Embed Size (px)

Citation preview

Seminar On Union Budget 2014 –

REIT, InvIT and FDI issues

Chamber of Tax Consultants — Delhi ChapterChamber of Tax Consultants — Delhi Chapter

and IFA India—northern region chapter

July 19, 2014

Sunil Jain

J. Sagar Associates

advocates & solicitors

Delhi | Gurgaon | Mumbai | Bangalore | Hyderabad

Contents

FDI in Defence manufacturing sector

FDI in construction/development and low-cost housing

FDI in Insurance sector

REIT and InvIT – basic regulatory features

Common tax regime – REIT and InvIT

2

Ponderables – problems for developers and solutions

Common tax regime – REIT and InvIT

Issues hanging even after a beneficial tax regime

Insurance sector

3

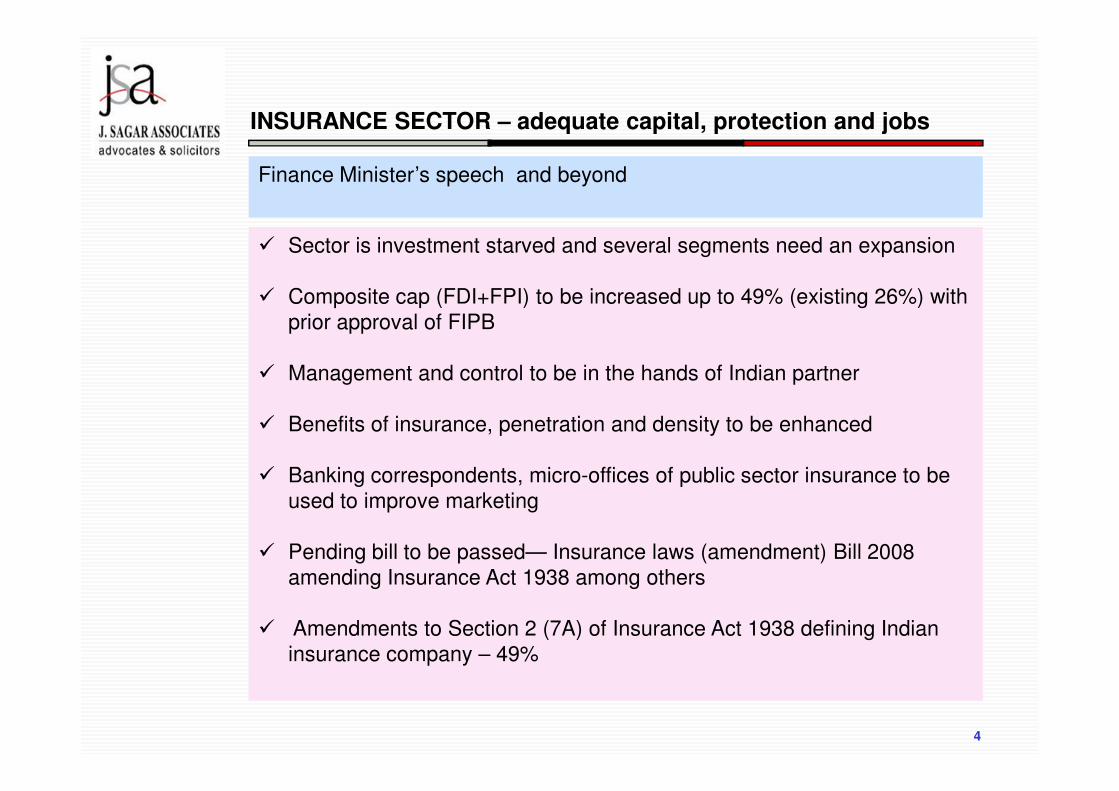

INSURANCE SECTOR – adequate capital, protection and jobs

Finance Minister’s speech and beyond

� Sector is investment starved and several segments need an expansion

� Composite cap (FDI+FPI) to be increased up to 49% (existing 26%) with

prior approval of FIPB

� Management and control to be in the hands of Indian partner

4

� Benefits of insurance, penetration and density to be enhanced

� Banking correspondents, micro-offices of public sector insurance to be

used to improve marketing

� Pending bill to be passed— Insurance laws (amendment) Bill 2008

amending Insurance Act 1938 among others

