Embed Size (px)

Citation preview

Journal of International Accounting, Auditing and Taxation 18 (2009) 73–84

Contents lists available at ScienceDirect

Journal of International Accounting,Auditing and Taxation

Relationships among budgetary leadership behavior, managerialbudgeting games, and budgetary attitudes: Evidence fromTaiwanese corporations

Cheng-Li Huanga, Mien-Ling Chenb,∗

a Department of Accounting, Tamkang University, 151 Ying-Chuan Road, Tamsui, Taipei, Taiwan, ROCb Graduate Institute of Management Sciences Accounting Section, Tamkang University, 151 Ying-Chuan Road, Tamsui, Taipei, Taiwan, ROC

a r t i c l e i n f o

Keywords:Attitudes towards the budgetary processBudgeting gamesContingent punishmentContingent reward

a b s t r a c t

In this paper, we examine the relationship among leadership behavior (contingent rewardvs. contingent punishment), managerial budgeting games (devious games vs. economicgames), and attitudes towards the budgetary process. Relationships were tested using astructural equation model that was estimated on the basis of questionnaire data from216 Taiwanese managers. The majority of respondents were accounting/finance managersemployed by manufacturing firms. Results reveal that contingent-reward leadership behav-ior has a direct and positive effect on attitudes toward the budgetary process, and an indirecteffect through economic games. On the other hand, we find evidence that contingent-punishment leadership behavior has only an indirect and negative effect on attitudes towardthe budgetary process through devious games, especially for non-accounting/finance man-agers. Managers who play economic games tend to have positive attitudes towards thebudgetary process, while those who play devious games do not. The findings should beuseful to management in understanding what effective leadership behavior is in the budget-preparation process in Taiwan, and assessing how budgeting games are likely to be adoptedby Taiwanese managers.

© 2008 Elsevier Inc. All rights reserved.

1. Introduction

The business world has become more competitive and global. To maintain competitive advantage, many organizationsare striving constantly to increase their effectiveness and efficiency. Budgeting is a management tool that can be used to helpfirms operate more efficiently and effectively. Organizations use budgets as a critical tool for coordinating the allocation ofresources, managing and controlling their operations, and evaluating performance (Fisher, Frederickson, & Peffer, 2002; Vander Stede, 2000).

In the budget-preparation process, managers propose their budgets and superiors, based on the objectives of the projects,allocate resources to the managers. Effective budget preparation helps to plan the operations of the firm, and the resultingbudget serves as a mutually agreed upon control device for monitoring the activities of the various sub-units. Therefore,budget preparation should be done carefully and accurately. However, due to limited resources, managers may play budgetinggames to obtain their desired budget requests. It is therefore important for the superior in charge of resource allocation tobe able to identify the games that managers play, to be aware of the impact of such games on the budgeting process, and

∗ Corresponding author. Tel.: +886 2 2601 5310x3116.E-mail addresses: [email protected] (C.-L. Huang), [email protected] (M.-L. Chen).

1061-9518/$ – see front matter © 2008 Elsevier Inc. All rights reserved.doi:10.1016/j.intaccaudtax.2008.12.007

74 C.-L. Huang, M.-L. Chen / Journal of International Accounting, Auditing and Taxation 18 (2009) 73–84

to determine which budgetary leadership behavior is appropriate for guiding managers towards positive budgetary processattitudes.

Much of the research in behavioral accounting has explored the relationship among superior leadership behavior, man-agerial budgeting games, and budgetary attitudes in Western countries (Collins, Munter, & Finn, 1987; Collins, Seiler, & Clancy,1984). Little research in this area has focused on Eastern countries. Taiwan is an important player in the global economy(Bruce et al., 2005). Taiwanese companies have earned universal praise and an important place in the global supply chain fortheir innovative ability and efficiency in the information technology (IT) industry. Many multinational corporations value theadvantages of the IT industry in Taiwan and have established subsidiaries there. In 2007, there was approximately $153.40(US$ 100 million) of foreign investment in Taiwan, and the annual rate of increase was approximately 10.17%1. The purposeof this study is to examine whether superior leadership behaviors in the preparation of the budget affect budgeting gamesand budgetary attitudes in Taiwan.

The remainder of this paper is organized as follows. The literature review is in Section 2. Section 3 describes the conceptualmodel and develops a set of research hypotheses. Section 4 describes the data and sampling frame from Taiwanese managersand the measures used in the study. Results are presented in Section 5. Section 6 discusses the results. Conclusions, limitations,and recommendations for future research are set forth in Section 7.

2. Prior literature

2.1. Budgetary leadership behavior: contingent reward and contingent punishment

It is well known that leadership behavior plays a critical role in the effective management of subordinates because suchbehavior is an important determinant of employee attitudes, perceptions, and behaviors (Podsakoff, Bommer, Podsakoff,& Mackenzie, 2006). In the budget-preparation process, some superiors exhibit what is referred to as contingent-rewardbehavior while others adopt contingent-punishment behavior. Contingent reward is positive feedback from the superior. Forexample, the superior pays a compliment if the manager does outstanding work in preparing his or her budget, gives specialrecognition if the manager’s work performance in preparing his or her budget is exemplary, or shows a great deal of interestif the manager suggests a new and better way of preparing the budget.

On the other hand, contingent punishment is negative feedback from the superior. For example, the superior reprimandsthe manager if the work in preparing a budget is consistently less than acceptable, criticizes the manager if the work isnot as good as the work of others, or even recommends against a pay increase if the work is substandard. Contingent-reward leadership behavior is thought to make managers feel good and lead to positive motivation, while contingent-punishment leadership behavior is thought to make managers feel bad and lead to negative motivation (Hofstede, 1968).Several leadership studies conclude that for improving various work-related attitudes, contingent-reward behavior is moreeffective than contingent-punishment behavior (Cherrington & Cherrington, 1976; Podsakoff, Todor, & Skov, 1982). Most ofthe time, feelings of success or failure determine an employee’s attitude towards the budget and the level of performance towhich the employee will aspire in the future.

However, the precise effects of contingent punishment on attitudes are not clear. Some studies (e.g. Podsakoff et al., 1982)found that contingent punishment had no effect on the behavior or attitude of subordinates, while others (Collins et al., 1987;Mackenzie, Podsakoff, & Rich, 2001) found that contingent punishment had positive effects on behavior or attitude. Collinset al. (1987) found that contingent punishment was correlated positively with managers’ budgetary attitudes. Mackenzie etal. (2001) pointed out that contingent punishment has beneficial effects when it is meted out in response to inappropriate ordysfunctional behavior. Dorfman et al. (1997) examined leadership in Western and Asian countries and found that contingentpunishment had a desirable effect only in the United States, but in other countries had an equivocal or undesirable effect.They also found that the different effects of leadership behaviors are usually viewed as culturally specific.

2.2. Budgeting games and attitudes toward the budget

In business, games exist ubiquitously in the budgeting process (Hansen, Otley, & Van der Stede, 2003; Jensen, 2003; Richard& Craig, 2004). In this study, we define budgeting games as managerial behavior designed to achieve budgetary requests. Weconsider two types of budgeting games: devious games and economic games. Devious games are non-straightforward tacticsto obtain extra budget requests, while economic games are straightforward tactics to obtain reasonable budget requests(Collins, Almer, & Mendoza, 1999).

Devious (non-straightforward) games include the following:

• Horatio at the bridge: A manager tries hard to keep what was in last year’s (period’s) budget.• Piggyback: A manager attaches items that are likely to be cut from the budget, if separately submitted, to other projects

that are certain to be approved.

1 Department of statistics, Ministry of Economic Affairs, R.O.C. Website: http://2k3dmz.moea.gov.tw/GNWEB/Indicator/Indicator01.aspx?rptcod=E09.

