Embed Size (px)

Citation preview

Final Report

51A1199512 February 2010

Revision No 4

DEPARTMENT OF AGRICULTURE, FISHERIES AND FORESTRY

(DAFF)

LEGAL FOREST PRODUCTS ASSURANCE – A RISK ASSESSMENT FRAMEWORK FOR ASSESSING THE LEGALITY

OF TIMBER AND WOOD PRODUCTS IMPORTED INTO AUSTRALIA

51A11995

PREFACE

This report is issued by Poyry Forest Industry Pty Ltd (Pöyry) to the Department of Agriculture, Fisheries and Forestry (DAFF) for its own use. No responsibility is accepted for any other use.

The report provides a methodology for categorising imported wood products by illegality risk. The report also contains the opinion of Pöyry as to the usefulness of previous methodologies for quantifying trade in illegally-sourced wood products.

Pöyry has no responsibility to update this report for events and circumstances occurring after the date of this report.

Grant Fenton Rudolf van Rensburg

SENIOR CONSULTANT SENIOR CONSULTANT

Contact details:

Grant FentonLevel 5, (Box 22)437 St. Kilda RoadMELBOURNE, VIC 3004AustraliaTel. +61 3 9863 3700Fax +61 3 9863 3707

Poyry Forest Industry Pty Ltd

Copyright © Pöyry Forest Industryi

51A11995

SUMMARY

Poyry Forest Industry Ltd (Pöyry) has been engaged by the Department of Agriculture, Fisheries and Forestry (DAFF) to review existing methodologies for assessing illegality of imported timber and wood products. Based on this review, Poyry was to develop a more accurate and reliable methodology for quantifying the volume and value of illegally-sourced wood products imported into Australia. This project supports the Australian Government’s commitment to combat illegal logging and associated trade.

The methodology review concluded that the current methods lacked reliable data on which to base policy. Problems were found at each stage in the wood supply chain from accurate knowledge of the operating and regulatory environments covering sustainability and “legality” of forest management and timber harvesting, to data tracking the often complex log and subsequent product flows from the forests to primary and secondary manufacturing. Further complicating the situation is that much wood crosses borders via transhipment of logs and timber products from producer countries to secondary manufacturing countries and from there to consumer countries. When coupled with the imprecision in current trade statistics the review concluded that current methods to estimate volumes or values of timber and wood product imports from illegal sources are very unreliable.

These findings led Poyry to develop an alternative approach that is based on developing a risk assessment framework based on transparent assessments of governance arrangements within wood supplying countries.

Review of existing Methodologies and Approaches

Limited literature exists which either develops or describes in detail a methodology to estimate the volume and value of illegally logged timber and wood product trade. Most of this literature is limited to examining the process of the illegal timber trade and the legislative framework. Referenced academic research and scientific studies mainly focus on the environmental issues associated with illegal logging, rather than issues associated with illegal trade of timber and wood products.

The reviewed analyses used primarily secondary data sources, including unqualified estimates, anecdotal evidence, or were based on limited research. Many reports on illegal logging did not assess the accuracy or reliability of illegal logging estimates, and therefore can leave readers with a false impression of precision which can then be perpetrated via citations in other papers. We saw a number of instances where specific estimates were repeated in the reviewed reports with the citations occuring as circular references, and are not linked to the original source.

The following overviews the three most prevalent components of the methodologies reviewed. These include the mass balance approach, trade statistic discrepancies, and the application of country-level corruption indices. In some instances, these quantitative calculations were supported by qualitative assessments based on field investigation and interviews.

Copyright © Pöyry Forest Industryii

51A11995

Mass Balance ApproachThe mass balance approach maps timber flows for each country to identify discrepancies between legal log removals, legal imports, domestic production and exports. For this approach to be effective, it should be possible to compare reported export volumes with the mass balance estimates of export volumes. The usefulness of this method depends on the accuracy and availability of log supply data. However, this data is frequently unreliable and incomplete.The discrepancy between reported harvesting and actual supply can only be measured if reliable domestic wood to product conversion rates and production figures are available. Commonly, in many of the key wood product producing countries such as Indonesia, Malaysia and China, the downstream processing industry is extremely fragmented, particularly the sawn wood sector. In many sectors (especially sawmilling) it is impossible to estimate either the installed capacity, or to quantify production.

The mass balance approach is complex and difficult to calculate even in developed countries, where one would expect reasonably reliable trade and production data to be available.

Export Statistics

The comparison of export statistics from source countries with import statistics from receiving countries has been used in previous methodologies as an approach to identify potential illegally-sourced wood. However, analysis of trade data alone cannot be used to accurately estimate illegally-sourced trade. A review of regional trade statistics highlighted numerous discrepancies, including the misreporting of volume, incorrect HS-code classifications and the use of ‘Other’ as a description for a significant volume of trade. It is evident that, although value is consolidated and reported at the product group level, import volumes simply cannot be reported this way due to differences in the physical measurement processes between countries.

Corruption Indices

The application of country level corruption indices has been used to estimate volumes and values for illegal logging and the processing and trade in illegally-logged timber products. This approach relies on there being a definable relationship between the corruption indices and the volume and value of production. However, corruption indices are broadly based measures (that include non-forestry activities) and therefore do not necessarily capture the regulatory environment specific to the forest industry and the changes in that environment over time. For example, South Africa has a medium CPI, yet the forest industry in South Africa is largely based on plantation-sourced logs supplied by mostly private companies who have achieved FSC.

Risk Assessment Framework

Pöyry has considered the limitations of the previous methodologies applied in this area and has attempted to utilise the appropriate elements of these processes to develop a more robust methodology. Our research shows that direct quantification

Copyright © Pöyry Forest Industryiii

51A11995

of the volume and value of illegally-sourced wood products is extremely difficult, if not impossible, to measure with sufficient accuracy to produce reliable estimates. Rather than relying on an absolute figure for illegally-sourced wood product imports, the proposed methodology focuses on an assessment of risk of illegally sourcing imports based on the governance of the industry and regulatory environment in the country of harvest or production. The assessment process could apply to the forestry-growing and processing industry in each country, the individual industry sectors or even to individual products (such as sawn timber, paper or engineered wood products at the six-digit HS code level of differentiation.

This risk-based methodology stages are:

Stage 1 – Product Selection: The first stage in the process is to select the products or product groups to be assessed. Products are identified according to the World Customs Organisation Harmonised Commodity Description and Coding System (HS) to different HS code categories (e.g. 4 or 6 digit code according to the nature of the wood products for which risk of illegality is to be determined).

Stage 2 – Exporting Country Identification: Once a product/HS code has been selected, the import values of this product can be broken down by source country.

Stage 3 – Domestic Risk Assessment: The domestic risk assessment considers three risk areas; country-level corruption, industry governance (government) and industry measures. This assessment stage has deliberately been broadened to reduce reliance on the country-level risk factors alone, which we found to create potentially misleading impressions for certain countries with more robust industry-specific measures to control illegal activities. Consequently, the domestic risk assessment considers aspects such as forest management policy, regulatory environment and enforcement. The risk rating for an exporting country is more focused on the risk factors of industry governance rather than on the country as a whole. Industry measures are important to capture, but difficult to assess in a quantitative and consistent fashion. We believe recognised certification scheme accreditation offers a viable proxy to a qualitative assessment. Products manufactured using domestically-sourced raw material that is certified shall be considered low risk.

Stage 4 – Fibre Supply Surety: This stage of the assessment evaluates the percentage of imported raw material used to produce any given product in any given country. This percentage of the product is assigned a risk factor in line with the risk(s) associated with the supplying country(ies).

Stage 5 – Risk Rating: In this stage, the stage 3 and 4 risk ratings are combined to create an overall risk rating that incorporates the Domestic Risk and Fibre Supply Surety risk dimensions.

Further Development

The development required to enable the methodology to be implemented is detailed below.

The Domestic Risk Model requires further development through a stakeholder and industry expert consultation process. Discussion with organisations such as

Copyright © Pöyry Forest Industryiv

51A11995

Transparency International, ITTO and the World Bank, which have in-country experience, would be a logical starting point.

We recommend that the output from the DAFF commissioned report of forest certification schemes be assessed for inclusion in this methodology to assist with the risk assessment.

A database is required with the appropriate processing capability and functionality to process the large volume of trade statistics and to apply the respective industry, country-level and fibre surety risk factors.

The various review processes (frequency of review etc.) must be developed and responsibilities assigned.

Benefits of this Approach

The methodology has been developed to be implemented in Australia however the application of this methodology on a regional level is possible and a regionally coordinated approach will likely improve the chances of driving change in governance and reduce the diversion of suspect product to less discerning markets.

The methodology presented will provide a sufficiently reliable result while remaining straightforward to implement. Outputs from this process can be used to provide a risk assessment at the country, sector or six-digit HS code levels for forest products.

The results of the risk analyses can be used to track the success of initiatives to reduce the trade in illegally-sourced wood products in each of the supply countries. Risk profile adjustments will be subject to changes in the forestry governance arrangements which are observable over time.

The results can also be used by Australian importers as an information source of supply risk. The methodology could be adopted by industry associations, or at the regional level through one of the forestry processes. The results of the risk analyses should be a key consideration in the development of Industry codes with regard imported wood based products. By operating at the industry, sector or six-digit HS code level, this methodology would provide an important input for estimating the risk that products are derived from illegally-harvested sources. Importers could then seek to procure products covered by legally-sourced wood verification systems that have the capacity to address the level of risk that has been identified during the due diligence process.