� Amendments to Section 2 (7A) of Insurance Act 1938 defining Indian

insurance company – 49%

Defence Manufacturing

Sector

5

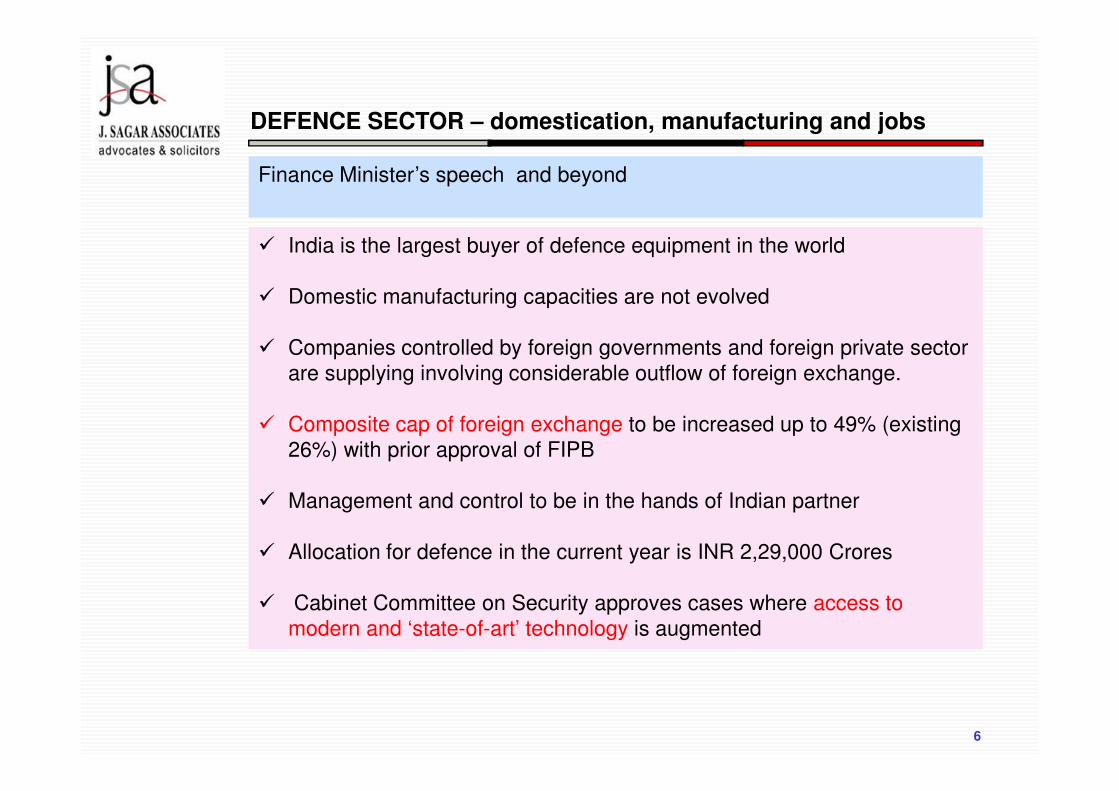

DEFENCE SECTOR – domestication, manufacturing and jobs

Finance Minister’s speech and beyond

� India is the largest buyer of defence equipment in the world

� Domestic manufacturing capacities are not evolved

� Companies controlled by foreign governments and foreign private sector

are supplying involving considerable outflow of foreign exchange.

6

� Composite cap of foreign exchange to be increased up to 49% (existing

26%) with prior approval of FIPB

� Management and control to be in the hands of Indian partner

� Allocation for defence in the current year is INR 2,29,000 Crores

� Cabinet Committee on Security approves cases where access to

modern and ‘state-of-art’ technology is augmented

Construction/housing Sector

7

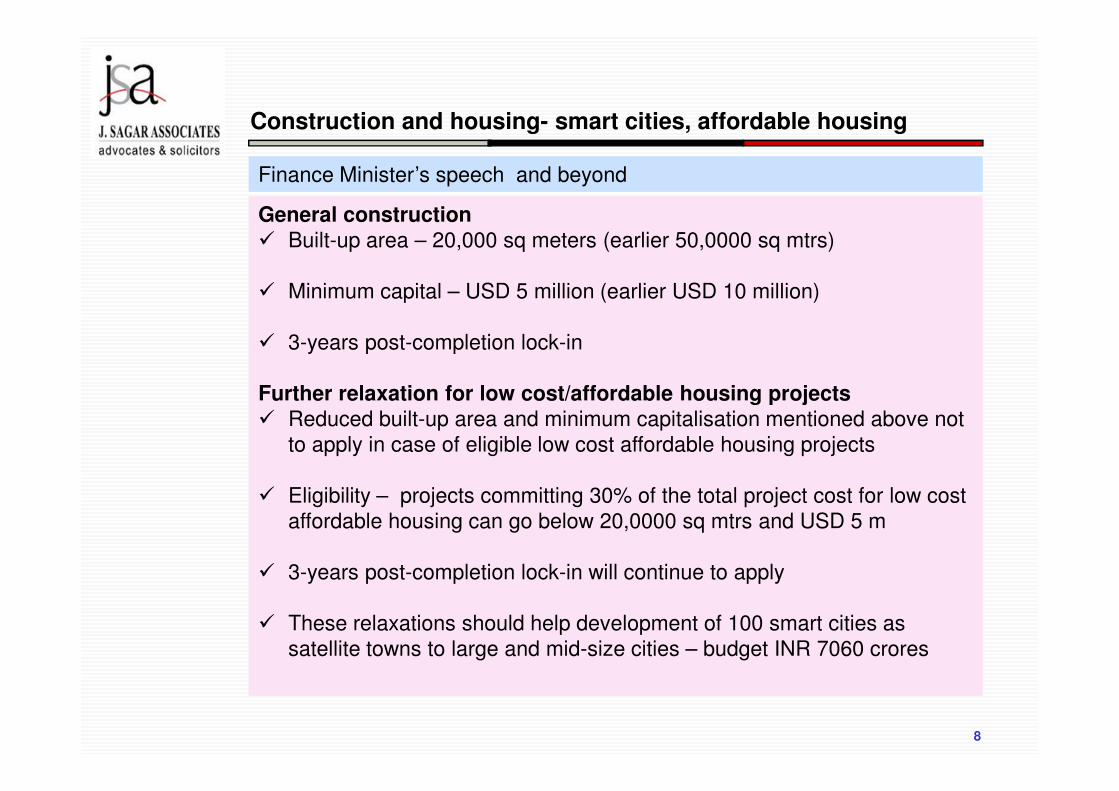

Construction and housing- smart cities, affordable housing

Finance Minister’s speech and beyond

General construction� Built-up area – 20,000 sq meters (earlier 50,0000 sq mtrs)

� Minimum capital – USD 5 million (earlier USD 10 million)

� 3-years post-completion lock-in

Further relaxation for low cost/affordable housing projects

8

Further relaxation for low cost/affordable housing projects� Reduced built-up area and minimum capitalisation mentioned above not

