Embed Size (px)

Citation preview

Target Publications Pvt. Ltd. Chapter 03: Reconstitution of Partnership (Admission of Partner)

1

03 Reconstitution of partnership(admission of partner)

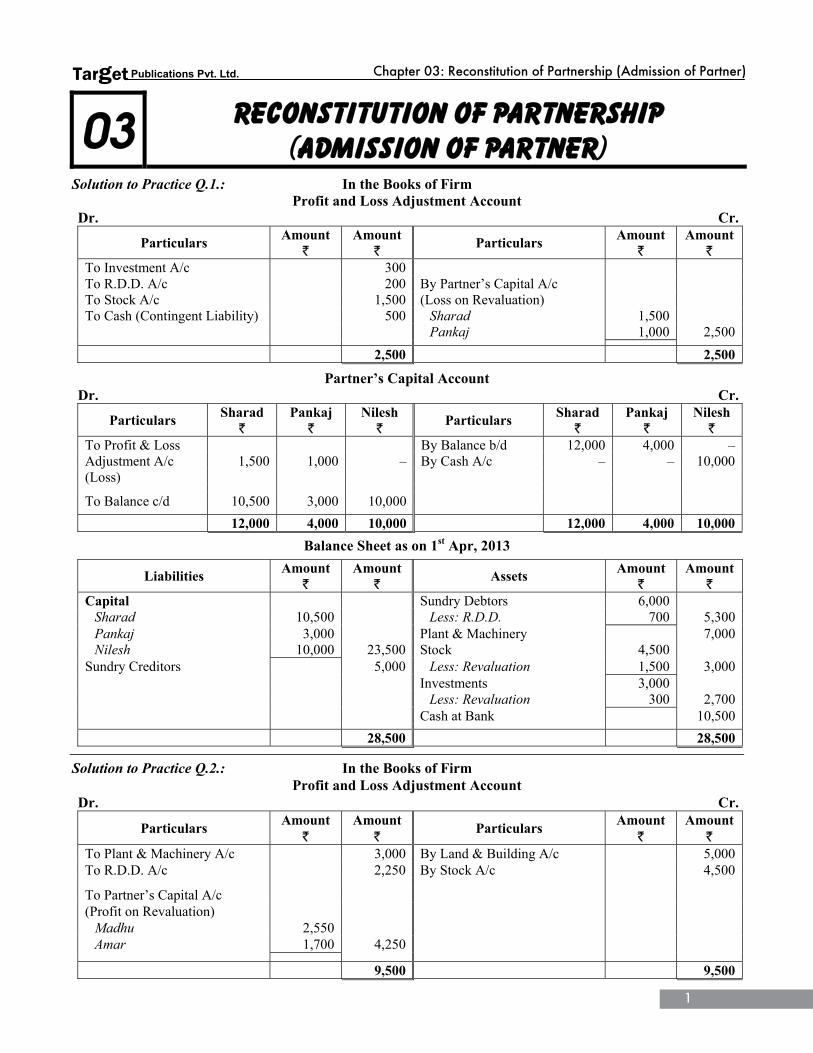

Solution to Practice Q.1.: In the Books of Firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Investment A/c 300 To R.D.D. A/c 200 By Partner’s Capital A/c To Stock A/c 1,500 (Loss on Revaluation) To Cash (Contingent Liability) 500 Sharad 1,500 Pankaj 1,000 2,500 2,500 2,500

Partner’s Capital Account Dr. Cr.

Particulars Sharad `

Pankaj `

Nilesh `

Particulars Sharad `

Pankaj `

Nilesh `

To Profit & Loss By Balance b/d 12,000 4,000 –Adjustment A/c 1,500 1,000 – By Cash A/c – – 10,000(Loss) To Balance c/d 10,500 3,000 10,000

12,000 4,000 10,000 12,000 4,000 10,000 Balance Sheet as on 1st Apr, 2013

Liabilities Amount `

Amount `

Assets Amount `

Amount `

Capital Sundry Debtors 6,000Sharad 10,500 Less: R.D.D. 700 5,300Pankaj 3,000 Plant & Machinery 7,000Nilesh 10,000 23,500 Stock 4,500

Sundry Creditors 5,000 Less: Revaluation 1,500 3,000 Investments 3,000

Less: Revaluation 300 2,700 Cash at Bank 10,500

28,500 28,500 Solution to Practice Q.2.: In the Books of Firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Plant & Machinery A/c 3,000 By Land & Building A/c 5,000To R.D.D. A/c 2,250 By Stock A/c 4,500 To Partner’s Capital A/c (Profit on Revaluation)

Madhu 2,550 Amar 1,700 4,250

9,500 9,500

2

Target Publications Pvt. Ltd. Std. XII (Commerce): Book-Keeping & Accountancy

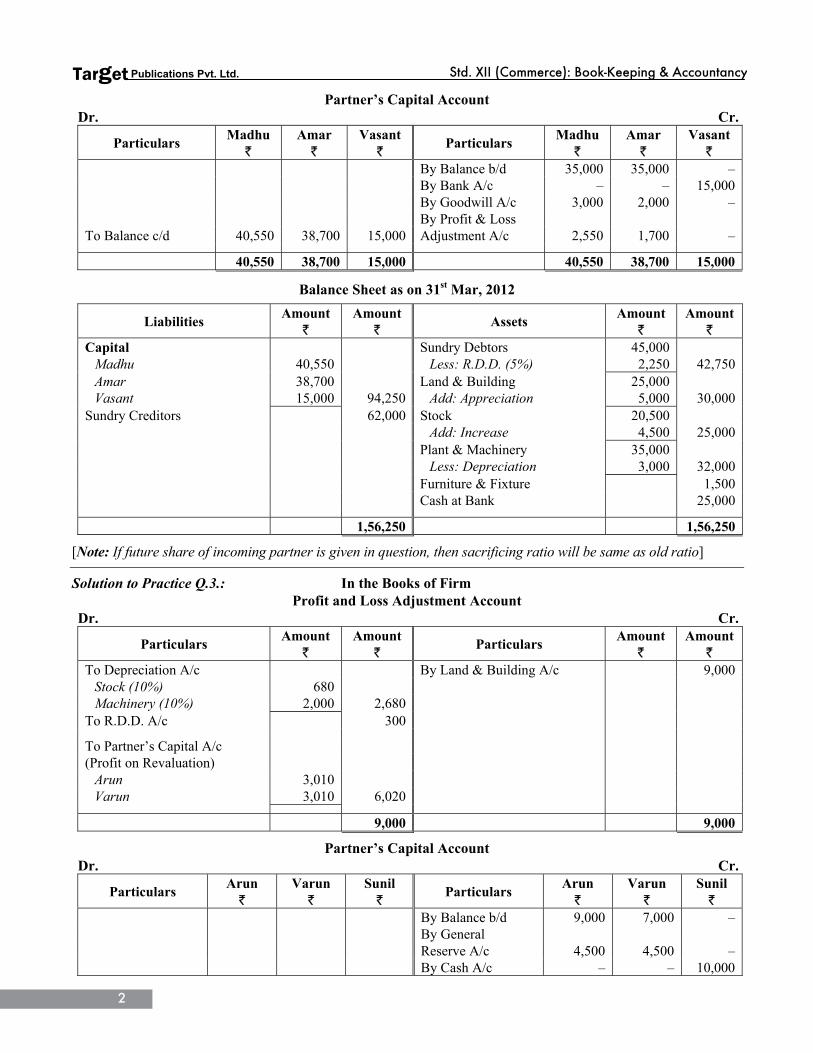

Partner’s Capital Account Dr. Cr.

