Embed Size (px)

Citation preview

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 1/50

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 2/50

TABLE OF CO NTE NTS V IS IO N 2 0 2 0

A B L E -P w C R E P O R T | 3

Foreword

Executive Summary

Chapter 1: The Vision for 2020W hat are Biopharm aceutical Products?The Size of the Prize

Chapter 2: Overview of the Global Biologics SectorThe Size and C om position of the G lobal Biologics M arketThe Size and C om position of the G lobal Biosim ilars M arketThe Key Differences betw een Biologics and C onventional Pharm aceuticalsThe Regulatory Environm ent

Chapter 3: Overview of the Indian Biologics SectorThe Size and C om position of the Indian Biologics M arket

Chapter 4: Competitive AnalysisA ustraliaC entral & Eastern EuropeC hinaIsraelLatin A m ericaSingaporeSouth KoreaTaiw an

Chapter 5: Key Recommendations for the Medium Term (2015)Research & D evelopm entM anufacturing & C om m ercialisation

H um an C apitalThe Regulatory Fram ew orkInnovationIntellectual Property

Chapter 6: Key Recommendations for the Longer Term (2020)C reate a Fram ew ork for Intelligent RegulationInvoke “M arket Pull”Seek O pportunities for G row th through A cquisitionsEncourage H ighly Skilled Expatriates to C om e H om eLeverage India’s Expertise in H olistic and Traditional M edicine

Conclusion

Appendix 1: Exchange Rates

Appendix 2: The Global Pipeline for Biosimilars

Appendix 3: Biologics with Patents expiring between 2010 and 2020

Acronyms

Acknowledgements

Selected Bibliography

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 3/50

FOREWORD V IS IO N 2 0 2 0

A B L E -P w C R E P O R T | 4

Evolution of new drugs continues to be an increasingly daunting task. The en-blockpatents expiry of older sm all m olecule drugs w ith little to add by w ay of discovery ofnew ones is at once a challenge and an opportunity.

This challenge is on one hand leading to hunt of new m olecules from the depths of theocean to prospecting new chem ical com plexes through nanotechnologies w hileopening up larger m arket opportunities in the generics space. H ow ever the genericsm arket w ill see a lot of consolidation due to entry of large global players w hose energiesw ould be diverted from the hitherto patents of sm all m olecules, to now , in the changedcontext, generics, w hich offers the traditional low hanging fruit to profit from .

It is in this context that the developm ent of biopharm a drugs becom es very im portantespecially in the context of India. W ith the advent of the product patent regim e, there isan air of expectancy to develop new ideas. There can be no better area to do this thanBiopharm a. Biopharm a as w e know encom passes the range from recom binanttechnology based biosim ilars to developm ent of large antibodies structures –the m A Bs.W hile in the year 2009 the global biopharm a m arket w as said to be about $ 137 billionstrong, India has but a m iniscule share of 1.4% in it. H ow ever Indian biopharm a isgrow ing at a scorching pace and registered a 17% grow th over the last year, w hich isreally the bright silver lining.

The D epartm ent of Pharm aceuticals in the G overnm ent of India has taken up the task ofaddressing this opportunity. In partnership w ith the prem ier biotechnology industrybody A BLE and pre-em inent consultant leader in the life sciences sector –Pw C , the

D epartm ent of Pharm aceuticals has sought to prepare a detailed docum ent –TheVision 2020 BioPharm a Strategy. This w ould for the first tim e bring out the m ultifacetedchallenge and the break-through possibilities in the biopharm a sector for the Indianindustry.

I am sure that the industry w ould benefit from it and so w ould the governm ent forfinding new w ays to address the grow th and developm ent of the biopharm a industry inIndia for m aking it the future leading global hub. Thank you.

Ashok KumarSecretary, D epartm ent of Pharm aceuticalsM inistry of Chem icals & Fertilizers

G overnm ent of IndiaN ew D elhi12th July 2010

The Vision 2020 Bio Pha rmaStra te g y: This w o uld fo r the f irstt ime bring out the mult ifa cetedcha lleng e an d the brea k-t hro ug h po ssibilities in thebiopha rma secto r for the Indian

industry.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 4/50

FOREWORD V IS IO N 2 0 2 0

A B L E -P w C R E P O R T | 5

The Biopharma Challenge

The biopharm a drugs sector is the next big block-buster aw aiting right techno-scientific entrepreneurship.India cannot afford to m iss this opportunity. The present grow th rates of over 30% but scratch the surface.

The challenge is how to do it given the prom ises on one hand and constraints of w orld class hum an resources,infrastructure, discovery funding and the appropriate policy m ix on the other. The Vision 2020 BioPharm aStrategy docum ent w ould be path-breaking in pointing out direction to accom plish this difficult task. A BLEand Pw C have com e together through painstaking research and w ide experience including first handinterview s to prepare this docum ent.

I hope the industry, the academ ia and all the stake-holders find it useful. W e encourage them to contribute toit and join us in the task of building India as the next big destination for global biopharm a.Thank you.

Devendra ChaudhryJoint Secretary

D epartm ent of Pharm aceuticalsM inistry of C hem icals & FertilisersG overnm ent of India12th July 2010

The Indian Pharm aceutical Industry has been a global leader in the cause of providing high quality affordablem edicines to the w orld. W ith a gradual shift from sm all m olecules to biologics, the vision, the m ission and thetactical planning for the Indian Biopharm aceutical Industry has yet to be evinced. This w as the task given to us

by the D epartm ent of Pharm aceuticals and this report is the result. A t the outset w e w ould like to thank theD epartm ent for reposing faith in A BLE & Pw C to deliver on this im portant task.

This report analyses the global environm ent w ith reference to m arkets, regulations, governm ent initiativesand identifies key areas for the G overnm ent to play a m ajor role in building the required capacities andcapabilities. A n enabling ecosystem - infrastructure, regulatory fram ew ork and a skilled w orkforce are som eof the factors that w ill ensure that India becom es a leading producer of affordable biopharm aceutical drugs inthe next decade.

Recognising that the strategic w ay forw ard is through Innovation and the ability of Indian com panies to createIntellectual Property, the report identifies long term initiatives that the G overnm ent can im plem ent to fosterinnovation.

W e hope this report presents an understanding of the opportunity for Indian Biopharm a and a direction for allstakeholders to realize this opportunity.

Sujay ShettyLeader –Pharm a Life SciencesPricew aterhouseCoopers

Vijay ChandruPresident - A BLE

The Vision 2020

BioPha rma Strat eg ydocument w ould bepa th -brea king inpoint ing outdirection...

Recog nising tha t t he stra teg ic w a y forw a rd is through Innovat ion a ndth e a bility o f Ind ia n co mpa nies to crea te Intellectua l Property.. .

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 5/50

EXECUT IVE SUM M A RY V IS IO N 2 0 2 0

A B L E -P w C R E P O R T | 6

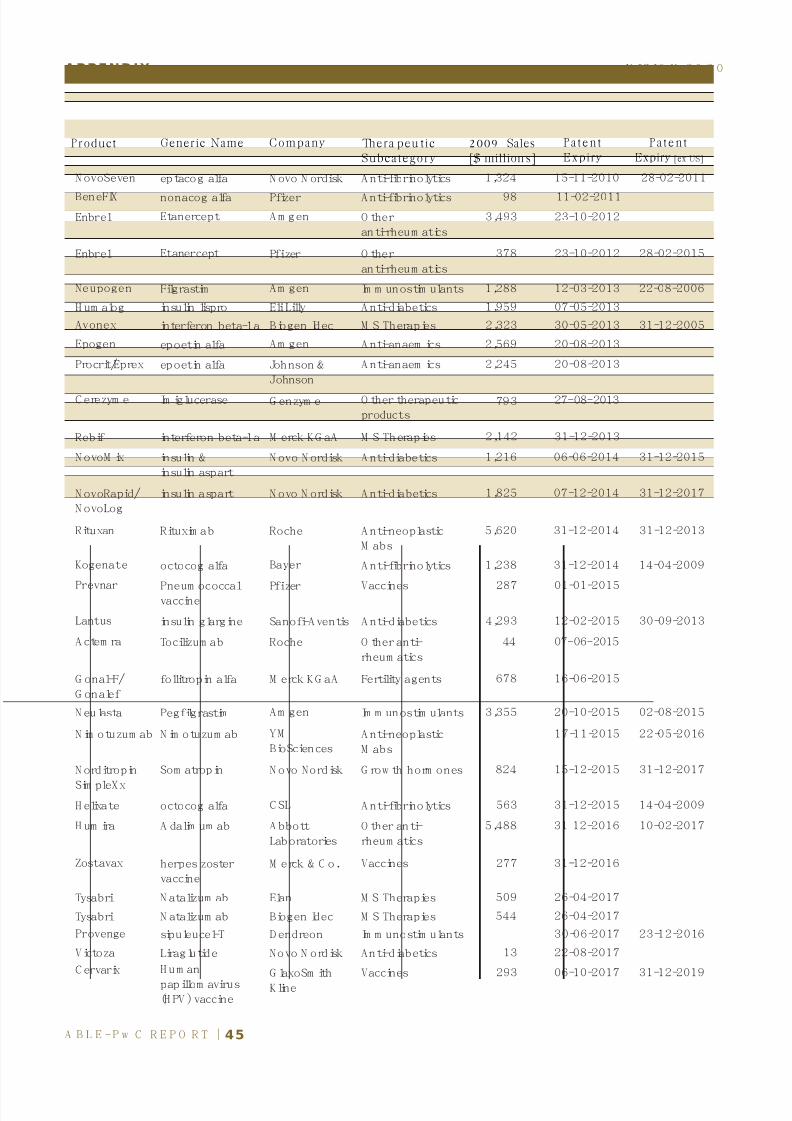

In 2010, the D epartm ent of Pharm aceuticals (D oP) of the G overnm ent of India (G O I) set the nation’sbiopharm aceutical industry (BioPharm a) a lofty goal: to becom e a leading global producer of affordable“biopharm aceutical”products by 2020. The m arket is currently w orth about U S $137 billion, but it is grow ingvery rapidly. Indeed, industry experts estim ate that it could be w orth U S $319 billion by 2020. M oreover, atleast 48 products w ith com bined sales of nearly US $73 billion in 2009 are due to com e off patent over thenext decade. So the potential is huge.