to apply in case of eligible low cost affordable housing projects

� Eligibility – projects committing 30% of the total project cost for low cost

affordable housing can go below 20,0000 sq mtrs and USD 5 m

� 3-years post-completion lock-in will continue to apply

� These relaxations should help development of 100 smart cities as

satellite towns to large and mid-size cities – budget INR 7060 crores

REIT and InvIT- basics

9

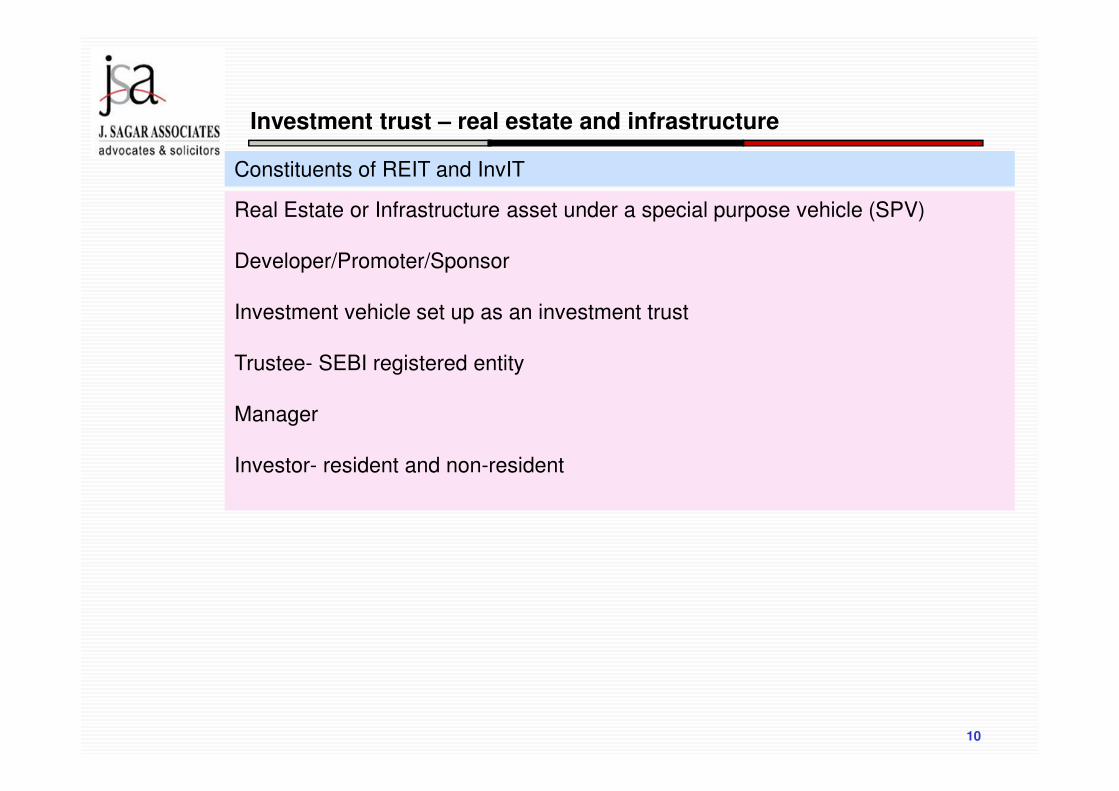

Investment trust – real estate and infrastructure

Real Estate or Infrastructure asset under a special purpose vehicle (SPV)

