Embed Size (px)

Citation preview

Asset Recovery Department

01 April, 2014

To All Branches / Offices

Circular No. 4016 / ARDC 204 / 2014-15

Reg: Review of NPA Recovery Policy

The NPA Recovery Policy of the Bank has been reviewed and approved by the Board of

Directors. The revised NPA Recovery Policy is attached as annexure to this circular and

also published in “Drisya – Announcements” and “Drisya - ARD Home” page. The revised

policy comes into effect from 01-04-2014.

A summary of changes brought about in the revised policy is given below:

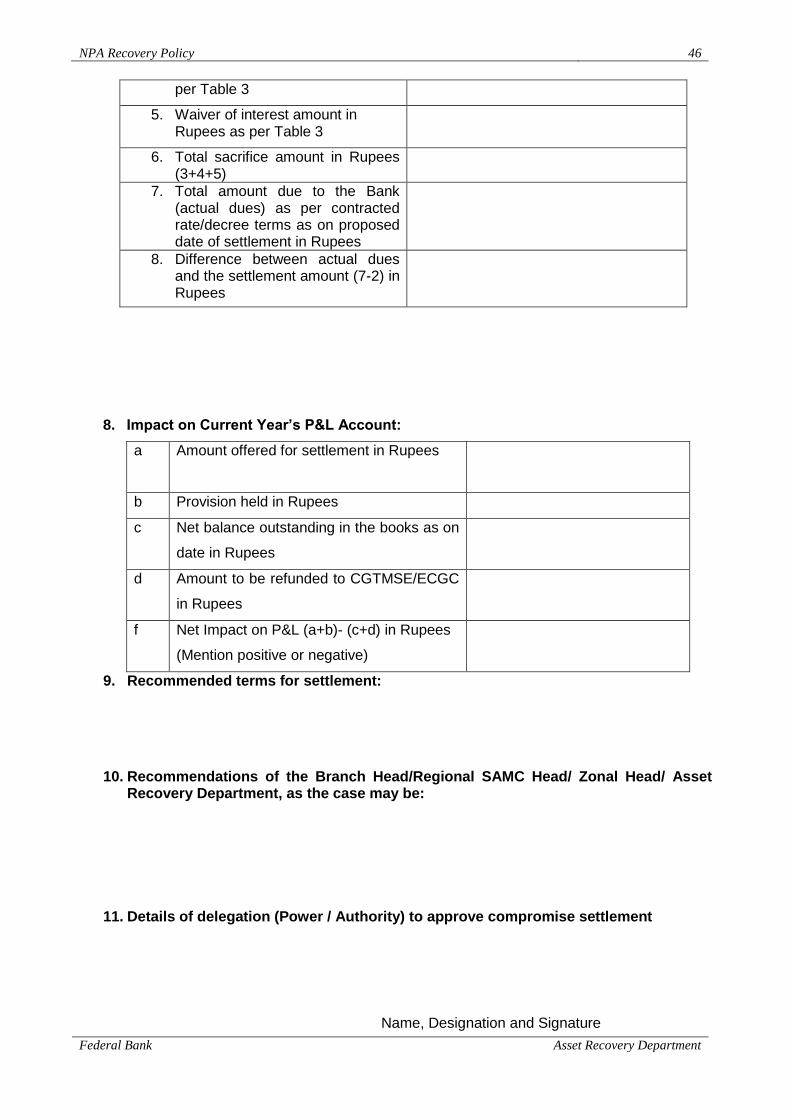

1. Compromise Proposals: Pricing for dues and sacrifice computation has been modified.

The minimum and maximum interest rates for sacrifice computation have been fixed as

simple interest at Bank’s Base Rate and simple interest at Bank’s Base Rate + 6%

respectively, based on the age of NPA and the risk score. The revised compromise

worksheet and C422 have been published in “Drisya – Announcements” and “ARD

Home” page.

All Branches / SAMCs / Regional and Zonal Offices shall ensure that only the

revised compromise worksheets are used for dues and sacrifice computation while

submitting compromise proposals from 01-04-2014.

2. Revised Compromise worksheets (Table 1,2,3) and C 422 are attached to the revised

NPA Recovery Policy.

3. Procedure for valuation of security property of NPA accounts has been brought in line with

the valuation policy of the Bank.

4. Power / Authority for approving compromise proposals of NPAs has been revised.

5. Power / Authority for according sanction for extending period of compromise settlements;

filing Suit / Revenue Recovery application; permitting extension of time to the bidder of

security under SARFAESI sale; verification of draft plaints / RR application; permitting

Waiver of Legal Actions; permitting filing / not filing of appeals against decree from Civil

Courts / Debt Recovery Tribunals; and permitting partial release of securities in NPA

accounts (not as part of a compromise settlement of full liability) has been revised.

6. Power / Authority to sanction NPA Recovery related expenses has also been revised.

All employees of the Bank are requested to refer the revised NPA Recovery Policy and comply

with the revised guidelines in matters relating to NPA recovery.

Syriac Joseph

Deputy General Manager

Asset Recovery Department

NPA Recovery Policy 2

Federal Bank Asset Recovery Department

NPA Recovery Policy

(with effect from 01-04-2014)

Table of Contents

1. Introduction ...................................................................................................................... 4

2. Objectives ........................................................................................................................ 4

3. Non-Performing Assets [NPA] .......................................................................................... 4

4. Categories of NPA ........................................................................................................... 5

5. Guidelines for classification .............................................................................................. 5

6. Recovery function and Structure ...................................................................................... 6

7. Monitoring and Review of NPA accounts – submission of reports .................................... 7

8. Follow up actions ............................................................................................................. 8

9. Appropriation of recovery in NPAs and interest application .............................................. 9

10. Valuation of securities in NPAs ........................................................................................ 9

11. Settlement of NPA accounts under compromise ............................................................ 10

12 Power/Authority to approve compromise settlement of NPAs ......................................... 15

13. Special Scheme for One Time Settlement [OTS] of small value NPAs ........................... 18

14. One Time Settlement of NPAs in Micro and Small Enterprises Sector. .......................... 19

15. Restructuring of NPAs .................................................................................................... 20

16. Right of Recompense .................................................................................................... 20

17. Lok Adalats .................................................................................................................... 20

18. SARFAESI Act Proceedings .......................................................................................... 22

19. Debt Recovery Tribunals and Appellate Tribunals ......................................................... 24

20. Recovery Camps ........................................................................................................... 24

21. Recovery through legal action ........................................................................................ 25

22. Waiver of legal action ..................................................................................................... 25

23. Identification of Willful Defaulters and submission of reports to RBI and Credit Information Bureaus ......................................................................................................................... 26

24. Non Banking Assets ....................................................................................................... 28

25. Suits / cases against the Bank relating to NPAs ............................................................. 29

26. Sale of NPA ................................................................................................................... 29

27. Power / Authority for according sanction for filing Suit / Revenue Recovery application. 29

28. Power / Authority for permitting Waiver of Legal Actions ................................................ 30

29. Power / Authority for permitting filing / not filing of appeals against decree from Civil Courts / Debt Recovery Tribunals ............................................................................................. 30

30. Power / Authority for permitting partial release of securities in NPA accounts (not as part of a compromise settlement of full liability) ..................................................................... 31

31. Power / Authority to sanction NPA Recovery related expenses...................................... 32

32. Submission of Reports to the Board / Finance Committee / Audit Committee ................ 35

33. Submission of Reports to Managing Director & CEO ..................................................... 36

NPA Recovery Policy 3

Federal Bank Asset Recovery Department

34. Submission of Reports to Reserve Bank of India and Credit Information Bureaus ......... 36

35. Scope for Audit .............................................................................................................. 37

36. Staff Accountability ........................................................................................................ 37

37. Review of the policy ....................................................................................................... 38

38. Custodian of the policy ................................................................................................... 38

39. Other Policies ................................................................................................................ 38

40. Annexure I – Eligibility Score Card [Table 1] .................................................................. 40

41. Annexure II - Basis for pricing [Table 2] ......................................................................... 41

