Embed Size (px)

Citation preview

September 2014Regulatory Intelligence GroupFor private circulation [email protected]

Regulatory Impact AssessmentBanking

2

Contents

Preface Report of the Committee to Review Governance of Boards of Banks in India - Initiative long overdueOur point of view on key RBI guidelines issued in July 2014Other guidelines issued by RBI during the monthContacts

2

3

571519

Regulatory Impact Assessment | 3

Preface

After the formation of new government at the center, we have seen increased collaboration between RBI and finance ministry to stimulate growth in the economy . In his maiden budget speech, Finance Minister Arun Jaitley stressed on a modern monetary policy framework which the RBI would develop in consultation with the Central Government. Apart from this, they are also working towards the common goals of financial inclusion and increasing the presence and competency of Indian banks at a global level. However, it is imperative that they first remove the lacunas existing in the banking sector to ensure a smooth and effective implementation of these developmental and growth objectives.

One of the major hindrances in achieving the above objectives are the lack of governance focus prevalent in the banking sector, especially the public sector banks. While their performance has improved marginally in the last quarter, the PSU banks are still facing the pressure of increasing NPAs due to fresh slippages, high expenses and inadequate provisioning, which has led to stressed balance sheets. The recent arrest of the MD of a well-known public sector bank has again brought to light the governance weaknesses existing in the PSU banks. Despite being one of the most heavily regulated banking sectors in the world, such glaring issues necessitate the need to take a step back and contemplate on what changes are required in the present scheme of things to facilitate a better governance model in the banking sector before implementing any other initiatives within the banking domain.

The PJ Nayak Committee Report on Governance of Board of Banks in India, which was issued in May 2014, attempts to address the root causes of a deficient bank governance framework. The committee has adopted a two tier approach, addressing issues faced by the public sector and the private sector separately. In the latter part of this issue, we have highlighted some of the important recommendations made by the PJ Nayak committee along with our perspective on the same. We trust that you would find the same useful.

On the regulatory front, the master circulars for 2014-15 were released on July 1, 2014. Apart from this, some guidelines were issued to support the Government’s agenda of reviving the stagnating economy while some notifications were introduced in order to simplify the regulatory reporting requirements. Additionally, in line with the budget, the RBI issued guidelines for stimu-lating growth in the infrastructure sector.

With the economy picking up steam and the monsoon deficit shrinking, Indian economy is poised to benefit from the measures taken by the new Government. The sliding crude prices are also benefitting the govern-ment. With all major economic indicators supporting government in its objective of stimulating growth, it needs to be seen as to how RBI is going to manage the growth inflation dynamics in the coming quarters, given the stickiness of the food inflation due to supply side bottlenecks.

4

Report of the Committee to Review Governance of Boards of Banks in India - Initiative long overdue

Regulatory Impact Assessment | 5

Report of the Committee to Review Governance of Boards of Banks in India - Initiative long overdueThe Indian financial system has always placed the Banks at the top of the pyramid with its key roles being focused on maturity transformation and liquidity gener-ation. Although the Banking system has definitely played this role, it has not been effective in meeting the myriad needs of the economy in an efficient and effective manner, exposing the financial system to the risk of instability. Given the fiduciary nature of Banking, the aspect of governance assumes paramount importance, especially to ensure stability, and this was the reason, why the Committee to Review Governance of Boards of Banks in India was constituted under the chairmanship of the seasoned Banker, Mr.P.J.Nayak on January 20, 2014. The two tier structure of the scheduled commer-cial banking structure in India – Public Sector Banks and Private Sector Banks – though necessary from a develop-mental standpoint, has resulted into much inefficiency on account of the differential governance schema within which, the Public Sector Banks and the Private Sector Banks operate. The Public Sector Banks are subject to excessive interference• From the regulator - by way of differential regula-

tions. Regulations have been issued separately for public sector banks

• From the government – to meet the government driven development objectives

• From the Central Vigilance Department – with a focus towards penalization for lack of following procedure, irrespective of the intent, thereby impairing their ability to take commercially viable and prudent decisions in a time bound manner

While the Private Sector Banks do not suffer from the aforesaid restrictions, there is definitely an issue of moral hazard which drives their deficiencies in the governance framework.

