Embed Size (px)

Citation preview

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

114

After analyzing the secondary data, in this chapter the researcher has dealt with

“The relationship between MAS and Employee‟s Productivity” and “The

relationship between MAS and Profitability” in order to have precise comparison

between the banks. Hypotheses have also been tested in this chapter. Some

important statistical tools such as, Karl Pearson‟s coefficient correlation,

Coefficient of Determination and Fisher‟s z- transformation have also been

applied to make this analysis more scientific.

In this chapter has been divided into two parts.

5.1 Relationship between MAS and Employee‟s Productivity.

5.2 Relationship between MAS and Profitability.

In order to have an in-depth study, the researcher has framed the

following hypotheses i.e.

Ho1: The MAS and Employee’s productivity are independent to each other.

Ho2: The MAS and Profitability are independent to each other.

5.1 Relationship between MAS and Employee’s

Productivity

This chapter has also been divided into following sub- parts.

5.1.1 The concept of Employee‟s Productivity.

5.1.2 Employee‟s Productivity in Banks.

5.1.3 Relationship between MAS and Employee‟s Productivity.

5.1.4 Comparison of PNB and HDFC Bank on the basis of Employee‟s

Productivity.

5.1.1 Concept of Employee’s Productivity

Productivity is one of the most common terms under used of people.

Particularly, business community is more concerned about this term.

Historically this term never remained out of the dictionary of the human being.

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

115

There are many definitions of productivity. But widely it is considered as ratio of

output to input. There is a constant change in the generic concept

of productivity. There are many concept related to productivity. In different

periods, people focused on different facets of productivity. Sometime

labor productivity is important and other time resource productivity becomes

significant.

In simple words we can define employee productivity as the output per worker

or output per hour. With the increase in part-time employment and temporary

and contract workers, many businesses use hours worked rather than output per

worker to measure productivity.

Definition

“Economists define employee productivity as the output per worker or output

per hour. With the increase in part-time employment and temporary and

contract workers, many businesses use hours worked rather than output per

worker to measure productivity.”

“The amount of output per unit of input (labor, equipment, and capital). There

are many different ways of measuring productivity. For example, in a factory

productivity might be measured based on the number of hours it takes to

produce a good, while in the servicesector productivity might be measured

based on the revenue generated by an employee divided by his/her salary.”

According to economist Paul Krugman- “Businesses live and die by productivity. A productive company has lower

operating costs and can sell its products or services at lower prices, bringing

increased volume and profits. Employee productivity is key to organizational

success and to a country's economy. Employee productivity must increase if the

overall standard of living is to increase.”

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

116

Why is Employee’s Productivity Calculated?

Any successful business knows much of its success is due to diligent workers

with excellent productivity. Employees who put forth extra effort often make a

big difference in company profits. The employees who do only what the job

duties require, and no more, can stymie the progress of a company. It is

important to motivate all employees to reach their full potential and maximal

level of productivity. Companies that recognize and encourage increased

productivity are likely to be more successful than their counterparts.

Economists define employee productivity as the output per worker or output per

hour. With the increase in part-time employment and temporary and contract

workers, many businesses use hours worked rather than output per worker to

measure productivity.

Factors Affecting Employees’ Productivity

Employees are more or less productive based on a variety of objective and

subjective factors, including the work environment, motivation, workflow

processes and technology. Objective data--such as billable hours, number of

products sold, items assembled or claims processed--measure employee

productivity. Employers also use subjective measures. The important factors are

given below:

1. Work Environment

Telecommuting and collaboration have changed the work

environment.

Telecommuting, flexible scheduling and staffing and collaboration are changing

how, where and when employees work. Regardless of their work environment,

having the necessary materials and tools to do their work is vital to employee

engagement and productivity.2

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

117

2. Employee Motivation

Workers take pride in their contributions to success.

Open and honest communication, positive feedback and shared performance

expectations all affect productivity. Being able to see a project through to its

completion or having a clear understanding of their role in the work motivates

employees better than top-down management approaches.

3. Work Processes

Look for improvement opportunities in work processes.

All work is a process--a series of actions that bring about a result. Frequently,

workers develop processes over time with little or no formal planning. Work-

flow processes affect employee productivity, and managers of productive work

groups understand this and champion process improvement.

Alfred Edward Perlman, president of Penn Central Railroad, once said that if a

process has been used for two years, it should be re-evaluated for improvement

opportunities.

4. Technology

Learning new computer programs affects productivity.

Technology has improved productivity in areas such as supply-chain

management and financial transactions. Technology can also reduce

productivity, at least in the initial phases of implementation. Often, employees

are expected to learn a new technology while doing their daily work. This

reduces their immediate productivity and lengthens the learning curve for the

new technology, which, in turn, delays the anticipated productivity associated

with the new technology.

A lag is created between technology implementation and increased employee

productivity. Technology requires that employers revise their definition of

employee productivity. When employees complain about the amount of time

they must spend writing and responding to e-mails, they're viewing this as

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

118

nonproductive time. But in the information economy, sharing information via e-

mails is part of the work and a component of productivity.