C.-L. Huang, M.-L. Chen / Journal of International Accounting, Auditing and Taxation 18 (2009) 73–84 75

• Relying on friendship: A manager relies on friendship with superiors to get what is wanted in the budget.• Incremental: A manager seeks an additional amount over last period’s budgetary amounts.• Camel’s nose: A manager asks for a small item knowing that he/she can ask for more once this item is in the budget since

large programs start from seemingly small beginnings.• Sacrificial lamb: A manager adds an unwanted and likely-to-be-cut item to the budget so the superior will not cut a wanted

item.• Crisis: A manager gets what he/she wants in the budget by letting superiors think the operation has a crisis and must have

the budgetary request.

Economic (straightforward) games include the following:

• All or nothing: A manager threatens the superior with shutting the operation down if the desired budget is withheld.• It’ll pay for itself: A manager tells the superior that the request will pay for itself.• Present facts: A manager presents the superior with the facts to get what he/she wants in the budget.• On-site visit: A manager invites the superior for visits to justify the request.

An important consequence of playing budgeting games is the impact on subsequent managerial attitudes towards thebudgetary process (Collins et al., 1999). From an agency theory perspective, if managers are motivated to misrepresenttheir private information (e.g. by engaging in devious games) to obtain their budget requests, these managers will exert lesseffort, which leads to inefficient use of the firm resources (Dunk & Nouri, 1998; Webb, 2002) and which may serve theirself-interests at the expense of the firm (Baiman, 1990). Such opportunistic behavior by managers greatly reduces the valueof the budgeting process (Baiman & Evans, 1983; Melumad & Reichelstein, 1987) because managers lie about their privateinformation that is required to coordinate the activities of disparate parts of an organization, and in turn destroy value fortheir organizations. In contrast to devious games, managers who adopt economic games are viewed as honestly revealingtheir private information in the budget.

Collins et al. (1987) found that managers who play devious games are less likely to meet their budgets than those whoplay economic games. Collins et al. (1999) indicate that devious games focus more on achievement of personal goals than thefirm’s overall goals. Personal goals are directly related to income (salary plus bonuses), the size of the staff, and discretionarycontrol over the allocation of resources (Schiff & Lewin, 1970). Conversely, economic games generally focus on rational andeconomic grounds for obtaining budget requests. Managers who play economic games are more willing to work toward thegoals of the company (Collins et al., 1999).

3. Conceptual model and hypotheses

3.1. The conceptual model

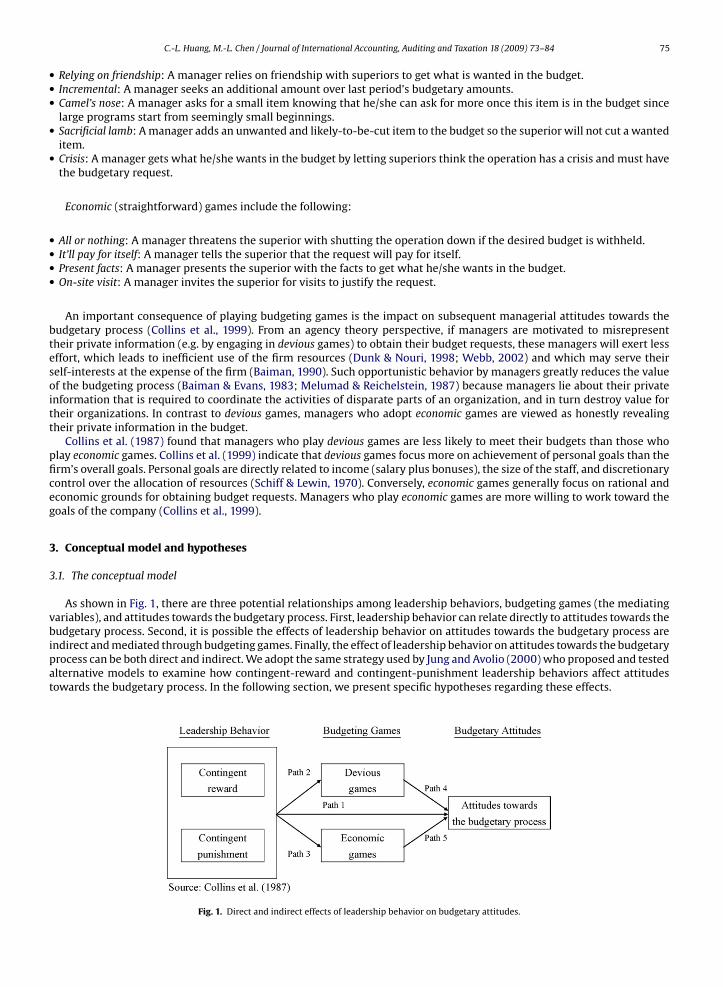

As shown in Fig. 1, there are three potential relationships among leadership behaviors, budgeting games (the mediatingvariables), and attitudes towards the budgetary process. First, leadership behavior can relate directly to attitudes towards thebudgetary process. Second, it is possible the effects of leadership behavior on attitudes towards the budgetary process areindirect and mediated through budgeting games. Finally, the effect of leadership behavior on attitudes towards the budgetaryprocess can be both direct and indirect. We adopt the same strategy used by Jung and Avolio (2000) who proposed and testedalternative models to examine how contingent-reward and contingent-punishment leadership behaviors affect attitudestowards the budgetary process. In the following section, we present specific hypotheses regarding these effects.

Fig. 1. Direct and indirect effects of leadership behavior on budgetary attitudes.

76 C.-L. Huang, M.-L. Chen / Journal of International Accounting, Auditing and Taxation 18 (2009) 73–84

3.2. Direct relationships with attitudes toward the budgetary process

Hofstede (1980) reported the Chinese are very high on “collectivism.” In such societies, “people from birth onwards areintegrated into strong, cohesive in-groups, which throughout people’s lifetime continue to protect them in exchange forunquestioning loyalty” (Hofstede, 1991, p. 260). In this context, Chinese people feel a deep need to save face. If a superiorrewards them in front of others, they will gain face, and in turn, work hard to support or achieve their budgets. However,if a superior punishes them in front of others, they will lose face, and in turn, withhold their support of the budget. Fahr,Podsakoff, and Cheng (1987) found that punishment behavior of any kind has significant dysfunctional effects on subordinateperformance in Taiwan. In contrast to punishment behaviors, previous studies of overseas Chinese (Dorfman et al., 1997;Fahr et al., 1987) indicate that contingent rewards may play a positive role in Chinese organizations. We, therefore, expectcontingent-reward leadership behavior in the budget-preparation process will have a positive effect on managerial attitudestowards the budgetary process, while contingent-punishment leadership behavior will have a negative effect as follows:

Hypothesis 1a. Contingent-reward leadership behavior will have a direct positive effect on managerial attitudes towardsthe budgetary process.

Hypothesis 1b. Contingent-punishment leadership behavior will have a direct negative effect on managerial attitudestowards the budgetary process.

Based on agency theory (regarding the problem of misrepresenting private information to get extra budget requests)and on the works of Collins et al. (1987, 1999), the following seem likely: (i) the more a manager plays devious (non-straightforward) games to obtain a desired budget, the lower the likelihood that the manager will have a positive attitudetowards the budgetary process, and (ii) the more a manager plays economic (straightforward) games to obtain a desiredbudget, the higher the likelihood that the manager will have a positive attitude towards the budgetary process. Thus, wehypothesize the following:

Hypothesis 2a. Devious games will have a negative effect on attitudes towards the budgetary process.

Hypothesis 2b. Economic games will have a positive effect on attitudes towards the budgetary process.

3.3. Indirect relationships: mediating effect of budgeting games

Under contingent-reward leadership behavior, managers are motivated to work hard to achieve their budgets; hence,managers would be more likely to play reasonable games (i.e. economic games) to obtain their desired budgets, and in turnhave positive attitudes towards the budgetary process. Under contingent-punishment leadership behavior, managers aremotivated to lie in the budgetary process because if they tell the truth they often get punished and if they lie they getrewarded. To cope with budget-related pressure, managers are more likely to play devious games to obtain their desiredbudget, and in turn have negative attitudes towards the budgetary process.

