Embed Size (px)

Citation preview

Document ofThe World Bank

Report No: 17736 - GH

PROJECT APPRAISAL DOCUMENT

ONA

PROPOSED CREDIT

IN THE AMOUNT OF SDR 37.6 MILLION(US$ 50.5 MILLION EQUIVALENT)

TO THE

REPUBLIC OF GHANA

FOR

GHANA TRADE AND INVESTMENT GATEWAYPROJECT (GHATIG)

June 5, 1998

Private Sector and FinanceAFRICA REGION

CURRENCY EQUIVALENTS

(Exchange Rate Effective March, 1998)Currency Unit = Cedis

2260.0 LC = US$1

FISCAL YEARJanuary 1 to December 31

ABBREVIATIONS AND ACRONYMS

CAS Country Assistance StrategyCEPS Customs, Excise and Preventive ServicesDDI Direct Developer IdentificationEIA Environmental Impact AssessmentEMP Environmental Management PlanEPA Environmental Protection AgencyEPZ Export Processing ZoneERSO Economic Reform Support OperationESAF Enhanced Structural Adjustment FacilityFIAS Foreign Investment Advisory ServicesFTZ Free Trade ZoneGCAA Ghana Civil Aviation AuthorityGEPC Ghana Export Promotion CouncilGFZB Ghana Free Zones BoardGIPC Ghana Investment Promotion CenterGIS Ghana Immigration ServicesGOG Government of GhanaGPHA Ghana Ports & Harbor AuthorityGPN General Procurement NoticeICB International Competitive BiddingICR Implementation Completion ReportISO International Standards OrganizationLRMC Long-run marginal CostNCB National Competitive BiddingNIRP National Institutional Renewal ProgramPIU Project Implementation UnitPPI Private Participation in InfrastructurePSAC Private Sector Adjustment CreditPSAG Private Sector Advisory GroupPSD Private Sector DevelopmentPSR Private Sector RoundtableQCBS Quality and Cost-based SelectionSOE Statement of ExpendituresTA Technical AssistanceTIP Trade and Investment Project

Vice President Jean Louis SarbibCountry Director Peter HarroldSector Manager Thomas W. AllenTask Manager Demba Ba

REPUBLIC OF GHANA

TRADE AND INVESTMENT GATEWAY PROJECT

CONTENTS

A. PROJECT DEVELOPMENT OBJECTIVE 2

(i) Background, Project Development Objectives and Key Performance Indicators 2

B. STRATEGIC CONTEXT 3

(i) CAS Objectives Supported by the Project: 3(ii) Main Sector Issues and Government Strategy 3(iii) Sector Issues to be Addressed by the Project and Strategic Choices 4

C. PROJECT DESCRIPTION SUMMARY 8

(i) Project Components (see Annexes II and III for detailed description and costbreakdowns) 8

(ii) Key Policy and Institutional Reforms Supported by the Project 11(iii) Benefits and Target Population 11(iv) Institutional and Implementation Arrangements 11

D. PROJECT RATIONALE 14

(i) Project Alternatives Considered and Reasons for Rejection 14(ii) Other Related Projects Financed by the Bank and/or

Other Development Agencies 15(iii) Lessons Learned and Reflected in Proposed Project Design 16(iv) Indications of Borrower Commitment and Ownership 17(v) Value Added of Bank Support: Rationale for Bank-Group Involvement 17

E. SUMMARY PROJECT ANALYSES 18

(i) Economic Assessment 18(ii) Financial Assessment 18(iii) Technical Assessment 19(iv) Institutional Assessment 19(v) Social Assessment 19(vi) Environmental Assessment 20(vii) Participatory Approach 20

F. SUSTAINABILITY AND RISKS 20

(i) Sustainability 20(ii) Critical Risks (see fourth column of Annex I) 22(iii) Possible Controversial Aspects 23

G. MAIN LOAN CONDITIONS 23

(i) Conditions of Negotiations 23(ii) Conditions of Board 23(iii) Conditions of Effectiveness 23(iv) Other Conditions: During Project Implementation 23

