Embed Size (px)

Citation preview

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

1

REconfigured REtail in Europe

Trade Promotion Management and Optimization

in the Midst of a Perfect Storm

Himanshu Pal

Director of Retail Insights - Kantar Retail

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

2

Retailing Environment is Evolving Rapidly…

Source: Kantar Retail

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

3

Current Retailing Environment Resembles a ‘Perfect Storm’

Source: Kantar Retail analysis

Country C

Channel

Customer

Consumer C

C

C

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

“Insanity is doing the same thing over and over again and expecting different results.”

Albert Einstein

4

Riding Through the ‘Perfect Storm’ Needs a New Approach

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

5

Riding Through the ‘Perfect Storm’ Needs a New Approach

Source: Kantar Retail

Understand the Current Retail

Landscape

Decode the Future Disruptions,

Challenges and Opportunities

Plan and Develop / Enhance Capabilities

Needed to Win in the Future

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

6

Current Retailing Environment Resembles a ‘Perfect Storm’

Source: Kantar Retail analysis

Country C

Channel

Customer

Consumer C

C

C

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

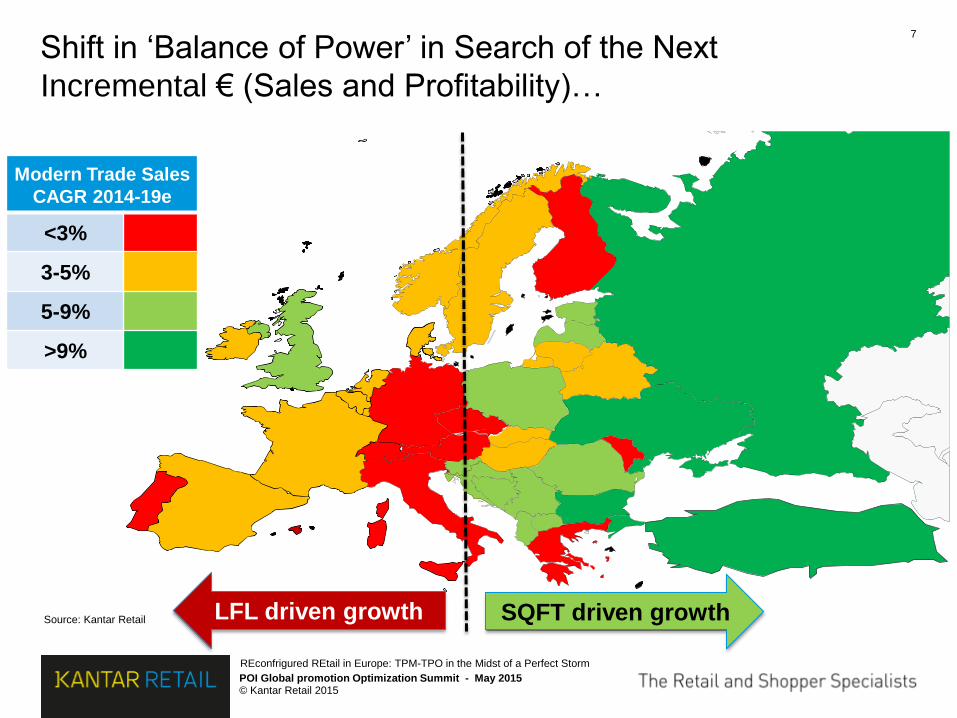

7

Shift in ‘Balance of Power’ in Search of the Next

Incremental € (Sales and Profitability)…

Source: Kantar Retail

Modern Trade Sales

CAGR 2014-19e

<3%

3-5%

5-9%

>9%

LFL driven growth SQFT driven growth

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

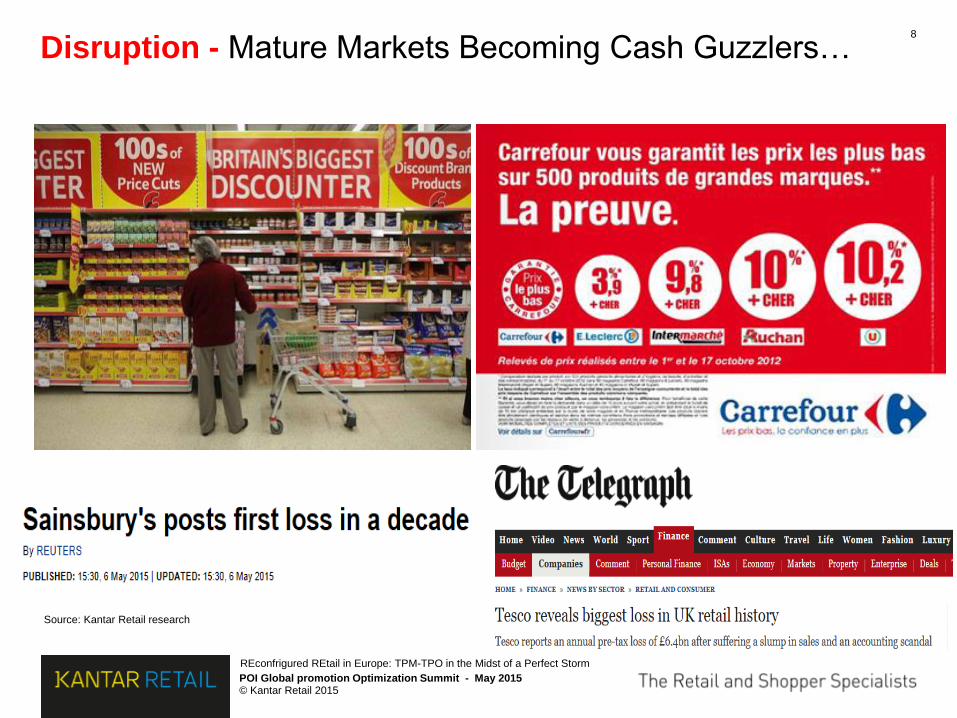

8

Disruption - Mature Markets Becoming Cash Guzzlers…

Source: Kantar Retail research

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

Emerging markets exited in

last 3 years by global retailers

9

Disruption - Emerging Markets No Longer Shock Proof…

Source: Kantar Retail research

Inconsistent Execution

Brazil India Political & Economic Instability

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

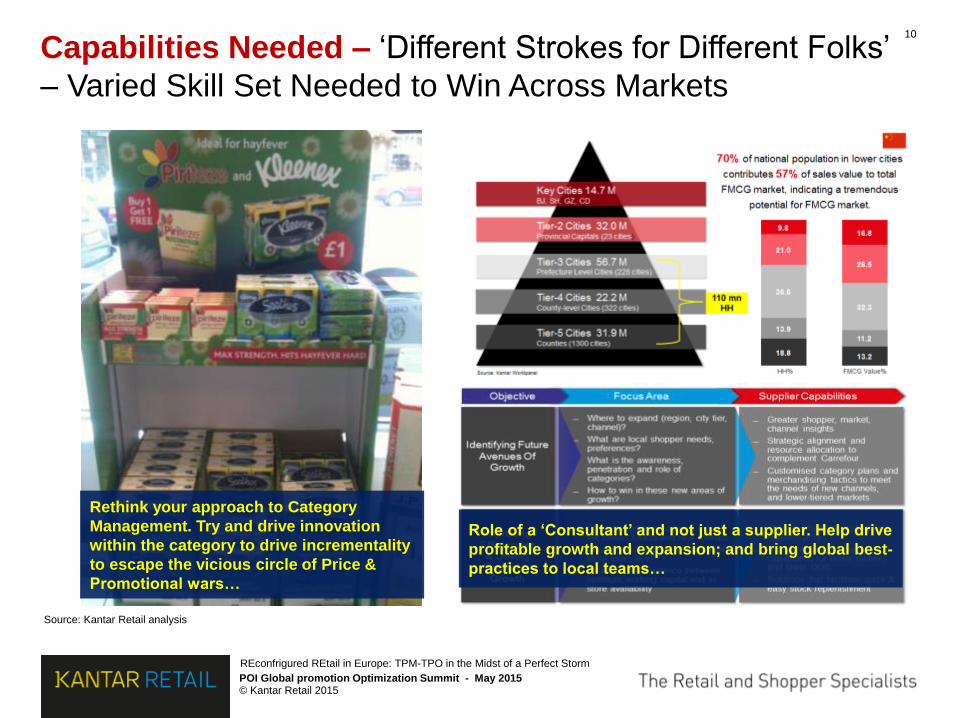

10

Capabilities Needed – ‘Different Strokes for Different Folks’

