Embed Size (px)

Citation preview

Report No. 1 5658-CHA

ChinaFruit and Vegetable Marketing PerformanceNovember 6,1996

Rural and Social Development Operations DivisionChina and Mongolia DepartmentEast Asia and Pacific Regional Office

Doacmune of te W d Bank

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS(as of May 1996)

Currency Unit= Yuan (Y)$1.00 = Y 8.30

Y 1.00 = $0.12

FISCAL YEAR

January 1 - December 31

WEIGHTS AND MEASURES

Metric Systemand

1 hectare = 15 muI jin = 0.5 kg

PRINCIPAL ABBREVIATIONS AND ACRONYMS USED

GDP - Gross Domestic ProductGVAO - Gross Value of Agricultural OutputMIT - Ministry of InternalTradeMOA - Ministry of AgricultureSSB - State Statistical BureauVAT - Value Added Tax

Vice President (Acting) Nicholas C. Hope, EAPDirector : Nicholas C. Hope, EA2Division Chief Joseph Goldberg, EA2RSStaff Member Albert Nyberg, EA2RS

CONTENTS

PREFACE ................................ , iii

EXECUTIVE SUMMARY .v

1. INTRODUCTION .1A. Sector Overview .1B. Objectives .2C. Report Organization .2

2. PRODUCTION AND CONSUMPTION .3A. Production Structure .3B. Consumption .5C. Prices .8D. Income Impacts on Consumption and Production .9

3. REGULATORY AND POLICY FRAMEWORK .10A. Regulatory Issues .10B. Policy .12C. Market Information .14

4. MARKET STRUCTURE .16A. The Marketing Chain .17B. Post-Harvest Handling and Quality Control .19

5. MARKET PERFORMANCE .23A. Operational and Allocative Efficiency .23B. Price Transmissivity .26

6. CONCLUSIONS AND RECOMMENDATIONS .30

ANNEX 1: RULES AND REGULATIONS GOVERNING THE USE OFCHEMICALS ON FRUIT AND VEGETABLES .35

STATISTICAL ANNEX .39

- ii -

TABLES IN TEXT

Table 2.1: Per Capita Purchases (Urban) and Consumption (Rural) ofSelected Food Items .......................................................... 7

Table 2.2: Expenditure and Own Price Elasticities .......................................................... 7Table 4.1: Free-Market Sales Volume ......................................................... 16Table 5.1: Beijing Wholesale-Retail Market Margins ...................................................... 27Table 5.2: Construction of Synthetic Price Margins ......................................................... 28Table 5.3: Illustrative Price Margins ......................................................... 28

FIGURES IN TEXT

Figure 2.1: Consumer Price Seasonal Indices .......................................................... 8Figure 5.1: Seasonal Sales Distribution ......................................................... 25Figure 5.2: Monthly Distribution of Annual Sales (Three Wholesale Markets) .............. 25

- iii -

PREFACE

This report is largely based on the findings of a World Bank mission that visitedChina in October 1995. The mission members were Albert Nyberg (EA2RS-missionleader), Zhengxuan Zhu (EA2CH-Operations Officer, Agriculture), Edward Chobanian(Consultant-Agroindustry), and Donald Taylor (Consultant-Marketing Specialist).

The mission worked closely with counterpart staff from the Green FoodDevelopment Center of the State Farms Bureau, Ministry of Agriculture, who providedconsiderable background information, statistical data, and logistical support. Ms. ChengConghong (Vice Chairperson) was the principal counterpart and Messrs./Ms. Dou Ming,Li Furong, and Sun Hong accompanied the mission on field visits. Staff of the Ministryof Agriculture, Beijing, Shanghai, Shandong, and Yunnan Municipal/Provincial Bureausof Agriculture were helpful in providing production and marketing information duringmany discussions. Particularly helpful and interesting were the numerous State Farmmanagers, smallholder farmers, exporters, traders and trading company staff, wholesalemarket managers and staff, and retailers who provided information on market operations.

- v -

EXECUTIVE SUMMARY

Conclusions

1. A decade of rapid income growth, particularly for urban residents, has led toincreased expenditures for fruits and vegetables and increased demand for a wide varietyof foods while reducing demand for food staples such as cabbage. This has translatedinto higher producer prices for vegetables (relatively more stable prices for fruits), adoubling and tripling of vegetable and fruit areas, and increased farmer income.Vegetable production has shifted away from cabbage toward "finer" vegetables-although cabbage remains the most widely grown and consumed vegetable. Fruitproduction remains concentrated in traditional apples and citrus.

2. Fruit and vegetable marketing has evolved from a planned distribution system to abroad network of competitive and well-integrated markets. Price levels and price changesare rapidly and widely transmitted to market centers across China by networks ofwholesalers and traders. Provincial and municipal authorities have intervened modestlyin fruit and vegetable factor markets (land and input subsidies, etc.), but the productmarket has been largely left to the nonpublic sectors. This largely private wholesale-retail marketing system is highly competitive and internally efficient, despite highmarketing margins, and has performed impressively over the past decade. Othermarketing entities, such as institutional vendors, processors, and exporters exist but theyserve niche markets and do not offer competition to the wholesale-retail system. Withoutcompetitive systems such as distribution centers, auctions, farmer-retailer contracting,etc., it is not possible to determine or ensure the wholesale-retail system is efficient.

3. Government should maintain a flexible regulatory framework toaccommodate the development of more efficient marketing systems. The complexityof future systems will preclude direct government intervention lest efficiency bereduced. Further adjustments in the prevailing marketing system will be necessary toaccommodate complex changes in future market channels, institutions, volumes, andcomposition. High-volume, low-margin systems have developed elsewhere and moreefficient alternative marketing structures will evolve in China to provide an increasinglyurban population with an increasingly diverse array of food items.

The Role of Government in Marketing

4. Reducing quantity and quality losses is the most important initiative forimproving market efficiency, increasing farmer incomes, and reducing urbanconsumer food expenditures. Reducing estimated marketing losses from 30 to 20percent would save 19 million tons of vegetables for sale and consumption, with afarmgate value of Y 17.5 billion (1994). Various methods are employed in other

- vi -

countries to enhance quality and reduce losses but these have not been widely adopted inChina, which reflects the lack of understanding of their benefits. Without suchinformation, risk-averse farmers and low-margin traders have no adoption incentive.Over time, these methodologies will become industry norms but adoption could beaccelerated by widely demonstrating their benefits. This could be accomplished by, first,establishing a Post-Harvest Research Institute, under the Ministry of Agriculture, todevelop systematic information on marketing losses and test alternative methods forreducing those losses. These would include practices such as on-farm precooling ofvegetables, farm-level sorting and grading, and technologies such as rigid crates for on-farm harvesting and off-farm transportation, alternative packaging materials, mechanicalhandling and conveying equipment, alternative transport modes including refrigeratedrail/road transport, temporary use of cold storages, etc. Second would be farmereducation using traditional training and extension materials plus pilot projects todemonstrate the efficacy of these practices and technologies.

5. Standardized grades would assist in increasing farm income, give consumersmore options, permit traders to base their purchase on samples, and improve theusefulness of market information. But equally important, grades are essential fordeveloping the export trade. Grading is implicit at all transfer points, but is notinstitutionalized. Without Government guidance, grades and standards would emergeover time, but the sector may face multiple and inconsistent grades before an industrystandard is agreed. This initiative also would require substantial training of both farmersand marketing staff.

6. Given the potential health risk from toxic residues and unsanitaryvegetables, enforcement of existing phytosanitary regulations should bestrengthened. Strict adherence to these regulations is necessary to further develop theexport market. Farmer training is an important element in improving regulatorycompliance.

7. The Government could assist market development by consolidating themarketing information system and making it more comprehensive. To improve theefficiency of production and market decisions, the market information system should beconcentrated in one ministry, expanded to include information from sources other thanwholesale markets, and distribute quantity information along with price data. Also,situation and outlook information (assessment of production conditions and probablemarketings) should be disseminated similar to that currently released by the Ministry ofAgriculture for grains and oilseeds.

8. Village-based cooperative marketing organizations would increase farmincome by providing participants with increased market power, reducing the pricerisk of individual farmers, and permitting them to enjoy a portion of the marketingmargin. Such organizations are difficult to organize and manage effectively.Consequently, some organizational assistance would probably be required ofGovernment; but it is critical that farmers, not Government control the cooperatives.

- vii -

9. Various producer subsidies through the National and Municipal Vegetable BasketProjects have contributed to increased suburban vegetable production, improved farmerincomes, and made available a wide variety of vegetables at "reasonable" cost. Theseinitiatives have demonstrated the efficacy of "protected" production, which is now widelypracticed. Given this success, it is timely to refocus project objectives towardimproving marketing efficiency.

10. Discontinue the guidance price policy. It was designed to protect urbanconsumers from "price gouging" by retailers but it has been relatively ineffective. Giventhe numerous retailers in urban centers, competition should effectively prevent excessivemargins.

Another Consideration

11. The abundant labor force, limited land resources, and diverse agroclimaticenvironment suggests China has a potential comparative advantage in horticulturalproduction. However, this potential should be further studied as this study did notundertake a comparative advantage analysis of horticultural crops. With a comparativeadvantage, farm income could be increased not only by producing more vegetables tomeet increasing domestic requirements, but also to serve the regional export market.Foreign exchange earnings from horticultural exports should be greater than the foreignexchange savings that would result from producing import substitution crops such asgrain, oilseeds, and cotton. To exploit that potential, improvements would be required inmarket infrastructure and product quality.

- 1 -

1. INTRODUCTION

1.1 Horticultural crops comprise one of the most dynamic subsectors of agriculture.China's farmers now produce more than 150 million tons of fruits and vegetablesannually, making China the world's largest fruit and vegetable producer. A combinationof two major factors has led to this rapid growth. The relaxation of government controlsover the subsector permitted farmers to reallocate their resources to more efficientproduction modes. The subsequent fruit and vegetable supply response was possible onlybecause consumers were demanding more fresh vegetables, which increased prices,thereby sending incentive signals to farmers. Rising fruit and vegetable productionincreased farmer incomes despite marketing inefficiencies.

A. SECTOR OVERVIEW

1.2 Between 1984 and 1994, the Gross Value of Agricultural Output (GVAO)increased from about Y 560 to Y 980 billion (1990 constant terms) implying an averagegrowth rate of about 5.5 percent (Annex Table AL.1). Fruit and vegetable areas arerelatively small but, due to their high value, they contribute a disproportionately largeshare of agricultural output value. The real gross output value of vegetables (includingmelons) increased at an average annual rate of 10.5 percent between 1984 and 1994 andthe share of GVAO contributed by vegetables increased from 6 to 9 percent. A portion ofthis increase is attributable to changes in the production mix as higher-quality (andhigher-value) vegetables were increasingly produced. The output value of fruitproduction is not reported separately but is included with other perennial tree crops (tea,mulberry, etc.). The importance of cereal production is declining but continues to makethe largest contribution to GVAO accounting for 25 percent of agricultural value in 1994.