H ow ever, biopharm aceutical products are very m uch m ore difficult to develop and m anufacture thantraditional pharm aceuticals. The com petition –both from m anufacturers of branded products and from otherem erging countries keen to m ake their m ark in the biopharm aceutical space –is also likely to be intense.

If India is to achieve its aim , it w ill therefore have to act fast –and the G O I w ill have to play a m ajor supportingrole by creating a suitable physical, financial, legislative and regulatory infrastructure. The private sector w illinvest in building the necessary m anufacturing capacity, if that enabling infrastructure is in place. But it cannotprovide the roads and ports, fiscal incentives, law s, regulations and other such features that w ill also beneeded to put India at the forefront of biopharm aceutical production.

This report focuses on the changes that w ill be required to provide such an infrastructure. It explores the keydifferences betw een biopharm aceutical therapies and conventional therapies, together w ith the im plicationsfor developm ent and m anufacturing; analyses the com petitive landscape; and identifies the m easures the G O Iw ill need to im plem ent w ithin the next five and 10 years, respectively. It does not attem pt to quantify theprecise am ount of m anufacturing capacity that w ill be required; it focuses, rather, on the big picture.

W e believe that India should aim to capture 10% of the global m arket for biosim ilars –i.e., follow -on versionsof original biopharm aceutical products –by 2020, and becom e one of the top five producers in the w orld.W e estim ate that the G O I w ill need to invest at least U S$1 billion over the next five years to im plem ent them easures w e have identified. D oing so could yield rich returns; if India’s Biopharm a industry succeeds inrealising this aspiration, it w ill bring in additional revenues of US $4.3 billion a year.

The GOI will have to playa major supporting role by

creating a suitable physical,financial, legislative andregulatory infrastructure.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 6/50

1.1 WHAT ARE BIOPHARMACEUTICAL PRODUCTS?

The w ord “biopharm aceutical” is a com posite of the w ords “biotechnology”and“pharm aceuticals”, and reflects the convergence of w hat w ere once tw o distinct industries.So it is probably helpful to begin by discussing precisely w hat biopharm aceutical productscom prise. They are m edicines typically derived from living system s and produced usingbiotechnology –e.g., vaccines, blood and blood com ponents, som atic cells, gene therapies

and recom binant therapeutic proteins.

O ver the past decade, the BioPharm a industry has developed m any such “biologics”, as theyare also called. A nd follow -on versions of som e of the earliest biologics m ade viarecom binant D N A technology, including biosynthetic “hum an”insulin and hum an grow thhorm one, are now available. These are know n as “biosim ilars”.

H ow ever, the biopharm aceuticals m arket extends w ell beyond m edicines. It also includesdiagnostics, sophisticated drug delivery and rem ote m onitoring devices, and healthm anagem ent services. O nly a few biopharm aceutical com panies –e.g., Fresenius and BaxterH ealthcare –currently offer such services, but other com panies are likely to follow suit as thespotlight sw itches to the secondary-care sector (see Figure 1). D iagnostics, devices andhealth m anagem ent services are m ajor subjects in their ow n right. This report therefore

focuses on the burgeoning m arket for biosim ilars –and, m ore specifically, on how India canbest prepare to capture a share of that business.

Figure 1: The Biopharmaceutical Space

Source: Pricew aterhouseC oopers

A B L E -P w C R E P O R T | 7

Chapter 1

The Vision for 2020

India should aim to become one of the world’s five leading producersof affordable biopharmaceutical drugs by 2020. Biopharmaceuticalproducts include: vaccines, blood and blood components, somatic cells,

gene therapies and recombinant therapeutic proteins.

V IS IO N 2 0 2 0

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 7/50

1.2 THE SIZE OF THE PRIZE The biosim ilars m arket is still in its infancy, and is largely concentrated in less heavily

regulated regions such as Latin A m erica and A sia at present. But industry analysts estim atethat it could be w orth m ore than U S $43 billion by 2020. (A ll subsequent references are to U Sdollars, and all figures have been converted into dollars for ease of com parison, using theexchange rates detailed in A ppendix 1.)

A ging populations and higher expectations are boosting dem and for good m edicines, andbiologics now have a very successful track record. H ow ever, m any biologics cost thousands –or even hundreds of thousands –of dollars. Biosim ilars, by contrast, typically sell for betw eenabout 15% and 75% of the price of the original versions. So they are m ore affordable –inboth m ature econom ies w ith increasingly cash-strapped healthcare system s and em ergingeconom ies w ith increasingly affluent inhabitants (see Figure 2).

Figure 2: The Forces Shaping the Biosimilars Market

Source: Pricew aterhouseC oopers

Biosim ilars have considerable com m ercial potential, but exploiting that potential w ill not beeasy. For one thing, biosim ilars are m uch m ore difficult to develop and m anufacture thantraditional generics. The regulatory pathw ays for getting them approved are also less w ellestablished, and the com petition –both from innovator com panies and from rival biosim ilarsproducers –is likely to be intense. W e shall discuss these challenges, and how India shouldrespond to them in m ore detail in the follow ing pages.

A B L E -P w C R E P O R T | 8

V IS IO N 2 0 2 0CH A PTE R | 1

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 8/50

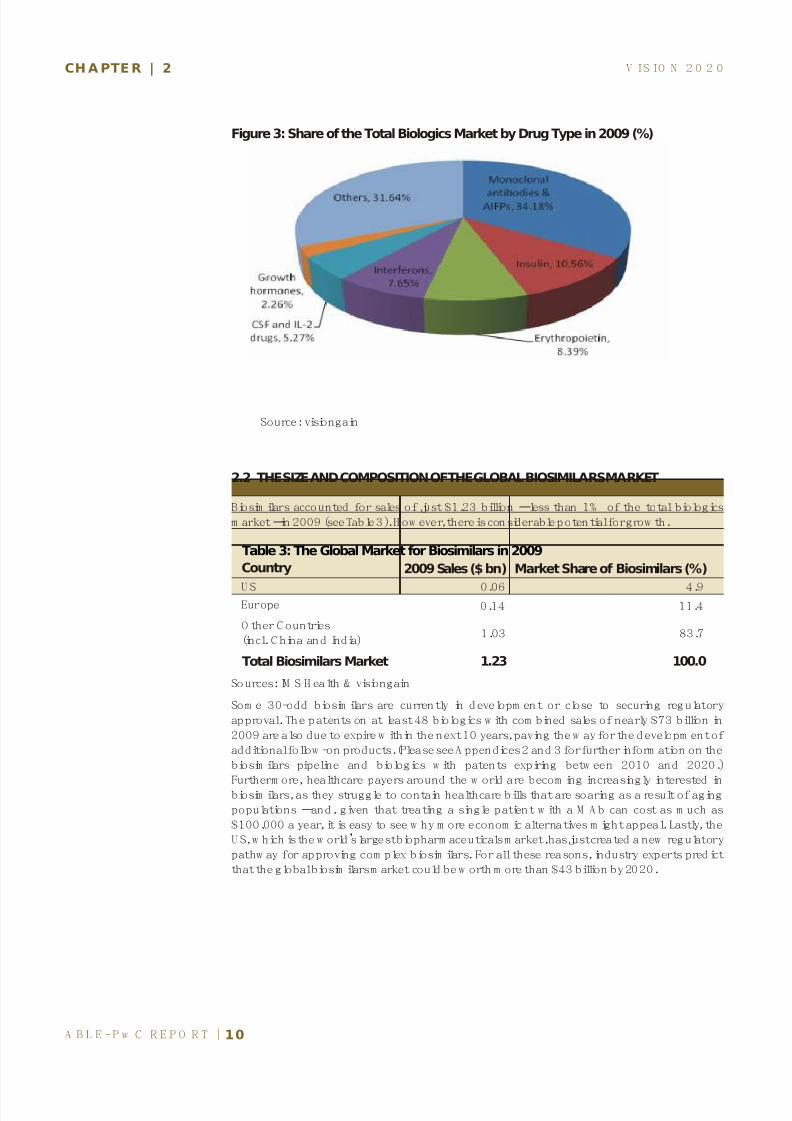

M easured by drug type, m onoclonal antibodies (M A bs) led the m arket. They accounted form ore than one-third of all sales of biologics in 2009, follow ed by insulin and erythropoietin(see Figure 3).

