Embed Size (px)

Citation preview

Reinsurance for Asset-Liability Management

6 Sep 2016

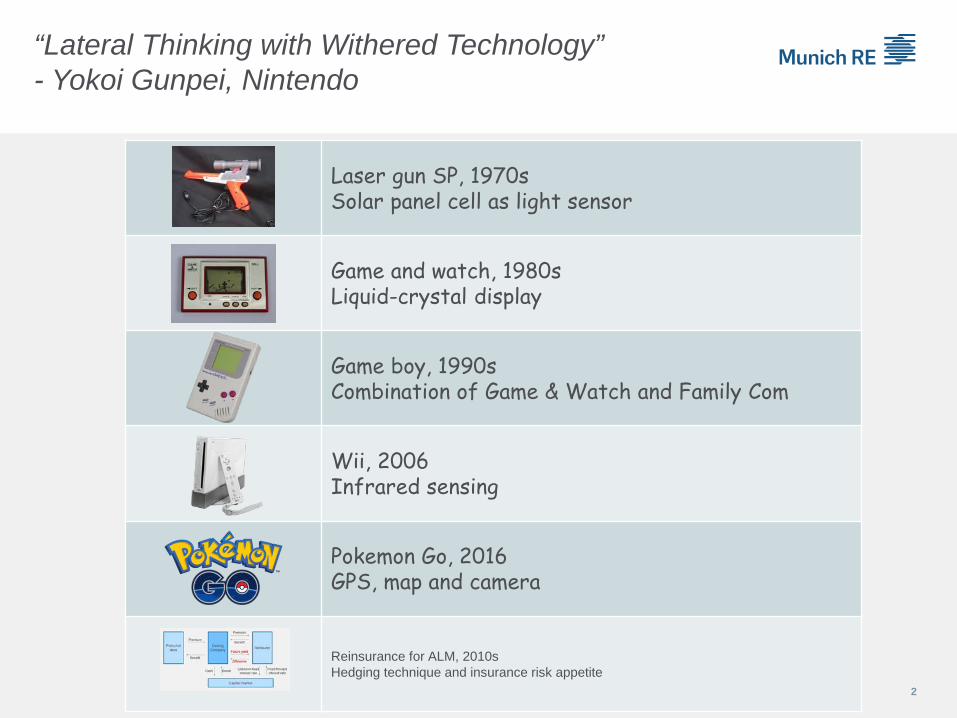

Laser gun SP, 1970sSolar panel cell as light sensor

Game and watch, 1980sLiquid-crystal display

Game boy, 1990sCombination of Game & Watch and Family Com

Wii, 2006Infrared sensing

Pokemon Go, 2016GPS, map and camera

Reinsurance for ALM, 2010sHedging technique and insurance risk appetite

“Lateral Thinking with Withered Technology”- Yokoi Gunpei, Nintendo

2

Problem 1: Forward starting swap embedded in regular premium products

0 1 2 3 4 5 6 7 8 9 10Cashflow 90 90 90 90 90 90 90 90 90 90 -1,000Net liability value @ 2% -0 91 184 279 376 475 576 679 784 891 1,000Net liability value @ 1% 49 140 232 324 418 513 608 705 802 901 1,000Implied duration 52.97 25.51 16.02 11.04 7.85 5.56 3.78 2.33 1.09

-200

-

200

400

600

800

1,000

1,200

-1,200

-1,000

-800

-600

-400

-200

-

200

10Y Regular Premium Endowment, no lapse, no mortality

Forward starting interest rate positions

Translate to a high liability duration

It is also reinvestment problem

3

Problem 2: Swaption position if dynamic lapse is concerned

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20Shortfall between SV and MV 322 295 266 237 207 175 142 108 72 35 96 67 36 4 - - - - - - -Surrender value 1,0001,0001,0001,0001,0001,0001,0001,0001,0001,0001,1001,1111,1221,1331,1451,1561,1681,1791,1911,2031,215Asset value (Book value 2% yield) 1,0001,0201,0401,0611,0821,1041,1261,1491,1721,1951,2191,2431,2681,2941,3191,3461,3731,4001,4281,4571,486Asset value (Market value 4% yield) 678 705 734 763 793 825 858 892 928 965 1,0041,0441,0861,1291,1741,2211,2701,3211,3741,4291,486