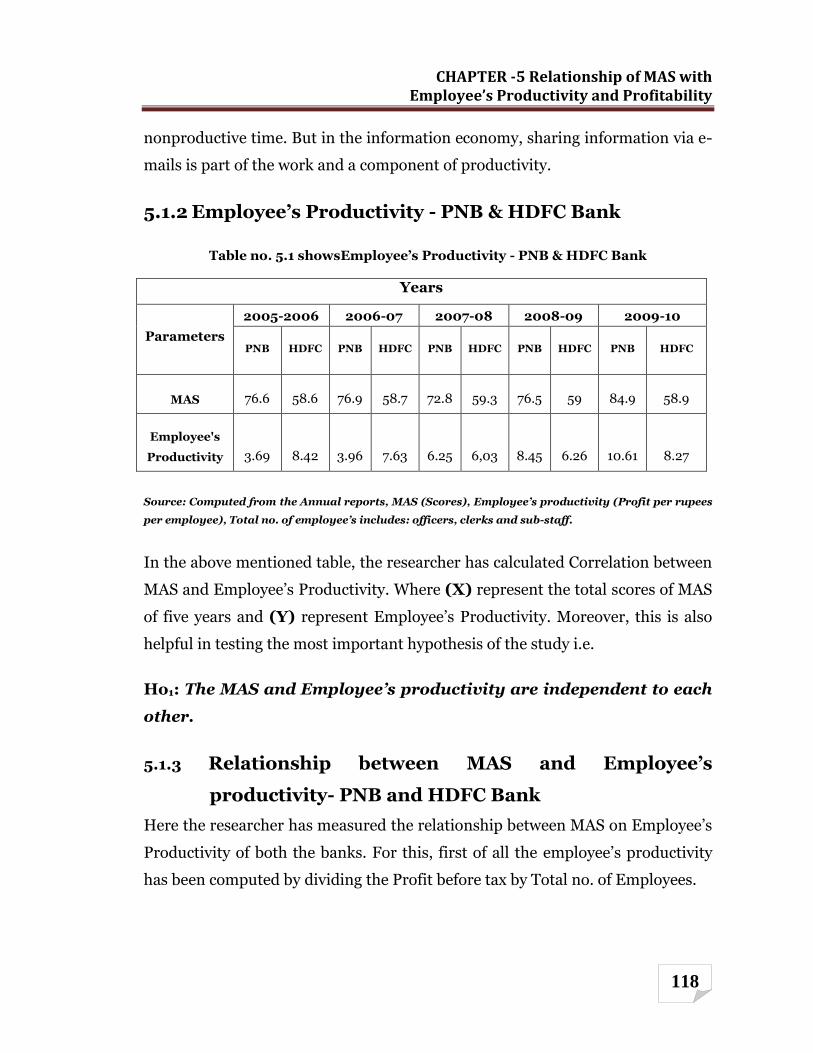

5.1.2 Employee’s Productivity - PNB & HDFC Bank

Table no. 5.1 showsEmployee’s Productivity - PNB & HDFC Bank

Years

Parameters

2005-2006 2006-07 2007-08 2008-09 2009-10

PNB HDFC PNB HDFC PNB HDFC PNB HDFC PNB HDFC

MAS 76.6 58.6 76.9 58.7 72.8 59.3 76.5 59 84.9 58.9

Employee's

Productivity 3.69 8.42 3.96 7.63 6.25 6,03 8.45 6.26 10.61 8.27

Source: Computed from the Annual reports, MAS (Scores), Employee’s productivity (Profit per rupees

per employee), Total no. of employee’s includes: officers, clerks and sub-staff.

In the above mentioned table, the researcher has calculated Correlation between

MAS and Employee‟s Productivity. Where (X) represent the total scores of MAS

of five years and (Y) represent Employee‟s Productivity. Moreover, this is also

helpful in testing the most important hypothesis of the study i.e.

Ho1: The MAS and Employee’s productivity are independent to each

other.

5.1.3 Relationship between MAS and Employee’s

productivity- PNB and HDFC Bank

Here the researcher has measured the relationship between MAS on Employee‟s

Productivity of both the banks. For this, first of all the employee‟s productivity

has been computed by dividing the Profit before tax by Total no. of Employees.

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

119

Table no. 5.2 Computation of Employee’s Productivity of both the banks.

Computation of Employee's Productivity - PNB and HDFC Bank

Years PNB

HDFC Bank

PBT

Tot.

no. of

empl.

Employee's

Prod. MAS

PBT

Tot.

no. of

empl.

Employee's

Prod. MAS

2005-06 2140.5 58047 3.69 76.6 1253.5 14878 8.42 58.6

2006-07 2268.8 57316 3.96 76.9 1638.8 21477 7.63 58.7

2007-08 3500 56025 6.25 72.8 2280.6 37836 6.03 59.3

2008-09 4917 58205 8.45 76.5 3299.3 52687 6.26 59

2009-10 6042.7 56928 10.61 84.9 4289.1 51888 8.27 58.9

(Rs in crore)

Source: Computed from the Annual reports, Employee’s Productivity= profit per Rs. per employee.

On the basis of the above table, the correlation between MAS and Employee‟s

Productivity of two banks is shown in table below:

Table no. 5.3

Computation Karl Pearson's Correlation Coefficient of PNB and HDFC

Bank on the basis of Employee's Productivity

Parameters PNB HDFC Bank

Correlation r r2 r r2

MAS & Employee's Productivity 0.64 0.40 -0.83 0.69

Source: Annual reports

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

120

The above table reveals that correlation value of PNB in the case of MAS and

Employee‟s Productivity is 0.64 which is positive high degree of correlation and

for HDFC is -0.83, which is negative moderate high degree of correlation. The

conclusion arrive that implementation of MAS increasing the employee‟s

productivity at a positive high rate in PNB, but in case of HDFC it is negative

moderate high rate.

So, in PNB the employee‟s productivity increases with the high score of MAS.

Though, the employee‟s productivity which is 40% depends on MAS. Here, it is

clear that the PNB is far better position than HDFC.

5.1.3 Comparison of PNB and HDFC Bank on the basis of

Employee’s Productivity

In order to test the hypothesis the above table no. 5.4 shows the coefficient of

correlation of PNB and HDFC and their z-test values, standard error and Z-value

for both the banks.

Comparison of PNB and HDFC Bank on the basis of Employee’s

Productivity

Parameter

PNB HDFC PNB HDFC

r1 r2 Z1 Z2

σ Z1-

Z2

Z-

va

lue

Ho(<1.96)

Employee's

Productivity 0.64 -0.83 0.76 -1.19 1 1.95 A

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

121

The null hypothesis stated that the MAS and Employee’s productivity are

independent to each other. Since, the computed value of z 1.95is less than

the table value of z 1.96at 0.05 level of significance; therefore, the null

hypothesis is accepted. Hence it can be safely said that there is no significant

difference in the MAS and employees‟ productivity. So, it can be concluded that

the MAS and Employee‟s productivity are independent to each other.

But employee‟s productivity is a positive aspect which no company would like to

be negative. Here, the correlation between MAS and Employee‟s Productivity in

HDFC Bank is negative -0.83, whereas in PNB it is positive 0.64. Therefore, it

can be concluded that employee‟s productivity in PNB is better than HDFC

Bank.

5.2 Relationship between MAS and Profitability

This chapter has also been divided into following sub- sections.

5.2.1 The concept of profitability.

5.2.2 Profitability in Banks.

5.2.3 Relationship between MAS and Profitability.

5.2.4 Comparison of PNB and HDFC Bank on the basis of Profitability.

5.2.1 Meaning and Concept of Profitability

Profitability means ability to make profit from all the business activities of an

organization, company, firm, or an enterprise. It shows how efficiently the

management can make profit by using all the resources available in the market.

According to Harward & Upton, “profitability is the „the ability of a given

investment to earn a return from its use.” However, the term „Profitability‟ is not

synonymous to the term „Efficiency‟. Profitability is an index of efficiency; and is

regarded as a measure of efficiency and management guide to greater efficiency.

