Embed Size (px)

Citation preview

Regulation and Supervision After the Storm

February 8, 2012

Global Financial Development Report 2013 GFDR Seminar

– After the onset of the global financial crisis: much discussion about “not wasting” the crisis, and using it to push for needed reforms

• Basel Committee • Financial Stability Board (FSB) • Dodd-Frank Act, Vickers report, etc.

– Much has been done, but is it appropriate? • Does it address the sources of future financial crises?

Introduction Introduction What changed? What are likely impacts? What’s missing? Conclusion

– Recommendations for regulatory reform developed in academic fora

• Geneva Report (2009) • LSE Report on the Future of Finance,(2010) • Squam Lake Working Group (2010) • CEPR Future of Banking (2010)

– Common themes: • Information asymmetries and structure of incentives under which agents operate in

the financial system are fundamental sources of weakness in financial systems • Incentive issues need to be more fully reflected in the design of regulatory systems

– We take the discussion a step further, and outline an approach to the regulation of financial systems that would place issues of asymmetric information and incentives at its center.

Introduction Introduction What changed? What are likely impacts? What’s missing? Conclusion

• Key issues – Post-crisis transformation of regulatory practices around the world – Specific issues for emerging market and developing economies

• Questions … and preliminary answers – Lessons from the crisis? … Incentive breakdowns – What has changed? … A few things, but more is needed – How big are the likely impacts? … Manageable, but large in some regions – What’s missing? ... Addressing incentive issues

Introduction Introduction What changed? What are likely impacts? What’s missing? Conclusion

Introduction: Lessons learned from the global financial crisis

• Shortcomings in the micro prudential approach – Promoted regulatory arbitrage – Focused on risks in individual institutions, did not sufficiently reflect systemic risk – Rules poorly designed, some increased systemic risk – Implementation constrained by capacity and incentives of regulators/supervisors

• Shortcomings in market discipline – Basel II sought to expand the role of market discipline elements – Rating agencies given a role in the evaluation of the risks in the portfolio under Pillar I – Explicit role for market discipline introduced under Pillar III – But underlying assumptions not met due to information asymmetries and perverse

incentives

Introduction What changed? What are likely impacts? What’s missing? Conclusion

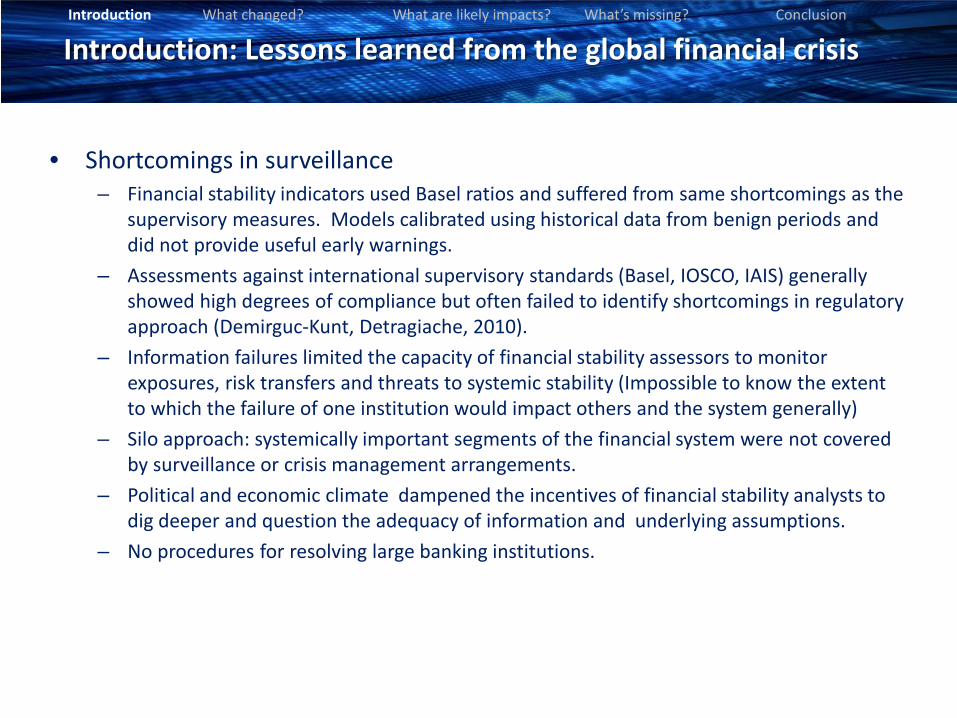

Introduction: Lessons learned from the global financial crisis

• Shortcomings in surveillance – Financial stability indicators used Basel ratios and suffered from same shortcomings as the

supervisory measures. Models calibrated using historical data from benign periods and did not provide useful early warnings.

– Assessments against international supervisory standards (Basel, IOSCO, IAIS) generally showed high degrees of compliance but often failed to identify shortcomings in regulatory approach (Demirguc-Kunt, Detragiache, 2010).

– Information failures limited the capacity of financial stability assessors to monitor exposures, risk transfers and threats to systemic stability (Impossible to know the extent to which the failure of one institution would impact others and the system generally)

– Silo approach: systemically important segments of the financial system were not covered by surveillance or crisis management arrangements.

– Political and economic climate dampened the incentives of financial stability analysts to dig deeper and question the adequacy of information and underlying assumptions.

– No procedures for resolving large banking institutions.

Introduction What changed? What are likely impacts? What’s missing? Conclusion

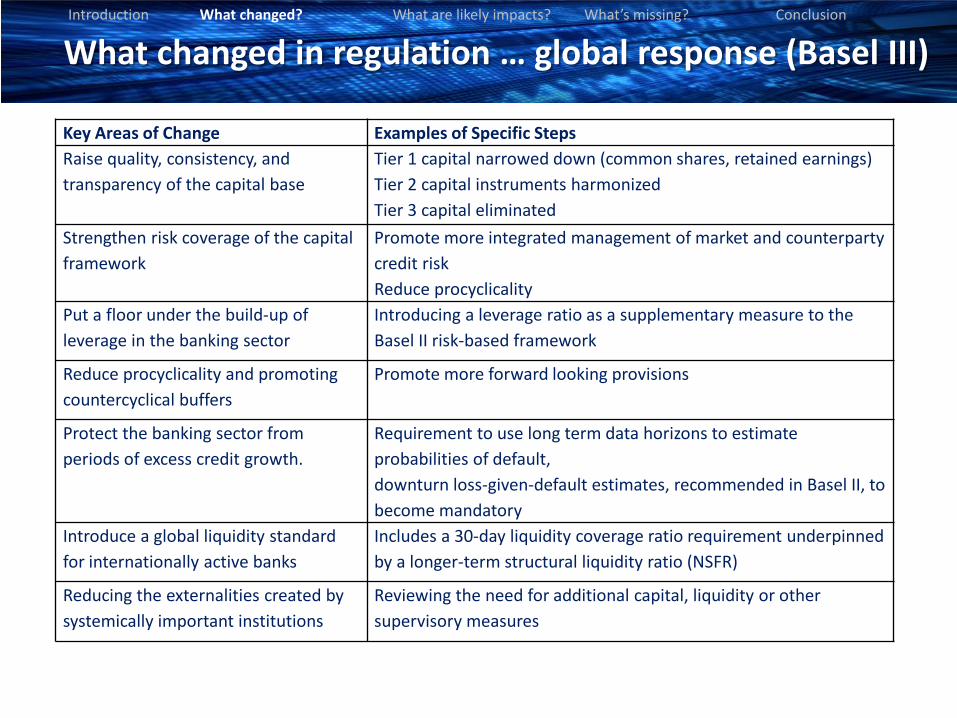

What changed in regulation … global response (Basel III) Introduction What changed? What are likely impacts? What’s missing? Conclusion

Key Areas of Change Examples of Specific Steps Raise quality, consistency, and transparency of the capital base

Tier 1 capital narrowed down (common shares, retained earnings) Tier 2 capital instruments harmonized Tier 3 capital eliminated

Strengthen risk coverage of the capital framework

Promote more integrated management of market and counterparty credit risk Reduce procyclicality

Put a floor under the build-up of leverage in the banking sector

Introducing a leverage ratio as a supplementary measure to the Basel II risk-based framework

Reduce procyclicality and promoting countercyclical buffers

Promote more forward looking provisions

Protect the banking sector from periods of excess credit growth.

Requirement to use long term data horizons to estimate probabilities of default, downturn loss-given-default estimates, recommended in Basel II, to become mandatory

Introduce a global liquidity standard for internationally active banks

Includes a 30-day liquidity coverage ratio requirement underpinned by a longer-term structural liquidity ratio (NSFR)

Reducing the externalities created by systemically important institutions

Reviewing the need for additional capital, liquidity or other supervisory measures

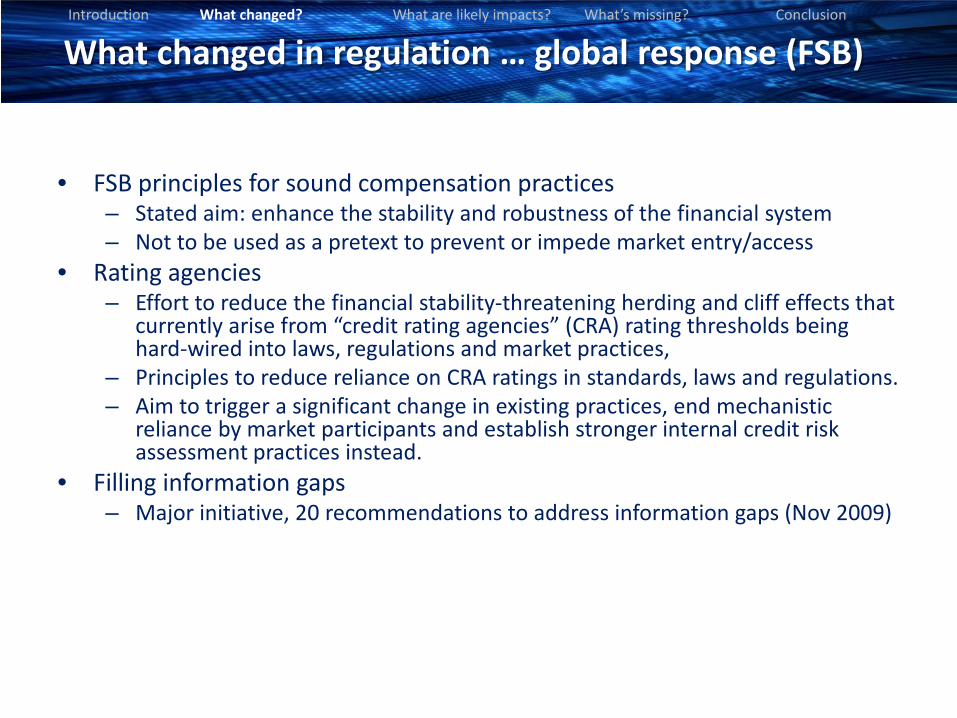

What changed in regulation … global response (FSB) Introduction What changed? What are likely impacts? What’s missing? Conclusion

• FSB principles for sound compensation practices – Stated aim: enhance the stability and robustness of the financial system – Not to be used as a pretext to prevent or impede market entry/access

• Rating agencies – Effort to reduce the financial stability-threatening herding and cliff effects that

currently arise from “credit rating agencies” (CRA) rating thresholds being hard-wired into laws, regulations and market practices,

– Principles to reduce reliance on CRA ratings in standards, laws and regulations. – Aim to trigger a significant change in existing practices, end mechanistic

reliance by market participants and establish stronger internal credit risk assessment practices instead.

• Filling information gaps – Major initiative, 20 recommendations to address information gaps (Nov 2009)

What changed in regulation … global response (FSB) Introduction What changed? What are likely impacts? What’s missing? Conclusion

• FSB proposals to deal with too-big-to-fail (TBTF) issues – New international standard (‘Key Attributes of Effective Resolution Regimes’); – Requirements for resolvability assessments and for recovery and resolution

planning for global SIFIs, and for the development of institution-specific cross-border cooperation agreements;

– Requirements for banks determined to be globally systemically important to have additional loss absorption capacity tailored to the impact of their default, to be met with common equity;

– More intensive and effective supervision of all SIFIs.

• FSB/Basel Committee published an initial list of “global SIFIs” – 29 banks, to meet resolution planning requirements by end-2012. – National authorities may extend these requirements to other institutions. – G-SIFI list to be updated and published by the FSB each November. – Methodology and data publicly available so that markets and institutions can

replicate the authorities’ determination.