-

200

400

600

800

1,000

1,200

1,400

1,600

-

200

400

600

800

1,000

1,200

1,400

1,600

Single Premium Whole Life with Surrender Value guaranteed

Shortfall between SV and MV Surrender value Asset value (Book value 2% yield) Asset value (Market value 4% yield)

Assumptions•Single Premium Whole Life with surrender value jumps at the end of year 10

•Liability duration calculated based on flat lapse

•Asset is zero coupon bond with duration same as liability

Loss if interest rate rises; will lapse be higher at higher interest rate?New DST?

4

Problem 3: Invest into cross currencies swap

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

%

10Y AUD Government Bond yield JGB repackaged AUD yield

• Instead of investing directly into e.g. AUD bonds, it is possible to invest into bonds in a different currency e.g. JGB, and use cross currency swaps to generate the return in the required currency

• Under perfect world assumptions, the two returns are the same

• However, due to different credit risks of governments, demand and supply of derivatives for hedging etc, the two investment yields are not the same, and hence the possibilities of “pickup”

• Investing into cross currency swaps directly however causes accounting mismatchAsset: market valueLiability: book valueSource: Bloomberg 5

Underlying Economics of Modco (Coinsurance fund withheld)

Ceding Company Reinsurer

Premium

Increase in reserve

In very short: Coinsurance but assets remains at cedant

Claims

Release of reserve

Modco rate * reserve

Increase in reserve (Reserving interest

rate part)

This is economically an interest rate swap embedded in (re)insurance:• If modco rate = reserving

interest rate, no investment risk transfer

• If modco rate = actual investment yield, investment risk transfer to reinsurer 6

Reinsurance solution for problem 1

Ceding Company ReinsurerPolicyhol

ders

Capital market

Premium

Benefit

Cash Bonds Fixed forward interest rate

Unknown fixed interest rate

Premium

Benefit

Future yield

ΔReserve

TInt rate

1Int rate

2Int rate

3Int rate

4Int rate

5Int rate

6Int rate

7Int rate

8Int rate

9Int rate

10 Reserve PremiumInvestment

incomeChange in

reserve ClaimP&L before reinsurance RI CFs

P&L after reinsurance

0 0.00 1 2.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 91.33 89.54 1.79 91.33 0.00 0.00 -0.00 -0.00 2 2.0% 1.5% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 184.48 89.54 3.17 93.15 0.00 -0.45 0.45 -0.00 3 2.0% 1.5% 1.5% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 279.50 89.54 4.57 95.02 0.00 -0.91 0.91 -0.00 4 2.0% 1.5% 1.5% 3.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 376.41 89.54 7.33 96.92 0.00 -0.05 0.05 -0.00 5 2.0% 1.5% 1.5% 3.0% 1.0% 0.0% 0.0% 0.0% 0.0% 0.0% 475.27 89.54 8.39 98.85 0.00 -0.93 0.93 -0.00 6 2.0% 1.5% 1.5% 3.0% 1.0% 1.5% 0.0% 0.0% 0.0% 0.0% 576.10 89.54 9.90 100.83 0.00 -1.39 1.39 -0.00 7 2.0% 1.5% 1.5% 3.0% 1.0% 1.5% 1.8% 0.0% 0.0% 0.0% 678.95 89.54 11.71 102.85 0.00 -1.60 1.60 0.00 8 2.0% 1.5% 1.5% 3.0% 1.0% 1.5% 1.8% 2.2% 0.0% 0.0% 783.85 89.54 13.91 104.91 0.00 -1.46 1.46 0.00 9 2.0% 1.5% 1.5% 3.0% 1.0% 1.5% 1.8% 2.2% 2.0% 0.0% 890.86 89.54 15.98 107.00 0.00 -1.49 1.49 0.00 10 2.0% 1.5% 1.5% 3.0% 1.0% 1.5% 1.8% 2.2% 2.0% 3.0% 1,000.00 89.54 18.99 -890.86 1,000.00 -0.62 0.62 0.00