42. Annexure III – Dues and Sacrifice Computation [Table 3] .............................................. 42

43. Annexure IV – C422 [Format of proposal for compromise settlement]............................ 44

44. Annexure V – Format of request for OTS for small value NPAs ..................................... 47

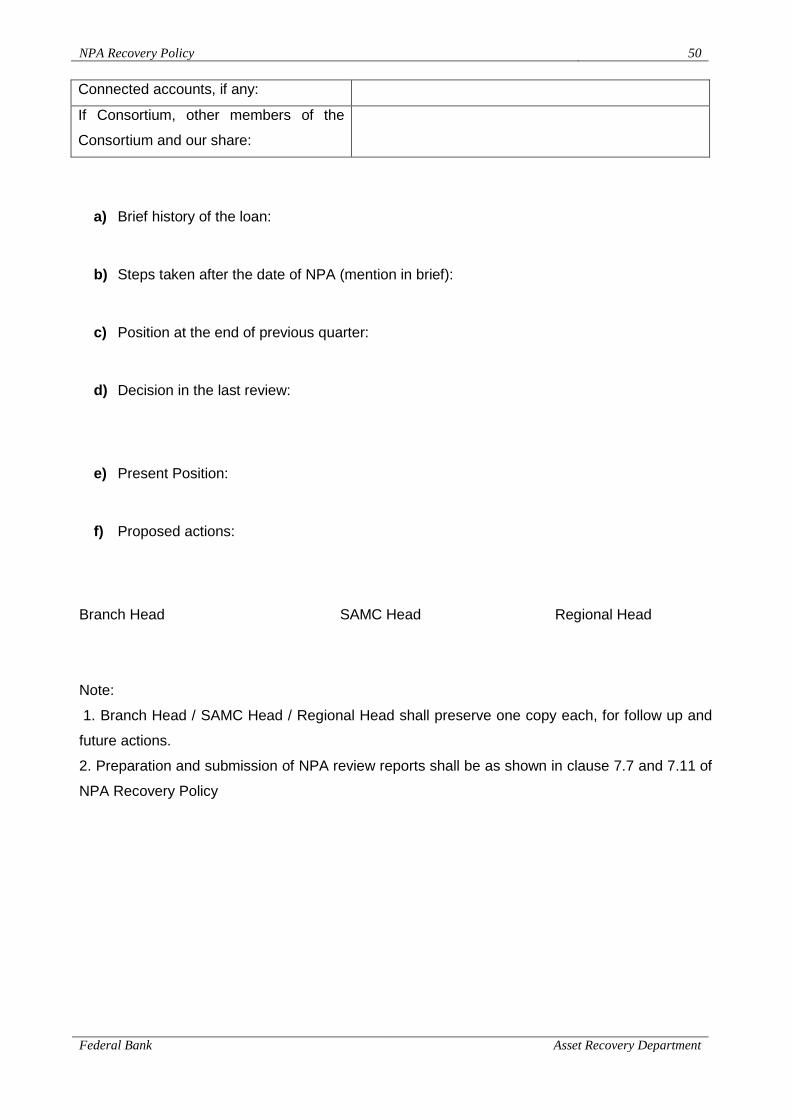

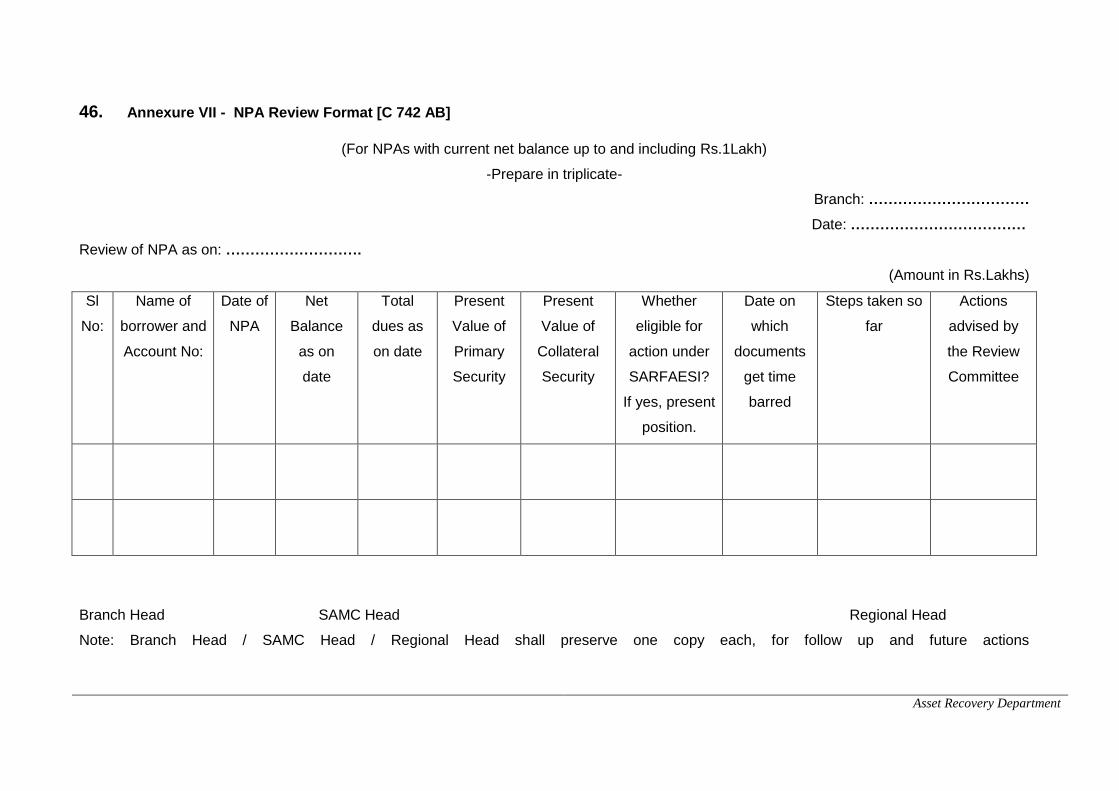

45. Annexure VI - NPA Review Format [C 742 A] ................................................................ 48

46. Annexure VII - NPA Review Format [C 742 AB] ............................................................ 53

NPA Recovery Policy 4

Federal Bank Asset Recovery Department

1. Introduction

1.1. This policy document shall be called “NPA Recovery Policy”.

1.2. The NPA recovery policy sets out policies and processes of the Bank for identifying and

managing non-performing assets, reviewing non-performing assets and recovering the money

due to the Bank. The document also sets out processes and resources for compliance of

regulatory guidelines on NPAs, ongoing monitoring of such assets, and establishes authority to

approve actions directly related to NPAs.

1.3. The policy envisages that the Board and the top management receive timely and

appropriate information about the Bank’s Non-Performing Asset portfolio, including classification

of Non-Performing Assets and resolution thereof.

1.4. The NPA Recovery Policy was adopted by the Board of Directors of the Bank in April

1999. The policy has been reviewed every year to keep abreast with the changes consistent with

evolving business and regulatory environment.

2. Objectives

2.1. The broad objectives of the NPA Recovery Policy are as follows:

a. Reduce stock of Non Performing Loan Assets of the Bank

b. Maximise recovery in Non-Performing Asset accounts through consistent and continuous

follow up, settlement, legal actions, sale of assets, etc.

c. Upgrading of assets classified as NPA at the earliest by collecting past dues and / or

rectification of deficiencies which lead to classification.

d. Adhering to statutory and regulatory requirements.

3. Non-Performing Assets [NPA]

3.1. A Non-Performing Asset [NPA] is an asset, including a leased asset, loan or investment

asset, which ceases to generate income for the Bank. NPA, as defined by the Reserve Bank of

India in the ‘Prudential Norms on Income Recognition, Asset Classification and Provisioning

pertaining to Advances’ is a loan or an advance where;

a. interest and / or installment of principal remain overdue for a period of more than 90 days in

respect of a term loan,

b. the account remains ‘out of order’ in respect of an Overdraft/Cash Credit (OD/CC),

c. the bill remains overdue for a period of more than 90 days in the case of bills purchased and

discounted,

d. the installment of principal or interest there on remains overdue for two crop seasons for

short duration crops,

e. the installment of principal or interest there on remains overdue for one crop season for long

duration crops,

f. the amount of liquidity facility remains outstanding for more than 90 days, in respect of a

securitization transaction undertaken in terms of RBI guidelines on securitization.

NPA Recovery Policy 5

Federal Bank Asset Recovery Department

g. the overdue receivables representing positive mark-to-market value of a derivative contract

remain unpaid for a period of 90 days from the specified due date for payment.

3.2. An account should be treated as 'out of order' if the outstanding balance remains

continuously in excess of the sanctioned limit/drawing power. In cases where the outstanding

balance in the principal operating account is less than the sanctioned limit/drawing power, but

there are no credits continuously for 90 days as on the date of Balance Sheet or credits are not

enough to cover the interest debited during the same period, these accounts should be treated as

'out of order'.

3.3. Any amount due to the Bank under any credit facility is ‘overdue’, if it is not paid on the

due date fixed by the Bank.

3.4. The Bank shall classify its assets as Non-Performing, strictly based on and completely

adhering to the norms and guidelines issued by Reserve Bank of India, from time to time.

4. Categories of NPA

4.1. Non-Performing Assets shall be classified into the following three categories based on the

period for which the asset has remained nonperforming and the extent to which realisation of the

dues is possible.

a. Substandard Assets - a substandard asset would be one, which has remained NPA for a

period less than or equal to 12 months.

b. Doubtful Assets - an asset would be classified as doubtful if it has remained in the sub-

standard category for a period of 12 months. An asset, classified as doubtful asset, is further

classified as “Doubtful 1” during the first year, as “Doubtful 2” during the next two years and

as “Doubtful 3” beyond three years.

c. Loss Assets - a loss asset is one where loss has been identified by the Bank or internal or

external auditors or the RBI inspection, but the amount has not been written off wholly.

4.2. The classification as above need not necessarily follow the chronological order in

instances where frauds are involved or where there is considerable deterioration in the value of

securities.

5. Guidelines for classification

5.1. Classification of assets should be done according to the prudential norms on income

recognition, asset classification and provisioning pertaining to advances, published by the

Reserve Bank of India from time to time.

5.2. The Bank should not delay or postpone the identification of NPAs, especially in respect of

high value accounts. The responsibility for ensuring proper asset classification shall lie with the

Asset Recovery Department of the Bank. The process shall normally be system driven, with

validation levels built into the accounting software. Doubts in asset classification due to any

reason shall be settled by the Asset Recovery Department within one month from the date on

which the account would have been classified as NPA as per extant guidelines.