Copyright © Pöyry Forest Industryv

51A11995

CONTENTS

PREFACE I

SUMMARYII

1 INTRODUCTION 1

2 LITERATURE REVIEW 3

2.1 Key Findings 32.2 Analysis of existing Approaches 42.2.1 Mass Balance Approach 52.2.2 Trade Statistics Discrepancies 62.2.3 Country-Level Corruption Indices 8

3 METHODOLOGY 10

3.1 Conceptual Framework 113.1.1 Process Stage Explanation 123.1.2 Worked Example for >6mm HW Sawnwood (HS440729) 193.2 Further Development of Methodology 233.3 Implementation of the Methodology 24

APPENDIX 1: LITERATURE REVIEW A1-1

APPENDIX 2A: AUSTRALIAN TRADE STATISTICS A2A-1

1 AUSTRALIAN TRADE STATISTICS 1

1.1 Introduction 11.2 Product Selection and Country of Origin 11.3 Product Sub-codes 71.4 Furniture 71.5 Paper and Board 101.6 Wood 15

APPENDIX 2B – IMPORT TABLES A2B-1

Appendix 3 – SFM Certification and Chain of Custody A3-1

Copyright © Pöyry Forest Industryvi

51A11995

1 INTRODUCTION

The consideration of an illegal logging policy to support the Government’s election commitments is a priority for the Department of Agriculture, Fisheries and Forestry (DAFF). In support of this work, the Forest and Wood Products Council (FWPC) has recommended the need for an up-to-date assessment of the risk, volume and value of illegally logged timber and wood products imported into Australia.

Ideally, development of a reliable methodology to assess which sources of wood and wood products were from legally-sourced supplies and which were not would be straightforward. In this ideal world, necessary production, import and export data and legal harvesting approval processes would be readily available and transparency would be the norm.

Unfortunately, based on our on-ground experience underscored by the knowledge gained from the literature review, the data needed to ascertain legality of wood is imperfect, and transparency associated with governance and management of timber production forests is limited. In the most glaring example of data shortcomings, import declarations (sawnwood, furniture, paper products, wood-based panels) do not currently require the country of origin (country of harvest) to be recorded. This means that furniture imported from China could incorporate wood from illegally-sourced logs from Congo and there would be no way to flag these imports as containing illegally-sourced wood.

We recognised early on the constraints imposed by data limitations and consequently went back to first principles to develop an alternative approach to quantifying illegally-sourced wood product imports.

One of the first stumbling blocks of any approach to this issue is dealing with the question of what constitutes a legal source of wood and what is an illegal source? We found many different definitions of “legality” in the literature review (Appendix 1). In our view, none of these allow a reliable practical demarcation between legally-sourced product and illegally-sourced product. By practical we mean a process that could be applied routinely to the range of wood products imported to this country.

Given the data limitations set out above we believe that such binary demarcation is simply not possible and consequently we did not attempt to formally assign products as being legally- or illegally-sourced. Instead, we have developed a risk-profiling approach to assign a higher or lower risk of a wood product being from illegal sources. The risk can be quantified by applying subjective and quantitative criteria that rely on a combination of country- and industry-specific expert knowledge, and reliable data from known sources.

The new element in the proposed method is that the assessment of governance extends from the national (exporting country) level through the industry sector level to the product level. Under this model, improvements in industry-specific governance through greater transparency and accountability of the legality of their business practices supported by monitoring and auditing requirements, enables the risk associated with a particular product sourced from a specific country to be adjusted accordingly. This allows a more nuanced evaluation of risk versus the alternative of applying the overall country risk, commonly measured by the

Copyright © Pöyry Forest Industry1

51A11995

Corruption Perception Index (“CPI”), and applying that across the board to the wood products-based industry in that country.

This report explains the conceptual framework for the proposed methodology which, if implemented, will enable a more robust assessment of the risk of importing illegally logged timber and wood products into Australia. In addition, components of the proposed methodology may also be utilised by importers to more accurately assess the legality risk of their timber and wood product imports in line with an industry code of conduct for the procurement of legally sourced timber and wood products.

The process followed by Pöyry in undertaking this study is illustrated Figure 1-1.Figure 1-1:Project Process

DAFF/Poyry kick off meeting

Project Methodology

Literature review

Australian Import Statistics

Review

SynopsisCritique

DAFF workshop

- Product identification

- Country Selection

Country ReviewDraft

methodology DAFF workshop Draft Report

Pöyry’s proposed methodology will be guided by the limitations of existing methodologies identified in the literature review, the trade statistics and in-country analyses of governance arrangements for both government and industry.

An example of the assessment process and resultant risk rating is provided for a hardwood sawnwood product. The methodology can also be applied to other products and sectors. We propose the following product categories as a way to ensure national consistency in the classification of products when applying the due diligence risk management process at a more targeted level:

Solid wood products;

Composite wood products;

Manufactured wood products;

Other manufactured wood products;

Wood packaging and pallets;

Pulp, paper and paperboard;

Other paper and paperboard products;

Wood fibre products; and

Other products of wood origin.

Copyright © Pöyry Forest Industry2

51A11995

2 LITERATURE REVIEW

The literature review was used to identify and to better understand previously reported methodologies for quantifying the volume of trade in illegal timber and wood products. This was also used to identify weaknesses or limitations as the basis for developing an alternative methodology. The focus of the review was on the forest product trade within countries in the Asia-Pacific region, although we canvassed publications from a much broader list of countries and regions to capture the key methodologies.

The key publications reviewed included:

Seneca Creek Associates and Wood Resources International 2004,” “Illegal” Logging and Global Wood Markets: The Competitive Impacts on the U.S. Wood Products Industry”. American Forest and Paper Association.

Pöyry Forest Industry, 2005, “Overview of illegal logging”. DAFF.

Schloenhardt, A., 2008. “The illegal trade in timber and timber products in the Asia Pacific region”, Australian Institute of Criminology, Canberra.

WWF, 2008. “Illegal wood for the European market”.

Smith, W., 2002. “The global problem of illegal logging”, ITTO Tropical forest update, Vol. 10, No 1. 2002.

Guertin, C., 2003. “Illegal logging and illegal activities in the forestry sector: Overview and possible issues for the UNECE Timber Committee and FAO European Forestry Commission”, Quebec wood export bureau.

FERN, 2002. “Illegal logging and the global trade in illegally-sourced timber; a crime against forests and people”.

Chatham House, 2004. “FLEGT & Trade- What will the impacts be?”, Royal Institute of International Affairs, London.

SCION, “Implications for the New Zealand Wood Products Sector of Trade Distortions due to Illegal Logging”. Ministry of Agriculture and Forestry. 2007

Limited literature exists which either develops or describes in detail a methodology to estimate the volume and value of illegally logged timber and wood product trade. The majority of this literature is limited to estimating the extent of illegal timber trade within a legislative and governance framework based primarily on an assessment of the broad corruption indices for individual countries. Most referenced academic research and scientific studies focus on the environmental issues associated with illegal logging, rather than issues of illegal trade.

2.1 Key Findings

The methodologies used to quantify legality typically lack robustness or reliability.

The data utilised in many of these analyses has been secondary, based on anecdotal evidence or on limited research.

Copyright © Pöyry Forest Industry3

51A11995

Many reports lack an assessment of the accuracy or reliability of illegal logging estimates.

The same estimates that appear in many of the reviewed reports rely on circular references, and are not linked to the original source. Only a small number of core documents provide the foundation for subsequent works.

Many of the published quantification approaches have relied significantly on country-based criteria such as the Corruption Perception Index (CPI) produced by Transparency International.

A process for accurately quantifying the illegal wood products trade is extremely difficult without significant investment in a much-improved data collection system.

There are many definitions of “illegal” in the literature, illustrating the difficulty in defining the term. Some parties include unsustainable harvesting as illegal, whilst others consider all harvested wood supplied with the appropriate permits and approvals, no matter the risk of corruption within the approval process, to be legal.

Some of the literature reviewed describes the product in question as ‘suspect’ rather than illegal. The classification or ‘suspect’ avoids the definitive classification of ‘illegal’ which is difficult to defend given the limitations in the methodologies and data reliability.

The likelihood of diversion of illegal wood products to less discerning markets is considered high. This increases the importance of understanding the supply chain for converted or reprocessed products. Pöyry have described this in the methodology developed as ‘Fibre supply surety’.

Much of what is considered illegal or high risk is processed domestically into wood products and furniture. This increases the difficulty in utilising trade statistic discrepancies and mass balance approach to estimate illegal logging activity.

The Seneca Creeki, 2004 report, which has become a key source document, for many subsequent reports, employs logical methods, including assessments of the reliability and accuracy of estimates to quantify the illegal trade of wood products from source countries. The authors recognise the limitations in the accuracy of the results due to limited practicable methods and lack of access to reliable data, not as a result of error or lack of diligence. The Seneca report utilises the classification of ‘suspicious’ rather than ‘illegal’. This may reflect the belief that making defendable statements regarding quantification of illegal or legal volume is currently impossible.

The full literature review is provided in Appendix 1.