– Varied Skill Set Needed to Win Across Markets

Source: Kantar Retail analysis

Rethink your approach to Category

Management. Try and drive innovation

within the category to drive incrementality

to escape the vicious circle of Price &

Promotional wars…

Role of a ‘Consultant’ and not just a supplier. Help drive

profitable growth and expansion; and bring global best-

practices to local teams…

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

11

Current Retailing Environment Resembles a ‘Perfect Storm’

Source: Kantar Retail analysis

Country C

Channel

Customer

Consumer C

C

C

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

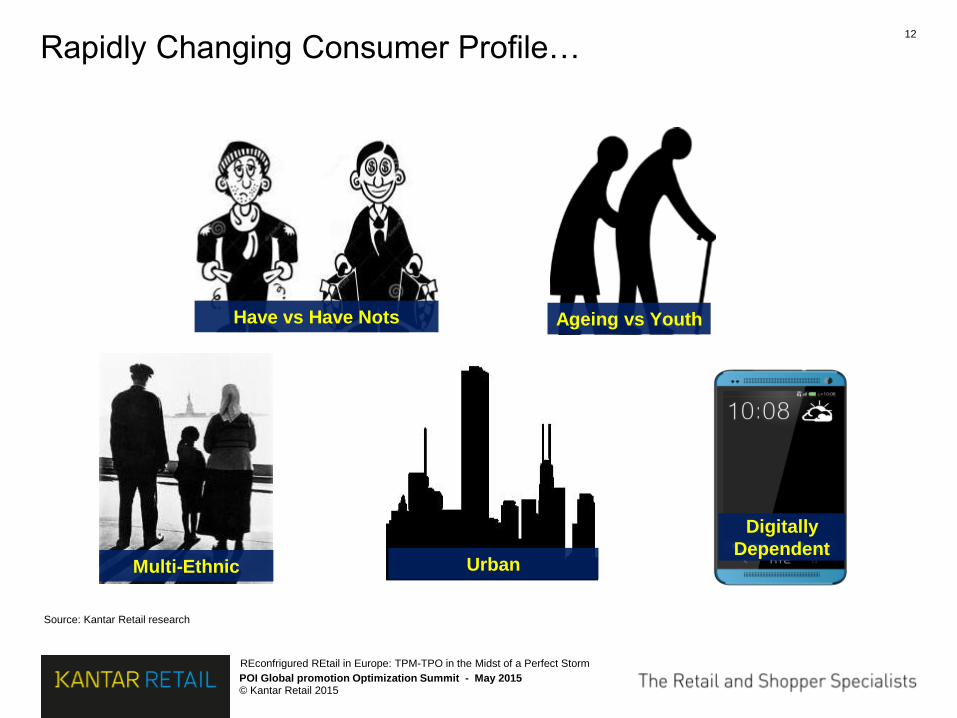

12

Rapidly Changing Consumer Profile…

Source: Kantar Retail research

Have vs Have Nots Ageing vs Youth

Multi-Ethnic Urban

Digitally

Dependent

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

13

Changing Consumer Profile Influencing Shopper

Expectations, Behaviour and Definition of VALUE…

Source: Kantar Retail research and analysis

I need to reduce spend

Buy fewer things

Cheaper store

Buy cheaper things

Cheaper brands

PromotionsPrivate label

Shopper decision tree

The Economic Landscape

The Demographic Landscape

Technology Changes

Volumes down 3-6%

across Spain,

Portugal, Italy,

Greece

Carrefour France

hypermarket

transactions down 40

million versus 2007

Aldi, Biedronka, Lidl,

Kaufland, Mercadona

UK: Promotions 40%

of all sales

European PL %

2006: 22%

2012:27%

SHOPPER DECISION TREE

Quick & Easy Access

Optimised Assortment

Solutions (Snacking, Lunch Meal)

Optimum Pack Size

Value For Money

Service / Experience

SHOPPER NEEDS

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

14

Disruption – Shopper Definition of VALUE No Longer

Limited to Price…

Source: Kantar Retail analysis

Real Value = Price + Time + Quality + Experience

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

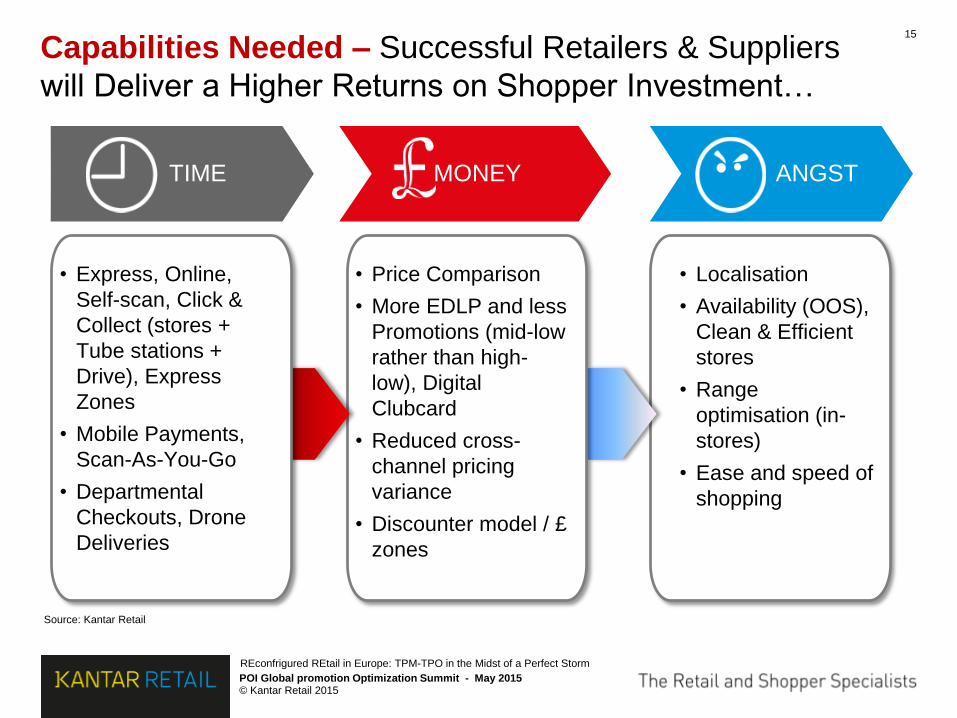

15

Capabilities Needed – Successful Retailers & Suppliers

will Deliver a Higher Returns on Shopper Investment…

Source: Kantar Retail

• Localisation

• Availability (OOS),

Clean & Efficient

stores

• Range

optimisation (in-

stores)