Particulars Madhu `

Amar `

Vasant `

Particulars Madhu `

Amar `

Vasant `

By Balance b/d 35,000 35,000 – By Bank A/c – – 15,000 By Goodwill A/c 3,000 2,000 – By Profit & Loss To Balance c/d 40,550 38,700 15,000 Adjustment A/c 2,550 1,700 –

40,550 38,700 15,000 40,550 38,700 15,000

Balance Sheet as on 31st Mar, 2012 Liabilities Amount

` Amount

` Assets Amount

` Amount

`Capital Sundry Debtors 45,000

Madhu 40,550 Less: R.D.D. (5%) 2,250 42,750Amar 38,700 Land & Building 25,000Vasant 15,000 94,250 Add: Appreciation 5,000 30,000

Sundry Creditors 62,000 Stock 20,500 Add: Increase 4,500 25,000

Plant & Machinery 35,000 Less: Depreciation 3,000 32,000 Furniture & Fixture 1,500 Cash at Bank 25,000

1,56,250 1,56,250

[Note: If future share of incoming partner is given in question, then sacrificing ratio will be same as old ratio] Solution to Practice Q.3.: In the Books of Firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Depreciation A/c By Land & Building A/c 9,000Stock (10%) 680 Machinery (10%) 2,000 2,680

To R.D.D. A/c 300 To Partner’s Capital A/c (Profit on Revaluation)

Arun 3,010 Varun 3,010 6,020

9,000 9,000

Partner’s Capital Account Dr. Cr.

Particulars Arun `

Varun `

Sunil `

Particulars Arun `

Varun `

Sunil `

By Balance b/d 9,000 7,000 – By General Reserve A/c 4,500 4,500 – By Cash A/c – – 10,000

Target Publications Pvt. Ltd. Chapter 03: Reconstitution of Partnership (Admission of Partner)

3

By Goodwill A/c 4,000 4,000 – By Profit & Loss To Balance c/d 20,510 18,510 10,000 Adjustment A/c 3,010 3,010 –

20,510 18,510 10,000 20,510 18,510 10,000 Cash Account

Dr. Cr.

Particulars Amount `

Particulars Amount `

To Balance b/d 2,500 To Sunil’s Capital A/c 10,000 To Goodwill A/c 8,000 By Balance c/d 20,500 20,500 20,500

Goodwill Account Dr. Cr.

Particulars Amount `

Particulars Amount `

To Arun’s Capital A/c 4,000 By Cash A/c 8,000To Varun’s Capital A/c 4,000 8,000 8,000

Balance Sheet as on 1st Apr, 2012 Liabilities Amount

` Amount

` Assets Amount

` Amount

`Capital Stock 6,800

Arun 20,510 Less: Depreciation (10%) 680 6,120Varun 18,510 Motor Van 4,200Sunil 10,000 49,020 Machinery 8,000

Sundry Creditors 21,000 Less: Depreciation (10%) 2,000 6,000Bills Payable 8,500 Land & Building 20,000

Add: Appreciation 9,000 29,000 Furniture 7,000 Sundry Debtor 6,000

Less: R.D.D.(5%) 300 5,700 Cash in Hand 20,500 78,520 78,520

[Note: If future share of incoming partner is given in question, then sacrificing ratio will be same as old ratio.] Solution to Practice Q.4.: In the Books of firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To R.D.D. A/c 1,000 By Machinery A/c 13,333To Building A/c 3,667 To Partner’s Capital A/c (Profit on Revaluation)

Ramesh 6,500 Suresh 2,166 8,666

13,333 13,333

4

Target Publications Pvt. Ltd. Std. XII (Commerce): Book-Keeping & Accountancy

Partner’s Capital Account Dr. Cr.

Particulars Ramesh `

Suresh `

Mahesh `

Particulars Ramesh `

Suresh `

Mahesh `

By Balance b/d 40,000 20,000 –To Balance c/d 40,000 20,000 15,000 By Cash A/c – – 15,000

40,000 20,000 15,000 40,000 20,000 15,000

Partner’s Current Account Dr. Cr.

Particulars Ramesh `

Suresh `

Particulars Ramesh `

Suresh `

To Profit & Loss A/c 9,000 3,000 By Balance b/d 4,000 6,000 By General Reserve A/c 5,250 1,750 By Profit & Loss Adjustment A/c 6,500 2,166To Balance c/d 12,750 8,916 By Goodwill A/c 6,000 2,000

21,750 11,916 21,750 11,916

Cash Account Dr. Cr.

Particulars Amount `

Particulars Amount `

To Balance b/d 9,000 To Mahesh’s Capital A/c 15,000 To Goodwill A/c 8,000 By Balance c/d 32,000 32,000 32,000

Balance Sheet as on 1st Apr, 2012

Liabilities Amount `

Amount `

Assets Amount `

Amount `

Capital Stock 8,000Ramesh 40,000 Machinery 20,000Suresh 20,000 Add: Revaluation 13,333 33,333Mahesh 15,000 75,000 Land & Building 22,000

Sundry Creditors 12,000 Less: Revaluation 3,667 18,333Current A/c Sundry Debtors 18,000

Ramesh 12,750 Less: R.D.D. 1,000 17,000Suresh 8,916 21,666 Cash 32,000

1,08,666 1,08,666

Solution to Practice Q.5.: In the Books of Firm Profit and Loss Adjustment Account

Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Plant & Machinery A/c 1,000 By Sundry Creditor A/c 800To Stock A/c 300 To Bills Receivable A/c 500 By Partner’s Capital A/c (Loss on Revaluation) Manoj 500 Sunil 500 1,000 1,800 1,800

Target Publications Pvt. Ltd. Chapter 03: Reconstitution of Partnership (Admission of Partner)

5

Partner’s Capital Account Dr. Cr.

Particulars Manoj `

Sunil `

Raj `

Particulars Manoj `

Sunil `

Raj `

To Bills Receivable A/c 6,500 – – By Balance b/d 30,000 20,000 –To Profit & Loss By General Reserve A/c Adjustment A/c 500 500 – By Cash A/c – – 8,000 By Goodwill A/c 3,500 3,500 –To Balance c/d 31,000 27,500 8,000

38,000 28,000 8,000 38,000 28,000 8,000 Cash Account

Dr. Cr.

Particulars Amount `

Particulars Amount `

To Balance b/d 7,000 To Raj’s Capital A/c 8,000 To Goodwill A/c 7,000 By Balance c/d 22,000 22,000 22,000

Goodwill Account Dr. Cr.

Particulars Amount `

Particulars Amount `

To Manoj’s Capital A/c 3,500 By Cash A/c 7,000To Sunil’s Capital A/c 3,500 7,000 7,000

Balance Sheet as on 1st Apr, 2012 Liabilities Amount

` Amount

` Assets Amount

` Amount

`Capital Plant & Machinery 24,000

Manoj 31,000 Less: Revaluation 1,000 23,000Sunil 27,500 Stock 14,000Raj 8,000 66,500 Less: Revaluation 300 13,700

Sundry Creditors 4,000 Furniture 10,000Less: Written Off 20% 800 3,200 Sundry Debtors 8,000

Bills Payable 7,000 Cash 22,000 76,700 76,700

[Note: If future share of incoming partner is given in question, then sacrificing ratio will be same as old ratio] Solution to Practice Q.6.: In the Books of Firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Equipments A/c 5,000 By R.D.D. A/c 5,500 By Premises A/c 9,500To Partner’s Capital A/c By Creditors A/c 1,000(Profit on Revaluation)

