Embed Size (px)

Citation preview

Renewable Energy Build Out: Progress to Date and the Path Ahead

Steven G. ChalkDeputy Assistant Secretary for Renewable EnergyU.S. Department of Energy

August 4, 2008

U.S. Renewable Electricity Capacity by

Source (2000-2007)

Status of Renewable Electricity in the U.S.

Although renewable energy (excluding hydropower) is still a relatively small portion of both U.S. and global electricity supplies, U.S. renewable energy installations have nearly doubled since 2000

Sources: EIA, AWEA, IEA PVPS, Navigant, SEIA, GEA

MW

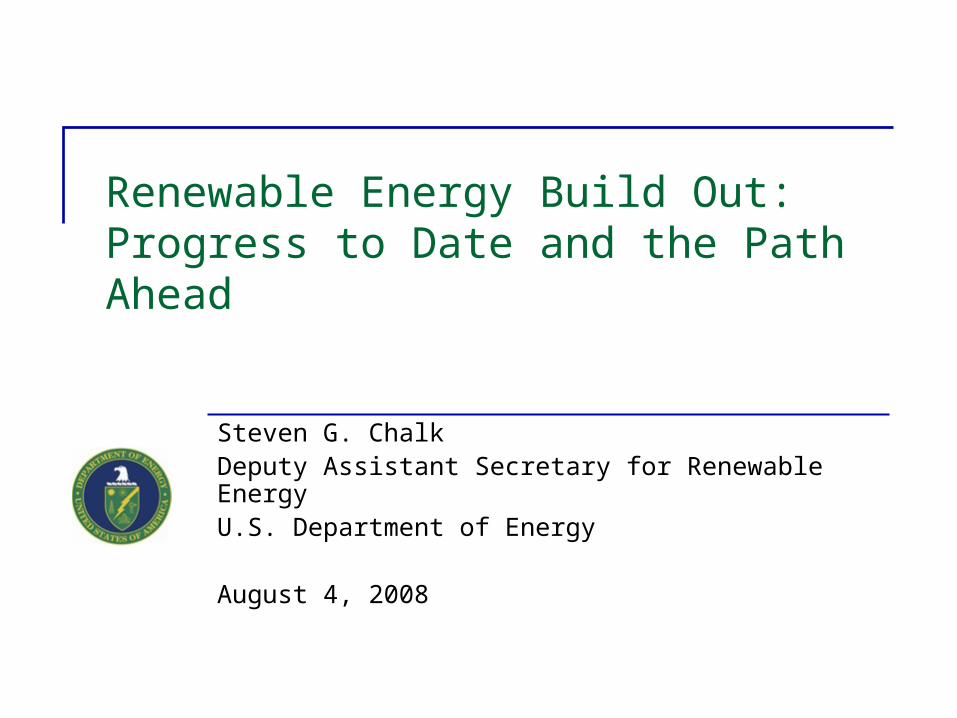

In Context: Global Renewable Energy Development

843 GW 9.5 GW 74 GW 5.1 GW 0.4 GW 45 GW

0

10

20

30

40

50

60

70

80

90

2002 2003 2004 2005 2006 2007 (projected)

UnitedStates

EuropeanUnion

2006EU: 9.1% of total installed capacityUS: 2.5% of total installed capacity

Renewable Electricity Installed Capacity (2002-2007) –United States and the European Union

Gig

aw

att

s

United States European Union

GDP (2006) $13,060 Billion $13,080 Billion

Total Nameplate Capacity (2006) 1,076 GW 720 GW

*Excludes Hydropower

What Europe has done to promote GW-scale clean energy:

• EU renewable energy targets have been in place since 1997

• In March 2007, EU leaders reached a binding agreement that 20% of the 27 member countries’ energy should be produced from renewable sources by 2020

• Individual countries have large incentives for RE development, including renewable portfolio standards, feed-in tariffs, capital subsidies, and other fiscal incentives

• Instituted stable, long-term policies

Germany’s Renewable Energy Sources Act (EEG) first regulated feed-in tariffs in 1991, and underwent major updates in 2000 and 2004. EEG stipulates purchase amounts of renewable energy for local power companies (with feed-in tariffs provided for a set duration at a declining rate).