7

Reinsurance solution for problem 2 and 3

Ceding Company Reinsurer

Premium

Benefit

Modco rate

ΔReserveSwaptions or

swaps

Problem Asset hold by Cedant

Return credited to Reinsurer

Investment risks transferred to reinsurer

Hedging instruments run by reinsuer

2 Bonds Coupon + capital loss of bonds on mass lapse

Asset loss at mass lapse

Swaption

3 JGB JGB coupon Cross currency risks

Cross currency swaps

8

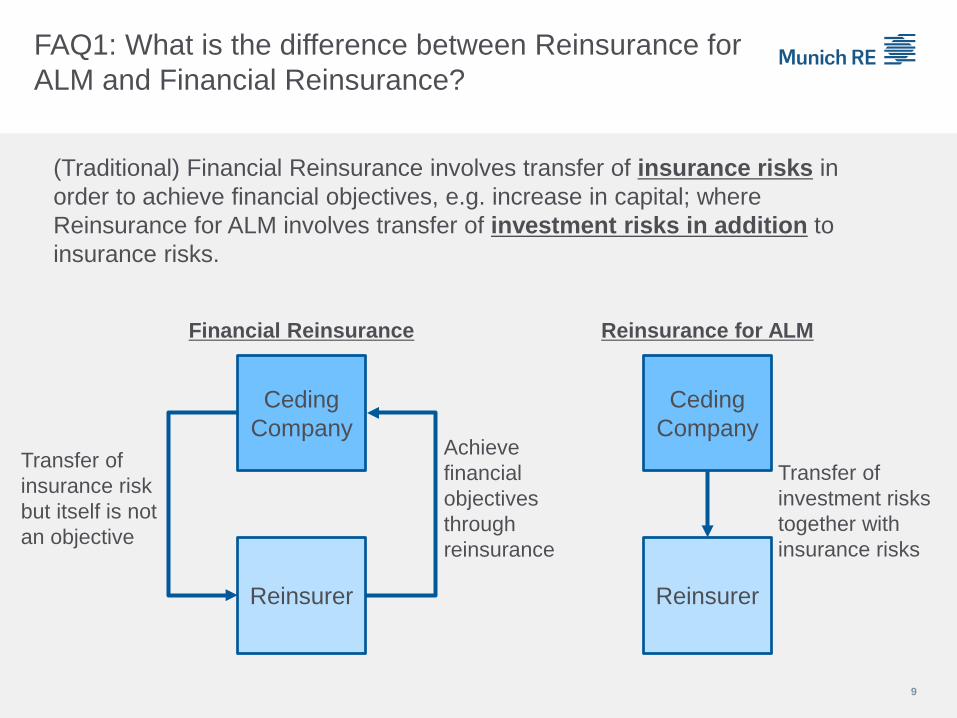

FAQ1: What is the difference between Reinsurance for ALM and Financial Reinsurance?

(Traditional) Financial Reinsurance involves transfer of insurance risks in order to achieve financial objectives, e.g. increase in capital; where Reinsurance for ALM involves transfer of investment risks in addition toinsurance risks.

Ceding Company

Reinsurer

Financial Reinsurance

Transfer of insurance risk but itself is not an objective

Achieve financial objectives through reinsurance

Ceding Company

Reinsurer

Reinsurance for ALM

Transfer of investment risks together with insurance risks

9

FAQ2: Why should I use reinsurance rather than derivatives

Pros Cons

Reinsurance • Better accounting treatment if reinsurance accounting applies

• Can use insurance profit to subsidize hedge cost

• Less operational burden• Diversification of hedge

counterparty through reinsurance

• More holistic; can achieve multiple objectives at the same time

• Conceptually more complicated

• Scrutiny by auditors and regulators possible

• Need of transfer of insurance risks

Derivatives • More freedom in choosing risks to take or hedge

• Hedge accounting not easy or even not possible

• Heavy operational and compliance burden for running derivatives 10

FAQ3: Is reinsurance more expensive than derivatives?

