Embed Size (px)

Citation preview

REIT (Real Estate Investment Trust)

Valuation 101Would You Like a Dividend with Your Funds

From Operations?

Question the Other Day….

“Help! I have to value a real estate investment trust (REIT) as part of a case study in an interview.”

“How should I do it? I looked online, but all the templates and examples seem too complicated.”

The Short Answer

• Yes, REIT valuation can get complex… but you can also take an 80/20 approach and get decent results without a huge investment of time

• Point #1: You must understand the basic characteristics of REITs before valuing them

• Point #2: You must know whether your REIT follows U.S. GAAP or IFRS – all other online articles ignore the differences

• Point #3: REIT Valuation is not that much different – Public Comps, Precedent Transactions, and the DCF still work… but with a few differences and additions

Lesson Outline

• Part #1: Basic characteristics of REITs and differences in accounting and key metrics under U.S. GAAP vs. IFRS

• Part #2: How to build a simple projection model for a REIT

• Part #3: How to extend it into a Discounted Cash Flow (DCF) or Dividend Discount Model (DCM)

• Part #4: How to add a Net Asset Value (NAV) Model for U.S. REITs and Public Comps for both types of REITs

Basic Characteristics of REITs

• A real estate investment trust (REIT) is a company that buys, sells, develops, and operates properties or other real estate assets

• It must distribute a high percentage of Net Income in the form of Dividends, maintain high % of Real Estate Revenue and Assets, etc.

• And: The REIT pays nothing, or very little, in corporate income taxes

• Implication #1: REITs are always maintaining, acquiring, developing, renovating, and selling properties – project each one

• Implication #2: REITs constantly need to raise Debt and Equity

Basic Characteristics of REITs• Implication #3: Buying/selling/revaluing of properties makes

