Embed Size (px)

Citation preview

Referencer for Quick Revision

B o a r d o f S t u d i e s

( A c a d e m i c )

I C A I

Intermediate Course Paper-4:

Taxation

A compendium of subject-wise capsules published in the

monthly journal “The Chartered Accountant Student”

INDEX

Paper No.

Subject Page No.

Edition of Students’ Journal

Topics

4A Income-tax Law

1-5 April 2020 Advance Tax, Tax Deduction at Source and Introduction to Tax Collection at Source

5-8 April 2020 Provisions for Filing Return of Income and Self-Assessment

4B Indirect Taxes

9-11 February 2020 Registration

12-13 February 2020 Tax Invoice: Credit and Debit Notes

08 April 2020 The Chartered Accountant Student

INCOME TAX LAW INCOME TAX LAW : A CAPSULE FOR QUICK RECAP

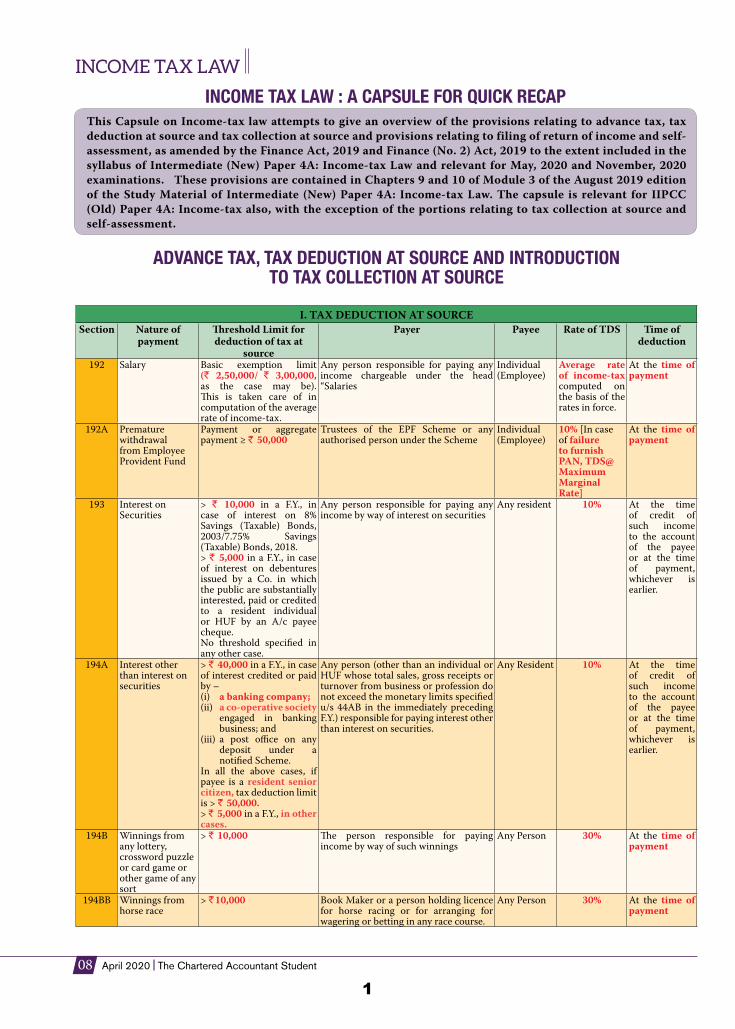

ADVANCE TAX, TAX DEDUCTION AT SOURCE AND INTRODUCTION TO TAX COLLECTION AT SOURCE

This Capsule on Income-tax law attempts to give an overview of the provisions relating to advance tax, tax deduction at source and tax collection at source and provisions relating to filing of return of income and self-assessment, as amended by the Finance Act, 2019 and Finance (No. 2) Act, 2019 to the extent included in the syllabus of Intermediate (New) Paper 4A: Income-tax Law and relevant for May, 2020 and November, 2020 examinations. These provisions are contained in Chapters 9 and 10 of Module 3 of the August 2019 edition of the Study Material of Intermediate (New) Paper 4A: Income-tax Law. The capsule is relevant for IIPCC (Old) Paper 4A: Income-tax also, with the exception of the portions relating to tax collection at source and self-assessment.

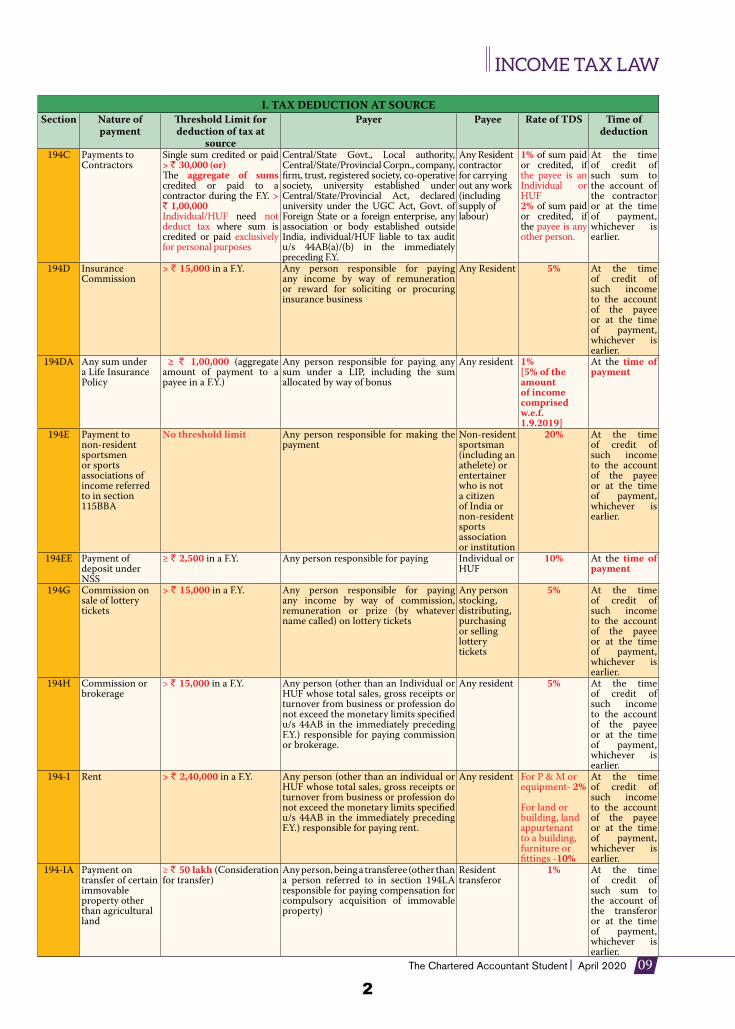

I. TAX DEDUCTION AT SOURCESection Nature of

payment�reshold Limit for deduction of tax at

source

Payer Payee Rate of TDS Time of deduction

192 Salary Basic exemption limit (R 2,50,000/ R 3,00,000, as the case may be). �is is taken care of in computation of the average rate of income-tax.

Any person responsible for paying any income chargeable under the head “Salaries

Individual (Employee)

Average rate of income-tax computed on the basis of the rates in force.

