Embed Size (px)

Citation preview

We thank Tyler Henry, Tejaswi Javagal, Robert Savickas, Cheick Samake, John Scruggs, Jahangir Sultan, andseminar participants at the Saint Louis University, the University of Georgia, the 2007 Financial ManagementAssociation meeting, the 2007 Washington Area Finance Conference, and the 2007 Southern Finance Asso-ciation meeting for helpful comments.

*Correspondence author, John Cook School of Business, 3674 Lindell Blvd, St Louis, Missouri 63108. Tel: �1-314-977-7204, Fax: �1-314-977-3897, e-mail: [email protected]

Received November 2008; Accepted August 2009

■ Naresh Bansal is at John Cook School of Business, Saint Louis University, St Louis, Missouri.

■ Robert A. Connolly is at Kenan-Flagler Business School, University of North Carolina, ChapelHill, North Carolina.

■ Chris Stivers is at Terry College of Business, University of Georgia, Athens, Georgia.

The Journal of Futures Markets, Vol. 30, No. 8, 753–779 (2010)© 2009 Wiley Periodicals, Inc.Published online in Wiley InterScience (www.interscience.wiley.com).DOI: 10.1002/fut.20439

REGIME-SWITCHING IN STOCK

INDEX AND TREASURY FUTURES

RETURNS AND MEASURES OF

STOCK MARKET STRESS

NARESH BANSAL*ROBERT A. CONNOLLYCHRIS STIVERS

We investigate bivariate regime-switching in daily futures-contract returns for theUS stock index and ten-year Treasury notes over the crisis-rich 1997–2005 period.We allow the return means, volatilities, and correlation to all vary across regimes. Wedocument a striking contrast between regimes, with a high-stress regime thatexhibits a much higher stock volatility, a much lower stock–bond correlation, and ahigher mean bond return. The high-stress regime is associated with higher averagevalues of stock-implied volatility, stock illiquidity, and stock and bond futures tradingvolume. The lagged implied volatility from equity-index options is useful in modelingthe time-varying transition probabilities of the regime-switching process. Our find-ings support the notions that: (1) stock market stress can have a material influence

754 Bansal, Connolly, and Stivers

Journal of Futures Markets DOI: 10.1002/fut

on Treasury bond pricing, and (2) the diversification benefits of combinedstock–bond holdings tend to be greater during times with relatively high stock mar-ket stress. © 2009 Wiley Periodicals, Inc. Jrl Fut Mark 30:753–779, 2010

INTRODUCTION

For decades, researchers have recognized the central role of the joint distribu-tion of equity and bond returns in asset pricing, portfolio allocation, and riskmanagement problems. Recent work has documented substantial time-variationin the comovement of stock and bond returns. Further, the sustained negativestock–bond return correlation that was occasionally experienced in the late1990s and early 2000s seems at odds with models emphasizing traditionallong-term fundamentals in the sense of Campbell and Ammer (1993) or Famaand French (1989).1

Economic and political crises can temporarily shock financial markets inthe sense of Kodres and Pritsker (2002). Recent examples of such crisesinclude the 1997 Asian financial crisis, the 1998 Russian currency devaluationand debt default, the 1999 Brazilian currency crisis, the 2001 terrorism crisis, andthe 2003 Iraq war. Understanding the impact of such market shocks and theirrelative influences on stock and Treasury bond markets is an important goal infinancial economics.

Motivated by the episodic nature of stock market crises, this study proposesand estimates a bivariate regime-switching model on daily futures-contractreturns for the US stock index and ten-year Treasury notes. The model allows thereturn means, volatilities, and correlations to all vary across regimes. We areinterested in whether the regime-switching estimation identifies a high-stress,high-stock-volatility regime that also exhibits prominent differences in bond-related parameters, especially the stock–bond correlation and mean bond return.

Our other goal in this study is to track the dynamics of other stock marketstress measures relative to this joint distribution. One step we take in thisdirection is to examine whether other measures of stock market stress vary reli-ably across the estimated regimes. We study the following nonreturn measuresof stock market stress: the implied volatility level from equity-index options(VIX), the daily VIX variability, a price-impact measure (PIM) and a return-reversal measure (RRV) of stock illiquidity, and the trading volume in stockfutures contracts.2 These variables do not directly relate to Treasury bond

1Among the substantial contributions, see Fleming, Kirby, and Ostdiek (1998, 2001, 2003), Scruggs andGlabadanis (2003), Hartmann, Straetmans, and Devries (2004), Connolly, Stivers, and Sun (2005, 2007), Gulko(2002), and Li (2002).2By nonreturn measures, we mean measures that do not rely solely on realized stock market returns. Ourprice-impact measure of aggregate stock illiquidity follows from Amihud (2002) and our return-reversalmeasure of stock illiquidity follows from Pastor and Stambaugh (2003).

Regime-Switching in Stock and T-notes Futures Returns 755

Journal of Futures Markets DOI: 10.1002/fut

prices. Rather, we use these variables to describe stock market conditions,where relatively higher average values of these “market conditions” variablesare another way to qualify times of stock market stress.

Our work examines data from the 1997 to 2005 period, which featuresepisodes of high stock volatility, but has consistently low inflation and lowvariability in inflation. Thus, we expect that the stock volatility would be bothappreciably higher and appreciably more variable than the comparable T-bondvolatility over this period. This fits with our focus on stock market stress.Further, the low, stable inflation makes it unlikely that inflation concerns aredriving the observed negative correlations in the sense of Campbell and Ammer(1993). We estimate our models over the entire period and for two subperiodsto evaluate subperiod consistency; 1997–2000 and 2001–2005.

Our work features daily futures returns, rather than spot returns, for severalreasons.3 First, futures contracts on the S&P 500 and Treasury securities are verywidely traded and the corresponding returns are derived from prices on a singlecontract, rather than an aggregation of the price quotes from many differentsecurities. Thus, the futures returns mitigate potential microstructure-relatedmeasurement concerns. Ahn, Boudoukh, Richardson, and Whitelaw (2002)elaborate on this point and find that daily futures returns do not display the pos-itive autocorrelation that is evident in daily spot portfolio returns. Second, thefutures contracts are derivatives in zero net supply with a maturity of a fewmonths. Thus, the trading volume in the contracts can better be characterized ashaving a direct relation to hedging demand over a specific and modest horizon.

We document a striking contrast between a higher-stress and lower-stressregime. In the higher-stress regime, we find much higher stock volatility, amuch lower stock–bond correlation, and a higher bond return mean. The vari-ance of the stock returns is at least three times higher than the variance in thelow-stress regime for our overall period and our two subperiods. The correla-tion between the stock index and ten-year T-note futures returns is at least 0.5lower in the high-stress regime than the correlation in the low-stress regime,both for our overall period and our two subperiods. Finally, the regime-specificmean return for the daily ten-year T-note futures return is reliably positive inthe high-stress regime and insignificantly negative in the low-stress regime,again for our overall period and for the subperiods.

We also document that our measures of stock market stress are reliablyand substantially higher preceding high-stress regime days. Not surprisingly,the lagged VIX averages 30.5% on high-stress regime days vs. 19.8% on low-stress days. Further, the absolute daily VIX change for high-stress regime daysis over twice that for low-stress regime days.3Although our primary work evaluates futures returns, we also find qualitatively similar results when investi-gating comparable spot returns.

756 Bansal, Connolly, and Stivers

Journal of Futures Markets DOI: 10.1002/fut

The high-stress regime days are also associated with high stock illiquidity.Both our measures of stock illiquidity, estimated using stock return and volumedata through day t � 1, are reliably greater when day t is classified as a high-stress regime day. This finding also contributes by showing that a negativestock–bond correlation is associated with higher stock illiquidity, which sup-ports the reasoning in Pastor and Stambaugh (2003) for selecting their partic-ular specification for their return-reversal measure.4

Given our results for these nonreturn measures of stock market stress, anatural question is whether these stress measures are useful as explanatoryvariables for time-varying transition probabilities (TVTP) in the regime-switchingprocess. We extend our analysis in this direction. We find that the lagged VIXlevel is useful in modeling time-varying transition probabilities for the regime-switching process: a higher lagged VIX indicates a higher probability of transi-tioning from the low-stress to the high-stress regime and a higher probability ofstaying in the high-stress regime. The lagged daily VIX variability and PIM illiq-uidity measures are also informative about the transition probabilities in somecases, in a manner consistent with the VIX level results.

This study differs from earlier related studies, such as Hartmann et al.(2004), Gulko (2002), and Connolly et al. (2005, 2007), in several key aspects.First, we use a bivariate regime-switching model that has a natural interpreta-tion as considering regime changes in the “entire joint stock–bond return distribution,” rather than simply correlations or comovements. Second, weconduct a multidimensional analysis to better understand the differences inthe market conditions across a high-stress and low-stress regime. In addition tocomparing the return parameters between the two regimes, we also investigatethe differences across regimes in option-derived stock-implied volatility, stockilliquidity, and trading volume. Third, our work features short-term futuresreturns, rather than spot returns, which allows us to mitigate potentialmicrostructure concerns.

