Embed Size (px)

Citation preview

© 2015 UOP LLC. A Honeywell Company All rights reserved.

A New Look at Integration Opportunities

Refining-Petrochemical IntegrationStan S. Carp

Sr. Manager, Configuration and

Process Consultancy

29/07/2017 6th Petrochemical Conclave Gandhinagar, Gujarat, India

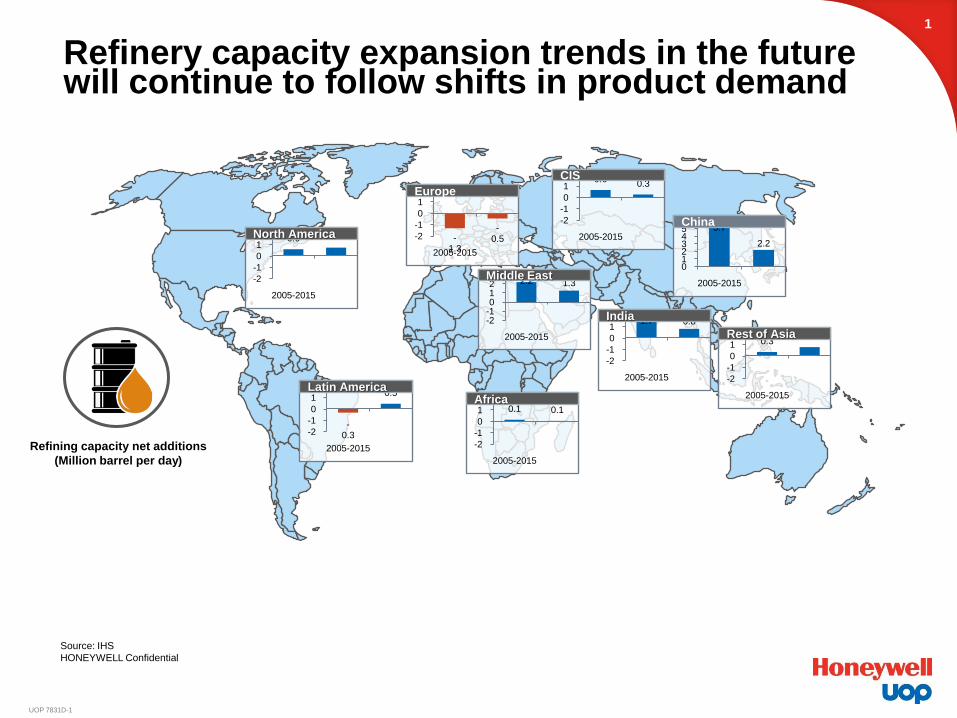

Refinery capacity expansion trends in the future will continue to follow shifts in product demand

1

UOP 7831D-1

Refining capacity net additions

(Million barrel per day)

