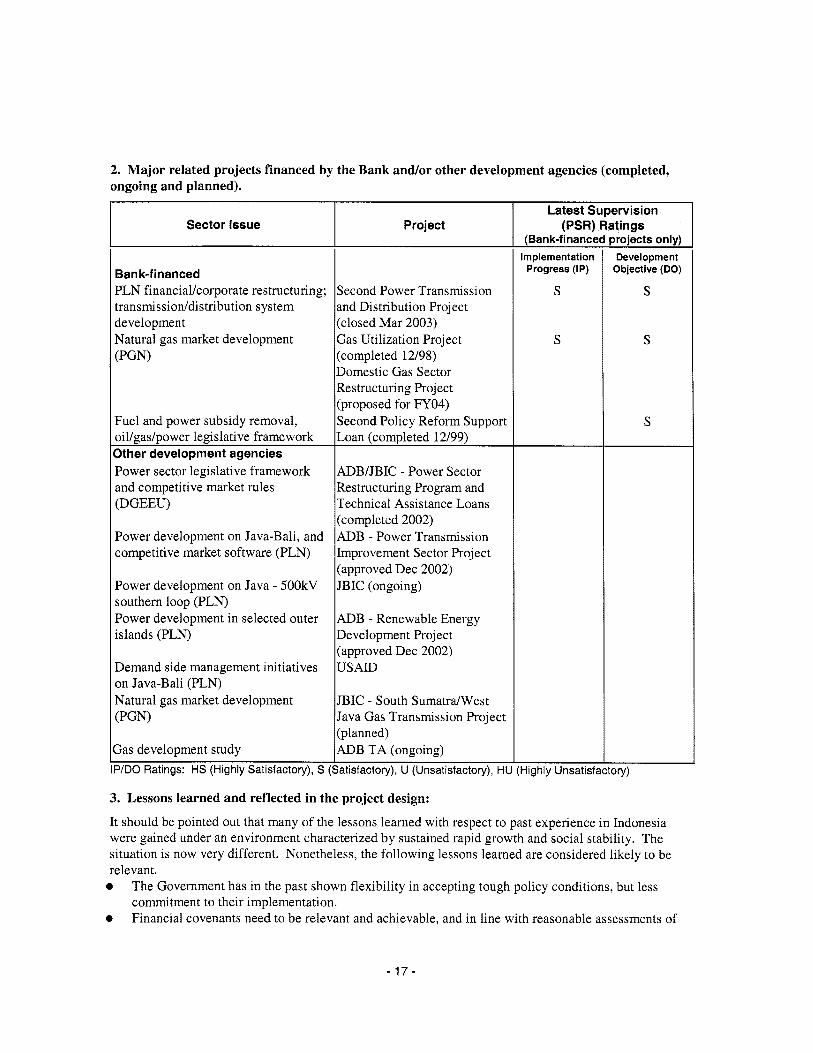

2. M a j o r related projects financed by the Bank and/or other development agencies (completed, ongoing and planned).

~ Sector Issue

Ban k-financed PLN financial/corporate restructuring; transmission/distribution system development Natural gas market development

I

(PGN)

Fuel and power subsidy removal, oil/gas/power legislative framework Other development agencies Power sector legislative framework and competitive market rules (DGEEU)

Power development on Java-Bali, and competitive market software (PLN)

Power development on Java - 500kV southern loop (PLN) Power development in selected outer islands (PLN)

Demand side management initiatives on Java-Bali (PLN) Natural gas market development (PGN)

Gas development study

Project

Second Power Transmission and Distribution Project (closed Mar 2003) Gas Utilization Project (completed 12/98) Domestic Gas Sector Restructuring Project (proposed for FY04) Second Policy Reform Support Loan (completed 12/99)

ADB/JBIC - Power Sector Restructuring Program and Technical Assistance Loans (completed 2002) ADB - Power Transmission Improvement Sector Project (approved Dec 2002) JBIC (ongoing)

ADB - Renewable Energy Development Project (approved Dec 2002) USAID

JBIC - South Sumatra/West Java Gas Transmission Project (planned) ADB TA (ongoing)

I I IP/DO Ratings: HS (Highly Satisfactory), S (Satisfactory), U (Unsatisfactory), H l

Latest Supervision (PSR) Ratings

(Ban k-fj nance Implementation

Progress (IP)

S

S

Highly Unsatisf:

srojicts only) Development

Objective (DO)

S

S

S

ory)

3. Lessons learned and reflected in the project design:

I t should be pointed out that many of the lessons learned with respect to past experience in Indonesia were gained under an environment characterized b y sustained rapid growth and social stability. The situation i s now very different. Nonetheless, the following lessons learned are considered likely to be relevant.

0 The Government has in the past shown flexibility in accepting tough policy conditions, but less commitment to their implementation.

0 Financial covenants need to be relevant and achievable, and in line with reasonable assessments o f

- 1 7 -

implementing agency financial performance. Appropriate performance indicators and monitoring are essential. Attention needs to be given to accurate cost estimates and on application of contingencies, as well as to availability o f counterpart funding.