As discussed in Guidolin and Timmermann (2006) (GT), the vast majorityof existing work with regime switching has only considered univariate models.GT model the joint distribution of monthly stock and bond returns in a bivari-ate regime-switching model that allows for multiple states.5 Although theirfocus is on asset allocation (using monthly data), our focus is on how the cor-relation and other market characteristics differ in times of market stress usingdaily data.

4Pastor and Stambaugh (2003) argue that measures of stock market illiquidity should be negatively associat-ed with the stock–bond correlation, and they use this belief as a key criteria in selecting the specification fortheir return-reversal regression.5For other recent related work that features regime switching, see Ang and Bekaert (2002a, 2002b, 2002c,2004).

Regime-Switching in Stock and T-notes Futures Returns 757

Journal of Futures Markets DOI: 10.1002/fut

This article proceeds as follows. We discuss our data in the next section, andour third section presents the basic regime-switching model and estimationresults. Then, our fourth section examines the association between the nonre-turn measures of stock market stress and the estimated regimes, and the lastsection concludes.

DATA AND VARIABLE CONSTRUCTION

Our empirical work uses the following times series over the 1997 to 2005 sam-ple period:

(1) Daily returns on the S&P 500 futures contracts and futures contractson the ten-year Treasury Note (T-note); (2) daily trading volume on each ofthese two futures contracts and a standardized measure of trading volume thatis constructed to control for growth over time and the quarterly seasonality offutures contract trading; (3) equity-index-implied volatility from Chicago BoardOptions Exchange (CBOE) index option contracts; (4) two different measuresof market-wide stock illiquidity, based on the return-reversal measure (RRV)from Pastor and Stambaugh (2003) and the price-impact measure (PIM) fromAmihud (2002). It is important to note that we construct both the PIM andRRV illiquidity measures so that a higher value indicates a less liquid (or moreilliquid) market.

Futures Data

We collect daily data from Datastream on six specific futures contracts, cover-ing the sample period of January 1, 1997 through December 31, 2005. Forcomputing returns, we use the continuous futures series computed byDatastream for the S&P 500 and the T-note futures contracts. The continuousseries uses the price of the nearest to maturity contract until the month inwhich the contract expires. Then, the series rolls over at that point to the nextnearest to maturity contract.6 This switch of the series as one rolls into thematurity month will result in an artificial return on that day. Accordingly, whencomputing returns, we discard those four days a year.

The principal S&P500 contract is traded on the Chicago MercantileExchange (CME) both in an open outcry and electronic market. Pit trading takesplace between 8:30 a.m. and 3:15 p.m. (CST). The E-mini S&P 500 contract,introduced in September 1997, trades on the CME’s Globex electronic tradingsystem, with the E-mini contract being one-fifth the size of the full contract.

6Carchano and Pardo (2009) analyze the different rollover date selection criteria used in constructing con-tinuous stock index futures contract return series, and find that the choice of the rollover date does notinduce any significant differences in the resulting return series.

758 Bansal, Connolly, and Stivers

Journal of Futures Markets DOI: 10.1002/fut

The T-note futures contracts trades on the Chicago Board of Trade(CBOT), both in an open outcry and electronic market. Open outcry tradingbegins at 7:20 a.m. and closes at 2:00 p.m. (CST). Our trading volume data forthe electronic trading of the Treasury futures commences in August 2000,which is the earliest available from the exchange. Electronic trading began in1994, but trading volume was very small, relative to the open outcry trading,until about 2000. Thus, there are some difference between the stock and T-note futures trading times.7

Our empirical work focuses on the ten-year T-note futures contract forseveral reasons. First, for our principal analysis, we desire a futures contractwhere the underlying asset is a longer-term bond, whose maturity shouldroughly correspond to the bond holdings in a portfolio that is allocated acrossstock, bonds, and the money market. Second, we desire a very widely tradedcontract where prices should rapidly respond to changing conditions. In oursample, the ten-year T-note futures contract has the largest trading volume.Over 1997–2005, the average daily trading volumes (including both open-auctionand electronic volume) of the futures contracts with different horizons are367,958 for the ten-year contract, 287,036 for the 30-year contract, 192,860for the five-year contract, and 19,251 for the two-year contract.

Table I, Panel A, reports on the means, correlations, volatilities, and otherdescriptive statistics for the stock index and ten-year T-note futures returns forour full sample and both subperiods. We report on the daily returns from close-to-close prices.8 As expected, note that the stock volatility is much higher thanthe bond volatility.

For the futures trading volume, we wish to capture the economically rele-vant trading so we include both open outcry pit trading and electronic trading.For the stock index futures, we gather the total futures volume for the regularS&P 500 futures contract and for the E-mini S&P 500 futures contract. Wedivide the E-mini volume by five to reflect that the contract is one-fifth the size ofthe full contract. For the bond futures, we gather the total futures trading volumefor both the ten-year and the 30-year Treasury futures contract. We feel that thissummed volume will fairly reflect the trading in longer-term Treasury futures.

As might be expected, there is a significant increase in the futures volumeover time. Further, there are substantial quarterly trends associated with the

7To examine if the timing mismatch affects our empirical analysis, it would be desirable to re-estimate ourmodels using the returns constructed from 2 p.m.(CST) prices for the S&P 500 contract. Fleming et al.(1998) perform such a test for their empirical exercise and find that their results are not qualitatively differ-ent when using the stock futures returns from 2:00 p.m. in place of close-to-close returns. However, we don’thave access to such data. Instead, we re-estimate our primary model with comparable daily spot returns(instead of daily futures returns) and find qualitatively similar results.8The average futures returns may seem low, but remember that these average returns do not include the risk-free interest rate because of the nature of futures returns.

Regime-Switching in Stock and T-notes Futures Returns 759

Journal of Futures Markets DOI: 10.1002/fut

maturity cycle of the contracts. In order to compare trading volume over time,we need a method to detrend and standardize the trading volume. We proposea simple metric that measures the percentage increase over a lagged movingaverage.

Our standardized, detrended, futures volume measure is calculated as fol-lows. First, we calculate a lagged moving average using observations from theprior four months that fall at the same point in the quarterly cycle as the obser-vation in question. For example, consider the trading day of May 18, 2005.May is the second month in the quarterly cycle, where the quarterly contractsmature in March, June, September, and December. Thus, we calculate theaverage trading volume for all trading days that fall in February 2005,

TABLE I

Summary Data Statistics

1997–2005 1997–2000 2001–2005

Stock Ten-Year Stock Ten-Year Stock Ten-YearIndex T-note Index T-note Index T-note

Panel A: Statistics for the daily futures returns

Mean 0.0052 0.0161 0.024 0.011 �0.010 0.020Standard deviation 1.229 0.380 1.323 0.327 1.148 0.418Skewness �0.134 �0.272 �0.343 �0.162 0.111 �0.318Excess Kurtosis 3.208 1.522 3.481 1.156 2.561 1.336r1 �0.010 0.027 �0.010 0.076 �0.012 0.002r2 �0.038 �0.023 �0.057 �0.011 �0.014 �0.027Ljung–Box test 15.69 14.50 19.56 16.90 13.39 13.38

for ten lags: (p-value) (0.109) (0.151) (0.034) (0.077) (0.203) (0.203)Stock–bond Correlation �0.160 0.011 �0.289

Std. Std. Std.Mean Dev. Mean Dev. Mean Dev.

Panel B: Statistics for the nonreturn market-stress variables

Stock implied volatility (VIX) 23.5 7.49 25.3 4.77 22.1 8.87Daily VIX variability 1.11 1.18 1.30 1.34 0.95 1.01Stock futures volume 0.088 0.387 0.053 0.388 0.115 0.384Treasury futures volume 0.077 0.441 0.0083 0.471 0.132 0.407PIM illiquidity 0.171 0.058 0.211 0.056 0.140 0.037RRV illiquidity (�100) 0.144 0.373 0.144 0.404 0.145 0.346

Notes. Panel A reports the descriptive statistics for the daily returns on the S&P 500 and ten-year T-note futures contracts. Thereturns are in daily percentage units, and ri refers to the i th autocorrelation. The Ljung–Box test statistic evaluates ten lags jointly forstatistically significant autocorrelations, with the p-value in parentheses. Panel B reports on the following “stock-market-stress” vari-ables: (1) the level of implied volatility from equity index options (VIX), (2) the daily VIX variability, defined as the absolute value of thedaily change from close-to-close values, (3) our standardized, detrended daily trading volume on both the stock index and Treasuryfutures contracts, and (4) two different measures of market-wide stock illiquidity, based on the Price-Impact measure (PIM) fromAmihud (2002) and the Return-Reversal (RRV) measure from Pastor and Stambaugh (2003). Each variable is explained in detail inData And Variable Construction section. Statistics are reported in separate columns for the overall sample, 1997–2005, and for thetwo subperiods, 1997–2000 and 2001–2005.