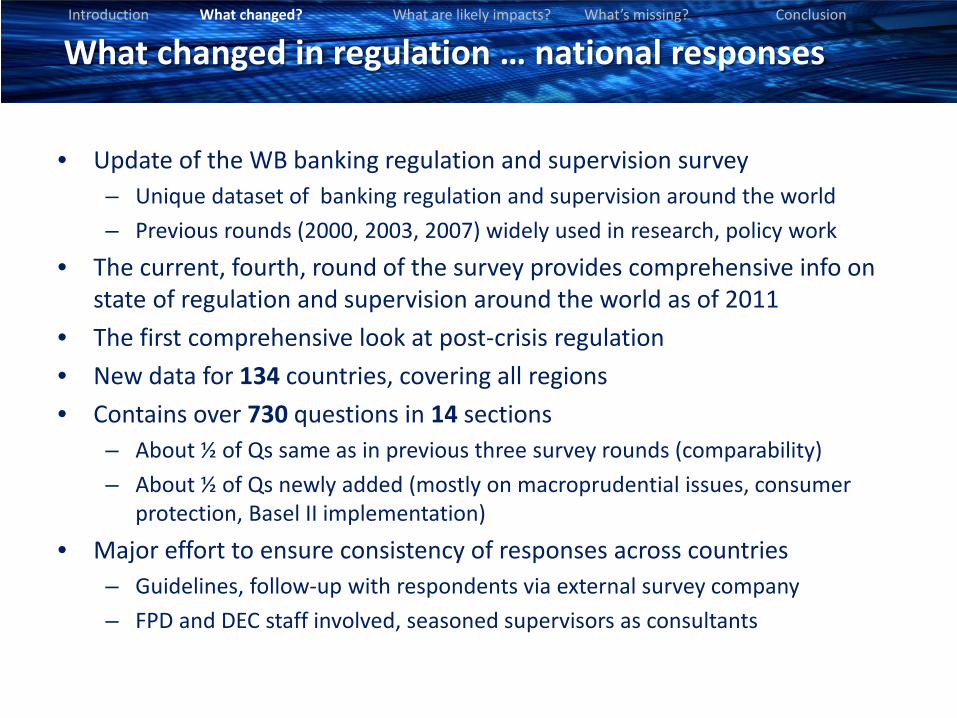

• Update of the WB banking regulation and supervision survey – Unique dataset of banking regulation and supervision around the world – Previous rounds (2000, 2003, 2007) widely used in research, policy work

• The current, fourth, round of the survey provides comprehensive info on state of regulation and supervision around the world as of 2011

• The first comprehensive look at post-crisis regulation • New data for 134 countries, covering all regions • Contains over 730 questions in 14 sections

– About ½ of Qs same as in previous three survey rounds (comparability) – About ½ of Qs newly added (mostly on macroprudential issues, consumer

protection, Basel II implementation) • Major effort to ensure consistency of responses across countries

– Guidelines, follow-up with respondents via external survey company – FPD and DEC staff involved, seasoned supervisors as consultants

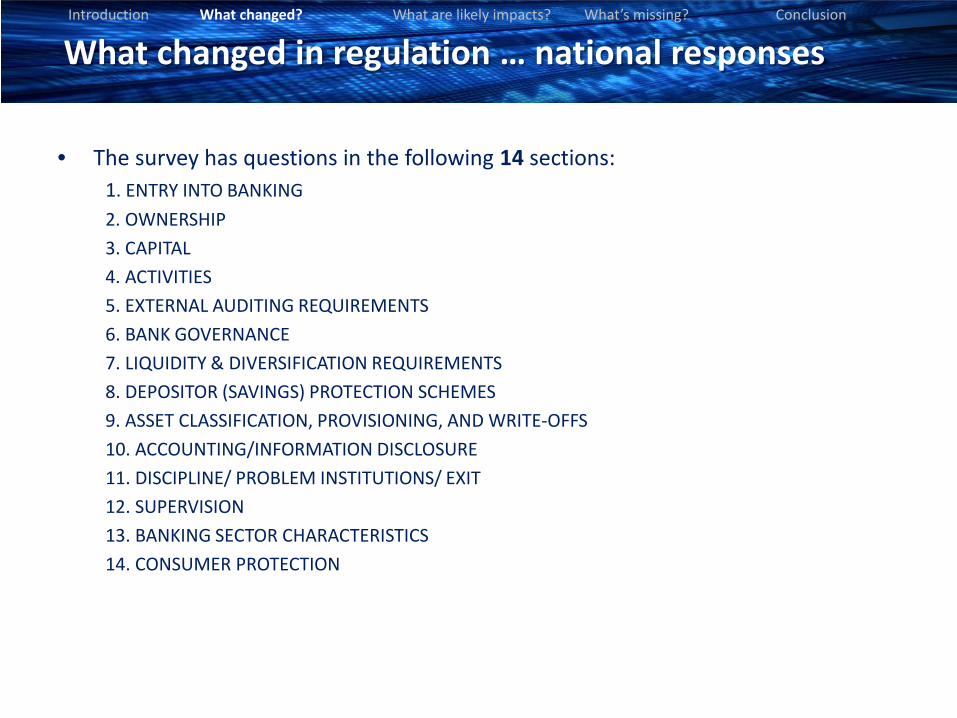

What changed in regulation … national responses Introduction What changed? What are likely impacts? What’s missing? Conclusion

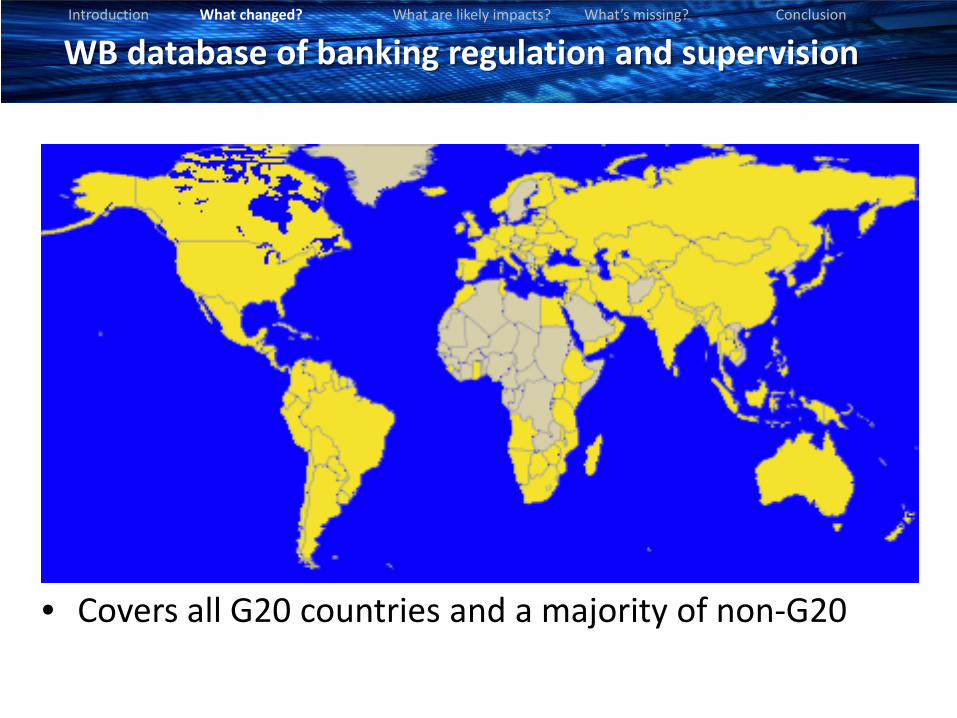

WB database of banking regulation and supervision Introduction What changed? What are likely impacts? What’s missing? Conclusion

• Covers all G20 countries and a majority of non-G20

• The survey has questions in the following 14 sections: 1. ENTRY INTO BANKING 2. OWNERSHIP 3. CAPITAL 4. ACTIVITIES 5. EXTERNAL AUDITING REQUIREMENTS 6. BANK GOVERNANCE 7. LIQUIDITY & DIVERSIFICATION REQUIREMENTS 8. DEPOSITOR (SAVINGS) PROTECTION SCHEMES 9. ASSET CLASSIFICATION, PROVISIONING, AND WRITE-OFFS 10. ACCOUNTING/INFORMATION DISCLOSURE 11. DISCIPLINE/ PROBLEM INSTITUTIONS/ EXIT 12. SUPERVISION 13. BANKING SECTOR CHARACTERISTICS 14. CONSUMER PROTECTION

What changed in regulation … national responses Introduction What changed? What are likely impacts? What’s missing? Conclusion

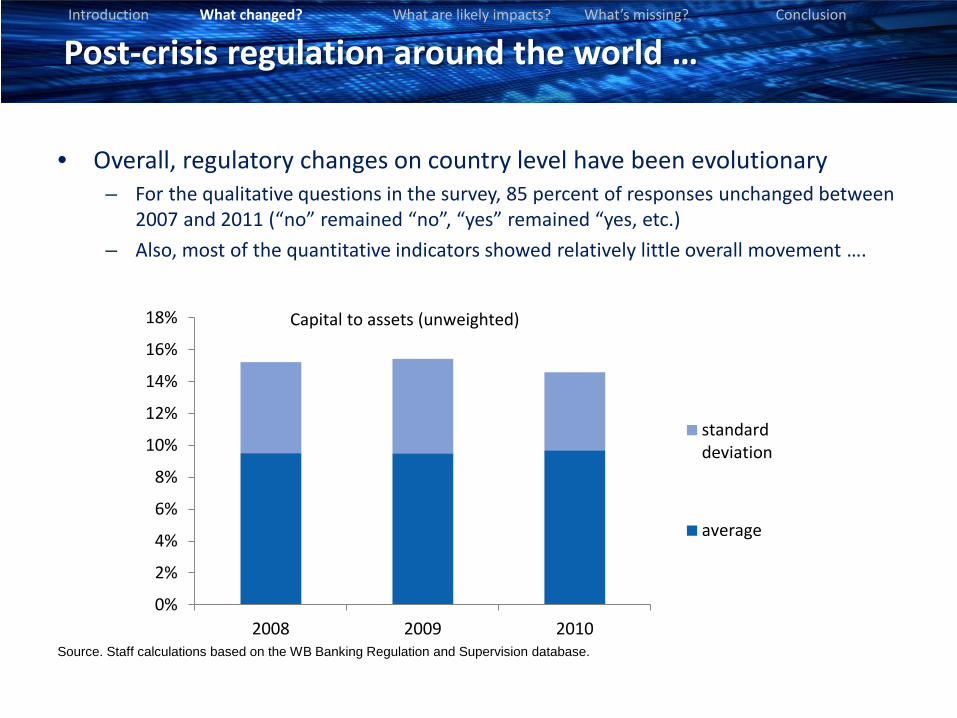

• Overall, regulatory changes on country level have been evolutionary – For the qualitative questions in the survey, 85 percent of responses unchanged between

2007 and 2011 (“no” remained “no”, “yes” remained “yes, etc.) – Also, most of the quantitative indicators showed relatively little overall movement ….

Post-crisis regulation around the world … Introduction What changed? What are likely impacts? What’s missing? Conclusion

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2008 2009 2010

standarddeviation

average

Capital to assets (unweighted)

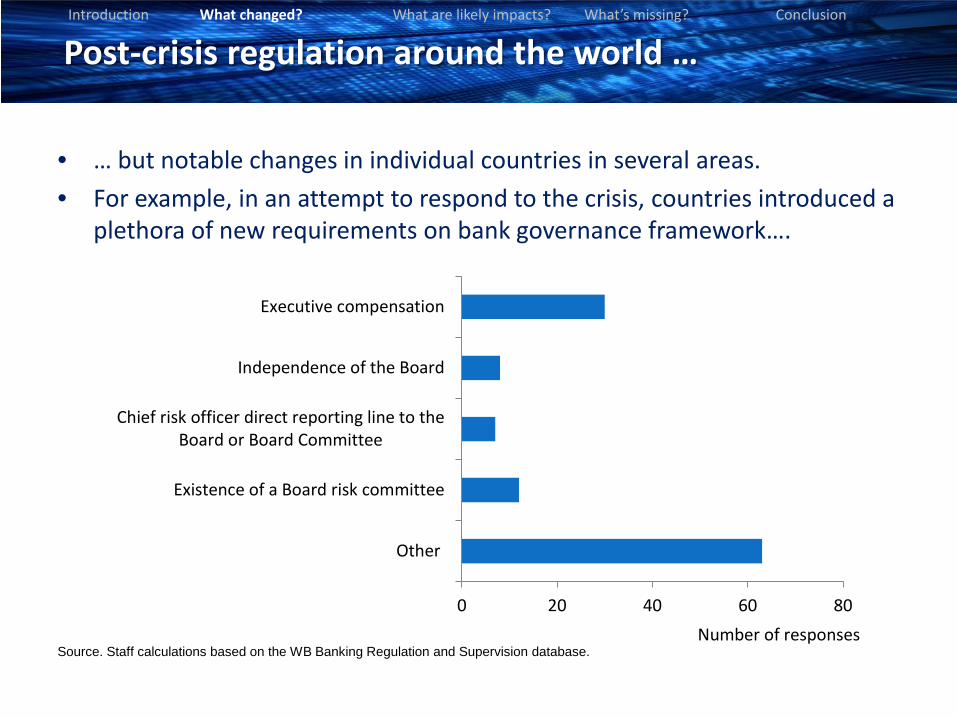

• … but notable changes in individual countries in several areas. • For example, in an attempt to respond to the crisis, countries introduced a

plethora of new requirements on bank governance framework….

Post-crisis regulation around the world … Introduction What changed? What are likely impacts? What’s missing? Conclusion

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0 20 40 60 80

Other

Existence of a Board risk committee

Chief risk officer direct reporting line to theBoard or Board Committee

Independence of the Board

Executive compensation

Number of responses

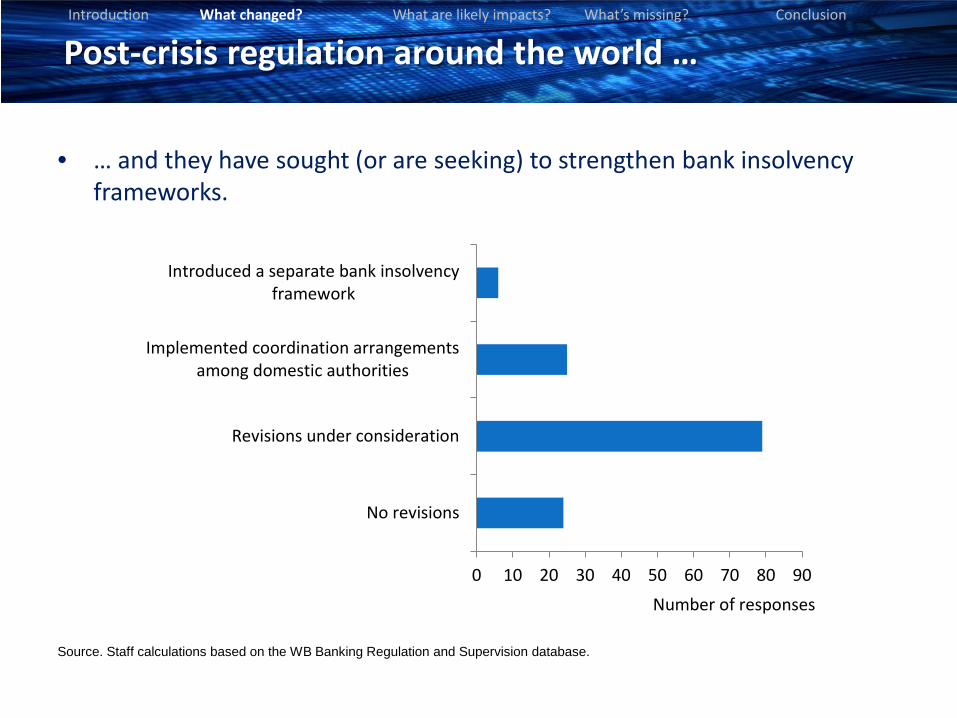

• … and they have sought (or are seeking) to strengthen bank insolvency frameworks.