.

U.S. and European Renewable Electricity Installed Capacity*U.S. and European Renewable Electricity Installed Capacity*

Although total electric capacity is lower in the European Union than the United States, the EU has more renewable electricity capacity installed

Past Investments Have Dramatically Reduced Renewable Energy Costs

Renewable energy can come online at a rate and scale that matters

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007

Per

cen

t o

f A

nn

ua

l Ca

pa

city

Ad

diti

ons

0

20

40

60

80

100

To

tal A

nn

ua

l Ca

pa

city

Ad

diti

on

s (G

W)

Wind Other Renewable

Gas (CCGT) Gas (non-CCGT)

Coal Other non-Renewable

Total Capacity Additions (right axis)

Source: EIA, Ventyx, AWEA, IREC, Berkeley Lab

Renewable energy has been contributing to a growing portion of U.S. electric capacity additions (40% in 2007; up from 1% in 2002)

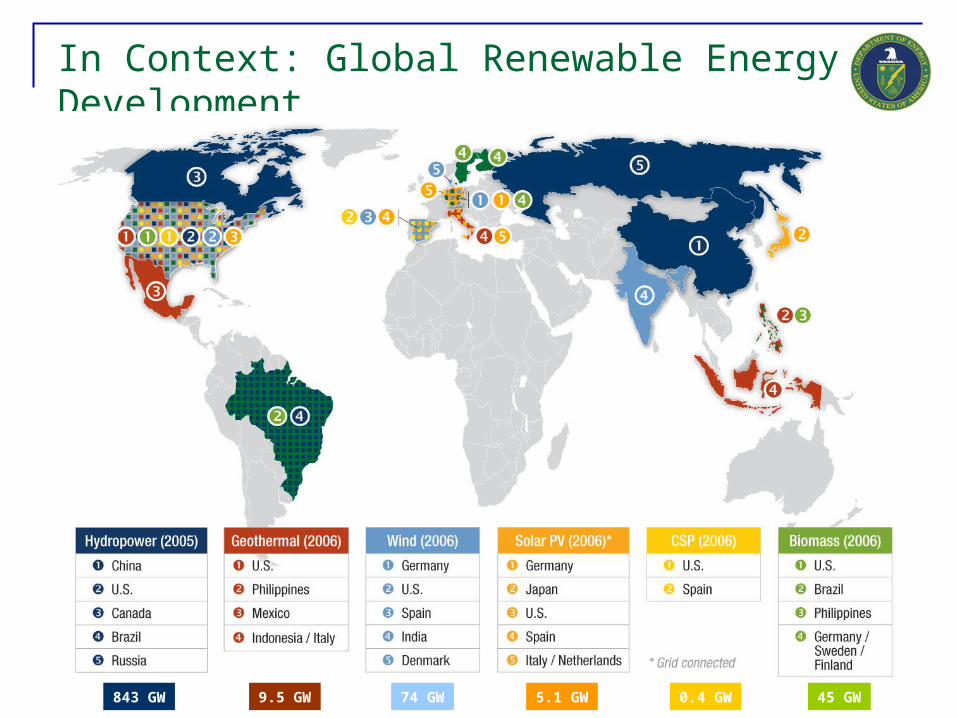

20% Wind in the U.S. is Possible (300 GW by 2030)

Annual and Cumulative Wind Installations by 2030Annual and Cumulative Wind Installations by 2030

Achieving 20% Wind will require energy infrastructure improvements, stable state and federal policies, and technology improvements

• RATE OF SCALE-UP: Installation rates need to increase to ~16 GW/yr by 2018 until 2030

• INVESTMENTS: Over $1 trillion in economic investment

• BENEFITS: o half million jobs for manufacturing, installation and operations; o new property tax revenues; o natural gas demand reduced by ~7 billion ft3/day; o 25% of expected electric sector CO2 emissions avoided in 2030; o 8% reduction in electricity sector water consumption

• 20% WIND REQUIRES: significant changes in transmission systems to deliver wind energy; improved turbine technology to generate wind power; and large expanded markets to purchase and use it

