Embed Size (px)

Citation preview

Regulatory change management for investment suitability and beyond: A business differentiator

IntroductionIt may come as no surprise that in spite of turbulent financial markets, most global and local private banks in Asia are continuing to invest heavily in their operations in order to keep pace with the agility needed to service the growing market of Asian multi-millionaires.

As digitally savvy and wealthy customers look out for more sophisticated engagement via online channels, banks also strive to find smarter ways to on-board these new channels and scale them across markets while being compliant. Although banks

show the willingness to embrace such changes, they are limited by their internal inefficiencies and less than agile IT infrastructure.

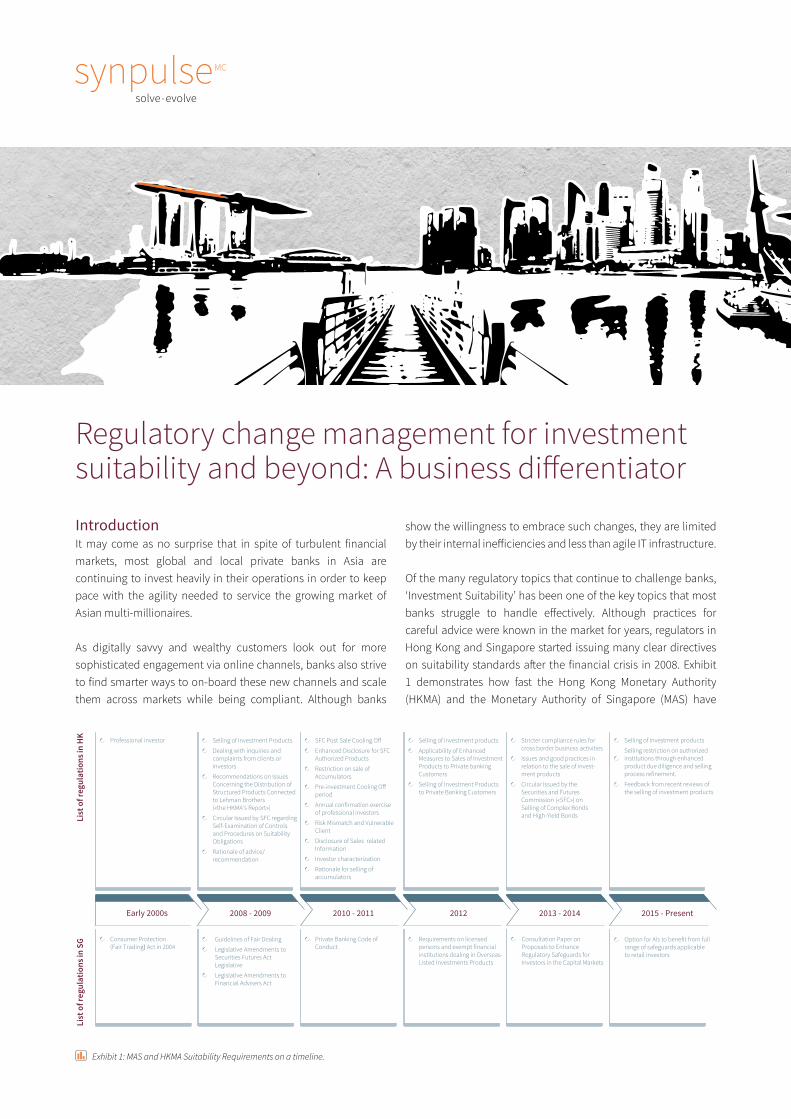

Of the many regulatory topics that continue to challenge banks, ‘Investment Suitability’ has been one of the key topics that most banks struggle to handle effectively. Although practices for careful advice were known in the market for years, regulators in Hong Kong and Singapore started issuing many clear directives on suitability standards after the financial crisis in 2008. Exhibit 1 demonstrates how fast the Hong Kong Monetary Authority (HKMA) and the Monetary Authority of Singapore (MAS) have