Post-crisis regulation around the world … Introduction What changed? What are likely impacts? What’s missing? Conclusion

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0 10 20 30 40 50 60 70 80 90

No revisions

Revisions under consideration

Implemented coordination arrangementsamong domestic authorities

Introduced a separate bank insolvencyframework

Number of responses

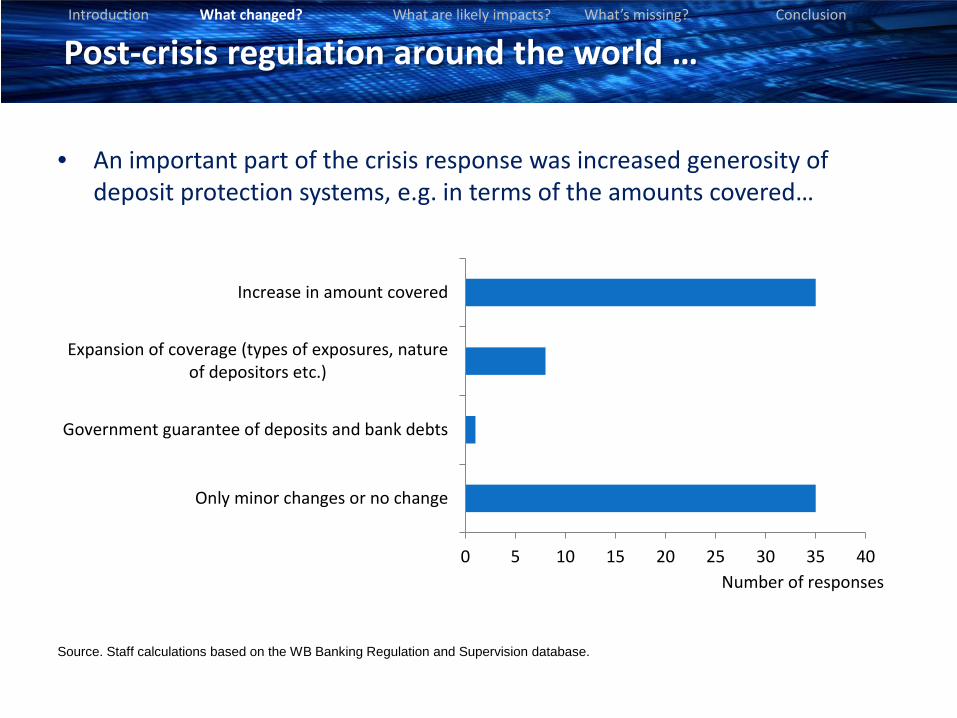

• An important part of the crisis response was increased generosity of deposit protection systems, e.g. in terms of the amounts covered…

Post-crisis regulation around the world … Introduction What changed? What are likely impacts? What’s missing? Conclusion

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0 5 10 15 20 25 30 35 40

Only minor changes or no change

Government guarantee of deposits and bank debts

Expansion of coverage (types of exposures, natureof depositors etc.)

Increase in amount covered

Number of responses

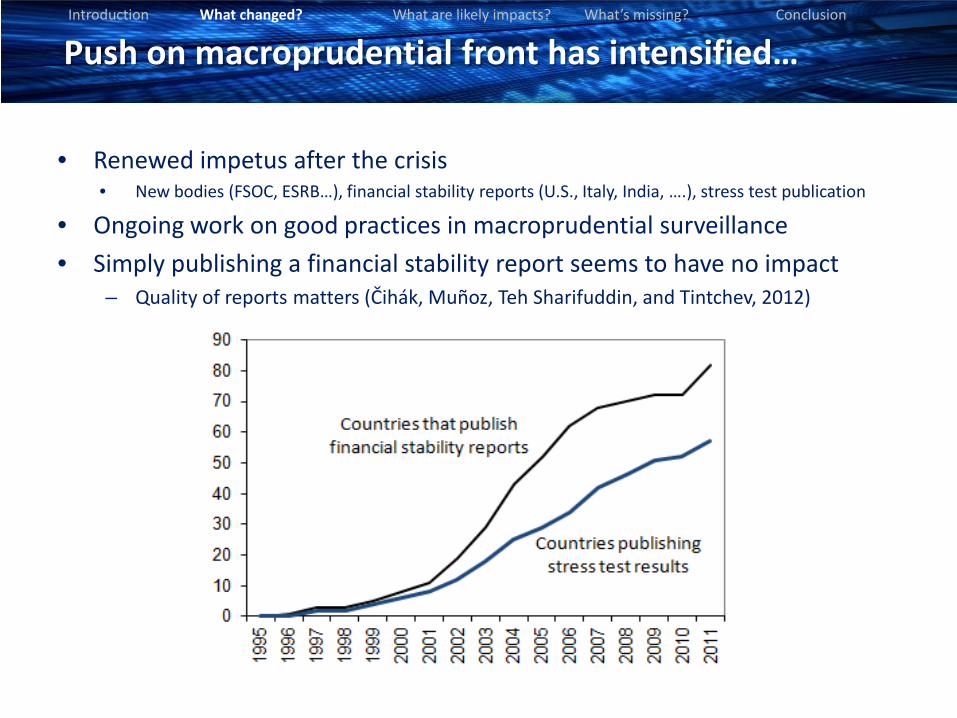

• Renewed impetus after the crisis • New bodies (FSOC, ESRB…), financial stability reports (U.S., Italy, India, ….), stress test publication

• Ongoing work on good practices in macroprudential surveillance • Simply publishing a financial stability report seems to have no impact

– Quality of reports matters (Čihák, Muñoz, Teh Sharifuddin, and Tintchev, 2012)

Push on macroprudential front has intensified… Introduction What changed? What are likely impacts? What’s missing? Conclusion

Push to implement new Basel rules continues… Introduction What changed? What are likely impacts? What’s missing? Conclusion

2000 2005 2010 2015 2020

Developed

Developing

median deviation

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0

10

20

30

40

50

60

70

80

90

100

StandardizedApproach

Foundation IRBApproach

Advanced IRBApproach

2007 survey

2011 survey

% o

f cou

ntrie

s ado

ptin

g Ba

sel I

I

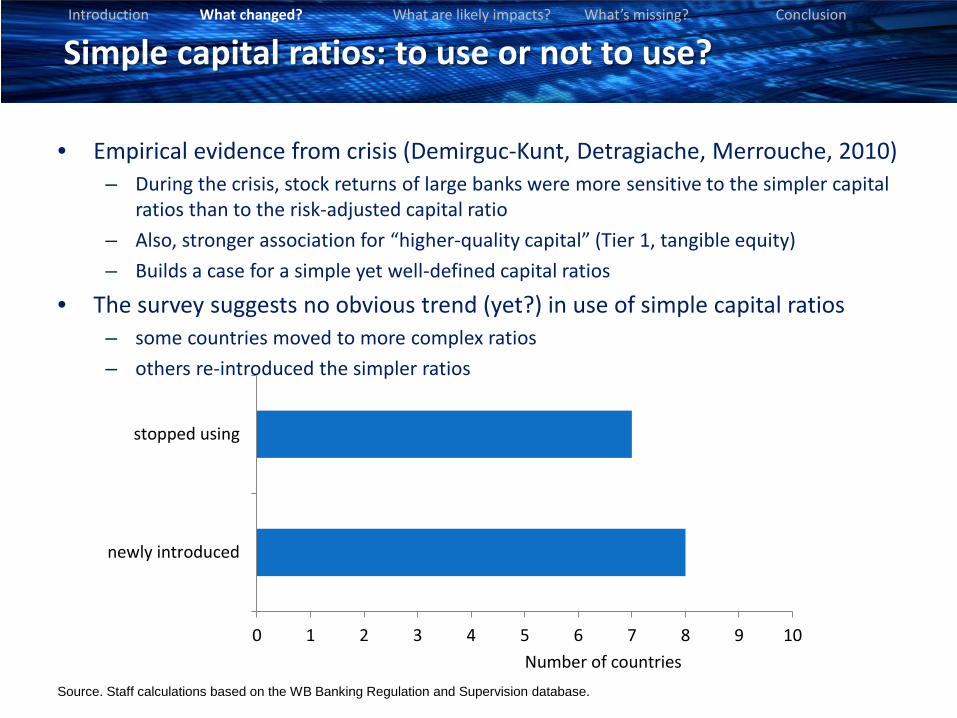

• Empirical evidence from crisis (Demirguc-Kunt, Detragiache, Merrouche, 2010) – During the crisis, stock returns of large banks were more sensitive to the simpler capital

ratios than to the risk-adjusted capital ratio – Also, stronger association for “higher-quality capital” (Tier 1, tangible equity) – Builds a case for a simple yet well-defined capital ratios

• The survey suggests no obvious trend (yet?) in use of simple capital ratios – some countries moved to more complex ratios – others re-introduced the simpler ratios

Simple capital ratios: to use or not to use? Introduction What changed? What are likely impacts? What’s missing? Conclusion

0 1 2 3 4 5 6 7 8 9 10

newly introduced

stopped using

Number of countries Source. Staff calculations based on the WB Banking Regulation and Supervision database.

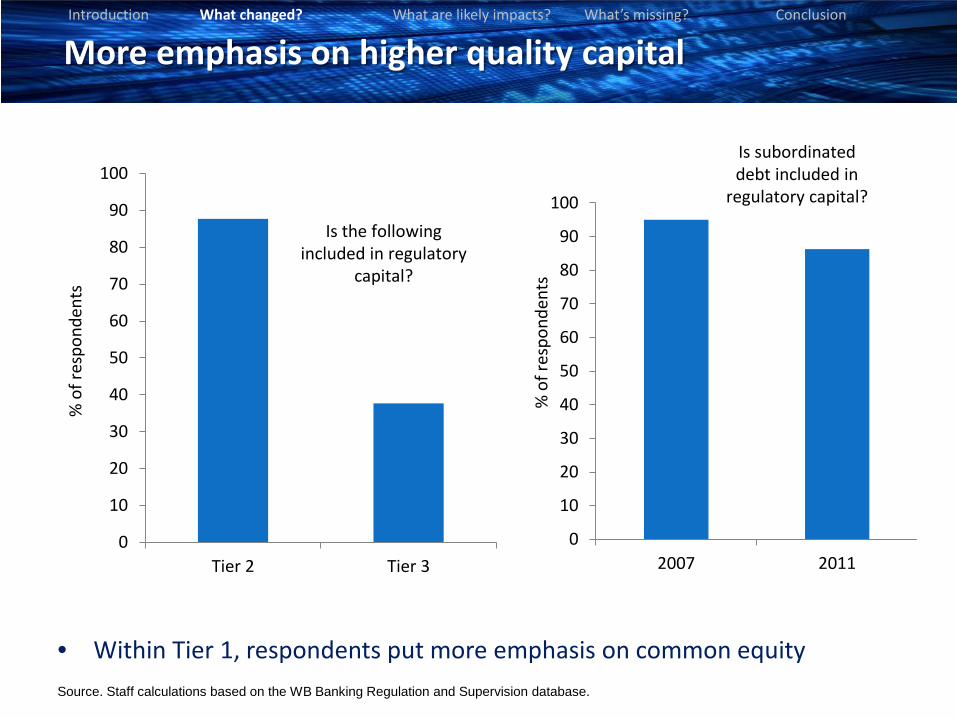

• Within Tier 1, respondents put more emphasis on common equity

More emphasis on higher quality capital Introduction What changed? What are likely impacts? What’s missing? Conclusion

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0

10

20

30

40

50

60

70

80

90

100

Tier 2 Tier 3

Is the following included in regulatory

capital?

% o

f res

pond

ents

0

10

20

30

40

50

60

70

80

90

100

2007 2011

Is subordinated debt included in

regulatory capital?