• Ease and speed of

shopping

• Price Comparison

• More EDLP and less

Promotions (mid-low

rather than high-

low), Digital

Clubcard

• Reduced cross-

channel pricing

variance

• Discounter model / £

zones

• Express, Online,

Self-scan, Click &

Collect (stores +

Tube stations +

Drive), Express

Zones

• Mobile Payments,

Scan-As-You-Go

• Departmental

Checkouts, Drone

Deliveries

MONEY ANGST TIME

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

16

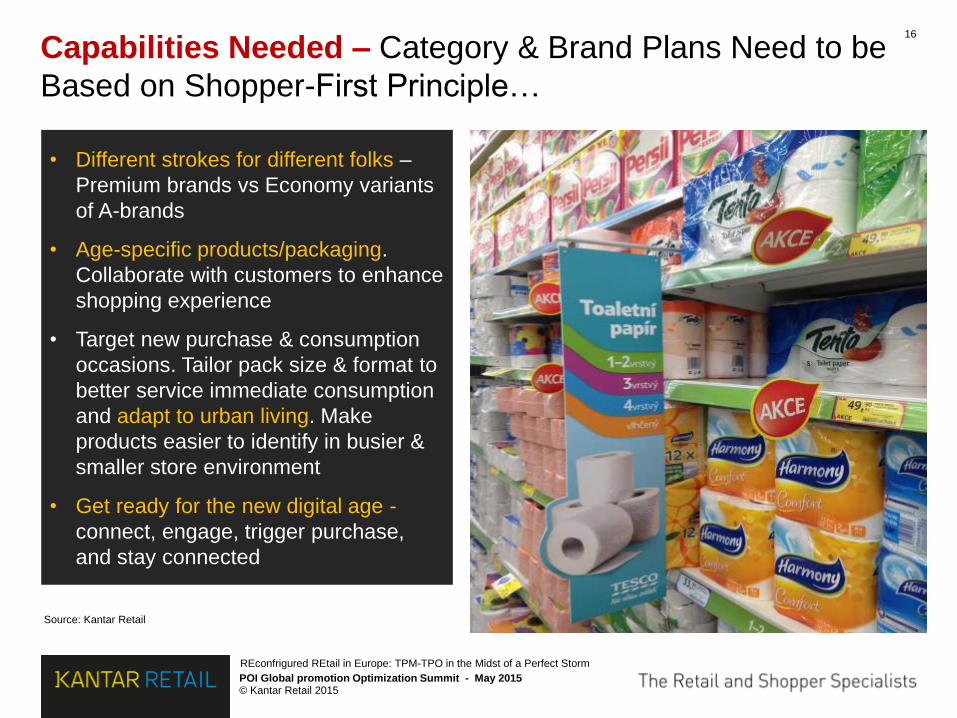

Capabilities Needed – Category & Brand Plans Need to be

Based on Shopper-First Principle…

Source: Kantar Retail

• Different strokes for different folks –

Premium brands vs Economy variants

of A-brands

• Age-specific products/packaging.

Collaborate with customers to enhance

shopping experience

• Target new purchase & consumption

occasions. Tailor pack size & format to

better service immediate consumption

and adapt to urban living. Make

products easier to identify in busier &

smaller store environment

• Get ready for the new digital age -

connect, engage, trigger purchase,

and stay connected

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

17

Current Retailing Environment Resembles a ‘Perfect Storm’

Source: Kantar Retail analysis

Country C

Channel

Customer

Consumer C

C

C

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

18

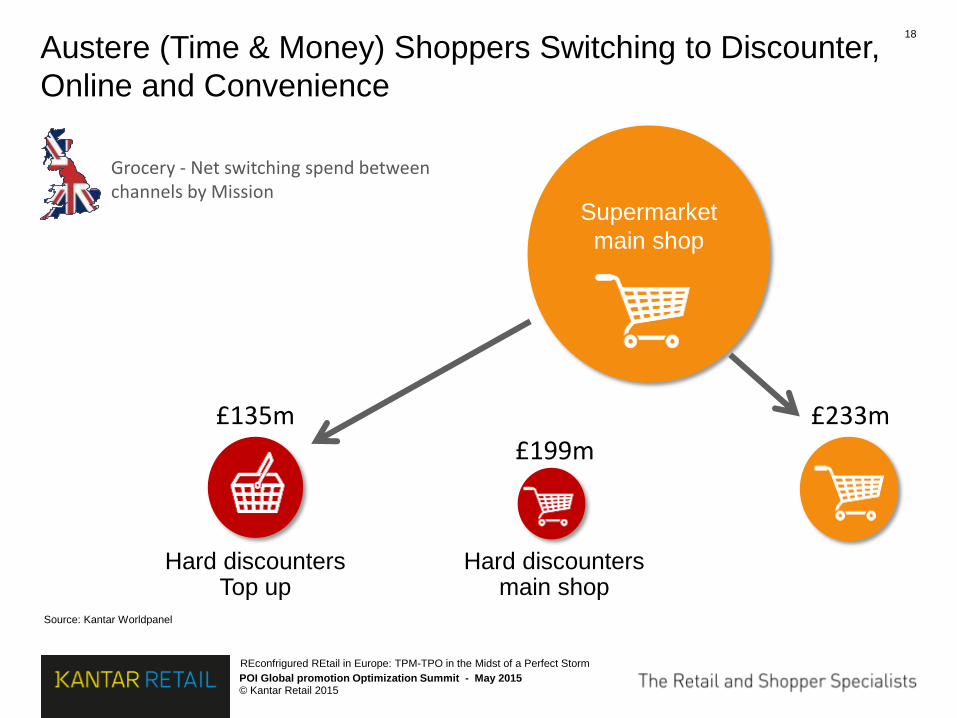

Austere (Time & Money) Shoppers Switching to Discounter,

Online and Convenience

Source: Kantar Worldpanel

Grocery - Net switching spend between channels by Mission

Supermarket

main shop

Hard discounters main shop

Hard discounters Top up

£233m

£199m

£135m

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

19

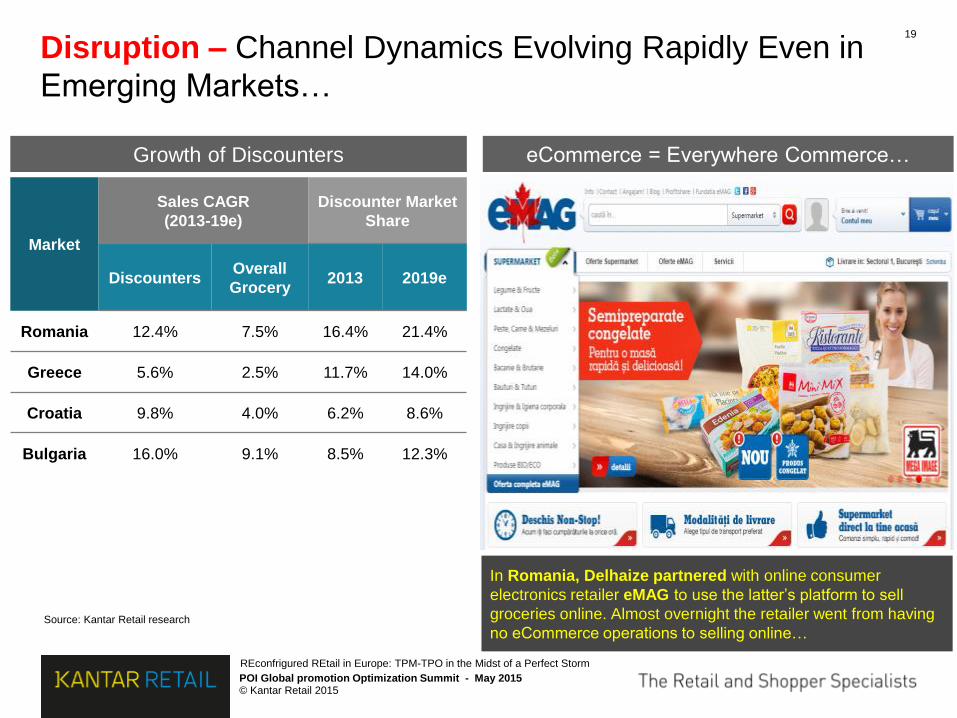

Disruption – Channel Dynamics Evolving Rapidly Even in

Emerging Markets…

Source: Kantar Retail research

In Romania, Delhaize partnered with online consumer

electronics retailer eMAG to use the latter’s platform to sell

groceries online. Almost overnight the retailer went from having

no eCommerce operations to selling online…

Market

Sales CAGR

(2013-19e)

