Embed Size (px)

Citation preview

Recommendation: BUY Sandstorm Gold (SNDXF)

Industry Overview

2

• Gold mining is capital intensive

• Capital is very expensive for small exploration and production (E&P) miners, known as “junior miners”

• Debt financing is unavailable due to lack of current cash flow to service the debt and high risk

• Equity financing dilutes current shareholders

• Exploration costs are going up

• Increasingly complex exploration

• Declining ore grades

• Energy intensive process

Industry Overview

3

• Gold prices going up – scarcity and inflation

• Increasingly difficult to replace current reserves

• Global government debt load increasing investor demand for inflation hedge

CEO Explains business model:http://www.youtube.com/watch?feature=player_embedded&v=VVQjuyOE_ag

Industry Overview

4

Company Profile

The Company is a growth focused company that seeks to acquire gold purchase agreements (“Gold Streams”) from companies that have advanced stage development projects or operating mines. In return for making up front payments to acquire a Gold Stream, Sandstorm receives the right to purchase, at a fixed price per ounce, a percentage of a mine’s gold production for the life of the mine. Sandstorm helps other companies in the resource industry grow their businesses, while acquiring attractive assets in the process. The Company is focused on acquiring Gold Streams from mines with low production costs, significant exploration potential and strong management teams. The Company currently has seven Gold Streams.

5

Company Profile

6

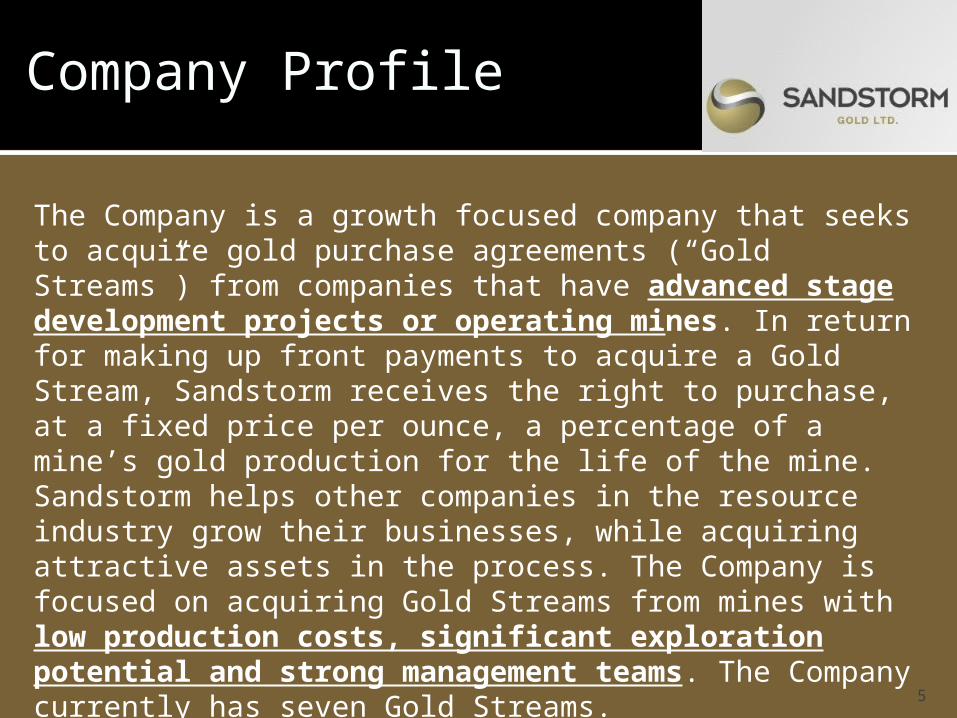

Sandstorm investment(lower counterparty risk)