The committee recognized the above issues and came out with multiple regulations to address these challenges to help move towards a stronger governance model, thereby promoting financial stability. The recommen-dations that are addressed towards Public Sector Banks mainly cover the following themes:• Diluting the stake of the government through the

creation of a Banking Investment Company Model, with the role of the government eventually reduced to that of an investor with a focus on returns and the Banking Investment Company serving as a passive

sovereign wealth fund for the government• Creating an Authorized Bank Investors framework

with defined exposure concentration norms, to ensure funding for the aforementioned Banking divestment program

• Facilitate a re-capitalization framework for the distressed Banks by allowing for private equity exposure, including sovereign wealth funds, with a controlling stake being allowed up to a maximum of 40 percent

• Eliminating the conflict of interests existent within the current operating model for the Public Sector Banks by revising the requirements around Board composition, appointment of key management personnel, inde-pendence requirements for non-executive directors and proportionate voting rights

While the recommendations for the private sector Banks also include the requirements around elimination of conflict of interest, some of the additional themes of recommendations given their moral hazard issues, include the following:• Increased responsibilities on the Audit Committee

Chairman• Actual and perceived segregation between the Board

and management to ensure adequate protection of shareholder interests

• Claw back provisions with respect to stock options and bonus payouts for officers and directors

• RBI powers over appointment of independent directors in special circumstances – where RBI believes that boards are not independent of controlling stakeholders

The above changes will definitely help Banks, both public and private, to re-align the focus of their Boards, towards a more constructive approach towards what the committee has defined as seven key themes which are essential towards ensuring a sustained growth and overall financial stability. The key themes are as enlisted below• Business Strategy• Financial Reports and their integrity• Risk• Compliance• Consumer Protection• Financial Inclusion• Human Resources

6

There may be other items that may be discussed at the Board level, the same need to be discussed by way of exception rather than a norm. Given the increased capital requirements from the Banking system under the BASEL 3 norms, banks need to plan and allocate capital more effectively through effective strategy and risk management and hence, there has been a greater focus on the two key themes, Business Strategy and Risk. A similar view has been endorsed by the committee report as well.

Although the changes suggested are progressive and forward looking and have a high probability of being implemented, the timelines around the implementation seem to be a challenge, given the need for political backing to bring about a significant overhaul in the legislative framework. While the government has promised a development mandate on multiple domains, there is yet a lot of ground they need to cover and only time will tell the prioritization that the government will attach to this initiative. It is, thus, suggested that the RBI and the Government collaborate in achieving this objective along with their other mutual agendas. The Central Bank may issue directives to the extent of its powers basis the PJ Nayak committee report recommen-dations till the time the government addresses other pressing issues.

Regulatory Impact Assessment | 7

Our point of view on key RBI guidelines issued in July 2014

8

Flexible Structuring of Long Term Project Loans to Infrastructure and Core Industries

RBI Circular reference: RBI/2014-15/126Date of notification: July 15, 2014Applicable entities: All Scheduled Commercial Banks

Background & ObjectiveIn the Union Budget 2014-15, presented on July 10, 2014, the Hon’ble Finance Minster announced that:“Long term financing for infrastructure has been a major constraint in encouraging larger private sector participation in this sector. On the asset side, banks will be encouraged to extend long term loans to infrastructure sector with flexible structuring to absorb potential adverse contingencies, sometimes known as the 5/25 structure. On the liability side, banks will be permitted to raise long term funds for lending to infra-structure sector with minimum regulatory pre-emption such as CRR, SLR and Priority Sector Lending (PSL).”

Banks have not been able to provide long-tenor financing owing to asset-liability mismatches on account of higher asset tenors and lower liability tenors limiting the Banks ability to provide infrastructure finance to a maximum period of 12-15 years. After factoring in the initial construction period and repayment moratorium, the repayment of the bank loan is compressed to a shorter period of 10-12 years leading to higher loan installments, which not only strains the viability of the project, but also constrains the ability of promoters to generate additional capital for further investments.

To mitigate the Asset-Liability Management (ALM) problems faced by banks in extending project loans to infrastructure and core industries sectors, and also to ease the raising of long term resources for project loans to infrastructure and affordable housing sectors, the Reserve Bank of India has issued a number of instruc-tions to banks specifying the operational guidelines and incentives in the form of flexibility in loan structuring and refinancing, and also granting exemptions from regulatory pre-emptions, such as, cash reserves ratio (CRR), statutory liquidity ratio (SLR) and Priority Sector Lending (PSL).