At the time of payment

192A Premature withdrawal from Employee Provident Fund

Payment or aggregate payment ≥ R 50,000

Trustees of the EPF Scheme or any authorised person under the Scheme

Individual (Employee)

10% [In case of failure to furnish PAN, TDS@ Maximum Marginal Rate]

At the time of payment

193 Interest on Securities

> R 10,000 in a F.Y., in case of interest on 8% Savings (Taxable) Bonds, 2003/7.75% Savings (Taxable) Bonds, 2018. > R 5,000 in a F.Y., in case of interest on debentures issued by a Co. in which the public are substantially interested, paid or credited to a resident individual or HUF by an A/c payee cheque. No threshold specified in any other case.

Any person responsible for paying any income by way of interest on securities

Any resident 10% At the time of credit of such income to the account of the payee or at the time of payment, whichever is earlier.

194A Interest other than interest on securities

> R 40,000 in a F.Y., in case of interest credited or paid by –(i) a banking company;(ii) a co-operative society

engaged in banking business; and

(iii) a post office on any deposit under a notified Scheme.

In all the above cases, if payee is a resident senior citizen, tax deduction limit is > R 50,000.> R 5,000 in a F.Y., in other cases.

Any person (other than an individual or HUF whose total sales, gross receipts or turnover from business or profession do not exceed the monetary limits specified u/s 44AB in the immediately preceding F.Y.) responsible for paying interest other than interest on securities.

Any Resident 10% At the time of credit of such income to the account of the payee or at the time of payment, whichever is earlier.

194B Winnings from any lottery, crossword puzzle or card game or other game of any sort

> R 10,000 �e person responsible for paying income by way of such winnings

Any Person 30% At the time of payment

194BB Winnings from horse race

> R10,000 Book Maker or a person holding licence for horse racing or for arranging for wagering or betting in any race course.

Any Person 30% At the time of payment

1

INCOME TAX LAW

The Chartered Accountant Student April 2020 09

I. TAX DEDUCTION AT SOURCESection Nature of

payment�reshold Limit for deduction of tax at

source

Payer Payee Rate of TDS Time of deduction

194C Payments to Contractors

Single sum credited or paid > R 30,000 (or)�e aggregate of sums credited or paid to a contractor during the F.Y. > R 1,00,000Individual/HUF need not deduct tax where sum is credited or paid exclusively for personal purposes

Central/State Govt., Local authority, Central/State/Provincial Corpn., company, firm, trust, registered society, co-operative society, university established under Central/State/Provincial Act, declared university under the UGC Act, Govt. of Foreign State or a foreign enterprise, any association or body established outside India, individual/HUF liable to tax audit u/s 44AB(a)/(b) in the immediately preceding F.Y.

Any Resident contractor for carrying out any work (including supply of labour)

1% of sum paid or credited, if the payee is an Individual or HUF2% of sum paid or credited, if the payee is any other person.

At the time of credit of such sum to the account of the contractor or at the time of payment, whichever is earlier.

194D Insurance Commission

> R 15,000 in a F.Y. Any person responsible for paying any income by way of remuneration or reward for soliciting or procuring insurance business

Any Resident 5% At the time of credit of such income to the account of the payee or at the time of payment, whichever is earlier.

194DA Any sum under a Life Insurance Policy

≥ R 1,00,000 (aggregate amount of payment to a payee in a F.Y.)

Any person responsible for paying any sum under a LIP, including the sum allocated by way of bonus

Any resident 1%[5% of the amount of income comprised w.e.f. 1.9.2019]

At the time of payment

194E Payment to non-resident sportsmen or sports associations of income referred to in section 115BBA

No threshold limit Any person responsible for making the payment

Non-resident sportsman (including an athelete) or entertainer who is not a citizen of India or non-resident sports association or institution

20% At the time of credit of such income to the account of the payee or at the time of payment, whichever is earlier.

194EE Payment of deposit under NSS

≥ R 2,500 in a F.Y. Any person responsible for paying Individual or HUF

10% At the time of payment

194G Commission on sale of lottery tickets

> R 15,000 in a F.Y. Any person responsible for paying any income by way of commission, remuneration or prize (by whatever name called) on lottery tickets

Any person stocking, distributing, purchasing or selling lottery tickets

5% At the time of credit of such income to the account of the payee or at the time of payment, whichever is earlier.

194H Commission or brokerage

> R 15,000 in a F.Y. Any person (other than an Individual or HUF whose total sales, gross receipts or turnover from business or profession do not exceed the monetary limits specified u/s 44AB in the immediately preceding F.Y.) responsible for paying commission or brokerage.

Any resident 5% At the time of credit of such income to the account of the payee or at the time of payment, whichever is earlier.

194-I Rent > R 2,40,000 in a F.Y. Any person (other than an individual or HUF whose total sales, gross receipts or turnover from business or profession do not exceed the monetary limits specified u/s 44AB in the immediately preceding F.Y.) responsible for paying rent.

Any resident For P & M or equipment- 2%

For land or building, land appurtenant to a building, furniture or fittings -10%

At the time of credit of such income to the account of the payee or at the time of payment, whichever is earlier.

194-IA Payment on transfer of certain immovable property other than agricultural land

≥ R 50 lakh (Consideration for transfer)

Any person, being a transferee (other than a person referred to in section 194LA responsible for paying compensation for compulsory acquisition of immovable property)

Resident transferor

1% At the time of credit of such sum to the account of the transferor or at the time of payment, whichever is earlier.

2

10 April 2020 The Chartered Accountant Student

INCOME TAX LAW I. TAX DEDUCTION AT SOURCE

Section Nature of payment

�reshold Limit for deduction of tax at

source

Payer Payee Rate of TDS Time of deduction

194-IB Payment of rent by certain individuals or HUF

> R 50, 000 for a month or part of a month

Individual/ HUF (other than Individual/HUF whose total sales, gross receipts or turnover from business or profession exceed the limits specified u/s 44AB in the immediately preceding F.Y.) responsible for paying rent.

Any Resident 5% At the time of credit of rent, for the last month of the P.Y. or the last month of tenancy, if the property is vacated during the year, as the case may be, to the account of the payee or at the time of payment, whichever is earlier

194-IC Payment under specified agreement referred to in section 45(5A)

No threshold limit Any person responsible for paying any sum by way of consideration, not being consideration in kind, under a registered agreement, wherein L or B or both are handed over by the owner for development of real estate project, for a consideration, being a share in L or B or both in such project, with payment of part consideration in cash.

Any Resident 10% At the time of credit of such income to the account of the payee or at the time of payment, whichever is earlier.

194J Fees for professional or technical services/ Royalty/ Non-compete fees/ Director’s remuneration

> R 30,000 in a F.Y., for each category of income. (However, this limit does not apply in case of payment of director's remuneration).

Any person, other than an individual or HUF;However, in case of fees for professional or technical services paid or credited, individual/HUF, whose total sales, gross receipts or turnover from business or profession exceed the monetary limits specified u/s 44AB in the immediately preceding F.Y., is liable to deduct tax u/s 194J, except where fees for professional services is credited or paid exclusively for his personal purposes.