1.3 China's food self-sufficiency objective has lingered from the prereform period.Self-sufficiency ratios in the two major food components, grain and fruits andvegetables, reflect different pictures. Since 1978, grain self-sufficiency has twice cycledfrom less than to greater than 100 percent and in 1995 again became a net importer.Alternatively, fruit and vegetable self-sufficiency has consistently improved with netexports continuing to increase (1985-94).

1.4 Per capita consumption of fruits and vegetables now exceeds that of food grainboth in terms of quantity and value. Consumer expenditures for vegetables haveincreased rapidly, although the quantity consumed has declined as consumption patternshave shifted away from coarse to "fine" vegetables. Also, far greater quantities of bothfruits and vegetables are consumed by high-income earners than by low-income earners.

- 2 -

B. OBJECTIVES

1.5 As the Government disengaged from direct intervention in fruit and vegetablemarketing, the market structure was transformed into a highly competitive wholesale-retail marketing system, which has adapted well to the rapidly changing demand andsupply situation. However, the marketing process remains costly. The overall purposesof this study were to assist in: (a) identifying means and methods of improving themarketing process that would contribute to further increasing farmer incomes, and(b) better defining Government's role in regulating markets while relying on marketforces to promote alternative marketing systems and achieve supply-demand balances.

1.6 Specific objectives of the study were to:

(a) determine a policy and regulatory environment conducive to efficient foodmarketing;

(b) identify government marketing roles in information services andregulatory issues such as grades and standards, health and hygiene, etc.;

(c) identify constraints to the adoption of practices and technology whichwould improve marketing efficiency;

(d) assess the status of competitive market structures, marketing institutionsand channels and prospects for future development; and

(e) determine if "price spikes" occurred in the fruit and vegetable market (asoccurred in food grain prices) during 1993-95 and, if so, identify theircauses.

C. REPORT ORGANIZATION

1.7 Recent changes in fruit and vegetable supplies and farm prices are reviewed in thefirst section of Chapter 2. Secondly, demand and consumption and the future implicationof income changes on demand is discussed. Lastly, it reviews consumer prices. Chapter3 reviews the regulatory and policy framework applying to fruits and vegetable marketsand discusses the role of government in: (a) introducing-enforcing grades and standards,and (b) collecting-disseminating market information. Market structures are discussed inChapter 4, including the problems of post-harvest handling and quality control. Chapter5 analyzes market performance in terms of efficiency and price transmission. Chapter 6contains the study's conclusions and recommendations.

-3-

2. PRODUCTION AND CONSUMPTION

A. PRODUCTION STRUCTURE

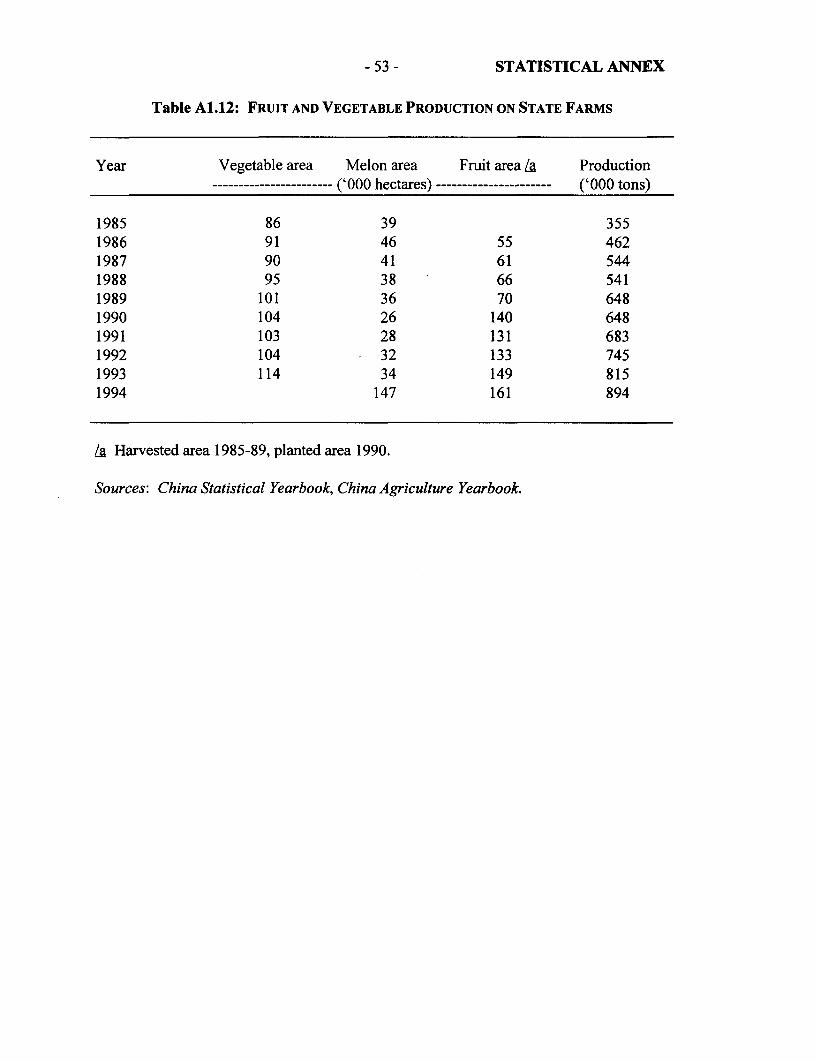

2.1 Almost all vegetables are produced on small farms. Statistical data suggest that 2to 3 percent of the vegetable and melon areas are on State Farms, but much of this land issubleased to individual farmers and the mode of production is distinctly small farm;however, the State Farm may perform some of the marketing functions. The structure ofState Farms better lends itself to fruit production and marketing and they account for 2 to3 percent of actual fruit production.