H. READINESS FOR IMPLEMENTATION 24

I. COMPLIANCE WITH BANK POLICIES 24

ANNEXES

Annex 1. Project Design Summary

Annex 2. Detailed Project Description

Annex 3. Estimated Project Costs

Annex 4. Cost-Benefit Analysis Summary

Annex 5. Financial Summary

Annex 6. Procurement and Disbursement Arrangements

Table A. Project Costs by Procurement Arrangements

Table Al. Consultant Selection Arrangements

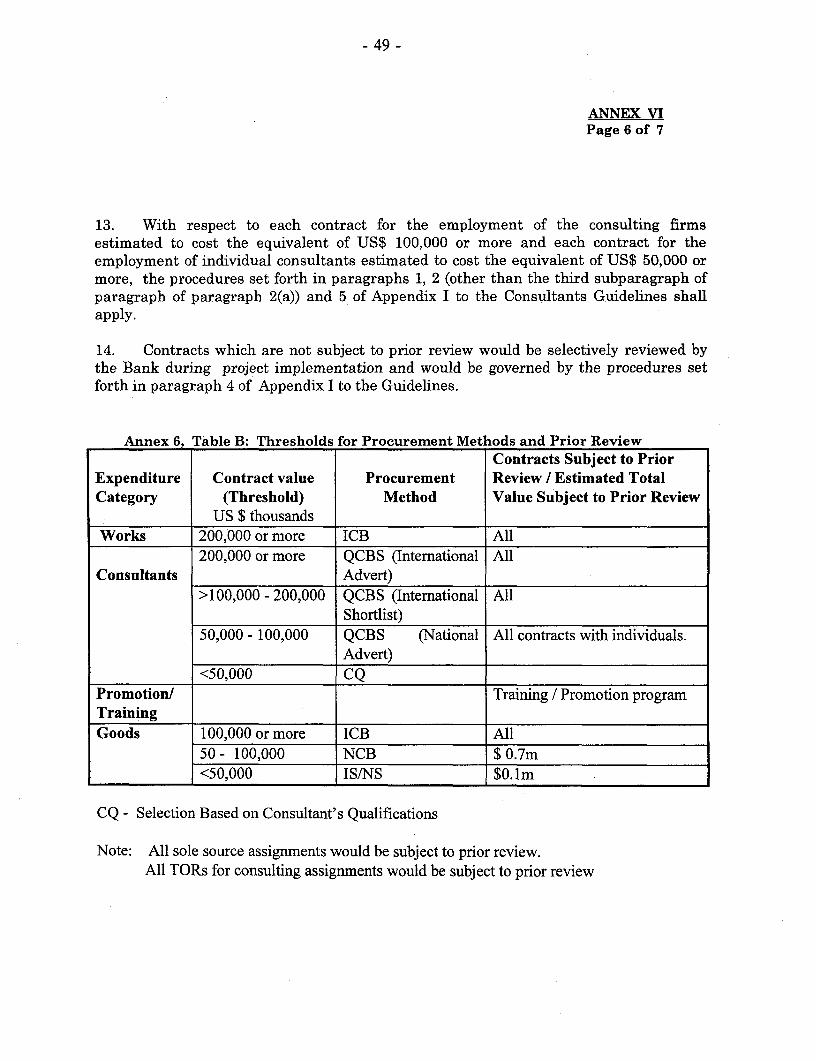

Table B. Thresholds for Procurement Methods and Prior Review

Table C. Allocation of Loan Proceeds

Annex 7. Project Processing Budget and Schedule

Annex 8. Documents in Project File

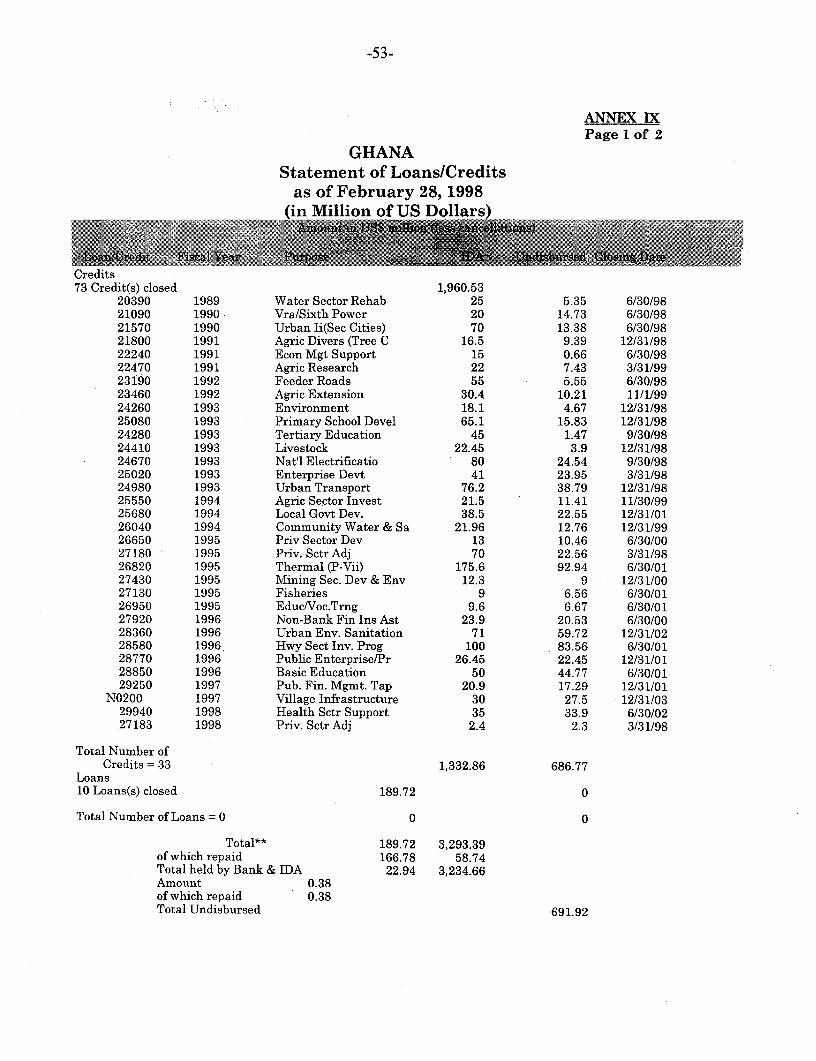

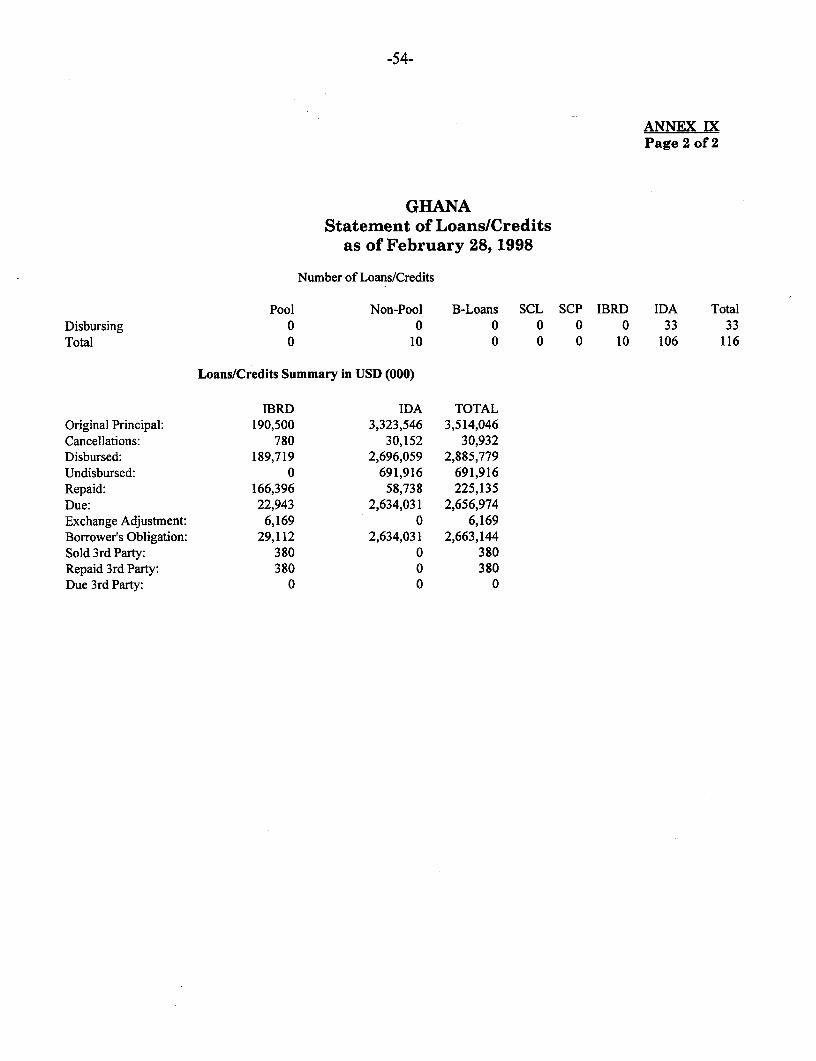

Annex 9. Statement of Loans and Credits

Annex 10. Country at a Glance

Annex 11. Letter of Sector Development Policy

Annex 12. Environmental Assessment, Social and EnvironmentalAnalyses

MAP: IBRD 23606

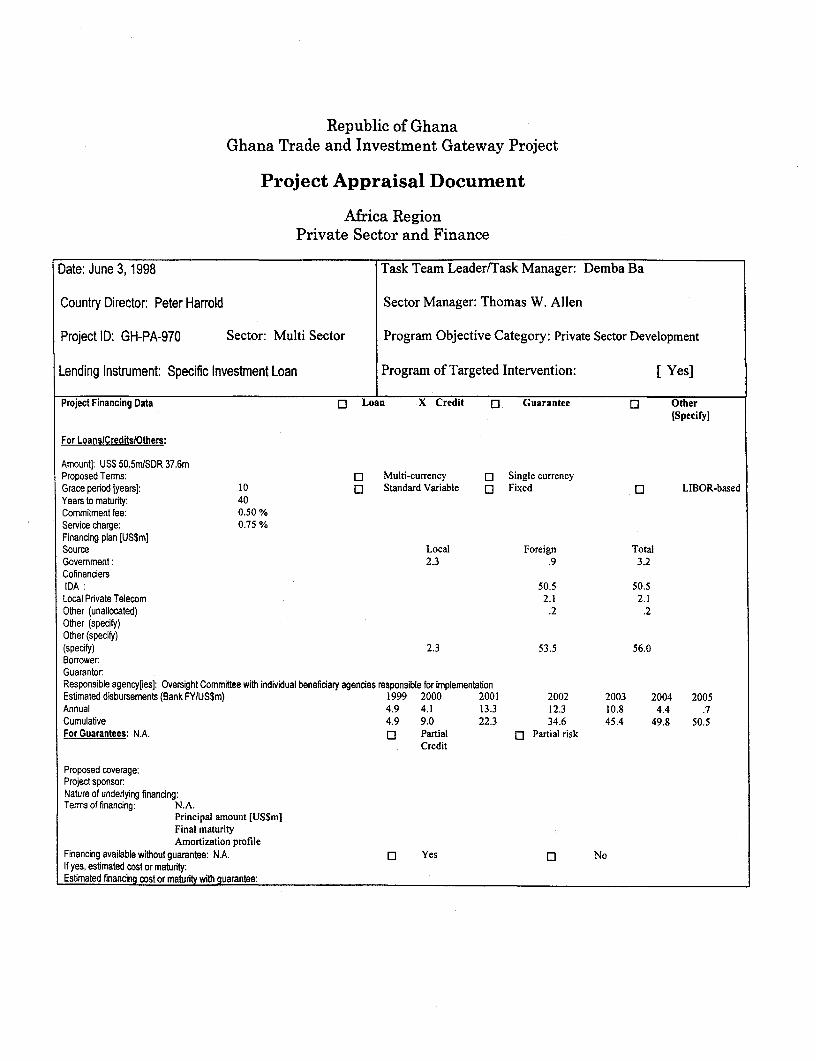

Republic of GhanaGhana Trade and Investment Gateway Project

Project Appraisal Document

Africa RegionPrivate Sector and Finance

Date: June 3, 1998 Task Team Leader/Task Manager: Demba Ba

Country Director: Peter Harrold Sector Manager: Thomas W. Allen

Project ID: GH-PA-970 Sector: Multi Sector Program Objective Category: Private Sector Development

Lending Instrument: Specific Investment Loan Program of Targeted Intervention: [ Yes]

Project Financing Data D Loan X Credit D Guarantee a Other[Specify]

For LoanslCreditslOthers:

Amount]: US$ 50.5m/SDR 37.6mProposed Terms: D Multi-currency Q Single currencyGrace period [years]: 10 Q Standard Variable [] Fixed a LIBOR-basedYears to maturity: 40Commitment fee: 0.50 %Service charge: 0.75 %Financing plan [US$m]Source Local Foreign TotalGovemment: 2.3 .9 3.2CofinanciersIDA : 50.5 50.5Local Private Telecom 2.1 2.1Other (unallocated) .2 .2Other (specify)Other (specify)(specify) 2.3 53.5 56.0Borrower:GuarantorResponsible agencyries]: Oversight Committee with individual beneficiary agencies responsible for implementationEstimated disbursements (Bank FY/US$m) 1999 2000 2001 2002 2003 2004 2005Annual 4.9 4.1 13.3 12.3 10.8 4.4 .7Cumulative 4.9 9.0 22.3 34.6 45.4 49.8 50.5For Guarantees: N.A. Q Partial Q Partial risk

Credit

Proposed coverage:Project sponsor.Nature of underlying financing:Terms of financing: N.A.

Principal amount [US$m]Final maturityAmortization profile

Financing available without guarantee: N.A. j Yes C NoIf yes, estimated cost or maturity:Estimated financing cost or maturity with guarantee:

-2-

A. Project Development Objective

(i) Background, Project Development Objectives and Key Performance Indicators

(See Annex I for Performance Indicators)

1. The Project development objective is to attract a critical mass of export-orientedinvestors to Ghana to accelerate export-led growth as well as facilitate trade.

2. After almost fifteen years of sustained economic reform, Ghana's businessenvironment today is one of the best in Africa for private sector development.Benchmark studies commissioned for the Gateway Project (see para. 9 below) confirmedthat Ghana compares favorably to Togo and Kenya (potential competitors) -- and hasadvantages which make it attractive even in relation to Mauritius and Dubai (consideredbest practice). Yet foreign investors in Asia, Europe and the Americas are largelyunaware of the country's business potential -- both as a platform for production for worldmarkets, and more broadly, as a gateway to the West African sub-region.

3. International experience suggests that a well-functioning, privately-developed andmanaged Export Processing Zone (EPZ) can be a powerful way to break through the wallof ignorance of a country's potential -- and "kickstart" a country's visibility in the globalbusiness arena. Ghana already has taken some initial steps towards establishing anEPZ. It has provided the appropriate enabling legal and regulatory environment byenacting the Investment Promotion Center Act of 1994 and the Free Zone Act of 1995(para. 8 below). And it has acquired industrial sites in a high potential business area (inthe environs of the capital, and near to port and other transport facilities) to makeavailable to a private EPZ developer. But three further measures are needed to translatethese promising initial moves into a successful, privately-developed and managed EPZ,which the Gateway Project aims to support.

4. First, the prospects for success will be greatly enhanced if the EPZ is developedand operated by a private operator with the reputation -- and networks -- in theinternational marketplace capable of attracting export-oriented manufacturing tenantsinto (what for them is) a new and uncertain environment. Preliminary indications arethat such an EPZ operator can indeed be attracted into Ghana -- but only if the operatoris provided with a credible assurance that some key off-site infrastructure andinstitutional issues are addressed first (see paras. 11-12). Support by IDA for theGateway Project would provide the requisite assurance.

5. Second, although the private operator would have full responsibility for all on-siteinfrastructure investments, a series of complementary physical investments are neededimmediately off-site -- power, water, waste-treatment and telecommunications hook-ups;and a short road from the EPZ to Ghana's existing transport infrastructure. In theordinary course of events, it could take many years (even with Ghana's recentcommitment to move rapidly towards the private delivery of infrastructure services)before these services would be made available by Ghana's infrastructure providers. TheGateway Project accelerates this process by providing targeted resources to cover thecosts of investment in the off-site infrastructure needed for the success of the EPZ.

- 3 -

6. Third, in order for an EPZ to be a successful platform for attracting export-oriented manufacturing investors, a variety of complementary trade facilitation servicesneed to work effectively (e.g. port and transport, customs and immigration). Wfhileinstitutional reforms are underway in public agencies, it will take many years beforetheir service standards, country-wide, meet international standards. In the interim, toensure that trade facilitation for the EPZ works smoothly, the Ghanaian authorities havedeveloped very precise performance benchmarks which the Gateway Secretariat willrequire from the country's customs, immigration and investment promotion agencies --and have established clear mechanisms for holding these agencies accountable forperformance. Meeting the benchmarks will require substantial efforts on the part of eachof these agencies and thus, the Project will provide the financial support needed tounderpin these efforts.