Any Resident 2% - Payee engaged only in the business of operation of call centre10% - Others

At the time of credit of such sum to the account of the payee or at the time of payment, whichever is earlier.

194LA Compensation on acquisition of certain immovable property other than agricultural land

> R 2,50,000 in a F.Y. Any person responsible for paying any sum in the nature of compensation or enhanced compensation on compulsory acquisition of immovable property

Any Resident 10% At the time of payment

194M(w.e.f.

1st Sep, 2019)

Payments to contractors (or)Commission / brokerage (or) Fees for professional services

> R 50,00,000 in a F.Y. Individual or HUF other than those who are required to deduct tax at source u/s 194C or 194H or 194J

Any Resident 5% At the time of credit of such sum to the account of the payee or at the time of payment, whichever is earlier.

194N (w.e.f.

1st Sep, 2019)

Cash withdrawals > R 1 crore - a banking company or any bank or banking institution

- a co-operative society engaged in carrying on the business of banking or

- a post office

Any person @2% of sum exceeding R 1 crore

At the time of payment of such sum

Notes –(1) Section 206AA requires furnishing of PAN by the deductee to the deductor, failing which the deductor has to deduct tax at the

higher of the following rates, namely, -(i) at the rate specified in the relevant provision of the Income-tax Act, 1961; or(ii) at the rate or rates in force; or(iii) at the rate of 20%.

(2) �e threshold limit given in column (3) of the table is with respect to each payee

3

INCOME TAX LAW

The Chartered Accountant Student April 2020 11

II. ADVANCE PAYMENT OF TAXLiability for payment of advance tax [Sections 207 & 208]• TaxshallbepayableinadvanceduringanyF.Y.inrespectofthetotalincome(TI)oftheassesseewhichwouldbechargeableto

tax for the A.Y. immediately following that F.Y. • Advance tax is payable during a F.Y. in every case where the amount of such tax payable by the assessee during the year is

R 10,000 or more.• However,anindividual resident in India of the age of 60 years or more at any time during the P.Y., who does not have any

income chargeable under the head “Profits and gains of business or profession” (PGBP), is not liable to pay advance tax.Instalments of advance tax and due dates [Section 211]Advance tax payment schedule for corporates and non-corporates (other than an assessee computing profits on presumptive basis u/s 44AD or section 44ADA) – Four instalments

Due date of instalment Amount payableOn or before 15th June Not less than 15% of advance tax liability.On or before 15th September Not less than 45% of advance tax liability (-) amount paid in earlier instalment.On or before 15th December Not less than 75% of advance tax liability (-) amount paid in earlier instalment or instalments.On or before 15th March �e whole amount of advance tax liability (-) amount paid in earlier instalment or instalments.Advance tax payment by assessees computing profits on presumptive basis u/s 44AD(1) or section 44ADA(1)An eligible assessee, opting for computation of profits or gains of business or profession on presumptive basis in respect of eligible business referred to in section 44AD(1) or in respect of eligible profession referred to in section 44ADA(1), shall be required to pay advance tax of the whole amount on or before 15th March of the F.Y.However, any amount paid by way of advance tax on or before 31st March shall also be treated as advance tax paid during the F.Y. ending on that day.Interest for defaults in payment of advance tax [Section 234B](1) Interest u/s 234B is attracted for non-payment of advance tax or payment of advance tax of an amount less than 90% of

assessed tax. (2) �e interest liability would be 1% per month or part of the month from 1st April following the F.Y. upto the date of

determination of total income u/s 143(1) and where regular assessment is made, upto the date of such regular assessment. (3) Such interest is calculated on the amount of difference between the assessed tax and the advance tax paid. (4) “Assessed tax” means the tax on total income determined u/s 143(1)/under regular assessment, as the case may be, less TDS

& TCS, any relief of tax allowed u/s 89, any tax credit allowed to be set off in accordance with the provisions of section 115JD.

(5) Where self-assessment tax is paid by the assessee u/s 140A or otherwise, interest shall be calculated upto the date of payment of such tax and reduced by the interest, if any, paid u/s 140A towards the interest chargeable under this section.

Interest for deferment of advance tax [Section 234C](a) Manner of computation of interest u/s 234C for deferment of advance tax by corporate and non-corporate assessees:

In case an assessee, other than an assessee who declares profits and gains in accordance with the provisions of section 44AD(1) or section 44ADA(1), who is liable to pay advance tax u/s 208 has failed to pay such tax or the advance tax paid by such assessee on its current income on or before the dates specified in column (1) below is less than the specified percentage [given in column (2) below] of tax due on returned income, then simple interest@1% per month for the period specified in column (4) on the amount of shortfall, as per column (3) is leviable u/s 234C.

Specified date(1)

Specified %(2)

Shortfall in advance tax(3)

Period(4)

15th June 15% 15% of tax due on returned income (-) advance tax paid up to 15th June 3 months

15th September 45% 45% of tax due on returned income (-) advance tax paid up to 15th September 3 months

15th December 75% 75% of tax due on returned income (-) advance tax paid up to 15th December 3 months

15th March 100% 100% of tax due on returned income (-) advance tax paid up to 15th March 1 month

Note – However, if the advance tax paid by the assessee on the current income, on or before 15th June or 15th September, is not less than 12% or, as the case may be, 36% of the tax due on the returned income, then, the assessee shall not be liable to pay any interest on the amount of the shortfall on those dates.

(b) Computation of interest u/s 234C in case of an assessee who declares profits and gains in accordance with the provisions of section 44AD(1) or section 44ADA(1):In case an assessee who declares profits and gains in accordance with the provisions of section 44AD(1) or section 44ADA(1), who is liable to pay advance tax u/s 208 has failed to pay such tax or the advance tax paid by the assessee on its current income on or before 15th March is less than the tax due on the returned income, then, the assessee shall be liable to pay simple interest at the rate of 1% on the amount of the shortfall from the tax due on the returned income.