Based on the Bank’s experience in Indonesia and in the region, particular attention was paid to: Ensuring simple and transparent project design, not dependent on any related components financed by other donors. Adopting realistic implementation and disbursement schedules. Preparing a detailed procurement plan, involving a relatively small number o f packages under single responsibility contracts. Providing a small set of focused but realistic loan conditionalities, particularly with regard to financial covenants. Ensuring that key Government commitments have been undertaken prior to loan negotiations (e.g. increases in power tariffs). Establishing a strong and well staffed P IU with full responsibility for coordination and management o f the Project, and a Project Environment Team (PET) for coordinating and overseeing al l aspects o f the Environmental Management Plan (EMP) and Land Acquisition and Resettlement Policy Framework. The Project w i l l also provide close supervision o f PLNs own capacity building program for implementing the institutional strengthening aspects o f the Project’s EMP.

4. Indications of borrower commitment and ownership:

The Project has been included in the l i s t o f priority projects in the sector. In June 2002, a limited Cabinet meeting agreed that P L N could proceed with discussions relating to 16 loans from multilateral and bilateral sources already in the pipeline (amounting to an envelope o f US$804 million) including specifically for this project. In addition, despite the difficult political and economic environment the country has been facing over the past several years, a number o f notable steps have already been taken b y the Government and P L N to address some o f the sector issues and demonstrate commitment to the Proiect (see also B-2). ” .

Electricity Law. .The new Electricity Law was passed on September 23, 2002, potentially paving the way for a competitive power market operation (at least on Java-Bali) over the medium to long term. In addition to preparing the groundwork for the establishment o f the new regulatory agency (EMSA), the Directorate General for Electricity and Energy Utilization (DGEEU) has already drafted the majority of supporting regulations, rules, and codes. Notably, DGEEU recently issued i t s blueprint for implementing the Electricity Law over the period 2003-2010. PLN’s Restructuring Program. In May 2001, P L N engaged Bank-financed consultants to design i t s restructuring implementation program, and the new organizational design, job descriptions and performance indicators have been approved for implementation b y PLN’s Board o f Commissioners. In addition, P L N initiated a wide-ranging efficiency drive initiative, following up on the findings o f the special audit o f PLN undertaken in 1999 (Annex 11). Financial Restructuring Measures. In parallel, the GO1 has already taken steps to improve PLN’s financial position, through the approval in June 2001 o f the conversion o f Rp29 tri l l ion o f PLN’s overdue interest (plus fines) to equity, and the unpaid principal o f Rp5 tri l l ion was converted to a new 20 year loan. Also, in December 2001, the Government paid Rp6.7 tri l l ion to P L N in order to cover three years o f “targeted” subsidies relating to the costs o f supplying PLN’s lowest consumption customers. Significantly, the Government has agreed in principle that power tariffs w i l l reach pre-crisis levels b y 2005 (i.e., US7 centskwh), permitted P L N to increase tariffs b y 6% on average per quarter during 2002, and confirmed power tariff increases for 2003 that w i l l result in an average tariff o f about US6.8cikWh. Finally, P L N has now successfully renegotiated or closed out the

- 1 8 -

majority o f power purchase agreements (PPAs) entered into prior to the crisis, and has reached agreement on the payment o f arrears to those IPPs with currently-operating power plants. Establishment of Project Implementation Unit (PIU) and Preparation of Bidding Documents. PLN's PIU was established on September 18, 2002 b y P L N President Director Decree No. 134.WOlO/DIR/2002 specifically for this Project, and the preparation o f bidding documents began shortly afterward.

5. Value added of Bank support in this project:

The most important value added o f the Banks participation in this project i s :

(a) I t s continuing involvement in Indonesia's power sector to ensure that PLN's financial and corporate restructuring plan i s effectively introduced, given that the Banks last operation in the sector closed in March. Based on this involvement--the first operation since the crisis-- the Bank i s sending an important signal to the international community that significant progress has been made b y the GO1 and P L N in resolving sectoral issues (such as passing the Electricity Law, regularly increasing the tariff and resolving the IPP issue) and that the time i s right to resume badly needed private investments in the sector , In this context, the Bank i s cooperating with the ADB and JBIC, which are also sending the same message (through already approved loans). The fact that PLN has achieved i t s present level o f financial viability (with Government help), and developed a plan for a rational corporate structure, would probably not have been accomplished without the Banks active involvement. Yet, further Bank oversight i s required i f some o f the most critical restructuring outcomes are to be achieved. Indeed, the Bank's resumption o f lending to P L N has already encouraged other donors to help that agency meet i t s huge investment needs, and w i l l also contribute to renewed confidence for the private sector's participation in the sector.

(b) Its involvement in the domestic gas sector (via PGN), helping develop a rational gas pricing structure and restructuring PGN, since these reforms could not be achieved without the Bank's technical assistance and support (to implement the TA). Such restructuring i s crucial to pave the way for the private sector to re-enter this subsector, so that gas requirements for power generation and industry can be met.