% o

f res

pond

ents

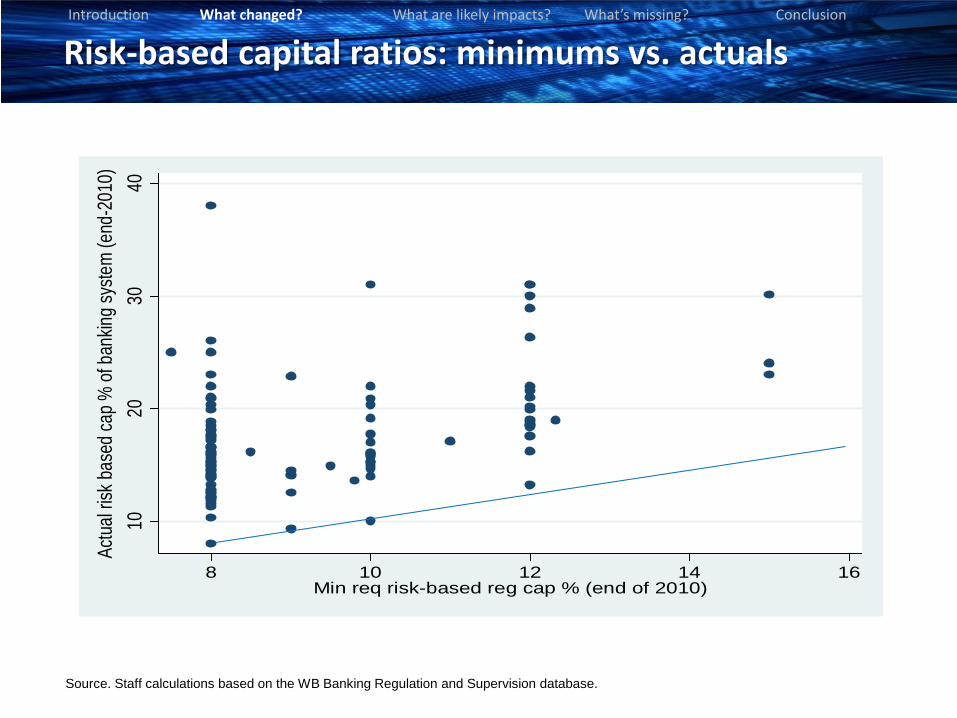

Risk-based capital ratios: minimums vs. actuals

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

Introduction What changed? What are likely impacts? What’s missing? Conclusion

1020

3040

Actua

l risk

base

d cap

% of

bank

ing sy

stem

(end

-201

0)

8 10 12 14 16Min req risk-based reg cap % (end of 2010)

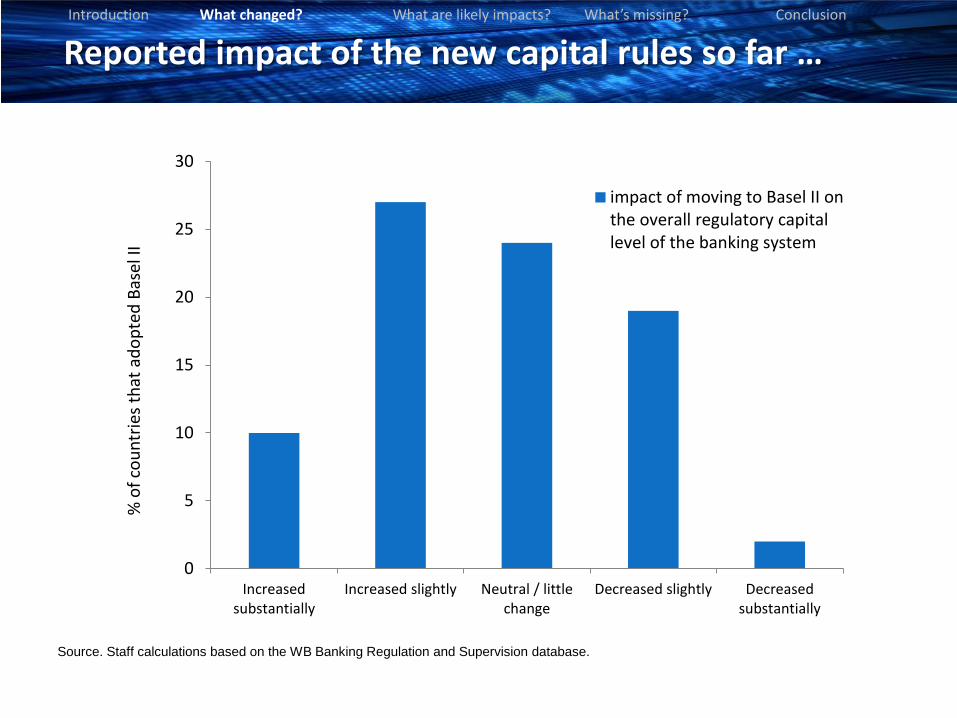

Reported impact of the new capital rules so far … Introduction What changed? What are likely impacts? What’s missing? Conclusion

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0

5

10

15

20

25

30

Increasedsubstantially

Increased slightly Neutral / littlechange

Decreased slightly Decreasedsubstantially

impact of moving to Basel II onthe overall regulatory capitallevel of the banking system

% o

f cou

ntrie

s tha

t ado

pted

Bas

el II

• Objective: Analyze the implications of the Basel III regulatory measures for emerging market

and developing countries

• Scope of the analysis

– Impact of Basel III capital requirements

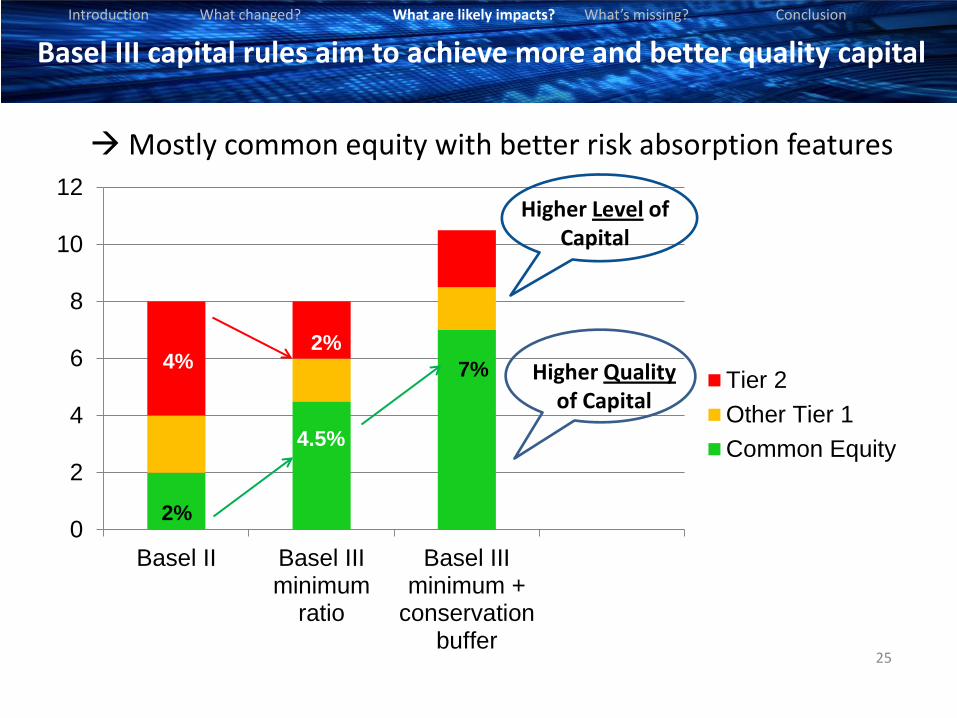

• Higher and better quality capital • Mostly common equity with loss absorbing features • Deductions from current core capital the amount of intangible and qualified assets that

have less loss-absorbing qualities • Such assets can be included in capital only up to 15 % • Implementation period: gradual phase in from 2013 with introduction of deductions

from 2014 to meet 7% common equity ratio (w/ conservation buffer) by 2019

– Impact of liquidity requirements (promote longer term funding of assets and reduce reliance on volatile, wholesale funding sources—Net Stable Funding Ratio (NSFR)

– No analysis of LCR (short term liquidity coverage ratio)—data issues

– No analysis of leverage ratio—data issues

• Caveats: Analysis very preliminary and incomplete – Used Bankscope data and company reports as a basis for the computations – Many missing data to be refined and explored and assumptions to be verified and

checked with staff with knowledge of specific country cases

What are the likely impacts of the new Basel rules? Introduction What changed? What are likely impacts? What’s missing? Conclusion

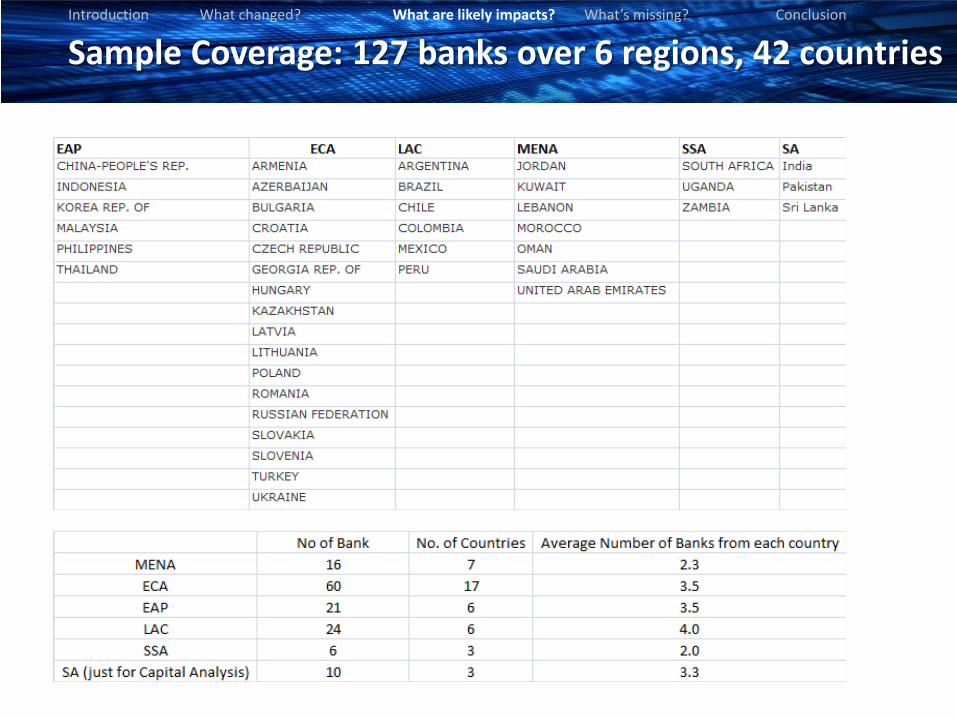

Sample Coverage: 127 banks over 6 regions, 42 countries Introduction What changed? What are likely impacts? What’s missing? Conclusion

25

0

2

4

6

8

10

12

Basel II Basel IIIminimum

ratio

Basel IIIminimum +

conservationbuffer

Tier 2Other Tier 1Common Equity

Higher Quality of Capital

Higher Level of Capital

4.5%

7% 4% 2%

2%

Basel III capital rules aim to achieve more and better quality capital

Mostly common equity with better risk absorption features

Introduction What changed? What are likely impacts? What’s missing? Conclusion

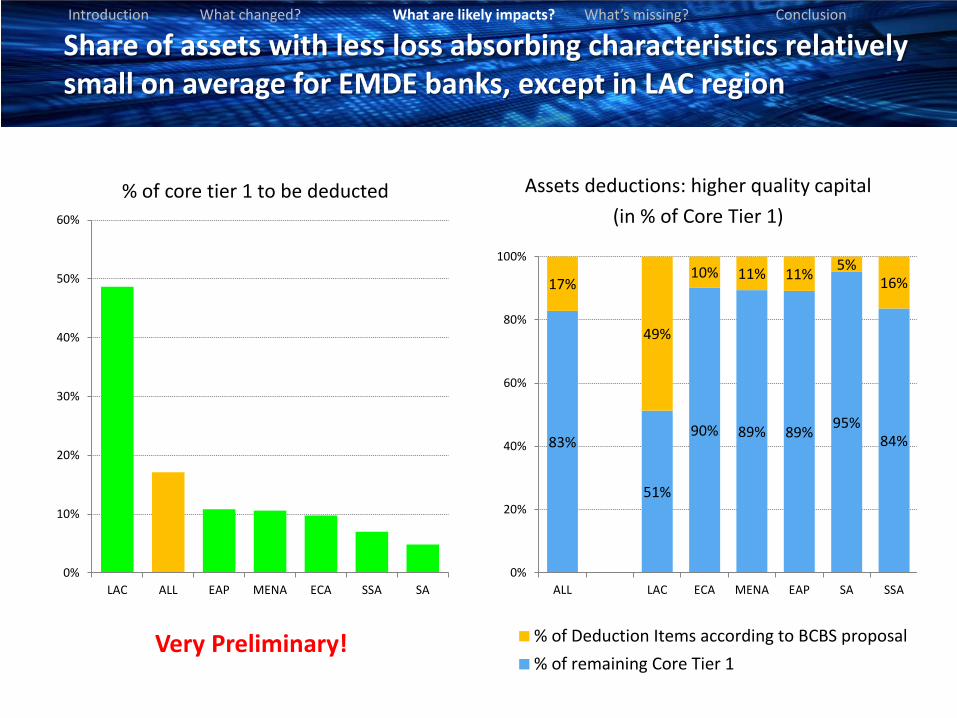

Share of assets with less loss absorbing characteristics relatively small on average for EMDE banks, except in LAC region

Assets deductions: higher quality capital (in % of Core Tier 1)

Introduction What changed? What are likely impacts? What’s missing? Conclusion

83%

51%

90% 89% 89% 95% 84%

17%

49%

10% 11% 11% 5% 16%

0%

20%

40%

60%

80%

100%

ALL LAC ECA MENA EAP SA SSA

% of Deduction Items according to BCBS proposal% of remaining Core Tier 1

Very Preliminary!

0%

10%

20%

30%

40%

50%

60%

LAC ALL EAP MENA ECA SSA SA

% of core tier 1 to be deducted

As a result, the needed increase in capital to meet the new capital requirements can be large for some regions

Introduction What changed? What are likely impacts? What’s missing? Conclusion

8.99%

1.54%

0.55%

6.90%

0.59%

7.49%

0%

2%

4%

6%

8%

10%

Core T1Ratio,

current

Deductions Increase inMkt RWA

Basel IIICore T1Ratio,

current

Cum.retainedearnings,2011-12

Basel IIICore Ratio,

2012

Impact of Basel Regulation on Core Capital Ratio by end 2012, sample average

Current and adjusted capital ratios, with and without retained earnings

Very Preliminary!