Discounter Market

Share

Discounters Overall

Grocery 2013 2019e

Romania 12.4% 7.5% 16.4% 21.4%

Greece 5.6% 2.5% 11.7% 14.0%

Croatia 9.8% 4.0% 6.2% 8.6%

Bulgaria 16.0% 9.1% 8.5% 12.3%

Growth of Discounters eCommerce = Everywhere Commerce…

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

20

Disruption – Traditional Channel Boundaries are Blurring

Source: Kantar Retail

Rossmann Drugstore (Poland) Carrefour Hypermarket (Poland) Biedronka Discounter (Poland)

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

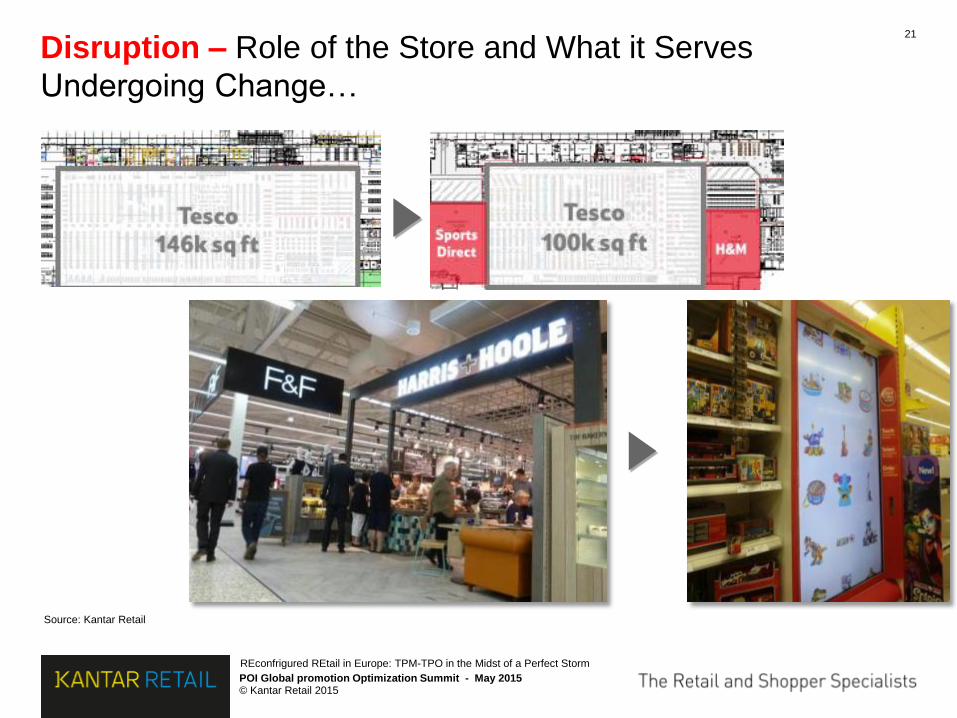

21

Disruption – Role of the Store and What it Serves

Undergoing Change…

Source: Kantar Retail

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

22

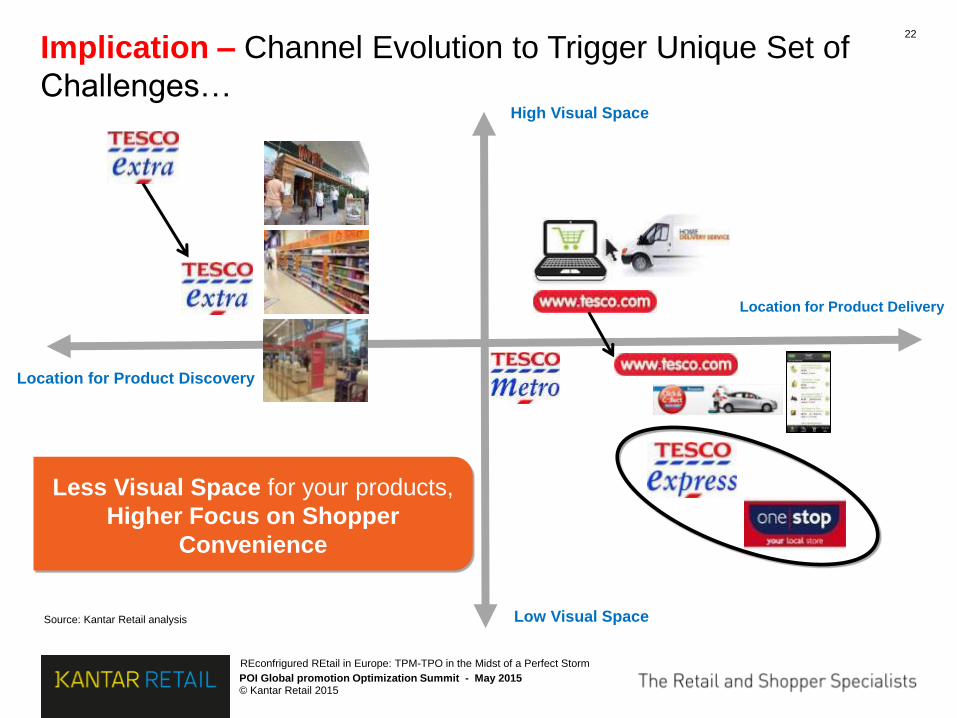

Implication – Channel Evolution to Trigger Unique Set of

Challenges…

Source: Kantar Retail analysis

Less Visual Space for your products,

Higher Focus on Shopper

Convenience

Location for Product Discovery

High Visual Space

Location for Product Delivery

Low Visual Space

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

23

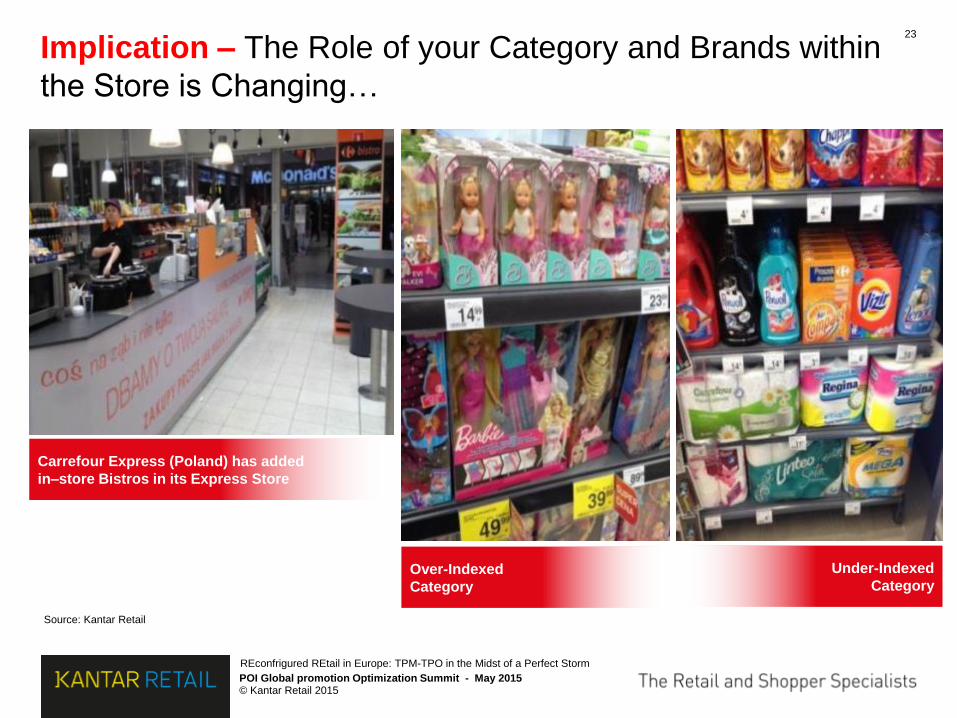

Implication – The Role of your Category and Brands within

the Store is Changing…

Source: Kantar Retail

Carrefour Express (Poland) has added

in–store Bistros in its Express Store

Over-Indexed

Category