The relationship between contingent-reward and contingent-punishment leadership behavior and budgeting games hasreceived empirical support from Collins et al. (1987). Budgeting games are important in their own right as criterion variables.However, they are of special interest in this study because of their potential to facilitate a better understanding of themechanisms through which contingent reward and contingent punishment influence the attitudes of the managers towardsthe budgetary process. Thus, we hypothesize the following:

Hypothesis 3a. Contingent-reward leadership behavior will have an indirect positive effect, mediated through economicgames, on attitudes towards the budgetary process.

Hypothesis 3b. Contingent-punishment leadership behavior will have an indirect negative effect, mediated through deviousgames, on attitudes towards the budgetary process.

4. Methods

4.1. Sample and data collection

Data used to test the hypothesized relationships were obtained by asking managers in listed Taiwanese companies (bothstock exchange market and over-the-counter market) to complete questionnaires. Because the questionnaire was translatedinto Chinese, we paid significant attention to the pre-testing of the questionnaire. The aim of the pre-testing was to ensurethat the items used to measure each variable were unambiguous and that they captured the phenomena that we wereinterested in studying. The pre-testing included feedback from 15 managers regarding the clarity of the questionnaire.

After revising the questionnaire on the basis of comments received, a copy of the instrument was mailed to a randomsample of 1250 Taiwanese managers2. Data were collected between August and October 2005. A total of 228 questionnaires

2 There were 691 firms listed at stock exchange market and 287 firms listed at over-the-counter market during our survey period (2005). Initially, wechose 800 budget managers by functional area randomly from 800 listed companies and sent the questionnaire to each of these managers by post. Six weeks

C.-L. Huang, M.-L. Chen / Journal of International Accounting, Auditing and Taxation 18 (2009) 73–84 77

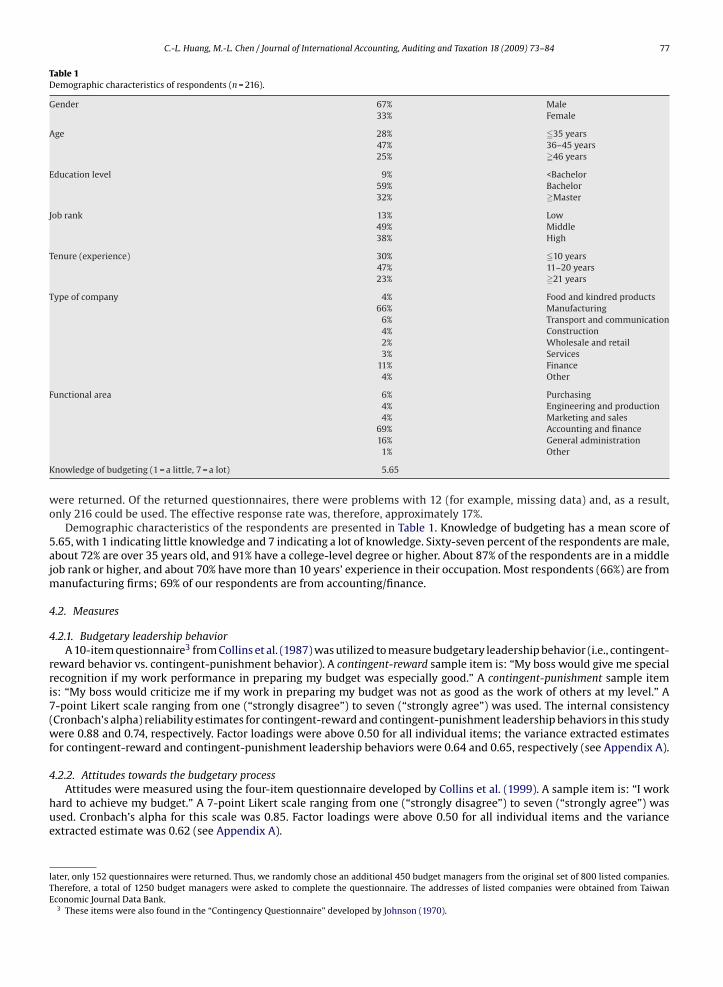

Table 1Demographic characteristics of respondents (n = 216).

Gender 67% Male33% Female

Age 28% �35 years47% 36–45 years25% �46 years

Education level 9% <Bachelor59% Bachelor32% �Master

Job rank 13% Low49% Middle38% High

Tenure (experience) 30% �10 years47% 11–20 years23% �21 years

Type of company 4% Food and kindred products66% Manufacturing

6% Transport and communication4% Construction2% Wholesale and retail3% Services

11% Finance4% Other

Functional area 6% Purchasing4% Engineering and production4% Marketing and sales

69% Accounting and finance16% General administration1% Other

Knowledge of budgeting (1 = a little, 7 = a lot) 5.65

were returned. Of the returned questionnaires, there were problems with 12 (for example, missing data) and, as a result,only 216 could be used. The effective response rate was, therefore, approximately 17%.

Demographic characteristics of the respondents are presented in Table 1. Knowledge of budgeting has a mean score of5.65, with 1 indicating little knowledge and 7 indicating a lot of knowledge. Sixty-seven percent of the respondents are male,about 72% are over 35 years old, and 91% have a college-level degree or higher. About 87% of the respondents are in a middlejob rank or higher, and about 70% have more than 10 years’ experience in their occupation. Most respondents (66%) are frommanufacturing firms; 69% of our respondents are from accounting/finance.

4.2. Measures

4.2.1. Budgetary leadership behaviorA 10-item questionnaire3 from Collins et al. (1987) was utilized to measure budgetary leadership behavior (i.e., contingent-

reward behavior vs. contingent-punishment behavior). A contingent-reward sample item is: “My boss would give me specialrecognition if my work performance in preparing my budget was especially good.” A contingent-punishment sample itemis: “My boss would criticize me if my work in preparing my budget was not as good as the work of others at my level.” A7-point Likert scale ranging from one (“strongly disagree”) to seven (“strongly agree”) was used. The internal consistency(Cronbach’s alpha) reliability estimates for contingent-reward and contingent-punishment leadership behaviors in this studywere 0.88 and 0.74, respectively. Factor loadings were above 0.50 for all individual items; the variance extracted estimatesfor contingent-reward and contingent-punishment leadership behaviors were 0.64 and 0.65, respectively (see Appendix A).

4.2.2. Attitudes towards the budgetary processAttitudes were measured using the four-item questionnaire developed by Collins et al. (1999). A sample item is: “I work

hard to achieve my budget.” A 7-point Likert scale ranging from one (“strongly disagree”) to seven (“strongly agree”) wasused. Cronbach’s alpha for this scale was 0.85. Factor loadings were above 0.50 for all individual items and the varianceextracted estimate was 0.62 (see Appendix A).

later, only 152 questionnaires were returned. Thus, we randomly chose an additional 450 budget managers from the original set of 800 listed companies.Therefore, a total of 1250 budget managers were asked to complete the questionnaire. The addresses of listed companies were obtained from TaiwanEconomic Journal Data Bank.