Capital declines by 1.5 pp

9.0% 9.5%

11.6% 11.5%

8.2% 8.3%

9.4%

6.9%

4.5%

9.5% 9.5%

6.8% 7.4%

8.1%

7.5%

5.2%

10.5% 10.7%

7.2% 7.8%

9.1%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

ALL LAC ECA MENA EAP SA SSA

Core Tier 1 Ratio Basel III Core Ratio, 2010New Basle III Core Ratio, 2012

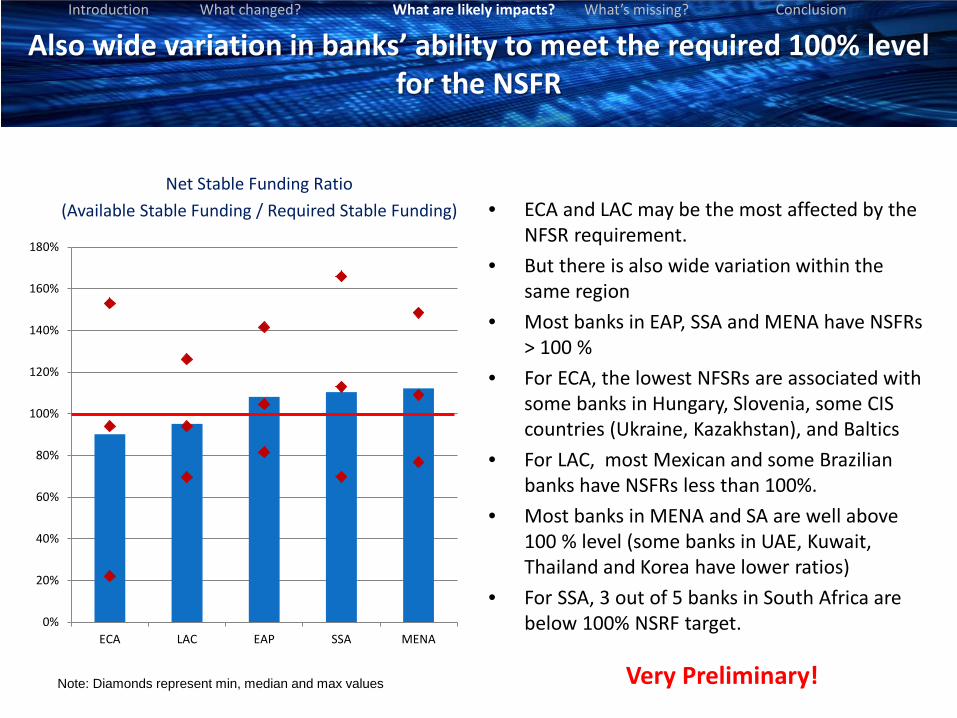

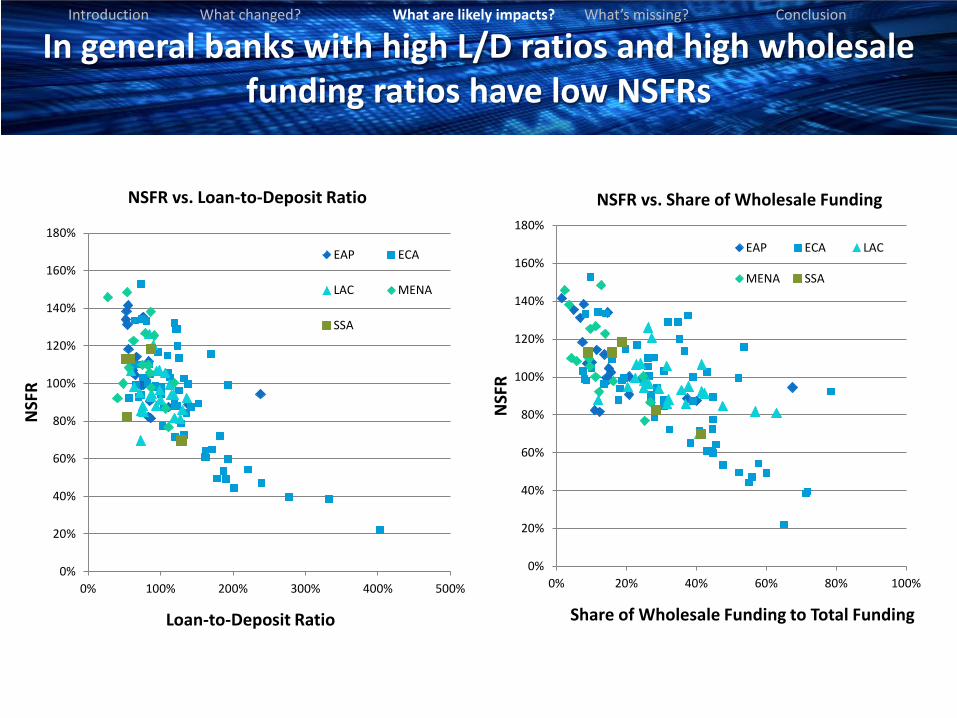

Also wide variation in banks’ ability to meet the required 100% level for the NSFR

Net Stable Funding Ratio (Available Stable Funding / Required Stable Funding)

• ECA and LAC may be the most affected by the NFSR requirement.

• But there is also wide variation within the same region

• Most banks in EAP, SSA and MENA have NSFRs > 100 %

• For ECA, the lowest NFSRs are associated with some banks in Hungary, Slovenia, some CIS countries (Ukraine, Kazakhstan), and Baltics

• For LAC, most Mexican and some Brazilian banks have NSFRs less than 100%.

• Most banks in MENA and SA are well above 100 % level (some banks in UAE, Kuwait, Thailand and Korea have lower ratios)

• For SSA, 3 out of 5 banks in South Africa are below 100% NSRF target.

Note: Diamonds represent min, median and max values

Introduction What changed? What are likely impacts? What’s missing? Conclusion

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

ECA LAC EAP SSA MENA

Very Preliminary!

In general banks with high L/D ratios and high wholesale funding ratios have low NSFRs

Introduction What changed? What are likely impacts? What’s missing? Conclusion

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

0% 100% 200% 300% 400% 500%

NSF

R

Loan-to-Deposit Ratio

NSFR vs. Loan-to-Deposit Ratio

EAP ECA

LAC MENA

SSA

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

0% 20% 40% 60% 80% 100%

NSF

R

Share of Wholesale Funding to Total Funding

NSFR vs. Share of Wholesale Funding

EAP ECA LAC

MENA SSA

• Basel III may have varying degrees of impact on EMDEs across regions, with

wide variations also within a given region.

• ECA and LAC regions seem to be the most vulnerable to the LT liquidity requirement (NSFR), where dependence on wholesale funding (ECA) or Loan to Deposit ratios are high (ECA and some LAC). However, other factors may also affect the level of NSFR (e.g., different amounts of government securities in asset portfolios—low levels may result in low NSFRs)

• Further challenges may be ahead in meeting the NSFR requirement: e.g., upcoming rollover needs of European banks and sovereigns may raise the cost of term funding and result in competition for deposits. There are also challenges associated with holding high levels of (liquid) government securities: this would help in meeting the NSFR target but expose the bank to higher sovereign risk

• These findings should be interpreted with caution. The analysis is very preliminary and is subject to significant data problems. Lack of available data and benchmarks for the analysis also calls for further analysis of the assumptions used in the computations.

What do these estimates tell us about Basel III impacts? Introduction What changed? What are likely impacts? What’s missing? Conclusion

What are some of the risks with the response?

• Implementation – Resources – Partial responses – National priorities versus level playing field – Need for flexibility

• Design – Basel framework, despite recent improvements, is still primarily a micro prudential

regulatory response (“raise bank capital standards”), not explicitly founded in optimal control theory and likely to fail as conditions change

– Economic theory identifies fundamental sources of weakness : • Asymmetric information • Perverse incentives.

– Missing in Basel is explicit assessment of sources of market failures/externalities – FSB agenda has begun to incorporate elements to address perverse incentives and

asymmetric information --e.g., compensation practices, moral hazard in SIFIs, and information gaps

Introduction What changed? What are likely impacts? What’s missing? Conclusion

Alternative framework for financial system oversight

• Alternative approach would move issues of asymmetric information and incentives to center of the regulatory framework.

• Alternative is an evolution of existing approaches but has a different emphasis

• Asymmetric information: – Enhanced disclosures (examples):

• Major counterparty and sectoral exposures of the firm • Benchmarks for the evaluation of the models used to value assets and risk exposures.

– Permit investors /creditors to assess directly the solvency/liquidity of financial institutions and not rely on Basel -- potentially multiple measures that can evolve as conditions change

– Allows simplification of regulatory measures

• Incentive issues: – adverse selection, moral hazard, principal-agent and monitoring problems, rational

herding, ad contagion -- supported by wide academic literature – The identification of incentive problems would require a specific analysis of incentives --

an incentive audit

Introduction What changed? What are likely impacts? What’s missing? Conclusion

Outline of an incentive audit

• Approach would need to be evolved but elements could include: – underlying legal, institutional and regulatory environment; – ownership and governance structure of financial institutions; – compensation practices; – conflicts of interest; – explicit and implicit guarantees.

• Audit could be conducted through a sequenced analysis that would proceed from higher level to progressively more detailed questions that would identify for the particular environment the relevant incentives that motivate decision making.

• Sequenced approach would enable the audit to drill down and identify factors that could lead to market failures and excessive risk taking in the particular environment (Chai and Johnston 2000)

• Incentive audits would become a key part of the financial stability analysis and FSAPs.

Introduction What changed? What are likely impacts? What’s missing? Conclusion

Differences compared with existing approaches

• Clearly delineates the responsibilities of public bodies (market failures/externalities/systemic risk) and those of private investors (risks in individual firms, contracts and instruments).

• Focuses on addressing failures creates less incentives for regulatory arbitrage. • Rebalancing use of public resources away from micro management of risk and

capital adequacy in financial institutions to one that focused on the sufficiency of information disclosures, factors that influence the incentives to monitor activities, corporate governance, conflicts of interest, explicit and implicit guarantees etc.

• Potentially better attuned to a country's circumstances (an incentive based approach starts with an analysis of the structural characteristics of the individual country, and drills down to identify the sources of perverse incentives/market failure in that specific context; regulatory solutions tailored to the country's circumstances).

• Focus on incentives provides a framework to integrate the different branches of policies that impact the financial system, specifically: (1) financial regulation and supervision; (2) crisis management and safety net arrangements; and (3) competition policy.

Introduction What changed? What are likely impacts? What’s missing? Conclusion

Incentive audits: practical/implementation issues Incentive issues and macroprudential policy

• Alternative approach would be consistent and can inform the new emphasis on a macroprudential approach.

• The development of macroprudential approaches is still at an early stage and so far has emphasized the use of prudential tools to address systemic risk (FSB/IMF/BIS 2011).

• Under the alternative approach financial regulatory policy should be directed towards the fundamental sources of weakness.

• Macroprudential policy would have the aims of identifying and mitigating systemic risk, and should have the capacity to look beyond systemic risk, to identify and address the fundamental sources that give rise to it :

– Asymmetric information and perverse incentives – Market failures due to negative externalities that give rise to systemic risk – Failures in regulatory and supervisory practices – Failures in crisis management arrangement

Introduction What changed? What are likely impacts? What’s missing? Conclusion

Incentive audits: practical/implementation issues Differences in policy responses

• Difference of approach would be in the assessment tools and policy response. • For example FSB/IMF/BIS (2011) recommends dealing with systemic risk by building

capital and liquidity buffers to enhance resiliency (on SIFS to deal with risks in interconnections and pro cyclical buffers to deal with pro cyclicality)

• The alternative framework would identify and correct the incentive distortions/ information frictions that contribute to the buildup of excessive risk at source e.g.

• In interconnectedness: – serious information gaps that prevented the assessment of exposures and

network risks; – incentives in the micro prudential regulations that encouraged risk transfers; – moral hazard associated with the failure of the crisis management

• In pro-cyclicality: – distortions created by the risk weightings on different types of loans; – procedures for the calibration of risk models, provisioning policies, the valuation

of collateral etc; – compensation policies that reward short-term performance; and – incentives to take on excessive debt created by tax system, bankruptcy

procedures, etc

• Central to the different approaches is the question of the effectiveness of the response: would it be possible to mitigate systemic risk without addressing the underlying failures and incentives that give rise to it?

Introduction What changed? What are likely impacts? What’s missing? Conclusion

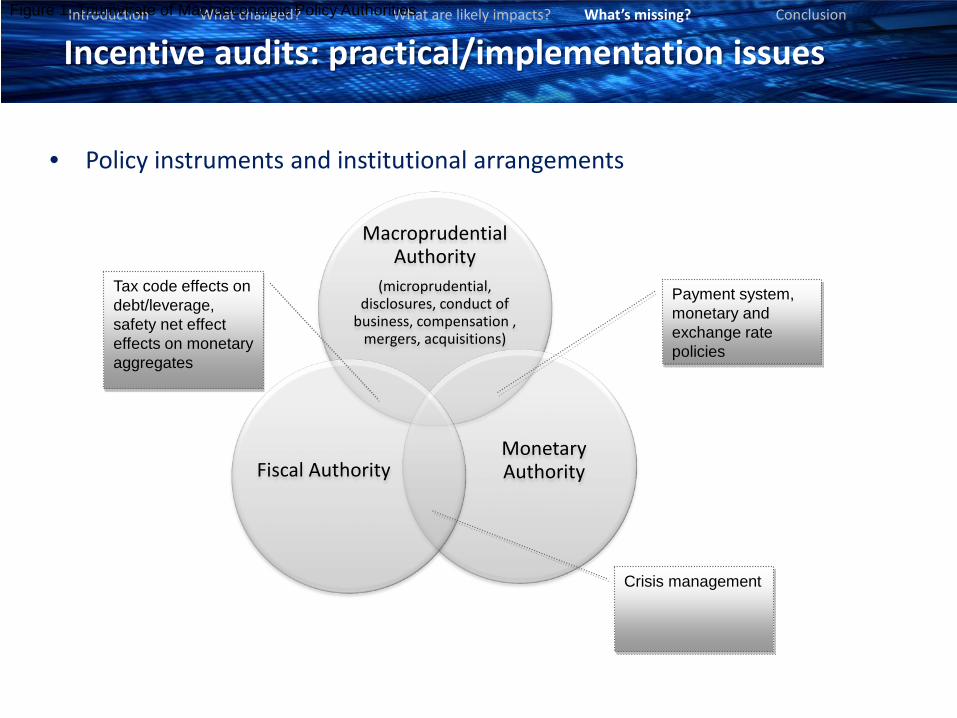

Incentive audits: practical/implementation issues Policy instruments

• The main policy instruments under the alternative approach would be instruments to correct "failures" in the financial system. The scope of the potential failures is potentially very broad and only a subset could be under the direct control of the macroprudential authority. The following instruments could be considered: – micro prudential tools (capital and liquidity requirements, provisioning and

collateral policies, prompt corrective action) tailored to address systemic risks; – disclosure requirements that could be graduated depending on the threat to

systemic risk and which would cover both regulated and unregulated entities; – conduct of business rules, intended to address conflicts of interest and

transparency of financial transactions, to be applied to all financial firms, agents, auditors and rating agencies;

– compensation practices in financial firms that pose a threat to systemic stability; – mergers and acquisitions involving financial firms that pose or potentially pose a

threat to financial stability; – cease and desist orders covering both regulated and unregulated entities

intended to deal with threats to systemic stability; and – resolution regimes for financial firms intended to address moral hazard .