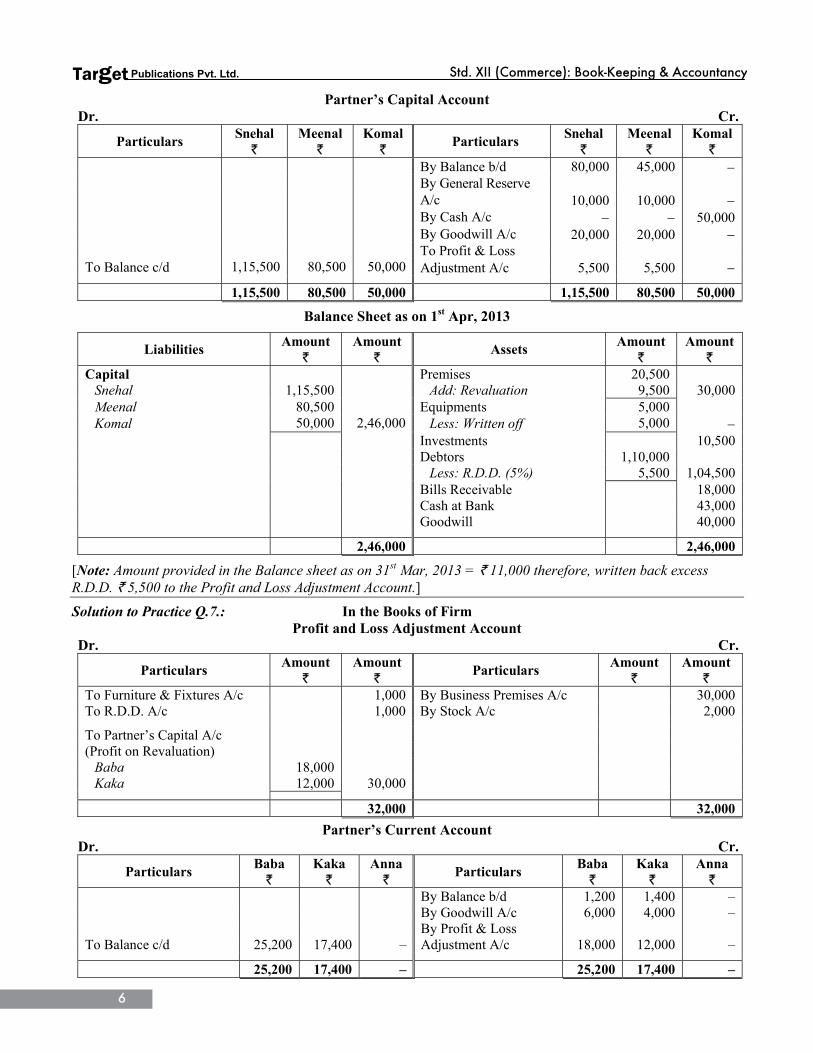

Snehal 5,500 Meenal 5,500 11,000

16,000 16,000

6

Target Publications Pvt. Ltd. Std. XII (Commerce): Book-Keeping & Accountancy

Partner’s Capital Account Dr. Cr.

Particulars Snehal `

Meenal `

Komal `

Particulars Snehal `

Meenal `

Komal `

By Balance b/d 80,000 45,000 − By General Reserve A/c 10,000 10,000 − By Cash A/c − − 50,000 By Goodwill A/c 20,000 20,000 − To Profit & Loss To Balance c/d 1,15,500 80,500 50,000 Adjustment A/c 5,500 5,500 −

1,15,500 80,500 50,000 1,15,500 80,500 50,000 Balance Sheet as on 1st Apr, 2013

Liabilities Amount `

Amount `

Assets Amount `

Amount `

Capital Premises 20,500Snehal 1,15,500 Add: Revaluation 9,500 30,000Meenal 80,500 Equipments 5,000Komal 50,000 2,46,000 Less: Written off 5,000 −

Investments 10,500 Debtors 1,10,000 Less: R.D.D. (5%) 5,500 1,04,500 Bills Receivable 18,000 Cash at Bank 43,000 Goodwill 40,000 2,46,000 2,46,000

[Note: Amount provided in the Balance sheet as on 31st Mar, 2013 = ` 11,000 therefore, written back excess R.D.D. ` 5,500 to the Profit and Loss Adjustment Account.] Solution to Practice Q.7.: In the Books of Firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Furniture & Fixtures A/c 1,000 By Business Premises A/c 30,000To R.D.D. A/c 1,000 By Stock A/c 2,000 To Partner’s Capital A/c (Profit on Revaluation)

Baba 18,000 Kaka 12,000 30,000

32,000 32,000

Partner’s Current Account Dr. Cr.

Particulars Baba `

Kaka `

Anna `

Particulars Baba `

Kaka `

Anna `

By Balance b/d 1,200 1,400 – By Goodwill A/c 6,000 4,000 – By Profit & Loss To Balance c/d 25,200 17,400 – Adjustment A/c 18,000 12,000 –

25,200 17,400 – 25,200 17,400 –

Target Publications Pvt. Ltd. Chapter 03: Reconstitution of Partnership (Admission of Partner)

7

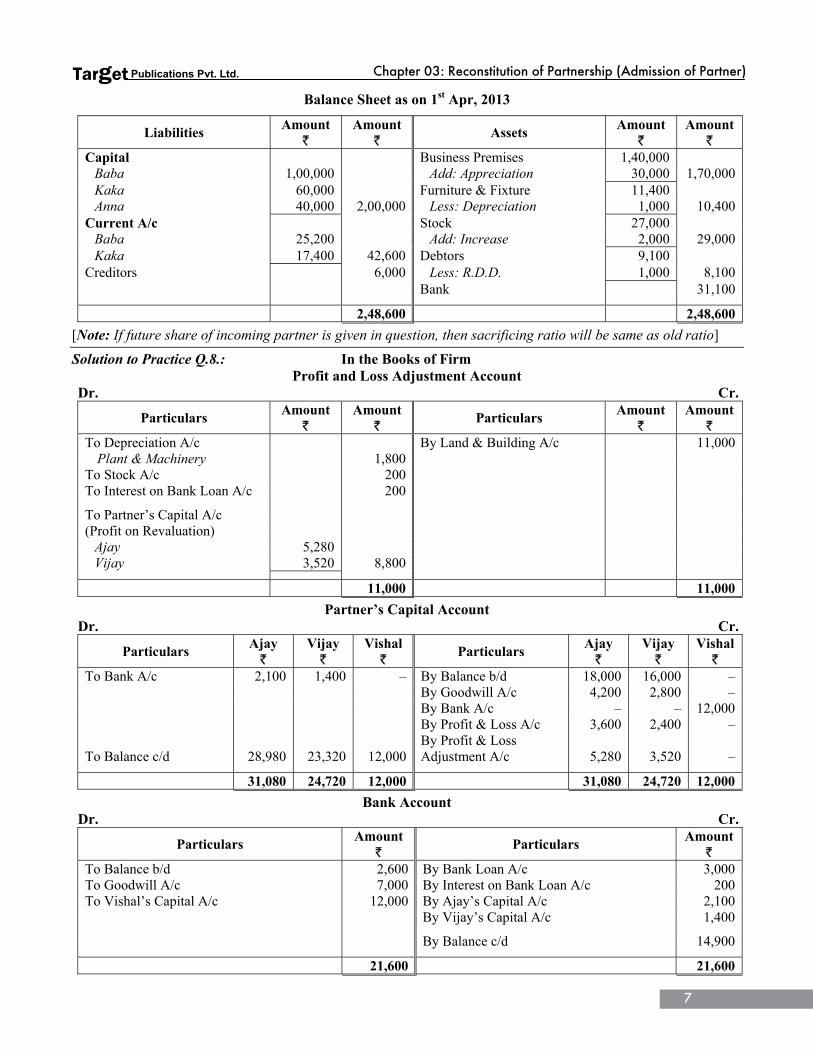

Balance Sheet as on 1st Apr, 2013 Liabilities Amount

` Amount

` Assets Amount

` Amount

`Capital Business Premises 1,40,000

Baba 1,00,000 Add: Appreciation 30,000 1,70,000Kaka 60,000 Furniture & Fixture 11,400Anna 40,000 2,00,000 Less: Depreciation 1,000 10,400

Current A/c Stock 27,000Baba 25,200 Add: Increase 2,000 29,000Kaka 17,400 42,600 Debtors 9,100

Creditors 6,000 Less: R.D.D. 1,000 8,100 Bank 31,100

2,48,600 2,48,600

[Note: If future share of incoming partner is given in question, then sacrificing ratio will be same as old ratio] Solution to Practice Q.8.: In the Books of Firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Depreciation A/c By Land & Building A/c 11,000 Plant & Machinery 1,800 To Stock A/c 200 To Interest on Bank Loan A/c 200 To Partner’s Capital A/c (Profit on Revaluation)

Ajay 5,280 Vijay 3,520 8,800

11,000 11,000

Partner’s Capital Account Dr. Cr.