Key Directives issued by RBIThe issues with respect to long term financing to infrastructure sector and other core industries have been examined by the Reserve Bank of India (RBI). It is clarified that RBI has not prescribed any ceiling or

floor on repayment period of loans, except in the case of special regulatory treatment for asset classification on restructuring1. Paragraph 1.3 of Master Circular – Prudential Norms on Income Recognition, Asset Classification and Provisioning pertaining to Advances, urges banks to ensure that while granting loans and advances, realistic repayment schedules are fixed on the basis of cash flows with borrowers as it would go a long way to facilitate prompt repayment by the borrowers and thus improve the record of recovery in advances. Further, in terms of circular DBOD.No.BP.BC.144/21.04.048-2000 dated February 29, 2000 on ‘Income Recognition, Asset Classification, Provisioning and other related matters and Capital Adequacy Standards - Takeout Finance’, banks can refinance their existing infrastructure project loans by entering into take-out financing agreements with any financial institu-tion (FI) on a pre-determined basis. If there is no pre-de-termined agreement, a standard account in the books of a bank can still be taken over by other banks/FIs, subject to guidelines on ‘Transfer of Borrowal Accounts from one Bank to Another’ issued vide circular DBOD.No.BP.BC-104/21.04.048/2011-12 dated May 10, 2012.

Further, in partial modification to the above-mentioned circular dated February 29, 2000, banks were advised, vide circular DBOD.BP.BC.No.98/21.04.132/2013-14 dated February 26, 2014 on ‘Framework for Revitalising Distressed Assets in the Economy - Refinancing of Project Loans, Sale of NPA and Other Regulatory Measures’, that if they refinance any existing infra-structure and other project loans by way of take-out financing, even without a pre-determined agreement with other banks / FIs, and fix a longer repayment period, the same would not be considered as restruc-turing if the following conditions are satisfied:

i. Such loans should be ‘standard’ in the books of the existing banks, and should have not been restructured in the past;

ii. Such loans should be substantially taken over (more than 50% of the outstanding loan by value) from the existing financing banks/Financial institutions; and

iii. The repayment period should be fixed by taking into account the life cycle of the project and cash flows from the project.

In view of the above, RBI’s instructions do not come in the way of banks’ structuring long term project

Regulatory Impact Assessment | 9

financing products, insofar as the prudential and regulatory framework is meticulously observed while structuring such products. However, as banks have certain misgivings that such refinancing of long term project loans may be construed as restructuring, and the estimated cash flows (balance debt in the form of bullet payment) at the end of each refinancing period may not be allowed to be counted in the appropriate maturity buckets for the purpose of ALM, the RBI clarifies that it would not have any objection to banks’ financing of long term projects in infrastructure and core industries sector as suggested above, provided certain conditions that the RBI has laid down in this circular which can be accessed through the following link:

Flexible Structuring of Long Term Project Loans to Infrastructure and Core Industries (http://rbi.org.in/scripts/NotificationUser.aspx?Id=9101&Mode=0)

It may be noted that this new structure will apply to new loans to infrastructure projects and core industries projects sanctioned after the date of this circular. Further, RBI instructions on ‘take-out finance’ (circular dated February 29, 2000) and ‘transfer of borrowal accounts’ (circular dated May 10, 2012) will cease to be applicable on any loan to infrastructure and core industries projects sanctioned under these instructions. RBI will review the instructions at periodic intervals.

*In the interest of saving time of the reader, we have not pasted the full instructions issued by RBI in the document and only relevant portions have been pasted.

ImplicationsUnder the instructions banks are encouraged to extend long term loans to infrastructure sector with flexible structuring to absorb potential adverse contingencies, also known as the 5/25 structure (where insfrastructure loans for 25 years are given with a facility to refinance the same every 5 years by another Bank as per the original amortization schedule for the balance value of the loan). The guidelines issued are applicable only to new loans sanctioned to infrastructure/core industries project loans. It may be pertinent to note that since the

instructions apply only to new loans sanctioned, the existing projects which have been stalled due to want of adequate cash flows will not be benefited. The following are the implications of the instructions issued by RBI:• Banks may modify their credit policies to incorporate

the above mentioned financing and the same needs to be approved by the board.

• Only term loans to infrastructure projects, as defined under the Harmonised Master List of Infrastructure of RBI, and projects in core industries sector, included in the Index of Eight Core Industries (base: 2004-05) published by the Ministry of Commerce and Industry, Government of India, (viz., coal, crude oil, natural gas, petroleum refinery products, fertilisers, steel (Alloy + Non Alloy), cement and electricity - some of these sectors such as fertilisers, electricity generation, distribution and transmission, etc. are also included in the Harmonised Master List of Infrastructure sub-sec-tors) - will qualify for such refinancing as mentioned by the RBI.

• ‘Framework for Revitalising Distressed Assets in the Economy - Refinancing of Project Loans, Sale of NPA and Other Regulatory Measures’ will apply to such loans along with other extant regulations. The banks will have to ensure that if the Debt facility becomes an NPA at any stage of the loan, further refinancing is to stop immediately.

