Embed Size (px)

Citation preview

2015Enforcement

Report

Protecting Investors and Supporting

Healthy Capital Markets Across Canada

2015 ENFORCEMENT REPORT

TAB

LE O

F C

ON

TEN

TS

About IIROC 1

Message from CEO and Vice President, Enforcement 2

The Role of Enforcement 3

IIROC’s Enforcement Process 4

Enforcement Priorities and Themes 6

Selected Case Highlights 8

Key Policy Initiatives and Developments 17

Enforcement Statistics 20

Appendix A – IIROC Disciplinary Actions 26

Appendix B – Enforcement Information Sources 28

Appendix C – Types of Disciplinary Proceedings 29

Glossary of Terms 30

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 1

The Investment Industry Regulatory Organization of Canada

(IIROC) is the national, self-regulatory organization (SRO)

responsible for the oversight of Canada’s investment dealers,

as well as trading activities on debt and equity marketplaces

in Canada.

IIROC is one part of the Canadian securities regulatory

framework, that consists of 10 provincial and three territorial

securities regulators (collectively the Canadian Securities

Administrators [CSA]), as well as three SROs, IIROC, the

Mutual Fund Dealers Association (MFDA) and La Chambre

de la sécurité financière, whose activities are overseen by

CSA members.

IIROC’s regulatory mandate is to set and enforce high-

quality regulatory and investment industry standards, protect

investors and strengthen market integrity while supporting

healthy capital markets. IIROC pursues this mandate by

developing, testing for compliance with and enforcing a

broad spectrum of member and market proficiency, conduct

and prudential rules.

All investment dealers (also referred to as Dealer Members)

and Canadian marketplaces overseen by IIROC are subject to

a rigorous regulatory approval process. Individuals wanting to

work at IIROC-regulated firms in specific roles (for example,

client-facing advisors and individuals in a supervisory role

who have responsibility for ensuring compliance with IIROC

rules and other applicable regulations) must apply to IIROC

for approval. Individual applicants must satisfy all of IIROC’s

proficiency requirements and be assessed to be “fit and

proper” before IIROC will approve them to work at a Dealer

Member in these types of roles. They must also invest in their

professional development by completing a minimum number

of continuing education requirements over the course of a

three-year continuing education cycle.

IIROC’s vision is to be known for its integrity, transparency,

fairness and balance. IIROC aims for excellence and regulatory

best practices. Its actions are driven by sound, intelligent

deliberation and consultation.

AB

OU

T II

RO

C

2015 ENFORCEMENT REPORT2

We are pleased to present IIROC’s 2015 Enforcement Report, providing an overview of our efforts to protect investors through fair, effective and timely enforcement of our rules.

IIROC sets high professional and ethical standards and enforces rules regarding the proficiency, business and financial conduct of IIROC-regulated firms and their staff, as well as market integrity rules, all of which ensure that Canada’s capital markets operate in a fair and orderly manner.

We are committed to investigating complaints and taking action against those who have failed to meet their regulatory obligations, as you will see from the cases highlighted in this report. In addition, we place great emphasis on the importance of firm compliance and in particular its supervisory responsibilities. In every case, we review the adequacy of firm supervision and hold firms accountable where warranted. We take action where there is a failure to address significant compliance findings or clear failure to demonstrate an effective and strong compliance system.

In 2015, we completed 124 investigations nationally, a material portion of which focused on supervision conducted by firms and individual supervisors. Of particular note are the extraordinary steps taken against Jacob Securities Inc. which was suspended due to the risk of imminent harm resulting from the firm’s serious and systemic compliance deficiencies.

We also would like to thank our regulatory partners at the CSA and other regulatory and law enforcement authorities, with whom we work to provide a comprehensive framework to protect Canadian investors. IIROC has in place more than a dozen formal agreements with our partners in Canada and abroad, which we are working to strengthen and extend to other organizations.

For example, this past year IIROC signed a Memorandum of Understanding with La Chambre de la sécurité financière in Quebec to enhance oversight by coordinating our enforcement

actions. We are negotiating similar agreements with other organizations to enable greater efficiency and consistency of the public interest supervisory system.

While we can take pride in these accomplishments, we also know that with better tools, we can and must do better. Two additional tools we are seeking are the ability to enforce decisions through the courts and immunity for good faith regulatory actions.

IIROC regularly collects fines levied against firms that have broken its rules, but over the years, our national collection rate for fines owed by individuals is less than 20 per cent. It is true that sometimes these individuals have no assets, but some disciplined individuals evade payment by simply ceasing to be IIROC registrants. This is unacceptable, as it undermines the disciplinary process. Investors must be confident that firms and individuals are complying with the rules and that any breach of these rules will result in real consequences.

The Governments of Alberta and Quebec have taken action to address this regulatory gap through legislative amendments that give IIROC the power to enforce disciplinary decisions through the courts. Unsurprisingly, annual collection rates in those two provinces usually exceed the national rate. We thank these governments for their action.

IIROC is actively encouraging other provincial and territorial governments to adopt similar legislative measures, so that IIROC can provide a consistent level of protection to all investors across Canada. This would foster investor confidence in our markets and the regulatory system that is their underpinning, and it would do so at no material cost to governments or taxpayers.

IIROC carries out its regulatory activities under the authority of either the provisions of securities legislation or recognition orders issued by Canadian securities regulators. If these securities administrators were to carry out these regulatory M

ESSA

GE

FRO

M T

HE

CEO

&

VIC

E PR

ESID

ENT,

EN

FOR

CEM

ENT

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 3

THE

RO

LE

OF

ENFO

RC

EMEN

T

duties directly, they and their staff would be protected by legislation which provides immunity for acts done in good faith in the performance of any duty or exercise of power under securities law.

Even though these regulatory responsibilities are delegated to IIROC by the securities administrators, these legal protections do not apply to IIROC. As a result, IIROC’s Board and its staff, as well as our disciplinary hearing panels, are exposed to potential legal action, based on regulatory actions taken or powers exercised in good faith as part of IIROC’s public interest mandate.

So another tool IIROC needs to more effectively protect the investing public is immunity provisions in securities legislation for the performance of the regulatory responsibilities assigned to us. This would allow IIROC to act in the public interest, without fear of lawsuits related to its regulatory role.

We believe it is vital that IIROC has the tools necessary to vigorously and effectively protect the public and we ask that you consider supporting our call for legislative reform as you read about the enforcement activities contained in this report.

Andrew J. KrieglerPresident & CEO

Elsa RenzellaVice President, Enforcement

IIROC’s Enforcement Department (Enforcement) is responsible for the enforcement of IIROC’s Dealer Member rules, relating to the sales, business and financial conduct of its Dealer Members and their registered employees, as well as the Universal Market Integrity Rules (UMIR) relating to the trading activity on all Canadian equity marketplaces.

Enforcement plays a key role in IIROC’s efforts to protect investors and support healthy capital markets across Canada. Enforcement works with IIROC’s other departments (including Complaints and Inquiries, the various compliance groups, Trading Review & Analysis, and Registration) to ensure timely identification, investigation and prosecution of regulatory misconduct, as well as the detection and pre-emptive disruption of potential misconduct.

Enforcement must be:

FAIR

IIROC’s enforcement process is fair and impartial. Prosecutions are based on thorough investigations; hearings are transparent and conducted by impartial hearing panels, chaired by legal professionals.

EFFECTIVE

Enforcement aims to promote compliance within the investment industry by sending strong regulatory messages that deter potential wrongdoers and help to build investor confidence in the Canadian capital markets.

TIMELY

Timely investigation and prosecution of misconduct protects investors and strengthens the public’s confidence in self-regulation.

2015 ENFORCEMENT REPORT4

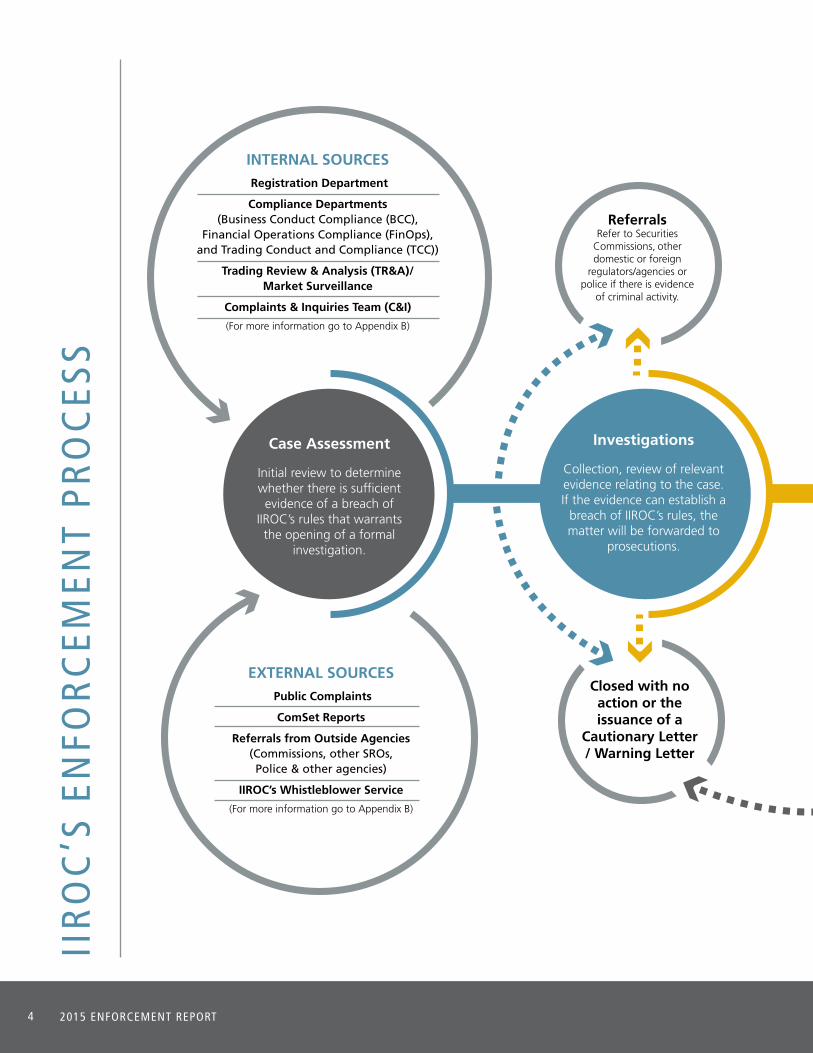

Case Assessment

Initial review to determine whether there is sufficient evidence of a breach of

IIROC’s rules that warrants the opening of a formal

investigation.

Investigations

Collection, review of relevant evidence relating to the case. If the evidence can establish a

breach of IIROC’s rules, the matter will be forwarded to

prosecutions.

EXTERNAL SOURCES

Public Complaints

ComSet Reports

Referrals from Outside Agencies (Commissions, other SROs, Police & other agencies)

IIROC’s Whistleblower Service

(For more information go to Appendix B)

Closed with no action or the issuance of a

Cautionary Letter / Warning Letter

ReferralsRefer to Securities

Commissions, other domestic or foreign

regulators/agencies or police if there is evidence

of criminal activity.

