Embed Size (px)

Citation preview

Regulatory Obligations of Money Services Businesses in the Caribbean

Contents Company Background

Legislative Background

How FATF Guidelines have affected the remittanceindustry

The Money Service Business (MSB) Model and how itdiffers from other traditional industry players

Challenges to the Money Services Business (MSB) and its’ customers

Company Background

GraceKennedy Money Services (GKMS) is a subsidiary of GraceKennedy Ltd.

GKMS has managed the Western Union brand for the past 20 years

Now manages this business in eight (8) Caribbean territories

Company also owns and operates cambio(FxTrader) and bill payment (Bill Express) businesses

Where We Are

The MSB Landscape

Transaction-based financial services: remittances, bill payment, cheque-cashing, foreign exchange etc.

Informal community-based outlets

Agency model, engaging independent agents to provide services on behalf of a master agent

Many money services are also offered by traditionalfinancial institutions as value-added services

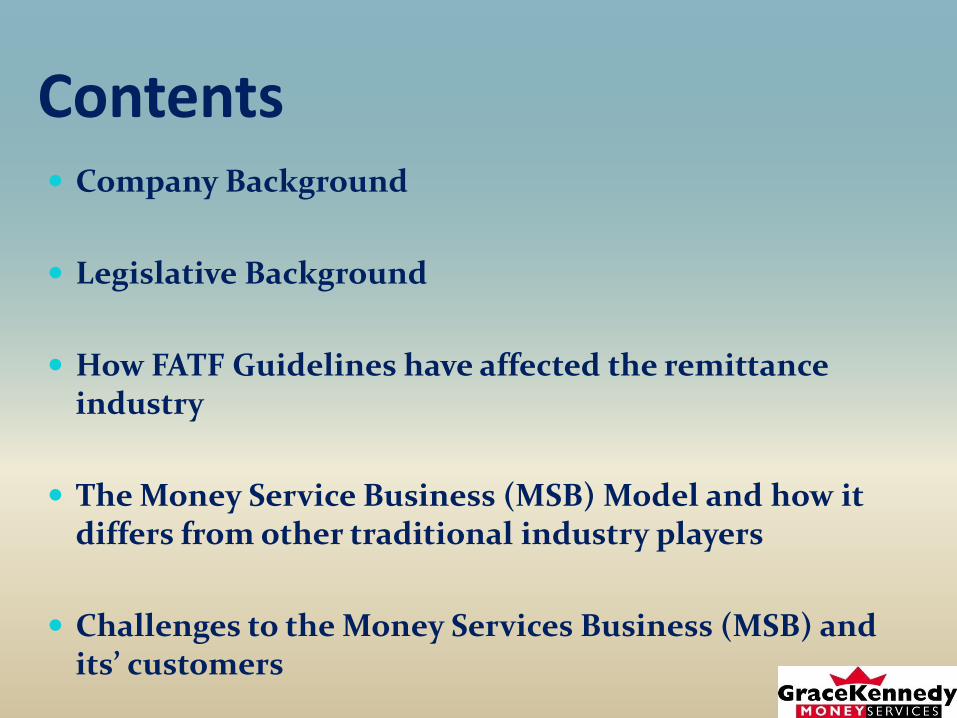

Legislative Background In 1990 the Financial Action Task Force (FATF) released 40

recommendations to challenge money laundering (and another 9 after 9/11 which focused on terrorism)

Regional legislation is largely based on this FATF Guidance

FATF Standards stipulate:

Criminalisation of Money Laundering – Rec 1

Customer Due Diligence (KYC) – Rec 5

Record-keeping – Rec 10

Reporting of suspicious transactions – 13

Internal Policies and Procedures (Training, internalcontrols, audit) – Rec 15

Transaction Monitoring and Reporting – Rec 11

How have these stipulations affectedthe Remittance Industry throughout

the region?