Net Income fluctuate, creating the need for alternative metrics

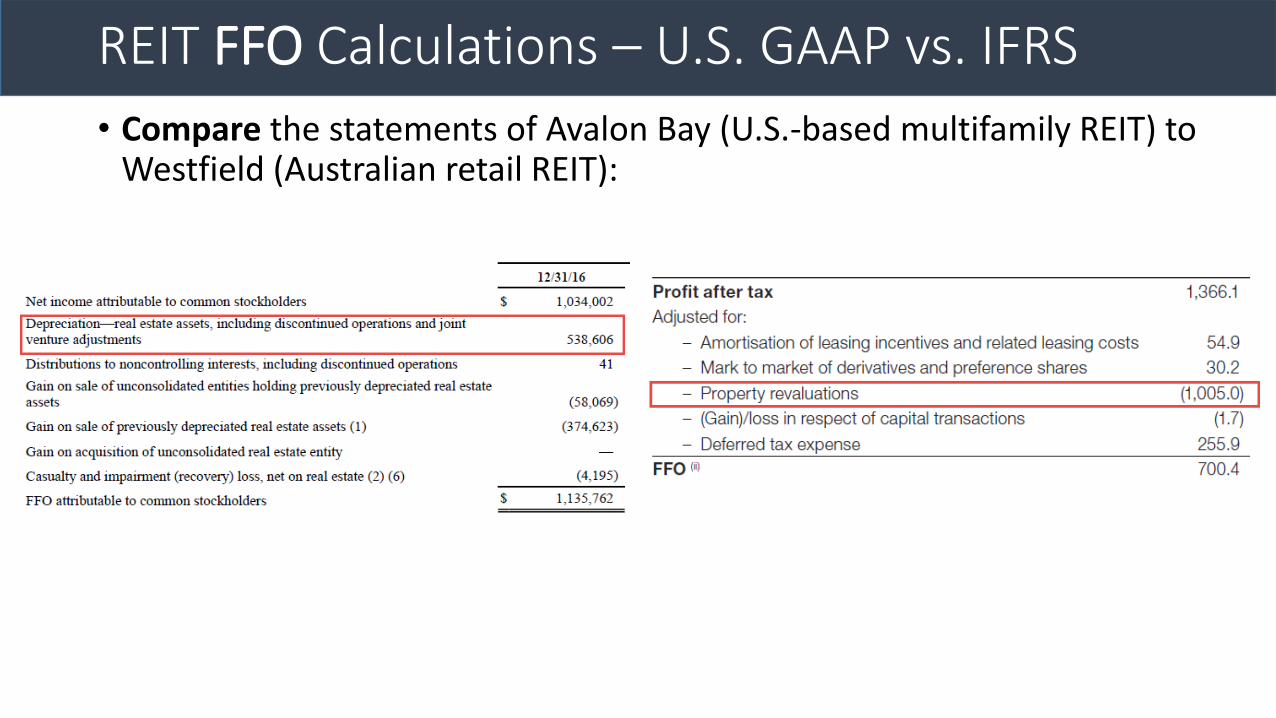

• Funds from Operations (FFO): Net Income + RE Depreciation & Amortization + Losses / (Gains) + Impairments

• U.S. GAAP: Depreciation on the Income Statement is huge

• IFRS: No Depreciation, but REITs mark their properties to market value and record Unrealized (Fair Value) Gains/Losses on the IS!

• IFRS: The D&A component of FFO will be 0, and Losses / (Gains) will be much bigger

REIT FFO Calculations – U.S. GAAP vs. IFRS

• Compare the statements of Avalon Bay (U.S.-based multifamily REIT) to Westfield (Australian retail REIT):

Basic Characteristics of REITs

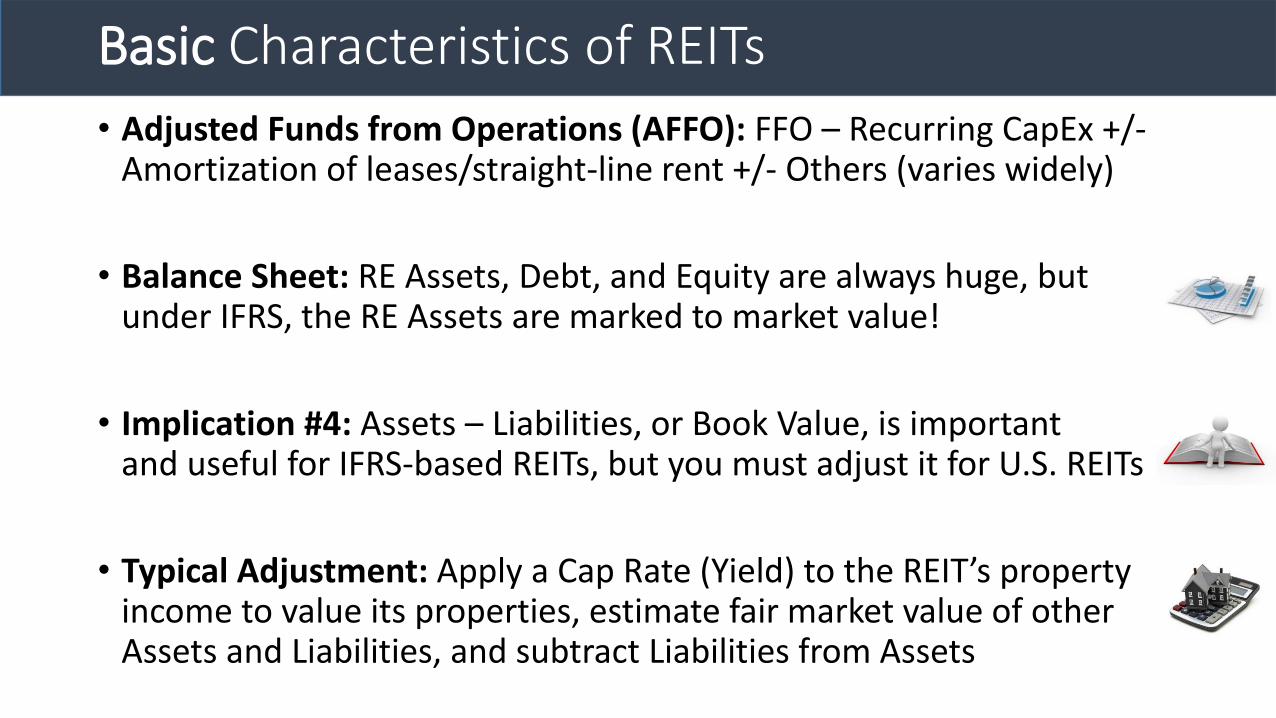

• Adjusted Funds from Operations (AFFO): FFO – Recurring CapEx +/-Amortization of leases/straight-line rent +/- Others (varies widely)