3 These items were also found in the “Contingency Questionnaire” developed by Johnson (1970).

78 C.-L. Huang, M.-L. Chen / Journal of International Accounting, Auditing and Taxation 18 (2009) 73–84

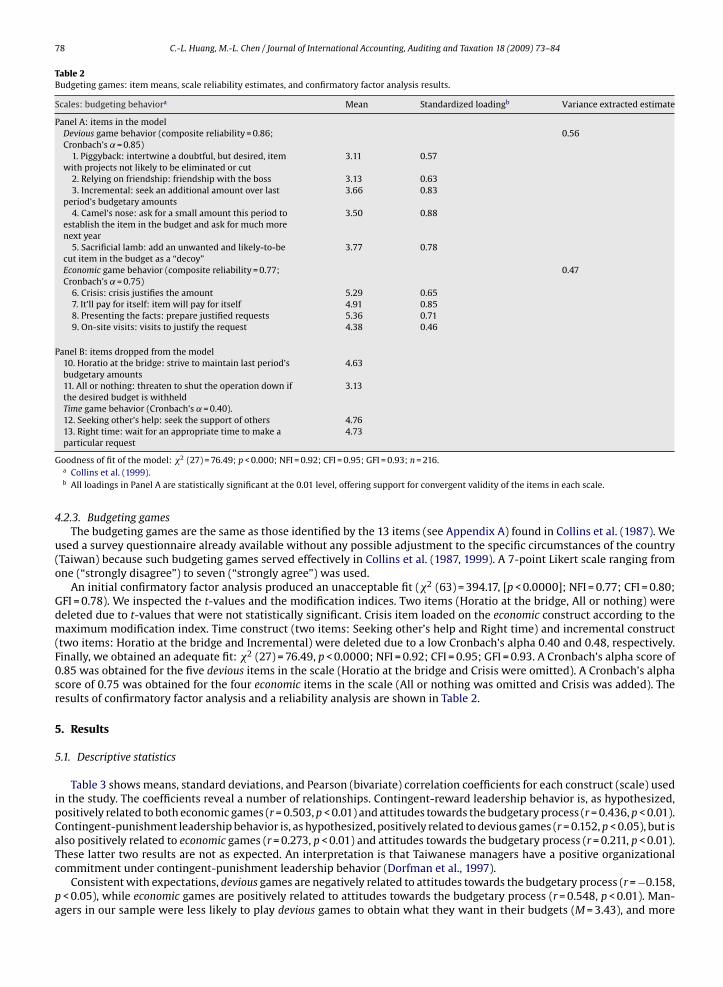

Table 2Budgeting games: item means, scale reliability estimates, and confirmatory factor analysis results.

Scales: budgeting behaviora Mean Standardized loadingb Variance extracted estimate

Panel A: items in the modelDevious game behavior (composite reliability = 0.86;Cronbach’s ˛ = 0.85)

0.56

1. Piggyback: intertwine a doubtful, but desired, itemwith projects not likely to be eliminated or cut

3.11 0.57

2. Relying on friendship: friendship with the boss 3.13 0.633. Incremental: seek an additional amount over last

period’s budgetary amounts3.66 0.83

4. Camel’s nose: ask for a small amount this period toestablish the item in the budget and ask for much morenext year

3.50 0.88

5. Sacrificial lamb: add an unwanted and likely-to-becut item in the budget as a “decoy”

3.77 0.78

Economic game behavior (composite reliability = 0.77;Cronbach’s ˛ = 0.75)

0.47

6. Crisis: crisis justifies the amount 5.29 0.657. It’ll pay for itself: item will pay for itself 4.91 0.858. Presenting the facts: prepare justified requests 5.36 0.719. On-site visits: visits to justify the request 4.38 0.46

Panel B: items dropped from the model10. Horatio at the bridge: strive to maintain last period’sbudgetary amounts

4.63

11. All or nothing: threaten to shut the operation down ifthe desired budget is withheld

3.13

Time game behavior (Cronbach’s ˛ = 0.40).12. Seeking other’s help: seek the support of others 4.7613. Right time: wait for an appropriate time to make aparticular request

4.73

Goodness of fit of the model: �2 (27) = 76.49; p < 0.000; NFI = 0.92; CFI = 0.95; GFI = 0.93; n = 216.a Collins et al. (1999).b All loadings in Panel A are statistically significant at the 0.01 level, offering support for convergent validity of the items in each scale.

4.2.3. Budgeting gamesThe budgeting games are the same as those identified by the 13 items (see Appendix A) found in Collins et al. (1987). We

used a survey questionnaire already available without any possible adjustment to the specific circumstances of the country(Taiwan) because such budgeting games served effectively in Collins et al. (1987, 1999). A 7-point Likert scale ranging fromone (“strongly disagree”) to seven (“strongly agree”) was used.

An initial confirmatory factor analysis produced an unacceptable fit (�2 (63) = 394.17, [p < 0.0000]; NFI = 0.77; CFI = 0.80;GFI = 0.78). We inspected the t-values and the modification indices. Two items (Horatio at the bridge, All or nothing) weredeleted due to t-values that were not statistically significant. Crisis item loaded on the economic construct according to themaximum modification index. Time construct (two items: Seeking other’s help and Right time) and incremental construct(two items: Horatio at the bridge and Incremental) were deleted due to a low Cronbach’s alpha 0.40 and 0.48, respectively.Finally, we obtained an adequate fit: �2 (27) = 76.49, p < 0.0000; NFI = 0.92; CFI = 0.95; GFI = 0.93. A Cronbach’s alpha score of0.85 was obtained for the five devious items in the scale (Horatio at the bridge and Crisis were omitted). A Cronbach’s alphascore of 0.75 was obtained for the four economic items in the scale (All or nothing was omitted and Crisis was added). Theresults of confirmatory factor analysis and a reliability analysis are shown in Table 2.

5. Results

5.1. Descriptive statistics

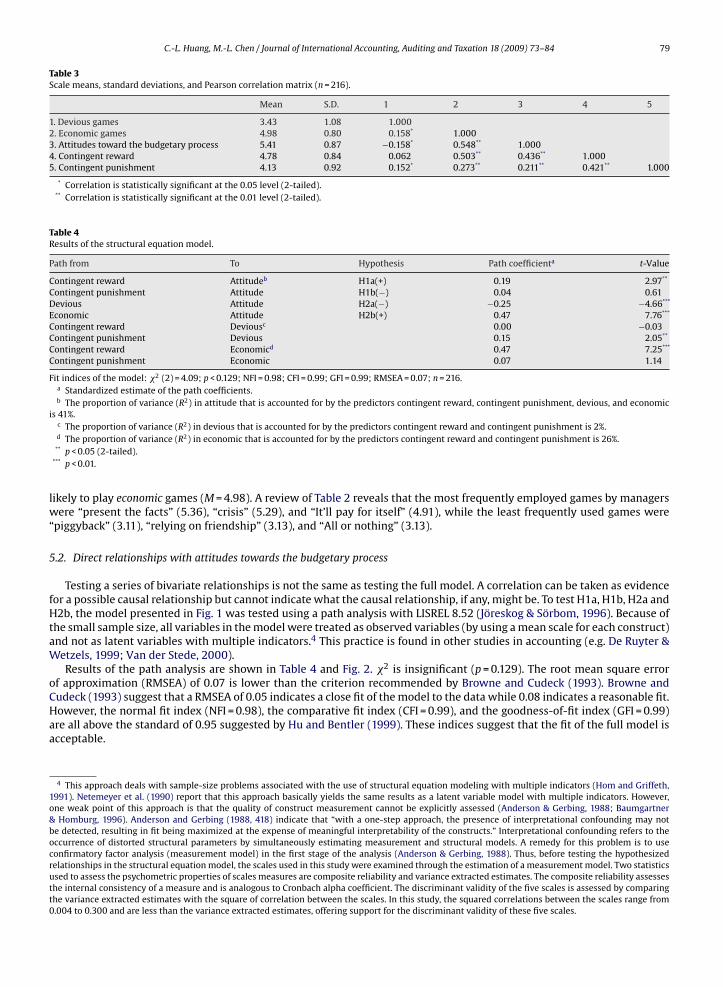

Table 3 shows means, standard deviations, and Pearson (bivariate) correlation coefficients for each construct (scale) usedin the study. The coefficients reveal a number of relationships. Contingent-reward leadership behavior is, as hypothesized,positively related to both economic games (r = 0.503, p < 0.01) and attitudes towards the budgetary process (r = 0.436, p < 0.01).Contingent-punishment leadership behavior is, as hypothesized, positively related to devious games (r = 0.152, p < 0.05), but isalso positively related to economic games (r = 0.273, p < 0.01) and attitudes towards the budgetary process (r = 0.211, p < 0.01).These latter two results are not as expected. An interpretation is that Taiwanese managers have a positive organizationalcommitment under contingent-punishment leadership behavior (Dorfman et al., 1997).