760 Bansal, Connolly, and Stivers

Journal of Futures Markets DOI: 10.1002/fut

November 2004, August 2004, and May 2004 (the prior four months thatoccur at the same point in the quarterly cycle). We then take the trading vol-ume from May 18, 2005 and subtract this lagged moving average.9 Finally, wetake the resulting difference and divide by the same lagged moving average.

In our view, this measure is intuitively appealing in several dimensions.First, it is in the spirit of a “volume return” in that it is a difference in levelsdivided by the lagged level. The resulting number can be interpreted as the per-centage increase in that day’s volume, relative to the average volume over thelagged moving average. Second, the method serves to standardize the volumeby detrending the series without relying on a linear trend that may not be agood fit to the data. Third, the measure does not require the estimation of anycoefficients that rely upon observing the entire sample, so the measure can becalculated in real time as soon as the day’s volume is observed. Finally, ourmoving average uses observations going back one year but only for months thatare in the same point in the quarterly cycle. Thus, hopefully, our procedureshould act to standardize and detrend the volume series by controlling both forthe long-term growth and quarterly seasonalities that are evident in the futuresvolume series.

Stock-Implied Volatility and Stock Liquidity Measures

To measure the implied volatility of the US stock market, we rely on the origi-nal VIX measure produced by the CBOE, now denoted as VXO by the CBOE.This daily series measures the implied volatility of a hypothetical at-the-moneyoption on the S&P 100 stock index with 22 trading days until expiration. TheCBOE constructs this VIX as a weighted average of the implied volatilitiesextracted from eight different options. Specifically, these are call and putoptions written at the two strike prices closest to the money plus the two options(both puts and calls) nearest to expiration, excluding options that are withinone week of expiration. The implied volatilities account for dividend paymentsand the possibility of early exercise.

For the stock illiquidity measures, we use two well-known measures thatare constructed using only the daily return and volume data from CRSP. Weconstruct measures based on Amihud’s (2002) price-impact measure, denoted asPIM, and Pastor and Stambaugh’s (2003) return-reversal measure, denoted as RRV. While PIM is closely correlated with price-impact measures based onhigh-frequency data (Hasbrouck, 2005), RRV adequately captures many of theknown historical properties of the stock market liquidity (Pastor and

9This detrending method is in the spirit of the procedure in Bessembinder and Seguin (1992), who subtracta 100-day moving average to detrend the futures volume.

Regime-Switching in Stock and T-notes Futures Returns 761

Journal of Futures Markets DOI: 10.1002/fut

Stambaugh, 2003). We construct our two liquidity measures such that theymeasure market illiquidity; in other words, higher values indicate markets thatare more illiquid. We measure illiquidity over a rolling 22-consecutive-trading-day period. This allows us to construct a daily time series for aggregate illiquid-ity. In our time series, the aggregate illiquidity on day t refers to illiquiditymeasured over a backward-looking 22-trading-day period ending on day t.Therefore, PIMt�1 or RRVt�1 refers to the illiquidity estimated over the period t � 22 to t � 1.

From a computational perspective, the two illiquidity measures are similarin some ways. In both, we first estimate the illiquidity measures for individualstocks, and then take a cross-sectional average to get the market-wide illiquiditymeasure, and finally scale up the series to make it relatively stationary. For thecross-sectional average, we include only those stocks that meet the followingconditions: (a) there should be more than 15 observations to estimate illiquidi-ty measure of individual stocks, (b) it should be a ordinary share (CRSP sharecode 10 or 11), (c) it should be listed on NYSE/AMEX (CRSP exchange code 1or 2), (d) share price should be between $5 and $1000, (e) the first (or the lastday) that stock appears (or disappears) on CRSP should not fall between the22-trading-day period. The values for share code, exchange code, and shareprice for purpose of sample stock selection are the values as of the beginning ofthe 22-trading-day period. To scale up the resulting series, we multiply bymt�m1, where mt is the total dollar value of the stocks (included in the cross-sectional average) as of the beginning of that period and m1 is the correspon-ding value for the first 22-trading-day period in January 1997.

Our two illiquidity measures differ in the first step, that is the estimationof illiquidity measure of individual stocks. The return-reversal measure ofPastor and Stambaugh is based on the idea that the price changes accompany-ing large volumes tend to be reversed when market-wide liquidity is low.Specifically, the liquidity value for stock i in a 22-consecutive-trading-day peri-od ending on day t is given by

(1)

(2)

where and are the return and the dollar volume (measured in mil-lions), respectively, of stock i on day d in the 22-trading-day period, is theexcess return given by where is the CRSP value-weighted mar-ket return on day d, and is the excess return residual. If we regard

as a proxy for order-flow, then represents an order-flow returnreversal. RRV is the negative of the estimated value of ( ). We flip the signin order to make it a measure of illiquidity.

gi,tgi,t

gi,tsign(rei,d,t)

ei,d�1,t

rm,d,tri,d,t � rm,d,t

rei,d�1,t

voli,d,tri,d,t

RRVi,t � � gi,t

rei,d�1,t � ui,t � fi,t � ri,d,t � gi,t � sign(re

i,d,t).voli,d,t � ei,d�1,t

762 Bansal, Connolly, and Stivers

Journal of Futures Markets DOI: 10.1002/fut

The price-impact measure of Amihud (2002) measure is based on the ideathat there is a positive relationship between the price change and the net order-flow, which results from the information asymmetry between market makersand traders. Following Amihud (2002), we use the illiquidity ratio as a price-impact proxy. We remove the stock-days with zero volume and measure theilliquidity value for stock i in a 22-consecutive-trading-day period ending onday t as

(3)

where and are the return and the dollar volume (measured in mil-lions), respectively, of stock i on day d in the 22-trading-day period, and isthe number of days the stock i traded (nonzero volume) in the 22-trading-dayperiod. Thus, both our measures are illiquidity measures, where a higher valueindicates a less liquid market (or more illiquid market).

Table I, Panel B, reports on summary statistics for the “market stress” vari-ables featured in this study; specifically the stock-implied volatility VIX, the dailyVIX variability, our standardized measures of stock and long-term Treasuriesfutures trading volume, and the RRV and PIM measures of stock illiquidity.

REGIME-SWITCHING RESULTS

The Regime-Switching Model

Our model simultaneously estimates regime-specific correlations, means, andvariances for daily stock index and ten-year T-note futures returns. The modelis given by

(4)

(5)

where the s and b subscripts are markers for stock and bond futures returns;the superscript j indicates the regime for the regime-specific parameters, with j � 1 for the low-stress regime or j � 2 for the high-stress regime; and arethe daily close-to-close returns of the stock index and Treasury futures; and

are the regime-specific mean returns; and are the regime-specific stan-dard deviations; and and are the return shocks. The return shocks followa standard bivariate normal distribution with regime-specific correlations .

The j state variable is modeled with constant transition probabilities, ,where is the probability of being in regime j for day t (the second subscript),given that day t � 1 is in regime j (the first subscript). Thus, for example, equals the probability of day t being in regime 2, given that day t � 1 is in regime 1.

p12

pjj

pjj

rjhb,ths,t

sjbsj

smjb

mjs

rb,trs,t

rb,t � mjb � sj

bhb,t

rs,t � mjs � sj

shs,t

Di,t

voli,d,tri,d,t

PIMi,t �1

Di,ta

Di,t

d�1

ƒ ri,d,t ƒvoli,d,t

Regime-Switching in Stock and T-notes Futures Returns 763

Journal of Futures Markets DOI: 10.1002/fut

We use the S&P 500 futures to represent the stock index futures and the ten-year T-note futures to represent the longer-term Treasury futures.

The means, standard deviations, correlations between the residuals, andthe transition probabilities are regime-specific parameters to be simultaneouslyestimated. We estimate the model by maximizing the log-likelihood function forthe bivariate normal density while allowing for regime-switching between thetwo states.

Our two-state regime-switching specification only considers the basic dis-tributional parameters for each states; the regime-specific means, variances,and correlations. This simple specification parsimoniously captures the notionof two states for the joint distribution of the daily returns of stock index andten-year T-note futures contracts. Our investigation is motivated by the possi-bility of a less common higher-stress regime and a more common lower-stressregime, where stress corresponds to the stock index futures volatility. By focus-ing on a two-state framework, we can readily compare the regime differences inthe other measures of stock market stress (listed in Table I, Panel B).10

We acknowledge several limitations to this simple specification. First, thisspecification does not include any lagged returns in Equations (4) and (5),which would be suggested if the daily returns exhibited significant autocorrela-tions. However, as shown in Table I, Panel A, the autocorrelations in the dailyreturns are very modest. Based on the Ljung-Box test statistics, we cannotreject the null that the first ten autocorrelations are jointly zero for the overallsample period and the second-half subperiod. In addition, on evaluating thestandardized return residuals that follow from estimating Equations (4) and(5), we observe that the autocorrelations remain similarly modest.11 Finally, inuntabulated work, we estimate alternate versions of the bivariate two-statemodel that include either one lagged return or two lagged returns as additionalexplanatory variables. We find that the estimated coefficients on the laggedreturns are jointly statistically insignificant and that the core estimation resultsremain essentially the same.