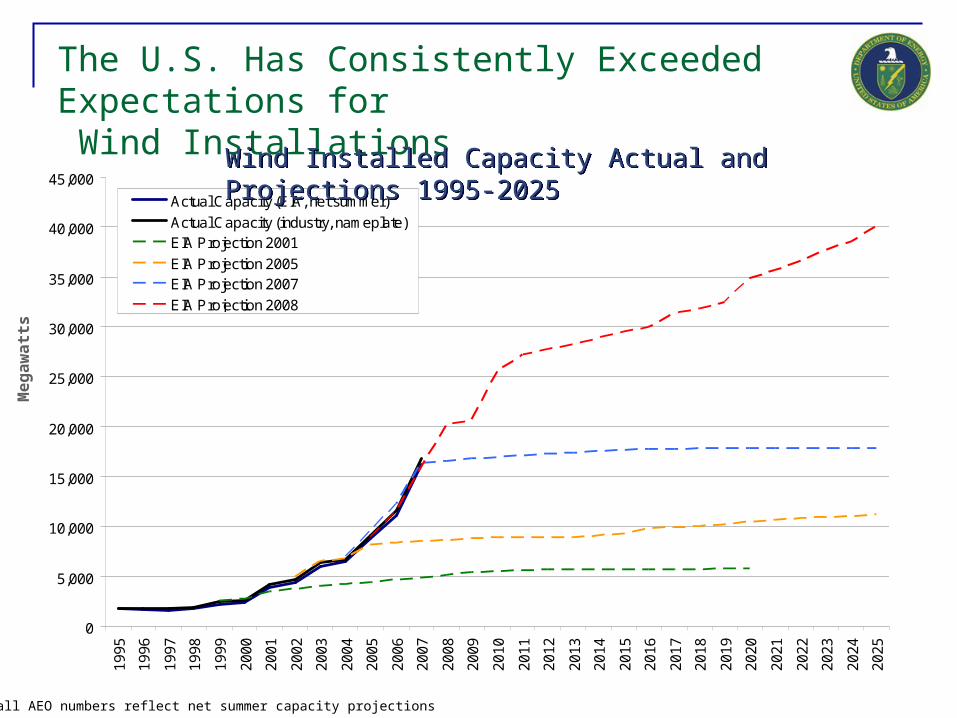

The U.S. Has Consistently Exceeded Expectations for Wind Installations

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Actual Capacity (EIA, net summer)

Actual Capacity (industry, nameplate)EIA Projection 2001

EIA Projection 2005EIA Projection 2007

EIA Projection 2008

Note: all AEO numbers reflect net summer capacity projections

Me

ga

wa

tts

Wind Installed Capacity Actual and Projections 1995-2025Wind Installed Capacity Actual and Projections 1995-2025

• Enhanced Geothermal Systems (EGS): engineered reservoirs that have been stimulated to extract economical amounts of heat from unproductive geothermal resources.

• DOE-sponsored, MIT-led study “The Future of Geothermal Energy”

• Found: potential to tap up to 100 GW of energy in the first 10 km of rock underneath the U.S. by 2050 (one-tenth of current U.S. generating capacity)

• Congress funded DOE Geothermal Program in Fiscal Year 2008 with $20 million – this is being used primarily to explore R&D and demonstration projects of EGS systems

EGS Exploration and DevelopmentEGS Exploration and Development

Future GW-Scale Renewable Energy Technologies: Enhanced Geothermal Systems (EGS)

Opportunity to limit the risk of substantial upfront drilling costs of geothermal energy (hydrothermal and EGS)

The Problem: High risk, significant early-

stage drilling costs necessary to quantify

geothermal potential of a site inhibit the deployment of

geothermal energy.

Potential Solution: Cost-Shared Exploratory Drilling Program

• Developer must have an adequate resource site and ability to successfully develop and finance the project in order to be eligible for funding.

• Government provides ~30% cost for drilling exploratory wells; developer provides other ~70%. Government cost-share may vary depending on risk.

• Developer repays government (with interest) upon drilling a successful well.• Information obtained from drilling both successful & unsuccessful wells is

provided to the government.• Government compiles a database of drilling information.

U.S. EGS Resource Map (10 km depth)U.S. EGS Resource Map (10 km depth)

New Effort: Water Power Technologies

• It is estimated the resource potential of ocean energy is on par with conventional hydropower (which currently makes up 7% of U.S. electricity generation)

Worldwide Commercial Plants in Operation

Type/

Project NameLocation Technology

Size (MW)

Year of Op.