A B L E -P w C R E P O R T | 9

Chapter 2

Overview of the Global Biologics Sector

With global sales of biologics reaching nearly $137 billion in 2009 and thepatents on at least 48 biologics due to expire over the next decade, industryexperts predict that the global biosimilars market could be worth more than

$43 billion by 2020. But biologics differ from conventional pharmaceuticals insome fundamental ways.

V IS IO N 2 0 2 0

2.1 THE SIZE AND COMPOSITION OF THE GLOBAL BIOLOGICS MARKET

In 2009, global sales of biologics totalled $136.6 billion (see Table 1). Avastin (bevacizum ab)headed the list of best sellers, w ith sales of $5.74 billion, w hile Rituxan (rituzim ab) andH um ira (adalim um ab) cam e second and third, respectively (see Table 2).

Table 2: The 10 Top Selling Biologics in 2009Brand Drug Name 2009 Sales ($bn)

Avastin bevacizum ab 5.74

Rituxan rituxim ab 5.62

H um ira adalim um ab 5.48

H erceptin trastuzum ab 4.86

Lantus insulin glargine 4.29

Enbrele tanercept 3.87

Rem icade inflixim ab 3.51

N eulasta pegfilgrastim 3.35

Epogen epoetin alfa 2.56

Avonex interferon beta-1a 2.32

Source: EvaluatePharm a

69.02

41.68Europe

10.29

14.40

1.20

136.59

2009 Sales ($ bn)

Table 1: The Global Market for Biologics in 2009

C ountry

U S

Japan

A sia/A frica/A ustralasia

Latin A m erica

Total Biologic Drugs Market

Source: visiongain & Pricew aterhouseCoopers analysis

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 9/50

CH A PTE R | 2

Figure 3: Share of the Total Biologics Market by Drug Type in 2009 (%)

Source: visiongain

2.2 THE SIZE AND COMPOSITION OF THE GLOBAL BIOSIMILARS MARKET

Biosim ilars accounted for sales of just $1.23 billion –less than 1% of the total biologicsm arket –in 2009 (see Table 3). H ow ever, there is considerable potential for grow th.

Som e 30-odd biosim ilars are currently in developm ent or close to securing regulatoryapproval. The patents on at least 48 biologics w ith com bined sales of nearly $73 billion in2009 are also due to expire w ithin the next 10 years, paving the w ay for the developm ent ofadditional follow -on products. (Please see A ppendices 2 and 3 for further inform ation on thebiosim ilars pipeline and biologics w ith patents expiring betw een 2010 and 2020.)

Furtherm ore, healthcare payers around the w orld are becom ing increasingly interested inbiosim ilars, as they struggle to contain healthcare bills that are soaring as a result of agingpopulations –and, given that treating a single patient w ith a M A b can cost as m uch as$100,000 a year, it is easy to see w hy m ore econom ic alternatives m ight appeal. Lastly, theU S, w hich is the w orld’s largest biopharm aceuticals m arket, has just created a new regulatorypathw ay for approving com plex biosim ilars. For all these reasons, industry experts predictthat the global biosim ilars m arket could be w orth m ore than $43 billion by 2020.

A B L E -P w C R E P O R T | 10

V IS IO N 2 0 2 0

Sources: IM S H ealth & visiongain

Table 3: The Global Market for Biosimilars in 2009

Country 2009 Sales ($ bn) Market Share of Biosimilars (%)

U S 0.06 4.9Europe 0.14 11.4

O ther C ountries(incl. C hina and India)

1.03 83.7

Total Biosimilars Market 1.23 100.0

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 10/50

A B L E -P w C R E P O R T | 11

V IS IO N 2 0 2 0CH A PTE R | 2

2.3 THE KEY DIFFERENCES BETWEEN BIOLOGICS AND CONVENTIONALPHARMACEUTICALS

H ow ever, biologics differ from conventional pharm aceuticals in som e fundam ental w ays. In

the next section, w e shall discuss these differences, together w ith their im plications for thedevelopm ent, m anufacturing and m arketing of biosim ilars.

2.3.1 Differences in Therapeutic Targets

Biologics typically address diseases conventional drugs cannot treat very effectively –such ascancer and genetic disorders. They can therefore com m and prem ium prices in m ost m arketsw hen they are first launched, because there are no effective therapeutic alternatives.

2.3.2 Differences in Product Attributes

But biologics are very com plex products. C onventional drugs are derived from chem icals,consist of relatively few m olecular ingredients, are quite sm all and can easily be characterisedthrough their chem ical structures, using established analytical techniques such as m assspectrom etry. Biologics, by contrast, are derived from genetically m odified m icroorganism sor anim al cell lines. M ost biologics also consist of m any m olecular ingredients, are m uchlarger than conventional drugs (betw een 100 and 1,000 tim es larger) and have com plexstructures that cannot be com pletely characterised by the m ethods used for conventionaldrugs.

2.3.3 Differences in Manufacturing Processes and Infrastructure Required

Biologics likew ise differ crucially from conventional drugs in that the m ethods by w hich they

are m anufactured greatly influence their therapeutic characteristics. The sam e starteringredients m ay deliver quite different results, depending on the system that is used.Sim ilarly, a slight variation in the starter ingredients or external m anufacturing conditionsm ay yield a different product, even if the living system from w hich it is derived is the sam e.These differences can render a biologic unsafe or ineffective. H ence the fact that the patentsprotecting biopharm aceuticals often include the processes used to m anufacture them asw ell as their chem ical com position.

M oreover, the process flow s typically used to m anufacture proteins or antibodies, and theunit operations involved in those process flow s, have very little overlap w ith the process flow sand unit operations typically involved in the production of sm all m olecules (see Tables 4 and5). These differences in the m anufacturing processes and infrastructure required to producesm all m olecules and proteins or M A bs m ean that the latter are m ore expensive to

m anufacture in term s of both capital costs [per square feet (sq. ft.)] and operating costs.

Biologics likewise differ crucially from conventional drugsin that the methods by which they are manufactured greatlyinfluence their therapeutic characteristics.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 11/50

A B L E -P w C R E P O R T | 12

V IS IO N 2 0 2 0CH A PTE R | 2

M ore specifically, w hereas m ost of the equipm ent needed to m anufacture sm all m oleculescan be sourced locally, m ost of the equipm ent needed to m anufacture biologics m ust beim ported, although som e subsidiaries of European and U S vendors have now set up shop inIndia (e.g., M illipore C orporation, Sartorius and C lestra). The initial capital investm ent istherefore m uch greater. The skills required to m anufacture biologics –e.g., a know ledge ofcell line engineering, ferm entation, m icrobiology, protein purification (chrom atography,m em brane separations, lyophilisation, protein folding, etc.) and aseptic processing –are alsom uch m ore dem anding.

Table 5: Key Differences in Manufacturing of Conventional Drugs and BiologicsSmall Molecules Proteins/MAbs

C hem ical synthesis Expressed in m icro-organism s(bacteria,yeast, fungi, m am m alian cells)

M ay involve harsh conditions likeextrem es of pH , tem perature andpressure, flam m able organic solvents

G enerally aqueous processing usingm ild conditions

Bulk active pharm aceutical ingredientavailable as a stable solid at roomtem perature

Requires form ulated bulk solution w ithcold storage

Form ulated for oral delivery(tablets, capsules, syrup) or topicalapplication (ointm ent, spray)

Form ulated as a sterile vial, pre-filledsyringe or cartridge for injection or infusionw ithout term inal steam sterilization

M anufacturing facility is generally notdesigned for aseptic processes

M anufacturing facility is designed foraseptic processes

Supply chain m ay include differentm anufacturers for drug interm ediate,bulk drug and form ulated drug product

Vertically integrated up to form ulatedbulk; at m ost fill-finish can be decentralized.N o concept of drug interm ediate

Source: Pricew aterhouseC oopers

Table 4: Typical Process Flows

Small Molecules Proteins/MAbs

C hem ical reaction C ell banking

Solvent extraction Seed ferm entation (or inoculum developm ent)C rystallization Production ferm entation/cell culture

Vacuum or air drying H arvesting (cell separation)

M illing C oncentration and purification (m ultiple steps dependingon product and host organism )

Blending Bulk form ulation, bulk lyophilisation

A septic fill-finish (vials, cartridges, syringes, etc.)

Source: Pricew aterhouseC oopers

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 12/50

A B L E -P w C R E P O R T | 13

V IS IO N 2 0 2 0CH A PTE R | 2

2.3.4 Differences between Biosimilars and Generics

Biosim ilars are thus m ore difficult to develop and m anufacture than traditional generics for anum ber of reasons. First, it is alm ost im possible to produce an exact replica of a biologic

because changes to the structure of the m olecule can take place during the productionprocess. Biosim ilars, unlike generics, m ust therefore be subjected to additional clinicaltesting to ensure that they have sim ilar pharm acokinetic profiles to those of the originalproducts, and do not cause unexpected adverse responses or im m une reactions. Second, theprocesses used to m anufacture biosim ilars are inherently m uch m ore com plex than thoseused to m anufacture generics. A nd, lastly, since biosim ilars are injectable products w hichcannot be term inally steam sterilised, all processing m ust be perform ed under aseptic(sterile) conditions.