Next, our simple specification does not allow for conditional heteroskedas-ticity, or volatility clustering, within a regime. While our return data does exhib-it volatility clustering (as is common in daily returns), the volatility clustering ismuch more modest for our two-state model than that for the simple return

10We do not evaluate whether a three-state, or greater, model is a better fit, as we desire parsimony here. Inthis sense, we acknowledge that our regime-switching model is potentially incorrect, in an absolute sense.Tests of this sort are particularly difficult because some parameters are not defined under the null hypothesis.Hansen (1996) discusses this problem in a related context, and Gong and Mariano (1997) address these dif-ficult issues squarely.11By standardized return residual, we refer to a transformed return series that is equal to: (the differencebetween the raw return and the regime-specific mean return) divided by (the estimated regime-specific stan-dard deviation).

764 Bansal, Connolly, and Stivers

Journal of Futures Markets DOI: 10.1002/fut

series. We report more details on volatility clustering in Model Evaluation sec-tion. Further, our intent is not to model conditional volatility within a regime,but rather to evaluate a two-state approach for all the return distributionalparameters.

Finally, we acknowledge that our estimation must be considered a quasi-maximum likelihood estimation, in the sense of Bollerslev and Wooldridge(1992). This is because, although the standardized return residuals from the two-state estimation are appreciably closer to normally distributed than the simplereturn series, the standardized return residuals still exhibit excess kurtosis andnegative skewness. We report more distributional details in Model Evaluationsection, after first presenting the estimation results in the next section.

Estimation Results

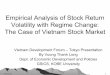

Table II presents the basic estimation results for our regime-switching modelfor the full 1997–2005 sample period and for the 1997–2000 and 2001–2005subperiods.12 Figure 1, Panel A displays the estimated filtered probability ofbeing in the high-stress regime over time. Note that we consider the funda-mental distinction for the high-stress regime to be higher stock return volatili-ty. Figure 1, Panel B plots rolling stock–bond correlations calculated using dayst to day , relative to regime-day t.

We begin by discussing the economic plausibility of our estimation. InTable II, over our 1997–2005 sample, the low-stress regime is the predominantregime with an expected duration of 80 days, whereas the high-stress regimehas an expected duration of 44 days. In Figure 1, 34.8% of the observationshave a �50% chance of being in the high-stress regime. These results support thenotion of a predominant low-stress regime, corresponding to more typicaltimes, and an abnormal high-stress regime, corresponding to more stressful times.Consistent with the notion that the high-stress regime corresponds to crisisperiods, high-stress regime episodes in Figure 1 correspond to the Asian finan-cial crisis in the fall of 1997, the Russian currency devaluation and debt defaultin the fall of 1998, the Brazilian currency crisis in early 1999, the terrorism crisisin September 2001, and the preparation for and invasion of Iraq in the fall of2002 and spring of 2003.

With respect to the stock–bond correlation, we find that the correlation inthe high-stress regime is appreciably lower than that in the low-stress regime.For the 1997–2005 period, the estimated correlation is 0.143 in the low-stressregime vs. �0.429 in the high-stress regime, a difference of over 0.57. For the

t � 21

12We also evaluate an additional five-year subperiod that spans 1999–2003 and, thus, mixes the samplesfrom the two subperiods in Table II. We find that the estimated parameters for the 1999–2003 period arequalitatively consistent with those reported in Table II.

Regime-Switching in Stock and T-notes Futures Returns 765

Journal of Futures Markets DOI: 10.1002/fut

1997–2000 and 2001–2005 subperiods, the regime correlation differences arealso sizable at 0.69 and 0.52, respectively. These differences in stock–bond cor-relations across the regimes are all statistically significant, based on a LikelihoodRatio Test. A casual inspection of the two plots in Figure 1 indicates that thereis a substantial overlap between the high-stress regime and negative stock–bond correlations. Such a finding supports the economic rationale behindcross-market hedging in times of stock market stress.

TABLE II

A Regime-Switching Model for Daily Stock Index and Ten-Year T-note Futures Returns

Panel A: 1997–2005 Panel B: 1997–2000 Panel C: 2001–2005

Low High Low High Low HighStress Stress Regime Stress Stress Stress Stress

Coeff. (j � 1) (j � 2) Difference (j � 1) (j � 2) (j � 1) (j � 2)

r j 0.143 �0.429 0.572 0.404 �0.289 �0.018 �0.547(0.032)1 (0.038)1 [�0.001] (0.047)1 (0.056)1 (0.037) (0.035)1

0.858 1.706 �0.848 1.000 1.734 0.738 1.651(0.028) (0.056) [�0.001] (0.038) (0.076) (0.021) (0.062)0.370 0.397 �0.027 0.295 0.373 0.416 0.419

(0.0079) (0.013) [0.116] (0.0100) (0.017) (0.011) (0.015)0.050 �0.077 0.128 0.079 �0.068 0.030 �0.083

(0.024)2 (0.062) [0.059] (0.043)3 (0.087) (0.027) (0.081)�0.0012 0.048 �0.049 �0.0030 0.035 �0.0021 0.061(0.0094) (0.015)1 [0.008] (0.013) (0.021)3 (0.014) (0.021)1

0.0125 0.0194 0.0061(0.0045) (0.0094) (0.0030)

0.0229 0.0308 0.0134(0.0079) (0.015) (0.0061)

Duration 80 days 44 days 52 days 32 days 164 days 75 daysLog-likelihood �4314.67 �1853.68 �2343.12

Notes. This table reports results from estimating the following two-state, bivariate regime-switching model on the daily returns ofS&P 500 and ten-year T-note futures:

Where the s and b subscripts indicate stock and bond terms, respectively; the superscript j indicates regime-specific parameters, withj � 1 for the low-stress regime or j � 2 for the high-stress regime; and are the stock index and T-note futures returns; and are the regime-specific mean returns; and are the regime-specific standard deviations; and and are the return shocks,which follow a standard bivariate normal distribution with regime-specific correlations . The j state variable is modeled with constanttransition probabilities, , where , is the probability of being in regime j for day t (the second subscript), given that day t � 1 is inregime j (the first subscript).

The means, standard deviations, correlations, and transition probabilities are regime-specific parameters to be estimated. We esti-mate the model by maximizing the log-likelihood function for the bivariate normal density with regime switching. Standard errors are inparentheses. 1, 2, and 3 indicate 1%, 5%, and 10% p-values for whether the estimated regime-specific means and correlations are dif-ferent than zero. The second-last row reports the expected duration of the respective regime. In Panel A, the column labeled as“Regime Difference” reports the regime differences for the estimated return parameters, with a p-value in brackets for the null that therespective parameters are the same for both regimes.

pjjpjj

rjhb,ths,tsj

bsjs

mjbmj

srb,trs,t

rb,t � mjb � sj

bhb,t

rs,t � mjs � sj

shs,t

p21

p12

mjb

mjs

sjb

sjs

766 Bansal, Connolly, and Stivers

Journal of Futures Markets DOI: 10.1002/fut

We now turn our attention to regime-specific volatility and regime-specificmeans of the stock index and T-note futures returns. Although a higher volatil-ity in the stock index futures is taken to be the prominent feature of the high-stress regime, it is not obvious as to how the volatility of the T-note futures willrespond in the high-stress regime. From Table II, the stock return variance in the high-stress regime is nearly four (three and five) times the stock variance inthe low-stress regime over the full sample period (first subperiod and second

Panel A: Filtered Probability of Being in the High-stress Regime

0

0.2

0.4

0.6

0.8

1

1/19

97

7/19

97

1/19

98

7/19

98

1/19

99

7/19

99

1/20

00

7/20

00

1/20

01

7/20

01

1/20

02

7/20

02

1/20

03

7/20

03

1/20

04

7/20

04

1/20

05

7/20

05

�1�0.8�0.6�0.4�0.2

00.20.40.60.8

1

1/19

97

7/19

97

1/19

98

7/19

98

1/19

99

7/19

99

1/20

00

7/20

00

1/20

01

7/20

01

1/20

02

7/20

02

1/20

03

7/20

03

1/20

04

7/20

04

1/20

05

7/20

05

Panel B: 22-Day Correlations for Stock Index and T-Note Futures

FIGURE 1Times Series of regime movements and correlations for stocks and bonds.

Panel A displays the time series of the regime movements from our Table II estimation on the dailyreturns of stock index and ten-year T-note futures contracts. The filtered probability of being in the

high-stress regime is plotted over time. For Panel A, the following crisis periods are denoted by the thickline on the horizontal axis: the Asian financial crisis in the fall of 1997, the Russian currency devaluationand debt default in the fall of 1998, the Brazilian currency crisis in early 1999, the terrorism crisis in the

fall of 2001, and the preparation for and invasion of Iraq in the fall of 2002 and spring of 2003.Panel B displays the time series of 22-trading day correlations between the stock index and ten-year

T-note futures, where the day t value is the correlation over days t to t � 21. The sample spans1997–2005.