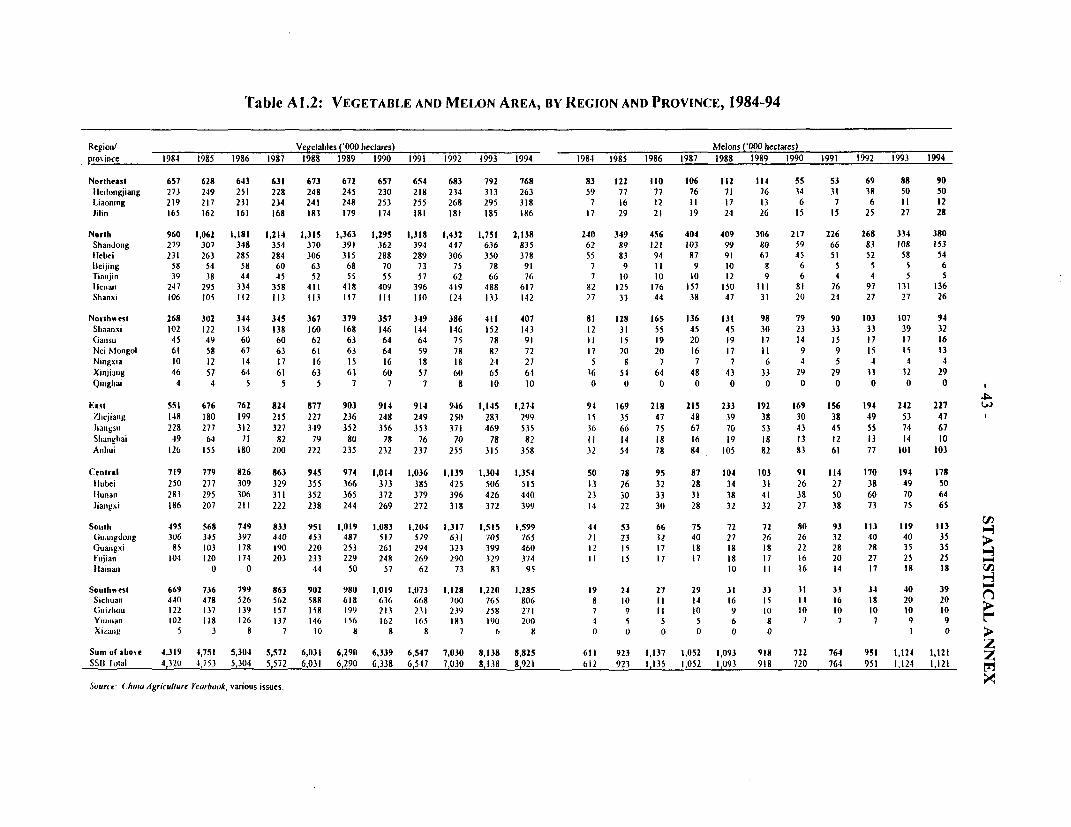

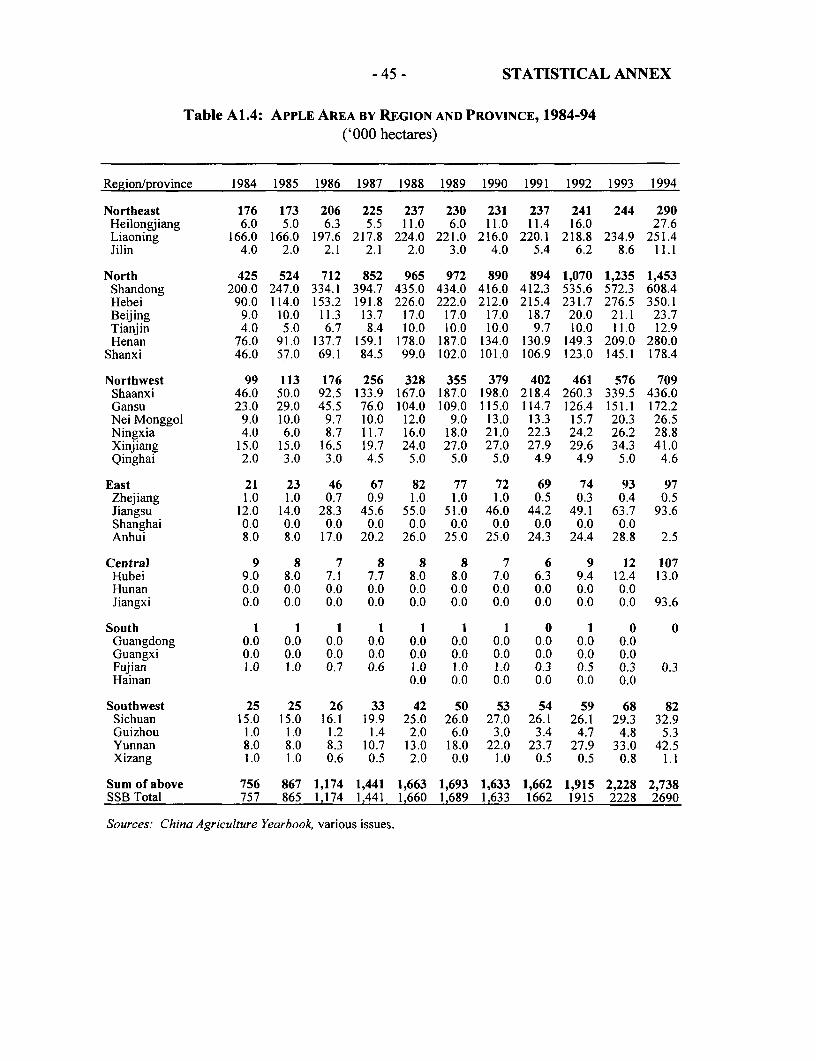

2.2 The vegetable area (including melons), of 10 million hectares (ha) in 1994,occupies about 10 percent of the planted agricultural area of China, but vegetable land isdouble and triple cropped, resulting in vegetables occupying a smaller proportion of thecultivated area. Anecdotal evidence suggests that area and production under "protectedcultivation" (plastic tunnels and greenhouses) have increased very rapidly, but officialstatistics do not separately record this information. As orchards are perennial crops, theircultivated and planted areas coincide (7.2 million ha in 1994).

Sources of Growth

2.3 Detailed area and production data by vegetable variety are limited but suggest thatvegetable subsector growth is attributable to the expansion of land allocated to vegetableproduction, and changes in vegetable composition with "fine" vegetables (snow peas,green garlic, green beans, cucumber, etc.) replacing "staple" vegetables (Chinesecabbage, round cabbage, radish, etc.). Cabbage area declined by 100,000 ha between1989 and 1991, but still occupied 19 percent of the total vegetable area. The area plantedto many of the "fine" vegetables increased by 20 percent or more over the same threeyears. Although the vegetable area is expanding, total vegetable production and averageyields are declining because lower-yielding fine vegetables are replacing high-yieldingcabbage.

2.4 The fruit area and production increased by more than 225 and 250 percent,respectively, over the decade; suggesting that area increases accounted for most of theincreased production. Apples and citrus are the most important fruits, collectivelyaccounting for 50 percent of fruit production. Pears, bananas, and grapes comprise thesecond tier, accounting for a further 25 percent of production; numerous temperate andtropical fruits comprise the balance.

2.5 In the absence of an age distribution of trees, it is difficult to assess productivitychanges in orchard crops as different varieties commence and reach full production atvarious ages. Given this caveat, it appears that virtually all of the production increases of

- 4 -

300 and 90 percent for apples and pears were attributable to expanded areas. Citrusproduction increased by 275 percent, assisted by a 50 percent increase in yield. Grapeand banana production quadrupled and yields doubled. It must be appreciated that grapesand bananas each occupy only about 2 percent of the fruit orchard area.

Locations of Growth

2.6 The total vegetable area doubled between 1984 and 1994, in part, due toimplementation of the Vegetable Basket Project (paras. 3.12-3.14), which includedinfrastructure and production input subsidies. Shandong expanded its vegetable area by200 percent over the decade and surpassed Sichuan as the leading vegetable province in1994 (in terms of area). The highest rate of vegetable growth was in the group ofsouthern provinces (Guangdong, Guangxi, Fujian, and Hainan), which more than tripledthe planted areas. Other important vegetable-producing provinces include Hubei, Henan,and Jiangsu. The area planted to melons fluctuated widely, but generally increased overthe 1985-94 decade. The major melon production areas are the North China Plain and thelower Yangtze valley.

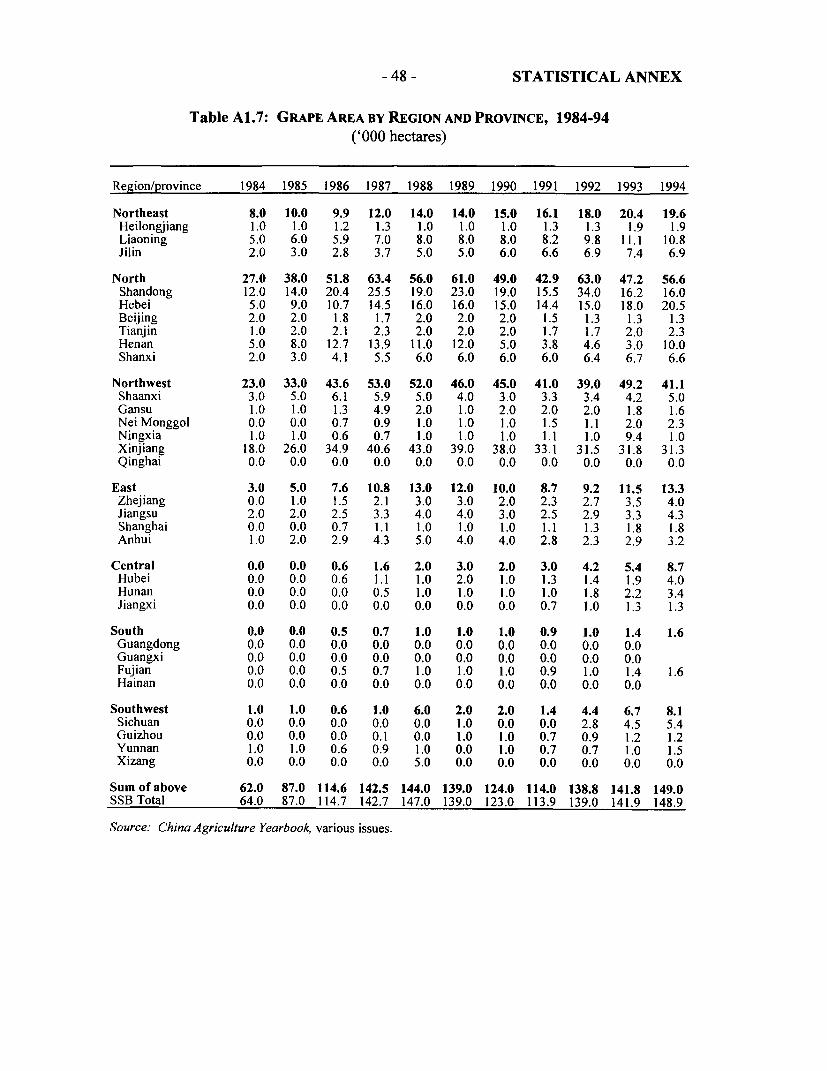

2.7 Apples are produced throughout the country, except for the southern tier ofprovinces, but are concentrated in the high-yielding North China Plain. Citrus productionis located primarily in the southern and coastal provinces. Banana production is highlyconcentrated in the southern provinces, particularly Guangdong, which produces morethan 50 percent of the nation's output. Although grapes are widely scattered across thecountry, there are two concentrations, Xinjiang Autonomous Region and the North ChinaPlain; each area contributes about one-third of national production. National pearproduction, which occurs in every province, increased the least of the five major fruits.

Trade Impacts on Supply

2.8 A wide variety of fresh and selected dried fruits-vegetables are imported but thevolume is minor, typically less than 1,000 tons per variety, except for tropical fruits,which are imported in significant quantity. However, exports of fresh/dried fruits-vegetables have increased rapidly in recent years, totaling over 3.5 million tons and $3.0billion in 1994 and 1995. Exports reduced domestic supplies by about 2 percent.

2.9 Although international trade has a relatively unimportant supply impact, the tradestatistics for fruits reveal important quality aspects of production and consumption.Vegetable statistics are too aggregated to evaluate individual varieties. About 265,000tons of apples were exported during the three-year period 1992-94. The nominal exportprice (unit value) was $413 per ton. Apple imports, although small, have doubled in eachof the last five years; 1994 imports were 3,438 tons. The average import price during1992-94 was $925 per ton, or more than double the export unit value. This demonstratesa small but growing demand for high-quality, high-value produce that is not met fromdomestic producers. It also demonstrates the need to introduce grades and standards intothe food marketing system. The same pattern emerges for orange exports and imports.

The average unit value of exports and imports was $372 and $590 per ton, respectively,for 1992-94; meanwhile the "world" price of oranges' averaged $444 per ton.

2.10 As horticultural production is labor-intensive and given China's resourceendowment, especially the diverse agroclimatic environment, it should enjoy acomparative advantage in fruit and vegetable production. Thus, in addition to serving thelarge domestic market, Chinese production could potentially service a regional exportmarket. However, to exploit that potential, quality must be improved and additionalinfrastructure must be developed. This further illustrates the need for the introductionand usage of standardized grades.

