Embed Size (px)

Citation preview

Remittances: characteristics and development perspective

Judith van DoornSocial Finance Programme, ILO www.ilo.org/[email protected]

What’s next……

• Remittances and the ILO

• ILO field studies - characteristics- development issues

• Suggested future work areas

Remittances and the ILO

ILO Labour Standards migrant workers have the right to transfer

(part of) their earnings and savings through their preferred channel;

Migration – Labour Conference 2004

Access to finance- market-conform, and incentives-based- partnerships

Remittances and the ILO

Activities

• Platforms

• Field studies - B’desh, Nepal, Senegal

• Pilot projects ….. (next step)

Characteristics

Volume of remittances

Bangladesh: $ 1.8 billionNepal: > $ 1 billion Senegal: $ 300 million

Informal transfers are huge…..

Characteristics

Why are informal transfers so popular?Better exchange rate (hundi – Nepal)

Non-financial services

No access to banking services

No experience with banking (Nepal example)

Characteristics

Remittances as % of recipients’ income

Bangladesh: > 50%

Senegal: up to 90%...

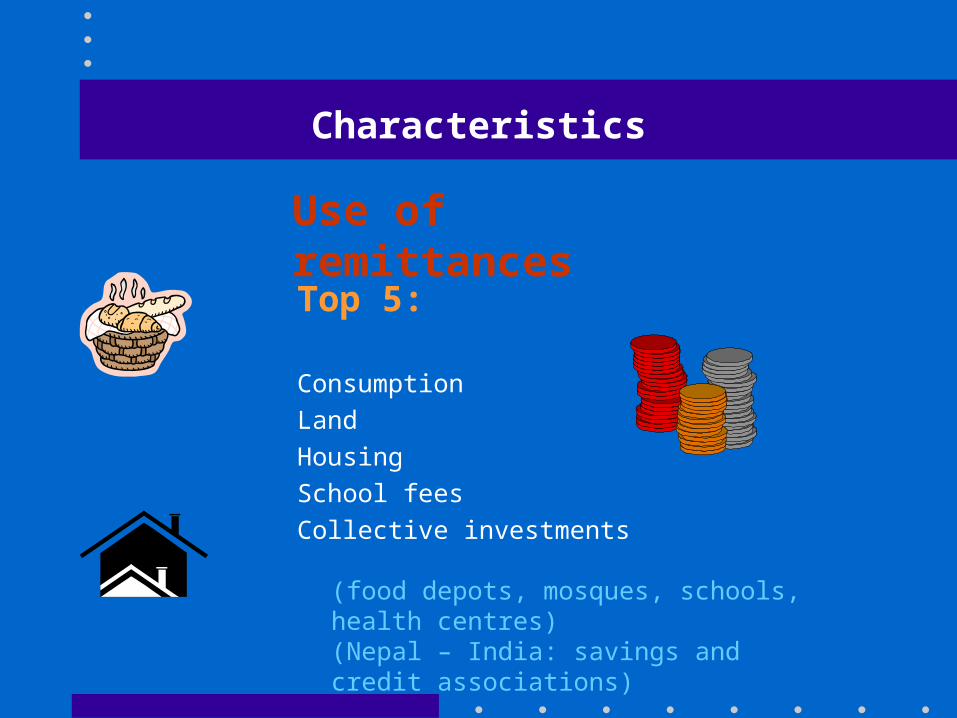

Characteristics

Top 5:

Consumption

Land

Housing

School fees

Collective investments

(food depots, mosques, schools, health centres)(Nepal – India: savings and credit associations)

Use of remittances

Development

Savings

• Availability of suitable savings products?

• Trust in formal savings mechanisms?

• Demands from the (extended) family?

• Some migrants are saving abroad

Access to banking services

Bangladesh- Islami BankPro-active approach to attract remittances.

Staff visited migrants at work place and at home.

Developed fine-tuned products (e.g. accounts for migrants’ associations)

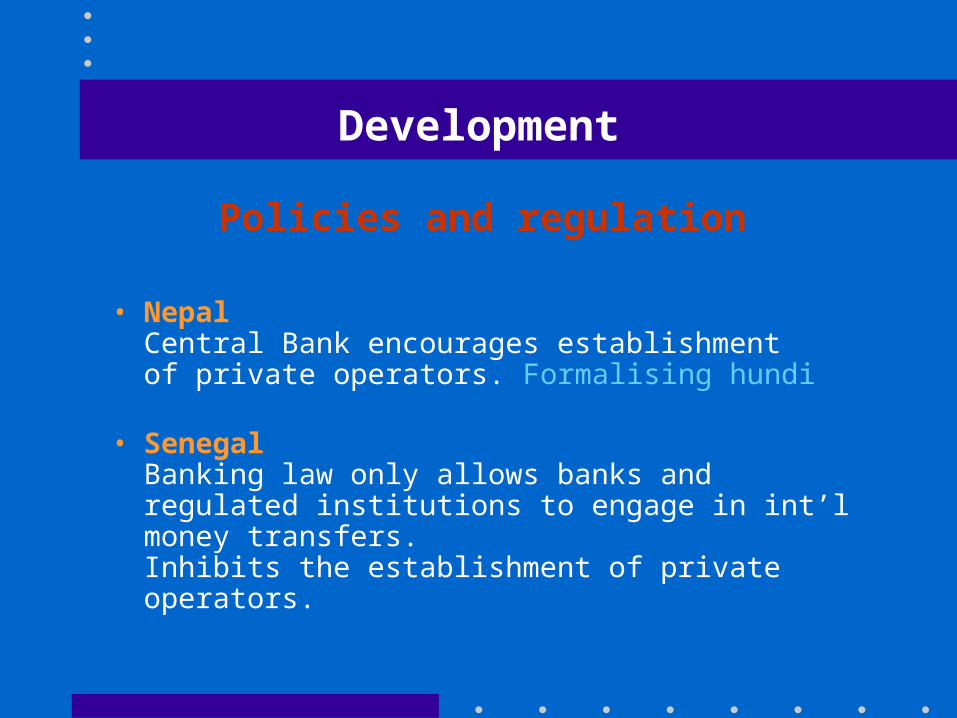

Development

Development

Policies and regulation

• NepalCentral Bank encourages establishment of private operators. Formalising hundi

• SenegalBanking law only allows banks and regulated institutions to engage in int’l money transfers. Inhibits the establishment of private operators.

Development

Policies and regulation

Bangladesh

• Government encourages B’deshi banks to open correspondent relationships with financial institutions abroad.

• Remittances are tax free

Development

Remittances are mainly used for consumption.What is their development impact?

• Study, Bangladesh: multiplier effect: 3.3 on GNP 2.8 on consumption0.4 on investment

• Remittances often larger than ODA

Remittances to Senegal increased over the last 5 years7% -> 82% of ODA. ODA decreased during that same period.

Development

• Do remittances create inequalities in the community?

No clear answer. Example Nepal

Suggested work areas

• Development actorsLink financial institutions (e.g. banks – MFIs)Assist financial insitutions to develop follow-up products

• EmployersTransfer remittances

• Trade unions / civil societyInform migrants of remittance issues

• GovernmentsFacilitate / stimulate

Remittances: characteristics and development perspective

Judith van DoornSocial Finance Programme, ILO www.ilo.org/[email protected]