These challenges m ean that it typically costs $10-40 m illion to develop a biosim ilar,com pared w ith just $1-2 m illion for a traditional generic. The gestation period for clinicaldevelopm ent, regulatory approval and scale-up to com m ercial production is also m uchlonger (typically, about seven years versus tw o or three years), so the risk to capital is m uch

higher. The cost differential betw een a biosim ilar and the original product is thus m uchsm aller –a fact that som e countries, such as Japan, have recognised by introducingdifferentiated pricing regulations for biosim ilars and generics.

M oreover, since biosim ilars are not easily show n to be bioequivalent to the original products(as traditional generics are), they are not norm ally interchangeable (i.e., a pharm acist cannotsubstitute a biosim ilar for the original version). So any com pany that m anufactures abiosim ilar w ill need to em ploy a specialised sales force (or enter into a m arketing agreem entw ith a third party) to encourage physicians to prescribe it.

2.3.5 Differences in Regulation

The m any differences betw een biologics and conventional drugs –and hence betw eenbiosim ilars and generics –have resulted in very different criteria for regulatory approval.Sm all m olecule bulk is approved based on analytical characterisation of the active m oiety andidentification of any im purities above a specified threshold. The form ulated product isapproved based on dissolution tests and/or bioequivalence/bioavailability studies in healthyvolunteers. These are generally quick, relatively inexpensive and do not require asophisticated clinical infrastructure.

H ow ever, all biosim ilars currently require pre-clinical testing in anim als (rodents, dogs orother relevant species) to G ood Laboratory Practice (G LP) standards and clinical testing toG ood C linical Practice (G C P) standards to establish their pharm acokinetics, im m unogenicityand com parative efficacy against the original product. Som e countries (or groups ofcountries, like the European U nion) also insist on clinical trials in their local populations orsourcing of the original reference product from the country or region concerned.

Fulfilling these stipulations is very tim e-consum ing and expensive. It also requires clinical andbioanalytical expertise and infrastructure, and the use of clinical research organisations(C RO s) w ith specific dom ain and country know ledge. Furtherm ore, the original product m aynot be one that is routinely prescribed in India. So only a few investigators and trial sites m ayhave the clinical experience to com ply w ith internationally accepted protocols.

There are other obstacles, too. It is relatively easy to im plem ent m ost process changes, scalechanges and site changes for sm all m olecules by show ing in-vitro characterisation datathrough high-perform ance liquid chrom atography (H PLC ), low m olecular w eight m assspectrom etry and other such techniques. But there are not yet any guidelines for biosim ilarsin term s of defining w hich changes can be perm itted through in-vitro testing and w hether in-vitro testing can be perm itted for “w ell characterised proteins”(w hich are m ainly sm aller

proteins w ithout com plex glycosylation).

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 13/50

A B L E -P w C R E P O R T | 14

V IS IO N 2 0 2 0CH A PTE R | 2

Sophisticated protein characterisation tools m ay be needed to justify use of in-vitro testing toestablish com parability (e.g., m ass spectrom etry and high frequency nuclear m agneticresonance (N M R) spectroscopy for m acrom olecules, cell-based assays, affinitym easurem ents, specificity to receptor binding, enzym e-linked im m unosorbent assays

(ELISA ) and gel electrophoresis). The specifications for recom binant proteins and M A bsgenerally also include establishing lim its for host cell proteins, host cell D N A and endotoxins,w hile products m ade using m am m alian cell cultures have specifications on viral clearance.Perform ing the analysis and characterisation tests required to m eet such specificationsrequires different skills from those involved in the analysis and characterisation of sm allm olecules.

2.4 THE REGULATORY ENVIRONMENT Regulatory pathw ays for approving original biologics have been created around the w orld.H ow ever, the m em ber states of the European U nion, Japan and A ustralia (w hich adopted theEuropean system ) are currently the only countries w ith established biosim ilar m arket

authorisation pathw ays. The U S, w hich is the w orld’s largest biologics m arket, has justpassed legislation to create such a pathw ay, but som e of the details still have to be finalised.

2.4.1 The Regulatory Environment in the US

In the U S, original biologics gain access to the m arket through tw o regulatory pathw ays:

•The Public H ealth Service A ct (PH S, 1944) –w hich covers the m ajority of biologics and isenforced by the FD A via tw o departm ents: the C enter for Biologics Evaluation andResearch (C BER), w hich m ostly regulates blood products, cellular products and vaccines;and the C enter for D rug Evaluation and Research (C D ER), w hich m ostly regulates biologicsproduced by biotechnological m ethods (e.g., M A bs and therapeutic proteins). Biologicsfalling under the PH S are approved through the Biological License Applications (BLA )

procedure.

•The Food D rug & C osm etic Act (FD& C , 1938) –w hich covers conventional pharm aceuticalsand certain natural proteins (e.g., insulins and grow th horm ones) and is also enforced bythe FD A . Biologics falling under the FD & C are approved through the N ew D rug A pplication(N D A ) procedure.

A t present, biosim ilars can only be approved for originals authorised under the FD & C , w hichm eans that it is only possible to m arket a very lim ited range of biosim ilars (the sim plerproteins) in the U S. A pplications m ust be subm itted to the C D ER through the A bbreviatedN D A (A N D A ) pathw ay. A pplication data from the already approved reference product can beused in support of the biosim ilar, although the FD A can request further docum entation ofthe new product’s safety and efficacy relative to the reference product (e.g., through clinicaltrials).

H ow ever, in June 2010, the U S Federal G overnm ent passed the “Biologics Price Com petitionand Innovation A ct”to create a regulatory approval pathw ay for biosim ilar versions of m orecom plex biologics approved under the PH S. The A ct distinguishes betw een biosim ilars and“interchangeable”biosim ilars, and establishes a different burden of proof for each category;a biosim ilar m ust possess no clinically m eaningful differences in safety, purity and potencyfrom the original product, w hereas an “interchangeable”biosim ilar m ust produce the sam eclinical result as the original product in any given patient and present no additional risk if apatient is sw itched from the original product to the biosim ilar. The A ct also includes a 12-yearperiod of data exclusivity for all original products (w ith a six-m onth extension for productssupported by paediatric studies) and introduces a new “patent inform ation exchange”process, in w hich the biosim ilar applicant is required to provide inform ation about itsm anufacturing process to the innovator com pany and both parties are then required to

identify the key patents they believe either need to expire or can be successfully challenged.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 14/50

A B L E -P w C R E P O R T | 15

V IS IO N 2 0 2 0CH A PTE R | 2

The FDA m ust still provide guidance on the clinical data it requires, although the nature ofthat guidance has not yet been specified. A nd the process is unlikely to provide a fast route tom arket; there is considerable scope for disagreem ent during the patent inform ationexchange period, for exam ple. N evertheless, industry com m entators w idely regard the A ct

as w elcom e progress.

2.4.2 The Regulatory Environment in the European Union

M anufacturers of all pharm aceuticals, including biologics, can apply to the EuropeanM edicines A gency (EM A ) for m arketing authorisation in the 27 European U nion m em berstates. A pproval is regulated through the 2001 C ode for H um an M edicines Directive (C H M D )and its subsequent am endm ents. The CH M D provides an abbreviated pathw ay for theapproval of traditional generics and, follow ing tw o am endm ents in 2003 and 2004, alsocovers biosim ilars.

The EM A has issued various guidelines on the data biosim ilar m anufacturers need to supply

w ith their applications, including specific guidelines for the approval of grow th horm ones,insulins, epoetin products and granulocyte-colony stim ulating factors (G -C SF). It is stillpreparing guidelines for the approval of interferons and M A bs, but has already approved anum ber of biosynthetic grow th horm ones as w ell as biosim ilar versions of epoetin andfilgrastim .

The EM A assesses a biosim ilar based on w hether its safety, quality and efficacy arecom parable to that of the original drug. The extent to w hich clinical trials have to beconducted to provide this inform ation is at the agency’s discretion. The regulations furtherstipulate that original drugs approved before 2005 enjoy m arketing exclusivity for 10 years, ifthey w ere approved through the centralised European U nion procedure. If they w ereapproved in individual m em ber states, varying m arketing exclusivity periods apply. H ow ever,for original drugs approved after 2005, a data exclusivity period of eight years applies. A n

additional tw o years of m arketing exclusivity –or three years, if the product is approved for anew indication w ith significant clinical advantages –can be granted.

2.4.3 The Regulatory Environment in Japan

The Japanese M inistry of H ealth, Labour and W elfare (M H LW ) issued guidelines for theapproval of biosim ilars in M arch 2009. A ll m anufacturers of biosim ilars are required tosupport their applications w ith data from clinical trials, inform ation on the m anufacturingm ethods used and evidence of the product’s long-term stability, as w ell as supporting datafrom use of the product in other countries.

The M H LW has now approved biosim ilar versions of som atropin and erythropoietin. It hasalso introduced a reim bursem ent pricing regim e specifically for biosim ilars. W hereas allgenerics m ust be priced at no m ore than 70% of the price of the original drugs in order to beadm itted to the N ational H ealth Insurance (N H I) list of reim bursable drugs, biosim ilarscom m and a 10% prem ium on this ceiling –and can thus be priced at up to 77% of the priceof the original products.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 15/50

A B L E -P w C R E P O R T | 16

Chapter 3

Overview of the Indian Biologics Sector

The Indian biopharmaceuticals market is currently worth nearly $2 billion ayear and growing rapidly. Moreover, approximately 20 companies are alreadyproducing biosimilars, and about 50 such products (including imports and

multiple brands of the same products) are already available on the domesticmarket. So India has made a good start.