Company Profile

7

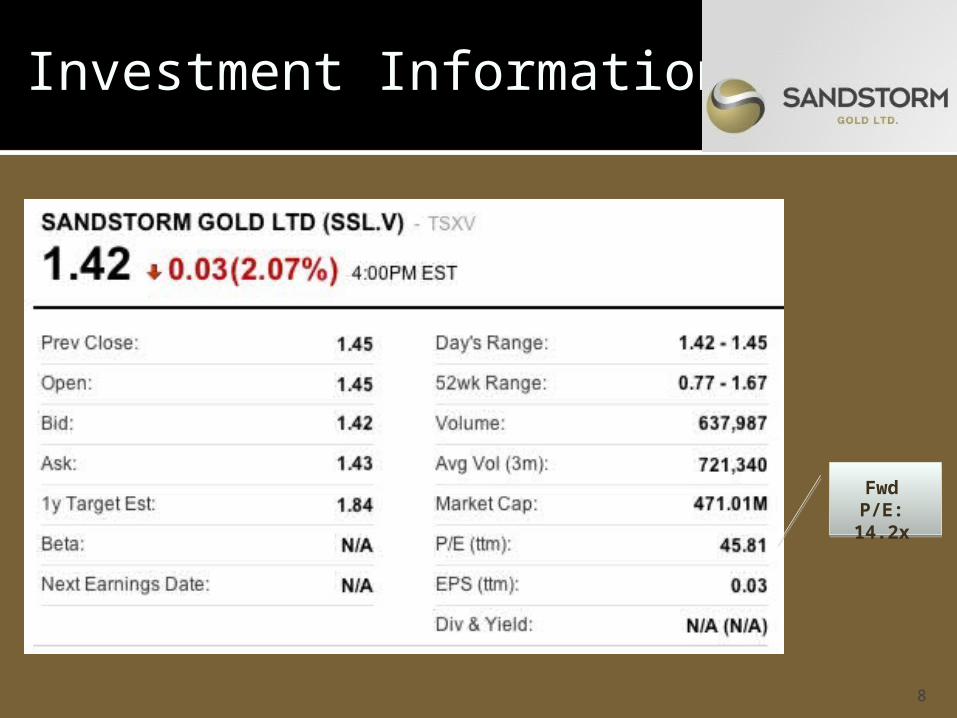

Investment Information

8

Fwd P/E: 14.2x

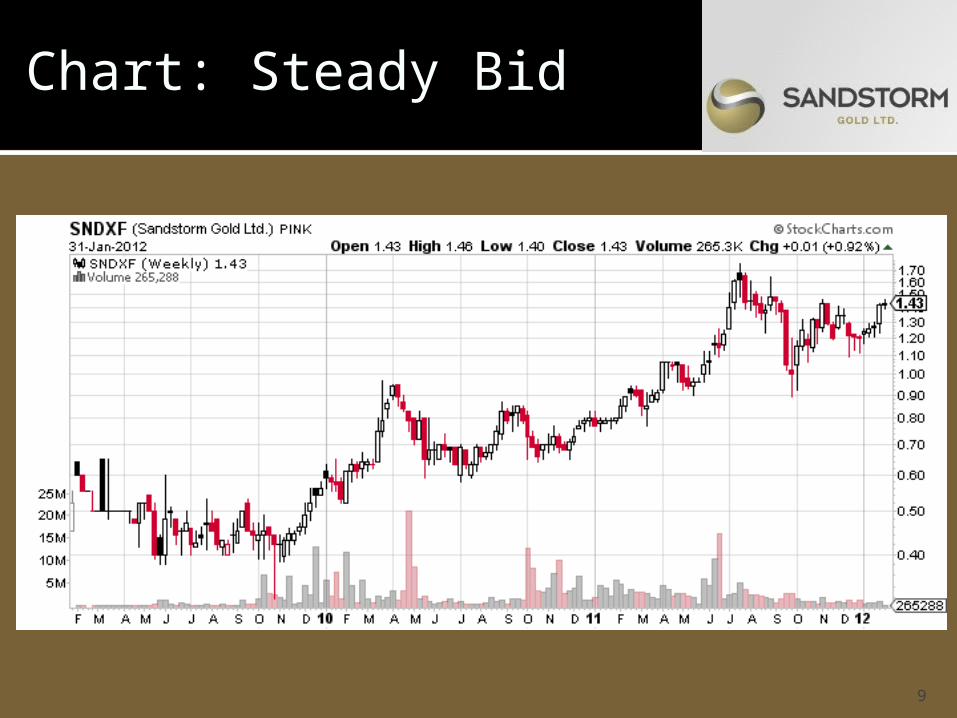

Chart: Steady Bid

9

Key Investment Points

#1: Experienced Management

#2: Large growth opportunity

#3: Significantly undervalued

10

Management

11

• Watson began as CFO at age 26 at Silver Wheaton