INTERNAL SOURCES

Registration Department

Compliance Departments (Business Conduct Compliance (BCC),

Financial Operations Compliance (FinOps), and Trading Conduct and Compliance (TCC))

Trading Review & Analysis (TR&A)/ Market Surveillance

Complaints & Inquiries Team (C&I)

(For more information go to Appendix B)

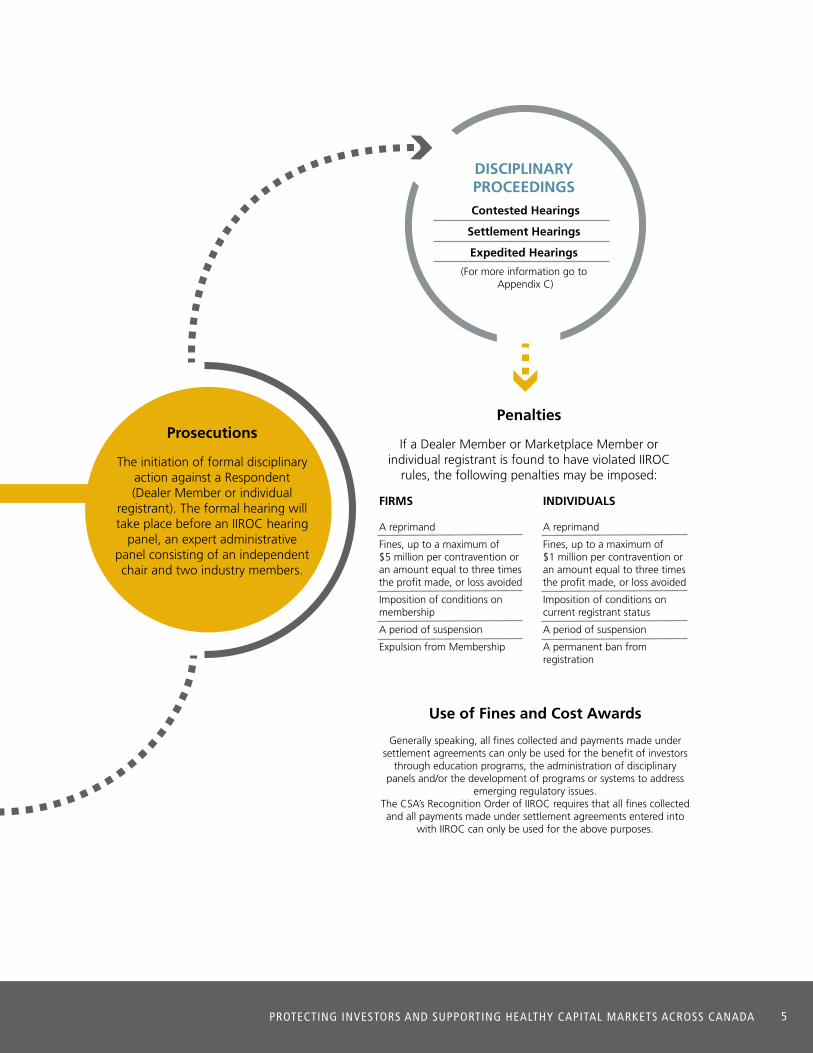

DISCIPLINARY PROCEEDINGS

Contested Hearings

Settlement Hearings

Expedited Hearings

(For more information go to Appendix C)

Prosecutions

The initiation of formal disciplinary action against a Respondent (Dealer Member or individual

registrant). The formal hearing will take place before an IIROC hearing

panel, an expert administrative panel consisting of an independent chair and two industry members.

Penalties

If a Dealer Member or Marketplace Member or individual registrant is found to have violated IIROC

rules, the following penalties may be imposed:

FIRMS

A reprimand

Fines, up to a maximum of $5 million per contravention or an amount equal to three times the profit made, or loss avoided

Imposition of conditions on membership

A period of suspension

Expulsion from Membership

INDIVIDUALS

A reprimand

Fines, up to a maximum of $1 million per contravention or an amount equal to three times the profit made, or loss avoided

Imposition of conditions on current registrant status

A period of suspension

A permanent ban from registration

Use of Fines and Cost Awards

Generally speaking, all fines collected and payments made under settlement agreements can only be used for the benefit of investors

through education programs, the administration of disciplinary panels and/or the development of programs or systems to address

emerging regulatory issues. The CSA’s Recognition Order of IIROC requires that all fines collected and all payments made under settlement agreements entered into

with IIROC can only be used for the above purposes.

IIR

OC

’S E

NFO

RC

EMEN

T PR

OC

ESS

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 5

Case Assessment

Initial review to determine whether there is sufficient evidence of a breach of

IIROC’s rules that warrants the opening of a formal

investigation.

Investigations

Collection, review of relevant evidence relating to the case. If the evidence can establish a

breach of IIROC’s rules, the matter will be forwarded to

prosecutions.

EXTERNAL SOURCES

Public Complaints

ComSet Reports

Referrals from Outside Agencies (Commissions, other SROs, Police & other agencies)

IIROC’s Whistleblower Service

(For more information go to Appendix B)

Closed with no action or the issuance of a

Cautionary Letter / Warning Letter

ReferralsRefer to Securities

Commissions, other domestic or foreign

regulators/agencies or police if there is evidence

of criminal activity.

INTERNAL SOURCES

Registration Department

Compliance Departments (Business Conduct Compliance (BCC),

Financial Operations Compliance (FinOps), and Trading Conduct and Compliance (TCC))

Trading Review & Analysis (TR&A)/ Market Surveillance

Complaints & Inquiries Team (C&I)

(For more information go to Appendix B)

DISCIPLINARY PROCEEDINGS

Contested Hearings

Settlement Hearings

Expedited Hearings

(For more information go to Appendix C)

Prosecutions

The initiation of formal disciplinary action against a Respondent (Dealer Member or individual

registrant). The formal hearing will take place before an IIROC hearing

panel, an expert administrative panel consisting of an independent chair and two industry members.

Penalties

If a Dealer Member or Marketplace Member or individual registrant is found to have violated IIROC

rules, the following penalties may be imposed:

FIRMS

A reprimand

Fines, up to a maximum of $5 million per contravention or an amount equal to three times the profit made, or loss avoided

Imposition of conditions on membership

A period of suspension

Expulsion from Membership

INDIVIDUALS

A reprimand

Fines, up to a maximum of $1 million per contravention or an amount equal to three times the profit made, or loss avoided

Imposition of conditions on current registrant status

A period of suspension

A permanent ban from registration

Use of Fines and Cost Awards

Generally speaking, all fines collected and payments made under settlement agreements can only be used for the benefit of investors

through education programs, the administration of disciplinary panels and/or the development of programs or systems to address

emerging regulatory issues. The CSA’s Recognition Order of IIROC requires that all fines collected and all payments made under settlement agreements entered into

with IIROC can only be used for the above purposes.

2015 ENFORCEMENT REPORT6

Enforcement remains committed to IIROC’s goal of investor protection and the promotion of healthy capital

markets by maintaining a strong focus on:

• the protection of seniors and vulnerable investors;

• unsuitable investment recommendations;

• fi rms’ supervision of trading and retail operations; and

• manipulative and deceptive trading.

In 2015, a significant number of Enforcement cases focused on suitability issues. Consistent with past years,

suitability represented over one-third of complaints reviewed by IIROC. Almost 50 per cent of prosecutions

against individual registrants involved violations of suitability, once again making it IIROC’s top matter

prosecuted for the year.

This year also highlighted the susceptibility of seniors and vulnerable clients to unsuitable

recommendations. In all but a few, this year’s suitability cases involved elderly and/or vulnerable clients.

Many of our suitability cases displayed common themes of excessive trading and/or improper use of margin

for clients who were not advised of or did not understand the risks.

Enforcement also prosecuted cases dealing with conflicts of interest, an issue that has become an

increasingly important regulatory concern. Conflict of interest was one of the key areas of regulatory

priority for IIROC highlighted in its 2015 Annual Consolidated Compliance Report. Rules relating to the

management of specific conflicts of interest are already in place. While there are various provisions in IIROC

Rules that relate to specific conflict of interest situations, Rule 42 expressly sets out the existing obligations

on managing conflicts of interest with clients which includes consideration of the best interest of clients.

This year, IIROC conducted its first prosecution under Rule 42 against Mackie Research Capital Corporation.

Enforcement also took action on several occasions against individual registrants who engaged in conduct

unbecoming by failing to act honestly and in good faith. These cases, involving misappropriation or misuse

of client funds, forgery of documentation and false statements, demonstrate that the failure to observe high

standards of conduct and ethics will result in the most serious of sanctions – a permanent bar or suspension

from registration.

In terms of market cases, IIROC continued to monitor for manipulative and deceptive trading strategies.

This resulted in prosecutions involving activities commonly known as spoofing. In addition, Enforcement

continues to focus on the obligation of Dealer Members providing access to the markets to properly

supervise both their own employees and their clients to help prevent and detect manipulative and

deceptive activities.

ENFO

RC

EMEN

T PR

IOR

ITIE

S &

TH

EMES

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 7

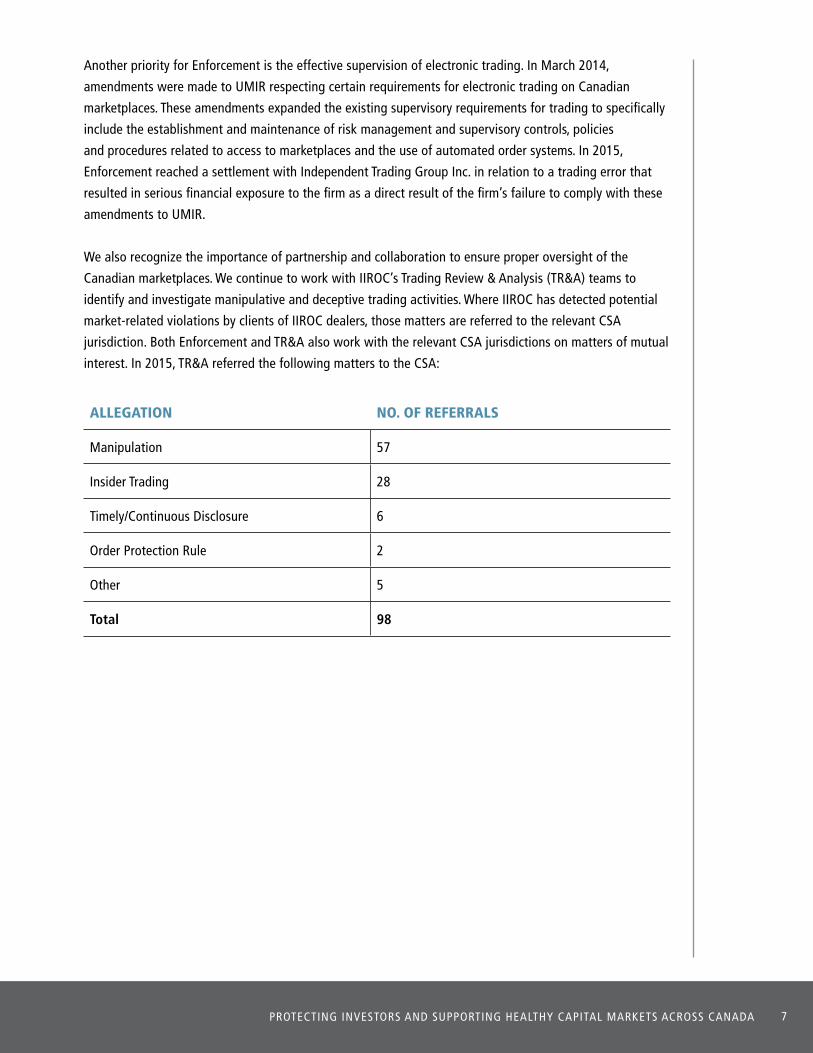

Another priority for Enforcement is the effective supervision of electronic trading. In March 2014,

amendments were made to UMIR respecting certain requirements for electronic trading on Canadian

marketplaces. These amendments expanded the existing supervisory requirements for trading to specifically

include the establishment and maintenance of risk management and supervisory controls, policies

and procedures related to access to marketplaces and the use of automated order systems. In 2015,

Enforcement reached a settlement with Independent Trading Group Inc. in relation to a trading error that

resulted in serious financial exposure to the firm as a direct result of the firm’s failure to comply with these

amendments to UMIR.