4

12 April 2020 The Chartered Accountant Student

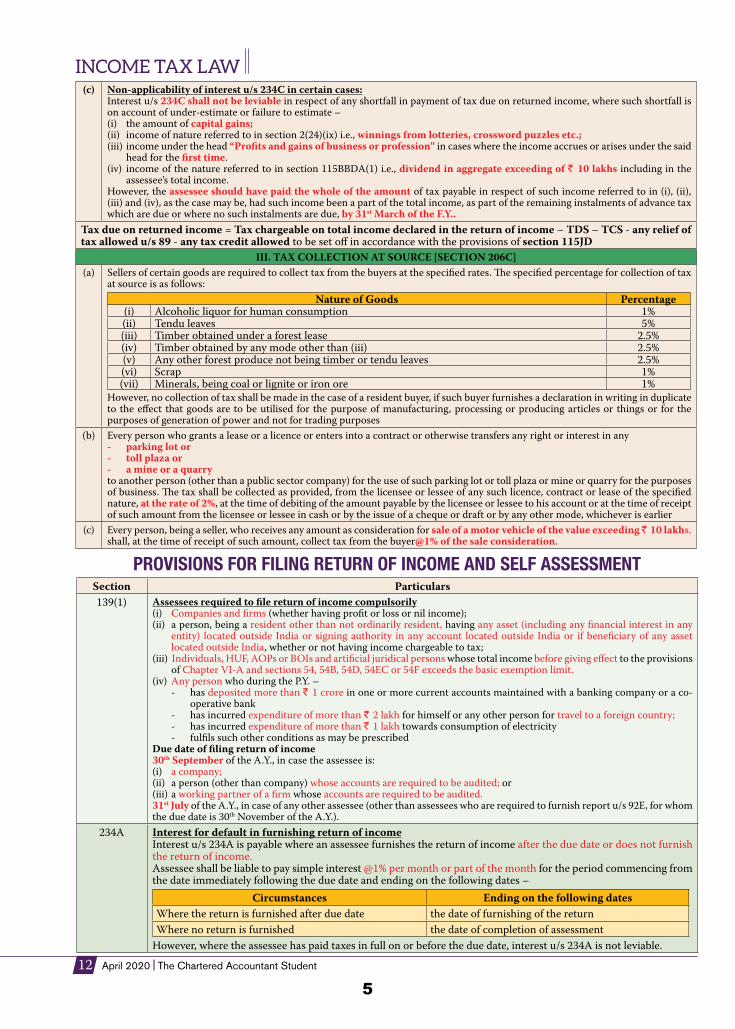

INCOME TAX LAW (c) Non-applicability of interest u/s 234C in certain cases:

Interest u/s 234C shall not be leviable in respect of any shortfall in payment of tax due on returned income, where such shortfall is on account of under-estimate or failure to estimate –(i) the amount of capital gains;(ii) income of nature referred to in section 2(24)(ix) i.e., winnings from lotteries, crossword puzzles etc.; (iii) income under the head “Profits and gains of business or profession” in cases where the income accrues or arises under the said

head for the first time.(iv) income of the nature referred to in section 115BBDA(1) i.e., dividend in aggregate exceeding of R 10 lakhs including in the

assessee’s total income.However, the assessee should have paid the whole of the amount of tax payable in respect of such income referred to in (i), (ii), (iii) and (iv), as the case may be, had such income been a part of the total income, as part of the remaining instalments of advance tax which are due or where no such instalments are due, by 31st March of the F.Y..

Tax due on returned income = Tax chargeable on total income declared in the return of income – TDS – TCS - any relief of tax allowed u/s 89 - any tax credit allowed to be set off in accordance with the provisions of section 115JD

III. TAX COLLECTION AT SOURCE [SECTION 206C](a) Sellers of certain goods are required to collect tax from the buyers at the specified rates. �e specified percentage for collection of tax

at source is as follows:Nature of Goods Percentage

(i) Alcoholic liquor for human consumption 1%(ii) Tendu leaves 5%(iii) Timber obtained under a forest lease 2.5%(iv) Timber obtained by any mode other than (iii) 2.5%(v) Any other forest produce not being timber or tendu leaves 2.5%(vi) Scrap 1%(vii) Minerals, being coal or lignite or iron ore 1%

However, no collection of tax shall be made in the case of a resident buyer, if such buyer furnishes a declaration in writing in duplicate to the effect that goods are to be utilised for the purpose of manufacturing, processing or producing articles or things or for the purposes of generation of power and not for trading purposes

(b) Every person who grants a lease or a licence or enters into a contract or otherwise transfers any right or interest in any - parking lot or - toll plaza or - a mine or a quarry to another person (other than a public sector company) for the use of such parking lot or toll plaza or mine or quarry for the purposes of business. �e tax shall be collected as provided, from the licensee or lessee of any such licence, contract or lease of the specified nature, at the rate of 2%, at the time of debiting of the amount payable by the licensee or lessee to his account or at the time of receipt of such amount from the licensee or lessee in cash or by the issue of a cheque or draft or by any other mode, whichever is earlier

(c) Every person, being a seller, who receives any amount as consideration for sale of a motor vehicle of the value exceeding R 10 lakhs, shall, at the time of receipt of such amount, collect tax from the buyer@1% of the sale consideration.

PROVISIONS FOR FILING RETURN OF INCOME AND SELF ASSESSMENTSection Particulars139(1) Assessees required to file return of income compulsorily

(i) Companies and firms (whether having profit or loss or nil income);(ii) a person, being a resident other than not ordinarily resident, having any asset (including any financial interest in any

entity) located outside India or signing authority in any account located outside India or if beneficiary of any asset located outside India, whether or not having income chargeable to tax;

(iii) Individuals, HUF, AOPs or BOIs and artificial juridical persons whose total income before giving effect to the provisions of Chapter VI-A and sections 54, 54B, 54D, 54EC or 54F exceeds the basic exemption limit.

(iv) Any person who during the P.Y. –- has deposited more than R 1 crore in one or more current accounts maintained with a banking company or a co-

operative bank- has incurred expenditure of more than R 2 lakh for himself or any other person for travel to a foreign country;- has incurred expenditure of more than R 1 lakh towards consumption of electricity- fulfils such other conditions as may be prescribed

Due date of filing return of income30th September of the A.Y., in case the assessee is:(i) a company; (ii) a person (other than company) whose accounts are required to be audited; or(iii) a working partner of a firm whose accounts are required to be audited.31st July of the A.Y., in case of any other assessee (other than assessees who are required to furnish report u/s 92E, for whom the due date is 30th November of the A.Y.).

234A Interest for default in furnishing return of incomeInterest u/s 234A is payable where an assessee furnishes the return of income after the due date or does not furnish the return of income.Assessee shall be liable to pay simple interest @1% per month or part of the month for the period commencing from the date immediately following the due date and ending on the following dates –

Circumstances Ending on the following datesWhere the return is furnished after due date the date of furnishing of the returnWhere no return is furnished the date of completion of assessment

However, where the assessee has paid taxes in full on or before the due date, interest u/s 234A is not leviable.

5

INCOME TAX LAW

The Chartered Accountant Student April 2020 13

234F Fee for default in furnishing return of incomeWhere a person who is required to furnish a return of income u/s 139, fails to do so within the prescribed time limit u/s 139(1), he shall pay, by way of fee, a sum of –(i) R 5,000, if the return is furnished on or before the 31st December of the A.Y.;(ii) R 10,000 in any other caseHowever, if the total income of the person does not exceed R 5 lakhs, the fees payable shall not exceed R 1,000

139(3) Return of lossAn assessee can carry forward or set off his/its losses provided he/it has filed his/its return u/s 139(3), within the due date specified u/s 139(1). ExceptionsLoss from house property and unabsorbed depreciation can be carried forward for set-off even though return has not been filed before the due date.

139(4) Belated ReturnA return of income for any P.Y., which has not been furnished within the time allowed u/s 139(1), may be furnished at any time before the:(i) end of the relevant A.Y.; or(ii) completion of the assessment,whichever is earlier.