V IS IO N 2 0 2 0

3. 1 THE SIZE AND COMPOSITION OF THE INDIAN BIOLOGICS MARKET

The Indian biologics m arket consists prim arily of vaccines, m onoclonal antibodies,recom binant proteins and diagnostics. In the 2009/10 financial year, it w as w orth $1.9 billion–62% of the $3 billion generated by the biotechnology industry as a w hole (i.e., includingbioagricultural and bioindustrial products, bioinform atics and bioservices). The top 15biopharm aceutical com panies accounted for nearly $1.2 billion of this sum (see Table 6).

Table 6: The Top 15 Biopharmaceutical Companies Operating in the Indian Market

Rank in2010

Co mpa ny 2009-10Revenues1($ million s)

2008-09Revenues1($ million s)

% Chang e

Biocon 257.00 198.71 29.34

2 2Serum Institute of India 185.13 242.63 -23.7

3 Panacea Biotec 153.15 130.06 17.76

4 2Reliance Life Sciences 98.01

5 2N ovo N ordisk 74.49 71.87 3.64

6 Shantha Biotech 73.00 53.80 35.32

7 Indian Im m unologicals 59.43 50.41 17.89

8 Bharat Biotech 59.17 52.50 12.70

9 Eli Lilly 40.73 35.72 13.85

10 Bharat Serum s 38.12 30.50 25.00

11 H afkine Biopharm a 36.80

12 C adila H ealthcare 32.12 20.41 57.40

13 G laxoSm ithKline 26.86 18.18 47.75

14 Intervet India 26.48

15 Intas Biopharm a 25.05 19.44 28.82

1

Source: BioSpectrumN otes: (1) Revenues are for the Indian fiscal year, w hich runs from 1 A pril to 31 M arch;(2) BioSpectrum estim ates.

3.1.1 Vaccines

The vaccines sector (including hum an and anim al vaccines) represented the largest slice ofthe pie, w ith estim ated sales of $475 m illion in 2009/10, up from $436 m illion the previousyear. H um an vaccines generated about 80% of this revenue, w ith dom estic sales reaching$218 m illion and exports reaching $163 m illion. Sales of hum an vaccines are forecast togrow by 10-13% a year over the next five years, as better education and aw areness about

disease prevention, rising disposable incom es and governm ent participation boost dem and.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 16/50

A B L E -P w C R E P O R T | 17

V IS IO N 2 0 2 0CH A PTE R | 3

H ow ever, the m arket is clearly shifting from traditional “w hole-cell”pertussis vaccines tocom bination vaccines and “acellular”preparations. D om estic players such as Bharat Biotechand Shantha Biotech (w hich w as bought by Sanofi-Aventis for $783 m illion in July 2009)have already received m assive orders for pentavalent vaccines from the G O I for

im m unisation program m es in the states of H im achal Pradesh, Kerala, Tam il N adu, Jam m uand Kashm ir and Karnataka. D em and for new er products like the pneum ococcal conjugate,m eningococcal conjugate and hum an papillom avirus vaccines is also stim ulating thepaediatric and adolescent segm ent of the m arket, w hile flu vaccines w ill continue to play abig role in expanding the adult segm ent. A nd breakthrough products like Shanchol –thebivalent oral cholera vaccine jointly developed by Shantha Biotech and the InternationalVaccine Institute –w ill boost dem and in the m arket as a w hole.

3.1.2 Diagnostics and Targeted Therapeutics

The diagnostics and therapeutics sectors have also expanded in recent years. The diagnosticsm arket is currently w orth about $436 m illion, w ith m olecular diagnostics accounting forsales of about $300 m illion in 2009/10. The m arket is grow ing at 15-20% annually, w ithrevenues split equally betw een the m ultinationals –e.g., Roche, Siem ens (w hich hasacquired Bayer D iagnostics) and A bbott –and dom estic players –e.g., Tulip G roup, TransasiaBiom edicals, RFC L (D iagnova), Span D iagnostics and Trivitron. G radual acceptance of theconcept of personalised m edicine is driving m uch of this grow th.

M eanw hile, the therapeutics sector accounted for 15% of India’s biologics m arket in2009/10, w ith cancer therapies clocking up sales of $68 m illion. O ncology products are avery profitable line of business for m any Indian biopharm aceuticals m anufacturers becausethey address an area of high unm et need and thus com m and prem ium prices. U ptake of suchm edicines is also increasing, as dom estic producers m ake less expensive versions than those

m ade by the m ultinationals and a grow ing num ber of Indian patients get m edical insurance.

Oncology productsare a very profitableline of business formany Indianbiopharmaceuticalsmanufacturersbecause they addressan area of high

unmet need and thuscommand premiumprices.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 17/50

A B L E -P w C R E P O R T | 18

V IS IO N 2 0 2 0CH A PTE R | 3

3.1.3 Oral Diabetes Drugs and Insulins

The oral diabetes m arket is currently w orth about $338 m illion, w hile the insulin (and insulinanalogues) m arket is w orth about $133 m illion. N ovo N ordisk dom inates the latter, w ith

m ore than 50% of all sales, follow ed by Eli Lilly w ith 22% . H ow ever, both m arkets aregrow ing rapidly, as India becom es the “diabetes capital”of the w orld. Betw een 1995 and2005, the num ber of patients w ith diabetes doubled from 20 m illion to 40 m illion, and it isprojected to increase by another 70 m illion over the next 25 years. D em and for insulinanalogues is grow ing especially rapidly; the m arket increased at a com pound annual grow thrate of 32% , m easured in term s of value, in 2007-09. N ovel delivery devices w ill alsocontribute to the expansion of the m arket in the future.

3.1.4 Biosimilars

A bout 20 Indian com panies are already producing biosim ilars. D r. Reddy’s Laboratories,Ranbaxy, Biocon, Shantha Biotech, Reliance Life Sciences, Panacea Biotec and Intas

Biopharm aceuticals are am ong those that lead the w ay. But several other w ell-know ncom panies have recently entered the field, including G lenm ark, C ipla and Lupin Pharm a. InJune 2010, for exam ple, C ipla announced that it w as spending $65 m illion on stakes in tw obiotechnology com panies –M abPharm and BioM ab, based in India and H ong K ong,respectively –to bolster its presence in the global biosim ilars space.

A bout 50 biosim ilars have already reached the Indian m arket, and they are typically sold atdiscounts of as m uch as 85% , putting them w ithin reach of the m asses. In 2009/10,dom estic sales of erythropoietin rose to $22 m illion w hile sales of c-G C SF rose to $11 m illion,sales of interferons rose to $22 m illion and sales of streptokinase rose to $15 m illion.M oreover, dem and is likely to grow considerably, as India becom es m ore affluent. U Sinvestm ent bank G oldm an Sachs estim ates that the num ber of Indians w ith annual incom esof betw een $6,000 and $30,000 (m easured in term s of purchasing pow er parity) w ill

increase by 250-300 m illion during the next decade alone.

The global biosim ilars m arket has even m ore potential for the m ost efficient Indianbiosim ilars m anufacturers, since the m arket w ill be characterised by price com petition, evenw hen there are only a very lim ited num ber of rival products. That said, the m anufacturers ofbranded products are likely to use second-generation products w ith m ore convenientadm inistration schedules as a m eans of defending their territory. Som e of thesem anufacturers m ay also try to crow d out the com petition by producing their ow n biosim ilars.So the com petition is likely to be intense.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 18/50

A B L E -P w C R E P O R T | 19

Chapter 4

Competitive Analysis

India’s main national competitors in the biopharmaceutical space includeChina, Israel, South Korea, Singapore and Taiwan. These countries have initiateda number of infrastructure support and policy initiatives that provide anenvironment conducive to the growth of strong domestic industries.

V IS IO N 2 0 2 0

4

Big BioPharma is not the only threat to India’s biosimilars manufacturers. Theindustry is still in its infancy; however, a number of emerging economies have beenactively building up their biopharmaceutical expertise, and some countries areclearly positioning themselves to capitalise on increasing demand for biosimilars.The following section provides an overview of India’s key competitors. (We havetreated Central and Eastern Europe, and Latin America collectively.)

4.1 AUSTRALIA

A ustralia is one of the w orld’s leading established centres of biopharm aceutical expertise(together w ith the U S, Europe and C anada), thanks to a first-class research base and robustpatent regim e. The country is hom e to som e 450 biotechnology com panies and 600 m edicaltechnology com panies. In M arch 2010, m ore than 150 biotechnology and healthcarecom panies w ith a com bined m arket capitalisation of $47 billion w ere listed on the A ustralianStock Exchange –by far the biggest being C SL, w hich specialises in pharm aceuticals,vaccines and plasm a products.

4.1.1 Government Initiatives

The A ustralian G overnm ent is keen to m aintain this lead. It allocated about $7 billion forinvestm ent in science and biotechnology in 2009/10, although the tw o sectors fared lessfavourably in this year’s budget. The C om m onw ealth Scientific and Industrial ResearchO rganisation (C SIRO ) is the national body responsible for prom oting scientific research inA ustralia. It oversees various initiatives, including the C ooperative Research C entresprogram m e, w hich provides funding and other form s of support for long-term public-privatecollaborations aim ed at com m ercialising scientific innovations.