5.3. The classification of an asset as NPA should be based on the record of recovery. The

availability of security or net worth of borrower/ guarantor should not be taken into account for the

purpose of treating an advance as NPA or otherwise.

NPA Recovery Policy 6

Federal Bank Asset Recovery Department

6. Recovery function and Structure

6.1. The structure of recovery function in the Bank shall be as follows:

a. Asset Recovery Department at Head Office

b. Stressed Asset Management Cells attached to Zones [SAMC]

c. Asset Recovery Branches [at least one in each of the Zones]

d. Recovery Officers attached to Regional Office

e. Branches

f. External Recovery Agents

6.2. Asset Recovery Department at Head Office shall be primarily responsible for managing

NPA recovery functions in the Bank as a whole.

6.3. Stressed Asset Management Cells [SAMCs] attached to each Zonal Office shall monitor

the progress in recovery of NPA accounts and guide the branches in recovery measures. Each

SAMC shall be responsible for the overall supervision and monitoring of recovery processes of

the branches attached to it.

6.4. Principal Officers of branches and the Officers who are entrusted by the Principal Officers

with the responsibility of managing NPA recovery shall be directly responsible for executing the

recovery actions and upgrading NPA accounts. Every possible step shall be taken to upgrade a

Non Performing Account to ‘standard” category. Branches shall initiate the recovery process

immediately after an account is classified as Non-Performing and ensure that the account is

upgraded to “standard” category at the earliest.

6.5. Zonal Head shall be responsible to ensure that the NPA recovery functions across the

Zone are carried out regularly and the goals set up by the Corporate Office in NPA front are

achieved. The Regional Head shall monitor, co-ordinate and control the NPA recovery functions

of the respective Region.

6.6. Asset Recovery Department shall co-ordinate with SAMCs and Regional Heads and

provides necessary guidance for recovery operations.

6.7. Asset Recovery Branches shall act as Nodal Offices for coordinating / follow up of all

applications filed / to be filed before the Debt Recovery Tribunals and Appellate Tribunals

functioning at the respective centers and also extend necessary support and guidance to

branches for NPA recovery. Asset Recovery Branches shall be reporting directly to Asset

Recovery Department at Head Office in all functional matters. Asset Recovery Branches shall

supplement the NPA recovery efforts in the Zone as a whole, in many different manners.

6.8. The Bank shall maintain a panel of Recovery Agents for augmenting the recovery efforts

of the branches, adhering to the guidelines of Reserve Bank of India and Bank’s outsourcing

policy and policy on engagement of Recovery Agents. The Bank should have a Board approved

policy for engaging external Recovery Agents for NPA recovery. The empanelment of agencies /

persons as Recovery Agents shall be done centrally by Asset Recovery Department at Head

Office. Asset Recovery Department shall conduct ongoing reviews of performance of Recovery

Agents and submit reports to the Managing Director & CEO on a quarterly basis.

NPA Recovery Policy 7

Federal Bank Asset Recovery Department

6.9. The Bank shall post its own Officers as Recovery Officers attached to its Regional Offices

under the direct control of the Regional Heads. The Recovery Officers shall extend all necessary

support to branches in NPA recovery and in preventing slippage of accounts to NPA category.

6.10. Corporate Office shall fix gross NPA level targets and NPA recovery targets for the Bank

as a whole, and for different Zones. Zonal Offices shall distribute their targets to the Regions and

Branches and take all necessary steps and measures to achieve the targets of Gross NPA level

and recovery of NPAs. Asset Recovery Department at Head Office shall be responsible for the

overall achievement of various targets related to NPAs, for the Bank as a whole.

7. Monitoring and Review of NPA accounts – submission of reports

7.1. Non Performing Accounts of all categories with net balance up to Rs.10Lakhs shall be

monitored individually by the respective SAMC.

7.2. Non Performing Accounts of all categories with net balances of Rs.10Lakhs and above

shall be monitored individually by Asset Recovery Department on a continuous basis.

7.3. Branches / Regions / SAMCs / Zones shall be responsible for follow up and recovery of all

NPAs, irrespective of the amount, whether technically written off or not, even though monitoring

and overseeing of NPAs are segregated as shown in 7.1 and 7.2 above.

7.4. SAMC along with the Regional Head concerned shall review all NPA accounts of the

branches attached to it, irrespective of the amount, at least once in a quarter.

7.5. Regional Heads shall participate in the NPA review process actively. The Zonal Heads

shall oversee NPA review and ascertain progress from time to time.

7.6. Asset Recovery Department shall review all NPA accounts with net balances of

Rs.10Lakhs and above on an ongoing basis.

7.7. The NPA Review Officer and the supervising official in Asset Recovery Department at

Head Office shall prepare review reports for each of the NPAs with net balances of Rs.10Lakhs

and above and place the same before the higher authorities for completing the review process.

Once the review process is completed, the review reports shall be forwarded to the Branch and

SAMC concerned for further actions. Asset Recovery Department shall follow up the progress in

recovery with each of the branches / SAMCs on individual account basis. The process of review

and submission of review reports shall be as follows:

NPAs with net balance Review Reports

to be prepared by

Review to be conducted by

Up to Rs.10Lakhs Branch concerned SAMC and Regional Head, once in a

quarter.

Rs.10Lakhs up to Rs.25Lakhs HO / ARD Head of Asset Recovery Department

and another Officer of ARD not below

Chief Manager, once in a quarter.

Above Rs.25L upto Rs.100L HO / ARD Head of ARD and the General

Manager & Chief Risk Officer, once in

a quarter.

Rs.100Lakhs up to Rs.500Lakhs HO / ARD The General Manager & Chief Risk

Officer and one of the senior

NPA Recovery Policy 8

Federal Bank Asset Recovery Department

executives in DGM cadre or above in

Head Office, once in a quarter.

Rs.500Lakhs and above HO/ARD Board of Directors, through Credit

Committee of the Board, once in a

quarter

7.8. Individual review reports in respect of top 25 NPA borrowers with net balances up to

Rs.500Lakhs in each category (Substandard, Doubtful, Loss), excluding technically written off

accounts, shall be placed before the Credit Committee of the Board once in a quarter [separate

memorandum for each category].

7.9. Newly classified NPA accounts [fresh slippage] with net balance of Rs.500Lakhs and

above shall be reported to the Board of Directors once in a quarter.

7.10. Asset Recovery Department at Head Office shall place a memorandum before the Board

of Directors, with the details of recovery in NPAs on a quarterly basis, with particular reference to

recoveries of Rs.50Lakhs and above.

7.11. Review of NPAs as above shall be done in prescribed formats. The format C742A

[Annexure VI] shall be used for the review of NPAs with current net balance above Rs.1Lakh, The

format C742AB [Annexure VII] shall be used for the review of NPAs with current net balance up to

and including Rs.1Lakh.

7.12. Asset Recovery Department at Head Office shall place a review note before the Board of

Directors, on SARFAESI and other recovery actions initiated during the period on a quarterly

basis.

8. Follow up actions

8.1. Non Performing Accounts of all categories shall be directly followed up by the branches.

Follow up actions shall include sending letters, meeting the borrowers in person and persuading

to regularize / settle the dues, meeting co-obligants, guarantors etc and convincing them to settle

the dues, etc.

8.2. It shall be ensured that the securities charged to the Bank are intact and are not alienated.

Securities shall be inspected at periodic intervals and the correct value properly recorded.

8.3. Liquid securities and pledged goods shall be appropriated to reduce the balance

outstanding.

8.4. If an account has become NPA due to cash flow problems, the repayment program may

be re-scheduled based on the revised cash flow projections. This would enable the Bank to

maintain the asset quality at the same level for one year and asset quality can be upgraded after

one year, if the repayment is received as per the re-drawn schedule.

8.5. In the case of sick but viable industrial units, prospects for rehabilitation shall be looked

into and nursing program be evolved.

8.6. Possibility of CDR and internal restructuring by Bank shall be explored.

8.7. The advance shall be recalled if the activity is not continuing in the expected manner or if

there is evidence of diversion / siphoning of funds.

8.8. Possibility of settlement through compromise shall be explored in all cases of NPAs.

NPA Recovery Policy 9

Federal Bank Asset Recovery Department

8.9. In the case of accounts coming under priority sector, Revenue Recovery proceedings

shall be initiated.

8.10. ECGC / CGTMSE claims, if any, shall be lodged with the respective agencies and

followed up for early settlement of the claim.

8.11. In the case of all eligible accounts, action under SARFAESI Act shall be initiated as and

when an account turns NPA. In all cases eligible for recovery actions under SARFAESI Act,

demand notice under section 13(2) of SARFAESI Act shall be issued to all borrowers / co-

obligants / guarantors within 10 days of the account being classified as NPA.

8.12. In case all the efforts to regularize / settle the account fails or if alienation of the securities

charged to the Bank is anticipated, the Bank shall resort to other legal remedies. It shall be

ensured that documentation is proper and complete. Irregularities, if any, shall be got rectified

before resorting to legal action.

8.13. If found necessary, SAMCs shall entrust the follow-up of an account to Recovery Agents

empanelled by the Bank for augmenting the recovery efforts of branches.

8.14. If recovery / settlement of accounts is found to be difficult and time consuming, the Bank

shall explore the possibility of exiting the loan through sale to ARCs / other banks / FIs.

8.15. If all avenues for recovery are exhausted, the Bank may examine the option of write off of

the balance dues.