Though, profitability is an important yardstick for measuring the efficiency, the

extent of profitability cannot be taken as a final proof of efficiency. Sometimes

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

122

satisfactory profits can mark inefficiency and conversely, a proper degree of

efficiency can be accompanied by an absence of profit. The net profit figure

simply reveals a satisfactory balance between the values receive and value given.

The change in operational efficiency is merely one of the factors on which

profitability of an enterprise largely depends. Moreover, there are many other

factors besides efficiency, which affect the profitability.

Definitions

“Each business unit works to earn maximum profits. The existence,

continuance and expansion of the business depends on its capacity to earn a

good amount of the business depends on its capacity to earn a good amount of

profits every year. The ability to earn profits is called profitability. The

profitability of a business concern is the net result of a large number of

decisions and policies.”

Dr.A.K. Garg

"Earnings are now the focus as results will be an indication of companies'

future profitability. Banks will benefit from increasing capital spending and

their stocks are still cheap."

TomokatsuMori R. S. Kulshrestha has rightly stated, “Profit in two separate business

concern may be identical, yet, many a times, it usually happens that their

profitability varies when measured in terms of size of investment”.

As Weston and Brigham rightly notes, “to the financial management profit

is the test of efficiency and a measure of control, to the owners a measure of the

worth of their investment, to the creditors the margin of safety, to the

government a measure of taxable capacity and a basis of legislative action and to

the country profit is an index of economic progress, national income generated

and the rise in the standard of living”, while profitability is an outcome of profit.

In other words, no profit drives towards profitability.

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

123

Reasons for Computing Profitability

Whether you are recording profitability for the past period or projecting

profitability for the coming period, measuring profitability is the most important

measure of the success of the business. A business that is not profitable cannot

survive. Conversely, a business that is highly profitable has the ability to reward

its owners with a large return on their investment. Increasing profitability is one

of the most important tasks of the business managers. Managers constantly look

for ways to change the business to improve profitability. These potential changes

can be analyzed with a pro forma income statement or a Partial Budget. Partial

budgeting allows you to assess the impact on profitability of a small or

incremental change in the business before it is implemented.

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

124

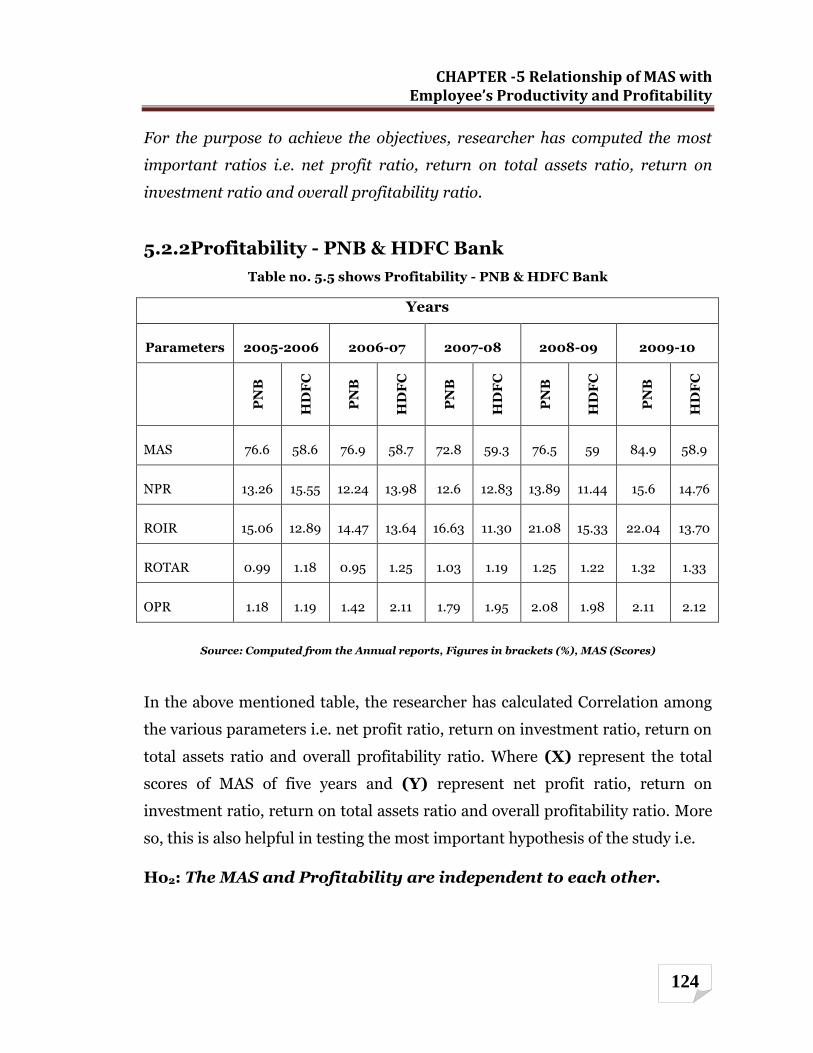

For the purpose to achieve the objectives, researcher has computed the most

important ratios i.e. net profit ratio, return on total assets ratio, return on

investment ratio and overall profitability ratio.

5.2.2Profitability - PNB & HDFC Bank

Table no. 5.5 shows Profitability - PNB & HDFC Bank

Years

Parameters 2005-2006 2006-07 2007-08 2008-09 2009-10

PN

B

HD

FC

PN

B

HD

FC

PN

B

HD

FC

PN

B

HD

FC

PN

B

HD

FC

MAS 76.6 58.6 76.9 58.7 72.8 59.3 76.5 59 84.9 58.9

NPR 13.26 15.55 12.24 13.98 12.6 12.83 13.89 11.44 15.6 14.76

ROIR 15.06 12.89 14.47 13.64 16.63 11.30 21.08 15.33 22.04 13.70

ROTAR 0.99 1.18 0.95 1.25 1.03 1.19 1.25 1.22 1.32 1.33

OPR 1.18 1.19 1.42 2.11 1.79 1.95 2.08 1.98 2.11 2.12

Source: Computed from the Annual reports, Figures in brackets (%), MAS (Scores)

In the above mentioned table, the researcher has calculated Correlation among

the various parameters i.e. net profit ratio, return on investment ratio, return on

total assets ratio and overall profitability ratio. Where (X) represent the total

scores of MAS of five years and (Y) represent net profit ratio, return on

investment ratio, return on total assets ratio and overall profitability ratio. More

so, this is also helpful in testing the most important hypothesis of the study i.e.

Ho2: The MAS and Profitability are independent to each other.