B. Strategic Context

(i) CAS Objectives Supported by the Project: CAS document number: Report No. 17002-GHDate of latest discussion: August 13, 1997

"Accelerated economic growth for a sustainable attack on poverty"

7. The proposed Project is fully consistent with IDA's Country Assistance Strategy(CAS) for Ghana, which defines poverty reduction as its central goal. The CAS recognizesthat one of the key requirements for sustainable poverty reduction is higher rates ofeconomic growth by restoring sustainable fiscal balance and promoting privateinvestment for exports. Moreover, given a population growth rate of about 3 percent perannum, an average annual GDP growth rate of less than 5 percent during the last decadehas not been sufficient to significantly reduce poverty levels. It is estimated that anannual GDP growth rate of 8-10 percent would be required for significant povertyreduction. In order to achieve the level of investment required to obtain the targetedgrowth rate, Ghana must consciously develop and consolidate its "competitiveadvantages" and cater to export markets. The proposed Project is designed to helpremove the constraints to the development of trade and exports, and to attract directinvestments for industrial and infrastructure development. The Project is an integralpart of the Ghana Gateway Program, designed to make Ghana a middle-income countryby the year-2020, i.e., Ghana's "Vision 2020".

(ii) Main Sector Issues and Government Strategy

8. The enactment of the Ghana Investment Promotion Center Act of 1994 and theFree Zone Act of 1995 were the first crucial actions taken under the strategy. The Actsconstitute an adequate framework, providing favorable investment and export incentivesto enterprises, especially free zone companies, while setting out the rules and regulationsgoverning private sector participation in the development of free zones. The incentivesinclude extensive tax holidays, accelerated depreciation, and sales of up to 30 percent ofthe value of free zone products in the domestic market.

9. The Government has acquired sites in Tema, Takoradi, and Kumasi which havebeen reserved for private development as free zones. To further assess the viability ofthe concept, the Government of Ghana (GOG) commissioned a survey of foreign investors

- 4 -

to compare Ghana's investment climate to those of Mauritius and Dubai (considered bestpractices) and Togo and Kenya (potential competitors). The survey evaluated Ghana'scompetitiveness and positioning as a candidate for increased foreign direct investmentrelative to the comparators in several areas that influence site-location decisions. Theseinclude: political risk, international trade agreements, investment regime, exportpromotion incentives, foreign exchange regime, labor regime, transport, infrastructureand the financial sector. The main finding of the survey was that Ghana has favorableinvestment and export incentives. Its foreign exchange regime is at par with that of thecomparators. Its labor regime is satisfactory, and an available supply of adequatelyskilled and trainable labor represents a major competitive advantage. In general, thetransportation system is at par with that of its comparators and the costs of air and seafreight are competitive. However, Ghana's basic infrastructure, particularly itselectricity, is slightly below that of the comparators. While both telephone and electricityrates are competitive, this advantage is undermined by the quality of the lines andfrequent power outages. Potential investors could be deterred by these deficiencies, asthey not only interrupt production, but also could damage both the machinery and itsoutput. In summary, by drawing upon the experiences of its competitors and the bestpractices in this area, Ghana was shown to have the required environment which,combined with an EPZ to address the infrastructure shortcomings, can enable it toattract a critical mass of exporters and accelerate the growth of exports. In the finalanalysis, it is the quality of infrastructure and business services which will attractinvestors and not the incentive code and thus great attention has been paid to assessingneeded upgrades to infrastructure.

10. A thorough assessment of the infrastructure requirements for the EPZ and ademand forecast for space in the Tema zone suggests that in the base-case, over fortythousand square meters of under-roof space will be required over the first four years ofoperation primarily from industries (e.g. agro-processing, wood processing, textiles,garments, horticulture, fish processing, apparel manufacturing, etc.) and services (e.g.teleport and tourism).

(iii) Sector Issues to be Addressed by the Project and StrategicChoices

11. The Project will address two critical constraints to the increased inflows of foreigndirect investment for the acceleration of exports: (a) the provision of limited off-siteinfrastructure around the Tema EPZ, to attract a private developer who would providepotential investors with required on-site infrastructure in the Tema EPZ; and (b) theremoval of important, but narrow, institutional capacity constraints to increased foreigninvestment.

12. The GOG recognizes that, over the medium-term, the success of institutionaldevelopment or efficiency improvements at the level of individual agencies or enterprisesis predicated by a well-functioning public administration/civil service system. Hence, itscommitment, under the National Institutional Renewal Program (NIRP), is to tacklepublic sector efficiency issues. A key feature of public sector reform is the importance ofensuring that the agencies and enterprises are held accountable for service delivery. ThisProject deviates from traditional technical assistance projects in that it establishesaccountability relationships between the service delivery agencies (who are beneficiaries

- 5 -

under the Project) and the policy making/executive bodies, with feedback provided on aregular basis from recipients of the services.

Provision of Off-site Infrastructure for the Tema EPZ

13. The investment component of the Project will facilitate the development of aprivately-financed and owned EPZ with physical on-site infrastructure of internationalstandards. To achieve this, GOG has allotted 1,200 acres of land near Tema fordevelopment as the first EPZ in Ghana. The goal of this Project is to lease a first lot ofthis land to a suitable private investor/developer using a combination of internationalcompetitive bidding and direct marketing. The GOG has developed a two-prongedstrategy for identifying and securing a qualified developer to begin development of thearea. Although the GOG has already identified a potential developer, until that deal isconfirmed, it intends to aggressively market free zone development opportunities to otherqualified developers. This approach underscores the need by the GOG to secure itselfagainst withdrawals of proposals by current prospects.

14. Under this component, the Project will finance: (a) a well-targeted internationalmarketing plan for attracting experienced developers/investors of international repute todevelop and manage the Tema EPZ; and (b) off-site infrastructure links with theproposed EPZ including: (i) water connection; (ii) sewage and solid waste treatment forthe EPZ; (iii) electricity link; (iv) access roads to the site; and (v) an environmentalassessment and mitigation plan. The off-site communication links to the EPZ will be builtand operated by one of the local private telephone companies on the basis of termsdefined under their licensing agreement. For the railways link between the EPZ and theTema Port, the Project will finance a detailed feasibility and economic analysis todetermine the viability of such an investment. An OECF study (February 1998)identified a number of bottlenecks in the existing port operations and some of theseactivities are being addressed by the Ghana Ports and Harbor Authority (GPHA). Theproposed Project will complement these internal efforts of GPHA with support for minor,but high impact, physical improvements which will enhance operations such as breakbulk and cargo handling. Support will also be provided to relocate the devanning areaoutside of the port area.

15. GOG and IDA agreed during negotiations to prepare a Memorandum ofUnderstanding defining performance indicators to ensure that infrastructure providedunder the Project is efficiently managed and operated after it is handed over to theutilities. The GOG and IDA have also agreed that the disbursement of the first tranchefor off-site development will be contingent upon the effectiveness of the lease agreementbetween the developer and the Ghana Free Zone Board (GFZB). At such time, tender forpre-qualification and contractual arrangements for civil work design will commence.GOG and IDA have agreed in a side letter to a time-bound process for finding a suitabledeveloper.

Trade Facilitation

16. The reform of customs and port administrative processes is essential to Ghana'sobjective of becoming an important trade and investment center. The Project will defineand implement reforms in quality control and the methods, processes and proceduresused by Customs Service, Ports and Harbors, Civil Aviation and Immigration in their

-6

dealings with investors, exporters and others, eg., tourists. The Project would aim tolower the cost of doing business in Ghana, inter alia, by reducing the time between cargoarrival and release to levels reflecting "world class best practice" and by reducing, to"lowest world class" levels, the user costs associated with processing documentation andcomplying with mandated procedures. Isolated processes within separate governmentagencies would be connected with processes carried out by commercial users of thesystem, in order to create additional transparency in rules and regulations, improveinformation flows and coordinate document processing. Ghanaian customs and portsprocessing standards would conform to those issued by the International Chamber ofCommerce and the International Standards Organization (ISO) and would comply withISO 9000. The achievement of the kind of "breakthrough service improvements" impliedby ISO 9000 certification should serve as further indication to multinationalcorporations of Ghana's serious and effective commitment to make its country investorand commercial trader "friendly." The proposed Project will help tackle (part of) thisagenda with specific and targeted interventions in the following front line agencies.

17. Ghana Free Zones Board (GFZB): Attracting a developer capable of bringinganchor-tenants, who will constitute the critical mass of export-oriented firms, is key tothe success of the Gateway Project. This is the raison d'etre of the GFZB. Hence, it isessential for it to have a focused strategy to clearly define activities which will propel itinto a proactive implementing organ for the Ghana Free Zones Program. GFZB'sstrategy is to implement a well-targeted marketing plan for attracting free zonedevelopers and enterprises as detailed in the recently completed FDI Demand Study.This marketing plan will be complemented by: (a) the design of information systemswhich will provide the GFZB with the appropriate technological support to undertake allaspects of promotion and facilitation (e.g. investor tracking and investor/enterprisesmanagement functions); and (b) a comprehensive capacity building program aiimed atimproving service delivery within GFZB staff, both in terms of proactive promotion aswell as investor hospitality and related facilitation functions.

18. Targeted Investment Promotion (GIPC): The improvement in Ghana's investmentclimate increases the challenge for the Ghana Investment Promotion Center (GIPC) toensure a demonstrable improvement in investment performance, while offering itsservices efficiently with value for money. The proposed Project will: (a) support thedevelopment and implementation of a 2nd Five-Year Corporate Plan to enhance GIPC'sability to undertake aggressive and targeted investment promotion; (b) enable it to trainstaff to enhance the institution's strategic perspective in areas such as informationgathering, environmental scanning and industry analysis; and (c) create an enhancedtracking system to measure the efficiency of incentives offered, as well as the results ofspecific investment promotion activities.

19. Simplification of Immigration Procedures for Investors: The absence of writtenprocedures impedes the ability of the Ghana Immigration Service (GIS) to respond pro-actively to new initiatives such as the Gateway Project. The GIS intends to implementmeasures to improve the quality of its services, including the reduction of formalities andprocedures and creating a fast track lane for investors at major ports of entry, and thegranting of a temporary visa of 30 days to all foreign visitors upon arrival. Theorganizational audit carried out in April 1998, noted also that GIS is committed tocarrying out its mandate, but is hampered by a lack of resources, a strategic vision and aformal training program. While a comprehensive overhaul of GIS is beyond the scope of

-7-

this Project, the Project will support: (a) selective re-training of staff to help create aculture of facilitation and service provision, and to help immigration officers project anappealing image to visitors; and (b) process and technology improvements. The revisedorganizational structure of GIS would include internal and external mechanisms toprovide feedback on GIS performance. These mechanisms would include private sectorparticipation and would be consistent with the GOG's trade and investment promotionobjective.