• Raised over $1B in funding for SLW operations

• Left to form Sandstorm

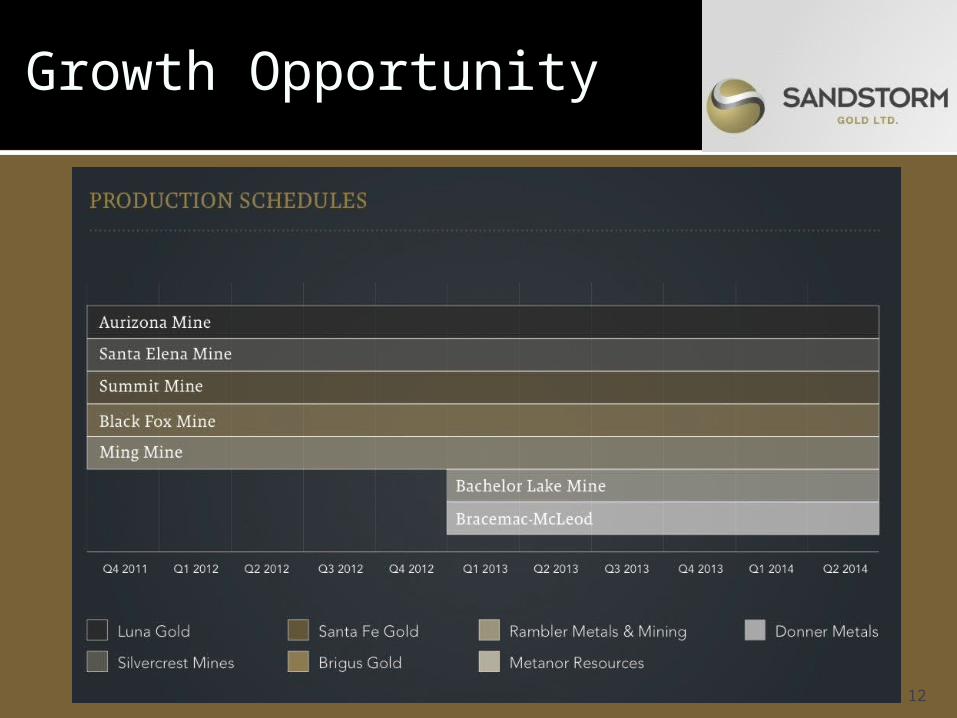

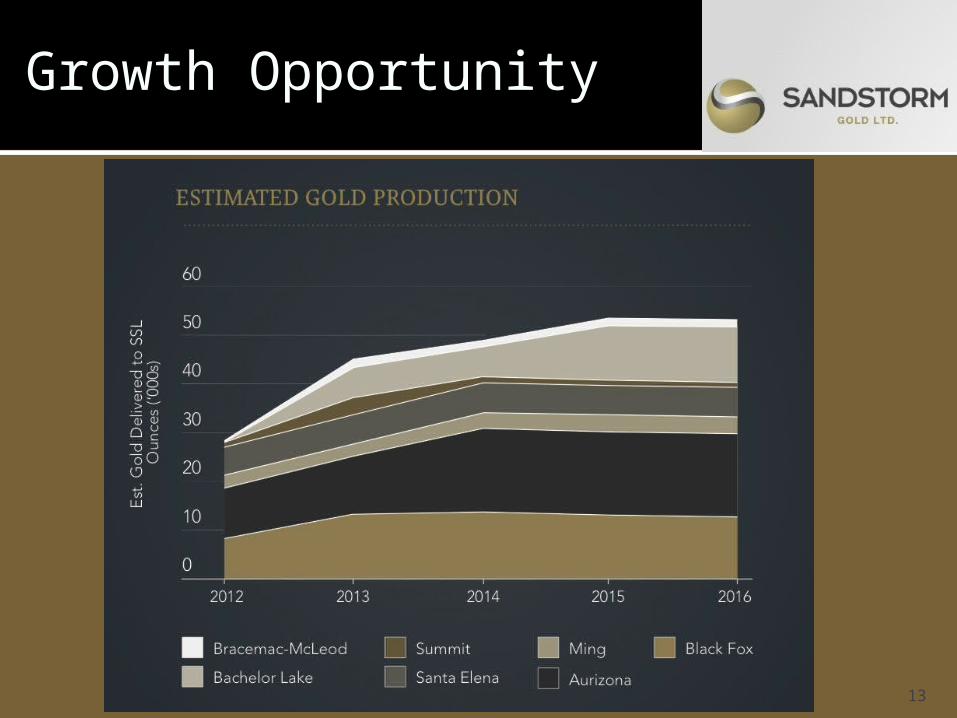

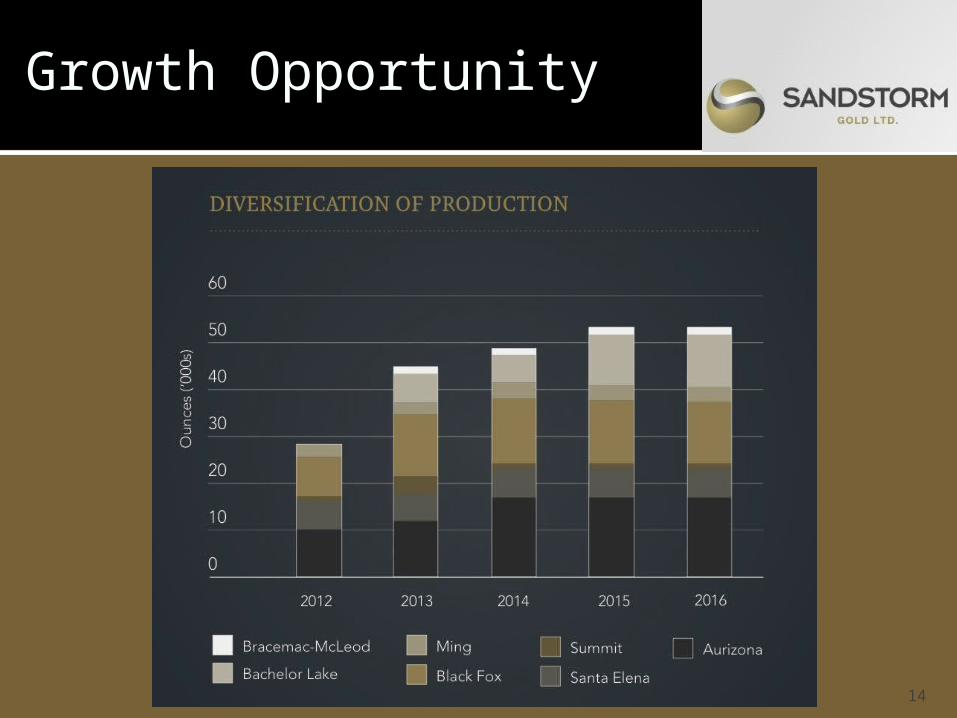

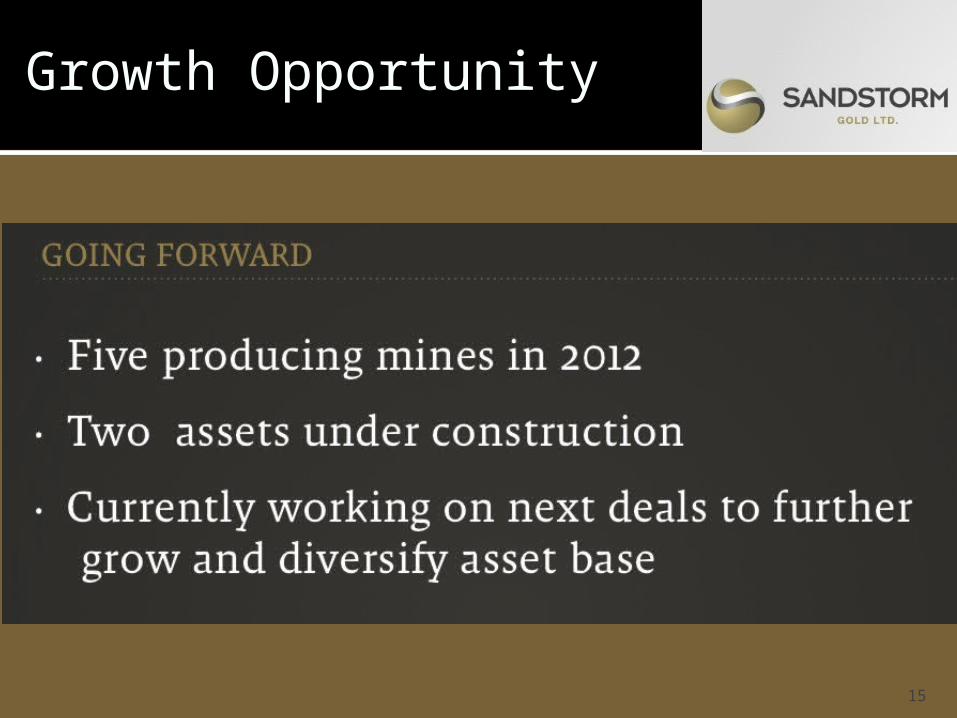

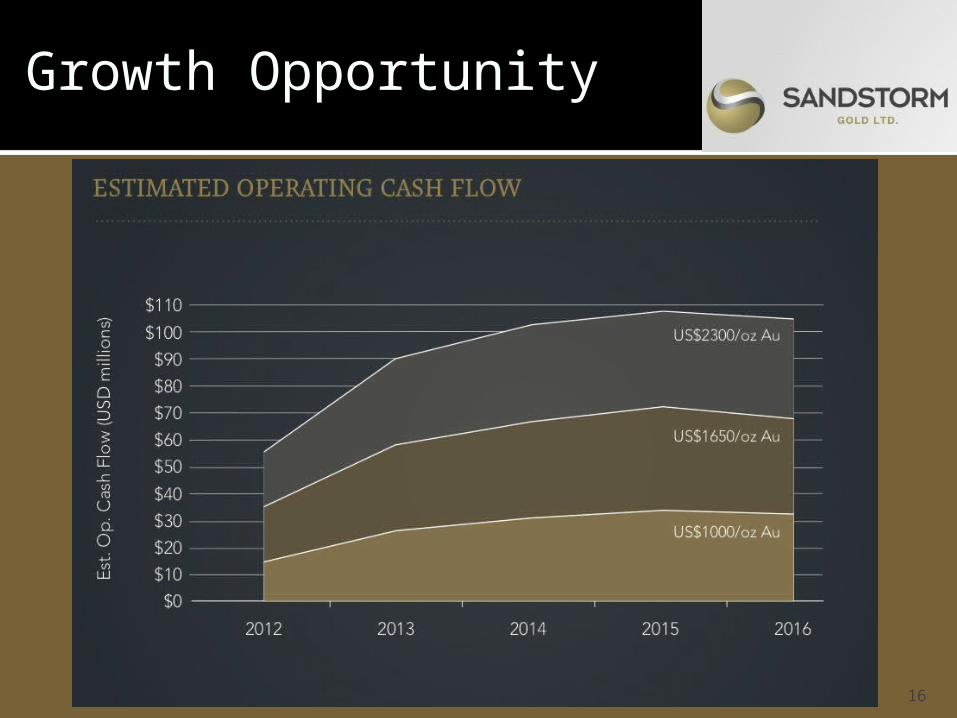

Growth Opportunity

12

Growth Opportunity

13

Growth Opportunity

14

Growth Opportunity

15

Growth Opportunity