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

125

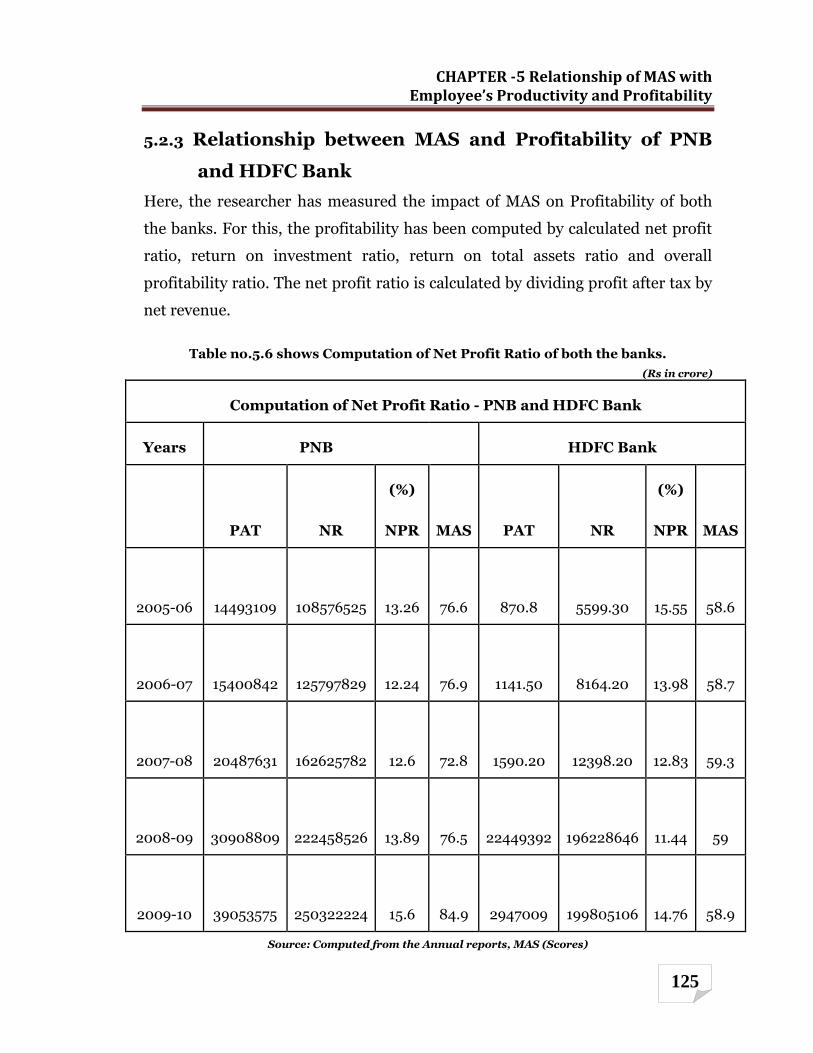

5.2.3 Relationship between MAS and Profitability of PNB

and HDFC Bank

Here, the researcher has measured the impact of MAS on Profitability of both

the banks. For this, the profitability has been computed by calculated net profit

ratio, return on investment ratio, return on total assets ratio and overall

profitability ratio. The net profit ratio is calculated by dividing profit after tax by

net revenue.

Table no.5.6 shows Computation of Net Profit Ratio of both the banks.

(Rs in crore)

Computation of Net Profit Ratio - PNB and HDFC Bank

Years PNB

HDFC Bank

PAT

NR

(%)

NPR MAS

PAT

NR

(%)

NPR MAS

2005-06 14493109 108576525 13.26 76.6 870.8 5599.30 15.55 58.6

2006-07 15400842 125797829 12.24 76.9 1141.50 8164.20 13.98 58.7

2007-08 20487631 162625782 12.6 72.8 1590.20 12398.20 12.83 59.3

2008-09 30908809 222458526 13.89 76.5 22449392 196228646 11.44 59

2009-10 39053575 250322224 15.6 84.9 2947009 199805106 14.76 58.9

Source: Computed from the Annual reports, MAS (Scores)

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

126

On the basis of the above table, the correlation between MAS and Profitability of

the two banks is shown in table below:

Table no.5.7

Computation Karl Pearson's Correlation Coefficient of PNB and

HDFC Bank on the basis of Net Profit Ratio

Parameter PNB HDFC Bank

Correlation r r2 r r2

MAS & Net profit ratio 0.86 0.74 -0.69 0.48

The above table reveals that correlation value of PNB in the case of MAS and net

profit ratio is 0.86 which is positive moderate high degree of correlation and for

HDFC is -0.69, which shows negative high degree of correlation. The result

reveals that implementation of MAS increasing the net profit ratio is moderate

high in PNB and negative high degree in HDFC.

So, in PNB the profitability increases with the high score of MAS. Though the

profitability is 74% it depends on MAS. Here, it is clear that the PNB is far better

than HDFC.