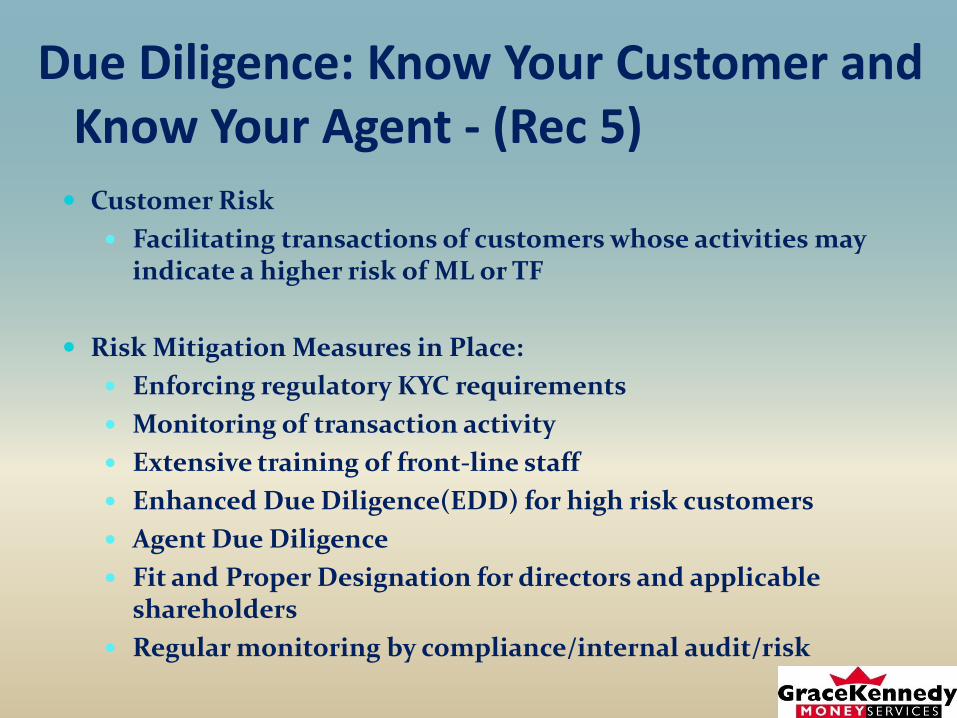

Due Diligence: Know Your Customer and Know Your Agent - (Rec 5) Customer Risk

Facilitating transactions of customers whose activities mayindicate a higher risk of ML or TF

Risk Mitigation Measures in Place:

Enforcing regulatory KYC requirements

Monitoring of transaction activity

Extensive training of front-line staff

Enhanced Due Diligence(EDD) for high risk customers

Agent Due Diligence

Fit and Proper Designation for directors and applicable shareholders

Regular monitoring by compliance/internal audit/risk

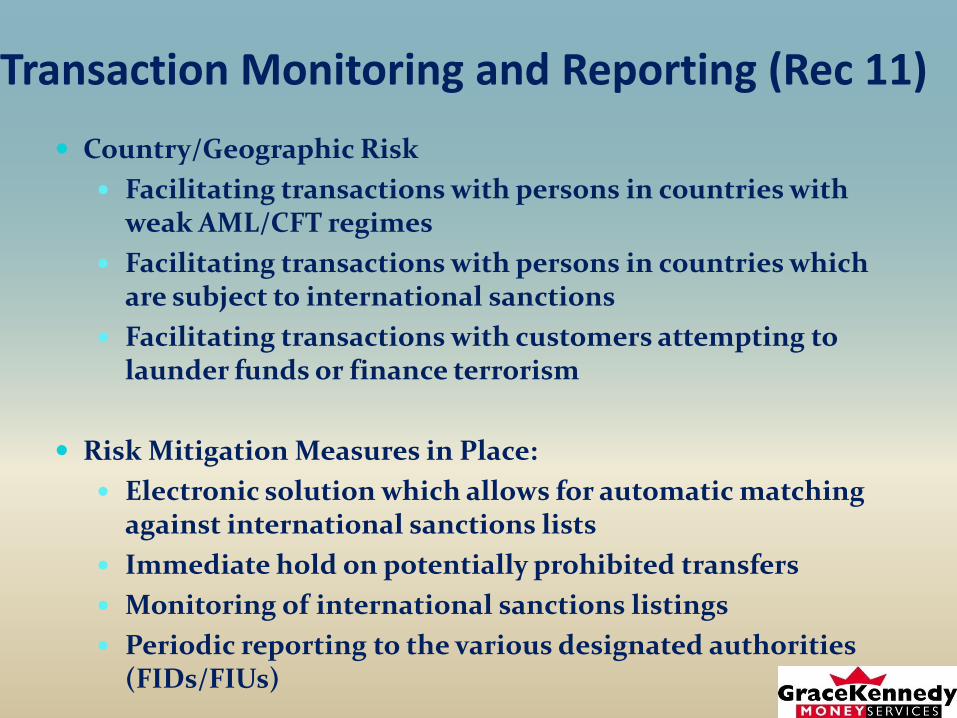

Transaction Monitoring and Reporting (Rec 11)