Consistent with expectations, devious games are negatively related to attitudes towards the budgetary process (r = −0.158,p < 0.05), while economic games are positively related to attitudes towards the budgetary process (r = 0.548, p < 0.01). Man-agers in our sample were less likely to play devious games to obtain what they want in their budgets (M = 3.43), and more

C.-L. Huang, M.-L. Chen / Journal of International Accounting, Auditing and Taxation 18 (2009) 73–84 79

Table 3Scale means, standard deviations, and Pearson correlation matrix (n = 216).

Mean S.D. 1 2 3 4 5

1. Devious games 3.43 1.08 1.0002. Economic games 4.98 0.80 0.158* 1.0003. Attitudes toward the budgetary process 5.41 0.87 −0.158* 0.548** 1.0004. Contingent reward 4.78 0.84 0.062 0.503** 0.436** 1.0005. Contingent punishment 4.13 0.92 0.152* 0.273** 0.211** 0.421** 1.000

* Correlation is statistically significant at the 0.05 level (2-tailed).** Correlation is statistically significant at the 0.01 level (2-tailed).

Table 4Results of the structural equation model.

Path from To Hypothesis Path coefficienta t-Value

Contingent reward Attitudeb H1a(+) 0.19 2.97**

Contingent punishment Attitude H1b(−) 0.04 0.61Devious Attitude H2a(−) −0.25 −4.66***

Economic Attitude H2b(+) 0.47 7.76***

Contingent reward Deviousc 0.00 −0.03Contingent punishment Devious 0.15 2.05**

Contingent reward Economicd 0.47 7.25***

Contingent punishment Economic 0.07 1.14

Fit indices of the model: �2 (2) = 4.09; p < 0.129; NFI = 0.98; CFI = 0.99; GFI = 0.99; RMSEA = 0.07; n = 216.a Standardized estimate of the path coefficients.b The proportion of variance (R2) in attitude that is accounted for by the predictors contingent reward, contingent punishment, devious, and economic

is 41%.c The proportion of variance (R2) in devious that is accounted for by the predictors contingent reward and contingent punishment is 2%.d The proportion of variance (R2) in economic that is accounted for by the predictors contingent reward and contingent punishment is 26%.** p < 0.05 (2-tailed).

*** p < 0.01.

likely to play economic games (M = 4.98). A review of Table 2 reveals that the most frequently employed games by managerswere “present the facts” (5.36), “crisis” (5.29), and “It’ll pay for itself” (4.91), while the least frequently used games were“piggyback” (3.11), “relying on friendship” (3.13), and “All or nothing” (3.13).

5.2. Direct relationships with attitudes towards the budgetary process

Testing a series of bivariate relationships is not the same as testing the full model. A correlation can be taken as evidencefor a possible causal relationship but cannot indicate what the causal relationship, if any, might be. To test H1a, H1b, H2a andH2b, the model presented in Fig. 1 was tested using a path analysis with LISREL 8.52 (Jöreskog & Sörbom, 1996). Because ofthe small sample size, all variables in the model were treated as observed variables (by using a mean scale for each construct)and not as latent variables with multiple indicators.4 This practice is found in other studies in accounting (e.g. De Ruyter &Wetzels, 1999; Van der Stede, 2000).

Results of the path analysis are shown in Table 4 and Fig. 2. �2 is insignificant (p = 0.129). The root mean square errorof approximation (RMSEA) of 0.07 is lower than the criterion recommended by Browne and Cudeck (1993). Browne andCudeck (1993) suggest that a RMSEA of 0.05 indicates a close fit of the model to the data while 0.08 indicates a reasonable fit.However, the normal fit index (NFI = 0.98), the comparative fit index (CFI = 0.99), and the goodness-of-fit index (GFI = 0.99)are all above the standard of 0.95 suggested by Hu and Bentler (1999). These indices suggest that the fit of the full model isacceptable.

4 This approach deals with sample-size problems associated with the use of structural equation modeling with multiple indicators (Hom and Griffeth,1991). Netemeyer et al. (1990) report that this approach basically yields the same results as a latent variable model with multiple indicators. However,one weak point of this approach is that the quality of construct measurement cannot be explicitly assessed (Anderson & Gerbing, 1988; Baumgartner& Homburg, 1996). Anderson and Gerbing (1988, 418) indicate that “with a one-step approach, the presence of interpretational confounding may notbe detected, resulting in fit being maximized at the expense of meaningful interpretability of the constructs.” Interpretational confounding refers to theoccurrence of distorted structural parameters by simultaneously estimating measurement and structural models. A remedy for this problem is to useconfirmatory factor analysis (measurement model) in the first stage of the analysis (Anderson & Gerbing, 1988). Thus, before testing the hypothesizedrelationships in the structural equation model, the scales used in this study were examined through the estimation of a measurement model. Two statisticsused to assess the psychometric properties of scales measures are composite reliability and variance extracted estimates. The composite reliability assessesthe internal consistency of a measure and is analogous to Cronbach alpha coefficient. The discriminant validity of the five scales is assessed by comparingthe variance extracted estimates with the square of correlation between the scales. In this study, the squared correlations between the scales range from0.004 to 0.300 and are less than the variance extracted estimates, offering support for the discriminant validity of these five scales.

80 C.-L. Huang, M.-L. Chen / Journal of International Accounting, Auditing and Taxation 18 (2009) 73–84

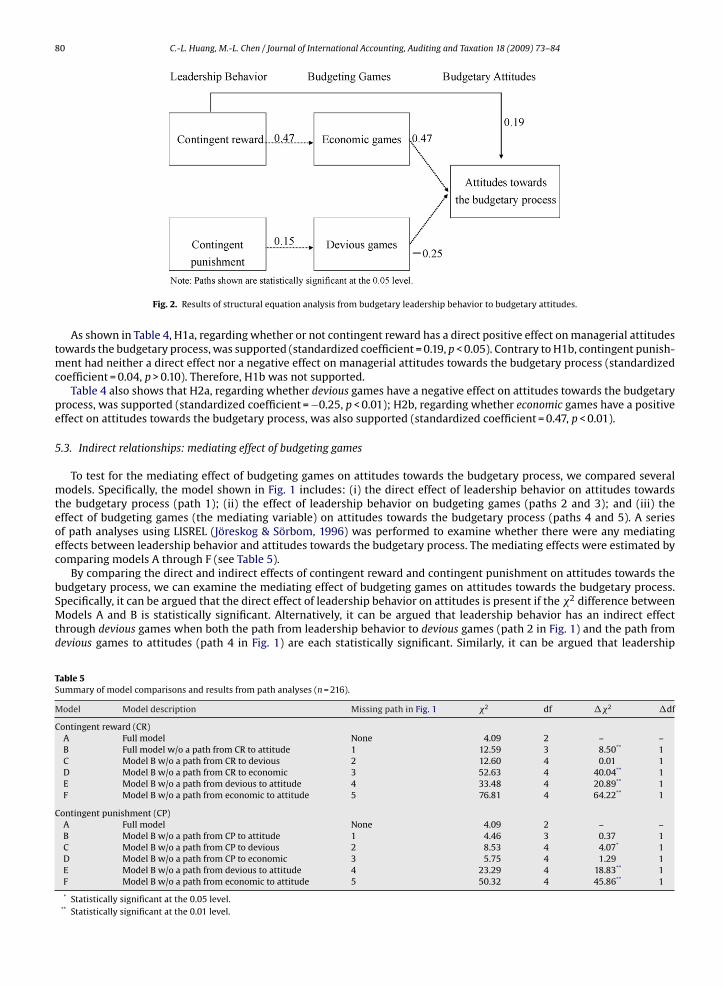

Fig. 2. Results of structural equation analysis from budgetary leadership behavior to budgetary attitudes.

As shown in Table 4, H1a, regarding whether or not contingent reward has a direct positive effect on managerial attitudestowards the budgetary process, was supported (standardized coefficient = 0.19, p < 0.05). Contrary to H1b, contingent punish-ment had neither a direct effect nor a negative effect on managerial attitudes towards the budgetary process (standardizedcoefficient = 0.04, p > 0.10). Therefore, H1b was not supported.