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

127

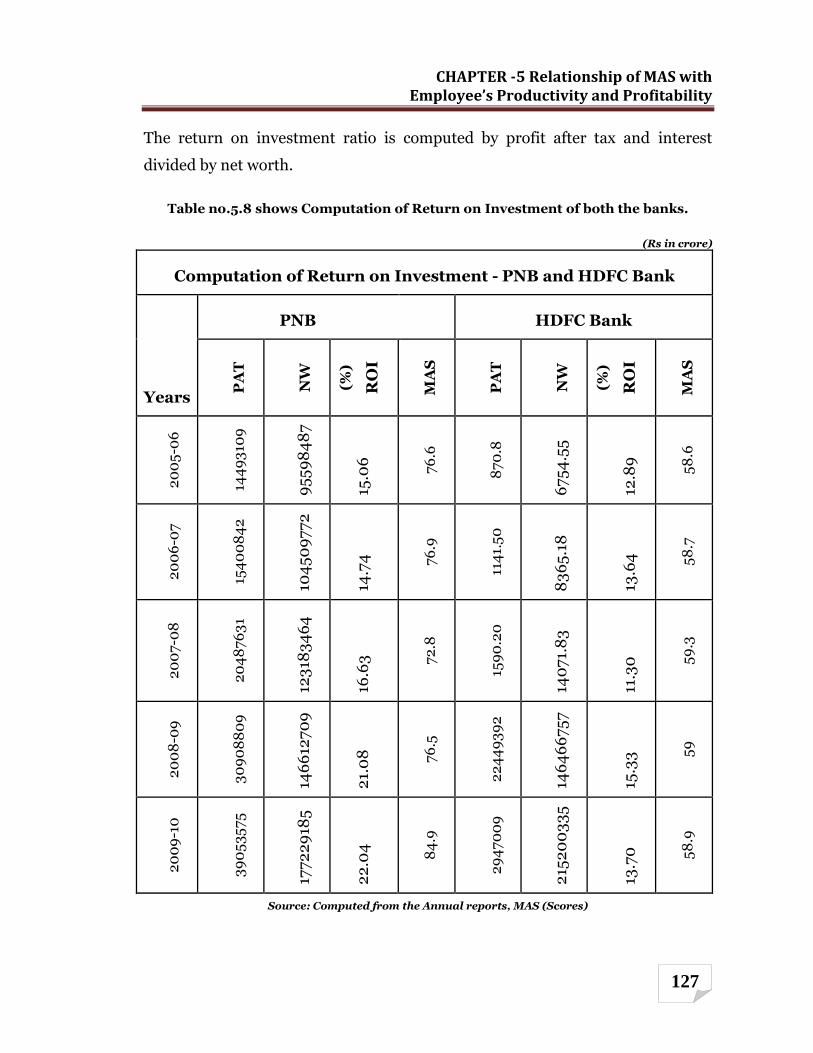

The return on investment ratio is computed by profit after tax and interest

divided by net worth.

Table no.5.8 shows Computation of Return on Investment of both the banks.

(Rs in crore)

Computation of Return on Investment - PNB and HDFC Bank

Years

PNB

HDFC Bank

PA

T

NW

(%)

RO

I

MA

S

PA

T

NW

(%)

RO

I

MA

S

20

05

-06

144

93

109

95

59

84

87

15.0

6

76

.6

87

0.8

67

54

.55

12.8

9

58

.6

20

06

-07

154

00

84

2

104

50

97

72

14.7

4

76

.9

114

1.5

0

83

65

.18

13.6

4

58

.7

20

07

-08

20

48

76

31

123

183

46

4

16.6

3

72

.8

159

0.2

0

140

71.

83

11.3

0

59

.3

20

08

-09

30

90

88

09

146

612

70

9

21.

08

76

.5

22

44

93

92

146

46

67

57

15.3

3 59

20

09

-10

39

05

35

75

177

22

918

5

22

.04

84

.9

29

47

00

9

215

20

03

35

13.7

0

58

.9

Source: Computed from the Annual reports, MAS (Scores)

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

128

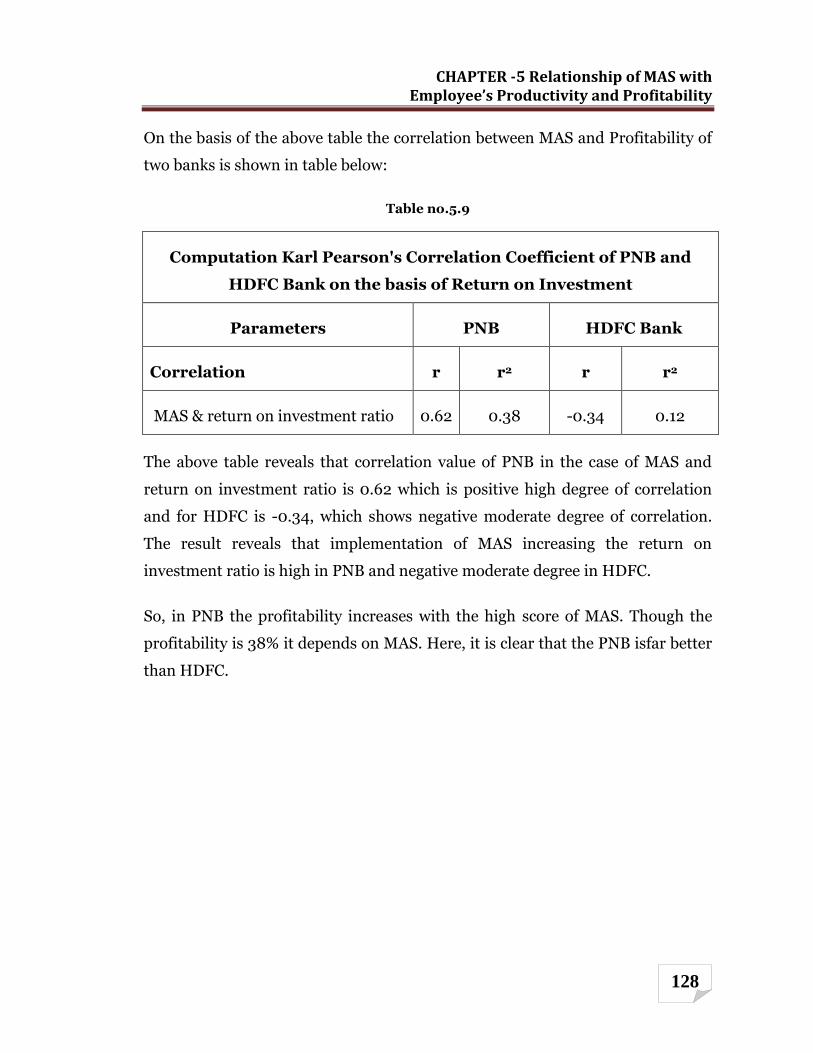

On the basis of the above table the correlation between MAS and Profitability of

two banks is shown in table below:

Table no.5.9

Computation Karl Pearson's Correlation Coefficient of PNB and

HDFC Bank on the basis of Return on Investment

Parameters PNB HDFC Bank

Correlation r r2 r r2

MAS & return on investment ratio 0.62 0.38 -0.34 0.12

The above table reveals that correlation value of PNB in the case of MAS and

return on investment ratio is 0.62 which is positive high degree of correlation

and for HDFC is -0.34, which shows negative moderate degree of correlation.

The result reveals that implementation of MAS increasing the return on

investment ratio is high in PNB and negative moderate degree in HDFC.

So, in PNB the profitability increases with the high score of MAS. Though the

profitability is 38% it depends on MAS. Here, it is clear that the PNB isfar better

than HDFC.