We also recognize the importance of partnership and collaboration to ensure proper oversight of the

Canadian marketplaces. We continue to work with IIROC’s Trading Review & Analysis (TR&A) teams to

identify and investigate manipulative and deceptive trading activities. Where IIROC has detected potential

market-related violations by clients of IIROC dealers, those matters are referred to the relevant CSA

jurisdiction. Both Enforcement and TR&A also work with the relevant CSA jurisdictions on matters of mutual

interest. In 2015, TR&A referred the following matters to the CSA:

ALLEGATION NO. OF REFERRALS

Manipulation 57

Insider Trading 28

Timely/Continuous Disclosure 6

Order Protection Rule 2

Other 5

Total 98

2015 ENFORCEMENT REPORT8

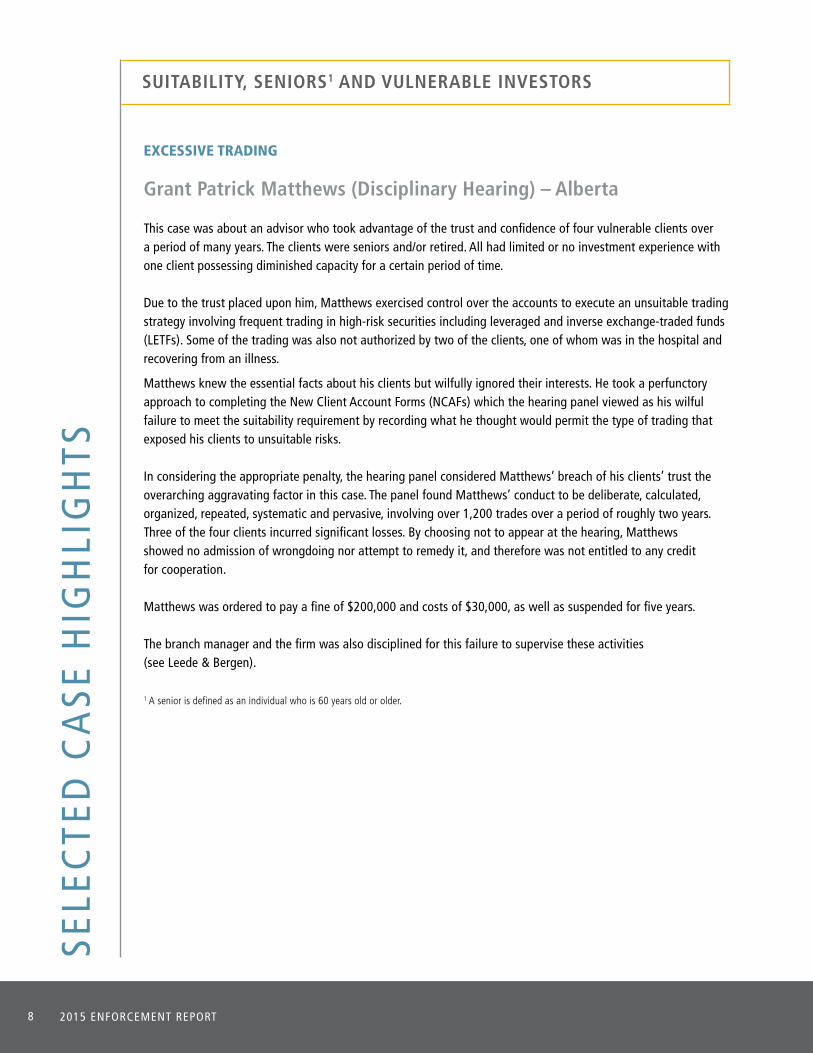

EXCESSIVE TRADING

Grant Patrick Matthews (Disciplinary Hearing) – Alberta

This case was about an advisor who took advantage of the trust and confidence of four vulnerable clients over a period of many years. The clients were seniors and/or retired. All had limited or no investment experience with one client possessing diminished capacity for a certain period of time.

Due to the trust placed upon him, Matthews exercised control over the accounts to execute an unsuitable trading strategy involving frequent trading in high-risk securities including leveraged and inverse exchange-traded funds (LETFs). Some of the trading was also not authorized by two of the clients, one of whom was in the hospital and recovering from an illness.

Matthews knew the essential facts about his clients but wilfully ignored their interests. He took a perfunctory approach to completing the New Client Account Forms (NCAFs) which the hearing panel viewed as his wilful failure to meet the suitability requirement by recording what he thought would permit the type of trading that exposed his clients to unsuitable risks.

In considering the appropriate penalty, the hearing panel considered Matthews’ breach of his clients’ trust the overarching aggravating factor in this case. The panel found Matthews’ conduct to be deliberate, calculated, organized, repeated, systematic and pervasive, involving over 1,200 trades over a period of roughly two years. Three of the four clients incurred significant losses. By choosing not to appear at the hearing, Matthews showed no admission of wrongdoing nor attempt to remedy it, and therefore was not entitled to any credit for cooperation.

Matthews was ordered to pay a fine of $200,000 and costs of $30,000, as well as suspended for five years.

The branch manager and the firm was also disciplined for this failure to supervise these activities (see Leede & Bergen).

1 A senior is defined as an individual who is 60 years old or older.

SUITABILITY, SENIORS1 AND VULNERABLE INVESTORSSE

LEC

TED

CA

SE H

IGH

LIG

HTS

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 9

IMPROPER USE OF MARGIN

Darin Lee Chung (Settlement) – British Columbia

The conduct at issue took place for close to a three-year period (June 2009 – March 2012). During that period, Chung inappropriately recommended extensive use of margin for a 72 year-old client, and engaged in personal financial dealings with the same client by borrowing money from him.

The client invested $200,000 and wanted a low risk profile that would generate a 5-6 per cent annual rate of return. Chung opened several accounts for the client including a margin account, for which he failed to explain the risks involved. The client accumulated significant margin debt at unreasonable levels that, for all practical purposes, overwhelmed the solvency of his overall portfolio.

Chung also borrowed $10,000 from the client without his firm’s knowledge. He promised to pay $11,000 within 30 days. More than three years passed before the client received any repayment.

Chung was fined $40,000 and suspended from registration in any capacity for five years. As a precondition for any future registration with IIROC, Chung is also required to demonstrate to IIROC staff that he has fully repaid the debt owing to his client or received a discharge from the client or his estate. He was also subject to six months strict supervision, followed by six months close supervision upon re-registration. Chung was ordered to pay costs of $5,000.

Probhash Mondal (Settlement) – Ontario

By way of settlement, Mondal admitted to making unsuitable recommendations and engaging in discretionary trading for one of his clients. The client had invested $2 million with Mondal, which represented the proceeds of a life insurance policy on the life of her late husband. Her goal was income generation and capital preservation.

Between February and April 2009, Mondal opened five margin accounts for the client and did not explain the risks to her. The accounts were initially marked as primarily low risk. Within three months, the risk tolerance was changed to 100 per cent high risk. This was done to reflect the short-term trading and the holdings in the accounts.

By November 2010, the account was comprised of 100 per cent equities, with a significant concentration in one security (reaching a high of 70 per cent). There was also significant use of margin which contributed to a growing debit balance in the accounts. As a result, the client accounts were charged approximately $50,000 in interest. Significant losses (including unrealized) were incurred between January and November 2010, of approximately $570,000.

Mondal was suspended for five years, fined $100,000 (inclusive of disgorgement) and required to pay costs of $10,000.

2015 ENFORCEMENT REPORT10

James Frederick Norman Mackie and Tricia Joanne Leadbeater (Settlement) – Alberta

Mackie and Leadbeater were part of an employee group at J.F. Mackie & Company Ltd. (subsequently Mackie Research Capital Corporation), at the time an investment dealer based in Calgary, which lent funds to a client who was a senior officer of a publicly traded issuer. While the loan to the senior officer was still outstanding, Mackie Research agreed to participate in a syndicate, led by another investment dealer, to underwrite a debenture offering of the issuer.

Mackie recommended and accepted orders for 14 clients in the offering but did not give these clients any prior notice of the loan to the senior officer. Similarly, Leadbeater, who was a portfolio manager with discretionary authority over managed accounts, purchased the offering for seven managed client accounts, without giving any prior notice of the loan.

A conflict of interest arose when Mackie Research was engaged to be syndicate member in the offering of the issuer, as the senior officer of the issuer was also indebted to Mackie and Leadbeater. This was an undeclared, but indirect, conflict of interest for Mackie and Leadbeater each time they recommended or purchased the offering for client accounts.

The failure to give clients prior notice of the loan to the senior officer of the issuer was a failure to disclose a conflict of interest and represented conduct unbecoming contrary to IIROC Dealer Member Rule 29.1.

Mackie was fined $30,000. Leadbeater was fined $40,000. Mackie and Leadbeater also paid costs of $2,500 each.

Mackie Research Capital Corporation (Settlement) – Ontario

This case dealt with three separate failures by the firm. The first failure involved an undisclosed conflict of interest, the second involved a failure to report certain required information to IIROC and the third was a failure to properly supervise an investment advisor.

Beginning with the first issue, the firm recommended and sold certain corporate bonds to its clients without disclosing that one of its investment advisors held a financial interest in the issuing corporation. The bonds were sold to a total of 25 clients over a six-month period.

The second issue involved the firm’s failure to report over a one-year period certain required information in an accurate or timely way to IIROC through the National Registration Database (NRD). The material information not reported on NRD included outside business activities of an advisor, the departure or leave of an advisor, and an accurate reporting of an advisor’s time devoted to outside business activities.

Finally, the firm admitted that it had failed to properly supervise an investment advisor, Harry Richard Newman. Newman was previously disciplined by IIROC for engaging in excessive trading in the account of an elderly client over a period of nearly three years.

As part of a settlement agreement, the firm agreed to pay a fine of $130,000 and costs of $20,000.

CONFLICT OF INTEREST

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 11

Brian Anish Kumar (Settlement) – Ontario

Kumar made improper use of client funds and forged copies of cheques and clients signatures to facilitate the unauthorized transfer of client funds into his personal brokerage account. Kumar repaid the clients and returned the funds before the commencement of the IIROC investigation.

However, his conduct represented a serious violation of his duties to his clients and his employer and was deliberate and planned, involving the fictitious copying of cheques, forging of client signatures and providing a false account statement.

This misconduct represented a serious divergence from the duty of a Registered Representative to act honestly and in good faith and observe a high ethical standard.

For this misconduct, the IIROC hearing panel agreed that a permanent prohibition on Kumar acting as a Registered Representative was reasonable. Kumar’s conduct violated the basic principles of trust and confidence underlying the securities industry. In addition, Kumar was fined $50,000 and ordered to pay costs of $5,000.

Roy William Orr (Settlement) – Quebec

Orr engaged in a number of deceptive and manipulative activities, including unauthorized trading, misappropriation of funds, forgery of account statements and the fabrication of false client records over a period of more than ten years.