9. Appropriation of recovery in NPAs and interest application

9.1. Interest realized on NPAs may be taken to income account, provided the credits in the

accounts towards interest are not out of fresh / additional credit facilities sanctioned to the

borrower concerned.

9.2. In the absence of a clear agreement between the Bank and the borrower for the purpose

of appropriation of recoveries in NPAs (i.e. towards principal or interest due), the accounting of

recoveries in NPAs shall be based on “first in first out” policy; ie. the earliest entry shall be

realized first. If different entries are made in the account on the same day, the realization shall be

in the order of charges, interest, and principal.

9.3. On an account turning NPA, the Bank should reverse the interest already charged and not

collected by debiting the Profit and Loss account. Such accrued interest and interest applied

thereafter should be recorded in the suspense account “Unrealized Interest” in the books. For the

purpose of computing Gross Advances, interest recorded in the suspense account should not be

taken into account.

10. Valuation of securities in NPAs

10.1. While conducting valuation of security properties in NPA accounts, the procedures and

guidelines stipulated in the Bank’s Valuation Policy shall be complied with.

10.2. Valuation of security properties shall be got done by external professionals / agencies

empanelled by the Bank. Such professionals / agencies should value the property, fix the value

and submit reports with comments on the nature of the property, its characteristics, etc in the

format prescribed by the Bank.

NPA Recovery Policy 10

Federal Bank Asset Recovery Department

10.3. Wherever valuation by external professional / agency is obtained for security properties in

NPAs, the Branch Head should also visit / inspect the security properties and confirm the value

reported by the external professional / agency. The branch head shall inform Asset Recovery

Department and the SAMC, of any adverse comments on the value arrived at by the external

valuer. Confirmation of valuation by the Branch Head shall be done in the format prescribed by

the Bank

10.4. In centres where external valuers are not empanelled, valuation of security property shall

be conducted by the officials of the Branch, for NPA loans and advances with net balance not

exceeding Rs.10Lakhs. Valuation report in C7E shall be submitted to SAMC.

10.5. If the current net balance in NPA is Rs.2500Lakhs or above, the valuation of the security

property shall be got conducted independently by two external valuers who are in the panel of the

Bank.

10.6. If there is any considerable negative variation in the value of the properties compared to

the previous valuation report, the Branch Head shall investigate and record the reasons for such

variations and report to SAMC and Asset Recovery Department.

10.7. Wherever guideline value fixed by the government is in force, it shall be taken into

consideration while valuing and the valuation shall be made in line with the guideline of valuation.

10.8. External valuers shall be rotated periodically. The property shall not be valued by the

same valuer who has valued the property last time.

10.9. All security properties in the nature of Land and / or Building in NPAs shall be valued /

revalued as above once in three years. However, if a proposal for compromise settlement of NPA

is received from the borrower, and if the existing valuation report is more than one year old (but

not older than three years), the property shall be revalued by the Branch Head and the valuation

report shall be prepared in the format C7E. Report in C7E shall be submitted along with the

previous valuation report which is not more than three years old. If the previous valuation report is

older than three years, fresh valuation shall be got conducted as laid down in clause 10.2, 10.3,

10.4, 10.5, 10.6, 10.7 and 10.8 above. If the committee approving the compromise proposal

desires so, a fresh valuation report shall be obtained, even in cases where the latest valuation

was done recently.

10.10. Assessment of realizable value of Securities while considering proposals for Compromise

Settlement of NPAs shall be done, as provided under clause 11 of this policy. Valuation of NPA

securities shall also be based on various aspects as contained specifically in Clause 11.14 to

11.19 of this policy document.

11. Settlement of NPA accounts under compromise

11.1. Settlement of non-performing advances under compromise shall be considered in the

following circumstances:

a. Borrower is not a wilful defaulter, or if the borrower is a wilful defaulter, settlement terms shall

be worked out to the maximum benefit of the Bank,

b. Activity of the borrower is stopped / become un-viable due to reasons beyond his control and

over-dues mounting up due to application of interest / penal interest and other charges and

the recovery of the debt has become doubtful,

NPA Recovery Policy 11

Federal Bank Asset Recovery Department

c. Value of primary / collateral securities is inadequate / nil,

d. Means of the borrower / guarantor / co-obligant are nominal,

e. All remedies available other than filing of suit are exhausted,

f. Legal position of the Bank is weak,

g. Legal action is expensive and time consuming and not commensurate with the amount

involved,

h. Borrower expired and the legal heirs approached for a settlement,

i. The unit is potentially sick where rehabilitation process is not likely to yield any results,

j. All possible steps for recovery have been taken and there is no considerable scope for

recovery.

11.2. The negotiation shall aim at recovering maximum dues and minimizing the sacrifice. In

cases where sufficient securities are available to cover the dues, the Bank shall opt for

compromise, only if it is beneficial for the Bank, considering other relevant factors.

11.3. If realizable value of primary / collateral and net worth is more than 100% of the total dues

as on the date of NPA, negotiation process shall not confine to the Notional Settlement Amount

computed by the Bank. Actual dues as per the books shall be advised to the borrower and

negotiation should start from such total/gross dues owed by the borrower.

11.4. Write off or compromise shall be resorted to, only if it is in the larger interest of the Bank.

Compromise / write off decisions shall be judicious.

11.5. Proposals for compromise settlement of NPAs shall be prepared in the specified format, C

422 [Annexure IV].

11.6. While submitting compromise/ write off proposal in accounts where claim has been

received from ECGC/CGTMSE, terms and conditions stipulated by the respective body should be

complied with. Prior permission / concurrence of ECGC / CGTMSE shall be obtained for

compromise settlement, if claim has been received in the NPA account.

11.7. Wilful defaulters, cases wherein any type of fraud is involved and borrowers defaulting due

to reasons beyond their control shall be distinguished.

11.8. All guidelines issued by Reserve Bank of India from time to time in respect of compromise

settlement of NPAs shall be complied with. Compromise settlement of NPAs for an amount below

the realizable value of securities shall not normally be permitted.

Write off / Waiver

11.9. A compromise/negotiated settlement involves certain amount of sacrifice on the part of the

Bank such as:

a. Waiver of interest / penal interest.

b. Reduction in the rate of interest as against the contracted rate

c. Charging of simple interest instead of compound interest

d. Scaling down of the debt/ write off of principal

NPA Recovery Policy 12

Federal Bank Asset Recovery Department

11.10. Write off refers to exemption of principal amount itself. Compromise settlement below the

outstanding principal amount is not normally envisaged. However, in exceptional cases where the

sanctioning authority is convinced that write off is inevitable under the prevailing situation,

compromise settlements involving write off of a certain portion of the principal amount may also

be considered, on a very selective basis. A specific note with reasons for allowing such

compromise settlements shall be recorded.

11.11. In respect of NPAs in which sufficient collateral security is available, write off of full or part

of the dues shall not normally be permitted.

Assessment of realizable value of securities

11.12. While assessing the value of securities available, for arriving at a compromise settlement,

proper weightage shall be given to its location, condition, marketable title, marketability and

possession thereof. Valuation of securities in NPAs shall be done as provided under clause 10 of

this document, with particular reference to clause 10.9.

11.13. If the primary/ collateral security is shared on first charge basis with other secured

creditor(s), the value to be considered shall be computed on pro rata basis with respect to the

principal outstanding of the said creditors.

11.14. Proper distinction shall be made between market value and realizable value of the

securities. Wide variation in value of property at the time of considering the OTS/Write off

compared to its valuation at the time of original sanction/renewal should be critically examined

and highlighted. Earlier valuations may also be correlated/ commented in the latest valuation

report. Wide variation in the valuation of securities at the time of considering the compromise

proposal may negate the bargaining power/pressure on the borrower to arrive at an amount more

favorable to the Bank.

11.15. Under the provisions of SARFAESI Act, sale of charged assets is much faster. Particularly

in such cases, there is no justification to build discount factor while arriving at realizable value of

the assets vis-à-vis market value. Therefore, it is important that the valuation reports are analyzed

and self-assessment is made about the genuineness of the market/realizable value of the

securities given by an external valuer keeping in mind the real-estate market and other attendant

factors prevailing in the area, so that it proves to be an effective tool for discussion/negotiation for

settlement amount.

11.16. In case it is found that due to the complex features of any of the security properties,

assistance and professional advice of an external valuer is required, the branch concerned may

be permitted by the Regional SAMC/Zonal Head to seek the assistance and professional advice

of one of the external valuers in Bank’s panel, even in cases where valuation of securities by

external agencies is not normally envisaged.

11.17. Valuation should also specify the value likely to be received under circumstances of

forced/ distress sale. All factors/circumstances relevant and having impact on the value/chances

of sale of the security property shall be examined and the valuation report should specify all

positive and negative features based on which the valuation is arrived at.