Under-Indexed

Category

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

24

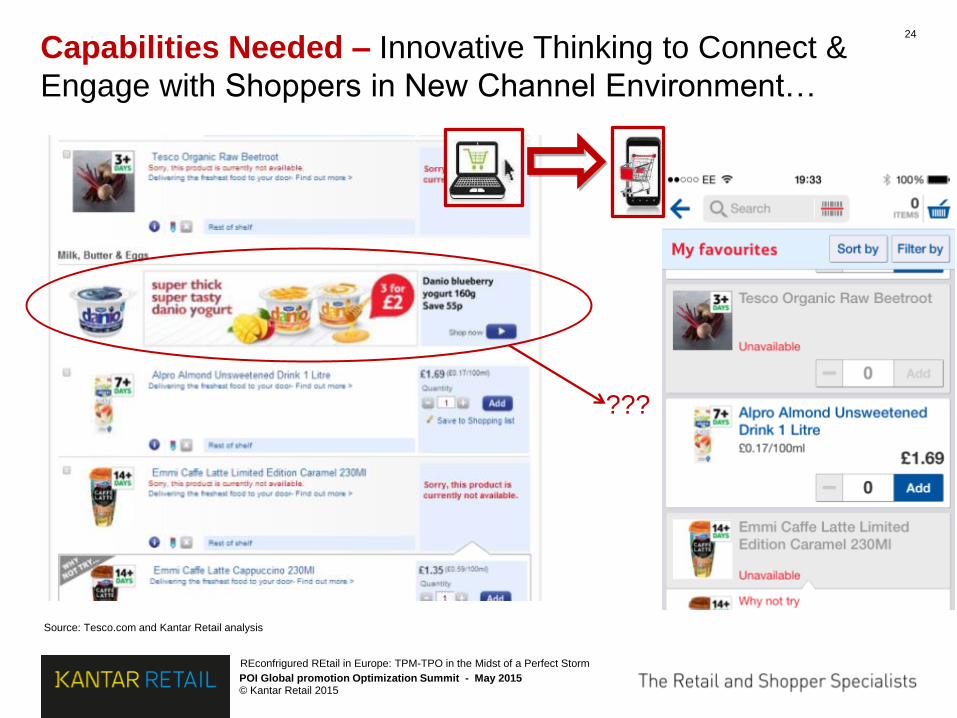

Capabilities Needed – Innovative Thinking to Connect &

Engage with Shoppers in New Channel Environment…

Source: Tesco.com and Kantar Retail analysis

???

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

25

Current Retailing Environment Resembles a ‘Perfect Storm’

Source: Kantar Retail analysis

Country C

Channel

Customer

Consumer C

C

C

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

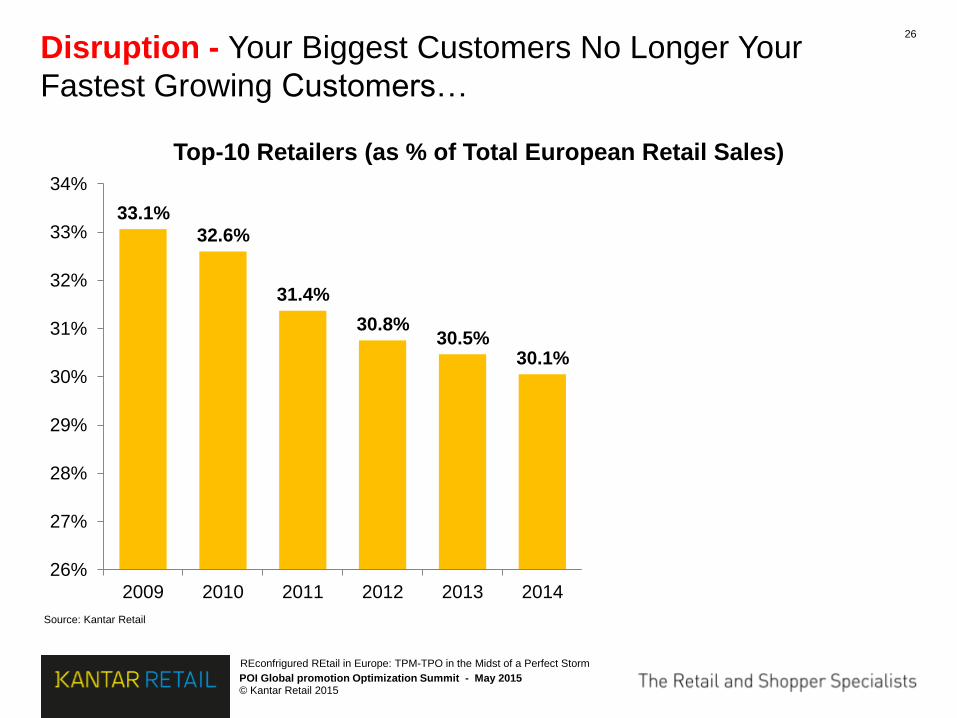

26

Disruption - Your Biggest Customers No Longer Your

Fastest Growing Customers…

Source: Kantar Retail

33.1%

32.6%

31.4%

30.8% 30.5%

30.1% 29.7%

29.3% 28.9%

28.5%

26%

27%

28%

29%

30%

31%

32%

33%

34%

2009 2010 2011 2012 2013 2014 2015E 2016E 2017E 2018E

Top-10 Retailers (as % of Total European Retail Sales)

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

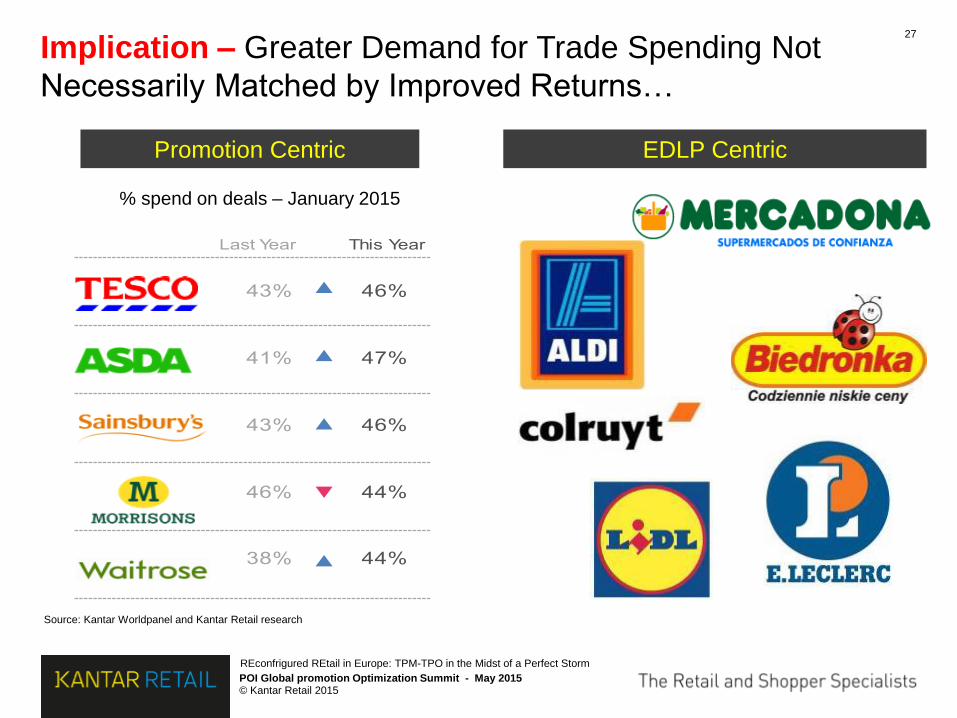

27

Implication – Greater Demand for Trade Spending Not

Necessarily Matched by Improved Returns…

Source: Kantar Worldpanel and Kantar Retail research

Spend on Deal - anuary

Last ear This ear

% spend on deals – January 2015

Promotion Centric EDLP Centric

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

Jose Luis Duran

(0 /2005 ‒ 2/200 )