Between 2002 and 2012, Orr fabricated 99 false monthly client account statements in which he inflated the net value of the accounts. In addition, he misappropriated funds from one client and in order to conceal that fact, prepared false portfolio evaluations, fabricated false accounts statements and rerouted mail to a third party.

The client in question was repaid by three Dealer Member firms at which Orr worked during the relevant period.

In approving the settlement agreement, the IIROC hearing panel concluded that Orr’s conduct “without a doubt” warranted a permanent bar since there was reason to believe Orr could not be trusted to act in an honest and fair manner in his dealings with the public, his clients and the securities industry as a whole. Orr was also fined $65,000, ordered to reimburse commissions generated in the amount of $3,600 and pay costs of $5,000.

MISREPRESENTATIONS & DECEPTIVE MISCONDUCT

2015 ENFORCEMENT REPORT12

Julian Robert Ricci (Disciplinary Hearing) – Ontario

Ricci was an investment advisor who admitted to making misrepresentations to his firm’s compliance staff by inflating certain clients’ net worth. He also admitted to falsely endorsing the signatures of several of his clients on account documents.

Ricci worked in a joint code with his senior partner, Douglas Eley. Together they used a leveraged investment strategy with their clients whereby the clients were able to borrow up to three times the amount of their net worth to buy securities. In order to implement the leveraged investment strategy, Ricci was required to submit a detailed suitability assessment to his firm containing information about his clients’ net worth, assets and liabilities. He admitted that he had inflated the net worth of about 30 per cent of his clients by about 30 per cent in these assessments. He reaped a direct economic benefit from these misrepresentations in the form of increased commissions and trailer fees earned on the leveraged investments. He also admitted to falsely endorsing the signatures of several clients on account documents that were submitted to his firm.

The hearing panel imposed a two-year suspension, a one-year period of strict supervision, a fine of $200,000 and costs of $15,000. Ricci appealed these sanctions to the Ontario Securities Commission (OSC), and in reasons released on March 6, 2015 the OSC dismissed the appeal. Eley was disciplined in 2014.

Zhenyu Li (Settlement) – Ontario

Li was a proprietary trader at National Bank Financial Inc. On twenty occasions over the course of three months, Li entered non-bona fide orders – orders that are entered without an intention to execute them – in the pre-opening on the TSX and TSXV to affect the Calculated Opening Price (COP) of certain securities for his own advantage.

The COP indicates the price at which trading in a security will commence at the opening of the market based on the orders entered to that point. Li’s pattern of order entry, a practice commonly known as “spoofing”, misrepresented the supply, demand, or price for the securities and was undertaken to achieve a profit. This practice is contrary to UMIR 2.2 which prohibits the use of manipulative or deceptive methods, acts or practices which harm market integrity and undermine market confidence.

Li agreed to a fine of $10,000, a suspension of access to IIROC-regulated marketplaces for one month, and was ordered to pay $1,500 in costs.

MANIPULATIVE AND DECEPTIVE TRADING – “SPOOFING”

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 13

Independent Trading Group (ITG) Inc. (Settlement) – Ontario

In 2013, IIROC implemented UMIR 7.1(6) and Policy 7.1, Part 7 – Specific Provisions Applicable to Electronic Access that, among other things, detailed the automated pre-trade controls that were expected of investment dealers to prevent trades from being entered that might cause the firm to exceed credit or capital thresholds.

On January 21, 2014, at the open of trading on the TSX, a trading error occurred at ITG whereby a sell order resulted in the firm becoming capital deficient by approximately $8 million. The trading error was inadvertent, resulting from a trader mistakenly ignoring a warning about the trade’s total value, but resulted in serious financial exposure to ITG.

The trading error could have been prevented had ITG taken reasonable steps to fulfil its trading supervision obligations under UMIR 7.1(6) and Policy 7.1, Part 7, by employing and verifying that it had in place adequate automated controls to prevent the entry of orders which would result in the firm exceeding pre-determined credit or capital thresholds. ITG was able to correct the capital deficiency shortly after the trading error occurred, which resulted in a profit to the firm.

The firm recognized that it should not retain any financial benefit from the trading error that resulted from its non-compliance with UMIR and agreed to pay a fine of $170,000 that took into account the profit made.

Brian Douglas Bergen and Leede Financial Markets Inc. (Settlement) – Alberta

This proceeding related to the supervision of Grant Patrick Matthews who was also disciplined by IIROC. Bergen, the branch manager, admitted that from December 2008 to May 2012, he failed to supervise the conduct of Matthews and report a complaint by one of the clients that formed part of the Matthews disciplinary action. The firm, Leede Financial Markets Inc. (Leede), similarly admitted that during the same period of time, it failed to execute its supervisory responsibilities over Matthews.

Matthews had employed an aggressive trading strategy that resulted in suitability, discretionary trading and excessive trading (churning) violations. The clients were all retired or approaching retirement and sustained losses ranging from 8-28 per cent of their accounts.

There were numerous red flags that should have prompted some supervisory queries. These red flags included the aggressive and high-risk nature of the trading strategy for clients who were vulnerable; dated NCAFs which were not regularly updated; the extraordinary trading volume for retirement accounts (over 1,200 total trades in the four client accounts over less than two years); and the fact that a small percentage of Matthews’ client base comprised approximately 87 per cent of his total gross commissions over a two-year period. Despite these flags, there was no written record of a single query by Bergen or by the compliance officer who conducted supervision on behalf of the firm.

SUPERVISION OF ELECTRONIC TRADING

RETAIL ACCOUNT SUPERVISION

2015 ENFORCEMENT REPORT14

One of the four clients affected also made a complaint to Matthews, which was subsequently provided to Bergen. He did not report such complaint to IIROC as required by Rule 3100(1). Instead, he took over the client from Matthews and pursued a more conservative investment strategy. His handling of the client complaint was an attempt to prevent the client from pursuing his complaint, and as such constituted conduct unbecoming, contrary to IIROC Rule 29.1.

Bergen was fined $50,000, suspended from acting in a supervisory capacity for one year, required to successfully re-write the Branch Manager’s course upon returning as a supervisor and pay costs of $2,500.

Leede was fined $90,000 and required to pay costs of $10,000.

Assante Capital Management Ltd. (Settlement) – Ontario

This case dealt with the firm’s supervisory failings of one of it sub-branches where Brian Malley, a former approved person, engaged in numerous regulatory violations which led to his permanent ban by IIROC in 2014 (see 2014 Annual Enforcement Report, p.11.)

Assante Capital Management Ltd. (Assante) had a branch office in Red Deer, Alberta. There were only three employees at this sub-branch including Brian Malley and Christine Malley, his wife, who was his immediate supervisor. Among other violations, Brian Malley made unsuitable recommendations for ten clients when he recommended that they hold highly concentrated positions in speculative securities. Christine was also disciplined for her role in failing to supervise Brian. Most of the clients suffered substantial losses in their accounts with decreases in value ranging from approximately 23-54 per cent.

While the firm was aware that the Malleys were spouses, it failed to adequately mitigate for the potential conflict of interest that existed as a result of this relationship. A heightened level of supervision was required to mitigate the potential for conflicts. It also failed in making the necessary compliance queries with respect to the account activity of Malley’s client accounts.

Assante was fined $400,000 and required to pay costs of $30,000.

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 15

Jacob Securities Inc.

On December 17, 2015 Enforcement staff brought an expedited hearing before a hearing panel regarding Jacob Securities Inc. (Jacob).

Staff sought an order suspending Jacob’s membership in IIROC or, in the alternative, imposing a monitor to assist Jacob in fulfilling its regulatory compliance obligations. The grounds in support of staff’s application were numerous. In particular, an Integrated Compliance Examination Report dated November 12, 2015 found significant and repeat deficiencies regarding supervision of trading activity, supervision of grey and restricted lists, conflicts of interest, management of outside business activities and basic corporate governance matters. A meeting between senior executives from Jacob and senior IIROC staff held shortly after the delivery of the Integrated Compliance Examination Report demonstrated that Jacob had no realistic plan in place to address the numerous deficiencies.

Subsequent to the delivery of the Integrated Compliance Examination Report, Jacob’s Chief Financial Officer resigned, the firm was temporarily capital deficient and the landlord locked Jacob’s business premises for two days for failure to pay rent. Although Jacob argued at the expedited hearing that it would retain a monitor to assist with rectifying the compliance deficiencies, the hearing panel ordered Jacob’s membership in IIROC be suspended immediately. The hearing panel held it was satisfied that IIROC staff had established the requisite risk of imminent harm and accordingly ordered the firm’s suspension along with other terms and conditions.

EXTRAORDINARY FIRM MEASURES

2015 ENFORCEMENT REPORT16

Northern Securities Inc. and Victor Philip Alboini (Appeal) – Ontario

In 2015, a long-running disciplinary proceeding was concluded when the Ontario Court of Appeal denied Northern Securities Inc. (NSI) and Victor Alboini’s motion for leave to appeal. The appeal stemmed from a 2012 disciplinary hearing involving NSI, its CEO, Victor Alboini, its Chief Compliance Officer, Frederick Vance, and its Chief Financial Officer, Douglas Chornoboy.

The hearing panel conducted a hearing on the merits and concluded that three counts had been proven against Alboini and NSI:

1. Alboini engaged in conduct unbecoming by improperly obtaining access to credit for his client, Jaguar Financial Corporation, and in doing so risked the capital of both NSI and its carrying broker;

2. NSI and Alboini repeatedly failed to ensure that they had adequate policies and procedures and corrected deficiencies noted by IIROC’s compliance groups in Business Conduct Compliance and Trading Conduct Compliance; and

3. NSI and Alboini filed or permitted to be filed inaccurate Monthly Financial Reports which failed to account for leasehold improvement costs, thereby misstating NSI’s risk adjusted capital.

NSI and Alboini sought a hearing and review by the OSC2 of the IIROC hearing panel’s decision. The hearing and review was held in 2013. In its decision, the OSC overturned and dismissed the second violation referenced above. The Commission further held that the conduct of the sanctions hearing was procedurally unfair to them and therefore set aside the sanctions and costs imposed. A new sanctions hearing was held before the OSC resulting in the following sanctions:

NSI and Alboini appealed the decisions of the OSC, both as to the contraventions of IIROC Rules and the sanctions ordered, to the Ontario Divisional Court. In June 2015, the Divisional Court dismissed the appeal in its entirety, finding that the decisions of the Commission were reasonable and the new sanctions hearing ordered by the Commission was procedurally fair. NSI and Alboini sought motion for leave to appeal the Divisional Court decision to the Court of Appeal, but the motion was denied in October 2015.

2 Chornoboy and Vance, while parties to the OSC hearing and review, did not participate at the hearings nor did they pursue an appeal to the Ontario Divisional Court. Accordingly, their disciplinary matters were completed in 2014.

APPEALS

Re Alboini: • A fine of $250,000 (reduced from $525,000)

relating to violation #1 above; • Disgorgement of commission of $244,985; • Suspension from IIROC registration for one year

(reduced from two years); • Suspension from acting as Ultimate Designated Person

(UDP) for two years (reduced from permanent ban); • A reprimand relating to violation #3 above; and • Costs of $62,500.

Re NSI: • A fine of $50,000; • A reprimand; and • Costs of $10,000.

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 17

Revised Sanction Guidelines

2015 was the inaugural year for IIROC’s

Revised Sanction Guidelines (which came into

effect February 2, 2015). The new guidelines are

a consolidation and update of the two previous

sanction guidelines, namely Dealer Member

Sanction Guidelines and UMIR Sanction

Guidelines, which were used by IIROC’s

predecessor organizations, the Investment

Dealers Association (IDA) and Market

Regulation Services (MRS) Inc.

