Embed Size (px)

Citation preview

Red Sky Energy

Focus on value creation

Rohan Gillespie, Managing Director

22nd August 2011g

Red Sky’s key assets

• Coal seam gas in Clarence Moreton Basin: h d fRight to earn 100%, earned 30% so far

Reserves independently certified (100% basis):Probable Reserves 2P 17PJPossible Reserves 3P 380PJContingent Resources 2C 629PJg

• Major shallow gas discovery in Clarence Moreton Basin: Attractive features:

Non conventional gas playNon conventional gas playShallow, hence low cost developmentLaterally extensiveThick – up to 500 metres

• Farm‐in to large block in Queensland: Targeting coal seam gas in Winton coals:

Right to earn 100%Expect 20 metres of gassy coalsSentry Petroleum drilling immediately to north

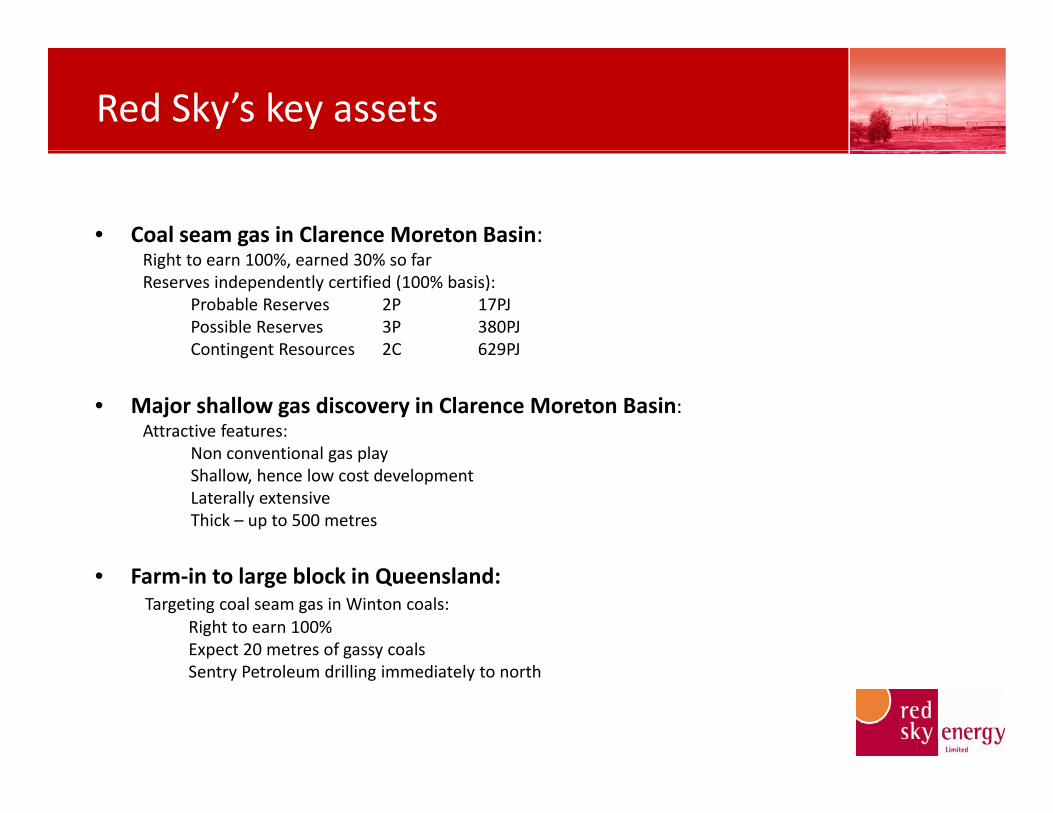

Comparison with peers

120

no reservesMarket

Capitalisation$m

80

100 .Metgasco

Icon Energy.i i l 3P

$

40

60 Exoma EnergyBlue Energy

Comet Ridge

Pl G

....minimal 3P

no reserves

Red Sky Energy20

Planet Gas..

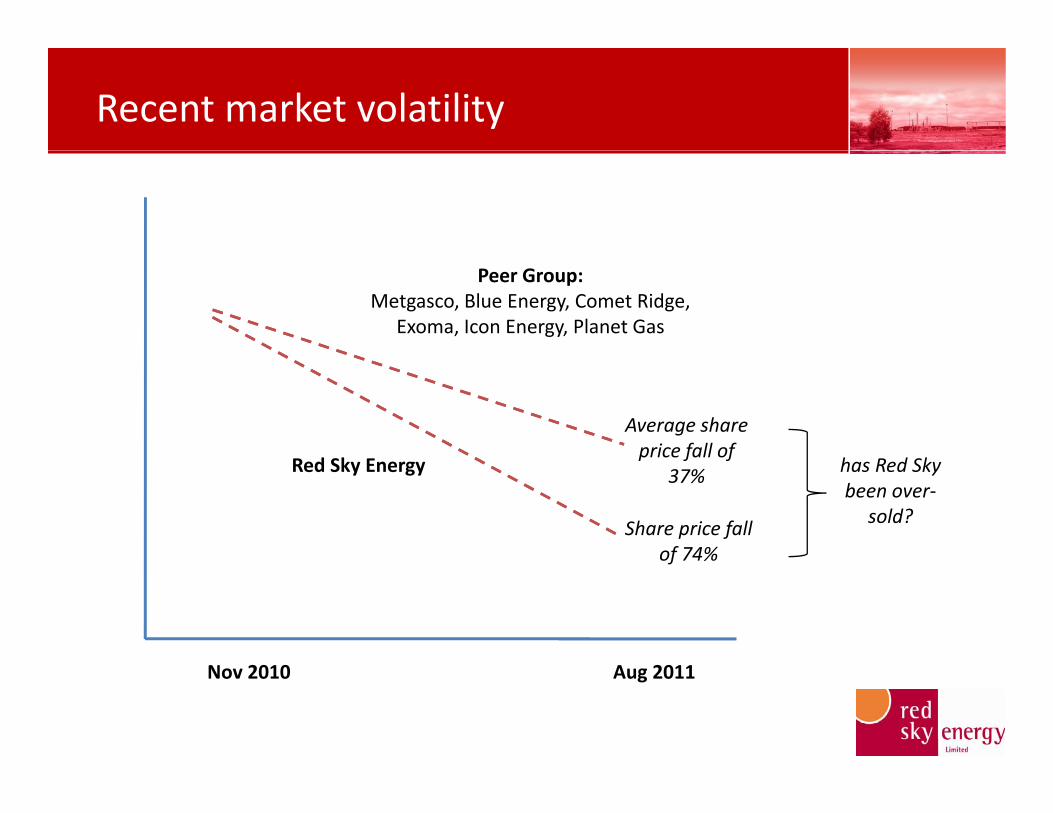

Recent market volatility

Peer Group: Metgasco, Blue Energy, Comet Ridge,

Exoma, Icon Energy, Planet Gas

d k

Average share price fall of

h d kRed Sky Energyp f f

37%

Share price fall of 74%

has Red Sky been over‐

sold?