Particulars Ajay `

Vijay `

Vishal `

Particulars Ajay `

Vijay `

Vishal `

To Bank A/c 2,100 1,400 – By Balance b/d 18,000 16,000 – By Goodwill A/c 4,200 2,800 – By Bank A/c – – 12,000 By Profit & Loss A/c 3,600 2,400 – By Profit & Loss To Balance c/d 28,980 23,320 12,000 Adjustment A/c 5,280 3,520 –

31,080 24,720 12,000 31,080 24,720 12,000 Bank Account

Dr. Cr.

Particulars Amount `

Particulars Amount `

To Balance b/d 2,600 By Bank Loan A/c 3,000To Goodwill A/c 7,000 By Interest on Bank Loan A/c 200To Vishal’s Capital A/c 12,000 By Ajay’s Capital A/c 2,100 By Vijay’s Capital A/c 1,400 By Balance c/d 14,900 21,600 21,600

8

Target Publications Pvt. Ltd. Std. XII (Commerce): Book-Keeping & Accountancy

Goodwill Account Dr. Cr.

Particulars Amount `

Particulars Amount `

To Ajay’s Capital A/c 4,200 By Bank A/c 7,000To Vijay’s Capital A/c 2,800 7,000 7,000

Balance Sheet as on 1st Apr, 2012

Liabilities Amount

` Amount

` Assets Amount

` Amount

`Capital Plant & Machinery 18,000

Ajay 28,980 Less: Depreciation (10%) 1,800 16,200Vijay 23,320 Stock 4,000Vishal 12,000 64,300 Less: Revaluation 200 3,800

Sundry Creditors 7,000 Land & Building 16,000Bills Payable 4,000 Add: Revaluation 11,000 27,000

Debtor 10,000 Bills Receivable 3,400 Bank 14,900 75,300 75,300

[Note: If future share of incoming partner is given in question, then sacrificing ratio will be same as old ratio] Solution to Practice Q.9.: In the Books of Firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Stock A/c 3,500 By Building A/c 4,350To R.D.D. A/c 4,000 By Creditors A/c 502To Claim for Damages 1,000 By Partner’s Capital A/c (Loss on Revaluation) Ram 912 Shyam 1,368 Bharat 1,368 3,648 8,500 8,500

Partner’s Capital Account

Dr. Cr.

Particulars Ram `

Shyam `

Bharat`

Laxman`

Particulars Ram `

Shyam `

Bharat`

Laxman`

To Goodwill A/c 7,500 11,250 11,250 10,000 By Balance b/d 20,000 27,000 30,000 –To Profit & Loss By General Adjustment A/c 912 1,368 1,368 – Reserve A/c 4,000 6,000 6,000 – By Bank A/c – – – 25,000To Balance c/d 25,588 35,382 38,382 15,000 By Goodwill A/c 10,000 15,000 15,000 –

34,000 48,000 51,000 25,000 34,000 48,000 51,000 25,000

Target Publications Pvt. Ltd. Chapter 03: Reconstitution of Partnership (Admission of Partner)

9

Bank Account Dr. Cr.

Particulars Amount `

Particulars Amount `

To Balance b/d 22,000 To Laxman’s Capital A/c 25,000 By Balance c/d 47,000 47,000 47,000

Goodwill Account

Dr. Cr.

Particulars Amount `

Particulars Amount `

To Ram’s Capital A/c 10,000 By Ram’s Capital A/c 7,500To Shyam’s Capital A/c 15,000 By Shyam’s Capital A/c 11,250To Bharat’s Capital A/c 15,000 By Bharat’s Capital A/c 11,250 By Laxman’s Capital A/c 10,000 40,000 40,000

Balance Sheet as on 1st Apr, 2013

Liabilities Amount `

Amount `

Assets Amount `

Amount `

Capital A/c Bills Receivable 4,500Ram 25,588 Trade Debtors 60,000Shyam 35,382 Less: New R.D.D. 4,000 56,000Bharat 38,382 Stock in Trade 35,000Laxman 15,000 1,14,352 Less: Depreciation (10%) 3,500 31,500

Bills Payable 10,000 Furniture 2,000Trade Creditors 30,000 Building 29,000

Less: Decrease 502 29,498 Add: Appreciation (15%) 4,350 33,350Loan from ‘Usha’ 20,000 Cash in Hand 500Claim for Damages 1,000 Cash at Bank 47,000 1,74,850 1,74,850

Solution to Practice Q.10.: In the books of Firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Plant & Machinery A/c 4,000 By Land & Building A/c 7,000To Provision for Doubtful By Stock A/C 1,000Debts A/c 700 To Furniture & Fixtures A/c 1,000 To Partner’s Capital A/c (Profit on Revaluation) Santosh 1,380 Ritu 920 2,300 8,000 8,000

10

Target Publications Pvt. Ltd. Std. XII (Commerce): Book-Keeping & Accountancy

Partner’s Capital Account Dr. Cr.

Particulars Santosh

` Ritu

`

Mitali `

Particulars Santosh

` Ritu

`

Mitali `

To Bank A/c 3,000 2,000 – By balance b/d 32,000 22,000 – By General Reserve A/c 7,200 4,800 – By Goodwill A/C 6,000 4,000 – By Bank A/C – – 12,000 By Profit & Loss To Balance c/d 43,580 29,720 12,000 Adjustment A/c 1,380 920 –

46,580 31,720 12,000 46,580 31,720 12,000

Balance Sheet as on 1st Apr, 2012

Liabilities Amount

`

Amount `

Assets Amount

` Amount

` Sundry Creditors 10,000 Cash at Bank 35,000Capital Sundry Debtors 7,000 Santosh 43,580 Less: R.D.D. 700 6,300 Ritu 29,720 Land & Building 25,000 Mitali 12,000 85,300 Add: Revaluation 7,000 32,000 Stock 11,000 Add: Revaluation 1,000 12,000 Plant & Machinery 12,000 Less: Revaluation 4,000 8,000 Furniture & Fixtures 3,000 Less: Revaluation 1,000 2,000 95,300 95,300

Solution to Practice Q.11.: In the Books of Firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount

`

Amount `

Particulars Amount

` Amount

` To Outstanding Legal By Land & Building A/c 1,900 Expenses A/c 650 To Reserve for doubtful debts A/c 1,000 To Plant & Machinery A/c 4,500 By Partner's Capital A/c (Loss on revaluation) Raman 2,550 Naman 1,700 4,250 6,150 6,150

Target Publications Pvt. Ltd. Chapter 03: Reconstitution of Partnership (Admission of Partner)

11

Partner’s Capital Account Dr. Cr.