2.2 Analysis of existing Approaches

Three primary methods are currently used: the mass balance approach, trade statistics review and the application of country-level corruption indices. We reviewed each and tested them to identify strengths and weaknesses of the methodologies, and usefulness of results generated. As an adjunct we also identified components that could be incorporated into an alternative methodology.

Copyright © Pöyry Forest Industry4

51A11995

2.2.1 Mass Balance ApproachThe mass balance approach, or input-output modelling, as it is sometimes called, maps timber trade flows for each country to identify discrepancies between legal log removals, legal imports, domestic production and exports. In theory, it should be possible to compare reported export volumes, as captured by the exporting countries’ customs or port authority data, with the actual export volumes.This approach has been used in a number of studies to estimate illegal logging activity. However, for the reasons set out below, this approach provides at best an indication of a potential problem and cannot be used to accurately quantify the value or volume of illegal harvesting or trade.The method relies on having access to accurate log supply data, including imported logs. The Seneca Creek report concluded that the majority of illegally-harvested logs are consumed domestically giving rise to illegally-sourced lumber and other wood products that may then be exported. In terms of logs, discrepancies between reported harvesting and actual supply could only be estimated and reconciled if reliable domestic log consumption figures were available. However, in many of the key wood product producing countries, such as Indonesia, Malaysia and China, the downstream processing industry is extremely fragmented, particularly for sawnwood and therefore log consumption numbers are not reliably known.In conclusion, in these countries the installed capacity for timber processing is unknown, and therefore to quantify domestic wood product production or domestic log consumption. This problem manifests itself in different ways, but often in the data. The published data is often contradictory and inconsistent, indicating a high level of error or inaccuracy in recording. The following examples illustrate this point. In Figure 2-2 annual production statistics for a range of wood products change erratically year on year as reported by a single source.Figure 2-2:Indonesian Wood Product Production, 2000 - 2008

0

2

4

6

8

10

12

14

16

2000 2001 2002 2003 2004 2005 2006 2007 2008

- million m3/tonne -

Others

Pulp (Ton)

Particle board

Chipwood

Veneer

Sawntimber

Plywood

Source: Indonesian MoF

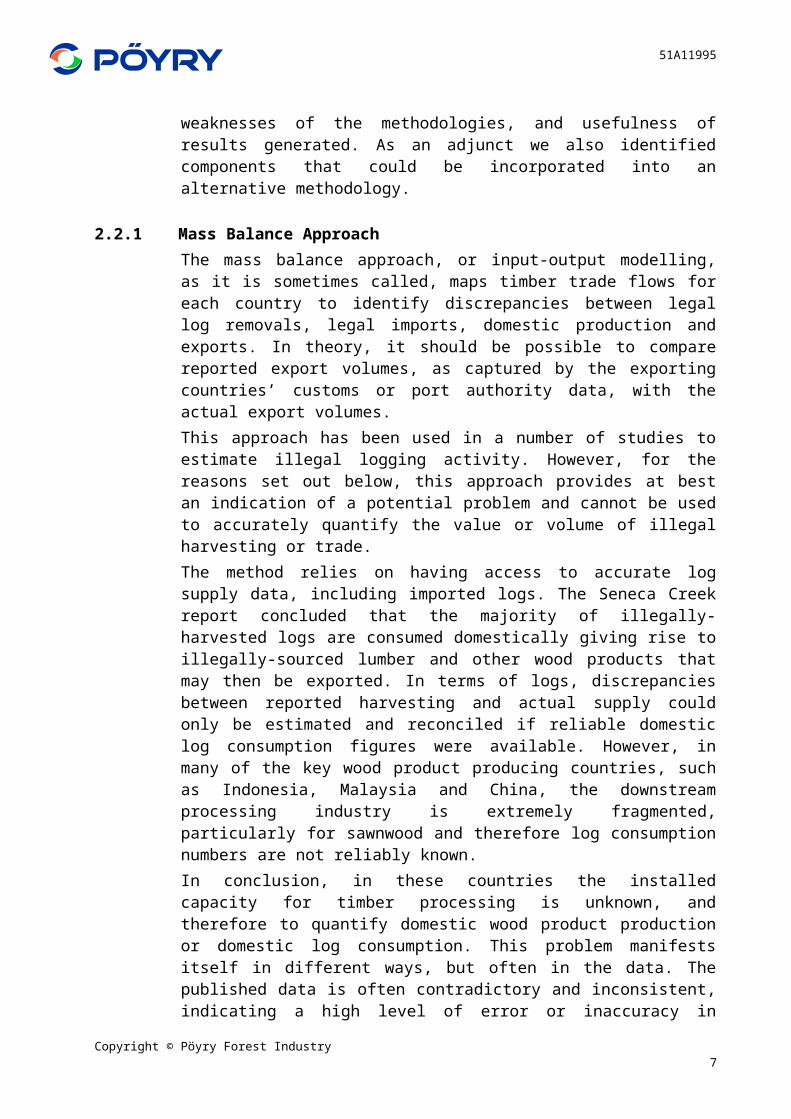

Figure 2-3 compares Indonesian pulp production figures for the years 2003 to 2007 as reported by the Ministry of Forestry, the Ministry of Industry and FAO. Significant discrepancies show up among the data sets, with no discernable pattern

Copyright © Pöyry Forest Industry5

51A11995

of deviation. Consequently, the output of any mass balance calculation and therefore the conclusions reached, would vary considerably depending on which data were used. These inconsistencies in data make it difficult to know which source to use in calculating the mass balance.Figure 2-3:Indonesian Pulp Production by Source, 2003-2007

0

1

2

3

4

5

6

7

2003 2004 2005 2006 2007

- million tonne -

Pulp MoF Pulp MoI Pulp FAO

Source: Indonesian MoF, MoI, FAO

When production figures of acceptable reliability are available, it is possible to convert these to Round Wood Equivalent (RWE). RWE is the volume of roundwood (or logs) required to manufacture these products and is calculated by applying country and industry-specific conversion factors. Unfortunately, these conversion factors vary widely country to country and even within countries. The differences arise because of factors such as log size and shape, processing technology, and product mix. As an example, planed and (usually dried) appearance timbers have a lower recovery than rough sawn structural timbers. If the RWE-calculated consumption figure is significantly different to the reported or official figure, then this points to a problem, possibly with data collection, but does not necessarily constitute illegality. In Malaysia, for example, small-scale harvesting does not require a permit, and therefore the volume of logs from these ‘private’ (but legal) supplies is not captured in official statistics.The method also relies heavily on comparison of calculated and reported trade figures. However, as the next section details, there are documented sources of inaccuracy in reported trade figures.

2.2.2 Trade Statistics Discrepancies

Another approach to identifying potential illegally-sourced wood products is to compare export statistics from the source country with import statistics from the receiving country. This exercise highlights a number of large discrepancies which indicate why analysis of trade data alone cannot be used to accurately estimate illegally-sourced trade:

Copyright © Pöyry Forest Industry6

51A11995

Trade figures can potentially include illegally-sourced wood products that have been exported legally and fully reported, i.e. the data for both exporting and importing countries will be consistent.

Volumes of illegal products may bypass controls in both the export and import countries as may legally produced product in order to avoid duties and customs. This may include smuggling or involve corruption at the port.

Descriptions of the World Customs Organisation Harmonised System are sometimes unclear and do not cover all products in sufficient detail to differentiate all products of interest from a legality perspective. As a result, inconsistencies in the classification of products, either intentionally or by mistake, may occur.

Recording to the incorrect code may be used to avoid export and import duties.

Mistakes in data capture are evident. These can be as simple as a misplaced decimal point.

The export country typically reports the value at Free on Board (FOB)ii, whereas the importing country typically declares a Cost Insurance & Freight (CIF)iii or Custom Import Value (CV) value. This can make reconciliation and discrepancy identification extremely difficult and create considerable inaccuracies. Although Australian Customs captures the data to make a single-value estimate of annual trade, the supporting data inputs are not publicly available.

Each country has its own system and associated reliability or diligence in collecting and collating the data.

The timing of the data capture creates discrepancies.

The use of ‘other’ for describing significant volumes of product is prevalent. This may be difficult to avoid without adding further complexity or levels to the HS system.

The classification of large volumes of paper products as ‘Country not specified’ has been noted. This is particularly evident for coated and uncoated paper imports.

Level of detail in product description and classification is lacking and perhaps difficult to improve on, given the already complex nature of the Harmonised System.

Copyright © Pöyry Forest Industry7

51A11995

Although the importation of wood species listed by CITES iv can only be undertaken with an importation license, available statistics do not indicate volumes of such products. One might assume that the granting of a license provides some assurance of legality.

Australian Customs does not record the species of solid wood products imported, nor whether certification under a recognised scheme has been achieved.

2.2.3 Country-Level Corruption Indices

Corruption indices have been utilised in a number of illegal logging and wood product studies. Since the correlation was made as part of the Seneca report, many have applied a corruption index factor to estimate illegal activity. There is some merit in applying this factor. However, it is commonly criticised for being overly simplistic. The corruption indices available can be of real value, but they are not usually adjusted to reflect the industry-specific risk or industry governance.

Nevertheless, there appears to be a strong correlation between the CPI and the perceived risk of illegal forest products being exported from key supply countries. However, use of a corruption index at a country level will not capture the robustness and enforcement of the systems within the forestry sector. Some countries ranked medium or high on the corruption index may already have appropriate forestry regulations, monitoring, auditing and enforcement in place.