• The banks will have to device a robust stress testing mechanism for analyzing the potential cash flows from projects at the time of initial appraisal. The stress tests may be so designed that they take into account the risk that there may be a probability the loan may not be refinanced by other banks.

• The ALM desk of the banks will have to conduct behavioral study of the cash flows from such projects (including amortization of loans and bullet repay-ments) in due course with the experience gained for such financing in order to plot the cash flows on ALM statements.

• The directives issued by the RBI through this circular shall be covered under internal/ concurrent audit of the banks to ensure compliance with the same.

10

Issue of Long Term Bonds by Banks – Financing of Infrastructure and Affordable HousingRBI circular reference: RBI/2014-15/127Date of notification: July 15, 2014Applicable entities: All Scheduled Commercial Banks

Background & ObjectiveALM mismatches existent in the Banking system on account of limited ability of the Banks to raise long term capital to fund long term infrastructure projects have resulted in the issue of this guideline. The liability profile of the Bank was of a much shorter tenor as compared to the associated tenor for infrastructure lending. RBI, therefore, came out with the guideline to resolve this conundrum. Banks can now issue long-term bonds which will be exempt from regulatory pre-emptions such as the Cash Reserve Ratio (CRR), the Statutory Liquidity Ratio (SLR) and Priority Sector Lending (PSL) so far as the money raised is used for funding of such infrastructure and affordable housing projects.

Key Directives issued by RBIIssue of Long Term Bonds by Banks – Financing of Infrastructure and Affordable Housing Banks can issue long-term bonds with a minimum maturity of seven years to raise resources for lending to (i) long term projects in infrastructure sub-sectors, and (ii) affordable housing.

Type of bond The instrument shall be fully paid, redeemable and unsecured and would rank pari-passu along with other uninsured, unsecured creditors.

Currency of issueThe bonds shall be denominated in Indian Rupees.

Maturity periodThe minimum maturity period of the long-term bonds shall be seven years.

AmountThere will not be any restriction on the quantum of such bonds to be issued by banks; however, the regu-latory incentives will be restricted to the bonds that are used to incrementally finance long term projects in infrastructure and loans for affordable housing. Any incremental infrastructure and affordable housing loans acquired from other banks and financial institutions to be reckoned for regulatory incentives will require prior approval of RBI.

Regulatory IncentivesCompliance with reserve requirementsThese bonds will be exempted from computation of net demand and time liabilities (NDTL) and would therefore not be subjected to CRR/SLR requirements. However, this exemption will be subject to a ceiling of the eligible credit mentioned above. Thus, DTL for the bank which has issued these long term bonds will be computed as below:DTL = Demand and Time Liabilities (DTL) for the purpose of maintaining CRR & SLR - Minimum of (EC and Outstanding long term bonds issued to finance infra-structure loans and affordable housing loans)

Relaxation in priority sector lending norms Eligible bonds will also get exemption in computation of Adjusted Net Bank Credit (ANBC) for the purpose of Priority Sector Lending (PSL), as per the computation specified in the circular.

OptionsThe bonds should be issued in plain vanilla form without call or put option.

Rate of interestThe bonds may be issued with a fixed or floating rate of interest. The floating rate of interest shall be referenced to market determined benchmark rates.

Method of issue The bonds may be issued through a public issue or private placement in full compliance with SEBI guidelines / norms including mandatory rating and listing.

Cross-holdingCross-holding of such bonds among the banks will not be permitted.

Eligibility for deposit insuranceThe bonds will not be eligible for deposit insurance.

Regulatory/Statutory complianceBanks issuing long-term bonds shall be required to comply with all relevant statutory and regulatory requirements.

FEMA requirementBanks shall comply with the FEMA requirements, if applicable.Reporting requirements

Regulatory Impact Assessment | 11

The banks issuing long term bonds shall submit a report to Department of Banking Supervision (DBS), Reserve Bank of India giving details of the bonds issued, such as amount raised, maturity of the instrument, rate of interest, together with a copy of the offer document, soon after the issue is completed.

ReviewThe RBI will review these instructions periodically, particularly those relating to computation of DTL for the purpose of exemption from CRR/SLR as also computa-tion of ANBC for the purpose of PSL.The directives on Housing Loans Eligible under Priority Sector Lending issued by RBI in this regard can be accessed through the following link:Issue of Long Term Bonds by Banks- Financing of Infrastructure and Affordable Housing (http://rbi.org.in/scripts/NotificationUser.aspx?Id=9103&Mode=0)*In the interest of saving time of the reader, we have

not pasted the full instructions issued by RBI in the document and only relevant portions have been pasted.