11.18. Market value of securities shall be shown in all proposals for compromise settlements.

11.19. The following factors shall be considered while assessing the value of securities:

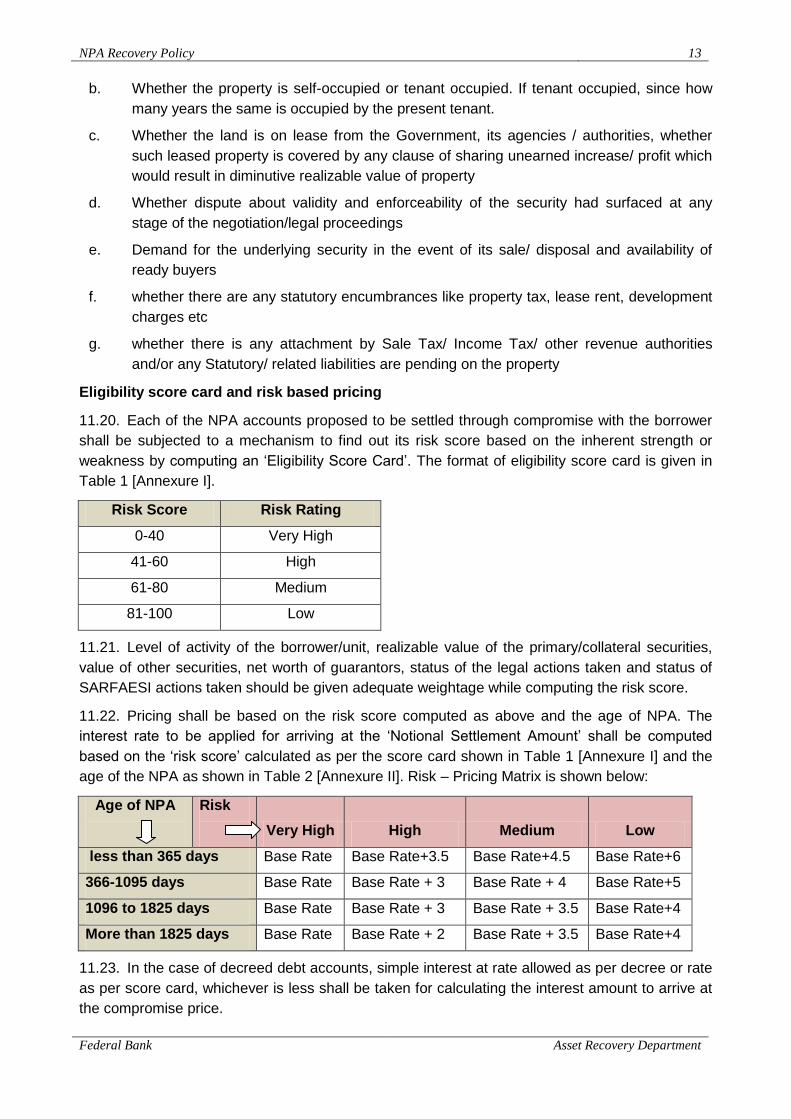

a. Nature of the property - Whether commercial or residential

NPA Recovery Policy 13

Federal Bank Asset Recovery Department

b. Whether the property is self-occupied or tenant occupied. If tenant occupied, since how

many years the same is occupied by the present tenant.

c. Whether the land is on lease from the Government, its agencies / authorities, whether

such leased property is covered by any clause of sharing unearned increase/ profit which

would result in diminutive realizable value of property

d. Whether dispute about validity and enforceability of the security had surfaced at any

stage of the negotiation/legal proceedings

e. Demand for the underlying security in the event of its sale/ disposal and availability of

ready buyers

f. whether there are any statutory encumbrances like property tax, lease rent, development

charges etc

g. whether there is any attachment by Sale Tax/ Income Tax/ other revenue authorities

and/or any Statutory/ related liabilities are pending on the property

Eligibility score card and risk based pricing

11.20. Each of the NPA accounts proposed to be settled through compromise with the borrower

shall be subjected to a mechanism to find out its risk score based on the inherent strength or

weakness by computing an ‘Eligibility Score Card’. The format of eligibility score card is given in

Table 1 [Annexure I].

Risk Score Risk Rating

0-40 Very High

41-60 High

61-80 Medium

81-100 Low

11.21. Level of activity of the borrower/unit, realizable value of the primary/collateral securities,

value of other securities, net worth of guarantors, status of the legal actions taken and status of

SARFAESI actions taken should be given adequate weightage while computing the risk score.

11.22. Pricing shall be based on the risk score computed as above and the age of NPA. The

interest rate to be applied for arriving at the ‘Notional Settlement Amount’ shall be computed

based on the ‘risk score’ calculated as per the score card shown in Table 1 [Annexure I] and the

age of the NPA as shown in Table 2 [Annexure II]. Risk – Pricing Matrix is shown below:

Age of NPA

Risk

Very High High Medium Low

less than 365 days Base Rate Base Rate+3.5 Base Rate+4.5 Base Rate+6

366-1095 days Base Rate Base Rate + 3 Base Rate + 4 Base Rate+5

1096 to 1825 days Base Rate Base Rate + 3 Base Rate + 3.5 Base Rate+4

More than 1825 days Base Rate Base Rate + 2 Base Rate + 3.5 Base Rate+4

11.23. In the case of decreed debt accounts, simple interest at rate allowed as per decree or rate

as per score card, whichever is less shall be taken for calculating the interest amount to arrive at

the compromise price.

NPA Recovery Policy 14

Federal Bank Asset Recovery Department

11.24. If the current rate of interest applicable to the loan is less than the rate as per score card,

simple interest at the current rate of interest shall be taken.

Dues and Sacrifice Computation – Concept of Notional Settlement Amount [NSA]

11.25. The ‘Notional Settlement Amount’ shown in Table 3 [Annexure III] is expected to give an

indication of the minimum amount to be collected from the borrower for settling the NPA account.

It does not, however, mean that the Bank can be fully satisfied on realization of such amount.

Actual dues of the borrower as on date of settlement shall be calculated and every attempt should

be made to collect the amount required to avoid any sacrifice / loss to the Bank. Notional

Settlement Amount will be considerably lower than the actual dues of the borrower and hence it

cannot be treated as the preferred amount for compromise settlement.

11.26. Efforts shall be made to negotiate and secure better offer than the ‘Notional Settlement

Amount’, especially where the realizable value of the security property is more than the NSA

arrived at.

11.27. If the borrower, under compelling circumstances, is unable, to pay the amount arrived at

on the basis of Table III, the best possible offer, depending upon merits and attendant

circumstances of individual case, may be considered by the Bank as a deviation case; reasons

and proper justification for the sacrifice shall be placed on record by the recommending/

sanctioning authority.

11.28. In all cases possible, lump sum remittances of the compromised sum shall be insisted. In

case installment payment facility is sought for, as far as possible, maximum amount shall be

collected as immediate payment at the first installment itself.

11.29. The “Notional Settlement Amount”/settlement amount may be different from the “actual

balance outstanding” due to application of interest at contracted rate or allowing operations in the

account or due to credit received and adjusted to interest suspense in the system, etc. The

amount to be waived in such cases will be different from that allowed in the compromise. In such

cases Zonal Head may permit the branches to close the account by accepting the compromise

amount in the case of compromises approved by the Zonal Level Committee. In all other cases,

such permission shall be obtained from HO/ARD. The balance amount, if any, remaining in the

account may be reversed from P& L A/c.

11.30. There may be cases where the offer amount is higher than the Notional Settlement

Amount, but less than the actual dues as per decree/ the account balance as per the contract etc.

In such cases as party is offering an amount higher than the Notional Settlement Amount, there is

no sacrifice as per Table III. However, as the amount offered is less than the actual dues, Zonal

Head may, subject to merits, permit the branch to treat the account as closed waiving the balance

dues after adjusting the compromise amount, even in cases where the compromise was

approved by HO.

11.31. In cases where suits/OAs are pending (not decreed) before courts/ DRTs, the branch

concerned should explore the possibility of getting the compromise recorded by the Court/DRT by

filing a Joint Memo of Compromise and to draw a compromise decree incorporating the terms of

compromise with a default clause entitling the Bank to recover the entire Suit/OA claim in the

event of the failure of the borrowers to settle the account, as per terms of compromise. Even in

cases where lump sum / part payment is received, memo shall be filed in the court / DRT.

NPA Recovery Policy 15

Federal Bank Asset Recovery Department

11.32. If the compromise amount is less than the current net balance, credit for the difference

amount shall be obtained by the branch concerned from Asset Recovery Department, for write

off, forwarding the full details of approval of the compromise.

11.33. In cases where the borrower makes part remittances towards down payment / installments

and interest suspense in the account got wiped off, resulting in increase in write off amount as

against the terms of sanction, Regional SAMC may permit the Branch concerned to reverse the

amount from the P&L account, as there is no actual write off.

11.34. In cases involving consortium advances, the Bank's decision should be the result of an

independent analysis.

11.35. Release of one or more of the security properties before the full settlement of the liability

may be allowed by the compromise approval committee as part of the compromise process, after

ensuring that value of the remaining securities will be sufficient enough to cover/recover the

remaining amount due to the Bank. Current realizable value of the securities proposed to be

released, amount proposed to be remitted for releasing the securities, current realizable value of

the remaining securities and balance amount due to the Bank after releasing the securities should

be the criteria to be taken into account for release of securities. Title, enforceability, marketability

etc. of the remaining securities should be examined before decisions are taken for release of any

securities. Partial release of securities not as part of compromise settlement of full liability shall be

based on norms prescribed under clause 30 of this document.

11.36. In cases where the same borrower’s different accounts are being considered for

compromise settlement, the sacrifice computation shall be made for each of such accounts

separately and a consolidated position shall be shown in the compromise proposal [C 422].

11.37. Branches/Offices shall seek clarifications from HO/ARD, wherever required, and act upon

on the guidelines issued by ARD, wherever there is scope for different interpretation of any of the

clauses of the compromise rules.