Hence to be of real value, the CPI must be supported by other relevant analyses on an industry or product level. South Africa is a good example of this point. This country scores 4.9/10 on the Transparency International 2008 corruption index, which if applied in isolation would indicate a medium risk of sourcing illegal forest products. However, the forest industry in South Africa processes mainly plantation-sourced logs with over 85% of plantations FSC certified. The forestry sector is rigorously controlled by mostly private companies. Consequently, despite its unfavourable CPI rating, South Africa has a very low risk as a source of illegal logs or wood products.

Figure 2-4 illustrates how the risk ranking of South Africa may change if measured at an industry level rather than on the basis of the country level CPI.

Copyright © Pöyry Forest Industry8

51A11995

Figure 2-4:Perceived Corruption Relationship to % suspected illegal Supply

Our conclusion from the literature review and our review of the methodologies for estimating illegally-sourced wood is that direct quantification of volume and value of illegally-sourced wood products is extremely difficult, if not impossible, due to data limitations.

Copyright © Pöyry Forest Industry9

51A11995

3 METHODOLOGY

The lack of an available method to recommend for DAFF to apply to estimate illegally-sourced logs and wood products imports to Australia has led the report authors to develop the methodology outlined in this section as a practical way to circumvent these limitations.

The Pöyry approach assesses legality in terms of potential risk, using risk factors and criteria that we believe can provide a more reliable estimate. Rather than producing an absolute figure for illegally-sourced wood products, the methodology presented creates a framework for assessing the risk that timber and wood products are associated with illegally-sourced logs, and this can be applied periodically to flag changes as a consequence of improvements in governance. In addition, the risk assessment can be applied to a type of product or industry sector for individual countries.

As noted, changes in risk level will largely be driven by changes in governance both at a national-government and industry-sector level. This method may be applied to track the performance of initiatives of producer countries to reduce the importation of illegally-sourced timber and wood products.

Previous reports and methodologies focus on quantification at a point in time. The intention of this approach is to have a methodology that tracks progress in reducing illegally-sourced wood products. Such a tool would assist any future assessment of the effectiveness of policies developed to combat illegal logging and associated trade. Therefore, the method is intended to deliver confidence in the risk assessments generated, and also to be consistently replicable to detect change.

The methodology developed depends on the reliability of country import statistics. The analysis of wood product trade statistics has highlighted a need to improve reporting and reliability in some areas. A review of Australian import statistics and key imported wood products is provided in Appendix 2A.

We have allowed for the later inclusion of certification status as an element of the methodology, but have not considered this in the current process. This is because certification status is not currently captured by Australian customs, but is known to the importer. Pöyry believes certification status is an important factor which Australian importers could use as part of a responsible purchasing policy. A number of certification schemes focus on sustainability, while others focus only on verifying the legal origins of timber and wood products. The performance of some of these schemes is being independently assessed by a separate consultancy for DAFF, and we recommend that the output from this other report be assessed for inclusion in this methodology to assist with the risk assessment.

Copyright © Pöyry Forest Industry10

51A11995

3.1 Conceptual Framework

A five-stage methodology has been developed, as illustrated in Figure 3-5 below.Figure 3-5:Methodology Flow Diagram

ProductIdentification(HS codes ex

Australian customs)

Stage 1ProductIdentificationIdentifies imported productdown to 4-6 digit HarmonisedCommodity Description and CodingSystem (HS code)

Stage 3aDomestic Risk AssessmentEvaluates and weights the risk thatdomestic sources of logs to producethe product are from illegal sourcesusing 2 criteria: National (CPI) andIndustry Governance by Government

Stage 2Export CountryIdentificationIdentifies the country that is thesource of the imported product

Product 1 Product 2 Product 3

Country 1 Country 2 Country 3

Risk Factor Weighting Weighted Risk

CPI (country level)- published corruption index from

reputable source%

Industry Governance(Government)

Structured Forest PlanningRegulatory Environment

Transparency & AccountabilityEnforcement

Industry/Trade Data

%

Total Weighted Domestic Risk

Stage 4Fibre SupplySurety AssessmentEvaluates the risk that knownsources of imported fibre used toproduce the product imported toAustralia were from illegal sources

Risk Factor

legality of imported fibre supply- Identify source country (may not be country of origin)

- Apply Domestic Risk value-Consideration of domestic import controls

Total Imported Fibre Supply Risk by Each Supply Country

Stage 5Risk RatingProvides an aggregated riskrating for a specific product/country

Risk Factor x Risk rating

Total weighted domestic risk-CPI and Governance

% of fibre supplythat is from

domestic sources(not certified)

-

- Industry measures % of fibre supplycertified -

Total Imported fibre supply risk -Country 1

% of fibre supplyex country 1 -

Total Imported fibre supply risk -Country 2

% of fibre supplyex country 2 -

Total Imported fibre supply risk -Country ....

% of fibre supplyex country 3 -

Total Risk Rating

Stage 3bDomestic Risk AssessmentApplies a lower risk rating to theportion of imports that is known to becertified under a recognised scheme(this component of the DomesticRisk Model to be developed followingcertification scheme reviewconsultancy being undertaken forDAFF)

Risk Factor

Industry MeasuresPortion of Certified product is caterorised as low risk

Total % Certified

Copyright © Pöyry Forest Industry11

51A11995

The following explains in more detail each stage of the process and the further work required to bring this into practical application. This is followed by a worked example using >6mm HW sawnwood (HS440729) to illustrate how the methodology is applied.

3.1.1 Process Stage Explanation

Stage 1 - Product Selection

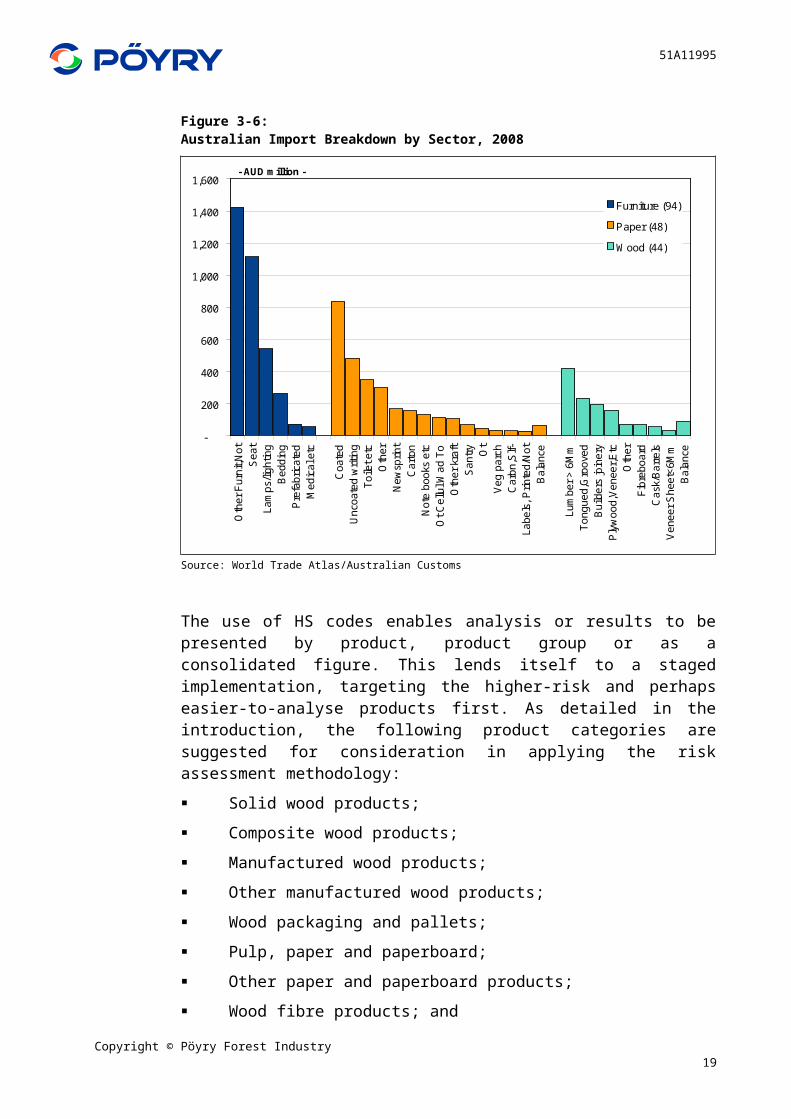

The first stage in the process is to select the products or product groups to be assessed. Products are identified according to the World Customs Organisation Harmonised Commodity Description and Coding System (HS) to different HS code categories (e.g. 4 or 6 digit according to the nature of the wood products for which risk of illegality is to be determined). This classification provides the consistency needed to ensure outputs are comparable over time. The three key product groups selected for more detailed review in this study are solid wood products and panels (HS44), paper products (HS48) and furniture (HS94). Figure 3-6 presents the product groups for the three key import categories down to a 4-digit HS code. These products are further broken down (to 6-digit HS level) in Appendix 2B.