Lars Oloffson

(0 /2009 ‒ 03/2012)

George Plassat

(0 /20 2 ‒ Present)

Sales (EUR billions) including Franchises € 94.97bn € 83.54 bn € 90.02 bn

No. of Markets operated (at end of term) 32 33 33

No. of Stores (at end of term or March ‘ 5) 15,430 9,771 11,845

Operating Profit (EUR billions) 3,300 2,182 2,387

Sales growth (CAGR) 7.4% (7.5)% 2.6%

Avg. Gross Margin (%) 21.4% 20.6% 20.2%

Gross Profit growth (CAGR) 3.9% (1.7)% (1.9)%

Avg. Recurring Operating Margin (%) 4.2% 3.2% 3.0%

Recurring Operating Profit growth (CAGR) 0.3% (9.8)% 3.0%

Avg. Inventory (or Stock) Turns 9.9 10 10

Avg. Dividend Pay-out 1.01 0.94 0.62

Share Price (Movement) (21.5)% (36.0)% 86.0%

Market Capitalisation (EUR billions) € 19.4 bn € 11.9 bn € 24.0 bn

Change in Market Capitalisation (EUR billion) € 5.3 bn € 7.4 bn € 12.1 bn

Avg. Free Cash Flow (EUR bn) € 1.3 bn € 1.0 bn € 0.2 bn

28

Disruption - Short-term Returns Mentality Taking Centre

Stage…

Source: Carrefour and Kantar Retail analysis

Opera

tio

ns

Scale

R

OI

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

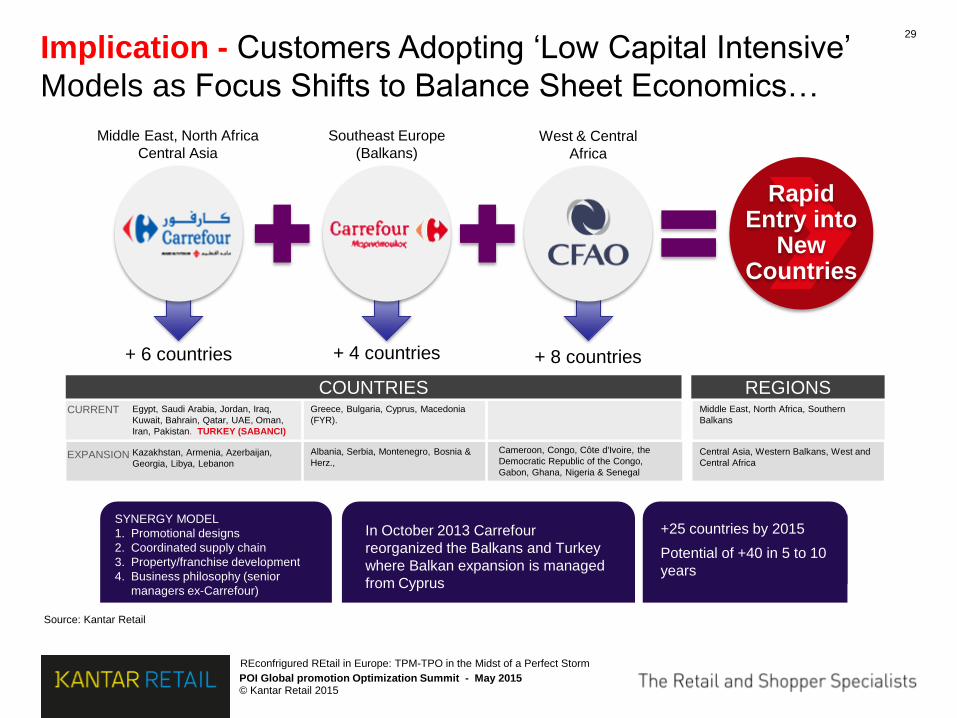

29

Implication - Customers Adopting ‘Low Capital Intensive’

Models as Focus Shifts to Balance Sheet Economics…

Source: Kantar Retail

REGIONS COUNTRIES CURRENT

EXPANSION

Egypt, Saudi Arabia, Jordan, Iraq,

Kuwait, Bahrain, Qatar, UAE, Oman,

Iran, Pakistan. TURKEY (SABANCI)

Kazakhstan, Armenia, Azerbaijan,

Georgia, Libya, Lebanon

Greece, Bulgaria, Cyprus, Macedonia

(FYR).

Albania, Serbia, Montenegro, Bosnia &

Herz.,

Middle East, North Africa, Southern

Balkans

Central Asia, Western Balkans, West and

Central Africa

Cameroon, Congo, Côte d'Ivoire, the

Democratic Republic of the Congo,

Gabon, Ghana, Nigeria & Senegal

+ 8 countries

West & Central

Africa

+ 6 countries

Middle East, North Africa

Central Asia

+ 4 countries

Southeast Europe

(Balkans)

Rapid Entry into

New Countries

SYNERGY MODEL

1. Promotional designs

2. Coordinated supply chain

3. Property/franchise development

4. Business philosophy (senior

managers ex-Carrefour)