-0.3

0.5

-2

-1

0

1

2

2005-2015

Latin America

0.6 0.7

-2

-1

0

1

2

2005-2015

North America

0.60.3

-2

-1

0

1

2

2005-2015

CIS

-1.3

-0.5-2

-1

0

1

2

2005-2015

Europe

2.2 1.3

-2-10123

2005-2015

Middle East

0.1 0.1

-2

-1

0

1

2

2005-2015

Africa

5.7

2.2

0123456

2005-2015

China

1.7 0.8

-2

-1

0

1

2

2005-2015

India

0.30.8

-2

-1

0

1

2

2005-2015

Rest of Asia

Source: IHS

HONEYWELL Confidential

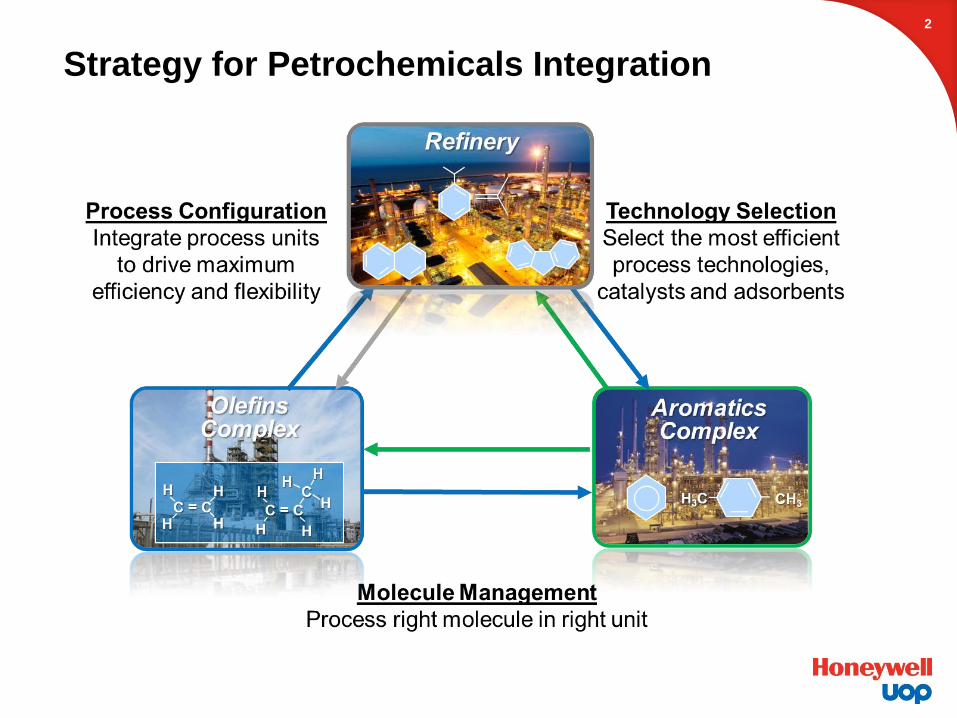

Strategy for Petrochemicals Integration

2

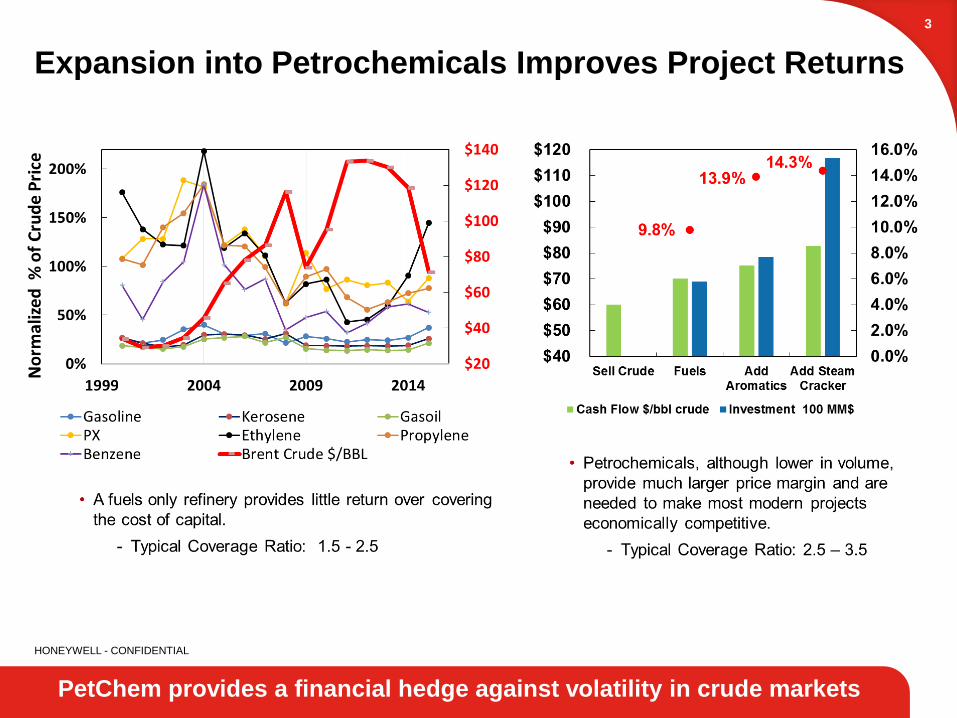

Expansion into Petrochemicals Improves Project Returns

PetChem provides a financial hedge against volatility in crude markets

3

HONEYWELL - CONFIDENTIAL