In 2009, the federal governm ent also launched “Com m ercialisation A ustralia”, a newinitiative to com m ercialise A ustralian research and ideas. The program m e offers variousform s of help, including up to $43,667 to pay for specialist advice and services; up to$174,670 (payable over tw o years) to assist w ith the recruitm ent of experienced executives;

proof-of-concept grants of $43,668 to $218,338 to test the com m ercial viability of aproduct, process or service; and repayable early-stage com m ercialisation grants of $218,338to $1.7 m illion to develop a new product, process or service to the stage w here it can betaken to m arket.

Individual states have supplem ented these initiatives w ith their ow n program m es.Q ueensland is particularly notable for its efforts; it has invested about $3 billion in the sector,and now has 90 core biotechnology com panies em ploying 1,900 scientists as w ell as som e66 biopharm aceutical research institutes em ploying 5,700 researchers. Q ueensland w ill alsohost A ustralia’s first m ajor contract m anufacturing facility for biologics, w hich is due to becom pleted in 2012.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 19/50

A B L E -P w C R E P O R T | 20

V IS IO N 2 0 2 0CH A PTE R | 4

4.1.2. Research Base

A ustralia has num erous w orld-class m edical research organisations, including the G arvanInstitute, Institute for M olecular BioScience, M enzies Research Institute, John C urtin School

of M edical Research, and A ustralian Institute of Bioengineering and N anotechnology.

4.1.3 Regulation

The A ustralian Therapeutic G oods Adm inistration (TG A ) is responsible for approving andregulating the m arketing of m edicines in A ustralia. The TG A has adopted the EM A’sguidelines for regulating biosim ilars.

4.1.4 Investment Incentives

The A ustralian G overnm ent offers tax concessions for biotechnology-related R& D . Theexisting system w ill be replaced in July 2010 w ith a new 45% refundable tax credit forcom panies w ith an annual turnover of less than $17 m illion. C om panies w ith a turnover of

m ore than $17 m illion can claim 40% .

4.2 CENTRAL & EASTERN EUROPE

The biotechnology sector in C entral and Eastern Europe is sm aller and less developed than itis in W estern Europe. There are currently about 260 biotechnology com panies in the region;29 are engaged in developing m edicines, 55 operate in other areas such as veterinarytherapeutics and industrial biotechnology, and the rem aining 176 provide biotechnologyservices like contract research, diagnostics, m anufacturing and analytical services.

H ungary, Poland and the C zech Republic lead the w ay. H ungary has 67 com panies engagedin developing hum an m edicines or providing bioservices. Poland has 38 such com panies, andthe C zech Republic 29. W e have therefore focused on these three countries in the details

below .

4.2.1 Government Initiatives and Investment Incentives

In 2004, the H ungarian G overnm ent established a Research and Technology InnovationFund to support the country’s biotechnology efforts. It contributes half the fund’s incom e;the rest com es from H ungary’s 26,000 private com panies, w hich are expected to pay at least0.25% of their turnover into the fund as an “innovation contribution”.

In 2005, the H ungarian G overnm ent also launched a five-year plan to develop thebiotechnology sector, w ith corporate tax breaks for foreign direct investm ents and newcom panies. Tax credits are offered on R& D investm ents, and R& D corporate tax allow ancesare generous, particularly if a com pany locates its laboratory at a university or public research

institute. Tailor-m ade incentive packages are available for biotechnology investm ents ofm ore than $8 m illion that result in the creation of at least 10 new jobs, and highly educatedstudents can be em ployed tax-free in educational and research activities.

The Polish G overnm ent likew ise provides grants for com panies that conductbiopharm aceutical R& D , via the biotechnology division of the State Com m ittee for ScientificResearch. G rants typically range from $50,000 to $100,000. A nd the C zech G overnm entsupports biotechnology com panies through C zechInvest, its investm ent and businessdevelopm ent agency. C zechInvest has identified nine key areas of investm ent, including lifesciences, m edical devices and R& D –w ith particular em phasis on m olecular biology,

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 20/50

A B L E -P w C R E P O R T | 21

V IS IO N 2 0 2 0CH A PTE R | 4

biom edicine and biotechnologies, and the developm ent of new m aterials designed toadvance the life sciences.

4.2.2 Research Base

M ost of the biotechnology-related R& D conducted in C entral and Eastern Europe isperform ed at universities or institutes, and collaboration w ith industry is lim ited. H ungaryhas eight research institutes specialising in biom edical research, including a genetics andim m unobiology departm ent at Sem m elw eis University, Budapest. Poland has about 40universities, hospitals and research institutes engaged in biotechnology-related R& D , as w ellas five technology parks. In D ecem ber 2009, it also set up a new incubator, calledScience2Business, to support the com m ercialisation of scientific discoveries and inventions.The incubator w ill cover five sectors: biotechnology, telem edicine, renew able energy,inform atics and m obile technologies. The C zech Republic has 300 biotechnology institutesand 10 established technology parks and clusters. The governm ent is currently building anew biotechnology park at M asaryk U niversity, in Brno, and an international clinical researchcentre that it hopes w ill be able to com pete w ith the top research hubs around the w orld.

4.2.3 Regulation

A ll the new European U nion m em ber states w ere required to bring their regulatoryfram ew orks into line w ith the rules prevailing in the rest of the bloc during the accessionprocess. They w ere also required to harm onise their patent protection law s w ith those inW estern Europe, although full harm onisation w ill not occur until 2011-2019, depending onthe country and product.

4.2.4 Access to Capital There is very little private funding from venture capital sources and angel investors inH ungary, Poland and the C zech Republic. The m ajority of the funding for biotechnology-

related research com es from state or European U nion fram ew ork program m es and structuralfunds.

4.2.5 Access to Talent

A ll three countries have a highly educated w orkforce and labour costs are very m uch low erthan they are in W estern Europe. H ow ever, H ungary has clearly stated that it does not w antto com pete on the basis of low w ages and is actively trying to w oo talented H ungarianscientists w orking overseas back to their hom eland.

4.3 CHINA

C hina’s biopharm aceuticals sector is entering w hat has been called a “golden age”, thanksto substantial investm ent from the central governm ent, w hich w ants to see it becom e one ofthe country’s leading industries by 2020. A num ber of Chinese biopharm aceuticalenterprises have entered into alliances w ith global biopharm aceutical research institutionsand m ultinationals, prim arily to develop therapeutic vaccines, M A bs and recom binantproteins. The central governm ent is also prom oting the developm ent of strongerregulations, better enforcem ent of the patent protection law s and various other m easures tosupport the industry.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 21/50

A B L E -P w C R E P O R T | 22

V IS IO N 2 0 2 0CH A PTE R | 4

4.3.1 Government Initiatives

C hina expressly stated in its National M edium - and Long-Term Science and TechnologyD evelopm ent Plan O utline (2006–2020) that it aim s to acquire expertise in various cutting-

edge technologies in the biopharm aceutical space over the next 15 years. These includetarget discovery, drug m olecule design, gene operation and protein engineering, stem cellengineering and a new generation of industrial biotechnology tools. The central governm entalso issued a new regulation on the registration of drug technology transfers in A ugust 2009,w hich should prom ote technological innovation, w hile the C hinese N ational D evelopm entand Reform C om m ission (N D RC ) has secured an additional $65 m illion of funding to supportadvances in biological m edicine, bio-breeding and biom edical engineering.

H ow ever, the governm ent has already im plem ented 19 price-cutting initiatives for m edicinesand plans to m ake m ore cuts in the future. This m ay affect the country’s biopharm aceuticalrevenue grow th, but w ill benefit C hinese patients –and the overall increase in volum e m aybe sufficient to offset the reduction in per-unit sales.

4.3.2 Protection of Intellectual Property

C hina is m aking significant efforts to im prove the protection of intellectual property rights incom pliance w ith the requirem ents of the W orld Trade O rganisation. Several m ultinationalshave now established R& D centres in C hina, indicating that there is grow ing globalconfidence in the country’s patent-protection regim e.

4.3.3 Regulatory and Funding Reforms

The C hinese State Food and D rug A dm inistration (SFD A ) is introducing new policies toencourage innovation, restrict im itation and encourage biopharm aceutical outsourcing.C hina is also in the process of establishing an effective venture capital system to attractforeign venture capital into the dom estic BioPharm a industry.

4.3.4 Biotechnology Clusters

C hina’s central and local governm ents have built m ore than 100 biotechnology parks. Som eof these parks have been very successful –e.g., Shanghai Zhangjiang H igh-tech Park, w hichhas attracted num erous m ultinational and dom estic com panies, including Roche, N ovartisBiom edical Research, Kirin Kunpeng Biopharm a, W uxi Pharm aTech and Shanghai LeadD iscovery. H ow ever, m any parks still have high vacancy rates.

4.3.5 Enterprise Development

A num ber of C hinese biopharm aceutical com panies have joined forces to enhance theiroverall strength. The biopharm aceutical giant C N BG is one such instance; it w as form ed by

m erging six m ajor biological product institutes in Beijing, Shanghai, C hangchun, W uhan,Lanzhou and C hengdu w ith tw o biopharm aceuticals m anufacturers (Beijing Tiantan andC hengdu Rongsheng). C N BG now em ploys 10,000 people across C hina.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 22/50

A B L E -P w C R E P O R T | 23

V IS IO N 2 0 2 0CH A PTE R | 4

4.3.6 Increasing Focus on R&D

C hinese biopharm aceutical com panies are increasingly aw are of the need to invest in R& D .Shenyang Sunshine Pharm a, w hich invests 10% of its revenues in R& D , has developed

several successful products, for exam ple, and various other com panies are now investing intechnology platform s for upstream R& D and clinical studies. C hina’s support bioservicessubsector is also expanding rapidly. Several hundred C RO s currently operate in C hina,offering integrated or specialised services, and som e of these C RO s are evolving from one-offstudy vendors into viable, strategic long-term players.