+25 countries by 2015

Potential of +40 in 5 to 10

years

In October 2013 Carrefour

reorganized the Balkans and Turkey

where Balkan expansion is managed

from Cyprus

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

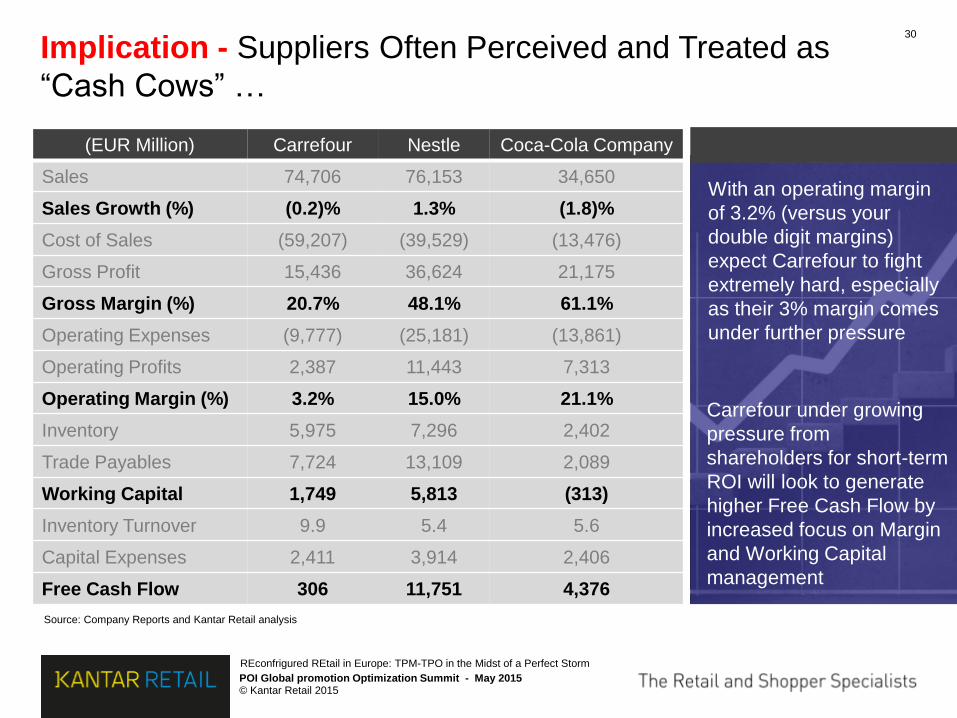

30

Implication - Suppliers Often Perceived and Treated as

“Cash Cows” …

Source: Company Reports and Kantar Retail analysis

(EUR Million) Carrefour Nestle Coca-Cola Company

Sales 74,706 76,153 34,650

Sales Growth (%) (0.2)% 1.3% (1.8)%

Cost of Sales (59,207) (39,529) (13,476)

Gross Profit 15,436 36,624 21,175

Gross Margin (%) 20.7% 48.1% 61.1%

Operating Expenses (9,777) (25,181) (13,861)

Operating Profits 2,387 11,443 7,313

Operating Margin (%) 3.2% 15.0% 21.1%

Inventory 5,975 7,296 2,402

Trade Payables 7,724 13,109 2,089

Working Capital 1,749 5,813 (313)

Inventory Turnover 9.9 5.4 5.6

Capital Expenses 2,411 3,914 2,406

Free Cash Flow 306 11,751 4,376

With an operating margin

of 3.2% (versus your

double digit margins)

expect Carrefour to fight

extremely hard, especially

as their 3% margin comes

under further pressure

Carrefour under growing

pressure from

shareholders for short-term

ROI will look to generate

higher Free Cash Flow by

increased focus on Margin

and Working Capital

management

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

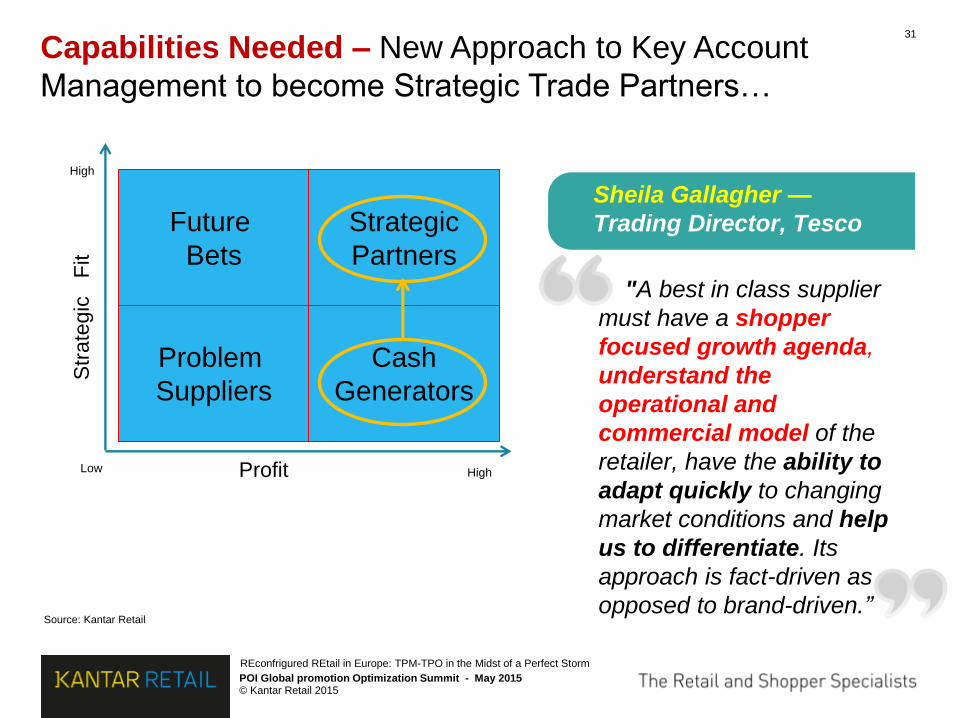

31

Capabilities Needed – New Approach to Key Account

Management to become Strategic Trade Partners…

Source: Kantar Retail

Sheila Gallagher —

Trading Director, Tesco

"A best in class supplier

must have a shopper

focused growth agenda,

understand the

operational and

commercial model of the

retailer, have the ability to

adapt quickly to changing

market conditions and help

us to differentiate. Its

approach is fact-driven as

opposed to brand-driven.”

Future

Bets

Problem

Suppliers

Cash

Generators

Strategic

Partners

Str

ate

gic

F

it

Profit

High

High Low

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

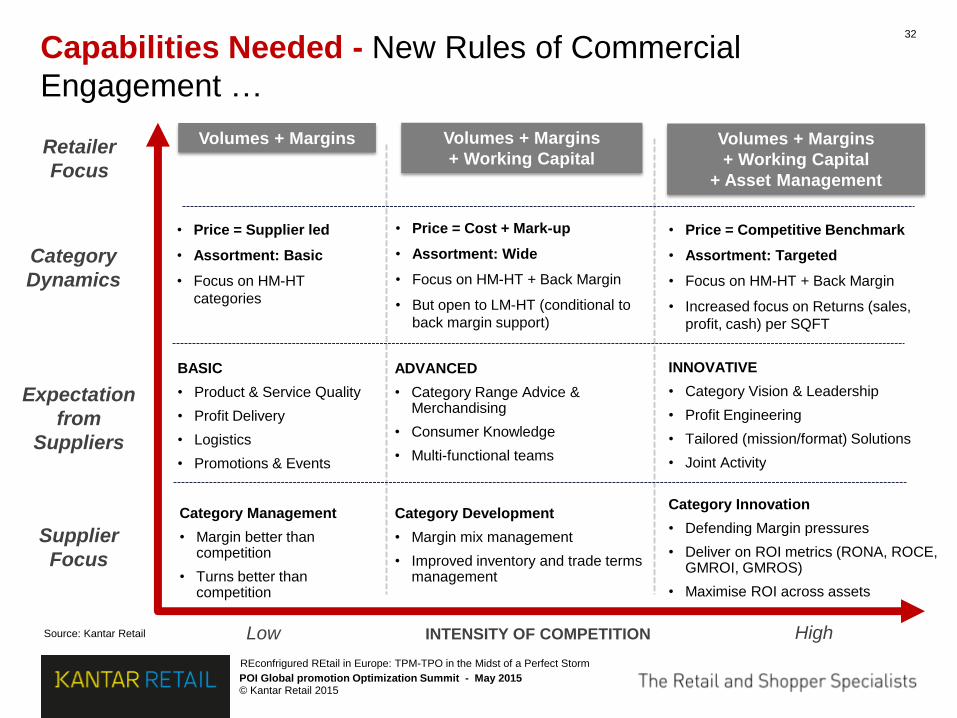

32

Capabilities Needed - New Rules of Commercial

Engagement …

Source: Kantar Retail

Volumes + Margins Volumes + Margins

+ Working Capital Volumes + Margins

+ Working Capital

+ Asset Management

Expectation

from

Suppliers

Retailer

Focus

• Price = Supplier led

• Assortment: Basic

• Focus on HM-HT

categories

• Price = Cost + Mark-up

• Assortment: Wide

• Focus on HM-HT + Back Margin

• But open to LM-HT (conditional to

back margin support)

• Price = Competitive Benchmark

• Assortment: Targeted

• Focus on HM-HT + Back Margin

• Increased focus on Returns (sales,

profit, cash) per SQFT

Category

Dynamics

BASIC

• Product & Service Quality

• Profit Delivery

• Logistics

• Promotions & Events

ADVANCED

• Category Range Advice & Merchandising

• Consumer Knowledge

• Multi-functional teams

INNOVATIVE

• Category Vision & Leadership

• Profit Engineering

• Tailored (mission/format) Solutions

• Joint Activity

Low High INTENSITY OF COMPETITION

Supplier

Focus

Category Management

• Margin better than competition

• Turns better than competition

Category Development

• Margin mix management

• Improved inventory and trade terms management

Category Innovation

• Defending Margin pressures

• Deliver on ROI metrics (RONA, ROCE, GMROI, GMROS)

• Maximise ROI across assets

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

33

Conclusion – Some Food for Thought…

• Operating in a Polarised World: Where is the next incremental sales ($ / £)

going to come from?