of 74%

Nov 2010 Aug 2011

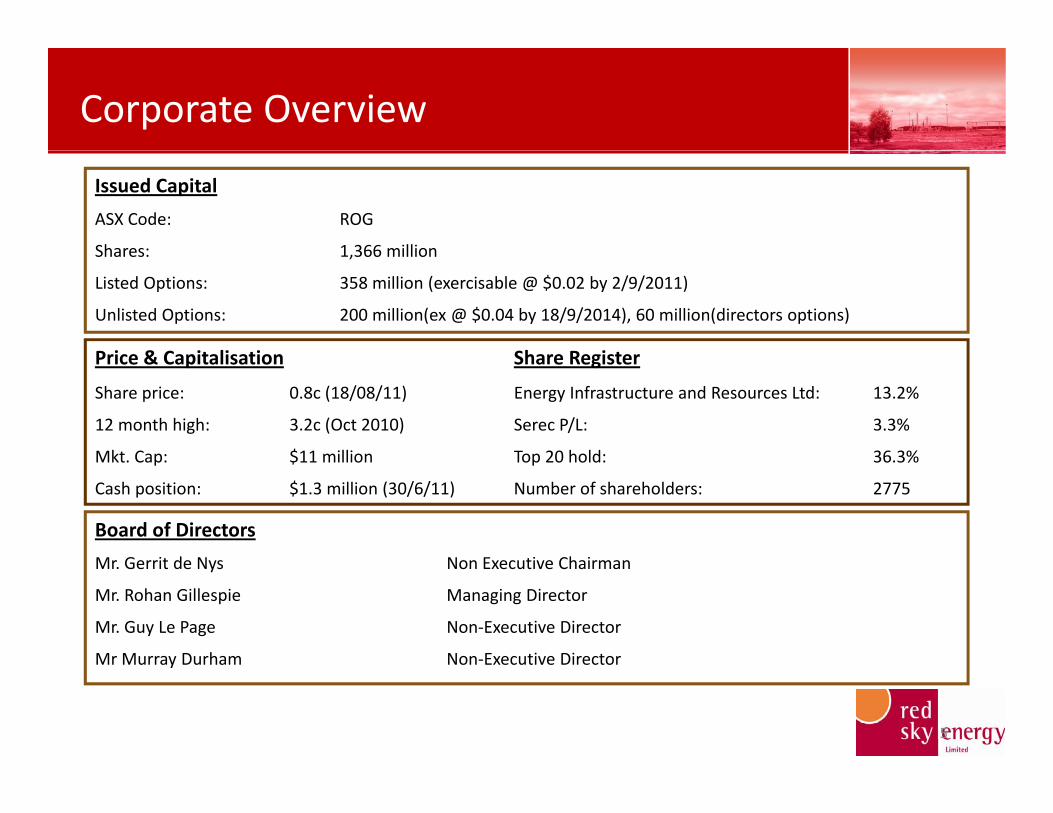

Corporate Overview

Issued Capital

ASX Code: ROG

Shares: 1 366 millionShares: 1,366 million

Listed Options: 358 million (exercisable @ $0.02 by 2/9/2011)

Unlisted Options: 200 million(ex @ $0.04 by 18/9/2014), 60 million(directors options)

Price & Capitalisation Share RegisterPrice & Capitalisation Share Register

Share price: 0.8c (18/08/11) Energy Infrastructure and Resources Ltd: 13.2%

12 month high: 3.2c (Oct 2010) Serec P/L: 3.3%

Mkt Cap: $11 million Top 20 hold: 36 3%Mkt. Cap: $11 million Top 20 hold: 36.3%

Cash position: $1.3 million (30/6/11) Number of shareholders: 2775

Board of Directors

Mr Gerrit de Nys Non Executive ChairmanMr. Gerrit de Nys Non Executive Chairman

Mr. Rohan Gillespie Managing Director

Mr. Guy Le Page Non‐Executive Director

Mr Murray Durham Non‐Executive Director

5

Mr Murray Durham Non Executive Director

Red Sky Energy team

• Rohan Gillespie: Managing Director. As Vice President and Chief Operating Office, Rohan created and led BHP Billiton’s CSG business . He has extensive experience in gas commercialisation including power generation and petrochemicals. Prior roles include credit executive with Commonwealth Bank, corporate development with Ceramic Fuel Cells and Renewable Energy Corp, and gas business development with BHP Petroleum.

• Gerrit de Nys: Non executive Chairman. Gerrit has an impressive trackrecord of business building. HeGerrit de Nys: Non executive Chairman. Gerrit has an impressive trackrecord of business building. He formed the construction materials division of the Hong Kong based Shui On Group, and with IMC Group he grew the shipyard operations in Thailand into a business enterprise. Gerrit is also a non executive director with Horizon Oil.

• Guy Le Page: Non‐executive Director. Guy is a Director and Corporate Advisor for RM Capital, which specialises in resources. He is actively involved in a range of corporate initiatives from mergers and acquisitions, initial public offerings to valuations, consulting and corporate advisory roles.

• Murray Durham: Non‐executive Director. Murray spent his early career as a geologist with Shell in Canada. Since then he has built extensive commercial experience in gas marketing with BHP Billiton and Apache.