For the purpose of illustrating the methodology >6mm HW sawnwood (HS440729) has been selected and we have taken this through the 5-stage process in the following section.Figure 3-6:Australian Import Breakdown by Sector, 2008

-

200

400

600

800

1,000

1,200

1,400

1,600

Oth

er F

urni

t,Not

Sea

tLa

mps

/ligh

ting

Bed

ding

Pre

fabr

icat

edM

edic

al e

tc

Coa

ted

Unc

oate

d w

ritin

gTo

ilet e

tcO

ther

New

sprin

tC

arto

nN

ote

book

s et

cO

t Cel

lul W

ad T

oO

ther

kra

ftS

antry O

tV

eg p

arch

Car

bn,S

lf-La

bels

, Prin

ted/

Not

Bal

ance

Lum

ber >

6M

mTo

ngue

d,G

roov

edB

uild

ers

join

ery

Ply

woo

d,V

enee

r,Etc

Oth

erFi

breb

oard

Cas

k/B

arre

lsV

enee

r She

et<6

Mm

Bal

ance

- AUD million -

Furniture (94)

Paper (48)

Wood (44)

Source: World Trade Atlas/Australian Customs

Copyright © Pöyry Forest Industry12

51A11995

The use of HS codes enables analysis or results to be presented by product, product group or as a consolidated figure. This lends itself to a staged implementation, targeting the higher-risk and perhaps easier-to-analyse products first. As detailed in the introduction, the following product categories are suggested for consideration in applying the risk assessment methodology:

Solid wood products;

Composite wood products;

Manufactured wood products;

Other manufactured wood products;

Wood packaging and pallets;

Pulp, paper and paperboard;

Other paper and paperboard products;

Wood fibre products; and

Other products of wood origin.

Domestic risk assessments for imported products produced from recycled and plantation-grown softwood fibre, such as newsprint, which have good forest governance arrangements and accredited systems of management in place, may be readily determined and may be accorded lower priority. In contrast, products sourced primarily from logs harvested from native forests, especially from tropical hardwood forests, will typically require more rigorous assessment. This is because these products are less likely to be supplied from sources with well-established governance arrangements and management systems. For the same reason more rigorous assessments will also likely be needed for product primarily obtained from less-structured sources such as small to medium enterprises, customary owners and local forest communities, in developing countries.

Stage 2 – Exporting Country Identification

Once a product/HS code has been selected, the import values of this product can be broken down by source country. Our research indicates that 95% of the total imported value for each selected product typically comes from a small number of countries. Consequently, we recommend focusing more resources on analysing these main supply countries, and fewer resources on the minor import countries. Country-level risk assessment is detailed in Stage 3.

The Australian customs import statistics, as made available by World Trade Atlas (WTA), identify the exporting or source country for wood product imports to Australia. However this may not be the original source country for the logs (or lumber) used to produce the product and this issue is dealt with in Stage 4 of the methodology.

Copyright © Pöyry Forest Industry13

51A11995

Stage 3 – Domestic Risk Assessment

The Domestic Risk Model (DRM) has three components:

1. Country-level corruption

2. Industry Governance (Government)

3. Industry Measures.

Component 1 – Country-Level Corruption

Measurement of country level corruption is possible through publicly available corruption perception indices. Pöyry has reviewed corruption indices published by the Global Integrity Index and Transparency International. The Corruption Perception Index (CPI) produced by Transparency International, has been selected as a basis for this methodology. This index has a comprehensive listing of countries, providing a country ranking and an absolute score from 1 to 10. It is this absolute score that is applied to the model.

The Corruption Perceptions Index (CPI) measures the perceived level of public-sector corruption in 180 countries and territories around the world. The CPI is a "survey of surveys", based on 13 different expert and business surveys.

The CPI 2009 is calculated using data from the following independent organisations:

Africa Development Bank- Country Policy and Institutional Assessments 2008

Asian Development Bank -Country Performance Assessment Ratings

Bertelsmann Foundation- Bertelsmann Transformation Index

Economist Intelligence Unit -Country Risk Service and Country Forecast 2009

Freedom House -Nations in Transit 2009

Global Insights, formerly World Markets Research Centre- Country Risk Ratings 2009

Institute for Management Development - World Competitiveness Report 2008 and 2009

Political and Economic Risk Consultancy, Hong Kong - Asian Intelligence 2008 and 2009

World Economic Forum - Global Competitiveness Report 2008 and 2009 (WEF 2008 and

World Bank - Country Policy and Institutional Assessments for IDA Countries (WB 2008).

Not all sources rank all countries of the index. Because the coverage of these surveys and assessments is not identical, the number of sources from which each country’s score is derived is not the same for all countries. A country must be covered by a minimum of 3 different sources to be ranked in the CPI. A full explanation of the Transparency International Corruption Perception Index is

Copyright © Pöyry Forest Industry14

51A11995

available at: www.transparency.org/policy_research/surveys_indicies/cpi/2009/methodology

The Transparency International CPI ranking applies a value from 1 to 10. The higher the number, the lower the level of perceived corruption. This score will be weighted as a component of the DRM.

Component 2 – Industry Governance (Government)

In our experience, much of the risk of illegally-sourced wood arises due to poor forestry sector governance at the national and/or regional government levels. Consequently, Component 2 of the methodology, assessment of industry governance, is primarily concerned with the regulatory environment, and focuses on controls at a national or regional government level.

By its very definition, illegality implies the breaking of laws or regulations. Consequently, we have developed criteria to first identify what laws/regulations countries/jurisdictions have in place to control the management and harvest of logs. We then seek to understand whether those laws/regulations are being implemented.

From the literature review we found that little work has been done to evaluate the quality of governance in the forestry sector. Consequently, given the importance of the governance assessment to the proposed methodology, significant effort will be required to develop robust governance assessment criteria. We believe that despite having an Australian import focus, the resulting criteria would also be applicable for other countries seeking to evaluate illegally-sourced wood.

Forest industry governance instruments and process, and the diligence (and independence) with which they are implemented differ widely among countries exporting forest products into Australia. Given this diversity, we believe this component of the domestic risk evaluation is most appropriately quantified by benchmarking the instruments and processes in source countries against criteria that specify the governance processes we believe to be essential to limit the risk of illegal logging.

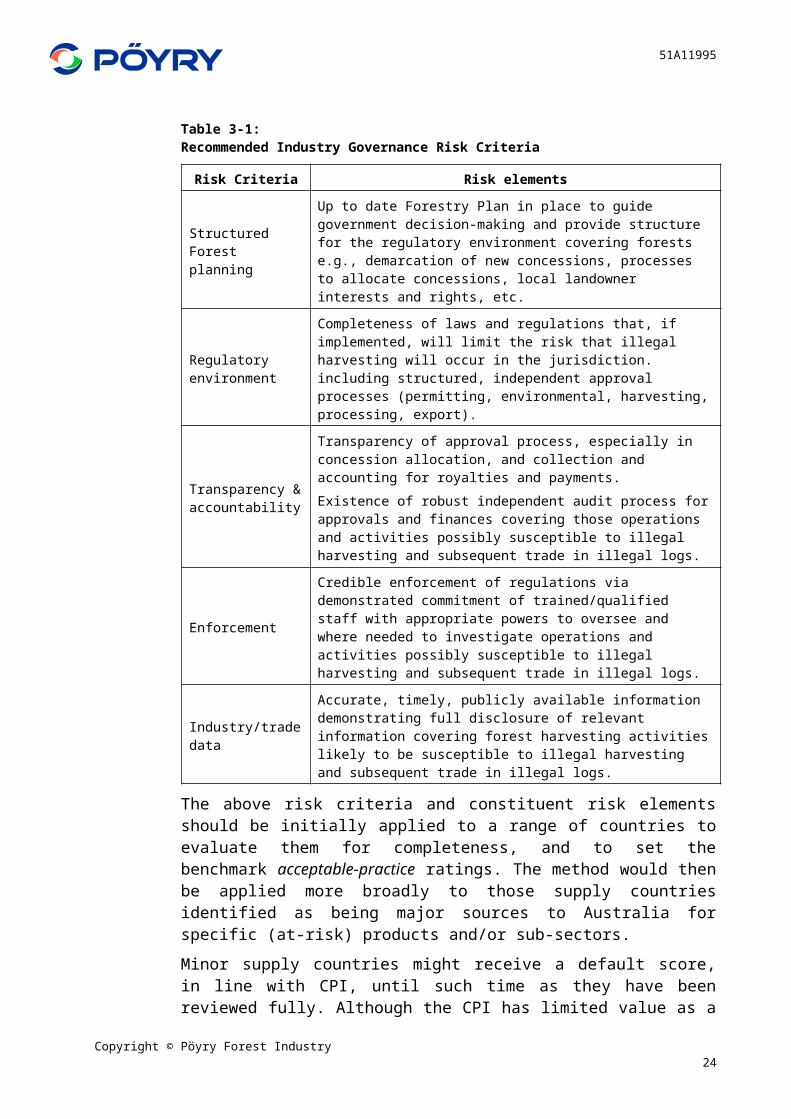

The following are our recommended industry governance risk criteria (.). We believe these criteria cover the key instruments and mechanisms governments use to control forestry operations taking place under their jurisdiction. We have broken these risk criteria down to constituent risk elements that provide further clarity as to the specific industry governance elements to be used to evaluate supply countries.

Copyright © Pöyry Forest Industry15

51A11995

Table 3-1:Recommended Industry Governance Risk Criteria

Risk Criteria Risk elements

Structured Forest planning

Up to date Forestry Plan in place to guide government decision-making and provide structure for the regulatory environment covering forests e.g., demarcation of new concessions, processes to allocate concessions, local landowner interests and rights, etc.