• There would need to be a mechanism for coordination with other policies that impact incentives and systemic risk, especially central banking and fiscal policies

Introduction What changed? What are likely impacts? What’s missing? Conclusion

Incentive audits: practical/implementation issues

• Policy instruments and institutional arrangements

Introduction What changed? What are likely impacts? What’s missing? Conclusion

Macroprudential Authority

(microprudential, disclosures, conduct of

business, compensation , mergers, acquisitions)

Monetary Authority

Fiscal Authority

Payment system, monetary and exchange rate policies

Crisis management

Tax code effects on debt/leverage, safety net effect effects on monetary aggregates

Figure 1. Triumvirate of Macroeconomic Policy Authorities

Conclusion

• It would be wrong to conclude from the recent crisis experience that just "regulating more" is the way to go.

– Regulatory efficiency and regulatory gaps are the real issue. – Market discipline and regulatory/supervisory discipline are complementary (when

regulation is ineffective or has gaps, market discipline breaks down )

• It would be also wrong to conclude that more complex regulations, such as more complex systems to calculate risk-weighted asset ratios, are necessarily better than simpler ratios.

• Complicated regulations are trying to mimic markets in estimating economic capital required by each institution commensurate with its risk, but they may end up leading to regulatory arbitrage and manipulated ratios.

• More fundamentally, changes in ratios are unlikely to address the underlying failures in economic incentives that led to the global financial crisis.

Introduction What changed? What are likely impacts? What’s missing? Conclusion

Conclusion

• We call for a bolder re-orientation of the regulatory approach, so that it has at its core identification of incentive problems on an on-going basis.

• The challenge of financial sector regulation is to align private incentives with public interest without taxing or subsidizing private risk-taking.

• Credible threats of market entry and exit, healthy competition, and disclosure of quality information are essential in getting this balance right.

Introduction What changed? What are likely impacts? What’s missing? Conclusion

Conclusion

• Specifically, we propose “incentive audits” as a tool to help identify and address perverse incentives faced by financial institutions, market participants, regulators, supervisors and politicians, before they give rise to systemic risk.

• These audits need to be combined with some basic but well-defined capital and liquidity ratios (more difficult for market participants to circumvent), strong enforcement of transparency and use of complementary market signals.

• In this context, transparency does not mean simply more mindless reporting. what matter is not the sheer volume of information, but the clarity and comparability of the disclosures.

Introduction What changed? What are likely impacts? What’s missing? Conclusion

Thank you for your comments and suggestions!

Global Financial Development Report 2013 GFDR Seminar

(Additional slides included for your information)

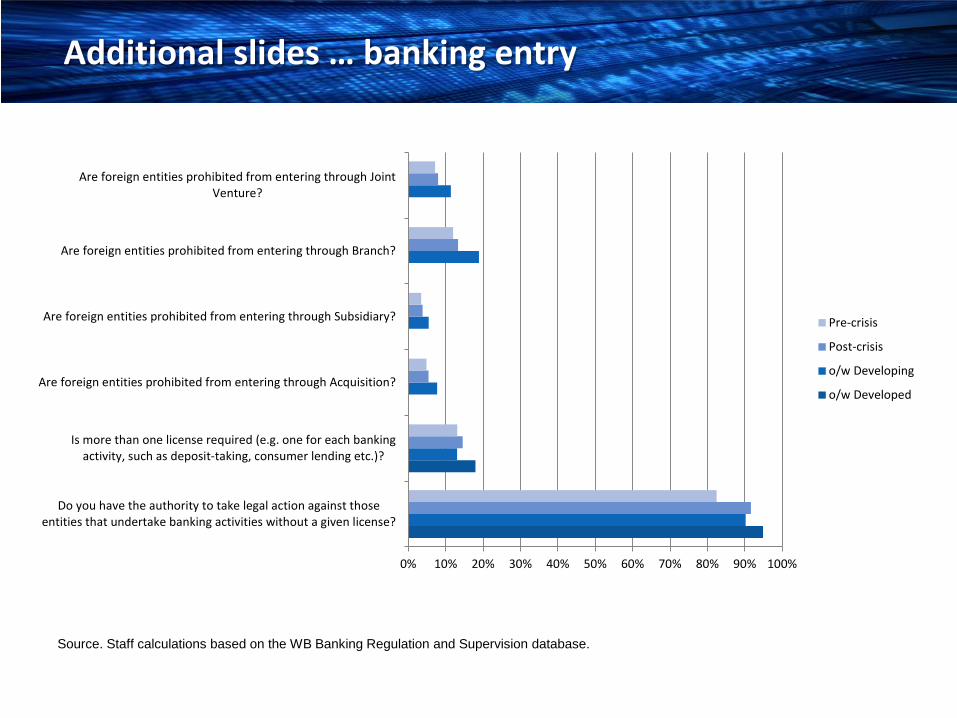

Additional slides … banking entry

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Do you have the authority to take legal action against thoseentities that undertake banking activities without a given license?

Is more than one license required (e.g. one for each bankingactivity, such as deposit-taking, consumer lending etc.)?

Are foreign entities prohibited from entering through Acquisition?

Are foreign entities prohibited from entering through Subsidiary?

Are foreign entities prohibited from entering through Branch?

Are foreign entities prohibited from entering through JointVenture?

Pre-crisis

Post-crisis

o/w Developing

o/w Developed

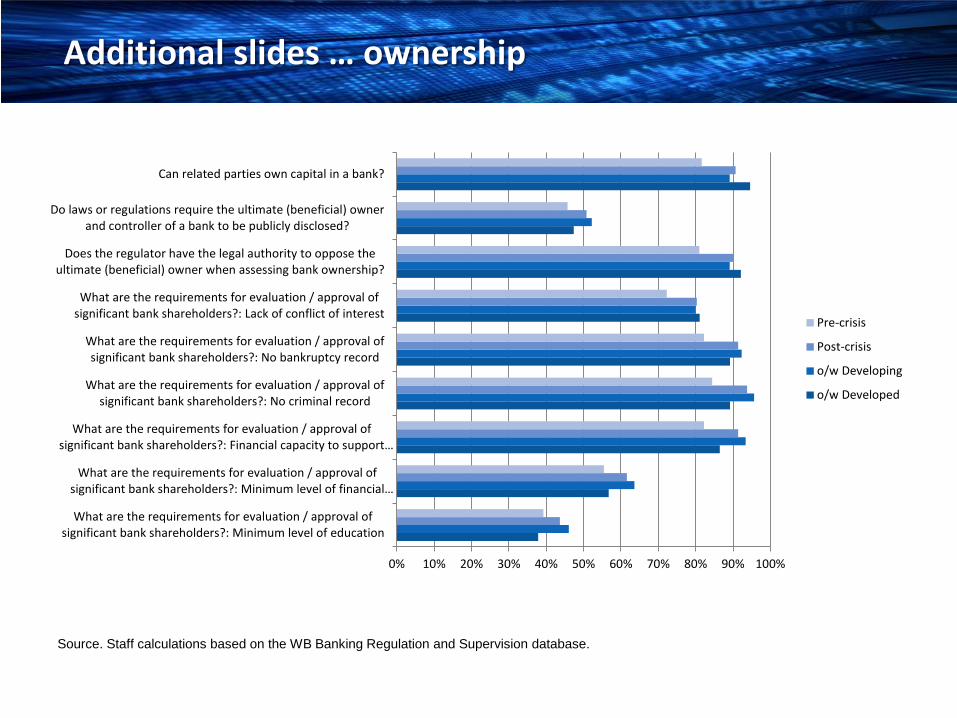

Additional slides … ownership

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

What are the requirements for evaluation / approval ofsignificant bank shareholders?: Minimum level of education

What are the requirements for evaluation / approval ofsignificant bank shareholders?: Minimum level of financial…

What are the requirements for evaluation / approval ofsignificant bank shareholders?: Financial capacity to support…

What are the requirements for evaluation / approval ofsignificant bank shareholders?: No criminal record

What are the requirements for evaluation / approval ofsignificant bank shareholders?: No bankruptcy record

What are the requirements for evaluation / approval ofsignificant bank shareholders?: Lack of conflict of interest

Does the regulator have the legal authority to oppose theultimate (beneficial) owner when assessing bank ownership?

Do laws or regulations require the ultimate (beneficial) ownerand controller of a bank to be publicly disclosed?

Can related parties own capital in a bank?

Pre-crisis

Post-crisis

o/w Developing

o/w Developed

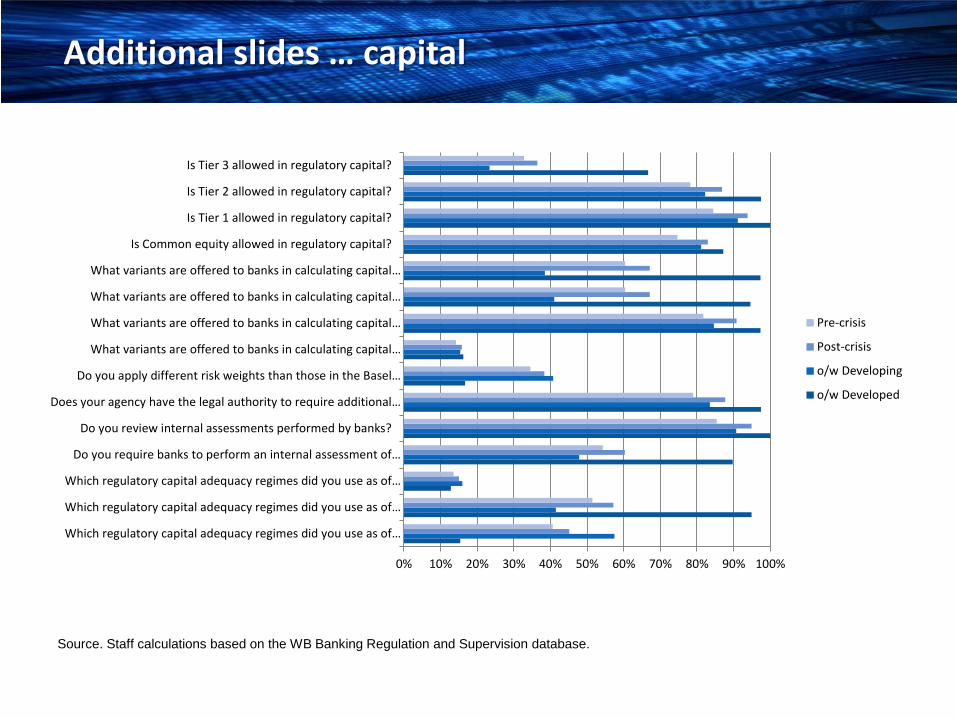

Additional slides … capital

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Which regulatory capital adequacy regimes did you use as of…

Which regulatory capital adequacy regimes did you use as of…

Which regulatory capital adequacy regimes did you use as of…

Do you require banks to perform an internal assessment of…

Do you review internal assessments performed by banks?

Does your agency have the legal authority to require additional…

Do you apply different risk weights than those in the Basel…

What variants are offered to banks in calculating capital…

What variants are offered to banks in calculating capital…

What variants are offered to banks in calculating capital…

What variants are offered to banks in calculating capital…

Is Common equity allowed in regulatory capital?

Is Tier 1 allowed in regulatory capital?

Is Tier 2 allowed in regulatory capital?

Is Tier 3 allowed in regulatory capital?

Pre-crisis

Post-crisis

o/w Developing

o/w Developed

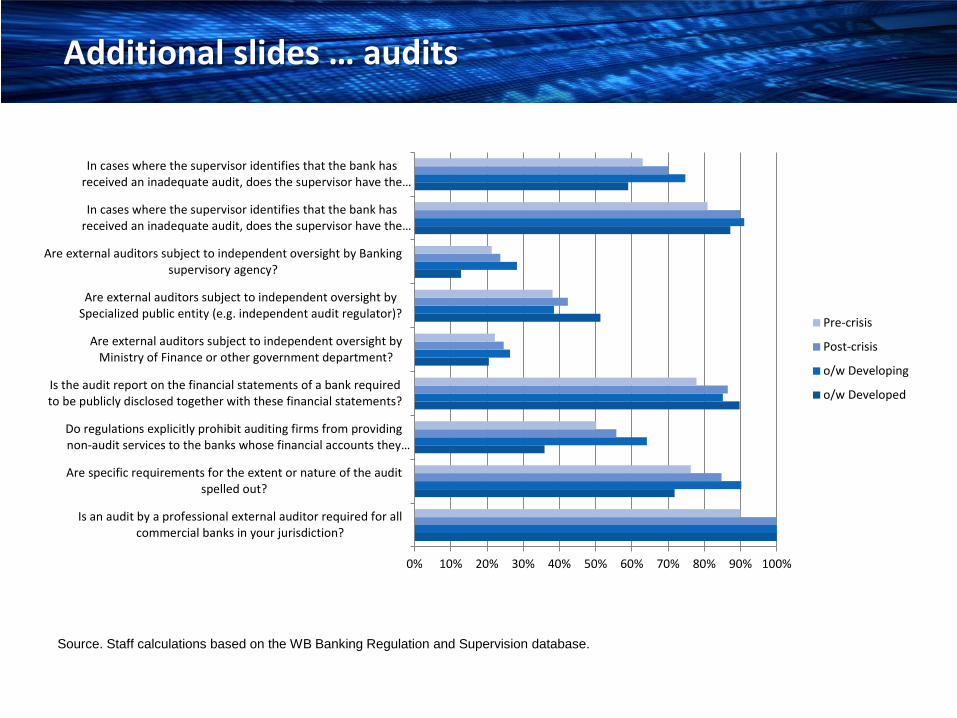

Additional slides … audits

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Is an audit by a professional external auditor required for allcommercial banks in your jurisdiction?