The guidelines, along with related Staff

Policy statements, ensure consistency and

promote greater transparency by clearly

communicating to stakeholders how IIROC

will approach sanctioning decisions in

enforcement proceedings.

The settlement with Scotia Capital Inc. (see

summary below) was one case where staff

applied its new policy statement relating to

Credit for Cooperation. According to its policy

statement, staff advised that “a record of

cooperation that is proactive and exceptional

will be considered a mitigating factor for

the sanctions sought against a respondent”

in a disciplinary proceeding. In the Scotia

Capital case, staff accepted that the firm had

demonstrated “proactive and exceptional

cooperation” by self-identifying a contravention

of IIROC Rules, conducting an extensive

internal review and sharing the results with

staff, and the extensive remedial steps taken.

This “proactive and exceptional cooperation”

was taken into account by staff in agreeing to

the sanction against Scotia Capital, and not

requiring payment of any costs.

Scotia Capital Inc. (Settlement) – Ontario

Scotia Capital acquired a division of another

Dealer Member, DWM Securities Inc., in 2011,

which subsequently amalgamated with Scotia

Capital in late 2013. Scotia Capital discovered

that the division had failed to establish and

maintain an adequate system of compliance

and supervision to ensure that its clients were

qualified to purchase funds offered pursuant to

prospectus exemptions. A large number of funds

were sold to clients where the documentation

in their files did not support their eligibility to

purchase the funds in question.

Upon becoming aware of the failings,

Scotia Capital undertook a comprehensive

internal review to determine the scope of the

problem. Scotia Capital promptly reported

the matter to, and shared the results of the

internal review with IIROC. The firm also

took measures to remediate the problem by

enhancing its compliance procedures and

policies and introducing a remediation plan

to compensate affected clients for any losses

suffered. In addition, Scotia Capital took

internal disciplinary measures against certain

investment advisors who failed to adequately

discharge their know-your-client obligations.

Scotia Capital paid a fine of $500,000 and

agreed to donate the internal fines collected

to charity.K

EY P

OLI

CY

IN

ITIA

TIV

ES A

ND

DEV

ELO

PMEN

TS

2015 ENFORCEMENT REPORT18

The IIROC hearing panel accepted that giving

credit for proactive and exceptional cooperation

in mitigation of sanctions was important to

encourage self-reporting and thorough internal

reviews and was consistent with the objectives

of the IIROC disciplinary process, namely to

protect the integrity of Canada’s capital markets

and maintain high standards of conduct.

Authority to Collect Fines

One key priority for Enforcement has been

strengthening the ability to collect fines

against individuals who have been disciplined.

Payment of monetary penalties is mandatory

for firms and individuals who wish to remain

members or registrants of IIROC. While IIROC

regularly collects fines against Dealer Members,

collecting from individuals has proven to

be much more challenging. In 2015, IIROC

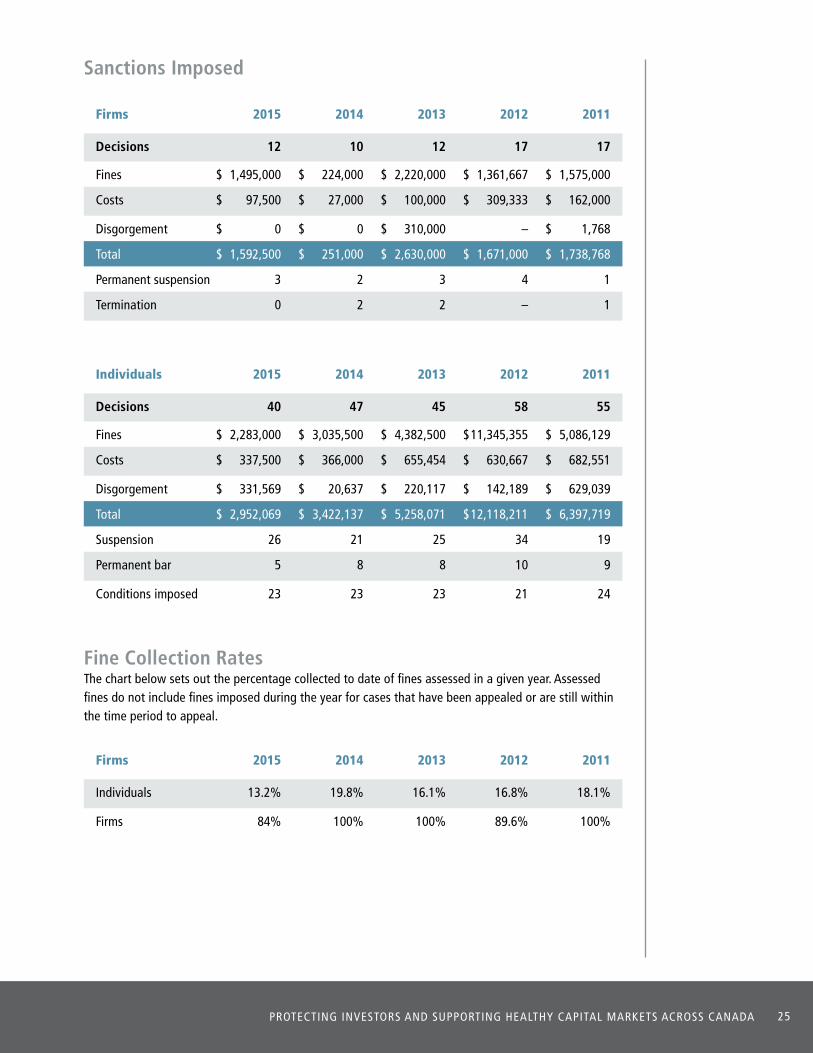

collected 13.2 per cent of penalties levied

against individuals.

While some disciplined individuals are unable

to pay fines, others avoid payment by simply

leaving the securities industry and abandoning

their registration with IIROC. IIROC’s limited

collection ability undermines the credibility

of its disciplinary process and the sanctions

imposed. Individuals who break IIROC rules

should be subject to real penalties which can

be collected by IIROC.

Currently, IIROC has the legal authority to

enforce fines in Alberta and Quebec. Not

surprisingly, the collection rates in those

jurisdictions are generally higher than the

national average. Extending this authority

further would send a strong message of

deterrence to potential wrongdoers and would

support investor confidence in the system. To

that end, IIROC has been taking active steps to

pursue this authority, reaching out to various

stakeholders, namely the securities regulators

and government officials responsible for

securities regulation across the country.

As IIROC continues with this pursuit, IIROC

still makes every reasonable effort to collect

penalties imposed against disciplined firms and

individuals. A disciplined party’s failure to pay

their fine will result in IIROC taking immediate

steps to suspend them until payment is made.

IIROC also publishes the Unpaid Fines Report

which lists individual registrants who, since

2008, have failed to pay fines, disgorgement,

and/or costs imposed as a result of disciplinary

action taken against them. This list is available

on IIROC’s website and is updated on a

quarterly basis.

It should be noted that the report is intended

to enhance transparency relating to IIROC’s

collection rate for fines and other monetary

sanctions and is not meant to be a list of

individuals currently indebted to IIROC.

Accordingly, the report may include the names

of individuals who received a bankruptcy

discharge subsequent to the order being made.

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 19

Information Sharing – La Chambre de la sécurité financière

As a public interest regulator, IIROC recognizes

the importance of collaborating with the CSA,

SROs and other regulators who oversee the

financial services industry. Such partnerships

are essential to achieving the mutual goal of

protecting investors and supporting healthy

capital markets. To that end, over the years

IIROC has entered into various Memoranda of

Understanding (MOUs) with various regulators

in Canada and abroad that facilitate the sharing

of information and enable greater efficiency

and consistency of the supervisory system in the

public interest.

In November 2015, IIROC entered into another

Memorandum of Understanding (MOU) with La

Chambre de la sécurité financière (CSF). Under

this MOU, IIROC and the CSF will share each

other’s disciplinary decisions.

Each organization has committed to review the

status of their respective registered individual

who has been sanctioned by the other body.

This review may then result in an investigation

or other appropriate action. This review

will take place whether or not the person

sanctioned is still registered with the CSF

or IIROC.

This arrangement aims to prevent disciplined

individuals from avoiding regulatory

consequences by merely changing their

registration to another organization, carrying

on business under another designation or

continuing to work in an unregistered capacity.

This protocol serves as a further example

of IIROC’s commitment to work with other

regulators to enhance investor protection

and improve the efficiency and consistency of

regulatory oversight.

Consolidated Enforcement Rules Project

The goal of this project is to consolidate and

rationalize the Enforcement rules from each

of IIROC’s predecessor organizations (IDA and

MRS Inc.).

The proposed consolidated rules will simplify

and improve the enforcement of both the

Dealer Member Rules and UMIR, by bringing

the applicable procedural rules, currently

contained in these two rulebooks, together into

a single set of rules (the Consolidated Rules).

The Consolidated Rules have been submitted

for final review and approval by the CSA. Upon

receipt of the CSA’s approval, IIROC will move

to implement the consolidated rules promptly.

2015 ENFORCEMENT REPORT20

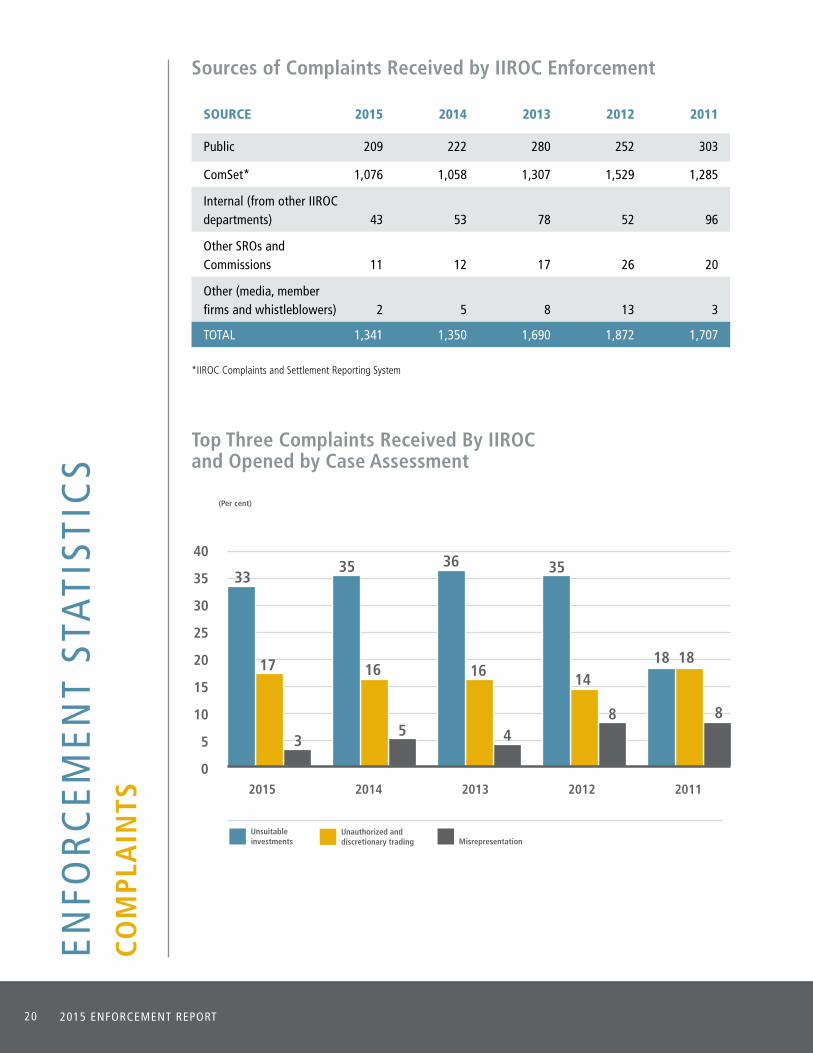

Sources of Complaints Received by IIROC Enforcement

SOURCE 2015 2014 2013 2012 2011

Public 209 222 280 252 303

ComSet* 1,076 1,058 1,307 1,529 1,285

Internal (from other IIROC departments) 43 53 78 52 96

Other SROs and Commissions 11 12 17 26 20

Other (media, member firms and whistleblowers) 2 5 8 13 3

TOTAL 1,341 1,350 1,690 1,872 1,707

*IIROC Complaints and Settlement Reporting System

Top Three Complaints Received By IIROC and Opened by Case Assessment

ENFO

RC

EMEN

T ST

ATI

STIC

SC

OM

PLA

INTS

(Per cent)