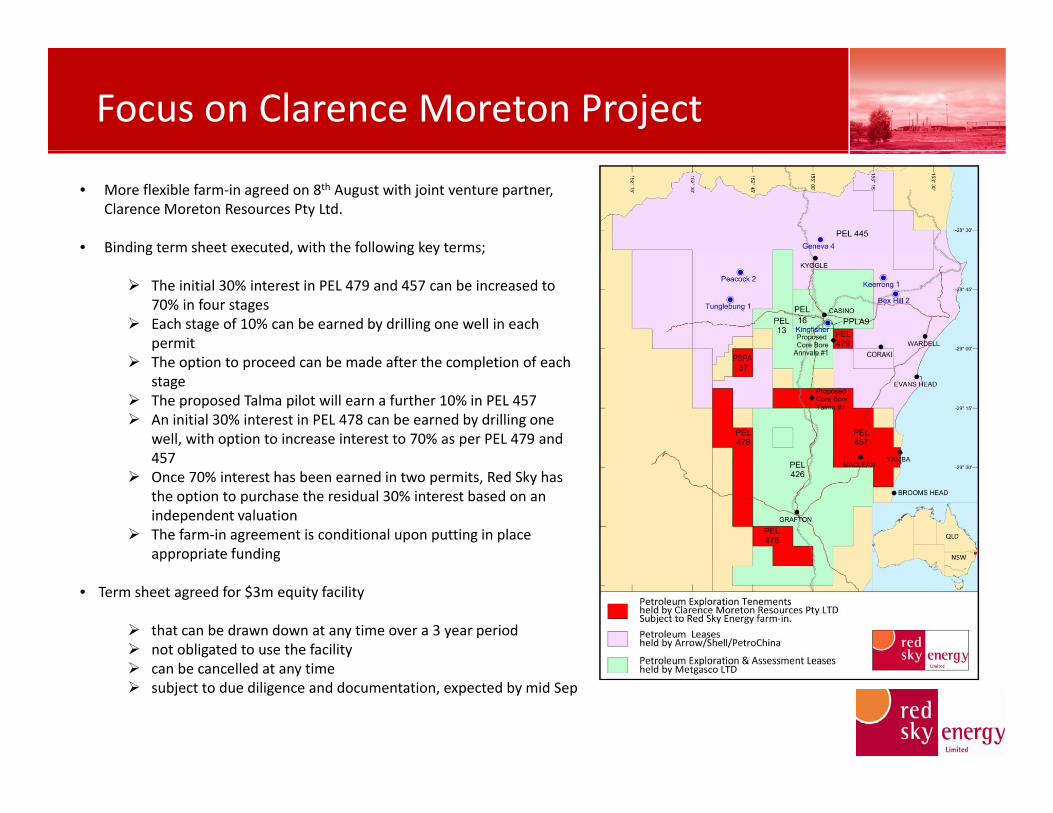

Focus on Clarence Moreton Project

• More flexible farm‐in agreed on 8th August with joint venture partner, Clarence Moreton Resources Pty Ltd.

• Binding term sheet executed, with the following key terms;g , g y ;

The initial 30% interest in PEL 479 and 457 can be increased to 70% in four stagesEach stage of 10% can be earned by drilling one well in each permitThe option to proceed can be made after the completion of each stageThe proposed Talma pilot will earn a further 10% in PEL 457An initial 30% interest in PEL 478 can be earned by drilling one well, with option to increase interest to 70% as per PEL 479 and 457457Once 70% interest has been earned in two permits, Red Sky has the option to purchase the residual 30% interest based on an independent valuationThe farm‐in agreement is conditional upon putting in place appropriate fundingpp p g

• Term sheet agreed for $3m equity facility

that can be drawn down at any time over a 3 year periodnot obligated to use the facility

b ll dcan be cancelled at any timesubject to due diligence and documentation, expected by mid Sep

Clarence Moreton Project

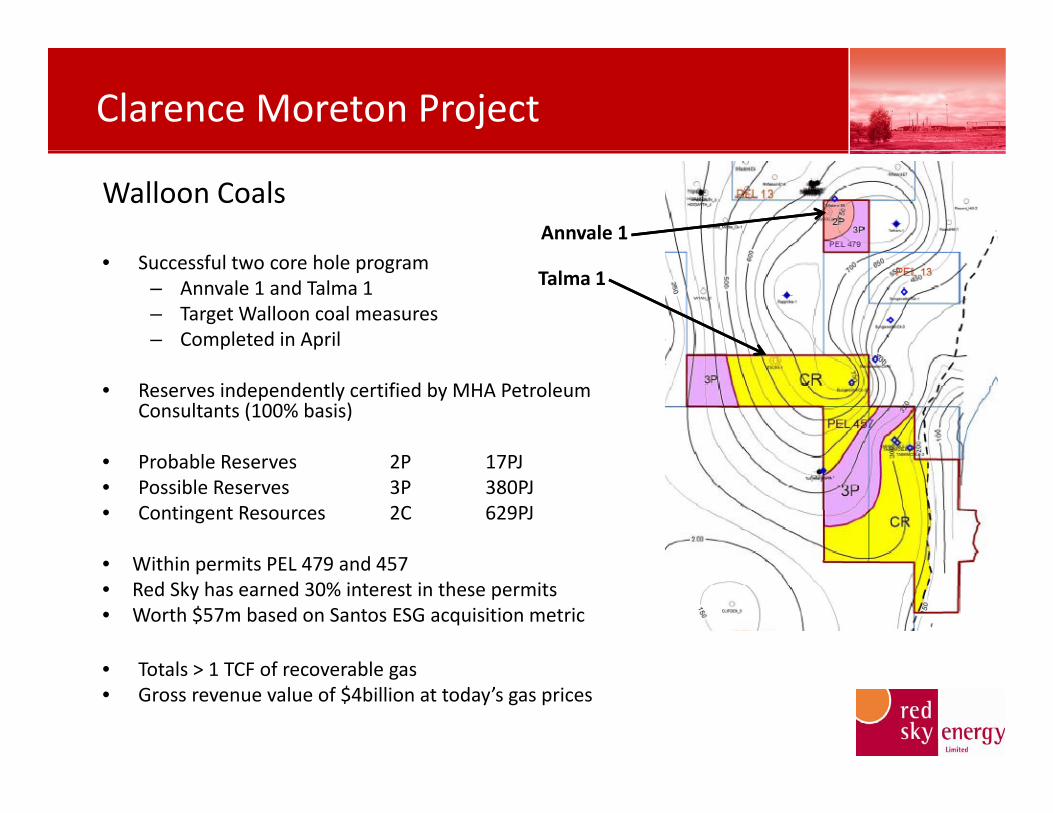

Walloon Coals Annvale 1

• Successful two core hole program– Annvale 1 and Talma 1– Target Walloon coal measures– Completed in April

Talma 1

• Reserves independently certified by MHA Petroleum Consultants (100% basis)

P b bl R 2P 17PJ• Probable Reserves 2P 17PJ• Possible Reserves 3P 380PJ• Contingent Resources 2C 629PJ

• Within permits PEL 479 and 457• Within permits PEL 479 and 457 • Red Sky has earned 30% interest in these permits• Worth $57m based on Santos ESG acquisition metric

T l 1 TCF f bl• Totals > 1 TCF of recoverable gas• Gross revenue value of $4billion at today’s gas prices