WAVE

Aguçadora Wave ParkPóvoa de Varzim, Portugal

Pelamis Wave Energy Converter 2.25 2007

TIDAL

RITE ProjectEast River, New York

Verdant Free Flow Turbines 0.120 2007

TIDAL

Annapolis Royal PlantBay of Fundy, Nova Scotia

Tidal barrage; Straflo turbine-generator 20 1984

TIDAL

La RanceBretagne, France Tidal barrage, Bulb

Turbines 240 1966

Wave: Pelamis—Ocean Power Delivery

Tidal: Verdant—Power RITE Turbine

• Fiscal Year 2008 – Congress appropriated $10 million for Water Power R&D

Pro

du

ctRoadblocks to Renewable Energy Growth

Barriers Potential Solutions

TransmissionPlan, build and pay for new transmission using the Power Marketing Authorities’ eminent domain; build cost of transmission into electricity purchase price

Grid integrationIncreased R&D and public-private collaboration for load balancing and RE storage technologies; experiment in suitable sites, such as Hawaii

Siting Interagency collaboration (e.g., between DOE and DOI) that works to create Programmatic Environmental Impact Statements and open federal lands for RE developmentPermitting

Public perception and education

Promote link between greenpower and siting/permitting/transmission

Financing

Recognition of life cycle costing; Use power purchasing authority of the government to stimulate development (to meet pre-existing EPAct 2005 goals); Loan guarantees; Clean Energy Bank; Long-term power purchase agreements

Manufacturing and materialsIncentives for domestic, high-quality materials and manufacturing supply-

chain to support rapid growth; strategic materials

Qualified workforce development

Partner with universities, community colleges, and vocational schools to expand curricula and enrollment

Uncertain policy environment (e.g., on-again-off-again production tax credit)

Need for stable, long-term production incentives that are phased out over time. Need policies for investors (for capital risk, supply-chain development, project development cycle, etc.)

Access to: 1. Market 2. Capital 3. Product

Mar

ket

Ca

pita

l

Pro

du

ctRoadblocks to Renewable Energy Growth

Barriers Potential Solutions

TransmissionPlan, build and pay for new transmission using the Power Marketing Authorities’ eminent domain; build cost of transmission into electricity purchase price

Grid integrationIncreased R&D and public-private collaboration for load balancing and RE storage technologies; experiment in suitable sites, such as Hawaii

Siting Interagency collaboration (e.g., between DOE and DOI) that works to create Programmatic Environmental Impact Statements and open federal lands for RE developmentPermitting

Public perception and education

Promote link between greenpower and siting/permitting/transmission

Financing

Recognition of life cycle costing; Use power purchasing authority of the government to stimulate development (to meet pre-existing EPAct 2005 goals); Loan guarantees; Clean Energy Bank; Long-term power purchase agreements

Manufacturing and materialsIncentives for domestic, high-quality materials and manufacturing supply-

chain to support rapid growth; strategic materials

Qualified workforce development

Partner with universities, community colleges, and vocational schools to expand curricula and enrollment

Uncertain policy environment (e.g., on-again-off-again production tax credit)

Need for stable, long-term production incentives that are phased out over time. Need policies for investors (for capital risk, supply-chain development, project development cycle, etc.)