Prices are Increasing

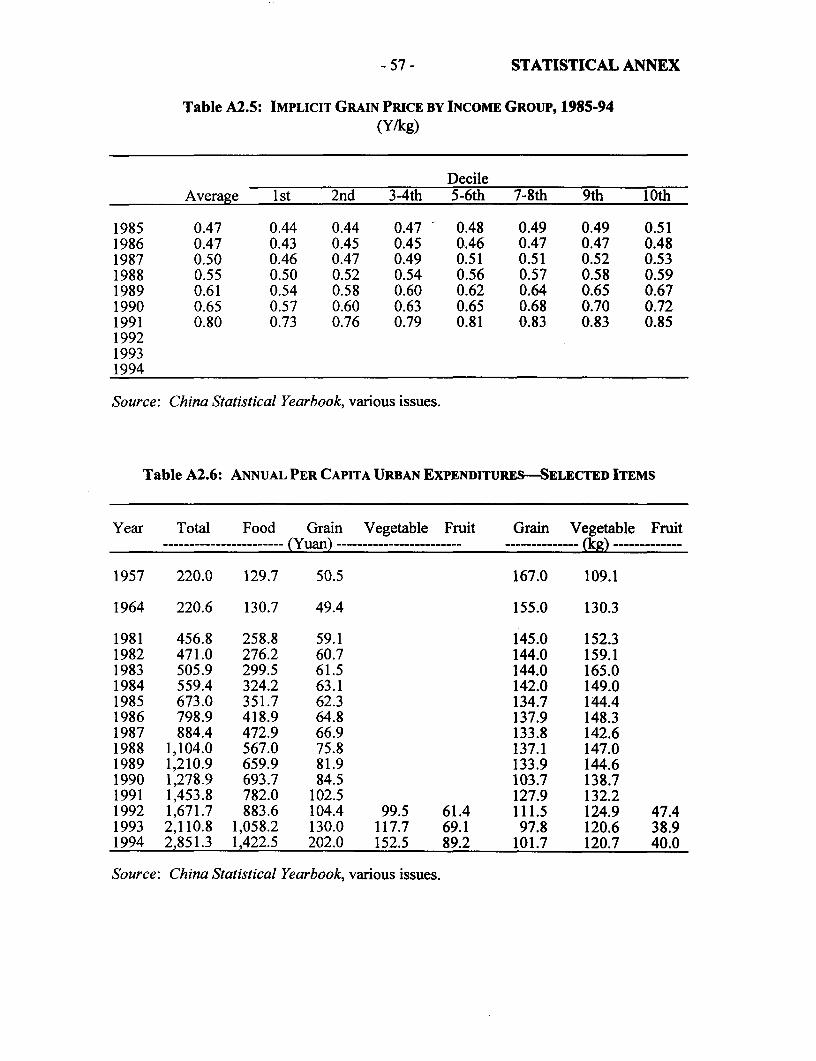

2.11 National annual average farmgate prices for fresh vegetables (collectively) andindividually for apples and citrus/oranges were reported until 1992, and subsequentlydiscontinued (Annex Table A4.1). However, price indices have been computed through1994. These prices and price indices reflect not only price changes in the variouscommodities, but also incorporates quality and composition changes. The index of freshvegetable prices (farmgate) increased rapidly from the mid-1980s. Prices doubledbetween 1985 and 1990, and doubled again by 1994, increasing much more rapidly thanthe overall farm product price index and providing an important incentive for farmers toproduce more vegetables. In contrast, the farmgate fruit price index increased by only 45and 20 percent, respectively, during the two time intervals.

2.12 Fresh vegetable prices, in constant terms, increased by 150 percent between 1984and 1992, although they experienced a "down cycle" in 1988-89. The real price of applesand citrus/oranges reached a peak in 1988 and plateaued for apples; but citrus/orangeprices declined and in 1992 were below 1984 prices.

2.13 There is anecdotal evidence indicating a supply shift is occurring in vegetableproduction, but without more detailed statistics it is not possible to measure this shift.Given the increasing real average prices, it appears demand for fine, high-qualityvegetables is increasing more rapidly than supply. The price increases are a partialreflection of the composition change with less coarse and more fine vegetablesproduced/sold. Alternatively, it appears that increases in apple and citrus production haveexceeded demand increases.

B. CONSUMPTION

2.14 Cross-section data from the annual urban consumption and expenditure surveysconducted by the State Statistical Bureau (SSB) clearly indicate that per capitaconsumption of fruits and vegetables increase as incomes increase; this is fully consistent

World Bank; Commodity Markets and the Developing Countries, A World Bank Quarterly. EECindicative imnport price (CIF) Paris, navel oranges, Mediterranean Exporters.

- 6 -

with consumption theory. However, these data just as clearly indicate that vegetableconsumption declined during the 1985-94 decade-a period when urban incomesincreased rapidly.

2.15 It is difficult to reconcile these two data sets. But, declining per capita vegetableconsumption may be partially explained by the changing preference of Chineseconsumers for improved quality and less quantity. Earlier vegetable consumptionconsisted primarily of coarse vegetables, such as cabbage, but as incomes increased overtime consumers prefer more "fine" vegetables. [Although declining in importance,cabbage remains the most important vegetable in the diet, 32.3 kilograms (kg)/capita in1994.]

2.16 Other possible explanations for declining vegetable consumption include:(a) vegetable purchase statistics in earlier years overstated consumption as substantialwastage occurred-particularly in winter-stored vegetables, such as cabbage; and(b) improved grading, quality control, and marketing increased the edible proportion ofthe vegetables marketed; thus, losses formerly absorbed by consumers are nowconsidered post-harvest losses.

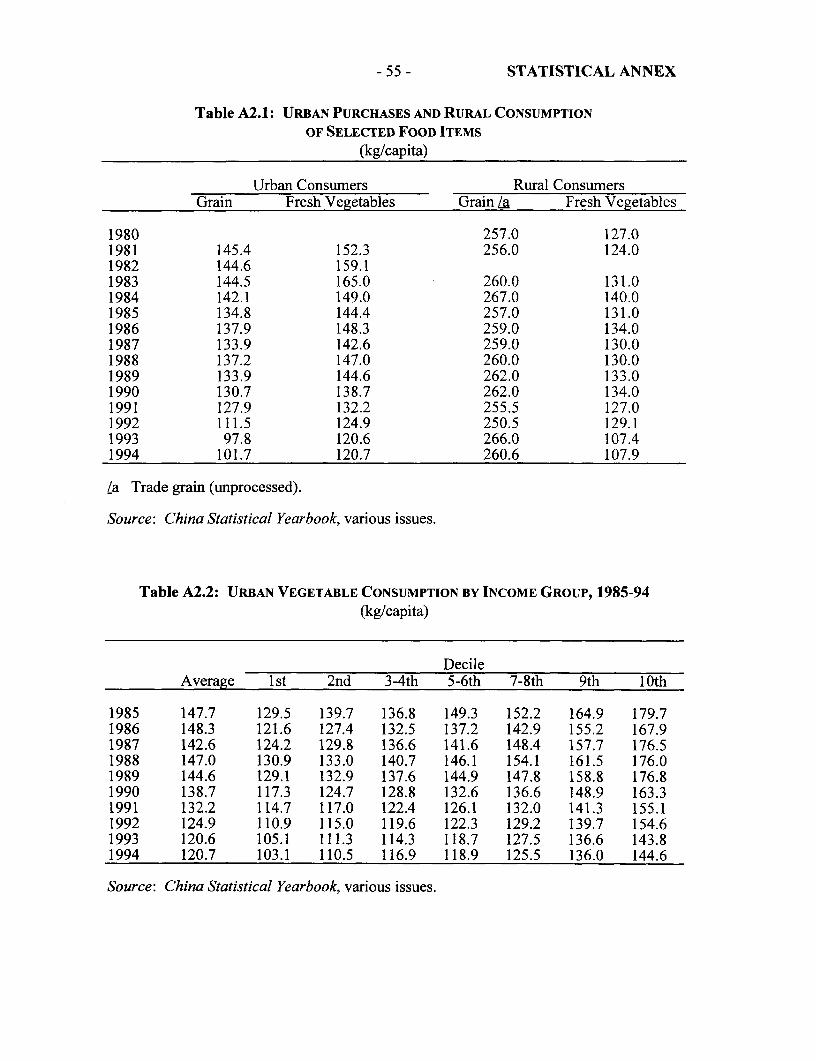

2.17 Parallel changes in per capita consumption of grain and fresh vegetables by urbanand rural consumers are illustrated in Table 2.1. Fruits and vegetables are the mostimportant component of urban diets in both expenditure and volume terms. Urban percapita fresh vegetable consumption remained relatively stable during the 1980s butstarted to decline in 1990; by 1994 consurnption was about 20 percent below the 1988peak of 147 kg. Between 1992 and 1994, per capita consumption of fresh vegetablesdeclined marginally (from 124.9 to 120.7 kg) but expenditure increased more than 50percent. This further indicates the shift from low- to high-quality (price) vegetables andin the face of rapid price increases confirms a high expenditure elasticity for vegetables.Consumers in the highest income decile consume about 40 percent more fresh vegetablesthan consumers in the lowest income decile. Urban fruit consumption data are availableonly since 1992 and have averaged about 40 kg per capita. Consumers in the highestincome decile consume about 100 percent more fruit than those in the lowest decile.Rural household consumption of fresh vegetables reportedly declined from a 1984 peakof 140 to 107 kg/capita in 1994 with a precipitous decline between 1992 and 1993. In theabsence of a major calamity, such a decline seems improbable and it is likely that achange occurred in survey techniques, methodology, or definition.

Elasticity Coefficients

2.18 Several scholars have estimated income (or expenditure) and price elasticitycoefficients for selected food items. Some of the more recent are those estimated by Fan,et al.,2 Gao, et al.3, and Chern and Wang.4 Different models were used, different

2 Fan, Shenggen, E. Wailes, and G. Cramer, "Household Demand in Rural China: A Two-Stage LES-AIDS Model," American Journal ofAgricultural Economics, Vol. 77 (February 1995), pp. 54-62.

- 7 -

disaggregation levels were employed (Fan, et al. analyzed only rural households and Gao,et al. analyzed only urban households), and varying results were obtained. Chern andWang used a more sophisticated model and estimated elasticities under conditions ofnonrationing and rationing, using quadratic expenditure systems, and are summarized inTable 2.2.

TABLE 2.1: PER CAPITA PURCHASES (URBAN) AND CONSUMPTION (RURAL) OFSELECTED FOOD ITEMS

(kg/capita)

Urban Consumers Rural ConsumersYear Grain Fresh Vegetables Grain /a Fresh Vegetables

1980 257.0 127.01981 145.4 152.3 256.0 124.01982 144.6 159.1 260.0 132.01983 144.5 165.0 260.0 131.01984 142.1 149.0 267.0 140.01985 134.8 144.4 257.0 131.01986 137.9 148.3 259.0 134.01987 133.9 142.6 259.0 130.01988 137.2 147.0 260.0 130.01989 133.9 144.6 262.0 133.01990 130.7 138.7 262.0 134.01991 127.9 132.2 255.5 127.01992 111.5 124.9 250.5 129.11993 97.8 120.6 266.0 107.4/l1994 101.7 120.7 260.6 107.9/l

/a Trade grain (unprocessed).Lb There is no official explanation for the precipitous decline in consumption between 1992 and 1993.

Source: China Statistical Yearbook, various issues.

TABLE 2.2: EXPENDITURE AND OWN PRICE ELASTICITIES /a

No rationing lk Rationing l2Item Expenditure Own Price Expenditure Own Price

Grain -0.06 0.05 - -Fresh Vegetables 0.47 -0.42 -0.36 -0.59Dry Vegetables 1.15 -0.88 -1.08 -0.97Fruits 1.58 -1.09 -0.88 -0.95

/a Linear systems estimates yielded statistically similar coefficients; thus, only the quadratic systemestimates are listed.

Lb As both grain and vegetable oil were rationed during the 1985-90 period, the systems were estimatedusing two alternative specifications; the first assumed all grain and vegetable oil were unrationedmarket purchases, and the second assumed all grain and vegetable oil expenditures were quota rationpurchases with coupons.