139(5) Revised ReturnIf any omission or any wrong statement is discovered in a return furnished u/s 139(1) or belated return u/s 139(4), a revised return may be furnished by the assessee at any time before the:(i) end of the relevant A.Y.; or(ii) completion of assessment,whichever is earlier.�us, belated return can also be revised.

139A Permanent Account Number (PAN)As per section 139A(1), the following persons mentioned in column (2), who have not been allotted a permanent account number (PAN), to apply to the Assessing Officer within the time specified in column (3) for the allotment of a PAN –

Persons required to apply for PAN Time limit for making such application(1) (2) (3)(i) Every person, if his total income or the total income of any other

person in respect of which he is assessable under the Act during any P.Y. exceeds the maximum amount which is not chargeable to income-tax

On or before 31st May of the A.Y. for which such income is assessable

(ii) Every person carrying on any business or profession whose total sales, turnover or gross receipts are or is likely to exceed R 5 lakhs in any P.Y.

Before the end of that F.Y. (P.Y.).

(iii) Every person being a resident, other than an individual, which enters into a financial transaction of an amount aggregating to R 2,50,000 or more in a F.Y.

On or before 31st May of the immediately following F.Y.

(iv) Every person who is a managing director, director, partner, trustee, author, founder, karta, chief executive officer, principal officer or office bearer of any person referred in (iii) above or any person competent to act on behalf of such person referred in (iii) above

On or before 31st May of the immediately following F.Y. in which the person referred in (iii) enters into financial transaction specified therein.

Quoting of PAN is mandatory in all the following documents:(a) in all returns to, or correspondence with, any income-tax authority;(b) in all challans for the payment of any sum due under the Act;(c) in all documents pertaining to such transactions entered into by him, as may be prescribed by the CBDT in the

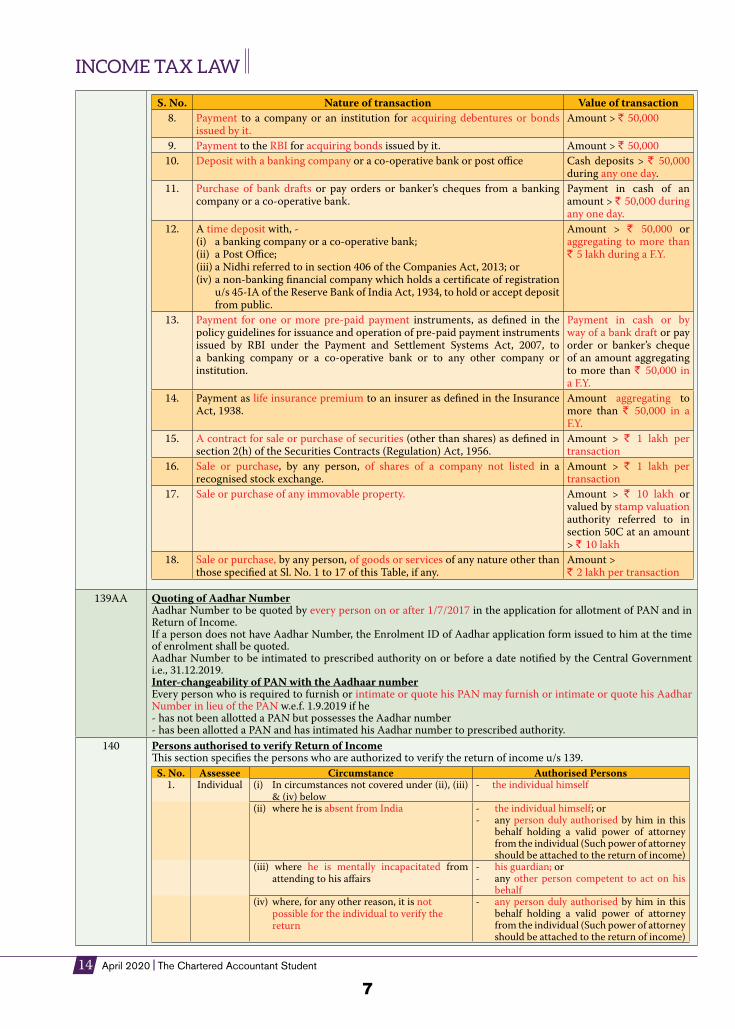

interests of revenue. In this connection, CBDT has notified the following transactions, namely:

S. No. Nature of transaction Value of transaction1. Sale or purchase of a motor vehicle or vehicle, other than two wheeled vehicles. All such transactions2. Opening an account [other than a time-deposit referred to at Sl. No.12 and

a Basic Savings Bank Deposit Account] with a banking company or a co-operative bank

All such transactions

3. Making an application to any banking company or a co-operative bank or to any other company or institution, for issue of a credit or debit card.

All such transactions

4. Opening of a demat account with a depository, participant, custodian of securities or any other person registered under SEBI Act, 1992.

All such transactions

5. Payment to a hotel or restaurant against a bill or bills at any one time. Payment in cash of an amount > R 50,000.

6. Payment in connection with travel to any foreign country or payment for purchase of any foreign currency at any one time.

Payment in cash of an amount > R 50,000

7. Payment to a Mutual Fund for purchase of its units Amount > R 50,000

6

14 April 2020 The Chartered Accountant Student

INCOME TAX LAW

S. No. Nature of transaction Value of transaction8. Payment to a company or an institution for acquiring debentures or bonds

issued by it. Amount > R 50,000

9. Payment to the RBI for acquiring bonds issued by it. Amount > R 50,00010. Deposit with a banking company or a co-operative bank or post office Cash deposits > R 50,000

during any one day.11. Purchase of bank drafts or pay orders or banker’s cheques from a banking

company or a co-operative bank.Payment in cash of an amount > R 50,000 during any one day.

12. A time deposit with, - (i) a banking company or a co-operative bank;(ii) a Post Office; (iii) a Nidhi referred to in section 406 of the Companies Act, 2013; or (iv) a non-banking financial company which holds a certificate of registration

u/s 45-IA of the Reserve Bank of India Act, 1934, to hold or accept deposit from public.

Amount > R 50,000 or aggregating to more than R 5 lakh during a F.Y.

13. Payment for one or more pre-paid payment instruments, as defined in the policy guidelines for issuance and operation of pre-paid payment instruments issued by RBI under the Payment and Settlement Systems Act, 2007, to a banking company or a co-operative bank or to any other company or institution.

Payment in cash or by way of a bank draft or pay order or banker’s cheque of an amount aggregating to more than R 50,000 in a F.Y.

14. Payment as life insurance premium to an insurer as defined in the Insurance Act, 1938.

Amount aggregating to more than R 50,000 in a F.Y.

15. A contract for sale or purchase of securities (other than shares) as defined in section 2(h) of the Securities Contracts (Regulation) Act, 1956.

Amount > R 1 lakh per transaction

16. Sale or purchase, by any person, of shares of a company not listed in a recognised stock exchange.

Amount > R 1 lakh per transaction

17. Sale or purchase of any immovable property. Amount > R 10 lakh or valued by stamp valuation authority referred to in section 50C at an amount > R 10 lakh

18. Sale or purchase, by any person, of goods or services of any nature other than those specified at Sl. No. 1 to 17 of this Table, if any.