ImplicationsThe following will be the impact of these guidelines on the banks:•Banks can issue long-term bonds with a minimum

maturity of seven years to raise resources for lending to(i) Long term projects in infrastructure sub-sectors; and(ii) Affordable housing, both of which have been

defined in the circular•These bonds will be exempted from computation of

net demand and time liabilities (NDTL) and would therefore not be subjected to CRR/SLR requirements. However, this exemption will be subject to a ceiling of the eligible credit mentioned in the circular. The eligible credit for this purpose will be calculated as follows:

Where,A = Outstanding ‘Standard’ loans1 to Infrastructure sector (project loans) and affordable housing on the date of this circularB = Outstanding ‘Standard’ loans1 to Infrastructure sector (project loans) and affordable housing on the date of issuance of the bonds

• Additionally, it may be noted that the issue of this circular

will result in the further deepening of bond markets due

to the many bank bond issues that may be coming up.

Period Eligible Credit = EC

From the date of circular till March 31, 2015 B - 0.84A

April 1, 2015 – March 31, 2016 B - 0.7A

April 1, 2016 – March 31, 2017 B - 0.56A

April 1, 2017 – March 31, 2018 B - 0.42A

April 1, 2018 – March 31, 2019 B - 0.28A

April 1, 2019 – March 31, 2020 B - 0.14A

April 1, 2020 onwards B

12

Export of Goods and Services – Project Exports

RBI circular reference: RBI/2014-15/141Date of notification: July 22, 2014Applicable entities: Category – I Authorised Dealer Banks

Background & ObjectiveEarlier the project exports and deferred service exports proposals for contracts exceeding USD 100 Million were presented before the working group committee comprising of representatives from Exim bank, ECGC and the RBI. The exporters used to submit the proposals with the help of AD-1 banks which may have led to delays in certain cases. RBI has issued this guideline with a view to simplify the approval process and increase operational efficiency.

Key Directives Issued by RBITo further liberalise and simplify the procedure, it has been decided as under:i) The structure of Working Group (consisting of repre-

sentatives from Exim bank, ECGC & RBI), which has hitherto been permitted to consider project exports and deferred service exports proposals for contracts exceeding USD 100 Million in value will now be dispensed with. The AD banks / Exim Bank can now consider awarding post-award approvals without any monetary limit and permit subsequent changes in the terms of post award approval within the relevant FEMA guidelines / regulations. Project and service exporters may accordingly approach AD banks / Exim Bank based on their commercial judgment. The respective AD bank / Exim Bank should monitor the projects for which post-award approval has been granted by them; and

ii) The stipulation of time limit of 30 days for the exporter undertaking Project Exports and Service contracts abroad to submit form DPX1/ PEX-1 /TCS-1 to the Approving Authority (AA) for seeking post award approval will not apply henceforth.

The revised Memorandum of Instructions on Project and Service Exports (PEM) is enclosed in the circular.

The directions contained in the circular have been issued under sections 10(4) and 11(1) of the Foreign Exchange Management Act (FEMA), 1999 (42 of 1999) and are without prejudice to permissions / approvals, if any, required under any other law.

*In the interest of saving time of the reader, we have not pasted the full instructions issued by RBI in the document and only relevant portions have been pasted.

ImplicationsRBI has liberalized and simplified the procedure related to approval process of project exports. Following are the major implications that emanate from this guideline:• The AD banks / Exim Bank can now consider awarding

post-award approvals without any monetary limit and permit subsequent changes in the terms of post award approval within the relevant FEMA guidelines / regula-tions. Hence, the need for an exporter to submit form DPX1 / PEX-1/TCS-1 to the Approving Authority has been done away with.

• RBI has revised Memorandum of Instructions on Project and Service Exports (PEM) to reflect the above changes.

• Banks would need to update their internal governance documentation across all the governance functions, such as audit, compliance and risk.

Regulatory Impact Assessment | 13

Compilation of R-return: Reporting under FETERS-Discontinuation of ENC and Sch 3 to 6 fileRBI circular reference: RBI/2014-15/151Date of notification: July 28, 2014Applicable entities: Category - I Authorised Dealer Banks

Background and ObjectivePreviously, AD banks were submitting the various returns like XOS (export outstanding statements), ENC (Export Bills Negotiated / sent for collection) for acknowledge-ment of receipt of Export documents, Sch.3 to 6 (reali-zation of export proceeds), relating to Export transaction under FEMA to RBI under Foreign Exchange Transactions - Electronic Reporting System (FETERS). These various returns were being managed either on a different solo application or manually.