20. Ghana Ports and Harbor Authority (GPHA): Under the Gateway Project, theoperations of the ports will be improved by reducing the cost of operations and shorteningthe turn-around time for ships and clearance time for cargo. Increased private sectorparticipation in the management and operation of the ports is the strategic choice madeby the GOG to achieve these objectives. Under the proposed Project, GPHA will beconverted into a Landlord Port Authority, while the operations will be outsourced to theprivate sector, i.e., container operations, dockyards, sites maintenance and services, etc.,before the year-2000.

21. Customs Excise and Preventive Services (CEPS): Customs does not currently havethe tools, methodology or corporate culture to be an effective institution for deliveringcustoms services in a manner which is consistent with the Gateway objectives. Inparticular, importers and exporters, as well as potential investors, have identified that:(a) the current regulations are too complex to comply with; (b) valuation procedures arenot consistent with international norms; (c) trade is impeded by long delays in entriesand exits being presented to customs and high error rates on import entries; and (d) theperception of CEPS as a para-military organization hinders its ability as a tradefacilitator. There is an implicit high cost imposed on Ghana's industry due to theseprocedures, in terms of foregone employment and export earnings. These issues wereconfirmed and are presented in detail in the CEPS Organizational and InstitutionalAudit (March 1998) and Trade Facilitations and Effective Customs Control Report(March 1998). Under the proposed Project, CEPS will re-engineer customs clearanceprocesses to: (i) develop cargo clearance procedures and customs/shipper informationinterfaces which are simple, which minimize redundant data entry and which complywith international best practice; and (ii) simplify customs' tariffs and valuationprocedures and reduce the number of commodity descriptions and detailed scheduleapplications. This will reduce the need for refined determinations of cargo value and willminimize, correspondingly, the interpretive latitude left to customs officials.

22. Ghana Civil Aviation Authority (GCAA): Aviation plays a key role in supporting ahigh-growth, outwardly-oriented development strategy. The primary objective is todevelop a strategic framework for the development of Ghana's Civil Aviation Sectorwhich is supportive of the goals of the Gateway Project. This includes the development ofGhana's economy into a major regional hub for the physical distribution of goods and thecollateral development of gateway services including transport, transshipment, financial,insurance, third party logistics, information and other services related to regionaldistribution, transshipment and transit. GOG has already enacted a policy of "liberalizedskies" which implies, inter alia, an institutional reform of the GCAA. The reformedGCAA should have full charge of safety regulations; pilot, carrier and facility licensing;and air navigation and air traffic control. Airport operations and development should beunder the control of an independent airport authority. Under the proposed Project and intandem with the Public Enterprise and Privatization Technical Assistance Project

- 8 -

(PEPTA), the GOG will prepare and implement a coherent, comprehensive andintegrated strategy for the Civil Aviation Sector, which can serve as a guide and roadmap for all subsequent reforms, initiatives and privatization activities. This roadmapwould be adopted by end- 1999.

C. Project Description Summary

(i) Project Components (see Annexes II and III for detaileddescription and cost breakdowns)

1.0 Infrastructure Investments

11 Off-site Infrastructure Investment for *Civilworks 33.40 59.66 29.98 59.37the Tema EPZ, including: * Goods

* Services. Access road, side drainage and 6.08 - 10.86 5.79 11.47

associated civil works.* Water supply systems, wastewater 19.86 35.46 18.93 37.49

disposable systems and off-sitedrainage systems.

* Supply and installation of 2.36 4.21 2.26 4.48electricalpower and transformers.

a Telecom Infrastructure (local 2.10 3.75 0 0private)

* Feasibility studyfor railway 1.50 2.68 1.50. 2.97corridor

* Contracting to Oversee Civil 1.50 2.68 1.50 2.97works

1.2 Construction of Container devanning *Civil works 3.50 6.25 3.15 6.24area outside of the port, and * Goodsimprovement of port container and * Servicesairport cargo facilities

1.3 Implementation of the Environmental *Institutional building 2.00 3.57 1.80 3.56Management Plan (EMP) and support *Equipmentto the EPA.

Total Investment Component 38.90 69.46 34.93 69.17

Category Indicative % of , DA 11 % fCompoenet Cost Tot F Totaol

2.0 Investment promotion and Removalof administrative bottlenecks

2.1 CEPS: The Project would finance the *Institutional building, 2.25 4.02 1.92 3.80implementation of CEPS strategic * Physical/Equipment,business plan covering changes in * Behavioral change/operational procedures and human communicationresources and ISO 9000 compliance.

2.2 GPHA: Expertise, equipment, *Regulation, 1.75 3.13 1.72 3.41training, operational support to re- + Institutional buildingengineer GPHA into a Landlord + TransactionAuthority. Feasibility study for *Equipmentextension and dredging of quay 2,development of Electronic DataInterchange (EDI) at Tema port.Private Sector Participation in portactivities

2.3 GCAA: The Project would finance Regulation, 1.00 1.79 .96 1.90the conversion of GCAA into a +Institutional buildingregulatory agency and the * Transactionoperationalization of the "liberalizedskies policy" with emphasis on policyreform and institutional redesign,increased private participation inprovision of infrastructure andobtaining private participation inmanagement and development ofKIA.

2.4 GIS: The Project would finance (i) *Institutional building 1.18 2.11 1.00 1.98assistance in preparing operating * Physical/Equipmentprocedures, benchmarking GIS *Behavioral changeprocessing of immigration functionsas they relate to trade facilitation; (ii)technology infrastructure and ; (iii)retraining of staff in trade facilitation.

- 10 -

2.5 GIPC. Country and Investment *Investment 2.75 4.91 2.34 4.63 lPromotion: Preparation and promotionlimplementation of well targeted *Capacity buildinginvestment and country promotion *Increase awarenessactivities; staff training and private * Stakeholderssector surveys; preparation and involvementimplementation of a strategy to developbackward linkages between foreigninvestors and local suppliers; and supportfor a program to build consensus amongstdomestic stakeholders in favor ofreforms.

2.6 GFZB: The Project will finance * Marketing 2.40 4.29 2.32 4.59implementation of the Developer & * InstitutionalTenants marketing plans, improvement of buildingservice delivery of staff in promotion andfacilitation, development of oversightcapabilities.

2.7 Gateway Project Coordination and *Program & Project 2.87 5.13 2.56 5.07Project Management: The Project would Managementhelp finance recurrent expenditures anddevelop the institutional capacity tomanage and coordinate the GatewayProject and infrastructure unit.

2.8 Setting the Stage for Gateway II The * Policy 0.50 .89 .50 .99Project would support work aimed at * Institutionaldeveloping further policies, instruments buildingand implementation strategies forexample in project finance; vocationskills development, and tourismdevelopment.

Total: Capacity Building in Trade 14.70 26.25 13.37 26.38Facilitation Components

PPF-Telecom 2.00 3.57 2.00 3.96Unallocated .40 .71 .25 .50

Total Project Costs 56.00 100% 50.50 100%

- 11 -

(ii) Key Policy and Institutional Reforms Supported by the Project

23. The Project will address some important but narrow institutional capacityconstraints of front line agencies which deal with investors and exporters. Instruments tofacilitate increased private sector participation such as project finance, franchising andconcessions, will also be supported. The approach used in the Technical Assistance (TA)component departs from traditional technical assistance projects in that it establishesaccountability relationships between the service-delivering agency (which arebeneficiaries under the Project) and the policy making/executive bodies, who will usefeed-back from recipients to assess compliance.

(iii) Benefits and Target Population

24. In keeping with Ghana's objective of sustainable poverty reduction through jobcreation and increased levels of economic growth, the Gateway Project is designed tofacilitate the higher levels of private foreign and domestic investment necessary toachieve this growth. The Project would benefit three broad target groups: (a) the localpopulation; (b) private investors; and (c) the GOG. For the local population, the Projectwill lead to a reduction in unemployment through the creation of more job opportunitiesand through improvements in the skills and mobility within the labor force. For theGOG, the Project is expected to attract a flow of foreign direct investment that will havea positive effect on the balance of payments. It will also help increase the capacity ofgovernment agencies dealing with the private sector. In addition, the fiscal impact hasbeen estimated at US$ 75 million for the 15-year period, mostly from personal incometaxes of new employees and service businesses operating around the EPZ and estimatedleasing fees from the developer of the EPZ. For private foreign and domestic investors,benefits will come from reduced uncertainties and transaction costs associated with doingbusiness in Ghana, as well as the availability of ready sites for export processingindustries and the simplification of trade procedures.

(iv) Institutional and Implementation Arrangements

Implementation period : Seven years, 1999 to 2005Executing Agencies : Individual beneficiariesProject Coordination : Oversight Committee/Gateway Secretariat

Institutional Arrangements

25. In view of the multi-sectoral implications of this program, the Cabinet of GOG hasformed an inter-ministerial Oversight Committee to coordinate the design andimplementation of the Gateway Project and inter-agency policy issues. The OversightCommittee is supported by a Secretariat which will act as a Project Implementation Unit(PIU) to monitor and coordinate all reporting for the institutional developmentcomponents, as well as the on-site and off-site infrastructure component, while eachbeneficiary will be fully responsible for implementing the components within theframework of the Gateway Project. The Gateway Secretariat will be established andfinanced under the purview of the Oversight Committee. The Secretariat will be staffedwith a project coordinator, an accountant, procurement specialist and office support staff.

- 12 -

26. While each implementing agency would have primary responsibility for theimplementation of its own components, the Secretariat will be the vehicle forcoordination, monitoring, contact, follow-up and reporting between IDA, theimplementing agencies and the Oversight Committee. A performance contract will besigned between the Oversight Committee and each beneficiary agency which will be heldaccountable for the delivery of project outputs. This performance contract will includemeasurable indicators and the means of verification as defined in the Project's LogicalFramework. The signing of these contracts will be a prior action for credit effectiveness.

27. During negotiations GOG agreed to include a private sector representative on theOversight Committee. In view of the amount of infrastructure work under the Project,an Infrastructure Coordinator will also be appointed to the Gateway Secretariat withresponsibility for the implementation of the off-site development and infrastructurereforms.

28. The Environmental Mitigation Plan, and the Monitoring and Risk contingencyplans must be translated into a concrete environmental action-oriented instrument (i.e.Environmental Management Plan (EMP)) and its implementation would coincide withthe Project's start. The EMP shall be updated every two years and quarterlyenvironmental reports on the implementation of the EMP and other enhancementmeasures will be prepared for the Oversight Committee and IDA.