Amount >R 2 lakh per transaction

139AA Quoting of Aadhar NumberAadhar Number to be quoted by every person on or after 1/7/2017 in the application for allotment of PAN and in Return of Income.If a person does not have Aadhar Number, the Enrolment ID of Aadhar application form issued to him at the time of enrolment shall be quoted.Aadhar Number to be intimated to prescribed authority on or before a date notified by the Central Government i.e., 31.12.2019.Inter-changeability of PAN with the Aadhaar numberEvery person who is required to furnish or intimate or quote his PAN may furnish or intimate or quote his Aadhar Number in lieu of the PAN w.e.f. 1.9.2019 if he - has not been allotted a PAN but possesses the Aadhar number- has been allotted a PAN and has intimated his Aadhar number to prescribed authority.

140 Persons authorised to verify Return of Income �is section specifies the persons who are authorized to verify the return of income u/s 139.

S. No. Assessee Circumstance Authorised Persons1. Individual (i) In circumstances not covered under (ii), (iii)

& (iv) below- the individual himself

(ii) where he is absent from India - the individual himself; or- any person duly authorised by him in this

behalf holding a valid power of attorney from the individual (Such power of attorney should be attached to the return of income)

(iii) where he is mentally incapacitated from attending to his affairs

- his guardian; or - any other person competent to act on his

behalf(iv) where, for any other reason, it is not

possible for the individual to verify the return

- any person duly authorised by him in this behalf holding a valid power of attorney from the individual (Such power of attorney should be attached to the return of income)

7

INCOME TAX LAW

The Chartered Accountant Student April 2020 15

140 S. No. Assessee Circumstance Authorised Persons2. Hindu

Undivided Family

(i) in circumstances not covered under (ii) and (iii) below

- the karta

(ii) where the karta is absent from India - any other adult member of the HUF(iii) where the karta is mentally incapacitated

from attending to his affairs- any other adult member of the HUF

3. Company (i) in circumstances not covered under (ii) to (vi) below

- the managing director of the company

(ii) (a) where for any unavoidable reason such managing director is not able to verify the return; or

(b) where there is no managing director

- any director of the company

- any director of the company(iii) where the company is not resident in India - a person who holds a valid power of

attorney from such company to do so (such power of attorney should be attached to the return).

(iv) (a) Where the company is being wound up (whether under the orders of a court or otherwise); or

(b) where any person has been appointed as the receiver of any assets of the company

- Liquidator

- Liquidator

(v) Where the management of the company has been taken over by the Central Government or any State Government under any law

- the principal officer of the company

(vi) Where an application for corporate insolvency resolution process has been admitted by the Adjudicating Authority under the Insolvency and Bankruptcy Code, 2016.

- insolvency professional appointed by such Adjudicating Authority

4. Firm (i) in circumstances not covered under (ii) below

- the managing partner of the firm

(ii) (a) where for any unavoidable reason such managing partner is not able to verify the return; or

(b) where there is no managing partner.

- any partner of the firm, not being a minor

- any partner of the firm, not being a minor5 LLP (i) in circumstances not covered under (ii)

below- Designated partner

(ii) (a) where for any unavoidable reason such designated partner is not able to verify the return; or

(b) where there is no designated partner.

- any partner of the LLP

- any partner of the LLP6. Local

authority- - the principal officer

7. Political party

- - the chief executive officer of such party (whether he is known as secretary or by any other designation)

8. Any other association

- - any member of the association or the principal officer of such association

9. Any other person

- - that person or some other person competent to act on his behalf.

140A Self-AssessmentWhere any tax is payable on the basis of any return required to be furnished u/s 139, after taking into account –(i) the amount of tax, already paid, (ii) the tax deducted or collected at source (TDS/TCS)(iii) any relief of tax claimed u/s 89(iv) any tax credit claimed to be set-off in accordance with the provisions of section 115JD (i.e., alternate minimum

tax).the assessee shall be liable to pay such tax together with interest and fee payable under any provision of this Act for any delay in furnishing the return or any default or delay in payment of advance tax before furnishing the return.

Where the amount paid by the assessee falls short of the aggregate of the tax, interest and fee as aforesaid, the amount so paid shall first be adjusted towards the fee payable and thereafter, towards interest and the balance shall be adjusted towards the tax payable.

8

INDIRECT TAXES

The Chartered Accountant Student February 2020 07

GOODS AND SERVICES TAX: A CAPSULE FOR QUICK RECAP

REGISTRATIONNature of registration

Persons liable to registration

Compulsory registration in certain cases

Persons not liable for registration

Applicable threshold limit

The subject-wise capsules published in the Students’ Journal every month are one among the many initiatives of Board of Studies which aim at providing quality academic inputs to students of Chartered Accountancy Course. The Capsule is an educational aid that assist students in quick revision of select topics of a subject. This Capsule covers the topics “Registration” and “Tax invoice, credit and debit notes” of Paper 4B Indirect Taxes of Intermediate Course (Old as well as New). The Capsule is based on the GST law as amended by the significant notifications/circulars issued till 31st October, 2019 and is thus, relevant for students appearing in May, 2020 examination. This Capsule should not be taken as a substitute for the detailed study of these topics. Students are advised to refer to the August, 2019 Edition of Study Material along with Statutory Update for May 2020 examination for comprehensive study and revision.

�e registration in GST is PAN based and State specific.

One registration per State/UT.

However, a business entity having separate places of business in a State may obtain separate registration

for each of its places of business .

GST identification number called “GSTIN” - a 15-digit number and a certificate of registration

incorporating therein this GSTIN is made available to the applicant on the GSTN common portal.

Registration under GST is not tax specific, i.e. single registration for all the taxes i.e. CGST, SGST/UTGST,

IGST and cesses.

�ose who exceed threshold limit

States with threshold limit of R 10 lakh for both goods and services

States with threshold limit of R 20 lakh for both goods and services

States with threshold limit of R 20 lakh for services and R 40 lakh for goods (exclusive)

Inter-State supplier

Person engaged exclusively in supplying goods/services/both not liable to tax/wholly exempt from tax

Non-resident taxable persons

Persons making inter-State supplies of

taxable services up to R 20 lakh

Casual taxable person

Agriculturist limited to supply of produce out of cultivation of

land

A person who supplies on behalf

of some other taxable person (i.e. an Agent of some

Principal)

Persons making inter-State

taxable supplies of notified

handicraft goods up to R 20 lakh

Person receiving supplies on which

tax is payable by recipient on reverse charge

basis

Persons making only reverse

charge supplies

Person/class of persons notified by the Central/State

Government

Casual Taxable Persons making

inter-State taxable supplies

of notified handicraft goods up to R 20 lakh

Taxable Supplies

Exempt supplies

Inter State supplies

Aggregate TurnoverExports

In case of transfer of business on account of succession, etc.

In case of amalgamation/ demerger by an order of High Court etc.