3 Gao, X.M., E. Wailes, and G. Cramer, "Partial Rationing and Chinese Urban Household Food DemandAnalysis," Journal of Comparative Economics, Vol. 22 (1996), pp. 43-62.

4 Chem, Wen S. and G. Wang, "The Engel Function and Complete Food Demand System for ChineseUrban Households," China Economic Review, Vol. 4, No. 1, 1994, pp. 35-57.

- 8 -

C. PRICES

Consumer Prices

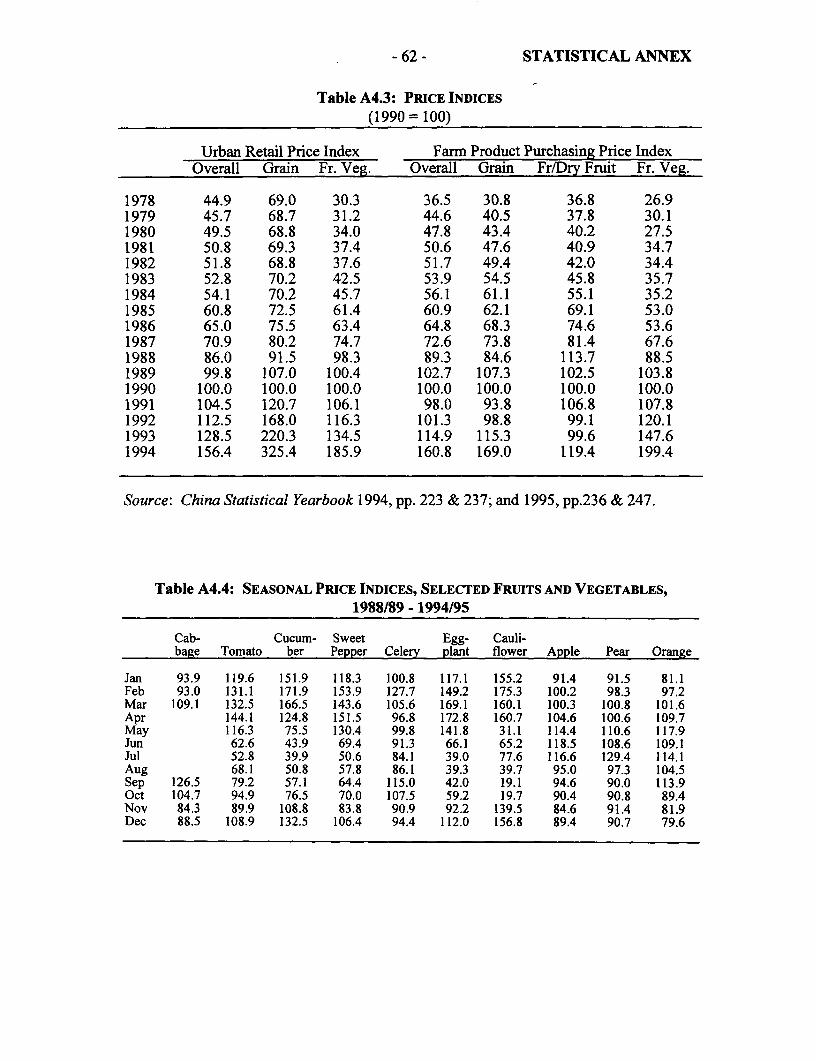

2.19 Since 1980, retail vegetable prices have increased consistently and more rapidlythan retail prices in general. The All Retail Price Index increased 250 percent between1978 and 1994, while fresh vegetables increased by 500 percent (85 percent increasebetween 1990 and 1994). Government intervention in the vegetable market has beenminor since the mid-1980s and retail vegetable prices have generally moved in parallelwith farmgate prices.

Seasonal Prices5

2.20 Some vegetables are available for only a few months during and immediatelyfollowing harvest as they are too perishable or of too little value to store fresh, but manyvegetable varieties are available year-round as winter crops are either grown in southernlocations or in sheltered production facilities (greenhouses and plastic tunnels). Storablefruits are placed in cold storage following harvest for off-season consumption.

2.21 A seasonal price index was calculated for Chinese cabbage to represent atraditional vegetable "staple." Also, fresh vegetable and fresh fruit seasonal price indiceswere constructed by consolidating six vegetable price indices (tomatoes, cucumbers,sweet peppers, celery, eggplant, and cauliflower) and three fruit indices (apples, pears,and oranges). The indices are represented in Figure 2.1. The seasonal index starts withSeptember rather than January to accommodate Chinese cabbage, which is generallyavailable for only 7 to 8 months of the year.

FIGURE 2.1: CONSUMER PRICE SEASONAL INDICES

160

14 0 - - - - - - - - - - - - - -

40

Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug

+--Fruit --- Vegetables +-Cabbage]

5 Derived from monthly retail prices in 20 major cities using 1988 to 1995 data.

- 9 -

2.22 Cabbage and fine vegetable prices follow traditional seasonal patterns, which arevery low during summer, increasing during autumn and winter to reach peaks in earlyspring. The volatility of individual vegetables is much greater than indicated by theaggregate index as individual vegetable price peaks may be four times the level of pricelows. Despite large increases in winter greenhouse production over the past severalyears, there is no indication that summer-winter price differentials have diminished.Separate indices were constructed for a few cities (Beijing, Shanghai, Shenyang, Wuhan,and Chengdu) to evaluate seasonal price variation geographically. The only discernibledifference was the tendency for more volatile prices to prevail in northern cities and lessvolatility in the south. There is no evidence of abnormal price volatility, or "spikes," invegetable prices in late 1993 or early 1994.

2.23 Fruits mature and are harvested over a 2- to 3-month period. Fruits have betterstorability than vegetables; consequently, fruit prices have less seasonal volatility thanvegetables. The fruit price index is lowest during harvest months, and graduallyincreases (consistent with storage costs) over the winter and peaks just prior to thefollowing harvest. Intraseasonal price volatility is ±20 percent. There is no evidence thatseasonal price fluctuations diminished between 1988 and 1995.

D. INCOME IMPACTS ON CONSUMPTION AND PRODUCTION

2.24 Income-induced dietary changes in Chinese consumers are occurring at relativelylow income levels as Chinese food consumption patterns are similar to those achieved inneighboring countries at per capita income levels two to three times higher than China'scurrent level. Derived elasticities indicate that as incomes increase, Chinese consumerswill eat more fruit; but consumption statistics from other East Asian countries suggestthat at high-income levels, total fruit consumption will plateau and eventually decline.But Chinese incomes are unlikely to reach these levels within the near future, despitehigh growth rates. As Chinese consumers demand greater fruit variety, new varieties willbe planted. But yields of traditional fruits average 25 to 35 percent of the yields in nearbycountries; therefore, applying more modern production practices and technology wouldpermit China to meet future fruit consumption requirements from the area that iscurrently devoted to fruit orchards. However, in reality, slow adoption of thesemethodologies will likely result in increased fruit orchard areas in the near term.

2.25 The transition toward consuming a wider variety of vegetables will doubtlesslycontinue, but total vegetable consumption is unlikely to decline much further as percapita consumption is already relatively low by East Asian standards. For every kilogramof "fine" vegetables that replace cabbage in the collective Chinese diet, about 50,000 haof additional land is needed to produce the replacement vegetables due to the much loweryield of "fine" vegetables. However, yields of "fine" vegetables are about 50 percent ofthe yields in nearby East Asian countries, again indicating that much of the increasedproduction requirement could potentially be met through increased productivity.

- 10-

3. REGULATORY AND POLICY FRAMEWORK

A. REGULATORY ISSUES

3.1 Government marketing agencies are typically bureaucratic and inefficient andunable to react rapidly to market conditions. Thus, marketing functions are best left tothe private sector. However, the Government has important roles in market regulationand policy. These include grades and standards for both health/nutrition issues (exposureto hazardous chemical and biological residues) and for differentiating products, licensingfees and taxes, and accurate market information.

Phytosanitary

3.2 The phytosanitary regulatory framework is appropriate; however, enforcement islax. A series of rules and regulations govern nonchemical fertilizer and pesticide use onfruits and vegetables. The Ministry of Agriculture is responsible for enforcing theseregulations and phytosanitary/quarantine stations are located in major markets and atsome rail stations, seaports, and airports. If produce moves outside the province oforigin, a phytosanitary certificate is required. Chemical fertilizers and green manures arepromoted for use on vegetables; animal manures are discouraged and human waste isprohibited. However, it is neither possible to supervise applications by all farmers nortest for pesticide residuals on all marketed produce, and it is acknowledged that bothanimal and human waste are frequently applied as fertilizer. Most pesticides approvedfor vegetable application are relatively nontoxic and rapidly degrade. Pesticideregulations are contained in Annex 1. Zero pesticide residue is required for export items.

The Benefits of Introducing Grades and Standards

3.3 Most fruits and vegetables are marketed by variety without regard to quality.Consequently, quality is determined by each buyer's individual criteria, by visualinspection. There would be several benefits if quality were quantified and defined as aspecific grade. Produce would be more precisely described, permitting buyers topurchase on the basis of description, or samples, instead of individually sorting throughan entire shipment of produce. It would differentiate produce, permitting farmers toreceive differentiated prices for their produce and earn a higher income. It wouldfacilitate market reporting as prices would apply to specific grades of vegetables, not toan "average" grade. Also, the differentiated prices would benefit low-income consumersby making available lower-quality produce at lower prices.

3.4 Despite the lack of official grades, grading is a routine element in the marketingprocess. Exporters carefully grade the produce destined for export lest the importer rejectthe consignment. Luxury supermarkets just as carefully grade the produce they receive

- 11 -

prior to making it available for sale. Some wholesalers who purchase for resale in largecity markets grade and purchase only that produce which meets their individual criteria.Most retailer vendors make quality separations of their produce to enable them to chargedifferential prices. Consumers implicitly grade the products when they individuallyselect the particular vegetable they wish to purchase.

3.5 But, grades and standards have not been institutionalized save for the GreenFoods trademark. (The Green Foods Development Center is a subsidiary of the StateFarms Bureau of MOA). Their standards were developed because of an incident ofassumed pesticide poisoning on fruits and vegetables. Green Food standards integratevarious environmental, production, processing, and marketing factors. Criteria include,inter alia: (a) production on suitable soils in an environmentally sound manner; (b) pestmanagement must not rely solely on chemical pesticides; (c) plant nutrition must not relysolely on chemical fertilizers nor include human waste; and (d) the resulting productsmust be "clean" and free of chemical residues. Production conditions are monitored andthe produce is inspected. If all the criteria are met, the produce is permitted to be soldusing the Green Food logo. Vegetables sold under the Green Food trademark representonly a fraction of total vegetable sales, but they are sold at premium prices.