4.3.7 Greater International Collaboration

A grow ing num ber of C hinese nationals w ho have resided overseas are returning to theirhom e country and taking im portant positions in the dom estic BioPharm a industry. They areusing their connections to forge pow erful international alliances.

4.4 ISRAEL The Israeli biopharm aceuticals sector has grow n im pressively over the last decade, as a resultof its strong track record in research. The country devotes 35% of its research activities to thelife sciences and has the largest num ber of scientists per capita in the w orld. Its expertise inneurological disorders, cancer and autoim m une diseases is particularly notew orthy, but it isalso a global leader in regenerative m edicine and cell therapy. M oreover, w ith a highpercentage of graduates in m athem atics, physics and com puter sciences, it is w ell placed tom ake an im pact in interdisciplinary technologies such as bioinform atics and proteom ics.

4.4.1 Government Initiatives

The Israeli G overnm ent declared the life sciences industry –and biotechnology in particular –

a “preferred sector”in 2005. The O ffice of the C hief Scientist (O C S) of the M inistry ofIndustry, Trade and Labour is responsible for adm inistering governm ent policy regarding thesupport and encouragem ent of industrial R& D . It operates various support program m es,including grants of up to 50% of the approved budget for m arket-driven com petitive R& Dprojects, up to 66% for start-up com panies and advanced generic technology, and up to85% for technology incubators. The O C S also participates in bi-national funding initiativesw ith the U S, U K, A ustralia, Singapore, C anada and Korea; and recently launched a newfunding route to bridge the gap betw een basic and applied research, w ith grants of up to$95,000.

4.4.2 Research Base

Biopharm aceutical research is carried out at seven universities, five colleges and 10

specialised institutes as w ell as the m ajor hospitals. The leading universities also havecom m ercial offices of technology transfer to facilitate the com m ercialisation of theirresearch.

4.4.3 Technology Incubators

Israel has 23 high-technology incubators, one of w hich is dedicated to biotechnology andtw o to industry-related technologies. Each incubator houses up to 15 com panies andprovides funding of about $500,000 per com pany for the first tw o or three years of its life,

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 23/50

A B L E -P w C R E P O R T | 24

V IS IO N 2 0 2 0CH A PTE R | 4

w hen the risk is highest and private funding is scarce. A n estim ated 1,000 high-techcom panies have “graduated”so far, but a report subm itted to the Knesset financesubcom m ittee for prom oting and assisting high-tech technology suggests that the successrate has fallen in recent years. Betw een July 2006 and June 2009, only 100 com panies

m anaged to raise $500,000 or m ore. The subcom m ittee has now convened to consider anum ber of options, including extending the incubation period.

4.4.4 Regulation

Israel has aligned its regulatory fram ew ork w ith those in the U S and European U nion, andm edications approved by the FD A or EM A are approved m uch m ore quickly than those thathave not received such approval. The Israeli M inistry of H ealth and FDA have also signed am utual recognition agreem ent to enable full acceptance and recognition by the FDA ofclinical trials conducted in Israel for new drugs and m edical devices. Israel’s IP law sconcerning technology-based products and services, pharm aceuticals and other em ergingsectors likew ise closely resem ble those of the U S and European U nion.

4.4.5 Investment Incentives

The Israel Investm ent C entre (IIC ) of the M inistry of Industry and Trade offers com panies inknow ledge-based industries and their investors various tax incentives and grants. Investorsm ay apply for one of tw o incentives: governm ent participation of up to 32% in capitalinvestm ents for creating jobs in export industries; or accelerated depreciation and a taxholiday of up to 10 years on undistributed profits, based on the capital that has beencom m itted to job creation in export industries. (The precise am ount of the benefit dependson the location.)

4.4.6 Access to Capital

Israel has a robust financial infrastructure and w ell-developed venture capital industry.

H ow ever, fledgling biopharm aceutical com panies have had a hard tim e raising capitalfollow ing the global dow nturn in the capital m arkets last year. In the first quarter of 2010,Israeli high-tech com panies raised only $234 m illion from venture investors (both local andforeign), less than in any preceding quarter for the past five years. The life sciences sectorattracted over a third of this m oney, but m uch of it w as directed tow ards m ore developedbusinesses.

The K nesset finance subcom m ittee for prom oting and assisting high-tech technology is nowreview ing a num ber of proposals for supporting the sector. They include creating a privatefund w ith state leveraging, offering incentives for venture capital investm ent in seedcom panies and establishing “second-stage incubators”to prom ote “industrialisation”.

4.5 LATIN AMERICA

Latin A m erica’s biotechnology industry is grow ing at an im pressive rate. Bioagricultural andbioindustrial applications (biofuels) account for m ost of this grow th, but the BioPharm asector is also getting stronger. The m ost active countries in the region are A rgentina, Braziland C hile. Brazil has m ore than 100 biopharm aceutical com panies, w hile A rgentina andC hile have about 23 and 15 such com panies, respectively. A ll three countries have alsobecom e centres for clinical research. In 2009, there w ere m ore than 425 trials in C hile alone.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 24/50

A B L E -P w C R E P O R T | 25

V IS IO N 2 0 2 0CH A PTE R | 4

4.5.1 Government Initiatives

The A rgentinian G overnm ent has im plem ented several program m es to prom ote basicresearch and technological investm ent. In 2007, it also established a M inistry of Science and

Technology specifically to encourage scientific and technological innovation. The M inistryadm inisters tw o governm ent-backed funds: the Fund for Scientific and TechnologicalResearch and the A rgentine Technology Fund.

Brazil introduced a national biotechnology policy in the sam e year, and undertook to invest$5.8 billion over a 10-year period, w ith approxim ately 60% of the funds com ing from publicsources. C hile has likew ise taken significant steps to incorporate biotechnology into itseconom y. The N ational Innovation Board for C om petitiveness, w hich reports to thePresident, is responsible for coordinating the efforts of the governm ent agencies concerned.These include the C hilean N ational C om m ission for Scientific and Technological Research(C O N IC YT), w hich supports basic research and the developm ent of resources, principally byfinancing academ ic research and collaborations betw een universities and private firm s; andthe C hilean Econom ic D evelopm ent Agency (C O RFO ), w hich prom otes the

com m ercialisation of new technologies and products.

4.5.2 Research Base

A rgentina has m ore researchers per active person than any other country in Latin A m erica,and over 115 A rgentinian research institutes and universities are engaged in biotechnology-related research. But m ost of this w ork is in the field of bioagriculture. Brazil, by contrast, hasa strong reputation in fundam ental biopharm aceutical research, although it has been lesssuccessful in com m ercialising that research. It can call on several strong public researchinstitutions specialising in health biotechnology, including the O sw aldo C ruz Foundation inRio de Janeiro and the Institute Butantan in SãoPaulo.

M eanw hile, C hile has 61 university research centres, 15 incubators and 10 technology

transfer centres. It is also building a num ber of research nuclei as part of its M illenniumScientific Initiative, w hich has been partly funded by the W orld Bank. Five such nuclei havenow been established, including the M illennium Institute for A dvanced Studies in C ellBiology and Biotechnology, the C enter for Scientific Studies and the M illennium Institute forFundam ental and A pplied Biology. A gain, how ever, hum an health accounts for a relativelysm all percentage of the country’s biotechnology activities.

4.5.3 Regulation

M ost Latin A m erican countries (including A rgentina, Brazil and C hile) have now aligned theirlocal regulations w ith the D eclaration of Helsinki, C ouncil for International O rganisations ofM edical Sciences, and International C onference on H arm onisation-G ood C linical Practice(IC H -G C P) guidelines, and all have a regulatory agency responsible for pharm aceuticals,

m edical devices and clinical research. But there are still significant differences in the level ofregulatory sophistication in the region.

4.5.4 Intellectual Property Protection

A rgentina, Brazil and C hile are all signatories to the A greem ent on Trade Related A spects ofIntellectual Property Rights (TRIPS). But although C hile scores highly for its enforcem ent ofthe rules on patent protection, A rgentina and Brazil fare less w ell. The International PropertyRights Index (2010) aw ards the latter tw o countries scores of 64 and 84, respectively(significantly below India’s score of 53).

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 25/50

A B L E -P w C R E P O R T | 26

V IS IO N 2 0 2 0CH A PTE R | 4

4.5.5 Investment Incentives

A rgentina offers various incentives for biotechnology-related research under Law 26,270,including accelerated am ortisation of incom e tax, early reim bursem ent of value-added tax

(VAT) and tax credit bonds for services purchased from governm ent-ow ned researchinstitutes. Brazil has also enacted an “Innovation Law ”, w hich provides tax incentives forR& D , deductions on expenses related to patent filing and prosecution, and partial paym entof the salaries of R& D scientists em ployed by biotechnology com panies. C hile has adopted asim ilar approach, w ith tax incentives for R& D , subsidies of up to $30,000 to financeinternships and subsidies of up to $730,000 to support innovation in the areas of goods,services, processes and organisational or trading m ethods.