11.38. The Managing Director & CEO shall, if found necessary, amend and approve the

methodology of computing the Notional Settlement Amount by bringing in appropriate changes in

the eligibility score card, computation of minimum amount of interest to be collected and

computation of dues and sacrifice, except in critical factors affecting the value of settlement

amount and the power / authority granted by the Board to approve compromise settlements.

11.39. Compromise settlements approved shall specify a last date for settling the dues by the

borrower. Compromise terms will not be valid thereafter. Branches should send letters to

borrowers withdrawing the compromise offer, immediately after the expiry of settlement date.

11.40. Any request from branches to completely write off the balance outstanding in NPA

accounts, as there is no possibility of recovering any amount thereof, shall be processed and

disposed off, based on the computations worked out in Table 1, Table 2 and Table 3 of the

compromise procedure and the power / authority to approve compromise proposals.

11.41. Amount of write-off and total sacrifice shall be computed based on the ‘Notional

Settlement Amount’ computed for compromise settlement using Table 3 [Annexure III].

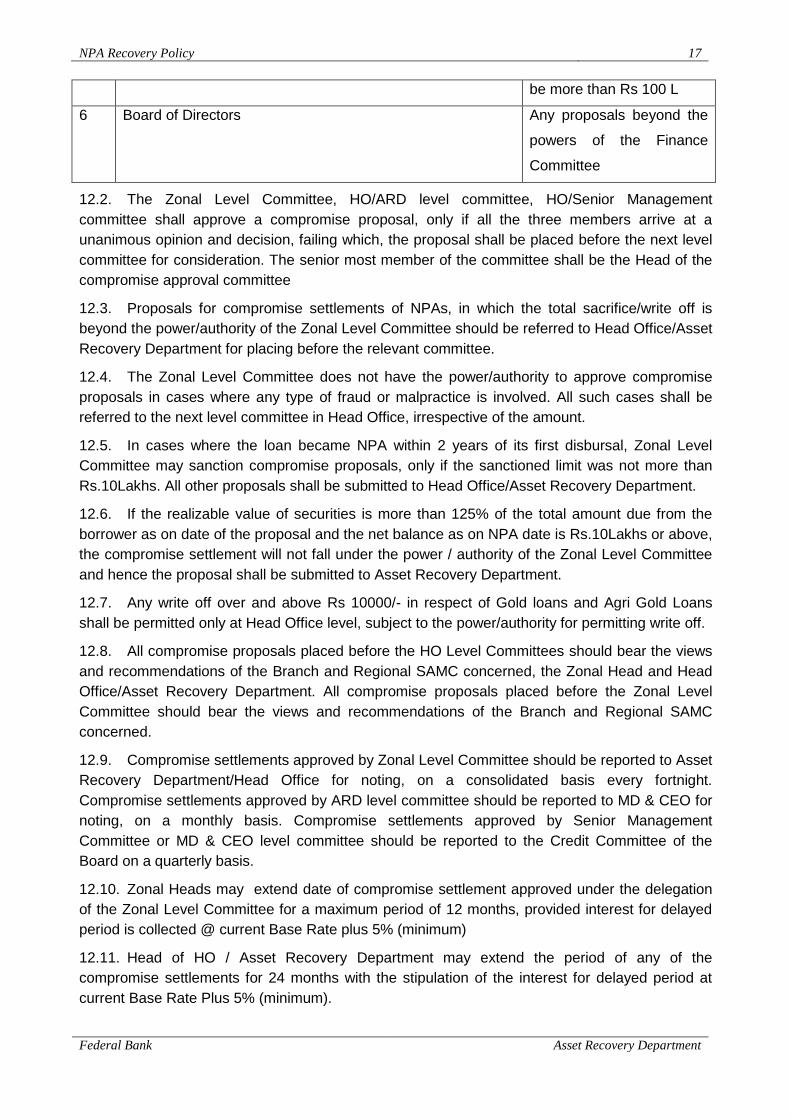

12. Power/Authority to approve compromise settlement of NPAs

NPA Recovery Policy 16

Federal Bank Asset Recovery Department

12.1. The proposals for compromise settlement of NPAs or complete write off of balance due

shall be examined by various committees as per the chart shown below and approval may be

granted, subject to merits of each of the cases.

SL

No

Approval

Committee

Members Total sacrifice on

compromise settlement

as per Table III

1 Zonal level

Committee

1. Zonal Head

2. An Officer of the Zonal Office, not

below the rank of Chief Manager

3. An Officer of the Zonal Office, not

below the rank of Manager (Admn)

Maximum Rs 7.50 L, out of

which write off should not

be more than Rs 1.50 L

2 HO/ARD level

Committee

1. The General Manager & Chief Risk

Officer

2. DGM of Asset Recovery

Department

3. An Executive in HO not below the

rank of DGM(other than ARD) as

nominated by MD& CEO

Maximum Rs 50 L, out of

which write off should not

be more than Rs 10 L

3 HO/Senior

Management

Committee

1. Executive Director

2. The General Manager & Chief Risk

Officer

3. Two of the senior Executives in

DGM cadre or above in Head

Office (other than ARD) as

nominated by the MD & CEO

Quorum - Presence of at least 3 members;

either Executive Director or the General

Manager & Chief Risk Officer shall

essentially be present.

Maximum Rs 150 L, out of

which write off should not

be more than Rs 30 L

4 HO/Managing

Director &

CEO level

committee

1. Managing Director

2. Executive Director

3. The General Manager & Chief risk

Officer

4. One of the senior Executives in

DGM cadre or above in Head

Office (other than ARD) as

nominated by the MD & CEO.

Presence of at least 3 members; if MD &

CEO is not present, post approval

concurrence of MD & CEO should be

obtained.

Maximum Rs 250.00 L, out

of which write off should

not be more than Rs 50 L

5 Credit Committee of the Board Maximum Rs 500 L, out of

which write off should not

NPA Recovery Policy 17

Federal Bank Asset Recovery Department

be more than Rs 100 L

6 Board of Directors Any proposals beyond the

powers of the Finance

Committee

12.2. The Zonal Level Committee, HO/ARD level committee, HO/Senior Management

committee shall approve a compromise proposal, only if all the three members arrive at a

unanimous opinion and decision, failing which, the proposal shall be placed before the next level

committee for consideration. The senior most member of the committee shall be the Head of the

compromise approval committee

12.3. Proposals for compromise settlements of NPAs, in which the total sacrifice/write off is

beyond the power/authority of the Zonal Level Committee should be referred to Head Office/Asset

Recovery Department for placing before the relevant committee.

12.4. The Zonal Level Committee does not have the power/authority to approve compromise

proposals in cases where any type of fraud or malpractice is involved. All such cases shall be

referred to the next level committee in Head Office, irrespective of the amount.

12.5. In cases where the loan became NPA within 2 years of its first disbursal, Zonal Level

Committee may sanction compromise proposals, only if the sanctioned limit was not more than

Rs.10Lakhs. All other proposals shall be submitted to Head Office/Asset Recovery Department.

12.6. If the realizable value of securities is more than 125% of the total amount due from the

borrower as on date of the proposal and the net balance as on NPA date is Rs.10Lakhs or above,

the compromise settlement will not fall under the power / authority of the Zonal Level Committee

and hence the proposal shall be submitted to Asset Recovery Department.

12.7. Any write off over and above Rs 10000/- in respect of Gold loans and Agri Gold Loans

shall be permitted only at Head Office level, subject to the power/authority for permitting write off.

12.8. All compromise proposals placed before the HO Level Committees should bear the views

and recommendations of the Branch and Regional SAMC concerned, the Zonal Head and Head

Office/Asset Recovery Department. All compromise proposals placed before the Zonal Level

Committee should bear the views and recommendations of the Branch and Regional SAMC

concerned.

12.9. Compromise settlements approved by Zonal Level Committee should be reported to Asset

Recovery Department/Head Office for noting, on a consolidated basis every fortnight.

Compromise settlements approved by ARD level committee should be reported to MD & CEO for

noting, on a monthly basis. Compromise settlements approved by Senior Management

Committee or MD & CEO level committee should be reported to the Credit Committee of the

Board on a quarterly basis.

12.10. Zonal Heads may extend date of compromise settlement approved under the delegation

of the Zonal Level Committee for a maximum period of 12 months, provided interest for delayed

period is collected @ current Base Rate plus 5% (minimum)

12.11. Head of HO / Asset Recovery Department may extend the period of any of the

compromise settlements for 24 months with the stipulation of the interest for delayed period at

current Base Rate Plus 5% (minimum).

NPA Recovery Policy 18

Federal Bank Asset Recovery Department

12.12. General Manager in charge of Recovery functions in HO may, on a case to case basis

and depending up on merits, waive interest for delayed period, either fully or partially, for any of

the compromise settlements approved by any of the committees / Board.

12.13. No compromise settlement approved earlier shall be treated as valid on expiry of 24

months from the due date specified earlier. Fresh proposal for settlement shall be worked out,

subject to the norms prevailing as on the date of new proposal.

12.14. If the loan for which compromise settlement is proposed had been originally sanctioned or

last renewed by the Head of the compromise approving committee earlier, in his individual

capacity, the compromise proposal should be submitted to the next level committee for

consideration.

12.15. Power /Authority granted herein above shall be used by the respective authorities most

judiciously. Decisions of the committee shall be fully based on merits; no compromise settlement

shall be approved for the sole reason that it otherwise falls within the powers of the committee,

amount wise.