Developer/Promoter/Sponsor

Investment vehicle set up as an investment trust

Trustee- SEBI registered entity

Constituents of REIT and InvIT

10

Manager

Investor- resident and non-resident

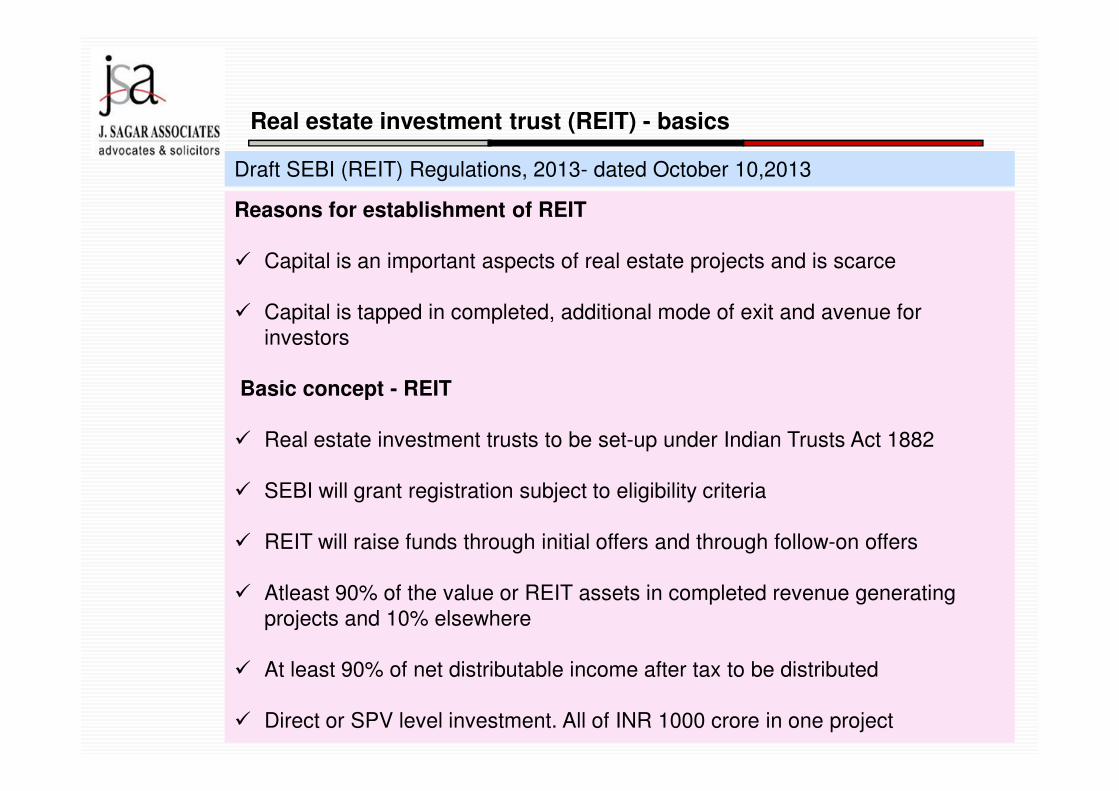

Real estate investment trust (REIT) - basics

Reasons for establishment of REIT

� Capital is an important aspects of real estate projects and is scarce

� Capital is tapped in completed, additional mode of exit and avenue for

investors

Basic concept - REIT

Draft SEBI (REIT) Regulations, 2013- dated October 10,2013

11

Basic concept - REIT

� Real estate investment trusts to be set-up under Indian Trusts Act 1882

� SEBI will grant registration subject to eligibility criteria

� REIT will raise funds through initial offers and through follow-on offers

� Atleast 90% of the value or REIT assets in completed revenue generating

projects and 10% elsewhere

� At least 90% of net distributable income after tax to be distributed

� Direct or SPV level investment. All of INR 1000 crore in one project

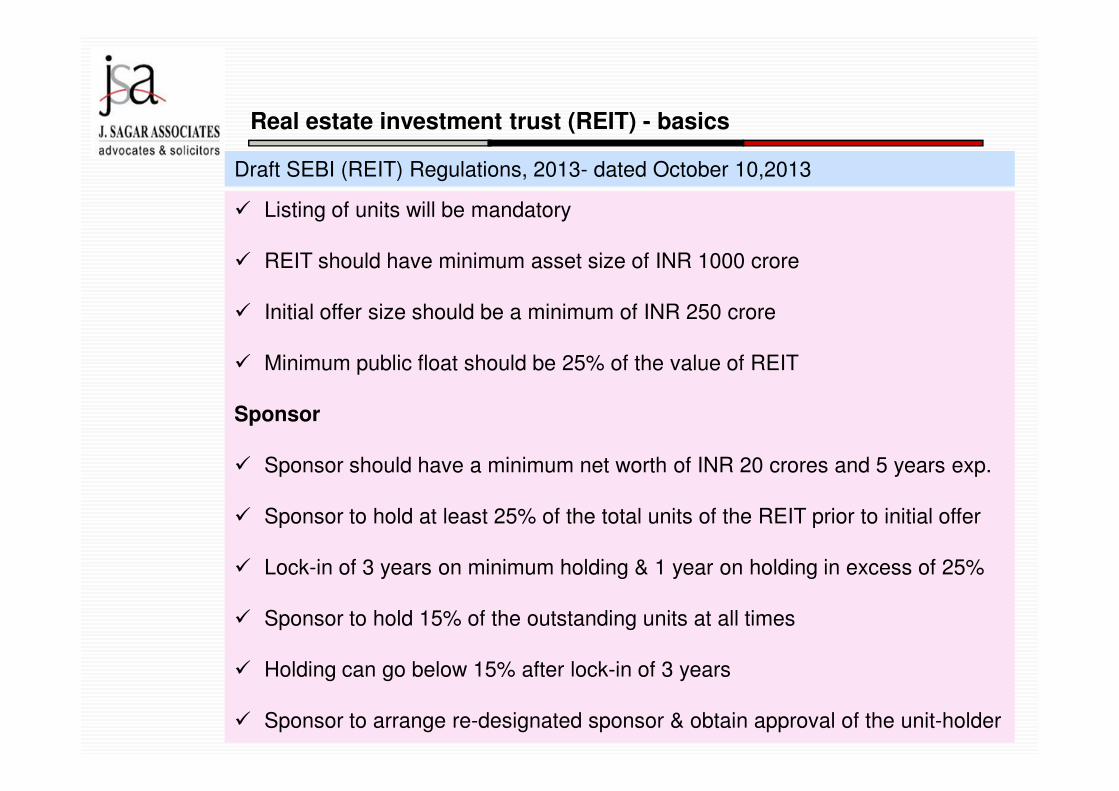

Real estate investment trust (REIT) - basics

� Listing of units will be mandatory

� REIT should have minimum asset size of INR 1000 crore

� Initial offer size should be a minimum of INR 250 crore

� Minimum public float should be 25% of the value of REIT

Draft SEBI (REIT) Regulations, 2013- dated October 10,2013

12

Sponsor

� Sponsor should have a minimum net worth of INR 20 crores and 5 years exp.

� Sponsor to hold at least 25% of the total units of the REIT prior to initial offer