Access to: 1. Market 2. Capital 3. Product

Mar

ket

Ca

pita

l

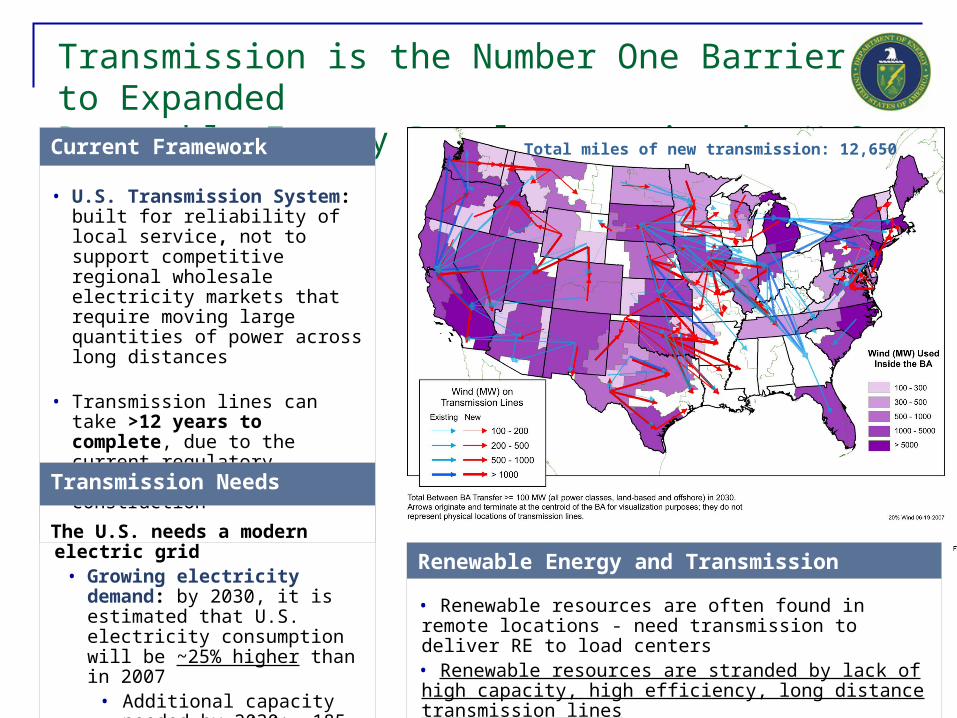

Transmission is the Number One Barrier to Expanded Renewable Energy Development in the U.S.

Current Framework

• U.S. Transmission System: built for reliability of local service, not to support competitive regional wholesale electricity markets that require moving large quantities of power across long distances

• Transmission lines can take >12 years to complete, due to the current regulatory environment, planning and construction

Transmission Needs

The U.S. needs a modern electric grid

• Growing electricity demand: by 2030, it is estimated that U.S. electricity consumption will be ~25% higher than in 2007

• Additional capacity needed by 2030: ~185 GW

Total miles of new transmission: 12,650

Renewable Energy and Transmission

• Renewable resources are often found in remote locations - need transmission to deliver RE to load centers• Renewable resources are stranded by lack of high capacity, high efficiency, long distance transmission lines

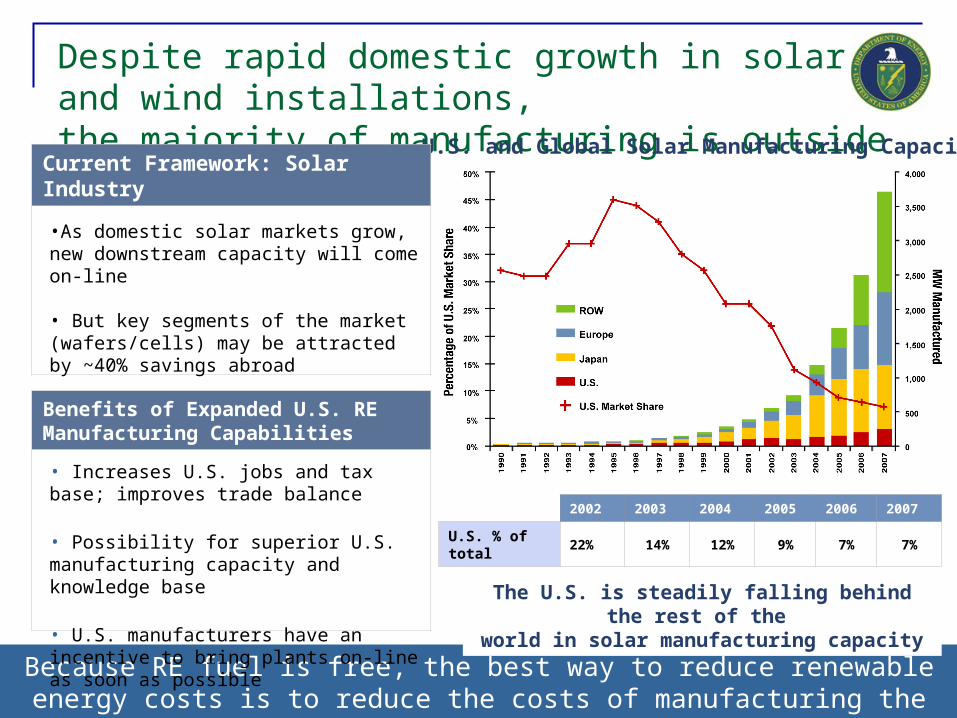

Despite rapid domestic growth in solar and wind installations, the majority of manufacturing is outside the U.S.