Unsuitableinvestments

Unauthorized and discretionary trading Misrepresentation

0

5

10

15

20

25

30

35

40

2015

13 19 32

3335

1617

35 4

16 14

8

18 18

8

36 35

2014 2013 2012 2011

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 21

INV

ESTI

GA

TIO

NS

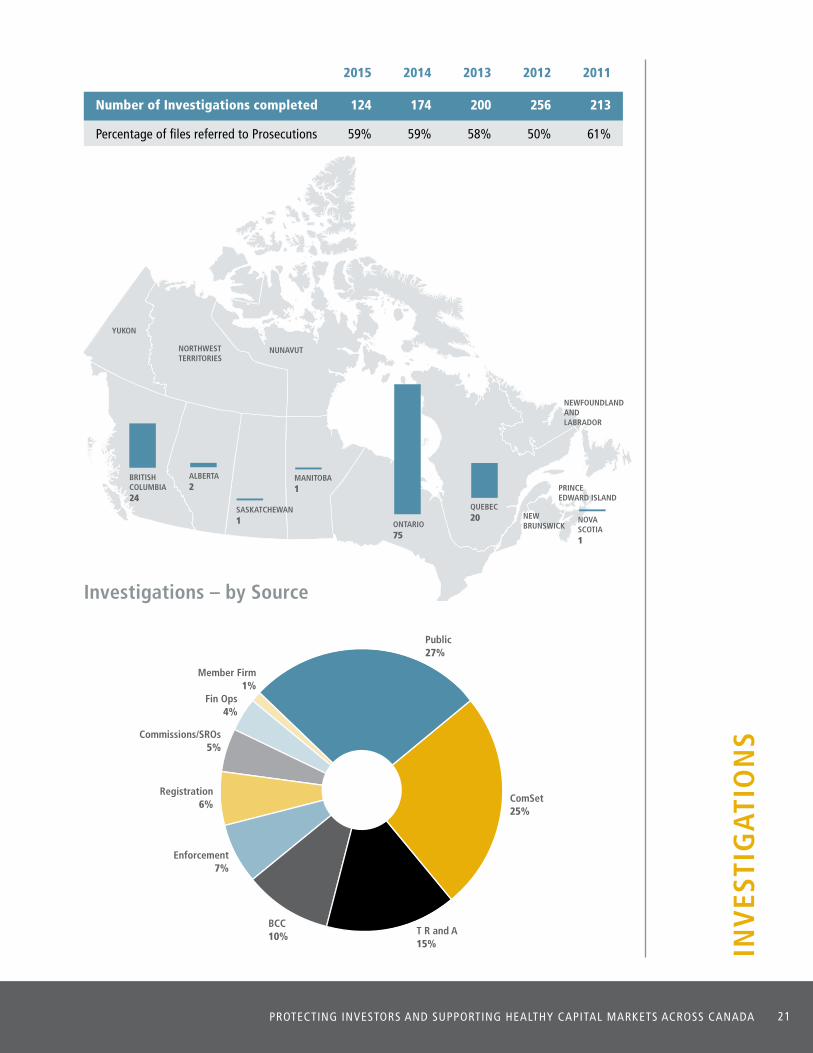

2015 2014 2013 2012 2011

Number of Investigations completed 124 174 200 256 213

Percentage of files referred to Prosecutions 59% 59% 58% 50% 61%

ONTARIO75

MANITOBA1

ALBERTA2

BRITISHCOLUMBIA24

SASKATCHEWAN1

QUEBEC20

INVESTIGATIONS

NOVASCOTIA1

NEWFOUNDLANDANDLABRADOR

NUNAVUT

YUKON

NORTHWESTTERRITORIES

NEWBRUNSWICK

PRINCEEDWARD ISLAND

Investigations – by Source

Public 27%

ComSet 25%

T R and A 15%

BCC 10%

Enforcement 7%

Registration 6%

Fin Ops 4%

Member Firm 1%

Commissions/SROs5%

2015 ENFORCEMENT REPORT22

PRO

SEC

UTI

ON

S

ONTARIO22

MANITOBA3

ALBERTA10BRITISH

COLUMBIA10

SASKATCHEWAN1

QUEBEC6 NOVA

SCOTIA

NEWFOUNDLANDANDLABRADOR

NUNAVUT

YUKON

PROSECUTIONS

NORTHWESTTERRITORIES

NEWBRUNSWICK

PRINCEEDWARD ISLAND

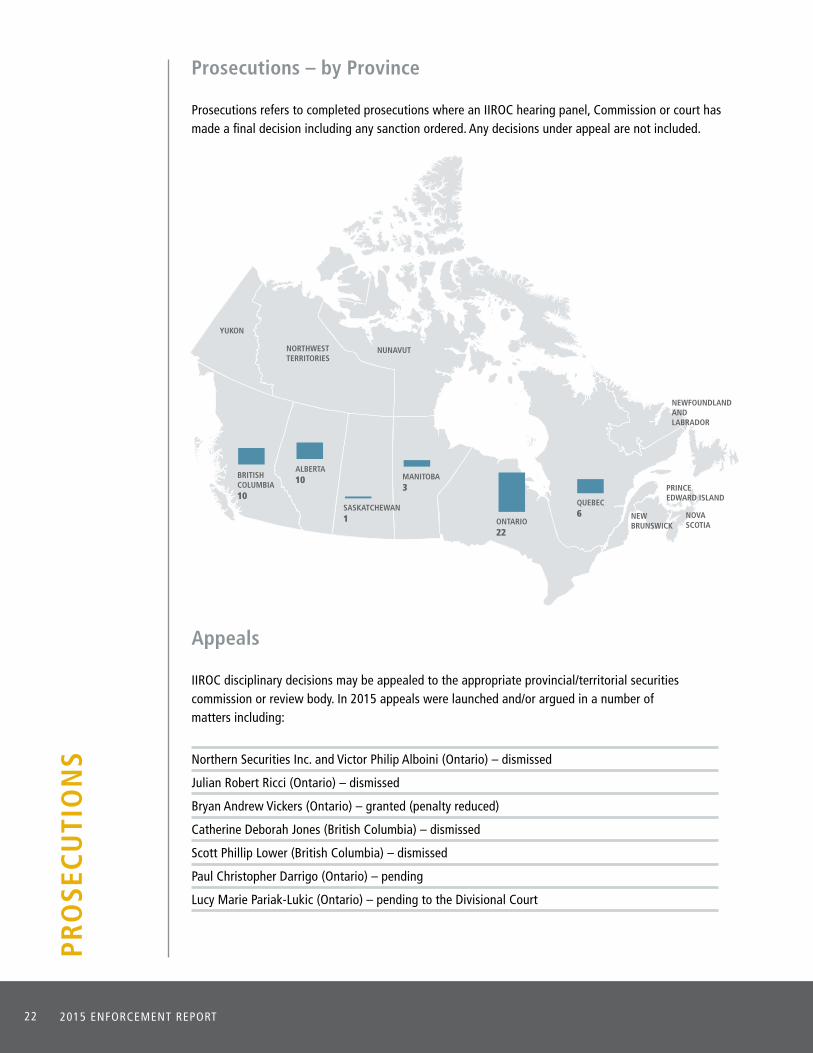

Prosecutions – by Province

Prosecutions refers to completed prosecutions where an IIROC hearing panel, Commission or court has made a final decision including any sanction ordered. Any decisions under appeal are not included.

Appeals

IIROC disciplinary decisions may be appealed to the appropriate provincial/territorial securities commission or review body. In 2015 appeals were launched and/or argued in a number of matters including:

Northern Securities Inc. and Victor Philip Alboini (Ontario) – dismissed

Julian Robert Ricci (Ontario) – dismissed

Bryan Andrew Vickers (Ontario) – granted (penalty reduced)