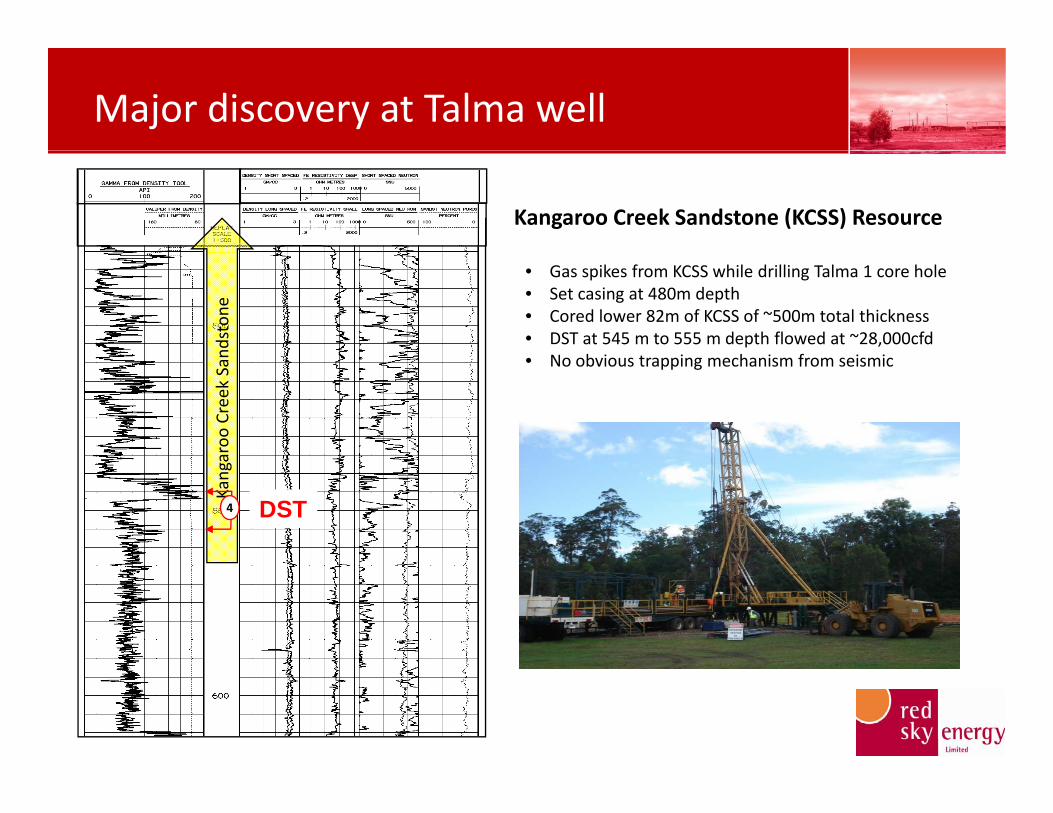

Major discovery at Talma well

Kangaroo Creek Sandstone (KCSS) Resource

• Gas spikes from KCSS while drilling Talma 1 core hole• Set casing at 480m depth• Cored lower 82m of KCSS of ~500m total thickness • DST at 545 m to 555 m depth flowed at ~28,000cfd