Regulatory environment

Completeness of laws and regulations that, if implemented, will limit the risk that illegal harvesting will occur in the jurisdiction. including structured, independent approval processes (permitting, environmental, harvesting, processing, export).

Transparency & accountability

Transparency of approval process, especially in concession allocation, and collection and accounting for royalties and payments. Existence of robust independent audit process for approvals and finances covering those operations and activities possibly susceptible to illegal harvesting and subsequent trade in illegal logs.

Enforcement

Credible enforcement of regulations via demonstrated commitment of trained/qualified staff with appropriate powers to oversee and where needed to investigate operations and activities possibly susceptible to illegal harvesting and subsequent trade in illegal logs.

Industry/trade data

Accurate, timely, publicly available information demonstrating full disclosure of relevant information covering forest harvesting activities likely to be susceptible to illegal harvesting and subsequent trade in illegal logs.

The above risk criteria and constituent risk elements should be initially applied to a range of countries to evaluate them for completeness, and to set the benchmark acceptable-practice ratings. The method would then be applied more broadly to those supply countries identified as being major sources to Australia for specific (at-risk) products and/or sub-sectors.

Minor supply countries might receive a default score, in line with CPI, until such time as they have been reviewed fully. Although the CPI has limited value as a stand-alone measure of risk within the forestry sector, it provides some indication of risk until the necessary assessment of the regulatory environment and industry governance can be undertaken.

The party undertaking the assessment of industry governance, even with a well-defined ranking model, will need to have an in-depth understanding of sector level controls and be abreast of developments. There are a number of international organisations that focus on governance issues. These experts could be engaged to facilitate the development of the assessment process or to undertake the assessment. There may be scope to engage companies such as Transparency International to provide an industry-targeted index that is applicable at the regional level.

Another alternative is to utilise the findings and processes of the ITTO Objective 2000. In 2000 ITTO members re-stated their commitment, originally made in 1990 to moving as rapidly as possible towards achieving exports of tropical timber and

Copyright © Pöyry Forest Industry16

51A11995

timber products from sustainably-managed sources. This commitment was renamed 'ITTO Objective 2000'. It remains a central goal of the Organization, supported by renewed efforts to improve the respective capacities of governments, industries and communities to manage their forests, to add value to their forest products, and to maintain and increase the transparency of the trade and access to international markets.

Component 3 – Industry Measures

In well-regulated countries, evidence of adherence to externally-imposed (government) regulations is sufficient to reduce the risk of illegally-sourced logs/fiber entering the value chain. However, in some instances industry sectors and individual companies have been motivated to voluntarily adopt measures to reduce the risk that illegal logs/fiber will enter their value chain. Adopting these measures allows them to take a higher public profile, and through this to distance themselves from their peers who do not.

The most transparent of such mechanisms are the so-called certification schemes where companies select from among competing certification standards e.g., FSC and PEFC and go through a process to demonstrate that their operations meet the standards required. We noted earlier in the introduction to this section that we have not incorporated certification into this process for several reasons, but that this should be done once the findings from a separate consultancy are made available to DAFF.

Other than certification, we are aware of the following industry/company-based mechanisms to reduce the risk of illegal logs/fiber entering their sector/manufacturing processes:

Existence of industry bodies providing industry- or sector-level governance

Membership of international industry bodies

Visibility and reliability of production and trade data

Adoption of legality verification and chain of custody schemes to demonstrate product legality (measured as a portion of total supply)

Existence and appropriateness of industry codes and responsible purchasing policies

Presence of internal audit processes to ensure adherence to industry codes and/or government regulations.

However, the practicality of evaluating the above factors multiplies with the number of sectors/companies to be evaluated. The information needed to evaluate the effectiveness of self-imposed mechanisms is not available except via information supplied by the company/industry association.

Poyry has experience gained from valuing forestry and forest industry projects where we have to carefully evaluate company-supplied data covering log supplies and sources, approvals, plans, processing efficiencies etc. In our experience, many companies struggle to supply information in the first instance, and then the auditor and company have to commit significant time to develop a consensus view on key

Copyright © Pöyry Forest Industry17

51A11995

facts. Consequently we recommend that users firstly evaluate externally-verified sources of opinion on the legality of sources.

Therefore, we recommend that users evaluate the outputs from the separate certification consultancy to ascertain whether the findings from this work have application to this purpose. The criteria derived from this work would ideally be based around sources of data that could be independently verified. Examples include evidence of third-party certification and auditing. For this process, we recommend that the criteria to drive the third DRM component be finalised based on the outcome of the separate consultancy.

In the interim, we recommend the DRM just include the CPI and Industry Governance Components, and the relevant weightings during this interim period are discussed in the following section. As companies/sectors develop and can credibly verify that they have in place processes to reduce the risk of illegally-sourced logs/fibre/lumber entering their production processes, these can be recognised and the DRM score will reduce accordingly.

Domestic Risk Assessment Process

The following outlines how the values derived for the three DRM risk components are combined to give a domestic risk rating. We recommend that the risk components be weighted to emphasise the industry governance rating versus the country-level CPI value, as it is this component that will reflect the industry-specific focus that is the unique part of this methodology. The Industry Initiatives component, being certification, is an absolute. The percentage of raw material that is certified is considered low risk.

In recommending the initial settings below, we noted that the country-level CPI risk and industry governance components overlap. This is because forestry-specific regulations are more likely to be bypassed through corrupt activity. We have compensated via the weightings, and thus have biased the overall domestic risk score towards industry governance risk components over the country-level CPI risk. Applying these principles suggests a default 80% for industry governance and a 20% weighting to the country-level CPI risk.

We recommend that the above be applied to an initial suite of countries sectors/products and companies. The ranking system outlined above should be refined based on the experience gained from applying the benchmarks and importantly, evaluating the resolution that can be supported by available data sources.

This aspect of the methodology will require tapping expert opinion to explore and refine the risk factors and risk elements for each DRM component to focus on those deemed to be more robust. This should also involve external stakeholders with an interest in Australia’s position on this to ensure the appropriate elements are captured and that improvements in these elements of the risk assessment actually reflect an improvement in the risk profile for a given industry or product.

Stage 4 – Fibre Supply Surety

A portion of Australia’s wood product imports are produced in countries that are not the original source of the logs/fibre used in their production. Consequently, a

Copyright © Pöyry Forest Industry18

51A11995

mechanism is required to capture the risk that illegal logs/fibre/lumber are used to produce these products. The supply surety risk evaluation applies to countries reliant partly or wholly on imported logs/fibre/lumber, where the original source country is unknown, or where the country of origin is perceived to be of high risk.

A score card approach in developing a supply surety index considers imports as a percentage of total supply. This is expanded to incorporate the number of supply countries, the perceived risk of the respective supply countries, the type of wood product imported and the controls in place to address illegal wood product imports.

Of the total wood product imported, it is impossible to differentiate between product consumed domestically versus what is processed and re-exported. Given the complete lack of transparency and all of the problems associated with the mass balance approach we have adopted a simplistic approach to resolving this problem. This stage assumes that the proportion of imported log/fibre/lumber deemed to be at risk of being from illegal sources is applied to the total domestically-sourced log/fibre/lumber that country’s exports.

For example, if a country imports 20% (by volume) of the total volume of logs processed nationally, and all of this imported material is from sources at risk of being from illegal sources, then 20% of the sawnwood, 20% of wooden furniture, and 20% of wood fibre-based paper products exported from the manufacturing country would be assumed to be at risk of being from illegal sources according to the fibre surety index.

If the reporting of source country were to be introduced as mandatory in Australia, then this stage in the process would be considerably more robust.

Stage 5 – Risk Rating

The output of the previous stages is categorisation into an infinite number of risk categories. Given that the methodology creates an amalgam of quantitative and qualitative rankings out of a total (maximum) score of 10 we demarcated three categories “low”, “medium” and “high”. The recommended ranges for each category of the DRM components and the fibre surety are as follows:

“low” ≥6.6/10,

“medium” >3.3/10 and <6.6/10 and

“high” ≤3.3.

The calculation can stop here, or be further refined if certification or chain of custody evidence is available. Although this is not currently the case at a national level, individual importers know the status of their products and could adjust the risk factors accordingly.

3.1.2 Worked Example for >6mm HW Sawnwood (HS440729)

In order to illustrate this process, a single product, >6 mm hardwood sawnwood, has been selected. Although some of the trade figures contained in the illustrative example (Table 3-3 below) are real, the model is not intended to reflect the actual risk profile for this product and these countries.

Copyright © Pöyry Forest Industry19

51A11995

Stage 1 – Product Selection

For the purpose of illustrating the methodology, hardwood sawnwood (HS 440729 ‘other tropical wood’) has been selected.

Stage 2 – Exporting Country Identification

The following countries exported this product to Australia during 2008. They have been ranked in importance high to low in terms of volume.