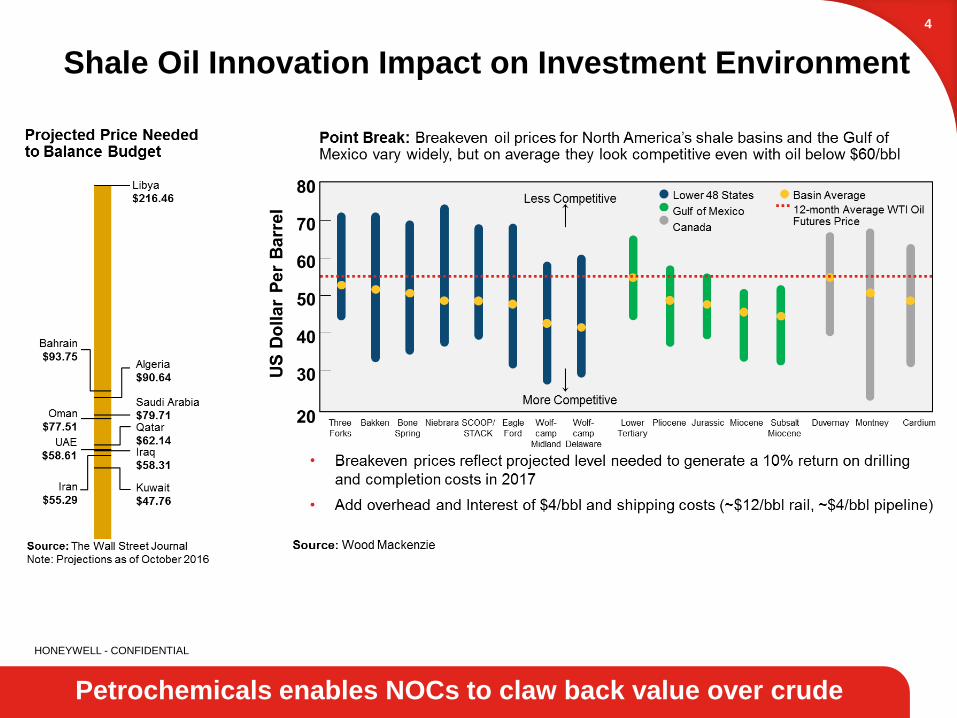

Shale Oil Innovation Impact on Investment Environment

Petrochemicals enables NOCs to claw back value over crude

4

HONEYWELL - CONFIDENTIAL

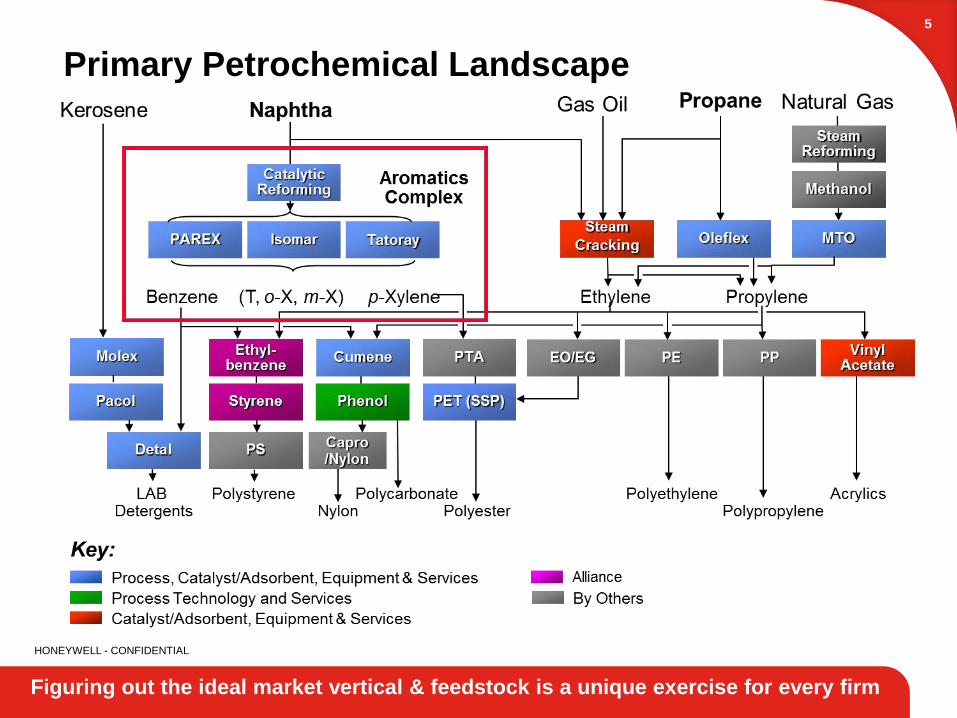

Primary Petrochemical Landscape

Figuring out the ideal market vertical & feedstock is a unique exercise for every firm