13. Special Scheme for One Time Settlement [OTS] of small value NPAs

13.1. To reduce the stock of small value NPAs, Asset Recovery Department shall periodically

announce Special Scheme for One Time Settlement of small value NPAs including Technically

Written Off accounts and suit filed/decreed debt /RR initiated accounts, with current net balance

up to and including of Rs.100,000/-. Accounts classified and remained as NPA in the books of the

Bank for a minimum period of 1 year as on the date of proposal for OTS shall be treated as

eligible to be included under such OTS Scheme.

13.2. While announcing the OTS Scheme, the date of commencement and date of expiry of the

Scheme shall be invariably specified. Once the Scheme is announced, Branches shall

immediately identify the eligible borrowers, meet them and persuade them to settle the accounts

through the Scheme.

13.3. Branches shall submit the proposal for OTS in the prescribed format [Annexure V] to the

Regional SAMC concerned.

13.4. Branches shall try to get all accounts eligible under the scheme settled in a phased

manner, without waiting till the expiry of the scheme.

13.5. In the case of suit filed accounts, Branches / Regional SAMCs may seek the assistance of

the respective advocates for effective out of court settlement. In pending suits, wherever possible,

refund of court fee shall also be obtained by recording the compromise.

13.6. Only such accounts in which no fraud is involved or suspected shall be considered for

settlement under this scheme. If the borrower concerned is related to any of the employees of the

Bank, OTS shall not be considered.

13.7. The accounts which come under any debt waiver scheme approved by the Government

shall not be considered for OTS under this scheme. Subsidy, if any, shall not be treated as part of

the compromise amount.

13.8. Accounts in which compromise under any other scheme/policy has been sanctioned

earlier shall not be considered under this Scheme.

NPA Recovery Policy 19

Federal Bank Asset Recovery Department

13.9. Accounts in the names of any of the present or former employees of the Bank or accounts

in which any of the present or former employees of the Bank is co-obligant or guarantor shall not

be considered for compromise under the Scheme.

13.10. Terms of settlement:

Period for which

the account

remained as NPA

Minimum amount for settlement #

Secured Loans Unsecured Loans

1 year and above

up to and including

3 years

80% of the net balance 65 % of the net balance

Above 3 years up

to and including 5

years

70% of the net balance 50% of the net balance

Above 5 years 60% of the net balance 35% of the net balance

# The amount stipulated is the minimum required for OTS. Branches/ SAMCs shall

endeavor to recover the maximum amount for settlement. Net balance means net

balance as on the date of compromise proposal.

13.11. Staff accountability in respect of such accounts shall be considered by the SAMC on the

strength of the particulars available in the OTS format and a serious view needs to be given, only

in respect of cases in which any fraud or malpractices or unethical practices are found to have

been involved or mala fides are suspected. Zonal Heads may take appropriate decisions in all

other cases. Branches need not be advised to submit staff accountability reports separately.

13.12. Zonal Offices shall allow one time settlement of eligible accounts, based on the general

norms prescribed above. A Committee consisting of the Zonal Head and another two officers of

the Zonal Office, one of whom should be an officer not below the rank of Senior Manager, shall

grant sanction for one time settlement of eligible accounts.

13.13. All such cases of OTS allowed by the Zonal Office shall be reported to Asset Recovery

Department at Head Office for noting, on a fortnightly basis. A copy of the OTS proposal cum

Sanction Order should be forwarded to Asset Recovery Department at Head Office.

13.14. Calculations and computations prescribed for compromise settlement of NPAs ( Table

1,2,3 ) need not be done for one time settlement of small value NPAs as covered herein above.

14. One Time Settlement of NPAs in Micro and Small Enterprises Sector.

14.1. In order to extent timely and adequate assistance to potentially viable Micro and Small

Enterprises (MSE) units which have already become sick or are likely to become sick, the Bank

shall announce from time to time, Scheme for One Time Settlement [OTS] of NPAs in Micro and

Small Enterprises Sector, as per the guidelines issued by Reserve Bank of India.

14.2. This shall be a non-discretionary and non-discriminatory scheme, applicable for units

originally classified as Micro or Small Enterprises at the time of granting the credit facility.

NPA Recovery Policy 20

Federal Bank Asset Recovery Department

14.3. Cases of fraud, malfeasance and willful defaults shall not be eligible to be included under

the Scheme.

14.4. The terms of the Scheme shall be as per the guidelines issued by Reserve Bank of India

from time to time.

15. Restructuring of NPAs

15.1. The Bank, for economic or legal reasons relating to the borrower's financial difficulty, may

permit restructuring of Non-Performing Assets classified as 'substandard' and 'doubtful'

categories. Restructuring would normally involve modification of terms of the advances /

securities, which would generally include, among others, alteration of repayment period /

repayable amount/ the amount of installments / rate of interest (due to reasons other than

competitive reasons).

15.2. Accounts of borrowers indulged in frauds and malfeasance shall not be eligible for

restructuring.

15.3. Prior permission from HO / Asset Recovery Department shall be obtained for restructuring

or rescheduling of NPA accounts. After obtaining permission from Asset Recovery Department,

the respective Business Department, Regional Credit Hub or National Credit Hub may process

and take appropriate decisions on the proposal for rescheduling / restructuring.

15.4. Bank shall not restructure accounts with retrospective effect. While a restructuring

proposal is under consideration, the usual asset classification norms would continue to apply. The

process of NPA classification of an asset should not stop merely because restructuring proposal

is under consideration. The asset classification status as on the date of approval of the

restructured package by the competent authority would be relevant to decide the asset

classification status of the account after restructuring / rescheduling / renegotiation.

15.5. Reserve Bank of India guidelines for restructuring of loan accounts shall be strictly

followed while restructuring NPA accounts.

15.6. BIFR cases are not eligible for any types of restructuring without the express approval of

BIFR.

15.7. The Bank shall participate in the CDR Mechanism wherever found appropriate. Wherever

the Bank is the lead institution / major stakeholder, it shall take the responsibility to work out a

preliminary restructuring plan in consultation with other stakeholders and submit to the CDR Cell.

16. Right of Recompense

16.1. The Bank extends concessions, compromise settlements, restructuring, etc to its

borrowers, based on the operating status of the loan account / unit, financial position, income

generation and repayment capacity of the borrower / guarantor, etc. The Bank should incorporate

a ‘Right of Recompense’ clause in the sanction letter and other documents, while approving

concessions, compromise settlements and restructuring, to the effect that when such borrowers /

units turn the corner and rehabilitation is successfully completed, the sacrifices undertaken by the

Bank should be recouped from these borrowers / units out of their future profits/cash accruals.

17. Lok Adalats

NPA Recovery Policy 21

Federal Bank Asset Recovery Department

17.1. Lok Adalat is a legally constituted authority, for resolution of disputes through conciliation.

It functions under the aegis of State, District and Taluk Legal Services Authorities headed by

judges from High Court, District court and senior most Judicial Officer within the Taluk

respectively. Lok Adalats attempt to settle both pending suit filed cases as well as pre litigation

cases. Lok Adalats grant awards, which are treated as decree and can be straight away executed

in a court of law.

17.2. If there is scope for early settlement of NPA accounts by referring to Lok Adalat, the Bank

may file an application before the Secretary of the High Court Legal Services Committee /

Secretary of the District Legal Services Authority / Chairman of the Taluk Legal Services

Committee organizing the Lok Adalat for referring those NPA accounts to the Lok Adalat, in states

where the system is in place.

17.3. In the case of suits pending before court or applications pending before DRT, the Bank

may refer to Lok Adalat by making an application to the court / DRT, wherever applicable and

permissible.

17.4. Settlements arrived at Lok Adalats generally involve granting of concessions. The Bank

shall arrive at a suitable decision in accordance with the terms laid down in this document for

compromise settlements.

17.5. At the time of settlement, lumpsum remittance of the compromise amount shall be

insisted. If, in any case, deferred payment is permitted, such period shall not exceed three years,

with provision for payment of interest for the full period.

17.6. The award made by a Lok Adalat is final and binding on all parties to the dispute, and no

appeal will lie to any court against the award. It shall be ensured that the award is properly drawn.

The details of each item of securities including mortgaged properties, if any, should be drawn as

a separate schedule to the award and charge over the scheduled properties should be specifically

mentioned in the body of the awad. There shall be a default clause in the award enabling the

Bank to recover the entire amount due as on date with interest and cost personally from

borrowers / co-obligants / guarantors and also by sale of the security properties.

17.7. In case the borrowers do not pay within the stipulated period the dues to the Bank in terms

of the compromise recorded in the award of the Lok Adalat, Bank shall file application before the

Court / DRT concerned as per the terms of the default clause therein.

17.8. No court fee is payable for referring any matter or case, including pre litigation matter, to

the Lok Adalat. Where a compromise or settlement is arrived at by a Lok Adalat in a case referred

to it by a Court, the court fee paid in such cases shall be got refunded, wherever applicable.

17.9. In view of the fact that the settlement of accounts through Lok Adalat attracts no litigation

expenses and enables the Bank to realize the dues without much delay, Bank shall make use of

the opportunities for settling maximum number of irregular accounts through Lok Adalats.