Because RE fuel is free, the best way to reduce renewable energy costs is to reduce the costs of manufacturing the ‘widgets;’ manufacturing also creates jobs and RE expertise within the U.S.

The U.S. is steadily falling behind the rest of the world in solar manufacturing capacity

2002 2003 2004 2005 2006 2007

U.S. % of total 22% 14% 12% 9% 7% 7%

U.S. and Global Solar Manufacturing CapacityCurrent Framework: Solar Industry

•As domestic solar markets grow, new downstream capacity will come on-line

• But key segments of the market (wafers/cells) may be attracted by ~40% savings abroad

Benefits of Expanded U.S. RE Manufacturing Capabilities

• Increases U.S. jobs and tax base; improves trade balance

• Possibility for superior U.S. manufacturing capacity and knowledge base

• U.S. manufacturers have an incentive to bring plants on-line as soon as possible

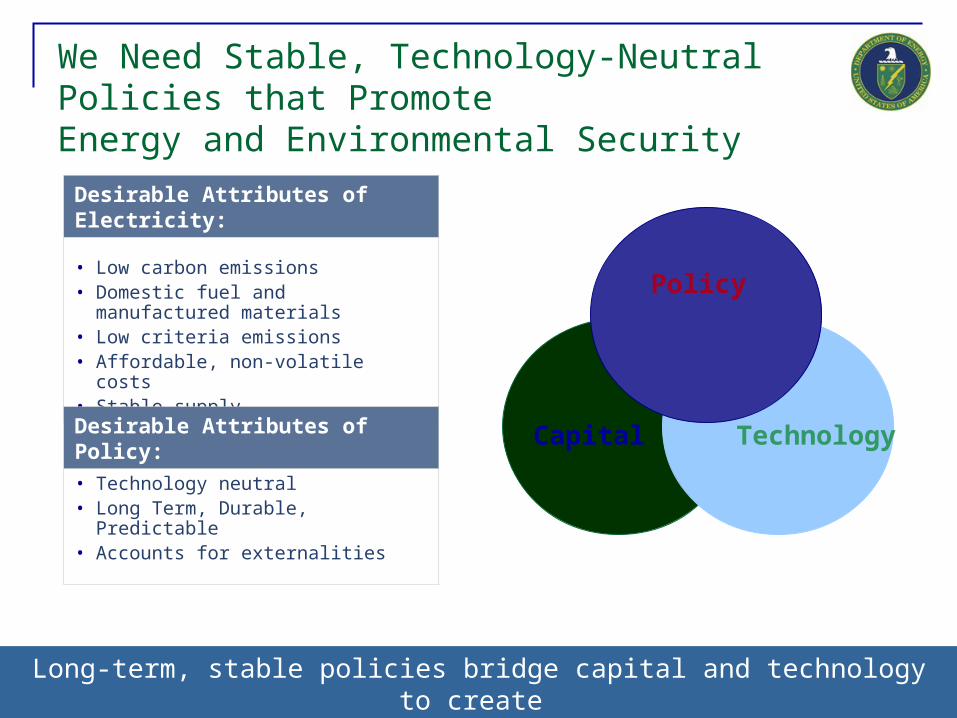

We Need Stable, Technology-Neutral Policies that Promote Energy and Environmental Security

Long-term, stable policies bridge capital and technology to create a robust renewable energy market

Desirable Attributes of Electricity:

• Low carbon emissions• Domestic fuel and manufactured

materials• Low criteria emissions• Affordable, non-volatile costs• Stable supply

Desirable Attributes of Policy:

• Technology neutral• Long Term, Durable, Predictable• Accounts for externalities

Capital Technology

Policy