16

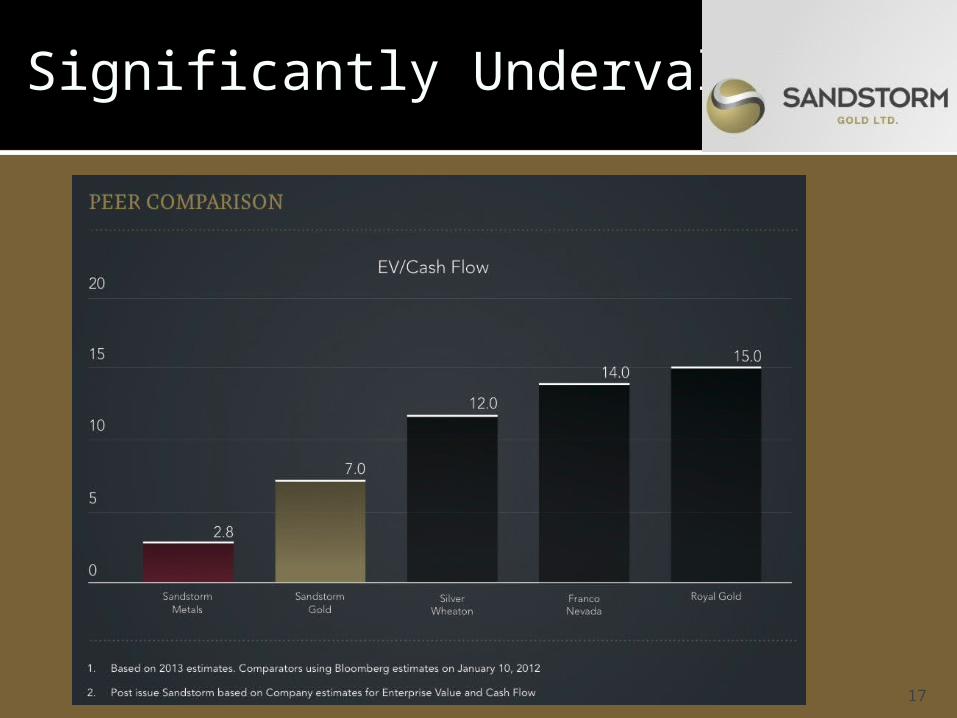

Significantly Undervalued

17

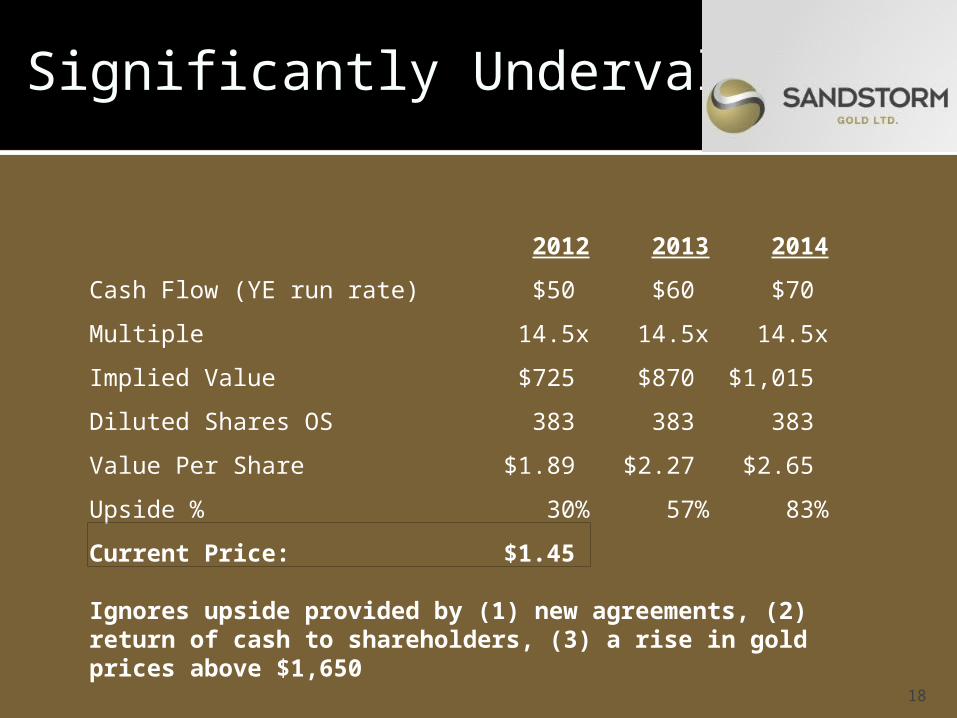

Significantly Undervalued

18

Ignores upside provided by (1) new agreements, (2) return of cash to shareholders, (3) a rise in gold prices above $1,650

2012 2013 2014

Cash Flow (YE run rate) $50 $60 $70

Multiple 14.5x 14.5x 14.5x

Implied Value $725 $870 $1,015

Diluted Shares OS 383 383 383

Value Per Share $1.89 $2.27 $2.65

Upside % 30% 57% 83%

Current Price: $1.45

Significantly Undervalued

19

Why the valuation discount to peers?

1.Illiquid: Should improve as company grows2.Small: Many institutional buyers have restrictions on market cap / share price3.Perceived risk of early-stage growth story, customer concentration, focus on smaller mining companies

What is NOT causing the valuation discount?

1.Poor management2.Unproven business model3.Lack of market opportunity4.Risky balance sheet / lack of financial liquidity5.Poor governance practices6.Low quality financial reporting / audit7.Inadequate investor relations

Significantly Undervalued

20

Upcoming Catalysts:

1.Earnings in February

2.Additional agreement announcements

• Current financial liquidity = $70M

• Enough to fund OpCF growth of approx. $20M

3.Potential for QE3, return of inflation in China

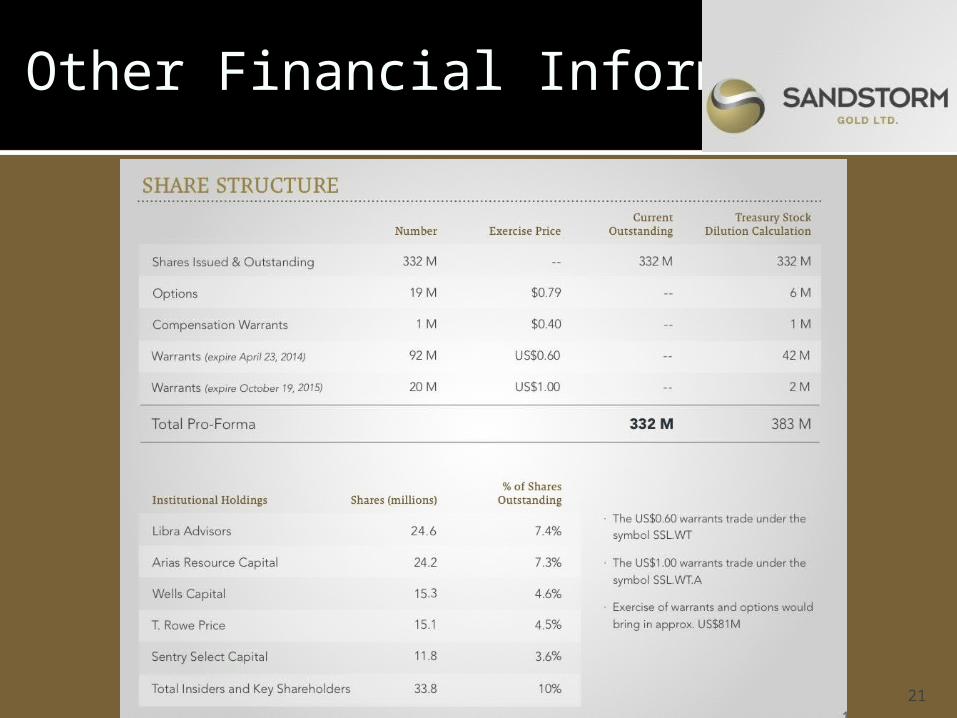

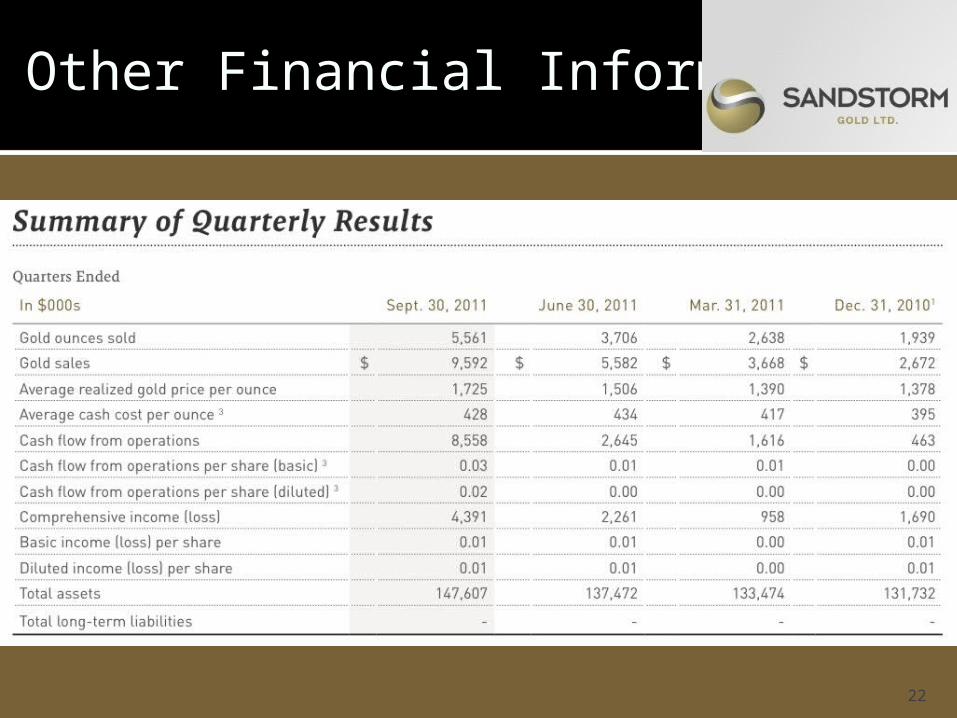

Other Financial Information

21

Other Financial Information

22

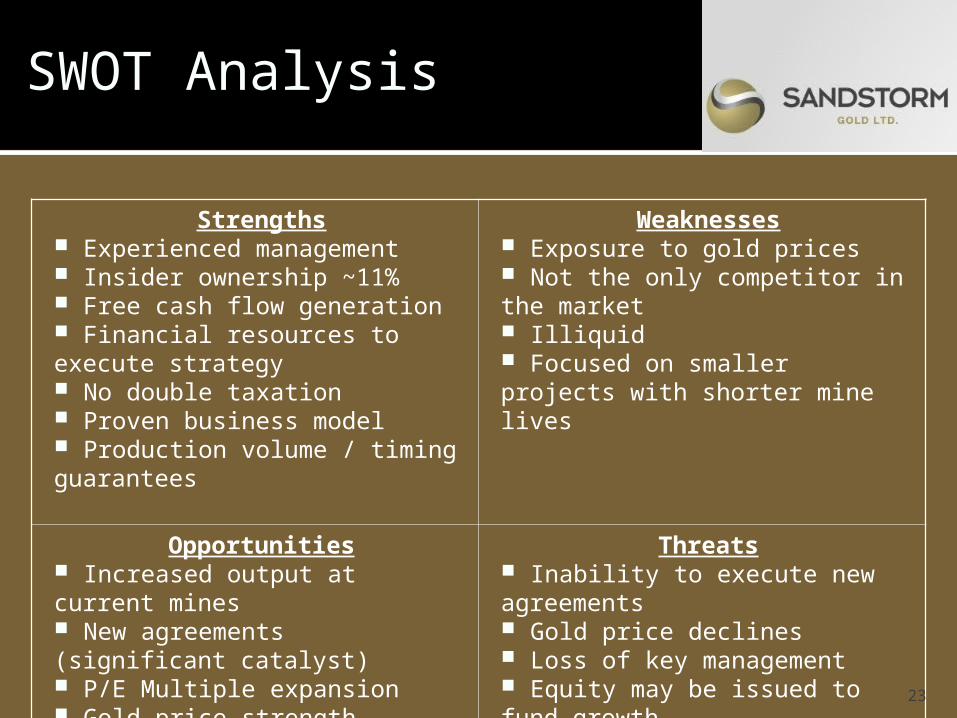

SWOT Analysis

Strengths Experienced management Insider ownership ~11% Free cash flow generation Financial resources to execute strategy No double taxation Proven business model Production volume / timing guarantees

Weaknesses Exposure to gold prices Not the only competitor in the market Illiquid Focused on smaller projects with shorter mine lives