Early 2000s

Lis

t o

f re

gu

lati

on

s in

HK

Lis

t o

f re

gu

lati

on

s in

SG

Professional investor

Consumer Protection(Fair Trading) Act in 2004

Private Banking Code of Conduct

Requirements on licensed persons and exempt financialinstitutions dealing in Overseas-Listed Investments Products

Option for AIs to benefit from fullrange of safeguards applicable to retail investors

2008 - 2009 2010 - 2011 2012 2013 - 2014 2015 - Present

Selling of Investment Products

Dealing with inquiries and complaints from clients or investors

Recommendations on IssuesConcerning the Distribution ofStructured Products Connectedto Lehman Brothers («the HKMA's Report»)

Circular Issued by SFC regarding Self-Examination of Controls and Procedures on Suitability Obligations

Rationale of advice/ recommendation

SFC Post Sale Cooling O�

Enhanced Disclosure for SFC Authorized Products

Restriction on sale of Accumulators

Pre-investment Cooling O� period

Annual confirmation exercise of professional investors

Risk Mismatch and Vulnerable Client

Disclosure of Sales related Information

Investor characterization

Rationale for selling of accumulators

Selling of investment products

Applicability of Enhanced Measures to Sales of Investment Products to Private banking Customers

Selling of Investment Products to Private Banking Customers

Selling of investment products

Selling restriction on authorizedinstitutions through enhanced product due diligence and sellingprocess refinement.

Feedback from recent reviews ofthe selling of investment products

Consultation Paper on Proposals to Enhance Regulatory Safeguards for Investors in the Capital Markets

Stricter compliance rules for cross border business activities

Issues and good practices in relation to the sale of invest-ment products

Circular Issued by the Securities and Futures Commission («SFC») on Selling of Complex Bonds and High-Yield Bonds

Guidelines of Fair Dealing

Legislative Amendments toSecurities Futures Act Legislative

Legislative Amendments toFinancial Advisers Act

Exhibit 1: MAS and HKMA Suitability Requirements on a timeline.

synpulse | 2

been spelling out their requirements in this topic. In the last few years, many banks have resorted to tactical solutions to address these suitability requirements. However, these solutions have resulted in added administrative overheads to their Relationship Managers (RMs)and created complex control structures that are heavily scrutinized during regulatory reviews.

Two years ago, Synpulse published an article that illustrated ways of how some industry leaders have approached the topic of suit- ability in a distinctive way. The article on «Investment Suitability: Transforming your advisory framework»1 and the points raised then have relevance, even in today’s ever-changing regulatory environment. Tackling Investment Suitability ChallengesImplementing a suitability framework in a pragmatic way requires deep understanding of the private banking industry in terms of regulatory requirements, clients, investment products and risk management.

There are three key steps to implementing a robust suitability framework (Exhibit 2):

Formulate a pragmatic «Portfolio approach» to ensure that client’s investments are assessed at portfolio level instead

of a transaction level, making it more meaningful in a private banking setup.

Implement «pre-trade checks» in the order management system in a way that the Relationship Managers (RMs) only need to focus on failed suitability checks and follow the clear recommended actions presented via a unified dashboard.

Devise a periodic «Portfolio monitoring» mechanism to ensure that the client’s portfolios are monitored to detect unusual portfolio performance, risk mismatch, concentration risks etc. in order to address suitability risk in a proactive and timely manner.

Majority of the large banks in the region have a good understanding on the principles of a successful suitability framework. However, they seem to be constrained with the challenges that IT change management process and IT infrastructure present. This takes us towards concept of digitalization and organization agility where the industry needs to identify efficient ways of conducting business which extends towards the space of regulatory and compliance topics.