• Balance Sheet: RE Assets, Debt, and Equity are always huge, but under IFRS, the RE Assets are marked to market value!

• Implication #4: Assets – Liabilities, or Book Value, is important and useful for IFRS-based REITs, but you must adjust it for U.S. REITs

• Typical Adjustment: Apply a Cap Rate (Yield) to the REIT’s property income to value its properties, estimate fair market value of other Assets and Liabilities, and subtract Liabilities from Assets

Simple Projection Model for a REIT

• Step #1: Project revenue and expenses for the REIT’s existing (“same-store”) properties – assume rental growth and margins

• Step #2: Make assumptions for the REIT’s acquisition and development/renovation plans, such as annual spending, an operating income yield on that spending, and a margin

• Step #3: Assume that the REIT also divests properties, records Gains/Losses, and loses revenue and operating income as a result

• Step #4: Add up all the property-level revenue and expenses

Simple Projection Model for a REIT

• Step #5: Project corporate-level items, such as Depreciation, SG&A, Maintenance CapEx, and Working Capital, in the traditional ways (e.g., % of revenue or expenses)

• Step #6: Make Dividends a % of FFO, AFFO, or similar metric

• Step #7: Assume Debt and/or Equity Issued based on the Cash balance before financing vs. a minimum Cash Balance (small % of expenses)

Extension into a DCF or DDM

• Step #1: For a DCF, start by linking in the revenue, expenses, etc. from your projection model to calculate Unlevered FCF

• Differences: Can ignore corporate taxes in most cases, but you must include all CapEx spending and asset disposals!

• Also: Track Stock Issued if the REIT keeps issuing it continually

• Step #2: Project revenue growth, margins, D&A, CapEx, and Asset Sales beyond the end of projections to get ~10 years total

• Step #3: Make a simple assumption for future Stock Issuances

Extension into a DCF or DDM

• Step #4: Calculate Terminal Value with a Terminal EBITDA multiple or the Gordon Growth Method, and back into Implied Equity Value

• Implied Share Price: Make sure you divide Implied Equity Value by (Current Share Count + Estimated # of Future Shares to Be Issued)

• DDM: Similar, except you use Cost of Equity instead of WACC, use P / FFO or variants for Terminal Value, and discount and sum up Dividends instead

• Recommendation: We still like the Unlevered DCF because it’s easier to set up (no need to forecast interest, Debt, etc.)

NAV Model and Public Comps

• Only U.S.-Based REITs: For IFRS ones, properties values already appropriate, so Book Value is fairly close to NAV

• First: Project the forward “Net Operating Income” (operating income from properties) and divide by an appropriate “Cap Rate” or “Yield”

• Second: Value the other assets; small premium for Construction, set Goodwill/Intangibles to 0, and the rest should stay about the same

• Third: Adjust the Liabilities – main adjustment is to take the fair market value of Debt if interest rates or credit risk have changed

NAV Model and Public Comps

• Fourth: Subtract the adjusted Liabilities from the adjusted Assets to calculate Net Asset Value (NAV), and then NAV per Share

• Public Comps: Typically screen based on Real Estate Assets, Geography, and Sub-Industry (e.g., Hotel REITs or Retail REITs)

• Metrics: Can still calculate Equity Value, Enterprise Value, EBITDA, EV / EBITDA, etc.