29. The GOG would open and maintain a Project Account in Ghanaian Cedi in acommercial bank on terms and conditions satisfactory to IDA. It will make an initialdeposit into the account in an amount equivalent to US$1 million to finance itscontribution to the Project. Furthermore, it will deposit into the Project Account by April15 of each year, until the completion of the Project, any amounts which will be requiredto timely replenish the Project Account back to the amount of the initial deposit.

30. The Gateway Secretariat would require accounting and financial managementservices to oversee the Project's financial aspects, which would be provided by anindependent accounting firm or qualified individual. All Project accounts, the SpecialAccount, the Statement of Expenditures (SOE) and the financial statements of theProject beneficiaries would be audited at the end of each fiscal year by an independentauditor acceptable to IDA. In view of the complex and varied procurement content of theProject, the PIU will employ a full time procurement specialist, who would providesupport to implementing agencies in carrying out their responsibility for procurementrelated to their components. The procurement specialist and each implementing agencywould update procurement schedules and provide reports on related activities to ensurecompliance with IDA requirements. Agreement has been reached with the borrower onthe standard processing procedures for procurement of civil works, goods and consultantsservices.

31. Semi-annual Project reviews would be conducted jointly by IDA and GOG, witheach implementing agency to review the implementation of all components, including thestatus of procurement and disbursement. A joint IDA-GOG mid-term review wouldmonitor the overall Project execution, key project activities, project implementationschedule, and supervision plans. They will also identify implementation issues anddevelop solutions. Following Project completion, scheduled for December 2005, anImplementation Completion Report (ICR) would be prepared jointly by IDA and GOG.

- 13 -

Consultants, contractors and suppliers would be selected in accordance with Bankguidelines, on the basis of proven experience. In line with the Bank's Africa Regionalguidelines, wherever possible, local consultants will be used. Where foreign consultantsare used for lack of requisite local skills, special efforts will be made to promote andstrengthen local capacity through the transfer of skills to the domestic industry usinglocal counterpart teams. Consultant and advisor contracts would include provisions fortraining and transfer of skills to local counterparts to carry-on with the programindependently. Each beneficiary would, therefore, appoint counterparts who would workclosely with the advisor and would also make adequate preparations before the arrival ofthe advisor in order to ensure the effective utilization of his/her services.

Accounting, Financial Reporting and Auditing Arrangements

32. A local private accounting firm (or individual accountant), acceptable to IDA, willbe responsible for project financial management using an accounting system andfinancial management satisfactory to IDA (an accounting/financial management manualwill be produced which will include the organizational structure, chart of accounts andaccounting and financial procedures which will be followed throughout the duration ofthe Project).

33. The signature of a two-year audit contract with a qualified audit firm acceptableto IDA will be a condition of credit effectiveness. During negotiation, agreement wasreached on the following points:

* the Project's accounts and supporting documents will be audited by anindependent auditor accepted by IDA, pursuant to international audit principles;

* to provide IDA with an audit report for the fiscal year in question, certified by theauditor, no later than six months after the end of each fiscal year;

- to provide IDA with any other information regarding the Project's accounts andaudit it may request from time to time; and

* the accounting records of the Special Account, the Project Account and the SOEswill be audited : (i) every month during the first eighteen months counting fromthe effective date; and (ii) every six months during the remaining periods, andthese audits will be sent to IDA no later than two months following the end of theaudited period.

Monitoring and Evaluation Arrangements

34. Semi-annual progress reports, prepared on the basis of the Projectimplementation plan and the logical framework would be provided by the beneficiaries toIDA through the Gateway Secretariat. IDA will carry-out regular supervision missionsand a mid-term review. Finally, The GOG will transmit a completion report to IDAwithin six (6) months of the Project closing date.

35. In order to ensure continuous monitoring of project impacts (which are long-termin nature), it is proposed that funding should be made available to the executing agencyof the EMP, through the provision of a clause in the leasing agreement stating thecommitment to allocate a specific amount of resources to the EPA.

- 14 -

D. Project Rationale

(i) Project Alternatives Considered and Reasons for Rejection

(a) Single operation covering priority aspects (Front line agencies and Off-siteinfrastructure) of the Gateway Project : It has been decided to process these twocomponents as one project despite the fact that implementation of the off-site investmentcomponent will be contingent upon the GOG finding a private investor/manager tofinance the on-site investment in the EPZ. This way of structuring the Project providesfor the need to send a positive signal to maximize leveraging of private investment andmeets the pre-requisite of the private developer while ensuring that public investmentsare not made. IDA and GOG have nonetheless agreed on an exit clause, should adeveloper not be found within a specific time-frame.

(b) Include various components under different ongoing technical assistance(TA) projects: Another alternative was to include different aspects of the TAcomponent in various on-going projects. However, this was eliminated because it wouldhave significantly increased the complexity of the on-going projects and adverselyaffected their implementation.

(c) Government-financed Export Processing Zone: Another option was to assistGOG in financing and developing the EPZ with IDA or other donor resources. Thisoption was rejected due to the failure of numerous Government-financed EPZselsewhere in Africa. We have not rejected the possibility of credit-enhancementinstruments (such as using, for example, the partial risk IDA guarantees instrument ifit is made available at some point) to strengthen the Project finance structure ifconsidered necessary.

(d) Free-standing large infrastructure project : This option was rejected becauselarge on-site infrastructure investments are expected to and should come from theprivate sector and Government involvement in the provision of on-site infrastructure wasnot considered a necessary part of the Project.

- 15 -

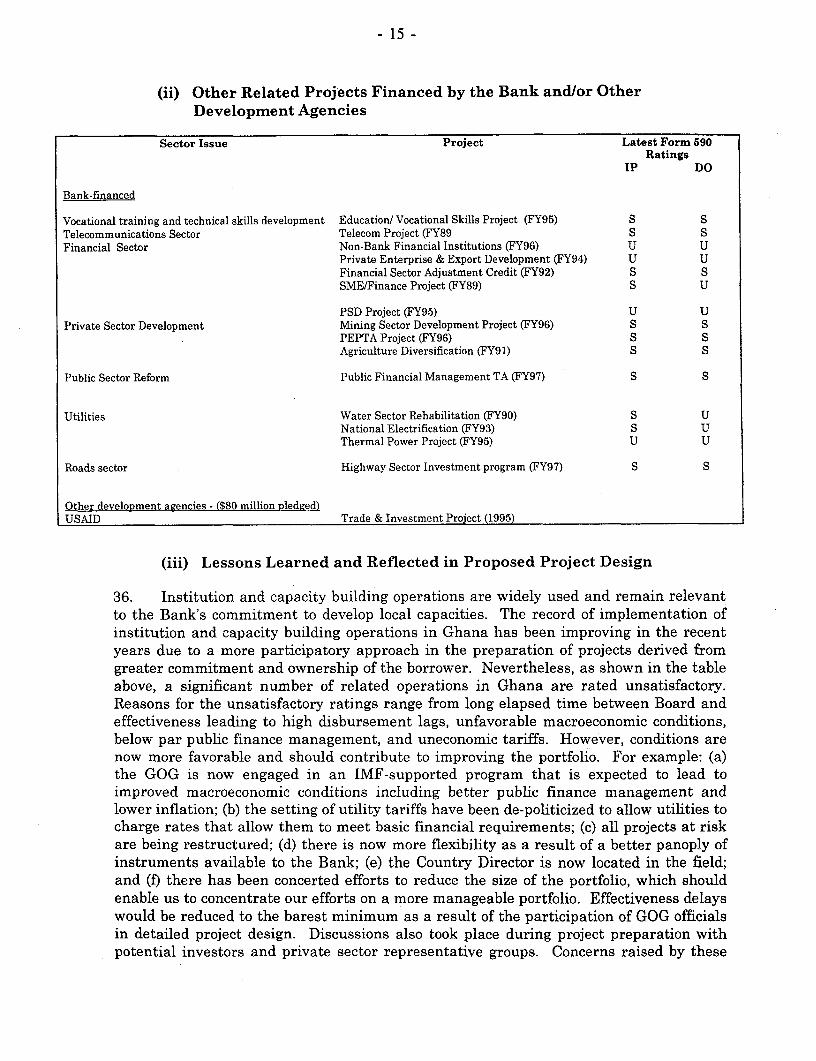

(ii) Other Related Projects Financed by the Bank andl/or OtherDevelopment Agencies

Sector Issue Project Latest Form 590Ratings

IP DO

Bank-financed

Vocational training and technical skills development Education/ Vocational Skills Project (FY95) S STelecommunications Sector Telecom Project (FY89 S SFinancial Sector Non-Bank Financial Institutions (FY96) U U

Private Enterprise & Export Development (FY94) U UFinancial Sector Adjustment Credit (FY92) S SSME/Finance Project (FY89) S U

PSD Project (FY95) U UPrivate Sector Development Mining Sector Development Project (FY96) S S

PEPTA Project (FY96) S SAgriculture Diversification (FY91) S S

Public Sector Reform Public Financial Management TA (FY97) S S

UJtilities Water Sector Rehabilitation (FY90) S UNational Electrification (FY93) S UThermal Power Project (FY95) U U

Roads sector Highway Sector Investment program (FY97) S S

Other development agencies - ($80 million pledged)USAID Trade & Investment Project (1995)

(iii) Lessons Learned and Reflected in Proposed Project Design

36. Institution and capacity building operations are widely used and remain relevantto the Bank's commitment to develop local capacities. The record of implementation ofinstitution and capacity building operations in Ghana has been improving in the recentyears due to a more participatory approach in the preparation of projects derived fromgreater commitment and ownership of the borrower. Nevertheless, as shown in the tableabove, a significant number of related operations in Ghana are rated unsatisfactory.Reasons for the unsatisfactory ratings range from long elapsed time between Board andeffectiveness leading to high disbursement lags, unfavorable macroeconomic conditions,below par public finance management, and uneconomic tariffs. However, conditions arenow more favorable and should contribute to improving the portfolio. For example: (a)the GOG is now engaged in an IMF-supported program that is expected to lead toimproved macroeconomic conditions including better public finance management andlower inflation; (b) the setting of utility tariffs have been de-politicized to allow utilities tocharge rates that allow them to meet basic financial requirements; (c) all projects at riskare being restructured; (d) there is now more flexibility as a result of a better panoply ofinstruments available to the Bank; (e) the Country Director is now located in the field;and (f) there has been concerted efforts to reduce the size of the portfolio, which shouldenable us to concentrate our efforts on a more manageable portfolio. Effectiveness delayswould be reduced to the barest minimum as a result of the participation of GOG officialsin detailed project design. Discussions also took place during project preparation withpotential investors and private sector representative groups. Concerns raised by these

- 16 -

groups have been addressed in the design of the Project. During implementation,periodic assessments would be made of the impact of the program on all stakeholdergroups, and remedial action would be taken to mitigate negative effects. However, thereare still issues that need continued focus and strengthening, including: (i) development ofthe borrower's capacity to implement and manage the TA components, including closersupervision efforts by the GOG; (ii) consultants' abilities to transfer skills to localcounterparts; (iii) development of local consultant capacity; (iv) counterpart staffing; and(v) greater attention to monitoring indicators.