Tax and Fees Impacts on Marketing Costs

3.6 The Government licenses various activities and either charges fees or authorizesmarketing agencies to do so to cover certain expenses. Also, the Government levies taxesfor revenue. In this regard, wholesale markets are authorized to levy fees on marketparticipants, based on produce value, and collect value-added taxes (VAT) on behalf ofGovernment. Maximum wholesale market fees are 2 percent and fruit/vegetable VAT is7 percent. Retail vegetable vendors are exempt from VAT.

3.7 However, the Government must ensure that informal charges do not place anonerous burden on marketing agencies. Some Chinese provinces allegedly levy fees fortruck transit that are 10 to 15 percent of the produce value. While transit fees arejustified, and are levied on freight transporters who use public roads in most countries,the fee level should be an appropriate contribution to road maintenance and services andnot a major revenue source. Transporting fruit from Yunnan to Shanghai requirestransiting four provinces, which could increase the marketing cost by 60 percent if all theprovinces charged a 15 percent transit fee. Some municipalities/provinces issue specialpermits to vegetable transporters, which (theoretically) exempt them from"extraordinary" fees and levies.

Market Entry

3.8 Entry into fruit and vegetable marketing is exceptionally open. Retail vendingrequires only payment of a market stall fee (Y 4 to Y 6/day) to the district authorities.Some retail marketplaces are unable to accommodate new retailers as available space isfully occupied. However, this constraint is often avoided by selling in a nearbyunauthorized location or by itinerant peddling. Also, marketplaces in new residential

- 12-

areas are frequently opened. There are no constraints to operating a fruit and vegetableshop in a permanent structure other than zoning regulations. Private entrepreneurs haverented numerous convenience food stores (previously state retail outlets), some of whichstock high-value fruits.

3.9 Becoming a fruit and vegetable wholesale trader is considerably simpler thantrading in other agricultural commodities where minimum capitalization requirementsmust be met. A wholesaler must have a tax document, readily obtained from the TaxOffice, specifying the tax rate and type (7 percent VAT on wholesale fruits andvegetables). The only other requirement is a license issued by the Industry andCommerce Bureau located in the wholesale marketplace. The wholesale marketadministration levies a fee on the value of the produce sold and charges rental fees for thespace occupied.

3.10 Many new marketplaces are municipally owned but collective and othernongovemment-owned marketplaces are increasing rapidly (Annex Table A3.1). Landfor market construction is a serious constraint and is the principal reason that most newmarkets have suburban locations. Market management must register with the Tax Officeto collect VAT on its behalf. Other requirements include arranging for CommerceBureau representation, market information collection-dissemination, and meetingenvironment regulations on sanitation and waste disposal.

B. POLICY

3.11 Market liberalization commenced in 1985 in the smaller cities but, by 1988, wasextended to medium and large cities as well. As the central government relaxed itsresponsibility for supplying urban residents, the authority to intervene in markets wasdelegated to provincial, municipal, and city officials. Day-to-day responsibility restedwith the Agriculture and Commercial Bureaus. An element of municipal policy was topreserve agricultural land generally and vegetable land particularly. Beijing Municipalityaddressed this issue by requiring 1.5 units of new agricultural land be developed toreplace each unit of agricultural land lost to urbanization.

3.12 A National Vegetable Basket Project was introduced by MOA in 1988 with theobjectives of adjusting/improving supplies, reforming production and marketing,rationalizing prices, strengthening market infrastructure, and improving year-roundsupply availability. Under state auspices three national production "bases" weredeveloped: (a) a subtropical base in Guangdong/Guangxi/Fujian provinces; (b) a summer-autumn base in Shandong/Anhui/Henan; and (c) a Chinese cabbage base in North China.It was anticipated that the establishment of these bases would assist in providing year-round supplies and reduce seasonal price volatility.

3.13 Basically, however, municipal governments were responsible for their ownvegetable supplies and they proceeded to develop vegetable production "bases" in nearbyand distant suburbs for seasonal production and a portion of off-season supplies. Eachcity specified an amount, or proportion, of the suburban vegetable base land on which

- 13 -

Chinese cabbage was to be planted for autumn production. Except for the cabbagerequirement, farmer participants were free to grow the varieties of their choice, with theproviso that the produce be sold in wholesale or retail markets within the municipality. Avariant of this process operated in Shanghai where, in addition, the municipality wouldcontract with local farmers for eight specific vegetables (Chinese cabbage, roundcabbage, bok choy-two varieties, radish, celery, spinach, and a leafy vegetable) to bedelivered to designated wholesale markets. The municipality also contracts with farmergroups in other provinces for vegetables but without specifying variety, price, or quantity.Vegetable Basket Projects have been remarkably effective in increasing croppingintensity of vegetable land and expanding the availability of winter and off-seasonvegetables.

3.14 The municipal governments provided subsidized infrastructure (all-season roads,irrigation, electricity, etc.), inputs (fertilizer, pesticide, plastic for mulch and protectedproduction, and metal frames for greenhouses and tunnels), and one-time cash subsidiesto convert land to vegetable use. New wholesale facilities were promoted and partiallyfinanced (subsidized) to diversify marketing channels and new technologies wereintroduced, particularly "protected" (under plastic) production and new varieties that werehigher yielding and more resistant to pests, and more tolerant of drought and temperatureextremes-to extend the traditional season.

3.15 It is estimated that Beijing Municipality, county, and local governments investedY 700 million in the vegetable production base between 1992 and 1994. Similarly,various jurisdictions invested Y 250 million to establish 20,000 mu of plastic tunnels insuburban Shanghai. Inputs are made available at prices 33 to 50 percent below marketprices and one-time cash payments of Y 100 to Y 200/mu are paid.

3.16 Investments in suburban production bases and production subsidies have resultedin a Beijing vegetable self-sufficiency ratio of about 0.70. However, about 75 percent ofthe vegetables marketed in wholesale markets originate in other provinces. Alternatively,about 25 or 30 percent of the Shanghai wholesale market supplies are obtained from otherprovinces. Much of these supplies are obtained through formal economic links withproduction centers in other provinces and joint ventures between the municipality and theproduction center (county).

3.17 The Vegetable Basket Project is now moving into the next phase with newobjectives and goals. Some of the more important are: (a) improve quality-50 percentof all marketing will be "clean" vegetables by 2000; (b) further increase protectedproduction and reduce volume disparities between peak and slack seasons; (c) expandfarmer marketing organizations to increase marketing scale and lower cost; (d) strengthenmarket information network; and (e) improve post-harvest handling, including sorting-grading.

3.18 Municipal governments established a Guidance Price Policy in 1994 in reactionto rapid and large food price increases and to prevent retail "price gouging." This policy,

- 14 -

enforced by municipal and district price bureaus and departments, established maximumretailer margins and applied to 13 selected vegetables, but were often exempted duringseasonal production periods. Guidance prices are based on the wholesale price; thus;

if the wholesale price is: maximum permissible margin is:Y 1.00 or more perjin (in = 0.5 kg) 50 percentY 0.70-1.00 perjin 40 percentY 0.70 or less per jin 30 percent

Guidance prices apply to: Chinese cabbage, round cabbage, cucumber, celery, eggplant,sweet (green) pepper, tomato, spinach, greens, lentil, potato, radish, and white gourd.The Municipal/District Price and Industrial Commerce Bureaus monitor retail prices andif the price exceeds the guidance level, the retailer is subject to a fine. It is doubtful thatthis policy has been effective in curtailing price increases.

Cabbage Policy

3.19 Cabbage receives individual policy attention by municipal governments. Whenfarmers agree to participate in the Vegetable Basket-Vegetable Production Baseprograms, they also agree to plant a specified amount, or proportion, of their land tocabbage in the autumn production cycle. The cabbage requirement ranges from one-fourth to one-third of the vegetable base, except farmers are exempted from thisrequirement if their land is under protected production (greenhouses and plastic tunnels).NMunicipal programs tend to fall into two categories: (a) the municipality agrees to buy aminimum quantity at a minimum price and sells, through state shops, to consumers atprices not to exceed a specified maximum [Beijing requires 80,000 mu of cabbage beplanted, agrees to purchase 100,000 tons at Y 0.16/kg, injects a Y 0.0684/kg handlingsubsidy and sells at prices not to exceed Y 0.26/kg. Parallel sales occur in the freemarkets, and retail prices were maintained below Y 0.26 in 1994]; and (b) themunicipality specifies only the cabbage area, may or may not provide a cash subsidy on amu basis, and lets the market determine prices [Kunming requires that cabbage be plantedin 25 percent of the autumn-planted vegetable base, and provides a Y 100/mu cashsubsidy].

C. MARKET INFORMATION

3.20 Market information in China has historically been gathered as inputs forgovernment policy decisions (a chief concern is vegetable price inflation), ratherthan utilized to assist in the more efficient operation of markets. Fruit and vegetablemarket information systems are still in their infancy and several different marketinformation systems are in effect. The MOA Information Center maintains the widestnetwork and assembles information from: (a) within the Ministry; (b) wholesale marketsunder MOA management/ownership; (c) other ministries and bureaus; and (d) cities/municipalities. The Information Center is responsible for primary analysis anddistribution. Summaries are published in the Economic Daily newspaper, radio andtelevision networks, and disseminated to 42 major wholesale markets, 35 cities/

- 15 -

municipalities and 800 subscribers, on a nonpaying basis. The Ministry of Internal Trade(MIT) Information Center undertakes similar but independent data collection, analyses,and dissemination.

3.21 SSB assembles information from various ministries, bureaus, provinces andmunicipalities and is the source of official marketing statistics. The Price Bureaumonitors and records price information (but not volume data) in the retail markets, whichalso is transmitted to MOA and MIT Information Centers. This information, collecteddaily, is consolidated into monthly averages, which limits its analytical value as much ofthe price volatility is moderated in the averaging process.

3.22 Major wholesale markets maintain a market information office and publish daily(or weekly) market reports for local media and subscribers. Detailed price (daily average,minimum, and maximum), quantity, value, and variety information are maintained by thewholesale markets as they are the basis for market fees and taxes. But only the price andvariety information is evaluated and published. Quantity information is valuable anduseful in analyzing prices and price changes and should be distributed along with theprice data to assist market participants to make better-informed decisions. To improvethe efficiency of production and marketing decisions, the "data base" orientation ofprevailing market information systems must be expanded to include information fromsources other than wholesale markets. This would include crop reporting on fruits andvegetables currently undertaken on grains to provide qualitative assessment of productionconditions and probable marketings. The regular reporting of farmers' planting intentionsand actual plantings of specific vegetable varieties are indicators of future marketsupplies and permit farmers to adjust their production mix to incorporate varieties likelyto be in short supply. This becomes more important as consumers' income andconsumption of nontraditional vegetables increase. Also, reports on fruits in storagewould provide further information on potential marketings.