With a view to simplify the procedure for filing the various returns and for better monitoring, a compre-hensive IT- based system called Export Data Processing and Monitoring System (EDPMS) has been developed which will facilitate the banks to report all the above mentioned returns through a single platform.

Key Directives issued by RBIA comprehensive IT- based system called Export Data Processing and Monitoring System (EDPMS) has been operationalized with effect from March 01, 2014 and facilitating AD banks to report various returns through a single platform.

It is advised that ENC and Sch. 3 to 6 file submitted under FETERS will be discontinued with effect from first fortnight of September 2014 as the information contained in these returns are available through EDPMS. AD banks should ensure to report all the ENC and Sch.3 to 6 transaction data for which export shipping bills/invoices are generated prior to march 01, 2014 by August 31, 2014. In exceptional cases after August 31, 2014, the same data may be submitted after seeking technical support from RBI at email.

With effect from first fortnight of September 2014, only two files (Viz. BOP6 file and QE file) need to be submitted under FETERS and other guidelines relating to FETERS data submission laid in A.P. (DIR Series) Circular No. 84 dated February 29, 2012 will remain unchanged.

Implications• With effect from 15th of September 2014, only two

files (Viz. BOP6 file and QE file) will be needed to be submitted under FETERS.

• All Category - I Authorised Dealer Banks should ensure to report all the ENC and Sch.3 to6 transaction data on EDPMS for which export shipping bills / invoices are generated prior to March 1, 2014 by August 31, 2014.

• ENC and Sch. 3 to 6 files will henceforth be submitted on EDPMS.

14

Other Guidelines issued by RBI in the Month

Regulatory Impact Assessment | 15

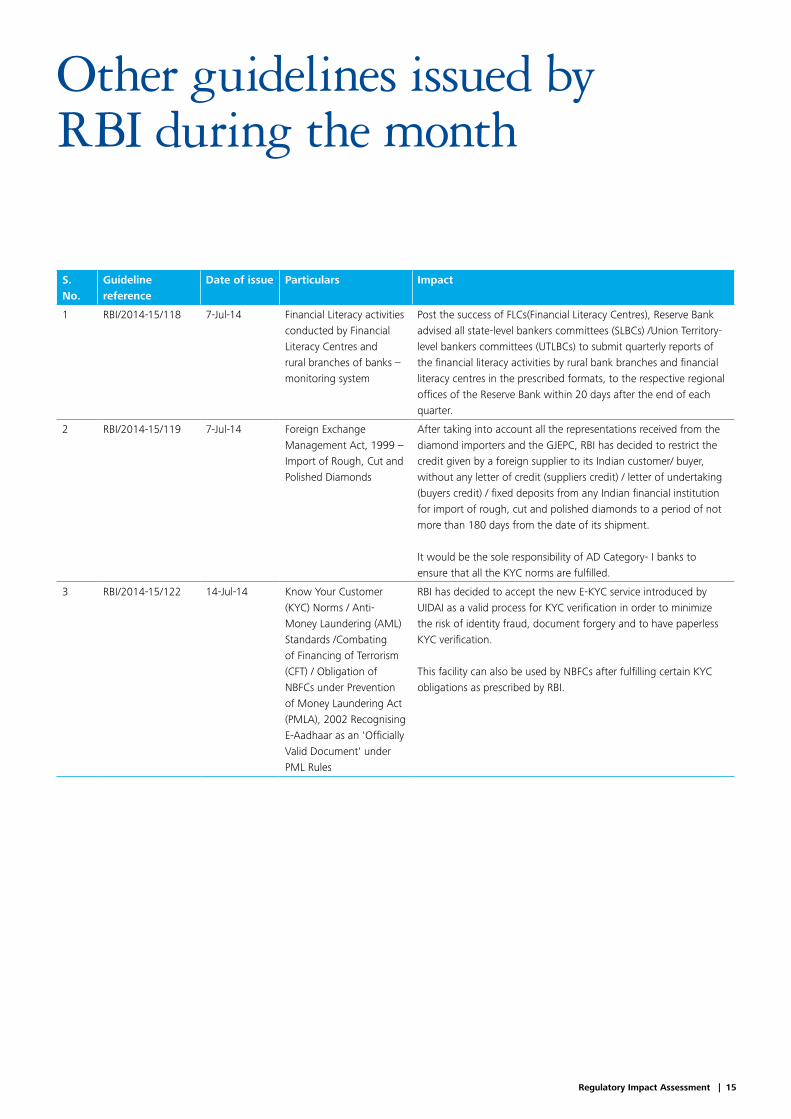

Other guidelines issued by RBI during the month

S. No.

Guideline reference

Date of issue Particulars Impact

1 RBI/2014-15/118 7-Jul-14 Financial Literacy activities conducted by Financial Literacy Centres and rural branches of banks – monitoring system