Country/Geographic Risk

Facilitating transactions with persons in countries with weak AML/CFT regimes

Facilitating transactions with persons in countries whichare subject to international sanctions

Facilitating transactions with customers attempting to launder funds or finance terrorism

Risk Mitigation Measures in Place:

Electronic solution which allows for automatic matchingagainst international sanctions lists

Immediate hold on potentially prohibited transfers

Monitoring of international sanctions listings

Periodic reporting to the various designated authorities(FIDs/FIUs)

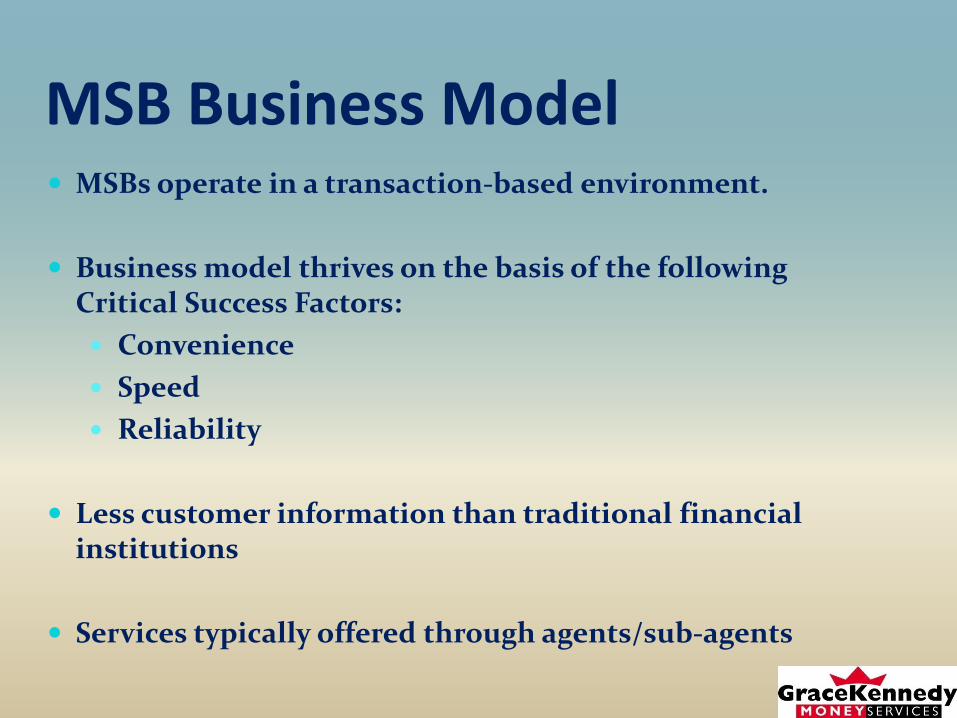

MSB Business Model MSBs operate in a transaction-based environment.

Business model thrives on the basis of the followingCritical Success Factors:

Convenience

Speed

Reliability

Less customer information than traditional financialinstitutions

Services typically offered through agents/sub-agents

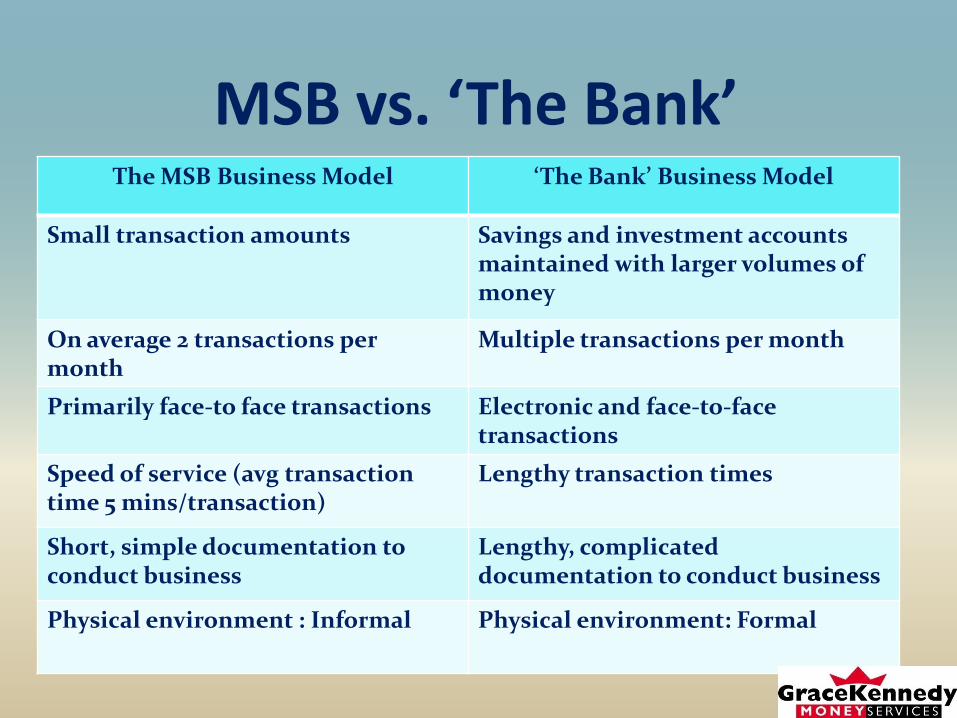

MSB vs. ‘The Bank’ The MSB Business Model ‘The Bank’ Business Model

Small transaction amounts Savings and investment accounts maintained with larger volumes of money

On average 2 transactions per month

Multiple transactions per month

Primarily face-to face transactions Electronic and face-to-face transactions

Speed of service (avg transaction time 5 mins/transaction)