Table 4 also shows that H2a, regarding whether devious games have a negative effect on attitudes towards the budgetaryprocess, was supported (standardized coefficient = −0.25, p < 0.01); H2b, regarding whether economic games have a positiveeffect on attitudes towards the budgetary process, was also supported (standardized coefficient = 0.47, p < 0.01).

5.3. Indirect relationships: mediating effect of budgeting games

To test for the mediating effect of budgeting games on attitudes towards the budgetary process, we compared severalmodels. Specifically, the model shown in Fig. 1 includes: (i) the direct effect of leadership behavior on attitudes towardsthe budgetary process (path 1); (ii) the effect of leadership behavior on budgeting games (paths 2 and 3); and (iii) theeffect of budgeting games (the mediating variable) on attitudes towards the budgetary process (paths 4 and 5). A seriesof path analyses using LISREL (Jöreskog & Sörbom, 1996) was performed to examine whether there were any mediatingeffects between leadership behavior and attitudes towards the budgetary process. The mediating effects were estimated bycomparing models A through F (see Table 5).

By comparing the direct and indirect effects of contingent reward and contingent punishment on attitudes towards thebudgetary process, we can examine the mediating effect of budgeting games on attitudes towards the budgetary process.Specifically, it can be argued that the direct effect of leadership behavior on attitudes is present if the �2 difference betweenModels A and B is statistically significant. Alternatively, it can be argued that leadership behavior has an indirect effectthrough devious games when both the path from leadership behavior to devious games (path 2 in Fig. 1) and the path fromdevious games to attitudes (path 4 in Fig. 1) are each statistically significant. Similarly, it can be argued that leadership

Table 5Summary of model comparisons and results from path analyses (n = 216).

Model Model description Missing path in Fig. 1 �2 df ��2 �df

Contingent reward (CR)A Full model None 4.09 2 – –B Full model w/o a path from CR to attitude 1 12.59 3 8.50** 1C Model B w/o a path from CR to devious 2 12.60 4 0.01 1D Model B w/o a path from CR to economic 3 52.63 4 40.04** 1E Model B w/o a path from devious to attitude 4 33.48 4 20.89** 1F Model B w/o a path from economic to attitude 5 76.81 4 64.22** 1

Contingent punishment (CP)A Full model None 4.09 2 – –B Model B w/o a path from CP to attitude 1 4.46 3 0.37 1C Model B w/o a path from CP to devious 2 8.53 4 4.07* 1D Model B w/o a path from CP to economic 3 5.75 4 1.29 1E Model B w/o a path from devious to attitude 4 23.29 4 18.83** 1F Model B w/o a path from economic to attitude 5 50.32 4 45.86** 1

* Statistically significant at the 0.05 level.** Statistically significant at the 0.01 level.

C.-L. Huang, M.-L. Chen / Journal of International Accounting, Auditing and Taxation 18 (2009) 73–84 81

behavior has an indirect effect through economic games when both the path from leadership behavior to economic games(path 3 in Fig. 1) and the path from economic games to attitudes (path 4 in Fig. 1) are each statistically significant. Results ofthese model comparisons are summarized in Table 5.

As shown in Table 5, under contingent reward, although the �2 difference between Models B and E (��2 = 20.89, �df = 1,p < 0.01) is statistically significant, the difference between Models B and C (��2 = 0.01, �df = 1, p > 0.05) is not statisticallysignificant for devious games. The result indicates the relationship between contingent-reward leadership behavior andattitudes towards the budgetary process is not mediated by the use of devious games. The �2 difference between ModelsB and D (��2 = 40.04, �df = 1, p < 0.01) and between Models B and F (��2 = 64.22, �df = 1, p < 0.01) are both statisticallysignificant for economic games. This result suggests that the relationship between contingent-reward leadership behaviorand attitudes towards the budgetary process is mediated by the use of economic games. Thus, Hypothesis 3a, regardingwhether or not contingent-reward leadership behavior will have an indirect positive effect, mediated through economicgames, on attitudes towards the budgetary process, is supported.

As shown in Table 5, under contingent punishment, the �2 difference between Models B and C (��2 = 4.07, �df = 1,p < 0.05) and between Models B and E (��2 = 18.83, �df = 1, p < 0.01) are both statistically significant for devious games.This result indicates an indirect effect from contingent punishment to attitudes, mediated through devious games. Althoughthe �2 difference between Models B and F (��2 = 45.86, �df = 1, p < 0.01) is statistically significant, the difference betweenModels B and D (��2 = 1.29, �df = 1, p > 0.10) is not statistically significant for economic games. This result indicates thatthe relationship between contingent-punishment leadership behavior and attitudes towards the budgetary process is notconditional on economic games. Thus, Hypothesis 3b, regarding whether or not contingent punishment behavior willhave an indirect negative effect, mediated through devious games, on attitudes towards the budgetary process, is sup-ported.

5.4. Further analysis

Since the majority of respondents were accounting/finance managers employed by manufacturing firms, a further analysiswas done to examine whether the model for accounting/finance managers and other managers is different. The results5

show that under contingent-reward leadership behavior, accounting/finance and non-accounting/finance managers are morelikely to use economic games than devious games. However, there are different effects of contingent-punishment leadershipbehavior on devious and economic games between these two groups. Under contingent-punishment leadership behavior,non-accounting/finance managers are more likely to use devious games than economic games, while accounting/financemanagers are not.

6. Discussion

With respect to Hypothesis 1a, contingent-reward leadership behavior has a direct positive effect on managerial attitudestoward the budgetary process. However, Hypothesis 1b is not supported: contingent-punishment leadership behavior has noeffect on managerial attitudes towards the budgetary process. These findings are not consistent with those reported by Collinset al. (1987), who did not find that contingent reward affects attitudes toward the budgetary process directly, but found thatcontingent punishment affects attitudes toward the budgetary process directly and positively. According to Hofstede (1980),the Chinese are “collectivists” with a deep need to save face (Wong, Tjosvold, & Su, 2007). This finding may explain why,with Taiwanese managers, contingent-reward leadership behavior has a direct positive effect on managerial attitudes towardthe budgetary process. Our findings are supported by previous research, which shows that contingent-reward leadershipbehavior plays a positive role in Chinese organizations (Dorfman et al., 1997; Fahr et al., 1987).

Contingent-punishment leadership behavior is found to have no effect on managerial attitudes towards the budgetaryprocess. This finding may be explained by previous research, which shows that Taiwanese managers have a positive orga-nizational commitment under contingent-punishment leadership behavior (Dorfman et al., 1997). A positive organizationalcommitment may neutralize the direct and negative effect of contingent-punishment leadership behavior on managerialattitudes towards the budgetary process.

With respect to Hypothesis 2a, we find that devious games have a negative effect on attitudes towards the budgetaryprocess. This result is consistent with Collins et al. (1987) and Collins et al. (1999) and supports agency-theory predictions.Baiman (1990) maintains that managers with self-interest will play devious games to get extra budget requests and will makeless effort to protect the accuracy of the budgeting process or achieve the firm’s goals. With respect to Hypothesis 2b, wefind that economic games have a positive effect on attitudes towards the budgetary process, a result consistent with Collinset al. (1987) and Collins et al. (1999). Managers who play economic games to obtain their budget requests tend to work hardto maintain the proper functioning of the budgetary process as well as to achieve their budgetary targets.

With respect to Hypothesis 3a, the results suggest that the relationship between contingent-reward leadership behaviorand attitudes towards the budgetary process is mediated through economic games. Thus, if the superior exhibits contingent-reward behavior in the budget-preparation process, managers are more likely to adopt economic games to obtain what they

5 The tables for this analysis are available from the authors upon request.

82 C.-L. Huang, M.-L. Chen / Journal of International Accounting, Auditing and Taxation 18 (2009) 73–84

really need in their budget requests. In turn, such managers will have better attitudes towards the budgetary process. Withrespect to Hypothesis 3b, the results suggest that the relationship between contingent-punishment leadership behavior andattitudes towards the budgetary process is mediated through the use of devious games. To avoid being punished while stillachieving expectations, managers are likely to play devious games such as “packing” their budget requests with “sacrificiallambs” to divert attention from other projects, “piggybacking” their budget requests on other projects that are certain tobe approved, or routinely “increasing” their budget requests over past budgets. In turn, these managers may not expend asmuch effort towards the budgetary process.