Post the success of FLCs(Financial Literacy Centres), Reserve Bank advised all state-level bankers committees (SLBCs) /Union Territory-level bankers committees (UTLBCs) to submit quarterly reports of the financial literacy activities by rural bank branches and financial literacy centres in the prescribed formats, to the respective regional offices of the Reserve Bank within 20 days after the end of each quarter.

2 RBI/2014-15/119 7-Jul-14 Foreign Exchange Management Act, 1999 – Import of Rough, Cut and Polished Diamonds

After taking into account all the representations received from the diamond importers and the GJEPC, RBI has decided to restrict the credit given by a foreign supplier to its Indian customer/ buyer, without any letter of credit (suppliers credit) / letter of undertaking (buyers credit) / fixed deposits from any Indian financial institution for import of rough, cut and polished diamonds to a period of not more than 180 days from the date of its shipment.

It would be the sole responsibility of AD Category- I banks to ensure that all the KYC norms are fulfilled.

3 RBI/2014-15/122 14-Jul-14 Know Your Customer (KYC) Norms / Anti-Money Laundering (AML) Standards /Combating of Financing of Terrorism (CFT) / Obligation of NBFCs under Prevention of Money Laundering Act (PMLA), 2002 Recognising E-Aadhaar as an 'Officially Valid Document' under PML Rules

RBI has decided to accept the new E-KYC service introduced by UIDAI as a valid process for KYC verification in order to minimize the risk of identity fraud, document forgery and to have paperless KYC verification.

This facility can also be used by NBFCs after fulfilling certain KYC obligations as prescribed by RBI.

16

4 RBI/2014-15/132 17-Jul-14 Liberalised Remittance Scheme (LRS) for resident individuals-Increase in the limit from USD 75,000 to USD 125,000 (Corrected)

RBI, in this notification, has decided to increase the liberalised remittance limit for resident individuals from USD 75,000 to USD 125,000 under the Liberalised Remittance Scheme (LRS).

5 RBI/2014-15/133 18-Jul-14 Foreign Direct Investment – Reporting under FDI Scheme

For the purpose of classification of activities under the industrial classification system, the Department of Industrial Policy and Promotion (DIPP), Ministry of Commerce and Industry & Government of India has decided to switch over to the National Industrial Classification 2008 (NIC 2008) from the NIC 1987 version.

Henceforth, all the Indian companies are required to report the details of the issue of shares, convertible debentures, partly paid shares and warrants in form FC-GPR, to the Regional Office concerned, within 30 days of issue of shares / convertible debentures and any sale from a person resident in India to a person resident outside India or vice versa, are required to be reported by the transferor / transferee resident in India to the AD Bank in form FCTRS, within 60 days from the date of receipt or payment of the amount of consideration.

Also, Indian companies are required to report the NIC Codes in the FCGPR and FCTRS forms as per the NIC 2008 version.

Additionally, RBI has decided to introduce a uniform State and District code list for reporting of details of foreign direct investment by Indian companies in Form FCGPR. This list can be accessed on the RBI website

Regulatory Impact Assessment | 17

6 RBI/2014-15/1349 18-Jul-14 Rupee Drawing Arrangement – Delegation of work to Regional Offices

AD Category-I Banks should submit the duly approved annual review note by their board for the Rupee/ Foreign Currency Drawing Arrangement with non-resident exchange house for the first time in the prescribed format to the Chief General Manager, Reserve Bank of India, Foreign Exchange Department, before 30th June every year for the period covering January 1 to December 31.

7 RBI/2014-15/135 18-Jul-14 Money Transfer Service Scheme – Delegation of work to Regional Offices

RBI has now decided to delegate the work related to authorization of Indian Agents to the Regional Offices of the Reserve Bank. Thus, the application for necessary permission to act as an Indian Agent under MTSS should be made to the respective Regional Office of the Foreign Exchange Department of the Reserve Bank under whose jurisdiction the registered office of the applicant falls.