Aggregate Turnover will be computed on All-India basis for same PAN

+ + + =

• Thresholdlimitelaboratedseparately in the diagram below.

• Manipur,Mizoram,Nagalandand Tripura

• ArunachalPradesh,Meghalaya,Sikkim, Uttarakhand, Puducherry and Telangana

• JammuandKashmir,Assam,Himachal Pradesh, All other States

• transferee liable to be registered from the date of succession of business

• transferee liable to be registered from the date on which Registrar of Companies issues incorporation certificate giving effect to order of High Court etc.

9

08 February 2020 The Chartered Accountant Student

INDIRECT TAXES

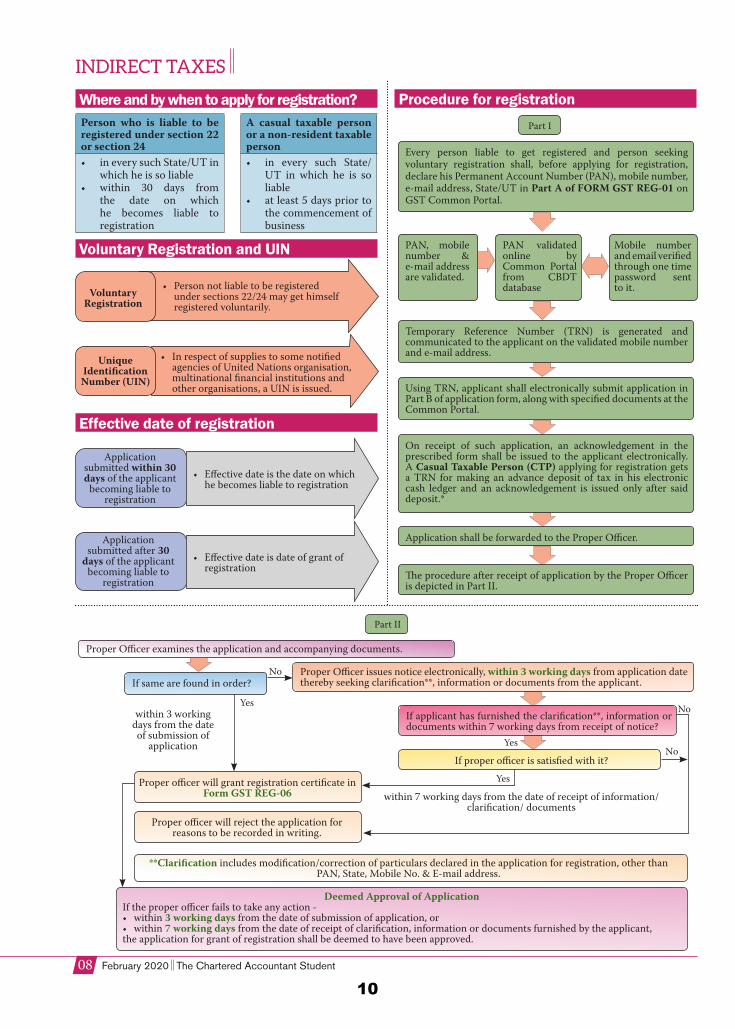

Voluntary Registration and UIN

Effective date of registration

Procedure for registration

Voluntary Registration

Application submitted within 30 days of the applicant

becoming liable to registration

Application submitted after 30

days of the applicant becoming liable to

registration

Part I

Part II

Every person liable to get registered and person seeking voluntary registration shall, before applying for registration, declare his Permanent Account Number (PAN), mobile number, e-mail address, State/UT in Part A of FORM GST REG-01 on GST Common Portal.

Temporary Reference Number (TRN) is generated and communicated to the applicant on the validated mobile number and e-mail address.

Using TRN, applicant shall electronically submit application in Part B of application form, along with specified documents at the Common Portal.

Application shall be forwarded to the Proper Officer.

�e procedure after receipt of application by the Proper Officer is depicted in Part II.

Proper Officer examines the application and accompanying documents.

Proper officer will grant registration certificate in Form GST REG-06

Proper officer will reject the application for reasons to be recorded in writing.

**Clarification includes modification/correction of particulars declared in the application for registration, other than PAN, State, Mobile No. & E-mail address.

Deemed Approval of ApplicationIf the proper officer fails to take any action -• within3 working days from the date of submission of application, or• within7 working days from the date of receipt of clarification, information or documents furnished by the applicant,the application for grant of registration shall be deemed to have been approved.

Proper Officer issues notice electronically, within 3 working days from application date thereby seeking clarification**, information or documents from the applicant.

If applicant has furnished the clarification**, information or documents within 7 working days from receipt of notice?

If proper officer is satisfied with it?

within 7 working days from the date of receipt of information/ clarification/ documents

within 3 working days from the date of submission of

application

Yes

Yes

Yes

No

No

No

On receipt of such application, an acknowledgement in the prescribed form shall be issued to the applicant electronically. A Casual Taxable Person (CTP) applying for registration gets a TRN for making an advance deposit of tax in his electronic cash ledger and an acknowledgement is issued only after said deposit.*

PAN, mobile number & e-mail address are validated.

PAN validated online by Common Portal from CBDT database

Mobile number and email verified through one time password sent to it.

Unique Identification Number (UIN)

• Personnotliabletoberegisteredunder sections 22/24 may get himself registered voluntarily.

• Effectivedateisthedateonwhichhe becomes liable to registration

• Effectivedateisdateofgrantofregistration

• Inrespectofsuppliestosomenotifiedagencies of United Nations organisation, multinational financial institutions and other organisations, a UIN is issued.

If same are found in order?

Person who is liable to be registered under section 22 or section 24 • ineverysuchState/UTin

which he is so liable• within 30 days from

the date on which he becomes liable to registration

A casual taxable person or a non-resident taxable person• in every such State/

UT in which he is so liable

• atleast5dayspriortothe commencement of business

Where and by when to apply for registration?

10

INDIRECT TAXES

The Chartered Accountant Student February 2020 09

Special procedure for registration of CTP and NRTP

Amendment of Registration

Cancellation of registration

Suspension of registration

Revocation of cancellation

Casual Taxable Person Non-resident Taxable Person

A Casual taxable person is one who has a registered business in some State in India, but wants to effect supplies from some other State in which he is not having any fixed place of business.

Casual Taxable Person

GST law prescribes special procedure for registration, as also for extension of the operation period of such Casual or Non-

Resident taxable persons.

�ey have to apply for registration at least 5 days in advance before making any supply.

Registration is granted to them or period of operation is extended only after they make advance deposit of the

estimated tax liability.

Registration is granted to them for the period specified in the registration application or 90 days from the

effective date of registration.

Except for the changes in some core information in the registration application, a taxable person shall be able to make amendments without requiring any specific approval from the tax authority.

In case the change is core fields of information, the taxable person will apply for amendment within 15 days of the event necessitating the change. �e Proper Officer, then, will approve the amendment within the next 15 days. For changes in non-core fields, no approval of the Proper Officer is required, and the amendment can be affected by the taxable person on his own on the common portal.