N b i i h i f i indston

e

• No obvious trapping mechanism from seismic

aroo

Creek San

Kanga

4 DST

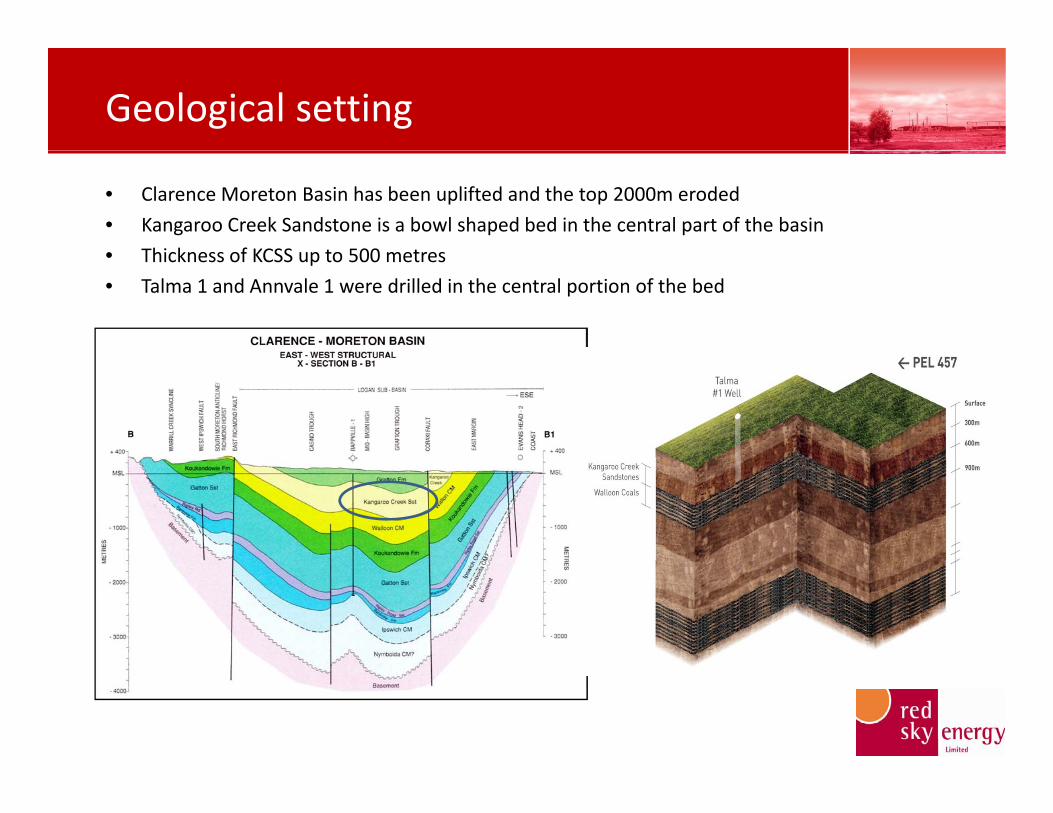

Geological setting

• Clarence Moreton Basin has been uplifted and the top 2000m eroded

• Kangaroo Creek Sandstone is a bowl shaped bed in the central part of the basin

• Thickness of KCSS up to 500 metres• Thickness of KCSS up to 500 metres

• Talma 1 and Annvale 1 were drilled in the central portion of the bed

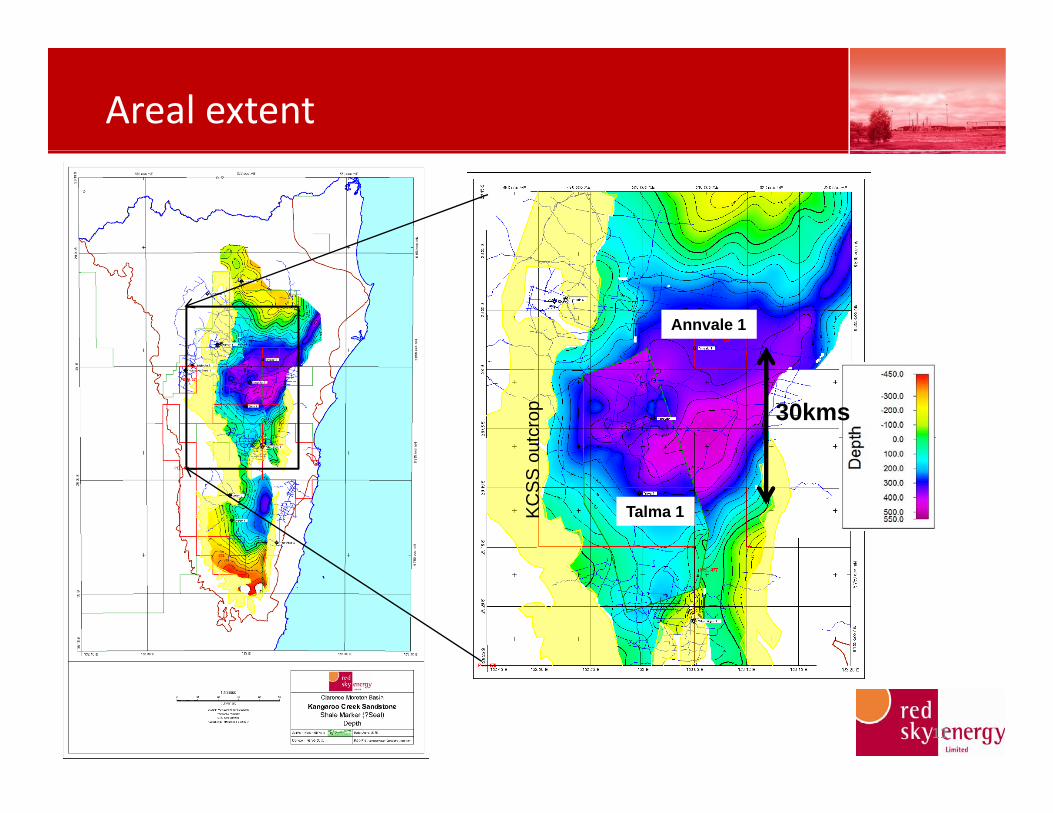

Areal extent

Annvale 1

outc

rop 30kms

KCSS

oTalma 1

11

Reservoir properties

• Attractive features:

• Shallow, hence low cost developmentShallow, hence low cost development• Laterally extensive• Thick – up to 500 metres• Expect minimal water extraction during gas production• Not expected to use fraccingNot expected to use fraccing

• Porous but tight reservoir, with porosity 10 ‐ 12% and permeability generally less than 1mD, with high permeability streaks along the clay‐rich bedding planesg p

• The sands will contain a significant volume of gas but will flow predominantly from the high permeability streaks

• Gas‐in‐place range: If total thickness of KCSS is gas charged, estimated gas‐in‐place range is 3.0 to 6.5 PJ per km2

f• Extent of KCSS within PEL 457 and 479 – 320km2 – up to 2TCF gas‐in‐place

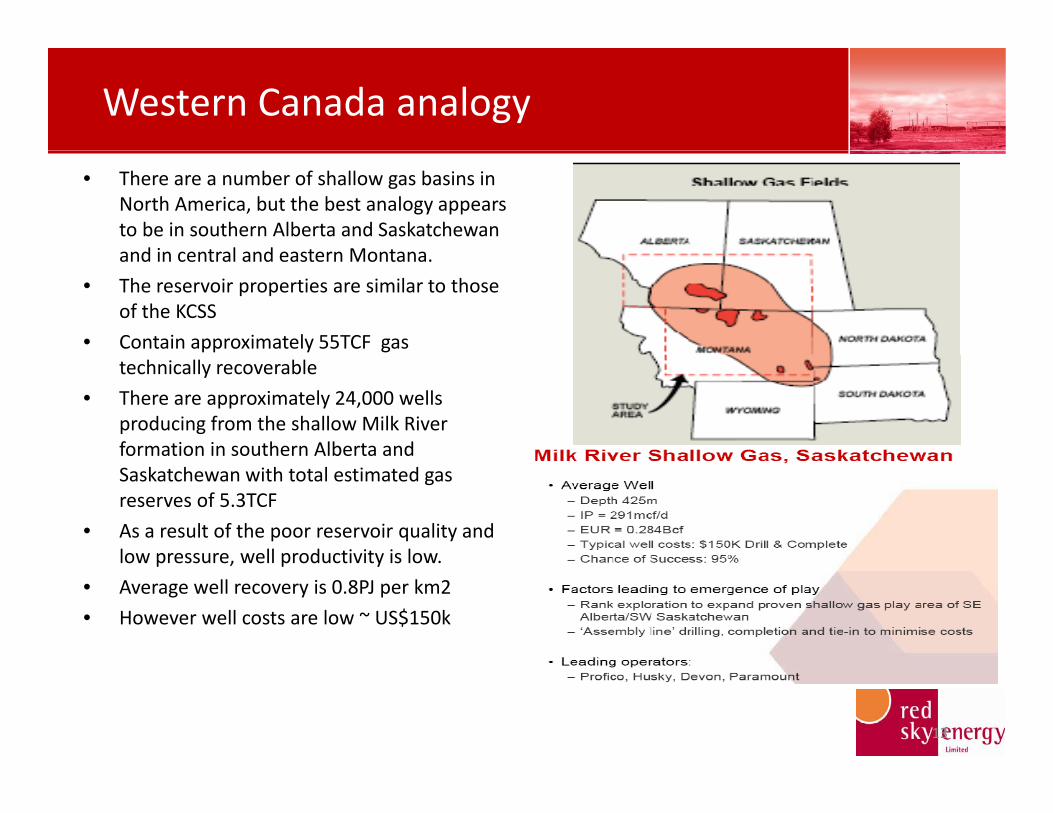

Western Canada analogy

• There are a number of shallow gas basins in North America, but the best analogy appears to be in southern Alberta and Saskatchewan and in central and eastern Montanaand in central and eastern Montana.

• The reservoir properties are similar to those of the KCSS

• Contain approximately 55TCF gas technically recoverable

• There are approximately 24,000 wells producing from the shallow Milk River formation in southern Alberta and Saskatchewan with total estimated gas reserves of 5.3TCF

• As a result of the poor reservoir quality and low pressure well productivity is lowlow pressure, well productivity is low.