8 RBI/2013-14/137

RBI/2013-14/137

21-Jul-14 Know Your Customer (KYC) Norms/Anti-Money Laundering (AML) Standards/ Combating of Financing of Terrorism (CFT)/ Obligation of Authorised Persons under Prevention of Money Laundering Act (PMLA), 2002 – Money Changing Activities – Recognising E-Aadhaar as an ‘Officially Valid Document’ under PML Rules

Know Your Customer (KYC) Norms/Anti-Money Laundering (AML) Standards/ Combating of Financing of Terrorism (CFT)/ Obligation of Authorised Persons under Prevention of Money Laundering Act (PMLA), 2002 – Money Transfer Service Scheme – Recognising E-Aadhaar as an ‘Officially Valid Document’ under PML Rules

RBI has now decided to accept the new E-KYC service introduced by UIDAI as a valid proof in order to minimize the risk of identity fraud, document forgery to have paperless KYC verification.

This facility can also be used by NBFC after fulfilling certain KYC obligations as prescribed by RBI.

18

9 RBI/2014-15/142 22-Jul-14 Loans against Gold Ornaments and Jewellery for Non-Agricultural End-uses

•The ceiling of INR 1 lakh is no longer applicable for loans against gold jewellery for non agricultural purposes. However, banks will need to have a Board approved policy in place with respect to the ceiling on the quantum of loans.

•The requirement to maintain minimum margin in case of such loans has been done away with.

•Interest on such loans needs to be charged at monthly intervals and recognised on accrual basis, provided the account is classified as ‘standard’ account. This requirement applies to existing loans as well. This aspect will have to be taken into consideration by the accounting desk and the credit team of the bank.

•LTV of 75% needs to be maintained at all times during the tenure of the loan. For the purpose of calculation of LTV, accrued interest should also be included in the total outstanding loan amount.

•The valuation of gold needs to be determined on the basis of the methodology prescribed by RBI circular on 'Lending against Gold Jewellery' dated January 20, 2014.

•Value of gold may be obtained from gold prices disseminated by India Bullion and Jewellers Association Ltd. Additionally, historical spot gold price data disseminated by a commodity exchange regulated by the Forward Markets Commission in a manner consistent with the Bank's Board approved policy may also be used.

•The guidelines with respect to tenor of the loans, income recognition, asset classification and provisioning remain same as the guidelines contained in the 2013 circular.

Thus, with the introduction of these guidelines, RBI aims to give more autonomy to banks with respect to granting loans for non-agricultural purposes against gold jewellery.

10 RBI/2014-15/147 25-Jul-14 Issue of Prepaid Forex Cards- Due Diligence and Adherence to KYC norms

The RBI is of the view that prepaid foreign currency cards are a form of foreign currency, similar to foreign currency notes or travellers cheques. The AD Category- I Banks selling pre-paid foreign currency cards for travel purposes will have to ensure that the same rigorous standards of due diligence and KYC are followed as they would, in case they were selling foreign currency notes/ travelers cheques to their customers. Hence the Banks would need to define a specific KYC policy with respect to the process of issue of such cards.

11 RBI/2014-15/152 28-Jul-14 Trade Credits for Imports into India — Review of all-in-cost ceiling

The existing all-in-cost ceiling for trade credits for imports into India i.e. LIBOR + 350 bps for maturities up to five years will continue to be applicable till December 31, 2014.

12 RBI/2014-15/153 28-Jul-14 External Commercial Borrowing (ECB) Policy — Review of all-in-cost ceiling

The existing all-in-cost ceiling for ECBs i.e. 6 month LIBOR* + 350 bps for average maturity of 3 to 5 years and 6 month LIBOR* + 500 bps for average maturity more than 5 years will continue to be applicable till December 31, 2014.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.This material and the information contained herein prepared by Deloitte Touche Tohmatsu India Private Limited (DTTIPL) is intended to provide general information on a particular subject or subjects and is not an exhaustive treatment of such subject(s). This material contains information sourced from third party sites (external sites). DTTIPL is not responsible for any loss whatsoever caused due to reliance placed on information sourced from such external sites. None of DTTIPL, Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this material, rendering professional advice or services. The information is not intended to be relied upon as the sole basis for any decision which may affect you or your business. Before making any decision or taking any action that might affect your personal finances or business, you should consult a qualified professional adviser.

No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this material.

©2014 Deloitte Touche Tohmatsu India Private Limited. Member of Deloitte Touche Tohmatsu Limited

Contacts

Muzammil PatelSenior Director, [email protected]+91 22 6185 5490

Vivek Iyer Director, [email protected]+91 22 6185 5558

Abhinava Bajpai Director, [email protected]+91 22 6185 5557

For further information, send an e-mail to [email protected].