The results of our further analysis found that there are different effects of contingent-punishment leadership behavior ondevious games and economic games between accounting/finance managers and non-accounting/finance managers. Account-ing/finance managers are resources users, but they mostly play the role of resource-allocation checkers. This fact may explainwhy under contingent-punishment leadership behavior, non-accounting/finance managers are more likely to use deviousgames than economic games, while accounting/finance managers are not.

7. Conclusions and limitations

7.1. Conclusions

In the budgeting process, the superior’s budgetary leadership behavior can play an important role in motivating andenabling subordinate managers to contribute toward the effectiveness of the organization. In Taiwan, under contingent-reward leadership behavior in the budget-preparation process, managers will be more likely to play economic games thandevious games to obtain their budget requests. Playing economic games can have a positive effect on managerial attitudestowards the budgetary process. However, to cope with the pressure that they feel when their superior uses contingentpunishment, managers are more likely to play devious games than economic games to obtain their budget requests. Playingdevious games has a negative effect on managerial attitudes towards the budgetary process, and such behavior may bedysfunctional to the firm.

This study suggests that Taiwanese management should adopt contingent-reward leadership behavior in the budget-preparation process to motivate managers to use economic games to obtain their budget requests, and in turn have betterattitudes towards the budgetary process. Under contingent-punishment leadership behavior, non-accounting/finance man-agers are more likely to play devious games than economic games. Superiors should communicate with these managers tobetter understand the purposes of the budget proposals before deciding how to allocate budget resources.

Taiwan is an important player in the global economy. There are many multinational corporations operating in Taiwan.The findings of this study should be useful to management in trying to understand what effective leadership behavior isin the budget-preparation process in Taiwan, and in assessing how budgeting games are likely to be adopted by Taiwanesemanagers.

7.2. Limitations

The results of our study are subject to a number of limitations. First, the data consisted solely of managers’ percep-tions, which is always a concern. Second, it is problematic to question managers about their engagement in dysfunctionalbehavior because they may not wish to disclose information about such behavior (Van der Stede, 2000). Third, thisstudy attempted to isolate one small issue (the effect of budgetary leadership behavior on budgetary attitudes medi-ated by budgeting games) within multiple, complex environments (e.g. team group, division, corporation). Controllingfor one or more of the variables that had to be omitted to limit the scope of the work (e.g. manufacturing firms vs.other firms) could have yielded different results. Fourth, we do not know whether or not managers who play bud-geting games have their budget requests granted. Future research may examine dyad (the immediate superior andsubordinate managers) budgeting games in allocating and obtaining resources. Fifth, because of sample-size problems,all variables in the model were treated as observed variables (by using a mean scale for each construct) and not aslatent variables with multiple indicators. The quality of construct measurement may not be explicitly assessed. Finally,since this study relies on data from only 216 respondents from Taiwan and approximately 2/3 of respondents areaccounting/finance managers employed by manufacturing firms, the results are not generalizable to other Taiwanese con-texts.

Acknowledgements

The authors would like to thank the Editor and two anonymous reviewers for their helpful comments and suggestions.

Appendix A. Appendix A

See Tables A.1–A.3 .

C.-L. Huang, M.-L. Chen / Journal of International Accounting, Auditing and Taxation 18 (2009) 73–84 83

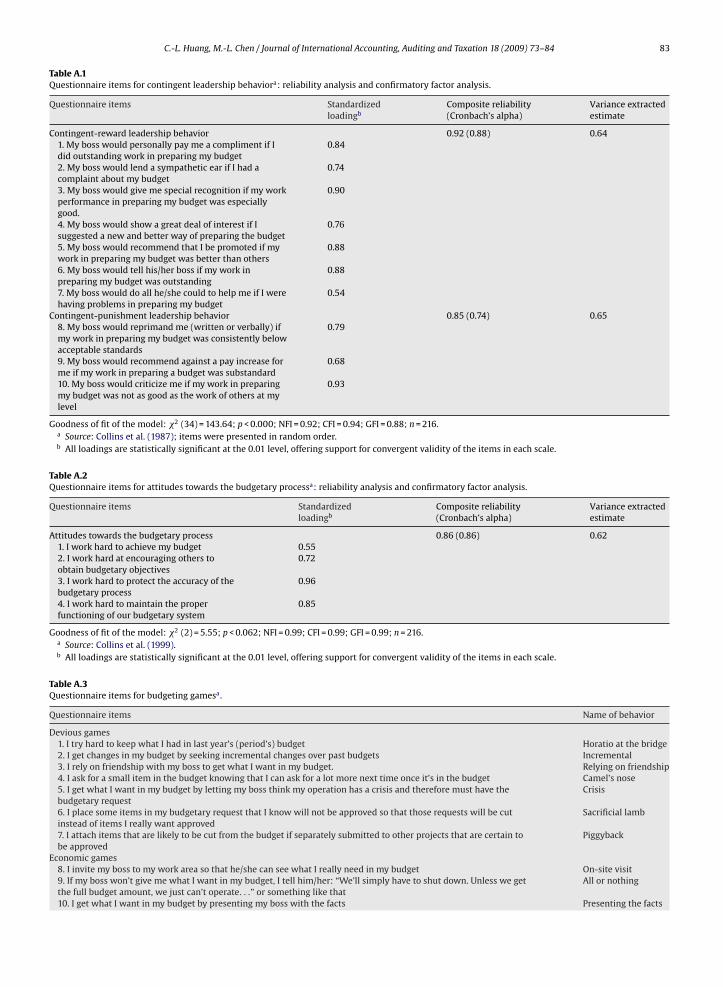

Table A.1Questionnaire items for contingent leadership behaviora: reliability analysis and confirmatory factor analysis.

Questionnaire items Standardizedloadingb

Composite reliability(Cronbach’s alpha)

Variance extractedestimate

Contingent-reward leadership behavior 0.92 (0.88) 0.641. My boss would personally pay me a compliment if Idid outstanding work in preparing my budget

0.84

2. My boss would lend a sympathetic ear if I had acomplaint about my budget

0.74

3. My boss would give me special recognition if my workperformance in preparing my budget was especiallygood.

0.90

4. My boss would show a great deal of interest if Isuggested a new and better way of preparing the budget

0.76

5. My boss would recommend that I be promoted if mywork in preparing my budget was better than others

0.88

6. My boss would tell his/her boss if my work inpreparing my budget was outstanding

0.88

7. My boss would do all he/she could to help me if I werehaving problems in preparing my budget

0.54

Contingent-punishment leadership behavior 0.85 (0.74) 0.658. My boss would reprimand me (written or verbally) ifmy work in preparing my budget was consistently belowacceptable standards

0.79

9. My boss would recommend against a pay increase forme if my work in preparing a budget was substandard

0.68

10. My boss would criticize me if my work in preparingmy budget was not as good as the work of others at mylevel

0.93

Goodness of fit of the model: �2 (34) = 143.64; p < 0.000; NFI = 0.92; CFI = 0.94; GFI = 0.88; n = 216.a Source: Collins et al. (1987); items were presented in random order.b All loadings are statistically significant at the 0.01 level, offering support for convergent validity of the items in each scale.

Table A.2Questionnaire items for attitudes towards the budgetary processa: reliability analysis and confirmatory factor analysis.

Questionnaire items Standardizedloadingb

Composite reliability(Cronbach’s alpha)

Variance extractedestimate

Attitudes towards the budgetary process 0.86 (0.86) 0.621. I work hard to achieve my budget 0.552. I work hard at encouraging others toobtain budgetary objectives

0.72

3. I work hard to protect the accuracy of thebudgetary process

0.96

4. I work hard to maintain the properfunctioning of our budgetary system

0.85

Goodness of fit of the model: �2 (2) = 5.55; p < 0.062; NFI = 0.99; CFI = 0.99; GFI = 0.99; n = 216.a Source: Collins et al. (1999).b All loadings are statistically significant at the 0.01 level, offering support for convergent validity of the items in each scale.