37. The Gateway Project incorporates recommendations from Economic Sector Work(ESW), completed on the sector (3 FIAS reports, MIGA reports), reports prepared byother donors (USAID, CIDA) and most importantly the work done by GIPC and GFZB.The preparation of the Project has been participatory. The GOG initiated a self-assessment of needs by all key agencies contributing to the high cost of doing business inGhana which resulted in an action plan for each agency in coordination with the Ministryof Finance and the Gateway Secretariat. These action plans also identify monitorableperformance indicators. To develop the borrower's implementation capacity, supportwould be provided to the PIU, GFZB and other agencies.

38. The experience with Export Processing Zones (EPZs)/Free Trade Zones (FTZs) inAfrica, while mixed, was also carefully reviewed. Numerous Government financed EPZs,in countries like Senegal, Liberia, Zaire, Botswana and Cameroon, failed due to problemssuch as political instability and an unsafe business environment, cumbersome regulatoryprocedures and inefficient institutional structures, high cost of doing business especiallydue to poor infrastructure, labor market rigidities, high minimum requirements forinvestment, employment or infrastructure services (electricity, etc.), or poor siteselection. However, there are a few African EPZIFPZ success stories and a number oflessons emerge from their experiences, as well as experiences elsewhere in the world.The more notable ones are: (a) private sector EPZ development and management must beencouraged; (b) if industrial estates are to remain in Government hands, it is essentialthat they be operated on a commercial basis (leases set out at commercial rates,managers paid competitive salaries, sound accounting practices, etc.); (c) private sectorprovision of infrastructure services should be encouraged; (d) true public/private sectorcooperation should be developed and regulatory processes should be streamlined; and (e)programs should have more competitive incentive packages without crippling provisionssuch as minimum investment requirements, etc.

39. Bank projects have confirmed the difficulty in identifying, agreeing andimplementing project components which cut horizontally across multiple, "stove pipe"government agencies and across the "exclusive territorial" domains of specific functionalagencies. The experience requires not only a strong initial commitment from top levelgovernment decision makers but also the creation of a transitional platform -- e.g.,special committee, task force, etc. -- which is empowered to maintain continuous pressurefor fundamental change and, importantly, which is also empowered to resolve inter-jurisdictional issues. With this caveat, experience also confirms that the benefitsresulting from supply chain development projects -- projects which typically transcendtraditional organizational boundaries and which actively engage the private sector, i.e.beneficial owners of cargoes, shippers and consignees-- are very great. This can lead to achain reaction of continuous process improvement in the delivery of logistics serviceswhich improve the competitiveness of manufacturers, distributors, exporters and

- 17 -

importers with resulting trickle down benefits for the entire economy. Supply chaindevelopment is a relatively new thematic focus within the Bank but offers the mosteffective way to lower transaction costs, bring buyers and sellers closer together in timeand cost and provide competitive access for emerging economies to the global marketplace.

40. The Ghana Free Zones Act clearly recognizes the importance of most of the lessonslearned. It lays out an attractive incentive package for private investors in the free zone.The proposed EPZ at Tema will also be entirely privately-financed, owned and managed,which will be one of the first in Africa. GOG plans to lease the land to private investorsfor a period of 50 years. In terms of provision of infrastructure services to the EPZ site,except the telecom sector which has been fully liberalized, GOG will have theresponsibility of providing off-site infrastructure services due to lack of private sectorproviders. GOG currently requires additional support on investment promotion andfacilitation activities. The institution and capacity building component is addressing thisneed at GIPC and at GFZB.

41. In order to ensure the efficient implementation of the EMP, the GOG is fullycommitted to provide and transfer the component cost to the plan's executing agency, theEPA. The GOG is also committed to the creation of the Gateway EnvironmentalManagement Unit and to ensure that the requisite human and institutional capacities areput in place. Strengthening the capacity building component prior to projectimplementation is a means of assuring the efficient and effective management of theenvironmental management plan.

(iv) Indications of Borrower Conmuitment and Ownership

42. GOG has expressed strong commitment to the Gateway Project by creating theGateway Oversight Committee, which is chaired by the Vice President of Ghana, and theGateway Secretariat at an early stage of the Project. GOG' s commitment to improve thebusiness environment in Ghana is also evident from the passing of the Free Zones Law(1995), as well as the Ghana Investment Promotion Center Act (1994). It has undertakenmeasures to liberalize banking laws, divest companies, including those in the mining,banking, insurance and telecommunications sectors, to maintain stringentmacroeconomic management. The Bank's challenge would be to build on the positivesteps being taken in Ghana to realize the objectives of the Gateway Project.

(v) Value Added of Bank Support: Rationale for Bank-GroupInvolvement

43. The Bank, IFC (including FIAS) and MIGA have been evaluating variousalternatives for the GOG to improve the business environment in Ghana. The GatewayProject provides the Bank Group the opportunity to adopt an integrated approach toPrivate Sector Development (PSD), involving adjustment lending (to influence policyreforms and political-will issues), technical assistance initiatives for the associated needsfor institution and capacity building, and investment lending to leverage strategic privatesector financing. Since the scope for larger amounts of external assistance is limited,Ghana will need to attract considerable new inflows of foreign private investment togenerate a stronger supply response to macroeconomic reforms. In support of this

- 18 -

strategy, the Gateway Project seeks to remove state involvement and intervention inareas of economic activity that can be handled more efficiently by the private sector. TheBank Group, through the wide range of lending and investment instruments available toit, is ideally suited to assist the GOG with the implementation of the strategy.

44. IFC and MIGA have been closely associated with the appraisal of this Project. IFChas been approached by the GOG and by one of the potential developers, and hasindicated its readiness to participate in the on-site infrastructure development in theform of equity and investment. MIGA has also been involved in project preparation andis willing to provide guarantees at the request of the developer. Moreover, duringappraisal, the IDA Guarantee staff made a presentation of their facilities and the GOGwill call on them as and when needed. These potential contributions relate to the on-siteinfrastructure component, rather than to the components of the proposed credit.

E. Summary Project Analyses

(i) Economic Assessment

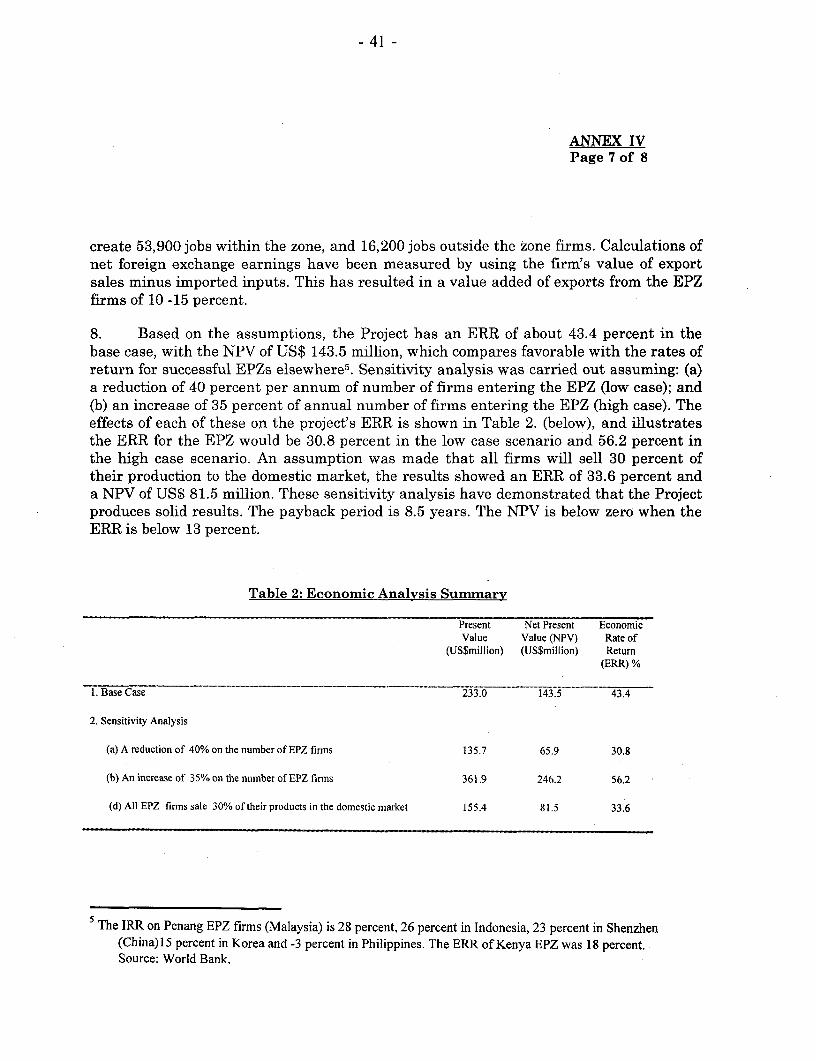

45. The results of the economic analysis (Annex IV) shows that the overall project canbe strongly justified in NPV and ERR terms. The cash flow was developed for the wholeproject and not per component. This was mainly because it is difficult to quantify theindirect benefits deriving from the capacity building component. The project has an ERRof about 43.4 percent in the base case, with the NPV of US$143.5 million, whichcompares favorable with the rates of return for successful EPZs elsewhere'. Sensitivityanalysis was carried out assuming: (a) a reduction of 40 percent per annum of number offirms entering the EPZ (low case); and (b) an increase of 35 percent of annual number offirms entering the EPZ (high case). The effects of each of these on the project's ERR isshown in Table 2 of the Annex IV, and illustrates that the ERR for the EPZ would be 30.8percent in the low case scenario and 56.2 percent in the high case scenario. Anassumption was made that all firms will sell 30 percent of their production to thedomestic market, the results showed an ERR of 33.6 percent and an NPV of US$ 81.5million.

46. The development of the EPZ is projected to create 53,900 jobs within the zone, and16,200 jobs outside the zone firms. Calculations of net foreign exchange earnings havebeen measured by using the firm's value of export sales minus imported inputs. This hasresulted in a value added of exports from the EPZ firms of 10 -15 percent.