Are specific requirements for the extent or nature of the auditspelled out?

Do regulations explicitly prohibit auditing firms from providingnon-audit services to the banks whose financial accounts they…

Is the audit report on the financial statements of a bank requiredto be publicly disclosed together with these financial statements?

Are external auditors subject to independent oversight byMinistry of Finance or other government department?

Are external auditors subject to independent oversight bySpecialized public entity (e.g. independent audit regulator)?

Are external auditors subject to independent oversight by Bankingsupervisory agency?

In cases where the supervisor identifies that the bank hasreceived an inadequate audit, does the supervisor have the…

In cases where the supervisor identifies that the bank hasreceived an inadequate audit, does the supervisor have the…

Pre-crisis

Post-crisis

o/w Developing

o/w Developed

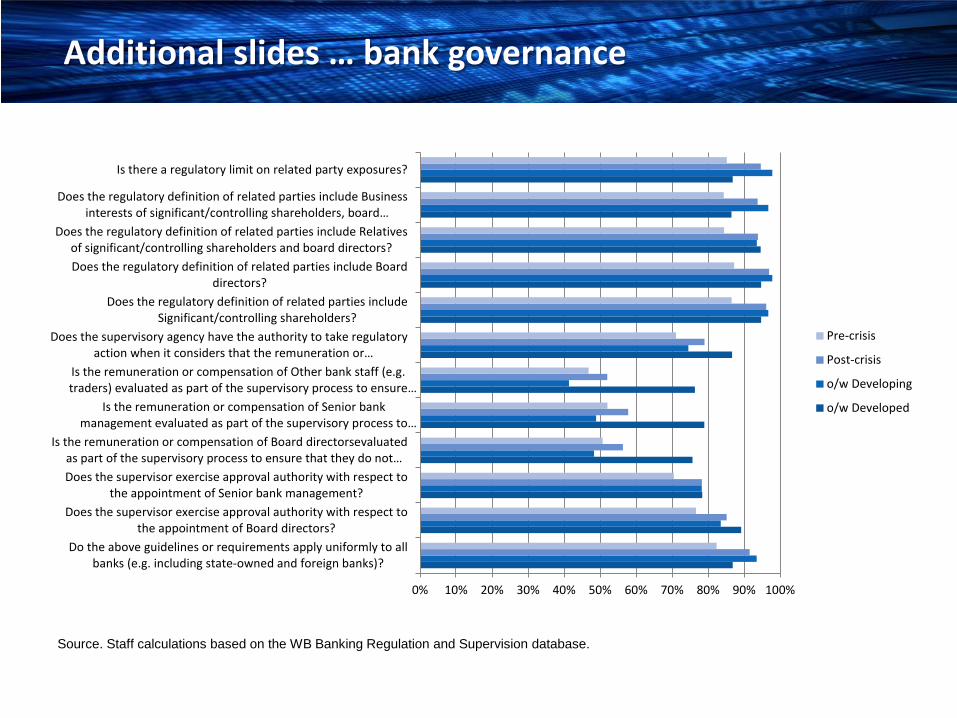

Additional slides … bank governance

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Do the above guidelines or requirements apply uniformly to allbanks (e.g. including state-owned and foreign banks)?

Does the supervisor exercise approval authority with respect tothe appointment of Board directors?

Does the supervisor exercise approval authority with respect tothe appointment of Senior bank management?

Is the remuneration or compensation of Board directorsevaluatedas part of the supervisory process to ensure that they do not…

Is the remuneration or compensation of Senior bankmanagement evaluated as part of the supervisory process to…

Is the remuneration or compensation of Other bank staff (e.g.traders) evaluated as part of the supervisory process to ensure…

Does the supervisory agency have the authority to take regulatoryaction when it considers that the remuneration or…

Does the regulatory definition of related parties includeSignificant/controlling shareholders?

Does the regulatory definition of related parties include Boarddirectors?

Does the regulatory definition of related parties include Relativesof significant/controlling shareholders and board directors?

Does the regulatory definition of related parties include Businessinterests of significant/controlling shareholders, board…

Is there a regulatory limit on related party exposures?

Pre-crisis

Post-crisis

o/w Developing

o/w Developed

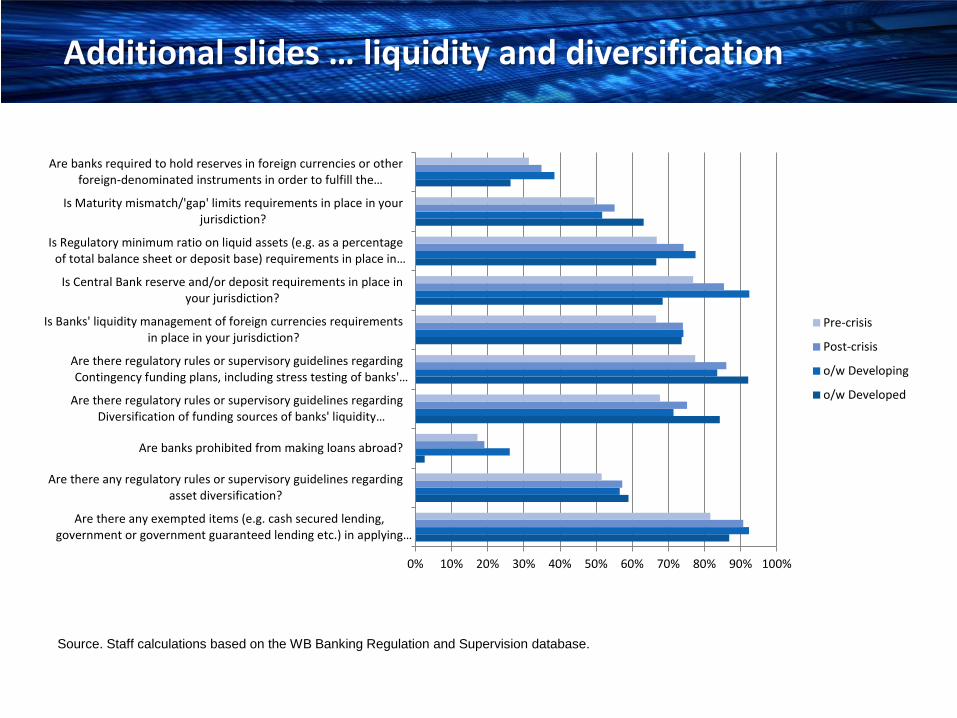

Additional slides … liquidity and diversification

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Are there any exempted items (e.g. cash secured lending,government or government guaranteed lending etc.) in applying…

Are there any regulatory rules or supervisory guidelines regardingasset diversification?

Are banks prohibited from making loans abroad?

Are there regulatory rules or supervisory guidelines regardingDiversification of funding sources of banks' liquidity…

Are there regulatory rules or supervisory guidelines regardingContingency funding plans, including stress testing of banks'…

Is Banks' liquidity management of foreign currencies requirementsin place in your jurisdiction?

Is Central Bank reserve and/or deposit requirements in place inyour jurisdiction?

Is Regulatory minimum ratio on liquid assets (e.g. as a percentageof total balance sheet or deposit base) requirements in place in…

Is Maturity mismatch/'gap' limits requirements in place in yourjurisdiction?

Are banks required to hold reserves in foreign currencies or otherforeign-denominated instruments in order to fulfill the…

Pre-crisis

Post-crisis

o/w Developing

o/w Developed

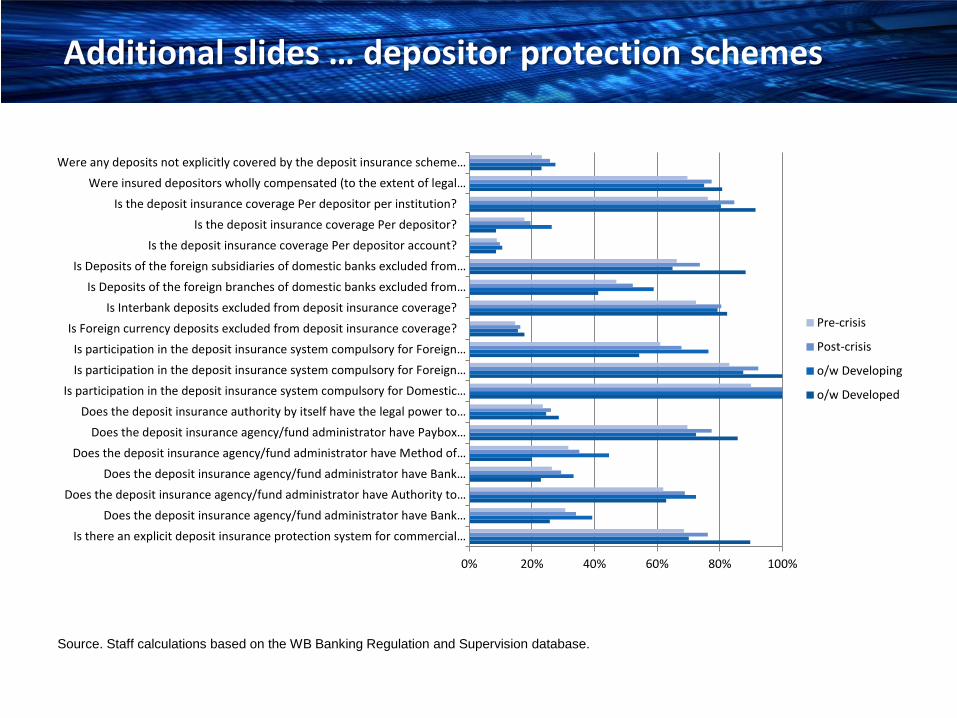

Additional slides … depositor protection schemes

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0% 20% 40% 60% 80% 100%

Is there an explicit deposit insurance protection system for commercial…Does the deposit insurance agency/fund administrator have Bank…

Does the deposit insurance agency/fund administrator have Authority to…Does the deposit insurance agency/fund administrator have Bank…

Does the deposit insurance agency/fund administrator have Method of…Does the deposit insurance agency/fund administrator have Paybox…

Does the deposit insurance authority by itself have the legal power to…Is participation in the deposit insurance system compulsory for Domestic…

Is participation in the deposit insurance system compulsory for Foreign…Is participation in the deposit insurance system compulsory for Foreign…

Is Foreign currency deposits excluded from deposit insurance coverage?Is Interbank deposits excluded from deposit insurance coverage?

Is Deposits of the foreign branches of domestic banks excluded from…Is Deposits of the foreign subsidiaries of domestic banks excluded from…

Is the deposit insurance coverage Per depositor account?Is the deposit insurance coverage Per depositor?

Is the deposit insurance coverage Per depositor per institution?Were insured depositors wholly compensated (to the extent of legal…

Were any deposits not explicitly covered by the deposit insurance scheme…

Pre-crisis

Post-crisis

o/w Developing

o/w Developed

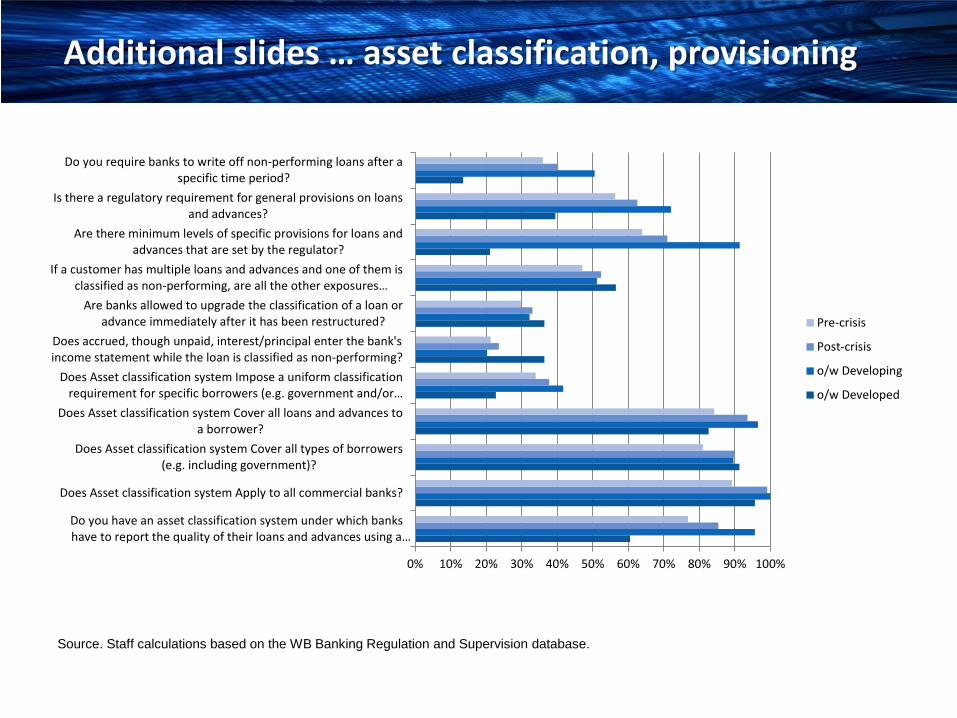

Additional slides … asset classification, provisioning

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Do you have an asset classification system under which bankshave to report the quality of their loans and advances using a…

Does Asset classification system Apply to all commercial banks?