4.5.6 Access to Capital

Latin A m erica’s venture capital industry is still undeveloped. H ow ever, experts anticipate thatit w ill grow rapidly in Brazil and C hile (though not in A rgentina) over the next few years. Brazilis one of the em erging countries w ith the greatest appeal for the investm ent com m unity,

thanks to the good econom ic m anagem ent of successive dem ocratic governm ents, the sizeof its dom estic m arket, the strength of its industrial sector and the significant tax incentivesavailable to venture investors. C hile also has a relatively strong econom y, based oncom m odity production, and a dynam ic, m odern entrepreneurial class.

4.6 SINGAPORE

Singapore is w ell-know n for being politically stable and business-friendly. It offers clear andconsistent governm ent guidelines, a reliable patent regim e, a first-rate physicalinfrastructure and a favourable tax environm ent; indeed, in 2009, the W orld Bank dubbed itthe w orld’s “easiest place in w hich to do business”. The city-state has also created a pow erfulbiopharm aceutical nexus. M ore than 30 m ultinationals have established regional

headquarters there, and N ovartis chose Singapore as the hom e for its prestigious Institute forTropical D iseases.

4.6.1 Government Initiatives

In the late 1990s, Singapore identified the biom edical sciences as an area w ith trem endousgrow th potential. Betw een 2000 and 2005, it put in place the key building blocks to establisha core biom edical research base. In the second phase of the initiative (2006-2010), it hasbeen focusing on strengthening its capabilities in translational and clinical research. It has putserious m oney into these efforts, w ith a com m itm ent of $9.8 billion for the four years endingD ecem ber 2010.

4.6.2 Research Base

Singapore has established a strong scientific foundation w ith seven research institutes andfive research consortia covering clinical sciences, genom ics, bioengineering, m olecular/cellbiology, m edical biology, bioim aging and im m unology. It has also m ade significant progressin translational and clinical research; dedicated Investigational M edicine U nits, m any of themco-located w ith institutes of higher learning, conduct early-phase trials in public hospitals,w hile the Singapore C linical Research Institute focuses on later-stage trials.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 26/50

A B L E -P w C R E P O R T | 27

V IS IO N 2 0 2 0CH A PTE R | 4

4.6.3 Biotechnology Clusters

Singapore has built a m ajor biom edical research hub that co-locates public-sector institutesand private-sector corporate laboratories. It is currently expanding the Biopolis (as the hub isknow n), w ith a 460,000 square-feet expansion that w ill bring its total research space to m orethan three m illion square feet.

4.6.4 Regulation

Singapore’s Health Sciences A uthority (H SA ) is actively involved in defining new regulatoryfram ew orks and pursuing new areas of research in regulatory science. The H SA has forgedstrong links w ith m any of the w orld’s leading regulatory agencies. In O ctober 2009,Singapore w as also accepted into the O EC D’s M utual A cceptance of D ata fram ew ork, w hichm eans that data from G LP-com pliant pre-clinical trials conducted in Singapore can beaccepted by 30 O ECD and non-O ECD m em bers, including the U S, EU and Japan.

4.6.5 Manufacturing Expertise

Singapore has a strong track record in both sm all-m olecule active pharm aceutical ingredient

and secondary m anufacturing. It is also building a substantial biologics m anufacturing base.Baxter, G laxoSm ithKline Biologicals and Roche have already opened biologicsm anufacturing plants in Tuas Biom edical Park, and Lonza is currently constructing a celltherapy m anufacturing plant w hich should be operational in 2011.

4.6.6 Access to Talent

Singapore has w orked hard to develop its expertise in the biosciences. Som e 4,000researchers are now engaged in biopharm aceutical R& D , including about 1,200 foreignnationals. In 2001, Singapore’s A gency for Science, Research and Technology (A *STA R) alsolaunched a national scholarship program m e to fund the education of 1,000 postgraduatestudents at the w orld’s top universities. To date, the agency has aw arded m ore than 500biom edical sciences scholarships, and m ore than 100 recipients have returned to w ork in the

city-state after com pleting their PhD s. A *STA R has likew ise introduced various aw ards toattract bright young researchers and develop a cadre of local clinician scientists.

4.7 SOUTH KOREA

In the late 1990s, the South K orean G overnm ent launched a program m e to m ake thecountry one of the top biotechnology pow ers by 2010. South Korea’s life sciences industry isnow the fourth largest in A sia. But the governm ent is not resting on its laurels; in 2006, itannounced a new initiative called “BioVision 2016”to invest another $14.3 billion in theindustry, w ith the aim of turning it into a $60-billion m arket over the next 10 years.

Singapore’s Health SciencesAuthority (HSA) is actively involved

in defining new regulatoryframeworks and pursuing newareas of research in regulatoryscience.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 27/50

A B L E -P w C R E P O R T | 28

V IS IO N 2 0 2 0CH A PTE R | 4

4.7.1 Government Initiatives

In 2008, the governm ent spent som e $930 m illion supporting biotechnology research andcom m ercialisation, as part of its BioVision 2016 program m e. It had three key objectives:

strengthening the scientific infrastructure to em phasise bioinform atics, nanobiotechnologyand synthetic biology; fostering the globalisation of the biotechnology industry; and creatingbiotechnology clusters.

4.7.2 Regulation

The Korean Food and D rug A dm inistration (KFDA ) has established a clear regulatoryapproval pathw ay for biosim ilars, w ith an am endm ent to the “Rules G overning the A pprovaland Exam ination of Biological Products”(effective as of July 15, 2009), w hich establishes thedefinition of a biosim ilar, and the publication of guidelines for the evaluation of biosim ilarson July 27, 2009.

4.7.3 Research Base

South Korea is still at the forefront of stem cell research, despite the setback that occurred in2006 w hen one of the country’s leading researchers w as charged w ith using fraudulent data.It also aim s to becom e a global leader in biosim ilars. In July 2009, shortly after the regulatorypathw ay for biosim ilars w as established, South Korean electronics giant Sam sungannounced that it w ould invest $389 m illion in biosim ilars over the next five years. O thersignificant developm ents include the successful com pletion of a South Korean clinical trial ofa biosim ilar version of Enbrel produced by Taiw anese drug developm ent com pany M ycenaxBiotech, and an agreem ent betw een U S-based H ospira and C elltrion to develop and m arketeight biosim ilars.

4.7.4 Biotechnology Clusters

South Korea is currently investing about $5 billion in the construction of tw o high-techm edical-industrial centres. The bigger of the tw o –the O song Bio-H ealth ScienceTechnopolis, based in C heongju (about 60 m iles south of Seoul) –is scheduled forcom pletion in 2012. It w ill house the K orean Food and D rug A dm inistration (KFDA ), KoreanN ational Institute of H ealth, Korea C enters for D isease C ontrol and Prevention, and variousother governm ent bodies as w ell as private com panies.

4.7.5 Clinical Trials Expertise

South Korea has earned a solid reputation as a place in w hich to perform clinical trials. It hashighly trained physicians and a good IT infrastructure, as w ell as plenty of urban hospitals(w hich m ake it easy to recruit trial patients).

4.7.6 Investment Incentives

The South Korean G overnm ent offers foreign investors in high-tech com panies a w ide rangeof tax incentives, including tax credits on corporate and personal incom e tax, acquisition tax,registration tax, property tax and aggregate land tax. It also operates a num ber of free tradezones and free econom ic zones.

8/20/2019 Report Bio Pharma Vision 2020

http://slidepdf.com/reader/full/report-bio-pharma-vision-2020 28/50

A B L E -P w C R E P O R T | 29

V IS IO N 2 0 2 0CH A PTE R | 4

4.8 TAIWAN

The Taiw anese G overnm ent form ulated a “Prom otion Plan for the Biotechnology Industry”in 1995, under w hich it enacted various law s and regulations relating to biotechnology; and

encouraged the private sector to invest in R& D , technology transfer, and the training anddevelopm ent of personnel. It has stepped up these efforts during the past decade, and agrow ing num ber of businesses are now focusing on the sector.

4.8.1 Government Initiatives

Betw een 2000 and 2008, the Executive Yuan’s National D evelopm ent Fund invested $394m illion in the biotechnology industry. Then, in M arch 2009, the Executive Yuan launched theTaiw an Biotechnology Takeoff Package, aim ed at boosting the sector and capturing a shareof the global m arket. This package com prises four key elem ents: strengthening the country’stranslational research and com m ercialisation skills; establishing a biotechnology venturecapital fund; founding a Food and D rug A dm inistration; and creating an integrated biotechincubation centre.

4.8.2 Biotechnology Clusters

Taiw an is establishing a num ber of large science parks focusing on biopharm aceuticalresearch and m anufacturing. It aim s to build tw o clusters: one in the Southern Taiw anScience Park (STSP) and the other in northern Taiw an’s Hsinchu Biom edical Science Park(H BSP). The STSP is already open for business, w ith nearly 20 biopharm aceutical com paniesfocusing on vaccines, bioagriculture, biom edical inspection and floriculture, as w ell ascom panies that m anufacture m edical equipm ent and devices. C onstruction of the H BSPstarted in O ctober 2009 and, once the park is com plete, it is expected to host about 30biopharm aceutical m anufacturers.