• Average well recovery is 0.8PJ per km2

• However well costs are low ~ US$150k

13

Potential producibility

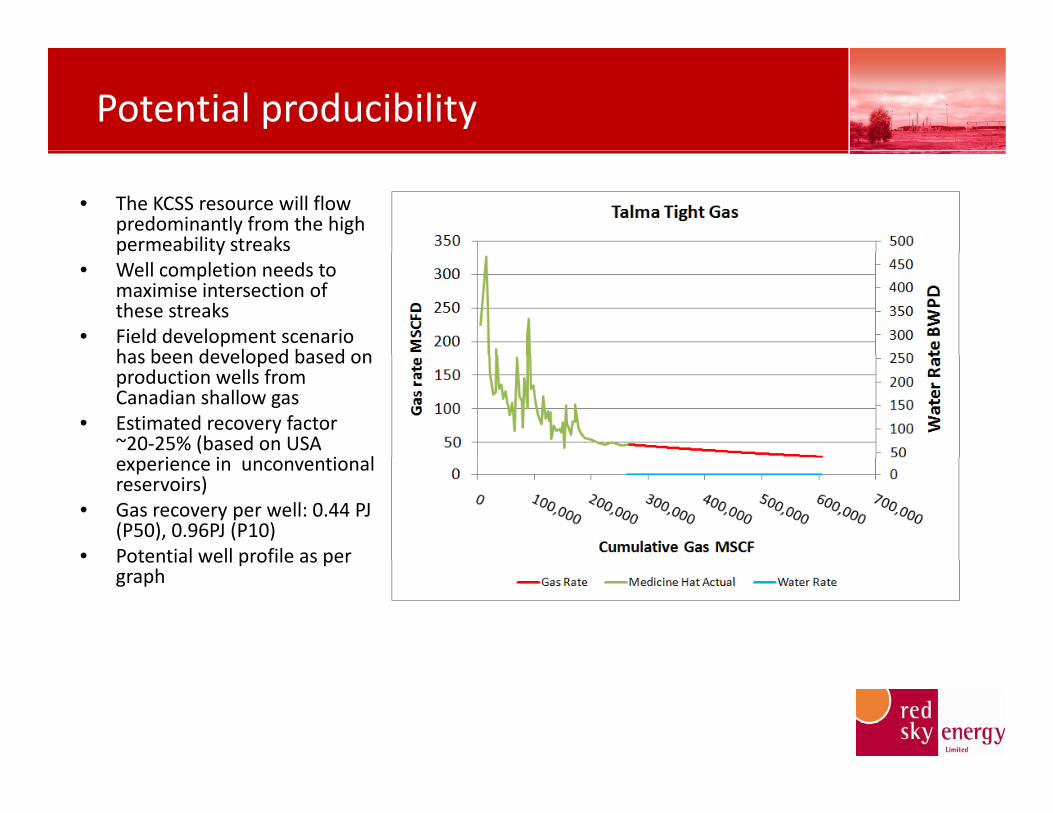

• The KCSS resource will flow predominantly from the high permeability streaksp y

• Well completion needs to maximise intersection of these streaks

• Field development scenario has been developed based onhas been developed based on production wells from Canadian shallow gas

• Estimated recovery factor ~20‐25% (based on USA

i i i lexperience in unconventional reservoirs)

• Gas recovery per well: 0.44 PJ (P50), 0.96PJ (P10)

• Potential well profile as perPotential well profile as per graph

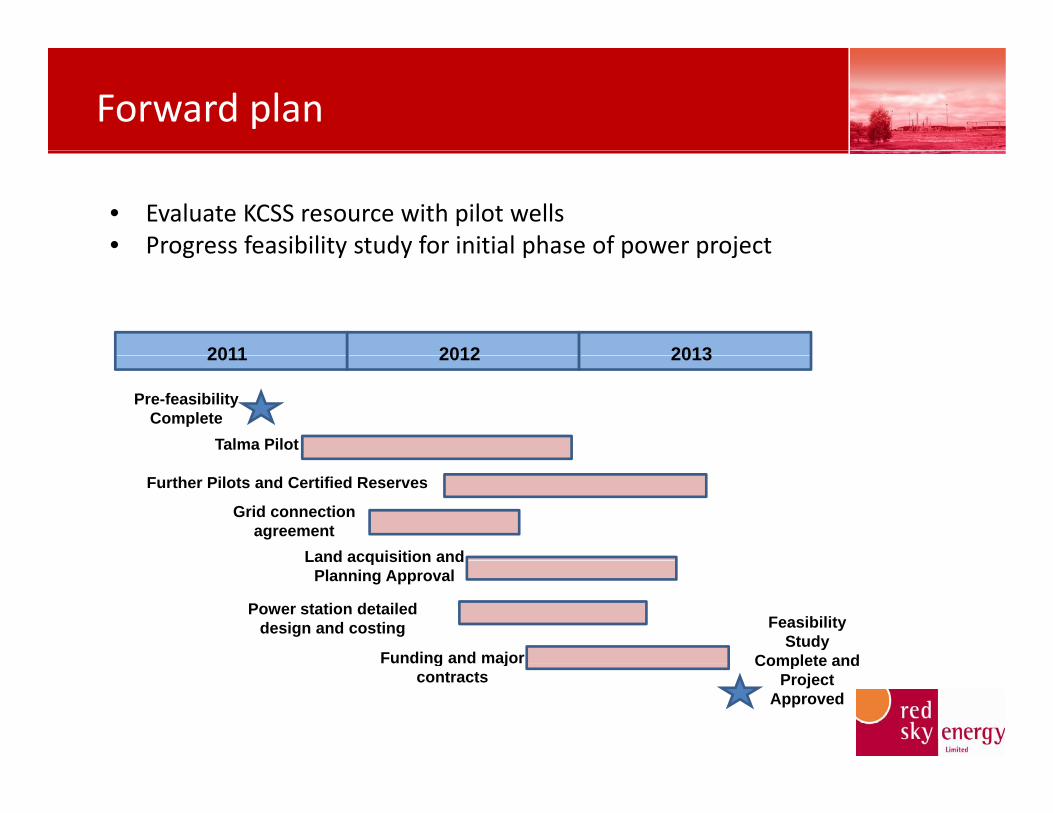

Forward plan

• Evaluate KCSS resource with pilot wells• Progress feasibility study for initial phase of power project

2011

Progress feasibility study for initial phase of power project

2012 20132011

Pre-feasibility Complete

Talma Pilot

2012 2013

Grid connection agreement

Land acquisition and

Further Pilots and Certified Reserves

Land acquisition and Planning Approval

Power station detailed design and costing

Funding and major

Feasibility Study

Complete andFunding and major contracts

Complete and Project

Approved

Resource evaluation plan

• Single well pilot, re‐enter Talma 1 core hole

Pl d t d ill th il t ll d i Q4 2011 ( bj t• Planned to drill the pilot well during Q4 2011 (subject to regulatory approvals which are pending)

• Commence production by year end

• Drill with air to avoid water contact with reservoir, and avoid expanding clays

• Operate the pilot well over an extended period

• Extended testing over several months could allow initial reserves certification.