• Understanding Changing Consumer Profile: Do we know them? Do we

understand where, what, when and how they shop?

• Embracing Real Value: Are we delivering Real Value (Time, Money and

Emotions) to shoppers? How do we collaborate with our customers to deliver

Real Value?

• Fundamental Change in Route-to-Market: What’s my strategy around Online, Discounters, and Convenience? How do we play in an Omni-channel

environment?

• Increased Complexity around Customer Planning: Have we identified

our rising stars? How are we going to work with our high-volume low-growth

customers? How are we going to deal with increased commercial complexity?

POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

34

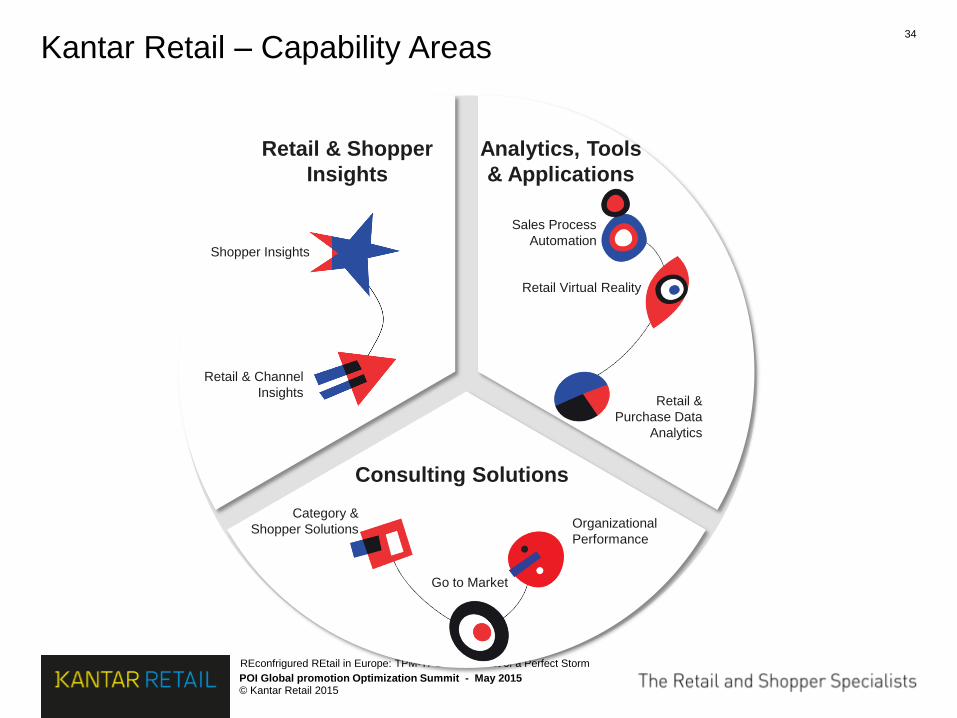

Kantar Retail – Capability Areas

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

POI Global promotion Optimization Summit - May 2015

Shopper Insights

Retail & Channel

Insights

Retail & Shopper

Insights

Retail &

Purchase Data

Analytics

Sales Process

Automation

Retail Virtual Reality

Analytics, Tools

& Applications

Organizational

Performance

Category &

Shopper Solutions

Go to Market

Consulting Solutions

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

35

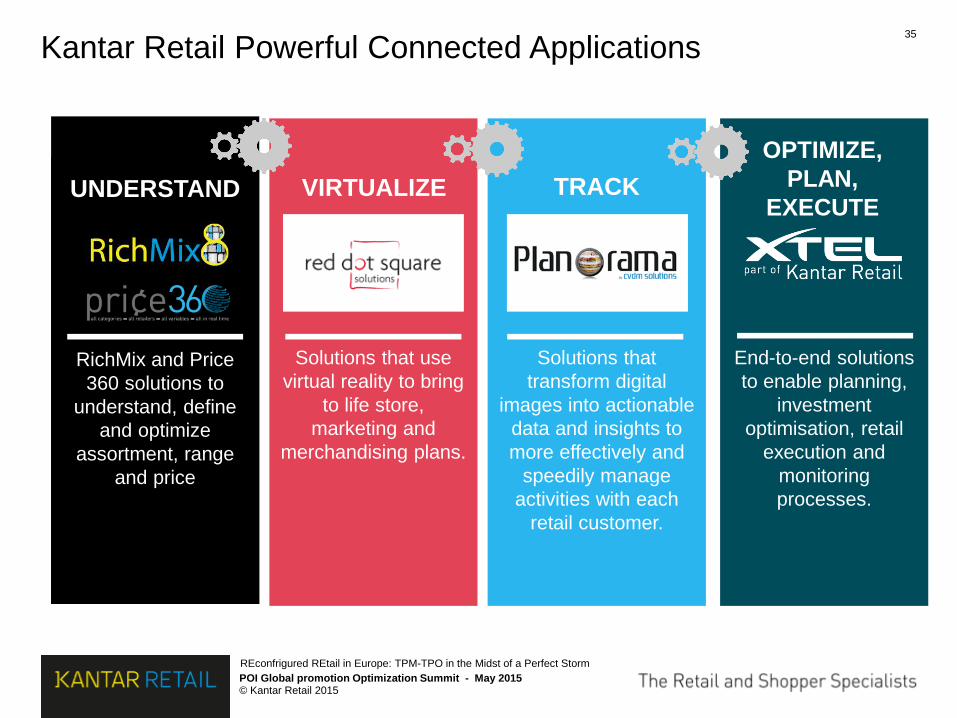

Kantar Retail Powerful Connected Applications

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

POI Global promotion Optimization Summit - May 2015

RichMix® is an

efficient assortment

tool that uses in-

depth analysis to

measure the

incremental impact of

changing the items

and facings in a

retailer’s mix

RichMix and Price

360 solutions to

understand, define

and optimize

assortment, range

and price

UNDERSTAND

End-to-end solutions

to enable planning,

investment

optimisation, retail

execution and

monitoring

processes.

OPTIMIZE,

PLAN,

EXECUTE

Solutions that use

virtual reality to bring

to life store,

marketing and

merchandising plans.

VIRTUALIZE

Solutions that

transform digital

images into actionable

data and insights to

more effectively and

speedily manage

activities with each

retail customer.

TRACK

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015

For further information please refer to

www.kantarretail.com

Contact:

Himanshu Pal

Director of Retail Insights

T: +44 (0) 2074 502 613

M: +44 (0) 7990 566 007

Himanshu_Pal

36

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2015 POI Global promotion Optimization Summit - May 2015

REconfrigured REtail in Europe: TPM-TPO in the Midst of a Perfect Storm

37