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

129

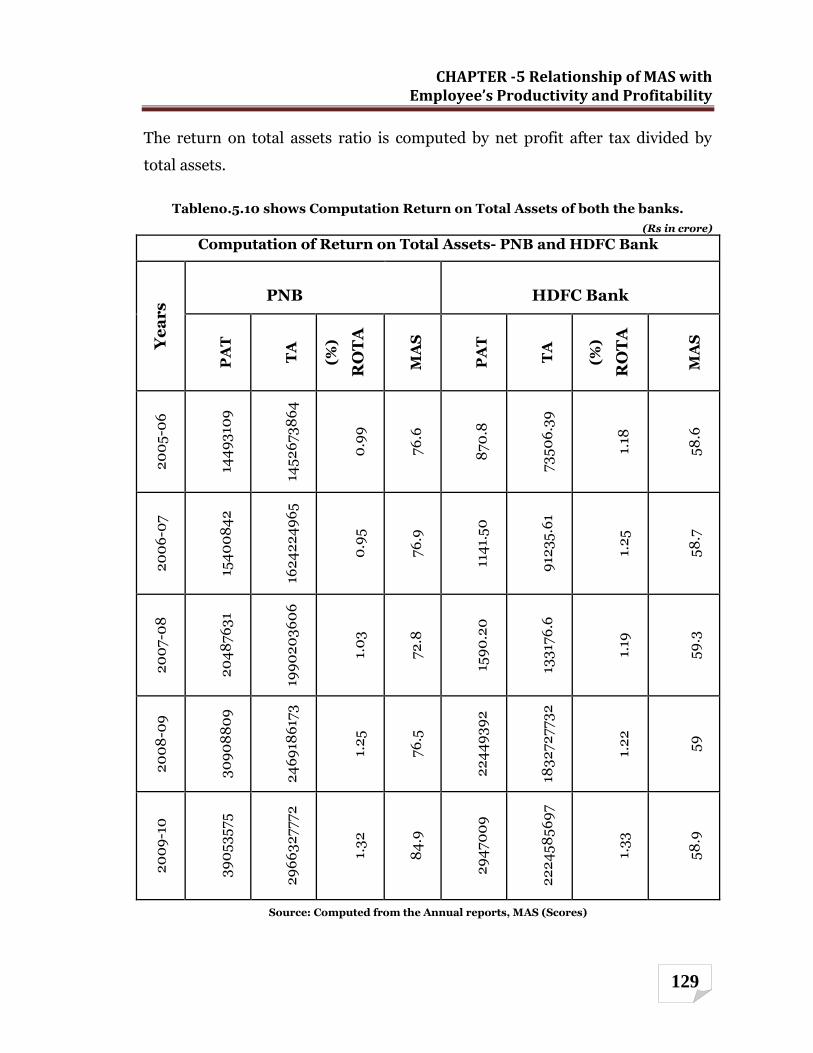

The return on total assets ratio is computed by net profit after tax divided by

total assets.

Tableno.5.10 shows Computation Return on Total Assets of both the banks.

(Rs in crore)

Computation of Return on Total Assets- PNB and HDFC Bank

Ye

ar

s PNB

HDFC Bank

PA

T

TA

(%)

RO

TA

MA

S

PA

T

TA

(%)

RO

TA

MA

S

20

05

-06

144

93

109

145

26

73

86

4

0.9

9

76

.6

87

0.8

73

50

6.3

9

1.18

58

.6

20

06

-07

154

00

84

2

162

42

24

96

5

0.9

5

76

.9

114

1.5

0

912

35

.61

1.2

5

58

.7

20

07

-08

20

48

76

31

199

02

03

60

6

1.0

3

72

.8

159

0.2

0

133

176

.6

1.19

59

.3

20

08

-09

30

90

88

09

24

69

186

173

1.2

5

76

.5

22

44

93

92

183

27

27

73

2

1.2

2

59

20

09

-10

39

05

35

75

29

66

32

77

72

1.3

2

84

.9

29

47

00

9

22

24

58

56

97

1.3

3

58

.9

Source: Computed from the Annual reports, MAS (Scores)

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

130

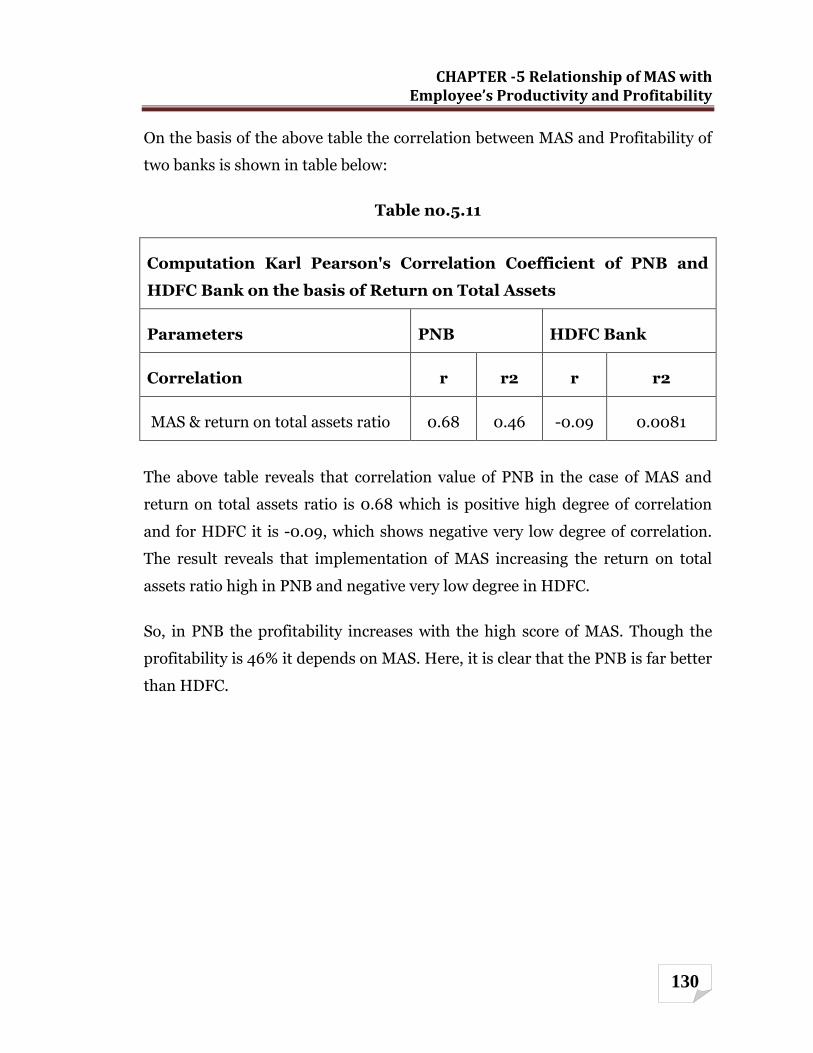

On the basis of the above table the correlation between MAS and Profitability of

two banks is shown in table below:

Table no.5.11

Computation Karl Pearson's Correlation Coefficient of PNB and

HDFC Bank on the basis of Return on Total Assets

Parameters PNB HDFC Bank

Correlation r r2 r r2

MAS & return on total assets ratio 0.68 0.46 -0.09 0.0081

The above table reveals that correlation value of PNB in the case of MAS and

return on total assets ratio is 0.68 which is positive high degree of correlation

and for HDFC it is -0.09, which shows negative very low degree of correlation.