� Lock-in of 3 years on minimum holding & 1 year on holding in excess of 25%

� Sponsor to hold 15% of the outstanding units at all times

� Holding can go below 15% after lock-in of 3 years

� Sponsor to arrange re-designated sponsor & obtain approval of the unit-holder

Real estate investment trust (REIT) - basics

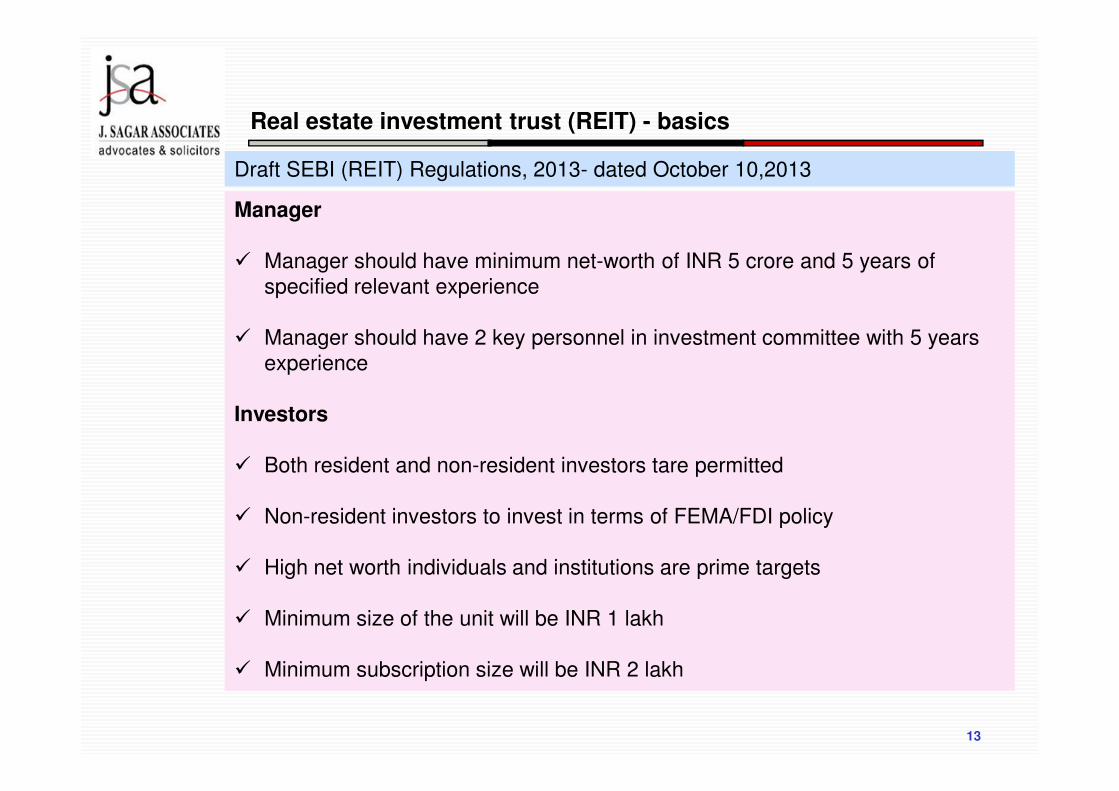

Manager

� Manager should have minimum net-worth of INR 5 crore and 5 years of

specified relevant experience

� Manager should have 2 key personnel in investment committee with 5 years

experience

Draft SEBI (REIT) Regulations, 2013- dated October 10,2013

13

Investors

� Both resident and non-resident investors tare permitted

� Non-resident investors to invest in terms of FEMA/FDI policy

� High net worth individuals and institutions are prime targets

� Minimum size of the unit will be INR 1 lakh

� Minimum subscription size will be INR 2 lakh

InvIT – basics

14

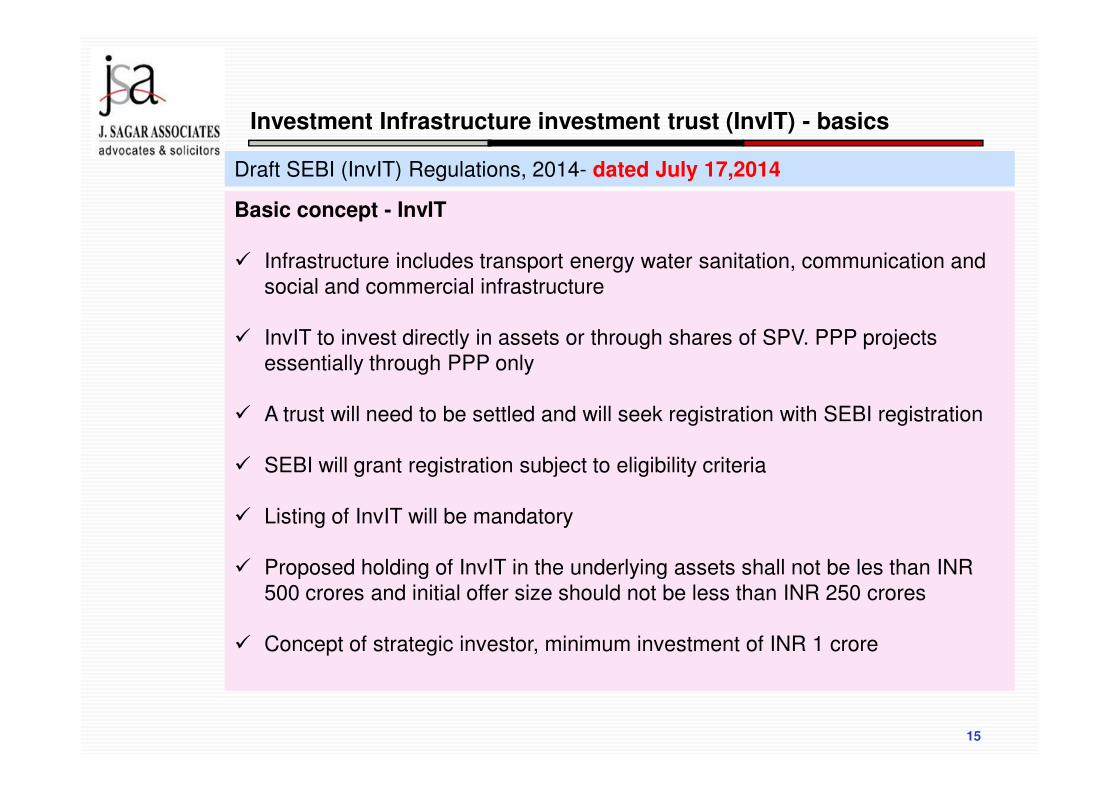

Investment Infrastructure investment trust (InvIT) - basics

Basic concept - InvIT

� Infrastructure includes transport energy water sanitation, communication and

social and commercial infrastructure

� InvIT to invest directly in assets or through shares of SPV. PPP projects

essentially through PPP only

Draft SEBI (InvIT) Regulations, 2014- dated July 17,2014

15

� A trust will need to be settled and will seek registration with SEBI registration