Lengthy transaction times

Short, simple documentation to conduct business

Lengthy, complicated documentation to conduct business

Physical environment : Informal Physical environment: Formal

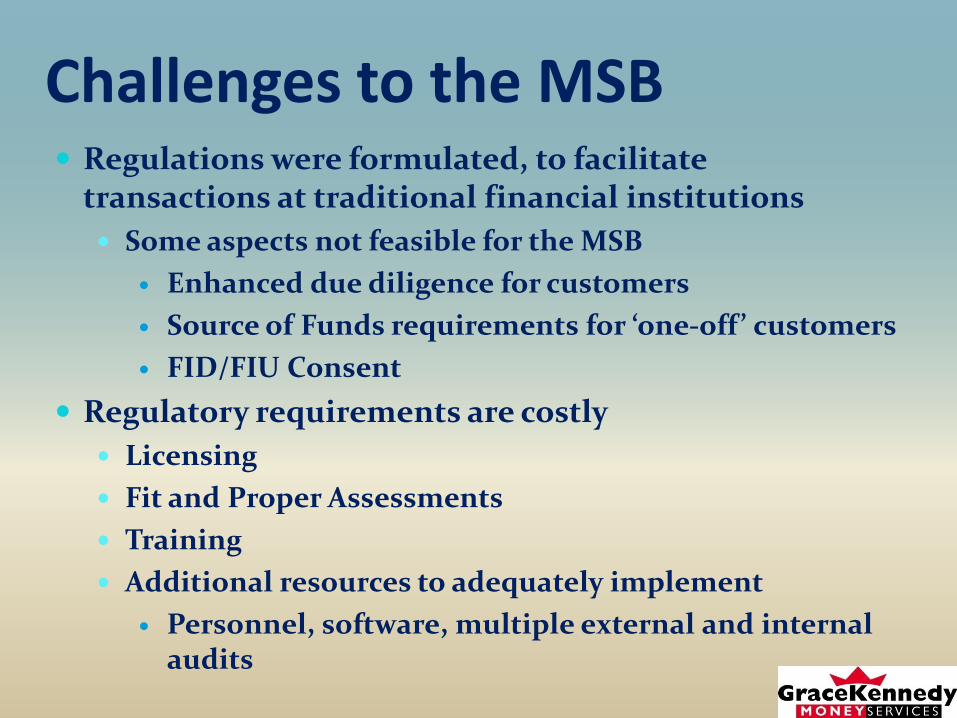

Challenges to the MSB Regulations were formulated, to facilitate

transactions at traditional financial institutions

Some aspects not feasible for the MSB

Enhanced due diligence for customers

Source of Funds requirements for ‘one-off’ customers

FID/FIU Consent

Regulatory requirements are costly

Licensing

Fit and Proper Assessments

Training

Additional resources to adequately implement

Personnel, software, multiple external and internalaudits

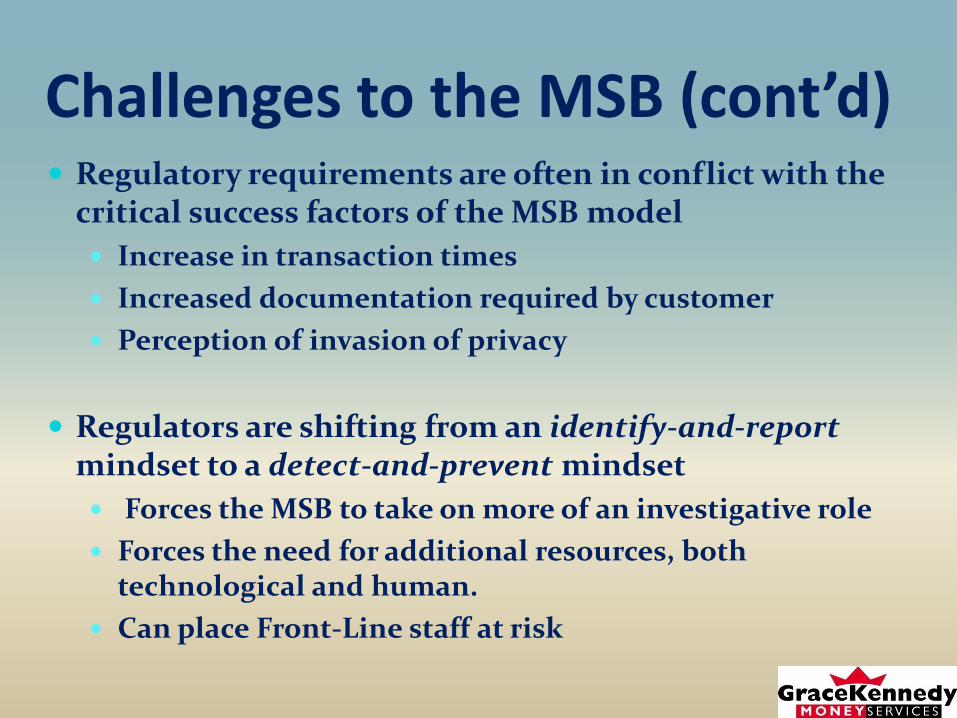

Challenges to the MSB (cont’d) Regulatory requirements are often in conflict with the

critical success factors of the MSB model

Increase in transaction times

Increased documentation required by customer

Perception of invasion of privacy

Regulators are shifting from an identify-and-reportmindset to a detect-and-prevent mindset

Forces the MSB to take on more of an investigative role

Forces the need for additional resources, both technological and human.

Can place Front-Line staff at risk

Challenges to the MSB (cont’d) Perception of MSBs as high risk

Has made banks hesitant about accepting MSB accounts

Increase in monitoring (increased audits, visits etc)

Lack of consistency across the industry

Creates a competitive advantage for companies with weaker standards

Lack of Public Education Campaign by the Regulatory Bodies

Hence customers blame the MSB

Customer confusion about what is regulatory and what is company policy.