Understanding client’s risk profile, knowledge and experience

Methodology to assess risk on a portfolio level and compare with client’s risk profile

Methodology to calculate concentration risk

Unified dashboard displaying suitability results

Exceptional handling

Standardized capturing of actions taken by the client

Holistic «portfolio level» assessment of suitability risks

Robust supervisory control and risk management framework

Generation of management data for overall suitability risks the bank is exposed to

Pragmatic «Portfolio approach» Integrated Pre trade Checks in Order Managers

Portfolio Monitoring

UK20%

Strategicbond funds

20%

Propety funds

15%

US10%

European10%

Asian5%

Japanese2%

Emerging Market3%

1 Article can be downloaded from our website at http://bit.ly/29AoC0q

The rule engine solution: Strategic perspectiveTraditionally banks have been big part of their change budget to implement the regulatory requirements (esp. suitability) and the corresponding control processes to ensure compliance. In spite of these large investments, most of the private banking businesses even today face formidable challenges based on two aspects. Firstly, there are still a lot of administrative overheads that the relationship managers and the clients face due to ineffective ways of implementing regulations that many times ignore the business context of private banking. This results in frustrated RMs,

unhappy clients and poorly implemented control processes that are heavily scrutinized by regulators. Secondly, the decentralized IT implementations spanning across multiple core banking components are too cumbersome and costly to maintain. This results in a less agile IT infrastructure that prevents scalability of regulatory implementations across geographies or channels.

A central rule engine (Exhibit 3) to develop and maintain the rules will not only allow ease of maintenance and future scalability but also enable central control and management of regulatory

Exhibit 2: Key steps in implementing a robust suitability framework.

synpulse | 3

Contact us

Prasanna VenkatesanAssociate [email protected]

Accredited InvestorProfessional Investor Private Banking ClientVulnerable Client

Client Profiling

Suitability checksCross border checks

Pre-trade Checks

Country Selling Restrictions

BCBS 239/FATCA/AEI ReportingKYC/AML Review

Reviews and Reporting

Portfolio Based SuitabilityReview

Account opening formsbased on client due diligence checks, account type etc.

Client onboarding

Digi

taliz

atio

n la

yer

(via

Rul

e En

gine

)Co

re B

anki

ng S

yste

mM

arke

t Dem

and

Multiple Regulatory Requirements Multiple Booking Centers

RM

Client

Regulators(Reporting)

Multiple Channels/Outputs

Client Data Transaction Data Portfolio Data Product Data Financial Data ...and more.

Data Integration

rules and internal controls. As such, the rule engine is designed only to maintain the business logic relevant to regulatory checks and envelopes around the existing core banking systems. This architecture facilitates aggregation of relevant client, product and portfolio information before the business logic can be executed. Such an implementation would enable other digital channels and different booking centers to connect to the rule engine and start leveraging the centrally developed regulatory rules. This significantly brings down the cost and time to market for new channel or new booking center integration.

The central maintenance of rules become paramount as regulators across different jurisdictions are coming in with aligned practices. Even in cases of BCBS 239 and CRS (FATCA/AEI) requirements, the rule engine allows central pooling of data and managing output in a bespoke way. A regulatory change needs to be implemented only in one place and standard practices are available across different channels and booking centers.

There are already established technology products in the market that allow such change agility that the banks could leverage. One of the products even offers visually customizable capabilities where a business user can directly adapt many configurations

(e.g. product scope) and simple business logic which makes the change even more efficient and controllable directly by business.Given the rapid increase in client’s demand for digital channels that are accessible across the globe, there comes a strong need to explore strategic ways of implementing regulations across different jurisdictions. Banks that head down this path will definitely have an edge over the others in gaining strategic market advantage. The advantage and agility is even more needed for the mid-sized private banks in order to be able increase their efficiency of conducting business by adopting digitalization in relevant regulatory and compliance topics.

With our many years of experiences in shaping the topics on regulatory and compliance, Synpulse has developed and showcased specialized skills in this area. Backed by both business and technology solution expertise, Synpulse is well positioned to offer its support to clients in streamlining their regulatory implementations in an effective and meaningful way.

About the author(s)Prasanna Venkatesan (Associate Partner), is the topic expert at Synpulse’s Singapore office. He is supported by Anu Meha (Senior Consultant) and Ajay Kumar (Consultant) .

Exhibit 3: Central rule engine that facilitates ease of implementation and scalability across channels and booking centers.