� SEBI will grant registration subject to eligibility criteria

� Listing of InvIT will be mandatory

� Proposed holding of InvIT in the underlying assets shall not be les than INR

500 crores and initial offer size should not be less than INR 250 crores

� Concept of strategic investor, minimum investment of INR 1 crore

Tax regime for Business

trust – REIT and InvIT

16

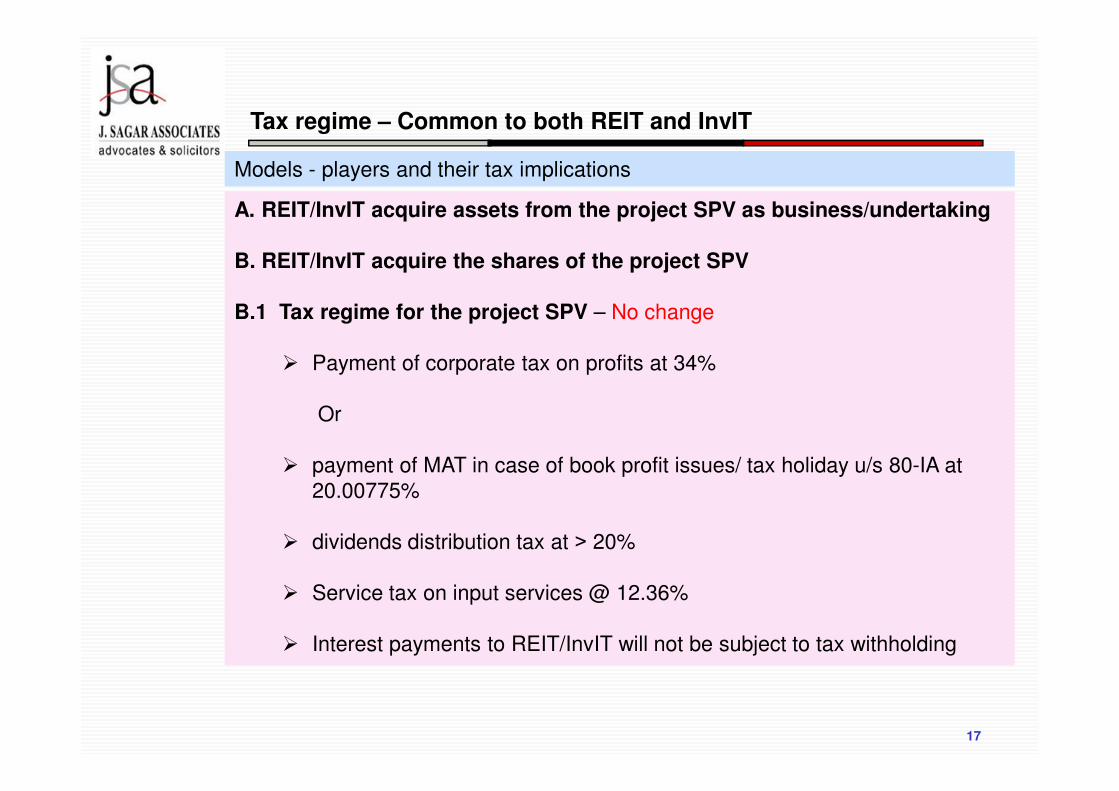

Tax regime – Common to both REIT and InvIT

A. REIT/InvIT acquire assets from the project SPV as business/undertaking

B. REIT/InvIT acquire the shares of the project SPV

B.1 Tax regime for the project SPV – No change

� Payment of corporate tax on profits at 34%

Models - players and their tax implications

17

Or

� payment of MAT in case of book profit issues/ tax holiday u/s 80-IA at

20.00775%

� dividends distribution tax at ˃ 20%

� Service tax on input services @ 12.36%

� Interest payments to REIT/InvIT will not be subject to tax withholding

Tax regime – Common to both REIT and InvIT

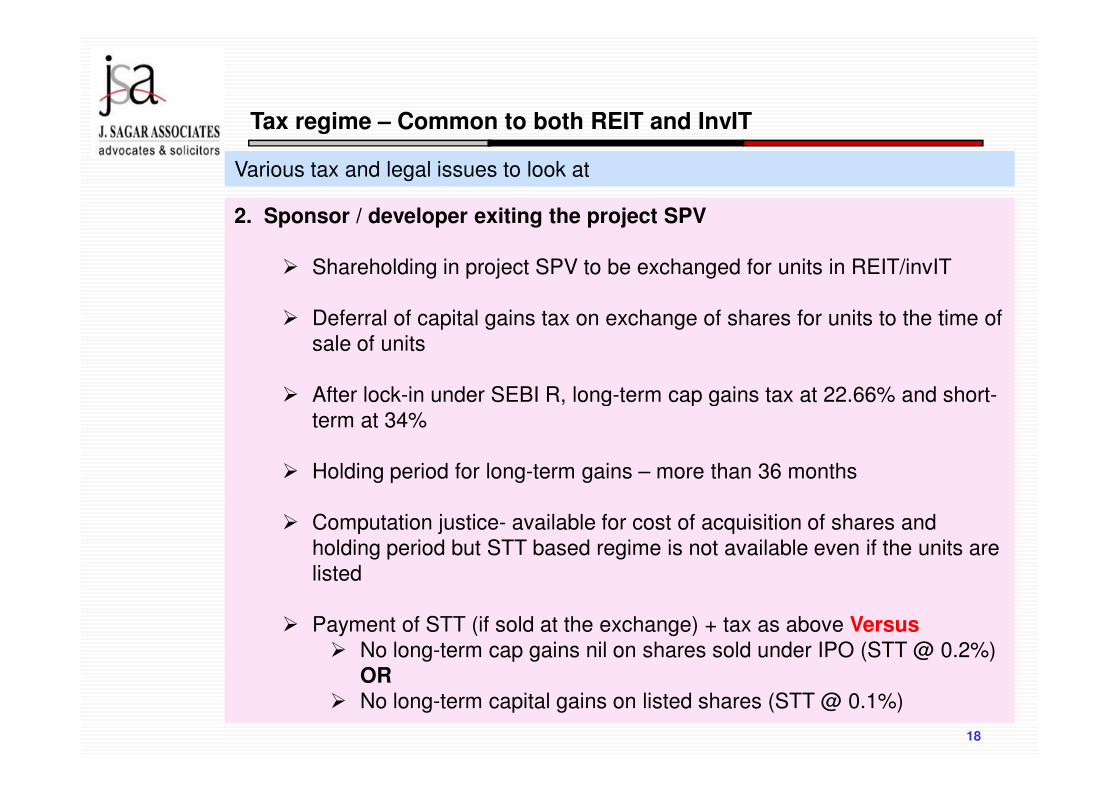

2. Sponsor / developer exiting the project SPV

� Shareholding in project SPV to be exchanged for units in REIT/invIT

� Deferral of capital gains tax on exchange of shares for units to the time of

sale of units

� After lock-in under SEBI R, long-term cap gains tax at 22.66% and short-

Various tax and legal issues to look at

18

� After lock-in under SEBI R, long-term cap gains tax at 22.66% and short-

term at 34%

� Holding period for long-term gains – more than 36 months

� Computation justice- available for cost of acquisition of shares and

holding period but STT based regime is not available even if the units are

listed

� Payment of STT (if sold at the exchange) + tax as above Versus� No long-term cap gains nil on shares sold under IPO (STT @ 0.2%)

OR� No long-term capital gains on listed shares (STT @ 0.1%)