(ii) Financial Assessment

47. Private participation in the on-site financing is a prerequisite for IDAparticipation in financing the off-site infrastructure. The lease rental paid by the investorcould be used to finance the GOG share of the off-site investment, thus reducing thefinancial impact of the Project on the GOG budget. In addition, investment in off-sitefacilities would generate direct user charges from water, power, telecommunications,sewage treatment etc. which would provide a return on the investment. The lease rental

lThe [RR on Penang EPZ firms (Malaysia) is 28%, 26% in Indonesia, 23% in Shenzhen (China)15% inKorea and -3% in the Philippines. The ERR of the Kenya EPZ was 18%. Source: World Bank.

- 19 -

to be paid by the investor/developer to GFZB would be decided during the internationalprocurement process. On the TA side, customs tariffs and port charges need to berationalized to make the ports competitive and the customs procedures more transparentand simpler.

(iii) Technical Assessment

48. In the TA component, the specific forms of assistance to each beneficiary havebeen defined based on an operational and organization diagnostic carried out for eachagency to clearly articulate its mission in terms of dealing with foreign investors, theconstraints it faces and the action plan being recommended to address those constraints.More importantly, each beneficiary agency would clearly define an oversight mechanismwhich is independent from public sector intervention and which will monitor the qualityof service delivered.

49. For the off-site infrastructure component, a feasibility study carried out duringproject preparation provided the technical and engineering specifications as well as areasonable cost estimate. Detailed technical and engineering specifications for the off-siteinfrastructure will be defined in collaboration with the private developer of the ExportProcessing Zone during project implementation.

(iv) Institutional Assessment

50. The Project is being developed by the agencies in a very participatory mannerwith all stakeholders. Each agency, therefore, is expected to have strong ownership forits component. To ensure that lack of project management capacities does not hamperimplementation, the Project will address institutional shortcomings through adecentralized and contractual implementation arrangement and extensive institutionaland capacity building support for the beneficiaries and coordinating agencies.

(v) Social Assessment

51. There are no maior social issues faced by this Project. The Gateway Project willinstead strengthen community development in the Tema municipality through thecreation of new job opportunities as well as development of the infrastructure which willbenefit the entire population in the Tema area. The cash wages to be paid to temporarylabor during construction, and the cash generated by the free zone during operations, willalso have significant social impact in the surrounding communities. At the same time,the improvement of the social infrastructure (improved drainage, and improved solidwaste management) will improve the quality of life of the communities and reduce theincidence of water related diseases. The compensation issues outlined in theEnvironmental Impact Assessment (EIA) study will be adequately addressed and thoseherdsmen losing their grazing areas, as well as the vegetable gardeners, will be properlycompensated. There is no involuntary resettlement issue in the area except for someillegal squatters in an old Ghana Broadcasting Corporation Building. This matter hasbeen highlighted in the EIA study and will be addressed by the Gateway Authorities.

- 20 -

(vi) Environmental Assessment

52. The Ghana Gateway Project is classified as Category A due to the fact that itcomprises both off-site and on-site infrastructure development that include: (a) waterconnection; (b) sewage and solid waste treatment for the EPZ; (c) electricity link; (d)telecommunication link; and (e) access roads to the Project site. According to theenvironmental study carried out by a team of consultants, and reviewed by theEnvironment Group of the Africa Region, there are no major negative environmentalproblems. The anticipated environmental problems from construction works (dust, noisefrom heavy machinery) and other problems expected during project operation, wereadequately addressed in the study. Project preparation, bidding and implementationtherefore incorporate specific measures to avoid negative impacts, and to improvecurrently inadequate environmental conditions in the Project area such as: (i)environmentally safe construction methods and techniques; (ii) environmental and socialcriteria to avoid environmental degradation of the Project site; and (iii) improvement ofsolid waste management in the final waste disposal sites in the Tema municipality. TheEIA includes costed mitigation and monitoring plans and an industrial risk contingencyplan, all of which clearly identify the institutional arrangements for the execution of therespective plans.

(vii) Participatory Approach

53. The Gateway Project has been prepared in a participatory manner, in that varioussectors of the economy have been closely involved. Private sector views were solicited onthe proposed activities and various government institutions, directly and indirectlyinvolved in the Project participate in different forms. Line ministries of frontlineagencies and regulatory agencies will be closely consulted throughout the Project toensure effective internalization. Financing institutions and other donors supporting theGateway will continue to be consulted. In addition, GOG has included private sectorrepresentation in the GFZB.

Participatory Approach Preparation Implementation Operation

Beneficiaries/community groups IS, CON IS, CON & COLIntennediary NGOs IS, CON, COL IS, CONAcademic institutions IS, CON, COL IS, CON & COLLocal government IS, CON & COL IS, CON & COLOther donors IS, CON & COL IS, CON & COLOtherNote: information sharing [IS]; consultation [CON]; and collaboration [COLJ.

F. Sustainability and Risks

(i) Sustainability

54. The Project is expected to have a lasting impact on Ghana's economic developmentby reducing the high cost of doing business and increasing Ghana's competitiveness inglobal markets through: (a) the reform of the legislative, regulatory and incentive

- 21 -

systems in "front-line" areas; (b) institutional strengthening and capacity buildingincluding skills development in key areas; (c) development of new instruments toincrease availability of know-how and financing, such as franchising and private sectorparticipation in infrastructure (PPI); and (d) country promotion and consensus building.It will address the issue of quality of infrastructure in a limited manner in the immediateterm by supporting the development of geographically-sited EPZ. The EPZ could be builtsuccessfully and the capacity building objectives could be achieved, while a number ofother problems that are beyond the scope of the Project could stymie the EPZ fromattaining commercial success or the port from being privatized. Hence its is important toview this Project as one that removes constraints and its success should be evaluated onthat basis.

55. Appropriate guidelines will be developed to facilitate the integration of theindividual Gateway Project components into the overall EMP of the EPZ. Individualplant contingency plans will be developed to fit into the EMP framework as well. Thiswill constitute the basis for self monitoring and regular environmental auditing as wellas provide input for quality assurance.

56. The Project will be sustainable if-

* The GOG remains committed to reforming the civil service and relying onexternal checks and balances as an oversight mechanism for public agenciesdelivering services to the private sector;

- There is a clear commitment and strong political will on the part of GOG toaddress the ports and customs issues and the issues related to privateparticipation in infrastructure services;

- For the investment component, a suitably-qualified private investor/developercommits to make the on-site investment in the development of the EPZ; and

* The institutionalization of a healthy public-private sector dialogue leads tomutual cooperation and partnership.

- 22 -

(ii) Critical Risks ( see fourth column of Annex I)

Risk Risk Rating Risk Minimization Measure

* Any laxity in fiscal and monetary ! Moderate * The GOG, has recently tightened its fiscalpolicies on GOG's part could lead to and monetary policies. Macroeconomicfurther currency depreciation and performance is being monitored by theincreased inflationary pressure which Bank and the Fund.could adversely affect investorconfidence. . _,

* The implementation capacity of various Moderate * Provide necessary technical assistance toministries and agencies may constrain ensure implementationthe quality of implementation. *_,_l

* Unavailability of counterpart funds may Substantial * Budget process will include adequate fundsaffect implementation. which will be placed, in advance, in the

Project Account. Proactive management of*._________________ _ .__ this risk during supervision

* Finding a developer; and on-site . Moderate No financing to EPZ will be approved untilinvestments by developers and off-site an on-site developer is found and hasinvestments by GOG are completed. agreed to make infrastructure investments.

Provide expertise in developer search. Use*__ _of IFC and MIGA to enhance the deal.

* Supply chain development initiatives Substantial . * Involving agency heads in the gatewaydesigned to make inter agency interfaces secretariat alid making it accountable forporous and administrative processes coherent policy implementation. Contract-transparent to users are resisted by like arrangements for delivery of qualityentrenched agencies which resist all service between agencies and gatewaypressures for change and which continue secretariat.to protect exclusive "territorial rights"within stove pipe organizational units * _.

* A number of other problems that are Moderate * The effective empowerment of an inter-beyond the scope of the Project could ministerial "gateway task force" to drivestill stymie the EPZ from attaining the change process with the high levelcommercial success or the port from support and commitment. Early in thebecoming privatized (those problems process, a high level private sector userscould be related to the state of the world group will be nominated and engaged toeconomy, perceptions of Ghana as a serve as an advisory panel and additionalplace that is friendly to private driver for fundamental reform of supplydevelopers, particulars of the chain support processes like customscommercial arrangements, the clearance and port administration of feesgovernment's negotiating style, or the and cargo release.legal and regulatory framework). * ._l

* Unavailability of human and Substantial * Budget process will include adequate fundsinstitutional resources, compliance and to be placed in a Special Account managedenforcement mechanism for efficient by the EPA. GFZB and EPA will agree on aimplementation may impede on quality mechanism for full funding of EMP.performance.

Overall Risk Medium

- 23 -

(iii) Possible Controversial Aspects

1. Adverse labor reaction to proposals for private participation in infrastructure,particularly in ports and customs,

2. The GOG enhancements for the on-site investor and the unbundling ofcommercial risks from sovereign risks could be an issue.