Table A.3Questionnaire items for budgeting gamesa.

Questionnaire items Name of behavior

Devious games1. I try hard to keep what I had in last year’s (period’s) budget Horatio at the bridge2. I get changes in my budget by seeking incremental changes over past budgets Incremental3. I rely on friendship with my boss to get what I want in my budget. Relying on friendship4. I ask for a small item in the budget knowing that I can ask for a lot more next time once it’s in the budget Camel’s nose5. I get what I want in my budget by letting my boss think my operation has a crisis and therefore must have thebudgetary request

Crisis

6. I place some items in my budgetary request that I know will not be approved so that those requests will be cutinstead of items I really want approved

Sacrificial lamb

7. I attach items that are likely to be cut from the budget if separately submitted to other projects that are certain tobe approved

Piggyback

Economic games8. I invite my boss to my work area so that he/she can see what I really need in my budget On-site visit9. If my boss won’t give me what I want in my budget, I tell him/her: “We’ll simply have to shut down. Unless we getthe full budget amount, we just can’t operate. . .” or something like that

All or nothing

10. I get what I want in my budget by presenting my boss with the facts Presenting the facts

84 C.-L. Huang, M.-L. Chen / Journal of International Accounting, Auditing and Taxation 18 (2009) 73–84

Table A.3 (Continued )

Questionnaire items Name of behavior

11. I get what I want in my budget by telling my boss that my requests will pay for themselves It’ll pay for itself

Time games12. I seek the help of others (other than my boss) to get what I what in my budget Seeking other’s help13. If times aren’t “right,” I’ll wait until the next budget period to ask for things in my budget Right time

Incremental games1. I try hard to keep what I had in last year’s (period’s) budget Horatio at the bridge2. I get changes in my budget by seeking incremental changes over past budgets Incremental

a Source: Collins et al. (1987); questionnaire items were presented in random order.

References

Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modeling in practice: A review and recommended two-step approach. Psychological Bulletin,103, 324–411.

Baiman, S. (1990). Agency research in management accounting: A second look. Accounting, Organizations and Society, 15(4), 341–371.Baiman, S., & Evans, J. H., III. (1983). Pre-decision information and participative management control systems. Journal of Accounting Research, 21(2), 371–395.Baumgartner, H., & Homburg, C. (1996). Applications of structural equation modeling in marketing and consumer research: A review. International Journal

of Research in Marketing, 13, 139–161.Browne, M. W., & Cudeck, R. (1993). Alternative ways of assessing model fit. In K. A. Bollen & J. S. Long (Eds.), Testing structural equation models (pp. 132–162).

Newbury Park, California: Sage Publications.Bruce, E., Matt, K., Pete, E., Dexter, R., Frederik, B., & Cliff, E. (2005). Why Taiwan matters. Business Week, 3933, 76–81.Cherrington, J. O., & Cherrington, D. J. (1976). Budget games for fun and frustration. Management Accounting, 57(7), 28–32.Collins, F., Seiler, R. E., & Clancy, D. K. (1984). Budgetary attitudes: The effects of role sender, stress, and performance evaluation. Accounting and Business

Research, 14(Spring), 163–168.Collins, F., Munter, P., & Finn, D. W. (1987). The budgeting games people play. The Accounting Review, 62(January), 29–49.Collins, F., Almer, E. D., & Mendoza, R. I. (1999). Budget games and effort: Difference between the United States and Latin America. Journal of International

Accounting Auditing & Taxation, 8(2), 241–267.De Ruyter, K., & Wetzels, M. (1999). Commitment in auditor–client relationships: Antecedents and consequences. Accounting, Organizations and Society,

24(January), 57–75.Dorfman, P. W., Howell, J. P., Hibino, S., Lee, J. K., Tate, U., & Bautista, A. (1997). Leadership in Western and Asian countries: Commonalities and differences

in effective leadership processes across cultures. Leadership Quarterly, 8(3), 233–274.Dunk, A. S., & Nouri, H. (1998). Antecedents of budgetary slack: A literature review and synthesis. Journal of Accounting Literature, 17, 72–96.Fahr, J. L., Podsakoff, P. M., & Cheng, B. S. (1987). Culture-free leadership effectiveness versus moderators of leadership behaviors: An extension and test of

Kerr and Jermier’s “substitutes for leadership” model in Taiwan. Journal of International Business Studies, 18, 43–60.Fisher, J., Frederickson, J. R., & Peffer, S. A. (2002). The effect of information asymmetry of negotiated budgets: An empirical investigation. Accounting,

Organizations and Society, 27(January), 27–43.Hansen, S. C., Otley, D. T., & Van der Stede, W. A. (2003). Practice developments in budgeting: An overview and academic perspective. Journal of Management

Accounting Research, 15, 95–116.Hofstede, G. H. (1968). The game of budget control. London: Tavistock.Hofstede, G. H. (1980). Motivation, leadership, and organization: Do American theories apply abroad? Organizational Dynamics, 9(1), 42–63.Hofstede, G. H. (1991). Cultures and organizations: Software of the mind. London, UK: McGraw-Hill.Hom, P. W., & Griffeth, R. W. (1991). Structural equations modeling test of a turnover theory: Cross-sectional and longitudinal analyses. Journal of Applied

Psychology, 76, 350–366.Hu, L., & Bentler, P. M. (1999). Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation

Modeling, 6(1), 1–55.Jensen, M. C. (2003). Paying people to lie: The truth about the budgeting process. European Financial Management, 9, 379–406.Johnson, R. D. (1970). An investigation of the interaction effects and motivational variables on task performance. Unpublished doctoral dissertation. Indiana

University.Jöreskog, K. G., & Sörbom, D. (1996). LISREL 8: User’s Reference Guide. Chicago, IL: Scientific Software International.Jung, D. I., & Avolio, B. J. (2000). Opening the black box: An experimental investigation of the mediating effects of trust and value congruence on transfor-

mational and transactional leadership. Journal of Organizational Behaviour, 21, 949–964.Mackenzie, S. B., Podsakoff, P. M., & Rich, G. A. (2001). Transformational and transactional leadership and salesperson performance. Journal of the Academy

of Marketing Science, 29(2), 115–134.Melumad, N. D., & Reichelstein, S. (1987). Centralization versus delegation and the value of communication. Journal of Accounting Research, 25(Supplement),

1–18.Netemeyer, R. G., Johnston, M. W., & Burton, S. (1990). Analysis of role conflict and role ambiguity in a structural equations framework. Journal of Applied

Psychology, 75, 148–157.Podsakoff, P. M., Todor, W. D., & Skov, R. B. (1982). Effects of leader contingent and noncontingent reward and punishment behaviors on subordinate

performance and satisfaction. Academy of Management Journal, 25, 810–821.Podsakoff, P. M., Bommer, W. H., Podsakoff, N. P., & Mackenzie, S. B. (2006). Relationships between leader reward and punishment behavior and subordinate

attitudes, perceptions, and behaviors: A meta-analytic review of existing and new research. Organizational Behavior and Human Decision Processes, 99,113–142.

Richard, S., & Craig, A. (2004). Games managers play at budget time. MIT Sloan Management Review, 45(3), 81–84.Schiff, M., & Lewin, A. (1970). The impact of budgets on people. The Accounting Review, 45(April), 259–268.Van der Stede, W. A. (2000). The relationship between the consequences of budgetary controls: Slack creation and managerial short-term orientation.

Accounting, Organizations and Society, 25(August), 609–622.Webb, R. A. (2002). The impact of reputation and variance investigations on the creation of budget slack. Accounting, Organizations and Society, 27(4/5),

361–378.Wong, A., Tjosvold, D., & Su, F. (2007). Social face for innovation in strategic alliances in China: The mediating roles of resource exchange and reflexivity.

Journal of Organizational Behavior, 28, 961–978.