Tax regime – Common to both REIT and InvIT

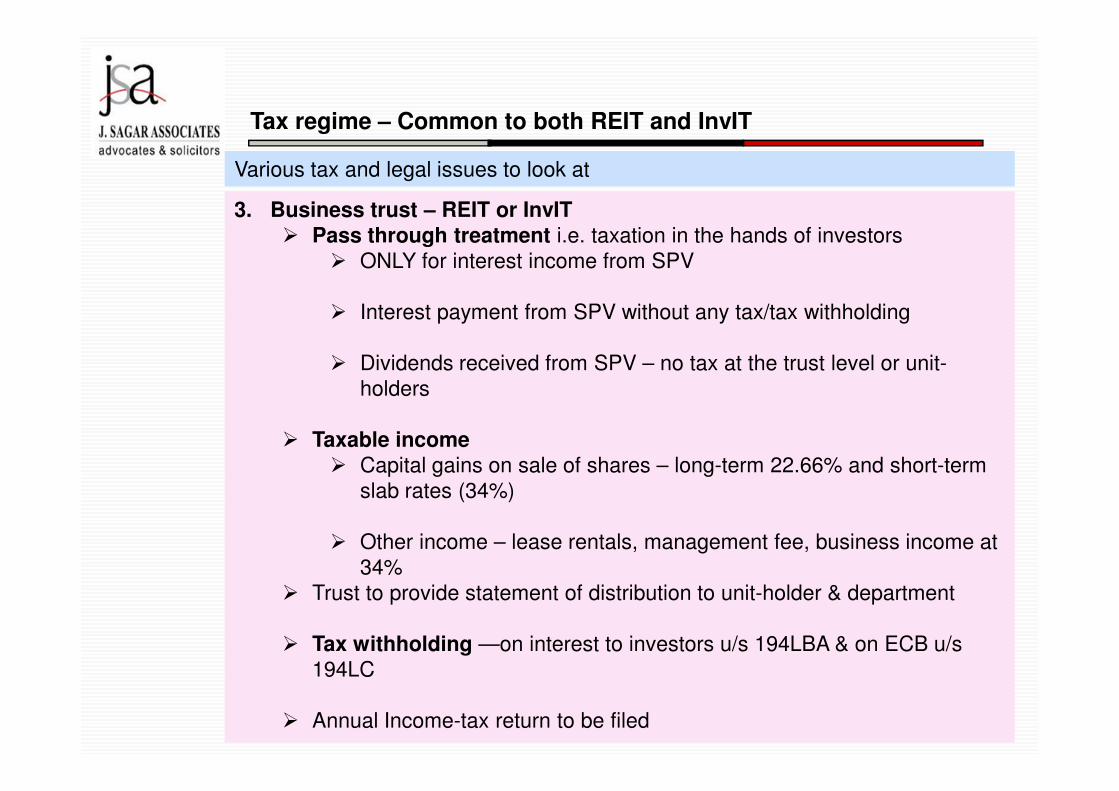

3. Business trust – REIT or InvIT� Pass through treatment i.e. taxation in the hands of investors

� ONLY for interest income from SPV

� Interest payment from SPV without any tax/tax withholding

� Dividends received from SPV – no tax at the trust level or unit-

holders

Various tax and legal issues to look at

19

holders

� Taxable income � Capital gains on sale of shares – long-term 22.66% and short-term

slab rates (34%)

� Other income – lease rentals, management fee, business income at

34%

� Trust to provide statement of distribution to unit-holder & department

� Tax withholding —on interest to investors u/s 194LBA & on ECB u/s

194LC

� Annual Income-tax return to be filed

Tax regime – Common to both REIT and InvIT

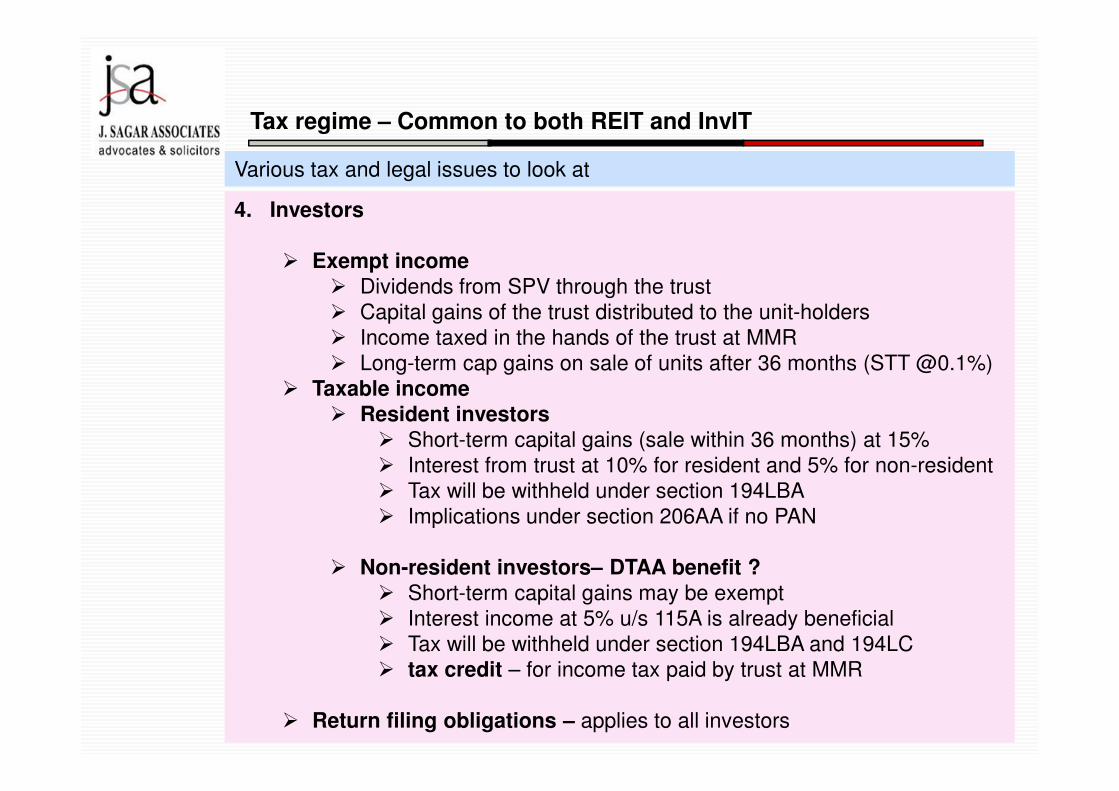

4. Investors

� Exempt income� Dividends from SPV through the trust

� Capital gains of the trust distributed to the unit-holders

� Income taxed in the hands of the trust at MMR

� Long-term cap gains on sale of units after 36 months (STT @0.1%)