17.10. Once the period for settlement as prescribed in the Award expires and the liability is not

settled either fully or partially by the borrower, the Bank shall advise the borrower that the terms

of the Award are no more valid and start recovery actions forthwith, based on the default clause

contained in the Award. The NPA shall not be allowed to be settled based on the expired Award,

with the same terms and conditions or even with interest for delayed period. New compromise

formula shall be arrived at by discussing with the borrower, to the advantage of the Bank or

without extra loss to the Bank.

NPA Recovery Policy 22

Federal Bank Asset Recovery Department

18. SARFAESI Act Proceedings

18.1. The Bank shall initiate the provisions of Enforcement of Security Interest under SARFAESI

Act 2002 in all applicable cases immediately after an account is classified as NPA.

18.2. As and when any secured loan account, where the provisions of SARFAESI Act 2002 are

applicable, is classified in the books of the Bank as NPA, the Bank shall require the borrower by

notice in writing (as per Sec 13(2) of the Act) to discharge in full the borrower’s liabilities to the

Bank within sixty days from the date of notice and advise that the Bank would otherwise be

entitled to exercise all or any of the following rights under section 13(4) of the Act:

a. Take possession of the secured assets of the borrower including right to transfer by way

of lease, assignment or sale for realising the secured asset;

b. Take over the management of the business of the borrower including the right to transfer

by way of lease, assignment or sale for realising the secured asset;

c. Appoint any person to manage the secured assets the possession of which has been

taken over by the Bank;

d. Require at anytime by notice in writing, any person who has acquired any of the secured

assets from the borrower and from whom any money is due or may become due to the

borrower, to pay the Bank, so much of the money as is sufficient to pay the secured debt.

18.3. The right to transfer by way of lease, assignment or sale shall be exercised only where the

substantial part of the business of the borrower is held as security for the debt. Where the

management of the whole of the business or part of the business is severable, the Bank may take

over the management of such business of the borrower which is relatable to the security or loan.

18.4. The notice issued under section 13(2) of the Act shall give the details of the amount

payable by the borrower and the secured assets intended to be enforced by the Bank in the event

of non-payment of the loan by the borrower. If on the receipt of the notice, the borrower makes

any representation or raises any objection and if the Bank comes to the conclusion that such

representation is not acceptable or tenable the Bank shall communicate within 15 days of receipt

of such representation or objection the reasons for non-acceptance of the representation or

objection to the borrower.

18.5. Where any action has been taken by the Bank against the borrower under provisions of

section 13(4) of the Act as mentioned above, all costs, charges and expenses properly incurred

by the Bank or any expenses incidental thereto, shall be recoverable from the borrower. Any

amount received by the Bank towards the accounts of the borrower shall, in the absence of any

contract to the contrary, be applied firstly, in payment of such costs, charges and expenses and

secondly, in discharge of the dues of the Bank and the residual amount shall be paid to the

person entitled thereto in accordance with his rights and interests.

18.6. If the dues of the Bank together with all costs, charges and expenses are tendered to the

Bank at any time before the date fixed for sale or transfer, the secured asset shall not be sold or

transferred by the Bank, and no further steps shall be taken by the Bank for transfer or sale of

that secured asset.

NPA Recovery Policy 23

Federal Bank Asset Recovery Department

18.7. Where the dues to the Bank are not fully satisfied with the sale proceeds of the secured

assets, the Bank may file an application to the Debts Recovery Tribunal having jurisdiction or a

competent court, as the case may be, for the recovery of the balance amount from the borrower.

18.8. The Bank may proceed against the borrowers / guarantors or sell the pledged assets

without taking any measures under section 13(4) of SARFAESI Act in relation to the secured

assets under this act.

18.9. The rights of the Bank under this act shall be exercised by the Officers of the Bank in the

rank of Chief Manager or above authorized in this behalf by the Bank.

18.10. Where the possession of any secured asset is required to be taken by the Bank or if any

of the secured asset is required to be sold or transferred by the Bank under the provisions of

SARFAESI Act 2002, the Bank may for the purpose of taking possession or control of any such

secured asset, if required, request in writing, the Chief Metropolitan Magistrate or the District

Magistrate within whose jurisdiction any such secured asset or other documents relating thereto

may be situated or found, to take possession thereof.

18.11. When the management of business of borrower is taken over by the Bank, the Bank may,

by publishing a notice in a newspaper published in English and in a newspaper published in an

Indian Language in circulation in place where the principal office of the borrower is situated,

appoint as many persons as it thinks fit to be directors of that borrower, if the borrower is a

company as defined in the Companies Act, 1956; or to be the administrator of the business of the

borrower, in any other case.

18.12. For initiating actions under SARFAESI Act, in all eligible and applicable NPA accounts

including suit filed, pending/decreed accounts, branches need not obtain permission from higher

authorities. However, the proceedings under the Act can be initiated only by an Authorised

Officer, not below the rank of Chief Manager. Branches where Principal Officer is below the rank

of Chief Manager shall get the assistance / guidance from the respective SAMC, Regional Office

or Asset Recovery Branch for initiating SARFAESI Act proceedings.

18.13. In case a successful bidder, in an auction conducted under SARFAESI proceedings,

approaches the Bank for time beyond the permissible period to remit the balance portion of the

bid amount, the Bank may selectively permit so, at its absolute discretion, provided, the bidder

agrees to pay interest for the period of delay. No extension of time to remit the initial amount (first

part of the bid amount) shall be granted under any circumstances. Authority to permit extension of

time to remit the second part of the bid amount or any portion thereof shall be as follows:

Authority Extension of time

(a) Zonal Head Full settlement within 3 months from the date of

auction, with interest for delayed period at

Bank’s current Base Rate + 5%

(b) Head of Asset Recovery Department Full settlement after 3 months but before 12

months from the date of auction, with interest for

delayed period at rate not less than Bank’s

current Base Rate + 5%

(c) General Manager in charge of Asset Any other cases not coming under (a) or (b)

NPA Recovery Policy 24

Federal Bank Asset Recovery Department

Recovery function / Chief Risk Officer above.

18.14. The Bank through any of its officers so authorized is entitled to bid the immovable property

at any subsequent sale under SARFAESI, where the sale of the property has been postponed for

want of a bid, for an amount not less than the reserve price.

19. Debt Recovery Tribunals and Appellate Tribunals

19.1. For recovery of loans involving Rs.10Lakhs or more, the Bank shall submit to the Debt

Recovery Tribunal (DRT) of competent jurisdiction in the prescribed form and manner as

stipulated in the Recovery of Debts Due to Banks and Financial Institutions Act, 1993 and DRT

(Procedure) Rules, 1993.

19.2. Accounts for which suit is to be filed before the DRT at places where the Bank has Asset

Recovery Branches shall be transferred to the respective Asset Recovery Branch with the

permission of Asset Recovery Department at Head Office. Asset Recovery Branch may conduct

the case directly through Bank’s Legal Officers or entrust to panel Advocate having regular

practice at the place where the Tribunal is functioning in consultation with SAMC and HO / Asset

Recovery Department.

19.3. New cases to be filed before DRT situated at places where the Bank does not have Asset

Recovery Branch may be entrusted with a panel Advocate having regular practice at the place

where the Tribunal is functioning in consultation with SAMC and HO / Asset Recovery

Department.

19.4. The primary responsibility for the follow up of matters transferred to or filed before the

DRT will be with the Asset Recovery Branch and in the absence of Asset Recovery Branch , with

the respective branch where the account is maintained. The branch shall report progress /

position of the cases pending before the DRT / Appellate Tribunal to Asset Recovery Department

under copy to SAMC.

19.5. Asset Recovery Department at Head Office shall issue necessary administrative

guidelines to Asset Recovery Branches / Other Branches about conducting of suits before the

DRTs, from time to time.

20. Recovery Camps

20.1. After completing review of NPAs every quarter, the Regional Head concerned, with the

support of SAMC and in consultation with the Zonal Head shall organize and conduct Recovery

Camps at selected branches to mobilize recovery. Recovery camps may be conducted at

individual branches or a cluster of branches depending on the number of accounts. Principal

Officers of branches participating in the camp along with Officers from SAMC and Regional Office

shall attend the camp.

20.2. During quarterly review of NPA accounts, branches shall identify borrowers to be called

for recovery camps and educate them about the benefits of settling the accounts through the

recovery camps.

20.3. All NPA accounts are eligible to be brought in to the camps, irrespective of the amount

involved and nature of NPA / activity.

NPA Recovery Policy 25

Federal Bank Asset Recovery Department

20.4. In principle compromise agreement may be reached at in the camps, which shall be taken

up with the respective Committee immediately for approval.

20.5. Zonal Offices shall supervise the timely conduct of recovery camps.

21. Recovery through legal action

21.1. Recovery through legal action is an expensive and time-consuming process. The Bank

should resort to legal recourse, only after exhausting all other remedies available for getting the

accounts settled.

21.2. Before initiating legal action for recovery of the amount due under the irregular loan

accounts, it shall be ensured that the loan documents such as DPN, Agreements, Balance

confirmations/acknowledgements, letter of request confirming creation of EM etc. available are

properly filled in and executed by the parties concerned.

21.3. The appropriate legal action for enforcement of loan documents and security charges for

recovery of dues shall be initiated before the expiry of the period prescribed under the law of

limitation. The Limitation Act prescribes the period within which rights can be enforced through a

Court of Law.

21.4. Application for permission to initiate legal action shall be submitted in the format C.145 to

the authority empowered to grant permission through Regional SAMC concerned.