Regime-Switching in Stock and T-notes Futures Returns 767

Journal of Futures Markets DOI: 10.1002/fut

subperiod). These differences in stock-return variances across the regimes areall statistically significant, based on a Likelihood Ratio Test. In contrast, the T-note futures variance in the high-stress regime is only 1.02–1.60 times the bond variance in the low-stress regime. The differences in T-note futuresvariances across the regimes are statistically insignificant in the overall periodand second subperiod. Thus, the increase in stock futures volatility when mov-ing from the low-stress regime to the high-stress regime is much more promi-nent than the comparable change in the T-note futures volatility.

We also observe interesting differences in the regime-specific meanreturns. For all three estimation periods, the mean of the ten-year T-notefutures returns is positive and statistically significant in the high-stress regimebut negative and statistically insignificant in the low-stress regime. The differ-ences in the regime-specific means are statistically significant in the overallperiod and second subperiod. In our view, these differences in regime-specificmeans are better interpreted as “realized means associated with a high-stressstock environment,” rather than an ex ante conditional risk premia for the bondreturns. Presumably, flight-to-quality or flight-to-liquidity effects in the high-stress regime could result in a higher regime-specific realized mean for the T-note futures returns.

The estimates for the regime-specific mean of the stock index futuresreturns are positive in the low-stress regime and negative in the high-stressregime. However, the stock mean is only statistically reliably different than zerofor the low-stress regime in the overall period and first subperiod. Although thestock’s regime-specific means are not precisely estimated in the high-stressregime (with the high volatility and shorter regimes), the negative values do fitthe notion of a flight-to-quality or flight-to-liquidity pricing effect in the high-stress regime. Again, as for the means of the T-note futures, we interpret theregime-specific means as “realized means associated with a high-stress out-come, ” rather than ex ante conditional risk premia.

Finally, for comparison, we also estimate our regime-switching modelusing daily spot returns of the stock index and ten-year Treasury notes. Theresults are reported in Appendix A. The return patterns are qualitatively com-parable to those in Table II for daily futures returns. For example, for the1997–2005 period with spot returns, the expected duration and stock–bondcorrelation during the low-stress regime is 71 days with r � 0.13 vs. 47 dayswith r� �0.32 for the high-stress regime.

Model Evaluation

In this subsection, we perform a series of evaluations for the two-state modelgiven by Equations (4) and (5). First, we discuss the evidence regarding volatility

768 Bansal, Connolly, and Stivers

Journal of Futures Markets DOI: 10.1002/fut

clustering in our sample. Second, we evaluate the fit of our two-state model, ascompared to a one-state distributional assumption.

To study volatility clustering (defined as the autocorrelation in the squaredreturn residuals), we run a regression where the squared standardized return isthe dependent variable and five lags of the squared standardized return are theexplanatory variables. For the standardized residuals for the stock index futuresreturns with the one-state distribution, the R-squared for the volatility-clusteringregression is 7.6% and the five lags jointly are statistically significant as explana-tory variables. This indicates that the daily return series in our study exhibitvolatility clustering. For the standardized residuals from the stock index futuresreturns with a two-state distribution as in our model, the R-squared for thevolatility-clustering regression falls to 1.7% with five lags remaining jointly sta-tistically significant.13 The decrease in the R-squared indicates that the volatilityclustering is much more modest for the two-state case than for the one-statecase. In addition, the excess kurtosis for the stock index futures is statisticallysignificant in both the cases, but is 84% lower in the two-state case (with anexcess kurtosis of 3.21 for the one-state case vs. 0.50 for the two-state case).14

To evaluate the fit of our two-state model as compared to an alternate one-state model, we perform the following two evaluations: (1) comparing the loglikelihood function values (Likelihood Ratio Test); and (2) comparing the val-ues of Akaike Information Criterion (AIC) and the Bayesian InformationCriterion (BIC). First, for the overall sample period, the log likelihood functionvalue is �4314.67 for the two-state case vs. �4566.01 for the one-state case.Thus, the x2 test statistic is 502.7, which rejects a null of a one-state distribu-tion with a 0.01% p-value. The same test statistic for the two subperiods, 228.9for 1997–2000 and 372.3 for 2001–2005, also reject a null of a one-state dis-tribution with a 0.01% p-value for both subperiods. Second, the AIC (BIC)value is 8653.34 (8721.8) for the two-state case vs. 9142.02 (9170.5) for theone-state case, over the full sample period. Subperiod results also indicate thatthe AIC and BIC values are substantially lower for the two-state case. As alower value indicates a preferred model, the AIC and BIC comparisons alsosupport our two-state approach.

13For the standardized return residual for the two-state regime-switching estimation, we refer to a probability-weighted standardized residual, calculated as follows: (a) regime-specific standardized residuals are calculatedfor each daily return using each respective regime’s mean and standard deviation from the model estimation,(b) the filtered probabilities of being in each regime for each day are retained from the estimation, and then(3) the probability-weighted standardized residual for a given day is equal to the sum of each regime’s proba-bility for that day times the respective regime-specific standardized return residual for that day.14For the daily T-note futures returns, the volatility clustering and excess kurtosis also decrease for the two-state case, as compared to the one-state case. However, the decrease is modest as compared to the decreasefor the stock index futures returns. This is not unexpected, as the volatility clustering and excess kurtosis islower to start with for the T-note futures returns.

Regime-Switching in Stock and T-notes Futures Returns 769

Journal of Futures Markets DOI: 10.1002/fut

To address the concern regarding the assumption of a bivariate normal dis-tribution, we compute the Jarque–Bera test statistic to evaluate goodness-of-fitfor normality. For the stock index futures returns, the Jarque–Bera test statisticis 961.8 for the one-state case (with the test statistic distributed as an asymp-totic x2 distribution with 2 degrees of freedom), which rejects a normalityassumption. By contrast, for the two-state case, the Jarque–Bera test statisticfor the standardized return residuals of the stock index futures is much lower at25.5 (although it still indicates a rejection of normality).

To conclude, our evaluation in this subsection indicates that: (1) volatilityclustering and excess kurtosis is appreciably lower for the stock index futuresreturns for our two-state estimation, as compared to a one-state distributionalassumption; and (2) a two-state distributional assumption is clearly a better fitthan a simpler one-state distribution. Given our goals in this study, these find-ings are attractive and provide support for our two-state approximation.

Implications for Stock–Bond Diversification

In all three of our estimation periods in Table II, the estimated stock–bond cor-relation is appreciably lower in the high-stress regime and the T-bond riskincreases only modestly in the high-stress regime, as compared to the substan-tial increase in the stock risk. The attractive feature of stock–bond diversifica-tion is that the diversification benefits are larger during times of higher stockmarket stress.

Consider a hypothetical portfolio that is 60% invested in stocks and 40%invested in ten-year Treasury notes. The diversification benefits are evidentwhen comparing the return standard deviation of this 60/40 portfolio with thatof a stock-only portfolio. When using the estimated parameters for the low-stress regime over our 1997–2005 sample, the daily return standard deviationfor the 60/40 portfolio is 0.56% vs. 0.86% for a stock-only portfolio. In con-trast, when using the estimated parameters for the high-stress regime over thesame sample, the daily return standard deviation for the 60/40 portfolio is0.97% vs. 1.71% for a stock-only portfolio. Thus, in comparison to a stock-onlyportfolio, the combined stock–bond holdings reduces the return standard devi-ation by 0.74% in the high-stress regime, as compared to a reduction of only0.30% in the low-stress regime. This result is because: (1) the stock–bond cor-relation is appreciably lower in the high-stress regime, and (2) the T-bond riskonly increases marginally in the high-stress regime, whereas the stock risk nearlydoubles. Subperiod comparisons are similar.

To conclude, our bivariate regime-switching model yields regimes withsubstantial persistence where the high-stress regime episodes correspond towell-known financial crises. The stock–bond correlations in the high-stress

770 Bansal, Connolly, and Stivers

Journal of Futures Markets DOI: 10.1002/fut

regime are always markedly lower than that in the low-stress regime. The high-stress regime exhibits much higher stock volatility and a lower stock mean, buta higher bond mean with little difference in the bond volatility. Our results sup-port the notion that the stock–bond diversification benefits are relatively largerduring the high-stress regime.

MEASURES OF STOCK MARKET STRESS ANDESTIMATED REGIMES

Variation in Measures of Stock Market Stress Across Regimes

The second part of our investigation looks at whether there are economically sig-nificant and systematic differences in other dimensions of market stress acrossour estimated regimes. If the regime estimation is picking up real variation ineconomic conditions, it seems plausible and intuitive that the high-stress regimewould also be associated with higher average values of these “market stress” vari-ables. Table III reports how these variables vary across the two regimes.