Catherine Deborah Jones (British Columbia) – dismissed

Scott Phillip Lower (British Columbia) – dismissed

Paul Christopher Darrigo (Ontario) – pending

Lucy Marie Pariak-Lukic (Ontario) – pending to the Divisional Court

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 23

Prosecutions – by Respondent Type

Prosecutions – by Hearing Type

see appendix C for description of Hearing types

Firms Individuals

0

10

20

30

40

50

60

70

80

2015

40 47 45 58 55

1210 12

171752

57 57

7572

2014 2013 2012 2011

Discipline Settlement

0

10

20

30

40

50

60

70

80

2015

39 36 38 54 40

1321 19

21

32

5257 57

7572

2014 2013 2012 2011

2015 ENFORCEMENT REPORT24

PRO

SEC

UTI

ON

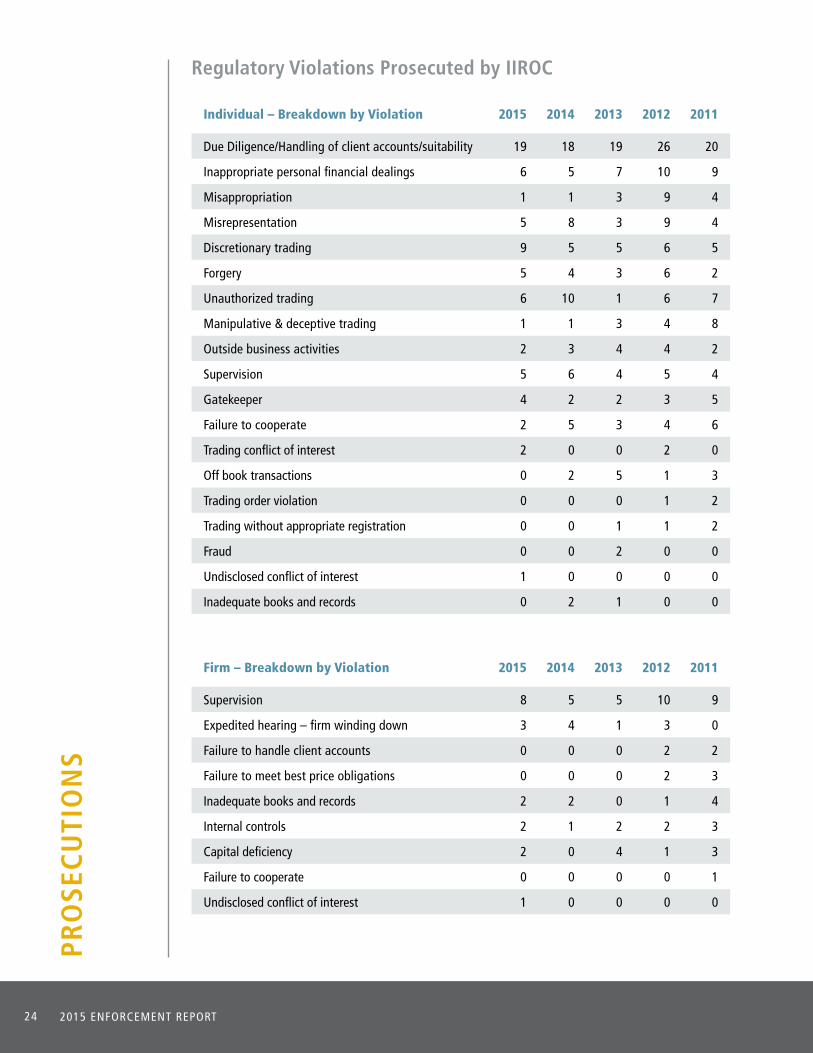

SRegulatory Violations Prosecuted by IIROC

Individual – Breakdown by Violation 2015 2014 2013 2012 2011

Due Diligence/Handling of client accounts/suitability 19 18 19 26 20

Inappropriate personal financial dealings 6 5 7 10 9

Misappropriation 1 1 3 9 4

Misrepresentation 5 8 3 9 4

Discretionary trading 9 5 5 6 5

Forgery 5 4 3 6 2

Unauthorized trading 6 10 1 6 7

Manipulative & deceptive trading 1 1 3 4 8

Outside business activities 2 3 4 4 2

Supervision 5 6 4 5 4

Gatekeeper 4 2 2 3 5

Failure to cooperate 2 5 3 4 6

Trading conflict of interest 2 0 0 2 0

Off book transactions 0 2 5 1 3

Trading order violation 0 0 0 1 2

Trading without appropriate registration 0 0 1 1 2

Fraud 0 0 2 0 0

Undisclosed conflict of interest 1 0 0 0 0

Inadequate books and records 0 2 1 0 0

Firm – Breakdown by Violation 2015 2014 2013 2012 2011

Supervision 8 5 5 10 9

Expedited hearing – firm winding down 3 4 1 3 0

Failure to handle client accounts 0 0 0 2 2

Failure to meet best price obligations 0 0 0 2 3

Inadequate books and records 2 2 0 1 4

Internal controls 2 1 2 2 3

Capital deficiency 2 0 4 1 3

Failure to cooperate 0 0 0 0 1

Undisclosed conflict of interest 1 0 0 0 0

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 25

Sanctions Imposed

Firms 2015 2014 2013 2012 2011

Decisions 12 10 12 17 17

Fines $ 1,495,000 $ 224,000 $ 2,220,000 $ 1,361,667 $ 1,575,000

Costs $ 97,500 $ 27,000 $ 100,000 $ 309,333 $ 162,000

Disgorgement $ 0 $ 0 $ 310,000 – $ 1,768

Total $ 1,592,500 $ 251,000 $ 2,630,000 $ 1,671,000 $ 1,738,768

Permanent suspension 3 2 3 4 1

Termination 0 2 2 – 1

Individuals 2015 2014 2013 2012 2011

Decisions 40 47 45 58 55

Fines $ 2,283,000 $ 3,035,500 $ 4,382,500 $ 11,345,355 $ 5,086,129

Costs $ 337,500 $ 366,000 $ 655,454 $ 630,667 $ 682,551

Disgorgement $ 331,569 $ 20,637 $ 220,117 $ 142,189 $ 629,039

Total $ 2,952,069 $ 3,422,137 $ 5,258,071 $ 12,118,211 $ 6,397,719

Suspension 26 21 25 34 19

Permanent bar 5 8 8 10 9

Conditions imposed 23 23 23 21 24

Fine Collection Rates The chart below sets out the percentage collected to date of fines assessed in a given year. Assessed fines do not include fines imposed during the year for cases that have been appealed or are still within the time period to appeal.

Firms 2015 2014 2013 2012 2011

Individuals 13.2% 19.8% 16.1% 16.8% 18.1%

Firms 84% 100% 100% 89.6% 100%

2015 ENFORCEMENT REPORT26

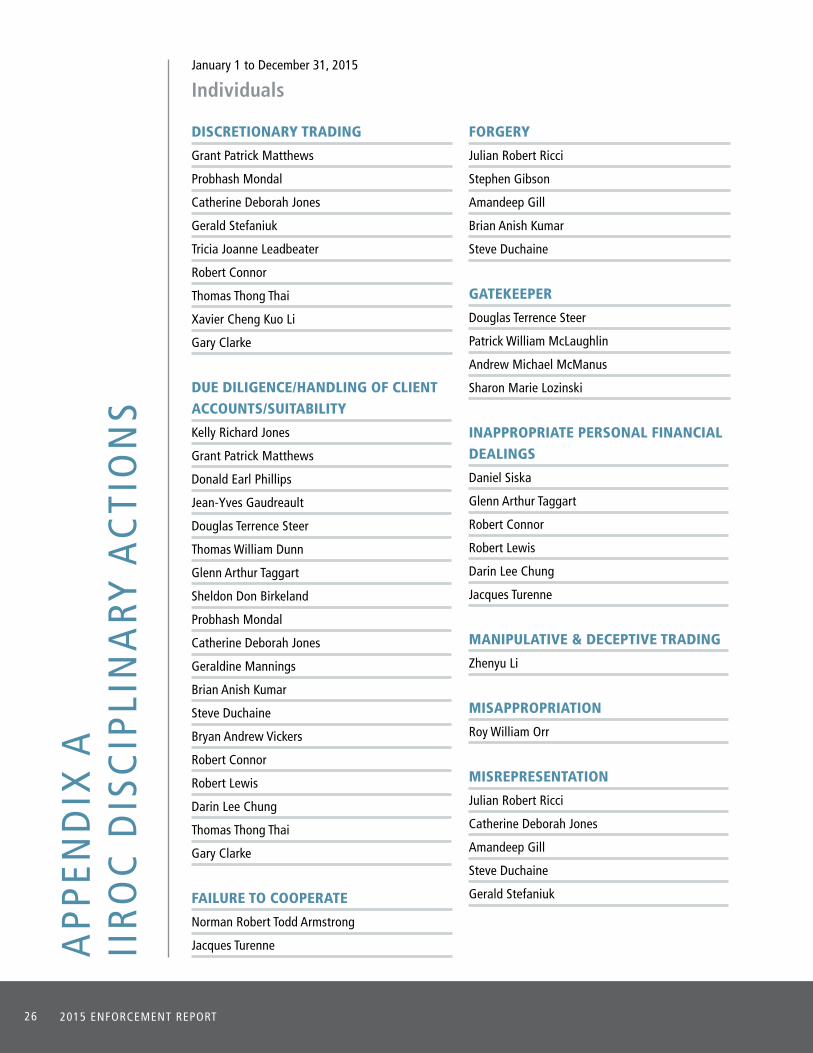

January 1 to December 31, 2015

Individuals

DISCRETIONARY TRADING

Grant Patrick Matthews

Probhash Mondal

Catherine Deborah Jones

Gerald Stefaniuk

Tricia Joanne Leadbeater

Robert Connor

Thomas Thong Thai

Xavier Cheng Kuo Li

Gary Clarke

DUE DILIGENCE/HANDLING OF CLIENT ACCOUNTS/SUITABILITY

Kelly Richard Jones

Grant Patrick Matthews

Donald Earl Phillips

Jean-Yves Gaudreault

Douglas Terrence Steer

Thomas William Dunn

Glenn Arthur Taggart

Sheldon Don Birkeland

Probhash Mondal

Catherine Deborah Jones

Geraldine Mannings

Brian Anish Kumar

Steve Duchaine

Bryan Andrew Vickers

Robert Connor

Robert Lewis

Darin Lee Chung

Thomas Thong Thai

Gary Clarke

FAILURE TO COOPERATE

Norman Robert Todd Armstrong

Jacques Turenne

FORGERY

Julian Robert Ricci

Stephen Gibson

Amandeep Gill

Brian Anish Kumar

Steve Duchaine

GATEKEEPER

Douglas Terrence Steer

Patrick William McLaughlin

Andrew Michael McManus

Sharon Marie Lozinski

INAPPROPRIATE PERSONAL FINANCIAL DEALINGS

Daniel Siska

Glenn Arthur Taggart

Robert Connor

Robert Lewis

Darin Lee Chung

Jacques Turenne

MANIPULATIVE & DECEPTIVE TRADING

Zhenyu Li

MISAPPROPRIATION

Roy William Orr

MISREPRESENTATION

Julian Robert Ricci

Catherine Deborah Jones

Amandeep Gill

Steve Duchaine

Gerald Stefaniuk

APP

END

IX A

II

RO

C D

ISC

IPLI

NA

RY A

CTI

ON

S

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 27

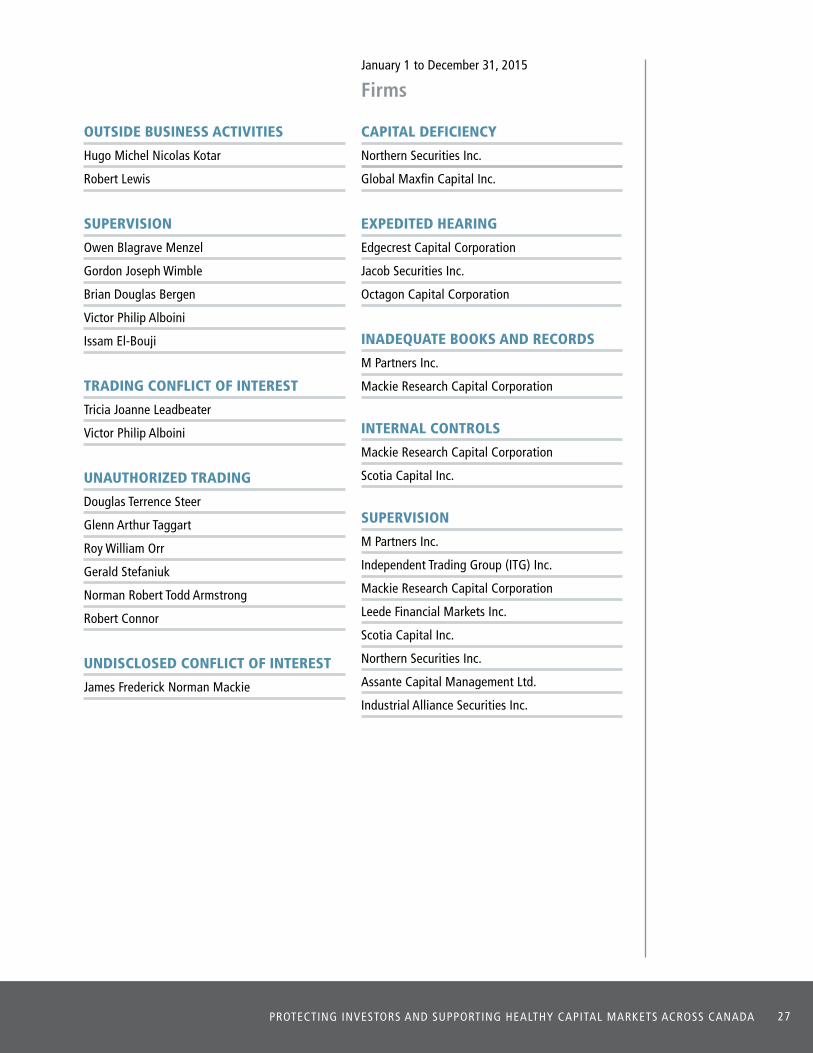

OUTSIDE BUSINESS ACTIVITIES

Hugo Michel Nicolas Kotar

Robert Lewis

SUPERVISION

Owen Blagrave Menzel

Gordon Joseph Wimble

Brian Douglas Bergen

Victor Philip Alboini

Issam El-Bouji

TRADING CONFLICT OF INTEREST

Tricia Joanne Leadbeater

Victor Philip Alboini

UNAUTHORIZED TRADING

Douglas Terrence Steer

Glenn Arthur Taggart

Roy William Orr

Gerald Stefaniuk

Norman Robert Todd Armstrong

Robert Connor

UNDISCLOSED CONFLICT OF INTEREST

James Frederick Norman Mackie

January 1 to December 31, 2015

Firms

CAPITAL DEFICIENCY

Northern Securities Inc.