--Business discontinued/ Transferred/

Amalgamated with other legal

entity/ Demerged or Otherwise disposed of

Change in the constitution of

the business

A registered person has not filed returns

for continuous 6 months (3 months for composition supplier)

Taxable person no longer liable to

be registered

Once a registered person has applied for cancellation of registration or the proper officer seeks to cancel his registration, proper officer may suspend his registration during pendency of proceedings relating to cancellation of registration filed by such registered person.

Registered person seeking cancellation shall apply for the same within 30 days of occurrence of the event warranting cancellation, in prescribed form, furnishing the details of inputs held in stock or inputs contained in semi-finished/finished goods held in stock and of capital goods held in stock on the date from which cancellation of registration is sought, liability thereon, payment, if any made & relevant documents.

Proper officer (PO) shall issue the order of cancellation within 30 days of submission of application for the same.

PO shall issue a SCN to the registered person who has to reply to said notice within 7 days.

Proceedings shall be dropped

C a n ce l l a t i o n order shall be issued within 30 days of reply to SCN where r e g i s t r a t i o n is liable to be cancelled

Where instead of replying to SCN, person furnishes all pending returns & makes full payment of tax along with interest & late fee.

In case where registration is cancelled suo-motu by the proper officer, the taxable person can apply within 30 days of service of cancellation order, requesting the officer for revoking the cancellation ordered by him. However, before so applying, the person has to make good the defaults (by filing all pending returns, making payment of all dues and so) for which the registration was cancelled by the officer.

However, if the officer concludes to reject the request for revocation of cancellation, he will first observe the principle of natural justice by way of issuing notice to the person and hearing him on the issue.

If satisfied, the proper officer will revoke the cancellation earlier ordered by him.

If reply to SCN is satisfactory

Where the registered person applies for cancellation Where the proper officer cancels the registration

Procedure for Cancellation

Voluntarily registered person has not

commenced the business within 6

months from the date of registration

Registration was obtained by means

of fraud, wilful misstatement or

suppression of facts

A registered person has contravened the

prescribed provisions

Registration can be

cancelled by the proper officer on his own

Registration can be

cancelled either by proper officer

or on an application

of the registered

person

Non-resident taxable person

A Non-Resident taxable person is one who is a foreigner and occasionally wants to effect taxable supplies from any State in India, and for that he needs GST registration.

Such person needs to register in the State from where he seeks to supply as a Casual taxable person.

11

10 February 2020 The Chartered Accountant Student

INDIRECT TAXES

Supplying exempted goods or services or both

Paying tax under composition levy

Paying tax at concessional rate under Notification No. 2/2019

CT(R)

TAX INVOICEImportant Contents of tax invoice Bill of Supply

Time limit for issuance of invoice

Who can raise a tax invoice?

Manner of issuing the invoice

Consolidated Tax Invoice

GSTIN of supplier

Consecutive Serial Number & date of issue

GSTIN of recipient, if registered

Name & address of recipient, if not registered

HSN

Description of goods or services

Quantity in case of goods

Total Value of supply

Taxable Value of supply

Tax rate – Central tax & State tax or Integrated tax, cess

Amount of tax charged

Place of supply

Address of delivery where different than place of supply

Tax payable on reverse charge basis

Signature of authorised signatory

Value of supply < R200

Tax Invoice

Bill of Supply

Tax

invo

ice

is n

ot

requ

ired

to b

e is

sued

Regi

ster

ed P

erso

n

Recipient is unregistered

Recipient does not require such invoice

Registered Person

Supplying taxable goods or services

Receiving taxable goods or services from unregistered supplier

Consolidated Tax Invoice shall be issued for such supplies at the close of each day in respect of all such supplies except supply of services by way of admission to exhibition of cinematograph films in multiplex screens

Supply of Goods Supply of services

Triplicate Duplicate

Original copy for recipient Duplicate copy for transporter; and Triplicate copy for supplier

Original copy for recipient; andDuplicate copy for supplier

�e serial number of invoices issued during a month / quarter shall be furnished electronically in FORM GSTR-1.

Taxable supply

Goods

Involving movement of

goods

At the time of removal

No movement of goods

At the time of delivery

Sale or return supplies

Within 30 days from the supply of services

Insurance, Banking - 45 days

Before or at the time of supply,

or within 6 months from the removal – whichever is

earlier

Services

In case of continuous supply of goods

before/at the time each successive statements of accounts is issued or each successive payment is received

• Whereduedateofpaymentisascertainablefrom the contract, invoice to be issued on/before due date of payment

• Whereduedateofpaymentisnotsoascertainable, invoice to be issued before/at the time of receipt of payment

• wherepaymentislinkedtothecompletionof an event, invoice to be issued on/before the date of completion of that event

In case of continuous supply of services

12

INDIRECT TAXES

The Chartered Accountant Student February 2020 11

Revised Tax Invoices to be issued in respect of taxable supplies effected during this period

Payment Voucher

Invoice

Consolidated Revised Tax Invoice (CTRI) may be issued in respect of taxable supplies made to an unregistered recipient

during this period

In case of inter-State supplies, CTRI cannot be issued in respect of all unregistered recipients if the value of a supply exceeds

R 2,50,000 during this period.

Particulars of the Debit and Credit Notes are also same as revised tax invoices

Where at the time of receipt of advance, rate of tax/ nature of supply is not determinable

Advance payment

Advance payment

Supply

Receipt Voucher

Receipt Voucher

Refund Voucher

Tax Invoice

Where Recipient is registered

Where Recipient is registered

under section 9(3)

Supplier is registered

Supplier is registered

Supplier is unregistered

Supplier is unregistered

Recipient will issue a Payment Voucher at the time of making payment to supplier.

Recipient shall issue Invoice

Where one or more tax invoices have issued for supply of any goods or services or both

Where one or more tax invoices have been issued for supply of any goods or services or both

Taxable value in invoice > Taxable value in

respect of such supply

where the goods supplied

are returned

by the recipient

OR OR

where goods or services or both

supplied are found to be

deficient

Tax charged in invoice > Tax payable in

respect of such supply

Taxable value in invoice < Taxable value in respect of such supply

Tax charged in invoice < Tax payable in respect of such supply

under section 9(3) under section 9(4)

Supplier is unregistered

Supplier is unregistered

under section 9(4)

Receives the supplies taxable on Reverse Charge basis

Receives the supplies taxable on Reverse

Charge basis

Revised Tax Invoice

Credit Notes

Debit Notes

Receipt Voucher

Refund Voucher

Invoice and Payment Vouchers to be issued by recipient of supply liable to pay tax under reverse charge

Where at the time of receipt of advance(i) rate of tax is not

determinabletax shall be paid at the rate of 18%

(ii) nature of supply is not determinable

same shall be treated as inter-State supply

Supplier

Supplier

Recipient

Recipient

Effective date of registration

Date of issuance of certificate of registration

Registered Supplier of

goods or services or both

Registered Supplier of

goods or services or both

Recipient of goods or services or

both

Recipient of goods or services or

both

may issue one or more credit notes for supplies made in a FY

may issue one or more debit notes for

supplies made in a FY

13