Particulars Raman `

Naman `

Shaman`

Particulars Raman `

Naman `

Shaman `

To Goodwill A/c 7,200 4,800 3,000 By Balance b/d 50,000 40,000 –To Profit & Loss By General Reserve Adjustment A/c 2,550 1,700 – A/c 2,400 1,600 – By Profit & Loss A/c 3,600 2,400 – By Cash A/c – – 60,000 To Balance c/d 55,250 43,500 57,000 By Goodwill A/c 9,000 6,000 –

65,000 50,000 60,000 65,000 50,000 60,000

Balance Sheet as on 1st Apr, 2012 Liabilities Amount

` Amount

` Assets Amount

` Amount

`Creditors 34,000 Land & Building 38,000Bills Payable 20,000 Add: Appreciation 1,900 39,900Outstanding Legal Expenses 650 Plant & Machinery 30,000Capital Less: Depreciation 4,500 25,500 Raman 55,250 Sundry Debtors 40,000 Naman 43,500 Less: Reserve for Doubtful Shaman 57,000 1,55,750 Debts 1,000 39,000 Closing Stock 26,000 Cash in Hand 80,000 2,10,400 2,10,400

Solution to Practice Q.12.: In the Books of Firm Profit and Loss Adjustment Account

Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Depreciation A/c By Building A/c 4,000Stock (5%) 350 By R.D.D. A/c 1,000Plant & Machinery (5%) 900 1,250 By Creditor A/c 1,000

To Interest on Bank Loan 350 To Partner’s Capital A/c (Profit on Revaluation)

Suryakant 2,200 Chandrakant 2,200 4,400

6,000 6,000

Partner’s Capital Account Dr. Cr.

Particulars Suryakant `

Chandrakant `

Tarachand`

Particulars Suryakant `

Chandrakant`

Tarachand`

By Balance b/d 18,000 22,000 –

By General Reserve A/c 6,000 6,000 –

By Cash A/c – – 12,000 By Goodwill 3,000 3,000 – A/c

12

Target Publications Pvt. Ltd. Std. XII (Commerce): Book-Keeping & Accountancy

By Bank Loan A/c – 6,350 –

By Profit & Loss To Balance c/d 29,200 39,550 12,000 Adjustment A/c 2,200 2,200 – 29,200 39,550 12,000 29,200 39,550 12,000

Cash Account Dr. Cr.

Particulars Amount `

Particulars Amount `

To Balance b/d 3,000 To Tarachand’s Capital A/c 12,000 By Balance c/d 15,000 15,000 15,000

Goodwill Account Dr. Cr.

Particulars Amount `

Particulars Amount `

To Suryakant’s Capital A/c 3,000 To Chandrakant’s Capital A/c 3,000 By Balance c/d 6,000 6,000 6,000

Balance Sheet as on 1st Apr, 2012

Liabilities Amount `

Amount `

Assets Amount `

Amount `

Capital Building 20,000Suryakant 29,200 Add: Appreciation (20%) 4,000 24,000Chandrakant 39,550 Plant & Machinery 18,000Tarachand 12,000 80,750 Less: Depreciation (5%) 900 17,100

Sundry Creditors 8,000 Stock 7,000Less: Written Off 1,000 7,000 Less: Depreciation (5%) 350 6,650

Furniture 8,000 Debtors 11,000 Cash 15,000

Goodwill 6,000 87,750 87,750

Solution to Practice Q.13.: In the Books of Firm Revaluation Account

Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Depreciation A/c By Stock A/c 1,000Furniture 300 By Creditors A/c 1,000

By Rent Receivable A/c 400To Partner’s Captial A/c (Profit on Revaluation)

Sohan 1,400 Mohan 700 2,100

2,400 2,400

Target Publications Pvt. Ltd. Chapter 03: Reconstitution of Partnership (Admission of Partner)

13

Partner’s Capital Account Dr. Cr.

Particulars Sohan `

Mohan `

Rohan `

Particulars Sohan `

Mohan `

Rohan `

To Profit & Loss A/c 4,000 2,000 – By Balance b/d 40,000 30,000 – By General Reserve A/c 8,000 4,000 – By Cash A/c – – 12,000 By Goodwill A/c 6,000 3,000 – By Profit & Loss To Balance c/d 51,400 35,700 12,000 Adjustment A/c 1,400 700 –

55,400 37,700 12,000 55,400 37,700 12,000 Balance Sheet as on 1st Apr, 2012

Liabilities Amount `

Amount `

Assets Amount `

Amount `

Capital Building 20,000Sohan 51,400 Furniture 6,000Mohan 35,700 Less: Depreciation (5%) 300 5,700Rohan 12,000 99,100 Stock 12,000

Creditors 16,000 Add: Revaluation 1,000 13,000Less: Written Off 1,000 15,000 Debtors 60,000 Less: New R.D.D. (50% of General Reserve) 12,000 48,000

Rent Receivable 400 Cash 27,000 1,14,100 1,14,100

[Note: If future share of Incoming partner is given in question, then sacrificing ratio will be same as old ratio.] Solution to Practice Q.14.: In the Books of Firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Goodwill A/c 20,000 By Buildings A/c 4,350To Stock A/c 3,500 By Creditors' A/c 1,000To Provision for Bad Debts A/c 3,500 To Provision for Damages A/c 1,000 By Partner's Capital A/c (Loss on revaluation) A 5,662 B 8,494 C 8,494 22,650 28,000 28,000

Partner’s Capital Account Dr. Cr.

Particulars A `

B `

C `

D `

Particulars A `

B `

C `

D `

To Profit & Loss By Balance b/d 20,000 27,000 30,000 –Adjustment A/c 5,662 8,494 8,494 – By General Reserve A/c 4,000 6,000 6,000 –To Balance c/d 18,338 24,506 27,506 30,000 By Cash A/c – – – 30,000

24,000 33,000 36,000 30,000 24,000 33,000 36,000 30,000

14

Target Publications Pvt. Ltd. Std. XII (Commerce): Book-Keeping & Accountancy

Balance Sheet as on 1st Apr, 2012 Liabilities Amount

` Amount

` Assets Amount

` Amount

`Creditors 73,000 Cash 42,000 Less: written off 1,000 72,000 Bills Receivable 4,500Bank Overdraft 50,000 Trade Debtors 59,000Provision for damages 1,000 Less: Provision for bad Capital debts 3,500 55,500 A 18,338 Stock 35,000 B 24,506 Less: Revaluation 3,500 31,500 C 27,506 Furniture 2,000 D 30,000 1,00,350 Buildings 43,500 Add: Appreciation 4,350 47,850 Goodwill 60,000 Less: Revaluation 20,000 40,000 2,23,350 2,23,350

Solution to Practice Q.15.: In the Books of Firm Profit and Loss Adjustment Account

Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Stock A/c 500 By Building A/c 3,600 By R.D.D. A/c 1,100To Partner’s Capital A/c By Mr. Pandit’s Loan A/c 200(Profit on Revaluation)

Arjun 3,300 Pandit 1,100 4,400

4,900 4,900

Partner’s Capital Account Dr. Cr.

Particulars Arjun `

Pandit `

Raman `

Particulars Arjun `

Pandit `

Raman `

By Balance b/d 22,000 17,000 – By Profit & Loss A/c 5,250 1,750 – By Bank A/c – – 8,000 By Goodwill A/c 16,875 5,625 – By Profit & Loss To Balance c/d 47,425 25,475 8,000 Adjustment A/c 3,300 1,100 –

47,425 25,475 8,000 47,425 25,475 8,000 Bank Account

Dr. Cr.