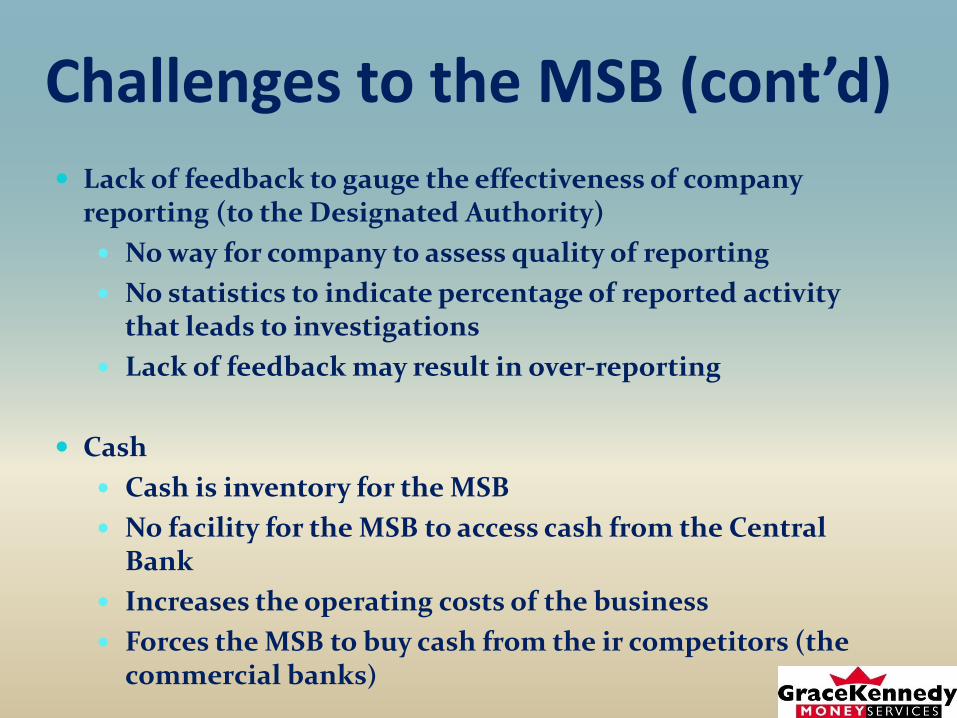

Challenges to the MSB (cont’d)

Lack of feedback to gauge the effectiveness of company reporting (to the Designated Authority)

No way for company to assess quality of reporting

No statistics to indicate percentage of reported activity that leads to investigations

Lack of feedback may result in over-reporting

Cash

Cash is inventory for the MSB

No facility for the MSB to access cash from the Central Bank

Increases the operating costs of the business

Forces the MSB to buy cash from the ir competitors (the commercial banks)

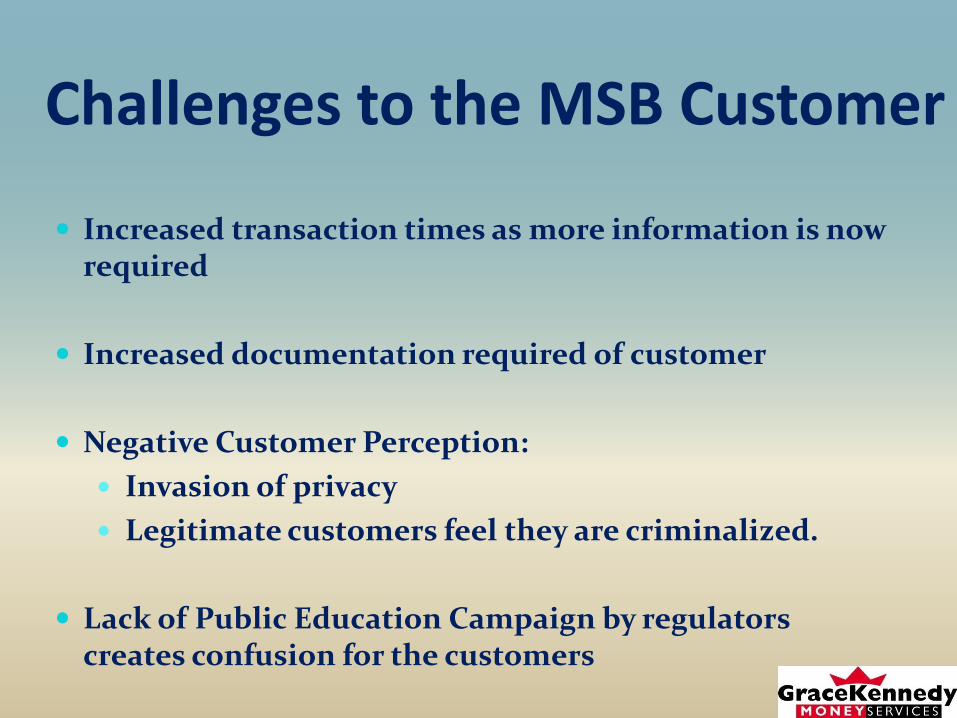

Challenges to the MSB Customer

Increased transaction times as more information is nowrequired

Increased documentation required of customer

Negative Customer Perception:

Invasion of privacy

Legitimate customers feel they are criminalized.

Lack of Public Education Campaign by regulatorscreates confusion for the customers

Summary Today, MSBs maintain robust programmes to ensure

compliance

Remaining compliant with regulatory requirements is costly:

Human resources

Time consuming

Technological requirements

Regulatory fees (licencing, Fit and Proper Assessments etc)

Negative perception of the MSB by other players in the sector

There is a lack of customer education by the regulatorsthroughout the region