TABLE III

Implied Volatility, Futures Volume, and Liquidity across Regimes

1997–2005 Period 1997–2000 Subperiod 2001–2005 Subperiod

Low High Diff in Low High Diff in Low High Diff in Stress Stress Means Stress Stress Means Stress Stress Means

19.83 30.45 10.621 23.19 28.97 5.781 16.89 31.39 14.491

(0.18) (0.30) (0.36) (0.14) (0.39) (0.411) (0.230) (0.436) (0.496)abs 0.781 1.72 0.9361 0.966 1.91 0.9391 0.642 1.49 0.8511

(0.020) (0.045) (0.064) (0.035) (0.104) (0.110) (0.021) (0.067) (0.070)0.158 0.197 0.0391 0.194 0.240 0.0461 0.129 0.159 0.0301

(0.006) (0.0089) (0.0098) (0.009) (0.008) (0.011) (0.004) (0.0080) (0.0082)0.068 0.285 0.2181 0.078 0.261 0.182 0.063 0.289 0.2261

(�100) (0.022) (0.055) (0.058) (0.035) (0.093) (0.096) (0.030) (0.059) (0.066)0.016 0.221 0.2051 0.0011 0.146 0.1451 0.014 0.293 0.2791

(0.012) (0.023) (0.024) (0.018) (0.031) (0.035) (0.015) (0.024) (0.029)0.051 0.126 0.0742 �0.031 0.078 0.1082 0.095 0.197 0.1021

(0.014) (0.020) (0.024) (0.021) (0.034) (0.039) (0.018) (0.023) (0.029)

Notes. This table report on the regime-specific averages for the VIX level, the daily variability of VIX, the futures volume, and thestock illiquidity. An observation-day is considered to be in a given regime when the filtered probability is greater than 50%, based onthe Table II model. For both the high-stress and low-stress regime-days t, the regime-specific mean and its standard deviation (inparentheses) are reported for: (1) the lagged level; (2) the daily VIX variability, defined as the average absolute VIX changebetween the close of day and day t � 1; (3) our lagged stock market-wide illiquidity measures, and , where highervalues are more illiquid; and (4) our lagged standardized volume measure for stock index and Treasury futures, and .The Diff in Means is the difference-in-means between the high-stress regime mean and the low-stress regime mean with statisticalsignificance indicated by 1, 2, 3 for p-values at the 0.1%, 1%, and 5% level, respectively. The table reports separately for the1997–2005, 1997–2000, and 2001–2005 periods.

BdVolt�1StVolt�1

RRVt�1PIMt�1tVIXt�1

BdVolt�1

StVolt�1

RRVt�1

PIMt�1

(¢VIXt)

VIXt�1

Regime-Switching in Stock and T-notes Futures Returns 771

Journal of Futures Markets DOI: 10.1002/fut

We evaluate and report regime-specific statistics for the “market stress”variables for trading day t � 1, relative to a given regime-day t. We make thischoice to provide temporal separation, which opens up the possibility that thevalue of the market-stress variable might contain information about the proba-bility of regime-switching (an issue that we evaluate in Regime-switching withTVTP section). In practice, due to the sizable durations of the regimes, thecomparisons are essentially the same if we instead report the averages of the values actually observed on regime-day t (instead of day t � 1).

Stock-implied volatility

We begin by discussing the implied volatility from option prices. For our esti-mation over the full sample, the average value of lagged VIX is 30.5% for thehigh-stress regime vs. 19.8% for the low-stress regime, or about 54% higher forthe high-stress regime. For all three periods in Table III, the regime differencein lagged VIX is sizable and statistically reliable at a 0.1% p-value.

We also compare the daily VIX variability between the high-stress and low-stress regime days. The daily VIX variability is evaluated as the average absolutedaily VIX change, defined as the absolute difference between the VIX close forday t and day t � 1. The daily variability in VIX is of interest in our study,because it may signal variability in the relative attractiveness of stocks andbonds. Such variability seems to fit with the observed negative stock–bond cor-relation in the high-stress regime. Over our full sample, the average absolutedaily VIX change in the high-stress regime is 2.2 times that in the low-stressregime. Subperiod results are similar.

Stock illiquidity

Table III also reports on how our two stock market-wide illiquidity measures,PIM and RRV, vary across the two regimes. We estimate both illiquidity meas-ures over the month preceding each trading day (using individual stock returnand volume data over days t � 1 to t � 22) and then evaluate for regime-specificdifferences in the illiquidity measures. For both illiquidity measures, we findthat the lagged stock illiquidity is higher for the high-stress vs. the low-stressregime days, with the difference being statistically significant at a p-value of0.1% or better. Subperiod results are consistent.

Futures trading volume

In our view, futures hedging is also likely to be higher during times of marketstress when flight-to-quality and/or flight-to-liquidity are more likely to haveimportant pricing influences. Accordingly, we are also interested in how futuresvolume varies across regimes. As detailed in Introduction section, our work

772 Bansal, Connolly, and Stivers

Journal of Futures Markets DOI: 10.1002/fut

here features a standardized, detrended volume measure that controls for long-term growth in the volume over time and the quarterly seasonality in futurestrading volume. Our standardized volume measure indicates the percentageincrease in that day’s volume, relative to the average volume over a lagged mov-ing average that is chosen to take into account the quarterly futures cycle. Weevaluate the standardized volume on day t � 1 relative to regime-day t.

We find that the lagged standardized trading volume for both the stockindex and long-term Treasury futures is appreciably higher for the high-stressregime days than for the low-stress regime days. Over the 1997–2005 period,the average trading volume for the stock index futures preceding the high-stress regime days is about 22% higher than the lagged moving average. In con-trast, the comparable average trading volume preceding the low-stress regimedays is only about 1.6% higher than the lagged moving average. This regime dif-ference of nearly 21% is statistically significant at a 0.1% p-value. Subperiodsresults are consistent. Regime differences in the standardized volume for thelong-term Treasury futures are qualitatively similar and statistically significant,but somewhat more modest.

To sum up, we find that the futures trading volume is appreciably higher pre-ceding high-stress regime days, as compared to the low-stress regime days. Thehigher futures volume in the high-stress regime may reflect both greater informa-tion flows and greater hedging demand. Presumably, agents could be hedging thegreater stock risk directly by shorting the stock futures, or collaterally with a cross-market hedge that increases their exposure to long-term Treasury securities.

Regime-Switching With TVTP

Given our results in Tables II and III, a natural question is whether either thestock-implied volatility, the stock illiquidity, or the stock index futures tradingvolume is informative about the transition probabilities for the regime-switchingprocess. In other words, are the lagged nonreturn measures of stock marketstress informative about the probability of switching regimes? Accordingly, weestimate the same regime-switching model, given by Equations (4) and (5), butnow allowing for TVTP.

Initially, we allow the transition probabilities to vary with lagged VIX, asfollows:

(6)

where j � 1 (regime-one) or j � 2 (regime-two); pjj(t) is the probability of stay-ing in regime j for day t (the second subscript) given that day t � 1 is already inregime j (the first subscript); VIXt�1 is the closing VIX on day t � 1. The , ,

s, s, and correlations between the s are parameters to be estimated.htdjcj

s jsmj

s

pjj(t) �ecj�djVIXt � 1

1 � ecj�djVIXt � 1

Regime-Switching in Stock and T-notes Futures Returns 773

Journal of Futures Markets DOI: 10.1002/fut

Table IV reports on the estimation for this VIX-TVTP model. It is reas-suring to see how robust our earlier findings about differences in stock–bondcorrelations and the stock volatilities are in all three estimation periods. Thepatterns in regime-specific means are also consistent with comparable resultsin Table II, but the statistical significance is weaker.

Importantly, note that all the estimated dj coefficients are statistically sig-nificant and indicate that: (1) the probability of shifting from the low-stressregime to the high-stress regime is increasing in lagged VIX, and (2) the proba-bility of shifting from the high-stress regime to the low-stress regime is decreas-ing in lagged VIX.