• Follow with two step out pilot wells (within 1 2kms)• Follow with two step out pilot wells (within 1‐2kms)

• Test different completion methods

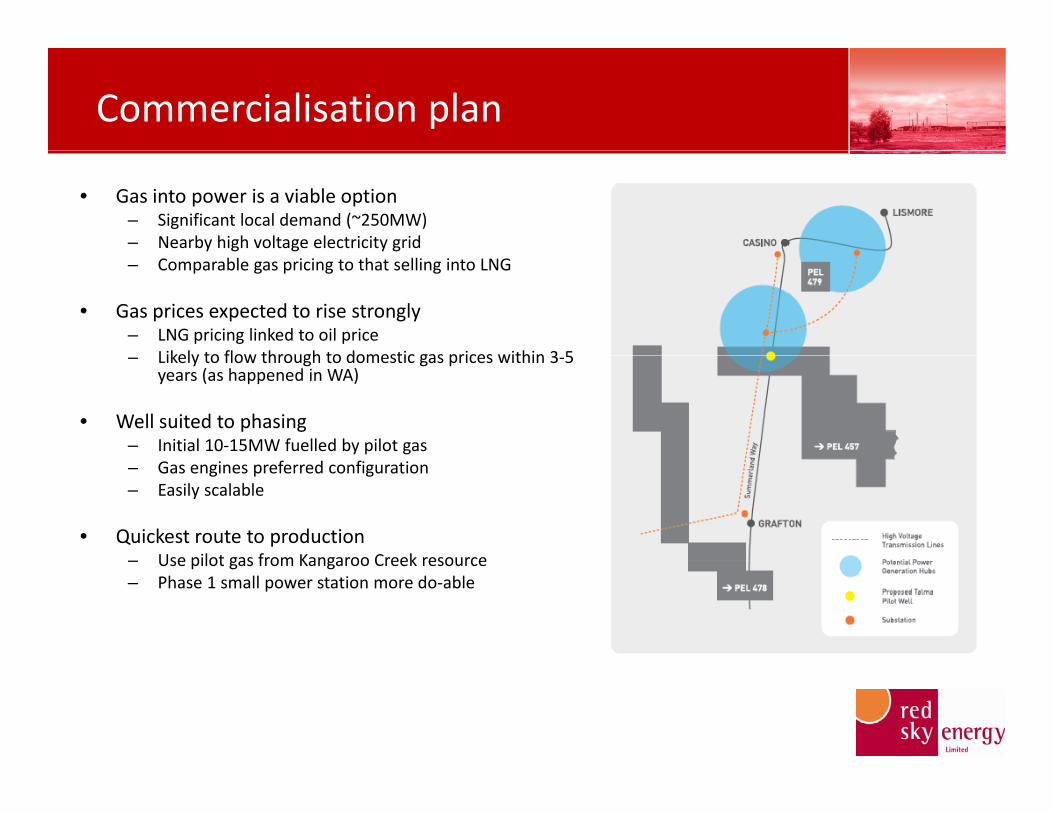

Commercialisation plan

• Gas into power is a viable option– Significant local demand (~250MW)– Nearby high voltage electricity grid– Comparable gas pricing to that selling into LNG

• Gas prices expected to rise strongly– LNG pricing linked to oil price

Likely to flow through to domestic gas prices within 3 5– Likely to flow through to domestic gas prices within 3‐5 years (as happened in WA)

• Well suited to phasing– Initial 10‐15MW fuelled by pilot gas– Gas engines preferred configuration– Easily scalable

• Quickest route to production– Use pilot gas from Kangaroo Creek resource– Use pilot gas from Kangaroo Creek resource– Phase 1 small power station more do‐able

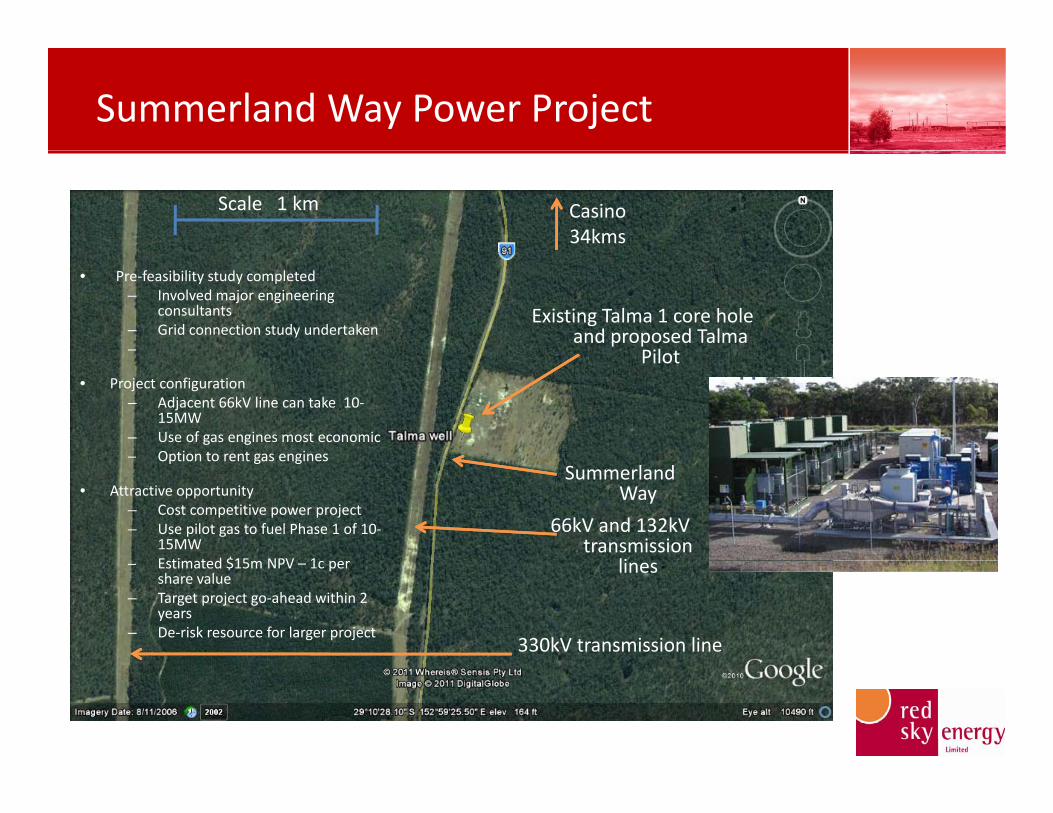

Summerland Way Power Project

Scale 1 km Casino34kms

Existing Talma 1 core hole and proposed Talma

Pilot

• Pre‐feasibility study completed– Involved major engineering

consultants– Grid connection study undertaken– Pilot

• Project configuration– Adjacent 66kV line can take 10‐

15MW– Use of gas engines most economic– Option to rent gas engines

Summerland Way

66kV and 132kV transmission

li

Option to rent gas engines

• Attractive opportunity– Cost competitive power project– Use pilot gas to fuel Phase 1 of 10‐