Particulars Amount `

Particulars Amount `

To Balance b/d 5,000 By Mr. Pandit’s Loan A/c 1,800To Raman’s Capital A/c 8,000 By Balance c/d 11,200 13,000 13,000

Target Publications Pvt. Ltd. Chapter 03: Reconstitution of Partnership (Admission of Partner)

15

Goodwill Account Dr. Cr.

Particulars Amount `

Particulars Amount `

To Arjun’s Capital A/c 16,875 To Pandit’s Capital A/c 5,625 By Balance c/d 22,500 22,500 22,500

Balance Sheet as on 1st Apr, 2012

Liabilities Amount

` Amount

` Assets Amount

` Amount

`Capital Building 18,000

Arjun 47,425 Add: Appreciation 20% 3,600 21,600Pandit 25,475 Plant & Machinery 14,000Raman 8,000 80,900 Sundry Debtors 9,000

Sundry Creditors 12,000 Less: R.D.D. 900 8,100 Stock 9,000 Less: Revaluation 500 8,500 Loose Tools 7,000

Cash A/c 11,200 Goodwill 22,500 92,900 92,900

[Note: If future share of incoming partner is given in question, then sacrificing ratio will be same as old ratio] Solution to Practice Q.16.: In the Books of Firm

Revaluation Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To R.D.D. A/c 500 To Stock A/c 1,000 To Depreciation A/c By Partner’s Capital A/c

Building (5%) 2,200 (Loss on Revaluation) Ketan 2,220 Chetan 1,480 3,700 3,700 3,700

Partner’s Capital Account

Dr. Cr.

Particulars Ketan `

Chetan `

Ratan `

Particulars Ketan `

Chetan `

Ratan `

To Plant A/c 15,000 – – By Balance b/d 72,000 48,000 –To Goodwill A/c 30,000 20,000 10,000 By General To Profit & Loss Reserve A/c 6,000 4,000 –Adjustment A/c 2,220 1,480 – By Bank A/c – – 15,900 By Goodwill A/c 36,000 24,000 –To Balance c/d 66,780 54,520 5,900

1,14,000 76,000 15,900 1,14,000 76,000 15,900

16

Target Publications Pvt. Ltd. Std. XII (Commerce): Book-Keeping & Accountancy

Balance Sheet as on 1st Apr, 2012 Liabilities Amount

` Amount

` Assets Amount

` Amount

`Capital Sundry Debtors 45,000

Ketan 66,780 Less: R.D.D. 1,000 44,000Chetan 54,520 Stock 17,000Ratan 5,900 1,27,200 Less: Decrease 1,000 16,000

Sundry Creditors 30,000 Investment 24,000 Plant 30,000 Less: Taken over by Ketan 15,000 15,000 Building 44,000 Less: Depreciation (5%) 2,200 41,800 Bank 16,400 1,57,200 1,57,200

Solution to Practice Q.17.: In the Books of Firm Journal Entries

Date Particulars L.F. Debit `

Credit `

1. Cash A/c To P's Capital A/c (Being capital introduced by new partner)

Dr. 25,000 25,000

2. Cash A/c To P's Capital A/c (Being proportionate amount of Goodwill brought in cash by P)

Dr. 19,500 19,500

3. P's Capital A/c To X's Capital A/c To Y's Capital A/c To Z's Capital A/c (Being goodwill brought in by P transferred to old partners)

Dr. 19,500 6,500 6,500 6,500

4. Bank Overdraft A/c To X's Capital A/c (Being bank overdraft taken over by X)

Dr. 8,000 8,000

5. Z’s Capital A/c Profit & Loss Adjustment A/c To Debtors A/c (Being debtors revalued and taken over by Z)

Dr. Dr.

12,000 1,000

13,000

6. Stock A/c To Profit & Loss Adjustment A/c (Being stock revalued)

Dr. 2,000 2,000

7. Profit & Loss Adjustment A/c To Buildings A/c To Machinery A/c (Being Buildings and Machinery depreciated by 15% and 10% respectively)

Dr. 3,000 3,000 4,000

8. X's Capital A/c Y's Capital A/c Z's Capital A/c To Profit & Loss Adjustment A/c (Being loss on revaluation transferred to capital accounts)

Dr. Dr. Dr.

2,000 2,000 2,000

6,000

Total: 96,000 96,000

Target Publications Pvt. Ltd. Chapter 03: Reconstitution of Partnership (Admission of Partner)

17

Balance Sheet as on 31st Mar, 2012 Liabilities Amount

` Amount

` Assets Amount

` Amount

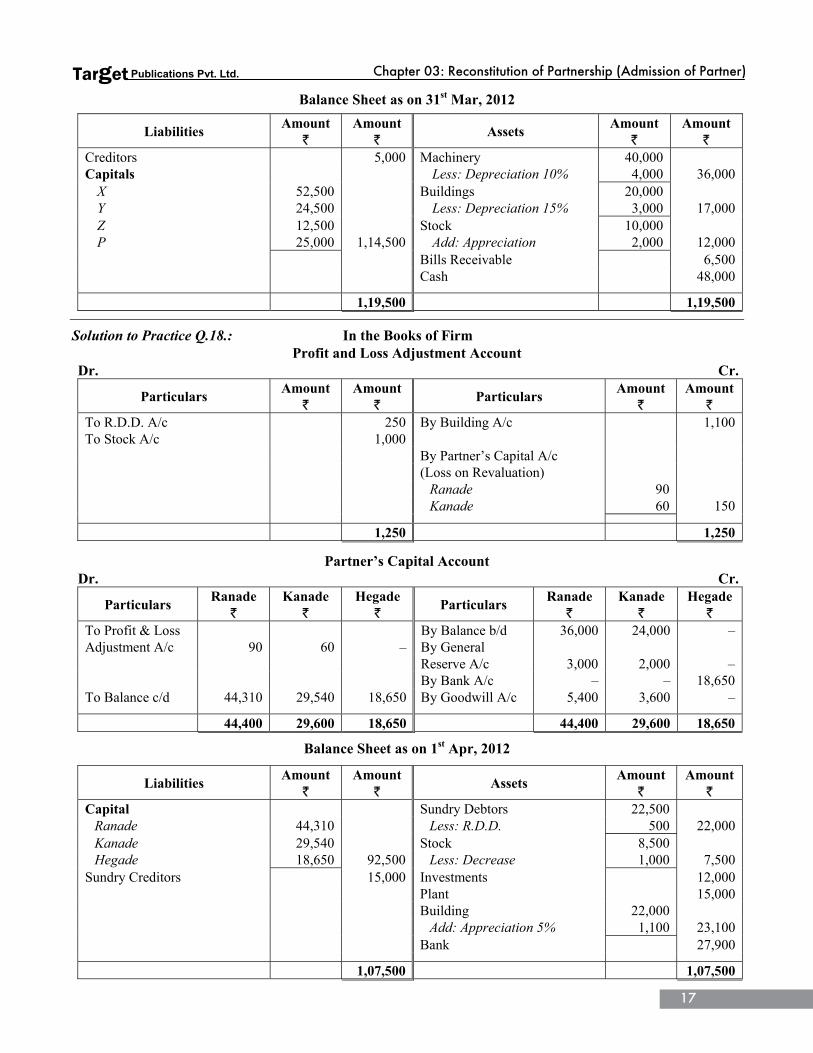

`Creditors 5,000 Machinery 40,000Capitals Less: Depreciation 10% 4,000 36,000 X 52,500 Buildings 20,000 Y 24,500 Less: Depreciation 15% 3,000 17,000 Z 12,500 Stock 10,000 P 25,000 1,14,500 Add: Appreciation 2,000 12,000 Bills Receivable 6,500 Cash 48,000 1,19,500 1,19,500

Solution to Practice Q.18.: In the Books of Firm Profit and Loss Adjustment Account

Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To R.D.D. A/c 250 By Building A/c 1,100To Stock A/c 1,000 By Partner’s Capital A/c (Loss on Revaluation) Ranade 90 Kanade 60 150 1,250 1,250

Partner’s Capital Account Dr. Cr.