The result reveals that implementation of MAS increasing the return on total

assets ratio high in PNB and negative very low degree in HDFC.

So, in PNB the profitability increases with the high score of MAS. Though the

profitability is 46% it depends on MAS. Here, it is clear that the PNB is far better

than HDFC.

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

131

The overall profitability ratio is calculated by dividing profit before tax by capital

employed.

Table no.5.12 shows Computation of Overall Profitability Ratio of both the banks.

(Rs in crore)

Computation of Return on Total Assets- PNB and HDFC Bank

Years

PNB

HDFC Bank

PB

T

CE

(%)

OP

R

MA

S

PB

T

CE

(%)

OP

R

MA

S

20

05

-06

214

0.5

4

135

72

615

15

1.5

8

76

.6

125

3.5

1

65

65

.9

1.9

1

58

.6

20

06

-07

22

68

.80

152

24

29

87

6

1.4

2

76

.9

163

8.7

7

77

54

6.4

8

2.1

1

58

.7

20

07

-08

35

00

.63

184

22

213

20

1.7

9

72

.8

22

80

.63

116

74

4.6

9

1.9

5

59

.3

20

08

-09

49

16.9

9

23

68

22

93

73

2.0

8

76

.5

32

99

.25

167

02

84

910

1.9

8

59

20

09

-10

60

42

.66

28

62

137

57

2

2.1

1

84

.9

42

89

.14

20

184

26

25

6

2.1

2

58

.9

Source: Computed from the Annual reports, MAS (Scores)

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

132

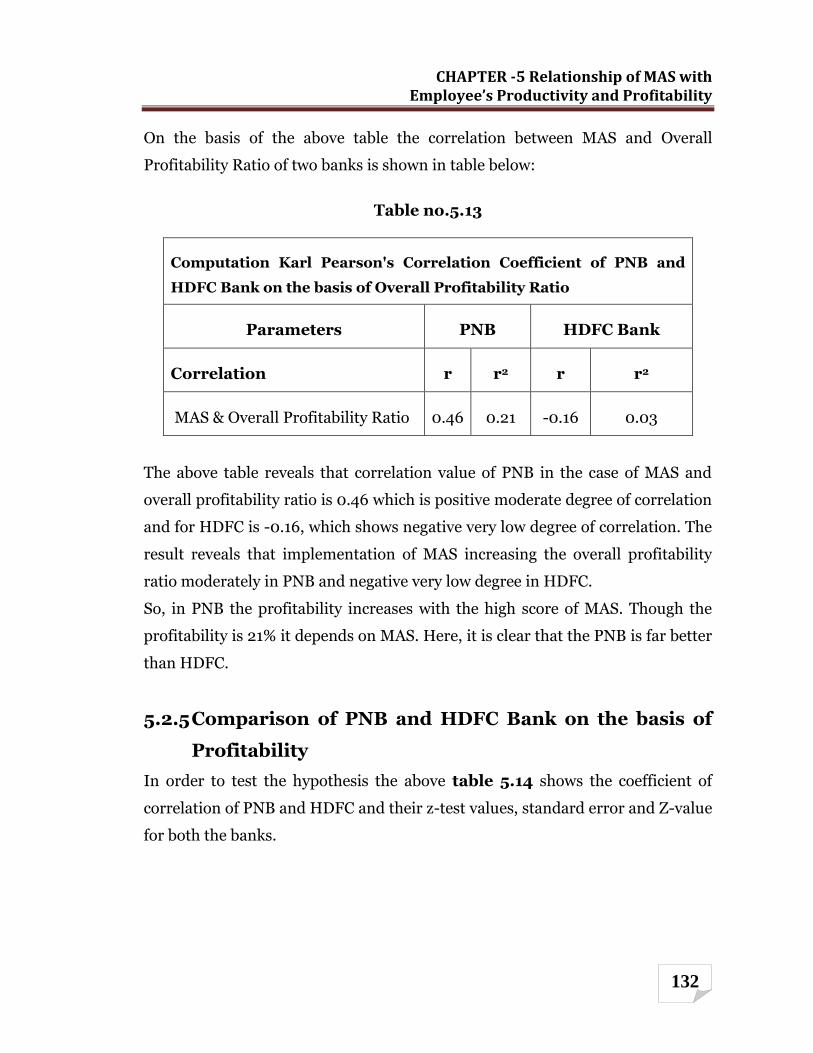

On the basis of the above table the correlation between MAS and Overall

Profitability Ratio of two banks is shown in table below:

Table no.5.13

Computation Karl Pearson's Correlation Coefficient of PNB and

HDFC Bank on the basis of Overall Profitability Ratio

Parameters PNB HDFC Bank

Correlation r r2 r r2

MAS & Overall Profitability Ratio 0.46 0.21 -0.16 0.03

The above table reveals that correlation value of PNB in the case of MAS and

overall profitability ratio is 0.46 which is positive moderate degree of correlation

and for HDFC is -0.16, which shows negative very low degree of correlation. The

result reveals that implementation of MAS increasing the overall profitability

ratio moderately in PNB and negative very low degree in HDFC.

So, in PNB the profitability increases with the high score of MAS. Though the

profitability is 21% it depends on MAS. Here, it is clear that the PNB is far better

than HDFC.