We also estimate comparable regime-switching models with TVTP substi-tuting for lagged VIX the following other four stock market stress variables: (1) thelagged daily VIX variability, defined as the average absolute daily VIX change

TABLE IV

VIX Level and Time-Varying Transition Probabilities

1997–2005 Period 1997–2000 Period 2001–2005 Period

Low High Low High Low High Stress Stress Stress Stress Stress Stress

Coeff. ( j � 1) (j � 2) (j � 1) (j � 2) (j � 1) (j � 2)

0.049 �0.260 0.425 �0.337 �0.008 �0.419(0.032) (0.034)1 (0.045)1 (0.060)1 (0.043) (0.050)1

0.729 1.794 0.964 1.836 0.652 1.634(0.025) (0.058) (0.033) (0.090) (0.027) (0.088)0.307 0.481 0.301 0.368 0.348 0.506

(0.010) (0.015) (0.009) (0.017) (0.023) (0.022)0.035 �0.047 0.045 �0.016 0.018 �0.052

(0.026) (0.067) (0.043) (0.107) (0.027) (0.076)0.011 0.025 �0.013 0.059 0.016 0.026

(0.009) (0.032) (0.012) (0.023)3 (0.014) (0.025)9.04 �7.44 9.29 �6.77 11.71 �9.60

(1.35)1 (1.82) (2.74)1 (4.42) (2.42)1 (3.72)3

�0.368 0.260 �0.283 0.311 �0.551 0.364(0.060)1 (0.065)1 (0.104)2 (0.166)4 (0.130)1 (0.147)3

Log-likelihood �4252.62 �1842.34 �2319.26% Observ. 68.3% 31.7% 69.8% 30.2% 62.5% 37.5%

Notes. This table reports on regime-switching for the joint stock-bond futures return distribution, when allowing for time-varying tran-sition probabilities. The return equations and estimation details are the same as for Table II, except for the time-varying transitionprobabilities, . The transition probabilities, may vary with lagged VIX as follows:

where j � 1 (regime-one) or j � 2 (regime-two); is the probability of being in regime j for day t (the second subscript) given that

day t � 1 is in regime j (the first subscript); is the closing VIX on day t � 1. The , j, s, djs, and correlations between thes are parameters to be estimated. We report separately on the 1997–2005, 1997–2000 and 2001 to 2005 periods. Standard errors

are in parentheses. 1, 2, 3, and 4 indicate 0.1%, 1%, 5%, and 10% p-values for whether the estimated regime-specific means, correla-tions, and the cj’s and dj’s are different than zero.

ht

cjs j

sm jsVIXt�1

pjj (t)

pjj(t) �ecj�djVIXt � 1

1 � ecj�djVIXt � 1

pjj (t),pjj (t)

dj

cj

mjb

mjs

sjb

sjs

rj

774 Bansal, Connolly, and Stivers

Journal of Futures Markets DOI: 10.1002/fut

over trading days t � 1 to t � 22; (2) the lagged PIM stock illiquidity measure,constructed from daily return and volume data over days t � 1 to t � 22; (3) thelagged RRV stock illiquidity measure, constructed from daily return and vol-ume data over days t � 1 to t � 22; and (4) the average of the lagged standard-ized stock futures volume over days t � 1 to t�22. We use the same specifica-tion as in Equation (6), except one of these four other variables replaces laggedVIX. For these four additional TVTP models, we find that only the models withlagged daily VIX variability and the lagged PIM have statistically reliably dj

coefficients and in only some cases.Table V reports on the model where the TVTP may vary with lagged daily

VIX variability. We find that the estimated d1 coefficient is negative for all threeperiods. This indicates the chance of shifting from the low-stress regime to the

TABLE V

Daily VIX Variability and Time-Varying Transition Probabilities

1997–2005 Period 1997–2000 Period 2001–2005 Period

Low High Low High Low High StressStress Stress Stress Stress Stress Stress

Coeff. ( j � 1) (j � 2) (j � 1) (j � 2) (j � 1) (j � 2)

0.152 �0.441 0.427 �0.344 �0.019 �0.546(0.031)1 (0.040)1 (0.044)1 (0.059)1 (0.036) (0.034)1

0.840 1.718 0.986 1.793 0.737 1.652(0.026) (0.056) (0.033) (0.091) (0.021) (0.058)0.375 0.386 0.303 0.363 0.416 0.419

(0.008) (0.012) (0.010) (0.018) (0.010) (0.015)0.050 �0.076 0.077 �0.076 0.030 �0.084

(0.024)3 (0.062) (0.043)4 (0.088) (0.027) (0.079)�0.004 0.052 �0.012 0.055 �0.0017 0.060(0.010) (0.015)1 (0.013) (0.023)3 (0.014) (0.020)2

6.45 3.84 5.48 2.66 6.25 3.34(0.879)1 (0.973)1 (0.874)1 (1.03)2 (1.54)1 (1.45)3

�2.65 �0.572 �1.98 �0.236 �1.69 0.612(0.803)1 (0.636) (0.678)2 (0.628) (1.84) (1.07)

Log-likelihood �4308.97 �1850.74 �2342.45% Observ. 63.8% 36.2% 66.9% 33.1% 64.5% 35.5%

Notes. This table reports on regime-switching for the joint stock–bond futures return distribution, when allowing for time-varyingtransition probabilities. The return equations and estimation details are the same as for Table II, except for thetime-varying transitionprobabilities, . The transition probabilities, , may vary with the lagged daily VIX variability as follows:

where j � 1 (regime-one) or j � 2 (regime-two); is the probability of being in regime j for day t (the second subscript) given thatday t � 1 is in regime j (the first subscript); is the lagged daily VIX variability, defined as the average daily absolutechange in the VIX value over days t � 1 to t � 22; the , , s, s, and correlations between the s are parameters to be esti-mated. We report separately on the 1997–2005, 1997–2000 and 2001–2005 periods. Standard errors are in parentheses. 1, 2, 3, and 4

indicate 0.1%, 1%, 5%, and 10% p-values for whether the estimated regime-specific means, correlations, and the cj’s and dj’s are dif-ferent than zero.

htdjcjs jsm j

s

Variability(VIX)t�1

pjj (t)

pjj (t) �ecj�djVariability (VIX)t � 1

1 � ecj�djVariability (VIX)t � 1

pjj(t)pjj (t)

dj

cj

mjb

mjs

sjb

sjs

rj

Regime-Switching in Stock and T-notes Futures Returns 775

Journal of Futures Markets DOI: 10.1002/fut

high-stress regime increases with lagged daily VIX variability. This result is statis-tically significant for only the overall period and the first subperiod.

Table VI report on the TVTP model with lagged PIM. We find that the esti-mated d1 coefficient is negative for all three periods, indicating the probabilityof switching from the low-stress regime to the high-stress regime tends toincrease with the PIM stock illiquidity. The estimated coefficient is statisticallysignificant in only the overall period and second subperiod. The estimated d2

coefficient has mixed results, so the PIM is not reliably informative about thetransition probabilities when in the high-stress regime.

Among the five TVTP models, the lagged VIX is clearly the strongest, mostreliable performer across the “market stress” variables that we examine. Thelagged daily VIX variability and lagged PIM provide consistent, but weaker,

TABLE VI

PIM Stock Illiquidity and Time-Varying Transition Probabilities

1997–2005 Period 1997–2000 Period 2001–2005 Period

Low High Low High Low HighStress Stress Stress Stress Stress Stress

Coeff. ( j � 1) (j � 2) (j � 1) (j � 2) (j � 1) (j � 2)

0.148 �0.459 0.408 �0.292 �0.019 �0.547(0.029)1 (0.037)1 (0.046)1 (0.057)1 (0.036) (0.035)1

0.860 1.737 0.991 1.754 0.738 1.653(0.025) (0.057) (0.033) (0.084) (0.022) (0.063)0.373 0.390 0.294 0.374 0.415 0.419

(0.008) (0.013) (0.010) (0.017) (0.010) (0.014)0.049 �0.082 0.082 �0.077 0.028 �0.082

(0.026)4 (0.056) (0.044)4 (0.097) (0.028) (0.076)�0.0049 0.0574 �0.0038 0.037 �0.0018 0.061(0.0098) (0.015)1 (0.012) (0.023) (0.014) (0.019)2

7.38 5.15 4.84 �0.49 9.41 6.33(1.01)1 (1.11) (1.23)1 (1.53) (1.75)1 (1.73)1

�18.32 �9.19 �6.40 15.28 �29.74 �12.55(4.79)1 (5.39)4 (6.45) (8.01)4 (10.12)2 (9.48)

Log-likelihood �4308.70 �1850.64 �2339.11% Observ. 66.6% 33.4% 65.9% 34.1% 62.8% 37.2%

Notes. This table reports on regime-switching for the joint stock–bond futures return distribution, when allowing for time-varyingtransition probabilities. The return equations and estimation details are the same as for Table II, except for the time-varying transitionprobabilities, . The transition probabilities, , may vary with the lagged PIM stock illiquidity as follows:

where j � 1 (regime-one) or j � 2 (regime-two); is the probability of being in regime j for day t (the second subscript) given thatday t � 1 is in regime j (the first subscript); is the lagged PIM illiquidity, which is constructed using daily returns and volume overdays t � 1 to t � 22; the , , s, s, and correlations between the s are parameters to be estimated. We report separately onthe 1997–2005, 1997–2000 and 2001–2005 periods. Standard errors are in parentheses. 1, 2, 3, and 4 indicate 0.1%, 1%, 5%, and 10% p-values for whether the estimated regime-specific means, correlations, and the cj’s and dj’s are different than zero.

htdjcjs jsm j

s

PIMt�1

pjj(t)

pjj(t) �ecj�djPIMt � 1

1 � ecj�djPIMt � 1

pjj(t)pjj(t)

dj

cj

mjb

mjs

sjb

sjs

rj

776 Bansal, Connolly, and Stivers

Journal of Futures Markets DOI: 10.1002/fut

information about the TVTP. The lagged RRV and stock futures volume are notreliable explanatory factors for the TVTP in any case.