3. Transparency in the selection of private participants in the provision of servicesand infrastructure.

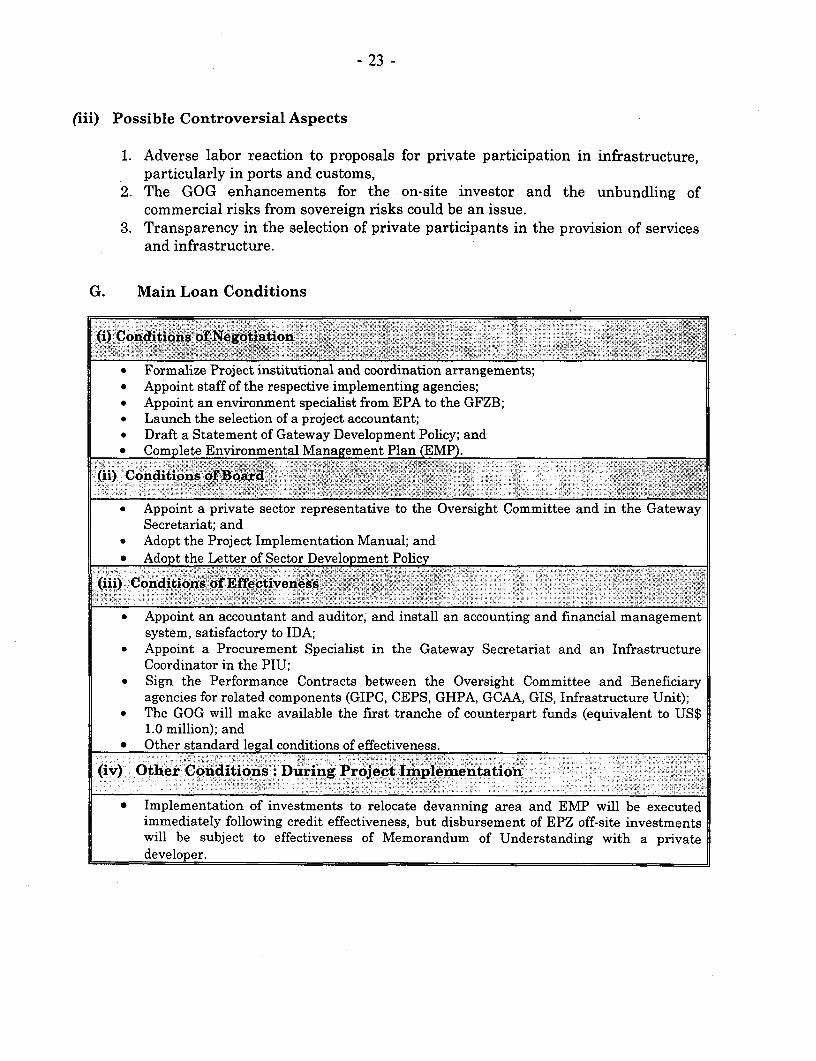

G. Main Loan Conditions

( Conditions of Negotiation l

* Formalize Project institutional and coordination arrangements;* Appoint staff of the respective implementing agencies;* Appoint an environment specialist from EPA to the GFZB;* Launch the selection of a project accountant;* Draft a Statement of Gateway Development Policy; and* Complete Environmental Management Plan (EMP).

(ii) Conditions orBoard

. Appoint a private sector representative to the Oversight Committee and in the GatewaySecretariat; and

* Adopt the Project Implementation Manual; and* Adopt the Letter of Sector Development Policy

(iii) Conditions of Effectiveness

* Appoint an accountant and auditor, and install an accounting and financial managementsystem, satisfactory to IDA;

. Appoint a Procurement Specialist in the Gateway Secretariat and an InfrastructureCoordinator in the PIU;

* Sign the Performance Contracts between the Oversight Committee and Beneficiaryagencies for related components (GIPC, CEPS, GHPA, GCAA, GIS, Infrastructure Unit);

* The GOG will make available the first tranche of counterpart funds (equivalent to US$1.0 million); and

* Other standard legal conditions of effectiveness.

(iv) Other Conditions: During Project Implementation

* Implementation of investments to relocate devanning area and EMP will be executedimmediately following credit effectiveness, but disbursement of EPZ off-site investmentswill be subject to effectiveness of Memorandum of Understanding with a privatedeveloper.

- 24 -

H. Readiness for Implementation

57. The procurement documents for the first year's activities are being prepared andwill be ready prior to effectiveness, to facilitate a prompt start to Project implementation.

I. Compliance with Bank Policies

58. This Project complies with all applicable Bank policies.

Country Director: Peter Harrold

Task Manager: Demba BA (AFTP1)

Technical Manager: Thomas W. Allen (AFTP1)

- 25 -

ANNEX IPage 1 of 4

GHANATrade and Investment Gateway Project

Project Design Summary

-NX-;-.~~~ia ' My fisv 47i .W m nt og;sNarrative Suiq~1CrAssuption

I. CAS Objectives: _ lIncreased private investment and * Achieve private investment of Macro-economic reports.exports. at least 10% of GDP by year-

2000. Trade statistics.* Growth rate of non-traditional

exports to average at least 20%per year by year-2000.

* 2,000 jobs created in year three;2,500 in year four; and 3,000 inthe fifth year followingcompletion of EPZ.

* Manufacturing growth to be atleast 8% per year by year-2000.

II. Project DevelopmentObjectives:A critical mass of export industries * 10 firms have been established GFZB reports Macro-economic stabilityare operating from a privately and are operating in second year Sustained political commitment todeveloped Export Processing Zone, after completion of civil works; Developer annual reports PSDin strict compliance with 20 by end-third year; and 30 byenvironmental guidelines. end-fourth year. Trade statistics

* Net export revenues areincreased by 25% in secondyear; by 30% in third year; andby 40% in fourth year after

_______________________________ _completion of the civil works.III. Project Outputs3.1. 1. A private developer with * Signed contract with developer. Signed lease agreements Promoters succeed in securinganchor tenants are found for the * On-site infrastructure. new industriesTema EPZ. Development plan. Effectiveness document

* Tenants occupancy plan. Promotion remains focused and3.1.2. Off-site Infrastructure for * Completion report. Firms annual reports. well targeted.Tema EPZ is completed. Investor perception

surveys. Commitments translate into actual3.1.3. Effective marketing of Ghana * 587 targeted workshops investmentsas a Foreign Direct Investment (FDI) between 1998-2002, with yield Supervis:on reportsdestination. of at least 8% site visits and a Utilities are restructured as part of

yield of $900 million of Annual report a well-defined privatizationinvestment firmly committed by strategy and are capable of

end-2002. Investor perception meeting EPZ demand and qualitysurveys of service requirements

- 26 -

ANNEX IPage 2 of 4

III. Project Outputs(Continued)

3.2.1. Cost of doing business * Organizational restructuring of GPHA isis reduced and front line completedagencies are trade facilitators. * Private sector participation in port Signed Lease, Suitable private operator is

operations, who will assume investments in agreement(s) with foundboth rehabilitation and expansion. private operator(s)

* New Ports Act which transforms the GPHA Private operator caninto a "landlord" structure, and grants Legislation establishing mobilize resources in agreater autonomy to the ports submitted to GPHA in its new role timely fashionparliament no later than end-1999.

* The devanning area is relocated outside the Supervision reports Efficiency gains areport no later than end-1999. realized by customers and

* A privately developed and financed Ports and Airport annual operator (s)Electronic Data Interchange is in place. statistics.

* Costs of loading import containers arereduced from US$168 in 1998 to US$80 by Annual ISO, ICCend-1999 and to international standards by certification.end-2000.

* Speed of unloading containers increasesfrom gross 12 boxes per ship hour to 20boxes per ship hour by end-1999 and 24boxes by year-2000.

* Average dwell time for imported containersdrops from 25 days in 1998 to 15 days byend-1999 and less than 7 days by year-2000.

Customs procedures are streamlined and Commitment of CEPSefficiency is improved (CEPS) in ensuring that reforms* Number of examinations at point of entry, of Ghana institute of are sustained.

cargo and documents, are reduced to one. Freight Forwarders* Cargo examination is reduced from 100% to

10% for statutory free goods, and 20% for (GIFF) reports.all dutiable goods.

* Appropriate customs regulation is in place to ISO, ICC annualallow direct delivery of containers between certificationthe port of Tema and the free zone enclaveno later than end-1999.

* A valuation system acceptable to allstakeholders is established.

* Number of overland customs check pointson road are reduced to I to Togo; 2 for RCI;and 2 to Burkina Faso.

* EPZ customs unit is operational in line withEPZ regulations.

- 27 -

ANNEX IPage 3 of 4

Narritive Summary Monitorable Indicators . -Means of Verification .sks & Assumptionsg

III. Project Outputs(Continued)

3.2.1 Cost ofdoing Immigration procedures for investors andbusiness is reduced and tourists are streamlinedfront line agencies are * Business and tourist visas issued on * Annual survey There are incentives for frontlinetrade facilitators. arrival upon payment of reasonable fees * GIS annual reports and agencies to sustain commitment

by end-1999. statistics to the spirit of service provider* Business/ Tourist visas are delivered * Airport statistics and trade facilitator.

within 48 hours at all Ghana consularmissions abroad, by year-2000. Autonomy of agency is upheld

* Services at entry points consolidated by GOGinto one (Immigration, Health and BNI)ensuring rapid clearance.

* 100 Immigration officers/ consulstrained in the Gateway concept by year-2000.

Agency establishes and maintainsCivil Aviation Sector high standards of professionalism* A future development scenario for the Air traffic data and credibility

civil aviation sector, reflecting GOG Flight permissionsgateway priorities is adopted by end- Legislation1999. Signed concession

* Regulation operationalizing liberalized agreements Privatization of Ghana Airways isskies policy is adopted by end-2000. done outside the scope of this

* KIA, management and development Project -- by Divestitureconcession is signed with private Implementationoperator by end-2000. Committee

* Ghana Airways is privatized by end-1999.

Adequate regulatory framework in placeand a regulatory agency is operational* Legislation and criteria governing Legislation

private sector participation ininfrastructure is adopted.

* Regulatory agency is adequately Regulatory agency reportsstaffed with qualified personnel, and and proceedingsoperational policies and guidelines inplace.

- 28 -

ANNEX IPage 4 of 4

IV. P ctoiponents Khpuf. 7:, . K . yerWca .-. Risks &i

1.0 Infrastructure and Development ofGeographically-sited EPZ

1.1 Implementation of EMP. US$2.00 million Contracts No unforeseen environmentalor resettlement issues

1.2 Construction of the off-site US$ 33.41 million Completion reports Investment for on-siteinfrastructure for the Tema EPZ. infrastructure comes from

private sources

1.3 Construction of devanning area US$ 3.50 million Detailed engineering design No design problems, costoutside port and improvement of port and bidding documents. overruns or geologicalcontainer facilities. problems

2.0 Trade Facilitation Capacity ofFront-line Institutions

2.1 CEPS- Conforming CEPS processing US$2.25 million Consultant report (roadmap) Timely availability ofstandards to ICC and ISO 9000. Counterpart funds

2.2 GPHA Concessioning of ports US$ 1.75 million Gateway Secretariat andactivities to the private sector and Oversight Committee may notbuilding capacity to regulate PPI; prove sufficiently powerful tofeasibility study for the extension and carry out all of the basicdredging of quay 2, landlord port. institutional reforms in the

Project.2.3 Converting GCAA into a regulatory US$ 1.00 millionagency, operationalization of open skies.

2.4 Modernization of Immigration Legal US$ 1.18 million Consultant report Beneficiary Agencies complyFramework, regulations and standard with terms of contract withoperating procedures. Oversight Committee.

2.5 Country and Investment Promotion US$ 2.75 million Annual Surveyssupport to GIPC.

2.6 Search for developer and oversight US$ 2.40 millioncapacity of GFZB.

2.7 Project Management & Program US$ 2.87 million Gateway Project progressCoordination. reports Project audit reports

2.8 Preparation of Gateway 11 US$ 0.5 million Project implementationprogress reports

- 29 -

ANNEX IIPage 1 of 5

GHANATrade and Investment Gateway Project

Detailed Project Description

Project Development Objectives