5.2.5 Comparison of PNB and HDFC Bank on the basis of

Profitability

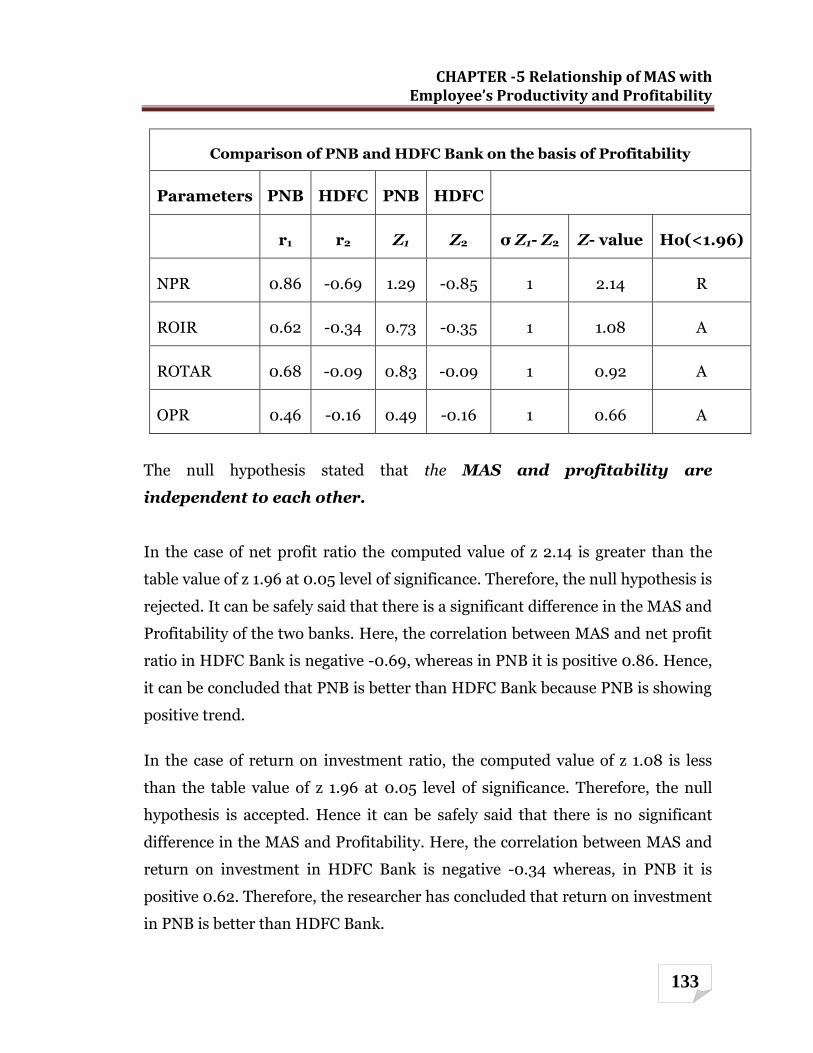

In order to test the hypothesis the above table 5.14 shows the coefficient of

correlation of PNB and HDFC and their z-test values, standard error and Z-value

for both the banks.

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

133

Comparison of PNB and HDFC Bank on the basis of Profitability

Parameters PNB HDFC PNB HDFC

r1 r2 Z1 Z2 σ Z1- Z2 Z- value Ho(<1.96)

NPR 0.86 -0.69 1.29 -0.85 1 2.14 R

ROIR 0.62 -0.34 0.73 -0.35 1 1.08 A

ROTAR 0.68 -0.09 0.83 -0.09 1 0.92 A

OPR 0.46 -0.16 0.49 -0.16 1 0.66 A

The null hypothesis stated that the MAS and profitability are

independent to each other.

In the case of net profit ratio the computed value of z 2.14 is greater than the

table value of z 1.96 at 0.05 level of significance. Therefore, the null hypothesis is

rejected. It can be safely said that there is a significant difference in the MAS and

Profitability of the two banks. Here, the correlation between MAS and net profit

ratio in HDFC Bank is negative -0.69, whereas in PNB it is positive 0.86. Hence,

it can be concluded that PNB is better than HDFC Bank because PNB is showing

positive trend.

In the case of return on investment ratio, the computed value of z 1.08 is less

than the table value of z 1.96 at 0.05 level of significance. Therefore, the null

hypothesis is accepted. Hence it can be safely said that there is no significant

difference in the MAS and Profitability. Here, the correlation between MAS and

return on investment in HDFC Bank is negative -0.34 whereas, in PNB it is

positive 0.62. Therefore, the researcher has concluded that return on investment

in PNB is better than HDFC Bank.

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

134

In the case of return on total assets ratio the computed value of z 0.92 is less

than the table value of z 1.96 at 0.05 level of significance. Therefore, the null

hypothesis is accepted. Hence it can be safely said that there is insignificant

difference in the MAS and Profitability. Here, the correlation between MAS and

return on total assets in HDFC Bank is negative -0.09, whereasin PNB it is

positive 0.68. Therefore, the researcher has concluded that return on total assets

in PNB is better than HDFC Bank.

In the case of overall profitability ratio, the computed value of z 0.66 is less than

the table value of z 1.96 at 0.05 level of significance. Therefore, the null

hypothesis is accepted. Hence it can be safely said that there is insignificant

difference in the MAS and Profitability. Here, the correlation between MAS and

overall profitability in HDFC Bank is negative -0.16. However, in PNB it is

positive 0.46. Therefore, the researcher has concluded that overall profitability

in PNB is better than HDFC Bank.

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

135

REFERENCES

1. A. J. Field, “The Concise Encyclopedia of Economics: Productivity"; 2008.

2. Annual reports of PNB.

3. Annual reports of HDFC Bank.

4. C.R.Kothari, Research Methodology- Methods and Techniques: New age

international (P) Ltd. Publishers.2nd Edition 2008

5. Gallup: Q12 Employee Engagement Surve2.

6. Harward&Upto, “Introduction to Business Finance”, McGraw Hill, New

York, 1961.

7. I. M. Pandey, “Financial Management”, 2002, Vikas Publishing House

Pvt.Ltd. New Delhi.

8. International Operations Management. Copenhagen, Denmark:

Copenhagen Business School Press, 2002.

9. Investor words.com.1

10. www.investors words.com.

11. K.K.Sharma, Arun Kumar, AlkaChaudhary-Statistics in Management

Studies: Krishna Prakashan Media (P) Ltd. 9th Edition 2008. Page no.8.212.

12. M. Y. Khan & P K Jain, “Financial Management – Text and Problems”, Tata

McGraw – Hill Publishing Company Limited, New Delhi, 2003.

13. New Economy Index: Technology, Innovation & New Economy Project.

14. P. Krugman,"The Age of Diminished Expectations: U.S. Economic Policy in

the 1990s";1997.

15. Plenert, Gerhard. The eManager: Value Chain Management in an

ecommerce World. Dublin, Ireland: Blackhall Publishing, 2001.

16. Productivity- Wikipedia.

17. Profitability-Wikipedia.

18. R.P.Varshney, Business Statistics: Jawahar Publication-Agra 5th Edition

2009-10.page,72.

CHAPTER -5 Relationship of MAS with Employee’s Productivity and Profitability

136

19. S.P.Guta, M.K.Gupta. Business Statistics: Sultan Chand & Sons Publishers

New Delhi 4th Edition. Page no.199,204, 525-526.

20. Stevenson, William J. Production and Operations Management. Boston,

MA: Irwin McGraw-Hill, 1999.

21. Vora, Jay A. "Productivity and Performance Measures: Who Uses Them."

Production and Inventory Management Journal 33, no. 1 (1992): 46-49.

22. www.businessdictionary.com.

![2 Movie Mas Febrero [Movie Mas Com]](https://img.pdfslide.us/doc/110x75/55947db61a28abb91b8b4698/2-movie-mas-febrero-movie-mas-com.jpg)