5

HONEYWELL - CONFIDENTIAL

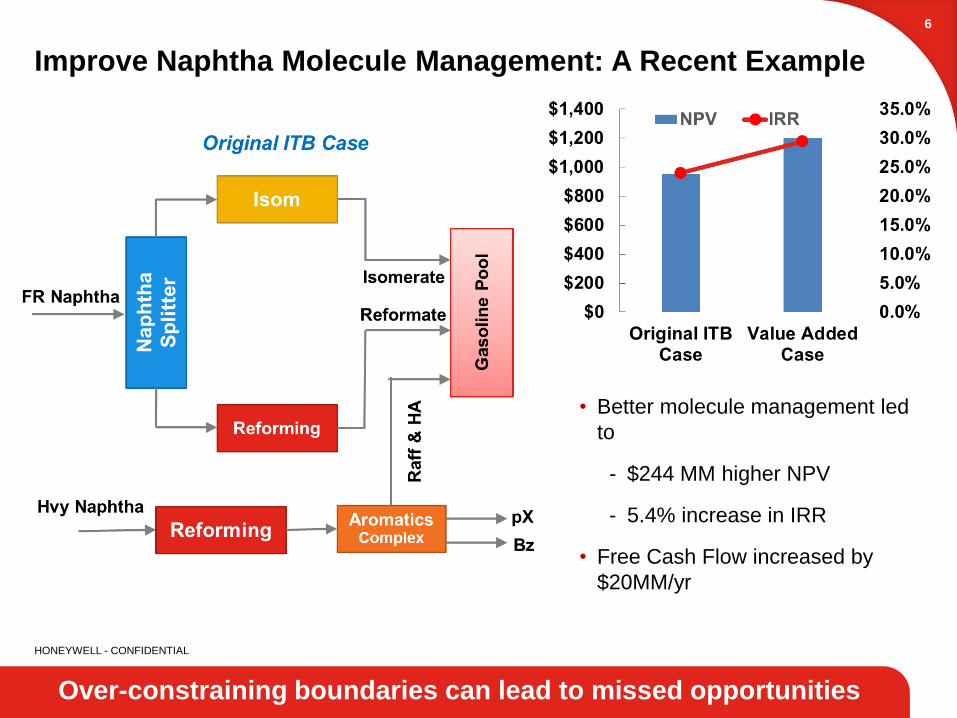

Improve Naphtha Molecule Management: A Recent Example

Over-constraining boundaries can lead to missed opportunities

6

• Better molecule management led

to

- $244 MM higher NPV

- 5.4% increase in IRR

• Free Cash Flow increased by

$20MM/yr

HONEYWELL - CONFIDENTIAL

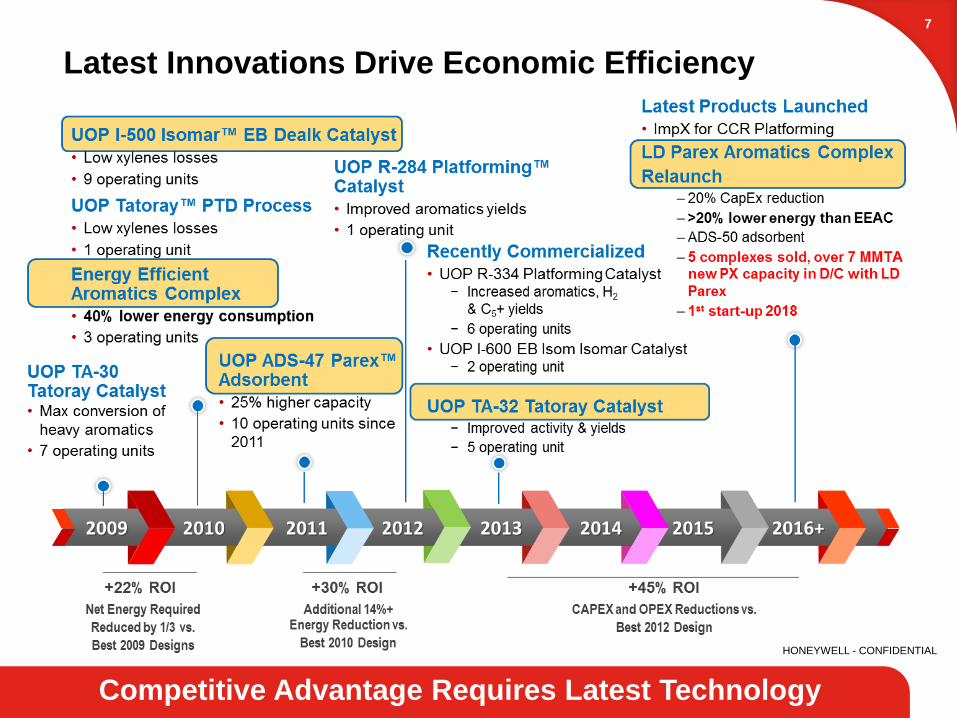

Latest Innovations Drive Economic Efficiency

Competitive Advantage Requires Latest Technology