-16-

4. MARKET STRUCTURE

4.1 Between 1978 and 1994, the total number of rural free markets doubled and urbanfree markets increased from zero to 17,880. Growth in free-market sales (real value) wasremarkable, increasing at an annual rate of 18 percent, reaching Y 900 billion in 1994-about one-half of which were food items. Annex Table A3.1 indicates the rapid growthin the traded value (current and constant terms) of major agricultural commodity groupsfrom 1978 to 1994.

4.2 Growth in quantity marketed TABLE 4.1: FREE-MARKET SALES VOLUME

(through free markets) was equallyremarkable (Annex Table A3.2). Table 1988 1994 Growth Rate

4.1 summarizes the sales volume and (million tons) (percent)growth rate between 1988 and 1994 for Grain 7.07 22.35 23grain, fruits, and vegetables. The sales Fruit 9.54 26.32 19

volume of vegetables is three times that Vegetables 26.51 64.10 17

of grain and double that of fruits; theannual growth rate was 17 to 23 percent for the various commodities.

4.3 The physical volume of grain sold through free markets remains a relatively smallproportion of total sales and consumption, reflecting Government's continued desire tocontrol grain marketing. However, the volume of fruits and vegetables sold through freemarkets, coupled with sales by farmers to nonagricultural residents and on-farmconsumption, is a very high proportion of production and consumption.

4.4 Since the mid-1980s, fruit and vegetable marketing has become increasinglyliberalized and pure competition conditions are generally met in all marketing stages. Aportion of the competition derives from nonprivate-market participants and in isolatedareas, where traded volumes are small, either municipal government or private-sectormarket dominance may exist. Municipal governments own, manage, and/or supervisemany market facilities, but active market intervention is limited primarily to establishingretail guidance prices and does not impact on market competitiveness.

4.5 Each municipality has its own structure of vegetable market ownership. Butregardless of the structure, a common element is a rapid increase in the proportion ofsales through free markets. Between the mid-1980s and mid-1990s the vegetablemarketing structure in Beijing changed from 220 state retail shops to 60 wholesalemarkets and 90,000 individual retail sellers and vendors-although 143 of the state shopsremain. Various estimates suggest that countrywide, 80 to 90 percent of retail fruit andvegetable sales are through private outlets at market-determined prices. Similarly, 75 to80 percent of nationwide wholesale fruit and vegetable sales are estimated to be throughfacilities managed by nongovernment entities.

- 17 -

A. THE MARKETING CHAIN

Producer Marketing

4.6 Small farmers sell an estimated 50 percent of their produce to traders at thefarmgate. The Government encourages direct retail sales by farmers and those locatednear urban centers often sell an estimated 25 percent of their produce in this manner.Other marketing arrangements include: direct wholesale marketing without use of traderintermediaries; and direct farm sales to institutions (this applies to very high-qualityproduce and consists of both spot and short-term contract sales). There is no evidence ofvegetable farmer marketing associations/cooperatives although some farmers jointlytransport their vegetables to the market; however, villagers often collectively marketfruit.

4.7 Successful farmer marketing cooperatives obligate individual participants to forgosome of their independence and rely on business-oriented managers for efficientmarketing decisions (i.e., to enable farmers to receive a larger share of consumers'expenditures). The establishment of such cooperatives often requires governmentassistance in organizing, advising leadership, and providing some infrastructure.However, it is crucially important for management to be farmer-controlled as thefundamental objective is to increase farmer member incomes, an objective that is dilutedby government-controlled cooperatives that are influenced by consumer as well asproducer interests.

Wholesale Marketing

4.8 There are approximately 2,100 fruit and vegetable wholesale markets nationwidethat fall into four management-supervision categories. The Ministry (Bureau) ofAgriculture typically manages wholesale markets in production areas where produce isassembled for shipment to consumption areas. Urban wholesale markets are largelymanaged and supervised by Departments within either (a) the Ministry of Internal Trade,or (b) the Municipality (Industry and Commerce Bureau). The final category is thecollective wholesale market, which includes village and farmer collectives, and groups oflocal entrepreneurs. Many of these markets have evolved from farmers' free marketsestablished early in the liberalization period and comprise some of the largest volumemarkets.

4.9 Wholesale market facilities vary widely. Some are open-air, in crowdedcongested areas with no display space, others are spacious open-air markets with samplesdisplayed alongside parked trucks, others are covered areas (floor and roof without walls)with display space and sorting/grading facilities, and still others include enclosedmultistory buildings with managerial, financial, and information offices with spaceavailable for storage. However, wholesale markets have neither integral cold storagefacilities, loading/unloading platforms, nor mechanical handling equipment.

4.10 Large cities have numerous wholesale markets that compete against each other assellers and buyers patronize the market of their choice. Wholesale markets vary in sizewith 500 or more sellers offering up to 5,000 tons per day in the larger markets. Traders

- 18-

from other provinces tend to patronize these larger markets. Smaller "neighborhood"wholesale markets handle more locally grown produce and individually handle smallervolumes than do the larger markets; although collectively they handle about 50 percent ofthe marketed produce. Market proximity is an important selection criterion for farmers aswell as retailers and institutional buyers.

4.11 There are wholesale markets in surplus production areas (counties) throughoutChina, some of which are quite large (Shouguang, Shandong). Buyers in these largermarkets represent both companies and individuals, and include state organizations,private trading organizations, institutions (schools, hospitals, hotels, military units, etc.),traders, and farmers. Traders purchasing produce for sale in deficit vegetable areas oftenbuy on a graded basis (i.e., they sort the vegetables in the market and buy only the itemsthat meet their quality criteria). Some marketing firms have horizontally integrated bystationing representatives in several producer wholesale markets to procure specificquantities and qualities of various produce for shipment and sale in various urbanwholesale markets. All of these representatives (agents) are in daily contact with theirprincipals and add their own knowledge to publicly available information, permitting theprincipal to direct specific procurement requests to the market agent that can make the"best buy."

Retailing is Overwhelmingly Small Scale, Private, and Highly Competitive

4.12 The bulk of retail sales are through vendors in temporary street markets (open foronly 2 to 3 hours in the early morning or late afternoon), or in semipermanent markets,with individual stalls open throughout most of the day. Only a small volume of retailtransactions occur in permanent structures such as supermarkets and convenience stores.Retailer vendors purchase their daily supplies from wholesalers and transport it to theretail site utilizing bicycles, tricycles and carts, and join farmer retailers who similarlytransport their own produce to market. Daily transactions of individual vendors, whotypically specialize in one group of commodities, fall within a 50 to 100 kg range.

4.13 Although some grading is undertaken in wholesale markets, a large portion of theproduce remains ungraded until it reaches the retailer. Retailers grade the material anddifferentiate prices for the various qualities. Also, vendors lower their prices near the endof the day as they have limited provision for overnight storage. Despite strongcompetition, retail margins are relatively high because operations are small-scale andphysical losses (costs) are high.

4.14 Several entrepreneurs propose to expand prepackaged fruit and vegetable sales inconvenience stores and supermarkets. However, there is no research indicating Chineseconsumers prefer prepackaging over self-select bins, which is practiced in most ofChina's retail markets and in retail outlets of most countries. Luxury supermarkets sellprepackaged fruit and vegetables but the clientele is predominately expatriate.Introducing prepackaged fresh vegetables designed for domestic consumers, withoutmarket research supporting this preference, could be a costly mistake.

- 19 -

Institutional Procurement

4.15 Institutions (academic institutions, hospitals, restaurants, hotels, military, somesupermarkets, etc.) employ three procurement methods: (a) self-procurement at thewholesale market; (b) daily order placement with specialized vendors late the previousevening or early in the morning, with mid-morning delivery; and (c) small volumesthrough direct purchase from suburban producers of fine vegetables. The latter twoarrangements involve excellent quality produce and require cleaning and pregrading-orthe institution (supermarket) will grade and return the cull material. The vendor typicallyfinances these transactions with weekly, biweekly, or monthly settlement.

Export Marketing

4.16 Fruit and vegetable exports total some 3.5 million tons ($3.0 billion), which is aminor proportion of production. Hong Kong and Japan are the destinations of most of theexports. It appears that exports to Japan are demand-driven. Japanese importers visitChina to identify potential sources of supply for specific high-quality vegetables. Jointventures are often formed with State Farm suppliers to produce specific varieties. About25 percent of requirements are contracted and the remaining 75 percent are spot procuredat the farmgate or wholesale market. When contracted, the importer prefinances a portionof the production costs. Also, the importer monitors production development, specifiesharvest date, arranges for delivery of standard or refrigerated containers (as required) tothe production area, and overland and sea transport. Farmers are paid cash for washed,cleaned, and graded vegetables that are packaged in 10 kg boxes and packed in containersin the field.

Processing

4.17 Although Chinese consumers eat a small amount of pickled and dried food items,most fruits and vegetables are consumed fresh. Few, if any, vegetables are producedspecifically for processing and no specific market channels apply to vegetables forprocessing. A small amount of vegetables are dehydrated, primarily for export. Butprocessors dehydrate "on demand"; they do not maintain stocks of dried vegetables butprocess only following receipt of an export order with spot purchase of raw material fromfarmers or in the wholesale market. Fruit juices are widely canned and consumed, butcanned fruits and vegetables are not an important element of the diet. A very smallfrozen fruit and vegetable market exists for institutions (hotels, etc.) and affluentconsumers who patronize supermarkets. Until frozen fruits and vegetables become morecompetitively priced and Chinese households increase their freezer-refrigeration capacity,frozen fruit and vegetable production and consumption will remain unimportant.

B. POST-HARVEST HANDLING AND QUALITY CONTROL

4.18 Historically, Chinese agricultural research addressed grain, vegetable oilseed, andcotton production issues; only recently has Government broadened its focus to providemodest attention to fruits and vegetables. However, production issues remain the locus ofconcern with no structured research addressing post-harvest losses of fruits and

- 20 -

vegetables. Post-harvest loss information is available only in the form of anecdotalobservations, estimates, and educated guesses.

4.19 Field handling following harvesting has a major impact on the quality of producethat enters the market channels. Most farmers have no knowledge of standardizing-grading (sizing, coloring, blemishes and bruise damage, etc.); thus, farm-level sorting islimited to the removal of physically damaged items. Also, field heat remains in theproduce as farmers practice neither mechanical nor water cooling. (Some vacuumcooling is applied to produce destined for export.)