• U.S. REITs: Will also use FFO and P / FFO, and NAV and P / NAV

• IFRS REITs: Book Value and P / BV in place of NAV and P / NAV

NAV Model and Public Comps

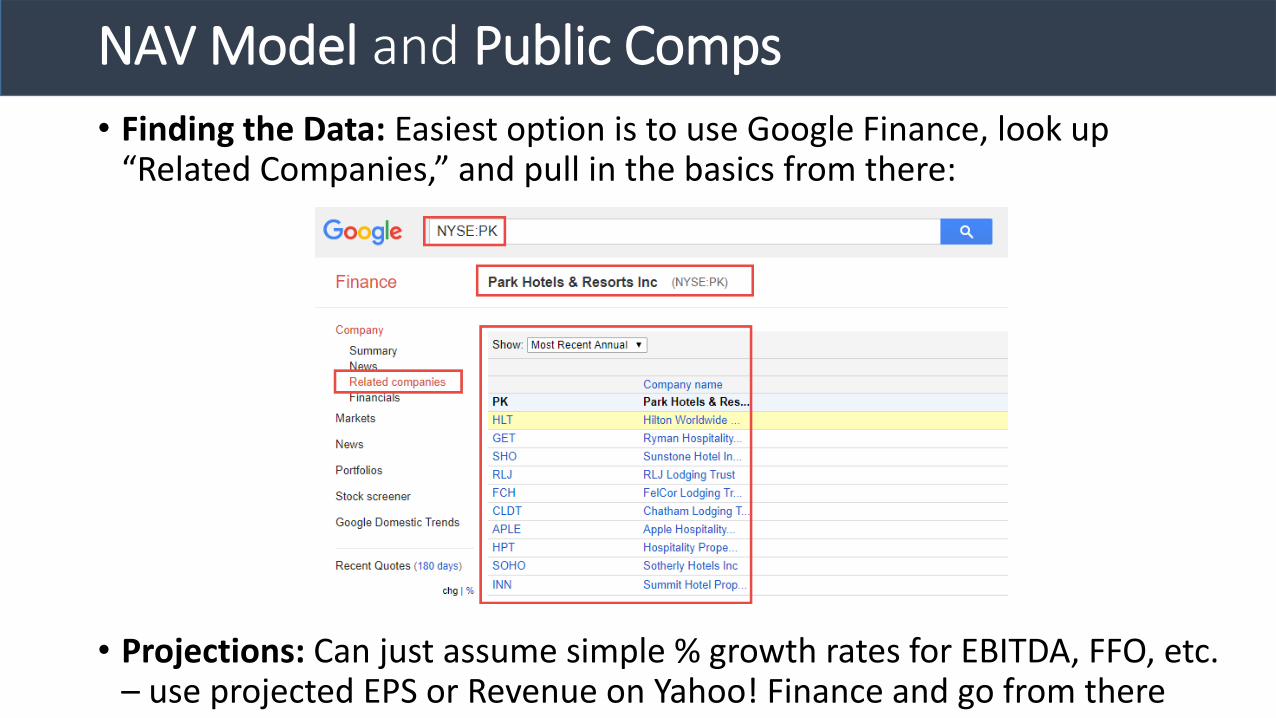

• Finding the Data: Easiest option is to use Google Finance, look up “Related Companies,” and pull in the basics from there:

• Projections: Can just assume simple % growth rates for EBITDA, FFO, etc. – use projected EPS or Revenue on Yahoo! Finance and go from there

Recap and Summary

• Part #1: Basic characteristics of REITs and differences in accounting and key metrics under U.S. GAAP vs. IFRS

• Part #2: How to build a simple projection model for a REIT

• Part #3: How to extend it into a Discounted Cash Flow (DCF) or Dividend Discount Model (DCM)

• Part #4: How to add a Net Asset Value (NAV) Model for U.S. REITs and Public Comps for both types of REITs

![PLife REIT”) - Investor Relations: IR Homeplifereit.listedcompany.com/misc/Full_year_2014...4. Q and Full Year . 2014. Key Highlights [cont’d] 8. Valuation Gain In Properties ―](https://img.pdfslide.us/doc/110x75/5ec616e190a1e3175f254194/plife-reita-investor-relations-ir-4-q-and-full-year-2014-key-highlights.jpg)