7

HONEYWELL - CONFIDENTIAL

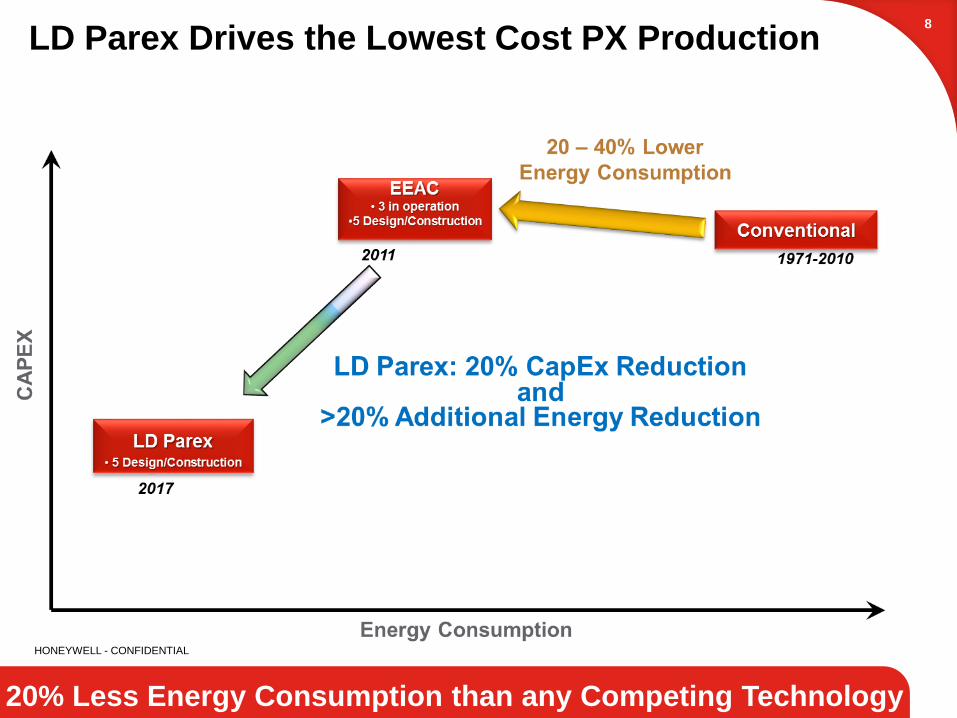

LD Parex Drives the Lowest Cost PX Production

20% Less Energy Consumption than any Competing Technology

8

HONEYWELL - CONFIDENTIAL

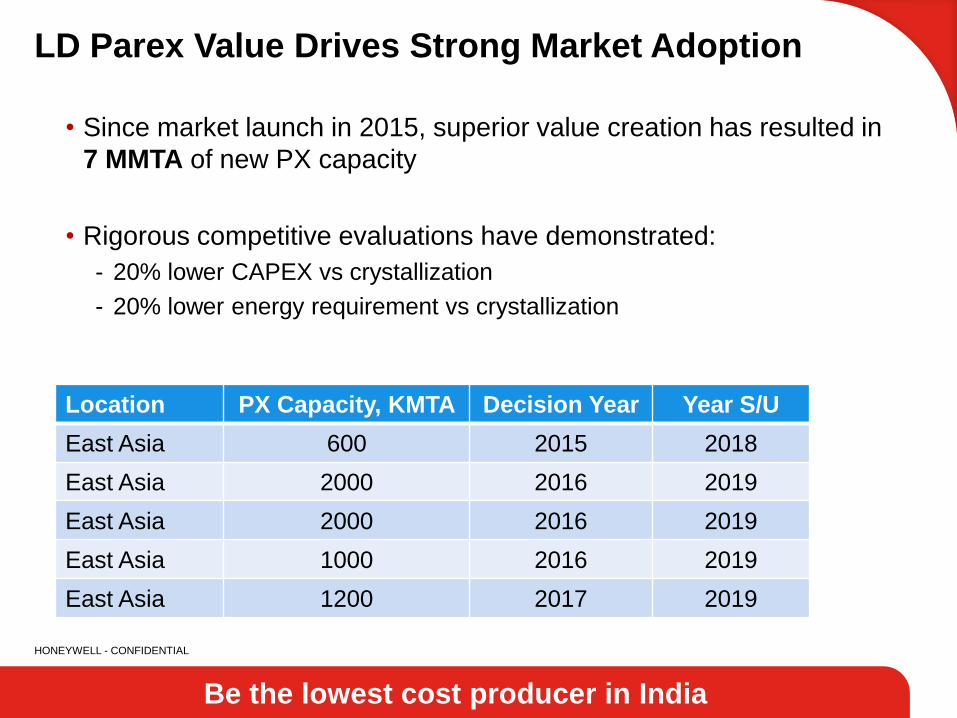

LD Parex Value Drives Strong Market Adoption

• Since market launch in 2015, superior value creation has resulted in

7 MMTA of new PX capacity

• Rigorous competitive evaluations have demonstrated:

- 20% lower CAPEX vs crystallization

- 20% lower energy requirement vs crystallization

Be the lowest cost producer in India

Location PX Capacity, KMTA Decision Year Year S/U

East Asia 600 2015 2018

East Asia 2000 2016 2019

East Asia 2000 2016 2019

East Asia 1000 2016 2019

East Asia 1200 2017 2019

HONEYWELL - CONFIDENTIAL

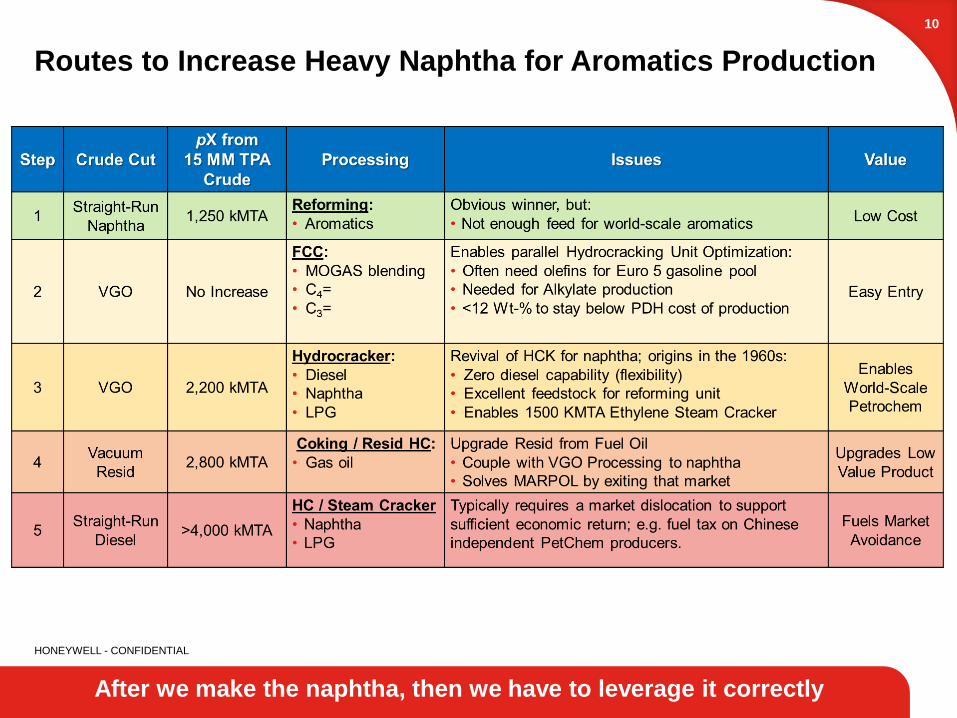

Routes to Increase Heavy Naphtha for Aromatics Production

After we make the naphtha, then we have to leverage it correctly

10

HONEYWELL - CONFIDENTIAL

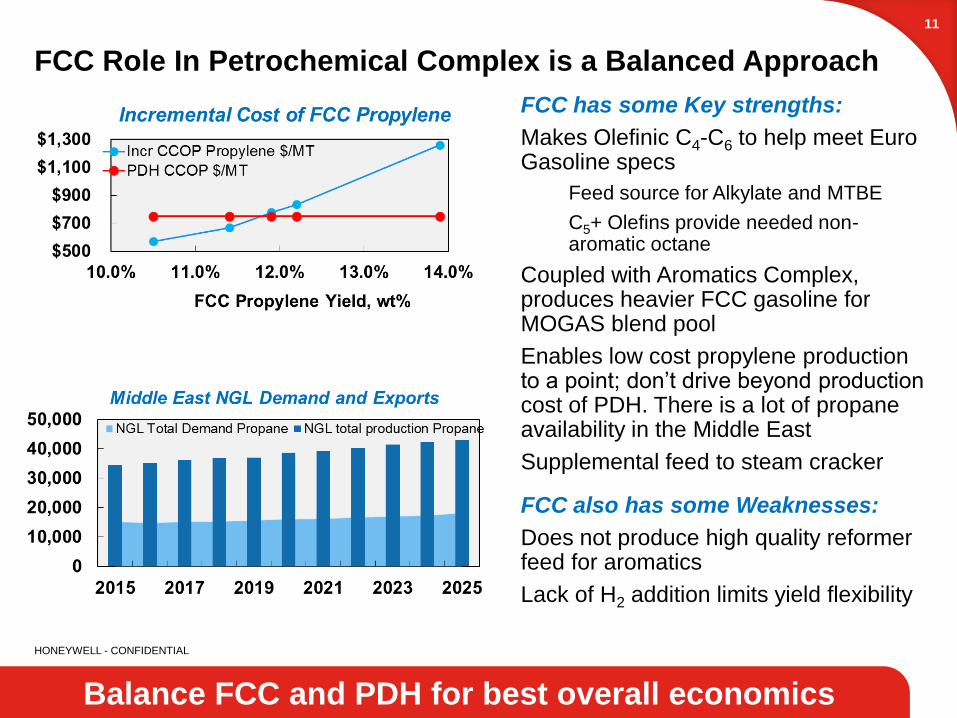

FCC Role In Petrochemical Complex is a Balanced Approach

Balance FCC and PDH for best overall economics

11

FCC has some Key strengths:

Makes Olefinic C4-C6 to help meet Euro Gasoline specs

Feed source for Alkylate and MTBE

C5+ Olefins provide needed non-aromatic octane

Coupled with Aromatics Complex, produces heavier FCC gasoline for MOGAS blend pool

Enables low cost propylene production to a point; don’t drive beyond production cost of PDH. There is a lot of propane availability in the Middle East

Supplemental feed to steam cracker

FCC also has some Weaknesses:

Does not produce high quality reformer feed for aromatics

Lack of H2 addition limits yield flexibility

HONEYWELL - CONFIDENTIAL

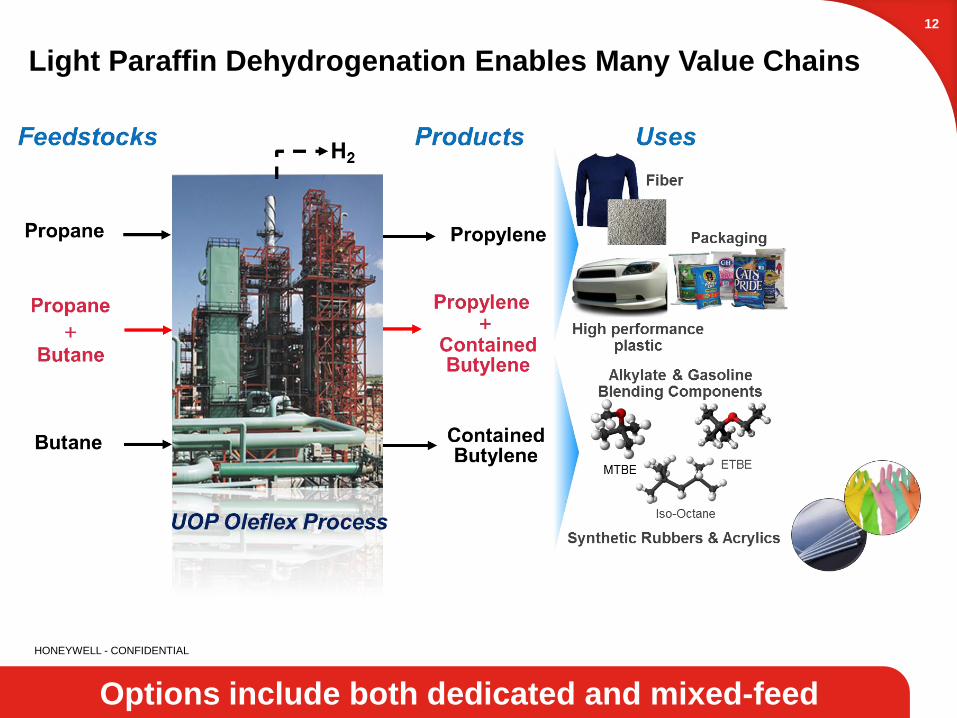

Light Paraffin Dehydrogenation Enables Many Value Chains

Options include both dedicated and mixed-feed

applications

12

HONEYWELL - CONFIDENTIAL

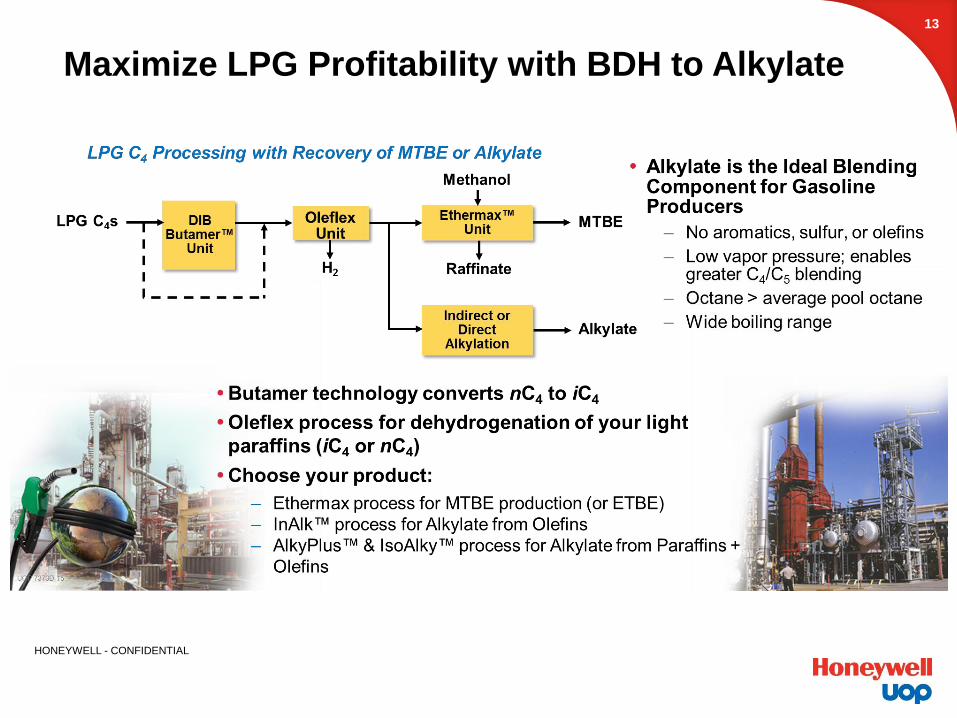

Maximize LPG Profitability with BDH to Alkylate

13

HONEYWELL - CONFIDENTIAL

Summary

Regional fuel demands will support local refining investments

Petrochemical integration enables higher quality investment

Latest technology advances provide a step-change in value creation over those just licensed 5 years ago

Leveraging latest available technologies is critical to maintaining a competitive position

New Petrochemical complexes will need refinery upgrades for Heavy Naphtha supply

Maximize the return on your R&P Integrated investment through:

– Understanding of market dynamics

– Selecting the right technology

– Optimal upfront configuration

14

15

UOP 7116-15

![RABIGH REFINING AND PETROCHEMICAL ساسϸا ϢاظنϠا ......23/05/2017 10:35 [(1 قفرم).docx] RABIGH REFINING AND PETROCHEMICAL COMPANY (A Saudi Arabian Joint Stock Company)](https://img.pdfslide.us/doc/110x75/6093ddff78d40270c056c30b/rabigh-refining-and-petrochemical-23052017-1035.jpg)