CONCLUSIONS

In this article, we study regime-switching in daily stock index and ten-year T-note futures returns. Our empirical work features a bivariate, two-state,regime-switching model that simultaneously estimates regime-specific means,variances, and correlations. We investigate the differences across regimes inrealized means, realized volatilities, stock–bond correlations, option-derivedstock-implied volatility, stock illiquidity, and futures trading volume. Our sam-ple period features multiple episodes of high equity risk but has stable infla-tion, which we feel is a good fit for our purposes.

We find a predominant low-stress regime (less-common high-stress regime)with an expected duration of 80 days (44 days). High-stress regime episodesoccur in proximity to well-known international economic and political crisissuch as the Asian financial crisis in the fall of 1997, the Russian currency deval-uation and debt default in the fall of 1998, the Brazilian currency crisis in early1999, the terrorism crisis in September 2001, and the Iraq war in 2003.

We document a striking contrast between regimes, with a high-stressregime that exhibits a much higher stock volatility, a much lower stock–bondcorrelation, and a higher bond-return mean. The high-stress regime days arepreceded by much higher VIX, higher stock illiquidity, and higher trading vol-ume in stock index and T-note futures contracts. The daily variability of VIX isalso appreciably higher during the high-stress regime. We also find that some ofthese measures of stock market stress, especially the lagged VIX, are useful inmodeling the TVTP of the regime-switching process.

In Pastor and Stambaugh (2003), they argue that measures of stock mar-ket illiquidity should be negatively associated with the stock–bond correlation,and they use this belief as a key criteria in selecting the empirical specificationfor their return-reversal measure. In our investigation, we document a tiebetween our two measures of stock illiquidity and the stock–bond correlations,and in a direction that supports the reasoning in Pastor and Stambaugh.

Collectively, our findings have two key implications for periods with rela-tively high equity risk, relatively high variability in equity risk, and modest T-bond risk; such as our 1997–2005 sample period. First, the diversificationbenefits of combined stock–bond holdings are greater during the episodes ofhigh stock market stress. Second, it appears that stock market stress can have amaterial influence on Treasury bond pricing and the joint stock–bond returndistribution. Of course, on a more primitive level, stock and bond pricing areboth endogenous to the underlying economic news and conditions. However,

Regime-Switching in Stock and T-notes Futures Returns 777

Journal of Futures Markets DOI: 10.1002/fut

in a market environment with modest T-bond risk and modest and stable infla-tion, our results suggest that stock market stress can be thought of as having aninfluence on T-bond pricing.

APPENDIX A

A regime-switching model for daily stock index and ten-year T-note spot returnsis given in Tabel AI.

TABLE AI

A Regime-Switching Model for Daily Stock Index and Ten-Year T-note Spot Returns

Sample Period: 1997–2005

Low Stress High Stress RegimeCoeff. ( j � 1) (j � 2) Difference

0.129 �0.319 0.448(0.038)*** (0.035)*** [�0.001]0.829 1.598 �0.769

(0.027) (0.055) [�0.001]0.388 0.566 �0.178

(0.010) (0.018) [�0.001]0.074 �0.015 0.089

(0.024)*** (0.051) [0.121]0.023 0.028 �0.006

(0.0112)** (0.015) [0.798]0.0140

(0.0046)0.0212

(0.0072)Duration 71 days 47 daysLog-likelihood �4811.05

Notes. This table reports results from estimating the following two-state, bivariate regime-switching model on the daily spot returnsof S&P 500 and ten-year Treasury notes:

Where the s and b subscripts indicate stock and bond terms, respectively; the superscript j indicates regime-specific parameters, withj �1 for the low-stress regime or j � 2 for the high-stress regime; and are the daily spot returns of stock index and ten-yearTreasury notes; and are the regime-specific mean returns; and are the regime-specific standard deviations; and and

are the return shocks, which follow a standard bivariate normal distribution with regime-specific correlations . The j state variableis modeled with constant transition probabilities, , which equals the probability that the regime in period t is j (the second subscript),given that the regime in period t � 1 is j (the first subscript).

The means, standard deviations, correlations, and transition probabilities are regime-specific parameters to be estimated. We esti-mate the model by maximizing the log-likelihood function for the bivariate normal density with regime switching. Standard errors arein parentheses. ***, **, and * indicate 1%, 5%, and 10% p-values for whether the estimated regime-specific means and correlationsare different than zero. The second-last row reports the expected duration of the respective regime. The column labeled as “RegimeDifference” reports the regime differences for the estimated return parameters, with a p-value in brackets for the null that the respec-tive parameters are the same for both regimes.

pjj

rjhb,t

hs,tsjbsj

smjbmj

s

rb,trs,t

rb,t � mjb � sj

bhb,t

rs,t � mjs � sj

shs,t

p21

p12

mjb

mjs

sjb

sjs

rj

778 Bansal, Connolly, and Stivers

Journal of Futures Markets DOI: 10.1002/fut

BIBLIOGRAPHY

Ahn, D., Boudoukh, J., Richardson, M., & Whitelaw, R. (2002). Partial adjustment orstale prices? Implications from stock index and futures return autocorrelations.Review of Financial Studies, 15, 655–689.

Amihud, Y. (2002). Illiquidity and stock returns: Cross-section and time-series effects.Journal of Financial Markets, 5, 31–56.

Ang, A., & Bekaert, G. (2002a). International asset allocation with regime shifts.Review of Financial Studies, 15, 1137–1187.

Ang, A., & Bekaert, G. (2002b). Regime switches in interest rates. Journal of Businessand Economic Statistics, 20, 163–182.

Ang, A., & Bekaert, G. (2002c). Short rate nonlinearities and regime switches. Journalof Economic Dynamics And Control, 26, 1243–1274.

Ang, A., & Bekaert, G. (2004). How do regimes affect asset allocation? FinancialAnalysts Journal, 60, 86–99.

Bessembinder, H., & Seguin, P. (1992). Futures trading activity and stock price volatil-ity. Journal of Finance, 47, 2015–2034.

Bollerslev, T., & Wooldridge, J. (1992). Quasi-maximum likelihood estimation andinference in dynamic models with time-varying covariances. EconometricReviews, 11, 143–172.

Campbell, J., & Ammer, J. (1993). What moves the stock and bond markets? A variancedecomposition for long-term asset returns. Journal of Finance, 48, 3–37.

Carchano, O., & Pardo, A. (2009). Rolling over stock index futures contracts. TheJournal of Futures Markets, 29, 684–694.

Connolly, R., Stivers, C., & Sun, L. (2005). Stock market uncertainty and the stock-bond return relation. Journal of Financial and Quantitative Analysis, 40, 161–194.

Connolly, R., Stivers, C., & Sun, L. (2007). Commonality in the time-variation ofstock-stock and stock-bond return comovements. Journal of Financial Markets,10, 192–218.

Fama, E., & French, K. (1989). Business conditions and expected returns on stocksand bonds. Journal of Financial Economics, 25, 23–49.

Fleming, J., Kirby, C., & Ostdiek, B. (1998). Information and volatility linkages in thestock, bond, and money markets. Journal of Financial Economics, 49, 111–137.

Fleming, J., Kirby, C., & Ostdiek, B. (2001). The economic value of volatility timing.Journal of Finance, 56, 329–352.

Fleming, J., Kirby, C., & Ostdiek, B. (2003). The economic value of volatility timingusing “realized” volatility. Journal of Financial Economics, 67, 473–509.

Gong, F., & Mariano, R. S. (1997). Testing under non-standard conditions in frequen-cy domain: With applications to markov regime switching models of exchangerates and the federal funds rate. Federal Reserve Bank of New York Technical StaffReport.

Guidolin, M., & Timmermann, A. (2006). An econometric model of nonlinear dynam-ics in the joint distribution of stock and bond returns. Journal of AppliedEconometrics, 21, 1–22.

Gulko, L. (2002). Decoupling. Journal of Portfolio Management, 28, 59–66.Hansen, B. (1996). Inference when a nuisance parameter is not identified under the

null hypothesis. Econometrica, 64, 413–430.

Regime-Switching in Stock and T-notes Futures Returns 779

Journal of Futures Markets DOI: 10.1002/fut

Hartmann, P., Straetmans, S., & Devries, C. (2004). Asset market linkages in crisisperiods. Review of Economics and Statistics, 86, 313–326.

Hasbrouck, J. (2005). Trading costs and returns for US equities: The evidence fromdaily data (Working Paper). New York University.

Kodres, L., & Pritsker, M. (2002). A rational expectations model of financial contagion.Journal of Finance, 57, 769–799.

Li, L. (2002). Macroeconomic factors and the correlation of stock and bond returns(Working Paper). Yale University.

Pastor, L., & Stambaugh, R. F. (2003). Liquidity risk and expected stock returns.Journal of Political Economy, 111, 642–685.

Scruggs, J., & Glabadanidis, P. (2003). Risk premia and the dynamic covariancebetween stock and bond returns. Journal of Financial and Quantitative Analysis,38, 295–316.