Figure 3-7:Source Countries for imports of “>6mm HW sawnwood (HS440729)” to Australia

Indonesia MalaysiaPapua New

Guinea

Solomon Islands China Myanmar Thailand Other

% imports 56.2 22.3 7.3 2.8 2.6 2.5 1.6 4.8

0

10

20

30

40

50

60% of Australian imports of >6mm tropical HW sawnwood (HS 440729)

Source: WTA

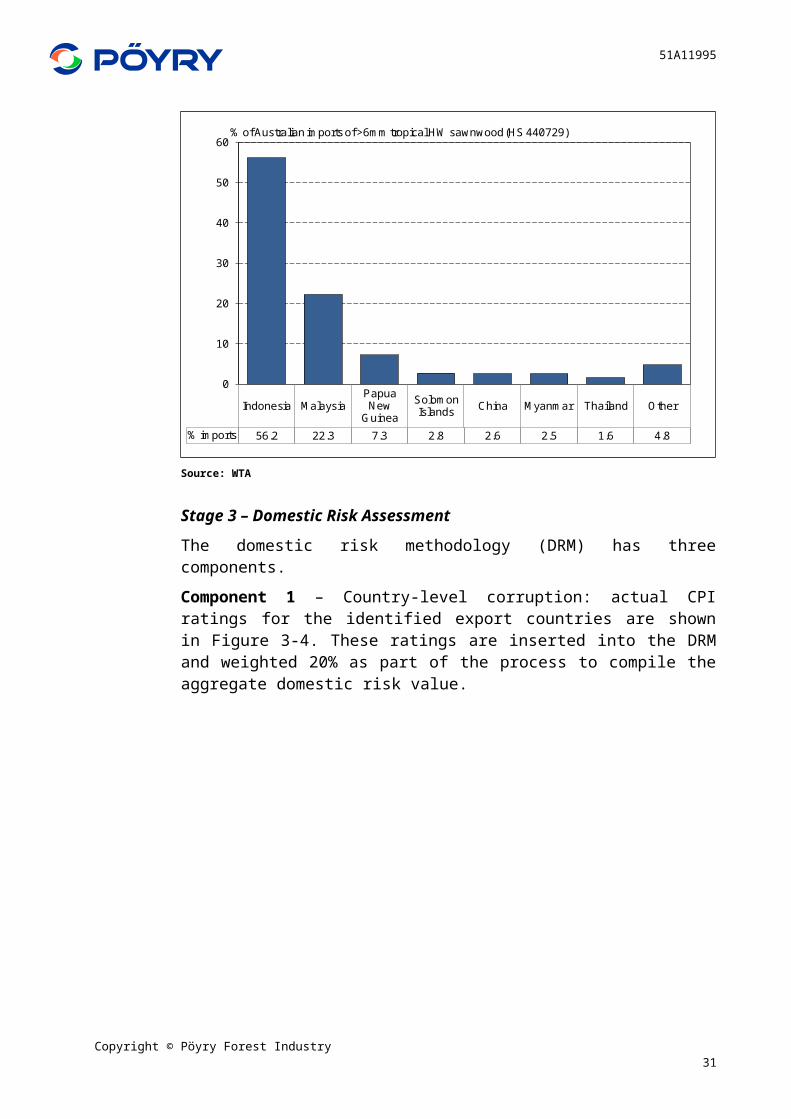

Stage 3 – Domestic Risk Assessment

The domestic risk methodology (DRM) has three components.

Component 1 – Country-level corruption: actual CPI ratings for the identified export countries are shown in Figure 3-4. These ratings are inserted into the DRM and weighted 20% as part of the process to compile the aggregate domestic risk value.

Copyright © Pöyry Forest Industry20

51A11995

Figure 3-8:Transparency International Corruption Percentage Index for Exporters of tropical Hardwood to Australia, 2008

2.6

5.1

2

2.93.6

1.3

3.5

0

1

2

3

4

5

6

7

8

9

10

Indo

nesi

a

Mal

aysi

a

Pap

ua N

ew

Gui

nea

Sol

omon

Is

land

s

Chi

na

Mya

nmar

Thai

land

- CPI ranking (1-10) -Less corrupt

Most Corrupt

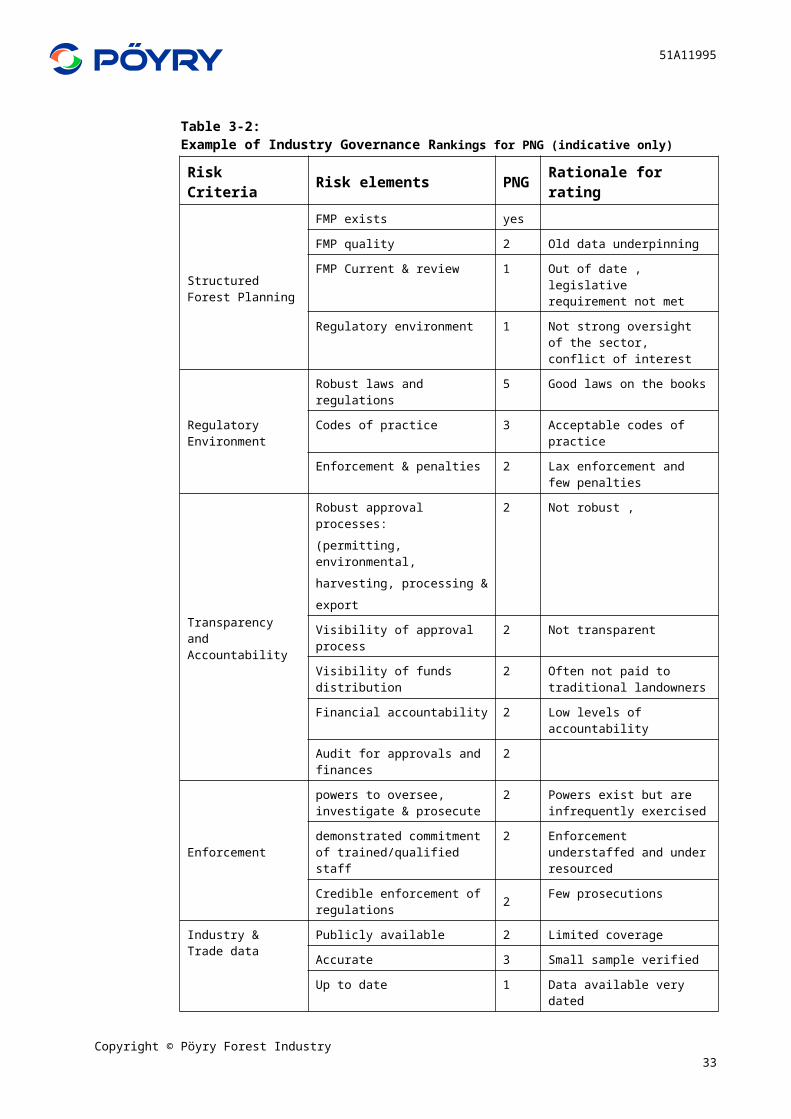

Component 2 – Industry Governance: The risk criteria and risk elements recommended as the starting point for this assessment were listed in the previous section. There is considerable work required to develop specific rankings for the range of countries potentially exporting illegally-sourced product into Australia, and also to rank what we termed best-practice benchmark countries. This work is outside the scope of this assignment.

The following provides an indicative ranking for PNG to highlight how the individual components are evaluated and the PNG relative ranking assigned.

Copyright © Pöyry Forest Industry21

51A11995

Table 3-2:Example of Industry Governance Rankings for PNG (indicative only)

Risk Criteria Risk elements PNG Rationale for rating

Structured Forest Planning

FMP exists yes

FMP quality 2 Old data underpinning

FMP Current & review 1 Out of date , legislative requirement not met

Regulatory environment 1 Not strong oversight of the sector, conflict of interest

Regulatory Environment

Robust laws and regulations 5 Good laws on the books

Codes of practice 3 Acceptable codes of practice

Enforcement & penalties 2 Lax enforcement and few penalties

Transparency and Accountability

Robust approval processes:(permitting, environmental, harvesting, processing &export

2 Not robust ,

Visibility of approval process 2 Not transparent

Visibility of funds distribution 2 Often not paid to traditional landowners

Financial accountability 2 Low levels of accountability

Audit for approvals and finances 2

Enforcement

powers to oversee, investigate & prosecute

2 Powers exist but are infrequently exercised

demonstrated commitment of trained/qualified staff

2 Enforcement understaffed and under resourced

Credible enforcement of regulations 2 Few prosecutions

Industry & Trade data

Publicly available 2 Limited coverage

Accurate 3 Small sample verified

Up to date 1 Data available very dated

Total aggregate score 2

Component 3 – Industry measures:

As discussed above, development of these criteria will be left pending the outcome from the separate DAFF certification consultancy.

Stage 4 – Fibre Supply Surety

As detailed in 3.1.1 the Fibre Supply Surety component address the risks associated with a suppling country relying on imported raw material for manufacture of the product exported to Australia.

The risk factors associated with these raw material products, by supply country, are captured and applied to the portion of product that is imported.