� Taxable income

Various tax and legal issues to look at

20

� Taxable income� Resident investors

� Short-term capital gains (sale within 36 months) at 15%

� Interest from trust at 10% for resident and 5% for non-resident

� Tax will be withheld under section 194LBA

� Implications under section 206AA if no PAN

� Non-resident investors– DTAA benefit ?� Short-term capital gains may be exempt

� Interest income at 5% u/s 115A is already beneficial

� Tax will be withheld under section 194LBA and 194LC

� tax credit – for income tax paid by trust at MMR

� Return filing obligations – applies to all investors

Tax regime – Common to both REIT and InvIT

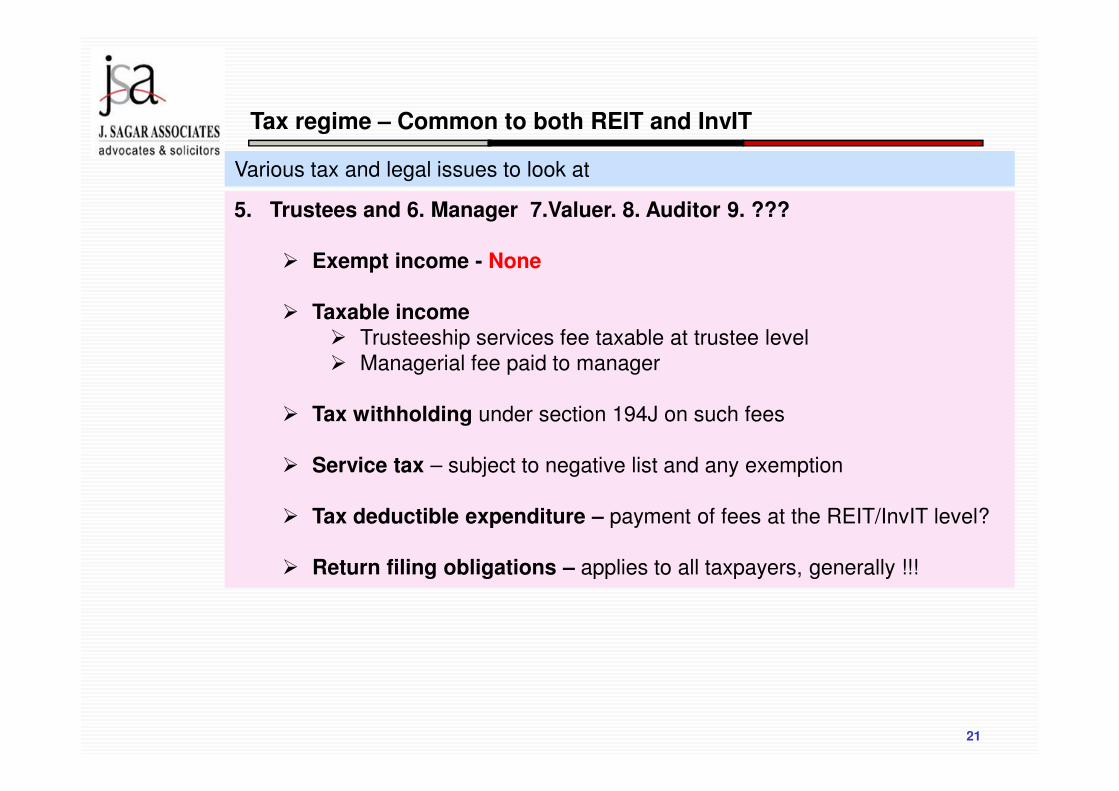

5. Trustees and 6. Manager 7.Valuer. 8. Auditor 9. ???

� Exempt income - None

� Taxable income� Trusteeship services fee taxable at trustee level

� Managerial fee paid to manager

Various tax and legal issues to look at

21

� Tax withholding under section 194J on such fees

� Service tax – subject to negative list and any exemption

� Tax deductible expenditure – payment of fees at the REIT/InvIT level?

� Return filing obligations – applies to all taxpayers, generally !!!

ISSUES – those that will need to be addressed

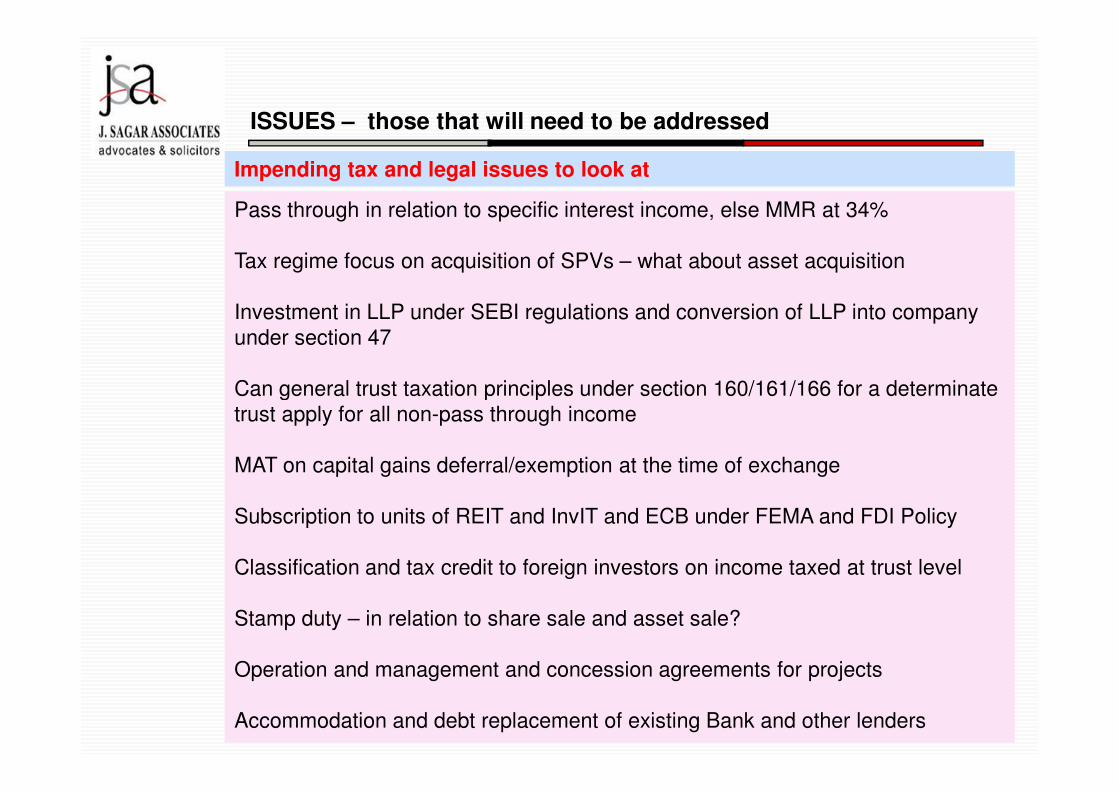

Pass through in relation to specific interest income, else MMR at 34%

Tax regime focus on acquisition of SPVs – what about asset acquisition

Investment in LLP under SEBI regulations and conversion of LLP into company

under section 47

Can general trust taxation principles under section 160/161/166 for a determinate

Impending tax and legal issues to look at

22

Can general trust taxation principles under section 160/161/166 for a determinate

trust apply for all non-pass through income

MAT on capital gains deferral/exemption at the time of exchange

Subscription to units of REIT and InvIT and ECB under FEMA and FDI Policy

Classification and tax credit to foreign investors on income taxed at trust level

Stamp duty – in relation to share sale and asset sale?

Operation and management and concession agreements for projects

Accommodation and debt replacement of existing Bank and other lenders

PONDERABLES – to be deliberated

What is the problem today?

What does the developer do? asset sale/share sale?

Problems and solutions

23

What is the driving factor for the investor?

Whether target rate of return matches with post-tax yields?

THANK YOU

24