These two areas o f value added should be assessed in the context o f the enormous importance o f the energy sector to the economy, the critical issues facing the sector, and the fact that prospects for successful outcomes are likely to be significantly enhanced b y the Banks involvement in addressing them. The required analytical work for the energy sector that has already been performed suggests that dialogue undertaken through AAA alone would not provide a level o f Bank attention sufficient to: (a) provide much support to P L N (or PGN) in implementing (and designing) their restructuring programs, particularly in terms of actions intended to restore PLN's financial viability; or (b) be a credible donor partner. For example, JBIC expects the Bank to address pricing and structural issues in the domestic gas sector in such a way that would support i t s proposed South Sumatra-West Java Gas Transmission project. B y the same token, ADB i s expecting the Bank to continue supervising and monitoring the implementation of PLNs corporate and financial restructuring activities, which complement ADB's sectoral restructuring activities.

Some o f the other important value added contributions are:

0

0

0

The Bank w i l l bring i t s international uti l i ty experience to bear in overseeing the introduction and procurement o f PLNs information systems. The Bank w i l l supervise PLNs program to strengthen i t s institutional capacity for environmental and social management (as outlined in the Project's EMP), thus imparting substantial s k i l l s to PLN staff. The technical assistance component relating to the domestic gas sector builds on a solid record o f

- 1 9 -

two successful prior projects with PGN, and prepares the way for a new lending operation with PGN that would include equally important TA. The market-sounding of international gas utilities to determine private sector interest in Indonesia’s downstream gas business has revealed a strong preference for Bank participation in the domestic gas sector, as i t would reduce the potential investors’ perception o f political r isks and offer a sound analysis o f policy issues

E. Summary Project Analysis (Detailed assessments are in the project file, see Annex 8)

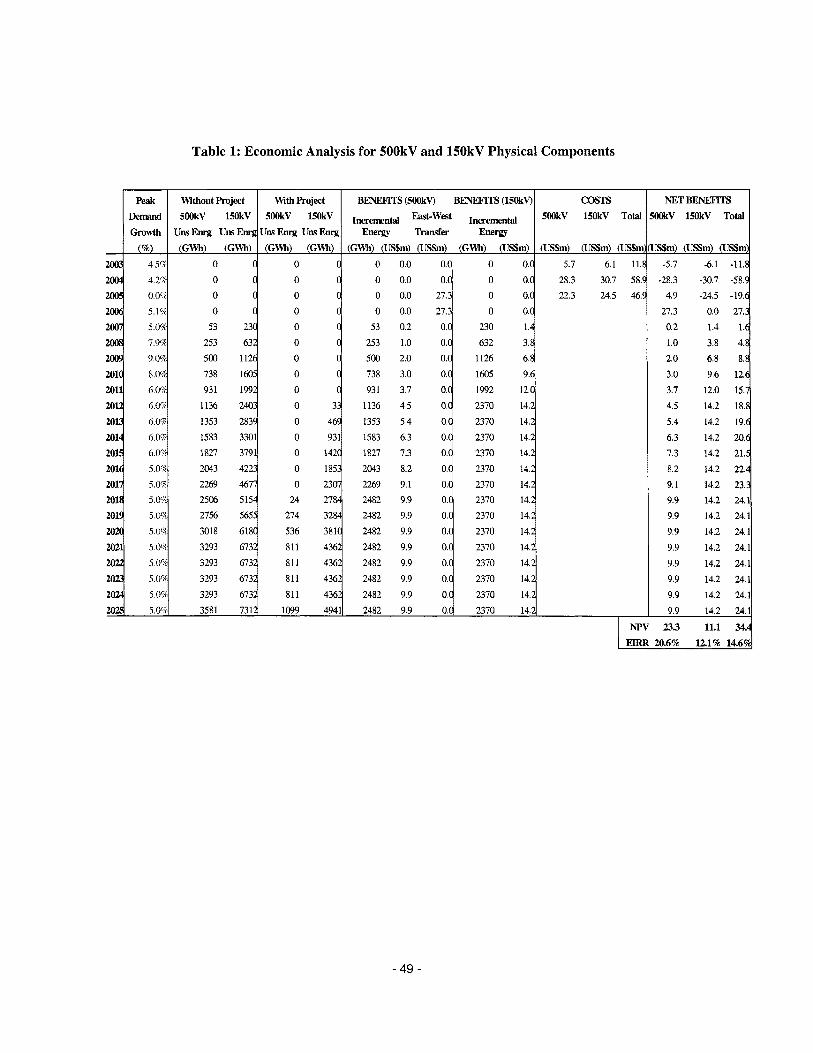

1. Economic (see Annex 4): Cost benefit NPV=US$34.4 million; ERR = 14.6 % (see Annex 4)

0 Cost effectiveness 0 Other (specify) Benefits that have been quantified for the economic analysis include: (i) the value o f the forecasted incremental demand growth with and without PLN’s 500kV and 150kV substation expansion program (which i s primarily intended to debottleneck the Java-Bali power system between transmission and subtransmission levels, and between subtransmission and distribution levels); and (ii) the avoided cost o f generation associated with relieving the (400MW) east-west Java power transfer constraint in the 500kV transmission system.