15MWE ti t d $15 NPV 1 lines

330kV transmission line

– Estimated $15m NPV – 1c per share value

– Target project go‐ahead within 2 years

– De‐risk resource for larger project

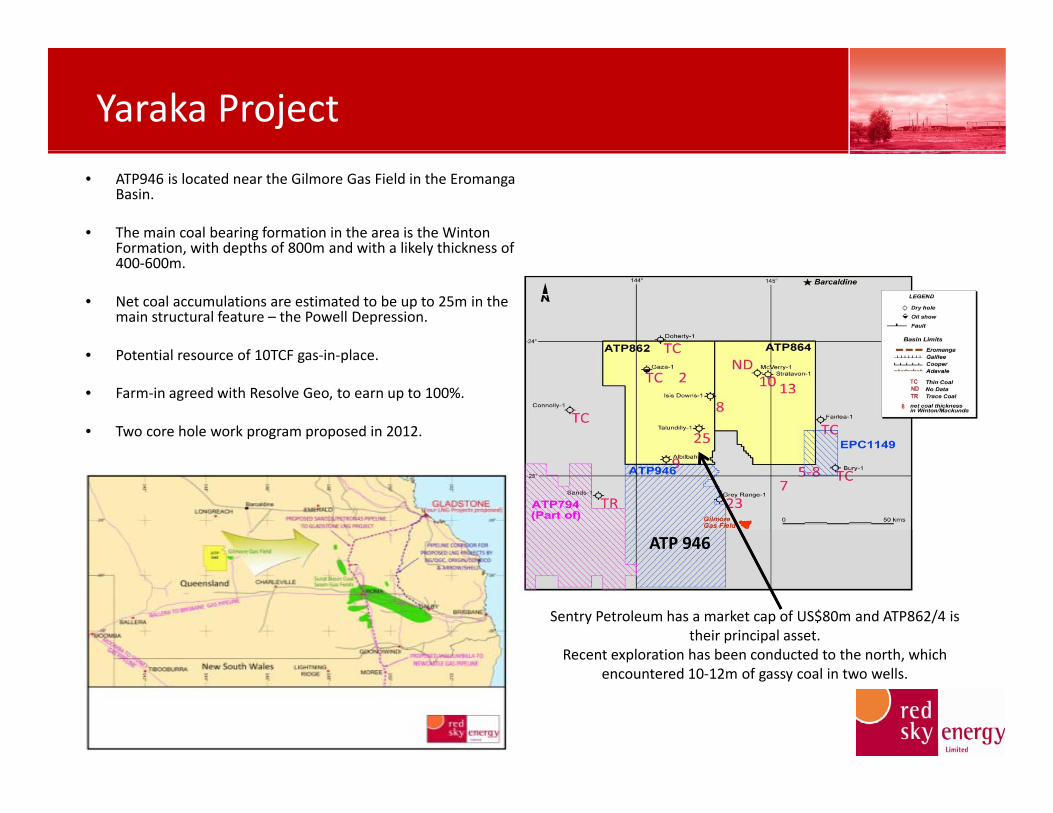

Yaraka Project

• ATP946 is located near the Gilmore Gas Field in the EromangaBasin.

• The main coal bearing formation in the area is the Winton Formation, with depths of 800m and with a likely thickness of , p y400‐600m.

• Net coal accumulations are estimated to be up to 25m in the main structural feature – the Powell Depression.

• Potential resource of 10TCF gas in place• Potential resource of 10TCF gas‐in‐place.

• Farm‐in agreed with Resolve Geo, to earn up to 100%.

• Two core hole work program proposed in 2012.

ATP 946

Sentry Petroleum has a market cap of US$80m and ATP862/4 is their principal asset.

Recent exploration has been conducted to the north, which encountered 10‐12m of gassy coal in two wells.

Fundamentals of gas in Eastern Australia

LNG market in Gladstone creates huge demand

• Three projects committed, another likely to follow– Initial 8 trains totalling ~34mtpa of LNG– Buyers want evidence full 20 years of contracted gas is there– Requires ~55TCF of gas– Another 27TCF of gas if third trains committed

• BG says they have enough for three trains ‐ 21TCF of resources• BG says they have enough for three trains ‐ 21TCF of resources– Need to convert all of this to reserves, unlikely to happen

Domestic gas market is significant as wellDomestic gas market is significant as well

• Power generation– No‐one is building any more coal fired generation– Last one was by QLD Govt owned CS Energy committed in 2004 y Q gy– Gas will supply most of growth– Requires ~20TCF of gas over next 20 years

• Industrial gas market– Needs ~7TCF over next 20 years

Significant recent news

Santos acquisition of Eastern Star Gas• Underpins CSG sector valuationsp• Priced at 50c per GJ of 3P reserves

LNG players need more gasLNG players need more gas• Santos ESG deal• Santos deal with Beach for 750PJ gas purchase agreement ex Moomba• BG Drillsearch deal to develop shale gas in Cooper Basin

Domestic gas prices to rise strongly• Santos Beach gas sale price linked to oil price

i l i d l• TRUenergy involvement in Santos ESG deal

Key value drivers for Red Sky

Low exploration riskLow exploration risk

Access to gas market

Well located

Experienced team

Funded thru next phaseFunded thru next phase

Significant potential upside

Contact Details

Red Sky Energy Limited

Level 17 500 Collins StreetLevel 17, 500 Collins Street

MELBOURNE, VIC, 3000

Ph: (03) 9614 0600

F (03) 9614 0550Fax: (03) 9614 0550

Rohan GillespieRohan Gillespie

Managing Director

Mob: 0438 722 443

E: [email protected]: [email protected]

23

Disclaimer

The information presented herein contains predictions, estimates and other forward looking statements that are subject to risk factors that are associated with the oil and gas business.Certain information in this presentation has been derived from third parties and, although Red Sky Energy has no reason to believe that it is not accurate, reliable or complete, it has not been independently audited or verified by Red Sky Energy. Although the company believes that its expectations are based on reasonable assumptions it can give no assurances that its goals will be achievedassumptions, it can give no assurances that its goals will be achieved.Important factors that could cause results to differ materially from those included in the forward‐looking statements include timing and extent of changes in commodity prices for oil and gas, the need to develop and replace reserves, environmental risks, drilling and operating risks, risks related to exploration and development, uncertainties about estimates of prospective contingent resources and reserves, competition, government regulation and the ability of the company to meet its stated goals.The purpose of this presentation is to provide background information to assist in obtaining a general understanding of the Red Sky Energy's proposals and objectives. This presentation is not to be considered as a recommendation by Red Sky Energy orThis presentation is not to be considered as a recommendation by Red Sky Energy or any of its subsidiaries, directors, officers, affiliates, associates or representatives that any person invest in its securities. It does not take into account the investment objectives, financial situation and particular needs of each potential investor. If you are unclear in relation to any matter or you have any questions, you should seek advice f t t fi i l d ifrom an accountant or financial adviser.