Opportunities Increased output at current mines New agreements (significant catalyst) P/E Multiple expansion Gold price strength Potential to expand deal size as company matures

Threats Inability to execute new agreements Gold price declines Loss of key management Equity may be issued to fund growth Counter party risk

23

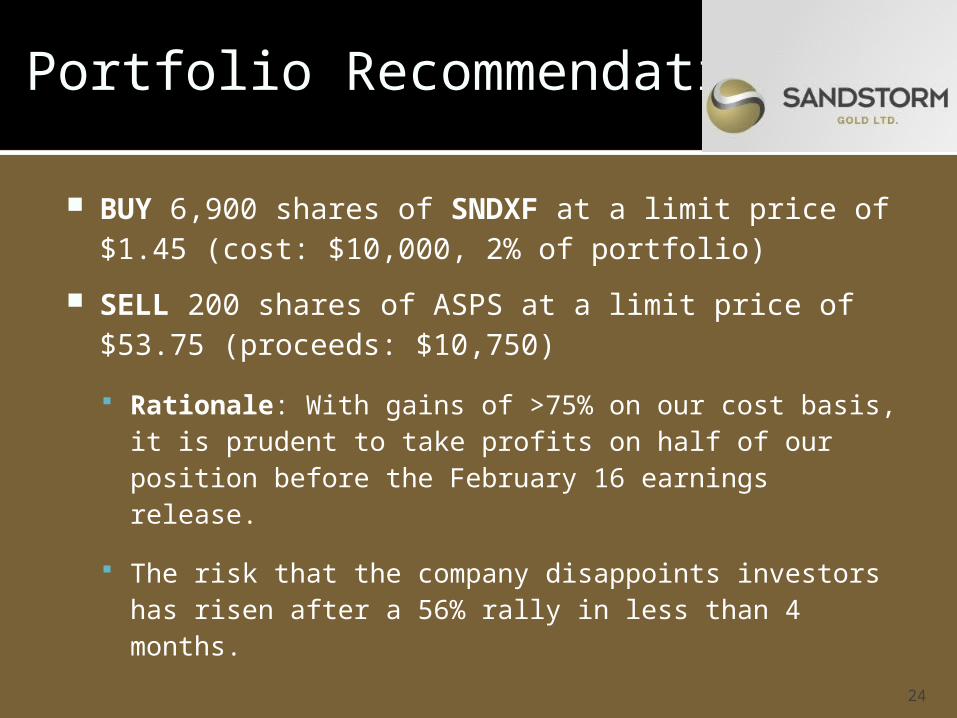

BUY 6,900 shares of SNDXF at a limit price of $1.45 (cost: $10,000, 2% of portfolio)

SELL 200 shares of ASPS at a limit price of $53.75 (proceeds: $10,750)

Rationale: With gains of >75% on our cost basis, it is prudent to take profits on half of our position before the February 16 earnings release.

The risk that the company disappoints investors has risen after a 56% rally in less than 4 months.

Portfolio Recommendation

24