Global Maxfin Capital Inc.

EXPEDITED HEARING

Edgecrest Capital Corporation

Jacob Securities Inc.

Octagon Capital Corporation

INADEQUATE BOOKS AND RECORDS

M Partners Inc.

Mackie Research Capital Corporation

INTERNAL CONTROLS

Mackie Research Capital Corporation

Scotia Capital Inc.

SUPERVISION

M Partners Inc.

Independent Trading Group (ITG) Inc.

Mackie Research Capital Corporation

Leede Financial Markets Inc.

Scotia Capital Inc.

Northern Securities Inc.

Assante Capital Management Ltd.

Industrial Alliance Securities Inc.

2015 ENFORCEMENT REPORT28

Internal Sources

Registration Department:On occasion, the circumstances surrounding the termination of an individual registrant requires further investigation.

Compliance Departments Business Conduct Compliance (BCC), Financial Operations Compliance (FinOps), and Trading Conduct and Compliance (TCC):Issues and deficiencies noted in compliance examination reports sometimes form the basis for some of Enforcement’s most significant disciplinary cases.

Trading Review & Analysis (TR&A)/ Market Surveillance:The TR&A and Market Surveillance Departments oversee all equity and debt trading on Canadian marketplaces and serve as Enforcement’s primary source of market-related information and enforcement referrals.

Complaints & Inquiries Team (C&I): The C&I Team is the primary contact for direct investor inquiries and complaints. C&I refers the majority of the complaints it receives, involving alleged regulatory violations, to Enforcement for further assessment. C&I can be reached by phone (1-877-442-4322), email ([email protected]) or by filing an online complaint form (www.iiroc.ca).

External Sources

ComSet ReportsIIROC rules require Dealer Members to inform IIROC, using IIROC’s Complaints and Settlement Reporting System (ComSet), when certain events occur, including when a Dealer Member receives a written client complaint, when criminal charges are laid against a Dealer Member or any of its individual registrants, or when a securities-related civil claim is brought by a client. These reportable events represent Enforcement’s primary source of external enforcement-related information, and the most significant source of enforcement cases.

Outside AgenciesEnforcement receives referrals from Canadian provincial securities regulators, international securities regulatory bodies and other public agencies, including law enforcement officials.

IIROC’s Whistleblower ServiceIIROC operates a Whistleblower Service designed to receive, evaluate and take prompt and effective action on information based on first-hand knowledge or tangible evidence of potential systemic wrongdoing, securities fraud and/or unethical behaviour by IIROC-regulated individuals or firms. The Whistleblower Service can be reached by phone (1-866-211-9001) or email ([email protected]).

Enforcement cases are based upon information drawn from a variety of internal and external sources.

APP

END

IX B

EN

FOR

CEM

ENT

INFO

RM

ATI

ON

SO

UR

CES

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 29

APP

END

IX C

TYPE

S O

F D

ISC

IPLI

NA

RY P

RO

CEE

DIN

GSContested Hearings

Where the Respondent does not admit the alleged violation of IIROC rules, a contested hearing will be held. In that case, staff must prove the allegations set out in the Notice of Hearing – the formal document that initiates disciplinary action. Similar to traditional court proceedings, an IIROC hearing involves staff presenting documentary evidence and oral evidence, through witnesses, in making its case. The Respondent has the right to challenge IIROC’s case by cross-examining witnesses and presenting their own evidence.

The hearing panel, which is normally comprised of one former judge and two active or retired industry members, decides whether IIROC has proven its case against the Respondent and if so, determines the appropriate penalty.

While IIROC does not have the legal authority to compel witnesses or Respondents to attend disciplinary hearings, a Respondent’s failure to attend their hearing does not affect Enforcement’s ability to proceed with the hearing. In these cases, the hearing will proceed in the Respondent’s absence and the hearing panel may accept the allegations as proven without any formal evidence being called.

Settlement HearingsSettlement hearings are held when staff and the Respondent agree, in writing, on the rule(s) violated by the Respondent, the underlying facts and the penalties to be imposed on the Respondent for the agreed violations. The parties must present the agreement to the hearing panel and explain why the panel should accept it. The panel may accept or reject the settlement agreement.

Like many other professional regulatory bodies, the majority of IIROC’s disciplinary matters are resolved by way of settlements.

Expedited HearingsGenerally speaking, an expedited hearing is an emergency proceeding that permits IIROC staff to quickly initiate a proceeding against a Dealer Member or individual registrant in order to protect investors in circumstances where a Dealer Member or individual registrant is not able to continue in business without contravening IIROC’s rules. Typically, such circumstances include: • Bankruptcy; • Financial or operating difficulty of a Dealer

Member; and• Criminal charges laid against the firm or

individual registrant.

At the conclusion of an expedited hearing, the panel has the authority to impose a variety of sanctions, similar to the regular disciplinary process. Examples of sanction terms include:

• Suspension of membership;• Immediately cease dealing with the public; and• Preservation of books and records for a period

of time.

Following the completion of an investigation, Enforcement staff will assess the evidence collected and decide whether to prosecute a Dealer Member or individual registrant for a breach of IIROC rules. When the decision is made to prosecute, formal disciplinary action will be initiated against the Dealer Member or individual registrant (both referred to as the Respondent in a disciplinary proceeding).

Formal disciplinary action will take the form of either a contested hearing or a settlement hearing. Expedited hearings are a third type of hearing to deal with urgent matters.

2015 ENFORCEMENT REPORT30

AMF (Autorité des marchés financiers)The AMF regulates Quebec’s financial markets and provides assistance to

consumers of financial products and services. It was established under An

Act respecting the Autorité des marchés financiers on February 1, 2004, and

oversees the regulation of Québec’s financial sector, notably in the areas

of insurance, securities, deposit institutions (other than banks) and the

distribution of financial products and services.

Chambre de la sécurité financièreA Quebec-based agency which oversees the training and professional conduct

of its members who work in the following areas: group savings plan brokerage,

financial planning, insurance of persons, group insurance of persons and

scholarship plan brokerage.

ComSet (Complaints and Settlement Reporting System)IIROC requires registered firms to report client complaints and disciplinary

actions including internal investigations, denial of registration and settlements;

and civil, criminal or regulatory action against the firm or its registered

employees. This information is reported through IIROC’s computerized

Complaints and Settlement Reporting System.

CSA (Canadian Securities Administrators) The CSA is the council of ten provincial and three territorial securities

regulators in Canada. The mission of the CSA is to facilitate Canada’s securities

regulatory system by protecting investors from unfair fraudulent practices and

by promoting fair, efficient and transparent markets through the development

of harmonized securities regulations, policies and practices.

ETFs (Exchange-traded funds) An investment fund that holds a group of investments such as stocks, bonds,

commodities that trades on a stock exchange like a stock. ETFs generally track

an index, such as a stock index like the S&P 500. Leveraged ETFs aim to deliver

multiples of the performance of the index they track. Some leveraged ETFs are

“inverse” or “short” funds, meaning that they seek to deliver the opposite of

the performance of the index they track.

GLO

SSA

RY

OF

TER

MS

PROTECTING INVESTORS AND SUPPORTING HEALTHY CAPITAL MARKETS ACROSS CANADA 31

IDA (Investment Dealers Association of Canada)The IDA served as a regulator and advocacy organization for security dealers

until 2006. In 2006, the IDA narrowed its focus to regulation and transferred

its association role to a separate and independent association, the Investment

Industry Association of Canada. The IDA and Market Regulation Services were

consolidated to form IIROC in 2008.

MarginMargin is the amount of equity an investor must provide in order to purchase

a security held in a “margin account.” A margin account allows clients to buy

and/or sell securities on credit and initially pay only part of the full price of the

transaction. The firm then grants credit or “loan value” based on the market

value and quality of the security held in the account. IIROC Rule 100 specifies

the margin requirements for various different securities. For example, if a client

holds a security listed on the TSX worth $50,000 and it has 50% loan value

(50% margin requirement) the maximum amount the member firm may lend

the client is $25,000 (requiring an initial margin deposit of $25,000).

MFDA (Mutual Fund Dealers Association) The MFDA regulates the operations, standards of practice and business conduct

of its members and their representatives. Its mandate is to enhance investor

protection and strengthen public confidence in the Canadian mutual

fund industry.

MRS (Market Regulation Services Inc.) Market Regulation Services was created as a joint initiative of the TSX and

the IDA. MRS amalgamated the in-house surveillance, trade desk compliance,

investigation and enforcement functions of the TSX and TSX Venture Exchange

to produce a single entity to monitor and enforce trading rules on multiple

marketplaces. IIROC was established in 2008 as a non-profit corporation

through the consolidation of the IDA and MRS.

NCAF (New Client Account Form)Securities firms and registered representatives are required to have new clients

complete this form to ensure the firm and the representative are aware of the

client’s financial position and investment objectives so that the firm and the

representative can assess the suitability of their advice.

2015 ENFORCEMENT REPORT32

SpoofingA trading strategy that is considered manipulative and deceptive. Spoofing is a

practice using limit orders that are not intended to be executed to manipulate

prices. Some spoofing strategies are related to the open or close of regular

market hours that involve distorting prices through the entry of non-bona fide

orders, checking for the presence of an “iceberg” order, affecting a calculated

opening price and/or aggressive trading activity near the open or close for an

improper purpose.

SRO (Self-Regulatory Organization) SRO refers to an organization that sets standards, monitors members for

compliance with those standards and takes appropriate action when those

standards are not met.

UMIR (Universal Market Integrity Rules)Market Regulation Services introduced the Universal Market Integrity Rules as

a common set of equity trading rules designed to ensure fairness and maintain

investor confidence. The UMIR continues to be IIROC’s market integrity rules.

GLO

SSA

RY

OF

TER

MS

1-877-442-4322

www.iiroc.ca

MONTRÉAL5 Place Ville Marie, Suite 1550 Montréal, Québec H3B 2G2Tel.: (514) 878-2854 Fax: (514) 878-3860Enforcement Matters only Fax: (514) 878-6324

TORONTO 121 King Street West, Suite 2000 Toronto, Ontario M5H 3T9Tel.: (416) 364-6133 Fax: (416) 364-0753Enforcement Matters only Fax: (416) 364-2998

CALGARYBow Valley Square 3 255-5th Avenue S.W., Suite 800 Calgary, Alberta T2P 3G6Tel.: (403) 262-6393 Fax: (403) 234-0861Enforcement Matters only Fax: (403) 265-4603

VANCOUVERRoyal Centre 1055 West Georgia Street, Suite 2800 P.O. Box 11164 Vancouver, B.C. V6E 3R5Tel.: (604) 683-6222 Fax: (604) 683-3491Enforcement Matters only Fax: (604) 683-6262