Particulars Ranade `

Kanade `

Hegade `

Particulars Ranade `

Kanade `

Hegade `

To Profit & Loss By Balance b/d 36,000 24,000 –Adjustment A/c 90 60 – By General Reserve A/c 3,000 2,000 – By Bank A/c – – 18,650To Balance c/d 44,310 29,540 18,650 By Goodwill A/c 5,400 3,600 –

44,400 29,600 18,650 44,400 29,600 18,650 Balance Sheet as on 1st Apr, 2012

Liabilities Amount `

Amount `

Assets Amount `

Amount `

Capital Sundry Debtors 22,500Ranade 44,310 Less: R.D.D. 500 22,000Kanade 29,540 Stock 8,500Hegade 18,650 92,500 Less: Decrease 1,000 7,500

Sundry Creditors 15,000 Investments 12,000 Plant 15,000

Building 22,000 Add: Appreciation 5% 1,100 23,100 Bank 27,900

1,07,500 1,07,500

18

Target Publications Pvt. Ltd. Std. XII (Commerce): Book-Keeping & Accountancy

Solution to Practice Q.19.: In the Books of Firm Profit and Loss Adjustment Account

Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Depreciation A/c Machinery (10%) 4,800 Building (10%) 11,400 16,200

To R.D.D. A/c 3,000 To Bills Receivable A/c 2,400 By Partner’s Capital A/c (Loss on Revaluation) Veena 10,800 Leela 10,800 21,600 21,600 21,600

Partner’s Capital Account

Dr. Cr.

Particulars Veena `

Leela `

Asha `

Particulars Veena `

Leela `

Asha `

To Bills Receivable By Balance b/d 90,000 60,000 –A/c 21,600 – – By General To Profit & Loss Reserve A/c 18,000 18,000 –Adjustment A/c 10,800 10,800 – By Bank A/c – – 80,000 By Current A/c 44,400 52,800 –To Balance c/d 1,20,000 1,20,000 80,000

1,52,400 1,30,800 80,000 1,52,400 1,30,800 80,000

Balance Sheet as on 1st Apr, 2012 Liabilities Amount

` Amount

` Assets Amount

` Amount

`Capital A/c Debtors 62,000

Veena 1,20,000 Less: R.D.D. 5,000 57,000Leela 1,20,000 Building 1,14,000Asha 80,000 3,20,000 Less: Depreciation (10%) 11,400 1,02,600

Sundry Creditors 1,80,000 Machinery 48,000 Less: Depreciation (10%) 4,800 43,200 Cash at Bank 2,00,000

Current A/c Veena 44,400 Leela 52,800 97,200 5,00,000 5,00,000

Solution to Practice Q.20.: In the Books of Firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount

`

Amount `

Particulars Amount

` Amount

` To Land & Building A/c 1,750 To Plant & Machinery A/c 1,225 To Stock A/c 1,435

Target Publications Pvt. Ltd. Chapter 03: Reconstitution of Partnership (Admission of Partner)

19

To R.D.D. A/c 1,575 By Partner’s Capital A/c (Loss on Revaluation) Kale 3,591 Gore 2,394 5,985 5,985 5,985

Partner’s Capital Account

Dr. Cr.

Particulars Kale `

Gore `

Pandhare `

Particulars Kale `

Gore `

Pandhare`

To Profit & Loss By Balance b/d 24,500 24,500 –Adjustment A/c 3,591 2,394 – By General To Cash A/c – 21,106 – Reserve A/c 3,000 2,000 – By Cash A/c – – 10,000 By Goodwill A/c – 7,000 –To Balance c/d 30,000 10,000 10,000 By Cash A/c 6,091 – –

33,591 33,500 10,000 33,591 33,500 10,000

Balance Sheet as on 1st Apr, 2014

Liabilities Amount `

Amount `

Assets Amount `

Amount `

Capital Land & Building 17,500Kale 30,000 Less: Depreciation 1,750 15,750Gore 10,000 Plant & Machinery 24,500Pandhare 10,000 50,000 Less: Depreciation (5%) 1,225 23,275

Creditors 38,000 Furniture 1,050Bills Payable 400 Stock 14,350 Less: Written Off (10%) 1,435 12,915

Debtors 31,500 Less: New R.D.D. (5%) 1,575 29,925 Cash 5,485 88,400 88,400

Solution to Practice Q.21.: In the Books of Firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Plant & Machinery A/c 7,000 By Land & Building A/c 10,000To Furniture A/c 300 By Stock A/c 9,000To R.D.D. A/c 4,500 To Partner’s Capital A/c (Profit on Revaluation)

Sukhadeo 4,320 Hanumant 2,880 7,200

19,000 19,000

20

Target Publications Pvt. Ltd. Std. XII (Commerce): Book-Keeping & Accountancy

Partner’s Capital Account Dr. Cr.

Particulars Sukhadeo `

Hanumant `

Shakuntala`

Particulars Sukhadeo `

Hanumant`

Shakuntala`

To Loan A/c 26,320 40,880 – By Balance b/d 70,000 70,000 – By Bank A/c – – 30,000 By Goodwill A/c 6,000 4,000 – By Profit & Loss To Balance c/d 54,000 36,000 30,000 Adjustment A/c 4,320 2,880 –

80,320 76,880 30,000 80,320 76,880 30,000 Balance Sheet as on 1st Apr, 2011

Liabilities Amount `

Amount `

Assets Amount `

Amount `

Capital Land & Building 50,000Sukhadeo 54,000 Add: Appreciation 10,000 60,000Hanumant 36,000 Plant & Machinery 70,000Shakuntala 30,000 1,20,000 Less: Depreciation (10%) 7,000 63,000

Creditors 1,24,000 Furniture 3,000Loan from Partners Less: Depreciation (10%) 300 2,700

Sukhadeo 26,320 Stock 41,000Hanumant 40,880 67,200 Add: Appreciation 9,000 50,000

Debtors 90,000 Less: R.D.D. (5%) 4,500 85,500 Cash at Bank 50,000 3,11,200 3,11,200

[Note: If future share of incoming partner is given in question, then sacrificing ratio will be same as old ratio] Solution to Practice Q.22.: In the Books of firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Building A/c 2,000 To Machinery A/c 4,000 To Debtors A/c 1,000 By Partners Capital A/c (Loss on Revaluation) Abhi 4,200 Anju 2,800 7,000 7,000 7,000

Partner’s Capital Account

Dr. Cr.

Particulars Abhi `

Anju `

Vivek `

Particulars Abhi `

Anju `

Vivek `

To Profit & Loss By Balance b/d 45,000 30,000 –Adjustment A/c 4,200 2,800 – By General To Cash A/c 13,200 8,800 – Reserve A/c 15,000 10,000 – By Cash A/c – – 15,000To Balance c/d 45,000 30,000 15,000 By Goodwill A/c 2,400 1,600 –

62,400 41,600 15,000 62,400 41,600 15,000

Target Publications Pvt. Ltd. Chapter 03: Reconstitution of Partnership (Admission of Partner)

21

Cash Account Dr. Cr.

Particulars Amount `

Particulars Amount `

To Balance c/d 4,000 By Abhi’s Capital A/c 13,200To Vivek’s Capital A/c 15,000 By Anju’s Capital A/c 8,800To Goodwill A/c 4,000 By Balance c/d 1,000 23,000 23,000

Goodwill Account

Dr. Cr.