4.20 Packing/packaging. Although fruits are packed in cardboard boxes of 10 to20 kg, vegetables are typically "overpacked" in bags, baskets, or other nonrigidcontainers and are "overstacked" on trucks, in storage, and in the market, causing severebruising and compression damage, leading to physical losses and quality deterioration.Some semiperishable vegetables such as onions, carrots, and potatoes can withstand suchtreatment, but most cannot. The use of sturdy, rigid packing containers would eliminatemuch of this problem. Also, the absence of mechanical handling equipment at markettransfer points results in rough manhandling and further quantity and quality losses. Bothvegetables and fruits are hand stacked, loaded and unloaded-palletizing and mechanicalhandling (including conveyors) is not practiced. An exception is export produce, whichis placed in freight containers after cleaning and grading at the production center (para.4.16). The further downstream these losses occur, the greater the cost as considerabletransportation and handling costs are incurred on the entire volume of produce.

4.21 In addition to precooling, rigid packaging, and mechanical handling, there areother marketing practices and handling technologies that would improve or maintainquality and value. But their application may be inefficient for lower-value produce as themarginal cost of improved handling may be greater than the marginal benefits ofincreased quantity and quality and greater than the marginal cost of incrementalproduction. These include:

Practice/technology Impact

Farm-level cleaning, Washing, standardizing produce by size and color and removing blemishedgrading, and sorting items to improve quality and value.

Cold storage Maintain quality and extend availability of seasonal production throughrefrigeration [more sophisticated controlled atmospheric storage refrigerates aninert gas environment (oxygen removed), but is unused in China].

Waxing Polishes fruit, leaving it with an attractive finish and reduces the respirationrate of fruit, thus extending its storage life. [vegetable waxing would beapplicable only to varieties with very high value.]

Based on subjective evaluation, post-harvest losses constitute a significant inefficiency inmarketing and largely accounts for the wide price spreads for fruits and vegetablesbetween farmer and consumer.

- 21 -

4.22 There is no general cold chain system for fruits and vegetables, although there areindividual operators of cold storage facilities and refrigerated transport. The availablerefrigerated storage facilities are used primarily for meat and fish and secondarily forfruit, but rarely for vegetables. There are several manufacturers of insulated andrefrigerated trucks, but they are used primarily for higher-value processed and preparedfoods. Railroads have semirefrigerated rail cars but they are rarely, if ever, used forvegetables. Also, with the exception of up-scale supermarkets and some conveniencestores, there is no retail-level refrigeration; street vendlors are obliged to sell their stockthe same day it is brought to market, particularly during summer months.

4.23 Fruits are often placed in cold storage for several months but with few exceptions(e.g., green garlic) vegetables are not. There are several reasons why refrigerated storageof vegetables is not more widely practiced: (a) the value of most vegetables is lowrelative to fruits-and to the refrigerated storage costs; (b) the storability of mostvegetables is relatively short (compared to fruits), even under refrigerated conditions[cold storage can extend the seasonal availability of vegetables only briefly]; and (c) thepricing of refrigerated storage is unattractive to relatively small volumes and rapidturnover. Owners of cold storage facilities have not learned how to merchandise theirservice by customizing it to meet the needs of different potential customers. Cold storagerental is typically based on individual rooms with minimum capacity of 100 tons for aone-month minimum period. A vegetable trader more typically requires 24 to 48 hourstorage for only a few tons. Therefore, cold storage operators should consider alternativepricing schedules (i.e., 24 hours, one week, etc.) and alternative space rental (i.e.,provision for renting space by the cubic meter as well as by the "room").

Agricultural Market Research and Extension

4.24 Horticultural research must expand beyond production issues to include marketresearch, quality maintenance, and post-harvest handling (field cooling, packaging,transporting, storage, etc.). The development of grades and standards should be a priorityelement of market research. This would permit prices and qualities to be better relatedand could be integrated into the market information network. In the absence of rigorousanalysis of post-harvest losses using alternative packaging materials, transport, andstorage modes, there is considerable uncertainty regarding which post-harvest _cLmologyto employ to reduce marketing costs. Market research information should be integratedinto extension programs just as production research is currently extended.

Infrastructure and Marketing Efficiency

Transportation

4.25 Various types of vehicles are used locally to transport fruits and vegetables fromfarm to market and local transport does not appear to be a marketing constraint.Similarly, truck transportation between production and nearby consuming areas (e.g.,Shouguang to Beijing) also appears sufficient. In several instances, as part of the"vegetable basket" program, municipal governments have provided subsidized transport

- 22 -

loans to families/groups to encourage fruit and vegetable transport. However, vehiclesused for fruit and vegetable transport are predominantly uninsulated and nonrefrigerated.The exception appears to be vendors who provide high-quality produce to institutionalcustomers (hotels, etc.). A priori, insulated or refrigerated truck transport would appearto be efficient; but since they are rarely used, they are apparently perceived to beinefficient.

4.26 Transcountry transport infrastructure is an important limiting factor to improvingmarketing efficiency and reducing post harvest losses. Transport infrastructure growthhas not been commensurate with the rapid growth of the economy and the need to moveincreasing volumes of freight. Road networks are inadequately developed to facilitaterapid movement over long distances and backhaul opportunities have not developed.Some firms are developing plans to move fruits and vegetables long distances byrefrigerated truck (Kunming to Shanghai), but economic viability requires commoditybackhauling.

4.27 Rail transport would appear to be a solution to fruit and vegetable transport, butuncontrolled temperatures and lengthy transit times limit usage to semiperishablecommodities such as onions, potatoes, etc. Refrigerated containers are used in exportingvegetables and facilitating intermodal transport of fruits and vegetables. However, thevalue of most vegetables is too low to absorb the cost of refrigerated container handling.

4.28 Small quantities of perishable vegetables are packed in insulated boxes (withfrozen thermal containers) and shipped medium distances by rail. These shipments aremade as high-cost, accompanied personal effects but are more rapid than typical railfreight shipments. Wastage is alleged to be less than 5 percent for these shipments. Thespeed and minimal loss makes this a viable transport option for some relatively high-value products. Similarly, air cargo is used for some fruit, vegetable, and flowershipments to a few Southeast Asian countries. However, the high cost prohibits domesticuse except for high-value, off-season produce and specialty items for some institutionalusers.

- 23 -

5. MARKET PERFORMANCE

A. OPERATIONAL AND ALLOCATIVE EFFICIENCY

5.1 The Chinese Government, like governments elsewhere, intervenes indirectly inthe vegetable market by supporting research on horticultural production, new seed varietydevelopment, improved agronomic practices, etc., in efforts to expand vegetable supplies(shift supply function outward). In addition, China's municipalities have provided cash,infrastructure, investment, and input subsidies to vegetable producers. These subsidieshiave: (a) intensified supply expansion; and (b) limited (but not eliminated) consumerprice increases.

5.2 While these interventions distort resource use at the production level, subsequentprices in the marketing chain are basically left to market forces-except for retailguidance prices, which are perceived to be relatively ineffective. Evaluation of marketprices suggests they are generally competitively determined, but are not necessarilyefficient. This potential inefficiency applies to both wholesale and retail leveltransactions.

5.3 Wholesale markets are certainly competitive. The large number of marketplacesand participants that compete for business ensures that transfer prices are competitivelydetermined. But without competitive systems that would provide an alternative methodof moving vegetables from producers to consumers, it is difficult to conclude that thewholesale marketing system is efficient.

5.4 In some large cities (Shanghai), distribution centers have replaced some wholesalemarkets in providing nonperishable products to convenience stores-and are beginning tohandle some perishable products such as vegetables. This should be encouraged asdistribution centers are likely to be more efficient and have external benefits, includingreduced traffic. The variety, quality and amount of vegetable exports are such a smallproportion of production that they constitute a niche market rather than competition.Institutional procurement (large enterprises, military, schools/universities, hotels, etc.) isa small but important component of vegetable demand, which might be more efficientlyhandled through farmer-buyer contracts that could be based on wholesale market pricesbut would benefit by physically bypassing the wholesale market. Although efficient,contracting is unlikely to develop until cooperative farmer marketing associationsdevelop that can consolidate, soIt, and grade farm produce and demonstrate the capacityto organize vegetable supplies on a regular and recurring basis. Auctioning is potentiallyan efficient marketing mode but cannot be practiced without defined grades and standardsto permit sample inspection and selling.

- 24 -

5.5 The retail vegetable market also is highly competitive as demonstrated by theestimated 90,000 Beijing retailers. But, given the large number of retailers and Beijing'sdaily vegetable requirements, each retailer handles only 100 to 150 kg per day; thus,"acceptable" incomes can be generated only with high margins. Therefore, while theretail market also is competitive, it also is not particularly efficient. Efficiency lies inretailer/vendors handling a larger volume with reduced unit margins to enable them toenjoy "reasonable" profits/incomes while providing consumers with lower-pricedproduce. The high-volume, low-margin structure prevails in many other countries.

5.6 Retailer associations that would facilitate large-volume procurement, and perhapsbypass one or more marketing stages, have not developed, but could be an efficientstructure. Although some trading organizations appear to be horizontally integrated withmarket agents widely dispersed in many wholesale markets, vertically integratedmarketing organizations that would perform several marketing functions have notdeveloped except for a few State Farms, which have integrated production with somemarketing activities. An innovative retailing experiment is underway involving itinerantvending whereby insulated vans enter residential areas and stay for a brief period to sellfresh produce prior to moving to another residential area. This practice is too recent toevaluate its efficiency.

Seasonality of Vegetable Marketing

5.7 The seasonality of vegetable production and marketing differs widely between thevarious climatic areas. Subsidized investments and inputs have led to substantialincreases in "protected production" of winter vegetables. Separate statistics ofgreenhouse-tunnel production are not maintained but anecdotal evidence suggests veryrapid increases during the last three to four years. Notwithstanding large increases in off-season production, a notable seasonality applies to vegetable prices and marketedvolumes. There has been remarkably little change in seasonal sales distribution ofvegetables in Beijing over the past decade. Monthly vegetable marketings are bimodal,with a modest peak in late spring-early summer (June and July) and another sharp peak inNovember. The large volume of cabbage marketed in November and stored for winterconsumption distorts the picture of overall vegetable availability. The monthly salesvolumes for 1984 and 1994, as a proportion of annual sales, are indicated in Figure 5.1.Seasonal price indices better reflect, in a countercyclical manner, the availability ofvegetables (when prices are high, availability is low and vice versa).