Does Asset classification system Cover all types of borrowers(e.g. including government)?

Does Asset classification system Cover all loans and advances toa borrower?

Does Asset classification system Impose a uniform classificationrequirement for specific borrowers (e.g. government and/or…

Does accrued, though unpaid, interest/principal enter the bank'sincome statement while the loan is classified as non-performing?

Are banks allowed to upgrade the classification of a loan oradvance immediately after it has been restructured?

If a customer has multiple loans and advances and one of them isclassified as non-performing, are all the other exposures…

Are there minimum levels of specific provisions for loans andadvances that are set by the regulator?

Is there a regulatory requirement for general provisions on loansand advances?

Do you require banks to write off non-performing loans after aspecific time period?

Pre-crisis

Post-crisis

o/w Developing

o/w Developed

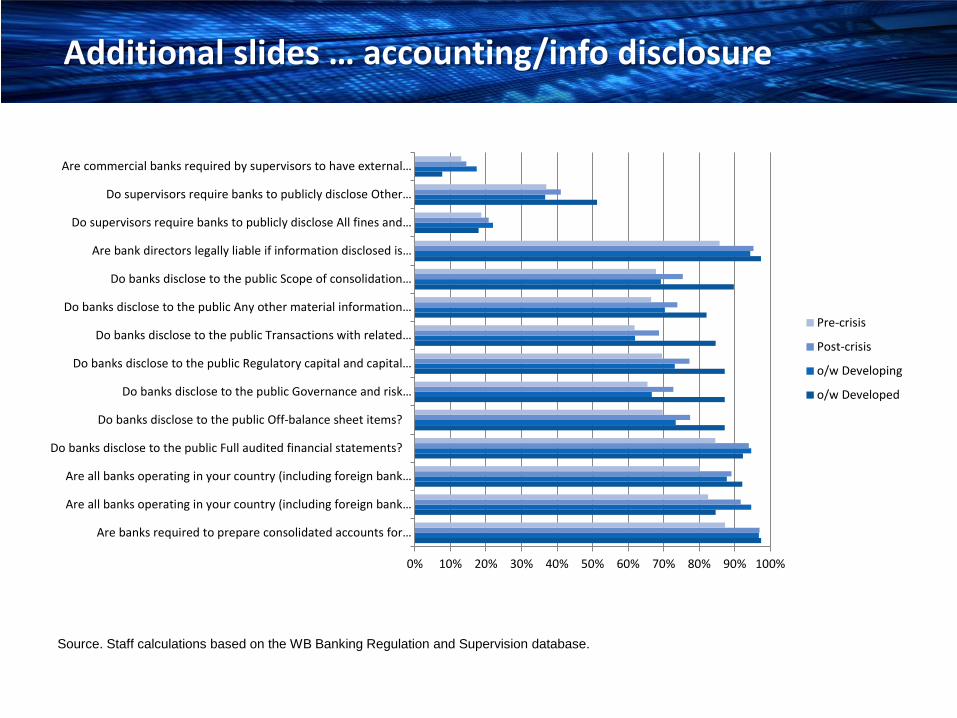

Additional slides … accounting/info disclosure

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Are banks required to prepare consolidated accounts for…

Are all banks operating in your country (including foreign bank…

Are all banks operating in your country (including foreign bank…

Do banks disclose to the public Full audited financial statements?

Do banks disclose to the public Off-balance sheet items?

Do banks disclose to the public Governance and risk…

Do banks disclose to the public Regulatory capital and capital…

Do banks disclose to the public Transactions with related…

Do banks disclose to the public Any other material information…

Do banks disclose to the public Scope of consolidation…

Are bank directors legally liable if information disclosed is…

Do supervisors require banks to publicly disclose All fines and…

Do supervisors require banks to publicly disclose Other…

Are commercial banks required by supervisors to have external…

Pre-crisis

Post-crisis

o/w Developing

o/w Developed

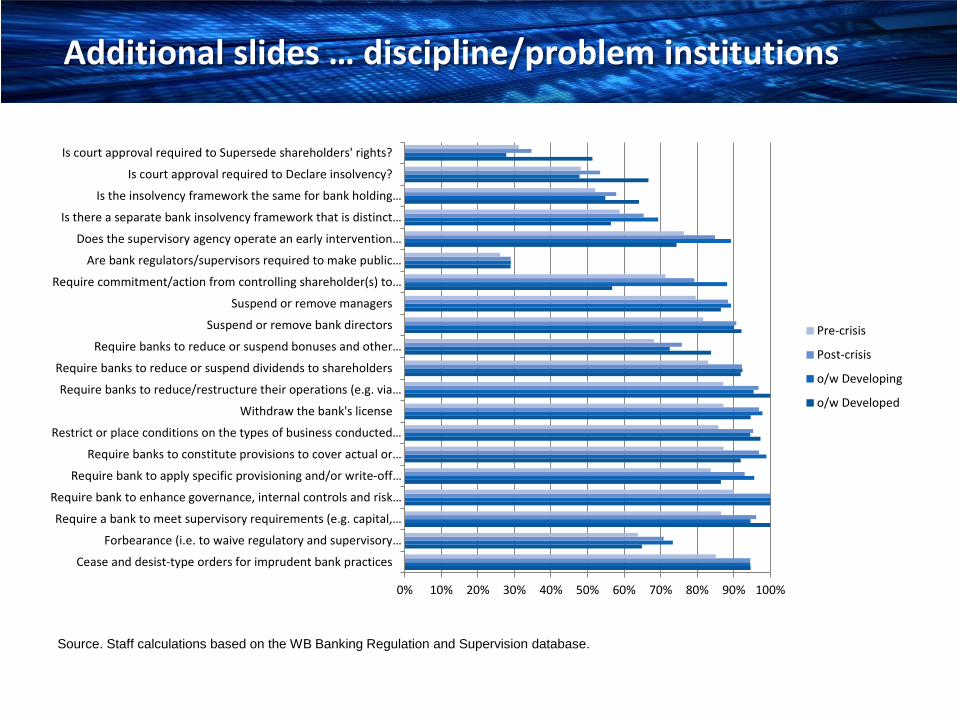

Additional slides … discipline/problem institutions

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Cease and desist-type orders for imprudent bank practices

Forbearance (i.e. to waive regulatory and supervisory…

Require a bank to meet supervisory requirements (e.g. capital,…

Require bank to enhance governance, internal controls and risk…

Require bank to apply specific provisioning and/or write-off…

Require banks to constitute provisions to cover actual or…

Restrict or place conditions on the types of business conducted…

Withdraw the bank's license

Require banks to reduce/restructure their operations (e.g. via…

Require banks to reduce or suspend dividends to shareholders

Require banks to reduce or suspend bonuses and other…

Suspend or remove bank directors

Suspend or remove managers

Require commitment/action from controlling shareholder(s) to…

Are bank regulators/supervisors required to make public…

Does the supervisory agency operate an early intervention…

Is there a separate bank insolvency framework that is distinct…

Is the insolvency framework the same for bank holding…

Is court approval required to Declare insolvency?

Is court approval required to Supersede shareholders' rights?

Pre-crisis

Post-crisis

o/w Developing

o/w Developed

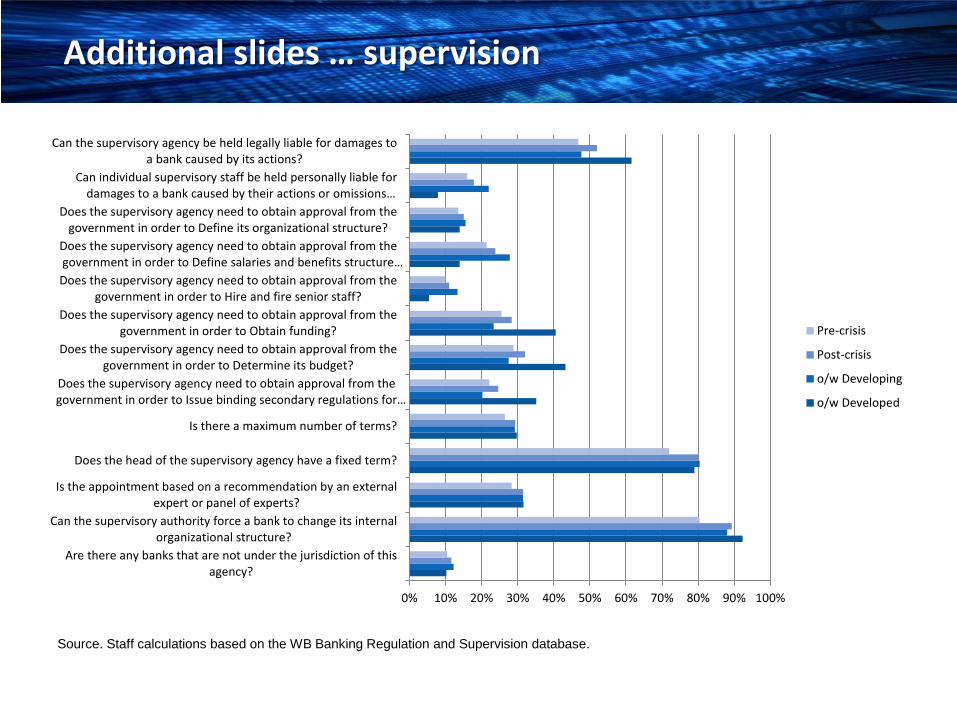

Additional slides … supervision

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Are there any banks that are not under the jurisdiction of thisagency?

Can the supervisory authority force a bank to change its internalorganizational structure?

Is the appointment based on a recommendation by an externalexpert or panel of experts?

Does the head of the supervisory agency have a fixed term?

Is there a maximum number of terms?

Does the supervisory agency need to obtain approval from thegovernment in order to Issue binding secondary regulations for…

Does the supervisory agency need to obtain approval from thegovernment in order to Determine its budget?

Does the supervisory agency need to obtain approval from thegovernment in order to Obtain funding?

Does the supervisory agency need to obtain approval from thegovernment in order to Hire and fire senior staff?

Does the supervisory agency need to obtain approval from thegovernment in order to Define salaries and benefits structure…

Does the supervisory agency need to obtain approval from thegovernment in order to Define its organizational structure?

Can individual supervisory staff be held personally liable fordamages to a bank caused by their actions or omissions…

Can the supervisory agency be held legally liable for damages toa bank caused by its actions?

Pre-crisis

Post-crisis

o/w Developing

o/w Developed

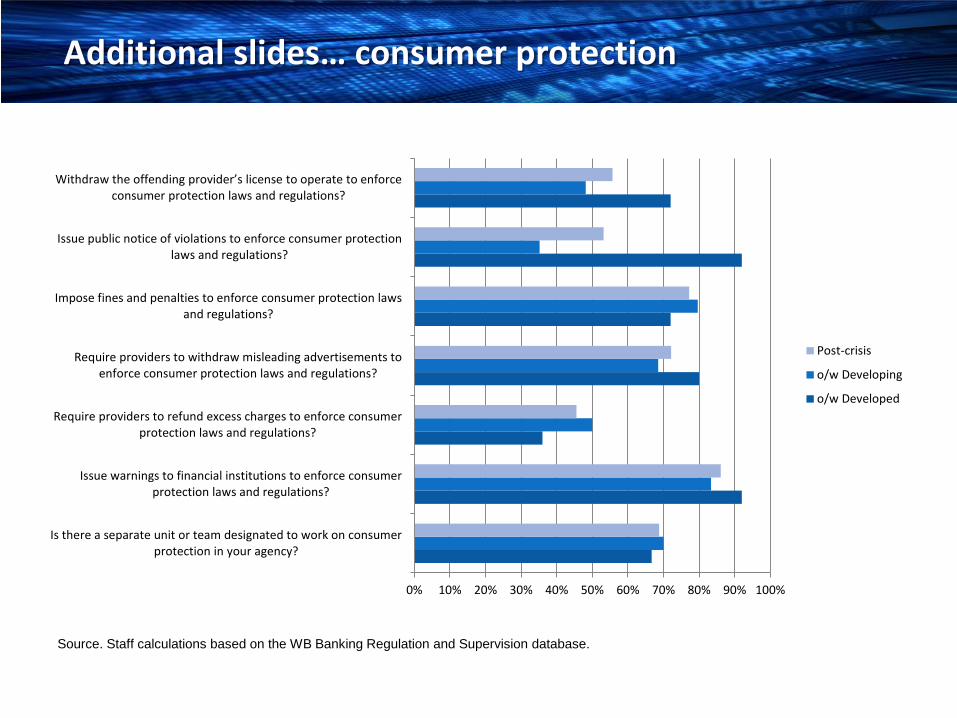

Additional slides… consumer protection

Source. Staff calculations based on the WB Banking Regulation and Supervision database.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Is there a separate unit or team designated to work on consumerprotection in your agency?

Issue warnings to financial institutions to enforce consumerprotection laws and regulations?

Require providers to refund excess charges to enforce consumerprotection laws and regulations?

Require providers to withdraw misleading advertisements toenforce consumer protection laws and regulations?

Impose fines and penalties to enforce consumer protection lawsand regulations?

Issue public notice of violations to enforce consumer protectionlaws and regulations?

Withdraw the offending provider’s license to operate to enforce consumer protection laws and regulations?

Post-crisis

o/w Developing

o/w Developed

![UKCP Supervision Policy - UK Council for Psychotherapy UKCP_Supervision_DocumentAM[3].doc UKCP Supervision Policy Contents 1. Introduction: Generic UKCP Supervision Policy Supervision](https://img.pdfslide.us/doc/110x75/5b42cf1b7f8b9a14058b595a/ukcp-supervision-policy-uk-council-for-psychotherapy-ukcpsupervisiondocumentam3doc.jpg)