Particulars Amount `

Particulars Amount `

To Abhi’s Capital A/c 2,400 By Cash A/c 4,000To Anju’s Capital A/c 1,600 4,000 4,000

Balance Sheet as on 1st Apr, 2014

Liabilities Amount

` Amount

` Assets Amount

` Amount

`

Capital A/c Building 30,000Abhi 45,000 Less: Depreciation 2,000 28,000Anju 30,000 Machinery 40,000Vivek 15,000 90,000 Less: Depreciation (10%) 4,000 36,000

Bills Payable 8,000 Furniture 2,000Creditors 12,000 Stock 16,000

Debtors 20,000 Less: New R.D.D. (5%) 1,000 19,000 Fixed Deposit in Bank 8,000 Cash in Hand 1,000

1,10,000 1,10,000

Solution to Practice Q.23.: In the Books of Firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Interest on Ragini's Loan By Reserve for Doubtful A/c 400 Debts A/c 900To Stock A/c 2,000 By Building A/c 6,000 To Partner's Capital A/c (Profit on revaluation) Ragini 3,000 Radha 1,500 4,500 6,900 6,900

22

Target Publications Pvt. Ltd. Std. XII (Commerce): Book-Keeping & Accountancy

Partner’s Capital Account Dr. Cr.

Particulars Ragini `

Radha `

Rashmi `

Particulars Ragini `

Radha `

Rashmi `

To Goodwill A/c 4,800 2,400 1,800 By Balance b/d 48,000 32,000 –To Partners Current By General Reserve A/c – 6,100 – A/c 6,000 3,000 – By Profit & Loss A/c 2,000 1,000 – By Cash A/c – – 20,000 By Stock A/c – – 4,000 By Goodwill A/c 6,000 3,000 – By Profit & Loss Adjustment A/c 3,000 1,500 – By Partners Current To Balance c/d 64,000 32,000 24,000 A/c 3,800 – 1,800 68,800 40,500 25,800 68,800 40,500 25,800

Balance Sheet as on 1st Apr, 2012

Liabilities Amount

` Amount

` Assets Amount

` Amount

`Capitals Building 51,000 Ragini 64,000 Add: Appreciation 6,000 57,000 Radha 32,000 Stock 42,000 Rashmi 24,000 1,20,000 Add: brought by Rashmi 4,000Current A/c Less: Reduction in value 2,000 44,000 Radha 6,100 Debtors 30,500Sundry Creditors 44,000 Less: RDD 600 29,900Ragini's Loan 6,500 Furniture 12,000 Office Equipments 7,000 Cash 21,100 Current Account Ragini 3,800 Rashmi 1,800 5,600 1,76,600 1,76,600

Solution to Practice Q.24.: In the Books of Firm

Profit and Loss Adjustment Account Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Depreciation A/c By Land & Building A/c 2,000Furniture (10%) 1,000 Stock (5%) 1,250 2,250

To R.D.D. A/c 1,750 By Partner’s Capital A/c (Loss on Revaluation) Ram 1,200 Krishna 800 2,000 4,000 4,000

Target Publications Pvt. Ltd. Chapter 03: Reconstitution of Partnership (Admission of Partner)

23

Partner’s Capital Account Dr. Cr.

Particulars Ram `

Krishna `

Hari `

Particulars Ram `

Krishna `

Hari `

To Bank A/c 6,000 4,000 – By Balance b/d 50,000 40,000 –To Profit & Loss By Bank A/c – – 25,000Adjustment A/c 1,200 800 – By Reserve A/c 9,000 6,000 –To Bank A/c 12,800 15,200 – By Goodwill A/c 6,000 4,000 – To Balance c/d 45,000 30,000 25,000

65,000 50,000 25,000 65,000 50,000 25,000 Balance Sheet as on 1st Apr, 2013

Liabilities Amount `

Amount `

Assets Amount `

Amount `

Capital Land & Building 40,000Ram 45,000 Add: Appreciation 2,000 42,000Krishna 30,000 Stock 25,000Hari 25,000 1,00,000 Less: Depreciation (5%) 1,250 23,750

Creditors 30,000 Furniture 10,000Bills Payable 5,000 Less: Depreciation (10%) 1,000 9,000 Debtors 35,000

Less: R.D.D. (5%) 1,750 33,250 Investments 20,000 Cash at Bank 7,000 1,35,000 1,35,000

Solution to Practice Q.25.: In the Books of Firm Profit and Loss Adjustment Account

Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Bills Receivable A/c 2,300 To Machinery A/c 4,800 To Building A/c 9,500 To R.D.D. A/c 3,000 By Partner's Capital A/c (Loss on Revaluation) Vishnu 9,800 Jay 9,800 19,600 19,600 19,600

Partner’s Capital Account Dr. Cr.

Particulars Vishnu `

Jay `

Asha `

Particulars Vishnu `

Jay `

Asha `

To Goodwill A/c 15,000 15,000 10,000 By Balance b/d 90,000 60,000 –To Bills Receivable By General Reserve A/c 20,700 – – A/c 18,000 18,000 –To Profit & Loss By Bank A/c – – 70,000Adjustment A/c 9,800 9,800 – By Goodwill A/c 10,000 10,000 – By Partner's Current To Balance c/d 1,05,000 1,05,000 70,000 A/c 32,500 41,800 10,000

1,35,500 1,14,800 70,000 1,35,500 1,14,800 70,000

24

Target Publications Pvt. Ltd. Std. XII (Commerce): Book-Keeping & Accountancy

Balance Sheet as on 1st Apr, 2012 Liabilities Amount

` Amount

` Assets Amount

` Amount

`Sundry Creditors 2,00,000 Cash at Bank 2,00,000 Capitals Debtors 72,000 Vishnu 1,05,000 Less: RDD 5,000 67,000 Jay 1,05,000 Building 95,000 Asha 70,000 2,80,000 Less: Depreciation 9,500 85,500 Machinery 48,000 Less: Depreciation 4,800 43,200 Current Accounts Vishnu 32,500 Jay 41,800 Asha 10,000 84,300 4,80,000 4,80,000

Solution to Practice Q.26.: In the Books of Firm Profit and Loss Adjustment Account

Dr. Cr.

Particulars Amount `

Amount `

Particulars Amount `

Amount `

To Stock A/c 1,100 To Depreciation A/c

Building (10%) 800 Furniture (10%) 200 1,000 By Partner’s Capital A/c

(Loss on Revaluation) Raja 1,400 Rani 700 2,100 2,100 2,100

Partner’s Capital Account Dr. Cr.

Particulars Raja `

Rani `

Kanchan `

Particulars Raja `

Rani `

Kanchan `

To Profit & Loss By Balance b/d 14,000 7,000 –Adjustment A/c 1,400 700 – By General Reserve A/c 4,000 2,000 – By Cash A/c – – 12,000 By Goodwill A/c 4,000 2,000 –To Balance c/d 24,000 12,000 12,000 By Cash A/c 3,400 1,700 –

25,400 12,700 12,000 25,400 12,700 12,000 Balance Sheet as on 1st Apr, 2013

Liabilities Amount `

Amount `

Assets Amount `

Amount `

Capital Building 8,000Raja 24,000 Less: Depreciation (10%) 800 7,200Rani 12,000 Furniture 2,000Kanchan 12,000 48,000 Less: Depreciation (10%) 200 1,800

Bills Payable 3,000 Debtors 16,000Creditors 10,000 Stock 11,000

Less: Decrease 1,100 9,900 Cash 26,100

61,000 61,000 [Note: If future share of incoming partner is given in question, then sacrificing ratio will be same as old ratio]