Copyright © Pöyry Forest Industry22

51A11995

Table 3-3 illustrates how each of the stages are considered in developing an overall risk profile for each supply country.Table 3-3:Worked Example, >6mm HW sawnwood (HS440729)Stage 1 Product Selection Timber >6mm HW (HS 440729)

Stage 2 Exporting Country Identification Indonesia Malaysia PNG Solomon IslandsChina Myanmar Thailand OtherPercentage 56.2 22.3 7.3 2.8 2.6 2.5 1.6 4.8

Stage 3 Domestic Risk AssessmentCPI (transparency International) 2.6 5.1 2 2.9 3.6 1.3 3.5

Weighting 20% 20% 20% 20% 20% 20% 20%Industry governance 5 3 2 2 6 1 5

Weighting 80% 80% 80% 80% 80% 80% 80%Total domestic risk rating 4.5 3.4 2.0 2.2 5.5 1.1 4.7

Domestic log supply 80% 80% 100% 100% 50% 90% 90% 0.82Sub total (%) 44.96 17.84 7.3 2.8 1.3 2.25 1.44 3.923106

Certified 10% 20% 10% 10% 30% 10% 35%Sub total (%) 4.50 3.57 0.73 0.28 0.39 0.23 0.50

Not certified 90% 80% 90% 90% 70% 90% 65%Sub total (%) 40.46 14.27 6.57 2.52 0.91 2.03 0.94

Stage 4 Fibre Supply SuretyImported supply (%) 11.24 4.46 0.00 0.00 1.30 0.25 0.16 3.98

Supply country 1 (value) 5.06 2.01 0.00 0.00 0.59 0.11 0.07Risk factor (ex log import risk) 2 3 3 4 5Supply country 1 (value) 3.37 1.34 0.00 0.00 0.39 0.08 0.05Risk factor (ex log import risk) 3 5 7 2 3Supply country 1 (value) 2.81 1.12 0.00 0.00 0.33 0.06 0.04Risk factor (ex log import risk) 5 5 4 3 4

The results of the risk calculation can be presented in a number of ways to assist the interpretation of the numerical results.

3.2 Further Development of Methodology

The development required to enable the methodology to be implemented is detailed below.

The accuracy of the model is dependent on the reliability/accuracy of Australian trade statistics. During the product selection stage, the availability of appropriate statistics and the completeness of the data should be assessed and corrective measures applied.

The Domestic Risk Model requires further development through a stakeholder and industry expert consultation process. Discussion with organisations such as Transparency International, ITTO and the World Bank, which have in-country experience, would be a logical starting point.

We recommend that the output from the DAFF commissioned report of certification schemes be assessed for inclusion in this methodology to assist with the risk assessment.

A database is required with the appropriate processing capability and functionality to process the large volume of trade statistics and to apply the respective industry, country level and fibre surety risk factors. The database must be able to deal with data in various formats as is the case with CPI and trade data country name formats.

Copyright © Pöyry Forest Industry23

51A11995

The various review processes (frequency of review etc) must be developed and responsibilities assigned.

3.3 Implementation of the Methodology

The methodology has been developed to be implemented in Australia however the application of this methodology on a regional level is possible and a regionally coordinated approach will likely improve the chances of driving change in governance and reduce the diversion of suspect product to less discerning markets.

The methodology presented will provide a sufficiently reliable result whilst not becoming complicated to a level that is cumbersome, confusing and difficult to manage. The participation of other regional countries, following agreement on the process and components of the risk analysis, would enable more resources to be applied to a targeted investigation of governance and would result in a lower investment for each participating country. As discussed previously, organisations such as Transparency International and ITTO who already undertake in-country analyses of risk in general and the effectiveness of forest management initiatives, may be able to support a Domestic Risk Analysis that is cost efficient.

The results of the risk analyses can be used to track the success of initiatives to reduce the trade in illegally-sourced wood products in each of the supply countries. The results can also be used by Australian importers as a resource for better understanding supply risk. Poyry believe the results of the risk analyses should be a key consideration in the development of Industry codes with regard imported wood based products and should assist with responsible purchasing decisions.

Copyright © Pöyry Forest Industry24

APPENDIX 1

Literature Review

Copyright © Pöyry Forest Industry1

51A11995

APPENDIX 1: LITERATURE REVIEW

Introduction

The purpose of this literature review is to gain an appreciation of the methodologies applied to quantifying the trade of illegal wood products and, where appropriate, to identify weaknesses or limitations in their usefulness. The focus of the review is on the forest product trade within countries in the Asia-Pacific region, although it quickly became evident that it was necessary to include publications focussing on a much broader list of countries and regions in order to capture the key publications.

Limited literature exists which either develops or describes in detail a methodology to estimate the volume and value of illegally logged timber and wood product trade. The majority of this literature is limited to examining the process of the illegal timber trade and the legislative framework. Most referenced academic research and scientific studies focus on the environmental issues associated with illegal logging, rather than illegal trade.

Generally, the data utilised in any of these analyses has been secondary, at best an unquantified estimate, based on anecdotal evidence or based on limited research. Many reports on illegal logging often do not include an assessment of the accuracy or reliability of illegal logging estimates and therefore can give the false impression to readers who quote these figures in good faith that the estimates are a true indication of the extent of illegal logging in any country. The same estimates that appear in many of the reviewed reports are referenced circularly, and are not linked to the original source.

Much of the literature about global trade of illegally logged timber and wood products is produced by environmental non-government organisations (ENGOs) and forestry-related associations. Many of these reports reference the findings presented in the Seneca Creekv, 2004 report, and thus the review of this report has been more comprehensive.

Findings

In undertaking the literature review, it became evident that many of the reports and work undertaken in providing estimates of illegal wood product volumes entering Australia has relied greatly on secondary, tertiary and extrapolated information that is generally available in the public domain, e.g. ENGO reports.

It is also evident that many of the published quantification approaches have relied significantly on country-based criteria such as the Corruption Perception Index (CPI) produced by Transparency International.

The literature review suggests that there are also many definitions of illegal, that the methodologies used to quantify legality lack robustness or reliability, and that only a small number of core documents have laid the foundation for subsequent works. The key assumptions from these core papers have been duplicated and re-

Copyright © Pöyry Forest IndustryA1-1

51A11995

used without further investigation into accuracy. Pöyry has focused its literature review on these core documents and the methodologies employed.

The Seneca report is the most comprehensive piece of work identified and reviewed by Pöyry. The Seneca report has become a key source document, the findings of which have been relied upon and quoted in many subsequent reports. This is perhaps indicative of the fact that the process for accurately quantifying the illegal wood products trade is extremely difficult without much improved data and the application of significant resources. Even with unlimited resources, the current lack of reporting systems and the inability to identify all corrupt or fraudulent undertakings mean that accurate quantification without the application of any subjective or arbitrary factors is currently unfeasible.

The Seneca report has employed logical methods, which include assessments of the reliability and accuracy of estimates, to quantify the illegal trade of wood products from selected countries. There are limitations in the accuracy of the results that the methodologies employed can deliver. This is not as a result of error nor lack of diligence but due to the limited practicable methods available without access to reliable data. The Seneca report utilises the classification of ‘suspicious’ rather than ‘illegal’. This perhaps reflects the belief that making defendable statements regarding quantification of illegal or legal volume is not currently possible.

The Seneca report includes an attempt at mass balance-type analyses of wood product trade. This may be overly simplistic and the base data assumptions from forest removals, trade data and domestic production are typically unreliable. The mass balance graphics as provided in the report are overly simplistic and do not capture the complexity of the wood products flow within these countries. Although, in theory, the mass balance approach can be quite useful in identifying suspicious trade activity, there are many barriers to its effective use. The mass balance approach relies on the availability of accurate log removal, domestic production and trade data. Domestic consumption of wood products is typically reported as apparent consumption and is calculated at Production + Imports – Exports. The real exports of a country can be compared to report only if domestic consumption and production figures are available with some confidence of accuracy. The complexity of the mass balance approach is further increased by the use of different, although appropriate, standards of measurement for various product groups.

An understanding of illegal logging is only somewhat useful in determining the legality of processed wood product imports. The likelihood of diversion of illegal wood products to less discerning markets is considered high. Much of what is considered illegal or high risk is processed domestically into wood products and furniture. The products can then be exported without the true volume of wood trade being captured. Pöyry cannot offer an estimate of the percentage of illegally-sourced wood products processed domestically with any confidence. It is clear that processed products are more difficult to trace back to the source and that domestic processing, particularly for the domestic market, effectively avoids border crossings where controls may be tighter.

From the number of papers reviewed, it is clear that a number of definitions of “illegal” have been applied. This illustrates the difficulty in defining legality. Some parties have included unsustainable harvesting whilst others consider all volume

Copyright © Pöyry Forest IndustryA1-2

51A11995

with the appropriate permitting and approvals, no matter the risk of corruption within the approval process, to be legal. There is no “right” definition, but this means that comparison of estimates is, by and large, impossible.

Some of the literature reviewed describes the product in question as ‘suspect’. This definition is somewhat more appropriate as it does not require the definitive classification as legal or illegal.

Literature Reviewed

1. Seneca Creek Associates and Wood Resources International 2004,” “Illegal” Logging and Global Wood Markets: The Competitive Impacts on the U.S. Wood Products Industry”. American Forest and Paper Association.

Synopsis

As the title suggests, the paper attempts to quantify the impact of illegally logged wood products on the US Wood Products Industry. The report focuses on key exporting and importing countries. It provides a comparison of the reported estimates of illegal production and trade by wood product, with revised estimates developed through infield research and country analysis.

The report provides not only an estimate of suspicious volume, but also clearly states the challenges in achieving accurate quantification of the problem. Key conclusions include:

The “illegal logging” issue is confused by, yet intricately related to, deforestation and poor forest practices.

The extent of illegal forest activity is impossible to know with any degree of certainty. Reported estimates are generally supported through anecdotal information only and supposition.