• No, definitely not• If reinsurer uses derivatives for hedging, the cost of production for this part is

fully market consistent• Insurance risk transfer has a cost but reinsurer can be a more efficient risk

taker due to global diversification

Diversifiable risks

Hedge-able risks

Systemic non-

hedgeable

Risk chargeMarket con-sistent cost Exclude

Reinsurance cost11

Hugo Choi, FSA, FRM, CFAHead of Financial Solutions Asia

Business Development DepartmentMunich Re Tokyo Life Branch

+81 (0)3 [email protected]

Thank you!Now your questions!

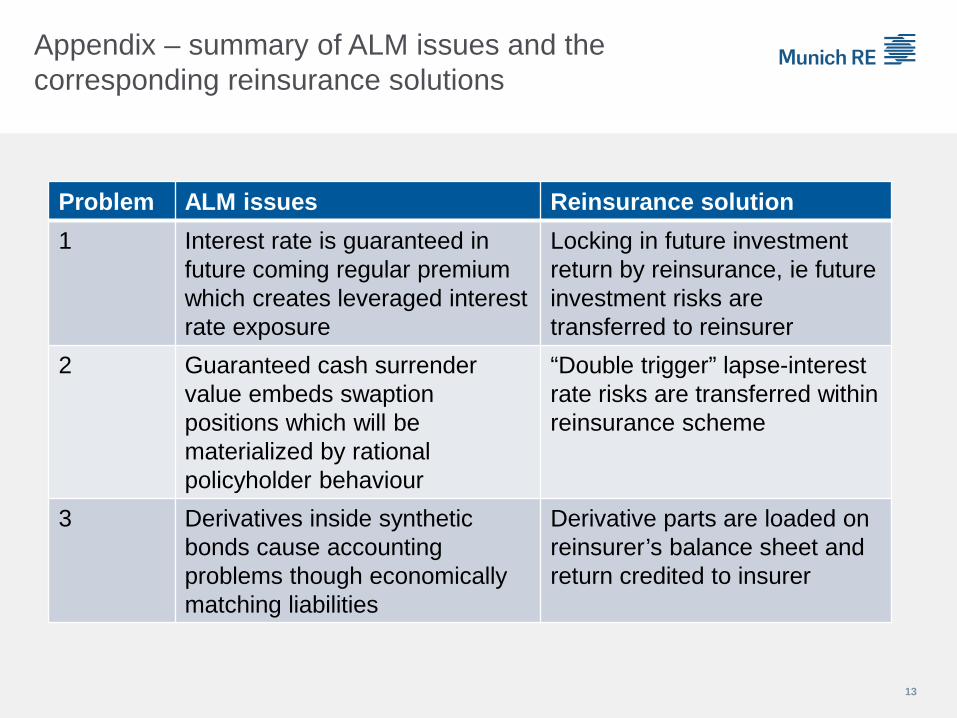

Appendix – summary of ALM issues and the corresponding reinsurance solutions

Problem ALM issues Reinsurance solution1 Interest rate is guaranteed in

future coming regular premium which creates leveraged interest rate exposure

Locking in future investment return by reinsurance, ie future investment risks are transferred to reinsurer

2 Guaranteed cash surrender value embeds swaptionpositions which will be materialized by rational policyholder behaviour

“Double trigger” lapse-interest rate risks are transferred within reinsurance scheme

3 Derivatives inside synthetic bonds cause accounting problems though economically matching liabilities

Derivative parts are loaded on reinsurer’s balance sheet and return credited to insurer

13